- Phân tích

- Tin tức và các công cụ

- Tin tức thị trường

Tin tức thì trường

- WTI trades in positive territory for the third consecutive day near $76.75 in Tuesday’s early Asian session.

- Libya's shutdown of production and exports fuelled fresh supply concerns, boosting the WTI price.

- The sluggish Chinese economy and oil demand concerns might cap the black gold’s upside.

West Texas Intermediate (WTI), the US crude oil benchmark, is trading around $76.75 on Tuesday. The WTI price extends its recovery on the back of a production halt in Libya, adding to supply fears fuelled by reports of escalating conflict in the Middle East.

Libya’s eastern government in Benghazi said Monday that crude oil production and exports would shut down amid a dispute with the internationally recognized western government in Tripoli over who should lead the central bank, per Bloomberg.

Libya produces around 1.2 million barrels per day, with more than 1 million bpd exported to the global market, said Matt Smith, lead oil analyst for the Americas at Kpler. The developments surrounding Libya's output cuts have triggered further supply concerns and boosted WTI prices.

"The biggest risk for the oil market is probably a further drop in Libyan oil production due to political tensions in the country, with a risk that production could fall from current levels of 1 million barrels per day to zero," noted Giovanni Staunovo, UBS analyst.

Furthermore, firmer expectations that the US Federal Reserve (Fed) will cut interest rates in its upcoming September meeting lift the WTI price. On Monday, San Francisco Fed President Mary Daly said that she believes it’s appropriate for the Fed to begin cutting interest rates. Lower interest rates generally support the WTI price as it reduces the cost of borrowing, which can boost economic activity, and oil demand.

However, the upside for black gold might be limited. China’s oil imports in July were down 12% from June and 3% from July 2023, raising fears of the country's economic health and future oil demand as China is the world’s largest importer of oil.

WTI Oil FAQs

WTI Oil is a type of Crude Oil sold on international markets. The WTI stands for West Texas Intermediate, one of three major types including Brent and Dubai Crude. WTI is also referred to as “light” and “sweet” because of its relatively low gravity and sulfur content respectively. It is considered a high quality Oil that is easily refined. It is sourced in the United States and distributed via the Cushing hub, which is considered “The Pipeline Crossroads of the World”. It is a benchmark for the Oil market and WTI price is frequently quoted in the media.

Like all assets, supply and demand are the key drivers of WTI Oil price. As such, global growth can be a driver of increased demand and vice versa for weak global growth. Political instability, wars, and sanctions can disrupt supply and impact prices. The decisions of OPEC, a group of major Oil-producing countries, is another key driver of price. The value of the US Dollar influences the price of WTI Crude Oil, since Oil is predominantly traded in US Dollars, thus a weaker US Dollar can make Oil more affordable and vice versa.

The weekly Oil inventory reports published by the American Petroleum Institute (API) and the Energy Information Agency (EIA) impact the price of WTI Oil. Changes in inventories reflect fluctuating supply and demand. If the data shows a drop in inventories it can indicate increased demand, pushing up Oil price. Higher inventories can reflect increased supply, pushing down prices. API’s report is published every Tuesday and EIA’s the day after. Their results are usually similar, falling within 1% of each other 75% of the time. The EIA data is considered more reliable, since it is a government agency.

OPEC (Organization of the Petroleum Exporting Countries) is a group of 13 Oil-producing nations who collectively decide production quotas for member countries at twice-yearly meetings. Their decisions often impact WTI Oil prices. When OPEC decides to lower quotas, it can tighten supply, pushing up Oil prices. When OPEC increases production, it has the opposite effect. OPEC+ refers to an expanded group that includes ten extra non-OPEC members, the most notable of which is Russia.

- EUR/USD failed to capture 1.1200 on Monday as markets pare back risk flows.

- Economic calendar remains tepid after blustery showing last week.

- EU inflation, US PCE inflation to dominate the late-week data docket.

EUR/USD pared back recent gains on Monday, slipping back from 1.1200 as traders ease off the gas pedal in broad-market Dollar-negative flows that sent Fiber into its highest bids in 13-months last week. Market risk appetite remains on balance to get the new trading week fired up, but Greenback pressure caught a relief as investors gear up for the long wait to key inflation figures due late this week.

Forex Today: A September rate cut now looks at US data releases

Preliminary EU Harmonized Index of Consumer Prices (HICP) inflation is slated for release on Friday, with little else of note in the way until then. Pan-EU core HICP inflation is forecast to tick down to 2.8% from 2.9% for the year ended in August.

Most of the trading week will be a quiet affair on the economic calendar. Q2 US Gross Domestic Product (GDP) figures are slated for Thursday, but are broadly expected to hold steady at 2.8% on an annualized basis. Friday could be a kicker for markets that are increasingly focused on the timing and pace of rate cuts from the Fed, with July’s US core Personal Consumption Expenditure - Price Index (PCE) inflation print set to hold steady at 0.2% MoM. The YoY PCE inflation figure is actually expected to tick upwards to 2.7% from 2.6%, but investors are confident that inflation has made enough progress towards the Fed’s 2% target that it will count as “close enough” to still keep the way open to a first rate cut on September 18.

What happened on Monday?

US Durable Goods Order in July rallied a surprising 9.9% MoM, well above the forecast 4.0% and entirely reversing the previous month’s revised -6.9% contraction.

Despite the upswing on Durable Goods Orders, some trepidation remains; excluding Transportation spending, Durable Goods Orders actually contracted -0.2% MoM, worse than the forecast 0.0% and the previous month’s tepid 0.1%, which was revised down from 0.5%.

EUR/USD price forecast

EUR/USD is on pace for its best single-month performance since November of 2022, up over 3.1% just in the month of August. Despite Monday’s technical exhaustion pullback, Fiber has gained ground for four consecutive trading weeks, and is bidding well above the 200-day Exponential Moving Average (EMA) at 1.0832.

Despite a healthy bid deep into bull country, Fiber is running a deep exposure to a bearish pullback, and a lack of topside momentum could see price action tumble all the way back to the 50-day EMA at 1.0925.

EUR/USD daily chart

Euro FAQs

The Euro is the currency for the 20 European Union countries that belong to the Eurozone. It is the second most heavily traded currency in the world behind the US Dollar. In 2022, it accounted for 31% of all foreign exchange transactions, with an average daily turnover of over $2.2 trillion a day. EUR/USD is the most heavily traded currency pair in the world, accounting for an estimated 30% off all transactions, followed by EUR/JPY (4%), EUR/GBP (3%) and EUR/AUD (2%).

The European Central Bank (ECB) in Frankfurt, Germany, is the reserve bank for the Eurozone. The ECB sets interest rates and manages monetary policy. The ECB’s primary mandate is to maintain price stability, which means either controlling inflation or stimulating growth. Its primary tool is the raising or lowering of interest rates. Relatively high interest rates – or the expectation of higher rates – will usually benefit the Euro and vice versa. The ECB Governing Council makes monetary policy decisions at meetings held eight times a year. Decisions are made by heads of the Eurozone national banks and six permanent members, including the President of the ECB, Christine Lagarde.

Eurozone inflation data, measured by the Harmonized Index of Consumer Prices (HICP), is an important econometric for the Euro. If inflation rises more than expected, especially if above the ECB’s 2% target, it obliges the ECB to raise interest rates to bring it back under control. Relatively high interest rates compared to its counterparts will usually benefit the Euro, as it makes the region more attractive as a place for global investors to park their money.

Data releases gauge the health of the economy and can impact on the Euro. Indicators such as GDP, Manufacturing and Services PMIs, employment, and consumer sentiment surveys can all influence the direction of the single currency. A strong economy is good for the Euro. Not only does it attract more foreign investment but it may encourage the ECB to put up interest rates, which will directly strengthen the Euro. Otherwise, if economic data is weak, the Euro is likely to fall. Economic data for the four largest economies in the euro area (Germany, France, Italy and Spain) are especially significant, as they account for 75% of the Eurozone’s economy.

Another significant data release for the Euro is the Trade Balance. This indicator measures the difference between what a country earns from its exports and what it spends on imports over a given period. If a country produces highly sought after exports then its currency will gain in value purely from the extra demand created from foreign buyers seeking to purchase these goods. Therefore, a positive net Trade Balance strengthens a currency and vice versa for a negative balance.

- USD/CAD remains on the defensive near 1.3485 in Tuesday’s early Asian session.

- Fed’s Daly believes it’s appropriate for the Fed to begin cutting interest rates.

- Higher crude oil prices support the CAD and create a headwind for USD/CAD.

The USD/CAD pair extends downside around 1.3485 during the early Asian session on Tuesday. Escalating geopolitical tensions in the Middle East provide some support to the commodity-linked Canadian Dollar (CAD) and weigh on USD/CAD. Later on Tuesday, the US Conference Board’s Consumer Confidence is due.

