- Аналітика

- Новини та інструменти

- Новини ринків

Новини ринків

USD/MXN remains on the back foot at the lowest levels since December 2015, making rounds to 16.75 while fading the early Monday’s corrective bounce during Tuesday’s Asian session.

That said, the Mexican Peso (MXN) pair dropped in the last seven consecutive days amid broad-based US Dollar weakness, mainly driven by the concerns that the downbeat US inflation clues will prod the US Federal Reserve (Fed) from lifting interest rates past July. Adding strength to the USD/MXN bearish bias are the downbeat options market signals for the pair.

That said, the one-month Risk Reversal (RR) of the USD/MXN pair, a measure of the spread between call and put prices, dropped to -0.015 by the end of Monday’s North American trading session, reversing the late Friday’s corrective bounce.

It should be noted that the options market gauge prints the second consecutive weekly RR with a -0.015 mark at the latest, following the previous weekly figure of -0.287.

In doing so, the options market figures defy the hopes of witnessing a corrective bounce in the USD/MXN price. However, traders should keep their eyes on the US Retail Sales and Industrial Production for June for clear directions.

Also read: USD/MXN defies gravity, rises from 7-year low as global economic uncertainty simmers

The latest survey of 2,000 British people by the YouGov institute suggests that the proportion of Britons who say Brexit was a mistake hit a new record high this month.

The macro update, shared via Reuters, highlights the lesser economic benefits from the vote to leave the European Union as a wrong one, per 57% of the respondents, than 32% who cheer the Brexit verdict.

“More than half - 55% - said they would vote to rejoin the EU, against 31% who said they would stay out, if a referendum were to be held today,” reported Reuters.

YouGov also cited the results as moderately shifting from those of January 2021.

It should be noted that the survey also marked a 63% of the British people considering Brexit as a failure.

Britain braces for more military spending

Elsewhere, UK Defense Ministry is planning to spend 2.5 billion pounds ($3.3 billion) on replenishing munitions and stockpiles that have been depleted by the war in Ukraine, per Reuters.

Market implications

Both the news appears less positive for the GBP/USD price, which in turn prods the Cable pair buyers around 1.3070 amid early Tuesday’s sluggish Asian session.

Also read: GBP/USD oscillates around 1.3070 ahead of key data events

- Silver Price struggles to defend upside break of yearly horizontal resistance-turned-support.

- Bearish moving average crossover, overbought RSI (14) favor XAG/USD sellers.

- Silver bulls need validation from $25.40 to aim for $26.10-15 resistance area.

Silver Price (XAG/USD) stays defensive around $24.85-90 during early Tuesday in Asia, fading the previous day’s upside break of a seven-month-old horizontal resistance despite the late Monday’s corrective bounce off $24.50 support.

In doing so, the XAG/USD takes clues from the overbought RSI while also justifying the bear cross on the daily chart to tease the commodity sellers. That said, the 50-SMA pierces off the 100-SMA from above and portrays the “bear cross”, which in turn suggests that the Silver buyers are running out of stem.

It’s worth noting, however, that the bullish MACD signals and the aforementioned key support zone, previous resistance surrounding $24.55-50, challenge the Silver bears from entering.

Following that, a quick fall toward the $24.00 round figure can’t be ruled out. However, a convergence of the 50-SMA and 100-SMA, around $23.60-55, will restrict the XAG/USD’s further downside.

On the flip side, Silver buyers need not only to cross the latest peak of $25.00 but should also remain firmer past the $25.40 hurdle comprising multiple levels marked since early April to retake control.

Even so, the double tops bearish formation around the $26.10-15 region appears a tough nut to crack for the XAGA/USD bulls.

Silver Price: Daily chart

Trend: Pullback expected

- GBP/USD oscillates around 1.3070 ahead of the US Retail Sales data.

- Market participants anticipate the Bank of England (BoE) will hike its interest rates by 50 basis points (bps) in August.

- The US Dollar posts modest gains due to the softer Chinese growth numbers, upbeat US Empire manufacturing survey.

The GBP/USD pair consolidates in a narrow range during the early Asian session on Tuesday as the market sentiment turns cautious ahead of the release of US Retail Sales and the UK Consumer Price Index (CPI). The major is trading around 1.3072, down 0.01% on the day.

The UK will release the Consumer Price Index (CPI) for June on Wednesday, which is expected to be 8.2% YoY, from 8.7% in May, while the core CPI is estimated to be 7.1%, unchanged from May. Market participants anticipate the Bank of England (BoE) will hike its interest rates by 50 basis points (bps) in August. However, the aggressive tightening policy from the BoE to bring inflation to the target level would dampen the economic prospects of Britain's economy.

On the other hand, the US Dollar Index, as measured by the Greenback against a basket of six foreign currencies, posts modest gains due to the softer Chinese Gross Domestic Product (GDP) data for the second quarter and the upbeat US Empire manufacturing survey from July. The Federal Reserve Bank of New York reported Monday that the NY Empire State Manufacturing Index dropped from -5.5 to 1.1, above expectations of -3.5.

Looking ahead, market participants will take cue from the US Retail Sales, which expected to rise 0.5% versus 0.3% prior. However, the key focus will be Wednesday's UK Consumer Price Index (CPI). This figure would have a significant impact on the pair and help determine the next direction for the GBP/USD pair.

- EUR/USD edges higher amid hawkish ECB signals, US Dollar’s retreat.

- ECB’s Nagel cites “sticky” inflation to favor rate hike in September, ECB’s Vasle emphasizes resilient and high core inflation.

- Mixed sentiment, unimpressive US data prod US Dollar bulls ahead of US Retail Sales.

- ECB talks, second-tier US data will also be watched for clear directions as bulls struggle to cross key resistance.

EUR/USD bulls keep flirting with the 1.1250 resistance for the third consecutive day amid the early hours of Tuesday’s Asian session, staying around the highest levels since February 2022. In doing so, the Euro pair justifies hawkish bias at the European Central Bank (ECB) while cheering the US Dollar’s retreat. However, a cautious mood ahead of today’s key US Retail Sales for June and a mixed mood in the market seems to prod the major currency pair’s buyers.

On Monday, European Central Bank (ECB) policymaker Boštjan Vasle said, “We need to keep tightening policy at our next meeting.” The policymaker emphasizes the resilient and high core inflation while favoring the hawkish move.

On the same line was ECB policymaker and Bundesbank Chief Joachim Nagel who said "I expect the ECB will raise interest rates later this month by 25 bps" as core inflation in the Eurozone is ‘very sticky’ but "For the September meeting, we will see what the data will tell us."

It should be noted that the looming fears of Germany’s recession and the recent easing in China’s economic recovery seem to prod the Euro bulls and allow the US Dollar to lick its wounds despite unimpressive data at home.

On Monday, New York (NY) Empire State Manufacturing Index for July eased to 1.1 from 6.6 prior and 0.0 market forecasts. The data failed to inspire the US Dollar Index (DXY) sellers initially before weighing on the DXY, probing Friday’s recovery backed by the upbeat prints of the University of Michigan’s (UoM) Consumer Sentiment Index and consumer inflation expectations for the said month.

Elsewhere, the return of the US-China tension and the market’s consolidation ahead of late July’s Federal Open Market Committee (FOMC) Monetary Policy Meeting also prod the EUR/USD bulls.

Against this backdrop, Wall Street closed with minor gains whereas the US Treasury bond yields remained pressured.

To overcome the inaction around the key upside hurdle, US Retail Sales for June, expected to rise to 0.5% versus 0.3% prior, will be crucial to watch. Also important will be the ECB talks and the US Industrial Production for June, expected -0.1% versus -0.2% prior.

Technical analysis

A higher high on prices joins a higher high on the RSI (14) line to validate the latest AUD/USD run-up. However, a clear upside break of the 1.1250 hurdle appears necessary for the Aussie pair buyers to target the February 2022 high of near 1.1495.

That said, the pullback moves appear unimpressive unless the quote stays beyond the previous resistance line stretched from early February, around 1.1160 by the press time.

- USD/CHF starts flat, and technical indicators suggest a possible upward correction.

- Sellers target the USD/CHF below 0.8300; overbought RSI hints at fading selling pressure.

- Resistance awaits at 0.8700, followed by key Fibonacci levels.

USD/CHF begins the Asian session almost flat, following Monday’s losses of 0.20% after printing a year-to-date (YTD) low of 0.8566 last Friday. Technical indicators turned flat alongside an overextended downtrend, which could pave the way for an upward correction. At the time of writing, the USD/CHF exchanges hands at 0.8605, up 0.03%.

USD/CHF Price Analysis: Technical outlook

From a daily chart perspective, the USD/CHF downtrend remains intact, with sellers eyeing a drop below the YTD low, exposing the pair to a new eight-year low below 0.8300. The Relative Strength Index (RSI) is in bearish territory but turned flat after reaching an overbought extreme level at 21.42, while the three-day Rate of Change (RoC) began to turn neutral, portraying that selling pressure faded, opening the door for a correction.

In that event, the USD/CHF first resistance would be the 0.8700 psychological level, followed by key resistance Fibonacci (Fibo) levels, with 38.2% and 50% Fibo, each at 0.8730 and 0.8780. Once those levels are cleared, the 0.8800 figure would be up next.

On the downside, the USD/CHF first support would be 0.8600, followed by the YTD low of 0.8566 and the 0.8500 psychological level.

USD/CHF Price Action – Daily chart

- AUD/USD remains depressed after two-day losing streak, fades late Monday’s corrective bounce.

- Fears surrounding China, dovish concerns about RBA joins market’s inflation woes to keep Aussie pair on the back foot.

