- Аналітика

- Новини та інструменти

- Новини ринків

Новини ринків

- US Dollar Index stays depressed after reversing from 11-week high.

- Yields, inflation expectations drop but activity data flash mixed signals to prod DXY bears.

- Absence of hawkish surprise from Fed, China-linked optimism exerts downside pressure on Greenback ahead of top-tier data.

- US CB Consumer Confidence can offer intraday directions but NFP, Fed’s preferred inflation gauge are the key.

US Dollar Index (DXY) remains on the back foot around 103.95 during the early hours of Tuesday’s Asian session, after reversing from an 11-week high to snap a two-day winning streak the previous day. In doing so, the Greenback’s gauge versus the six major currencies teases sellers ahead of the top-tier US data. However, the market’s cautious mood ahead of the releases and a light news line prods the DXY traders of late.

That said, the downbeat US Treasury bond yields joined the weakness in the US inflation clues to weigh on the US Dollar Index the previous day, especially amid China-linked optimism. Additionally, the Fed officials’ inability to please markets with a major hawkish surprise during the annual Jackson Hole Symposium also contributed to the Greenback’s weakness.

It’s worth noting that Fed Chair Jerome Powell showed readiness for rate hikes while pushing back rate cut bias during his key Jackson Hole speech. However, the policymaker also highlighted the data dependency and hence increased the importance of the incoming statistics, as well as amplified uncertainty about the US central bank’s next moves, which in turn weighed on the DXY. It should be noted that Cleveland Fed Bank President Loretta Mester favored a rate hike, even if not in September, while the odds of witnessing an increase in the Fed rate in November improved of late, per the CME’s FedWatch Tool.

Elsewhere, the inflation expectations, as per the 10-year and 5-year breakeven inflation rates from the St. Louis Federal Reserve (FRED) data, reverse Friday’s corrective bounce while declining to the fresh lows in five weeks.

Furthermore, the US Dallas Fed Manufacturing Business Index improved to -17.2 for August versus -21.6 expected and -20.0 prior. It’s worth noting that the details of the activity gauge were mixed as the new orders and prices paid for raw materials increased but the finished goods prices eased.

It should be noted that China’s halving of the stamp duty on stocks trading joined a Wall Street Journal (WSJ) piece suggesting Chinese Communist Party Chairman Xi Jinping’s indirect push for stimulus to favor market sentiment and offered additional negatives for the US Dollar Index.

Amid these plays, Wall Street closed on the green side for the second consecutive day while the US 10-year Treasury bond yields dropped three basis points (bps) to 4.20% and the two-year counterpart declined half a percent to 5.5% at the latest. That said, the US 10-year Treasury bond yields remain pressured near 4.19% by the press time whereas the S&P 500 Futures lack clear directions as we write.

Moving on, the cautious mood ahead of today’s US Conference Board’s (CB) Consumer Confidence Index for August, expected at 116.2 versus prior 117.00, will prod the Greenback and the markets. Above all, major attention will be given to the Fed’s preferred inflation gauge, namely the US Core Personal Consumption Expenditure (PCE) Price Index for July and Nonfarm Payrolls (NFP) for August.

Technical analysis

A six-week-old ascending support line around 103.65 precedes the tops marked in late June and early July around 103.55 to restrict the immediate downside of the US Dollar Index (DXY). Alternatively, a downward-sloping resistance line from March 15, close to 104.20 at the latest, guards the nearby upside of the DXY.

- USD/CAD oscillates in a narrow trading range between 1.3570-1.3610.

- Investors digest the Jackson Hole Symposium ahead of the key US labor and economic data.

- All eyes are on the Canadian annual GDP, US Nonfarm Payrolls.

The USD/CAD pair trades sideways around 1.3600 during the early Asian session on Tuesday. The US Dollar Index (DXY struggles to find a decisive direction and hovers around 104.00. Market participants await the US economic data and Canadian growth numbers for fresh impetus. The closely watched event this week will be the US Nonfarm Payroll due on Friday and it could trigger volatility in the market.

Investors digest the Jackson Hole Symposium and shift their focus to the US economic data. That said, Chairman Jerome Powell opened the door for an additional rate hike if required. However, it would be determined by incoming data. The market discounts modest odds of a hike in September, but the probability of a 25 basis point (bps) hike in November increased to nearly 70%, according to World Interest Rates Probabilities (WIRP). On Monday, the Federal Reserve Bank of Dallas revealed that the Manufacturing Index for August rose to -17.2 from -20 prior, better than the -21.6 expected.

On the Canadian Dollar front, a decline in oil prices weakens the Loonie as Canada is the largest exporter of crude to the US. Nevertheless, the positive development from China, the major oil importer in the world might lift the Loonie against its rivals. That said, Chinese authorities would reduce the 0.1% duty on stock trading to stimulate the capital market and strengthen investor confidence.

Last week, monthly Canadian Retail Sales for June expanded by 0.1% from the previous month. The figure came in better than the expectation of 0%. Market players will take cues from the Canadian annual Gross Domestic Product (GDP) on Friday. The weaker-than-expected growth number would convince the Bank of Canada (BoC) to maintain the interest rates unchanged at 5%.

Looking ahead, traders will keep an eye on the Canadian annual GDP for the second quarter. The growth number is expected to expand by 1.2%. On the US docket, market players will monitor the US Nonfarm Payrolls due on Friday. The market anticipated that the US economy would create more than 170K jobs in August. Traders will take cues and find trading opportunities around the USD/CAD pair.

- Silver Price remains sluggish as buyers run out of steam around monthly high.

- One-week-old horizontal region joins bearish MACD signals to restrict immediate XAG/USD upside ahead of descending resistance line from late July.

- RSI’s retreat from overbought territory also suggests a pullback towards 200-SMA.

- Fortnight-old rising support line, key Fibonacci ratios act as additional downside filters.

Silver Price (XAG/USD) remains lackluster around $24.25 during the early hours of Tuesday’s Asian session, after failing to cross a one-week-long horizontal hurdle the previous day.

That said, the bearish MACD signals join the RSI (14) line’s retreat from the overbought territory to suggest a consolidation in the XAG/USD price amid sluggish markets, as well as the cautious mood ahead of the mid-tier US data.

With this, the bright metal’s fall towards the $24.00 round figure appears imminent. However, the Silver Price remains on the buyer’s radar unless it stays beyond the 200-SMA support of around $23.85.

In a case where the XAG/USD remains bearish past $23.85, the 50% Fibonacci retracement of June-July upside and a two-week-old rising support line, respectively near $23.70 and $23.45, will challenge the bears.

It’s worth noting that the 61.8% Fibonacci retracement, also known as the “Golden Fibonacci Ratio, of around $23.30 acts as the final defense of the Silver buyers.

On the flip side, the aforementioned one-week-old horizontal resistance area surrounding $24.35-40 guards immediate recovery of the Silver Price ahead of a downward-sloping resistance line from July 20, close to $24.60 of late.

Silver Price: Four-hour chart

Trend: Pullback expected

US inflation expectations can be held responsible for the market’s latest dislike for the US Dollar, after fueling the Greenback to the multi-day high in the last week.

That said, the inflation expectations, as per the 10-year and 5-year breakeven inflation rates from the St. Louis Federal Reserve (FRED) data, reverse Friday’s corrective bounce while declining to the fresh lows in five weeks.

It should be noted that the 5-year and 10-year inflation expectations per the aforementioned calculations fall to 2.21% and 2.30% at the latest.

It’s worth observing that the Fed officials’ inability to please markets with a major hawkish surprise can join the latest weakness in the US inflation clues to weigh on the US Treasury bond yields and the Greenback.

However, the cautious mood ahead of today’s US Conference Board’s (CB) Consumer Confidence Index for August, expected at 116.2 versus prior 117.00, will prod the Greenback and the markets. Above all, major attention will be given to the Fed’s preferred inflation gauge, namely the US Core Personal Consumption Expenditure (PCE) Price Index for July and Nonfarm Payrolls (NFP) for August.

Also read: Forex Today: US Dollar weakens slightly as risk sentiment improves

- GBP/USD defends corrective bounce off 11-week low, edges higher of late.

- Convergence of previous support line, 61.8% Fibonacci retracement joins bearish MACD signal to prod Cable buyers.

- Key DMAs, resistance line from mid-July also challenge Pound Sterling buyers.

- Three-month-old horizontal support appears a tough nut to crack for bears.

GBP/USD grinds higher past 1.2600 after an upbeat start of the week, picking up bids near 1.2610 amid early Tuesday morning in Asia. In doing so, the Cable pair extends the late Friday’s corrective bounce off a three-month-old horizontal support zone towards the previously key technical supports.

That said, a convergence of the 61.8% Fibonacci retracement of the May-July upside and the previous support line from late June, around 1.2630 at the latest, restricts immediate recovery of the Pound Sterling buyers, especially amid the bearish MACD signals.

Even if the quote manages to cross the 1.2630 upside hurdle, the 100-DMA and 21-DMA will challenge the GBP/USD buyers respectively around 1.2645 and 1.2705.

In a case where the Cable pair remains firmer past 1.2705, a downward-sloping resistance line from mid-July, around 1. 2740 by the press time, will be crucial to watch for the bulls before taking control.

On the flip side, the aforementioned horizontal support zone comprising multiple levels marked since early June, close to 1.2550–35, will be crucial to keep the GBP/USD buyers hopeful.