Federal Reserve (Fed) Bank of San Francisco President Mary Daly’s remarks on Monday echoed comments from Fed Chair Jerome Powell at the Jackson Hole symposium, who said that he has gained confidence that inflation is on course to the 2% target and “the time has come for policy to adjust.” Fed’s Daly noted that she believes it’s appropriate for the Fed to begin cutting interest rates. This, in turn, continues to undermine the US Dollar (USD) against the Loonie.

According to the CME FedWatch Tool, the markets have fully priced in a 25 basis points (bps) rate cut, while the possibility of a deeper rate cut stands at 30%, down from 36.5 % last Friday.

Elsewhere, data released by the US Census Bureau on Monday showed that the US Durable Goods Orders climbed to 9.9% MoM in July from a -6.9% contraction in June. This figure came in better than the estimation of a 4% increase and registered the most significant gain since May 2020. The Greenback posted modest gains in an immediate reaction to the upbeat data.

On the Loonie front, the fear of wider conflicts in the Middle East and prospects of supply disruptions in Libya boost the crude oil prices and lift the CAD. It's worth noting that higher crude oil prices are likely to underpin the Loonie for the time being, as Canada is the leading exporter of Oil to the United States.

Canadian Dollar FAQs

The key factors driving the Canadian Dollar (CAD) are the level of interest rates set by the Bank of Canada (BoC), the price of Oil, Canada’s largest export, the health of its economy, inflation and the Trade Balance, which is the difference between the value of Canada’s exports versus its imports. Other factors include market sentiment – whether investors are taking on more risky assets (risk-on) or seeking safe-havens (risk-off) – with risk-on being CAD-positive. As its largest trading partner, the health of the US economy is also a key factor influencing the Canadian Dollar.

The Bank of Canada (BoC) has a significant influence on the Canadian Dollar by setting the level of interest rates that banks can lend to one another. This influences the level of interest rates for everyone. The main goal of the BoC is to maintain inflation at 1-3% by adjusting interest rates up or down. Relatively higher interest rates tend to be positive for the CAD. The Bank of Canada can also use quantitative easing and tightening to influence credit conditions, with the former CAD-negative and the latter CAD-positive.

The price of Oil is a key factor impacting the value of the Canadian Dollar. Petroleum is Canada’s biggest export, so Oil price tends to have an immediate impact on the CAD value. Generally, if Oil price rises CAD also goes up, as aggregate demand for the currency increases. The opposite is the case if the price of Oil falls. Higher Oil prices also tend to result in a greater likelihood of a positive Trade Balance, which is also supportive of the CAD.

While inflation had always traditionally been thought of as a negative factor for a currency since it lowers the value of money, the opposite has actually been the case in modern times with the relaxation of cross-border capital controls. Higher inflation tends to lead central banks to put up interest rates which attracts more capital inflows from global investors seeking a lucrative place to keep their money. This increases demand for the local currency, which in Canada’s case is the Canadian Dollar.

Macroeconomic data releases gauge the health of the economy and can have an impact on the Canadian Dollar. Indicators such as GDP, Manufacturing and Services PMIs, employment, and consumer sentiment surveys can all influence the direction of the CAD. A strong economy is good for the Canadian Dollar. Not only does it attract more foreign investment but it may encourage the Bank of Canada to put up interest rates, leading to a stronger currency. If economic data is weak, however, the CAD is likely to fall.

- GBP/USD pulled back on Monday, snapping a seven-day win streak.

- UK market flows were crimped with an extended weekend.

- Investors forced to wait until the end of the week for meaningful data.

GBP/USD trimmed recent gains to kick off the new trading week, slipping back below the 1.3200 handle on Monday and wrapping up a seven-day winning streak that took the pair up over 3% from 1.2800 to a 29-month high of 1.3230.

Forex Today: A September rate cut now looks at US data releases

UK markets were shuttered on Monday for a banking holiday, leaving Pound Sterling flows thin and giving the Greenback a further boost. Markets are paring back recent risk appetite after a splurge on the heels of the Federal Reserve all but confirming that rate cuts were coming in September, barring any drastic shifts in economic data.

The economic calendar for the upcoming trading week is expected to be relatively quiet. On Thursday, Q2 US Gross Domestic Product (GDP) figures are expected to remain steady at 2.8% on an annualized basis. On Friday, the focus will be on July’s US core Personal Consumption Expenditure - Price Index (PCE) inflation, which is forecasted to hold steady at 0.2% MoM. The YoY PCE inflation figure is anticipated to increase to 2.7% from 2.6%. Despite this, investors believe that inflation is close enough to the Fed’s 2% target to potentially lead to a rate cut in September.

In July, US Durable Goods Orders unexpectedly rose by 9.9% MoM, surpassing the forecast of 4.0% and reversing the previous month’s revised -6.9% contraction.

However, concerns persist as excluding transportation spending, Durable Goods Orders actually decreased by -0.2% MoM, worse than the anticipated 0.0% and the previous month’s 0.1%, which was revised down from 0.5%.

GBP/USD price forecast

Cable pulled back after a stellar run up the charts, chalking in nearly 4.5% growth over a mere eleven trading days. Monday looks set to bry the latest bull run, with prices wobbling at the top of an extreme overextension.

The immediate hurdle for short sellers will be to drag GBP/USD bids back down to the 50-day Exponential Moving Average (EMA) at 1.2860, and it might take a few extra attempts to kick off a bearish trend firm enough to bring price action back down to the 200-day EMA near 1.2700.

GBP/USD daily chart

Pound Sterling FAQs

The Pound Sterling (GBP) is the oldest currency in the world (886 AD) and the official currency of the United Kingdom. It is the fourth most traded unit for foreign exchange (FX) in the world, accounting for 12% of all transactions, averaging $630 billion a day, according to 2022 data. Its key trading pairs are GBP/USD, aka ‘Cable’, which accounts for 11% of FX, GBP/JPY, or the ‘Dragon’ as it is known by traders (3%), and EUR/GBP (2%). The Pound Sterling is issued by the Bank of England (BoE).

The single most important factor influencing the value of the Pound Sterling is monetary policy decided by the Bank of England. The BoE bases its decisions on whether it has achieved its primary goal of “price stability” – a steady inflation rate of around 2%. Its primary tool for achieving this is the adjustment of interest rates. When inflation is too high, the BoE will try to rein it in by raising interest rates, making it more expensive for people and businesses to access credit. This is generally positive for GBP, as higher interest rates make the UK a more attractive place for global investors to park their money. When inflation falls too low it is a sign economic growth is slowing. In this scenario, the BoE will consider lowering interest rates to cheapen credit so businesses will borrow more to invest in growth-generating projects.

Data releases gauge the health of the economy and can impact the value of the Pound Sterling. Indicators such as GDP, Manufacturing and Services PMIs, and employment can all influence the direction of the GBP. A strong economy is good for Sterling. Not only does it attract more foreign investment but it may encourage the BoE to put up interest rates, which will directly strengthen GBP. Otherwise, if economic data is weak, the Pound Sterling is likely to fall.

Another significant data release for the Pound Sterling is the Trade Balance. This indicator measures the difference between what a country earns from its exports and what it spends on imports over a given period. If a country produces highly sought-after exports, its currency will benefit purely from the extra demand created from foreign buyers seeking to purchase these goods. Therefore, a positive net Trade Balance strengthens a currency and vice versa for a negative balance.

- NZD/JPY declined on Tuesday's session to settle around 89.70.

- The RSI is hovering near the 50 midline, suggesting a neutral bias.

- The MACD is flat green, indicating a lack of clear momentum.

The NZD/JPY currency pair is facing renewed selling pressure on Tuesday, declining by 0.30% to trade around 89.70. Technical indicators display mixed signals, suggesting that the pair is likely to remain range-bound in the near term.

The Relative Strength Index (RSI) is fluctuating around the 50 midline at 46, indicating that neither buyers nor sellers have a clear advantage. This reading suggests that the pair is likely to continue its sideways movement within the current range. The Moving Average Convergence Divergence (MACD) is also showing a neutral bias, with flat green bars indicating that the bullish momentum is neither gaining nor losing strength.

NZD/JPY daily chart

As the pair seems to be stuck in a consolidation period and with indicators flat, the cross might continue trading in the 88.00-90.00 channel. A break above or below these levels might set the pace for the short term.

- USD/JPY stays under Ichimoku Cloud and 200-DMA at 151.22, maintaining downtrend with easing selling pressure.

- RSI trends upward, suggesting a potential short-term rally if USD/JPY surpasses 145.00.

- Resistance levels at 146.42 (Tenkan-Sen), 147.91 (Senkou Span A), and 149.39 (August 15 high).

- Below 144.00, key support at 141.69; further drop could target psychological 140.00 level.

The Japanese Yen (JPY) lost ground against the Greenback on Monday as the USD/JPY pair edged up 0.13% amid an uptick in US Treasury bond yields. At the time of writing, the pair was at 144.59 after bouncing off daily lows of 143.44.

