- Analytics

- News and Tools

- Market News

Новини ринків

- The EUR/GBP bounded into 0.8680 after EU data beats climbed over UK earnings miss.

- EU sentiment came in above expectations, while UK wages failed to meet the market median forecast.

- EUR/GBP traders will be looking ahead to Wednesday's joint CPI inflation reading for both the EU and the UK.

The EUR/GBP climbed around 0.4% on Tuesday in one of the pair's single-best trading days since early September, rising from the opening bids near 0.8648 to close out around 0.8682, and setting a high for the day at 0.8690.

With only inches to go from the 0.8700 handle, the Euro (EUR) finds itself heading into Wednesday's double-feature of UK and EU inflation figures.

UK Average Earnings missed the mark on Tuesday, with wages including bonuses for the quarter into August growing by 8.1% against the forecast 8.3% and coming in below the previous reading of 8.5%.

On the EU side, the ZEW Economic Sentiment Survey for October showed an unexpected rebound in economic confidence, with the index printing a firm 2.3 compared to the forecast -8 and previous reading of -8.9.

Wednesday sees UK Consumer Price Index (CPI) inflation numbers, with the headline annualized inflation reading expected to tick down from 6.7% to 6.5% for September.

On the EU side, EU CPI inflation is broadly expecting to hold steady, with the Core CPI reading for September to show flat at 0.2% for the month.

The European Central Bank (ECB) President Christine Lagarde is also expected to make an appearance, and investors will be keeping an eye out for any statements about the ECB's forecasts on possible interest rate moves.

EUR/GBP Technical Outlook

Despite Tuesday's bumper green bar for the day, the EUR/GBP remains trapped within familiar price action, with September's swing high into the 0.8700 handle seeing constraining technical resistance from a slowly descending 200-day Simple Moving Average (SMA).

On the downside the 50-day SMA is seeing some lift into the 0.8620, keeping bids trapped in the middle, and the last swing low into 0.8620 will be the level to beat for EUR/GBP sellers in the near-term.

EUR/GBP Daily Chart

EUR/GBP Technical Levels

- AUD/JPY rises and prints a new weekly high of 95.50 but remains within the 93.00/96.40 consolidation range.

- Immediate resistance for AUD/JPY stands at 95.50, followed by the 96.00 psychological level.

- Key supports are located at the top of the Kumo at 94.31 and 94.00.

The Australian Dollar (AUD) registers solid gains against the Japanese Yen (JPY) after minutes of the latest Reserve Bank of Australia (RBA) showed the central bank kept the door open for further tightening. The AUD/JPY is trading at 95.33, up 0.54%.

Despite rising towards a weekly high of 95.50, the AUD/JPY pair remains consolidated but unable to break below/above the 93.00/96.40 range, though as price action remains above the Kumo, the bias is mildly bullish. Therefore, the first resistance would be 95.50, Tuesday’s high, followed by the psychological 96.00 mark. A breach of the latter would expose the top of the aforementioned resistance level at 96.40 and the year-to-date (YTD) high of 97.67.

On the flip side, the AUD/JPY first support would be the top of the Kumo at 94.31, followed by the 94.00 figure. Once cleared, the cross would die towards the October 3 daily low of 93.01.

AUD/JPY Price Action – Daily chart

AUD/JPY Technical Levels

According to the Reserve Bank of Australia (RBA) Governor Michele Bullock's speech on Wednesday, Bullock said if inflation remains higher than expected, RBA will respond with policy.

Key quotes

“Bit more worried about inflation impact from supply shocks.”

“We are seeing demand slow, per capita consumption is declining.”

“Have not yet seen full impact of past rate rises on consumption.”

“If inflation remains higher than expected, will have to respond with policy.”

“We think we are running narrow path, but very alert to upside inflation risks.”

Market reaction

At the time of writing, the AUD/USD pair is trading near 0.6365,holding higher while adding 0.02% on the day.

- EURUSD currently trades around 1.0575 amid the risk-on mood and the softer USD.

- EU and German ZEW Economic Sentiment Survey for October came in better than expected.

- US Retail Sales for September rose 0.7% MoM, stronger than the 0.3% estimated.

- Market players await the Eurozone inflation data, US housing data.

The EURUSD pair hovers around 1.0575 after retreating from the 1.0600 mark during the early Asian session on Wednesday. The risk-on flows dominate the market and weigh on the US Dollar (USD) lower. Meanwhile, the US Dollar Index (DXY) corrects lower to 106.20 and US Treasury yields surges sharply, with the 10-year Treasury yield reaching 4.83%.

On Tuesday, the EU's ZEW Economic Sentiment Survey came in at 2.3 in October from an 8.9 drop in the previous reading, beating the market expectations. German ZEW Survey Economic Sentiment also showed an improvement by climbing to -1.1 from -11.4 in the previous reading.

The European Central Bank (ECB) President Christine Lagarde said that the ECB is watching energy prices and the Israel-Hamas conflict for inflation risks. Meanwhile, ECB's chief economist Philip Lane stated that they will keep interest rates high until inflation returns to 2%, but this may take time longer than expected due to several factors.

The economic data released by the US Census Bureau revealed that the Retail Sales for September came in at 0.7% MoM, beating the market expectation of 0.3%. Retail Sales Control Group climbed 0.6% MoM versus 0.2% prior. The data suggest strong momentum in consumption. Additionally, US Industrial Production rose by 0.3% MoM, stronger than expected. Capacity Utilization improved to 79.7, better than estimated.

The Greenback edged higher on the back of the upbeat US data, but the impact was short-lived. However, higher US Treasury yields might cap the downside of the USD.

Minneapolis Federal Reserve Bank President Neel Kashkari on Tuesday said that inflation has taken considerably longer than expected and is still too high. Earlier, Chicago Fed President Austan Goolsbee and Philadelphia Fed President Patrick Harker maintained their dovish stance. Harker stated that the central bank should not create new pressures in the economy by increasing the cost of borrowing. Traders will take more cues from the Fed officials this week. The hawkish comments might lift the USD and act as a headwind for the EUR/USD pair.

Looking ahead, market players will monitor the final reading of the Eurozone Consumer Price Index (CPI) for September and Construction Output for August due later in the day. Also, ECB's President Lagarde's speech could offer some hints about the further monetary policy path. On the US docket, the US Housing Starts and Building Permits will be released on Wednesday. These events could give a clear direction to the EUR/USD pair.

- US equities ended Tuesday mixed as Wall Street spreads on US Retail Sales beat.

- Tech stocks see losses after US restricts chip sales to China.

- Treasury yields spiked once again, 10-year yield sees 4.836%.

The Standard & Poor's (S&P) 500 major equity index closed Tuesday trading largely flat on the day, ending in the red a scant 0.01% to close at $4,373.20, down -0.43 points. The NASDAQ Composite saw a 0.25% loss to end the day down 34.24 points into $13,533.75, while the Dow Jones Industrial Average (DJIA) eked out a minor gain of 0.04%, rising 13.11 points to end the day at $33,997.65.

Equities mixed following the bumper US Retail Sales figures, with equity investors concerned about the Federal Reserve (Fed) failing to cut interest rates as quickly as markets would like.

US Retail Sales rose 0.7% in September vs. 0.3% anticipated

Chip stocks saw the majority of the day's declines after the US Presidential Administration announced plans to halt shipments to China of AI-based chip tech, with NVIDIA leading the way down for major chip makers, declining over 4% on the day.

The US Retail Sales data beat, coupled with solid earnings beats for both Bank of America and Goldman Sachs, sent US Treasury yields into 17-year highs as strong consumer activity and bumping summer profits show the Fed's interest rate hikes may not be tying down the US domestic economy as many investors would be hoping for in order to get the rate cut cycle started, and continued upbeat data printings will see the Fed punished even further out on anticipated rate cuts, which are currently seen not until the third quarter of 2024.

S&P 500 Technical Outlook

The S&P 500 remains strung up in near-term familiar territory, and remains capped below last week's swing high into $4,396, with the 50-day Simple Moving Average pressing down from $4,400.

October's early bounce from $4,199 sees the S&P index climbing from the 200-day SMA with prices caught between scissor handles from the 50- and 200-day SMAs.

S&P 500 Daily Chart

S&P 500 Technical Levels

- The AUD/NZD sees its single best trading day since June, climbing nearly 0.9% on Tuesday.

- The RBA's meeting minutes proved to be hawkish with the Aussie central bank seeing higher inflation risks.

- the Kiwi struggled after Monday's CPI inflation miss.

The AUD/NZD hustled up the charts to close Tuesday trading just shy of the 1.0800 major handle, driving the pair decisively back into prices not seen since September, with the Aussie (AUD) catching a firm bid from a hawkish Reserve Bank of Australia (RBA) while the Kiwi (NZD) struggles to find some pickup after missing Consumer Price Index (CPI) inflation expectations on Monday.

RBA Minutes: Case to hold was stronger, upside risks to inflation were a significant concern

The RBA's latest Meeting Minutes paved the way for the Australian reserve bank to hold interest rates higher for even longer than previously anticipated, driving the Aussie higher as markets firmly bid the AUD against its Antipodean neighbor.

