- Phân tích

- Tin tức và các công cụ

- Tin tức thị trường

Tin tức thì trường

Major US stock indexes finished trading in negative territory, which was caused by a decrease in shares of Nike (NKE) and The Walt Disney Company (DIS).

The focus was also on the United States data. As it became known, orders for durable goods rose in November, which was the last sign of increased demand for US products this year. Orders for durable goods - products designed for a period of at least three years, such as computers and trucks - increased by 1.3% compared to the previous month to $ 241.36 billion, seasonally adjusted in November. The overall increase was due to orders for airplanes, cars and military equipment. Economists were expecting a 2% increase in orders last month.

However, the final results of the studies submitted by Thomson-Reuters and the Michigan Institute showed that in December US consumers felt less optimistic about the economy than last month. According to the data, in December the consumer sentiment index fell to 95.9 points compared with the final reading for November 98.5 points and the preliminary value for December 96.8 points. It was predicted that the index will be 98 points.

Components of the DOW index showed mixed dynamics (15 in positive territory, 15 in negative territory). Caterpillar Inc. was the growth leader. (CAT, + 0.72%). Outsider were the shares of NIKE, Inc. (NKE, -2.29%).

The S & P indexes have completed trading in different directions. The utilities sector grew most (+ 0.2%). The health sector showed the greatest decline (-0.2%).

At closing:

Dow -0.11% 24,754.06 -28.23

Nasdaq -0.08% 6,959.96 -5.40

S & P -0.05% 2.683.34 -1.23

Sales of new single-family houses in November 2017 were at a seasonally adjusted annual rate of 733,000, according to estimates released jointly today by the U.S. Census Bureau and the Department of Housing and Urban Development. This is 17.5 percent (±10.4 percent) above the revised October rate of 624,000 and is 26.6 percent (±16.6 percent) above the November 2016 estimate of 579,000.

The median sales price of new houses sold in November 2017 was $318,700. The average sales price was $377,100.

-

Project U.S. 10-year treasury yield hitting 3 pct by end of 2018

U.S. stock-index futures were flat on Friday as investors digest a raft of important data and prepared to three-day weekend.

Global Stocks:

Nikkei 22,902.76 +36.66 +0.16%

Hang Seng 29,578.01 +210.95 +0.72%

Shanghai 3,297.36 -2.70 -0.08%

S&P/ASX 6,069.70 +9.30 +0.15%

FTSE 7,592.66 -11.32 -0.15%

CAC 5,362.83 -23.14 -0.43%

DAX 13,078.74 -31.00 -0.24%

Crude $57.98 (-0.65%)

Gold $1,271.40 (+0.06%)

Real gross domestic product (GDP) was essentially unchanged in October following 0.2% growth in September, as 9 of 20 industrial sectors expanded.

Service-producing industries rose 0.2%, mainly from growth in wholesale trade, retail trade and real estate. Meanwhile, goods-producing industries contracted 0.4%, largely due to the mining, quarrying, and oil and gas extraction sector.

The wholesale trade sector grew for the 9th time in 11 months in October, with a 1.4% rise more than offsetting September's decline of 0.9%. Six of nine subsectors expanded, led by wholesalers of machinery, equipment and supplies (+3.4%), personal and household goods (+3.2%) and petroleum products (+3.1%). The wholesaling of motor vehicles and parts declined 1.7% as automotive imports decreased.

New orders for manufactured durable goods in November increased $3.1 billion or 1.3 percent to $241.4 billion, the U.S. Census Bureau announced today. This increase, up three of the last four months, followed a 0.4 percent October decrease. Excluding transportation, new orders decreased 0.1 percent. Excluding defense, new orders increased 1.0 percent. Transportation equipment, also up three of the last four months, drove the increase, $3.3 billion or 4.2 percent to $80.9 billion.