USD/JPY Price Forecast: Technical outlook

The USD/JPY downtrend is intact as the exchange rate remains below the Ichimoku Cloud and the 200-day moving average (DMA) at 151.22. Nevertheless, sellers are losing some momentum, as depicted by the Relative Strength Index (RSI), remaining bearish, yet aiming up. That could pave the way for a leg-up before testing lower prices.

If USD/JPY clears 145.00, the next resistance emerges at the Tenkan-Sen at 146.42, followed by the Senkou Span A at 147.91. Further upside is seen at the confluence of the Kijun-Sen and the August 15 daily high of 149.39.

Conversely, if USD/JPY slumps below the 144.00 figure and the pair could tumble towards the latest cycle low seen at 141.69, before challenging 140.00.

USD/JPY Price Action – Daily Chart

Japanese Yen PRICE Today

The table below shows the percentage change of Japanese Yen (JPY) against listed major currencies today. Japanese Yen was the strongest against the US Dollar.

| USD | EUR | GBP | JPY | CAD | AUD | NZD | CHF | |

|---|---|---|---|---|---|---|---|---|

| USD | -0.02% | 0.00% | 0.01% | -0.01% | 0.00% | -0.00% | -0.01% | |

| EUR | 0.02% | 0.03% | 0.03% | -0.00% | 0.04% | -0.01% | -0.01% | |

| GBP | -0.01% | -0.03% | 0.02% | 0.00% | -0.02% | -0.02% | -0.05% | |

| JPY | -0.01% | -0.03% | -0.02% | -0.06% | -0.02% | -0.05% | -0.02% | |

| CAD | 0.01% | 0.00% | -0.00% | 0.06% | 0.03% | 0.00% | -0.01% | |

| AUD | -0.01% | -0.04% | 0.02% | 0.02% | -0.03% | -0.04% | -0.02% | |

| NZD | 0.00% | 0.00% | 0.02% | 0.05% | -0.00% | 0.04% | -0.03% | |

| CHF | 0.01% | 0.01% | 0.05% | 0.02% | 0.00% | 0.02% | 0.03% |

The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the Japanese Yen from the left column and move along the horizontal line to the US Dollar, the percentage change displayed in the box will represent JPY (base)/USD (quote).

- NZD/USD declined on Monday to 0.62000, testing crucial support levels.

- The MACD indicator is printing flat green bars, suggesting that the rally might have come to an end.

- The RSI points south suggesting a mounting selling traction.

In Monday's session, the NZD/USD pair declined by 0.40% to 0.6200, as buyers seem to be taking a breather, and the pair seems to have entered a consolidation period. It's worth noticing that the pair approached highs since January above 0.6230.

The Moving Average Convergence Divergence (MACD) indicator is printing flat green bars, which suggests that the consolidation is likely to continue in the short term. The Relative Strength Index (RSI) scaped overbought conditions and is now pointing downwards suggesting that the bulls are taking a breather.

NZD/USD daily chart

The NZD/USD pair faces immediate support at 0.6200 and 0.6150. A break below 0.6150 could lead to a further decline towards 0.6100, which is a major support level. On the upside, immediate resistance can be found at 0.6255. A consolidation above this level could pave the way for a further rally to retest the 0.6300 zone.

- AUD/USD declines amidst rising risk-off sentiment.

- China's PBOC keeps its 1-year MLF rate steady at 2.30%, which failed to trigger movements on the AUD.

- The RBA's hawkish stance supports the Australian Dollar.

The AUD/USD declined by 0.30% to 0.6775 in Monday's session as the Australian Dollar (AUD) edged lower despite hovering around a seven-month high near 0.6800. The decline was primarily attributed to a broad USD recovery and a cautious market sentiment.

Amidst a volatile economic backdrop in Australia, the Reserve Bank of Australia's (RBA) aggressive stance against rising inflation has dampened market expectations regarding multiple cuts, which has benefitted the Aussie.

Daily digest market movers: Australian Dollar declines due to USD strength, lower commodities weigh

- AUD/USD multi-day rally faces resistance around 0.6760 due to weak copper prices, despite a recovery in iron ore prices.

- AUD's recent strength was driven by a weaker US Dollar and improved risk appetite.

- In addition, monetary policy divergence between the RBA and the Federal Reserve (Fed) catalyzed the pair.

- On the Chinese front, China's PBOC kept its 1-year MLF rate unchanged at 2.30%, but further stimulus is anticipated as the economy struggles.

- July industrial profits in China may provide insights into the persisting weaknesses in the mainland economy.

- Any signs of weakness in the Chinese economy might weigh on the Aussie

AUD/USD technical outlook: Bullish momentum eases, support at 0.6750

The AUD/USD pair faced further downside pressure on Monday, as buyers are taking a breather. The Relative Strength Index (RSI) is at 62 with a downward tendency, while the Moving Average Convergence Divergence (MACD) presents decreasing green bars, suggesting a decrease in bullish momentum. Volume has been relatively stable, indicating a lack of significant buying or selling pressure.

Overall, the technical outlook for AUD/USD remains neutral. The RSI is still above its midpoint, and the MACD shows decreasing bullish momentum. Further consolidation or a reversal could be in play.

Immediate support levels can be seen at 0.6750, 0.6700 and 0.6650, while resistance levels may be encountered at 0.6800, 0.6850 and 0.6900.

Australian Dollar FAQs

One of the most significant factors for the Australian Dollar (AUD) is the level of interest rates set by the Reserve Bank of Australia (RBA). Because Australia is a resource-rich country another key driver is the price of its biggest export, Iron Ore. The health of the Chinese economy, its largest trading partner, is a factor, as well as inflation in Australia, its growth rate and Trade Balance. Market sentiment – whether investors are taking on more risky assets (risk-on) or seeking safe-havens (risk-off) – is also a factor, with risk-on positive for AUD.

The Reserve Bank of Australia (RBA) influences the Australian Dollar (AUD) by setting the level of interest rates that Australian banks can lend to each other. This influences the level of interest rates in the economy as a whole. The main goal of the RBA is to maintain a stable inflation rate of 2-3% by adjusting interest rates up or down. Relatively high interest rates compared to other major central banks support the AUD, and the opposite for relatively low. The RBA can also use quantitative easing and tightening to influence credit conditions, with the former AUD-negative and the latter AUD-positive.

China is Australia’s largest trading partner so the health of the Chinese economy is a major influence on the value of the Australian Dollar (AUD). When the Chinese economy is doing well it purchases more raw materials, goods and services from Australia, lifting demand for the AUD, and pushing up its value. The opposite is the case when the Chinese economy is not growing as fast as expected. Positive or negative surprises in Chinese growth data, therefore, often have a direct impact on the Australian Dollar and its pairs.

Iron Ore is Australia’s largest export, accounting for $118 billion a year according to data from 2021, with China as its primary destination. The price of Iron Ore, therefore, can be a driver of the Australian Dollar. Generally, if the price of Iron Ore rises, AUD also goes up, as aggregate demand for the currency increases. The opposite is the case if the price of Iron Ore falls. Higher Iron Ore prices also tend to result in a greater likelihood of a positive Trade Balance for Australia, which is also positive of the AUD.

The Trade Balance, which is the difference between what a country earns from its exports versus what it pays for its imports, is another factor that can influence the value of the Australian Dollar. If Australia produces highly sought after exports, then its currency will gain in value purely from the surplus demand created from foreign buyers seeking to purchase its exports versus what it spends to purchase imports. Therefore, a positive net Trade Balance strengthens the AUD, with the opposite effect if the Trade Balance is negative.

- Gold rises post-Powell's Jackson Hole comments on potential September policy easing.

- Powell cites inflation control, labor market concerns; Daly echoes rate cut expectations.

- US Durable Goods Orders jump 9.9% in July, showing economic strength; Middle East tensions boost Gold's appeal.

- US 10-year yields reach 3.81%; traders scale back on 50 bps cut bets, await Nonfarm Payrolls for more insights.

Gold extended its gains on Monday amid increasing bets that the US Federal Reserve (Fed) will begin to ease policy in September. This is a certainty following Fed Chair Jerome Powell's speech at Jackson Hole, when he said, “The time has come for policy to adjust." The XAU/USD trades at $2,516 per troy ounce, up by a minimal 0.16%.

Last Friday, Jerome Powell said that he was confident that inflation was on its way toward the Fed’s 2% goal and expressed worries about a weaker labor market, indicating that employment risks were skewed to the upside.

Powell gave the green light on interest rate cuts, adding that further cooling in the labor market is unwelcome.

Powell’s comments were echoed by San Francisco Fed President Mary Daly, who said, “The time to adjust policy is upon us. It's hard to imagine anything could derail a September rate cut.”

Daly added that it’s premature to know the size of interest rate cuts, yet stated that if the economy weakens “more than anticipated, we will need to be more aggressive.”

US Durable Goods Orders jumped from a -6.9% contraction in June to a 9.9% MoM expansion in July, exceeding the forecast for a 4% increase. This was the most significant gain since May 2020, hinting the economy is still resilient despite showing some signs of slowing down.

Bullion prices got a lifeline from rising tensions in the Middle East as the Israel-Hezbollah conflict escalated over the weekend. Fears that the conflict could broaden would be positive for the golden metal.