Forex Today: Dollar slides despite upbeat US data

The Kiwi broadly missed the mark in late Monday's CPI inflation reading, with the annualized figure into the third quarter flubbing the 5.9% forecast to print at 5.6% against the previous quarter's 6%.

Next up on the economic calendar data docket will be Thursday's Australian employment figures, followed by New Zealand trade balance figures late in the day.

The Australian Unemployment Rate for September is expected to print flat at 3.7%, while the Unemployment Change figure for the same period is expected to decline from 64.9K to 20K.

The Kiwi Trade Balance reading is slated for late Thursday at 21:45 GMT, when the NZ markets are heading into the early Friday Asia market session. NZ Trade Balance for the year into September last printed at $-15.54B.

AUD/NZD Technical Outlook

Tuesday's bullish pump in the AUD/NZD sent the pair straight into the 50-day Simple Moving Average (SMA), with the pair hanging just south of the 1.0800 major handle. Overall bids still remain in bearish territory, but only slightly, with the 200-day SMA hanging just overhead at 1.0820.

Despite the day's solid green bar for the Aussie, the pair remains firmly entrenched in the middle of 2023's consolidation, with the AUD/NZD testing into price levels that have plagued the pair for most of the year.

AUD/NZD Daily Chart

AUD/NZD Technical Levels

- EUR/GBP rose by more than 0.46% to monthly highs around 0.8680.

- The bulls gathered enough momentum and breached through the 20-day SMA.

- RSI and MACD indicate strong bullish momentum for the short term.

The EUR/GBP cross broke out on Tuesday and rose to a monthly high of 0.8690. Indicators gained ground on the daily chart and indicate that further upside may be on the horizon.

The Relative Strength Index (RSI) points north in positive territory, while the Moving Average Convergence (MACD) now exhibits green bars. On the four-hour chart, the RSI rose near the overbought threshold and was quickly rejected, while the MACD’s histogram prints rising bullish bars, indicating that the buyers have strong momentum in the short term. Back to the daily chart, the pair is above the 20 and 100-day Simple Moving Averages (SMA) but is still below the 200-day average, which is the next target for the bulls at the 0.8700 area. That being said, this overall outlook favours a neutral to bullish technical outlook for the EUR/GBP.

Support levels: 0.8660 (20-day SMA), 0.8630, 0.8615.

Resistance levels: 0.8680, 0.8700 (200-day SMA), 0.8730.

EUR/GBP Daily Chart

-638331756352115535.png)

- The EUR/JPY pushed higher in risk-off bidding on Tuesday, climbing into 158.6.

- The pair started off with an early dump into 157.10, but markets quickly reversed direction.

- Wednesday brings EU CPI inflation, Japan Trade Balance.

The EUR/JPY started Wednesday with a dip into 157.10 before broad-market risk appetite turn higher, sending the Euro (EUR) back into near-term highs against the Japanese Yen (JPY), and the pair is heading into Wednesday's trading session near 158.50.

the EU's ZRE Economic Sentiment Survey for October came in well above expectations, printing at 2.3 versus the expected -8, reversing the previous reading of -8.9.

Wednesday brings European Harmonized Index of Consumer Prices (CPI) inflation figures for September, with the month-on-month figure expected to hold steady at 0.3%.

Late in the day will be Japan's Trade Balance, during the early Asia Thursday market session, where Japan's Exports are expected to recover from -0.8% to 3.1% for the year into September, while Imports are expected to bounce from -17.8% to -12.9% for the same period.

EUR/JPY Technical Outlook

EUR/JPY remains well-bid on intraday candles with prices remaining buoyed above the 200-hour Simple Moving Average (SMA) currently rising into 157.60.

Tuesday's high of 158.62 represents a new five-week high for the pair, and the pair is set to resume knocking against the ceiling of long-running consolidation that has kept the EUR/JPY constrained since first climbing into the 158.00 neighborhood in June of this year.

Despite a lack of meaningful momentum, the EUR/JPY remains overall well-bid, refusing to sink too far from the 50-day SMA and prices squeezing into a consolidation tunnel between 157.00 and 15850.

EUR/JPY Daily Chart

EUR/JPY Technical Levels

During the Asian session, the key highlight will be the release of Chinese economic data, including GDP figures. Additionally, RBA Bullock is scheduled to participate in a panel discussion. During European trading hours, the focus will shift to the release of UK inflation data.

Here is what you need to know on Wednesday, October 18:

Another round of upbeat US economic data was released. Retail sales in September rose 0.7%, surpassing the market consensus of 0.3%. August numbers were revised higher. Industrial Production in September increased by 0.3%, exceeding expectations of a flat reading. These positive figures initially boosted the US Dollar, but the impact was short-lived. The DXY closed with minor losses around 106.20.

While US Treasury yields rose sharply, higher yields across the Atlantic offset the impact on the dollar. The 10-year Treasury yield reached 4.86%, while the German benchmark yield climbed 3.50% to 2.88%.

Despite the positive economic news, Wall Street's reception was mixed. The Dow Jones rose 0.04%, while the Nasdaq declined 0.25%. The earnings season continues on Wednesday, with Tesla, Morgan Stanley, Abbott, Netflix, and other companies reporting their results.

Wells Fargo on US Retail Sales:

Consumers are spending more at bars & restaurants, at auto dealers and online. That's true on both a monthly basis and on trend over the past year. Consumers are looking for nothing but a good time, and it is hard to resist seeing the upside risk to the outlook.

During the European session, the Japanese Yen (JPY) experienced a sharp spike in response to reports suggesting that the Bank of Japan (BoJ) was likely to revise its inflation forecast for the fiscal years 2023 and 2024. However, the Yen's momentum was short-lived, and it subsequently pulled back, erasing all its gains. The USD/JPY pair found support around 148.75 and, following upbeat US retail sales data, gained strength, breaking above 149.70. The pair is now approaching the 150.00 level, which is considered a potentially significant area for intervention by the authorities.

The Euro (EUR) strengthened against the Swiss Franc (CHF) and the Pound (GBP), supported by higher Eurozone bond yields. The EUR/USD pair briefly peaked near 1.0600 before pulling back, but it held above the 1.0560 level. Eurozone will release the final readings of September's Consumer Price Index (CPI) and Construction Output for August.

GBP/USD pair continues to trade within a range of 1.2130 and 1.2225 without a clear direction. Market focus now turns to the UK inflation data scheduled for release on Wednesday.

The Canadian Dollar (CAD) declined across the board after Canada reported a 0.1% decline in the Consumer Price Index (CPI) for September, contrary to expectations of a 0.1% increase. The annual inflation rate slowed from 4% to 3.8%. USD/CAD initially traded above 1.3700 but then pulled back to the 1.3640 area, trimming its gains.

During the Asian session, the New Zealand Dollar (NZD) remained weak, continuing to be impacted by the lower-than-expected New Zealand Q3 inflation reading. The NZD/USD pair trimmed losses during the American session but ultimately finished lower, slightly below 0.5900. The pair is currently trading near the key support area of 0.5860.

On Tuesday, the Australian Dollar (AUD) outperformed, bolstered by the hawkish minutes from the latest Reserve Bank of Australia (RBA) meetings. The AUD/USD pair saw gains for the second consecutive day, but it faced resistance upon reaching the 20-day Simple Moving Average (SMA) at 0.6380 and subsequently retraced to 0.6360. On Wednesday, RBA Governor Bullock will speak at the Australian Financial Security Authority Annual Summit Panel.

Gold rose despite higher yields but failed to retake levels above $1,930. Silver rebounded sharply at $22.35, rising toward $23.00.

Like this article? Help us with some feedback by answering this survey:

- USD/JPY trades steadily around 149.70, a slight gain of 0.14%.

- Concerns about potential intervention by Japanese authorities cap the upside.

- Rising US Treasury bond yields provide support to the pair.

The USD/JPY remains steady at around 149.70, capped on the upside by fears of intervention threats by Japanese authorities. the rise in US Treasury bond yields underpinned the major, though it remains exchanging hands below the 150.00 figure, with minuscule gains of 0.14%.

The pair is consolidated within the 149.00/150.00 mark, unable to break below/above the range decisively. Nevertheless, if USD/JPY aims above 150.00, the next resistance would be the 150.16 year-to-date (YTD) high, followed by the latest year high at 151.94.

Conversely, if USD/JPY drops below 149.00, first support would emerge at the Kijun-Sen line at 148.29. If the pair slides below that level, October 3, swing low at 147.37, would be up next.

USD/JPY Price Action – Daily chart

USD/JPY Key Technical Levels

- UK wage growth data comes in below expectations, casting doubts on further BoE rate hikes.

- US Retail Sales for September surpass expectations, with August data revised upwards.

- Speculations rise on a potential Fed rate hike in December; CME FedWatch Tool indicates a 42.90% probability.

The Pound Sterling (GBP) remains on the defensive vs. the US Dollar (USD) after data from the United Kingdom showed wages are decelerating. That and a solid Retail Sales report in the United States (US) weighed on Sterling. Therefore, the GBP/USD dipped below 1.2200, a loss of 0.25%.