Should the Pound Sterling remain bearish past 1.2535, the odds of witnessing a slump towards May’s monthly bottom of around 1.2300 can’t be ruled out.

Overall, GBP/USD remains on the bear’s radar event if the short-term recovery can’t be ruled out.

GBP/USD: Daily chart

Trend: Limited upside expected

- NZD/USD consolidates between 0.5895-0.5916 range

- The US dollar edges lower as the market sentiment improves on Tuesday.

- Investors await the Labour and economic data release from the US.

The NZD/USD pair oscillates in a narrow trading band between 0.5895-0.5916 region during the early Asian session on Tuesday. Meanwhile, the US Dollar Index (DXY) loses ground below the 104.00 mark. The major pair currently trades near 1.3596, losing 0.03% for the day.

Regarding the Jackson Hole Symposium, Federal Reserve (Fed) Chairman Jerome Powell stated that the additional rate hike cannot be ruled out if required, it would be determined by incoming data. According to World Interest Rates Probabilities (WIRP), the market discounts modest odds of a hike in September, but the probability of a 25 basis point (bps) hike in November increased to nearly 70%. About the data, the US Dallas Federal Reserve Manufacturing Index for August rose to -17.2 from -20 prior, better than the estimation of -21.6.

On the other hand, the Chinese finance ministry said that the authorities would reduce the 0.1% duty on stock trading to stimulate the capital market and strengthen investor confidence. Alongside the action by the Ministry of Finance, the China Securities Regulatory Commission (CSRC) is implementing measures to bolster market confidence in listed companies after the Chinese equities index slumped to nine-month lows. It’s worth noting that the positive headline surrounding China's economic conditions might lift the China-proxy Kiwi and act as a tailwind for the NZD/USD pair.

Last week, the chief economist of the Reserve Bank of New Zealand (RBNZ) said that policymakers would cut the OCR earlier than signaled if China experienced a more significant slowdown than the RBNZ anticipates.

Market participants await the top-tier economic calendar releases from the US. The JOLTs Job Openings figures from July, ADP Employment Change, and Nonfarm Payrolls will be due later this week. Also, the US Gross Domestic Product (GDP), ISM PMI, and Core Personal Consumption Expenditures (PCE) will be in the traders’ focus. Furthermore, New Zealand’s Building Permits MoM for July and Consumer Confidence will be released on Tuesday and Friday, respectively.

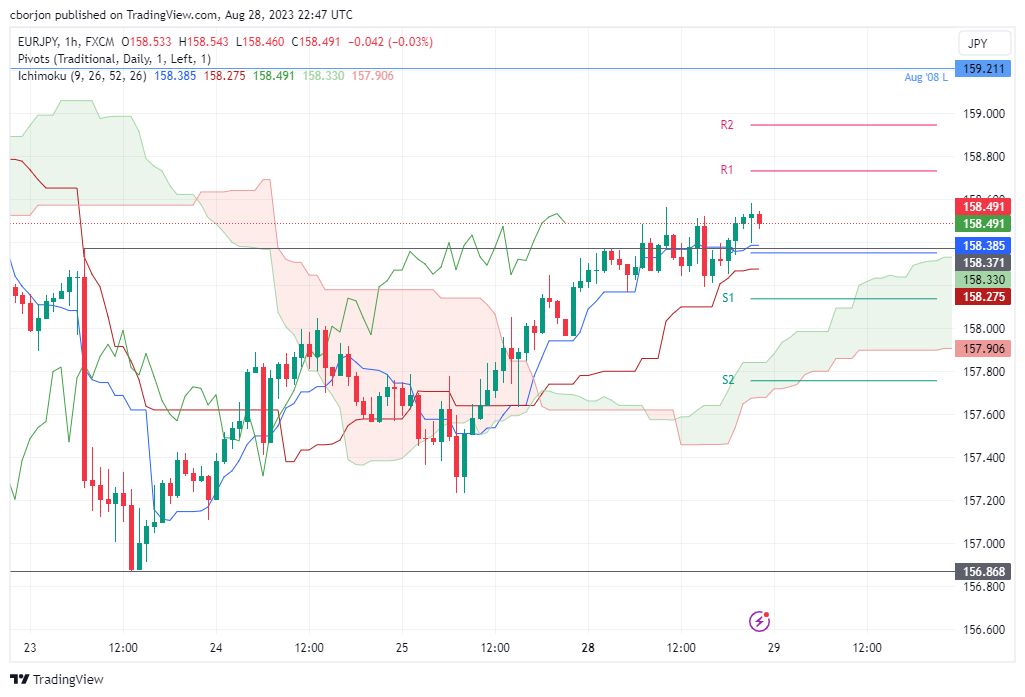

- EUR/JPY trades at 158.47, showing a neutral to downside bias as it hovers near the Tenkan-Sen line at 158.18, with key support and resistance levels in sight.

- Intraday charts suggest the pair may have peaked, dropping below the Tenkan Sen at 158.38, potentially triggering further losses towards the Kijun-Sen at 158.28.

- A climb towards the R1 pivot at 158.74 could set the stage for a retest of the year-to-date high at 159.49, depending on risk sentiment and market dynamics.

As the Asian session begins, the EUR/JPY registers minuscule losses after posting 0.31% of gains on Monday due to an improvement in risk appetite that dragged the pair from around daily lows of 157.97 to its high of 158.56. At the time of writing, the cross-currency pair trades at 158.47, down 0.03%.

EUR/JPY Price Analysis: Technical outlook

The EUR/JPY daily chart portrays the pair as neutral-biased, though slightly tilted to the downside, as it achieved a daily low below the August 18 swing low of 157.65. Nevertheless, the recent leg up could pave the way for retesting year-to-date (YTD) highs of 159.21 unless the EUR/JPY drops below the Tenkan-Sen line at 158.18, followed by the 158.00 mark. Once achieved, the next stop would be the August 23 daily low of 156.87, followed by the top of the Ichimoku Cloud (Kumo) at 155.96.

From an intraday perspective, the cross-currency pair appears to have peaked as EUR/JPY price action loses steam, with the pair failing to achieve a higher high that tests the 159.00 mark. If the EUR/JPY drops below the Tenkan Sen at 158.38, that could exacerbate further losses. The next support would be the Kijun-Sen at 158.28, followed by the S1 daily pivot at 158.14, and then the S2 pivot at 157.75.

Conversely, if EUR/JPY Climbs towards the R1 pivot at 158.74, a test of the YTD high at 159.49 is on the cards.

EUR/JPY Price Action – Hourly chart

- EUR/USD edges higher after snapping two-day downtrend at 11-week low.

- Euro ignores German exporters’ pessimism amid hawkish comments from French FinMin.

- US Dollar fails to extend Jackson Hole inspired gains as traders await top-tier inflation, employment data.

- Consumer sentiment figures from Germany, US will entertain intraday traders.

EUR/USD holds onto the week-start recovery gains around 1.0820 during the early hours of Tuesday’s Asian session. In doing so, the Euro pair cheers the US Dollar’s pullback while tracing the downbeat Treasury bond yields. It’s worth noting, however, that the mixed concerns about Germany and cautious mood ahead of this week’s top-tier inflation and employment data from the US and Eurozone checks the pair buyers.

US Dollar Index (DXY) dropped on Monday after posting the six-week uptrend even as the United States mid-tier activity data improves. That said, the US 10-year Treasury bond yields dropped three basis points (bps) to 4.20% and the two-year counterpart declined half a percent to 5.5% at the latest.

On Monday, Germany’s highly influential IFO institute published a survey of exporters and cited the deteriorating morale in August due to weak global demand. The poll also mentioned, “More and more companies are also complaining about being less able to compete at the global level.”

On the contrary, French Finance Minister Bruno Le Maire ruled out any reduction in interest rates in the coming months. The policymaker also said, “We also need to address inflation pressure in the services sector.”

It should be noted that the US Dallas Fed Manufacturing Business Index improved to -17.2 for August versus -21.6 expected and -20.0 prior. It’s worth noting that the details of the activity gauge were mixed as the new orders and prices paid for raw materials increased but the finished goods prices eased.

Above all, the improvement in the market’s sentiment, mainly backed by China, joined the Fed officials’ inability to please markets with major hawkish surprise seem to weigh on the US Treasury bond yields and the Greenback. However, looming economic concerns about the Old Continent keep the EUR/USD bears hopeful as the top-tier inflation numbers from the bloc and the US for August loom, together with the US employment report.

Moving on, Germany’s GfK Consumer Confidence Survey for September will become the immediate catalyst for the EUR/USD pair and may please the buyers in a case of matching the -24.3 expectations, versus -24.4 prior. Following that, the US Conference Board’s (CB) Consumer Confidence Index for August, expected at 116.2 versus prior 117.00, will entertain the intraday traders.

Technical analysis

A convergence of the 13-day-old falling resistance line and the 10-day SMA, around 1.0850 by the press time, restricts the immediate upside of the EUR/USD pair even as the nearly oversold RSI conditions lure the buyers.