US Treasury bond yields had recovered as the US 10-year benchmark note climbed one basis point to 3.81%. Meanwhile, traders decreased their bets that the Fed would cut rates by 50 bps at the September meeting.

The CME FedWatch Tool shows that market participants had fully priced in a 25 bps cut, while odds for a larger size stand at 30%, down from 36.5 % last Friday.

Now, with the Fed shifting toward the jobs market, the August Nonfarm Payrolls report will be the last piece of the puzzle to determine the size of the cut.

Daily digest market movers: Gold price advances ahead of next week’s US inflation report

- If US economic data continues to be soft, the Gold price uptrend will remain, which would increase speculation about a bigger rate cut.

- On Tuesday, the US Conference Board will reveal Consumer Confidence for August, which is expected to improve from 100.3 to 100.6.

- Gross Domestic Product (GDP) figures for Q2 in the second estimate are expected to improve from 1.4% to 2.8%.

- On Friday, the Fed’s favorite inflation gauge, the Core Personal Consumption Expenditures (PCE) Price Index, will be revealed. It is expected to rise from 2.6% to 2.7% YoY.

Technical outlook: Gold’s uptrend is intact as buyers eye $2,550

Gold’s uptrend remains in play, yet buyers have failed to reclaim the all-time high (ATH) of $2,531. A breach of the latter will expose the $2,550 mark, followed by the $2,600 mark.

On the flip side, if Gold achieves a daily close below $2,500, this will sponsor a test of the previous all-time high (ATH) of $2,483. If surpassed, Gold’s next support would be the May 20 peak of $2,450, followed by the 50-day Simple Moving Average (SMA) at $2,406.

Gold FAQs

Gold has played a key role in human’s history as it has been widely used as a store of value and medium of exchange. Currently, apart from its shine and usage for jewelry, the precious metal is widely seen as a safe-haven asset, meaning that it is considered a good investment during turbulent times. Gold is also widely seen as a hedge against inflation and against depreciating currencies as it doesn’t rely on any specific issuer or government.

Central banks are the biggest Gold holders. In their aim to support their currencies in turbulent times, central banks tend to diversify their reserves and buy Gold to improve the perceived strength of the economy and the currency. High Gold reserves can be a source of trust for a country’s solvency. Central banks added 1,136 tonnes of Gold worth around $70 billion to their reserves in 2022, according to data from the World Gold Council. This is the highest yearly purchase since records began. Central banks from emerging economies such as China, India and Turkey are quickly increasing their Gold reserves.

Gold has an inverse correlation with the US Dollar and US Treasuries, which are both major reserve and safe-haven assets. When the Dollar depreciates, Gold tends to rise, enabling investors and central banks to diversify their assets in turbulent times. Gold is also inversely correlated with risk assets. A rally in the stock market tends to weaken Gold price, while sell-offs in riskier markets tend to favor the precious metal.

The price can move due to a wide range of factors. Geopolitical instability or fears of a deep recession can quickly make Gold price escalate due to its safe-haven status. As a yield-less asset, Gold tends to rise with lower interest rates, while higher cost of money usually weighs down on the yellow metal. Still, most moves depend on how the US Dollar (USD) behaves as the asset is priced in dollars (XAU/USD). A strong Dollar tends to keep the price of Gold controlled, whereas a weaker Dollar is likely to push Gold prices up.

- The Canadian Dollar rose another quarter percent against the Greenback.

- Canada has a fresh GDP update looming ahead later in the week.

- Markets are recovering their composure after a Fed splurge last week.

The Canadian Dollar (CAD) is broadly higher on Monday, kicking off the new trading week with an across-the-board recovery thanks to easing bidding pressure in other categories rather than any bullish tilt within the CAD itself. The CAD rallied one quarter of one percent against the Greenback, tipping into a fresh multi-month high.

Canada remains absent from the economic calendar in any meaningful capacity until Friday. Canadian Gross Domestic Product (GDP) figures are due at the end of the week, but market flows are likely to get swamped out by a fresh print of US Personal Consumption Expenditure (PCE) inflation figures due at the same time.

Daily digest market movers

- The CAD rallied across the board on Monday, extending recent gains against the Greenback into a fourth straight week.

- CAD GDP figures are slated for Friday, with a quiet week on the cards in the meantime.

- US Durable Goods Orders gave an unexpected surge on Monday, keep risk appetite well-bid and limiting a Greenback rally.

- Despite topside risk flows, markets remain tepid as investors recover from a rate-cut splurge after Federal Reserve (Fed) Chairman Jerome Powell all but confirmed an initial rate cut on September 18.

- US PCE inflation figures are due to drop on markets on Friday, and forecasts are currently expecting the pace of consumer inflation pressures to hold steady at current levels.

Canadian Dollar price forecast

The Canadian Dollar (CAD) has found a fresh bullish push against the Greenback on Monday, kicking off a fourth straight week of gains against the US Dollar. USD/CAD traded into its lowest bids since March of this year as the CAD continues to gain ground against the USD, extending a fundamentals-based tailspin down the charts even further below the 200-day Exponential Moving Average (EMA) at 1.3625.

USD/CAD has ground its way through most of early 2024’s congestion zone between 1.3600 and 1.3400. If short momentum is unable to remain on top of things, a resurgence in bidders could see the pair climb quickly back into July’s price range above 1.3600.

USD/CAD daily chart

Canadian Dollar FAQs

The key factors driving the Canadian Dollar (CAD) are the level of interest rates set by the Bank of Canada (BoC), the price of Oil, Canada’s largest export, the health of its economy, inflation and the Trade Balance, which is the difference between the value of Canada’s exports versus its imports. Other factors include market sentiment – whether investors are taking on more risky assets (risk-on) or seeking safe-havens (risk-off) – with risk-on being CAD-positive. As its largest trading partner, the health of the US economy is also a key factor influencing the Canadian Dollar.

The Bank of Canada (BoC) has a significant influence on the Canadian Dollar by setting the level of interest rates that banks can lend to one another. This influences the level of interest rates for everyone. The main goal of the BoC is to maintain inflation at 1-3% by adjusting interest rates up or down. Relatively higher interest rates tend to be positive for the CAD. The Bank of Canada can also use quantitative easing and tightening to influence credit conditions, with the former CAD-negative and the latter CAD-positive.

The price of Oil is a key factor impacting the value of the Canadian Dollar. Petroleum is Canada’s biggest export, so Oil price tends to have an immediate impact on the CAD value. Generally, if Oil price rises CAD also goes up, as aggregate demand for the currency increases. The opposite is the case if the price of Oil falls. Higher Oil prices also tend to result in a greater likelihood of a positive Trade Balance, which is also supportive of the CAD.

While inflation had always traditionally been thought of as a negative factor for a currency since it lowers the value of money, the opposite has actually been the case in modern times with the relaxation of cross-border capital controls. Higher inflation tends to lead central banks to put up interest rates which attracts more capital inflows from global investors seeking a lucrative place to keep their money. This increases demand for the local currency, which in Canada’s case is the Canadian Dollar.

Macroeconomic data releases gauge the health of the economy and can have an impact on the Canadian Dollar. Indicators such as GDP, Manufacturing and Services PMIs, employment, and consumer sentiment surveys can all influence the direction of the CAD. A strong economy is good for the Canadian Dollar. Not only does it attract more foreign investment but it may encourage the Bank of Canada to put up interest rates, leading to a stronger currency. If economic data is weak, however, the CAD is likely to fall.

Federal Reserve (Fed) Bank of San Francisco Mary Daly hit newswires on Monday, cautioning that despite the clear signs of the need for rate adjustments, markets shouldn't run too far, too fast with expectations about the size and frequency.

Key highlights

The time to adjust policy is upon us. It's hard to imagine anything could derail sept rate cut.

I don't want to keep making policy tighter, as inflation comes down.

The labor market is completely in balance.

I am not hearing signs that firms are poised for layoffs.

I don't see signs of abrupt weakening in the labor market.

I don't see warning signs of weakness, but I want to be sure to adjust policy as we go.

It is too early to know how big rate cuts will be.

The most likely outcome is that we continue to get gradual inflation slowing, and a sustainable pace of labor market growth.

It is reasonable to adjust policy at normal cadence if the economy develops as expected.

If the economy weakens more than anticipated, we would need to be more aggressive.

It is reasonable to adjust policy at normal cadence if the economy develops as expected.

If the economy weakens more than anticipated, we would need to be more aggressive.

I do not want to see the labor market weaken further.

We want the labor market to stay about where it is. We need to adjust policy rate to keep it there.

I don't want to declare we are on the path to neutral.

We could see the neutral real rate to be as high as 1%.

We have a long way to go, and even after cutting rates we will be restrictive.

I expect growth to be at or a little below trend.

We are far from declaring victory, but we will get inflation to the goal.

