- Аналітика

- Новини та інструменти

- Новини ринків

Новини ринків

Japan's top currency diplomat Masato Kanda came out with verbal intervention remarks early Wednesday, according to Reuters.

Key quotes

“Dealing appropriately with FX moves”

“Closely communicating with us, overseas FX authorities”

“Closely watching FX moves with high sense of urgency”

“Japan is closely communicating with US authorities over forex on a regular basis”

“Shared mutual understanding that excessive forex move undesirable”

Market reaction

At the time of writing, USD/JPY is trading at 147.70 down 0.10% on the day.

- Poland is set for a critical parliamentary election, and the NBP's surprise rate cut continues to weaken the PLN.

- Poland's ruling Law & Justice party is facing down headwinds from a Ukrainian grain import ban.

- The Polish government, which campaigned on a platform of being tough on immigration, has been seen selling visas for profit.

The USD/PLN remains pinned to the upside ahead of the Federal Reserve’s (Fed) much–anticipated rate call on Wednesday. The Polish Zloty (PLN) remains a beleaguered currency as central bank blunders, European Union (EU) infighting, and government scandals knock around the currently ruling Law & Justice (PiS) party of Poland heading into next month’s critical parliamentary election.

The National Bank of Poland (NBP) recently slashed interest rates to the confusion of market participants everywhere, given the Polish inflation rate still remains above 10%. The Governor of the NBP, Adam Glapinski, has been accused of using the central bank’s authority to bolster support for the PiS.

Adam Glapinski is an open supporter of the PiS, and the surprise rate cut was seen as a way to temporarily ease borrowing and lending costs to improve the vote for the PiS in the upcoming election.

Poland recently moved to ban additional imports of Ukrainian grain, citing a need to protect their economy and their domestic farmers. Shipments of Ukrainian grains have increased in recent months as the Russian blockade of Ukrainian exports sees market excess sloshing into neighboring countries.

The European Union (EU) recently allowed a ban on Ukrainian grain excess to lapse, and Poland is coming under fire after President Andrzej Duda announced that Warsaw would simply disregard orders from Brussels and introduce their own ban on Ukrainian grain.

Poland, along with several other countries in the Eastern EU, are facing formal charges and lawsuits from Ukraine in both the EU trade courts and the World Trade Organization (WTO) over the grain bans.

President Andrzej Duda and the PiS dealt themselves a political blow this week after allegations of the country selling visas for profit to migrants who then used the credentials to travel to countries they would normally be banned from.

The PiS has undergone damage control, unexpectedly firing the part’s foreign minister for consular affairs, and terminating all contracts for external companies that handle visa processing. The head of the Polish foreign ministry’s legal and compliance department was also terminated.

Everything comes just as Poland is about to face an intense parliamentary election, where the PiS is seen struggling to maintain its vote share.

USD/PLN technical outlook

The Polish Zloty has struggled as of late, and continues to fall backwards against the Greenback (USD).

The USD/PLN pair is tapping into recent highs just north of 4.36, and an extended push could see the pair set to challenge fresh six-month highs above last week’s peak of 4.3841.

The pair’s technical stance remains firmly bullish, with both the Relative Strength Index (RSI) and Moving Average Convergence-Divergence (MACD) indicators all but breaking their seals in overbought territory.

The 200-day Simple Moving Average is currently providing support from 4.2377, and the 34-day Exponential Moving Average is racing to cross over into a bullish confirmation, currently pricing in near 4.2100.

USD/PLN daily chart

USD/PLN technical outlook

On Tuesday, US Treasury Secretary Janet Yellen stated that the US would show understanding over another yen-buying intervention by Japan "depends on the details" of the situation, according to Reuters.

Key quotes

"We usually communicate with them about these interventions and generally understand the need to smooth out following undue volatility, but not to attempt to influence the level of exchange rates,"

"So it depends very much on the details in our discussions with the Japanese,”

Market reaction

USD/JPY consolidates near 147.72 following the above the report. The pair is down 0.09% on the day.

- AUD/JPY rallies to 95.64, its highest level in one-and-a-half months, buoyed by RBA’s latest monetary policy minutes.

- Following resistance levels in sight: July 25 swing high at 95.85 and the psychological 96.00 mark.

- Downside risks remain, with key support levels at the Ichimoku Cloud top at 94.74 and the Tenkan-Sen line at 94.60.

The AUD/JPY printed solid gains on Tuesday, and as Wednesday’s Asian session begins, the cross-currency pair hovers around 95.39 after touching a new one-and-a-half-month high at 95.64.

The AUD/JPY daily chart portrays the pair as neutral to upward biased. Even though it formed a ‘bearish-harami’ until yesterday, the cross-currency pair extended its gains due to fundamental news, such as the latest Reserve Bank of Australia (RBA) monetary policy minutes. Discussions amongst the RBA members kept the door open for additional tightening and sparked Tuesday’s rally.

Hence, the AUD/JPY extended its gains and is set to test the July 25 swing high at 95.85. A breach of the latter would expose the 96.00 mark, followed by last year’s high at 97.67. Conversely, if the cross retreats below 95.00, the next support would emerge at the top of the Ichimoku Cloud (Kumo) at 94.74, followed by the Tenkan-Sen line at 94.60, and followed by the Kijun-Sen at 94.21.

AUD/JPY Price Action – Daily chart

AUD/JPY Technical Levels

- AUD/USD posts modest gain just above the mid-0.6400s ahead of the US key event.

- The Federal Reserve (Fed) is widely expected to hold the interest rates in the 5.25% to 5.5% range.

- Reserve Bank of Australia's (RBA) said additional tightening may be necessary if inflation proves more persistent than anticipated.

- Market players await Australian Westpac Leading Index, the People's Bank of China (PBoC) interest rate decision and Fed decision.

The AUD/USD pair edges higher during the early Asian session on Wednesday. Market players await the highly-anticipated the Federal Reserve (Fed) monetary policy meeting. The pair currently trades around 0.6455, gaining 0.04% on the day.

The Federal Reserve (Fed) is scheduled to announce the two-day monetary policy meeting on Wednesday and is widely expected to hold the interest rates in the 5.25% to 5.5% range.This, in turn, might exert some selling pressure on the Greenback (USD) and acts as a tailwind for the AUD/USD pair. On Tuesday, the US Census Bureau revealed that the US housing industry revealed mixed results in August. Housing Starts fell 11.3%, while building permits surged 6.9%.

On the Aussie front, the release of the Minutes from the Reserve Bank of Australia's (RBA) September monetary policy meeting revealed on Tuesday that additional tightening may be necessary if inflation proves more persistent than anticipated. However, the case for maintaining the status quo was stronger, and recent data have not materially altered the economic outlook.

Furthermore, the People's Bank of China (PBoC) will announce the interest rate decision on Wednesday in Asian session. Chinese central bank is expcted to keep its benchmark lending rate unchanged. Any signs from the Chinese authorities about the additional stimulus plans to deal with the the property crisis might lift the China-proxy Australia Dollar (AUD) against the USD.

Looking ahead, market participants will keep an eye on the Australian Westpac Leading Index for August for fresh impetus ahead of the People's Bank of China (PBoC) interest rate decision later in Asian session. The attention will shift to the Fed interest rate decision on Wednesday at 18:00 GMT. These events could give a clear direction to the AUD/USD pair.

- The EUR/GBP stepped back on Tuesday after a bullish breakout to kick off the week.

- The midweek sees UK inflation figures, and a rate hike from the BoE.

- Friday will cap off the economic calendar with UK Retail Sales, PMI figures for both currencies.

The EUR/GBP took a dip on Tuesday after starting the week strong, and the pair is backing into the 0.8620 neighborhood after the week kicked off with a decisive bullish breakout that couldn’t maintain momentum.

It’s a hectic week for the Pound Sterling (GBP) on the economic calendar. Wednesday will see inflation figures with the Consumer Price Index (CPI) expected to show an uptick to 0.7% from the previous decline of -0.4% for the month of Aug.

The annualized CPI figure for August is also expected to ramp up, forecast to print at 7.1% versus the previous 6.8%.

The UK is broadly expected to suffer from the stickiest, most stubborn inflation of all the advanced economies, and the Bank of England (BoE) will have its work cut out for it as it tries to rope in inflation without cutting the knees out from under the UK’s economy.

BoE benchmark rate to climb once more on Thursday

The BoE is expected to raise its benchmark interest rate by another 25 basis points on Thursday, bringing the headline interest rate to 5.5%.

Friday will close out the week with a bang, with UK Retail Sales expected to show further increases, as well as Purchasing Manager Index (PMI) figures that are slated on the docket for both the EU and the UK.

EUR/GBP technical outlook

The EUR/GBP kicked the week off with a bullish break of the descending trendline from July’s swing high of 0.8700, but momentum is proving a fickle beast ahead of a data-heavy back of the week.

The EUR hasn’t been able to maintain a firm hold of the pairing, despite the recent lift from August’s bottom near 0.8500, and the trendline break could work out to be temporary if GBP bulls find their feet heading into the back half of the week.

EUR/GBP daily chart

EUR/GBP technical levels

- EUR/JPY soared to a high of 158.23, above the 20-day SMA and then closed at 157.85.

- The bulls seem to have no more gas left in the tank to continue advancing.

In Tuesday’s session, the EUR/JPY cross failed to maintain its momentum, which took the pair to a high of 157.85, above the 20-day Simple Moving Average (SMA) and closed with mild gains at 157.85.

