- Phân tích

- Tin tức và các công cụ

- Tin tức thị trường

Tin tức thì trường

On Friday, the main US stock indexes rose slightly, helped by the rise in price of shares in Apple and other technology companies, but the fall of insurance companies and hospital operators has limited growth.

In addition, the focus was on the US. As it became known today, the consumer price index in September rose by 0.5%, noting the biggest increase in eight months. Economists predicted an increase of 0.6% due to higher gasoline prices. With the exception of food and energy, the basic consumer price index rose by 0.1%.

Retail sales in the US increased by 1.6% in September, reflecting the largest increase in two and a half years. The greatest increase was caused by new cars and trucks. With the exception of cars, sales grew by 1%. And sales, excluding cars and gasoline, climbed to smaller, but still stable, 0.5%. Economists predicted an increase in total sales of 1.7% and 0.3%, excluding cars.

Preliminary results of the studies, presented by Thomson-Reuters and the Michigan Institute, showed: the mood sensor among US consumers grew in October despite the average forecasts of experts. According to the data, in October the consumer sentiment index rose to 101.1 points compared to the final reading for September at the level of 95.1 points. According to average estimates, the index had to fall to the level of 95 points.

US enterprises increased their reserves in August in maximum nine months, which indicates a strong confidence in future demand. The Ministry of Trade reported that in August the volume of inventories increased by 0.7%, after rising in July by 0.3%. This was the biggest leap since November 2016. Sales also rose by 0.7% in August, compared with a 0.3% increase in July. This was the biggest increase in sales since December 2016.

Most components of the DOW index recorded a rise (16 out of 30). The leader of growth was shares of American Express Company (AXP, + 1.34%). Outsider were the shares of Verizon Communications Inc. (VZ, -1.05%).

Most sectors of the S & P index finished trading in positive territory. The base resources sector grew most (+ 0.5%). The utilities sector showed the greatest decrease (-0.5%).

At closing:

Dow + 0.13% 22.871.72 +30.71

Nasdaq + 0.22% 6,605.80 +14.29

S & P + 0.09% 2.553.17 +2.24

The October gain was broadly shared, occurring among all age and income subgroups and across all partisan viewpoints. The data indicate a robust outlook for consumer spending that extends the current expansion to at least mid 2018, which would mark the 2nd longest expansion since the mid 1800's.

While the early October surge indicates greater optimism about the future course of the economy, it also reflects an unmistakable sense among consumers that economic prospects are now about as good as could be expected. This "as good as it gets" outlook is supported by a moderation in the expected pace of growth in both personal finances and the overall economy, accompanied by a growing sense that, even with this moderation, it would still mean the continuation of good economic times.

Inventories manufacturers' and trade inventories, adjusted for seasonal variations but not for price changes, were estimated at an end-of-month level of $1,889.0 billion, up 0.7 percent (±0.1 percent) from July 2017 and were up 3.6 percent (±0.3 percent) from August 2016.

The total business inventories/sales ratio based on seasonally adjusted data at the end of August was 1.38. The August 2016 ratio was 1.40.

EURUSD: 1.1700 (EUR 575m) 1.1800 (515m)

USDJPY: 110.00 (370m) 111.00 (260m) 111.40 (265m) 112.50(580m) 112.60 (1.55bln) 112.65-70 (660m) 113.00 (1.2bln) 113.60 (345m)

GBPUSD: 1.3100 (Gbp340m)

AUDUSD: Ntg of note

USDCHF 0.9635 (USD 330m)

NZDUSD: 0.6940 (NZD 725m) 0.6975 (470m)

AUDNZD: 1.1000 (AUD 600m)

USDCAD: 1.2450 (USD 430m) 1.2465 (490m)

U.S. stock-index futures were higher on Friday as investors assessed quarterly results of Bank of America (BAC) and the U.S. data on consumer inflation and retail sales for September.

