- Phân tích

- Tin tức và các công cụ

- Tin tức thị trường

Tin tức thì trường

(raw materials / closing price /% change)

Oil 51.94 +0.13%

Gold 1,287.00 -1.23%

(index / closing price / change items /% change)

Nikkei +80.56 21336.12 +0.38%

TOPIX +4.19 1723.37 +0.24%

Hang Seng +4.69 28697.49 +0.02%

CSI 300 -0.38 3913.07 -0.01%

Euro Stoxx 50 +1.50 3607.77 +0.04%

FTSE 100 -10.80 7516.17 -0.14%

DAX -8.64 12995.06 -0.07%

CAC 40 -1.51 5361.37 -0.03%

DJIA +40.48 22997.44 +0.18%

S&P 500 +1.72 2559.36 +0.07%

NASDAQ -0.35 6623.66 -0.01%

S&P/TSX +14.20 15816.90 +0.09%

(pare/closed(GMT +3)/change, %)

EUR/USD $1,1765 -0,27%

GBP/USD $1,3188 -0,47%

USD/CHF Chf0,97812 +0,32%

USD/JPY Y112,19 +0,04%

EUR/JPY Y131,99 -0,23%

GBP/JPY Y147,969 -0,42%

AUD/USD $0,7844 -0,11%

NZD/USD $0,7170 -0,27%

USD/CAD C$1,25218 +0,05%

02:30 Australia Leading Index September -0.1%

11:30 United Kingdom Average earnings ex bonuses, 3 m/y August 2.1% 2.0%

11:30 United Kingdom Average Earnings, 3m/y August 2.1% 2.1%

11:30 United Kingdom ILO Unemployment Rate August 4.3% 4.3%

11:30 United Kingdom Claimant count September -2.8 1.0

12:00 Eurozone Construction Output, y/y August 3.4%

14:45 Eurozone ECB's Peter Praet Speaks

15:00 U.S. FOMC Member Dudley Speak

15:00 U.S. FOMC Member Kaplan Speak

15:30 Canada Manufacturing Shipments (MoM) August -2.6% -0.3%

15:30 U.S. Housing Starts September 1180 1174

15:30 U.S. Building Permits September 1272 1245

17:15 Eurozone ECB's Benoit Coeure Speaks

17:30 U.S. Crude Oil Inventories October -2.747 -4.750

22:00 U.S. Fed's Beige Book

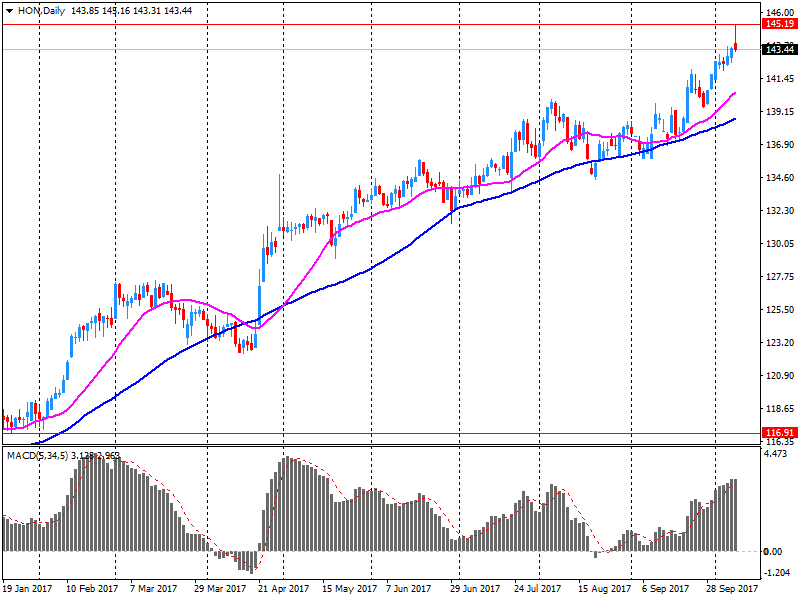

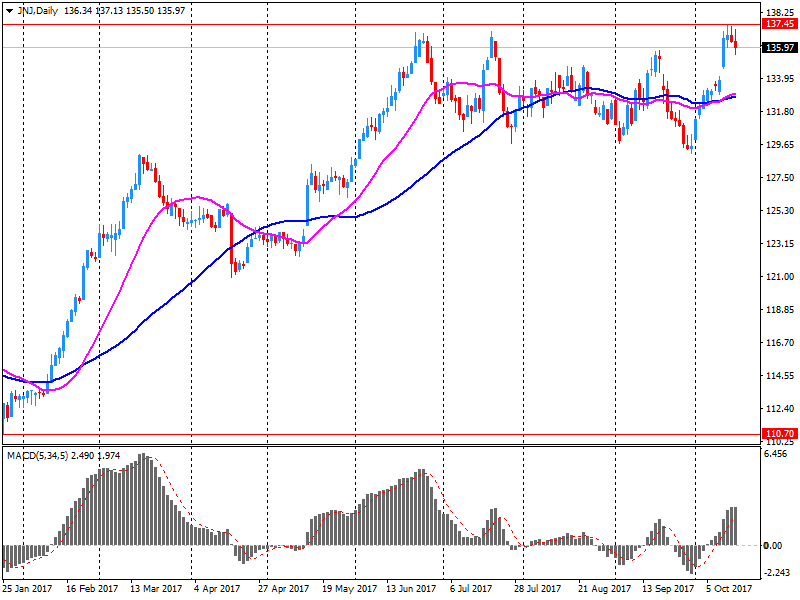

The major US stock indexes finished trading near zero, with the Dow Jones Industrial Average surpassing 23,000 for the first time, thanks to a more than 6 percent increase in UnitedHealth (UNH) shares and a more than 3 percent increase in Johnson & Johnson (JNJ ).