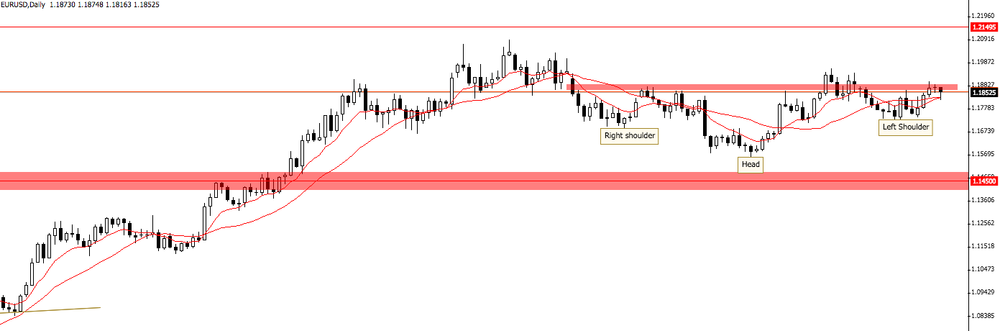

The scenario of a formation of an inverted chart pattern remains valid (Head and Shoulders).

However, for long entries we suggest you wait for the breakout of the neckline of that chart pattern.

(company / ticker / price / change ($/%) / volume)

| ALCOA INC. | AA | 49.25 | 0.26(0.53%) | 1387 |

| Amazon.com Inc., NASDAQ | AMZN | 1,173.00 | -1.76(-0.15%) | 1894 |

| Apple Inc. | AAPL | 174.72 | -0.29(-0.17%) | 43956 |

| AT&T Inc | T | 38.95 | 0.07(0.18%) | 35013 |

| Barrick Gold Corporation, NYSE | ABX | 14.47 | 0.04(0.28%) | 24356 |

| Boeing Co | BA | 295.26 | 0.23(0.08%) | 2743 |

| Caterpillar Inc | CAT | 154.65 | 0.01(0.01%) | 1324 |

| Chevron Corp | CVX | 124.9 | 0.08(0.06%) | 3264 |

| Cisco Systems Inc | CSCO | 38.42 | -0.11(-0.29%) | 581 |

| Citigroup Inc., NYSE | C | 75.98 | 0.16(0.21%) | 12047 |

| Exxon Mobil Corp | XOM | 83.9 | 0.05(0.06%) | 2597 |

| Facebook, Inc. | FB | 177.35 | -0.10(-0.06%) | 31150 |

| Ford Motor Co. | F | 12.64 | 0.01(0.08%) | 6965 |

| Freeport-McMoRan Copper & Gold Inc., NYSE | FCX | 18.15 | -0.03(-0.17%) | 19237 |

| General Electric Co | GE | 17.5 | 0.03(0.17%) | 63463 |

| Goldman Sachs | GS | 261.8 | 0.79(0.30%) | 921 |

| Home Depot Inc | HD | 188.9 | 0.82(0.44%) | 1180 |

| Intel Corp | INTC | 46.57 | -0.19(-0.41%) | 22064 |

| International Business Machines Co... | IBM | 151.8 | 0.30(0.20%) | 2345 |

| JPMorgan Chase and Co | JPM | 108.08 | 0.25(0.23%) | 5687 |

| McDonald's Corp | MCD | 171.83 | -0.02(-0.01%) | 117 |

| Merck & Co Inc | MRK | 56.76 | 0.16(0.28%) | 1231 |

| Microsoft Corp | MSFT | 85.7 | 0.20(0.23%) | 5754 |

| Nike | NKE | 62.44 | -2.33(-3.60%) | 79708 |

| Pfizer Inc | PFE | 36.27 | 0.03(0.08%) | 1675 |

| Procter & Gamble Co | PG | 91.79 | 0.12(0.13%) | 470 |

| Tesla Motors, Inc., NASDAQ | TSLA | 331.2 | -0.46(-0.14%) | 6591 |

| The Coca-Cola Co | KO | 45.83 | 0.23(0.50%) | 2254 |

| Twitter, Inc., NYSE | TWTR | 25.08 | 0.03(0.12%) | 37614 |

| Verizon Communications Inc | VZ | 53.1 | 0.09(0.17%) | 205 |

| Wal-Mart Stores Inc | WMT | 98.44 | 0.38(0.39%) | 2789 |

| Walt Disney Co | DIS | 109.87 | 0.30(0.27%) | 1777 |

| Yandex N.V., NASDAQ | YNDX | 31.7 | 0.26(0.83%) | 5370 |

Tesla (TSLA) reiterated with a Neutral at Tigress Financial

NIKE (NKE) reiterated with a Neutral at B. Riley FBR; target raised from $53 to $61

NIKE (NKE) reiterated with a Buy at Stifel

NIKE (NKE) reiterated with an Outperform at Telsey

NIKE (NKE) reported Q2 FY 2018 earnings of $0.46 per share (versus $0.50 in Q2 FY 2017), beating analysts' consensus estimate of $0.40.