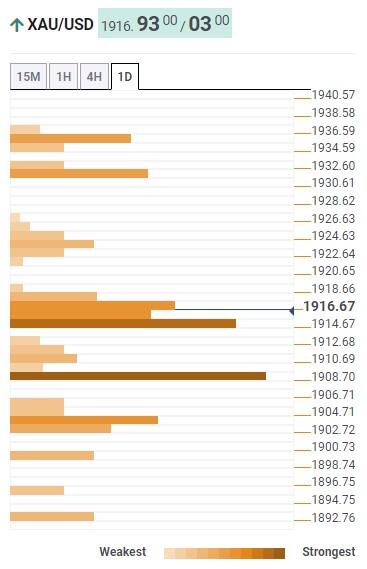

- Gold Price edges higher after positing the first weekly gain in five.

- Softer US Dollar, China-inspired optimism underpins XAU/USD run-up.

- Absence of hawkish surprise at Jackson Hole, softer yields also propel the Gold Price.

- United States CB Consumer Confidence will direct intraday moves, NFP, Fed’s favorite inflation gauge in the spotlight.

Gold Price (XAU/USD) holds onto the week-start strength despite retreating from a 13-day high during the late hours of Monday, edging higher to around $1,920 amid the initial Asian session on Tuesday. In doing so, the XAU/USD cheers the softer US Dollar and Treasury bond yields amid optimism surrounding China, one of the world’s biggest Gold customers. It’s worth noting that the cautious mood ahead of the key United States data, especially after the Federal Reserve (Fed) Chairman Jerome Powell’s emphasis on data dependency, prod the Gold buyers of late.

Gold Price benefits from softer yields, cautious optimism

Gold Price remains on the front foot after a stellar weekly rebound even as the upside momentum softens of late. That said, the XAU/USD cheers China-inspired risk-on mood, as well as the downbeat United States Treasury bond yields and the US Dollar, to lure buyers.

US Treasury bond yields marked the first weekly loss in five by reversing from the highest level since 2007 the last week. That said, the US Dollar Index (DXY) dropped on Monday after posting the six-week uptrend even as the United States mid-tier activity data improves.

On Monday, the US Dallas Fed Manufacturing Business Index improved to -17.2 for August versus -21.6 expected and -20.0 prior. It’s worth noting that the details of the activity gauge were mixed as the new orders and prices paid for raw materials increased but the finished good prices eased.

The downbeat Treasury bond yields and the Greenback could be linked to the absence of any hawkish surprises from the Federal Reserve (Fed) and other central major bankers during last week’s Jackson Hole Symposium. It’s worth noting that Fed Chair Jerome Powell showed readiness for rate hikes while pushing back rate cut bias during his key Jackson Hole speech.

However, the policymaker also highlighted the data dependency and hence increased the importance of the incoming statistics, as well as amplified uncertainty about the US central bank’s next moves, which in turn directed the market players toward the Gold. It should be noted that Cleveland Fed Bank President Loretta Mester favored a rate hike, even if not in September, while the odds of witnessing an increase in the Fed rate in November improved of late, per the CME’s FedWatch Tool.

Additionally, China’s halving of the stamp duty on stocks trading joined a Wall Street Journal (WSJ) piece suggesting Chinese Communist Party Chairman Xi Jinping’s indirect push for stimulus to favor market sentiment and the Gold Price upside.

Elsewhere, firmer equities and receding fears of recession also allow the Gold buyers to remain hopeful.

United States data will direct XAU/USD moves

While the aforementioned catalysts allow the Gold Price to edge higher, a slew of top-tier United States data stands ready to challenge the XAU/USD moves. Among them, the US Conference Board’s (CB) Consumer Confidence Index for August, expected 116.2 versus prior 117.00, will be the first to challenge the Gold buyers in case of printing the upbeat outcome.

It should be observed that the second-tier US housing data and JOLTS Job Openings for July could also entertain the XAU/USD intraday traders. However, major attention will be given to the Fed’s preferred inflation gauge, namely the US Core Personal Consumption Expenditure (PCE) Price Index for July and Nonfarm Payrolls (NFP) for August. Additionally, inflation data from the Eurozone and the growth numbers for India, as well as China’s official Purchasing Managers Indexes for August, will offer extra directions to the Gold traders.

Gold Price Technical Analysis

Gold Price remains between 50 and 200 Exponential Moving Average (EMA) while struggling to keep the buyers on board, especially amid the bearish signals from the Moving Average Convergence and Divergence (MACD) indicator.

However, firmer conditions of the Relative Strength Index (RSI) line, placed at 14, join the XAU/USD’s sustained trading beyond the $1,910 confluence to keep the bulls hopeful. That said, the 50-EMA joins a one-week-old rising trend line to highlight the stated $1,910 level as the short-term key support.

It’s worth noting that a convergence of the 200-EMA and 38.2% Fibonacci retracement of late July-August downside, near $1,925, restricts the short-term Gold Price upside.

Following that, a horizontal area comprising multiple tops marked since early August, close to $1,930, will act as the final defense of the XAU/USD sellers.

On the contrary, a clear downside break of the $1,910 support confluence could quickly drag the Gold Price toward the $1,900 round figure before highlighting the monthly low of around $1,884 for the bears.

Overall, the Gold Price is likely to stay on the recovery mode but the road to the upside appears long and bumpy.

Gold Price: Daily chart

Trend: Limited upside expected

- AUD/USD defends week-start rebound after snapping two-day losing streak.

- Market sentiment improves amid quiet start of the week, yields and Greenback dropped.

- Australia Retail Sales, Dallas Fed Manufacturing Business Index both improved.

- China stimulus, unimpressive Jackson Hole keep buyers hopeful ahead of speech from future RBA Governor Bullock, US CB Consumer Confidence.

AUD/USD edges higher past 0.6400 after a positive start of the week despite a quiet Monday. That said, the Aussie pair managed to cheer China-inspired optimism and a pullback in the US Treasury bond yields, as well as the upbeat Australia’s Retail Sales, the previous day. However, the cautious mood ahead of Reserve Bank of Australia (RBA) Deputy Governor Michele Bullock, to be the Governor in three weeks, prods the traders of the risk-barometer pair during early Tuesday in Asia.

China’s halving of the stamp duty on stock trading joined a Wall Street Journal (WSJ) piece suggesting Chinese Communist Party Chairman Xi Jinping’s indirect push for stimulus to favor market sentiment and the AUD/USD price.

Elsewhere, to the absence of any hawkish surprises from the Federal Reserve (Fed) and other central major bankers during last week’s Jackson Hole Symposium. It’s worth noting that Fed Chair Jerome Powell showed readiness for rate hikes while pushing back rate cut bias during his key Jackson Hole speech.

Talking about the data, Australia’s seasonally adjusted Retail Sales for July rose to 0.5% MoM versus 0.3% expected and -0.8% prior. On the other hand, the US Dallas Fed Manufacturing Business Index improved to -17.2 for August versus -21.6 expected and -20.0 prior.

While portraying the mood, Wall Street benchmarks closed in the green for the second consecutive day while the US 10-year Treasury bond yields dropped three basis points (bps) to 4.20% and the two-year counterpart declined half a percent to 5.5% at the latest.

Looking forward, a speech from the future RBA Governor Bullock will be crucial for the AUD/USD buyers as the Aussie central bank has paused the rate hikes in the last two consecutive meetings. Her will became more important as Australian Treasurer Jim Chalmers flagged expectations of witnessing substantially weaker Australian growth due to higher interest rates from the Reserve Bank of Australia (RBA) and China's slowdown.

Following that, the US Conference Board’s (CB) Consumer Confidence Index for August, expected at 116.2 versus prior 117.00, will entertain the AUD/USD traders. Above all, major attention will be given to the Fed’s preferred inflation gauge, namely the US Core Personal Consumption Expenditure (PCE) Price Index for July and Nonfarm Payrolls (NFP) for August.

Technical Analysis

Bullish MACD signals and nearly oversold RSI tease the AUD/USD bulls within a 13-day-old triangle formation, currently between 0.6450 and 0.6385. However, a downward-sloping resistance line from the mid-July, near 0.6510, acts as an extra hurdle for the buyers.

- GBP/JPY rose above 184.50, consolidating above the 20-day SMA.

- The daily and four-hour chart flash bearish signals.

The GBP/JPY cross closed on Monday with consecutive gains, but bulls seem to be running out of steam.

That being said, fundamentals favour the bulls over the bears. The Bank of Japan (BoJ) has stated changes to monetary policy will only be entertained once local wage and inflation indicators match their projections. On the other hand, investors are pricing in that the Bank of England (BoE) will lift rates to 6%, and monetary policy divergences should maintain the bullish bias intact. On the data front, investors will eye labour market data on Tuesday from Japan and Retail Sales figures from July on Wednesday.

However, on the daily chart for the short term, the Relative Strength Index (RSI) has turned flat above its midline. At the same time, the Moving Average Convergence (MACD) histogram displays increasing red bars, signifying that the bears are slowly gaining ground. There are also signs of exhaustion on the shorter four-hour chart, with the RSI and MACD turning flat in positive territory.

In terms of upcoming supports and resistances, immediate resistances for the bulls are given by the 185.00 area, followed by the 185.80 zone and the cycle high of 186.75 struck last Tuesday. On the downside, the 20-day SMA at 183.95 offers strong support for the cross. If lost, the pair could retest the 183.00 and 181.00 levels.

GBP/JPY Daily Chart

-638288569798510985.png)

- USD/CHF trades at 0.8840, tallying losses for a second consecutive day.

- Investors are still digesting Powell’s words on Friday. Meanwhile, the USD consolidates gains.

- The focus shifts to labour market reports from the US.