Certain support for the market was also provided by favorable data for the United States. The Bureau of Employment Accounting reported that in September, import prices in the US rose by 0.7 percent, which is the largest monthly increase since the increase of 0.7 percent in June 2016. Last time, import prices increased by more than 0.7 percent in May 2016 (then growth was 1.2 percent). Higher prices for imports of both fuel and non-fuel materials contributed to a general increase in import prices for September. Import prices in the US also increased on a 12-month basis, reaching 2.7 percent.

Meanwhile, the Fed said that industrial production in the US rose in September, as the effects of hurricanes Harvey and Irma began to disappear, and construction and utility production were restored. Industrial production increased by 0.3% after it decreased by 0.7% in August (revised from -0.9%.) Nevertheless, the July release was revised to -0.1% from +0.4 The economists predicted that in September industrial production will grow by 0.3%, while the total production growth increased by 0.2 percentage points to 76.0% from the revised 75.8% in August.

At the same time, the confidence of builders in the market of newly built houses for one family increased by four points to 68 in October, according to the housing market index (HMI) from the National Association of House Builders (NAHB) / Wells Fargo. This was the highest rate since May.

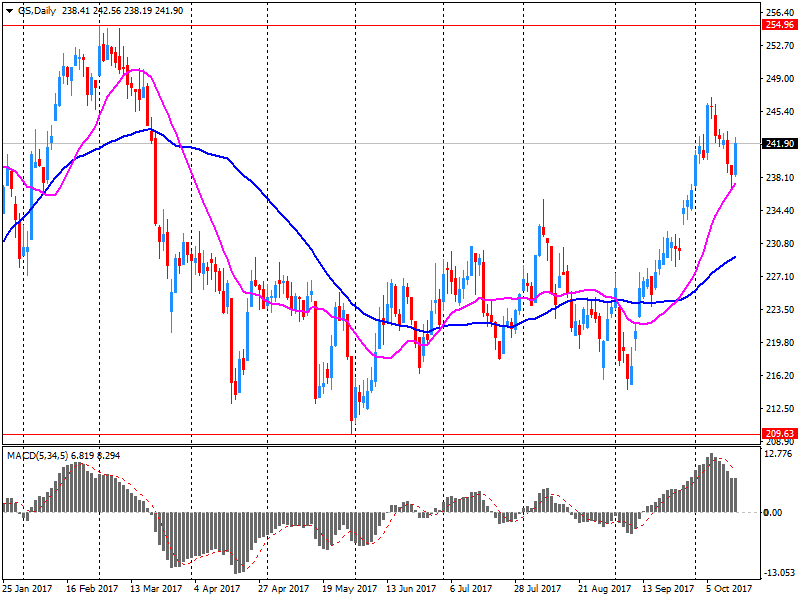

Most components of the DOW index finished trading in the red (17 of 30). Outsider were the shares of The Goldman Sachs Group, Inc. (GS, -2.69%). The leader of growth was UnitedHealth Group Incorporated (UNH, + 6.06%).

