- Аналітика

- Новини та інструменти

- Новини ринків

Новини ринків

- EUR/USD pares post-Fed gains within eight-day-old descending trend channel.

- Fears of ECB’s dovish hike prod Euro bulls, positioning for US Q2 GDP also weigh on prices.

- Upbeat oscillators, sustained trading beyond key horizontal support, rising trend line favor Euro buyers.

- 50-SMA will act as the last defense of EUR/USD bears before challenging yearly top.

EUR/USD reverses corrective bounce off a two-week low with an eight-day-old bearish trend channel, declining 0.07% intraday to 1.1080 amid the early hours of Thursday’s Asian session.

In doing so, the Euro pair consolidates the previous day’s gains amid hopes of witnessing a dovish outcome from the European Central Bank (ECB), other than the widely expected 0.25% rate hike from the ECB. It should be noted that the cautious mood ahead of the first readings of the US Gross Domestic Product (GDP) for the second quarter (Q2) Annualized, expected to ease to 1.8% from 2.0%, as well as the Durable Goods Orders for June, likely easing to 1.0% from 1.8% prior (revised), also weigh on the EUR/USD price.

Technically, the EUR/USD pair is likely to defy the latest bearish channel formation by taking clues from the bullish MACD signals and upbeat RSI (14).

Adding strength to the bullish bias for the Euro pair could be the successful trading above the five-week-old horizontal support zone, around 1.1000, as well as an upward-sloping support line stretched from late May, close to 1.0945 by the press time.

In a case where the EUR/USD remains weaker past 1.0945, the odds of witnessing a slump toward the monthly low of 1.0833 can’t be ruled out.

On the flip side, a clear break of 1.1110 will defy the bearish channel but the 50-SMA hurdle of around 1.1150 prods the Euro bulls before directing them to the yearly top marked on July 18 around 1.1275.

EUR/USD: Four-hour chart

Trend: Further upside expected

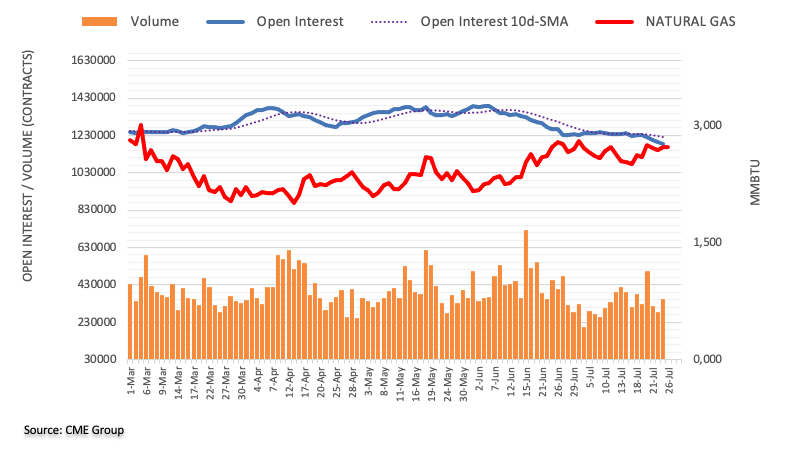

- Natural Gas Price recovers after posting the biggest daily loss in two weeks.

- Federal Reserve’s rate hike, readiness for September lift weigh on XNG/USD even as US Dollar remains depressed.

- Russian gas output drops 14.9% during January-June period.

- Risk catalysts, US GDP eyed for clear directions of the Natural Gas Price.

Natural Gas Price (XNG/USD) takes clues from Russia to pare the biggest daily loss in a fortnight around $2.70 during early Thursday morning in Asia. In doing so, the XNG/USD also reverses the Federal Reserve (Fed) inflicted losses as the US Dollar lacks upside momentum while market sentiment improves.

As per the latest Russia Natural Gas output data from the Rosstat statistics office, per Reuters, the natural gas output reached 267 billion cubic meters (bcm), down 14.9% from the same period in 2022. The energy update also states that Russia produced 34.6 bcm of natural gas in June, down 11.9% from the same month last year.

On Wednesday, Federal Reserve (Fed) matched the widely forecasted increase of 25 basis points (bps) to the benchmark Fed rates toward the multi-year high in the range of 5.25%-5.50%. Following the rate decision, Fed Chairman Jerome Powell tried to placate the hawks by showing readiness for a September rate hike as he said, that the June inflation Consumer Price Index was welcomed but “was only one month's report.”

It should be noted that the rejection of recession fears was also an effort to please the US Dollar buyers but failed. However, the commodities failed to cheer the USD’s weakness and rather slumped amid disappointment that the end of the global rate hike trajectory isn’t near.

Apart from the US Dollar weakness and Russia-inspired move, the market’s optimism ahead of the advance readings of the US Q2 GDP Annualized, expected to ease to 1.8% from 2.0%, as well as the Durable Goods Orders for June, likely easing to 1.0% from 1.8% prior (revised), also favor the XNG/USD bulls.

Additionally, a likely easing in the US Energy Information Administration’s (EIA) Natural Gas Storage Change for the week ended on July 21, from 41B to 23B, also underpins the XNG/USD rebound.

Technical analysis

Repeated failures to cross the three-week-old horizontal resistance area surrounding $2.78-79 directs the Natural Gas price towards the 21-DMA support of around $2.66.

- GBP/USD edges higher after positing two-day winning streak.

- Sustained break of 50-SMA, upbeat oscillators favor Pound Sterling buyers.

- Two-week-old horizontal resistance, convergence of important trend lines prod Cable buyers.

- US GDP, Durable Goods Orders test Pound Sterling bulls despite upbeat oscillators.

GBP/USD bulls take a breather after a two-day uptrend, making rounds to the weekly top surrounding 1.2960 amid the early hours of Thursday’s Asian session. In doing so, the Cable pair portrays the market’s cautious mood ahead of the top-tier data/events, as well as portrays consolidation ahead of the key upside hurdles.

It’s worth noting, however, that the bullish MACD signals and the upbeat RSI (14) line, now overbought, join the GBP/USD pair’s upside break of the 50-SMA to favor the pair buyers.

However, a two-week-old horizontal resistance area surrounding 1.2960-70 guards the immediate upside of the Pound Sterling.

Following that, a convergence of the previous support line stretched from late June and a fortnight-long descending trend line, close to 1.3010 at the latest, will act as the final defense of the GBP/USD pair sellers, a break of which won’t hesitate to challenge the yearly top around 1.3145.

On the flip side, a clear break of the 50-SMA level of around 1.2910 can direct the GBP/USD price toward the 50% Fibonacci retracement of its late June to early July upside, near 1.2865.

Even so, the 200-SMA and 61.8% Fibonacci retracement together could challenge the Cable pair bears around 1.2810-2800.

Overall, GBP/USD stays on the bull’s radar but the road towards the north is long and bumpy.

Elsewhere, the cautious mood ahead of the first readings of the US Gross Domestic Product (GDP) for the second quarter (Q2) and the European Central Bank’s (ECB) monetary policy meeting, as well as US Durable Goods Orders for June, prods the GBP/USD bulls.

Also read: GBP/USD shoots higher as Fed chair sticks to the data dependent script

GBP/USD: Four-hour chart

Trend: limited upside expected

- NZD/USD remains flat near the 0.6200 area after the Fed's decision and statement.

- As expected, the Federal Reserve (Fed) raises rates by 25 basis points (bps) to 5.25%–5.5%.

- Investors will shift their focus to US Q2 GDP, weekly Jobless Claims and Durable Goods Orders.

The NZD/USD pair remains steady around the 0.6200 mark in the early Asian session after hitting multi-day highs at 0.6235 and pulling back. The US dollar Index (DXY), a measure of the value of the Greenback against six other major currencies, weakened across the board following the Fed's decision and statement. The DXY dropped to 100.85 and rebounded above the 101.00 area. The US 10-year Treasury yield traded at around 3.87%, and the 2-year at 4.85%.

As widely expected, the Federal Reserve (Fed) raised interest rates by 25 basis points (bps) to 5.25%–5.5% on Wednesday. The rate was last seen just before the housing market collapse in 2007, and marked the highest level in more than 22 years.

During a news conference, Fed Chairman Jerome Powell stated that inflation has moderated somewhat since the middle of last year but that the Fed's 2% target "has a long way to go." Even so, he left room for the Fed to keep rates unchanged at its September meeting. He added that the Fed will consider the incoming data for additional rate hikes if needed.

On the other hand, the Reserve Bank of New Zealand (RBNZ) maintained the official cash rate (OCR) unchanged at 5.50% in the July meeting, which triggered further downside on the Kiwi. However, the downside potential for the NZD/USD pair appears limited as the market expects a more hawkish stance from the RBNZ.

