- Аналітика

- Новини та інструменти

- Новини ринків

Новини ринків

The former Bank of Japan (BoJ) policy board member Makoto Sakurai stated in an interview on Thursday that the central bank may scrap negative interest rates by the end of this year to adjust the currently excessive level of monetary easing.

Key quotes

“They could do it at any time and it won’t be a surprise, given the current economic recovery”

“The BOJ has appeared cautious, but they have steadily taken policy actions at a faster pace than expected”

“Changing the negative rate would lead to slight changes in the shape of the yield curve,”

“But the overall curve has already risen so it’s okay for the furthest part of short-term rates to increase.”

“There is too much extraordinary monetary easing now,”

“The problem with that is it does unnecessary things like continuing to expand the BOJ’s balance sheet.”

Market reaction

USD/JPY remains flat following the above comments from the former BoJ policymaker. At the time of press, the pair was down 0.04% on the day at 149.86.

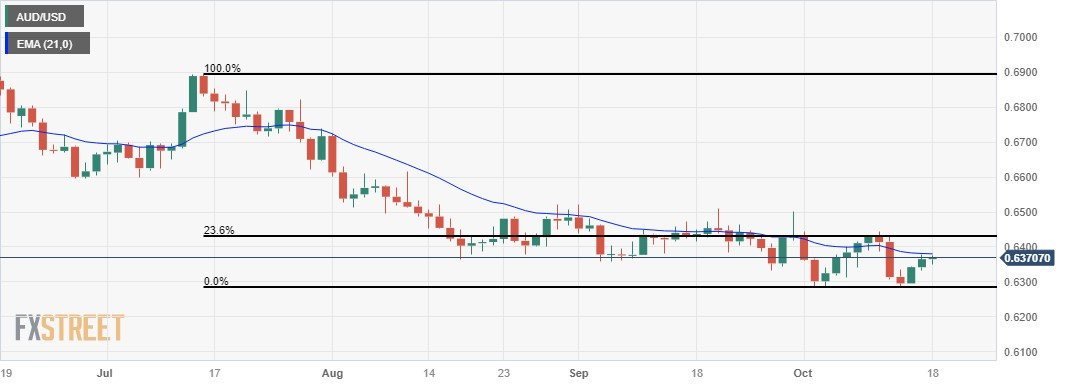

- The Aussie has rebounded firmly against the Kiwi in recent days, climbing nearly 2% from October's low.

- Despite the gains, the AUD's momentum could evaporate quickly with the pair stuck in familiar midrange territory.

- Thursday sees a fresh round of Aussie labor data which could kick off the next leg.

The AUD/NZD heads into a Thursday market session with Australian labor data on the cards, and investors will be looking for the Australian Unemployment Rate to hold steady at 3.7% for September, while the Aussie Employment change is expected to add at least 20K jobs in September compared to August's 64.9K.

Late Thursday will also see New Zealand Trade Balance figures as the Kiwi heads into the early Friday trading window, and Kiwi bidders will be hoping for a bounce in the headline annualized reading for September, which last came in at $-15.54B.

AUD/NZD Technical Outlook

The Aussie has rebounded firmly against the Kiwi as the NZD flubs market value, sending the AUD/NZD into median prices at the 200-day Simple Moving Average (SMA), with September's last swing high at 1.0918.

The Antipodean currency pair remains relatively on-balance for 2023 as the two currencies jockey but struggle to meaningfully develop long-term momentum in either direction. A technical floor has been priced in from the last swing low into 1.0640.

AUD/NZD Daily Chart

AUD/NZD Technical Levels

- The NZD/USD is trading into the floor, inches away from setting a new low for 2023 below 0.5846.

- Market sentiment has receded as investors see jitters over geopolitical tensions.

- Markets looking ahead to Fed Powell appearance later on Thursday, followed by NZ Trade Balance figures.

The NZD/USD slipped even further on Wednesday, declining into 2023's lows and set for a new yearly low below 0.5846.

Broad-market sentiment turned firmly risk-off on the trading day, and the Kiwi heads into the Thursday market session pinned to the floorboards.

The Gaza Strip conflict between Israel and Hamas continues to weigh on geopolitical stability concerns for the Middle East, with market tensions rising after a hospital explosion left over 500 civilians dead. Both Israel and Hamas have pointed fingers at the other, with Hamas claiming an Israeli targeted air strike demolished the building while Israel is blaming an errant Hamas missile.

The US Congress remains frozen in place, unable to elect a new Speaker of the House after Congressional Republicans ejected their own Speaker from the position. Congress has faced down to unsuccessful votes in two days trying to find a replacement, log-jamming government procedure and rattling investors with the US set to run into another funding standoff in four weeks.

Thursday brings US Initial Jobless Claims for the week into October 13th, and markets are expecting to see a small uptick in the number of new unemployment applicants, from 209K to 212K.

Later in the day Federal Reserve (Fed) Chair Jerome Powell will be delivering talking points at a luncheon hosted by the Economic Club of New York, and late Thursday will see New Zealand Trade Balance figures as NZ heads into the Friday early market session.

Kiwi investors will be hoping for an improvement in the headline Trade Balance for the annualized period into September, which last showed a $-15.54B undershoot in August.\

NZD/USD Technical Outlook

The Kiwi remains woefully underbid, testing into 2023's lows and set for a break of the year's bottom bids, and Kiwi price action continues to follow a declining 50-day Simple Moving Average (SMA) further down the charts.

A bearish continuation into fresh lows for the year will see the way open up for an extended decline into 2022's lows far below at 0.5511, while a bullish recovery will still face long-term technical resistance from the 200-day SMA currently rolling over into bearish acceleration from 0.6152.

NZD/USD Daily Chart

NZD/USD Technical Levels

Federal Reserve (Fed) Governor Michelle W. Bowman commented at a Fed Listens event on Thursday that inflation in the US has come down but is still too high.

Key quotes

“What has been somewhat surprising, however, is that the relative strength in goods spending has persisted, rather than reverting to its pre-pandemic trends.”

“This pattern we see in the US is also unusual relative to other advanced economies, where the composition of goods versus services spending appears to have returned to historical norms.”

Market reaction

At the time of press, the US Dollar Index was down 0.02% on the day at 106.54.

- EUR/USD remains on the defensive around 1.0538 amid the rising US Treasury yields.

- The US housing data showed mixed results on Wednesday.

- The Eurozone Harmonized Index of Consumer Prices (HICP) came in at 0.3% in September, as expected.

- US Jobless Claims, the Philly Fed index, the Federal Reserve Chair Powell’s speech will be closely watched events.

The EUR/USD pair struggles to gain and resumes its downside during the early Asian session on Thursday. The escalating geopolitical tension between Israel-Hamas and higher US Treasury bond yield exert some selling pressure on the pair. EUR/USD currently trades around 1.0538, up 0.01% for the day.

Meanwhile, the US Dollar Index (DXY), a measure of the value of the USD relative to a basket of foreign currencies, resumes its upward path, rising to 105.55. US Treasury yields edge higher, with the 10-year Treasury yield surging to 4.911%, the highest level since 2007.

That being said, a rise in bond yield and the cautious mood in the market boost the US Dollar (USD) broadly. Additionally, the Fed speakers reiterated their preference to keep rates on hold, their comments lift the US bond yields higher amid robust momentum in US growth.

The US housing market revealed mixed results on Wednesday. Building Permits fell to 1.475M in September, above the estimated of 1.45M, while Housing Starts rose to 1.35M, below the market consensus of 1.38M. However, there was nothing in the data to convince the FOMC to abandon its current guidance. According to the Beige Book, economic activity showed "little to no change" between September and early October.

The Harmonized Index of Consumer Prices (HICP) in the Eurozone released by Eurostat came in at 0.3% in September, data published by Eurostat showed Wednesday. The European Central Bank (ECB) President Christine Lagarde remarked that underlying inflation remains strong and wage growth remains historically high.

Market players will focus on the US Jobless Claims and the Philly Fed index. The Federal Reserve Chair Powell is also scheduled to speak. On the Euro docket, the Eurozone Current Account for August will be released. These events could give a clear direction to the EUR/USD pair.

- USD/CHF bounces off the 50-DMA support at 0.8957, currently trading near 0.8987.

- The 200-DMA at 0.9014 is a significant resistance, capping the pair's upside.

- Slowing inflation in Switzerland initially boosted the pair towards 0.9200.

- A recent decline in US bond yields, combined with a double-top pattern, has pressured the pair downwards.

The USD/CHF extended its losses towards the 50-day moving average (DMA) at 0.8957, though bounced off at that level, and finished Wednesday’s session at around 0.8987, capped on the upside by the 200-DMA. As Thursday’s Asian session begins, the major exchanges hands at 0.8987, almost flat.

Revisiting the USD/CHF after a week's absence, the pair trades in between the 50 and 200-DMA, with the latter at around 0.9014, exerting downward pressure on the pair. As inflation in Switzerland continued to slow down, traders bought the pair, lifting prices toward 0.9200. But the recent fall in US bond yields sparked the major’s recent leg down, coupled with a double-top chart pattern.