- Fed concerns, cautious optimism in the market puts a floor under the price.

- RBA Minutes will justify catalysts for “finely balanced” pause to rate hikes, US Retail Sales eyed amid Fed blackout.

AUD/USD languishes near 0.6820 after a downbeat week-start and a failure to defend the corrective bounce as traders await the Reserve Bank of Australia’s (RBA) latest monetary policy meeting minutes on early Tuesday. It’s worth noting that the Aussie pair’s latest weakness could be linked to the market’s fears of economic slowdown in China, as well as the US Dollar’s consolidation of the previous weekly loss, despite the latest retreat of the greenback. Also, concerns about the RBA’s inability to lift the interest rates further, as well as economic fears surrounding Canberra, weigh on the risk-barometer pair ahead of the key data/events.

On Monday, China’s headline statistics confirmed the market’s fears that Australia’s biggest customer is facing economic headwinds, which in turn joined the US-China chatters to flag fears surrounding Beijing and exert downside pressure on the AUD/USD.

That said, China’s second quarter (Q2) 2023 Gross Domestic Product (GDP) rose past the previous readings of 4.5% to 6.3% but eased below the analysts’ estimations of 7.3%. Further, the Industrial Production growth jumped to 4.4% YoY in June, compared to the 2.7% expected and 3.5% prior. However, the Retail Sales slumped to 3.1% from 12.7% prior and 3.2% market consensus. It should be noted that China’s June survey-based Jobless Rate for 24-year-olds jumped to a record high of 21.3%.

Elsewhere, US Treasury Secretary Janet Yellen said during a Bloomberg interview that the US is looking carefully at outbound investment controls on China while adding, “But they would be focused on a few sectors." The policymaker also clarified that these would not be broad controls that would have a fundamental impact on the investment climate in China. During the weekend, US Treasury Secretary Yellen spoke at a meeting of Group of 20 (G20) finance ministers and central bankers in India while saying, “I am eager to build on the groundwork that we laid in Beijing to mobilize further action.” Hence, the US-China tension is back in the spotlight but the pace of pessimism appears slow and mixed.

It’s worth mentioning that Australian Treasurer Jim Chalmers flagged economic fears for the Pacific major and exerted downside pressure on the AUD/USD.

Alternatively, softer prints of the New York (NY) Empire State Manufacturing Index for July, to 1.1 from 6.6 prior and 0.0 market forecasts, joined the market’s risk-on mood, to allow the AUD/USD bears to take a breather.

While portraying the mood, Wall Street closed with minor gains whereas the US Treasury bond yields remained pressured.

Looking ahead, the RBA Minutes will be observed to gauge the catalysts behind the pause in a rate hike trajectory and predict the future moves of the Australian central bank, which in turn can help the AUD/USD bears in case of posting dovish remarks. It should be observed that the incoming RBA Governor Michele Bullock isn’t known as a hawk and hence downbeat RBA Minutes and the aforementioned pessimism can allow her to keep the easy money policy on the table.

Elsewhere, US Retail Sales for June, expected to rise to 0.5% versus 0.3% prior, can help the US Dollar to grind higher amid the Fed policymaker’s blackout ahead of late July’s Federal Open Market Committee (FOMC) Monetary Policy Meeting.

Technical analysis

A clear U-turn from the 0.6900 mark directs AUD/USD bears toward a one-week-old rising support line surrounding 0.6765, a break of which will highlight the 200-DMA level of 0.6710 as the key challenge for the bears before retaking control.

- GBP/JPY bulls come up to test critical resistance.

- The bears are on the lookout for a downside continuation for the week ahead.

GBP/JPY is testing a key resistance area following a break of daily structure as the following will illustrate:

GBP/JPY daily charts

As illustrated on the daily charts above, there is a break in market structure taking place and a correction back into the neckline of the M-formation that would be expected to act as resistance. A move back below the trendline support will possibly see a downside continuation taking place for the week ahead.

Here is what you need to know for July 18:

During the Asian session, Australia will release The Reserve Bank of Australia minutes that could offer a few insights for the August rate decision, with the governor Phillip Lowe recently signalling that the RBA is taking a data-dependent approach. Thereafter, in the US, Retail Sales will be a focus which may have advanced for a third consecutive month in June and such an outcome would be expected to support the US Dollar.

Meanwhile, on Monday, the Greenback, as measured by the US Dollar index, DXY, posted modest losses after hawkish comments from the European Central BankGoverning Council member and Bundesbank President Nagel while lower Treasury yield also weighed.

There was an initial bid in the Greenback due to the stronger-than-expected July Empire manufacturing survey and weaker-than-expected Chinese growth numbers for the second quarter along with a disappointment in the June RetailSsales data. The US July Empire manufacturing survey of general business conditions index fell -5.5 to 1.1, stronger than expectations of -3.5. The DXY index travelled between 99.753 and 100.181.

EUR/USD subsequently hit a 16-1/2 month high at 1.1249 while ECB's Nagel, said, "I expect the ECB will raise interest rates later this month by 25 bp" as core inflation in the Eurozone is "very sticky” but "for the September meeting, we will see what the data will tell us." He added, "the economic recovery in the future course of the year could be somewhat more hesitant than expected in the June forecast, and core prices will probably stay "very high over the summer."

GBP/USD fell for a second day and is making a correction of the recent rally. GBP/USD travelled between a low of 1.3087 and 1.3108 in a tight range. Market expectations of further interest-rate rises from the Bank of England combined with a resilient UK economy have been supported the Pound Sterling of late. This week will hold UK inflation and Retail Sales as the key events along with the four by-elections that are likely to get some attention.

USD/JPY on Monday fell on the weakness in the US Treasury yields that set off some short covering in the yen.

However, there is speculation the Japanese central bank, the Bank of Japan may refrain from ending its stimulus measures or changing its yield-curve control policy. The BoJ Governor Ueda said not much has changed on bond market functionality from the BOJ’s last policy meeting in June. Meanwhile, markets were closed in Japan for the Marine Day holiday.

AUD/USD was offered in a continuation of the daily correction. The pair dropped from a high of 0.6843 to a low of 0.6787. The Reserve Bank of Australia minutes will be released and are expected to provide additional insight into the Board’s “finely balanced” decision to pause in July. ''Discussion on inflation risks is likely to be balanced. We have recently changed our RBA call, pencilling in an extended pause at the current cash rate of 4.1%, but we can’t entirely rule out a hike in August,'' analysts at ANZ Bank said. ''Looking into 2024 our base case remains an extended pause before easing toward the very end of the year driven by both a higher unemployment rate and confidence inflation is returning to the band.''

Meanwhile, precious metals prices on Monday closed moderately lower as the risk-on sentiment on Wall Street took away the appeal for both Gold and Silver. Additionally, the worries over Chinese demand for industrial metals were a factor, more so for Silver. ''As fears were rising that the Fed's bark could be as bad as its bite, weaker inflation is likely to tame these concerns for now and could see the yellow metal solidify in a higher range. With that said, CTAs could modestly add to upside flow north of $1974/oz,'' analysts at TD Securities said with regards to the Gold price.

Elsewhere, Bitcoin was weaker and fell below the $30k mark on regulatory worries. Crude oil prices posted moderate losses on weaker-than-expected Chinese economic reports and the restart of crude oil production in Libya as protesters left oilfields. WTI was down some 1.5% at $74.00 from $76.05.

Like this article? Help us with some feedback by answering this survey:

- AUD/JPY stalls at 95.00, with the Tenkan-Sen cross below the Kijun-Sen.

- Key technical indicators hint at shifting to a neutral bias in the AUD/JPY pair.

- AUD/JPY bullish resumption hinges on reclaiming the Tenkan-Sen line at 94.77.

AUD/JPY losses some steam after hitting a daily high of 94.91 and aims lower by 0.34% on a risk-off impulse. The AUD/JPY pair faced the Tenkan-Sen line but failed to gain traction past the 95.00 mark, exacerbating a fall to the current exchange rate. At the time of writing, the AUD/JPY Is trading at 94.52.

AUD/JPY Price Analisis: Technical outlook

From a medium-term bias, the AUD/JPY is neutral to upward biased, but more technical indicators suggest the pair would shift neutral. The cross of the Tenkan-Sen below the Kijun-Sen, and price action moving beneath both, are the first two bearish signals. Those, along with the cross of the Chikou Span, below the June 13 daily candle, opened the door for the AUD/JPY to consolidate within the June 13 daily high and low of 93.97/95.05, eyeing a fresh catalyst to break the top/bottom of the range.

The AUD/JPY must claim the Tenkan-Sen line at 94.77 for a bullish resumption. A breach of the latter will expose the 95.00 figure, followed by the Kijun-Sen line at 95.11, which, once cleated, could pave the way for further upside past the October 21 daily high of 95.74.

Conversely, for a bearish continuation, the AUD/JPY first support would be the current week low of 94.01, followed by the July 12 swing low of 93.23. Once both support levels give way, the 93.00 psychological level would be up next.

AUD/JPY Price Action – Daily chart

- XAU/USD bull’s battle to regain the 100-day SMA at $1,955.

- The focus is set on Tuesday’s Retail Sales data from the US.

At the start of the week, the XAU/USD traded in the $1,945 - $1,960 range as the USD fought back and traded resilient at the 99.90 area. However, US Treasury yield continued declining, limiting the Gold’s downside potential.

Retail Sales are expected to have increased by 0.5% in June, while the sales excluding the Automobile sectors have expanded by 0.3%. It's worth noticing that following soft inflation figures reported last week, signs of the US weakening may take the pressure off the Federal Reserve (Fed) to continue tightening so the US Treasury yields and hence the yellow metal’s price dynamics may see volatility following the data.