In the absence of economic data released from New Zealand, the USD's valuation is likely to continue to influence the pair's movement. Market participants will shift their focus to the US Advance GDP QoQ. Also, the weekly Jobless Claims and Durable Goods Orders are due later in the day.

- AUD/USD fades post-Fed recovery after snapping two-day winning streak.

- Disappointment from Australia inflation, China woes supersedes unimpressive FOMC, Powell’s speech to keep Aussie bears hopeful.

- More clues of Aussie inflation eyed for immediate directions, highlighting Q2 Export-Import Price Index.

- Advance readings of US Q2 GDP, Durable Goods Orders will be crucial for clear directions.

AUD/USD fails to cheer the Federal Reserve’s (Fed) inability to please the US Dollar bulls for long, despite an initial 50 pips jump to 0.6783, as it retreats to 0.6760 amid early Thursday morning in Asia. In doing so, the Aussie pair traders seem to convey their dovish bias about the Reserve Bank of Australia (RBA) after the previous day’s downbeat inflation data. Also weighing on the risk-barometer pair could be the market’s cautious mood ahead of the top-tier US data and mixed headlines about China.

Federal Reserve (Fed) matched the widely forecasted increase of 25 basis points (bps) to the benchmark Fed rates toward the multi-year high in the range of 5.25%-5.50%. Following the rate decision, Fed Chairman Jerome Powell tried to placate the hawks by showing readiness for a September rate hike as he said, that the June inflation Consumer Price Index was welcomed but “was only one month's report.” It should be noted that the rejection of recession fears was also an effort to please the US Dollar buyers but failed.

On the other hand, Australia’s headline Consumer Price Index (CPI) for the second quarter (Q2) of 2023 drops to 0.8% QoQ versus 1.0% expected and 1.4% prior while the Reserve Bank of Australia (RBA) Trimmed Mean CPI came in as 1.0% compared to 1.1% market forecasts and 1.2% prior for the said period. Further, the Monthly CPI matches 5.4% analysts’ expectations for June versus 5.6% prior.

Following the downbeat Aussie inflation data, Australian Treasurer Jim Chalmers praised the direction but also added that there is a long way to go to beat inflation.”

Elsewhere, fresh challenges to the US-China ties, due to Washington’s push for a law to keep China investments from US companies in check, also seem to tease the AUD/USD bears of late.

Amid these plays, Wall Street benchmarks edged lower while the US 10-year Treasury bond yields marked the first daily loss in three by closing around 3.87%. That said, the US Dollar Index (DXY) also declined and marked a two-day losing streak before posting lackluster moves of late.

Looking ahead, the second-quarter (Q2) Export Price Index and Import Price Index from Australia will be closely examined for more clues about inflation and the next RBA move. Following that, the advance readings of the US Q2 GDP Annualized, expected to ease to 1.8% from 2.0%, as well as the Durable Goods Orders for June, likely easing to 1.0% from 1.8% prior (revised), will be eyed for clear directions. It should be noted that the European Central Bank (ECB) monetary policy meeting will also affect the US Dollar and hence should be watched for a clear guide.

Technical analysis

A clear U-turn from a fortnight-old resistance line, near 0.6785 by the press time, directs AUD/USD toward a three-week-old rising trend line, close to 0.6740 at the latest.

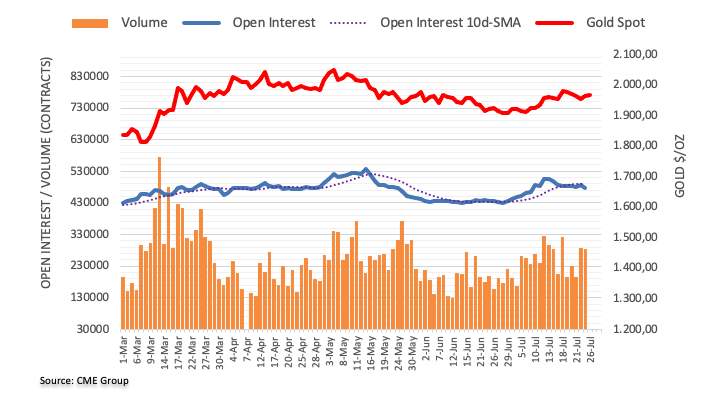

- Gold Price struggles to defend latest gains while fading upside momentum below key resistance.

- XAU/USD retreats as US Dollar licks Federal Reserve-inflicted losses.

- Fed announced 0.25% rate hike and Chairman Jerome Powell’s marked hawkish play but failed to inspire US Dollar, favoring Gold price.

- ECB needs to justify policy pivot concerns to weigh on XAU/USD, via softer Euro, US GDP eyed too.

Gold Price (XAU/USD) retreats from the weekly top, probing a two-day uptrend around $1,972 amid early hours of Thursday’s Asian session, as markets await more clues to defend the post-Federal Reserve (Fed) gains of the yellow metal. Also likely to have weighed on the XAU/USD could be the cautious mood ahead of the first readings of the US Gross Domestic Product (GDP) for the second quarter (Q2) and the European Central Bank’s (ECB) monetary policy meeting. Above all, the Federal Reserve and Chairman Jerome Powell’s inability to guide the market by meeting the 0.25% rate hike and leaving the door open for the September rate increase favored the Gold buyers before the pre-data anxiety prods the metal.

Gold Price edges higher as Federal Reserve, Powell fail to please US Dollar bulls

Gold Price refreshed weekly top after the US Federal Reserve (Fed) Interest Rate Decision, which matched the widely forecasted increase of 25 basis points (bps) to fuel the rate toward the multi-year high in the range of 5.25%-5. 50%. Following the rate decision, Fed Chairman Jerome Powell tried to placate the hawks by showing readiness for a September rate hike as he said, that the June inflation Consumer Price Index was welcomed but “was only one month's report.” It should be noted that the rejection of recession fears was also an effort to please the US Dollar buyers but failed.

Following the Fed event, the US Treasury bond yields and the US Dollar dropped, which in turn helped the Gold Price to remain firmer and refresh the weekly top around $1,978, before retreating amid cautious mood ahead of the top-tier data/events.

Mixed China headlines, United States data also favor XAU/USD bulls

Apart from the Fed-inspired run-up, the Gold Price also remains firmer as the biggest XAU/USD customer, namely China, shows readiness for further stimulus. It’s worth noting, however, that the fresh challenges to the US-China ties, due to Washington’s push for a law to keep China investments from the US companies in check, seem to prod the XAU/USD bulls of late.

Elsewhere, the Conference Board’s (CB) Consumer Confidence Index for July has been positive but the housing numbers for June are mixed. That said, the previously released inflation and employment clues haven’t been impressive. Even so, the International Monetary Fund (IMF) raised the US economic growth forecast for 2023 to 1.8% from 1.6% forecast in April.

ECB, US Q2 GDP eyed for Gold Price directions

Although the Gold Price is all set to register a fourth consecutive weekly gain, the ability of the European Central Bank (ECB) and the US Gross Domestic Product (GDP) for the second quarter (Q2) to renew the US Dollar upside and weigh on the XAU/USD can’t be ruled out. The same requires a close watch on these data/events. That said, US Durable Goods Orders for June and weekly Initial Jobless Claims also become important to watch for clear directions.

That said, the ECB is expected to follow the Fed while announcing a 0.25% increase in the benchmark interest rates. However, President Christine Lagarde’s ability to defend the hawks will be crucial to allow the Euro in staying firmer.

On the other hand, the advance reading of the US Q2 GDP Annualized is expected to ease to 1.8% from 2.0% while the Durable Goods Orders for June may also ease to 1.0% from 1.8% prior (revised). Both these data suggest challenges for the US Dollar and favor to the Gold Price and hence solid reaction to the positive surprise can’t be ruled out.

Gold Price Technical Analysis

Gold Price lures sellers as it fades the early-week rebound from the convergence of a 100-Exponential Moving Average (EMA) and a one-month-old rising support line, around $1,955 by the press time.

Also favoring the downside bias about the XAU/USD price could be the receding bullish power of the Moving Average Convergence and Divergence (MACD) indicator, as well as a retreat of the Relative Strength Index (RSI) line, placed at 14.

It’s worth noting, however, that a clear downside break of the $1,954 support confluence becomes necessary to convince the Gold sellers. Following that, a downward trajectory toward a two-month-old horizontal support zone near $1,930 and then to the previous monthly low of around $1,893 can’t be ruled out.

On the contrary, multiple tops marked since May 19 restrict short-term Gold Price upside near $1,985.

In a case where the Gold Price remains firmer past $1,985, the $2,000 round figure and March’s peak of around $2,010 will act as the final defense of the XAU/USD sellers.

Gold Price: Four-hour chart

Trend: Further downside expected

- USD/MXN bears are still in control as US Dollar weakness.

- A risk factor for the Peso remains developments in the US.