Given the backdrop, the USD/CHF pair is trading sideways. A break below the 50-DMA would expose the 0.8900 figure, followed by a September 11 swing low test of 0.8893. On the other hand, if USD/CHF reclaims the 200-DMA, the pair could rally and test the latest cycle high of 0.9088 before launching an attack toward the month-to-date (MTD) high of 0.9245.

USD/CHF Price Action – Daily chart

USD/CHF Technical Levels

- US equities see red for the mid-week as risk sentiment sours on Wednesday.

- Risk appetite is slumping as US Treasury yields rock into highs not seen in over a decade and a half.

- Middle East geopolitical concerns and a frozen US Congress are souring risk appetite.

The Standard & Poor's (S&P) 500 major equity index tumbled 58.60 points on Wednesday, closing down 1.34% to finish the day at $4,314.60 after broad-market risk appetite soured through the trading day, with investors pushed back into safe havens as the Gaza conflict escalation and a logjammed US Congress weigh on sentiment.

Geopolitical tensions around the Israel-Hamas conflict in the Gaza Strip continue to pin into the high end following a hospital explosion that claimed 500 civilians and left Israel and Hamas pointing the finger at the other over who was responsible for the deadly attack.

Wednesday's risk-off flows saw US equities fall across the board, with the Dow Jones Industrial Average (DJIA) falling 0.98% to close down 332.57 points at $33,665.08. The NASDAQ Composite saw deep red for Wednesday as tech stocks took the hardest hit of the day, with the tech index down 1.62% into $13,314.30, declining 219.44 points.

US Treasury yields rose with the 10-year T-note climbing above 4.9%, tipping into 4.928%, the 10-year's highest yield since early 2007.

Rate cost hikes are seeing spillover into other sectors with the popular US 30-year fixed mortgage median rate hitting 8% for the first time since 2000, a 23-year high.

Earnings season on Wall Street is seeing some grey clouds in an otherwise sunny profit reporting season, with 78% of earnings reports beating expectations.

Wednesday's biggest reporting losers include United Airlines which slid nearly 10% and Morgan Stanely which fell nearly 7% in its single worst trading day since 2020.

Headline earnings reporters for the rest of the day will be Netflix and Tesla, both of which report after the closing bell.

The US is facing political jitters as the US Congress remains frozen as US politicians struggle to elect a new Speaker of the House after previous Speaker Kevin McCarthy was ejected from the position by his own political party. Two failed votes in as many days leaves Congress hamstrung and unable to perform governance duties, and investors have one eye turned to the temporary funding stopgap that was delivered in the eleventh hour of the last funding standoff that froze Congress just a few weeks ago.

The temporary government funding measure is set to expire in only four weeks.

S&P Technical Outlook

The S&P's failed jumpstart into the 50-day Simple Moving Average (SMA) has the equity index set to face the $4,300 major handle just below current price action, and an extended decline will see the S&P taking a run at the 200-day SMA just past the $4,250 key level, which the index last rebounded from in early October.

on the top side, a descending trendline from July's peak of $4,607 is firming up, with lower highs firming up a short-side trend pattern in the medium-term.

S&P Daily Chart

S&P Technical Levels

- EUR/JPY declined to a daily low of 157.70, near the 20-day SMA and then closed at 157.96.

- Despite the correction, indicators suggest that the bulls have a slight upperhand in the short term.

- The 100 and 20-day SMAs seem to be converging to perform a bullish cross.

The EUR/JPY’s buyers seem to be taking profits on Wednesday, and the cross initially declined to a low of 157.70 and then closed at 157.86, holding above the key level of the 20-day Simple Moving Average (SMA). In line with that, indicators point towards a neutral to bullish outlook as the bulls need gather momentum as the cross contains sideways trade since the beginning of September.

The Relative Strength Index (RSI) on the daily chart printed a negative slope, still above its midline, while the Moving Average Convergence (MACD) exhibits decreasing green bars, suggesting that the bulls are struggling to gather momentum. On the four-hour chart, the RSI declined to negative territory. At the same time, the MACD is seen laying out flat red bars, which suggests that there is no evidence of strong bullish momentum in the shorter time frames and that the cross may consolidate Monday and Tuesday’s gains in the next sessions while traders await fresh fundamental catalysts to set their short-term trajectory. Back to the daily chart, the pair is above the 20,100 and 200-day Simple Moving Averages (SMA), which suggests that the bulls are in command on the broader scale.

Support levels: 157.50 (20-day SMA), 157.00, 156.50.

Resistance levels: 158.50, 159.00, 159.50.

EUR/JPY Daily Chart

-638332624476997907.png)

- Rising geopolitical tensions in the Middle East contribute to risk aversion, weighing on the Aussie Dollar.

- The AUD/JPY formed a dark-cloud-cover chart pattern indicating potential bearish momentum.

- Immediate support is identified at the top of the Ichimoku Cloud (Kumo) at 94.30, followed by the psychological level of 94.00.

AUD/JPY extends its losses for two straight days as Thursday’s Asian session begins, with the pair exchanging hands at around 94.94. On Wednesday, risk aversion dented demand for Aussie Dollars (AUD) amid growing tensions in the Middle East conflict, as the cross-pair printed losses of 0.36%.

From a technical standpoint, the AUD/JPY is trading sideways, trapped within the 94.00/95.00 range, unable to crack the top or the bottom. Price action in the last couple of days printed a dark-cloud-cover chart pattern, suggesting that further downside is expected.

In that case, AUD/JPY first support emerges at the Ichimoku Cloud (Kumo) fop at 94.30 before slumping to 94.00. Once those two levels are cleared, the cross-pair next support emerges at the October 3 swing low of 93.01, before dropping towards the July 28 swing low of 91.97.

On the flip side, AUD/JPY buyers must reclaim the 95.00 mark, if they would like to challenge the September 29 swing high of 96.92, before challenging the year-to-date (YTD) high of 97.67.

AUD/JPY Price Action – Daily chart

AUD/JPY Key Technical Levels

- The AUD/USD is backsliding into 0.6335 after Wednesday markets saw risk appetite evaporate.

- Investor confidence is souring as the Gaza conflict weighs on global sentiment and the US barrels towards yet another debt deadline standoff.

- Aussie traders will be looking ahead to Thursday's Australia labor data with an appearance from Fed Chair Powell on the cards.

The AUD/USD saw an early climb into a daily high of 0.6393 following hawkish, infaltion-fighting comments from Reserve Bank of Australia (RBA) Governor Michelle Bullock early Wednesday, but the bidding momentum would prove to be short-lived as broader market sentiment took a turn for the bearish, sending the AUD/USD back into 0.6330 as investors shake out of risk assets.

RBA’s Bullock: A bit more worried about the inflation impact from supply shocks

The Gaza Strip conflict continues to escalate after a rocket attack on a hospital in Gaza killed over 500 civilians, and both Israel and Hamas have exchanged accusatory barbs for the building explosion.

The US Congress remains hamstrung after two votes in as many days failed to establish a new Speaker of the House after previous Speaker Kevin McCarthy was dumped from the position by his own Republican party. Gridlock on selecting a new Speaker after two weeks of Congressional inactivity on governance duties sees investors concerned that the US could be racing into yet another funding partisan battle after the last one saw only a temporary stopgap funding measure, which is set to expire in four weeks' time.

US Treasuries are climbing into highs over a decade old, with the 10-year T-note hitting 4.928% on Wednesday, its highest since early 2007.

Forex Today: Gold jumps despite Dollar strength, focus turns to Australian jobs and Powell

Thursday will bring a fresh round of Australian Jobs figures, with the Aussie Unemployment Rate expected to hold at 3.7% for September, while investors will be looking for the Employment Change to add at least 20K jobs for the month, compared to August's 64.9K jobs addition.

On the US side, Initial Jobless Claims are forecast to tick slightly higher, with 212K new claimants expected for the week into October 13th compared to the previous week's 209K.

Federal Reserve (Fed) Chairman Jerome Powell is slated to give a speech later on Thursday. Fed Chair Powell will be delivering talking points at the Economic Club of New York's Luncheon.

AUD/USD Technical Outlook

The Aussie's bearish tip-over on Wednesday reaffirms the AUD/USD's downside bias, with the pair routinely facing rejection from a descending 50-day Simple Moving Average (SMA), which is currently painting into the 0.6400 handle on daily candlesticks.

The Aussie remains firmly in bear country for 2023, trading far below the 200-day SMA near 0.6650.

With the AUD/USD's 2023 lows sitting close by at 0.6285, a bearish continuation will see the pair pushed even deeper into red for the year, and the Aussie is trading into incredibly dark waters, down around 11.5% from the year's highs of 0.7157 set back in February.

AUD/USD Daily Chart

AUD/USD Technical Levels

The key event during the Asian session is the Australian employment report. Japan will release trade data, and China will update house prices. Later in the day, market participants will closely monitor the US Jobless Claims and the Philly Fed index. Federal Reserve Chair Powell is due to speak.

Here is what you need to know on Thursday, October 19:

The positive market sentiment that followed bright economic data from China was offset by rising tensions in the Middle East, higher yields and crude oil prices. The Dow Jones lost 0.98%, and the Nasdaq declined by 1.62%. Meanwhile, the price of WTI crude oil rose by 1.70%.