Most sectors of the S & P index recorded a decline. The largest decrease was shown in the financial sector (-0.4%). The healthcare sector grew most (+ 0.9%).

At closing:

DJIA + 0.17% 22,996.69 +39.73

Nasdaq -0.01% 6,623.66 -0.35

S & P + 0.07% 2.559.35 +1.71

Builder confidence in the market for newly-built single-family homes rose four points to a level of 68 in October on the National Association of Home Builders/Wells Fargo Housing Market Index (HMI). This was the highest reading since May.

"This month's report shows that home builders are rebounding from the initial shock of the hurricanes," said NAHB Chairman Granger MacDonald, a home builder and developer from Kerrville, Texas. "However, builders need to be mindful of long-term repercussions from the storms, such as intensified material price increases and labor shortages."

EUR/USD: 1.1760 (415 млн)

USD/JPY: 112.00 (111 млн)

AUD/USD: 0.7920 (605 млн), 0.7810 (330 млн)

U.S. stock-index futures were flat on Tuesday as investors assessed earnings reports from big corporates, including UnitedHealth (UNH), Morgan Stanley (MS), Goldman Sachs (GS) and Johnson & Johnson (JNJ).

Global Stocks:

Nikkei 21,336.12 +80.56 +0.38%

Hang Seng 28,697.49 +4.69 +0.02%

Shanghai 3,373.44 -5.03 -0.15%

S&P/ASX 5,889.61 +42.85 +0.73%

FTSE 7,548.27 +21.30 +0.28%

CAC 5,366.84 +3.96 +0.07%

DAX 13,021.56 +17.86 +0.14%

Crude $52.13 (+0.50%)

Gold $1,289.80 (-1.01%)

The rates of change for July and August were notably revised; the current estimate for July, a decrease of 0.1 percent, was 0.5 percentage point lower than previously reported, while the estimate for August, a decrease of 0.7 percent, was 0.2 percentage point higher than before. The estimates for manufacturing, mining, and utilities were each revised lower in July. The continued effects of Hurricane Harvey and, to a lesser degree, the effects of Hurricane Irma combined to hold down the growth in total production in September by 1/4 percentage point.

Capacity utilization for the industrial sector increased 0.2 percentage point in September to 76.0 percent, a rate that is 3.9 percentage points below its long-run (1972-2016) average.

U.S. import prices increased 0.7 percent in September, the U.S. Bureau of Labor Statistics reported today, after advancing 0.6 percent in August. The price index for U.S. exports rose 0.8 percent in September, after increasing 0.7 percent the previous month.

Hurricanes Harvey and Irma had a small impact on the collection of the import and export price index data for September, but no change in the estimation procedures.

(company / ticker / price / change ($/%) / volume)

| 3M Co | MMM | 219.65 | 0.93(0.43%) | 264 |

| ALCOA INC. | AA | 48.6 | 0.36(0.75%) | 5338 |

| Amazon.com Inc., NASDAQ | AMZN | 1,005.00 | -1.34(-0.13%) | 5322 |

| Apple Inc. | AAPL | 159.68 | -0.20(-0.13%) | 50758 |

| AT&T Inc | T | 36.29 | 0.12(0.33%) | 6704 |

| Barrick Gold Corporation, NYSE | ABX | 16.11 | -0.13(-0.80%) | 22216 |

| Boeing Co | BA | 255.75 | -4.00(-1.54%) | 15754 |

| Chevron Corp | CVX | 120.85 | 0.72(0.60%) | 634 |

| Cisco Systems Inc | CSCO | 33.68 | 0.14(0.42%) | 280 |

| Citigroup Inc., NYSE | C | 72.21 | 0.44(0.61%) | 63307 |

| Exxon Mobil Corp | XOM | 82.7 | -0.11(-0.13%) | 520 |

| Facebook, Inc. | FB | 174.82 | 0.30(0.17%) | 46809 |

| Ford Motor Co. | F | 12.1 | -0.02(-0.17%) | 17730 |

| Freeport-McMoRan Copper & Gold Inc., NYSE | FCX | 15.06 | -0.21(-1.38%) | 304301 |