Based on the daily chart, the EUR/JPY continues to show indications of bullish exhaustion, leading to a neutral to bearish technical outlook. The Relative Strength Index (RSI) shows a flat slope over its midline and suggests that the bullish momentum is slowly fading away. This is supported by the Moving Average Convergence (MACD), which lays out flat red bars. It's worth mentioning that the RSI has displayed a downward trend since the beginning of September and lines with the pair being constantly rejected by the 20-day SMA.

That being said, the pair is above the 100 and 200-day SMAs, highlighting the continued dominance of bulls in the broader perspective.

Support levels: 157.00, 155.00, 154.60 (100-day SMA).

Resistance levels: 158.00 (20-day SMA), 158.50, 159.00.

EUR/JPY Daily Chart

-638307575455157908.png)

- EUR/USD trades at 1.0677, extending its losses by 0.01% as US 10-year Treasury yields hit a 16-year high.

- Diverging rate hike expectations between the Fed and ECB could weigh on EUR/USD.

- Market participants await the Federal Reserve’s decision and updated economic projections for directional cues.

As the Asian session begins, the Euro (EUR) extends its losses by a minuscule 0.01% against the US Dollar (USD) as market participants prepare for the US Federal Reserve’s decision. The Greenback stages a comeback propelled by a jump in US Treasury bond yields. The EUR/USD is trading at 1.0677, following Tuesday’s losses of 0.12%.

Euro faces headwinds as the US Dollar gains strength on soaring Treasury yields, with all eyes on the upcoming Federal Reserve decision

US equities ended the day with losses. The US 10-year Treasury bond yield skyrocketed to a 16-year high at 4.367%, a headwind for the EUR/USD, which remains close to the 1.0700 figure, but it’s set to continue to print losses amidst speculations the Fed would deliver a hawkish hold.

Given that recent data in the United States (US) showed the robustness of the economy, with a hot jobs market, improvement in business activity, and consumer spending expanding – though at a lower rhythm – are reasons for the Fed Chair Powell and Co to keep “at it,” and hold rates higher for longer. Furthermore, last week’s Consumer and Producer Price Index (CPI and PPI) printed higher readings, justifying the need for higher rates.

Besides delivering its monetary policy decision, policymakers would update their economic projections regarding growth, unemployment rate, inflation, and the Federal Funds Rates (FFR). In June, Fed officials expected the FFR to peak at around 5.60%. Despite that, money market futures are pricing the FFR to peak at around 5.46%.

Data-wise, a scarce US economic docket revealed housing data, which came mixed. US Building Permits improved compared to July’s 0.1% expansion grew by 6.9%, while Housing Starts plunged -11.3%, beneath the -2.5% contraction estimated.

Across the pond, the Eurozone (EU) economic docket revealed inflation data. The Harmonised Index of Consumer Prices (HICP) for August came at 5.2% YoY, below 5.3% estimates, while core HICP stood at 5.3% unchanged, aligned with estimates.

Recently, some European Central Bank (ECB) officials signaled the ECB would not continue to tighten monetary conditions. Nevertheless, an ongoing economic deceleration in the bloc and a deposit rate at its highest level since the Euro’s inception at 4.00% could bring inflation towards its target.

A poll by Reuters showed that 70 economists commented the ECB is done hiking rates and that the deposit rate would end the year at its current 4.00% level. Although the ECB’s President Christine Lagarde refrained from saying that rates have peaked, money market futures see a 25% chance for additional hiking towards the end of the year.

Given the backdrop, if the Fed delivers a hawkish hold, expect further EUR/USD’s downside; otherwise, the single currency could rally and reclaim the 1.0700 level, with buyers eyeing 1.0800.

EUR/USD Price Analysis: Technical outlook

The daily chart portrays an ‘evening star’ in the making, as Tuesday’s candle was an ‘inverted hammer’, which could pave the way for further downside. Yet, upside risks remain, with the EUR/USD close to the 1.0700 figure. A hawkish hold by the Fed could open the door to test the September 14 swing low of 1.0632, followed by the 1.0600 figure ahead of plunging toward Mach’s low of 1.0516. Conversely, a dovish surprise and the EUR/USD could rally past the September 19 high at 1.0718 and target the 200-day Moving Average (DMA) at 1.0828.

- US equities trade tightly, fall back into recent ranges as Fed looms large.

- The Federal Reserve is set to keep rates steady for this meeting.

- FOMC to release their latest inflation expectations looking forward.

It’s all eyes on the Federal Reserve (Fed) for this week as the latest interest rate call on Wednesday from the Fed hangs over the markets. US equities were broadly back, albeit softly, and indexes spread towards the middle as investors brace for an updated playbook from the Federal Open Market Committee (FOMC).

The Standard & Poor’s 500 (S&P) slipped ten points to give up the $4,450.00 handle, settling the day down near $4,430.00 (-0.22%); The NASDAQ tech composite index declined 32 points to end the day near $13,678.00 (-0.23%); and the Dow Jones Industrial Average (DJIA) slid over 105 points to end Tuesday at $34,517.00 (-0.31%).

Stocks down, yields up ahead of Fed

As equity indexes backslid, treasury yields climbed again, with the 2-year note rising to 5.092 and the 10-year lifting to 1.365.

Wednesday will see the latest interest rate call from the Fed, where markets are broadly anticipating the US central bank to hold steady on their benchmark rates.

However, the FOMC will also be dropping its economic projections as well as its updated interest rate outlook. The data docket will be followed by the FOMC’s press conference 30 minutes later where investors will be keeping a close eye out for any changes in the Fed’s rhetoric stance.

S&P 500 technical outlook

Daily candlesticks have the major equity index firmly testing the bounds of a rising trendline, and an extended bearish slide could see the S&P kick into a further leg down to test the last swing low below $4,350.00.

Bullish momentum sees descending resistance from the upside as lower highs price in a ceiling north of the $4,500.00 handle.

The 100-day Simple Moving Average is on the rise, clearing $4,375.00 and could provide support for renewed bullish momentum in the index looking forward.

S&P 500 daily chart

S&P 500 technical levels

- USD/CLP trades neutral at 884.35, with technical indicators flat.

- The Chilean Central Bank kicking off its easing cycle contributes to the upward trajectory.

- The Federal Reserve (Fed) is expected to deliver a hawkish pause on Wednesday.

On Tuesday, the USD/CLP bulls are taking a breather after pushing the pair upwards by more than 3.82% in September and are consolidating gains at the 884.35 area.

Monetary policy divergences with the Federal Reserve (Fed) may explain the increase of the pair as since July, the Chilean Central Bank has already cut rates by 1.75%, and markets are discounting 1.50% more of easing in the remainder of 2023. The week's highlight for the CLP will be the release of the September 5 minutes on Friday, where investors will have a clearer outlook of the bank’s stance for the upcoming October and December meetings.

On the US side, rate swaps markets have practically priced in that the Federal Reserve (Fed) will hold rates steady at 5.25-5.50% on Wednesday. However, Chair Powell will try to convince the markets pausing won’t mean the end of the tightening cycle, leaving the door open for another hike. In addition, the fresh macro forecasts and the revision of the Federal Open Market Committee (FOMC) members' famous dot plots will be closely watched by investors to continue modelling their expectations.

USD/CLP Levels to watch

Considering the daily chart, the USD/CLP presents a bullish outlook. Despite turning flat, the Relative Strength Index (RSI) lies comfortably deep in positive territory, while the Moving Average Convergence (MACD) histogram prints rising green bars. On the other hand, the pair is above the 20,100,200-day Simple Moving Average (SMA), suggesting that bulls are clearly in command of the bigger picture.

Support levels: 884.00, 882.00, 880.00

Resistance levels: 895.00, 898.00, 900.00.

USD/CLP Daily Chart

-638307547470636875.png)

It is FOMC day, and it is a busy one. During the Asian session, New Zealand will release Q2 Current Account data, and Japan will report August trade data. Additionally, the Australian Westpac Leading Index will be released. The focus will be on the People's Bank of China (PBoC) interest rate decision. Later in the day, the UK will report August inflation data, and Germany will release wholesale inflation figures. During the American session, the Federal Reserve will announce its decision on monetary policy.

Here is what you need to know on Wednesday, September 20:

An important event during the Asian session will be the decision of the People's Bank of China regarding interest rates. The 1-year Loan Prime Rate is expected to remain at 3.45% after last month's cut.

The key event on Wednesday will be the Federal Reserve's decisions. Market participants expect the central bank to keep the Fed Fund rate unchanged at 5.25-5.50%. The focus will be on the statement, the economic projections, and Powell's press conference.

Data released on Tuesday showed mixed numbers from the US housing sector. Housing Starts tumbled 11.3% in August, while Building Permits jumped 6.9%.

During the American session, the US Dollar Index rose amid deteriorating market sentiment and higher US Treasury yields. The DXY rebounded to 104.80, rising above 105.00.

EUR/USD failed to hold above 1.0700 and pulled back, remaining within a downward channel. The final reading of the Eurozone Harmonized Index of Consumer Prices came in at an annual rate of 5.2% in August, revised from the preliminary 5.3%. Germany will report the August Producer Price Index on Wednesday, with a decline expected in the annual rate from -6% to -12.8%.

USD/JPY posted its highest daily close since November but remains below 148.00. Japan will release August trade data on Wednesday.

USD/CHF rose again and hit intraday monthly highs but is still unable to break above 0.9000. The Swiss State Secretariat for Economic Affairs (SECO) will release its Autumn 2023 Economic Forecasts report. On Thursday, the Swiss National Bank is expected to announce a 25 basis point rate hike to 2%.