At the start of the week, the USD traded soft against most of its rivals, and the DXY index consolidated the 0.80% gains seen on Thursday and Friday. Nonfarm payrolls and economic activity figures will be the week’s highlight for the US, and on the CHF’s side, investors await Retail Sales and Inflation figures from July and August.

After the Chairman of the Federal Reserve (Fed) Jerome Powell stated on Friday that the bank would maintain rates at restrictive levels until the economy shows signs of cooling, he also left the door open for another hike. He pointed out that the bank will proceed “carefully” in the next decisions. Following his words, the US bond yields rose, signifying that the markets placed bets on a more hawkish Fed.

In that sense, World Interest Rates Probabilities (WIRP) suggests that markets discount low odds of a hike in September, but the odds of a 25 basis point (bps) increase in November rose to nearly 70%. Focus now shifts to key labour market figures, including JOLT job Opening, ADP Employment Change, and August’s Nonfarm Payroll report, as a tighter labour market would give the Fed the green light to continue tightening.

USD/CHF Levels to watch

Analysing the daily chart, a neutral to bearish technical outlook is evident for USD/CHF, suggesting that the bears are gaining momentum but still do not have an upperhand over the bulls for the short term. The Relative Strength Index (RSI) has a negative slope above its midline, while the Moving Average Convergence (MACD) prints stagnant green bars. On the other hand, the pair is above the 20-day Simple Moving Average (SMA) but below the 100 and 200-day indicating that there is still some light for the bulls and that the bears have still more ground to cover

Support levels: 0.8830, 0.8800, 0.8780 (20-day SMA).

Resistance levels: 0.8890 (100-day SMA), 0.8915, 0.8950.

USD/CHF Daily Chart

-638288533769102203.png)

During the Asian session, Japan's labor market data is due, with the Unemployment Rate expected to remain at 2.5% in July. Later, current RBA Deputy Governor Michele Bullock will deliver a speech. In the US, the employment data round starts with the JOLTS report.

Here is what you need to know on Tuesday, August 29:

The US Dollar lost ground on a quiet Monday, as stocks in Europe and the US recorded gains. The US Dollar Index pulled back towards 104.00 while US Treasury yields retreated, with the 10-year yield falling to 4.20%.

Regarding US economic data, the Dallas Federal Reserve Manufacturing Index improved to -17.2 from -20, although the details were not particularly positive. On Tuesday, the JOLTS Job Openings report will be released, marking the beginning of several labor market figures, including Nonfarm Payrolls on Fridays. The core Personal Consumption Expenditure Price Index is scheduled for release on Thursday.

EUR/USD moderately rose above 1.0800 on Monday and remained above the 200-day Simple Moving Average. On Tuesday, the German Gfk Consumer Confidence survey is due, while later in the week, the focus will shift to August preliminary inflation figures.

GBP/USD rebounded after a five-day decline, struggling to break above 1.2600. The Pound was supported by improved risk sentiment.

USD/JPY marginally rose and settled around 146.50, marking its highest daily close since November. Japanese labor market data is scheduled for release on Tuesday.

USD/CAD traded sideways around 1.3600, holding onto recent gains. The overall trend remains upward, but a strong barrier exists at 1.3650.

AUD/USD moved sideways but finished higher following positive Australian retail sales data and a weaker US Dollar. On Tuesday, Michele Bullock, who will become the Governor of the Reserve Bank of Australia (RBA) in three weeks, will deliver a speech.

NZD/USD struggled to move away from the critical 0.5900 area, posting minor gains. The bias remains to the downside, but as long as it remains above 0.5900, there could be a corrective move higher.

Gold reached weekly highs above $1,925 as US yields retreated but later trimmed its gains. It is consolidating around $1,920. Silver traded sideways and finished flat around $24.20.

Like this article? Help us with some feedback by answering this survey:

- EUR/GBP trades at 0.8585, testing the 50-day Moving Average at 0.8583, with a daily close above potentially targeting the 0.8600 level.

- Hourly chart shows an upward bias as the pair forms a series of higher lows and higher highs, setting the stage for further gains.

- A breach below the 50-hour SMA at 0.8579 could trigger a pullback, with potential downside targets including Monday’s low of 0.8566 and last Friday’s low of 0.8560.

EUR/GBP climbed late in the New York session to gains above 0.8550, courtesy of a risk-on impulse and technical indicator, suggesting further upside is expected amid the lack of economic data on the UK calendar. The pair is trading at 0.8585, gains 0.11%.

EUR/GBP Price Analysis: Technical outlook

The cross-currency daily chart portrays the pair as neutral to downward biased, as the pair resumed upwards and is testing the 50-day Moving Average (DMA) at 0.8583. A daily close above the latter would expose the 0.8600 figure, followed by the August 14 high of 0.8632. Otherwise, if EUR/GBP stays below 0.8600, that could open the door for further weakness, and it might test the year-to-date (YTD) low of 0.8492.

The EUR/GBP hourly chart depicts the pair as upward biased, with the pair achieving successive series of higher lows and higher highs, which could pave the way for further upside. If EUR/GBP breaks above 0.8600, that could open the door for further gains, with the August 14 high at 0.8632 and the August 11 high at 0.8669. Conversely, if sellers break the 50-hour Simple Moving Average (SMA) ah 0.8579, a pullback is expected towards Monday’s low of 0.8566. A breach of the latter would expose last Friday’s low of 0.8560.

EUR/GBP Price Action – Hourly chart

- GBP/USD trades at 1.2601, up 0.19%, as a UK Summer Bank Holiday and falling US bond yields offer temporary relief to the beleaguered Pound.

- CME FedWatch Tool indicates nearly 50% odds for a 25 bps rate hike in November, keeping the pressure on the GBP/USD pair.

- A packed US economic calendar featuring jobs data and consumer confidence could introduce new volatility and potentially resume the pair’s downtrend.

The British Pound (GBP) stopped its free-fall on Monday against the US Dollar (USD) amidst a UK Summer Bank Holiday, which spurred choppy trading amongst most FX pairs during the overlap of the London-New York session. At the time of writing, the GBP/USD is trading at 1.2601, gaining 0.19%.

GBP gains slightly as US bond yields dip; busy US economic calendar to sway currency dynamics

The current week presents a busy US economic docket, contrary to the UK. On the latter, if not for a speech of the Bank of England (BoE) Chief Economist Huw Pill and the release of housing prices, the GBP/USD fate would lie mainly on the US Dollar dynamics.

However, Monday’s price action was mainly driven by a risk-on impulse, which weighed on global bond yields, particularly in the United States (US). US bond yields tumbled across the board, undermining the greenback, as shown by the US Dollar Index (DXY), a basket of six currencies that measures their performance against the buck, dropped 0.12%, down at 104.060.

Nevertheless, last week’s Jackson Hole speech by the US Federal Reserve (Fed) Chair Jerome Powell was seen as hawkish, as he emphasized the Fed’s commitment to tackle inflation, justifying higher rates if growth continues to be above trend, while the labor market remains tight. He added the US central bank is still data-dependent, noting they would proceed “carefully” when deciding regarding momentary policy.

Following Powell’s remarks, money market futures are confident the Fed will skip a rate hike in September. Nonetheless, for November, the story is different, with traders expecting a 25 bps rate hike, as shown by odds close to 50%, as shown by the CME FedWatch Tool.

Given the backdrop, the GBP/USD pair could resume its downtrend based on the latest data. However, a busy US economic docket could weaken the greenback. On Tuesday, jobs data, consumer confidence, and housing data could ignite volatility in the pair. Any surprises that justify further tightening can pave the way for further US Dollar strength and Sterling (GBP) weakness.

GBP/USD Price Analysis: Technical outlook

After falling below the August 3 low of 1.2620, the GBP/USD extended its losses below the 1.2600 figure but hovers around the latter as of writing. From a market structure perspective, the pair has achieved successive lower lows, opening the door for a bearish continuation. If the pair achieves a daily close above 1.2600, the pair could test last Friday’s high of 1.2654. Otherwise, the major would resume its downtrend toward the 1.2500 figure, followed by the 200-day Moving Average (DMA) at 1.2401.

- The EUR/USD rose near 1.0810, above the 200-day SMA of 1.0805.

- The USD and US yields consolidated after Jerome Powell’s speech on Friday.

- ECB’s hawks lift the Euro.

In Monday’s session, the USD is trading weak against most of its rivals, mainly driven by a slight consolidation and a risk-positive market environment. On the other hand, the European Central Bank's hawkish rhetoric is gaining more ground while markets still asses Jerome Powell’s speech on Friday.

During his speech at the Jackson Hole Symposium, Chair Powell didn’t commit to another hike but pointed out that the economy hasn’t cooled down as expected and that as long as inflation doesn't give in, the Federal Reserve (Fed) will maintain rates at a restrictive stance. As a reaction, the US yields sharply rose, as according to the CME FedWatch tool, investors are now betting on nearly 50% odds of a hike in November.

That said, US bond yields are pulling back on Monday, although they maintain elevated levels. The rate for the 2-year bond stands at 5.05%, whereas the rates for the 5-year and 10-year bonds are at 4.41% and 4.22%, respectively. In addition, the USD measured by the DXY index slightly retreated but still traded at its highest level since early June, above the 104.00 zone.