Currencies of most Latin American countries extended gains on Wednesday after a widely expected interest rate hike from the US Federal Reserve, with the Mexican Peso continuing its decline within the long-term bearish trend in USD/MXN.

Latam currencies have benefited from attractive yields this year given surging interest rates in the region. An important risk factor for the Mexican Peso remains developments in the US.

''If the US economy cools down more than expected, this would also weigh on the Mexican outlook. This would likely limit upside risks to inflation and could imply a sharper cut in Mexican interest rates and a correspondingly less attractive real interest rate outlook, which would weigh on the peso,'' analysts at Commerzbank explained.

''In our baseline scenario, however, we expect solid domestic demand and Banxico's vigilance to continue to support the peso in the face of a still uncertain inflation outlook.''

USD/MXN charts

The weekly chart shows the price in decline below the fresh key structure.

On the daily chart, the correction could be running out of steam and reversion to the downside could be the cards. Bears eye a break of support for the forthcoming days.

Market participants will continue to digest the FOMC meeting during the Asian session. Economic data due On Thursday includes the Export and Import Price Index in Australia. Later in the day, the ECB is expected to raise interest rates by 25 basis points. Additionally, key economic data from the US is due, including the preliminary Q2 GDP growth.

Here is what you need to know on Thursday, July 27:

The Federal Reserve (Fed) raised its key interest rates by 25 basis points to 5.25%-5.5%, as expected. The rate reached levels not seen in more than 11 years. The decision and the statement offered no surprises. Chair Powell mentioned that the June inflation Consumer Price Index was welcomed but “was only one month's report.” He added that if data suggests more hikes are needed, “that is the judgment we'll make.”

After the Fed and Powell delivered, the US dollar weakened but only modestly, and US yields pulled back moderately. The DXY dropped 0.25%, ending around 101.00. The US 10-year Treasury yield settled around 3.87%, and the 2-year at 4.85%. The focus will turn to economic data, starting on Thursday with the preliminary Q2 GDP data. The growth report will also include inflation indicators. At the same time, the weekly Jobless Claims and Durable Goods Orders are due.

EUR/USD rose after falling during six consecutive days, supported by a weaker US Dollar. The pair held above the 20-day Simple Moving Average (SMA), but found resistance at 1.1100. On Thursday, the European Central Bank (ECB) will announce its decision on monetary policy. A rate hike is expected, and the focus will be on the language.

Analysts at Nordea:

A 25bp rate hike at the ECB July meeting looks like a done deal, so all focus is on what the central bank will signal about the future. Will the ECB be in a pure data-dependent mode, or does it want to indicate that further hiking looks likely?

ECB Preview: Forecasts from 12 major banks, the final 25 bps?

GBP/USD rose for the second day in a row, holding firm above 1.2900, while EUR/GBP remains subdued, hovering around 0.8560. USD/CHF lost ground for the second day, reaching weekly lows under 0.8600.

Commerzbank on CHF

Price pressure in Switzerland has eased somewhat recently. Nevertheless, the SNB remains concerned about second-round effects. It is therefore likely to remain hawkish for the time being, favouring a strong franc. We have therefore adjusted our forecast slightly. However, we still see a moderately weaker franc in the course of the year since price pressure should ease and the SNB should increasingly tolerate a weaker franc.

AUD/USD finished lower but remained above the 20-day SMA and above 0.6730. The upside faces resistance below 0.6800. The Aussie weakened during the Asian session following softer-than-expected inflation data from Australia. On Friday, the Producer Price Index is due.

NZD/USD remained flat around 0.6215 as it continues to move sideways. The pair hit multi-day highs at 0.6235 and then pulled back. USD/CAD remains in a range below the 20-day SMA at 1.3230 and 1.3150.

Crude oil pulled back from monthly highs, falling less than 1%, with the WTI ending around $79.00. Gold rose after the FOMC meeting but failed to consolidate above $1,975. Silver also climbed but pulled back after testing levels above $25.00.

Like this article? Help us with some feedback by answering this survey:

- The Fed hiked rates by 25 bps as expected to 5.25-5.50%, its highest in 22 years.

- All eyes are now on ECB’s decision on Thursday, expected to deliver a 25 bps hike.

The EUR/USD is trading positive after 6 consecutive days of losses, precisely at 1.1090 and 0.37% gains during the session.

As expected, the Federal Reserve (Fed) hiked rates by 25 basis points and is positioned in the 5.25%-5.50% target. However, during the press conference, Chair Powell did not commit to a hike in September as ongoing decisions will depend on incoming data.

Regarding the economic assessment, Powell noted that economic activity and the labour market remain robust but that inflation remains too high.

That said, the DXY index fell to 101.030, showing a decrease of 0.26% on the day. Additionally, the US treasury yields on 2, 5 and 10-year are in negative territory at 4.85%, 4.11% and 3.87%, respectively, and applied further pressure on the USD.

Regarding Thursday's European Central Bank (ECB) decision, markets have largely priced in a 25 bps hike, and investors will look for clues regarding forward guidance. As for now, the odds of a hike according to the World Interest Rate Possibilities (WIRP) in Septmeber fell below 50%, but in October and December are largely priced in, so messaging will be key.

EUR/USD Levels to watch

According to the daily chart, the technical outlook for the EUR/USD has improved as indicators are starting to gain strength but still, the bears are holding their ground. The Relative Strength Index (RSI) with a slightly upward slope to the north, while the Moving Average Convergence Divergence (MACD) is still in negative territory, printing red bars. That being said, the bulls managed to defend the 20-day Simple Moving Average (SMA) so outlook for the EUR/USD is bright on the bigger picture.

Resistance levels: 1.1100, 1.1150,1.1190.

Support levels: 1.1050 (20-day SMA), 1.1030, 1.1000.

EUR/USD Daily chart

- USD/CAD has popped towards resistance and a bullish bias on the charts is eyed going forward.

- A break of last week's lows opens risk for a downside continuation.

USD/CAD is sidelined on the front side of the bearish trend and has not been rattled by what was a rather benign outcome form the Federal Reserve meeting. The Fed, raised its interest rate decision by a 25 bps rate hike to 5.25-5.50%, as expected.

Federal Reserve statement, and key notes

- Fed says FOMC vote was unanimous.

- CBO revises 2023 us real Gross Domestic Product growth forecast to 0.9% from 0.1% forecast in Feb due to H1 labour market strength.

- Fed: Will consider extent of additional firming to curb inflation.

- Fed: We will continue to reduce our bond holdings as described in previously announced plans.

- Fed: Tighter credit conditions are likely to weigh on economic activity, hiring and inflation, extent to which remains uncertain.

- Fed: Recent indicators suggest economic activity has been expanding at a moderate pace vs a modest pace in June statement.

- Fed: We will continue to assess additional information and its implications for policy.

- Fed: Banking system is sound and resilient.

As a result of the statement:

- Interest rate futures put chance of Fed hike at 18% in September, 36.5% in November post-FOMC.

- Probability of Fed hike was 18.9% in Sept, 37.3% in nov pre-FOMC.

Analysts said the FOMC meeting was as expected, with Chair Jerome Powell "playing it close to straight down the middle" between hawkish and dovish on the rates outlook going forward.

Nevertheless, the US Dollar was nudged lower, as seen by the DXY index, a measure of the Greenback against six major peers. It fell 0.345% at 1.1093.

USD/CAD daily chart

Consequently, USD/CAD popped towards trendline support and follow-through will see the price eyeing up overhead resistance as illustrated above. Should this hold, then there will be a focus on current support again. Overall, however, the price will be on the backside of the old bearish trendline and that leaves a bullish bias on the charts going forward. A break of last week's and this week's lows, however, opens risk for a downside continuation.

- XAG/USD jumped towards $24.90, its highest in six days.

- The Fed delivered a 25 bps hike as expected, but Chair Powell didn’t commit to further hikes.

- USD weakness and falling US yields allowed the metal to gain ground

In the middle of the week, the XAG/USD pair is trading strong, showing 0.88% of gains so far this day. As the market expected, the Federal Reserve (Fed) effectively raised the interest rate by 25 basis points. Fed's Chair Jerom Powell emphasized that “a rate hike in September is possible, but also stated that it is possible not to raise rates”. Powell also highlighted the importance of 'meeting by meeting' as the following decisions will be based on the data that comes out.

Following this, US treasury yields on 2, 5 and 10-year bonds which could be seen as the opportunity cost of holding precious metals, are trading lower at 4.82%, 4.09% and 3.85%, respectively. Additionally, the DXY index is losing ground at 0.30% below 101.00.

XAG/USD Levels to watch

According to the daily chart, there is a strong bullish momentum. The Relative Strength Index (RSI) with a slightly upward slope to the north, while the Moving Average Convergence Divergence (MACD) index prints smooth green bars indicating a favourable momentum for the bulls in the market. On the bigger picture, the metal is trading above the 20,100 and 200-day Simple Moving Averages (SMA)suggesting that bulls are in command.