As for now, market participants, as per the CME FedWatch Tool, have largely priced in 25 basis points (bps) hike in the next July 26 Fed meeting, but the odds of another hike in 2023 have fallen to 20% due to soft inflation figures. In that sense, these dovish bets on the Fed are responsible for the USD weakness, which allowed the XAU/USD to rally last week.

XAU/USD Levels to watch

The daily chart, suggests that the technical outlook for the XAU/USD is neutral to bullish as the bulls show signs of exhaustion. The Relative Strength Index (RSI) stands flat above its midline while the Moving Average Convergence Divergence (MACD) printed a lower green bar, suggesting that the buyers are losing strength.

Supports Levels: $1,945, $1,927 (20-day Simple Moving Average), $1,915.

Resistance Levels: $1,955 (100-day Simple Moving Average), $1,965, $1,990.

XAU/USD Daily chart

-638252241838409542.png)

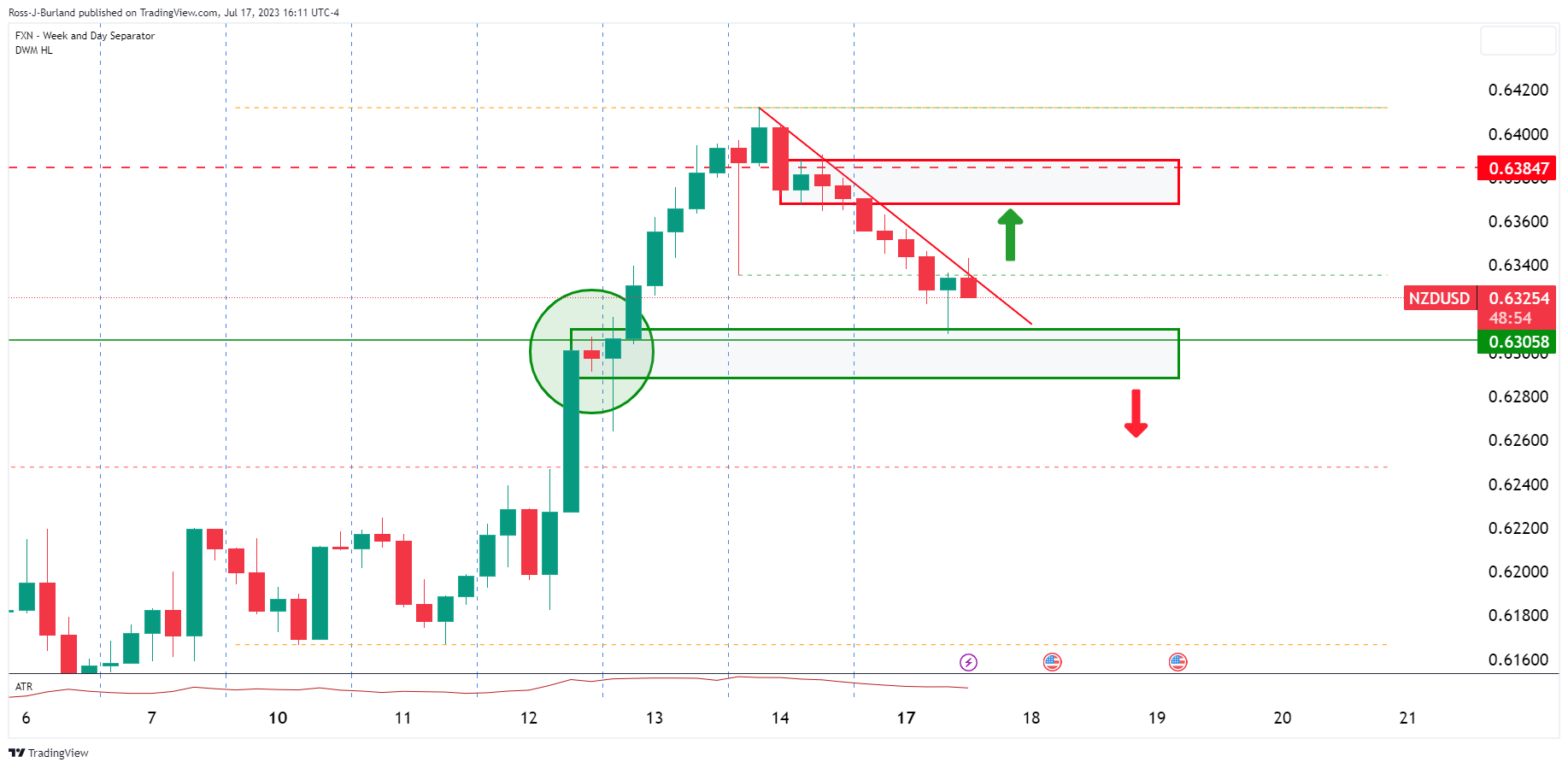

- NZD/USD bears are in the market, short-squeeze-eyed.

- Bulls eye a break of the trendline resistance following test below Friday's lows.

The New Zealand Dollar is lower by some 0.75% towards the close in New York trade and is down for the second straight session, after hitting the strongest level in over five months touched last Thursday. The price is on the front side of the dominant bearish trend and is coming into a coil which will lead to a breakout, eventually:

NZD/USD daily chart

A correction is underway and a continuation will be eyed for in due course.

NZD/USD H4 charts

We had breakout traders in the market and a long squeeze is moving in on prior resistance.

NZD/USD is on the front side of the bearish trendline and may have induced sellers due to the break below the prior day's lows. This leaves the trendline vulnerable to a break thereof and the prior support from which the downtrend originated.

- USD/CAD falls under 1.3200 as Canadian bond yields bolster CAD.

- Failure to break 1.3100 enables recovery, despite bearish RSI.

- USD/CAD’s recovery is reliant on reclaiming 1.3200, despite a bearish candle.

USD/CAD retreats below 1.3200 as the Canadian Dollar (CAD) gets underpinned by high Canadian bond yields, particularly the 10-year note at 3.385%, up 0.53%. In addition, the 20-day Exponential Moving Average (EMA), looming around the 1.3240 mark, was used by USD/CAD sellers to open fresh positions, weakening the pair. Therefore, the USD/CAD is trading at 1.3183, down 0.23%, after hitting a daily high of 1.3232.

USD/CAD Price Analysis: Technical outlook

From a technical perspective, the USD/CAD is downward biased, but failure to crack below the 1.3100 figure opened the door for recovery. After the USD/CAD printed a yearly low of 1.3092, the USD/CAD rallied towards 1.3220 before trimming some of those gains.

With the Relative Strength Index (RSI) aiming downwards at bearish territory would suggest that sellers remain in charge, except for the three-day Rate of Change (RoC), indicating that neither buyers/sellers are in control.

That said, if USD/CAD stays below 1.3200, first support emerges at 1.3150. A breach of the latter will expose the 1.3100 figure, followed by the year-to-date (YTD) low of 1.3092. Conversely, if USD/CAD buyers reclaim 1.3200, despite printing a bearish candle, that would expose the 20-day EMA at 1.3240. Once cleared, the USD/CAD would rally toward 1.3300, followed by the 50-day EMA at 1.3323, before testing the 200-day EMA at 1.3373.

USD/CAD Price Action – Daily chart

- The GBP/JPY trades with mild losses near 181.40.

- Soft Chinese data limits Yen’s upside potential.

- Eyes on Japan’s Trade Balance Data on Thursday and England’s CPI figures on Tuesday.

On Monday, the GBP/JPY cross trades near 181.40 after tallying two consecutive days of gains. The JPY’s upside potential is limited as weak Gross Domestic Product (GDP) data from Q2 and mixed Retail Sales from June from China may continue to soften the Japanese economy while markets await inflation data from the UK on Tuesday.

In the previous sessions, the markets recently speculated on a change in the bank's Yield Control Curve (YCC) due to growing local wages, which favoured the JPY, but still, there are no hints of the Bank of Japan’s (BoJ) officials. Following soft Chinese economic data, investors will focus on Trade Balance data from Japan from June to continue assessing a possible pivot from the BoJ’s ultra-dovish monetary policy stance.

On the other hand, inflation data from the UK will be Tuesday’s highlight. The Consumer Price Index (CPI) from the UK from June is expected to have dropped to 8.2% YoY from the previous 8.7%, while the Core CPI is predicted to remain unchanged at 7.1% YoY. Meanwhile, BoE’s tightening expectations remain steady as the World Interest Rate Probabilities (WIRP) tool suggests that a 50 basis points (bps) hike is largely priced in for the August 3rd meeting, followed by 25 bps hike in September, November and at the beginning of 2024.

In that sense, monetary policy divergences may continue to favour the GBP over the JPY.

GBP/JPY Levels to watch

The technical outlook for the GBP/JPY seems to have turned neutral for the short term. The Relative Strength Index (RSI) shows a flat slope while the Moving Average Convergence Divergence (MACD) remains in negative territory. To reignite momentum, the bulls must recover the 20-day Simple Moving Average (SMA) at 182.25.

Support Levels: 181.00, 180.50, 179.00.

Resistance Levels: 182.25 (20-day SMA), 182.50, 183.00.