Global Stocks:

Nikkei 21,155.18 +200.46 +0.96%

Hang Seng 28,476.43 +17.40 +0.06%

Shanghai 3,391.54 +5.44 +0.16%

S&P/ASX 5,814.15 +19.69 +0.34%

FTSE 7,543.63 -12.61 -0.17%

CAC 5,354.97 -5.84 -0.11%

DAX 112,991.00 +8.11 +0.06%

Crude $51.61 (+2.00%)

Gold $1,298.90 (+0.19%)

(company / ticker / price / change ($/%) / volume)

| ALCOA INC. | AA | 48.45 | 0.92(1.94%) | 5083 |

| ALTRIA GROUP INC. | MO | 65.49 | 0.14(0.21%) | 103429 |

| Amazon.com Inc., NASDAQ | AMZN | 1,007.10 | 6.17(0.62%) | 49274 |

| AMERICAN INTERNATIONAL GROUP | AIG | 62.49 | -0.06(-0.10%) | 47705 |

| Apple Inc. | AAPL | 156.56 | 0.56(0.36%) | 357517 |

| AT&T Inc | T | 35.88 | 0.02(0.06%) | 470187 |

| Barrick Gold Corporation, NYSE | ABX | 16.88 | 0.20(1.20%) | 9970 |

| Caterpillar Inc | CAT | 130.5 | 0.51(0.39%) | 32091 |

| Chevron Corp | CVX | 119.56 | 0.42(0.35%) | 99879 |

| Citigroup Inc., NYSE | C | 72.1 | -0.27(-0.37%) | 393274 |

| Exxon Mobil Corp | XOM | 82.6 | 0.17(0.21%) | 223416 |

| Facebook, Inc. | FB | 173.2 | 0.65(0.38%) | 158064 |

| Ford Motor Co. | F | 12.08 | -0.04(-0.33%) | 268075 |

| Freeport-McMoRan Copper & Gold Inc., NYSE | FCX | 14.75 | 0.24(1.65%) | 125431 |

| General Electric Co | GE | 23.13 | 0.08(0.35%) | 496049 |

| General Motors Company, NYSE | GM | 45.25 | 0.36(0.80%) | 114251 |

| Goldman Sachs | GS | 238.45 | -1.35(-0.56%) | 22254 |

| Google Inc. | GOOG | 993 | 5.17(0.52%) | 18315 |

| Hewlett-Packard Co. | HPQ | 20.89 | 0.49(2.40%) | 93571 |

| Home Depot Inc | HD | 164.92 | 0.33(0.20%) | 62111 |

| HONEYWELL INTERNATIONAL INC. | HON | 143 | -0.19(-0.13%) | 40147 |

| Intel Corp | INTC | 39.33 | 0.14(0.36%) | 254636 |

| International Business Machines Co... | IBM | 147.5 | 0.47(0.32%) | 46124 |

| JPMorgan Chase and Co | JPM | 95.4 | -0.59(-0.61%) | 213812 |

| McDonald's Corp | MCD | 164.17 | 0.26(0.16%) | 44108 |

| Microsoft Corp | MSFT | 77.4 | 0.28(0.36%) | 420976 |

| Nike | NKE | 50.97 | 0.14(0.28%) | 70534 |

| Pfizer Inc | PFE | 36.3 | -0.05(-0.14%) | 315858 |

| Procter & Gamble Co | PG | 92.4 | 0.25(0.27%) | 134160 |

| Starbucks Corporation, NASDAQ | SBUX | 56 | 0.03(0.05%) | 77285 |

| Tesla Motors, Inc., NASDAQ | TSLA | 357 | 1.32(0.37%) | 18837 |

| The Coca-Cola Co | KO | 46.12 | 0.01(0.02%) | 202173 |

| Twitter, Inc., NYSE | TWTR | 18.54 | 0.09(0.49%) | 50744 |

| United Technologies Corp | UTX | 119 | 0.18(0.15%) | 39484 |

| UnitedHealth Group Inc | UNH | 190.96 | -1.96(-1.02%) | 56027 |

| Verizon Communications Inc | VZ | 48.25 | -0.10(-0.21%) | 218712 |

| Walt Disney Co | DIS | 97 | 0.07(0.07%) | 91133 |

Visa (V) initiated with a Overweight at Stephens; target $125

McDonald's (MCD) target raised to $180 from $175 at RBC Capital Mkts

Citigroup (C) target raised to $79 from $75 at RBC Capital Mkts

HP (HPQ) target raised to $23 from $21 at Mizuho

Ford Motor (F) downgraded to Equal Weight from Overweight at Barclays

General Motors (GM) upgraded to Overweight from Equal Weight at Barclays

Advance estimates of U.S. retail and food services sales for September 2017, adjusted for seasonal variation and holiday and trading-day differences, but not for price changes, were $483.9 billion, an increase of 1.6 percent from the previous month, and 4.4 percent above September 2016.