Resistance levels: 25.00, 25.30, 25.50

Support levels: 24.50, 23.98 (20-day SMA), 23.84 (100-day SMA).

XAG/USD Daily chart

-638259988635581696.png)

FOMC Chairman Jerome Powell comments on the policy outlook and responds to questions from the press after the Federal Reserve's decision to raise the policy rate by 25 basis points to 5.25-5.5% following the July policy meeting.

Key quotes

"The economy is weathering the banking turmoil well."

"We want wage growth at a rate consistent with 2% inflation over time."

"We don't think that wages were an important cause of inflation early but are an important part of bringing inflation down now."

"There's a range of views on the Committee at this meeting and the next meeting, that will be reflected in the minutes."

"Could be cutting rates while continuing QT, the two are independent things, the active tool for policy is rates."

About Jerome Powell (via Federalreserve.gov)

"Jerome H. Powell first took office as Chair of the Board of Governors of the Federal Reserve System on February 5, 2018, for a four-year term. He was reappointed to the office and sworn in for a second four-year term on May 23, 2022. Mr. Powell also serves as Chairman of the Federal Open Market Committee, the System's principal monetary policymaking body. Mr. Powell has served as a member of the Board of Governors since taking office on May 25, 2012, to fill an unexpired term. He was reappointed to the Board and sworn in on June 16, 2014, for a term ending January 31, 2028."

FOMC Chairman Jerome Powell comments on the policy outlook and responds to questions from the press after the Federal Reserve's decision to raise the policy rate by 25 basis points to 5.25-5.5% following the July policy meeting.

Key quotes

"Even with a soft landing, you would still have some softening in labor conditions."

"We've seen softening not through higher unemployment but through fewer openings and quits."

"We hope it continues."

"Hiking until we get to 2% is a formula for going past target."

"If we see inflation coming down credibly, we can move down to a neutral level and then below neutral at some point."

"Not going to make a numerical assessment of when and where that would be."

About Jerome Powell (via Federalreserve.gov)

"Jerome H. Powell first took office as Chair of the Board of Governors of the Federal Reserve System on February 5, 2018, for a four-year term. He was reappointed to the office and sworn in for a second four-year term on May 23, 2022. Mr. Powell also serves as Chairman of the Federal Open Market Committee, the System's principal monetary policymaking body. Mr. Powell has served as a member of the Board of Governors since taking office on May 25, 2012, to fill an unexpired term. He was reappointed to the Board and sworn in on June 16, 2014, for a term ending January 31, 2028."

FOMC Chairman Jerome Powell comments on the policy outlook and responds to questions from the press after the Federal Reserve's decision to raise the policy rate by 25 basis points to 5.25-5.5% following the July policy meeting.

Key quotes

"There is a lot of uncertainty around the length of policy lags."

"No one should doubt that we will use tools to bring inflation to target."

"I would say policy is restrictive, more so after today's decision."

"We have come a long way, we are resolutely committed to returning inflation to target."

"Inflation has proven more resilient than expected."

"Policy is working about as we expected."

"I don't think we're targeting wage inflation."

"Seeing a cooling in private sector in job market in latest report."

"Lot of uncertainty about outlook to next meeting let alone next year."

"I don't think there will be cuts this year."

About Jerome Powell (via Federalreserve.gov)

"Jerome H. Powell first took office as Chair of the Board of Governors of the Federal Reserve System on February 5, 2018, for a four-year term. He was reappointed to the office and sworn in for a second four-year term on May 23, 2022. Mr. Powell also serves as Chairman of the Federal Open Market Committee, the System's principal monetary policymaking body. Mr. Powell has served as a member of the Board of Governors since taking office on May 25, 2012, to fill an unexpired term. He was reappointed to the Board and sworn in on June 16, 2014, for a term ending January 31, 2028."

- NZD/USD rose above 0.6200 and jumped to positive territory.

- Fed hiked rates by 0.25% as expected to 5.25-5.50%.

- Powell opened the door to “not hike rates” in September.

The NZD/USD cleared daily losses and jumped to positive territory towards the 0.6220 area.

The Federal Reserve (Fed) hiked rates by 25 basis points (bps) to the 5.25-5.50% target. In the presser, Jerome Powell didn’t commit to further hikes noting that ongoing decisions will depend fully on incoming data.

Regarding his economic assessment, he noted that economic activity remains robust, the labour tight, and inflation elevated. In addition, he stated that the Fed expect some “softening” of the labour market and some below-the-trend growth.

During the presser, the US Treasury yields fell sharply, which applied pressure on the USD. The 2-year yield fell to 4.86%, while the 5 and 10-year rates fell to 4.10% and 3.86%, all three with more than 0.50% losses.

NZD/USD Levels to watch

According to the daily chart, the outlook is neutral to bearish. The Relative Strength Index (RSI) Index is in positive territory, slightly above the middle line. At the same time, the Moving Average Convergence Divergence (MACD) index prints soft red bars suggesting that the bears are holding their ground. On the bigger picture, the pair holds above the 20,100 and 200-day Simple Moving Averages (SMA), which suggests that the buyers are in command.

Support levels:0.6223 (20-day SMA), 0.62139 (100-day SMA), 0.61978 (200-day SMA).

Resistance levels: 0.6240, 0.6300,0.6350

NZD/USD Daily chart

-638259947247772569.png)

- GBP/USD bulls have moved in for the kill on the Fed and Fed chair Powell.

- GBP/USD rides daily support and looks to extend the bullish trend.

GBP/USD has spiked to break the prior highs of the day and stays the course with regards to the technical bullish correction that is illustrated below. Meanwhile, GBP/USD is trading between 1.2875 and 1.2958 on the day but around the Fed, 1.2895 and 1.2985 have been the range so far.

The Federal Reserve, Fed, raised its interest rate decision by a 25 bps rate hike to 5.25-5.50%, as expected.

Federal Reserve statement, and key notes

- Fed says FOMC vote was unanimous.

- CBO revises 2023 us real Gross Domestic Product growth forecast to 0.9% from 0.1% forecast in Feb due to H1 labour market strength.

- Fed: Will consider extent of additional firming to curb inflation.

- Fed: We will continue to reduce our bond holdings as described in previously announced plans.

- Fed: Tighter credit conditions are likely to weigh on economic activity, hiring and inflation, extent to which remains uncertain.

- Fed: Recent indicators suggest economic activity has been expanding at a moderate pace vs a modest pace in June statement.

- Fed: We will continue to assess additional information and its implications for policy.

- Fed: Banking system is sound and resilient.

As a result of the statement:

- Interest rate futures put chance of Fed hike at 18% in September, 36.5% in November post-FOMC.

- Probability of Fed hike was 18.9% in Sept, 37.3% in nov pre-FOMC.

Fed chair Powell key comments

Federal Reserve Chairman Jerome Powell comments on the policy outlook and responds to questions from the press following the US Federal Reserve (Fed) decision to hike the policy rate:

Powell speech: Labor demand still substantially exceeds supply

Powell speech: We believe monetary policy is restrictive

Powell speech: Will be looking to see if signal from June CPI is replicated

Fed overview

Jerome Powell explains decision to hike interest rate by 25 bps in July, comments on policy

GBP/USD technical analysis

GBP/USD hourly chart shows the bulls are moving in.

The daily chart shows the price heading higher again, riding trendline support, following the recent daily correction.

FOMC Chairman Jerome Powell comments on the policy outlook and responds to questions from the press after the Federal Reserve's decision to raise the policy rate by 25 basis points to 5.25-5.5% following the July policy meeting.

Key quotes

"It is a good thing headline inflation has come down so much."

"It will strengthen public perception of inflation coming down."

"How do you balance the risks of doing too much and too little, and we're coming to a place where there is risks on both sides."

"We need to see inflation durably down, want to see core inflation coming down."

"Core inflation is still pretty elevated."

"We're going to need to hold policy at restrictive levels for some time."

"Unemployment rate at same level as lift off is real blessing."

"Some softening in labor conditions is still the likely outcome."

"Worst outcome would be to not deal with inflation."

"I do not believe policy has been restrictive enough for long enough to bring inflation to target."

"Still a long way to go."

"If incoming data tells us we need to do more, then we will do more."

"A more gradual pace does not automatically go to every other meeting."

"It makes all the sense in the world to slow down."

About Jerome Powell (via Federalreserve.gov)

"Jerome H. Powell first took office as Chair of the Board of Governors of the Federal Reserve System on February 5, 2018, for a four-year term. He was reappointed to the office and sworn in for a second four-year term on May 23, 2022. Mr. Powell also serves as Chairman of the Federal Open Market Committee, the System's principal monetary policymaking body. Mr. Powell has served as a member of the Board of Governors since taking office on May 25, 2012, to fill an unexpired term. He was reappointed to the Board and sworn in on June 16, 2014, for a term ending January 31, 2028."