The risk-off sentiment and stronger US yields pushed the US Dollar higher. The US Dollar Index (DXY) rose 0.35%, surpassing the 106.50 level. The 10-year Treasury yield climbed to 4.92%, reaching its highest level since 2007. Federal Reserve Chair Powell is scheduled to speak at the Economic Club of New York on Thursday, and his comments will be closely watched.

On Wednesday, US housing market data showed mixed figures. Building Permits dropped in September to 1.475 million, better than the expected 1.45 million, while Housing Starts rebounded to 1.35 million, slightly below the market consensus of 1.38 million. The Beige Book noted that economic activity had "little to no change" during September and early October.

Upcoming US data on Thursday includes Existing Home Sales, the Philly Fed index, and the weekly Jobless Claims report. Further signs of a robust economy and a tight labor market could keep the US Dollar in demand.

Gold initially jumped and reached $1,963, its highest level in two months, despite the moves in the bond market. The yellow metal later pulled back and settled around $1,950.

EUR/USD failed once again to rise above 1.0600 and turned to the downside, finding support around 1.0530. Risks remain tilted to the downside, but consolidation could persist if the pair remains above 1.0520.

The Pound initially rose following a higher-than-expected UK inflation reading but later gave up all its gains. GBP/USD is trading dangerously close to the key support area around 1.2120.

USD/JPY posted its highest daily close since October of last year, slightly below the 150.00 area. A rally above that area could lead to intervention from Japanese authorities, triggering volatility.

AUD/USD was rejected from above the 20-day Simple Moving Average (SMA) and reversed course near 0.6400, falling towards 0.6330. The key support level stands at 0.6285 (October lows). Australia will release the September employment report early on Thursday.

The New Zealand Dollar (NZD) lagged once again. The technical outlook for NZD/USD points to further losses, as it posted the lowest daily close in almost a year, below 0.5860.

The Canadian Dollar (CAD) did not benefit from the rally in crude oil prices. USD/CAD rose above 1.3700 and closed above it, leaving room for further upside potential.

Like this article? Help us with some feedback by answering this survey:

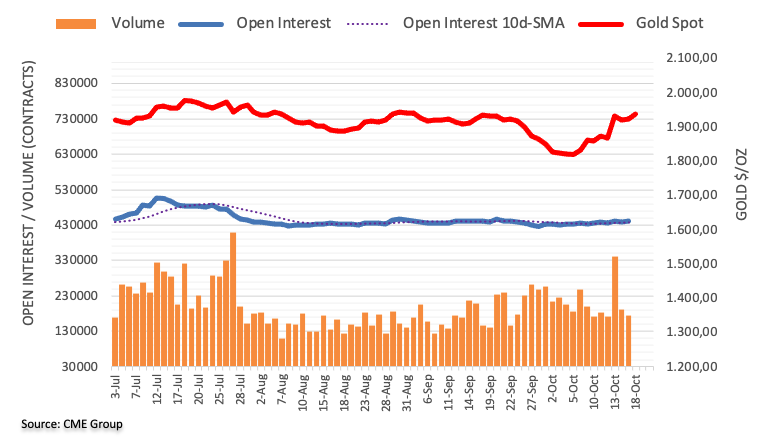

- Spot Gold climbed further on Wednesday, extending to $1,960 as investors reversed direction.

- Global geopolitical tensions and political instability in the US are seeing market jitters rattle risk assets.

- US Treasury yields continue to climb as investor's nerves shake out, 10-year hits highest yield since 2007.

Gold bids accelerated recent gains, climbing into the $1,960 handle as tensions over the Gaza Strip conflict and a hamstrung US Congress lacking a Speaker of the House give investors cause to pause, sending markets flowing back into safe havens.

XAU/USD is settling near $1,950 heading into the market close and remains up over 1.35% for Wednesday.

Gaza conflict, paralyzed US Congress weigh on risk appetite

An explosion rocked a Gaza hospital this week leaving over 500 civilians dead that were seeking refuge in the building as the Israel-Hamas conflict continues to escalate; Hamas claimed Israel had performed a targeted air strike on the building, while Israel blames a runaway errant Hamas rocket for the building demolition.

Market participants remain uneasy about the Gaza escalation after Iranian Finance Minister Ehsan Khandouzi recently stated that Iran would not remain a passive observer if "crimes in Gaza continue", aiming criticism at Israel and the US by extension.

On the US side, the US Congress remains hamstrung and frozen on federal action as Congress failed to elect a new Speaker of the House, with two votes in two days failing to elect a successor after the former Speaker of the House Kevin McCarthy was ousted from his position by his own Republican party two weeks ago.

The deadline on a temporary funding stopgap is set to unwind in four weeks' time, and investors are growing increasingly agitated as Congress continues to float dead in the water, unable to select a new Congressional speaker. US Treasury yields have climbed, with the 10-year T-note hitting a high of 4.928% on Wednesday.

XAU/USD Technical Outlook

Spot Gold extended over the 200-day Simple Moving Average for Wednesday while also breaking through the descending trendline from May's swing high of $2,079.76.

XAU/USD has climbed rapidly in recent weeks, lifting over 7.5% from early October's swing low into $1,810.

Gold bulls will be looking to turn old resistance into support from the $1,940 level, while the $1,900 major psychological handle will hopefully turn into a major bidding platform now that XAU/USD has decisively climbed over the level.

XAU/USD Daily Chart

XAU/USD Technical Levels

- GBP/JPY struggles to surpass the previous weekly high due to geopolitical tensions and a shift to safe-haven assets.

- Support lies at the intersection of the Kumo's bottom and the Kijun-Sen at 181.20.

- Resistance is found at 183.00, with the next hurdle at the October 12 high of 183.81.

The GBP/JPY consolidates inside the Ichimoku Cloud (Kumo), registering modest losses of 0.25% after failing to crack the previous weekly high of 182.80 amid a deteriorated risk appetite. Geopolitical reasons and flight to safe-haven peers weighed on the Pound Sterling (GBP), extending its losses for two consecutive days against the Japanese Yen (JPY), exchanging hands at around 182.03, slightly below the Tenkan-Sen line.

The daily chart portrays the pair as consolidated after diving towards the October 3 swing low of 178.03, with prices climbing to the 183.80 area before settling at current exchange rates. The cross-pair trades sideways, though slightly bearish tilted, as the GBP/JPY hovers near the bottom of the Kumo, which, once broken, could exacerbate an acceleration of the downtrend.

The first support is seen at the confluence of the bottom of the Kumo and the Kijun-Sen at 181.20. If that level is taken, the GBP/JPY would dive past the next support at 181.00, with sellers eyeing the October 3 daily low of 178.03 before setting their sights on the July 28 swing low of 176.30.

On the other hand, if GBP/JPY climbs above 183.00, that would expose the October 12 high at 183.81 before buyers challenge the top of the Kumo at around 184.20/35.

GBP/JPY Price Action – Daily chart

GBP/JPY Technical Levels

- USD/SEK records more than 1% gains rising above the 20-day SMA around 11.025.

- The USD is getting traction amid risk-off flows.

- The Fed Beige Book report didn’t report any relevant insights on the US economic activity.

- Despite rising inflation, markets discount low odds of further hikes by Riksbank.

On Wednesday, the USD/SEK rose above the 20-day Simple Moving Average (SMA) for the first time since September 25, driven by a broad-based US Dollar strength. Rising hawkish bets on the Federal Reserve (Fed) and negative market sentiment are the main drivers of the green currency’s strength.

Recent economic activity figures revealed that the US economy is holding strong despite the Federal Reserve's (Fed) contractionary monetary policy, and as the bank stated that is stance is data-dependant, the odds of a 25 hike in the December meeting rose to nearly 40% after strong Retail Sales and Industrial Production figures revealed on Tuesday. Those hawkish bets could also explain the increase in US Treasury bond yields, which increased to multi-week highs and also contributed to the upward movements of the USD.

On Wednesday, the Fed’s Beige book report on the US economic activity revealed no significant changes in the outlook since the September report and described the economy as “stable”.

On the SEK’s side, the Swedish Consumer Price Index (CPI) rose to 6.5% YoY, higher than the expected 6.3% but lower than the previous 7.5% reading. As for now, markets are expecting that the Riksbank won’t hike again in 2023 after September’s increase and analysts from Commerzbank Research stated that there is no upside for the SEK for the rest of the year as the Swedish bank is not acting decisively enough to combat inflation.

USD/SEK Levels to watch

Analysing the daily chart, USD/SEK exhibits signs of bulls recovering momentum. The Relative Strength Index (RSI) jumped above 50, while the Moving Average Convergence (MACD) presents decreasing red bars. Plus, the pair is now above the 20,100 and 200-day Simple Moving Averages (SMA), indicating that on the broader scale, the bulls are in command.

Support levels: 10.993 (20-day SMA),10.900,10.808 (100-day SMA).

Resistance levels: 11.055,11.105, 11.158.

USD/SEK Daily Chart

-638332542433182946.png)

- XAG/USD trades at around $22.85, a modest gain of 0.29%.

- Supports are identified at the psychological level of $22.50, the 50-DMA at $22.85, and the 20-DMA at $22.21.