GBP/JPY Daily chart

-638252179698182973.png)

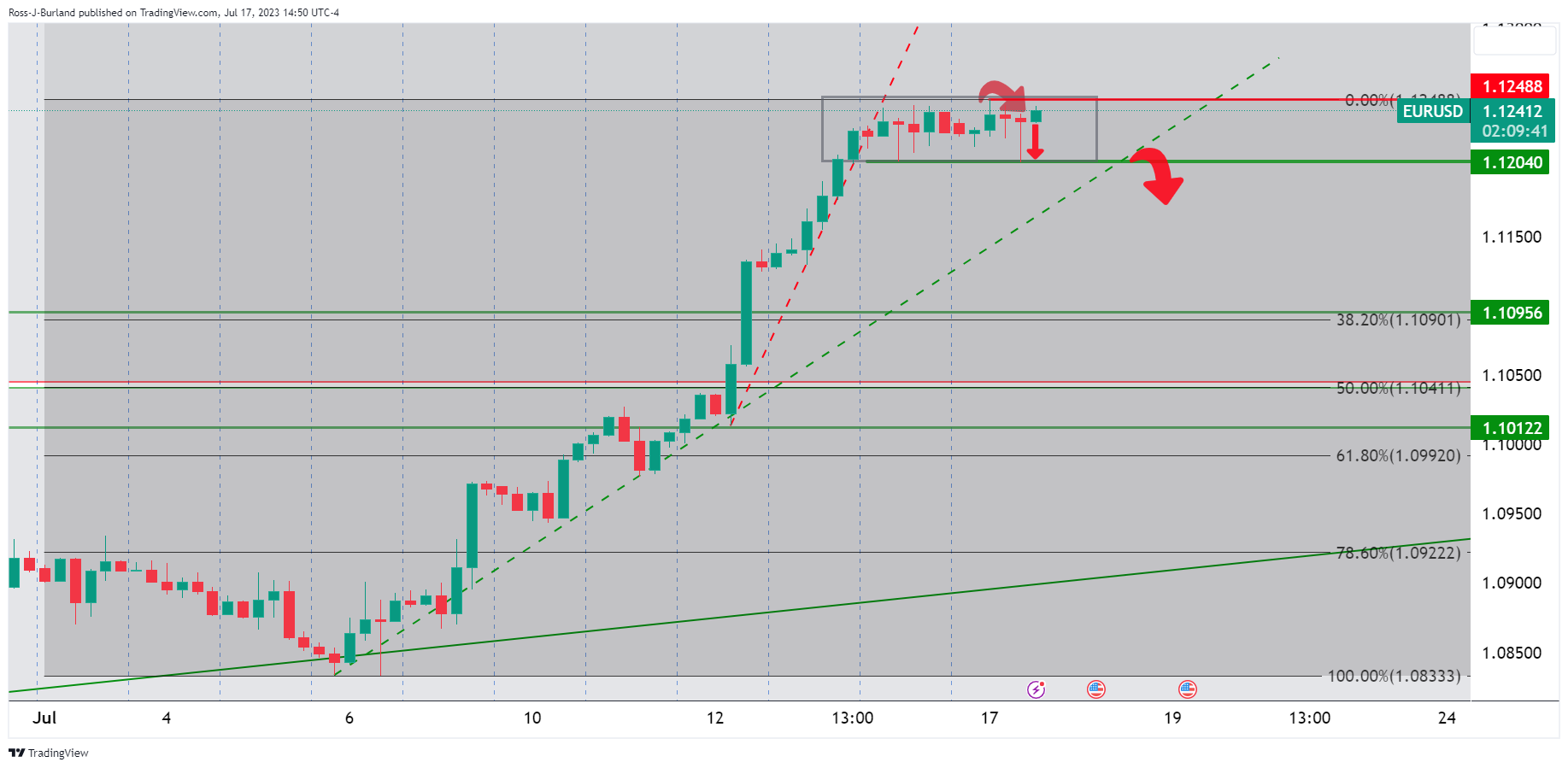

- EUR/USD bulls look to break the 1.1250s resistance.

- Bears are lurking following a series of higher closes.

EUR/USD was higher by some 0.18% in late New York trade after it fell from Monday's minor new trend high at 1.1249 to Friday's 1.12045 low before moving back to the upside with eyes on a break of channel resistance. The US Dollar is on the back foot again following last week's tumble — its biggest drop of the year — as the market prepares for US Retail Sales on Tuesday.

EUR/USD daily charts

Meanwhile, the price displaced to the upside and this could lead to a significant correction for the days ahead as the above daily chart illustrates.

EUR/USD H4 chart

The market is coiled and a breakout could be on the cards. However, the following shows, there are prospects of a bullish continuation also:

EUR/USD H1 chart

We had a recent spike to the downside as the hourly chart shows. we have subsequently rallied and a break of the 1.1250s could be imminent.

- GBP/USD suffers 0.08% drop as disappointing Chinese GDP data sparks flight to safety; exchange rate slips under 1.3100.

- Expectations of a 50 bps rate hike by the Bank of England in August maintain tension despite signs of looming UK recession.

- Upcoming UK Consumer Price Index and US Retail Sales figures heighten focus; investors gauge the impact of potential high inflation on GBP/USD trajectory.

GBP/USD lost traction during the North American session, falling below the 1.3100 figure due to an adverse market mood spurred by a weaker-than-expected economic recovery in China, which triggered a flight to safe-haven assets. The GBP/USD is trading at 1.3080, down 0.08%.

Imminent UK inflation data to keep GBP/USD within familiar levels

During the Asian session, China’s Gross Domestic Product (GDP) for the second quarter missed estimates portraying a gloomy economic outlook. Although Industrial Production expanded at a healthy rate, Retail Sales slowed sharply, from May’s 12.7% to 3.1% in June. However, data coming from the UK would greatly influence the pair.

On Wednesday, the UK will reveal the Consumer Price Index (CPI) for June, estimated at 8.2% YoY, from 8.7% in May, while the core CPI is awaited at 7.1%, unchanged from May. Expectations that the Bank of England (BoE) would raise rates by 50 bps in August remained high, with traders seeing the BoE lifting the Bank Rates to 6.25% in early 2024. Nevertheless, recent economic data indicates that the UK’s economy is at the brisk of a recession, which would be more profound, amidst high inflation levels and the BoE tightening monetary conditions.

High inflation numbers would only benefit GBP/USD longs, which could lift the exchange rate past the 2021 yearly low and the 1.3200 figure. As of writing, the US Dollar Index (DXY), a measure of the buck’s value vs. its peers, eases below the 100.000 mark, down by 0.09%, at 99.875.

Aside from this, GBP/USD traders remain laser-focused on the release of Retail Sales on Tuesday, expected to rise by 0.5%, above the prior month’s 0.3%. The latest US Consumer Sentiment report spurred speculations about June’s retail sales report, as consumers remain positive about the economy. Also, the US Federal Reserve (Fed) will unveil US Industrial production, estimated at 0% MoM, below May 0.2% expansion.

GBP/USD Price Analysis: Technical outlook

The GBP/USD remains upward biased but subject to a mean reversion move, after an overextended rally of twelve days, with the pair gaining almost 4%, though failing to crack the 2021 yearly low of 1.3160. Hence, GBP/USD sellers stepped in, dragging the price below the 1.3100 mark, which, if it holds, the GBP/USD could be headed for further losses. However, the release of important data from the United Kingdom (UK) would keep price action within familiar levels. On the downside, the GBP/USD remains below 1.3100 which could expose the 1.3000 mark, followed by the July 13 daily low of 1.2979.

- WTI sets its second day in a row of losses as investors continue to take profits following a three-week gain streak.

- Unexpected supply disruptions in Nigeria and Lybia may limit the downside’s potential.

- Eyes on Tuesday’s Retail Sales data from the US.

At the start of the week, the West Texas Intermediate (WTI) barrel fell below $75.00. The downside movements may be explained by investors taking profits and a slight recovery of the US Dollar.

The focus is set on Tuesday’s Retail Sales data from the US from June. As the USD significantly weakened following soft inflation figures from June which fueled dovish bets on the Federal Reserve (Fed), weak Retail Sales figure could fire another downwards leg for the Greenback. As for now, markets are expecting the headline figure to have increased 0.5% MoM in June while the sales excluding the Automobile sectors to have expanded 0.3% MoM.

Meanwhile, according to the CME FedWatch Tool, investors have largely priced in a 25 basis points (bps) hike in the next July 26 meeting of the Fed but the odds of another hike in 2023 have dropped to nearly 20%. In that sense, as higher interest rates tend to be negatively correlated with Oil prices, the WTI could regain momentum if markets continue to bet on a dovish Fed.

WTI Levels to watch

The daily chart suggest that the technical outlook is neutral to bearish for the short term. The Relative Strength Index (RSI) displays a negative slope but stands above its midline while the Moving Average Convergence Divergence (MACD) print lower green bars, indicating the the bullish momentum is slowly fading out. That being said, the price trading above the 100 and 20-day Simple Moving Averages (SMAs) suggests that on the bigger picture, the outlook favours the bulls.

Support Levels: $73.55 (100-day SMA), $72.80, $71.90 (20-day SMA).

Resistance Levels:$76.00, $77.00,$77.30 (200-day SMA).

WTI Daily chart

- AUD/USD registers 0.20% loss, buffeted by weak Chinese GDP and Retail Sales data; USD rebounds after its worst week since November 2022.

- US equities remain unscathed despite mixed Chinese economic data; Forex traders eye Tuesday’s US Retail Sales and Industrial Production figures.

- Leadership change at the Reserve Bank of Australia (RBA) adds an element of uncertainty; the release of RBA monetary policy meeting minutes eagerly awaited.

AUD/USD dropped from around the 0.6850 area amid a possible global economic outlook, as soft economic data from China weighed on the Australian Dollar (USD). That bolstered the US Dollar (USD), which posted its worst week since November 2022. At the time of writing, the AUD/USD is trading at 0.6822, with losses of 0.20%.