FOMC Chairman Jerome Powell comments on the policy outlook and responds to questions from the press after the Federal Reserve's decision to raise the policy rate by 25 basis points to 5.25-5.5% following the July policy meeting.

Key quotes

"Overall resilience of the economy, fact we've achieved disinflation so far without harm to economy, is a good thing."

"Stronger growth over time could add to inflation and may require a policy response."

"We're going to be careful about taking too much signal from a single reading on inflation."

"Will be looking to see if signal from June CPI is replicated."

"The totality of the data is important with particular focus on progress on inflation."

"September decision could be another hike or remaining where we are."

"It's really depending on the data and we don't have it yet."

About Jerome Powell (via Federalreserve.gov)

"Jerome H. Powell first took office as Chair of the Board of Governors of the Federal Reserve System on February 5, 2018, for a four-year term. He was reappointed to the office and sworn in for a second four-year term on May 23, 2022. Mr. Powell also serves as Chairman of the Federal Open Market Committee, the System's principal monetary policymaking body. Mr. Powell has served as a member of the Board of Governors since taking office on May 25, 2012, to fill an unexpired term. He was reappointed to the Board and sworn in on June 16, 2014, for a term ending January 31, 2028."

FOMC Chairman Jerome Powell comments on the policy outlook and responds to questions from the press after the Federal Reserve's decision to raise the policy rate by 25 basis points to 5.25-5.5% following the July policy meeting.

Key quotes

"We haven't made a decision to go every other meeting."

"We haven't made any decisions about any future meetings."

"The inter-meeting data came in broadly in line with expectations."

"June CPI was welcome but was only one month's report."

"Will be looking at the whole broader picture, looking for moderate growth."

"If data suggests more hikes are needed, that is the judgment we'll make."

"We believe monetary policy is restrictive."

"We have 8 weeks to September and looking at all the data until then."

About Jerome Powell (via Federalreserve.gov)

"Jerome H. Powell first took office as Chair of the Board of Governors of the Federal Reserve System on February 5, 2018, for a four-year term. He was reappointed to the office and sworn in for a second four-year term on May 23, 2022. Mr. Powell also serves as Chairman of the Federal Open Market Committee, the System's principal monetary policymaking body. Mr. Powell has served as a member of the Board of Governors since taking office on May 25, 2012, to fill an unexpired term. He was reappointed to the Board and sworn in on June 16, 2014, for a term ending January 31, 2028."

FOMC Chairman Jerome Powell comments on the policy outlook and responds to questions from the press after the Federal Reserve's decision to raise the policy rate by 25 basis points to 5.25-5.5% following the July policy meeting.

Key quotes

"Growth in consumer spending has slowed from earlier in the year."

"Still a strong pace of job growth."

"Continuing signs of labor supply and demand coming into better balance."

"Labor demand still substantially exceeds supply."

"Inflation has moderated somewhat."

"Getting back to 2% has a long way to go."

"Inflation expectations remain well anchored."

"We're highly attentive to risks inflation poses to both sides of mandate."

"We have been seeing effects of increases on demand in most rate-senstive sectors."

"Will take time for full effects to be realized."

"Will make decisions meeting by meeting."

"Remain committed to bringing inflation back to 2% goal."

About Jerome Powell (via Federalreserve.gov)

"Jerome H. Powell first took office as Chair of the Board of Governors of the Federal Reserve System on February 5, 2018, for a four-year term. He was reappointed to the office and sworn in for a second four-year term on May 23, 2022. Mr. Powell also serves as Chairman of the Federal Open Market Committee, the System's principal monetary policymaking body. Mr. Powell has served as a member of the Board of Governors since taking office on May 25, 2012, to fill an unexpired term. He was reappointed to the Board and sworn in on June 16, 2014, for a term ending January 31, 2028."

- Fed hikes rates by 25bps as expected.

- Gold price whipsawed in Fed volatility as the market awaits Fed's chair, Powell.

- Gold price leans towards trendline support, $1,963 and $1,975 are the breakout levels.

The Gold price has been whipsawed after the Federal Reserve, Fed, raised its interest rate decision by a 25 bps rate hike to 5.25-5.50%, as expected. At the time of writing, Gold is volatile between $1,973 and $1,965 so far as the market digests the statement and key points as follows:

Federal Reserve statement, and key notes

- Fed says FOMC vote was unanimous.

- CBO revises 2023 us real Gross Domestic Product growth forecast to 0.9% from 0.1% forecast in Feb due to H1 labour market strength.

- Fed: Will consider extent of additional firming to curb inflation.

- Fed: We will continue to reduce our bond holdings as described in previously announced plans.

- Fed: Tighter credit conditions are likely to weigh on economic activity, hiring and inflation, extent to which remains uncertain.

- Fed: Recent indicators suggest economic activity has been expanding at a moderate pace vs a modest pace in June statement.

- Fed: We will continue to assess additional information and its implications for policy.

- Fed: Banking system is sound and resilient.

As a result of the statement:

- Interest rate futures put chance of Fed hike at 18% in September, 36.5% in November post-FOMC.

- Probability of Fed hike was 18.9% in Sept, 37.3% in nov pre-FOMC.

Watch Fed's chair Powell live

Traders now await to hear from the Chairman, Jerome Powell who will be speaking to the press at the top of the hour.

The hawkish outcome could be that:

''Chair Powell emphasizes that actions taken since March have prevented credit conditions from tightening significantly. Meanwhile, labour market conditions and consumer spending remain too strong. Powell signals that more interest rate increases are likely needed,'' analysts at TD Securities said.

The base case, the analysts said:

''We expect Chair Powell to reiterate that the Fed remains data dependent and that economic data since the June FOMC meeting is yet to show convincing signs of slowing (despite nascent evidence of cooling inflation). Powell will also underscore that September is a “live” meeting.''

Dovish scenario, the analysts said:

''Powell mentions that the best course is to be patient given the totality of policy tightening and the ongoing reduction of credit supply. The chair plays up the recent deceleration in inflation as a positive sign and suggests that a soft landing is becoming more likely.''

Gold price technical analysis

Ahead of the Fed, daily and 15 min chart:

Gold price update, after Fed statement and interest rate decision:

So far, the price holds in bullish territory while on the front side of the trendline and above yesterday's highs and the day's low. $1,963 and $1,975 are the breakout levels.

- USD/JPY holds to daily losses at the 140.40 area.

- Fed hiked rates by 25 bps as expected to 5.25% and left the door open for further hikes.

- Eyes on BoJ's decision on Friday, expected to hold their dovish stance steady.

Following the Federal Reserve (Fed) decision, the USD DXY index continues to trade weak, near 101.19, and the USD/JPY stands with losses at 140.40.

The Federal Reserve (Fed) announced that it hiked rates by 25 basis points (bps) to the 5.25%-5.50% target, as expected, its highest in 22 years. The statement noted that economic activity and the labour market remain robust and that inflation is elevated. In addition, the Federal Open Market Committee (FOMC) opened the door to further hikes as they will consider monetary policy lags and its implications on economic activity in the next decision.

Following the decision, the US Treasury yields traded mixed. The 2-year yield stands neutral at 4.89%, while the 5- and 10-year rates jumped to 4.16% and 3.90%, both slightly unchanged.

Liver Coverage of Chair Powell's Press Conference

USD/JPY Daily chart

According to the daily chart, the technical outlook is neutral to bearish. On the positive side, according to the Moving Average Convergence Divergence (MACD), bears are losing ground as it is printing subtle red bars. On the other hand, the Relative Strength Index (RSI) fell below its midline and points south. On the bigger picture, the pair trading above the 100 and 200-day Simple Moving Average (SMA) indicated that the bulls are in command.

Support levels: 139.90, 138.70, 137.30(100-day SMA).

Resistance levels: 141.38 (20-day SMA), 142.00,143.00.

-638259920545666762.png)

- The Federal Reserve raised rates as expected by 25 basis points.

- The US dollar dropped modestly across the board after the FOMC decision.

- EUR/USD held within an intraday range above 1.1050.

The EUR/USD rose modestly from 1.1050 to 1.1079 after the Federal Reserve announced a 25 basis point rate hike. The US Dollar dropped modestly after the decision as US yields moved sideways.

Fed delivers as expected

The Fed raised its key interest rate to 5.25%-5.5%, the highest level in 22 years. The statement contained little changes compared to the previous meeting, and the vote in favor of the rate hike was unanimous. Now attention turns to Chair Powell's press conference. He is unlikely to declare an end to the hiking cycle and will reiterate that the Fed's policy is on a data-dependent path.