Total sales for the July 2017 through September 2017 period were up 3.9 percent from the same period a year ago. The July 2017 to August 2017 percent change was revised from down 0.2 percent to down 0.1 percent.

Retail trade sales were up 1.7 percent from August 2017, and up 4.7 percent from last year. Gasoline Stations were up 11.4 percent from September 2016, while Building Materials and Garden Equipment and Supplies Dealers were up 10.7 percent from last year.

The Consumer Price Index rose 0.5 percent in September on a seasonally adjusted basis, the U.S. Bureau of Labor Statistics reported today. Over the last 12 months, the all items index rose 2.2 percent.

The gasoline index increased 13.1 percent in September and accounted for about three-fourths of the seasonally adjusted all items increase. Other major energy component indexes were mixed, and the food index rose slightly.

The index for all items less food and energy increased 0.1 percent in September. The shelter index continued to increase, and the indexes for motor

vehicle insurance, recreation, education, and wireless telephone services also rose. These increases more than offset declines in the indexes for new

vehicles, household furnishings and operations, medical care, and used cars and trucks.

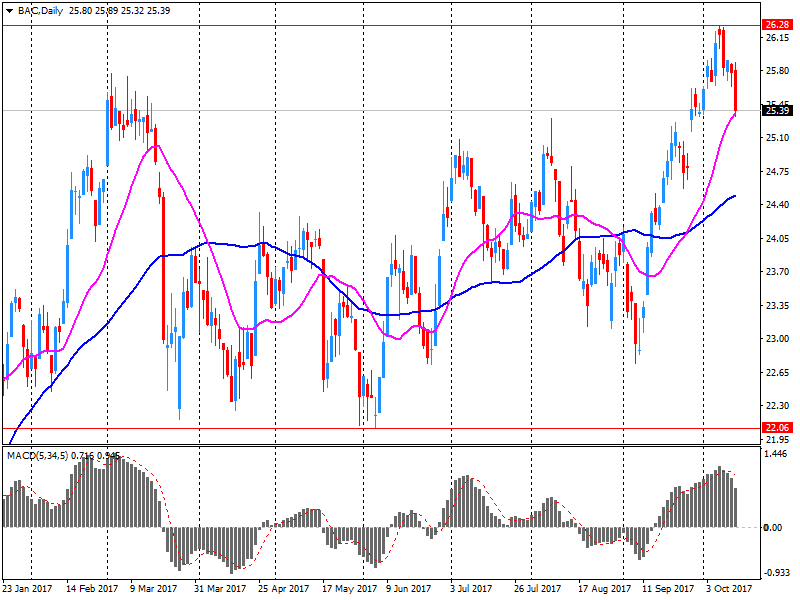

Bank of America (BAC) reported Q3 FY 2017 earnings of $0.48 per share (versus $0.41 in Q3 FY 2016), beating analysts' consensus estimate of $0.45.

The company's quarterly revenues amounted to $22.079 bln (+2.1% y/y), generally in-line with analysts' consensus estimate of $22.069 bln.

BAC rose to $25.70 (+0.98%) in pre-market trading.

The Producer and Import Price Index rose in September 2017 by 0.5% compared with the previous month, reaching 100.5 points (base December 2015 = 100). The rise is due in particular to higher prices for petroleum products, basic metals, semi-finished products of metal, and scrap.

Compared with September 2016, the price level of the whole range of domestic and imported products rose by 0.8%. These are some of the findings from the Federal Statistical Office (FSO).

EUR/USD: 1.1800(515 m), 1.1700(575 m)

USD/JPY: 113.00(119 m), 112.65/70(660 m), 112.60(155 m), 112.50(580 m)

China's exports grew at a slower-than-expected pace in September, data from the General Administration of Customs, cited by rttnews.

In dollar terms, exports climbed 8.1 percent year-over-year in September, below economists' forecast for an increase of 10.0 percent.