The Greenback managed to regain composure and leave behind part of the recent multi-day bearish move, which was accentuated following Chair Powell’s speech at Jackson Hole. While an interest rate cut by the Fed in September looks largely priced in, there are still significant data releases that could either reinforce that move or undermine it.

Here is what you need to know on Tuesday, August 27:

The US Dollar Index (DXY) retreated to new lows near 100.50 earlier on Monday, just to reverse that move and rebound to the proximity of the 101.00 barrier later in the day. The Conference Board will publish its Consumer Confidence gauge on August 27, seconded by the FHFA’s House Price Index.

The Greenback’s mild rebound seems to have been enough to spark a corrective knee-jerk in EUR/USD to the 1.1150 zone at the beginning of the week. On August 27, the final Q2 GDP Growth Rate in Germany is due.

GBP/USD traded within a tight range, eventually settling around the 1.3200 neighbourhood following a multi-day steep advance. The CBI Distributive Trades will be published on August 27.

USD/JPY alternated gains with losses after briefly dropping to three-week lows near 143.40 on the back of rising US yields and a decent bounce in the US Dollar. The next data release on the Japanese docket will be the final Coincident Index and Leading Economic Index on August 28.

The resurgence of the upside impulse in the Greenback favoured some selling pressure in the risk-associated space, motivating AUD/USD to give away some of its sharp advance seen last Friday. The next key event in Australia will be the RBA’s Monthly CPI Indicator, due on August 28.

Escalating geopolitical concerns and prospects of supply disruptions in Libya underpinned the continuation of the rebound in prices of WTI beyond the $77.00 mark per barrel on Monday.

Gold prices traded at shouting distance from their recent record levels, maintaining the trade above the $2,500 mark per ounce troy amidst rising geopolitical fears in the Middle East and hopes of rate cuts by the Fed in September. Silver prices surpassed the $30.00 mark per ounce to clinch new six-week highs.

- Dow Jones taps a new record high despite thin volumes.

- Moves in equities remain limited as investors recover from Fed splurge.

- Key US inflation data looms large at the end of the week.

The Dow Jones Industrial Average (DJIA) slipped higher to test a new record high of 41,419.65 on Monday, but investors are still recovering from last Friday’s surge after the Federal Reserve (Fed) all but confirmed that a new rate-cutting cycle would kick off in September.

US Durable Goods Orders helped to keep physical production stocks bid on Monday despite a general decline in the usual darling tech sector. US Durable Goods Order in July rallied a surprising 9.9% MoM, well above the forecast 4.0% and entirely reversing the previous month’s revised -6.9% contraction.

Despite the upswing on Durable Goods Orders, some trepidation remains; excluding Transportation spending, Durable Goods Orders actually contracted -0.2% MoM, worse than the forecast 0.0% and the previous month’s tepid 0.1%, which was revised down from 0.5%.

Most of the trading week will be a quiet affair on the economic calendar. Q2 US Gross Domestic Product (GDP) figures are slated for Thursday, but are broadly expected to hold steady at 2.8% on an annualized basis. Friday could be a kicker for markets that are increasingly focused on the timing and pace of rate cuts from the Fed, with July’s US core Personal Consumption Expenditure - Price Index (PCE) inflation print set to hold steady at 0.2% MoM. The YoY PCE inflation figure is actually expected to tick upwards to 2.7% from 2.6%, but investors are confident that inflation has made enough progress towards the Fed’s 2% target that it will count as “close enough” to still keep the way open to a first rate cut on September 18.

Dow Jones news

Caterpillar (CAT) is moving higher on Monday in sharp contrast to the wider market. The NASDAQ and S&P 500 sold off on Monday morning, while Caterpillar and a number of other Dow Jones index stocks gained ground. The Dow, in fact, reached yet another all-time high at 41,420 on Monday, following last week's decent Dow performance.

Read more: Caterpillar helps Dow Jones buck tide at start of eventful week

Dow Jones price forecast

Intraday price action sees some churn on an overall quiet Monday. Bids managed to clip into a fresh all-time high above 41,400.00 to kick off the new trading week, but the overall day is still tilted toward the low side as bulls try to run on empty.

The Dow Jones has chalked in an impressive 7.9% win streak since the first week of August, climbing from a swing low to 38,382.90 to etch in a fresh all-time high at 41,419.65. Despite the impressive run that tilted entirely into the bullish side, momentum is set to drain out of the index quickly as bidders run out of runway. The Dow Jones is poised for a relief pullback towards the 50-day Exponential Moving Average (EMA) at 39,946.29.

Dow Jones daily chart

Dow Jones FAQs

The Dow Jones Industrial Average, one of the oldest stock market indices in the world, is compiled of the 30 most traded stocks in the US. The index is price-weighted rather than weighted by capitalization. It is calculated by summing the prices of the constituent stocks and dividing them by a factor, currently 0.152. The index was founded by Charles Dow, who also founded the Wall Street Journal. In later years it has been criticized for not being broadly representative enough because it only tracks 30 conglomerates, unlike broader indices such as the S&P 500.

Many different factors drive the Dow Jones Industrial Average (DJIA). The aggregate performance of the component companies revealed in quarterly company earnings reports is the main one. US and global macroeconomic data also contributes as it impacts on investor sentiment. The level of interest rates, set by the Federal Reserve (Fed), also influences the DJIA as it affects the cost of credit, on which many corporations are heavily reliant. Therefore, inflation can be a major driver as well as other metrics which impact the Fed decisions.

Dow Theory is a method for identifying the primary trend of the stock market developed by Charles Dow. A key step is to compare the direction of the Dow Jones Industrial Average (DJIA) and the Dow Jones Transportation Average (DJTA) and only follow trends where both are moving in the same direction. Volume is a confirmatory criteria. The theory uses elements of peak and trough analysis. Dow’s theory posits three trend phases: accumulation, when smart money starts buying or selling; public participation, when the wider public joins in; and distribution, when the smart money exits.

There are a number of ways to trade the DJIA. One is to use ETFs which allow investors to trade the DJIA as a single security, rather than having to buy shares in all 30 constituent companies. A leading example is the SPDR Dow Jones Industrial Average ETF (DIA). DJIA futures contracts enable traders to speculate on the future value of the index and Options provide the right, but not the obligation, to buy or sell the index at a predetermined price in the future. Mutual funds enable investors to buy a share of a diversified portfolio of DJIA stocks thus providing exposure to the overall index.

- US Dollar recovers after declining on Friday due to Powell's dovish remarks.

- Markets anticipate 100 bps of easing by year-end and 200 bps total over the next 12 months.

- Focus turns to PCE data later this week.

The US Dollar, measured by the US Dollar Index (DXY), regained some ground on Monday, hovering around 101.00 after it had plummeting last week. Friday’s decline was attributed to Federal Reserve (Fed) Chair Jerome Powell's dovish remarks at the Jackson Hole Symposium, hinting at a potential shift toward a looser monetary policy stance by the central bank. This, in turn, caused the 10-year US yield to dip beneath 3.8%, which weighed heavily on the USD.

Despite positive economic growth that exceeds expectations, the market's eagerness for aggressive monetary easing appears misplaced. The current situation warrants caution, as the totality of data points toward a disconnect between economic fundamentals and market pricing.

Daily digest market movers: US Dollar remains vulnerable following Powell's dovish remarks

- Markets digest Powell’s dovish Jackson Hole speech with further easing expected.

- Powell signaled a shift in Fed policy, stating that "the time has come for policy to adjust."

- He also emphasized the importance of the labor market, noting an "unmistakable" slowdown.

- 100 bps of easing is predicted by year-end, with 200 bps total over the next 12 months.

- Odds of a 50 bps cut in September are 30-35%, contingent on upcoming data.

- Market participants await the August NFP report for further guidance on the Fed's path.

- This Friday’s Personal Consumption Expenditures (PCE) figures from July will be key.

DXY technical outlook: DXY finds support, bullish momentum might build

The DXY index has found support at its lowest levels since December, indicating a temporary pause in selling pressure. The Relative Strength Index (RSI) remains deep in oversold territory, suggesting that there is potential for further upward corrective movements.

The Moving Average Convergence Divergence (MACD) is exhibiting steady red bars, aligning with the RSI and providing additional evidence of potential upward momentum as there is more room to correct. That being said, there are no clear signs of a reversal and the DXY is exposed for further downside.

Key support levels to monitor are 100.50, 100.30 and 100.00, while resistance levels to watch are 101.00, 101.50 and 101.80.

US Dollar FAQs

The US Dollar (USD) is the official currency of the United States of America, and the ‘de facto’ currency of a significant number of other countries where it is found in circulation alongside local notes. It is the most heavily traded currency in the world, accounting for over 88% of all global foreign exchange turnover, or an average of $6.6 trillion in transactions per day, according to data from 2022. Following the second world war, the USD took over from the British Pound as the world’s reserve currency. For most of its history, the US Dollar was backed by Gold, until the Bretton Woods Agreement in 1971 when the Gold Standard went away.