On Thursday, the European Central Bank (ECB) will hold its Governing Council meeting. A 25 basis point rate hike is currently priced in, but the focus will be on any signs about the future path of monetary policy. Following the ECB decision, important US economic data will be released, including the first reading of Q2 GDP growth and the weekly jobless claims report.

EUR/USD levels to watch

The EUR/USD remains within an intraday range, with support at the 1.1050 area and limited around 1.1080. A decline below 1.1050 should add bearish pressure, initially exposing the daily low at 1.1037 and then the weekly low at 1.1020. On the upside, the Euro faces resistance around 1.1090. If it breaks above, more gains above 1.1100 seem likely, with the next resistance seen at 1.1115.

Technical levels

FOMC meeting statement comparison

June 14July 26, 2023

Recent indicators suggest that economic activity has continued to expandbeen expanding at a modestmoderate pace. Job gains have been robust in recent months, and the unemployment rate has remained low. Inflation remains elevated.

The U.S. banking system is sound and resilient. Tighter credit conditions for households and businesses are likely to weigh on economic activity, hiring, and inflation. The extent of these effects remains uncertain. The Committee remains highly attentive to inflation risks.

The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. In support of these goals, the Committee decided to maintainraise the target range for the federal funds rate at 5 to 5-1/4 to 5-1/2 percent. Holding the target range steady at this meeting allows theThe Committee will continue to assess additional information and its implications for monetary policy. In determining the extent of additional policy firming that may be appropriate to return inflation to 2 percent over time, the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments. In addition, the Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage-backed securities, as described in its previously announced plans. The Committee is strongly committed to returning inflation to its 2 percent objective.

In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook. The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee's goals. The Committee's assessments will take into account a wide range of information, including readings on labor market conditions, inflation pressures and inflation expectations, and financial and international developments.

Voting for the monetary policy action were Jerome H. Powell, Chair; John C. Williams, Vice Chair; Michael S. Barr; Michelle W. Bowman; Lisa D. Cook; Austan D. Goolsbee; Patrick Harker; Philip N. Jefferson; Neel Kashkari; Lorie K. Logan; and Christopher J. Waller.

Follow Fed meeting – Live coverage

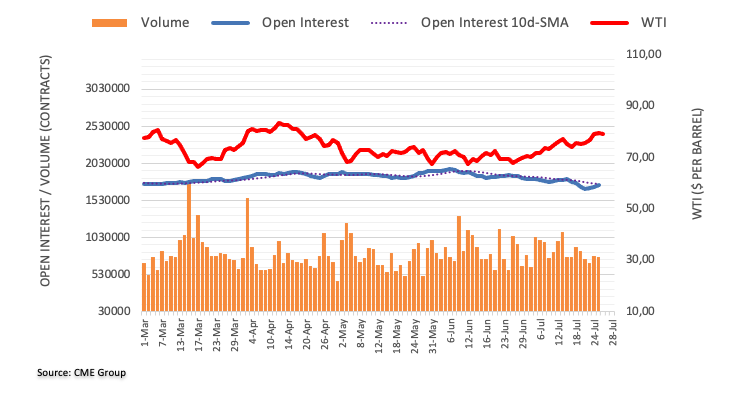

- WTI found support at a daily low of $78.66 and then recovered above $79.00 still holding daily losses.

- FOMC decision will be the session’s highlight – expected to deliver a 25 bps hike.

- EIA Crude Oil stocks fell in the third week of July by 0.6M, lower than expected.

The West Texas Intermediate (WTI) barrel trades soft on Wednesday as markets await the Federal Reserve (Fed) decision. In addition, the Energy Information Administration (EIA) reported a lower-than-expected decline in inventories in the week ending on July 21 and seem to be weighing on Oil prices.

On the other hand, the USD as per the DXY Index is declining, and US Treasury yields are decreasing ahead of the Federal Reserve's (Fed) announcement later in the session. Markets have already priced in a 25 basis point (bps) increase but are placing bets on a low likelihood of a similar increase in September (20%) and November (45%), respectively. Investors will need to model their expectations for the upcoming meetings based on the messaging regarding forward guidance since there won't be an updated macro forecast or dot plot. Its worth noticing that higher rates tend to cool down economic activity so the bets as to what the Federal Reserve will do following the decision may affect the WTI price dynamics.

On a positive note, the announcement on Tuesday that the Chinese government is to step up economic stimulus to bolster economic activity could provide support to the WTI as China is the largest Oil importer in the world, so a stronger economic activity would imply a greater Oil demand.

WTI Levels to watch

The daily chart of the WTI suggest a neutral to bullish outlook for the short term as buyers seem to be losing steam. The Relative Strength Index (RSI) has a neutral slope near the overbought threshold, while the Moving Average Convergence Divergence (MACD) printed a lower green, implying that the bulls are losing steam.

Resistance levels: $80.00,$81.00,$82.60.

Support levels: $76.70 (200-day SMA), $74.59 (20-day SMA),$73.50 (100-day SMA).

WTI Daily chart

-638259879133061271.png)

- XAG/USD gained ground and rose $24.90, showing 1% gains.

- The USD DXY trades soft near 101.10, while US Treasury yields are falling.

- Markets await a 25 bps hike by the Fed; messaging will be critical.

On Wednesday, the XAG/USD Silver spot price capitalised on the USD softness and falling US yields and jumped near the $25.00 area.

Ahead of the Federal Reserve (Fed) decision, the USD is trading soft, with the DXY index setting a consecutive day of losses after five straight days of gains. In addition, the 2-year American bond yield stands neutral at 4.88% and the 5 and 10-year rates fell to 4.14% and 3.87%, respectively, allowing the XAG/USD to gain traction.

Regarding the decision, markets have already priced in a 25 basis point (bps) hike, and the focus is on the Fed’s posture regarding forward guidance. Chair Powell commented in June that the considered “prudent” additional hikes but that monetary policy decisions will remain data dependent. As for now, according to the World Interest Rate Possibility (WIRP) tool, markets discount 20% odds of a hike in September and then 45% probabilities in November.

XAG/USD Levels to watch

The daily chart shows that the XAG/USD's technical outlook is neutral for the short term as indicators have turned somewhat flat, awaiting a catalyst. The Relative Strength Index (RSI) has a slight positive slope, while the Moving Average Convergence Divergence (MACD) prints fading green bars. However, the 20 and 100-day Simple Moving Averages (SMA) have already performed a bullish cross which could offer critical support to the grey metal. Traders should pay attention to these movements.

Support levels: $24.30, $24.00, $23.90 (20-day SMA).

Resistance levels: $25.00, $25.30, $25.50.

XAG/USD Daily chart

-638259836478471644.png)

The European Central Bank (ECB) is set to announce its Monetary Policy Decision on Thursday, July 27 at 12:15 GMT and as we get closer to the release time, here are the expectations as forecast by the economists and researchers of 12 major banks.

At the June meeting, the ECB raised its key interest rates by a quarter of a percentage point. The ECB is expected to raise rates by 25 basis points. The focus is on what the ECB will do after July.

Rabobank

We expect no policy surprises and little new information from the July meeting. The Council will try its best to avoid overly committing to a hike or a hold in September, as they await key incoming data and new staff projections. The communication challenge doesn’t stop there. The ECB will struggle to convincingly shift from a ‘higher rates’ to a ‘longer hold’ narrative. We could see the ECB adopt a new form of forward guidance to try to manage medium-term expectations, but its effects would probably be limited at best. A 25 bps rate hike has been well-telegraphed and is firmly priced. We believe that this takes the ECB to peak rates, but risks of a September hike are substantial.

Deutsche Bank

We expect the ECB to hike the deposit rate 25 bps to 3.75%. A further hike to 4.00% in September cannot be ruled out. Either way, the ECB does not want September to be seen as a turning point in the monetary policy cycle. The ECB wants the market to understand its commitment to the timely return of inflation to target and its willingness to go ‘higher and longer’ if necessary.

Credit Suisse

We expect the ECB to raise rates 25 bps to 3.75% in July. We expect the policy statement to remain unchanged but expect President Lagarde to keep the prospect of further tightening open to data developments.

TDS

A 25 bps hike is all but certain, with no changes to balance sheet policies; focus will be on how President Lagarde sets up September's decision. We expect a cautious tone, but ultimately a final hike that month.

SocGen

We expect continued hawkishness from the ECB, with another 25 bps hike in July. However, it may be premature to provide firm guidance for an additional hike in September already now, especially since more data (including 2Q GDP, July and August PMIs and inflation) and new staff forecasts will be available then. Still, with the ECB now firmly focusing on the labour market, we see little room for an easing of the hawkish bias just yet. We still see mainly upside risks to inflation and expect a final 25 bps hike in September before the focus shifts to the balance sheet at the end of the year. We believe that, beyond inflation, another reason for wanting a faster balance sheet reduction next year is the rapidly mounting losses caused by QE. The political fallout will only increase the longer inflation stays too high and the more losses are unveiled in the coming years. An option to ending the full PEPP reinvestments earlier than the end of next year is to sell APP bonds outright, but losses are expected to be significant in both cases.