GBP/USD failed to hold above 1.2400 and pulled back, staying near monthly lows. The UK's August inflation report is due on Wednesday. The annual Consumer Price Index rate is expected to rise from 6.8% to 7.1%. Such a number could likely solidify the odds of a rate hike from the Bank of England, which will announce its decision on Thursday.

The Consumer Price Index in Canada rose 0.4% in August, surpassing the market consensus of 0.2%. The annual rate rebounded from 3.3% to 4%. The Canadian Dollar (CAD) peaked after the announcement but then pulled back. USD/CAD lost ground and hit monthly lows at 1.3380 but finished far from the bottom around 1.3440.

TD Securities on Canada inflation:

Today's report leaves Q3 CPI tracking well above projections from the July MPR and will add to the Bank of Canada's concerns around persistent price pressures. We will still get one more inflation report ahead of the October BoC meeting and a softer growth outlook will allow the Bank to look through some of this persistence, but today's report should help reaffirm that the mission is not yet accomplished and upcoming meetings remain live for another hike.

NZD/USD rose above the 20-day Simple Moving Average and posted a daily close above 0.5900. The current indicators are modestly biased to the upside in the short term. New Zealand's Q2 Current Account data is due on Thursday, along with Q2 GDP data.

AUD/USD tested the resistance area around 0.6470 but failed to break higher. It maintains a mostly bullish bias ahead of the Asian session. The Westpac Leading Index is due on Wednesday.

Precious metals erased gains during the American session, driven by a stronger US Dollar. Silver retreated to $23.20, while Gold dropped to $1,930.

Like this article? Help us with some feedback by answering this survey:

- Gold price hit a two-week high at $1937.35 before retreating to $1931.77, down 0.06%.

- US 10-year Treasury bond yield reaches a 16-year high at 4.367%, weighing on gold.

- Investors keenly await the Federal Reserve’s ‘dot plots’ and updated economic projections for rate hike clues.

Gold price retreats after hitting a two-week high at $1937.35 as investors remain on the sidelines ahead of the US Federal Reserve monetary policy decision. US Treasury bond yields are climbing ahead of the Fed’s decision, a headwind for the yellow metal, which was shy of clashing with the 100-DMA. At the time of writing, the XAU/USD is trading at $1931.77, down 0.06%.

Gold retreats as investors await the Federal Reserve’s monetary policy announcement, with rising US Treasury yields adding pressure

Wall Street continues to print losses, while the US 10-year Treasury bond yield touches a 16-year high at 4.367%. Tomorrow, Fed Chair Jerome Powell and his colleagues are expected to keep rates at the current 5.25%-5.50% range and to keep them higher for longer, at least until July 2024, as drawn by the Fed money market futures.

Even though the latest round of data showed that inflation has registered back-to-back upticks, the US central bank is set to skip a rate hike in September. According to the CME FedWatch Tool, odds for the November and December meeting had been lowered, suggesting that traders are not expecting additional rate hikes toward the end of 2023.

Although the Fed’s decision is important, market participants would be focused on the ‘dot plots’ to review the US central bank interest rate path. According to the latest Summary of Economic Projections (SEP), the Fed’s median estimates rates to peak at 5.6%. A confirmation could catch off guard interest rate traders, which expect rates to be capped at 5.50%.

In the meantime, the US Dollar Index (DXY) remains firm at around 105.14, gains 0.06%, underpinned by high US Treasury bond yields. The US 10-year Treasury note yields 4.367%, its highest level in 16 years, a headwind for Gold prices.

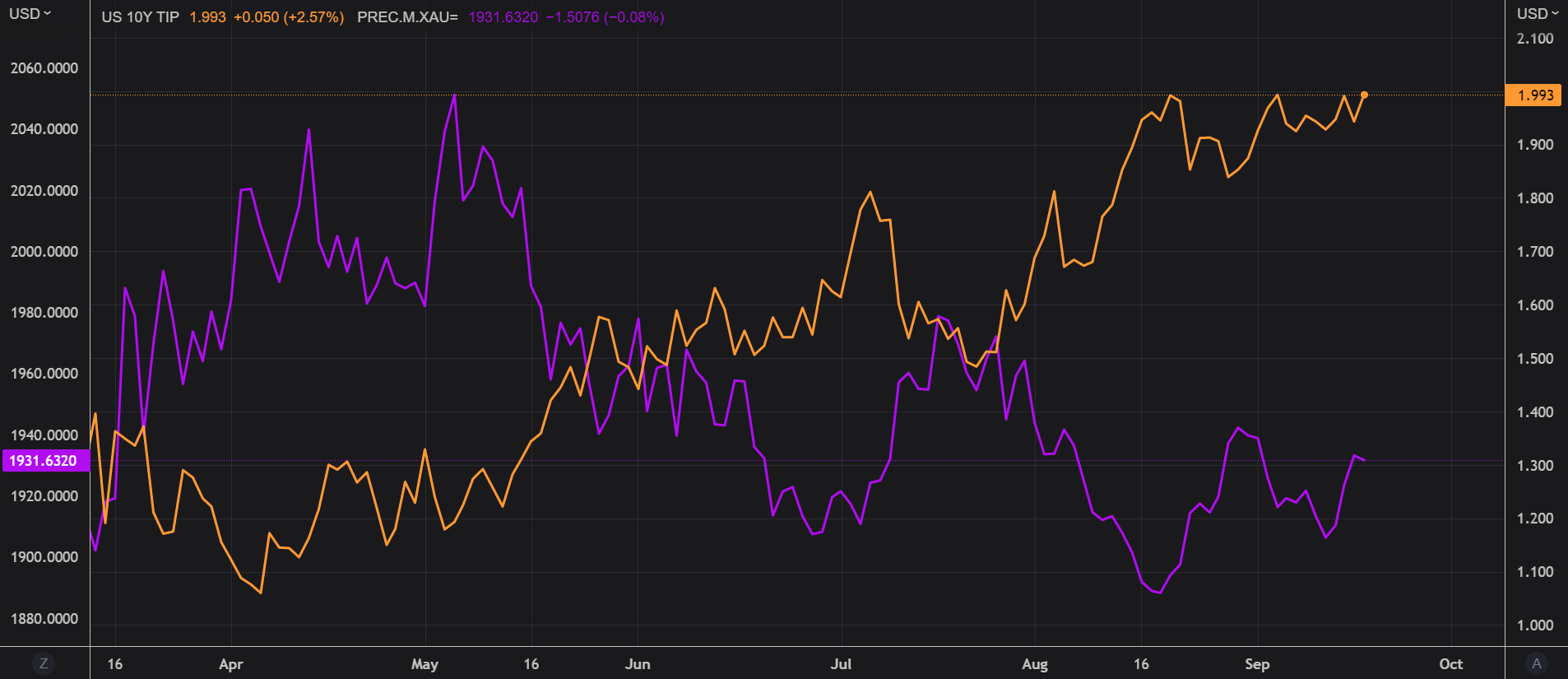

Meanwhile, Gold traders must also be aware of US Real yields, which could be followed using TIPS (Treasury Inflation Protected Securities) as a proxy. When the US 10-year TIPS coupon rises, XAU/USD’s price falls, as shown by the following chart, depicting the inverse correlation between the assets.

Source: Refinitiv

The US economic docket would feature the Fed’s decision on Wednesday, followed by US housing data, unemployment claims, and S&P Global PMIs.

XAU/USD Price Analysis: Technical outlook

Gold trades sideways inside a descending triangle, cushioned on the downside by a confluence of daily moving averages (DMAs), and the 100-DMA acts as resistance at $1945.20. Although it recorded a higher low on September 14 at $1901.11, it has failed to print a higher peak above the July 20 swing high at $1987.42. If buyers want to shift the bias to neutral, they must reclaim the latter. Otherwise, a break below the confluence of the 20 and 200-DMA around $1924.00 could pave the way to challenge $1900, followed by the August 21 daily low of $1884.89

- The USD/CAD is trying to recover the day’s losses after getting knocked lower.

- The Loonie is catching support from steadily-rising oil costs.

- The USD/CAD is recovering towards the 50% retrace of the day’s declines.

The USD/CAD started Tuesday in freefall, declining from the day’s open near 1.3480 and tapping into 1.3380. Rising oil prices are bolstering the Loonie (CAD), as concerns over global supply constraints knock crude barrel costs into the ceiling.

Despite the Loonie-led dip, the USD/CAD is recovering into the middle ground. Greenback (USD) traders are keeping light on their feet as the next showing from the Federal Reserve (Fed) rounds the corner.

Fed to hold on rates, but investors to watch the rhetoric

The Fed’s latest rate call will be dropping on markets on Wednesday, with the Fed’s rate call and ensuing press conference scheduled for 18:00 GMT tomorrow.

The Fed is broadly expected to stand pat on rates for the time being, holding benchmark rates at 5.5%. The Federal Open Market Committee (FOMC) will also be publishing their economic projections and inflation outlook figures, something that investors will be scrambling to process.

It’s a light economic calendar week for the CAD, and market momentum will be firmly in the hands of crude oil and Greenback traders.

USD/CAD technical outlook

The USD/CAD is drifting into the middle in late Tuesday trading, testing the waters near 1.3450 after the early session’s fast drop.

The pair declined 0.72% from Tuesday’s opening prices near 1.3475, but the mid-day recovery sees the pair nearing the 68% retracement of the day’s drop.

Rapidly increasing crude prices has sent the USD/CAD lower on the daily candlesticks, with the pair set to close in the red for seven of the last eight consecutive trading days.

The Dollar-Loonie pair has slid past the 200-day Simple Moving Average (SMA) in Tuesday’s trading. Continued selling pressure will see the pair challenging the last swing low near 1.3100, while an upside recovery will have to reclaim the 1.3700 handle to establish a determined uptrend.