The most important single factor impacting on the value of the US Dollar is monetary policy, which is shaped by the Federal Reserve (Fed). The Fed has two mandates: to achieve price stability (control inflation) and foster full employment. Its primary tool to achieve these two goals is by adjusting interest rates. When prices are rising too quickly and inflation is above the Fed’s 2% target, the Fed will raise rates, which helps the USD value. When inflation falls below 2% or the Unemployment Rate is too high, the Fed may lower interest rates, which weighs on the Greenback.

In extreme situations, the Federal Reserve can also print more Dollars and enact quantitative easing (QE). QE is the process by which the Fed substantially increases the flow of credit in a stuck financial system. It is a non-standard policy measure used when credit has dried up because banks will not lend to each other (out of the fear of counterparty default). It is a last resort when simply lowering interest rates is unlikely to achieve the necessary result. It was the Fed’s weapon of choice to combat the credit crunch that occurred during the Great Financial Crisis in 2008. It involves the Fed printing more Dollars and using them to buy US government bonds predominantly from financial institutions. QE usually leads to a weaker US Dollar.

Quantitative tightening (QT) is the reverse process whereby the Federal Reserve stops buying bonds from financial institutions and does not reinvest the principal from the bonds it holds maturing in new purchases. It is usually positive for the US Dollar.

- Mexican Peso slips as investors worry about the potential approval of controversial judiciary reforms, which could increase political risks.

- Morena's supermajority in Congress heightens fears of constitutional changes, leading to greater concentration of power and higher risk premiums.

- Dovish comments from Banxico Deputy Governor Galia Borja add pressure.

The Mexican Peso begins the week on the back foot, reversing most of last Friday’s gains. Losses of over 1.80% are seen in the Peso amid fears that the Mexican Congress could approve the Judiciary Reform bill and dovish comments from Deputy Governor Galia Borja. At the time of writing, the USD/MXN trades at 19.42 after bouncing off a daily low of 19.08.

Last Friday, the Instituto Nacional Electoral (INE) approved the Morena ruling party's supermajority in the Mexican Congress, raising investors' concerns that approving controversial changes to the Mexican Constitution could increase the country’s risks.

This is one of Monday's main drivers of USD/MXN price action. Now that Morena controls the lower house, the risks of the judiciary reform being approved have heightened, weighing on the Mexican Peso. Some analysts cited by El Financiero asserted that constitutional changes could lead to a greater concentration of power in the executive and impact the state of law.

Last week, Morgan Stanley recommended to its clients not to invest in shares in Mexico, citing fears that the judiciary reform could increase risk premiums in the country.

On Monday, Bank of Mexico Deputy Governor Galia Borja was interviewed by El Economista. She said that since June’s decision when the Governing Council left rates unchanged at 11.00%, they already had some elements about an economic slowdown in the second quarter.

“In the August decision, it was confirmed that economic activity was weakening compared to what we expected, which was effectively confirmed with the GDP data for the 2nd quarter,” said Borja.

She said that March and August rate cuts do not imply the abandonment of restrictive policy. Borja added that “the fact that we are adjusting it as has happened in March and August (of 2024) does not mean that we are going to the neutral or accommodative territory. That will take some time. So, from now on, there will still be another period in which the restrictive monetary stance will continue.”

Mexico’s economic docket will remain light. The Balance of Trade is expected to be released on August 27.

Across the border, Federal Reserve (Fed) Chair Jerome Powell, giving the green light last week to begin easing monetary policy, hurt the Greenback against most G7 FX currencies. Nevertheless, the US Dollar has gained some ground against the emerging market Mexican Peso.

Daily digest market movers: Mexican Peso depreciates also on geopolitical risks

- Another driver that weakened the Peso was the escalation of the Israel-Hezbollah conflict in the Middle East.

- Mexico's Balance of Trade is expected to show a deficit of $-1.47 billion in July, wider than June’s $-1.03 billion.

- Traders will eye the release of US Conference Board Consumer Confidence for August, Fed speakers, the release of Q2’s 2024 GDP, and the Fed’s preferred inflation gauge, the Core Personal Consumption Expenditures Price Index (PCE).

- Data from the Chicago Board of Trade (CBOT) suggests the Fed will cut at least 97 basis points (bps) according to the fed funds rate futures contract for December 2024.

Technical outlook: Mexican Peso weakens as USD/MXN jumps above 19.30

The USD/MXN daily chart suggests the uptrend remains intact, though buyers need to lift the exchange rate above last week’s peak at 19.53, which could exacerbate a rally to the 20.00 psychological figure. If those levels are cleared, the next stop would be the year-to-date (YTD) high at 20.22.

Conversely, if USD/MXN tumbles below 19.00, this could pave the way for a leg-down. The first support would be the August 19 low of 18.59, followed by the 50-day Simple Moving Average (SMA) at 18.48.

Mexican Peso FAQs

The Mexican Peso (MXN) is the most traded currency among its Latin American peers. Its value is broadly determined by the performance of the Mexican economy, the country’s central bank’s policy, the amount of foreign investment in the country and even the levels of remittances sent by Mexicans who live abroad, particularly in the United States. Geopolitical trends can also move MXN: for example, the process of nearshoring – or the decision by some firms to relocate manufacturing capacity and supply chains closer to their home countries – is also seen as a catalyst for the Mexican currency as the country is considered a key manufacturing hub in the American continent. Another catalyst for MXN is Oil prices as Mexico is a key exporter of the commodity.

The main objective of Mexico’s central bank, also known as Banxico, is to maintain inflation at low and stable levels (at or close to its target of 3%, the midpoint in a tolerance band of between 2% and 4%). To this end, the bank sets an appropriate level of interest rates. When inflation is too high, Banxico will attempt to tame it by raising interest rates, making it more expensive for households and businesses to borrow money, thus cooling demand and the overall economy. Higher interest rates are generally positive for the Mexican Peso (MXN) as they lead to higher yields, making the country a more attractive place for investors. On the contrary, lower interest rates tend to weaken MXN.

Macroeconomic data releases are key to assess the state of the economy and can have an impact on the Mexican Peso (MXN) valuation. A strong Mexican economy, based on high economic growth, low unemployment and high confidence is good for MXN. Not only does it attract more foreign investment but it may encourage the Bank of Mexico (Banxico) to increase interest rates, particularly if this strength comes together with elevated inflation. However, if economic data is weak, MXN is likely to depreciate.

As an emerging-market currency, the Mexican Peso (MXN) tends to strive during risk-on periods, or when investors perceive that broader market risks are low and thus are eager to engage with investments that carry a higher risk. Conversely, MXN tends to weaken at times of market turbulence or economic uncertainty as investors tend to sell higher-risk assets and flee to the more-stable safe havens.

USD/JPY plunged 2.2% to 144.37 last week. Bank of Japan Governor Kazuo Ueda stood by the decision to keep hiking rates, DBS Senior FX Strategist Philip Wee notes.

Ueda stands by the decision to keep hiking rates

“USD/JPY plunged 2.2% to 144.37 last week, opening the door to retesting the 141.70 low in early August.”

“At the special parliamentary hearing on August 23, Bank of Japan Governor Kazuo Ueda stood by the decision to keep hiking rates if the central bank’s median economic forecasts were met or exceeded.”

“Ueda attributed the brief market volatility from July 11 to August 5 to rising fears of a US recession from the Fed’s rate cut bias on rising joblessness, not the BOJ’s rate hike.”