- Immediate resistance lies at the 200-DMA at $23.31, with a key hurdle at the recent cycle high of $23.76.

Silver price (XAG/USD) clings to gains although US Treasury bond yields continued to rise. However, the white-metal, failed to reclaim the 200-day moving average (DMA), leaving Silver exposed to selling pressure, but at the time of writing, exchanges hands at $22.85, gaining 0.29%.

The daily chart portrays XAG/USD as neutral-downward biased, as the market structure registers lower highs and lower lows. Even though Silver has rallied from around October lows of $20.65, the ongoing rally is an impulse, which needs to clear the latest cycle high of $23.76. to pave the way for a bullish resumption.

Consequently, as XAG/USD’s downtrend remains in place, the current uptrend offers sellers a better entry price. Silver’s first support would be the psychological $22.50 figure after the white metal dropped below the 50=DMA at $22.85. Once those two areas are cleared, the next support would emerge at the 20-DMA at $22.21, followed by the $22.00 mark. Conversely, if XAG/USD climbs past the $23.00 figure, a challenge on the 200-DMA at $23.31 is on the cards.

XAG/USD Price Action – Daily chart

XAG/USD Technical Levels

- The EUR/GBP is strung along the midrange after dipping into a low of 0.8660 on Wednesday.

- The Euro's consolidation range against the Pound Sterling remains intact as the 0.8700 handle proves elusive.

- UK inflation held over expectations, ECB's Lagarde notes high wages.

The EUR/GBP declined from the day's opening bids of 0.8680 into an intraday low of 0.8660 before rebounding into 0.8670 as the Euro (EUR) twists into the middle against the Pound Sterling (GBP).

Uk Consumer Price Index (CPI) inflation came in above expectations, holding steady at 6.7% in for the year into September versus the forecast decline to 6.5%. Month-on-month CPI inflation saw a slight uptick into 0.5% from August's 0.4%.

UK Annualized Core CPI inflation (excluding the volatility of food and energies prices) likewise came in above expectancy, with September's figure printing at 6.1% compared to August's 6.2%, against the median forecast of 6.0%.

On the EU side, the Harmonized Index of Consumer Prices (HICP) for September printed as-expected, confirming the previous number and printing at 0.3%.

European Central Bank (ECB) President Christine Lagarde hit newswires on Wednesday, noting that underlying inflation remains quite strong, with wage growth remaining "historically high". Despite the inflationary concerns, ECB President Lagarde noted that worsening demand remains a critical downside risk.

ECB’s Lagarde: Underlying inflation is still strong, wage growth is historically high

EUR/GBP Technical Outlook

The EUR/GBP pair is drifting towards the 200-day Simple Moving Average (SMA) near the top-end of medium-term consolidation at the 0.8700 handle, and the major price level is set to remain a significant cap for the Euro-Pound pairing if bidders aren't able to extend from the last bullish bounce from 0.8620.

The EUR/GBP initially fell into 0.8525 in June, and has struggled to develop a meaningful trend ever since, bouncing between 0.8525 and 0.8700.

A bullish trend correction will see the EUR/GBP set for a challenge of late April's swing high into 0.8850.

EUR/GBP Daily Chart

EUR/GBP Technical Levels

- GBP/USD trades at 1.2166, down modestly after reaching a daily high of 1.2211.

- Escalating tensions between Hamas and Israel, with Iran's intensified rhetoric, drive risk aversion, weighing on the Pound.

- Despite higher UK inflation for September ar 6.7%, odds for a BoE rate hike in early November remain subdued.

The Pound Sterling (GBP) trimmed some of its earlier losses versus the US Dollar (USD) but remained on the defensive, registering modest losses of 0.%, as the GBP/USD exchanges hands at 1.2166 after hitting a daily high of 1.2211.

Pound Sterling on the defensive despite UK inflation surpassing estimates

Risk aversion is taking its toll on risk-perceived currencies like the British Pound. Tensions between Hamas and Israel increased after a blast hit a hospital in Gaza, with Palestinians blaming the latter. Consequently, Iran escalated its rhetoric despite US President Joe Biden clarifying that it was not Israel behind the attack.

Despite solid economic data in the US, including positive Retail Sales and Industrial Production figures, the recent rhetoric from US Federal Reserve (Fed) officials has remained dovish, even with inflation running nearly twice the Fed's target. Today's US data presented a mixed picture, with September's Housing Starts rising by 7%, surpassing expectations, while Building Permits declined by -4.4%.

Given these developments, the money market has not priced a 25-basis-point rate hike for November. Instead, the focus appears to be on the January meeting, with the odds of a rate hike standing at 51.65%.

In the meantime, the UK economic docket revealed that inflation in September was higher than expected, hitting 6.7% YoY, with estimates of 6.6%. Despite that, interest rate probabilities for the Bank of England (BoE) remain lower for a rate hike in early November after the BoE kept rates unchanged in September.

GBP/USD Price Analysis: Technical outlook

From a technical perspective, the GBP/USD is neutral to a downward bias and would accelerate its downtrend if it drops below the latest swing low of 1.2122, with sellers eyeing a test of October’s swing low of 1.2037. The 1.2000 figure would be up for grabs if the pair clears that level. On the upside, buyers must reclaim the October 13 high of 1.2225 to reclaim 1.2300.

According to Federal Reserve’s Beige Book, “most Districts indicated little to no change in economic activity since the September report.” The report noted that “the near-term outlook for the economy was generally described as stable or having slightly weaker growth.”

Key Takeaways from the Beige Book:

Most Districts indicated little to no change in economic activity since the September report.

Consumer spending was mixed, especially among general retailers and auto dealers, due to differences in prices and product offerings.

Banking contacts reported slight to modest declines in loan demand. Consumer credit quality was generally described as stable or healthy, with delinquency rates still historically low but slightly increasing.

Real estate conditions were little changed and the inventory of homes for sale remained low.

Manufacturing activity was mixed, although contacts across multiple Districts noted an improving outlook for the sector.

The near-term outlook for the economy was generally described as stable or having slightly weaker growth.

Expectations of firms for which the holiday shopping season is an important driver of sales were mixed.

Labor market tightness continued to ease across the nation. Most Districts reported slight to moderate increases in overall employment, and firms were hiring less urgently.

Prices continued to increase at a modest pace overall. Districts noted that input cost increases have slowed or stabilized for manufacturers but continue to rise for services sector firms. Increases in fuel costs, wages, and insurance contributed to growth in prices across Districts.

Overall, firms expect prices to increase the next few quarters, but at a slower rate than the previous few quarters

Market reaction

The US Dollar Index remained steady after the Federal Reserve's Beige Book release, hovering around 106.40, up 0.20% for the day. EUR/USD held slightly below 1.0550.

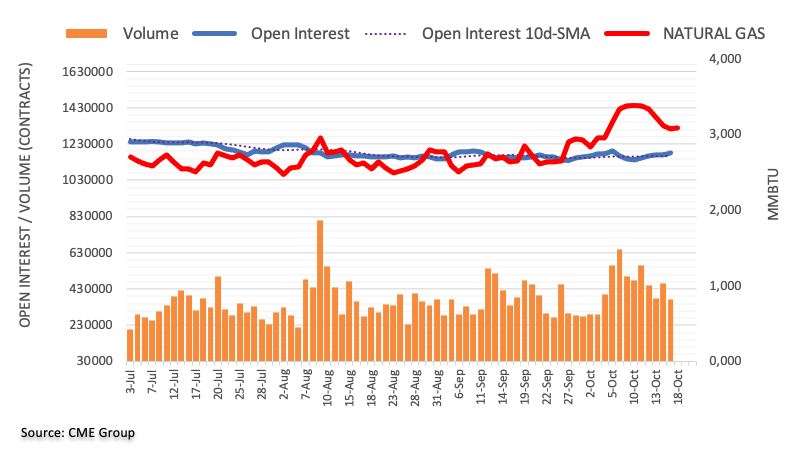

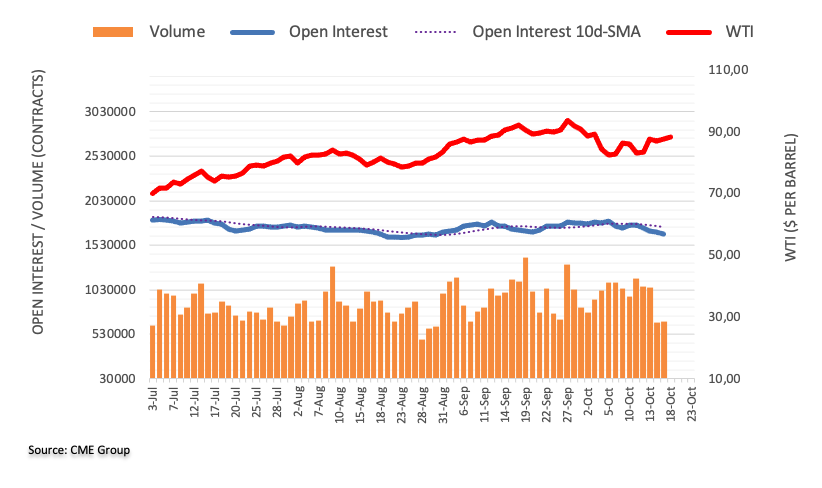

- WTI Crude Oil is seeing green for Wednesday despite broader market sentiment taking a hit.