USD/CAD daily chart

USD/CAD technical levels

Bank of Canada (BoC) Deputy Governor Sharon Kozicki said on Tuesday that interest rates need to remain high. She pointed out that they are concerned about the underlying inflation.

She explained that core measures of inflation have eased, but the latest Consumer Price Index report indicates that inflationary pressures are still broad-based.

Key takeaways from the speech:

Because inflation was very high last year, interest rates had to rise a lot. That’s why we acted forcefully and brought them up quickly. Inflation has come down, but it is still too high. And that tends to mean that real interest rates need to remain high.

When making monetary policy decisions, the Bank of Canada must consider the many ways that shifting economic circumstances affect different households. We don’t set our policy based on what is happening to one subset of households or to the price of any one good or service.

We are seeing signs that monetary policy is working. Both inflation and inflation expectations have come down, and excess demand in the economy is easing. And our past policy actions will continue to have an effect as they work their way through the economy.

However, in our most recent monetary policy decision, we also expressed concern about the persistence of underlying inflation. We will continue to evaluate whether the evolution of excess demand, inflation expectations, wage growth and corporate price-setting behaviour are consistent with achieving the 2% inflation target. We are prepared to raise the policy interest rate further if needed.

Market reaction

The USD/CAD is hovering around 1.3440, unaffected by Kozicki’s comments. The pair bottomed at 1.3378, the lowest in a month and then trimmed losses.

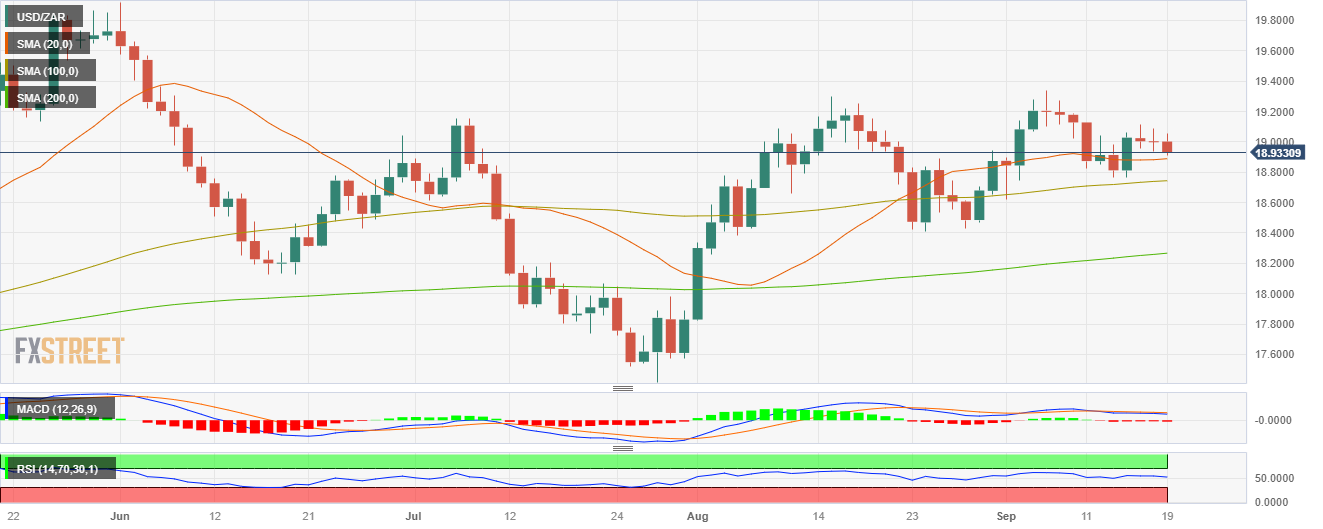

- USD/ZAR declined towards 18.933, near the 20-day SMA.

- South Africa reports August Inflation figures and July Retail Sales on Wednesday.

- Federal Reserve (Fed) is expected to pause but leave the door open for further hikes.

In Tuesday’s session, the USD/ZAR faced some selling pressure and declined to 18.933, down by 0.25%, and seems to be on its way to retest the 20-day Simple Moving Average at 18.880.

All eyes are on Wednesday. South Africa reports the August Consumer Price Index (CPI) with the headline figure expected to increase slightly to 4.8% YoY, while the core inflation rate is anticipated to remain stable at 4.7% YoY. Retail Sales from July are expected to come in at -1.0% YoY, compared to the 0.9% YoY decrease in June. Regarding the South African Reserve Bank meeting on Thursday, the decision will likely be to maintain its interest rates at 8.25% despite some previous expectations of a hike. As for now, for the next twelve years, markets aren’t foreseeing any hikes and discounts that the bank will maintain rates at 8.25%.

On the Fed’s side, Markets expect the bank to keep rates steady at 5.25-5.50%, but Chair Powell will likely show a hawkish tone and signal future rate hikes which could benefit the USD. Strong US economic performance, especially in services, and a mixed labour market suggest the Fed may leave room for one more hike to curb inflation risks.

USD/ZAR Levels to watch

The daily chart shows signs of bullish exhaustion for USD/ZAR. The Relative Strength Index (RSI) indicates a neutral stance above its midline, displaying a flat slope in the positive territory, while the Moving Average Convergence (MACD) presents neutral red bars. On the bigger picture, the pair is above the 20,100,200-day Simple Moving Average (SMA), suggesting that the bears are struggling to challenge the overall bullish trend.

Support levels: 18.880 (20-day SMA), 18.728 (100-day SMA). 18.500.

Resistance levels: 19.000, 19.050, 19.150.

USD/ZAR Daily Chart

- GBP/USD trades at 1.2395, showing slight gains, but remains below the key 1.2400 level.

- Federal Reserve expected to hold rates steady, while the Bank of England is anticipated to raise rates by 25 basis points.

- UK inflation data and the US Federal Reserve’s monetary policy decision are the key events to watch this week.

The British Pound (GBP) halts last week’s fall against the buck (USD) and prints minuscule gains vs. the latter despite rising US Treasury bond yields, as the UK and US central banks are expected to reaffirm its restrictive stance. Therefore, the GBP/USD is trading at 1.2395 after hitting a daily low of 1.2369, though it is still below the 1.2400 figure.

The British Pound steadies against the US Dollar as the Federal Reserve and the Bank of England are set to announce their monetary policy decisions

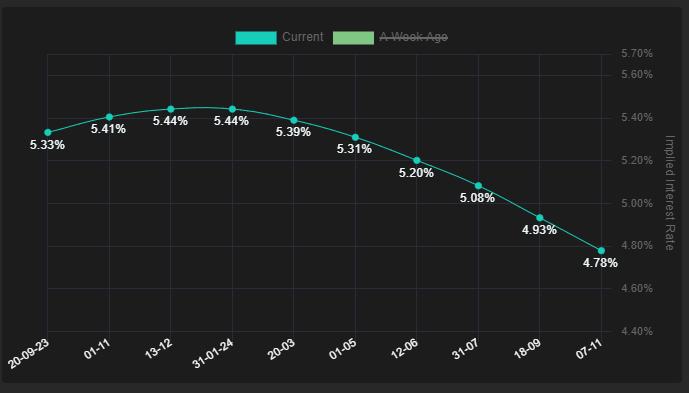

US equities extended its losses as sentiment deteriorates ahead of the central bank bonanza. The Federal Reserve is expected to hold rates unchanged amid the latest round of economic data, which revealed inflation in the consumer and producer side rose. In contrast, consumer spending expanded, though at a slower rhythm.

The Federal Funds Rate (FFR) would likely remain at the 5.25%-5.50% range, and in the same meeting, Fed officials would update their economic projections. In the June Summary of Economic Projections (SEP) the Fed anticipated 1% economic growth, a 4.1% unemployment rate, 3.2% PCE inflation, 3.9% core PCE inflation, and a peak FFR of 5.60%.

The swaps market shows the FFR would peak at current pricing, while estimates for the first rate cut are seen in July 2024, as shown by the picture below.

Source: Financialsource

Across the pond, the Bank of England’s (BoE) is foreseen to raise rates 25 bps to 6.50%, which, according to STIRs markets, would be the highest level expected. Even though the UK’s inflation has fallen from 11.1% to 6.8%, it’s the highest among developed countries, and it’s getting lowered at a slower pace than estimated. In addition, the economy in the UK is slowing more than economists forecast, which could deter the BoE from continuing to increase the Bank Rate amid risks of triggering a recession.

The UK economic docket will reveal inflation data ahead of the BoE’s decision on Wednesday. The Consumer Price Index (CPI) is expected to jump, while the core CPI would decelerate a tick. The week’s main event on the US front would be the Federal Reserve’s monetary policy decision, followed by the Fed Chair Jerome Powell press conference.

GBP/USD Price Analysis: Technical outlook

The downward bias remains intact, as shown by the daily chart. With the GBP/USD trading below the 50 and 200-day Moving Averages (DMAs) while drifting lower and printing successive series of lower highs and lows would keep the GBP/USD at around current levels. To shift its bias neutral, buyers must break the August 25 latest swing low at 1.2548; otherwise, further falls are expected, with sellers eyeing the May 25 low of 1.2308. Further downside is expected below that level, with the March 15 swing low at 1.2010.

- USD/MXN down 0.37%, trading at 17.0685, as the Mexican Peso recovers some of its losses.

- Investors turn cautious ahead of the Federal Reserve meeting, where updated economic projections are expected.

- Preliminary data from INEGI suggests the Mexican economy likely grew 3.4% YoY in August.

