- Analytics

- News and Tools

- Market News

Новини ринків

- The daily RSI shows a rise in selling traction, supported by the MACD depicting growing red bars.

- The hourly RSI indicates oversold conditions, signaling a potential pullback or bullish correction in the short term.

- Despite daily bearish tendencies, the pair still holds the 200-day SMA.

The NZD/USD pair declined to 0.6086, with a significant 0.77% downturn in Friday's session. The market sentiment leans heavily toward the sellers, however, there is a faint glimmer of hope for the buyers, as they still hold on to the 200-day Simple Moving Average (SMA).

On the daily chart, the Relative Strength Index (RSI) has fallen into negative territory, after recovering above 50 last week, which suggests increasing selling pressure. Moreover, the Moving Average Convergence Divergence (MACD) histogram features rising red bars which further indicate growing bearish sentiment in the market.

NZD/USD daily chart

Moving to the hourly chart, there is a stark contrast. The RSI values are in deep, oversold territories, indicating the recent selling pressure may be overextended. This often foretells a possible price pullback or bullish correction in the near term. Regarding the MACD histogram, the green bars suggest neutral momentum, even though they are flat, indicating no significant change in the shorter term but may also hint that the bulls are gearing up.

NZD/USD hourly chart

Taking both into account, while the daily chart may hint at a generalized negative posture, the hourly chart suggests the possibility of a reprieve for the bulls very soon. The fact that the NZD/USD pair is holding above the 200-day SMA also lends some weight to this counter-trend, bullish outlook.

- Silver's bullish streak leads above $25.00, defying broader market trends with over 1.40% gains.

- A new year-to-date high at $25.44 highlights XAG/USD’s resilience, with $26.00 now in sight as next resistance.

- Should Silver retreat below $25.00, a move towards $24.50 and potentially $24.01 could unfold, testing buyer strength.

Silver's price shines on Friday and registers solid gains of more than 1.40%, shrugging off Gold’s two consecutive days of losses. It rises 1.52%, trading at $25.18 a troy ounce at the time of writing. XAG/USD advanced even though the Greenback remains strong, underpinned by high US Treasury bond yields.

XAG/USD Price Analysis: Technical outlook

During the session, Silver printed a new year-to-date (YTD) high of $25.44, but the advance toward $26.00 was capped by an upslope support trendline that turned resistance. That sent XAG/USD retreating toward the current price levels. Nevertheless, the Relative Strength Index (RSI) indicator is still bullish, indicating that bullish momentum remains in charge, and the $26.00 resistance level could be up for grabs.

On the other hand, if XAG/USD falls below $25.00, sellers could launch an assault towards the $24.50 area, followed by the March 12 daily low of $24.01.

XAG/USD Price Action – Daily Chart

- Gold retreats from the $2,180 mark, reacting to hot US inflation data and Fed's cautious stance on policy easing.

- Rise in US Treasury yields post-PPI data release dampens XAU/USD’s appeal despite risk-off market sentiment.

- Gold remains subdued as Treasury yields inch higher and the US Dollar strengthens.

Gold spot retreated from around the $2,180 area on Friday, printing back-to-back negative sessions as market players' hope for the beginning of the US Federal Reserve's easing cycle has been delayed due to strong US economic data. Hotter-than-expected inflation figures justify Fed Chair Jerome Powell's remarks to be patient and stick to the current monetary policy stance until the disinflation process evolves. The XAU/USD trades at $2,157.66, down 0.20%.

Wall Street is set to finish Friday’s session on the back foot, reflecting a risk-off mood. Although the Gold price usually capitalizes on it, the rise of US Treasury yields after Thursday’s Producer Price Index (PPI) data kept XAU/USD offered in the European session and toward the end of the trading day.

The yellow metal remained under pressure even though US economic data failed to move the needle. The Fed revealed that Industrial Production improved in February. After that, University of Michigan Consumer Sentiment showed that Americans remain optimistic about the economic outlook.

The XAU/USD treads water as the US 10-year Treasury bond yield surges one basis point to 4.308%, while the US Dollar Index (DXY), a gauge of the buck’s performance versus other currencies, climbs 0.09% to 103.45.

Daily digest market movers: Gold retreats as US yields rise

- Friday’s economic data revealed that Industrial Production was 0.1% MoM, up from -0.5% contraction in January, and exceeded the consensus.

- Separately, the University of Michigan Consumer Sentiment on its preliminary reading was 76.5, below estimates and the previous reading of 76.9. Americans expect inflation to remain at 3% in the 12 months from March and for five years at 2.9%.

- The PPI was strong, at 1.6% YoY, up from 0.9%, while the core PPI stood at 2%, unchanged, with both figures exceeding the consensus.

- The US Department of Commerce revealed that Retail Sales missed estimates of 0.8% MoM and rose 0.6%, still an improvement compared to the prior month’s reading of -1.1%.

- The labor market remained tight as Initial Jobless Claims for the week ending March 9 dipped from 210K to 209K, below estimates of 218K.

- Given the backdrop of consumer and producer price indices in the US showcasing reaccelerating inflation, Fed officials should refrain from easing monetary policy.