At the same time, imports surged 18.7 percent in September from a year ago, faster than the expected growth of 15.0 percent.

The trade surplus totaled $28.47 billion in September versus the expected surplus of $38.0 billion.

EUR/USD

Resistance levels (open interest**, contracts)

$1.2011 (3250)

$1.1954 (3324)

$1.1915 (1388)

Price at time of writing this review: $1.1840

Support levels (open interest**, contracts):

$1.1771 (2001)

$1.1743 (3018)

$1.1710 (3115)

Comments:

- Overall open interest on the CALL options and PUT options with the expiration date November, 3 is 97649 contracts (according to data from October, 12) with the maximum number of contracts with strike price $1,2000 (6064);

GBP/USD

Resistance levels (open interest**, contracts)

$1.3418 (3437)

$1.3376 (3200)

$1.3347 (2232)

Price at time of writing this review: $1.3281

Support levels (open interest**, contracts):

$1.3225 (2160)

$1.3181 (1964)

$1.3123 (1269)

Comments:

- Overall open interest on the CALL options with the expiration date November, 3 is 35987 contracts, with the maximum number of contracts with strike price $1,3300 (3437);

- Overall open interest on the PUT options with the expiration date November, 3 is 31953 contracts, with the maximum number of contracts with strike price $1,3000 (2213);

- The ratio of PUT/CALL was 0.89 versus 0.89 from the previous trading day according to data from October, 12

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

Consumer prices in Germany were 1.8% higher in September 2017 compared with September 2016. In August 2017, the inflation rate as measured by the consumer price index was 1.8%, too. Compared with August 2017, the consumer price index increased by 0.1% in September 2017. The Federal Statistical Office (Destatis) thus confirms its provisional overall results of 28 September 2017.

In September 2017, the prices of energy products were up 2.7% year on year. The increase in energy prices was higher than the overall rise in prices and had a strong upward effect on the inflation rate. In September 2017, prices were up year on year especially for mineral oil products (+6.2%, of which heating oil: +12.9%; motor fuels: +4.5%) and electricity (+2.0%). Only gas prices declined on a year earlier (-2.5%). Excluding energy prices, the inflation rate would have been +1.7% in September 2017.

Spanish stocks closed fractionally lower Thursday, catching their breath after the prior day's rally that was sparked by worries abating over Catalonia's independence push, while Europe's main equity benchmark also struggled for direction.

The U.S. stock market heralded the beginning of third-quarter earnings season by finishing slightly lower on Thursday, even as Wall Street banks turned in generally upbeat results.

Stocks showed little movement Friday as markets opened in the Asia Pacific region, but more new highs could be in store with Japan topping 21,000 for the first time since 1996. The Nikkei NIK, +0.94% rose 0.3% early, touching 21,032, even as the yen strengthened slightly. Japan's benchmark index hit a two-decade closing high during the week.

© 2000-2026. Bản quyền Teletrade.

Trang web này được quản lý bởi Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

Thông tin trên trang web không phải là cơ sở để đưa ra quyết định đầu tư và chỉ được cung cấp cho mục đích làm quen.

Giao dịch trên thị trường tài chính (đặc biệt là giao dịch sử dụng các công cụ biên) mở ra những cơ hội lớn và tạo điều kiện cho các nhà đầu tư sẵn sàng mạo hiểm để thu lợi nhuận, tuy nhiên nó mang trong mình nguy cơ rủi ro khá cao. Chính vì vậy trước khi tiến hành giao dịch cần phải xem xét mọi mặt vấn đề chấp nhận tiến hành giao dịch cụ thể xét theo quan điểm của nguồn lực tài chính sẵn có và mức độ am hiểu thị trường tài chính.

Sử dụng thông tin: sử dụng toàn bộ hay riêng biệt các dữ liệu trên trang web của công ty TeleTrade như một nguồn cung cấp thông tin nhất định. Việc sử dụng tư liệu từ trang web cần kèm theo liên kết đến trang teletrade.vn. Việc tự động thu thập số liệu cũng như thông tin từ trang web TeleTrade đều không được phép.

Xin vui lòng liên hệ với pr@teletrade.global nếu có câu hỏi.

ngân hàng