Nordea

A 25 bps rate hike at the ECB July meeting looks like a done deal, so all focus is on what the central bank will signal about the future. Our baseline continues to be one where the July hike eventually proves to be the last one in this cycle, though risks are clearly tilted towards the hiking cycle continuing also after this. A pause after July would likely require further falls in realised core inflation, downward revisions in staff inflation forecasts and more signs of monetary policy transmission in the real economy, for example in the form of softer labour market data, especially in the services sector. Hawkish rhetoric at the July meeting would question such a view, though in the end, the development of economic data carries a lot of weight for the outcome of the subsequent meetings.

Nomura

We expect one final hurrah from the ECB at its July meeting, where it is likely to again raise all its policy rates by 25 bps, bringing the depo rate to a terminal level of 3.75%. We think guidance is likely to be changed, to keep optionality open to hike further should the need arise. However, we do not expect a pre-commitment from the ECB to further hike, and Lagarde is likely to underscore data dependency. Yet, when push comes to shove in September, we think data by then will justify the ECB ending its hiking cycle and being on a pause until it begins cutting (which we believe is likely to take place in Q4 2024 at the earliest). We flag that market volatility is likely to be elevated on Thursday and Friday. In particular, the ECB will not have access to Friday’s flash inflation data when meeting. Consequently, we highlight that the ECB’s narrative following the meeting could quickly shift, should country-level inflation data surprise materially in either direction.

ING

The ECB looks set to hike rates by 25 bps on Thursday. With the bleak economic outlook and disinflation gaining traction, however, the end to rate hikes is near.

Citi

ECB has guided towards another 25 bps rate hike and is likely to deliver. Despite receding inflation and weakening growth, the ECB is unlikely to declare victory over inflation, leaving another 25 bps rate hike in September in play. However, the council may reveal growing confidence in the disinflationary trend, suggesting a more forward-looking reaction function, hence delivering the near promise of 25 bps and leaving 14 September completely open, largely subject to the next two flash inflation prints (31 July/August) and the new staff projections. It is worth noting that the euro area flash HICP print for July is due just 4 days after this meeting, but the ECB will be waiting just like the market (with no pre-release access).

Wells Fargo

The ECB announces its monetary policy decision on Thursday, where a 25 bps increase in the Deposit Rate to 3.75% is widely expected, including by us. We don't expect the ECB to offer a clear signal of future rate hikes at its July announcement, which may be taken as a sign that a peak in policy rates is close at hand. Ultimately, it should be the disinflation progress (or lack thereof) in the July and August CPI readings that will largely determine whether the ECB follows up with another rate hike in September.

Danske Bank

A 25 bps rate hike from the ECB this week is essentially a given. This outcome has been well communicated in advance by most members, and should not in itself lead to any noticeable market reaction. We do not expect firm guidance for September, either for a pause or a hike, but a repeat of data dependence and in particular in light of the significant amount of data released before the September meeting. The weakening growth momentum, as well as some softening in core inflation measures, will be decisive for a potential final hike of 25 bps at the September meeting. Further deterioration may change our baseline expectation of a final hike in September.

Standard Chartered

We expect the ECB to hike 25 bps this week; forward guidance is likely to become less clear. Lagarde is likely to keep the door open to further tightening but will stress data dependence. We lean towards a September pause on weaker economic momentum and easing inflation pressures. However, it will be a close call; an upside surprise to inflation would make a September hike more likely.

- USD/JPY tallies a third consecutive day of losses towards the 140.40 area.

- US Treasury yields are falling ahead of the Fed decision.

- JPY strength suggests that markets are concerned with a possible surprise by the BoJ on Friday.

On Wednesday, the JPY gained ground agains most of its rivals, and the USD/JPY pair declined towards 140.40. The USD trades soft ahead of the Federal Reserve (Fed) decision later in the session, while the Yen strengthened on the back of a possible surprise of the Bank of Japan (BoJ) on Friday.

Ahead of the Federal Reserve (Fed) decision later in the session, the USD is falling, and US Treasury yields are backing down. Markets have already priced in a 25 basis point (bps) hike and are betting on 20% odds of a similar hike in September and then on 45% probabilities in November. As there won’t be any updated macro forecast or dot plot, messaging regarding forward guidance will be key for investors modelling their expectations for the next meetings.

On the other hand, markets have been receiving mixed signals regarding the next BoJ decision in the last sessions. Masato Kanda, a top currency Japanese diplomat, suggested that a Yield Control Curve (YCC) is highly possible. At the same time, BoJ’s Governor Kazuo Ueda was quoted as saying that the bank will maintain its accommodative approach. While the BoJ has a history of surprising markets, the broad consensus is that it will hold its policy unchanged, but markets seem to be pricing in a possibility of a pivot.

USD/JPY Levels to watch

The USD/JPY technical outlook, according to the daily chart suggests a neutral to bullish outlook for the short term. On the one hand, indicators give mixed signals, with the Relative Strength Index (RSI) falling below it midline while the Moving Average Convergence Divergence (MACD) prints fading red bars. On the other, the pair trades above the 100 and 200-day Simple Moving Average (SMA), which suggests that the buyers are overall in command, but the Fed’s decision will dictate the short-term trajectory.

Support levels: 140.00,139.10,138.70.

Resistance levels: 141.58 (20-day SMA), 142.00, 143.00.

USD/JPY Daily chart

-638259799716526631.png)

Economists at Société Générale analyze EUR/JPY outlook and of ECB and BoJ meetings.

ECB to raise rates by 25 bps, BoJ will probably leave rates on hold

On Thursday, we expect the ECB to raise rates by 25 bps and likewise leave the door open for a further move if needed.

On Friday, the BoJ will probably leave rates on hold but will they tweak their yield-curve control policy this month? We expect a move in September but he recognises the uncertainty as to the timing. If the BoJ does widen the trading band for JGBs, the Yen has plenty of room to rally. If it does not, the JPY will very likely weaken modestly (and we may see intervention as the MOF reacts).

Given current expectations of the ECB being slightly more hawkish than the Fed, and given FX positioning (long EUR), the EUR/JPY can fall a lot faster than it can rise from here, even if there is a good chance of nothing much happening.

If policy rates were everything, the Australian Dollar would be cheaper, economists at Société Générale report.

Longer-term rates suggest more range-trading

If the AUD/USD pair starts trading short-term policy-rate expectations, the AUD may be in trouble.

Historically, longer-term rates have been more of a driver, and they suggest the pair is going nowhere. Either way, we see no catalysts for a significant AUD/USD rally.

See: AUD/USD is well-supported on dips to the 0.65 zone but gains remain blocked above 0.68 – Scotiabank

Economists at Credit Suisse analyze USD/JPY outlook ahead of the BoJ meeting.

The FX market is pricing in a significant probability of a hawkish development

The FX market is clearly pricing in a significant probability of a hawkish development such as widening the YCC trading band for the 10-year JGB or sending a strong message that the end of YCC is not far. We prefer to fade market sentiment and see better asymmetry in looking for a disappointingly dovish outcome.

We stick tight to our USD/JPY 135-152 forecast range for the quarter and would expect spot to target 145 quickly if the BoJ meets our expectations, especially if the Fed’s hike this week is not interpreted as a dovish one.

Economists at Scotiabank maintain a bullish GBP view.

Supportive yield differentials lift GBP

The GBP has recovered more than three-quarters of its sharp 2022 decline and is likely to remain well-supported by positive yield spreads moving forward, even as very tight monetary policy will compromise the UK growth outlook moving into next year.

We are upgrading our GBP forecast to 1.35 for the end of 2023 (from 1.30) and to 1.40 for the end of 2024 (from 1.28).

See: GBP/USD may find it hard to go much beyond the 1.30 level – HSBC

- The Q2 GDP is the first top-tier US economic report released after the FOMC meeting.

- With the Fed likely indicating it will remain "data-dependent," growth and inflation numbers from the GDP report could be critical.

- US Dollar Index could receive additional support from positive data.

The US Bureau of Economic Analysis (BEA) is scheduled to release its first estimate of the second-quarter Gross Domestic Product (GDP) on Thursday, July 27th at 12:30 GMT. According to market forecasts, the US economy is expected to expand at an annualized rate of 1.8% in Q2, following the 2% growth rate recorded in the first quarter.

This release will be the first major economic report following the Federal Reserve meeting, and the central bank is expected to continue its 'data-dependent' approach to monetary policy. As a result, the Q2 GDP figures will be closely watched by investors and analysts. It's worth noting that the first release of Q2 GDP typically has a greater potential to influence the markets than subsequent revisions.