GBP/USD weighed by BoE’s expected rate hike pause, solid US economic data

In the European session, jobs data from the UK showed that wages came slightly below estimates, reinforcing market participants' thesis that the Bank of England (BoE) is done raising rates. In the latest BoE meeting, the central bank decided to stay put in rates on a 5-4 vote split, even though inflation levels remain at three times the BoE’s target.

Before Wall Street opened, a tranche of US economic data showed that American consumers remain resilient, despite the 525 basis points of tightening by the Federal Reserve. US Retail Sales in September exceeded forecasts, though it trailed August’s upward-revised figures. That stirred speculations the Fed could hike rates at the December meeting, as shown by the CME FedWatch Tool with odds for a quarter of a percent hike at 42.90%.

Consequently, US Treasury bond yields skyrocketed, with the US 10-year benchmark note climbing twelve basis points at 4.83%. Still, the Greenback remained trading softer, as shown by the US Dollar Index (DXY), dropping 0.05%, at 106.15.

Meanwhile, Federal Reserve officials remained hawkish, as Richmond Fed President Thomas Barkin emphasized the US central bank's restrictive policy while adding he’s uncertain where rates would be three weeks from now.

Ahead of the week, GBP/USD traders are eyeing inflation figures for September, to be revealed on Wednesday. Across the pond, US housing data and Fed speakers would provide a fresh catalyst to the major.

GBP/USD Price Analysis: Technical outlook

The daily chart portrays the GBP/USD as neutral to downward biased. The 50=day moving average (DMA) crossing below the 200-DMA, formed a death-cross a bearish sign, warranting further downside. The first support would be last week's low of 1.2122 before diving towards 1.2100. A breach of the latter would expose the October 4 swing low of 1.2037.

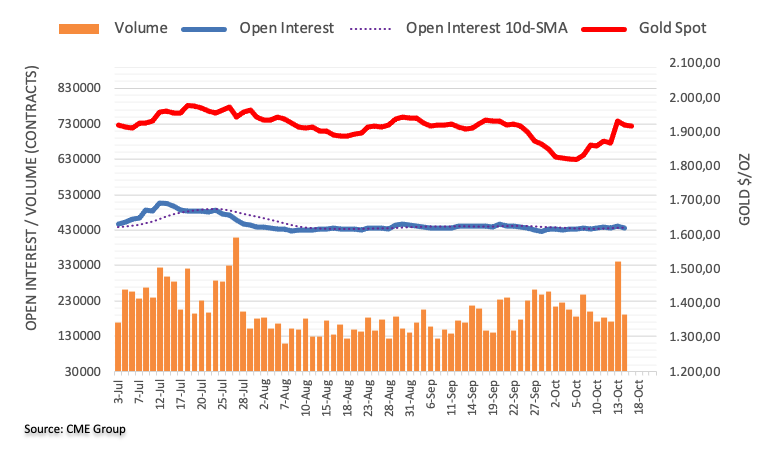

- Spot Gold prices are slipping back into the middle after Tuesday saw a push above $1,930.

- XAU/USD remains well-bid, sticking to the high end of last week's rally.

- Inflation fears remain a key factor in Gold prices as investors keep one foot in safety.

XAU/USD kicked off Tuesday trading near $1,919 before seeing a steady rise into an intraday high of $1,931.65, but the day's momentum is proving short-lived as Gold bids settle back into near-term consolidation $1,920.

US Retail Sales broadly beat market estimates, with the headline figure for September printing at 0.7% versus the forecast 0.3%, with the previous period also seeing an upwards revision from 0.6% to 0.8%.

US Retail Sales rose 0.7% in September vs. 0.3% anticipated

The Retail Sales beat sent the US Dollar (USD) broadly lower against the market, giving risk assets a solid push up the charts, and while spot Gold prices saw some bullish play as investors remain concerned about a bumper US economy threatening to push the Federal Reserve (Fed) further away from anticipated rate cuts in 2024, the US Retail Sales figure isn't a solid indicator of possible inflation.

XAU/USD Technical Outlook

Near-term action sees spot Gold prices bidding into the 50-hour Simple Moving Average (SMA), with action hobbled near $1,920 and bidders struggling to take XAU/USD higher, while short-sellers are seeing significant headwinds with Gold prices firmly bullish and trading well above the 200-hour SMA.

Daily candlesticks see XAU/USD facing a technical rejection from the 200-hour SMA near $1,930 after a 6.8% climb from the last swing low into $1,810, and near-term technical indicators are warning of possible consolidation on the charts with a flat 50-day SMA trapping prices in the middle.

XAU/USD Daily Chart

XAU/USD Technical Levels

- GBP/JPY took an initial ride down the charts into 181.02 in early Tuesday trading.

- A firm rebound sent the Guppy back into the day's highs near 182.80.

- Intraday action is caught in the middle with prices cycling the neutral pivot.

The GBP/JPY kicked off Tuesday trading near 182.66 before seeing a plunge lower, just missing the 181.00 handle before a quick snap rebound sent the pair into a fresh high for the day at 182.80, and the pair is now waffling into the midrange near the week's P0 neutral pivot point.

Near-term action has been sticking close to the median, with hourly candles routinely tapping the 50-hour Simple Moving Average (SMA) that is currently testing into 182.25.

Last week's declining overall momentum sees weekly pivots tightening their range, with R1 capped at 183.32 and S1 parked at 180.76.

4-hour candles likewise show the pair strung up in the middle with bids constrained between the 200-period SMA and a rising 50-period SMA.

On the daily candlesticks the Guppy is stuck closely to the 50-day SMA and trading far above the 200-day SMA with the pair up over 15% from the year's opening bids near 158.40. The pair remains incredibly well-bid in the long term, but a lack of continued momentum sees prices failing to make a decisive break for the last major swing high into 186.77, and the immediate bearish target currently sits at early October's low of 178.08.

GBP/JPY Hourly Chart

GBP/JPY Daily Chart

GBP/JPY Technical Levels

- The USD/CHF reversed its course after jumping to a daily high of 0.9032 and then settling slightly above 0.9000.

- The USD is struggling to gather momentum on a positive market mood.

- The US reported strong economic activity figures from September.

- Rising US Treasury yields may limit the downside for the pair.

In Tuesday’s session, the USD/CHF saw volatility, and after initially rising to a high above the 200-day Simple Moving Average (SMA) of 0.9032, it retreated towards 0.9000, still holding some daily gains. The market movers for the pair included US economic activity figures from September, while the Swiss economic calendar had nothing relevant to offer.

The US Census Bureau reported that Retail Sales came in at 0.7% MoM in September, higher than the 0.3% expected but decelerated from 0.8%. Furthermore, Industrial Production rose by 0.3% MoM in the same month versus the 0% expected, and both data points suggest that the US economy is resilient despite the Federal Reserve's (Fed) contractive monetary policy.

As a reaction, US yields continued rising, and the 2, 5, and 10-year rates rose to 5.22%, 4.88%, and 4.85%, respectively, with all three seeing more than 1.50% increases and approaching multi-week highs. In line with that, investors may be gearing up for another hike by the Federal Reserve as the combination of strong economic activity and inflation accelerating in September may justify one more 25 basis point (bps) increase in 2023. According to the CME FedWatch tool, the odds of a 25 bps hike in the December meeting rose to nearly 42%, while a pause in September is nearly to be priced in. For the rest of the week, the Federal Reserve’s Beige Book will provide further clues on Wednesday's US economic outlook and the weekly Jobless Claims report on Thursday.

USD/CHF Levels to watch

Observing the daily chart, the outlook is starting to tilt in favour of the bears, but they still have some work to do. The Relative Strength Index (RSI) has a negative slope below its midline, while the Moving Average Convergence (MACD) histogram presents bigger red bars. Additionally, the pair is below the 20 and 200-day Simple Moving Averages (SMAs) but above the 100-day SMA, indicating that the bulls still have some gas left in the tank in the broader picture.

Support levels: 0.8980, 0.8950, 0.8930.

Resistance levels: 0.9018 (200-day SMA), 0.9040, 0.9070.