- US Crude prices initially rose nearly $2/barrel on the day before broad-market risk aversion restrained prices.

- Middle East geopolitical tensions from the Gaza Strip escalation continue to weigh on energies.

West Texas Intermediary (WTI) Crude Oil prices are seeing further gains on Wednesday despite global markets seeing a broad turnaround into safe havens.

Following a rocket strike on a Gaza hospital that left over 500 civilians dead and both Israel and Hamas blaming the other side for devastating attack, investors are getting cold feet once more as geopolitical tensions surrounding the Gaza Strip conflict continue to draw taut.

Middle East tensions, US crude supply drawdown keeping barrel bids pushed into the green

As stability in Gaza continues to deteriorate, markets are increasingly concerned that tensions could rise to the point that the altercation could spill over into knock-on political disputes between the US and neighboring countries to the region. The nearby Strait of Hormuz, a major global energy supply chokepoint that sees a fifth of all global crude shipments, could see negative impact if geopolitical tensions continue to mount.

Adding to Crude Oil price pressures, US Crude Oil inventories reported a steeper-than-expected drawdown on Wednesday, with the Energy Information Administration's (EIA) barrel count seeing a decline of 4.491M barrels for the week into October 13th, much steeper than the forecast -0.3M drawdown and eating significantly into the previous week's 10.176M barrel buildup.

WTI Technical Outlook

WTI Crude Oil barrels touched a fresh daily high of $88.50 before slipping back into the $87.00 neighborhood as risk aversion weighs on markets, but Middle East tensions are keeping Crude prices bid into the green for Wednesday.

Daily candlesticks are struggling to shrug off the 50-day Simple Moving Average (SMA) currently parked near $85.13, and Wednesday's upside action sees WTI knocking on the underside of a rising trendline from late June's swing low into $67.14.

Despite WTI recently slipping from 2023's highs of $93.98 set back in September, Crude Oil remains in a bullish stance, with prices facing a bullish extension from the last turnaround from the $82.00 handle.

WTI Daily Chart

WTI Technical Levels

- USD/CHF declined to it lowest level since September 20, to a daily low of 0.8957.

- The Swiss currency is the best performer in the session.

- The USD holds its foot after mixed Housing market figures, eyes on the Fed’s Beige book.

In Wednesday’s session, the USD/CHF declined to its lowest level in over a month, below 0.8957 and then settled around 0.8970. On the one hand, the CHF is the top performer of the session, trading with gains against the EUR, GBP, JPY and USD. On the other hand, the green currency gained some ground ahead of the anticipated Federal Reserve (Fed) Beige book report and after mixed Housing data. On the Swiss side, nothing relevant was released during the European session.

The US Dollar measured by the DXY Index edged higher, reaching around 106.40, reflecting a modest 0.20% increase for the day. On the data front, Building Permits for September surpassed expectations at 1.475M, while Housing Starts fell short of expectations at 1.358M, showing a mixed housing scenario.

The upcoming release of the Fed's Beige Book is anticipated to offer a clearer perspective on US economic activity and labour market conditions, important for investors to continue placing their bets for the next Fed’s decisions. Meanwhile, US yields are observing a slight uptick, with the 2-year, 5-year, and 10-year rates climbing to 5.20%, 4.87%, and 4.86%, respectively, showing that markets may be gearing up for one last hike by the Fed in 2023. According to the CME FedWatch tool, the probability of a 25 basis points hike during the December meeting has risen to approximately 42%, while a pause in November is near to be priced in.

USD/CHF Levels to watch

The daily chart analysis indicates a neutral to bearish outlook for USD/CHF, as the bears show signs of taking control but still face challenges ahead.The Relative Strength Index (RSI) points south below its middle point, while the Moving Average Convergence (MACD) histogram exhibits larger red bars. Furthermore, the pair is below the 20 and 200-day Simple Moving Averages (SMAs), but above the 100-day SMA, implying that the bears have more work to do to confirm a bearish trend.

Support levels: 0.8950, 0.8930, 0.8900 (100-day SMA).

Resistance levels: 0.9015 (200-day SMA), 0.9040, 0.9070.

USD/CHF Daily Chart

-638332479298321915.png)

- The EUR/USD is extending its decline for Wednesday, backsliding into 1.0525.

- the EUR failed to complete a drive into the 1.0600 handle as market sentiment turns broadly lower.

- US Treasury yields are back on the rise, with the 10-year T-note yield at its highest price since 2007.

The EUR/USD kicked off Wednesday trading looking to reclaim the 1.0600 handle in the early sessions, but a resurgence of risk-off market flows has sent the Euro (EUR) back down against the US Dollar (USD), knocking the floor out of yesterday's low and testing the waters near 1.0520.

The pair is currently trading back up into 1.0550 in a relief pullback, but overall market sentiment continues to lean bearish and upside momentum is likely to remain limited.

Global tensions are rising as the Gaza Strip conflict between Israel and Hamas continues to escalate; the latest rocket strike on a hospital in Gaza sees one of the largest civilian death tolls in recent history, with over 500 shelter-seekers dead who were looking to take refuge in the hospital before a rocket struck the building. Both Israel and Hamas have blamed the other side for the building strike.

Hamstrung US Congress over failed Speaker vote making investors uneasy as funding crunch looms

In the US, political uncertainty is on the rise as the US Congress fails to select a new Speaker of the House, with two votes in two days failing to secure a nominee. With the US Congress paralyzed after the Republican majority ousted their own Speaker, the US is only 30 days away from the end of a short-term funding stopgap that was secured in the eleventh hour earlier this month.

With the US barreling towards another partisan funding clash in mid-November, uncertainty is on the rise and uneasy investors are pulling back into safe havens, propping up the USD and sending US Treasury yields into multi-year highs, with the 10-year Treasury hitting 4.928% on Wednesday, its highest yield since 2007.

EU Index of Consumer Prices (CPI) inflation figures on Wednesday came in as-expected, with September's CPI inflation coming in at 0.3%, and the European Central Bank (ECB) President Christine Lagarde noting that underlying inflation remains strong, with wage growth still "historically high".

ECB’s Lagarde: Underlying inflation is still strong, wage growth is historically high

Next up on the economic calendar will be US Initial Jobless Claims on Thursday, with investors forecasting 212K new jobless claimants for the week into October 13th, compared to 209K for the previous week.

US Federal Reserve (Fed) Chairman Jerome Powell will also be giving a speech tomorrow. Fed Chair Powell will be speaking at the Economic Club of New York Luncheon around 16:00 GMT Thursday.

EUR/USD Technical Outlook

The EUR/USD is continuing to face rejection from a firm descending trendline drawn from July's swing high at 1.1275. The pair is struggling to maintain a bullish bounce from the last major swing low into 1.0450, and a bearish continuation will see the pair set to make a new 10-month low.

Near-term resistance is coming from a bearish 50-day Simple Moving Average (SMA), currently descending into the 1.0700 chart region, while the 200-day SMA is beginning to rollover into a bearish pattern from just north of the 1.0800 handle.

EUR/USD Daily Chart

EUR/USD Technical Levels

- Geopolitical tensions escalate as Iran intensifies rhetoric against Israel, leading to heightened risk aversion.

- Mixed US data: Housing Starts rose by 7% in September, while Building Permits declined by 4.4%.

- Despite elevated inflation in New Zealand, the RBNZ is expected to maintain its current monetary policy stance..

The New Zealand Dollar (NZD) plunged to a new year-to-date (YTD) low of 0.5851 against the US Dollar (USD) on Wednesday, spurred by risk aversion and the jump in US Treasury bond yields. Geopolitical tensions underpin the Greenback to the detriment of high-beta currencies, like the Kiwi Dollar (NZD). The NZD/USD exchanges hands at around 0.5855, down 0.69%.

Kiwi Dollar faces selling pressure as risk aversion dominates

The market mood remains fragile as Wall Street registers losses. US President Biden's visit to the Middle East has failed to pour cold water into a conflict that could escalate further, as Iran’s intensified its rhetoric against Israel, as reported by Bloomberg. An explosion at a Gaza hospital re-ignited fears amongst traders of a possible escalation as global bond yields soared.

On Tuesday, US Retail Sales and Industrial Production portrayed the economy as solid, though failed to change the latest US Federal Reserve (Fed) officials dovish rhetoric, despite inflation being almost twice the Fed’s target. Today, US data was mixed, with September’s Housing Starts climbing 7%, exceeding forecasts, while Building Permits tanked -4.4%.

Given the backdrop, we could’ve expected a repricing for a hawkish Fed. Still, money market futures have disregarded a 25-bps hike for November, while December and January remain on, with the latter odds at 51.65%.

On the New Zealand front, the last Consumer Price Index (CPI) report revealed that inflation remains elevated, suggesting the Reserve Bank of New Zealand (RBNZ) would stick to its higher for a longer posture. Even though Wednesday’s Chinese data showed the economy is growing faster than foreseen, sentiment deterioration triggered outflows from risk-perceived currencies toward safe-haven peers.