The company's quarterly revenues amounted to $8.554 bln (+4.6% y/y), beating analysts' consensus estimate of $8.394 bln.

The company also said it expected to see Q3 revenue growth at or slightly below the rate of Q2. For FY 2018, it projected revenue growth in the mid-single digit range (versus analysts' consensus of +4%).

NKE fell to $63.20 (-2.42%) in pre-market trading.

The UK's current account deficit was £22.8 billion (4.5% of gross domestic product) in Quarter 3 (July to Sept) 2017, a narrowing of £3.0 billion from a revised deficit of £25.8 billion (5.1% of gross domestic product) in Quarter 2 (Apr to June) 2017.

The narrowing in the current account deficit was driven by a narrowing of the deficits on primary income by £1.8 billion, secondary income by £1.0 billion and total trade by £0.3 billion in Quarter 3 2017.

Gross fixed capital formation (GFCF), in volume terms, was estimated to have increased by 0.3% to £82.3 billion in Quarter 3 (July to Sept) 2017 from £82.1 billion in Quarter 2 (Apr to June) 2017.

Business investment was estimated to have increased by 0.5% to £45.9 billion in Quarter 3 2017 from £45.6 billion in Quarter 2 2017.

Between Quarter 3 2016 and Quarter 3 2017, GFCF was estimated to have increased by 2.4% from £80.4 billion; business investment was estimated to have increased by 1.7% from £45.1 billion.

UK gross domestic product (GDP) in volume terms was estimated to have increased by 0.4% between Quarter 2 (Apr to June) and Quarter 3 (July to Sept) 2017, unrevised from the second estimate of GDP.

Services remained the strongest contributor to growth in the output approach to GDP in Quarter 3 2017, with production also providing a positive contribution.

Household spending grew by 0.5% in Quarter 3 2017, providing the strongest contribution to the expenditure approach to GDP; while growth has increased compared with the first two quarters of 2017, the underlying story is one of a slowdown in growth of household spending, with quarter on same quarter a year ago growth at 1.0%, the lowest rate since Quarter 1 (Jan to Mar) 2012.

The most of cryptocurrencies had suffer a big depreciation this morning.

However, it may be interesting to see an opportunity to buy.

In special, ethereum (eth/usd) which is giving signs of a possible fake breakout of the consolidation zone.

The KOF Economic Barometer continues its upward tendency in December. It has risen further by roughly one point to 111.3 points (after revised 110.4 in November). The Barometer now stands at its highest reading since June 2010. The Swiss economy is in an upswing.

The high standing of the Barometer in December is driven mainly by the positive development of the indicators for the banking sector, after a less positive development in the last month.

In November 2017, household expenditure on goods bounced back by 2.2% in volume, after −2.1% in October. Energy consumption increased strongly, enhanced by average temperatures lower than usual (in contrast with October). Textile-clothing purchases bounced back also, as well as food consumption. Only transport equipment purchases declined.

EUR/USD

Resistance levels (open interest**, contracts)

$1.2000 (3536)

$1.1978 (3730)

$1.1949 (616)

Price at time of writing this review: $1.1858

Support levels (open interest**, contracts):

$1.1793 (4743)

$1.1746 (3631)

$1.1698 (3896)

Comments:

- Overall open interest on the CALL options and PUT options with the expiration date January, 5 is 93961 contracts (according to data from December, 21) with the maximum number of contracts with strike price $1,2200 (5585);

GBP/USD

Resistance levels (open interest**, contracts)

$1.3499 (2572)

$1.3476 (2481)

$1.3439 (859)