USD/CHF Daily Chart

-638331640319594549.png)

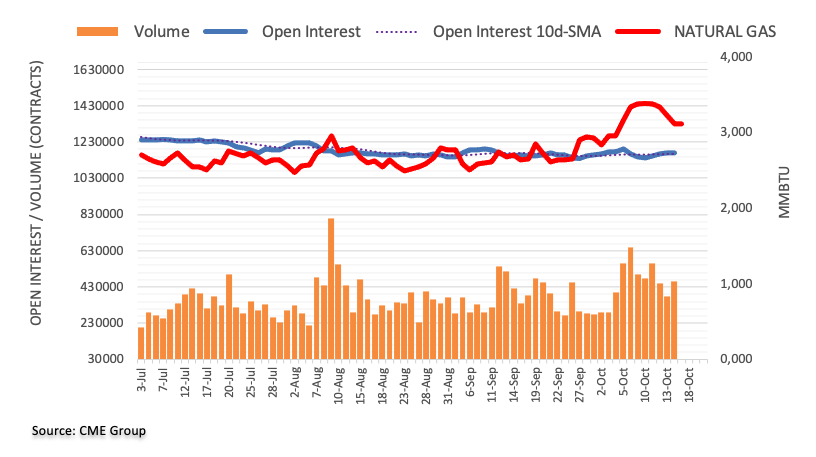

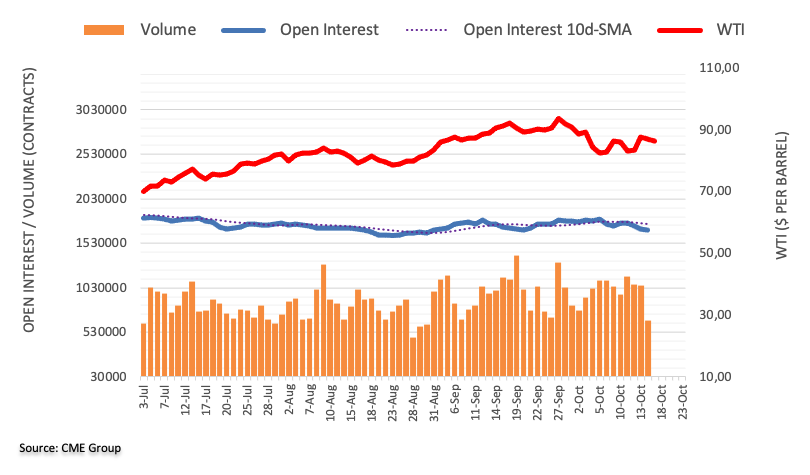

- Crude Oil prices are seeing some froth on Tuesday as energies get pulled in multiple directions.

- WTI barrel bids bounce between $86 and $84.50.

- Crude supply constraints may not be as bad as originally thought, but geopolitical stress continues to weigh.

West Texas Intermediary (WTI) is seeing some back-and-forth on Tuesday, but remains constrained near the $85.00/bbl price point as energies markets weigh inconsistent outcomes for crude oil markets.

The Israel-Hamas conflict escalation continues to stress out Crude Oil traders, but lack of immediate negative impact is keeping prices capped off. Geopolitical spillover could threaten stability in the nearby Strait of Hormuz, a major energy supply flow-through point that sees nearly a fifth of all global energy trade.

Deep supply cuts from member states of the Organization of the Petroleum Exporting Countries (OPEC) continue to keep crude barrel prices pinned higher, specifically Saudi Arabia and Russia's combined 1.3 million bpd production and export cuts. Despite major supply constraints that threaten to undershoot global demand, China's fossil fuels demand continues to wane as their domestic economy slows down more than expected, leaving more oil barrels on the table.

Iran recently re-entered global oil markets after the US eased export restrictions on the country, and lack of evidence that Iran was directly involved in the recent Israel-Hamas conflict escalation sees the US avoiding re-instating restrictions for the time being.

Hopes for a US-Venezuela crude oil exporting deal remain high with the US reaching a preliminary deal to allow the South American country to return to global oil exporting markets in exchange for a monitored presidential election next year in Venezuela.

A return for Venezuelan crude exports would be a surge for oil markets that already sees crude reserves rebounding firmer and faster than expected as global demand struggles to eat up enough of the already-constrained supply.

WTI Technical Outlook

Intraday action on the WTI chart is getting capped off by the 50-hour Simple Moving Average (SMA) near $85.75 as Crude Oil prices struggle to regain last week's late swing into the $87.00 handle, and Tuesday's early push into $86.00 proved to be short-lived as WTI Crude Oil barrels get stuck to the $85.00 level.

Daily candlesticks see WTI bids stuck to the 50-day SMA as energies struggle to push prices in either direction meaningfully. Crude Oil initially rose for four consecutive months from a 2023 low of $64.31 to a thirteen-month high of $93.98, but WTI is set to flub the trend and see softening prices for October as forward-looking supply constraint fears fail to solidify.

WTI Daily Chart

WTI Technical Levels

- AUD/USD advances, trading around 0.6371 after bouncing from daily lows.

- Richmond Fed President Thomas Barkin's comments on the restrictive policy stance, remains undecided for the upcoming FOMC meeting.

- Hawkish RBA meeting minutes hint at a potential rate hike in November, with a focus on Q3 inflation data.

The Aussie Dollar (AUD) edges higher vs. the US Dollar (USD) in the mid-North American session, rising more than 0.50% after hitting a daily low of 0.6332. Even though upbeat economic data from the United States (US) warranted lower exchange rates, tilted hawkish Reserve Bank of Australia’s (RBA) minutes bolstered the AUD. At the time of writing, the AUD/USD is trading at 0.6371.

AUD/USD gains momentum despite strong US Retail Sales, eyes on Chinese GDP data

The US economic docket recently featured the Richmond Fed President Thomas Barkin, who said that policy is already restrictive and he’s undecided regarding the upcoming FOMC monetary policy meeting in November. He added the US central bank can’t rely in longer-term higher bond yields to tighten monetary conditions.

Earlier, the US Bureau of Economic Analysis (BEA) revealed that Retail Sales in September crushed estimates of 0.3% MoM as figures jumped 0.7%, as consumers remain resilient. Later, the Federal Reserve announced that Industrial Production picked up despite having interest rates at higher levels.

During the Asian session, the latest Reserve Bank of Australia (RBA) meeting minutes portray the bank as hawkish, keeping the door open for a November hike as RBA officials eye Q3’s inflation report. Aside from this, Chiina’s data would reveal if the second largest economy continues to lose traction, as most analysts expect a slowdown in growth, with estimates circa 4.4% YoY, below the Chinese government projections of 5%.

A weak number on Chinese GDP could weigh on market sentiment, therefore dragging Aussie Dollar (AUD) prices lower. Otherwise, upbeat figures could trigger another AUD/USD pair leg-up.

AUD/USD Price Analysis: Technical outlook

After forming a bullish-piercing pattern, the AUD/USD extends its gains past Monday’s daily high of 0.6345, though shy of reclaiming 0.6400. A breach of the latter, the pair would test the 50-day moving average (DMA) at 0.6416 before threatening to crack the latest cycle high of 0.6445. On the other hand, the pair would resume its downtrend, towards 0.6300, before the AUD/USD challenges the year-to-date (YTD) low of 0.6285.

- The US Dollar cleared daily gains despite better-than-expected Retail Sales and Industrial Production figures from September.

- A positive market and risk-on flows weakened the USD.

- The US Treasury yields on the 2, 5, and 10-year bonds are approaching two-week highs, limiting the downside potential.

- The odds of a hike by the Fed in December rose to 42% according to the CME FedWatch tool.

The US Dollar (USD) measured by the US Dollar DXY Index rose to a high of 106.52 and then declined towards 106.15, below the 20-day Simple Moving Average (SMA) after the release of September’s Retail Sales and Industrial Production figures from the US. Both reports came in higher than expected, but risk-on flows dominate the market which isn’t allowing the green currency to gather momentum. However, higher US Treasury yields and rising hawkish bets on the Federal Reserve (Fed) may limit the downside for the USD.

The United State’s economic activity is still holding strong despite the Federal Reserve’s aggressive manoeuvres, and inflation figures revealed that the Consumer Price Index (CPI) slightly accelerated in September.

As Jerome Powell stated during the press conference from September’s decision, the Fed is still ready to resume hiking as long as data justifies another hike so this current outlook is making investors gear up for one last hike in 2023.

Daily Digest Market Movers: US Dollar continues weakening despite positive economic figures

- The US Dollar DXY rose to a high of 106.52 and then settled around 106.15, paring back its daily gains.

- US retail Sales came in at 0.7% MoM in September, higher than the 0.3% expected but decelerated from 0.8% in the previous month.

- Industrial Production rose by 0.3% MoM in the same month, vs the 0.0% expected.

- US yields continue rising, and the 2, 5 and 10-year rates rose to 5.18%, 4.84% and 4.83% respectively, with all three seeing more than 1.50% increases.

- According to the CME FedWatch tool, the odds of a 25 bps hike in the December meeting rose to nearly 42%.

- The Federal Reserve’s Beige Book, released on Wednesday, will provide further clues on the outlook for the US economy.

Technical analysis: US Dollar Index’s bears breach the 20-day SMA but 105.50 is the make-or-break level

The DXY index failed to hold on to its early bullish momentum which took it to a high of around 106.52 before declining to negative territory at around 106.05. Nevertheless, the index arguably remains in a bullish trend overall, holding above the key 200 and 100-day Simple Moving Averages (SMA).

Indicators on the daily chart point towards a strengthening bearish momentum, with the Moving Average Convergence Divergence (MACD) printing red bars after performing a bearish cross on October 6.

As the bulls have failed to defend the 20-day SMA, more downside may be on the horizon although 105.50 low is the key ‘line in the sand’ that would need to be crossed to turn the outlook particularly bearish.

Supports: 106.00, 105.80, 105.50.

Resistances: 106.20 (20-day SMA), 106.55, 107.00.

US Dollar FAQs

What is the US Dollar?

The US Dollar (USD) is the official currency of the United States of America, and the ‘de facto’ currency of a significant number of other countries where it is found in circulation alongside local notes. It is the most heavily traded currency in the world, accounting for over 88% of all global foreign exchange turnover, or an average of $6.6 trillion in transactions per day, according to data from 2022.