On the Euro’s side, Robert Holzmann from the ECB made it clear at the start of the week that he sees “a case for pushing on with rate increases without taking a pause” in case no surprises arise. Still, he confirmed the ECB’s data-dependent approach. In line with that, investors will eye crucial inflation figures from Germany and the EU from August to be released on Wednesday and Thursday to continue placing their bets on the ECB’s next decisions.

In the meantime, according to the World Interest Rates Probabilities (WIRP) tool, markets are currently discounting a 45% probability of a 25bps increase in the upcoming September 14, 2023 meeting. Moving forward, the likelihood of a 25bps hike stands at 66% in October, followed by a 75% chance of a similar increase in the December meeting. This anticipated rate hike trajectory would result in a target rate of 5%.

EUR/USD Levels to watch

From a technical standpoint, the EUR/USD maintains a bearish outlook for the short term, as observed on the daily chart. The Relative Strength Index (RSI) is comfortably positioned in the negative territory below its midline. It is also complemented by a negative signal from the Moving Average Convergence Divergence (MACD), which shows red bars, signalling bearish momentum. Moreover, the pair is below the 20,100 and 200-day Simple Moving Averages (SMAs), suggesting that the bears are firmly in control of the bigger picture.

Support levels: 1.0800 (200-day SMA), 1.0780, 1.0750.

Resistance levels: 1.0830,1.0850, 1.0900.

EUR/USD Daily Chart

-638288439937931668.png)

- AUD/USD registers gains of around 0.40%, as upbeat Australian retail sales data and falling US bond yields offer a respite from recent losses.

- CME FedWatch Tool shows a 49% chance of a 25 bps rate hike in November, keeping the pressure on AUD/USD despite its current gains.

- A packed economic calendar featuring US JOLTs report and remarks from RBA’s nominated Governor, Michelle Bullock, could introduce new volatility to the pair.

The Australian Dollar (AUD) reverses its course advances from around last week’s low of 0.6380 against the US Dollar (USD), bolstered by upbeat economic data, despite a hawkish rhetoric by the US Federal Reserve (Fed). Falling US bond yields lent a lifeline to the AUD, as the AUD/USD trades at 0.6428, gaining 0.42%.

AUD gains traction as US bond yields dip, as markets eye data releases

The AUD/USD is set to extend its losses after the US Federal Reserve Chair, Jerome Powell, delivered hawkish remarks at Jackson Hole. Even though the pair is staging a comeback after snapping two days of losses, the resumption of higher US bond yields could underpin the greenback in the near term.

Powell said that despite two good reports on inflation, it would be appropriate to tighten monetary policy and that they would proceed “carefully” when choosing to hike rates or stay put. Jay Powell states they would remain data-dependant and warranted additional hikes if “above trend growth” and employment remained solid.

Following Powell’s remarks, money market futures are confident the Fed will skip a rate hike in September, but the odds for November are rising, as shown by the CME FedWatch Tool seeing a 49% chance of a 25 bps rate hike,

The US Dollar Index, a gauge of the buck’s value against a basket of six currencies, drops to its daily low at 103.977, a headwind for the USD/MXN.

Developments in the Asian session witnessed China’s delivering stimulus amidst its troubled property sector and its equity markets. That spurred a risk-on response, with AUD/USD buyers propelling the currency pair back above the 0.6400 figure.

Data during the Asian session, the Australia economic docket revealed that retail sales for July jumped by 0.5% MoM, after a dismal 0.8% in June, exceeding estimates of 0.3%. However, it should be said that the Women’s World Cup boosted sales.

ANZ analysts think the trend in retail sales will continue to be lower. They said, “We think households will continue to tighten their spending throughout 2023. We do, however, see some upside to spending in 2024 as inflation moderates and real household incomes turn positive.”

On Tuesday, the US economic docket would feature the JOLTs report, housing prices, and the CB Consumer Confidence. The Reserve Bank of Australia’s (RBA) nominated Governor Michelle Bullock would cross newswires on the Australian front. That, alongside the release of Building Permits, Construction Work done, and the Consumer Price Index (CPI) for July on a monthly basis, could stir the AUD/USD.

AUD/USD Price Analysis: Technical outlook

The AUD/USD is likely to remain consolidated despite registering solid gains. For the pair to resume its uptrend, buyers must reclaim the latest swing high of 0.6488, ahead of challenging 0.6500. Otherwise, since the major remains in a downtrend, an extension below last week’s low of 0.6379, and the pair might test the year-to-date (YTD) low of 0.6364, ahead of diving towards the November 22 daily low at 0.6272.

- NZD/USD rose back above 0.5900, displaying nearly 0.20% gains.

- The USD DXY and US yields are retreating after sharply rising on Friday following Powell’s speech.

- Eyes on labour market and economic activity figures from the US.

On Monday, the NZD/USD gained traction and rose above 0.5900. No relevant data was released for the US and New Zealand and the upward momentum can be explained by the USD slightly retreating against its rivals, consolidating Thursday and Friday’s gains.

Markets are still assessing Jerome Powell’s words on Friday. He didn’t commit to another hike and addressed that the monetary policy is still data-dependant and the data justifies another hike. In addition, he stated that the economy hasn’t cooled down as expected and that they will retain rates at restrictive levels until inflation shows signs of deceleration.

All eyes are now on the US economic calendar releases this week, which include mid and high-tier labour market figures, including JOLTs Job Openings figures from July and ADP Employment Change and Nonfarm Payrolls from August. In addition, Gross Domestic Product (GDP), ISM PMI and Core Personal Consumption Expenditures (PCE) will also be closely watched for investors to model their expectations for the next Fed meetings.

In the meantime, according to the CME FedWatch tool, the odds of a hike in September are still low, but the probabilities increased nearly 50% for the November meeting.

NZD/USD Levels to watch

Based on the daily chart, it is evident that NZD/USD leans toward a bearish outlook in the short term. The Relative Strength Index (RSI) remains below its midline, deep in negative territory, showcasing a neutral slope near the oversold threshold. Similarly, the Moving Average Convergence Divergence (MACD) exhibits red bars, emphasizing the strengthening bearish momentum for NZD/USD. Also, the pair is below the 20,100 and 200-day Simple Moving Averages (SMAs), indicating a challenging position for the buyers in the bigger picture as the bears remain in command.

Support levels: 0.5900, 0.5870, 0.5850.

Resistance levels: 0.5940, 0.5950, 0.5980.

NZD/USD Daily Chart

-638288403803828007.png)

- USD/MXN trades at 16.7187, down 0.13%, as the Mexican Peso capitalizes on interest rate differentials and Banxico’s hawkish outlook.

- Despite Powell’s hawkish remarks, the US Dollar Index dropped to a daily low of 103.977, providing a tailwind for the Peso against the greenback.

- A busy week ahead features Mexican Q2 growth figures and key US economic indicators, which could introduce new volatility to the USD/MXN pair.

The Mexican Peso (MXN) resumed its gains against the US Dollar (USD) due to the interest rate differential of the former against the greenback, despite last Friday’s hawkish remarks by the US Federal Reserve Chair Jerome Powell. The USD/MXN is eyeing a fall to test the year-to-date (YTD) low of 16.6238, but it trades at 16.7187, down 0.13%.

USD/MXN dips as Banxico keeps its hawkish stance, and US Dollar Index retreats

US equities depict investors’ positive mood amid an absent US economic calendar. Last week’s Fed Chair Jerome Powell’s speech weighed on the USD/MXN, though by the end of the New York session, the MXN extended its gains. The US Dollar Index, a gauge of the buck’s value against a basket of six currencies, drops to its daily low at 103.977, a headwind for the USD/MXN.

The Fed Chair Jerome Powell said that despite two good reports on inflation, it would be appropriate to tighten monetary policy and that they would proceed “carefully” when choosing to hike rates or stay put. Powell states they would remain data-dependant and warranted additional hikes if growth and employment remained solid.

Developments in the Asian session witnessed China’s delivering stimulus amidst its troubled property sector and its equity markets. That spurred a risk-on response, though stocks remained pressured as global central banks would likely continue to tighten monetary conditions.

The Bank of Mexico (Banxico) policymakers remain hawkish on the Mexican front, as the latest meeting minutes revealed. Even though headline inflation continued to decelerate to 4.67% in August, the Mexican central bank would remain “cautious” given the inflationary outlook, with one member highlighting that Banxico could remain on hold for the rest of 2023.

In the week ahead, the Mexican economic agenda will deliver growth figures for the second quarter on Tuesday. The US docket will reveal Home prices, JOLTs Jobs Opening, and the CB Consumer Confidence indicator.

USD/MXN Price Analysis: Technical outlook

The pair remains downward biased, as the 20-day Simple Moving Average (SMA) turned flat, though it remains above the 50-day SMA. With the USD/MXN managing to print successive series of lower lows, the YTD low of 16.6238 could be tested in the near term, followed by the October 2015 daily low of 16.3267. Contrarily, the USD/MXN could shift bullish if it reclaims the 17.0000 figure.