| General Electric Co | GE | 23.29 | -0.07(-0.30%) | 55469 |

| General Motors Company, NYSE | GM | 45.95 | 0.19(0.42%) | 25916 |

| Goldman Sachs | GS | 245.85 | 3.44(1.42%) | 75281 |

| Intel Corp | INTC | 39.51 | -0.25(-0.63%) | 3235 |

| International Business Machines Co... | IBM | 146.7 | -0.13(-0.09%) | 638 |

| Johnson & Johnson | JNJ | 135.8 | -0.32(-0.24%) | 144527 |

| JPMorgan Chase and Co | JPM | 98.35 | 0.51(0.52%) | 29423 |

| McDonald's Corp | MCD | 165.03 | 0.02(0.01%) | 178 |

| Microsoft Corp | MSFT | 77.5 | -0.15(-0.19%) | 4865 |

| Procter & Gamble Co | PG | 93.2 | 0.06(0.06%) | 332 |

| Starbucks Corporation, NASDAQ | SBUX | 54.81 | -0.10(-0.18%) | 614 |

| Tesla Motors, Inc., NASDAQ | TSLA | 351.22 | 0.62(0.18%) | 10146 |

| The Coca-Cola Co | KO | 46.55 | -0.07(-0.15%) | 5225 |

| UnitedHealth Group Inc | UNH | 196.1 | 2.90(1.50%) | 17659 |

| Verizon Communications Inc | VZ | 48 | -0.09(-0.19%) | 340 |

| Visa | V | 108.4 | 0.10(0.09%) | 1358 |

| Wal-Mart Stores Inc | WMT | 85.89 | 0.15(0.17%) | 5555 |

| Walt Disney Co | DIS | 98.1 | -0.03(-0.03%) | 505 |

General Electric (GE) target lowered to $23 from $27 at Goldman

Freeport-McMoRan (FCX) downgraded to Sell from Hold at Deutsche Bank

Chevron (CVX) upgraded to Outperform from Neutral at Macquarie

UnitedHealth (UNH) reported Q3 FY 2017 earnings of $2.66 per share (versus $2.17 in Q3 FY 2016), beating analysts' consensus estimate of $2.57.

The company's quarterly revenues amounted to $50.322 bln (+8.7% y/y), generally in-line with analysts' consensus estimate of $50.383 bln.

The company also raised guidance for FY2017, projecting EPS approaching $10.00 (prior $9.75-9.90) versus analysts' consensus estimate of $9.86.

UNH rose to $196.00 (+1.45%) in pre-market trading.

Morgan Stanley (MS) reported Q3 FY 2017 earnings of $0.93 per share (versus $0.81 in Q3 FY 2016), beating analysts' consensus estimate of $0.81.

The company's quarterly revenues amounted to $9.197 bln (+3.2% y/y), beating analysts' consensus estimate of $9.048 bln.

MS rose to $ 49.55 (+1.25%) in pre-market trading.

Johnson & Johnson (JNJ) reported Q3 FY 2017 earnings of $1.90 per share (versus $1.68 in Q3 FY 2016), beating analysts' consensus estimate of $1.80.

The company's quarterly revenues amounted to $19.650 bln (+10.3% y/y), beating analysts' consensus estimate of $19.291 bln.

The company also raised FY2017 EPS guidance to $7.25-7.30 from $7.12-7.22 (versus analysts' consensus estimate of $7.18) and FY2017 revenues forecast to $76.1-76.5 bln from $75.8-76.1 bln (versus analysts' consensus estimate of $75.84 bln).

JNJ rose to $137.57 (+1.07%) in pre-market trading.

Goldman Sachs (GS) reported Q3 FY 2017 earnings of $5.02 per share (versus $4.88 in Q3 FY 2016), beating analysts' consensus estimate of $4.16.

The company's quarterly revenues amounted to $8.330 bln (+2.0% y/y), beating analysts' consensus estimate of $7.595 bln.