The Mexican Peso (MXN) erases some of its Monday’s losses versus the Greenback (USD) and reclaims the 20-day Moving Average (DMA) despite a firm US Dollar (USD), with traders bracing for tomorrow’s US Federal Reserve’s decision. At the time of writing, the USD/MXN is trading at 17.0685, down 0.37%.

USD/MXN trades lower despite a strong US Dollar, as investors await updated economic projections from the Federal Reserve

Investor sentiment has turned negative ahead of the Fed meeting. During the last economic projections, the Fed anticipated 1% economic growth, a 4.1% unemployment rate, 3.2% PCE inflation, 3.9% core PCE inflation, and the Federal Funds Rate (FFR) peaking at 5.60%. These projections will be updated and play a crucial role in shaping the Fed’s future policy decisions.

In the meantime, housing data was revealed and came worse than expected. Housing starts slumped 11.3% last month, the lowest level since June 2020. Data for July was revised lower to show starts accelerating to a rate of 1.447 million units instead of the previously reported 1.452 million units. Meanwhile, Building Permits jumped 6.9% above the prior month’s 0.1% expansion, the most significant rise in six months.

Meanwhile, US Treasury bond yields are trading in positive territory, with the 10-year note coupon yielding 4.337% amidst a US 20-year bond auction, while the Greenback, as shown by the US Dollar Index (DXY), is firm at around 105.12.

Across the border, the Mexican economic docket revealed a poll by the Instituto Nacional de Estadisitca Geografia e Informatica (INEGI), which shows the economy likely grew 3.4% in August compared with the same month a year earlier, in a preliminary estimate from the statistics agency.

USD/MXN Price Analysis: Technical outlook

At the beginning of the week, the USD/MXN could not crack the 100-DMA at 17.2091, opening the door for a pullback, which witnessed the pair breaching the 20-DMA at 17.1075. With that said, and with price action below most Moving Averages, the exotic pair could again test the psychological 17.00 figure. However, it must challenge the 50-DMA at 17..0101 before sliding towards the figure and beyond. For a bullish resumption, the USD/MXN must reclaim the 100-DMA, followed by the 17.5000 figure.

- XAG/USD met resistance at the 200-day SMA near $23.50 and then declined to $23.15

- The benchmark US 10-year bond yield threatens multi-year highs.

- The two-day FOMC meeting kicked off.

In Tuesday’s session, the Silver Spot price XAG/USD lost momentum and failed to conquer the 200-day Simple Moving Average. The main reason was that the US Treasury yields, often seen as the opportunity cost of holding non-yielding metals, recovered as markets await Wednesday's Federal Reserve (Fed) decision.

The 10-year bond yield reached 4.34% and trades near the crucial 4.36% threshold, which, in case of breaking it, would set a multi-year high since 2007. In addition, The 2-year yield stands at 5.08% with a 0.52% increase, while the 5-year yield is at 4.48%, up by 0.31%.

For Wednesday's Federal Reserve (Fed) decisions, despite markets anticipating a pause, a hawkish tone given by Chair Powell could boost US yields and apply further pressure on the grey metal. The US economy remains strong, mainly driven by the Services sector, while the US labour market is showing a mixed picture, and as the Fed want to see a cool down to mitigate inflation risks, it will likely leave the door open for one last hike.

XAG/USD Levels to watch

The technical analysis of the daily chart suggests a neutral to bearish stance for XAG/USD as the bears work on staging a recovery. With a downward trend below its midline, the Relative Strength Index (RSI) suggests that the bear’s momentum is strengthening, while the Moving Average Convergence (MACD) exhibits stagnant red bars. Moreover, the pair is below the 20,100 and 200-day Simple Moving Averages (SMAs), implying that the bears retain control on a broader scale, leaving the buyers vulnerable.

Support levels: $23.00, $22.80, $22.50

Resistance levels: $23.50 - 70 (200, 20 and 100-day SMA convergence),$24.00, $24.30

XAG/USD Daily Chart

-638307403703313911.png)

- The GBP/JPY couldn't maintain a bullish push, and is falling back to the midrange.

- Investors appear unwilling to dedicate to a direction as the BoE comes in for a landing.

- Japan trade balance figures could kick off JPY momentum for the Wednesday session.

The GBP/JPY is retesting the 183.00 handle after failing to recapture the 183.50 level in Tuesday trading.

The Pound Sterling (GBP) is trading softly in Tuesday markets, lacking momentum as investors largely sit on the sidelines ahead of this week’s central bank showings.

Japan trade balance up first, BoE in the barrel

Late Tuesday will see trade balance figures for Japan, due at 23:50 GMT. Exports and imports are both expected to decline, -1.7% and -19.4% respectively, and the overall Merchandise Trade Balance is forecast to decline ¥-659.1B.

Inflation data is inbound on Wednesday for the United Kingdom (UK), with the Consumer Price Index (CPI) headline for the month of August forecast to tick upwards to 0.7% from the previous month’s 0.4% decline.

The inflation read will serve as a precursor to the Bank of England’s (BoE) showing on Thursday, which is expected to raise rates to 5.5%, a 25-basis-point increase from 5.25%.

Inflation continues to plague the UK even as the British economy continues to wobble, and investors will be keeping a close eye on both inflation figures and the BoE’s Monetary Policy Summary.

The BoE’s rate call and following statement kick off at Thursday at 11:00 GMT.

Friday to close out the week with BoJ, UK retail figures

Friday brings the Bank of Japan’s (BoJ) own interest rate showing, which is broadly expected to maintain their -0.1% negative rate stance. Recent comments from BoJ officials teasing about the possible end of the negative rate regime pushed investors into the bullish camp, but the positioning may have been premature.

Japanese government officials were quick to head off the statements at the pass, noting that BoJ rate hikes would only come if the BoJ were able to hold interest rates above the 2% target mark, a goal that may prove illusory for the BoJ as inflation is expected to slump in Japan.

Friday will also close out the week with Retail Sales figures for the UK. Retail sales figures are forecast to gain 0.5% in August after the previous month’s -1.2% decline.

GBP/JPY technical outlook

The Guppy saw a tidy rejection from the 200-hour Simple Moving Average (SMA) in Tuesday trading, sending the pair back into the 183.50 handle after failing to capture 183.50.

Lower highs continue to plague the hourly candlesticks, and the bearish pattern from late August’s high of 186.77 remains intact.

On daily candlesticks the GBP/JPY is struggling to develop momentum, with the pair struggling to make space for itself away from the 34-day Exponential Moving Average (EMA). The 50-day SMA is currently climbing steadily into the 180.00 major psychological handle, and bidders will be looking to keep the pair afloat.

The Guppy has closed in the green for seven of the past eight months, leaving the pair incredibly overbought and exposed to downside shocks if the rug gets pulled out from beneath GBP bulls.

GBP/JPY daily chart

GBP/JPY technical levels

- USD/CHF continued stepping forward and rose near 0.8988.

- SNB meets on Thursday, and markets expect a 25 bps hike.

- The US reported mixed Housing data from August. US Yields recover.

On Tuesday, the USD/CHF continued gaining ground, increasing to 0.8980, and already tallied a 1.60% monthly gain. On the one hand, the Swiss National Bank is expected to deliver its last rate hike from this tightening cycle to 2%, while the Federal Reserve’s (Fed) cycle isn’t done yet.

In line with that, the Federal Open Market Committee (Fed), two-meeting kicked off on Tuesday and ended on Wednesday with the announcement of the monetary policy decision. It is widely expected that the Fed will hold rates steady at the 5.25-5.50% range but will hint at further rate hikes being necessary. Economic activity in the US was seen holding resilient, and as the Fed is expecting the economy to cool down, one last hike may be appropriate. In that sense, as investors discount that the Swiss National Bank (SNB) will end its last hike on Thursday, monetary policy divergences may continue pushing the pair upwards.

On the data front, the US reported that Building Permits accelerated to 1.543M in August, beating the expected and previous figures, while Housing Starts slightly decelerated to 1.283M.

USD/CHF Levels to watch

The daily chart analysis indicates a bullish outlook for the USD/CHF in the short term. The Relative Strength Index (RSI) is above its midline in positive territory, with a positive slope near 70, aligning with the positive signal from the Moving Average Convergence Divergence (MACD), which displays green bars, reinforcing the strong bullish sentiment. Plus, a bullish crossover between the 20 and 100-day Simple Moving Average (SMA) was recorded at the 0.8885 area, which could further boost the pair.

Support levels: 0.8950, 0.8900, 0.8885.

Resistance levels: 0.8985, 0.9000, 0.9038 (200-day SMA)

USD/CHF Daily Chart

-638307368149957855.png)

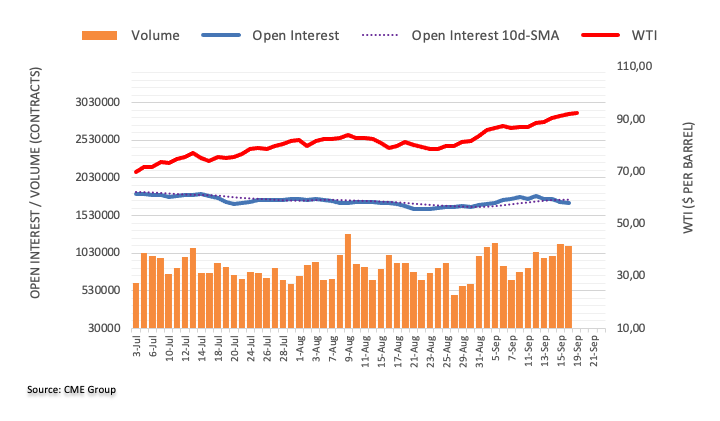

- US WTI crude chalks in a new ten-month high on Tuesday.