NZD/USD Price Analysis: Technical outlook

The NZD/USD falling to a new YTD low opened the door for further losses, with first support seen last year’s November 22 swing low of 0.5840. A breach of the latter would expose the November 3 daily low of 0.5740, followed by October 21, 2022, a swing low of 0.5599. On the other hand, if NZD/USD stays above 0.5900, that would keep buyers hopeful of reaching the 50-day moving average (DMA) at 0.5937.

- The Canadian Dollar is falling back into familiar lows on Wednesday as investors pull up stakes.

- Canada Housing Starts came in better than expected, but risk-off flows are dominating.

- Thin calendar docket for the CAD until Friday’s Retail Sales.

The Canadian Dollar (CAD) is falling back in the American market session as risk appetite takes a turn south, sending investors back into the US Dollar (USD) and taking the USD/CAD back up the charts.

Canada Housing Starts managed to eke out a better-than-expected print, with US housing data coming in mixed, but overall market sentiment has turned risk-off mid-week, and the US Dollar is rising across the board, sending the Loonie lower in lockstep with Crude Oil prices that are declining back into the day’s opening bids.

Daily Digest Market Movers: Canadian Dollar reverses course at the midway point as risk appetite turns tail

- Canadian Housing Starts beat expectations, showing 270.5 thousand additional homes begin constructed over the year into September.

- The data easily cleared the forecast 240K, and stepped over the last reading of 250.4K (revised downwards from 253K).

- US housing data landed with mixed results, with Building Permits beating expectations but Housing Starts flubbing the forecast.

- The US issued 1.475M new building permits in September, just above the 1.45M forecast but less than August’s 1.541M (revised down from 1.543M).

- US Housing Starts disappointed markets, with 1.358M houses or apartment units beginning construction in September, less than the expected 1.38M, but still an improvement over August’s 1.269M (revised down from 1.283M).

- Thursday still sees US Initial Jobless Claims, as well as a slew of speeches from Federal Reserve (Fed) officials, including Fed Chair Jerome Powell at 16:00 GMT tomorrow.

- Crude Oil saw bidding during the early Wednesday trading session, but the American market window is seeing investors hesitate, and Oil prices are falling back to where they started.

- Global geopolitical tensions over the Israel-Hamas conflict continue to weigh on investor risk appetite.

- The US is also suffering from its own homegrown political uncertainty as the US Government struggles to replace its House Speaker who was ejected by his own party.

- US Treasury yields have hit yet another high, with the US 10-year yield at its highest yield in seventeen years near 4.92%.

Technical Analysis: Canadian Dollar falls back as traders pile back into the Greenback

USD/CAD is breaking past the 1.3700 handle on Wednesday, testing into swing high prices that have become familiar territory in recent weeks. The pair has been in a massive range for a whole year, oscillating between highs just short of 1.4000 and lows in the 1.31s. It is once again approaching the range highs.

In fact the pair is wrestling with a major trendline at around 1.3685, drawn by connecting the October 2022 and March 2023 highs, and this is likely to present tough overhead resistance. Ideally a decisive break is required to definitively put this ceiling in the rear-view mirror.

Such a break would be characterized by a longer-than-average green weekly candle breaking cleanly through the resistance line, or three successive green weekly bars.

Despite the sideways primary trend, the intermediate and short-term trends are more bullish suggesting longs have their backs to the wind. This lends a bias to more upside, and if it were not for the major resistance line there would be a green light signaling ‘go’ – as it is it could prove a spoiler.

USD/CAD Weekly Chart

Canadian Dollar FAQs

What key factors drive the Canadian Dollar?

The key factors driving the Canadian Dollar (CAD) are the level of interest rates set by the Bank of Canada (BoC), the price of Oil, Canada’s largest export, the health of its economy, inflation and the Trade Balance, which is the difference between the value of Canada’s exports versus its imports. Other factors include market sentiment – whether investors are taking on more risky assets (risk-on) or seeking safe-havens (risk-off) – with risk-on being CAD-positive. As its largest trading partner, the health of the US economy is also a key factor influencing the Canadian Dollar.

How do the decisions of the Bank of Canada impact the Canadian Dollar?

The Bank of Canada (BoC) has a significant influence on the Canadian Dollar by setting the level of interest rates that banks can lend to one another. This influences the level of interest rates for everyone. The main goal of the BoC is to maintain inflation at 1-3% by adjusting interest rates up or down. Relatively higher interest rates tend to be positive for the CAD. The Bank of Canada can also use quantitative easing and tightening to influence credit conditions, with the former CAD-negative and the latter CAD-positive.

How does the price of Oil impact the Canadian Dollar?

The price of Oil is a key factor impacting the value of the Canadian Dollar. Petroleum is Canada’s biggest export, so Oil price tends to have an immediate impact on the CAD value. Generally, if Oil price rises CAD also goes up, as aggregate demand for the currency increases. The opposite is the case if the price of Oil falls. Higher Oil prices also tend to result in a greater likelihood of a positive Trade Balance, which is also supportive of the CAD.

How does inflation data impact the value of the Canadian Dollar?

While inflation had always traditionally been thought of as a negative factor for a currency since it lowers the value of money, the opposite has actually been the case in modern times with the relaxation of cross-border capital controls. Higher inflation tends to lead central banks to put up interest rates which attracts more capital inflows from global investors seeking a lucrative place to keep their money. This increases demand for the local currency, which in Canada’s case is the Canadian Dollar.

How does economic data influence the value of the Canadian Dollar?

Macroeconomic data releases gauge the health of the economy and can have an impact on the Canadian Dollar. Indicators such as GDP, Manufacturing and Services PMIs, employment, and consumer sentiment surveys can all influence the direction of the CAD. A strong economy is good for the Canadian Dollar. Not only does it attract more foreign investment but it may encourage the Bank of Canada to put up interest rates, leading to a stronger currency. If economic data is weak, however, the CAD is likely to fall.

- The US Dollar gained traction on Wednesday and trades strong against its main rivals.

- A negative market sentiment made the USD gain interest.

- Building Permits in the US from September came in better than expected. Housing Starts disappointed.

- Investors await Fed’s Beige Book report, to be released later in the session.

The US Dollar (USD) measured by the US Dollar Index (DXY) rose towards 106.60 and seems to be building strong support around the 20-day Simple Moving Average (SMA). Earlier in the session, the US reported mixed housing data and investors await the Federal Reserve’s Beige Book to continue placing their bets on the next monetary policy decisions from the American central bank. Several Fed officials will also be on the wires during the American session.

The United States’ economic activity is holding strong revealed by the latest reports including S&P Global PMIs, Industrial Production and Retail Sales. However, the Beige Book gives a clearer outlook on the current US economic situation through interviews with key business contacts, economists, and market experts gathered by each of the 12 Federal Reserve Districts.

Daily Digest Market Movers: US Dollar gains ground as markets turn cautious ahead of Fed’s Beige Book

- The US Dollar DXY rose near 106.60, seeing 0.40% daily gains.

- Building Permits from the US from September came in at 1.475M, higher than the 1.450M but still lower than the previous 1.541M.

- Housing Starts rose in September but lower than expected, coming in at 1.358M, lower than the 1.380M but above the last reading of 1.269M.

- The Fed’s Beige Book will provide a clearer outlook on the US economic activity and labour market situation.

- In the meantime, US yields are slightly rising, and the 2, 5 and 10-year rates rose to 5.21%, 4.92% and 4.91% respectively.

- According to the CME FedWatch tool, the odds of a 25 bps hike in the December meeting rose to nearly 42%.

Technical analysis: US Dollar Index’s bulls step in and present battle at the 20-day SMA

The DXY index managed to jump back above the 20-day Simple Moving Average (SMA) of 106.25, and technical indicators gained some ground on the daily chart on Wednesday. In the broader context, the index arguably remains in a bullish trend overall, holding above the key 200 and 100-day Simple Moving Averages (SMA).

With the Relative Strength Index (RSI) pointing north above 50 and the Moving Average Convergence Divergence (MACD) printing lower red bars – both are sending mildly supportive signals.

Supports: 106.20 (20-day SMA), 106.00, 105.80.

Resistances:106.70, 107.00, 107.30.

Risk sentiment FAQs

What do the terms"risk-on" and "risk-off" mean when referring to sentiment in financial markets?

In the world of financial jargon the two widely used terms “risk-on” and “risk off'' refer to the level of risk that investors are willing to stomach during the period referenced. In a “risk-on” market, investors are optimistic about the future and more willing to buy risky assets. In a “risk-off” market investors start to ‘play it safe’ because they are worried about the future, and therefore buy less risky assets that are more certain of bringing a return, even if it is relatively modest.

What are the key assets to track to understand risk sentiment dynamics?

Typically, during periods of “risk-on”, stock markets will rise, most commodities – except Gold – will also gain in value, since they benefit from a positive growth outlook. The currencies of nations that are heavy commodity exporters strengthen because of increased demand, and Cryptocurrencies rise. In a “risk-off” market, Bonds go up – especially major government Bonds – Gold shines, and safe-haven currencies such as the Japanese Yen, Swiss Franc and US Dollar all benefit.

Which currencies strengthen when sentiment is "risk-on"?