GS rose to $245.25 (+1.17%) in pre-market trading.

-

Monetary policy is not principle instrument for financial stability

-

First threat to BoE independence is thinking monetary policy can do more than it can

The ZEW Indicator of Economic Sentiment for Germany continued to improve in October 2017, however, not as strongly as in the previous month. The indicator currently stands at 17.6 points, which corresponds to an increase of 0.6 points compared with the September result. The indicator, however, still remains below the long-term average of 23.8 points.

The improved outlook for the coming six months is not least the result of the surprisingly positive growth figures seen in the previous months. In August, figures for both production and incoming orders were significantly better than expected. The framework conditions for German exports, which have already seen a significant rise, are further improved by positive growth figures for Europe.

Euro area annual inflation was 1.5% in September 2017, stable compared with August 2017. In September 2016 the rate was 0.4%. European Union annual inflation was 1.8% in September 2017, up from 1.7% in August 2017. A year earlier the rate was 0.4%. These figures come from Eurostat, the statistical office of the European Union.

The lowest annual rates were registered in Cyprus (0.1%), Ireland (0.2%) and Finland (0.8%). The highest annual rates were recorded in Lithuania (4.6%), Estonia (3.9%) and Latvia (3.0%). Compared with August 2017, annual inflation rose in eleven Member States, remained stable in seven and fell in nine.

UK House prices grew by 5% in the year to August 2017, experiencing a 0.5 percentage point increase from the previous month.

In terms of housing demand the Royal Institution of Chartered Surveyors' (RICS) residential market survey for August 2017 reported that headline price expectations remain subdued in the near term. However, at the 12-month horizon, prime central London remains the only area in which prices expectations are negative. In terms of demand, there was little change in buyer enquires during August, continuing a streak of flat or modestly negative readings into a ninth consecutive month.

The headline rate of inflation for goods leaving the factory gate (output prices) rose 3.3% on the year to September 2017, from 3.4% in August 2017.

Prices for materials and fuels (input prices) rose 8.4% on the year to September 2017, which is unchanged from August 2017.

Upward contributions from energy were offset by downward contributions from other industries, resulting in little change in the annual rates for both input and output prices.

Core output inflation was 2.5% on the year to September 2017, which is unchanged since July 2017.

The Consumer Prices Index including owner occupiers' housing costs (CPIH) 12-month inflation rate was 2.8% in September 2017, up from 2.7% in August 2017; it was last higher in March 2012.

The main contributors to the increase in the rate were rising prices for food and recreational goods, along with transport costs, which fell by less than they did a year ago.

These upward effects were partially offset by downward contributions from a range of goods and services, in particular clothing prices, which rose by less than they did a year ago.

The Consumer Prices Index (CPI) 12-month rate was 3.0% in September 2017, up from 2.9% in August 2017; it was last higher in March 2012.

EUR/USD: 1.1760 (415 m)

USD/JPY: 112.00 (111 m)

AUD/USD: 0.7920 (605 m), 0.7810 (330 m)

EUR/USD

Resistance levels (open interest**, contracts)

$1.1941 (2370)

$1.1876 (1397)

$1.1834 (279)

Price at time of writing this review: $1.1758

Support levels (open interest**, contracts):

$1.1704 (3088)

$1.1670 (4303)

$1.1631 (4968)

Comments:

- Overall open interest on the CALL options and PUT options with the expiration date November, 3 is 98824 contracts (according to data from October, 16) with the maximum number of contracts with strike price $1,2000 (6153);

GBP/USD

Resistance levels (open interest**, contracts)

$1.3400 (3444)

$1.3335 (1445)

$1.3299 (925)

Price at time of writing this review: $1.3251

Support levels (open interest**, contracts):

$1.3170 (2098)

$1.3145 (883)

$1.3116 (1265)

Comments:

- Overall open interest on the CALL options with the expiration date November, 3 is 37086 contracts, with the maximum number of contracts with strike price $1,3300 (3444);

- Overall open interest on the PUT options with the expiration date November, 3 is 32671 contracts, with the maximum number of contracts with strike price $1,3000 (2220);

- The ratio of PUT/CALL was 0.88 versus 0.87 from the previous trading day according to data from October, 16

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

-

Rate hikes abroad did not have "mechanical" implications for Australian rates

-

Judged steady policy consistent with growth and inflation targets

-

Members noted policy had been eased significantly more in other advanced economies

-

Rise in AUD driven by fall in USD, weighing on domestic inflation

-

Members discussed importance of risks in household balance sheets

-

Public infrastructure spending rising very strongly, last for a couple of years more

The September 2017 trend estimate (99,850) decreased by 0.3% when compared with August 2017.