Economic slowdown in China and expectations for positive US Retail Sales, a headwind for AUD/USD

US equities shrugged off mixed data from China that painted a gloomy economic outlook after the Gross Domestic Product (GDP) in China expanded by 0.8% QoQ, beneath the first quarter (Q1) by 2.2%, while on an annual basis, the economy grew at a 6.3% pace, below 7.1% forecasts, above Q1’s 4.5%. In the meantime, Industrial Production gathered pace, while Retail Sales decelerated sharply from 12.7% in May to 3.1% in June.

A light US economic docket keeps AUD/USD traders focused on the release of Retail Sales on Tuesday, which are expected to rise by 0.5%, above the prior month’s 0.3%. The latest US Consumer Sentiment report spurred speculations about June’s retail sales report, as consumers remain optimistic about the economy. On the same day, the US Federal Reserve (Fed) will unveil US Industrial production, estimated at 0% MoM, below May 0.2% expansion.

On the Australian front, news emerged the Reserve Bank of Australia (RBA) Governor Philip Lowe would not continue as the head of the bank and would be substituted by the current Deputy Governor Michele Bullock. Aside from this, the RBA would unveil its latest monetary policy meeting minutes.

AUD/USD Price Analysis: Technical outlook

The AUD/USD rally was capped shy of breaching the 0.6900 figure, exacerbating a downward correction, past the May 10 daily high of 0.6818, with the AUD/USD extending its fall toward a daily low of 0.6787 before trimming some of its losses. A daily close above 0.6818 could pave the way for AUD/USD to retest 0.6900. A decisive break will expose the 0.7000 figure, but firstly, the AUD/USD buyers must regain the February 21 high at 0.6919. Conversely, the AUD/USD first support would be 0.6800, followed by the current week’s low of 0.6787.

- EUR/JPY tallies a three-day winning streak and trades near the 20-day SMA at 156.30.

- JPY weakened following soft Chinese economic data.

- Eyes un Japanese Trade Balance data on Thursday and on BoJ’s upcoming decision.

At the start of the week, the JPY traded soft against most of its rivals including the USD,EUR and GBP as the Yen lost traction following soft economic data from China. Investors are still modeling their expectations towards the next Bank of Japan (BoJ) decision so Trade Balance data will be closely followed.

China released mixed June Retail Sales and soft Q2 Gross Domestic Product (GDP) figures. GDP came in at 0.8% QoQ, as predicted, compared to 2.2% in Q1, while the annualised pace was 6.3%, below the expected 7.1% and 4.5% in Q1. Retail Sales came in at 3.1% YoY versus 3.3% anticipated in June significantly dropping from the previous figure of 12.7% seen May, while Industrial Production came in at 4.4% YoY beating the 2.5% projected and the previous 3.5% in May. In that sense, as China is Japan’s main trading partner, following the release of the data the JPY weakened as a lower Chinese demand could contribute to Japan’s economy to soften.

That being said, attention is set on the next Bank of Japan (BoJ) decision. The markets speculated recently with a tweak in the bank’s Yield Control Curve (YCC) on the back of rising local wages which favoured the JPY. In addition, investors will keep an eye on any macro forecasts as Bloomberg reported that its likely that the BoJ will update its inflation projections.

On the other hand, the European’s macroecononmic calendar remains scarce this week as attention turns to next week European Central Bank (ECB) decision where markets are expecting a 25 basis points (bps) hike.

EUR/JPY Levels to watch

According to the daily chart, the downwards momentum is fading out and the bulls are taking the command. The Relative Strength Index (RSI) points north standing above its midline, while the Moving Average Convergence Divergence (MACD) prints decreasing red bars signalling that the bulls are gaining traction.

Resistance Levels: 156.30 (20-day Simple Moving Average), 157.00, 158.00

Support Levels: 156.00, 155.50, 155.00.

EUR/JPY Daily chart

-638252073551022509.png)

- USD/MXN ends a six-day losing streak, jumps 0.54%, driven by a risk-off market amid weak Chinese GDP and Retail Sales data.

- Despite Wall Street’s positive opening, concerns over China’s economic slowdown overshadow optimism; awaits key US and Mexico retail sales data.

- Potential rate cut by the Bank of Mexico in December 2023, coupled with the US Federal Reserve’s upcoming policy meeting, adds uncertainty to the USD/MXN.

USD/MXN snaps six days of losses and climbs from around 7-year lows reached at 16.7062, amid a light economic calendar in Mexico and the United States (US) and a risk-off environment. Weak data from China, namely Gross Domestic Product (GDP) for Q2 and Retail Sales, spurred fears for a global economic slowdown. The USD/MXN is trading at 16.8247, up 0.54%.

China’s economic deceleration and upcoming US data weighed on the Mexican Peso

Wall Street opened in the green, though it failed to underpin the USD/MXN pair. Data during the Asian session showed that China’s GDP grew 0.8% QoQ, beneath the first quarter (Q1) 2.2%, while on an annual basis, the economy expanded at a 6.3% pace, below 7.1% estimates, but exceeded Q1’s 4.5%. In the meantime, Industrial Production exceeded forecasts, while Retail Sales decelerated sharply from 12.7% in May to 3.1% in June.

Aside from this, the upcoming economic docket in the US will witness the release of Retail Sales on Tuesday, which are expected to rise by 0.5%, above the prior month’s 0.3%. Although the latest Nonfarm Payrolls report disappointed the markets and inflation numbers flash a disinflation process, the latest University of Michigan (UoM) Consumer Sentiment report could be a prelude to a positive retail sales report.

The same day, the US Federal Reserve (Fed), whose speakers entered the blackout period ahead of the upcoming monetary policy meeting on July 25-26, will unveil US Industrial production, estimated at 0% MoM, below May 0.2% expansion.

On the Mexican front, the calendar will reveal Retail Sales until Thursday, estimated at 3.5% YoY, below April’s 3.8%. Softer-than-expected readings could show that the economy would need lower interest rates, as the Bank of Mexico (Banxico) raised more than 700 basis points, keeping the TIIE at around 11.25%. It should be said; the disinflationary process is gathering pace, putting on the table, Banxico’s first rate cut by December 2023.

USD/MXN Price Analysis: Technical outlook

From a technical standpoint, the USD/MXN is set to continue its downtrend, but a correction is on the cards. If USD/MXN reclaims the July 14 daily open at 16.9172, that could form a bullish engulfing candlestick pattern that can lift the pair toward the 20-day Exponential Moving Average (EMA) at 17.0431. Nevertheless, the latter’s confluence with the 2016 yearly low would be difficult resistance to surpass, and if it happens, that could pave the way to retesting May 17 daily low turned resistance at 17.4038. Otherwise, if resistance holds at 17.0000, the USD/MXN could retest the yearly lows, followed by the October 2015 low at 16.3267

Economists at Commerzbank share their XAU/USD forecast.

Gold to move more or less sideways around $1,950 in the coming months

We expect Gold to move more or less sideways around $1,950 in the coming months.

Towards the end of the year, we continue to see some scope for an upward move (to $2,000). This is because the Fed's sharp rate hikes (by a total of 525 bps) are likely to be felt more strongly and it will become clear that the US economy is in recession. This, in turn, should put an end to any remaining rate hike speculation.

If, in the coming year, a further decline in inflation and the weakness of the economy even make rate cuts more likely, Gold should head to its all-time high.

The downside miss in US CPI has sent the USD reeling. Economists at TD Securities analyze Greenback’s outlook.

The turn is likely to extend into H2 and through next year

The USD is in steep free fall in the wake of the latest "positive" inflation report. We have been advocating USD shorts since the positioning-induced rally in May and think the recent price action is just the start of a broader bearish turn in H2.

We assess some medium term drivers like global growth and yield curve dynamics, front-end rate momentum and relative central bank policy, and volatility and valuation mechanics. The bulk of these drivers lean against the USD, underpinning our updated outlook that the USD has much room to fall through H2 and even through most of 2024.

Loonie trades little changed after Friday’s sharp tumble. Canadian CPI data on Tuesday will be key to determining how far the CAD slide extends, economists at Scotiabank report.

Lower inflation may weigh a bit more on the CAD in the short run

The CAD slipped off its high Friday all too easily, with the USD rebound threatening to undo some (at least) of the CAD’s strength that it has accumulated over the past week following the Bank of Canada rate hike.

There is a little data out today (Wholesale Sales for May are expected to rise 1.0% in the month) but CPI data on Tuesday may be key in determining how far the CAD slide extends in the short run (headline expected to dip to 3.0%, the top of the BoC’s medium term target range).

Lower inflation may weigh a bit more on the CAD in the short run but policymakers have been clear that progress beyond 3% is expected to be harder to come by. This will not be any sort of ‘all clear’ signal.

The CAD may ease a little more in the short run before recovering.

See – Canada CPI Preview: Forecasts from five major banks, better inflation, but not yet good enough

The Pound faces another pulsating week. Economists at Société Générale analyze GBP outlook.

A drop in core inflation could rein in the pessimism about the terminal rate exceeding 6.5% next year

The release of UK CPI on Wednesday will be closely watched in light of the sea change in expectations for the BoE. The strong wage data last week and agreement by the government to increase public sector pay by around 6% cemented expectations for 50 bps in August.

GBP/USD has not been this overbought since August 2020 so could be due for a snap back.

A drop in core inflation may not temper what happens with bank rate in August but could rein in the pessimism about the terminal rate exceeding 6.5% next year.

AUD/USD strength has extended to retest and again be capped at key resistance at 0.6891/0.6901. Economists at Credit Suisse analyze the pair’s outlook.