The Australian Dollar (AUD), the Canadian Dollar (CAD), the New Zealand Dollar (NZD) and minor FX like the Ruble (RUB) and the South African Rand (ZAR), all tend to rise in markets that are “risk-on”. This is because the economies of these currencies are heavily reliant on commodity exports for growth, and commodities tend to rise in price during risk-on periods. This is because investors foresee greater demand for raw materials in the future due to heightened economic activity.

Which currencies strengthen when sentiment is "risk-off"?

The major currencies that tend to rise during periods of “risk-off” are the US Dollar (USD), the Japanese Yen (JPY) and the Swiss Franc (CHF). The US Dollar, because it is the world’s reserve currency, and because in times of crisis investors buy US government debt, which is seen as safe because the largest economy in the world is unlikely to default. The Yen, from increased demand for Japanese government bonds, because a high proportion are held by domestic investors who are unlikely to dump them – even in a crisis. The Swiss Franc, because strict Swiss banking laws offer investors enhanced capital protection.

- USD/JPY trades above 149.80 as US 10-year Treasury bond yield hits its highest since 2007.

- Housing Starts in the US show a 7% increase, while Building Permits see a 4.4% drop.

- Fed officials adopt a neutral stance, reducing the chances of a November rate hike.

- Ex-BoJ Board member Sakurai hints at a potential end to negative rates.

The US Dollar (USD) pares its earlier losses against the Japanese Yen (JPY) and rises above the 149.80 area as the US 10-year Treasury bond yield climbs above 4.913%, its highest level since 2007. Risk aversion dominates the financial markets, though it failed to propel the Yen, as the major gains 0.05%.

US Dollar gains ground vs. Yen as risk-aversion drives the financial markets

US President Joe Biden's visit to Israel aimed to ease tensions within the Middle East spurred an escalation of the rhetoric, with Iran blaming Israel after an explosion at a Gaza hospital, which Biden clarified. Israel's chances of launching a ground attack at Gaza keep traders on edge, as portrayed by US equities posting losses while global bond yields surge.

The latest round of economic data showed that American households remain resilient amid an increase in September’s Retail Sales report. In addition, Industrial Production (IP) expansion portrays the US economy is robust. Wednesday’s economic data in the US revealed that Housing Starts rose 7% in September, while Building Permits plunged 4.4%.

Recent comments from US Federal Reserve officials show they have adopted a more neutral stance, which has diminished the chances for a hike in November, according to the CME FedWatch Tool. Nevertheless, odds for a quarter of a percent increase in January 2024 stand at 51.65%, keeping investors wary of further tightening.

On the Japanese front, an ex-Bank of Japan (BoJ) Board member, Sakurai, said the BoJ could end negative rates before tweaking the Yield Curve Control (YCC). A news article by Bloomberg reported the BoJ would upwardly revise its core inflation forecasts for fiscal years 2023 and 2024.

USD/JPY Technical Levels

It's too soon to tell if more policy rate action is needed, Federal Reserve (Fed) Governor Christopher Waller said on Tuesday and added that they can "wait, watch and see before making definitive moves on policy path," per Reuters.

Key quotes

"More action on policy rate would be needed if demand, economic activity keep up recent pace."

"Past few months' data 'overwhelmingly positive' for fed's employment, inflation goals."

"I will be watching how recently risen longer-term rates evolve and impact financial conditions, economic activity."

"I will be patient in waiting for data to document how spending evolves."

"Time will tell if higher rates dampen business spending, or subsidies and onshoring increase it."

"Anticipating unusually tight labor market to continue loosening, but watching closely."

"Will watch next several inflation reports for clearer indication it's on trajectory to 2%."

Market action

The US Dollar preserves its strength following these comments. At the time of press, the US Dollar Index was up 0.37% on the day at 106.58.

- Mexican Peso exchange rate with the US Dollar registers 0.90% gains, as USD/MXN buyers reclaim 18.00.

- Geopolitical tensions escalate with developments in the Israel-Hamas conflict and the potential involvement of Iran.

- Banxico’s Deputy Governor Mejia: Inflation would hit the central bank’s target in 2025, with the current policy stance.

Mexican Peso (MXN) remains offered early in Wednesday's North American session, particularly against the US Dollar (USD) amid a risk-off impulse spurred by threats of an escalation in the Israel-Hamas conflict. Consequently, Treasury bond yields in the United States (US) rose, lifting yesterday’s battered US Dollar. The USD/MXN trades at 18.18 after bouncing from daily lows of 17.96.

Geopolitics are taking center stage on Wednesday, after US President Joe Biden's visit to Israel. Biden said Israel was not responsible for a blast that hit a Gaza hospital contrary to Palestinian claims. His decision to back Israel’s version of events ignited tensions across the region, with Iran threatening to enter the conflict. The consequent risk aversion boosted the US Dollar, to the detriment of the emerging market currency.

Meanwhile, the lack of data in Mexico’s economic docket put the Bank of Mexico (Banxico) Deputy Governor Omar Mejia in the spotlight. In comments on a podcast, Mejia said the balance of inflation risks has not worsened, reported Reuters. The Banxico official added the current restrictive monetary policy is succeeding at curbing inflation to its target, and that it would reach Banxico’s target by the second quarter of 2025.

The US economic calendar featured Building Permits, which plummeted -4.4% compared to last month’s data, while Housing Starts improved to 7%, from August’s -12.5% plunge.

Daily Digest Market Movers: Mexican Peso sways with market sentiment; USD/MXN reaches 7-day peak

- US Retail Sales in September grew by 0.7% MoM, above forecasts of 0.3%, but trailed upward revised August’s 0.8%.

- Industrial Production rose 0.3% MoM, better than expected, and the previous month's 0.0% reading.

- Mexico’s GDP in 2023 is expected to hit 3.2%, according to the World Bank and the International Monetary Fund.

- New York Fed Empire State Manufacturing Index for October fell to -4.6, higher than forecasts of -7 but worse than September’s 1.9 expansion.

- Philadelphia Fed President Patrick Harker commented the current level of rates kept house buyers on the sideline, highlighting that the Fed is likely done hiking rates.

- According to the Financial Times, Chicago Fed President Austan Goolsbee said the fall in US inflation is not a blip.

- US Inflation expectations for one year rose from 3.2% to 3.8%, while for five years jumped to 3% from 2.8%.

- Mexico's Industrial Production (IP) for August improved by 5.2% YoY, exceeding forecasts of 4.6% and July’s 4.8% increase.

- Monthly, IP in Mexico rose 0.3%, as expected, but trailed the previous 0.5% reading.

- The US Consumer Price Index increased 3.7% YoY in September, unchanged from August but above forecasts of 3.6%.

- US core CPI dipped as expected to 4.1% from 4.3% in August.

- Mexico’s Consumer Price Index (CPI) grew by 4.45% YoY in September, slightly below the 4.47% estimated.

- The core CPI inflation in Mexico stood at a stickier 5.76% YoY, as widely estimated, but has broken below the 6% threshold.

- The Bank of Mexico (Banxico) held rates at 11.25% in September and revised its inflation projections from 3.5% to 3.87% for 2024, above the central bank’s 3% target (plus or minus 1%).

Technical Analysis: Mexican Peso outlook deteriorates, as USD/MXN buyers eye 18.50

The Mexican Peso continues to weaken against the US Dollar after the USD/MXN broke the resistance at 18.10, rallying to a new weekly high of 18.30 before retracing somewhat to current spot prices. Hence, the exotic pair bias remains bullish, and it might test the October 6 high of 18.48 before climbing towards 19.00. On the other hand, if USD/MXN dives below 18.10, traders could expect a test of the psychological 18.00 figure.

Banxico FAQs

What is the Bank of Mexico?

The Bank of Mexico, also known as Banxico, is the country’s central bank. Its mission is to preserve the value of Mexico’s currency, the Mexican Peso (MXN), and to set the monetary policy. To this end, its main objective is to maintain low and stable inflation within target levels – at or close to its target of 3%, the midpoint in a tolerance band of between 2% and 4%.

How does the Bank of Mexico’s monetary policy influence the Mexican Peso?

The main tool of the Banxico to guide monetary policy is by setting interest rates. When inflation is above target, the bank will attempt to tame it by raising rates, making it more expensive for households and businesses to borrow money and thus cooling the economy. Higher interest rates are generally positive for the Mexican Peso (MXN) as they lead to higher yields, making the country a more attractive place for investors. On the contrary, lower interest rates tend to weaken MXN. The rate differential with the USD, or how the Banxico is expected to set interest rates compared with the US Federal Reserve (Fed), is a key factor.

How often does the Bank of Mexico meet during the year?

Banxico meets eight times a year, and its monetary policy is greatly influenced by decisions of the US Federal Reserve (Fed). Therefore, the central bank’s decision-making committee usually gathers a week after the Fed. In doing so, Banxico reacts and sometimes anticipates monetary policy measures set by the Federal Reserve. For example, after the Covid-19 pandemic, before the Fed raised rates, Banxico did it first in an attempt to diminish the chances of a substantial depreciation of the Mexican Peso (MXN) and to prevent capital outflows that could destabilize the country.

The return of volatility to currency markets did not spare the Canadian Dollar from seeing some substantial movement during the month of September into early October. Economists at the National Bank of Canada analyze Loonie’s outlook.