Following the second world war, the USD took over from the British Pound as the world’s reserve currency. For most of its history, the US Dollar was backed by Gold, until the Bretton Woods Agreement in 1971 when the Gold Standard went away.

How do the decisions of the Federal Reserve impact the US Dollar?

The most important single factor impacting on the value of the US Dollar is monetary policy, which is shaped by the Federal Reserve (Fed). The Fed has two mandates: to achieve price stability (control inflation) and foster full employment. Its primary tool to achieve these two goals is by adjusting interest rates.

When prices are rising too quickly and inflation is above the Fed’s 2% target, the Fed will raise rates, which helps the USD value. When inflation falls below 2% or the Unemployment Rate is too high, the Fed may lower interest rates, which weighs on the Greenback.

What is Quantitative Easing and how does it influence the US Dollar?

In extreme situations, the Federal Reserve can also print more Dollars and enact quantitative easing (QE). QE is the process by which the Fed substantially increases the flow of credit in a stuck financial system.

It is a non-standard policy measure used when credit has dried up because banks will not lend to each other (out of the fear of counterparty default). It is a last resort when simply lowering interest rates is unlikely to achieve the necessary result. It was the Fed’s weapon of choice to combat the credit crunch that occurred during the Great Financial Crisis in 2008. It involves the Fed printing more Dollars and using them to buy US government bonds predominantly from financial institutions. QE usually leads to a weaker US Dollar.

What is Quantitative Tightening and how does it influence the US Dollar?

Quantitative tightening (QT) is the reverse process whereby the Federal Reserve stops buying bonds from financial institutions and does not reinvest the principal from the bonds it holds maturing in new purchases. It is usually positive for the US Dollar.

- NZD/USD bounces off a two-week low, trading around 0.5908.

- US Retail Sales for September surpass expectations; Industrial Production also beats forecasts.

- New Zealand's Q3 CPI comes in below estimates, with a yearly rate easing to 5.6%.

The New Zealand Dollar (NZD) remains defensive against the US Dollar (USD) and registers solid losses after dropping to a two-week low of 0.5870. However, buyers reclaim the 0.5900 figure, targeting a challenge of 0.5942, the 50-day moving average (DMA). At the time of writing, the NZD/USD is trading at 0.5908.

Kiwi Dollar reclaims 0.5900amid mixed economic data, eyes on Fed policymakers

The US Dollar stages a comeback after the US Bureau of Economic Analysis (BEA) revealed that Retail Sales rose above forecasts of 0.3%, at 0.7% MoM in September, though below upward revised August’s figures from 0.6% to 0.8%. Recently, the Fed revealed that Industrial Production exceeded forecast and August’s data of 0%, expanding at a 0.3% MoM pace.

Consequently, US Treasury bond yields advanced nine basis points at 4.80%, contrary to the Greenback as seen by the US Dollar Index (DXY). The DXY, which tracks the performance of the US Dollar vs. six currencies, drops 0.15%, at 106.05.

Meanwhile, Fed officials are crossing newswires, led by Richmond Fed President Thomas Barkin, saying the Fed has a restrictive policy stance and that despite longer-term rates having risen, the Fed can’t rely on them for further tightening. Barkin added that he’s unsure of his view on the upcoming monetary policy meeting.

Earlier in the Asian session, the New Zealand docket featured the Consumer Price Index (CPI), which rose by 1.8% in Q3, below estimates of 2%. Still, the yearly rate eased to 5.6% from 6%, the estimated 5.9%.

NZD/USD Price Analysis: Technical outlook

The NZD/SUD daily chart portrays the pair jumping off the weekly lows, though shy of challenging the 50-DMA At 0.5942. NZD buyers must reclaim the latter so they can threaten to claim 0.6000 before challenging the latest cycle high of 0.6055, October 11 high. Conversely, failure at the 50-DMA could open the door to test the year-to-date (YTD) lows of 0.5859.

- The EUR/USD is climbing for Tuesday after risk appetite in the broader markets returns.

- A clean beat for US Retail Sales figures is seeing investor sentiment improve, taking the USD lower.

- The Euro is getting pushed higher in the broad-market Greenback slump, heading back into 1.0600.

The EUR/USD firmly in the green for Tuesday after US Retail Sales beat market expectations and saw upside revision to previous figures, sending investor risk appetite into the ceiling and sending the US Dollar (USD) broadly lower, bolstering the Euro (EUR) and taking the EUR/USD up from the day's early low of 1.0532 and sending it within inches of the 1.0600 major handle.

Headline US Retail Sales figures for September broadly beat median market forecasts of 0.3%, printing at 0.7% and seeing an upwards revision in the previous month's reading from 0.6% to 0.8%.

US Retail Sales rose 0.7% in September vs. 0.3% anticipated

Earlier on Tuesday the EU's ZEW Economic Sentiment Survey also soundly beat expectations, coming in at 2.3, soundly beating the forecast -8 and marking in a full bounceback from the previous print of -8.9.

Market sentiment has gone full risk-on, sending the Greenback down across the board and bolstering the EUR/USD back into levels that the currency pair initially lost a hold of following last week's risk-off souring.

Coming up next on Wednesday will be European Harmonized Index of Consumer Prices for September, where the headline monthly figure is forecast to hold steady at 0.3%.

EUR/USD Technical Outlook

Intraday action for the EUR/USD sees the pair busting out of recent price levels, clearing over the 200-hour Simple Moving Average (SMA), but an overextension could quickly see near-term bids strung out in no-man's-land with little technical support.

Near-term price action is closing in on a heavy support/resistance zone from 1.0600 to 1.0620, while intraday swings are providing an intraday higher-lows support pattern.

Tuesday's reaction bid sees the EUR/USD re-challenging a descending trendline from 1.1250, and the EUR/USD remains firmly bearish, trading well below the 50-day SMA which is settling into 1.0700, forming technical resistance for any bullish breakouts.

EUR/USD Hourly Chart

EUR/USD Daily Chart

EUR/USD Technical Levels

- Canadian Dollar slumped 0.65% from the day’s open after US Retail Sales beat the market.

- Canada CPI inflation missed expectations, but Loonie traders are shrugging off the miss as the US Dollar recedes across the board.

- Crude Oil spot prices are dipping for Tuesday, hobbling excess gains for the CAD.

The Canadian Dollar (CAD) went V-shaped after markets saw a large run-up in the US Dollar (USD) ahead of Tuesday’s US Retail Sales reading, and a beat on the expected figure is seeing broad-market sentiment improving, sending the USD lower across the board, with the CAD shrugging off a miss for Canadian Consumer Price Index (CPI) figures.

Canada CPI inflation came in below expectations, but the Loonie is getting bolstered back into the day’s opening prices as investors pull out of the Greenback in a risk appetite bid. Crude Oil prices are also on the low side for Tuesday, pulling support out from beneath the CAD and constraining additional gains for the day.

Daily Digest Market Movers: Canadian Dollar plunges then recovers as markets corkscrew

- The USD/CAD spiked past 1.3700 in the runup to the US Retail Sales/Canada CPI data double-header.

- A solid beat for US Retail Sales on Tuesday, with the headline figure for September coming in at 0.7%, well above the forecast 0.3% and the previous figure getting revised from 0.6% to 0.8%.

- Canadian CPI inflation missed the mark, printing at 3.8% for the annualized period into September, under the 4% forecast-steady reading.

- A solid beat for US Retail Sales sent risk-hungry investors piling out of the USD and into riskier assets, sending the Greenback down across the board.

- USD/CAD recovered the day’s bids back towards the 1.3600 handle.

- A miss for Canadian CPI inflation is capping off Loonie gains against the Greenback.

- Crude Oil prices are also seeing downside pressure for Tuesday, limiting CAD upside momentum.

- CAD traders will be looking ahead to Friday’s Canadian Retail Sales to make up ground.

Technical Analysis: Canadian Dollar rebounds from pre-US Retail Sales runup, USD/CAD looking for 1.36

The USD/CAD spiked to a seven-month high in the early Tuesday session, before dropping back into Monday’s trading range after markets turned broadly risk-on, taking the pair back towards 1.3620, and intraday action is now tussling with the 50-hour Simple Moving Average (SMA) near 1.3635.

Tuesday’s spike-and-tumble for the USD/CAD leaves the pair constrained in near-term levels on the daily candlesticks, with technical support coming from the 50-day SMA near 1.3575, while last week’s swing high into the 1.3700 handle represents the figure to beat for USD/CAD bidders.

Canadian Dollar price today

The table below shows the percentage change of Canadian Dollar (CAD) against listed major currencies today. Canadian Dollar was the weakest against the Australian Dollar.

| USD | EUR | GBP | CAD | AUD | JPY | NZD | CHF | |

| USD | -0.38% | 0.01% | 0.09% | -0.62% | 0.08% | -0.11% | -0.08% | |

| EUR | 0.38% | 0.39% | 0.46% | -0.25% | 0.44% | 0.29% | 0.29% | |

| GBP | -0.03% | -0.41% | 0.07% | -0.65% | 0.04% | -0.13% | -0.12% | |

| CAD | -0.10% | -0.46% | -0.08% | -0.71% | -0.01% | -0.18% | -0.18% | |

| AUD | 0.62% | 0.23% | 0.63% | 0.71% | 0.69% | 0.52% | 0.54% | |

| JPY | -0.08% | -0.46% | -0.04% | 0.02% | -0.67% | -0.17% | -0.16% | |

| NZD | 0.12% | -0.26% | 0.12% | 0.18% | -0.52% | 0.17% | 0.00% | |

| CHF | 0.09% | -0.29% | 0.10% | 0.18% | -0.50% | 0.15% | 0.00% |

The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the Euro from the left column and move along the horizontal line to the Japanese Yen, the percentage change displayed in the box will represent EUR (base)/JPY (quote).