Support at 0.6707/0.6696 to ideally hold

Our bias is to look for dips to be well-supported ahead of a retest of 0.6891/0.6901 and with the USD itself holding a large bearish continuation pattern we stay biased for a break in due course with resistance then seen at 0.6922 initially ahead of the 78.6% retracement at 0.7009.

Support stays seen at 0.6784/83 initially, below which can ease the immediate upside bias for a pullback to 0.6749/43, then 0.6707/0.6696, but with buyers expected here.

- EUR/USD now gives away some gains following new tops near 1.1250.

- A technical correction seems to be shaping up.

EUR/USD comes under pressure and puts the 1.1200 region to the test on Monday.

While the continuation of the upside momentum appears favoured in the very near term, the pair’s current overbought conditions might spark a corrective knee-jerk. Further north of the 2023 top at 1.1248 (July 17), the pair is expected to meet the next resistance level of note at the 2022 high of 1.1495 recorded on February 10.

Looking at the longer run, the positive view remains unchanged while above the 200-day SMA, today at 1.0658.

EUR/USD daily chart

Statistics Canada will release June Consumer Price Index (CPI) data on Tuesday, July 18 at 12:30 and as we get closer to the release time, here are the forecasts by the economists and researchers of five major banks regarding the upcoming Canadian inflation data.

Headline CPI is seen declining to 3.0% year-on-year vs. the prior release of 3.4%. If so, headline inflation would be the lowest since March 2021 but still above the 2% target. On a monthly basis, it is expected to show a pace of 0.3% vs. the former release of 0.4%.

TDS

We look for headline CPI to rise by 0.3% MoM as base effects pull inflation to 3.0% for the first time since March '21. Food and energy will make modest contributions on a m/m basis while shelter will remain a key source of strength on rents and MIC. Core measures should edge lower by 0.1pp to 3.75% YoY, with CPI trim/median holding stable at 3.7% on a 3m saar basis.

NBF

In Canada, the CPI could have increased by 0.2% in June (before seasonal adjustment). If we’re right, the 12-month rate of inflation should come down from 3.4% to a 27-month low of 2.9%. The core measures preferred by the Bank of Canada should decrease as well.

RBC Economics

We expect to see a 2.9% rate in June, down from 3.4% in May and just below the top end of the BoC’s 1% to 3% target. That marks a dramatic slowdown from a peak rate of 8% a year ago. But the BoC will be focused on more recent MoM growth in the range of ‘core’ measures designed to provide a better gauge of underlying broader inflation pressures. And growth in those has been stickier at rates still above the BoC target. The BoC’s preferred median and trim CPI measures have been tracking in the range of 3 ½% to 4% at an annual rate and core services excluding shelter (BoC ‘super-core’) has been running closer to 5%.

CIBC

Canadian inflation likely decelerated further in June, reaching 3.0% YoY, although that may be the low water mark for a few months as base effects become less favourable. June’s data will compare this year’s gasoline prices with the very peak of those seen in 2022, which will be the main factor behind the expected deceleration. Core (excluding food/energy) price pressures have eased, but are not yet back to levels consistent with a 2% inflation target. However, food prices remain the primary source of inflationary pressure now, with less sign of deceleration than witnessed recently in the US.

Citi

We expect a 0.4% MoM increase in headline CPI in June, a similar increase as in May but with base effects still pushing the YoY reading lower to 3.1%. If anything, risks appear tilted slightly to the downside. The most important element of CPI data over the coming months will be the average of the annualized 3-month pace of CPI-trim and CPI-median that have remained stably too high in a 3.5-4% range for close to a year. But the substantial increase in April will drop out of the 3-month period in July suggesting 3-month core inflation will likely fall below this range in July, and thus create doubt around the need for still-higher rates in September as core inflation slows.

- USD/CHF is looking for a stabilized auction above 0.8600 amid a recovery in the US Dollar Index.

- US equities are expected to remain uncertain as further movement will be guided by the second-quarter result season.

- Fed Waller commented that two more interest rate hikes are still appropriate by the year-end.

The USD/CHF pair is aiming for stability above the round-level resistance of 0.8600 in the early New York session. The Swiss Franc asset has found some strength as the US Dollar Index (DXY) has printed a fresh day’s high after building a base below the psychological resistance of 100.00.

S&P500 is expected to open on a muted note following cues from overnight action in futures. US equities are expected to remain uncertain as further movement will be guided by the second-quarter result season. The overall market mood is quite cautious amid obscurity among market participants.

The US Dollar Index has refreshed its day’s high around 100.00. The action in the USD Index seems the outcome of oversold signals by momentum oscillators as fundamentals are still not supportive. Following USD’s action, the u-year US Treasury yields have also rebounded to near 3.81%.

As inflation has softened dramatically and the labor market is not extremely tight as it used to be, hopes for only one more interest rate from the Federal Reserve (Fed) by the year-end have remained firm. Contrary to that, Fed policymakers are still not convinced.

Last week, Fed Governor Christopher Waller commented that two more interest rate hikes are still appropriate by the year-end. While the commentary from Chicago Fed Bank Austan Goolsbee conveyed that inflation is progressively declining but still a lot of work to do.

On the Swiss Franc front, more interest rate hikes from the Swiss National Bank (SNB) are highly anticipated despite inflation having displayed a print below 2%. For keeping inflation steadily below 2%, SNB Chairman Thomas J. Jordan would raise interest rates further in September.

The Gold price has retreated 5% from this year’s high of $2,060. Economists at ANZ Bank analyze XAU/USD outlook.

Shifting expectations of the terminal rate are a short-term headwind

Tightness in the labour market and strong economic data are likely to keep the Fed hiking rates. This leaves a risk of pushing real rates higher in the short-term. And Gold is likely to underperform in such an environment.

Nevertheless, we hold our positive view for the medium term, as structural drivers remain intact. The ongoing decline in inflation will ultimately see the Fed pause its interest rate cycle at some point this year. Normally US yield start retreating at this point, reducing the opportunity cost for Gold investing.

A pause in rate hikes by the Fed amid other more hawkish central banks should see the US Dollar likely to weaken in the second half of this year. Further, the risk of a US recession is not completely off the table, which should attract haven fund flows into Gold into 2024.

AUD/USD retracted some of the gains made in June and formed a higher trough. Economists at Société Générale analyze the pair’s technical outlook.

At a crossroads

AUD/USD has re-established above the 200-DMA denoting regain of upward momentum. This is also highlighted by daily MACD which has been posting positive divergence and is now attempting a cross above equilibrium line.

The pair is now challenging the peak of June near 0.6890. Once this is overcome, an extended up-move is likely. Next potential objectives are located at 0.7000, the 76.4% retracement from January and 0.7160/0.7200 which represents a multiyear downsloping trend line hurdle.

Defence of the MA near 0.6700 would be crucial for persistence in up-move.

USD/JPY has reversed sharply from 145. Economists at ING analyze the pair’s outlook.

No need for intervention after all

It looks like investor positioning for a possible Bank of Japan policy tweak (28 July) and the softer US inflation data have foregone the need for intervention.

A sustained move lower in USD/JPY will require some follow-up – i.e. either from the BoJ or US data.

145 could now prove a solid cap. We target 130 for year-end.

USD/JPY – 1M 138 3M 135 6M 130 12M 120

- USD/JPY has picked strength around 138.50 following the footprints of the US Dollar Index.

- Hopes of only one more interest rate hike from the Fed have elevated due to supportive economic indicators.

- S&P500 futures have discovered some losses in Europe, portraying a cautious market mood.

The USD/JPY pair has recovered firmly to near 138.85 in the London session. The asset was demonstrating a non-directional performance amid an absence of a potential economic trigger. The recovery move has come following the footprints of the US Dollar Index (DXY). A power-pack action in the major would be propelled by the release of the monthly United States Retail Sales data.

S&P500 futures have discovered some losses in Europe, portraying a cautious market mood. US equities are expected to face tough times as the second-quarter result season has kicked off. Investors will keep an eye on banking and technology stocks amid bleak economic activities due to higher interest rates from the Federal Reserve (Fed).

The US Dollar Index (DXY) is making some serious efforts for delivering a break above the immediate resistance of 100.00. A decisive move would trigger a short-term recovery and might impact the appeal for the risk-perceived currencies. The yields offered on 10-year US Treasury bonds have dropped sharply to near 3.78%.

Hopes of only one more interest rate hike from the Fed have elevated due to supportive economic indicators. June’s inflation report has softened sharply as prices of second-hand automobiles have dropped and was sufficient to offset a mild increase in gasoline prices. The tight labor market has released some heat as Fed remained aggressively hawkish and now investors are shifting their focus toward the US Retail Sales data.

On the Japanese Yen front, the interest rate decision by the Bank of Japan (BoJ) will be keenly watched. Bloomberg reported that BoJ officials will likely raise their inflation forecast above 2% for this fiscal year at their July meeting, but their view for the following year is largely unchanged and may even be nudged down.

Investors should note that Japanese markets were closed on Monday on account of Marine Day.

USD/MXN oscillates in a narrow range around the 16.75 region. Economists at Société Générale analyze the pair's technical outlook.

Downtrend overstretched

USD/MXN has experienced a relentless downtrend after breaking below the sideways consolidation during 2021/2022. Although the move is a bit stretched, signals of a meaningful rebound are not yet visible.

Next potential objectives are at 16.60/16.40 and projections of 15.90. Achievement of these levels could result in a phase of rebound however reclaiming the 50-Day Moving Average near 17.40 is crucial for affirming a meaningful up-move.

- DXY navigates a tight range near the 100.00 mark.

- Another visit to the 2023 low remains in store near term.

DXY regains some composure and flirts with the psychological 100.00 zone on Monday.