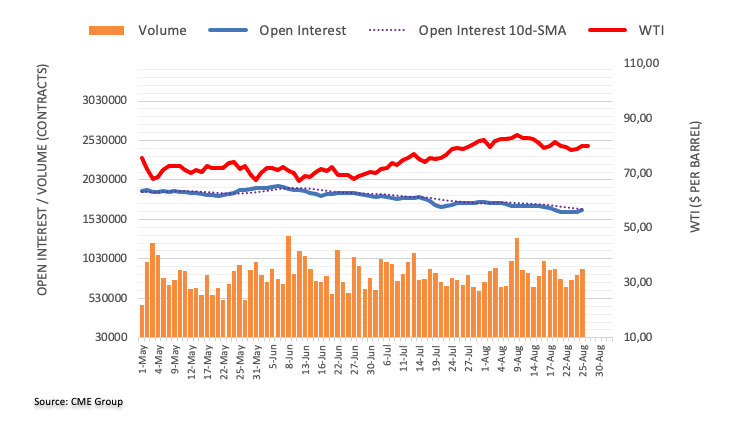

- WTI trades near $80.00 after jumping to a daily high near $80.80.

- The fragile Chinese economic situation limits upside potential. Economic support may favour Oil prices.

- Hawkish Jerome Powell may also limit the upside.

The West Texas Intermediate (WTI) climbed back above $80 at the start of the week. Still, its upside is limited due to the Chinese economic situation and investors placing bets on a more aggressive Federal Reserve (Fed). On the upside, markets monitor potential supports that the Chinese government may take.

Investors assess the Chinese situation and Powell’s words on Friday

Oil prices managed to maintain momentum despite Chinese economic woes. The real-estate sector remains fragile while the Evergrande’s stock plummeted more than 80%. In that sense, what is boosting Oil prices is the potential Chinese action to support and bolster the local economy.

On the other hand, the black gold may see further downside as Chair Powell stated that he is looking for the US economy to cool down and that the bank will maintain rates until inflation shows concrete evidence that it is decelerating.

In line with that, World Interest Rates Probabilities shows that markets are currently discounting a 90% probability of a no hike in the forthcoming Sep 20, 2023 meeting. Moving forward, the likelihood of a 25bps hike stands at 70% in November. This anticipated rate hike trajectory would result in a target rate of 5.75%. It is worth noticing that higher rates cool down economies, lowering the demand for energy and, hence, applying downward pressure on Oil prices.

WTI Levels to watch

The daily chart analysis suggests a neutral to bullish outlook for WTI, with the bulls gaining strength, although challenges persist. The Relative Strength Index (RSI) indicates positive momentum with an ascending slope just above its midline, while the Moving Average Convergence (MACD) presents lower red bars. Additionally, the pair is below the 20-day Simple Moving Average (SMA), but above the 100 and 200-day SMAs, highlighting the continued dominance of bulls in the broader perspective.

Support levels: $79.80, $78.20, $77.70

Resistance levels: $81.15 (20-day SMA), $82.00, $82.50

WTI Daily Chart

-638288355236161909.png)

- USD/JPY surges to a new YTD high of 146.68, buoyed by Wall Street’s upbeat opening and dovish comments from BoJ Governor Kazuo Ueda.

- Despite a dip in US 10-year Treasury yields, the pair maintains its bullish momentum, reflecting the Fed’s hawkish stance on further tightening.

- A packed economic calendar could introduce volatility, including key US and Japanese indicators.

USD/JPY resumes its uptrend, prints a new year-to-date (YTD) high of 146.68, on an upbeat sentiment, with Wall Street opening the week on a higher note amidst thin liquidity conditions due to the UK’s Summer Bank Holiday. Hence, the Japanese Yen (JPY) extended its losses to three straight sessions spurred by dovish remarks by the Bank of Japan’s (BoJ) Governor Kazuo Ueda. The pair exchanges hands at 146.60.

Japanese Yen extends its losses as Wall Street climbs and BoJ’s Ueda remains dovish

US equities resumed their uptrend following hawkish remarks by the US Federal Reserve (Fed) Chair Jerome Powell at Jackson Hole. Despite being data-dependent, Powell’s words reinforced the US central bank hawkish stance, which triggered a leg-up in the USD/JPY pair. He added that robust economic expansion and the constrained labor market would warrant further tightening by the Fed if those economic indicators don’t show signs of easing.

The USD/JPY advance stalled as US Treasury bond yields began to lose ground, particularly the US 10-year Treasury Note, with its coupon sliding two basis points at 4.22% and undermining the greenback.

On the Japanese front, the BoJ Governor Kazuo Ueda said that underlying inflation is still below target and justified the current “dovish” monetary policy stance by the BoJ, even though July’s core consumer inflation rose by 3.1%. Ueda added that inflation “is expected to decline.”

Although the BoJ tweaked its Yield Curve Control (YCC) to a 0.50%-1% flexible target, the 10-year Japanese Government Bonds (JGBs) yield has failed to break higher, which could shift the USD/JPY pair bias bearish. Once the BoJ signals it is ready to normalize its monetary policy, the USD/JPY could resume lower after posting gains of 11.85% in the year.

A busy economic calendar could rock the boat in the week ahead. The US docket would feature JOLTs report, the CB Consumer Confidence, the release of the Gross Domestic Product, the Fed’s preferred gauge for inflation, the core PCE, US employment data, and business activity. On the Japanese front, speeches by two BoJ members.

USD/JPY Price Analysis: Technical outlook

The US Dollar rally against the Japanese Yen is set to continue if not for vocal expressions of Japanese authorities threatening to intervene in the FX markets. After hitting a new YTD high, the USD/JPY could extend its gains towards the November 3 high at 148.45, followed by the October 31 high at 148.84, before piercing 149.00. The major’s downside risks emerge at the Tenkan-Sen line at 145.61. If breached, the next stop would be the August 23 swing low of 144.54.

- Silver price oscillates around $24.00 as investors await a fresh economic trigger.

- August economic data carry a higher impact as they will be considered primarily for September’s monetary policy.

- Silver price trades directionless near the 61.8% Fibonacci retracement at $24.12.

Silver price (XAG/USD) has traded in a narrow range marginally above $24.00 for the past four trading sessions. The white metal struggles to find direction despite Federal Reserve (Fed) Chair Jerome Powell delivering a hawkish commentary at the Jackson Hole Symposium on Friday.

Fed Powell kept doors open for more interest rate hikes as the achievement of price stability in the United States economy has a long way to go. Jerome Powell said that further policy action will be dependent on incoming data. Investors will keep focus on the labor market and the factory activity data. August economic data carry a higher impact as they will be considered primarily for September’s monetary policy.

The S&P500 opens on a positive note despite rising expectations of one more interest rate hike from the Fed in 2023. Cleveland Fed Bank President Loretta Mester said she supports one more interest rate hike, though not necessarily in September. The US Dollar Index (DXY) demonstrates a lackluster performance at around 104.00.

As per the CME Group Fedwatch Tool, there is a more than 80% chance of the Fed keeping interest rates unchanged in September, while the majority of investors are betting on an interest-rate hike in November.

Silver technical analysis

Silver price trades directionless near the 61.8% Fibonacci retracement (plotted from July 20 high at $25.27 to August 15 low at $22.23) at $24.12 on a two-hour scale. Upward-sloping 20-period Exponential Moving Average (EMA) at $24.17 is providing support to the Silver bulls.

The Relative Strength Index (RSI) (14) shifts into the 40.00-60.00 range from the bullish range of 60.00-80.00, which indicates that the bullish impulse has faded. However, the upside bias is still intact.

Silver two-hour chart

-638288287102464599.png)

- EUR/USD reverses two consecutive sessions of losses.

- The resumption of the selling pressure could see 1.0765 retested.

EUR/USD manages to regain some balance and reclaims the 1.0800 neighbourhood at the beginning of the week.

In case bears regain the upper hand, the pair could slip back to the August low of 1.0765 (August 25). South from here emerges the May low of 1.0635 (May 31) ahead of the 2023 low of 1.0481 (January 6).

A drop below the 200-day SMA, today at 1.0805, should keep extra pullbacks in store for the time being.

EUR/USD daily chart

- DXY trims part of the recent two-day advance.

- Bulls remain focused on the May high in the 104.70 zone.

DXY comes under pressure and confronts the key support at the 104.00 region at the beginning of the week.

Immediately to the upside turns up the August top at 104.44 (August 25), while the surpass of this level should open the door to a rapid test of the May high of 104.69 (May 31) prior to the 2023 peak of 105.88 (March 8).

While above the key 200-day SMA, today at 103.10, the outlook for the index is expected to shift to a more constructive one.

DXY daily chart

- USD/CAD oscillates in a narrow range around 1.3600 amid sideways US Dollar.

- Fed Powell at Jackson Hole diverged the focus of investors to economic data citing that the central bank will remain data-dependent.

- Canada’s Q2 GDP is expected to deliver a slower pace vs. Q1 figures, which would allow the BoC to maintain the status quo.

The USD/CAD pair oscillates in a narrow range near the round-level resistance of 1.3600 in the late European session. The Loonie asset remains sideways following the footprints of the US Dollar Index (DXY), which is struggling to find a decisive move, trading around 104.00.

S&P500 futures posted some decent gains in the London session, warranting a positive opening ahead. US equities are expected to remain in action as investors fully assessed the commentary from Federal Reserve (Fed) Chair Jerome Powell at the weekend.

The US Dollar remained muted marginally above 104.00 on Monday as investors shifted their focus toward upcoming economic data for August. Fed Powell at Jackson Hole diverged the focus of investors to economic data citing that the central bank will remain data-dependent for further action. Jerome Powell commented that two months of decline in inflationary pressures is only the beginning of what we need to build confidence in the inflation path.