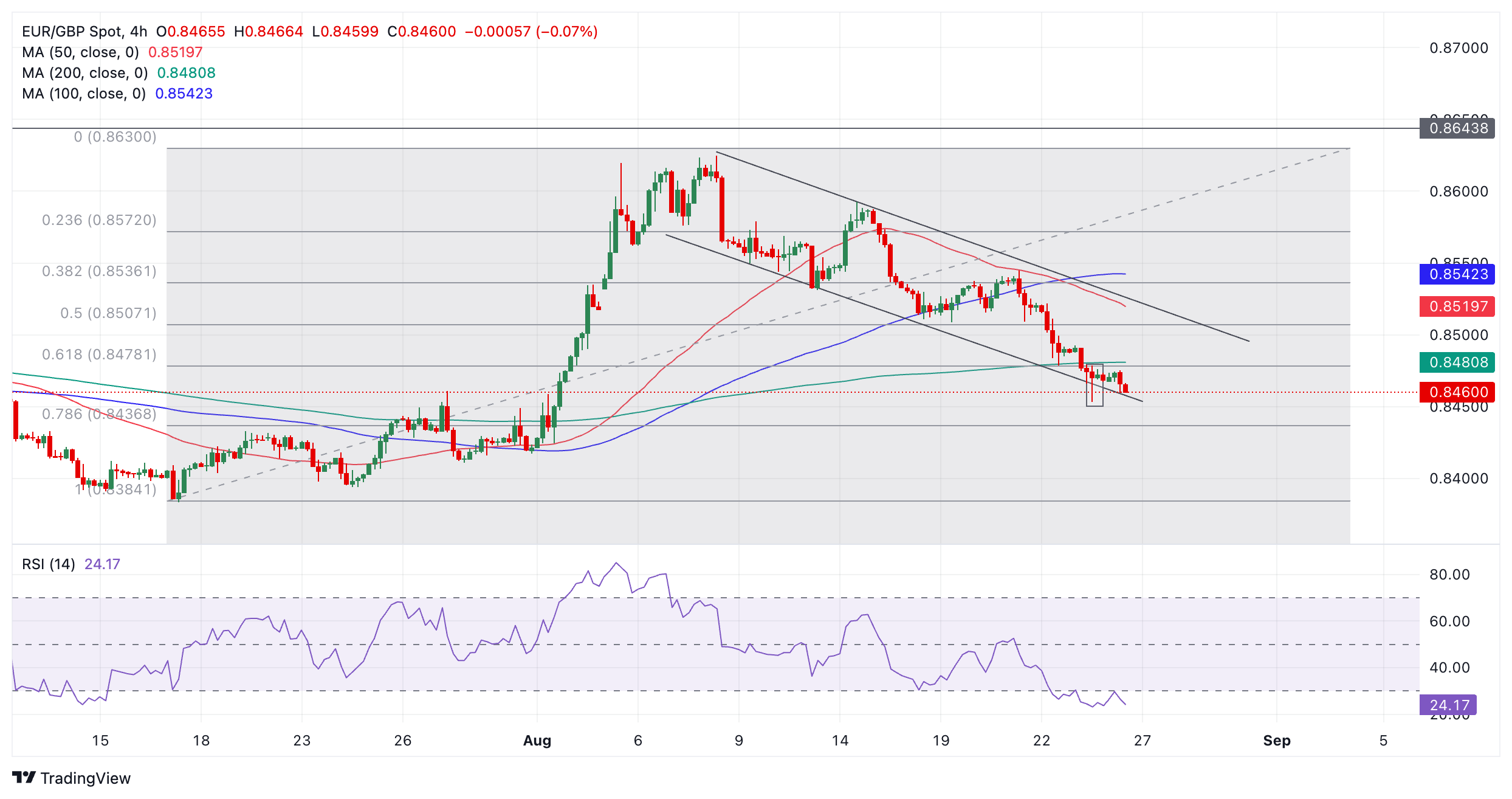

- EUR/GBP continues weak, bears eye the 0.8450 support.

- RSI flattened around 42, indicating an easing selling momentum.

- MACD shows rising red bars, suggesting a steady bearish pressure.

In Monday's session, the EUR/GBP pair extended its losses, dipping further below the 0.8500 support level to land at 0.8460.

The daily Relative Strength Index (RSI) has fallen to 42, indicating a shift in favor of the sellers but its slope flattened. The Moving Average Convergence Divergence (MACD) is printing rising red bars, suggesting that the bearish pressure is steady.

Volume has declined in recent sessions, indicating a lack of conviction among market participants. On the other hand, the pair has formed a series of lower lows suggesting that the bears are currently in command but seem to be struggling around the 0.8450-08500 area. In that sense after four sessions of losses and with momentum flattening, the pair might enter into consolidation as the sellers take a breather.

EUR/GBP daily chart

USD/JPY fell in response to Powell’s dovish remarks last Fri and extended its decline this morning following the escalation in geopolitical tensions between Israel and Hezbollah over the weekend, OCBC FX strategist Frances Cheung and Christopher Wong note.

Remain bias for downside play in USD/JPY

“Bullish momentum on daily chart faded while RSI fell. Risks skewed to the downside. Support at 142, 140.40 (61.8% fibo). Resistance at 144.50 (50% fibo retracement of 2023 low to 2024 high), 147.20 levels (21 DMA). We remain bias for downside play in USD/JPY.”

“Governor Ueda’s comments in parliament last Fri reinforced the view that BoJ rate hikes remain on the table while Powell’s ‘time has come’ speech at Jackson Hole reinforced the view that Fed’s next move is a cut.”

“Broader direction of travel for USD/JPY has changed as Fed-BoJ policies shifted from divergence to convergence and this should continue to underpin the downside for USD/JPY. In addition, geopolitical concerns is another factor that could add to support for safe-haven JPY.”

- Exhaustion signals as GBP/USD stalls after a 400-pip rally, with RSI indicating overbought conditions.

- A daily close below 1.3200 could trigger a pullback, with support levels at 1.3130, 1.3100, and further down at 1.3043.

- If the pair breaks above 1.3230, resistance levels to watch are 1.3250 and the psychological 1.3300 mark.

The Pound Sterling begins the week on a positive note, yet remains hovering around the 1.3200 figure, unable to break last Friday new year-to-date (YTD) high of 1.3230, and trades at 1.3204 almost flat.

GBP/USD Price Forecast: Technical outlook

Exhaustion is the name of the game for the GBP/USD. After achieving a 400-pip run that started on August 15th, the pair has failed to extend its gains after hitting a multi-year peak at 1.3230. Today’s price action is forming a ‘doji,’ which indicates indecision amongst buyers and sellers.

Momentum shows buyers are losing steam as the Relative Strength Index (RSI) remains overbought. Therefore, if the GBP/USD achieves a daily close below 1.3200, that could pave the way for a deeper pullback.

In that outcome, the first support would be the August 22 high at 1.3130 before the pair slides to 1.3100. In further weakness, the GBP/USD might hit 1.3043, and July’s 17 daily high turned support.

On the other hand, if GBP/USD rises past 1.3230, the next resistance would be 1.3250, followed by the 1.3300 mark.

GBP/USD Price Action – Daily Chart

British Pound PRICE Today

The table below shows the percentage change of British Pound (GBP) against listed major currencies today. British Pound was the strongest against the New Zealand Dollar.

| USD | EUR | GBP | JPY | CAD | AUD | NZD | CHF | |

|---|---|---|---|---|---|---|---|---|

| USD | 0.12% | 0.09% | -0.04% | -0.32% | 0.22% | 0.21% | -0.14% | |

| EUR | -0.12% | -0.09% | -0.15% | -0.43% | 0.00% | 0.10% | -0.25% | |

| GBP | -0.09% | 0.09% | -0.17% | -0.40% | 0.09% | 0.13% | -0.22% | |

| JPY | 0.04% | 0.15% | 0.17% | -0.26% | 0.34% | 0.47% | -0.02% | |

| CAD | 0.32% | 0.43% | 0.40% | 0.26% | 0.53% | 0.59% | 0.17% | |

| AUD | -0.22% | -0.01% | -0.09% | -0.34% | -0.53% | 0.09% | -0.26% | |

| NZD | -0.21% | -0.10% | -0.13% | -0.47% | -0.59% | -0.09% | -0.36% | |

| CHF | 0.14% | 0.25% | 0.22% | 0.02% | -0.17% | 0.26% | 0.36% |

The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the British Pound from the left column and move along the horizontal line to the US Dollar, the percentage change displayed in the box will represent GBP (base)/USD (quote).

Fed cut expectations sent the DXY Index to 100.72 last Friday, near December’s 100.62 low, but was still above the 99.58 low in July 2023, DBS Senior FX Strategist Philip Wee notes.

Still above the 99.58 low in July 2023

“Fed Chair Jerome Powell announced at Jackson Hole that the time has come to adjust monetary policy. Powell was crystal about the Fed’s shift from pulling down inflation from its peak towards preventing a further cooling in the labour market, adding that the Fed had ample room to respond to any risks here.”

“In the short term, the oversold DXY could consolidate on surprises in this week’s US data, especially the PCE deflator on August 30, pushing back the futures market’s bet for a 50 bps cut. However, we will assess the DXY’s prospects to trade below 100 over the medium term. The US monthly jobs report on September 6 will be critical.”

“Apart from the telegraphed rate cut in September, the Fed’s revisions to the Summary of Economic Projections will be significant. In June, the Fed projected 1-2 rate cuts in 2H24, followed by 200 bps of cuts over 2025-2026.”

- AUD/USD drops from 0.6800 with Aussie inflation under the spotlight.

- The Fed seems prepared to begin reducing interest rates from September.

- The near-term outlook of the US Dollar remains weak.

The AUD/USD pair falls from the monthly high of 0.6800 in Monday’s American session. The Aussie asset drops as the US Dollar (USD) edges higher. While the near-term outlook of the US Dollar remains vulnerable as the Federal Reserve (Fed) is widely anticipated to start reducing interest rates from the September meeting.

The US Dollar Index (DXY), which tracks the Greenback’s value against six major currencies, rises slightly to near 100.90 from the annual low of 100.53.

While the Fed seems certain to cut interest rates in September, traders remain split over the likely size. According to the CME FedWatch tool, 30-day Federal Funds futures pricing data shows that the likelihood of a 50-basis point (bps) interest-rate reduction is 36.5%, while rest of the bets are in favor of a 25-bps rate cut.

Meanwhile, the Australian Dollar (AUD) will be influenced by the monthly Consumer Price Index (CPI) data for July, which will be published on Wednesday. Economists estimated that price pressures declined sharply to 3.4% from 3.8% in June. An expected decline in the inflation data would bring expectations of interest rate cuts to the table.