The continuation of the decline of the dollar looks the most likely scenario for the time being. Against that, the breach of the current 2023 low at 99.57 (July 14) could spark a deeper pullback to the weekly low of 97.68 (March 30 2022).

Looking at the broader picture, while below the 200-day SMA at 104.31, the outlook for the index is expected to remain negative.

DXY daily chart

GBP/USD strength has stalled near term, but analysts at Credit Suissemaintain a bullish outlook for the 78.6% retracement of the 2021/2022 fall at 1.3414.

Support at 1.2909/03 ideally holds

GBP/USD strength has stalled near-term just ahead of price resistance at 1.3148/72, and we continue to look for this to cap at first for a pullback/pause.

With key resistance at 1.3000 broken and with the USD itself holding a large bearish continuation pattern weakness will stay seen as corrective ahead of a move above 1.3172 in due course with resistance then seen next at 1.3299/1.3300 ahead of the 78.6% retracement of the 2021/2022 fall at 1.3414, which we look to prove a tougher initial barrier.

Support is seen at 1.3020 initially, then 1.2983/75 initially, with 1.2909/03 ideally holding to keep the immediate risk higher. Below can see a deeper pullback to 1.12855/30 but with fresh buyers expected here.

In an interview with Bloomberg on Monday, US Treasury Secretary Janet Yellen said that there is a good chance that they will go ahead with outbound investment controls on China, per Reuters.

Key takeaways

"China has seen slower growth than expected after covid reopening."

"Chinese consumers are more focused on rebuilding savings; Chinese are concerned about sluggish growth."

"Not expecting a recession in the US."

"Making progress in getting inflation down."

"US tariffs on China reflected concern about unfair trade practices, those have not been addressed."

"US actions on China are not 'tit for tat', they reflect national security concerns."

"US is looking carefully at outbound investment controls on China, but they would be focused on a few sectors."

"These would not be broad controls that would have fundamental impact on investment climate in China."

"US has expressed concerns to China about hacking of government officials, private individuals."

Market reaction

These comments don't seem to be having a significant impact on risk mood. As of writing, US stock indx futures were trading little changed on the day.

-

Canadian Dollar reverses sharply lower against the US Dollar after a decline in Oil prices and strong sentiment data boosted the Buck.

-

Oil falls from weaker-than-expected Chinese growth data for Q2 and the reopening of Libya’s largest Oil field.

-

A thick knot of technical support levels just below 1.3100 further provides a technical foundation for the reversal.

The Canadian Dollar (CAD) reverses on a dime and slips lower against the US Dollar (USD) on Monday, tracking the decline in global Oil prices, Canada’s primary export. An unexpectedly strong Michigan Consumer Sentiment Index lends the USD confidence, giving momentum to the reversal in USD/CAD.

The USD/CAD pair trades in the 1.32s as the US session gets underway.

Canadian Dollar news and market movers

-

The Canadian Dollar trades lower against the US Dollar (bullish for USD/CAD) on the back of a fall in global Oil prices.

-

WTI Crude Oil declined from a peak above $77 a barrel to a low of $73.70 reached on Monday during the Asian session. Crude Oil is Canada’s largest export, so changes in price can impact on the demand and value of the CAD.

-

The fall in Oil price was put down to an unexpected slowdown in China’s second quarter GDP data and the resumption of Libyan supply after a brief outage, according to Oilprice.com.

-

Chinese GDP expanded by 6.3% in Q2 on year – below the 7.3% forecast by economists, according to data from the National Bureau of Statistics of China released on Monday morning.

-

Quarter-on-quarter Chinese GDP rose 0.8%, beating the 0.5% estimate, but lower than the 2.2% of Q1.

-

Oil prices were further depressed after Libyan production came back online following a brief outage amid protests by the Al-Zawi tribe over the kidnapping of the Libyan Finance Minister, Faraj Bumatari. His release led to the reopening of the Sharara and El Feel Oil fields on Monday, according to an analysis by Oilprice.com.

-

Several institutional analysts are bearish in the medium-term regarding the Canadian Dollar versus the US Dollar, seeing the pair likely rising to 1.37-38 during H2 of 2023.

-

Nomura expects rate differentials and greater growth in the US as the main factors driving USD/CAD higher.

-

For the National Bank of Canada, the negative effect of a global economic slowdown on commodity prices and Oil is the main factor that will drag CAD lower in H2, in a note cited on Poundsterlinglive.com.

-

After several lower-than-expected inflation releases last week put a damper on the Greenback, the release of the University of Michigan Consumer Sentiment Index on Friday reversed the slide.

-

US Michigan Consumer Sentiment rose to 72.6 in July according to preliminary data – well above the 65.5 predicted and the 64.4 previous.

-

This reinvigorated bullish expectations for US growth were overall positive for USD.

Canadian Dollar Technical Analysis: Bounces on a thick band of support

USD/CAD is in a long-term uptrend on the weekly chart, which began at the 2021 lows. Since October 2022, the exchange rate has been in a sideways consolidation within that uptrend. Given the old saying that ‘the trend is your friend’, however, the probabilities of an eventual continuation higher marginally favor longs over shorts.

USD/CAD appears to have completed a large measured move price pattern that began forming at the March highs. This pattern resembles a 3-wave ABC correction, in which the first and third waves are of a similar length (labeled waves A and C on the chart below).

-638251923659216886.png)

US Dollar vs Canadian Dollar: Weekly Chart

A confluence of support situated in the upper 1.3000s, which is made up of several longer moving averages and a major trendline, prevented last week’s decline from extending any lower and provided a foundation for a reversal on both Friday and Monday.

-638251923192210662.png)

US Dollar vs Canadian Dollar: Daily Chart

The long green up-bar that formed on Friday is a bullish engulfing Japanese candlestick reversal pattern. Combined with the long red down bar immediately before it also completes a two-bar bullish reversal pattern. If it is followed on Monday by a further bullish green close, the likelihood of a strong reversal and recovery are heightened. Taken together with the probable completion of the measured move pattern, the chances of a reversal higher are further increased.

It will take a decisive break above the 50-day Simple Moving Average (SMA) at circa 1.3400 to refresh the USD/CAD long-term uptrend. Bulls marginally have the upper hand, with the odds slightly favoring a recovery and a continuation higher.

Only a decisive break below 1.3050 would indicate the thick band of weighty support in the upper 1.30s has been definitively broken, bringing the uptrend into doubt.

A cautious start to the week leaves the USD trading mixed against its major currency peers. Shaun Osborne, Chief FX Strategist at Scotiabank, analyzes Greenback’s outlook.

The broader fall in the USD does appear to be overshooting the shift in spreads

Last week’s drop in the USD was significant – nearly 3% in DXY terms – and unusual. Investors may be divided over whether this was a one-off or whether the start of a bear phase in the USD started with a bang. The latter seems more likely; relative US growth and interest rate differentials have been a major prop for the USD during its bull run and those supports, especially yields, have been diminished.

The broader fall in the USD does appear to be overshooting the shift in spreads somewhat in the very short run but the move is not overly significant at this point and I still expect a somewhat softer USD tone to develop over the next few months as markets factor in the Fed reaching its policy cycle peak.

Senior Economist at UOB Group Alvin Liew assesses the latest Q2 GDP figures in Singapore.

Key Takeaways

Singapore’s preliminary 2Q23 GDP came in at 0.3% q/q SA, 0.7% y/y, better than Bloomberg’s and our more bearish forecasts. It was noted that the 1Q GDP growth was unchanged from the previous reading of 0.4% y/y (-0.4% q/q). While the growth outcome was soft, 2Q did manage to avoid another sequential contraction, which means Singapore have avoided a technical recession in 1H 2023.

Growth in 2Q continued to be dragged by the weakness in manufacturing (-1.3% q/q, -7.5% y/y in 2Q from -4.5% q/q, -5.3% y/y in 1Q) while services sector anchored growth as it picked up pace to 1.3% q/q, 3.0% y/y in 2Q (from 0.4% q/q, 1.8% y/y in 1Q) and construction activity also rose by 2.6% q/q, 6.6% y/y (from 0.3% q/q, 6.9% y/y in 1Q).

For now, we are keeping our more conservative GDP growth forecast of 0.7% in 2023, which is near the lower end of the official growth forecast range of 0.52.5%, reflecting our more cautious external and manufacturing outlook while the downtrend in the electronics sector has yet to find a bottom in the current cycle. We still think Singapore is not out of the woods yet in terms of the risk of a technical recession in 1H 2023, especially if the contraction in Jun manufacturing turns out much worse than MTI’s (implied) projection.

Based on MTI’s advance estimates, Singapore’s manufacturing sector contracted by -7.5% y/y in 2Q. Factoring the 6.5% y/y and 10.8% y/y contractions for industrial production in Apr and May, this implies that MTI expects the manufacturing sector to contract by a smaller -5.2% y/y in Jun. However, as we think that manufacturing may contract in excess of 10% in Jun, the risk of 2Q GDP’s 0.3% q/q growth being revised into negative territory is quite high.

- AUD/USD is oscillating above 0.6800 as the focus shifts to RBA minutes and US Retail Sales data.

- Investors are anxious to know the reasoning behind keeping interest rates unchanged at 4.10% by the RBA.

- AUD/USD has faced selling pressure while attempting to surpass the horizontal resistance plotted around 0.6900.

The AUD/USD pair is demonstrating a back-and-forth action above the round-level support of 0.6800 in the European session. The Aussie asset has turned sideways as investors are awaiting Reserve Bank of Australia (RBA) minutes, which will be published on Tuesday at 01:30 GMT. Investors are anxious to know the reasoning behind keeping interest rates unchanged at 4.10%.