This week, investors will keep an eye on the labor market and ISM manufacturing PMI data for August. For further policy action, market participants want to know whether labor market conditions are cooling or still remain extremely tight. Signs of a cooling labor market would stem pressure on the US Dollar.

On the Canadian Dollar front, investors are focusing on the April-June quarter Gross Domestic Product (GDP), which will be released on Friday at 12:30 GMT. As per Reuters, Q2 data is expected to show the economy grew at a slower pace of 1.1% from the 3.1% pace recorded for the January-March quarter. This would allow the Bank of Canada (BoC) to announce an unchanged interest rate decision and will keep interest rates steady at 5%.

- EUR/JPY extends the recovery beyond 158.00.

- Immediately to the upside turns up the 160.00 mark.

EUR/JPY advances for the third session in a row and surpasses the 158.00 mark on Monday.

If the move higher gathers extra impulse, the cross should challenge recent 2023 peaks near 159.50 (August 22) ahead of the key round level at 160.00. The surpass of the latter should not see any resistance level of note until the 2008 high at 169.96 (July 23)

So far, the longer term positive outlook for the cross appears favoured while above the 200-day SMA, today at 147.70.

EUR/JPY daily chart

UOB Group’s Senior Economist Julia Goh and Economist Loke Siew Ting review the latest inflation figures in Malaysia.

Key Takeaways

Headline inflation decelerated for an 11th straight month to 2.0% y/y in Jul (from +2.4% in Jun), marking the lowest level since Aug 2021. The outturn was close to ours and Bloomberg consensus (2.1%). This came on the back of a persistent slowdown in price gains of food, transport, and selected services (i.e. restaurants & hotel, communication, and recreation services & culture) amid base effects and continued government subsidies during the month.

We expect inflation to hover at the edge of 2.0% in the remaining months of the year, leading to an average inflation rate of 2.8% for the entire year of 2023 (BNM est: 2.8%-3.8%, 2022: 3.3%). Our view takes into consideration the government’s pledge to maintain most of its subsidies for 2H23, an absence of global supply shocks particularly energy and essential food items, as well as in-house expectations for the currency. Easing core CPI growth and services inflation further imply a continuation of disinflation trend in the coming months.

- US Dollar price action begins week in the red, eating into Friday’s gains.

- Traders face an eventful week with the monthly US jobs report out on Friday.

- US Dollar Index to test support levels without putting its uptrend at risk.

The US Dollar (USD) should be vulnerable to profit-taking these first few days of the week as traders have mulled the Jackson Hole speech from US Federal Reserve Chairman Jerome Powell. Although the speech did not hold any surprises, the repetition of the content was enough to dampen any hopes for an early Goldilocks scenario and saw yields spiking higher and rate cuts being pushed further down the line to mid-2024 at the earliest. Traders this week will focus on the coming macroeconomic data points for any sudden contractions that might urge the Fed to rethink its strategy and still cut sooner.

A very mild calendar for this Monday, especially with the United Kingdom bank holiday. Expect even more lower volumes than normal for a Monday, which means any moves in the markets need to be taken with a pinch of salt. One datapoint to look out for this Monday is the Dallas Fed Manufacturing Business Index for August, expected to contract further from -20 to -21.60.

Daily digest: US Dollar settles for less

- The overall takeaway for this week will be that markets now have pushed forward any possible rate cuts after the rather repetitive hawkish stance of the Fed. Hopes for early cuts and a Goldilocks scenario have dampened and been pushed toward mid-2024 at the earliest. Any datapoint this week that points to deterioration of the current economic conditions or health of the US economy might make investors double down on their bets that rate cuts still might come sooner since the Fed could be forced to start cutting in an attempt to protect US economic growth.

- At 14:30 GMT, the Dallas Fed Manufacturing Business Index for August is due to be published as the first data point to kick off this week. A contraction is expected from -20 to -21.6.

- Equities are jumping higher in Asia with the Japanese Topix index up 1.47% and the Hong Kong Hang Seng Index up 1.31%. The Hang Seng would have been higher if it had not been forced to drag along the 80% decline from construction group Evergrande, which is set to default anytime now. European markets are not applauding the moves in Asia as they are synthetically pushed higher because of the rate cuts and lower taxes from the Chinese finance ministry on stock trading.

- The CME Group’s FedWatch Tool shows that markets are pricing in an 80.5% chance that the Federal Reserve will keep interest rates unchanged at its meeting in September. This is the lowest number in weeks as markets start to consider the possibility of another rate hike.

- The benchmark 10-year US Treasury bond yield trades at 4.21% after touching a new yearly high last week on Monday at 4.3618%. After its stellar move, yields could start to slip lower a touch as markets have repriced the Jackson Hole communication.

US Dollar Index technical analysis: Look down

The US Dollar has been in a firm rally since mid-July and has been shooting for the stars last week with traders favoring the US Dollar again. The favoritism simply boiled down to the rate differential as the US is holding a higher interest rate and thus a better return on deposits against, for example, the Euro (EUR/USD) or the Japanese Yen (USD/JPY), which both have lower depositary rates than the Greenback. Seeing the steep incline from last week, a short pullback is more than granted, though support needs to be respected in order to keep the July rally ongoing and in good shape.

On the upside, 104.69, the high of May 31, comes into play as the level to beat to the upside. Once that level is broken and consolidated, look for a surge to 105, where 105.110 (the peak of March 15) is an ideal candidate for a double top. Should the Greenback be on a tear, expect then at least a test at 105.88 – the 2023 peak from March 8.

On the downside, several floors are likely to prevent a steep decline in the DXY. The first one now is the big figure at 104. Though seeing the current decline, that does not look strong enough to hold. Rather look for the 200-day Simple Moving Average at 103.14. That is a much better candidate in order to catch some profit-taking pressure and re-enter. In case it does not hold, the safety net at 102.33 comes into play with both the 55-day SMA and the 100-day SMA both just being inches away from each other.

USD/IDR is now seen extending the consolidation within 15,240 and 15,340 in the next weeks, notes Markets Strategist Quek Ser Leang at UOB Group.

Key Quotes

Last week, we held the view that USD/IDR “is likely to strengthen further, but March’s peak near 15,475 is likely out of reach”. However, USD/IDR traded in a range of 15,235/15,338 before ending the week largely unchanged at 15,290 (+0.07%). USD/IDR appears to have moved into a consolidation phase; this week, it is likely to trade sideways between 15,240 and 15,340.

Markets Strategist Quek Ser Leang at UOB Group suggests further consolidation lies ahead for USD/MYR in the short-term horizon.

Key Quotes

Last week, we held the view that USD/MYR “could consolidate for a few days first before rising to 4.6700 later on.” Our view did not materialise, as USD/MYR traded in a relatively quiet manner between 4.6330 and 4.6570.

The price movements appear to be consolidative, and USD/MYR could continue to trade in a range this week, likely between 4.6200 and 4.6700.

- USD/CHF recovers from 0.8820 as the Fed is expected to raise interest rates one more time this year.

- Fed Powell warned that the process of achieving price stability has a long way to go.

- Investors will keenly watch the US labor market and ISM Manufacturing PMI data for August.

The USD/CHF pair finds support after a correction near 0.8820 as chances of one more interest rate hike by the Federal Reserve (Fed) deepened. The Swiss Franc asset is expected to extend recovery further as further policy tightening by the Fed will widen the Fed-Swiss National Bank (SNB) policy divergence.

S&P500 futures add some gains in Europe, portraying strength in the risk appetite of the market participants. US equities were heavily bought on Friday despite Fed Chair Jerome Powell delivering a hawkish commentary. The appeal for risk-sensitive assets improved as Fed Powell reiterated the need for more interest rate hikes but it will be data-dependent.

Fed Powell warned that the process of achieving price stability has a long way to go. Therefore, the Fed is expected to keep interest rates higher for a longer period.

Cleveland Fed Bank President Loretta Mester said she supports one more interest rate hike, though not necessarily in September. She emphasized on achieving price stability by the end of 2025 and should not allow it to drift into 2026. After Mester and Powell’s hawkish commentary, chances of an interest rate hike in November shoot above 50%.

Investors will keenly watch the United States labor market and ISM Manufacturing PMI data for August, which will be released later this week.

Meanwhile, the Swiss Franc remains on tenterhooks as investors shift focus to the SNB interest rate decision, which will be announced later this month. Investors remain mixed about policy stance as Swiss inflation has come down to near 2%. It would be worth watching whether the SNB Chairman Thomas J. Jordan would remain hawkish to ensure inflation below 2% or allow the current monetary policy to demonstrate its ability to tame inflation.

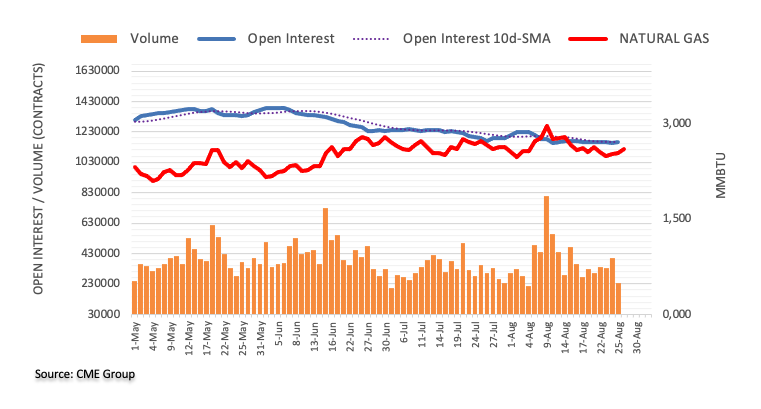

- Natural Gas price jumps in the US and Europe.