Canadian Dollar FAQs

What key factors drive the Canadian Dollar?

The key factors driving the Canadian Dollar (CAD) are the level of interest rates set by the Bank of Canada (BoC), the price of Oil, Canada’s largest export, the health of its economy, inflation and the Trade Balance, which is the difference between the value of Canada’s exports versus its imports. Other factors include market sentiment – whether investors are taking on more risky assets (risk-on) or seeking safe-havens (risk-off) – with risk-on being CAD-positive. As its largest trading partner, the health of the US economy is also a key factor influencing the Canadian Dollar.

How do the decisions of the Bank of Canada impact the Canadian Dollar?

The Bank of Canada (BoC) has a significant influence on the Canadian Dollar by setting the level of interest rates that banks can lend to one another. This influences the level of interest rates for everyone. The main goal of the BoC is to maintain inflation at 1-3% by adjusting interest rates up or down. Relatively higher interest rates tend to be positive for the CAD. The Bank of Canada can also use quantitative easing and tightening to influence credit conditions, with the former CAD-negative and the latter CAD-positive.

How does the price of Oil impact the Canadian Dollar?

The price of Oil is a key factor impacting the value of the Canadian Dollar. Petroleum is Canada’s biggest export, so Oil price tends to have an immediate impact on the CAD value. Generally, if Oil price rises CAD also goes up, as aggregate demand for the currency increases. The opposite is the case if the price of Oil falls. Higher Oil prices also tend to result in a greater likelihood of a positive Trade Balance, which is also supportive of the CAD.

How does inflation data impact the value of the Canadian Dollar?

While inflation had always traditionally been thought of as a negative factor for a currency since it lowers the value of money, the opposite has actually been the case in modern times with the relaxation of cross-border capital controls. Higher inflation tends to lead central banks to put up interest rates which attracts more capital inflows from global investors seeking a lucrative place to keep their money. This increases demand for the local currency, which in Canada’s case is the Canadian Dollar.

How does economic data influence the value of the Canadian Dollar?

Macroeconomic data releases gauge the health of the economy and can have an impact on the Canadian Dollar. Indicators such as GDP, Manufacturing and Services PMIs, employment, and consumer sentiment surveys can all influence the direction of the CAD. A strong economy is good for the Canadian Dollar. Not only does it attract more foreign investment but it may encourage the Bank of Canada to put up interest rates, leading to a stronger currency. If economic data is weak, however, the CAD is likely to fall.

When asked if he will vote in favor of holding policy rate unchanged at the next meeting, "policymakers will have a good debate," Federal Reserve Bank of Richmond President Thomas Barkin said on Tuesday.

Key takeaways

"Recent inflation report was only one report, after several good ones."

"Rate moves work through financial conditions."

"Longer-term rates have moved up, that has tightened conditions."

"The challenge with depending on rates is they can move."

"Don't know where rates will be three weeks from now, given what's happening globally."

"I believe we have a restrictive policy stance."

Market reaction

The US Dollar Index stays under modest bearish pressure following these comments and was last seen losing 0.15% on the day at 106.05.

- Mexican Peso is on the defensive, as the USD/MXN trades at around 17.90.

- Mexico’s economic calendar is light, with August’s Retail Sales awaited on Friday.

- Robust US Retail Sales and Industrial output lift US Dollar amid Fed Rate hike speculation.

Mexican Peso (MXN) is trimming some of its Monday gains against the US Dollar (USD) after a tranche of economic data from the United States (US) spurred a jump in US Treasury bond yields, which lifted the Dollar. Therefore, the USD/MXN reclaimed the psychological 18.00 figure, though it has retreated and hovers around 17.91, still posting gains of 0.25%.

The economic docket in Mexico is empty, except for August’s Retail Sales data on Friday, with estimates for a monthly basis at 0%, while annual figures are foreseen at 4.4%. Across the border, Retail Sales in September crushed estimates, and August numbers were upward revised, which could potentially influence US Federal Reserve (Fed) officials to reassess their current stance. Recently, Industrial Production exceeded last month’s figures and was unchanged annually.

Regarding geopolitical developments, which could sour market sentiment, US President Joe Biden is traveling to Israel to support the country and will meet with Israel Prime Minister Benjamin Netanyahu and Arab leaders.

Daily Digest Market Movers: Mexican Peso at the brisk of depreciating towards 18.00

- US Retail Sales in September grew by 0.7% MoM, above forecasts of 0.3%, but trailed upward revised August of 0.8%.

- Industrial Production rose 0.3% MoM, better than expected, and the previous month's 0.0% reading.

- Mexico’s 2023 GDP is expected to hit 3.2%, according to the World Bank and the International Monetary Fund.

- New York Fed Empire State Manufacturing Index for October plunged to -4.6, higher than forecasts of -7 but worse than September’s 1.9 expansion.

- Philadelphia Fed President Patrick Harker commented the current level of rates kept house buyers on the sideline, highlighting that the Fed is likely done hiking rates.

- Chicago Fed President Austan Goolsbee said the fall in US inflation is not a bleep, according to the Financial Times.

- Inflation expectations for one year rose from 3.2% to 3.8%, while for five years jumped to 3% from 2.8%.

- Mexico's Industrial Production (IP) for August improved by 5.2% YoY, exceeding forecasts of 4.6% and July’s 4.8% increase.

- Monthly, IP in Mexico rose 0.3% as expected but trailed the previous 0.5% reading.

- The US Consumer Price Index increased 3.7% YoY in September, unchanged from August but above forecasts of 3.6%.

- US core CPI dipped as expected to 4.1% from 4.3% in August.

- Mexico’s Consumer Price Index (CPI) grew by 4.45% YoY in September, slightly below the 4.47% estimated.

- The core CPI inflation in Mexico stood at a stickier 5.76% YoY, as widely estimated, but has broken below the 6% threshold.

- The Bank of Mexico (Banxico) held rates at 11.25% in September and revised its inflation projections from 3.5% to 3.87% for 2024, above the central bank’s 3% target (plus or minus 1%).

Technical Analysis: Mexican Peso drops as technical signs support a USD/MXN bullish bias

The Mexican Peso is trimming some of its Monday gains, but it remains below the 18.00 figure, maintaining its upward bias, unless the USD/MXN drops below the 200-day Simple Moving Average (SMA) at 17.75. In that case, the exotic pair could aim towards 17.50, followed by the 50-day SMA at 17.35. Contrarily, if the pair could re-test the 18.00 figure, which once broke, the pair could rally and test 18.20. Next resistance would be the October 6 high of 18.48.

Mexican Peso FAQs

What key factors drive the Mexican Peso?

The Mexican Peso (MXN) is the most traded currency among its Latin American peers. Its value is broadly determined by the performance of the Mexican economy, the country’s central bank’s policy, the amount of foreign investment in the country and even the levels of remittances sent by Mexicans who live abroad, particularly in the United States. Geopolitical trends can also move MXN: for example, the process of nearshoring – or the decision by some firms to relocate manufacturing capacity and supply chains closer to their home countries – is also seen as a catalyst for the Mexican currency as the country is considered a key manufacturing hub in the American continent. Another catalyst for MXN is Oil prices as Mexico is a key exporter of the commodity.

How do decisions of the Banxico impact the Mexican Peso?

The main objective of Mexico’s central bank, also known as Banxico, is to maintain inflation at low and stable levels (at or close to its target of 3%, the midpoint in a tolerance band of between 2% and 4%). To this end, the bank sets an appropriate level of interest rates. When inflation is too high, Banxico will attempt to tame it by raising interest rates, making it more expensive for households and businesses to borrow money, thus cooling demand and the overall economy. Higher interest rates are generally positive for the Mexican Peso (MXN) as they lead to higher yields, making the country a more attractive place for investors. On the contrary, lower interest rates tend to weaken MXN.

How does economic data influence the value of the Mexican Peso?

Macroeconomic data releases are key to assess the state of the economy and can have an impact on the Mexican Peso (MXN) valuation. A strong Mexican economy, based on high economic growth, low unemployment and high confidence is good for MXN. Not only does it attract more foreign investment but it may encourage the Bank of Mexico (Banxico) to increase interest rates, particularly if this strength comes together with elevated inflation. However, if economic data is weak, MXN is likely to depreciate.

How does broader risk sentiment impact the Mexican Peso?

As an emerging-market currency, the Mexican Peso (MXN) tends to strive during risk-on periods, or when investors perceive that broader market risks are low and thus are eager to engage with investments that carry a higher risk. Conversely, MXN tends to weaken at times of market turbulence or economic uncertainty as investors tend to sell higher-risk assets and flee to the more-stable safe havens.