US GDP: What else to look for in the Q2 preliminary report

In addition to the overall growth rate of close to 2.0% in the second quarter, the BEA report will include other figures that will be observed carefully. One of these figures is the Core Personal Consumption Expenditures (PCE) Index, a key inflation measure used by the Federal Reserve. According to market consensus, the Core PCE Index is expected to decline to 4% in Q2 from 4.9% in Q1, which would be the lowest level since the first quarter of 2021. Another inflation indicator that will be scrutinized is the GDP Price Deflator, also known as the GDP Product Price Index. This is expected to decline to 3% in Q2 from 4.1% in Q1, marking its lowest level since the fourth quarter of 2020.

At the same time (12:30 GMT), the US Durable Goods Orders and the weekly Jobless Claims reports are also due to be released. A few minutes later, European Central Bank (ECB) President Christine Lagarde is scheduled to deliver her post-meeting press conference. With the markets still digesting the outcome of the FOMC meeting held on Wednesday, volatility is likely to prevail.

How could the GDP release affect the US Dollar

The International Monetary Fund (IMF) has raised its US GDP growth estimate for 2023 from 1.6% in April to 1.8%, and its global growth estimate from 2.8% to 3.0%. However, the IMF has warned that global growth risks remain tilted to the downside. US growth expectations are higher than most European countries, struggling to avoid a recession. The growth divergence between the US and Europe could limit the decline of the US Dollar or the rally of EUR/USD. If the difference narrows, the situation could change.

If the Q2 GDP report shows higher-than-expected growth figures combined with hotter inflation numbers, the US Dollar could be poised for a significant rally against other currencies. Such a scenario would make markets consider it more likely that the Federal Reserve will raise interest rates again, and it would also demonstrate that the US economy remains strong and resilient despite monetary policy tightening.

A number in line with expectations, with an annualized growth rate of around 2%, and decreases in inflation indicators – such as the Core PCE Index from 4.9% to 4% or the GDP Price Deflator from 4.1% to 3%– have the potential to weigh on the US Dollar by pushing down US Treasury yields. Such figures would support the scenario of no further rate hikes from the Fed.

The worst scenario for the US economy – higher inflation and lower growth – is not necessarily the worst scenario for the US Dollar. The most negative potential outcome for the Greenback would be a negative surprise in growth numbers and inflation slowing down more than expected. Fears of a recession, combined with inflation falling toward the target too quickly, would likely trigger expectations of rate cuts, probably in the fourth quarter or the first quarter of next year.

GDP FAQs

What is GDP and how is it recorded?

A country’s Gross Domestic Product (GDP) measures the rate of growth of its economy over a given period of time, usually a quarter. The most reliable figures are those that compare GDP to the previous quarter e.g Q2 of 2023 vs Q1 of 2023, or to the same period in the previous year, e.g Q2 of 2023 vs Q2 of 2022.

Annualized quarterly GDP figures extrapolate the growth rate of the quarter as if it were constant for the rest of the year. These can be misleading, however, if temporary shocks impact growth in one quarter but are unlikely to last all year – such as happened in the first quarter of 2020 at the outbreak of the covid pandemic, when growth plummeted.

How does GDP influence currencies?

A higher GDP result is generally positive for a nation’s currency as it reflects a growing economy, which is more likely to produce goods and services that can be exported, as well as attracting higher foreign investment. By the same token, when GDP falls it is usually negative for the currency.

When an economy grows people tend to spend more, which leads to inflation. The country’s central bank then has to put up interest rates to combat the inflation with the side effect of attracting more capital inflows from global investors, thus helping the local currency appreciate.

How does higher GDP impact the price of Gold?

When an economy grows and GDP is rising, people tend to spend more which leads to inflation. The country’s central bank then has to put up interest rates to combat the inflation. Higher interest rates are negative for Gold because they increase the opportunity-cost of holding Gold versus placing the money in a cash deposit account. Therefore, a higher GDP growth rate is usually a bearish factor for Gold price.

US Dollar Index levels to consider

The US Dollar Index (DXY) began a recovery last week from one-year lows below 100.00 and climbed to 101.65, where the 20-day Simple Moving Average (SMA) capped the upside. The main bias remains bearish, but if the DXY manages to stay above 101.00, it could test the crucial SMA again, and a break higher could open the doors to a more sustained rally.

On the other hand, if the DXY drops below 101.00, renewed bearish pressures could push it towards 100.00 and then the year-to-date low at 99.56. A break below these levels would signal a resumption of the bearish trend that has been in place since November of last year.

-638259766328134187.png)

- EUR/USD manages to bounce off recent lows around 1.1020.

- A test of 1.1000 still appears in the pipeline in the near term.

EUR/USD stages a decent rebound after bottoming out around 1.1020 in the previous session on Wednesday.

Considering the recent price action, extra weakness should not be discarded and could motivate the pair to revisit the psychological support at 1.1000 the figure. The loss of the latter exposes a deeper correction to the interim 55-day and 100-day SMAs at 1.0901 and 1.0895, respectively.

Looking at the longer run, the positive view remains unchanged while above the 200-day SMA, today at 1.0706.

EUR/USD daily chart

FX market’s reaction to today’s Fed meeting will not depend very much on the expected 25 bps rate hike but on everything else surrounding the meeting, Esther Reichelt, FX Analyst at Commerzbank, reports.

Expectations of rate cuts are likely to be pushed back further into the future

We have underlined often enough that 25 bps more or less make no difference for the valuation of the Dollar. In my view, the most important point is: due to this intensified form of data dependence the Fed is likely to control market expectations of imminent rate cuts, which in turn is likely to be relevant for the Dollar outlook.

It is quite possible that the Fed will maintain the terminal rate for some time before considering rate cuts. Until it is clear whether the rate hike cycle really is over, the expectations of rate cuts are also likely to be pushed back further into the future.

In the end, the prospect of rate cuts is likely to initiate the next episode of sustainable Dollar weakness in particular as our central bank experts expect that the ECB will keep its key rate at the terminal rate next year, contrary to market expectations. However, that will only become an issue over the coming months. Today the focus instead rests on the fact that it is simply too early to have this discussion. For now, the Dollar will have to wait and see.

See – Fed Preview: Banks see a 25 bps hike as “a done deal”, focus on forward guidance

The Mexican Peso’s (MXN) bull run has extended to push the USD back to levels last seen in 2015.

Banxico’s aggressive tightening policy is poised to reverse later this year

Despite the market’s concern about the Peso’s possible overvaluation, low volatility, momentum, large cash inflows and Banxico’s high for long stance will support the Mexican currency in the short term.

Going forward, risk reversals seem to be positioning for a possible rebound in the USD sometime between 4Q2023 and 1Q2024, around the time when we could see Banxico’s first rate cut and the beginning of the Mexican and American presidential elections.

USD/MXN – Q3-23 17.30 Q4-23 17.90 Q1-24 17.90 Q2-24 18.30

- DXY extend the knee-jerk to the proximity of 101.00.

- Further recovery targets the 102.60 zone.

DXY remains on the defensive and adds to Tuesday’s pullback ahead of the FOMC event on Wednesday.

Ideally, the index should clear the 102.60 zone, where the provisional 55-day sits, to alleviate the downside pressure and allow a potential test of the July high in the mid-103.00s, seconded by the key 200-day SMA at 103.89.

Looking at the broader picture, while below the 200-day SMA, the outlook for the index is expected to remain negative.

DXY daily chart

- NZD/USD feels selling pressure around 0.6230 as investors await Fed policy for further guidance.

- The USD Index has found some support near 101.10 as investors are hoping that Fed Powell will deliver hawkish guidance.

- NZD/USD is trading inside the Ascending Triangle chart pattern, which indicates a sheer contraction in volatility.

The NZD/USD pair senses selling pressure while attempting to climb above the immediate resistance of 0.6230 in the early New York session. The Kiwi asset has faced pressure as the US Dollar Index (DXY) has attempted a recovery ahead of the interest rate decision by the Federal Reserve (Fed).

Analysts at Danske Bank expect the Fed to hike interest rates for the final time by 25 bps and then go on hold. While economic activity has still held up well, easing underlying inflation and declining inflation expectations limit the need for further rate hikes. They further expect the immediate market reaction to be muted, with risks skewed towards a hawkish reaction, if Powell still maintains the door open for another hike.

The USD Index has found some support near 101.10 as investors are hoping that Fed Powell will deliver hawkish guidance. S&P500 is expected to open on a negative note, following weak cues from overnight futures.

NZD/USD is trading inside the Ascending Triangle chart pattern on a daily scale, which indicates a sheer contraction in volatility. The horizontal resistance of the aforementioned chart pattern is plotted from May 10 high at 0.6382 while the upward-sloping trendline is placed from May 31 low at 0.5985.

The Kiwi asset is facing resistance near the 200-period Exponential Moving Average (EMA) around 0.6226, which indicates that the long-term trend is bearish.