- The US Dollar is set to weaken after its relentless peak last week.

- Uptrend still intact as price heads to $3.25.

Natural Gas price is jumping higher this morning in the US (+2.7%) and more substantially in Europe (+8%) as a perfect storm is brewing on the supply front. Several reports are coming in that Australian unions are losing control of the situation as several independent strikes are emerging in the port sector, putting at risk again the 10% volume of global gas supply for the coming weeks. To make matters worse, Norway is reporting that supply has been halted from its Troll field since Saturday for planned maintenance.

The US Dollar (USD), in the meantime, is facing some selling pressure after it peaked several times last week. The US Federal Reserve Chairman Jerome Powell reiterated that rates need to remain elevated for longer, which dampened the hope that was living in the markets for rate cuts in early 2024. These hopes are now placed toward the end of the second quarter. For this week, traders will be on edge with the US jobs report on Friday.

At the time of writing, Natural Gas is trading at $2.818 per MMBtu.

Natural Gas news and market movers

- India’s Gujarat State Petroleum Corporation is seeking to buy one cargo for late September delivery, according to inside traders. The tender is due to expire on August 28.

- European gas storage is at 92%, while France is lagging a touch with 88%.

- Norway has shut down its Troll gas field for maintenance, in another setback for European gas supply.

- Australian LNG workers are firing up local and independent strikes as unions are normally rounding up the voting on Monday for the improved Chevron wage proposal. The independent strikes make it more difficult for the unions to bring forward one single plan for all workers and local disruptions might trigger bigger supply issues further down the line.

- Tropical storm Idalia is set to hit Florida by Tuesday. Bigger parts of Alabama and Georgia are bound to be hit as well once it hits landfall.

- This week, all eyes on the market moving US jobs report on Friday.

Natural Gas Technical Analysis: crossing the river

Natural Gas is a textbook example of how technical analysis together with macro and fundamentals is a cocktail that works. Last week any news was in disfavor of the commodity, though support held and the ascending longer term trend channel is still very much intact. Seeing the current cocktail of supply drought, Natural Gas prices could jump to $3.25 if the current sentiment and the news flow keeps contributing to higher prices.

On the upside, $3 is still the level to watch once Natural Gas prices can reclaim $2.9. Should prices recover, look for a close above $2.935, the high of August 15, in order to confirm that demand is picking up again. More upside toward $3 and $3.065 (high of August 9) would be targets or levels to watch.

On the downside, the trend channel has done a massive job underpinning the price action. Aside for one small false break, ample support was provided near $2.60. The 55-day Simple Moving Average needs to give that much needed support at $2.69 ahead of the ascending trend channel at $2.61. Any falling knives can still be caught by the 100-day SMA near $2.55.

-638288089145356947.png)

XNG/USD (Daily Chart)

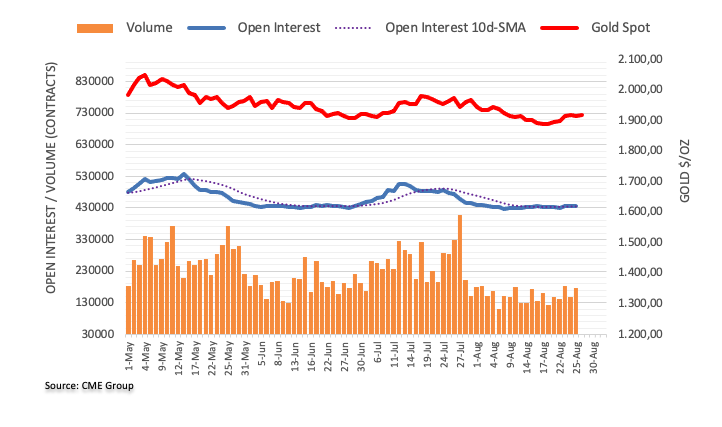

- Gold price turns sideways after a solid recovery as investors await fresh triggers for further action.

- Fed’s Powell kept doors open for further policy tightening to ensure price stability.

- Fed’s Mester supports one more interest rate hike, though not necessarily in September.

Gold price (XAU/USD) turned lackluster after defending the critical support of $1,900.00 on Monday. The precious metal consolidates as investors prepare for crucial economic indicators such as Nonfarm Payrolls (NFP) and ISM Manufacturing PMI for August, which will be released later this week. The impact of August economic data will be very significant as Federal Reserve (Fed) Chair Jerome Powell reiterated at the Jackson Hole Symposium that further policy action will be data-dependent.

Jerome Powell at Jackson Hole said that the achievement of price stability has a long way to go. Powell kept doors open for further policy tightening if economic data continues to remain supportive. After Powell’s commentary, investors expect that the central bank could raise interest rates in November as a last nail in the coffin.

Daily Digest Market Movers: Gold price shifts focus to economic data

- Gold price consolidates above $1,910.00 as investors digest the impact of the hawkish commentary from Fed Chair Jerome Powell at the Jackson Hole Symposium.

- Powell’s speech was very much in line with market expectations. The Fed’s chair confirmed that the central bank can raise interest rates further as the job of ensuring price stability has not been completed yet but promised that policymakers will remain very careful in upcoming policy meetings.

- Powell also emphasized that incoming data will be a major factor for further policy action.

- The central bank has evidence that inflation is getting more responsive to labor markets. Powell said that further signs of a tightening job market could warrant more Fed action.

- About achieving price stability, Jerome Powell said that "inflation remains too high, the process of bringing down inflation still has a long way to go, even with more favorable recent readings."

- The precious metal could face some selling pressure as Cleveland Fed Bank President Loretta Mester said she supports one more interest rate hike, though not necessarily in September.

- As per the CME Group Fedwatch Tool, there is a more than 80% chance of the Fed keeping interest rates unchanged in September, while the majority of investors are betting on an interest-rate hike in November.

- Fed’s Mester said that, after being done with hiking rates, the central bank needs to hold rates for a while. The policymaker emphasized on achieving price stability by the end of 2025 and should not allow it to drift into 2026.

- About rate cut discussions, Fed Mester is in favor of re-evaluating it in the second half of 2024. She believes that the central bank has a good shot at attaining 2% inflation without damage to the real economy.

- Philadelphia Fed Bank President Patrick Harker supports holding interest rates steady as labor markets are cooling. Harker added that interest rates could be increased if inflation reaccelerates.

- As Jerome Powell talked about dependency on incoming data for further policy action, United States Nonfarm Payrolls (NFP) and ISM Manufacturing PMI data for August will remain in focus this week.

- US hiring has slowed down in the past few months, but the Unemployment Rate has remained at historic lows and wage growth has been strong.

- Factory activity has been contracting for the past nine straight months as US firms are operating at lower capacity due to a bleak demand outlook.

- Also, US firms are clearing their old inventories as expansion plans have been postponed due to higher borrowing costs.

- The US Dollar Index (DXY) remains supported around 104.00 and is expected to turn lackluster as investors prepare for crucial economic indicators.

Technical Analysis: Gold price consolidates around $1,915

Gold price turns sideways around $1,915.00 after defending the crucial support of $1,900.00 as investors digest Powell’s hawkish commentary at the Jackson Hole Symposium. On a broader note, the precious metal is auctioning in a range of $1,904-$1,922 from Thursday. The yellow metal made two consecutive Spinning Top candlesticks, signaling indecisiveness among market participants. The precious metal regains territory above the 200-day Exponential Moving Average (EMA) at $1,907 but the 20-day EMA at $1,916 is still restricting its upside potential.

Fed FAQs

What does the Federal Reserve do, how does it impact the US Dollar?

Monetary policy in the US is shaped by the Federal Reserve (Fed). The Fed has two mandates: to achieve price stability and foster full employment. Its primary tool to achieve these goals is by adjusting interest rates.

When prices are rising too quickly and inflation is above the Fed’s 2% target, it raises interest rates, increasing borrowing costs throughout the economy. This results in a stronger US Dollar (USD) as it makes the US a more attractive place for international investors to park their money.

When inflation falls below 2% or the Unemployment Rate is too high, the Fed may lower interest rates to encourage borrowing, which weighs on the Greenback.

How often does the Fed hold monetary policy meetings?

The Federal Reserve (Fed) holds eight policy meetings a year, where the Federal Open Market Committee (FOMC) assesses economic conditions and makes monetary policy decisions.

The FOMC is attended by twelve Fed officials – the seven members of the Board of Governors, the president of the Federal Reserve Bank of New York, and four of the remaining eleven regional Reserve Bank presidents, who serve one-year terms on a rotating basis.

What is Quantitative Easing (QE) and how does it impact USD?

In extreme situations, the Federal Reserve may resort to a policy named Quantitative Easing (QE). QE is the process by which the Fed substantially increases the flow of credit in a stuck financial system.

It is a non-standard policy measure used during crises or when inflation is extremely low. It was the Fed’s weapon of choice during the Great Financial Crisis in 2008. It involves the Fed printing more Dollars and using them to buy high grade bonds from financial institutions. QE usually weakens the US Dollar.

What is Quantitative Tightening (QT) and how does it impact the US Dollar?