- US shale production to decline more than expected.

- Oil firmly bullish, aiming for $100.

West Texas Intermediary (WTI) crude oil barrels briefly peeked over the $93.00/bbl level in Tuesday trading. Oil is trading steadily higher as supply constraint worries send investors scurrying, sending the price of crude barrels soaring.

US shale production to slow further, oil markets squeezed higher

The Energy Information Agency (EIA) is warning that US shale production is set to decline further in October. The EIA’s Drilling Productivity Report has shale slated to produce 9.393 million bpd, the lowest level since May of this year.

Crude prices have been facing an enormous squeeze ever since Saudi Arabia and Russia announced extensions of their 1.3 million bpd production cuts through the end of the year. WTI crude prices have risen 15% in just four weeks as oil traders fear a global supply snap.

The global oil supply chain is expected to see a 2 million bpd deficit heading into the first quarter of 2024. With such a sharp deficit, global oil reserves are expected to dwindle away to nothing unless additional crude production projects are fired up and capacity is restored.

WTI technical outlook

WTI has closed in the green for ten of the past twelve straight weeks, and is knocking ten-month highs as crude gets pushed higher. US oil briefly saw the north side of $92/bbl, beore settling back to sub-$91.50/bbl.

On the daily candlesticks, there’s plenty of room for crude to run, with prices neatly breaking the 200-day Simple Moving Average (SMA) back in July, which currently rests near $77/bbl.

Further upside will see oil prices testing $92.50, a level that has seen significant rejection in the past.

On the low side, support is coming from the 34-day Exponential Moving Average (EMA) near $84/bbl, with the near-term floor priced in at the last swing low of $78/bbl in mid-August.

WTI daily chart

WTI technical levels

- USD/JPY remains near yearly highs as investors turn cautious ahead of the US Federal Reserve and Bank of Japan (BoJ) policy decisions.

- The Fed is expected to keep rates unchanged, with a focus on economic forecasts and the Federal Funds Rate (FFR) projections.

- The BoJ is not expected to raise rates but may provide insights into potential changes to its Yield Curve Control (YCC) and negative interest rate policies.

The USD/JPY remains subdued as Tuesday’s session begins, ahead of the US Federal Reserve’s decision on Wednesday, in which the US central bank is expected to keep rates unchanged at the 5.25%-5.50% range. The major is rising on the advancement in US Treasury bond yields and trades at 147.71, at around yearly highs.

USD/JPY trades at 147.71, buoyed by rising US Treasury yields, as markets look forward to key central bank meetings this week

Investors’ sentiment has turned sour ahead of the Fed. Besides the monetary policy decision, Fed Chair Jerome Powell and Co. will update their economic forecasts and Federal Funds Rate (FFR) expectancy. The last Summary of Economic Projections (SEP) witnessed policymakers expecting a 1% economic growth while the unemployment rate would climb to 4.1%. The Fed’s preferred inflation gauge, the PCE, is estimated at 3.2%, and the core PCE at 3.9%. The same report projects the FFR to peak at around 5.60%.

In the meantime, the Bank of Japan (BoJ) will also reveal its decision on September 22, in which the BoJ is not expected to raise rates. Still, it would be interesting to see if there are some expressions about additional tweaking to its Yield Curve Control (YCC) and discussions about ending its negative interest rates program.

Data-wise, August’s US building permits rose above estimates, and housing starts tumbled the most since 2020, down at -11.3%. On the Japanese front, its docket would feature the Balance of Trade for August, estimated at ¥-659.1B, while Exports are foreseen to shrink by -1.7%.

USD/JPY Price Analysis: Technical outlook

Consolidation is the name of the game with the USD/JPY pair. The threat of intervention by Japanese authorities refrains investors from opening fresh long bets in the pair, which could have easily tested the 150.00 threshold if not for the abovementioned. Initial resistance for the USD/JPY is seen at 148.00 before climbing towards the October 31 daily high at 148.84. A downward correction wil face the Tenkan-Sen at 146.92, followed by the Kijun-Sen at 146.19.

The Bank of Japan (BoJ) is getting closer to the end game, in the view of economists at TD Securities who expect USD/JPY to push to 135 in early 2024.

BoJ getting closer to the hiking trigger

The BoJ is getting closer to pulling the trigger to end its negative interest rate policy (NIRP). We believe the BoJ 2% inflation goal is clearly in sight, factoring in the latest inflation data and risks (as well as other events) on the horizon. We expect the BoJ to end its Yield Curve Control (YCC) policy at the Dec'23 meeting and exit NIRP in Jan'24 with a 10 bps hike in the policy balance rate.

Our accelerated timeline for BoJ normalization reinforces our out-of-consensus USD/JPY forecast, which sees a push towards 135 in early 2024.

The cross-fire that had hit the Australian Dollar throughout August (combination of high US rates and plummeting Chinese sentiment) has not ceased since the start of September. Economists at ING analyze AUD/USD outlook.

Still looking for a bottom

Moving ahead, we expect the US growth/Fed easing, and in turn, the global USD story, to be the key driver of AUD/USD. This is not to say that China will be put on the backburner, but a lot of the deterioration in Chinese growth is already priced into AUD, and things may gradually improve from here with monetary and fiscal stimulus being deployed in Beijing.

AUD/USD may still be searching for its bottom, but we still like a strong recovery into the new year, in line with USD decline story.

AUD/USD – 1M 0.63 3M 0.65 6M 0.68 12M 0.72

EUR/USD dropped despite the ECB’s decision to hike. Economists at UBS discuss the pair’s outlook.

Euro likely to rebound after dovish ECB message

The ECB hiked rates to a record high of 4% last week, its 10th consecutive increase. The decision was accompanied by an increase in the central bank’s inflation projections, which are now expected to average 5.6% this year and 3.2% in 2024-still well above the 2% target.

We remain most preferred on the Euro and least preferred on the US Dollar. The ECB’s move narrows the rate premium offered by the US, and we don’t expect rate cuts from the Eurozone’s central bank until at least June next year. An acceleration of quantitative tightening, with the ECB increasing the pace at which it shrinks its balance sheet, is also possible early next year.

We expect EUR/USD to rise to 1.12 by the end of the year.

The Rand strengthened about 0.5% vs. the USD last week. Economists at Société Générale analyze USD/ZAR technical outlook.

Direction lacking

USD/ZAR tested intermittent support near 17.40 representing the 38.2% retracement from 2021 and quickly reclaimed the 200-DMA. The bounce has so far remained stalled near August high of 19.30. A sideways consolidation is underway. Signals of a large decline are not yet visible; the 200-DMA near 18.35/18.10 should be an important support zone near term.

Daily MACD is within positive territory denoting prevalence of upward momentum. Once a break above 19.30 materializes, the uptrend is expected to resume. Next objectives would be at June high of 19.92 and projections of 20.25.

GBP/USD oscillates just below 1.24. Economists at OCBC Bank analyze the pair’s outlook.

25 bps hike likely

Risks skewed to the downside but at the same time, we observed a potential falling wedge, which may point to a bullish reversal at some point. We watch price action for confirmation.

We still expect a 25 bps hike at the upcoming MPC as wage growth remains red hot and core CPI remains elevated. That said, GBP could still trade on the back foot amid the BoE nearing the end of tightening cycle while stagflation concerns returned.

- Silver price stabilizes confidently above $23.00 as the focus shifts to Fed policy.

- The Fed is widely anticipated to keep interest rates unchanged at 5.25-5.50%.

- Silver price stabilizes above the horizontal resistance plotted around $23.12, which has turned into a support.

Silver price (XAG/USD) shifts auction above the crucial resistance of $23.00 as the US Dollar comes under pressure ahead of the interest rate decision by the Federal Reserve (Fed), which will be announced on Wednesday.

The S&P500 opens on a cautious note as investors remain uncertain over the interest rate guidance. The Fed is widely anticipated to keep interest rates unchanged at 5.25-5.50% but will keep doors open for further policy tightening.

Any discussion about rate cuts would improve the appeal for the risk-perceived assets and dampen the US Dollar. Economists at Goldman Sachs expect Fed officials to signal a full percentage point of cuts next year but to keep expectations of one more interest rate increase this year to a range of 5.50%-5.75%.

The US Dollar Index (DXY) finds support near 104.80 but the upside seems restricted as the Fed is expected to skip raising interest rates for the second time in its aggressive policy-tightening since March 2022. Meanwhile, the 10-year US Treasury yields to near 4.34%.

The US economy has remained resilient despite higher interest rates but investors see the economic recovery faltering as the Fed is expected to keep interest rates ‘higher for longer’. Meanwhile, the yields offered on five-year US bonds have increased from 10-year US Treasury yields, indicating that investors see a slowdown in the near term.

Silver technical analysis

Silver price stabilizes above the horizontal resistance plotted from September 7 high around $23.12, which has turned into a support. The 20-period Exponential Moving Average (EMA) at $23.20 is consistently providing support to the Silver bulls. The Relative Strength Index (RSI) (14) struggles to shift into the bullish range of 60.00-40.00.

Silver two-hour chart

-638307296092253924.png)

Economists at Commerzbank analyze EUR outlook after the ECB hiked its key rate last Thursday and ECB President Christine Lagarde signalled that the ECB is now likely to have reached the end of the rate hike cycle.