Price at time of writing this review: $1.3382

Support levels (open interest**, contracts):

$1.3326 (1850)

$1.3286 (2828)

$1.3243 (2774)

Comments:

- Overall open interest on the CALL options with the expiration date January, 5 is 32878 contracts, with the maximum number of contracts with strike price $1,3500 (4724);

- Overall open interest on the PUT options with the expiration date January, 5 is 33863 contracts, with the maximum number of contracts with strike price $1,3300 (2828);

- The ratio of PUT/CALL was 1.03 versus 1.05 from the previous trading day according to data from December, 21

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

-

Govt stance is economic growth needed to improve public finances

-

Govt will continue to work toward achieving primary budget surplus

Both economic and income expectations are on the rise, whilst propensity to buy has taken a slight hit. GfK forecasts an increase in consumer climate for January 2018 of 0.1 points in comparison to the previous month to 10.8 points.

Consumers currently see the German economy as displaying a strong upward trend. Economic expectations confirm this very good trend as they are displaying slight growth. Income expectations are in fact rising considerably and seem to have overcome their dip. Propensity to buy, on the other hand, has had to take a slight hit but is still maintaining its excellent level. The failed attempts to form a "Jamaica" coalition do not seem to have had any lasting damage on consumer moods.

As reported by the Federal Statistical Office (Destatis), the index of import prices increased by 2.7% in November 2017 compared with the corresponding month of the preceding year. In October 2017 and in September 2017 the annual rates of change were +2.6% and +3.0%, respectively. From October 2017 to November 2017 the index rose by 0.8%.

The index of import prices, excluding crude oil and mineral oil products, increased by 1.2% compared with the level of a year earlier.

The index of export prices increased by 1.2% in November 2017 compared with the corresponding month of the preceding year. In October 2017 and in September 2017 the annual rates of change were +1.5% and +1.7%, respectively. From October 2017 to November 2017 the export price index rose by 0.2%..

European stocks switched gears and finished higher Thursday, with Spanish stocks advancing before the results of Catalonia's regional election came in. The Stoxx Europe 600 index SXXP, +0.60% rose 0.6% to end at 390.69, led by gains for oil and gas and basic material companies. Utilities was the sole sector finishing lower. The index's win was its first after two losing sessions.

U.S. stocks closed higher on Thursday, with energy stocks helping major indexes to end points away from record territory. The latest economic data, which pointed to slight slowing from strong previous readings, further supported the market.

Asia-Pacific stocks largely rose early Friday in thin preholiday trade, following an overnight rebound in European equities and mild gains on Wall Street. But bitcoin prices BTCUSD, -5.43% slumped in morning trading, going from $15,800 to $13,200 in barely three hours, according to CoinDesk, before quickly rebounding above $14,000. Many of the biggest cryptocurrencies also fell significantly, with bitcoin cash plunging 27% in the past day.

© 2000-2026. Bản quyền Teletrade.

Trang web này được quản lý bởi Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

Thông tin trên trang web không phải là cơ sở để đưa ra quyết định đầu tư và chỉ được cung cấp cho mục đích làm quen.

Giao dịch trên thị trường tài chính (đặc biệt là giao dịch sử dụng các công cụ biên) mở ra những cơ hội lớn và tạo điều kiện cho các nhà đầu tư sẵn sàng mạo hiểm để thu lợi nhuận, tuy nhiên nó mang trong mình nguy cơ rủi ro khá cao. Chính vì vậy trước khi tiến hành giao dịch cần phải xem xét mọi mặt vấn đề chấp nhận tiến hành giao dịch cụ thể xét theo quan điểm của nguồn lực tài chính sẵn có và mức độ am hiểu thị trường tài chính.

Sử dụng thông tin: sử dụng toàn bộ hay riêng biệt các dữ liệu trên trang web của công ty TeleTrade như một nguồn cung cấp thông tin nhất định. Việc sử dụng tư liệu từ trang web cần kèm theo liên kết đến trang teletrade.vn. Việc tự động thu thập số liệu cũng như thông tin từ trang web TeleTrade đều không được phép.

Xin vui lòng liên hệ với pr@teletrade.global nếu có câu hỏi.

ngân hàng