The United Kingdom will release the Consumer Price Index (CPI) data on Wednesday, October 18 at 06:00 GMT and as we get closer to the release time, here are the forecasts by the economists and researchers of four major banks regarding the upcoming UK inflation print.

Headline CPI is expected to decline to 6.5% year-on-year vs. 6.7% in August while Core is also expected to fall two ticks to 6%. If so, headline inflation would be the lowest since March 2022 but still well above the 2% target.

Nomura

We forecast headline and services inflation to remain unchanged between August and September (at 6.7% and 6.8% respectively) but see a small fall in core inflation from 6.2% to 6.1%. 0.2pp. Looking further ahead, we expect headline inflation to fall to just under 4.5% by the end of this year, just over 2.5% at the end of next and a little below the 2% target at the end of 2025. As for core, we have 5.8%, 3.0% and 1.9% for the end of 2023, 2024 and 2025 respectively.

TDS

We look for September inflation data to echo the August data, with the headline rate remaining at 6.7% YoY and core edging down to 6.1% YoY. Focus for the MPC will continue to be on the services number, and here we see the YoY rate remaining 20 bps below the MPC's forecast (TDS: 6.8% YoY, BoE: 7.0%). Overall, further signs of improvements in inflation, and most importantly, a lack of a rebound after August's significant downside miss, would continue to suggest that the MPC will keep Bank Rate on hold at its November meeting.

Deutsche Bank

We expect September CPI to inch lower to 6.61% YoY and see the core gauge declining to 6.0%.

SocGen

We think the disinflationary trend should continue in September with headline inflation falling 0.2pp to 6.5% and core by 0.2pp to 6.0%.

Gold has been on a rollercoaster ride over the past month. Economists at Commerzbank analyze the yellow metal’s outlook.

Gold still expected to reach new record high of $2,100 by end-2024

We expect the Gold price to continue trending upwards in the medium to long term. That said, the recovery is likely to begin at a lower level, not to mention later than we had previously predicted. We now envisage a Gold price of roughly $1,900 at the end of December (previously $2,000).

As soon as there are clearer signs of an imminent recession in the US, i.e. from roughly next spring, rate cut speculation should increase and lend greater buoyancy to Gold. Our forecast for the Gold price at the end of 2024 therefore remains unchanged at a new record high of $2,100.

FOMC could cut rates in Q3 2024 if unfolding trends hold, according to economists at ANZ Bank.

Policy is now restrictive enough to get inflation back to 2%

We maintain our baseline view that the Fed Funds Rate (FFR) has peaked. US Federal Reserve officials appear to be gravitating toward the view that policy is now restrictive enough to get inflation back to 2%.

As confidence in peak rates builds, the question for policymakers is how long they will need to hold rates at that level. Ongoing strength in activity, employment and some inflation components imply no quick pivot.

We now expect the FOMC to first cut rates in Q3 2024. By then, we expect core inflation to be on a sustainable path towards target and there would be no reason for the FOMC to squeeze the economy with higher real rates.

- Silver price climbs to $23.00 as deepening Middle East tensions improve the safe-haven appeal.

- The US Dollar and long-term bond yields have recovered strongly after upbeat US Retail Sales data.

- Silver price jumps above the 50% Fibo retracement at $22.85.

Silver price (XAG/USD) prints a fresh two-week high at $23.00 as the appeal for bullion improves due to deepening Middle East tensions. Israel is ready for the ground invasion of the Gaza Strip from terror attacks from the Hamas military group.

The uncertainty over US President Joe Biden’s visit to Israel to support it in the war situation against Palestine and ensure the safety of civilians in Gaza has strengthened the demand for Gold and Silver.

Meanwhile, the US Dollar and long-term bond yields have recovered strongly after upbeat United States Retail Sales data. The US Census Bureau reported that consumer spending momentum expanded at a higher pace of 0.7% in September against estimates of 0.3%. Robust retail sales were prompted by upbeat demand for automobiles and dining out.

For fresh guidance on interest rates, investors shift focus to the speech from Federal Reserve (Fed) Chair Jerome Powell, which is scheduled for Thursday. It would be interesting to know whether Jerome Powell would join other teammates and support a steady interest rate policy due to rising Treasury yields or will consider some further policy-tightening appropriate.

Silver technical analysis

Silver price climbs above the 50% Fibonacci retracement (plotted from August 30 high at $25.00 to October low around $20.70) at $22.85. The white metal continues to find support from the 20-period Exponential Moving Average (EMA), which trades around $22.60.

The Relative Strength Index (RSI) (14) climbs into the bullish range of 60.00-80.00, which indicates that the bullish impulse has been activated.

Silver two-hour chart

-638331492930481587.png)

The trade-weighted US Dollar Index against a basket of 26 currencies is up more than 5% from its July low. Economists at the National Bank of Canada analyze Greenback’s outlook.

Interest rate differentials support Dollar appreciation

The USD's strength has been supported by widening interest rate differentials with its major trading partners. US yields were driven higher by resilient inflation and stronger-than-expected payroll job creation.

At this point, we still expect some USD appreciation until early 2024, which could be further boosted by renewed geopolitical tensions with the opening of a new front in an armed conflict, this time in the Middle East.

- EUR/USD partially reverses Monday’s marked gains.

- The pair could trade in a range bound theme in the short term.

EUR/USD fades the earlier bullish attempt to the 1.0580 region on Tuesday.

In case bulls regain the upper hand, the pair should surpass the monthly peak of 1.0639 (October 12) to allow for extra gains to, initially, the interim 55-day SMA at 1.0735 ahead of the weekly top of 1.0767 (September 12).

Meanwhile, further losses remain on the table as long as the pair navigates the area below the key 200-day SMA

EUR/USD daily chart

- USD/CAD jumped to near 1.3700 as US Retail Sales remained robust in September.

- The Canadian Dollar weakened as soft inflation data prompted hopes of a steady BoC policy.

- The market mood remains cautious amid deepening Middle East tensions.

The USD/CAD pair finds stellar buying interest and jumps to near the round-level resistance of 1.3700 after the United States Census Bureau reported robust consumer spending data and Statistics Canada reported a decline in price pressures in September.

US Retail Sales expanded at a robust pace of 0.7%, boosted by higher automobile demand and spending on dining out. The economic data excluding automobiles rose by 0.6%, almost at a double pace from expectations. Robust retail demand could spurt consumer inflation expectations and create discomfort for Federal Reserve (Fed) policymakers.

After upbeat US Retail Sales data, the US Dollar Index (DXY) recovered strongly to near 106.50. While expectations for interest rates at 5.25-5.50% seem unchanged for November monetary policy as Fed policymakers see higher long-term bond yields sufficient to restrict spending and investment.

Going forward, the US Dollar will dance to the tune of the speech from Fed Chair Jerome Powell, which is scheduled for Thursday. Fed Powell is expected to provide cues about the likely monetary policy action.

The market mood remains downbeat amid deepening Middle East tensions. Persistent risks of intervention by Iran and Yemen in the Israel-Palestine conflict could worsen the situation further.

On the Canadian Dollar front, a decline in consumer inflation has prompted expectations that the Bank of Canada (BoC) will keep interest rates unchanged ahead. The monthly headline and core Consumer Price Index (CPI) contracted by 0.1% while investors forecasted a growth of 0.1%. The annual headline and core CPI softened to 3.8% and 2.8% respectively.

Economists at Commerzbank analyze GBP outlook ahead of the UK Consumer Price Index (CPI) and labour market data.

Speculation about a further rate hike might gather momentum on unfavourable data

If the labour market and inflation data turn out to be unfavourable, speculation about a further rate hike might gather momentum again on the market. This would support Sterling temporarily.

However, we remain sceptical regarding the BoE’s determination to fight high levels of inflation – as the September meeting once again demonstrated – and therefore expect Sterling to ease over the coming months.

- DXY reverses Monday’s negative performance and retests 106.50.

- Further gains could see the 106.80 area revisited in the near term.

DXY manages to regain balance and advance to the 106.50 region on Tuesday.

Considering the ongoing price action, the surpass of the weekly high of 106.78 (October 12) could encourage the index to embark on a potential test of the 2023 top of 107.34 (October 3) in the short-term horizon.

In the meantime, while above the key 200-day SMA, today at 103.23, the outlook for the index is expected to remain constructive.

DXY daily chart

Economists at Rabobank expect poor levels of risk appetite to cap upside potential in AUD/USD in the months ahead.

AUD is sensitive to broad levels of risk appetite

If forthcoming domestic data releases suggest that the economic backdrop remains relatively resilient, further upside potential is likely for AUD/USD near-term as the market reassesses the risk of another RBA rate hike.

That said, the AUD is sensitive to broad levels of risk appetite. We expect that concerns over global growth and in particular the outlook for the Chinese economy, will limit upside potential for AUD/USD in the coming months.

- Industrial Production in the US continued to expand in September.

- US Dollar Index stays in positive territory after the data.

Industrial Production in the United States (US) grew 0.3% on a monthly basis in September, the Federal Reserve reported on Tuesday. This reading following the 0.4% expansion recorded in August and came in better than the market expectation for a no change.