FX market will largely wait and see what surprises the Fed might have in store

In the coming days and weeks, there should be increasing clarity about the extent to which there may still be a willingness in the ECB's monetary policy council to perhaps raise interest rates again. Or what conditions would have to be met for such a step. Such comments should tend to benefit the EUR, as the market currently seems to be betting on an end to the rate hike cycle, which could clear the way for rate cuts next year. Comments suggesting that rate cuts may still be a long way off would also be positive for the EUR.

However, it may also turn out that the Council members are largely in agreement that the end of the rate hike cycle has been reached. The market is then more likely to interpret this as a dovish stance by the ECB and the EUR could come under depreciation pressure.

In the short term, however, the focus is of course on the US Fed. Ahead of the rate decision on Wednesday the FX market will largely wait and see what surprises the Fed might have in store.

AUD drifted higher following tentative signs of improvement in China data. Economists at OCBC Bank discuss Aussie’s outlook.

Room for gains

Looking out, we still favour AUD to trade higher on of expectations that China growth could stabilise at some point, possibly warmer ties between Australia and China, and a more moderate-to-soft USD profile (as the Fed nears end tightening cycle and embarks on rate cut cycle in 2024).

We have shared that the tourism, education, and property sectors in Australia could benefit if relations between China and Australia further warm up, and this can be a positive for AUD.

Key downside risk factors that may affect AUD outlook are 1/ extent of CNH swings; 2/ if USD strength or Fed tightening cycle unexpectedly extends; 3/ global growth outlook – if DM’s slowdown deteriorates; 4/ any market risk-off event.

Break below 4.84 would lead USD/BRL downtrend to resume, analysts at Société Générale report.

5.01/5.04 is an important resistance zone

USD/BRL defended lower limit of a multi-month channel near 4.69 resulting in a phase of rebound. Interestingly, it has so far struggled to re-enter previous range. Upper band of that channel near 5.01/5.04 which is also the 200-DMA is an important resistance zone.

In case the pair fails to defend recent pivot low at 4.84, one more leg of downtrend can’t be ruled out towards 4.69, and 2022 low at 4.61/4.59.

- EUR/USD’s recovery briefly surpasses the key 1.0700 threshold on Tuesday.

- Next on the upside comes 1.0767 ahead of 1.0828.

EUR/USD trades in a volatile fashion and looks to consolidate a breakout of the 1.0700 hurdle on Tuesday.

If the rebound gathers extra steam, the pair should face a minor hurdle at the weekly high of 1.0767 (September 12) prior to the critical 200-day SMA at 1.0828.

While below the key 200-day SMA, the pair is likely to face extra weakness.

EUR/USD daily chart

Economists at the Bank of Montreal expect EUR/USD to struggle in the near-term but see the pair recovering toward the 1.10 level by the end of the year.

A deeper correction lower in EUR/USD heading toward year-end is not the base case

A deeper correction lower in EUR/USD heading toward year-end is not the base case, but downside risks have increased, particularly with the global trade backdrop looking poor and transatlantic economic divergence set to remain wide for another quarter or so. Closer ties between Russia and North Korea also portend higher levels of geopolitical risk in relation to the war in Ukraine.

The EUR is likely to struggle to maintain topside momentum over the near-term. However, the base case is for moderate EUR/USD strength to push the exchange rate back to 1.10 around the turn of the year.

- DXY extends the weekly retracement below 105.00.

- Further south comes the weekly low near 104.40.

DXY has been shedding ground for the last three sessions and has opened the door to extra losses in the near term.

In case the corrective decline picks up further pace, the index could extend the drop to, initially, the weekly low of 104.42 (September 11). A sustained pullback below the latter could prompt the index to embark on a potential test of the critical 200-day SMA, today at 103.03.

While above the key 200-day SMA, the outlook for the index is expected to remain constructive.

DXY daily chart

USD/MXN has reversed most of the early September gains. Economists at ING analyze the pair’s outlook.

MXN to find strong buying interest on dips

The Mexican Peso may be under pressure in September and October as Banxico unwinds its intervention forward book, but we expect it to find strong buying interest on dips.

A tough external environment could see the USD/MXN pair trade to 18.00 this month, but a good macro story favours 17 again soon.

See – USD/MXN: Defence of 16.60 can lead to a short-term bounce – SocGen

- EUR/JPY extends the weekly uptrend beyond 158.00.

- Next on the upside comes the YTD high.

EUR/JPY clinches its third session in a row of gains and manages to reclaim the 158.00 barrier and beyond on Tuesday.

In the meantime, the cross continues to face some consolidative range. Against that, a minor hurdle emerges at the so far monthly high of 158.65 (September 13) ahead of the 2023 top at 159.76 (August 30), which precedes the key round level at 160.00. The surpass of the latter should not see any resistance level of note until the 2008 high at 169.96 (July 23).

So far, the longer term positive outlook for the cross appears favoured while above the 200-day SMA, today at 148.84.

EUR/JPY daily chart

Markets are treading water ahead of the FOMC decision on Wednesday. Economists at Scotiabank analyze USD outlook.

USD in consolidation mood ahead of FOMC

Overall, markets appear in fairly constructive mood ahead of the Fed.

The Fed may not sound dovish but markets may need quite a lot more supportive evidence to push an expensive looking USD (certainly relative to short-term yield spreads against its major currency peers) even higher at this point.

US yields are bumping up against some key levels (5% or so for 2Y and 4.45% for 5Y) and a lot of good news still looks to be factored into the USD at this point.

Recall that the DXY had advanced for nine consecutive weeks through last Friday and that sort of run usually leaves any market prone to some sort of consolidation or correction – which appears to be playing out, at least ahead of the Fed.

- USD/CAD witnesses selling pressure as the US Dollar corrects sharply ahead of the Fed policy.

- Canada’s headline CPI expanded at a pace of 0.4% while annual CPI accelerated sharply to 4%.

- The BoC may keep interest rate policy stable ahead as the core inflation remains steady.

The USD/CAD pair witnesses an immense sell-off as the US Dollar weakens ahead of the interest rate decision by the Federal Reserve (Fed). The Loonie asset also faces selling pressure as Statistics Canada reported that the headline Consumer Price Index (CPI) expanded at a pace of 0.4% vs. expectations of 0.2%.

The annual headline inflation accelerated sharply to 4% against the estimates of 3.8% and the former release of 3.3%. The core CPI that excludes volatile oil and food prices expanded nominally by 0.1%, indicating subdued demand for non-durable goods and services. On an annualized basis, the core CPI rose to 3.3%.

Canada’s inflation for August is not expected to force the Bank of Canada (BoC) to deliver one more interest rate hike as the core inflation remains steady, which is generally considered for the monetary policy framework.

Meanwhile, the US Dollar Index (DXY) continues a two-day losing spell as the Fed is expected to skip raising interest rates in its September monetary policy on Wednesday. This would be the second time the Fed is expected to skip hiking interest rates in its historically aggressive tightening spell that started in March 2022.

As per the CME Group Fedwatch Tool, traders undoubtedly see interest rates remaining steady at 5.25%-5.50% after the Federal Open Market Committee (FOMC) meeting on Wednesday. For the rest of the year, traders anticipate almost a 58% chance for the Fed to also keep monetary policy unchanged.

Investors would look for the commentary about rate cuts as the US manufacturing sector is going through turbulent times. US firms are operating at lower capacity and working on achieving operational efficiency by controlling costs through lower inventory due to a deteriorating demand environment.

Kit Juckes, Chief Global FX Strategist at Société Générale, is worried about Sterling.

Sterling is only being held up by rate expectations

The more the market worries about the growth outlook in the UK, the more the prospect of further rate hikes beyond this week will a) fade away and b) scare investors.

Sterling, even more perhaps than the Euro, is only being held up by rate expectations. This week’s data calendar might not be too bad for the Pound if Retail Sales and the Services PMI both bounce and core CPI remains at 6.9%. But at best, that will delay what seems an inevitable move by GBP/USD back below 1.20.

- Housing Starts drops sharply while Building Permits rose above expectations in the US in August.

- US Dollar Index stays near daily lows below 105.00 after the data.

The monthly data published by the US Census Bureau revealed on Tuesday that Housing Starts tumbled 11.3% on a monthly basis in August, following a 2% increase (revised from 3.9%) recorded in July, to a seasonally adjusted annual rate of 1,283 million. This reading came in worse than the market expectation for a decline to 1,44 million.

In the same period, Building Permits, which rose 0.1% in July, increased 6.9%., to a seasonally adjusted annual rate of 1,543,000; surpassing the 1,445,000 of market consensus.

Market reaction

The US Dollar Index showed no immediate reaction to these figures and was last seen fluctuating near daily lows under 105.00.

- Annual inflation in Canada rose at a stronger pace than expected in August.

- USD/CAD trades deep in negative territory near 1.3400 after the data.

Inflation in Canada, as measured by the change in the Consumer Price Index (CPI), rose to 4% on a yearly basis in August from 3.3% in July. This reading came in higher than the market expectation of 3.8%. On a monthly basis, the CPI rose 0.4%, compared to analysts' estimate for an increase of 0.2%.

Moreover, the Bank of Canada reported that the monthly Core CPI, which excludes volatile food and energy prices, rose 0.1%, while the annual Core CPI edged higher to 3.3% from 3.2%.

Market reaction

USD/CAD edged lower with the immediate reaction and was last seen losing 0.65% on the day at 1.3400.

- AUD/USD climbs sharply above 0.6430 as the US Dollar faces selling pressure ahead of the Fed policy.

- The Fed is expected to keep interest rates higher long enough to ensure price stability.

- AUD/USD rebounds after discovering buying interest near the horizontal support plotted around 0.6364.