AUD/USD trades close to the monthly high of 0.6800 on a daily timeframe. The near-term outlook of the Aussie asset remains firm as the 10-day Moving Average (EMA) near 0.6700 is sloping higher. The 14-period Relative Strength Index (RSI) oscillates in the bullish range of 60.00-80.00, suggesting a strong upside momentum.

For a fresh upside, a decisive move above the round-level resistance of 0.6800 will push the asset higher to 0.6840, the higher level seen this year. A breach of the latter would drive the asset towards December 2023 high of 0.6870.

In an alternate scenario, a downside move below August 19 low of 0.6660 will expose the asset to June 28 low of 0.6620 and June 17 low of 0.6585.

AUD/USD daily chart

Australian Dollar FAQs

One of the most significant factors for the Australian Dollar (AUD) is the level of interest rates set by the Reserve Bank of Australia (RBA). Because Australia is a resource-rich country another key driver is the price of its biggest export, Iron Ore. The health of the Chinese economy, its largest trading partner, is a factor, as well as inflation in Australia, its growth rate and Trade Balance. Market sentiment – whether investors are taking on more risky assets (risk-on) or seeking safe-havens (risk-off) – is also a factor, with risk-on positive for AUD.

The Reserve Bank of Australia (RBA) influences the Australian Dollar (AUD) by setting the level of interest rates that Australian banks can lend to each other. This influences the level of interest rates in the economy as a whole. The main goal of the RBA is to maintain a stable inflation rate of 2-3% by adjusting interest rates up or down. Relatively high interest rates compared to other major central banks support the AUD, and the opposite for relatively low. The RBA can also use quantitative easing and tightening to influence credit conditions, with the former AUD-negative and the latter AUD-positive.

China is Australia’s largest trading partner so the health of the Chinese economy is a major influence on the value of the Australian Dollar (AUD). When the Chinese economy is doing well it purchases more raw materials, goods and services from Australia, lifting demand for the AUD, and pushing up its value. The opposite is the case when the Chinese economy is not growing as fast as expected. Positive or negative surprises in Chinese growth data, therefore, often have a direct impact on the Australian Dollar and its pairs.

Iron Ore is Australia’s largest export, accounting for $118 billion a year according to data from 2021, with China as its primary destination. The price of Iron Ore, therefore, can be a driver of the Australian Dollar. Generally, if the price of Iron Ore rises, AUD also goes up, as aggregate demand for the currency increases. The opposite is the case if the price of Iron Ore falls. Higher Iron Ore prices also tend to result in a greater likelihood of a positive Trade Balance for Australia, which is also positive of the AUD.

The Trade Balance, which is the difference between what a country earns from its exports versus what it pays for its imports, is another factor that can influence the value of the Australian Dollar. If Australia produces highly sought after exports, then its currency will gain in value purely from the surplus demand created from foreign buyers seeking to purchase its exports versus what it spends to purchase imports. Therefore, a positive net Trade Balance strengthens the AUD, with the opposite effect if the Trade Balance is negative.

- USD/CHF steadies below 0.8500 as the Fed looks all set to cut interest rates in September.

- The US Dollar fails to recover strongly despite upbeat US Durable Goods Orders data for July.

- Swiss Q2 Employment Level rose to 5.499 million.

The USD/CHF pair hovers below the psychological resistance of 0.8500 in Monday’s American session. The Swiss Franc asset remains in the bearish trajectory as Federal Reserve (Fed) September interest rate cuts have been fully priced in by market participants, which have weighed on the US Dollar (USD) and have improved the appeal of risky assets.

The S&P 500 opens a bullish note on Monday. The US Dollar Index (DXY), which tracks the Greenback’s value against six major currencies, edges higher from the annual low of 100.53. However, its near-term outlook remains bearish.

The confidence of investors that the Fed will begin reducing interest rates in September increased after the speech from Fed Chair Jerome Powell at the Jackson Hole (JH) Symposium on Friday indicated that the central bank is prepared to pivot to policy normalization. Jerome Powell said, “The time has come for policy to adjust.” Fed officials gear up for cutting interest rates as they worry that downside risks to the United States (US) labor market have increased. While policymakers remain confident that inflation is on track to sustainably return to the desired rate of 2%.

Meanwhile, upbeat US Durable Goods Orders data for July failed to prompt a strong recovery in the US Dollar. New orders for Durable Goods that drive core inflation rose at a robust pace of 9.9% from the estimates of 4%. In June, the economic data contracted sharply by 6.9%.

On the Swiss Franc front, the Q2 Employment Level rose to 5.499 million from the prior release of 5.481 million. Though the labor market swelled, it is less likely to impact market speculation for the continuation of interest rate cuts by the Swiss National Bank (SNB) in September.

Swiss Franc FAQs

The Swiss Franc (CHF) is Switzerland’s official currency. It is among the top ten most traded currencies globally, reaching volumes that well exceed the size of the Swiss economy. Its value is determined by the broad market sentiment, the country’s economic health or action taken by the Swiss National Bank (SNB), among other factors. Between 2011 and 2015, the Swiss Franc was pegged to the Euro (EUR). The peg was abruptly removed, resulting in a more than 20% increase in the Franc’s value, causing a turmoil in markets. Even though the peg isn’t in force anymore, CHF fortunes tend to be highly correlated with the Euro ones due to the high dependency of the Swiss economy on the neighboring Eurozone.

The Swiss Franc (CHF) is considered a safe-haven asset, or a currency that investors tend to buy in times of market stress. This is due to the perceived status of Switzerland in the world: a stable economy, a strong export sector, big central bank reserves or a longstanding political stance towards neutrality in global conflicts make the country’s currency a good choice for investors fleeing from risks. Turbulent times are likely to strengthen CHF value against other currencies that are seen as more risky to invest in.

The Swiss National Bank (SNB) meets four times a year – once every quarter, less than other major central banks – to decide on monetary policy. The bank aims for an annual inflation rate of less than 2%. When inflation is above target or forecasted to be above target in the foreseeable future, the bank will attempt to tame price growth by raising its policy rate. Higher interest rates are generally positive for the Swiss Franc (CHF) as they lead to higher yields, making the country a more attractive place for investors. On the contrary, lower interest rates tend to weaken CHF.

Macroeconomic data releases in Switzerland are key to assessing the state of the economy and can impact the Swiss Franc’s (CHF) valuation. The Swiss economy is broadly stable, but any sudden change in economic growth, inflation, current account or the central bank’s currency reserves have the potential to trigger moves in CHF. Generally, high economic growth, low unemployment and high confidence are good for CHF. Conversely, if economic data points to weakening momentum, CHF is likely to depreciate.

As a small and open economy, Switzerland is heavily dependent on the health of the neighboring Eurozone economies. The broader European Union is Switzerland’s main economic partner and a key political ally, so macroeconomic and monetary policy stability in the Eurozone is essential for Switzerland and, thus, for the Swiss Franc (CHF). With such dependency, some models suggest that the correlation between the fortunes of the Euro (EUR) and the CHF is more than 90%, or close to perfect.

BoE Governor Bailey’s comments at Jackson Hole Friday reflected a cautious near-term policy outlook, Scotiabank’s Chief FX Strategist Shaun Osborne notes.

BoE Gov Bailey maintains cautious policy outlook

“Bailey said it was too early to declare victory over inflation with price growth not sustainably back to target. The remarks support market pricing that suggests policymakers are likely to await more data before easing rates again late this year (November). GBP has drifted marginally lower in quiet trade, with UK markets closed for the bank holiday.”

“Cable losses are marginal from Friday’s 1.3230 high (highest since early 2022). Spot is consolidating ahead of minor trend support at 1.3178; weakness below trend support today could prompt a deeper correction in Cable but trend dynamics here remain bullish, suggesting limited scope for weakness for now—and the potential for gains to extend to 1.3330 moving ahead.”

“Cable support looks firm at 1.3125/30.”

EUR rose amid broad USD softness, OCBC FX strategists Frances Cheung and Christopher Wong note.

Potential rising wedge in the making

“Euro was last seen at 1.1164 levels. Bullish momentum on daily chart intact but RSI is in overbought conditions. Potential rising wedge in the making – typically associated with a bearish reversal. We do not rule out the risk of a pullback. Support seen at 1.1140, 1.1090. Resistance at 1.12, 1.1280 levels.”

“On recent ECB speaks, Holzmann said Sep cut is not a foregone conclusion while Chief Economist Lane said that a return to 2% inflation target is not secure yet.”

- EUR/GBP continues declining within a falling channel.

- It has reached oversold levels and could be poised for a recovery.

EUR/GBP continues trickling lower in a falling channel. The declining sequence of peaks and troughs indicates the pair is in a short-term downtrend, and given “the trend is your friend” this biases prices to further weakness.

EUR/GBP 4-hour Chart

The pair has touched down on the lower channel line, a historical support level that previously provided the launch pad for counter-trend reactions higher. There is a chance the same thing could happen again.