Other details of the report revealed that the Capacity Utilization held steady at 79.7%.

Market reaction

The US Dollar Index clings to modest daily gains slightly below 106.50 after this report.

Gold may gain from risk aversion and lower opportunity costs but its path may be bumpy, strategists at UBS report.

Choppy prices in the near term

Many investors seek Gold as a portfolio diversifier in times of geopolitical tension. Gold may also gain from shifting market expectations that the Fed hiking cycle has already come to an end and that US rates could potentially come down faster next year if the implications of the war cause a faster-than-anticipated slowing in US economic activity.

Investors should note that uncertainty over both the war and the outlook for US rates may lead to choppy prices for Gold in the near term. But equally, we believe those who have long Gold positions should hold these in anticipation of a recovery over the next 6-12 months. Our forecast is for Gold to reach $1,950 by end-June 2024.

The upward trend in USD/CAD is set to continue for the rest of the year. However, economists at CIBC Capital Markets expect Loonie to recover in 2024.

More weakness before a revival in 2024

With markets almost fully priced for another quarter point BoC hike this year, and not placing high enough odds on cuts next year, a recalibration will see the Loonie end 2023 weaker, with USD/CAD likely reaching 1.39 by then.

As the market shifts to account for what we see as a higher likelihood of Fed cuts next year, that will weigh on the broad USD in 2024, supporting the Loonie in the process, with USD/CAD likely ending 2024 at 1.31.

- US Retail Sales rise by 0.7% in September, above the 0.3% of market consensus.

- Core Retail Sales increase by 0.6%, the same as Control Group Sales.

- US Dollar gains momentum after the data, DXY climbs toward daily highs.

Retail Sales in the US rose 0.7% on a monthly basis in September to $704.9 billion, the data published by US Census Bureau showed on Tuesday. This reading followed the 0.8% (revised from 0.6%) increase recorded in August and came in better than the market expectation of 0.3%.

Retail Sales Ex-Autos rose 0.6% in the same period, compared to analysts' estimate of 0.2% . Retail Sales Control Group increased 0.6%.

Market reaction

The US Dollar gathered strength against its rivals. The US Dollar Index (DXY) rebounded from 106.15 and climbed to 106.40, approaching daily highs. The next US economic report is September Industrial Production at 13:15 GMT.

- USD/JPY delivered a volatile spike as BoJ set to raise inflation forecasts for the fiscal year of 2023 and 2024.

- The market mood is risk-averse due to deepening Middle East tensions.

- Fed Daly suggested that the recent surge in long-term bond yields is equivalent to one 25 bps interest rate hike.

The USD/JPY pair cracked to near 148.80 but recovered quickly to its broader trading range around 149.50 as the Bank of Japan (BoJ) is expected to announce inflation forecasts for the fiscal year of 2023 and 2024 sooner.

Bloomberg reported on Tuesday that BoJ’s new Core CPI forecast for the fiscal year 2023 is likely to approach 3%, up from 2.5% as of July, and be set at 2% or more in sight for the fiscal year 2024. A higher inflation forecast indicates that the BoJ is confident about an increase in wages, which would drive inflation higher.

The hopes of an intervention from the Japanese authority into the FX domain are diminishing. Japanese authorities are worried about further sell-off in the Japanese Yen and are holding volatile moves responsible for them. Historically, volatility spikes remain for days for a few weeks but the appeal for the Japanese Yen is weak from some quarters due to the adaptation of easy monetary policy by the BoJ. Therefore the authorities cannot reverse the tide against weak appeal for the Japanese Yen backed by expansionary monetary policy.

Meanwhile, S&P500 futures have posted significant losses in the European session, portraying a risk-off market mood due to deepening Middle East tensions. The US Dollar Index (DXY) retreated from 106.50 as Federal Reserve (Fed) policymakers supported keeping interest rates unchanged in November.

San Francisco Fed Bank President Mary Daly suggested that the recent surge in long-term bond yields is equivalent to one 25 basis points (bps) interest rate hike. The risk of lifting interest rates further could push the economy into a recession.

USD firms modestly. Economists at Scotiabank analyze Greenback’s outlook.

Soft data risks for the US may be rising

The USD is trading firmer overall but the ‘market-weighted’ DXY is trading off its earlier highs ahead of the North American session and effectively continues to consolidate within the October trading range.

Soft data risks for the US may be rising as interest rates start to bite on the USD economy and the broader USD rally still looks prone to some technical retrenchment after the DXY’s slide back from the low 107 medium-term resistance point at the start of the month.

EUR/USD rebounds on firmer than expected ZEW survey results. Economists at Scotiabank analyze the pair’s outlook.

Firm support on dips to the 1.0500 area

Germany’s ZEW survey for October delivered better-than-expected results. The current assessment reading softened – but less than expected – to 79.9 (from 79.4 last month) while the expectations component improved to -1.1 (from -11.4), also better than forecast. The data suggest clear improvement in sentiment as the ECB rate cycle (likely) peaks. This may be a prelude to a slightly better economic performance.

Intraday EUR gains have been capped around 1.0560/1.0565 resistance again but a firm close on Monday tilts technical risks towards a bit more pressure on the upper 1.05s and firm support on EUR dips to the 1.0500 area.

A push through 1.0560 should allow the EUR to retest 1.06+.

GBP/USD slips as wage data hint at moderation. Economists at Scotiabank analyze the pair’s outlook.

UK wage data for August came in a bit softer than expected

Average earnings eased to 8.1% YoY over the August quarter, down from 8.5% in July. Ex-bonus earnings eased to 7.8%, but from an upwardly-revised 7.9% in July. Markets view the break in the rising wage trend as tilting risks against another BoE hike before year-end but wage growth remains very strong overall and there is still some key data ahead (e.g. CPI on Wednesday) which may sway thinking again.

Loss of support at 1.2125 will edge risks towards a retest of 1.20 area in the next day or so, given soft/bearish underlying momentum.

Resistance is 1.2215/1.2225.

- EUR/JPY alternates gains with losses around 158.00.

- The continuation of the side-lined trade appears on the cards.

EUR/JPY navigates within a narrow range in the 158.00 region so far on Tuesday.

Considering the ongoing performance, further consolidation appears in store for the cross for the time being. In the meantime, the breakout of this range could put the September high of 158.65 (September 13) to the test ahead of the 2023 top at 159.76 (August 30).

So far, the longer term positive outlook for the cross appears favoured while above the 200-day SMA, today at 150.42.

EUR/JPY daily chart

The USD has been strengthening again but in a gradual manner, unlike the path seen last year. In the view of economists at HSBC, USD strength could be stickier this time round.

Stickier USD strength

The countercyclical support to the USD from slowing global growth should continue, but the fastest part of the latter’s deterioration may be behind us.

Global equity market performance has held up, benefiting from the earlier optimism of central banks reaching the end of their tightening cycles. Nonetheless, the grounds for significant optimism are not as compelling as they used to be, which could end up giving the USD more support than has been the case lately.

Some may believe that USD strength will reverse soon, especially given its overvaluation. However, the USD has been steadily strengthening over the past decade and it has been overvalued, as measured by the real effective exchange rate (REER), over the same period. We believe USD strength will be sturdier this time round.

- The Greenback trades sideways as Monday was full of geopolitical headlines.

- Expect some fireworks around 12:30 GMT with US Retail Sales numbers.

- The US Dollar Index is in the middle of October’s range.

The US Dollar (USD) was the steady boyfriend on Monday in a market that had seen a wild ride in commodities. Foremost, the energy complex had a wild ride on a bunch of comments from Iran, Turkey and the US on the Israeli-Palestinian situation. The US Dollar remained steady despite the headlines and made equities soar.

On the data front, traders can sink their teeth into US Retail Sales, which are due this Tuesday an hour before the US stock market opens. As always, the print could produce a knee-jerk reaction as often the initial moves get contradicted by the revision of the previous number. In other words, brace yourself for some volatility either way.

Daily digest: US Dollar becoming data-driven

- At the start for this Tuesday, the President of the New York Fed, John Williams, is due to speak around 12:00 GMT.

- In terms of data, this Tuesday is kicking off near 12:30 GMT with the Retail Sales numbers: The monthly Retail Sales for September are expected to head lower from 0.6% to 0.3%. The Control Group number was previously at 0.1% with no expectation foreseen this time around. Retail Sales ex Autos is heading from 0.6% to 0.2%.

- At 12:55 GMT, the Redbook Index is due to come out for the week of October 13. Previous reading was 4%.

- Around 13:15 GMT, the monthly Industrial Production release for September is due. Expectations are for the print to head from 0.4% to 0%.

- Expect some headlines from Michelle Bowman, a governor on the Federal Reserve’s board, around 13:20 GMT.

- Another two numbers due to come out near 14:00 GMT: US Business Inventories for August, expected to head from 0.% to 0.3%. Additionally, the National Association of Home Builders (NAHB) is due to print the monthly Housing Market Index for October, which is expected to head from 45 to 44.

- Around 14:45 GMT, some headlines are expected from Thomas Barkin from the Federal Reserve Bank of Richmond.

- Equities are very much mixed with European and US equities on the back foot, while Asian equities advancenear 1%.