The AUD/USD pair delivers an upside break of the consolidation formed in a range of 0.6430-0.6450 in the European session. The Aussie asset picks strength as the US Dollar Index (DXY) eases ahead of the Federal Reserve (Fed) monetary policy, which will be announced on Wednesday.

Investors see the Fed keeping interest rates steady at 5.25-5.50% as inflation is consistently cooling while economic prospects are strong. The labor growth in the United States economy has remained steady despite higher interest rates from the Fed. The Fed is expected to keep interest rates higher long enough to ensure price stability.

Meanwhile, the Australian Dollar will remain in action amid the interest rate policy by the People’s Bank of China (PBoC), which will be revealed on Wednesday. A dovish interest rate stance is expected from the PBoC due to upside risks to deflation amid bleak household’ demand.

The US Dollar Index drops sharply below the crucial support of 105.00 and is expected to remain vulnerable ahead.

AUD/USD rebounds after discovering buying interest near the horizontal support plotted from August 17 low around 0.6364 on a two-hour scale. The Aussie asset stabilizes above the 50-day Exponential Moving Average (EMA), which trades around 0.6340. Potential resistance is plotted from August 15 high at 0.6522.

The Relative Strength Index (RSI) (14) jumps above 60.0, which indicates that the bullish impulse has been triggered.

A decisive break above August 15 high around 0.6522 will drive the asset to August 9 high at 0.6571. Breach of the latter will drive the asset towards August 10 high at 0.6616.

On the flip side, a fresh downside would appear if the Aussie asset will drop below August 17 low around 0.6360. This would expose the asset to the round-level support of 0.6300 followed by 03 November 2022 low at 0.6272.

AUD/USD two-hour chart

-638307228317349671.png)

The big focus is on the Fed. Any moves in the dot, especially in 2024 will have a significant impact on markets, FX. Economists at OCBC Bank considered three potential scenarios with regard to 2024.

A more dovish dot plot would lead to dovish re-pricing, weighing on USD

A scenario of no-change to dot plot will come as a relief to risk assets. USD may ease as markets have already unwound their prior dovish bets to be aligned with the Fed’s Jun dot plot.

A case of more dovish dot plot (i.e. if the Fed looks for more cuts than what they have pencilled in) would lead to dovish re-pricing and that can weigh on USD.

A more hawkish dot plot (i.e. Fed looks for lesser cuts, dots shift higher) would lead to hawkish re-pricing. Yields can run higher, and USD can continue to trade higher. This would be a risk-off scenario for risk assets. In this scenario, alongside higher Oil prices, there will be upward pressure on inflation and yields. This may result in a deterioration of global growth/inflation mix and can cause headwinds to risk appetite and undermine Asian FX, especially those that are net oil importers, such as THB, PHP.

USD/CAD pushed support in the upper 1.34 area. Economists at Scotiabank analyze the pair’s outlook.

USD/CAD should run lower to test 1.3393

Losses through firm USD support in the upper 1.34 area point to more weakness in the near-term at least.

Short-term trend momentum is picking up more obviously, with the intraday and daily DMIs aligned bearishly for the USD.

USD/CAD should run lower to test 1.3393 (50% retracement of the July/September move up) which coincides with the early July spike high. A break below here puts the low 1.32s on the radar.

USD resistance is 1.3490/1.3495.

GBP/USD is holding a narrow consolidation range between support at 1.2370 and resistance at 1.2410. Economists at Scotiabank analyze Cable’s outlook.

A clear move through the low 1.24s will ease broader, bearish pressure

Short-term trend dynamics are bearish which should limit the scope for gains in the near term.

A clear move through the low 1.24s will ease broader, bearish pressure on the Pound but gains through 1.2550 are needed to suggest more sustainable gains.

The broader trend appears bearish still.

See: The downtrend in Sterling is likely to continue – Commerzbank

EUR/USD edges above 1.07 amid oversold conditions. Economists at Scotiabank analyze the pair’s technical outlook.

The very short-term trend looks constructive

The very short-term trend looks constructive and the EUR does look quite oversold (after nine consecutive weekly losses against the USD). But there is still quite a gap between current levels and points on the chart which would signal scope for more EUR strength.

A clear push through the 1.0765 point would be a bullish, short-term cue for the EUR at least.

- The US Dollar trades marginally in the green on Tuesday after a minor incurred loss on Monday.

- Traders will likely keep powder dry for the Fed interest rate decision on Wednesday.

- The US Dollar Index resides above 105.00, struggling to make new highs.

The US Dollar (USD) took a small step back at the start of this week with traders focusing on the main event on Wednesday with the US Federal Reserve (Fed) rate decision. Expectations are for no hike, though with the recent resurgence in headline inflation via energy prices, US Fed Chair Jerome Powell might be more hawkish than predicted.

Traders, meanwhile, have to split and divide their attention between the Fed and Capitol Hill, with a possible US government shutdown looming again. By Thursday, US House Speaker Kevin McCarthy needs to bring a new stopgap bill to the floor for a vote. If the House fails to pass the bill, the probability of a shutdown in October grows more dire.

Daily digest: US Dollar softens

- A bit more data this Tuesday arrives after the calm start on Monday with US housing data hitting the wires at 12:30 GMT. Building Permits are expected to stay steady near 1.445 million, a touch higher from the 1.443 million in July. Housing Starts are expected to head from 1.443 million to 1.445 million.

- Near 12:55 GMT, the US Redbook will be released. Previous number was 4.6%.

- The US Treasury will be auctioning 20-year Treasuries.

- Equities are in the red this Tuesday ahead of the US Fed meeting. Several trading desks are reporting some profit-taking ahead of a possible failure of the stopgap bill to avoid a US shutdown.

- The CME Group FedWatch Tool shows that markets are pricing in a 99% chance that the Federal Reserve will keep interest rates unchanged at its meeting in September. Traders though will need to watch out for any hawkish rhetoric from Powell as inflation has been ticking up recently.

- The benchmark 10-year US Treasury yield trades at 4.31% and peaked in early Monday trading before starting to sell off. A small flight to safe havens with US bonds being bought triggers a decline in yields.

US Dollar Index technical analysis: Facing selling pressure

THe US Dollar was facing some selling pressure on Monday, which actually is not a bad thing as such. After a ninth consecutive week of gains for the US Dollar Index (DXY), the Relative Strength Index (RSI) is a fair bit into overbought territory. A few days of sideways to lower would help cool down the rally a bit before entering the next leg up, where the US Fed rate decision could act as a catalyst.

The US Dollar Index (DXY) has edged up, reaching 105.41. This is just a sigh away from the 2023 high near 105.88. Should the DXY be able to close above there for the week, expect the US Dollar to go even stronger in the medium-turn.

On the downside, the 104.44 level seen on August 25 kept the Index supported on Monday, halting the DXY from selling off any further. Should the uptick that started on September 12 reverse and 104.44 gives way, a substantial downturn could take place to 103.04, where the 200-day Simple Moving Average (SMA) comes into play for support.

US Dollar FAQs

What is the US Dollar?

The US Dollar (USD) is the official currency of the United States of America, and the ‘de facto’ currency of a significant number of other countries where it is found in circulation alongside local notes. It is the most heavily traded currency in the world, accounting for over 88% of all global foreign exchange turnover, or an average of $6.6 trillion in transactions per day, according to data from 2022.

Following the second world war, the USD took over from the British Pound as the world’s reserve currency. For most of its history, the US Dollar was backed by Gold, until the Bretton Woods Agreement in 1971 when the Gold Standard went away.

How do the decisions of the Federal Reserve impact the US Dollar?

The most important single factor impacting on the value of the US Dollar is monetary policy, which is shaped by the Federal Reserve (Fed). The Fed has two mandates: to achieve price stability (control inflation) and foster full employment. Its primary tool to achieve these two goals is by adjusting interest rates.

When prices are rising too quickly and inflation is above the Fed’s 2% target, the Fed will raise rates, which helps the USD value. When inflation falls below 2% or the Unemployment Rate is too high, the Fed may lower interest rates, which weighs on the Greenback.

What is Quantitative Easing and how does it influence the US Dollar?

In extreme situations, the Federal Reserve can also print more Dollars and enact quantitative easing (QE). QE is the process by which the Fed substantially increases the flow of credit in a stuck financial system.

It is a non-standard policy measure used when credit has dried up because banks will not lend to each other (out of the fear of counterparty default). It is a last resort when simply lowering interest rates is unlikely to achieve the necessary result. It was the Fed’s weapon of choice to combat the credit crunch that occurred during the Great Financial Crisis in 2008. It involves the Fed printing more Dollars and using them to buy US government bonds predominantly from financial institutions. QE usually leads to a weaker US Dollar.

What is Quantitative Tightening and how does it influence the US Dollar?

Quantitative tightening (QT) is the reverse process whereby the Federal Reserve stops buying bonds from financial institutions and does not reinvest the principal from the bonds it holds maturing in new purchases. It is usually positive for the US Dollar.

It is – another – waiting day ahead of Wednesday’s FOMC meeting. Kit Juckes, Chief Global FX Strategist at Société Générale, analyzes the FX market outlook.

The Euro, and even more, the Pound, still look vulnerable

The market doesn’t expect a Fed hike but the dot-plot, which currently suggests there will be one more this year before a steady fall, thereafter, could see cuts pushed further out, while the tone of the statement is certain to be hawkish, as the FOMC reinforces the ‘higher for longer’ message.

Higher Oil prices and decreased pessimism about China can support AUD and CAD for now, but the Euro, and even more, the Pound, still look vulnerable.

Economists at ING analyze how Canadian inflation data could impact USD/CAD and BoC’s rate hike expectations.

Canadian CPI may put a BoC hike back on the table