Meanwhile, S&P500 futures have generated some losses in London. Losses in US-500 stocks basket futures indicate caution among market participants as firms have started posting second-quarter results.

After the soft US Consumer Price Index (CPI) and stable labor market, investors are shifting their focus on the United States monthly Retail Sales data, which will also release on Tuesday. Investors are expecting an expansion of 0.5% vs. the prior release of 0.3%. The US Dollar Index (DXY) has frozen below the psychological resistance of 100.00.

AUD/USD has faced selling pressure while attempting to surpass the horizontal resistance plotted from June 15 high at around 0.6900 on a four-hour scale. The Aussie asset has corrected to near the 20-period Exponential Moving Average (EMA) at 0.6816. The short-term trend has turned neutral while the secular-term trend is still positive.

The Relative Strength Index (RSI) (14) has slipped into the 40.00-60.00 range, which indicates that the upside momentum has faded. However, the upside bias is still intact.

Going forward, a recovery move above the intraday high at 0.6854 would expose the asset to the round-level resistance of 0.6900, followed by January 09 high around 0.6950.

In an alternate scenario, a further breakdown below July 13 high at 0.6742 would drag the Aussie asset toward July 06 high around 0.6688. Slippage below the latter would further drag the asset toward July 10 low around 0.6623.

AUD/USD four-hour chart

The Dollar continues to trade at weaker levels. USD is set to remain on weaker footing after heavy sell-off last week, economists at MUFG Bank report.

USD to continue correcting lower through the rest of this year

The Dollar has continued to sell-off since and the USS Dollar Index has now reversed almost three-quarters of the move higher recorded between the January and September of last year. It still leaves room for the USD to continue correcting lower through the rest of this year.

The latest IMM positioning report revealed that Leveraged Funds have built up short USD exposure in recent weeks but the total size of short positions are relatively modest and leaves room for further speculative selling in the near-term. However, one limitation of the report is that it only shows positioning up to the 11th July, and it is likely that short positions will have been increased further last week.

In the week ahead, there are no major US economic data releases or events that are likely to trigger a reversal of the US Dollar weakening trend ahead of the Fed’s next policy meeting on 26th July.

- EUR/JPY comes under selling pressure and revisits 155.00.

- The continuation of the uptrend appears the most likely scenario.

EUR/JPY reverses two consecutive daily gains and retests the 155.00 zone at the beginning of the week.

Despite the ongoing pullback, the cross remains poised to extend the recovery in the short-term horizon, with the immediate hurdle at the so far 2023 peak in the boundaries of 158.00 the figure (June 29).

In the meantime, the longer term positive outlook for the cross appears favoured while above the 200-day SMA, today at 145.95.

EUR/JPY daily chart

EUR/USD holds a tight range above 1.12. Economists at Scotiabank analyze the pair’s outlook.

Support seen at 1.1180/00

The EUR is firm and has not backed off last week’s highs in any significant way. Marginal new cycle highs today, limited losses ahead of 1.12 and bullish trend indicators keep the near-term focus higher.

A strong weekly close Friday (above retracement resistance and above the EUR’s 200-Week Moving Average) signal more gains ahead in the medium term (towards 1.15/16).

Support is 1.1180/00.

See – EUR/USD: Resistance at 1.1275 to cap at first, ahead of further strength to 1.1703/48 – Credit Suisse

GBP/USD consolidates as drift from the mid-1.31 area slows. Economists at Scotiabank analyze the pair’s outlook.

A bull flag pattern appears to be developing

Price action suggests that the Pound’s drift off last week’s high may be trying to base in the upper 1.3000s now. Spot looks to be consolidating the solid rise seen last week – and through July overall.

A bull flag pattern appears to be developing on the intraday chart.

Support is 1.3050/60.

Resistance is 1.3100/05, with the Pound likely to strengthen above here to retest 1.3145/50.

Goldilocks is having her day in the sun. Kit Juckes, Chief Global FX Strategist at Société Générale, analyzes FX outlook.

AUD and NZD to be weighed down by Chinese growth concerns

I think the fall in US inflation, while the US labour market remains tight and the economy continues to be supported by households spending savings accumulated in the COVID lockdowns, complicates the outlook, for the economy, the Fed and the Dollar. But it’s clear that for many (which will soon mean, the consensus) there’s a simple conclusion: Inflation has been defeated far more painlessly than feared or predicted by doom-mongering economists!

On we go to US Retail Sales and Industrial Production data this week, but it’ll take a shock to stall Goldilocks’ momentum.

The only G10 currencies which are likely to go on struggling against the Dollar, are AUD and NZD, weighed down by Chinese growth concerns, for now. What those concerns may do, is support AUD and NZD volatility, relative to the rest of the G10 currencies.

- US Dollar holds its ground early Monday after having suffered heavy losses last week.

- US Dollar Index fluctuates in a tight channel slightly below 100.00.

- US economic docket will not offer any high-impact data releases.

The US Dollar is managing to stay relatively resilient against its major rivals at the beginning of the week as markets adopt a cautious stance. The US Dollar Index (DXY) moved up and down in a tight range slightly below 100.00 on Monday after having lost more than 2% last week.

The US economic calendar will not feature any high-tier macroeconomic data releases that could impact the DXY's movements. Hence, the risk perception could continue to drive the US Dollar's valuation in the second half of the day.

China's real Gross Domestic Product (GDP) expanded at an annual rate of 6.3% in the second quarter, according to the release from China's National Bureau of Statistics (NBS) early Monday. This reading followed the 4.5% growth recorded in the first quarter but came in below the market expectation of 7.3%. Citigroup announced that they had lowered the full-year growth forecast for China to 5% from 5.5%. The Shanghai Composite lost nearly 1%, and US stock index futures traded in negative territory, reflecting the souring market mood.

Daily digest market movers: US Dollar is not out of the woods yet

- The US Dollar weakened last week as soft inflation data from the US revived expectations about the Federal Reserve reaching the terminal rate with a 25-basis-point (bps) rate hike in July.

- The Consumer Price Index (CPI) in the US rose 3% on a yearly basis in June, following the 4% increase recorded in May. The annual Producer Price Index (PPI) edged 0.1% higher in the same period.

- Commenting on the USD's outlook, "In case of an increasingly rapid fall in inflation and weakening economic data, the market might increasingly rely on key rates not remaining at high levels for a long time, whereas rate cuts before the end of the year are becoming increasingly likely," said Antje Praefcke, FX Analyst at Commerzbank. "That would cause the USD to ease further."

- The University of Michigan reported on Friday that the Consumer Confidence Index improved to 72.6 in July's flash estimate from 64.4 in May.

- The benchmark 10-year US Treasury bond yield holds steady at around 3.8% after having declined nearly 6% last week.

- The Federal Reserve Bank of New York will release the Empire State Manufacturing Survey for July.

- Markets are nearly fully pricing in a 25 bps Fed rate increase in July. The probability of one more rate hike in December stands at around 20%, according to the CME Group FedWatch Tool.

- Other data from China showed that Retail Sales increased 3.1% on a yearly basis in June, down sharply from 12.7% in May, while Industrial Production expanded 4.4% in the same period.

Technical analysis: US Dollar Index remains technically oversold

The US Dollar Index (DXY) closed in positive territory on Friday but struggled to extend its rebound on Monday. The Relative Strength Index (RSI) indicator on the daily chart remains below 30, suggesting that the DXY is still oversold. Hence, sellers could wait for a technical correction before betting on further USD weakness.

On the upside, 100.00 (psychological level) aligns as first resistance. A daily close above that level could open the door for a rebound toward 101.00 (former support, static level).

99.20 (static level from March 2022) could be seen as the next bearish target once the DXY completes a correction. Below that level, 99.00 (psychological level) is likely to act as interim support before 98.30 (200-week Simple Moving Average).

US Dollar FAQs

What is the US Dollar?

The US Dollar (USD) is the official currency of the United States of America, and the ‘de facto’ currency of a significant number of other countries where it is found in circulation alongside local notes. It is the most heavily traded currency in the world, accounting for over 88% of all global foreign exchange turnover, or an average of $6.6 trillion in transactions per day, according to data from 2022.

Following the second world war, the USD took over from the British Pound as the world’s reserve currency. For most of its history, the US Dollar was backed by Gold, until the Bretton Woods Agreement in 1971 when the Gold Standard went away.

How do the decisions of the Federal Reserve impact the US Dollar?

The most important single factor impacting on the value of the US Dollar is monetary policy, which is shaped by the Federal Reserve (Fed). The Fed has two mandates: to achieve price stability (control inflation) and foster full employment. Its primary tool to achieve these two goals is by adjusting interest rates.

When prices are rising too quickly and inflation is above the Fed’s 2% target, the Fed will raise rates, which helps the USD value. When inflation falls below 2% or the Unemployment Rate is too high, the Fed may lower interest rates, which weighs on the Greenback.

What is Quantitative Easing and how does it influence the US Dollar?

In extreme situations, the Federal Reserve can also print more Dollars and enact quantitative easing (QE). QE is the process by which the Fed substantially increases the flow of credit in a stuck financial system.

It is a non-standard policy measure used when credit has dried up because banks will not lend to each other (out of the fear of counterparty default). It is a last resort when simply lowering interest rates is unlikely to achieve the necessary result. It was the Fed’s weapon of choice to combat the credit crunch that occurred during the Great Financial Crisis in 2008. It involves the Fed printing more Dollars and using them to buy US government bonds predominantly from financial institutions. QE usually leads to a weaker US Dollar.

What is Quantitative Tightening and how does it influence the US Dollar?