When comparing national trend estimates for September 2017 with August 2017, sales for Other vehicles increased by 0.7%. By contrast, Passenger vehicles and Sports utility vehicles decreased by 1.0% and 0.1% respectively.

The largest upward movement across all states and territories, on a trend basis, was in Tasmania (1.5%), continuing an upward trend that began in April 2017.

The largest downward movement across all states and territories, on a trend basis, was in the Australian Capital Territory (-0.9%).

In the September 2017 quarter compared with the June 2017 quarter, the consumers price index (CPI) rose 0.5 percent (up 0.3 percent with seasonal adjustment).

Food prices rose 1.1 percent, influenced by higher prices for vegetables (up 6.2 percent).

Housing and household utilities rose 1.0 percent, influenced by local authority rates (up 3.5 percent), rentals for housing (up 0.6 percent), and purchase of new housing (up 1.1 percent).

Transport prices fell 1.1 percent, with cheaper petrol prices (down 1.7 percent), and international airfares (down 5.5 percent).

From the September 2016 quarter to the September 2017 quarter, the CPI inflation rate was 1.9 percent.

Housing and household utilities increased 3.0 percent, with purchase of new housing up 5.4 percent, and rentals for housing up 2.2 percent.

Food prices increased 2.8 percent, with vegetables up 9.0 percent.

Communication prices decreased 5.3 percent, with telecommunications services down 4.5 percent and equipment down 22 percent.

Stocks listed in Spain dropped Monday, weighing on the pan-European benchmark, after the central government in Madrid gave Catalonia's separatist leaders until Thursday to drop their push for independence. In Madrid, the IBEX 35 IBEX, -0.75% fell 0.8% to close at 10,181.40, falling for a third straight session. As the index extended its loss from the open, the broader Stoxx Europe 600 SXXP, +0.00% erased its gain to end flat at 391.41.

The global stock rally showed signs of slowing Tuesday, with many Asia-Pacific indexes little changed ahead of the start of the Chinese Communist Party's congress. One exception was Australia, where stocks rebounded thanks to stronger commodity prices. The S&P/ASX 200 XJO, +0.80% was recently up 0.7% as it got a lift from Rio Tinto RIO, +1.84% and BHP Billiton BHP, +1.45% . Their shares rose more than 1%, with Rio hitting another 3½-year high.

U.S. stocks closed higher Monday, with all three major indexes logging another round of records, as investors looked ahead to key corporate earnings reports that could set the tone for trading and determine whether the lofty levels of the equity market are justified.

© 2000-2026. Bản quyền Teletrade.

Trang web này được quản lý bởi Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

Thông tin trên trang web không phải là cơ sở để đưa ra quyết định đầu tư và chỉ được cung cấp cho mục đích làm quen.

Giao dịch trên thị trường tài chính (đặc biệt là giao dịch sử dụng các công cụ biên) mở ra những cơ hội lớn và tạo điều kiện cho các nhà đầu tư sẵn sàng mạo hiểm để thu lợi nhuận, tuy nhiên nó mang trong mình nguy cơ rủi ro khá cao. Chính vì vậy trước khi tiến hành giao dịch cần phải xem xét mọi mặt vấn đề chấp nhận tiến hành giao dịch cụ thể xét theo quan điểm của nguồn lực tài chính sẵn có và mức độ am hiểu thị trường tài chính.

Sử dụng thông tin: sử dụng toàn bộ hay riêng biệt các dữ liệu trên trang web của công ty TeleTrade như một nguồn cung cấp thông tin nhất định. Việc sử dụng tư liệu từ trang web cần kèm theo liên kết đến trang teletrade.vn. Việc tự động thu thập số liệu cũng như thông tin từ trang web TeleTrade đều không được phép.

Xin vui lòng liên hệ với pr@teletrade.global nếu có câu hỏi.

ngân hàng