CAD could stabilize and even appreciate in the later part of 2024

Looking at the drivers for the CAD, the short-term yield differential and still high Oil prices should be conducive to a stronger Dollar. That said, the recent risk-off USD appreciation has pushed back most major currencies. The rise of long-term yields hasn’t been accompanied by a significant reduction on the short end of the curve and leaves a lot of questions in regard to where the cycle is headed.

We believe the repricing of hikes for the Bank of Canada is likely overdone and the CAD could see an interval of weakness especially if the economy is to fall in technical recession in the coming quarters.

Our scenario also assumes difficulties for the US economy in the coming months and that should be accompanied by an easing in monetary policy by the Fed. That could set up a stabilization of the Canadian Dollar and even some appreciation in the later part of 2024.

Analysts at Natixis discuss the trends they see for the major currencies.

The Yen exchange rate depends on the BoJ's monetary policy strategy

Persistent inflation in the Eurozone will probably mean that the ECB will keep interest rates fairly high, while the Fed will be able to cut interest rates as disinflation in the US eases. This would favour an appreciation of the Euro against the Dollar, but on the other hand, the US is more attractive than the Eurozone for corporate investment: all things considered, we can expect the Euro to appreciate slightly against the Dollar.

The weak growth in China, due to population ageing, low productivity gains, rising household savings rate and weak investment, is prompting the Chinese authorities to seek a weakening of the Renminbi, hence the ongoing rate cuts in China, which will cause a depreciation of the RMB, albeit with the constraint of not doing too much damage to the financial situation of Chinese banks.

The fact that long-term interest rates remain very low in Japan, due to the yield curve control policy, should lead to a further depreciation of the Yen against the Dollar. This depreciation will end when Dollar interest rates fall and if the BoJ gradually abandons the YCC policy (the cap on 10-year interest rates), a move that is expected to start in 2024.

Economists at ING analyze AUD/USD outlook.

Eyeing new lows

We believe there is still room for another drop in AUD/USD. The new bottom may be 0.61/0.62.

The external environment remains very detrimental for the pair, which should stay under pressure unless the US data narrative flips, and that should not happen in the near term.

Improvements in Chinese sentiment are – if anything at all – very gradual.

AUD/USD – 1M 0.62 3M 0.66 6M 0.69 12M 0.72

See – AUD/USD: Limited upside potential in the coming months – Rabobank

- Silver price seems comfortable above $23.00 as Israel-Palestine conflicts deepen.

- Joe Biden remained ‘loud and clear’ that the US stands with Israel.

- Silver trades in a Rising Channel pattern in which each pullback is considered a buying opportunity.

Silver price (XAG/USD) shifts auction above the crucial resistance of $23.00, which has turned into support for bulls. The white metal strengthens as deepening conflicts between Israel and Palestine have strengthened the appeal for safe-haven assets.

The S&P500 opens on a bearish note amid a cautious market mood. The visit of US President Joe Biden to Israel has escalated fears of an intervention by Iran in the Israel-Palestine tensions. Joe Biden remained ‘loud and clear’ that the US stands with Israel. Also, Biden confirmed that the hospital in Gaza was bombed by Palestine, not by Israel.

Meanwhile, the US Dollar Index (DXY) seems well-supported near 106.00 as the United States economy is resilient despite headwinds of higher interest rates. The US Retail Sales rose by 0.7% in September while investors forecasted a growth by 0.3%. In August, the retail demand rose by 0.9%. US Census Bureau noticed that demand for automobiles and dining out remained upbeat.

For further guidance, investors will focus on the speech from Federal Reserve (Fed) Chair Jerome Powell, which is scheduled for Thursday. The guidance from Jerome Powell on the interest rates will be keenly watched.

Silver technical analysis

Silver trades in a Rising Channel chart pattern in which each pullback is considered as a buying opportunity by the market participants. Upward-sloping 20-period Exponential Moving Average (EMA) at around $23.00 indicates that the short-term trend is bullish. Horizontal resistance is plotted from September 22 high at $23.76.

The Relative Strength Index (RSI) (14) shifts into the bullish range of 60.00-80.00, which warrants more upside ahead.

Silver two-hour chart

-638332353261430669.png)

Economists at Danske Bank stress that labour markets have proven to be surprisingly resilient to the Fed’s tightening mode.

US labour markets defy slowdown expectations

We still think that the Fed is likely to maintain rates at current restrictive levels instead of hiking rates further, especially considering the recent tightening in financial conditions.

But all else equal, while we have called for the first Fed rate cuts already in Q1 2024, the most recent labour market data unequivocally increases the risk of rates staying high for longer than we have anticipated.

- EUR/USD comes under pressure following two daily advances.

- Further weakness could put the 1.0500 region back on the radar.

EUR/USD sets aside part of the positive first half of the week and revisits the 1.0550 region on Wednesday.

In case sellers regain the upper hand, the pair could put the 1.0500 neighbourhood to the test, while the loss of that region should expose a potential decline to the 2023 low at 1.0448 (October 3).

Meanwhile, further losses remain on the table as long as the pair navigates the area below the key 200-day SMA at 1.0820.

EUR/USD daily chart

- AUD/USD looks for further recovery to near 0.6400 on upbeat China data.

- US Biden said that the Pentagon has shown evidence that Israel didn’t bomb the hospital in Gaza.

- The US Dollar consolidates around 106.35 as investors shift focus to the speech from Fed Powell.

The AUD/USD pair remains on track to recapture the round-level resistance of 0.6400 in the early New York session. The Aussie asset discovered interest from buyers as upbeat China’s Gross Domestic Product (GDP) for the July-September quarter eased fears of a slowdown in the Asian economy.

Being a proxy for China’s economic prospects, the Australian Dollar strengthens against the US Dollar. China’s National Bureau of Statistics of China reported that the growth rate was 1.3% in the third quarter of 2023, significantly higher than expectations of 1.0% and the GDP growth of 0.5% in the April-June quarter. Annual GDP at 4.9%, outperformed expectations of 4.4% but remained lower than the former release of 6.3%.

Apart from the GDP data, Industrial Production was up at a steady pace of 4.5%. Annual Retail Sales expanded at a healthy pace of 5.5% in September vs. expectations of 4.9% and the August reading of 4.6%.

Meanwhile, the S&P500 opened on a negative note amid caution over US President Joe Biden’s visit to Israel to discuss over ground assault at the Gaza strip. Biden said that the Pentagon has shown evidence that Israel didn’t bomb the hospital in Gaza.

The US Dollar Index (DXY) consolidates around 106.35 as investors shift focus to the speech from Federal Reserve (Fed) Chair Jerome Powell, which is scheduled for Thursday. Major focus would be on the interest rate guidance as other Fed policymakers have been supporting keeping interest rates unchanged at 5.25-5.50% due to higher long-term US bond yields. The 10-year US Treasury yields rose to 4.85%.

The BoJ may be closer to contemplating as to whether additional flexibility in its yield curve control (YCC) policy is now desirable, economists at Rabobank report.

USD/JPY to move back to 148 in the coming quarter

Given the potential issues involved with maintaining its YCC policy at current settings and the risk that JPY weakness would accentuate any further strength in Oil prices, we see another tweak to policy as likely being on the cards in the months ahead.

While we expect that USD strength will dominate in the coming months, a policy tweak from the BoJ would likely reinforce psychological resistance in the USD/JPY 150.

Our forecast of a move back to USD/JPY 148 on a one-to-three-month view, assumes further policy normalisation by the BoJ.

In the wake of the developments in the Middle East, the Gold price has recently risen significantly and recovered its losses from the end of September/beginning of October. Strategists at Commerzbank analyze the yellow metal’s outlook.

A renewed steep increase in Oil would be likely if the military dispute in the Middle East were to escalate or widen

The Middle East conflict is currently posing a considerable upside risk. If it were to spill over into other countries in the region, the Gold price would presumably gain initially in its role as a safe haven.

If the military dispute in the Middle East were to escalate or widen, a renewed steep increase in the Oil price would be likely, which in turn would raise the risk of persistently high inflation and could then spark further rate hikes. As interest rates have already been increased noticeably, they would probably not rise as steeply as they did last year. All the same, this would certainly postpone any expectations of any interest rate cuts next year, which is what has lent support to the Gold price of late.

Source: Commerzbank Research

- DXY picks up upside traction and reverses two daily pullbacks in a row.

- The continuation of the rebound targets the 106.80 region.

DXY leaves behind the pessimism seen in the first half of the week and revisits the low-106.00s on Wednesday.

In case the bullish impulse accelerates, the surpass of the weekly high of 106.78 (October 12) could encourage the index to embark on a potential test of the 2023 top of 107.34 (October 3) in the short-term horizon.

In the meantime, while above the key 200-day SMA, today at 103.25, the outlook for the index is expected to remain constructive.

DXY daily chart

The Shekel has weakened sharply in response to the conflict between Hamas and Israel. Economists at MUFG Bank analyze ILS outlook.

Move above 4.00 level likely to prove short-lived

Recent history suggests ILS can weaken further during the conflict.

BoI intervention will help to dampen the scale of ILS sell-off.

ILS weakness could make BoI cautious about cutting rates as market expects.