- During last week's testimony at the US Congress, Fed Chairman Jerome Powell said that inflation is cooling while acknowledging that they could ease policy late in the year. However, he emphasized that it would depend on incoming data reassuring policymakers that inflation is sustainably moving toward the Fed’s 2% goal. The Fed’s next meeting is scheduled for March 19-20 next week.

- According to the CME FedWatch Tool, expectations for a May rate cut remain low, having dropped to 11% from 22%. However, the odds for June stand at 64%, down from 72%.

Technical analysis: Gold buyers take a breather below $2,170

Gold’s uptrend remains intact with the pair consolidating near the $2,160-$2,180 area. As a symmetrical triangle forms, expectations for an upside break could lift the XAU/USD toward the $2,200 figure. However, the Relative Strength Index (RSI) indicator exiting from overbought conditions suggests that buyers are taking a breather.

If buyers break the top of the range, they would challenge the current year-to-date (YTD) high of $2,195.15. Once surpassed, the $2,200 is up next. Otherwise, a drop below $2,160 might pave the way for a pullback. The first key support level would be the March 6 low of $2,123.80, followed by $2,100, followed by the December 28 high at $2,088.48 and the February 1 high at $2,065.60.

Gold FAQs

Gold has played a key role in human’s history as it has been widely used as a store of value and medium of exchange. Currently, apart from its shine and usage for jewelry, the precious metal is widely seen as a safe-haven asset, meaning that it is considered a good investment during turbulent times. Gold is also widely seen as a hedge against inflation and against depreciating currencies as it doesn’t rely on any specific issuer or government.

Central banks are the biggest Gold holders. In their aim to support their currencies in turbulent times, central banks tend to diversify their reserves and buy Gold to improve the perceived strength of the economy and the currency. High Gold reserves can be a source of trust for a country’s solvency. Central banks added 1,136 tonnes of Gold worth around $70 billion to their reserves in 2022, according to data from the World Gold Council. This is the highest yearly purchase since records began. Central banks from emerging economies such as China, India and Turkey are quickly increasing their Gold reserves.

Gold has an inverse correlation with the US Dollar and US Treasuries, which are both major reserve and safe-haven assets. When the Dollar depreciates, Gold tends to rise, enabling investors and central banks to diversify their assets in turbulent times. Gold is also inversely correlated with risk assets. A rally in the stock market tends to weaken Gold price, while sell-offs in riskier markets tend to favor the precious metal.

The price can move due to a wide range of factors. Geopolitical instability or fears of a deep recession can quickly make Gold price escalate due to its safe-haven status. As a yield-less asset, Gold tends to rise with lower interest rates, while higher cost of money usually weighs down on the yellow metal. Still, most moves depend on how the US Dollar (USD) behaves as the asset is priced in dollars (XAU/USD). A strong Dollar tends to keep the price of Gold controlled, whereas a weaker Dollar is likely to push Gold prices up.

- AUD/USD cycles just north of 0.6550.

- Little Aussie data to chew on leaves AUD/USD in the lurch.

- Next week: double-header showings from RBA and Fed.

The AUD/USD is churning just above 0.6550 as markets prepare for next week’s double feature from the Reserve Bank of Australia (RBA) and the US Federal Reserve (Fed). Both central banks are broadly expected to hold interest rates steady as investors focus on when rate cuts will come. According to the CME’s FedWatch Tool, money markets were recently thrown a curve ball, and bets of a June rate cut from the Fed have eased to 60%, down from 70% at the start of the week.

Next week also brings Australia’s latest labor and employment figures on Thursday, and median market forecasts expect Australia’s Employment Change in February to add 30K new jobs, while the Unemployment Rate is forecast to tick down to 4.0% from 4.1%. Preliminary Judo Bank Australian Purchasing Managers Index (PMI) figures for February are also scheduled for early Thursday.

Broader markets will be focusing full-bore on next Wednesday’s Fed rate statement, where the US central bank is also expected to update the Fed Dot Plot summary of interest rate expectations. The near-term end of the Dot Plot curve is expected to tick up to 5.5% from the current 4.6%. With markets pinning hopes on at least three 25 basis point rate cuts from the Fed in 2024, investor sentiment has been at odds with the Fed’s own rate outlook for the entire year. The Fed projected three rate cuts through 2024, while money markets priced in an eye-watering six or seven rate cuts through the year totaling nearly 200 basis points in rate trims for the year.

As the US economy continues to churn at a healthy clip and inflation remains stubbornly sticky, markets have had little choice but to slash rate cut expectations, and rate futures traders are half-heartedly hoping for a June rate cut.

AUD/USD technical outlook

AUD/USD spent most of the trading week on the low side, backsliding into the 200-hour Simple Moving Average (SMA) near 0.6580 on Thursday. The 50-hour and 200-hour SMAs have begun a bearish crossover near 0.6585 as intraday price action tilts into the bearish side. The Aussie-Dollar pair flubbed a brief bullish push into the 0.6640 early in the week.

Friday’s third of a percent decline has the Aussie clattering into the 200-day SMA against the US Dollar near 0.6560, and momentum is tilted into bear country as the pair fails to find bullish momentum after a rebound from the last swing low into the 0.6450 handle.

AUD/USD hourly chart

AUD/USD daily chart

- On the daily chart, sellers remain in control despite the improvement of the RSI and MACD.

- While the daily chart emits bearish signals, the hourly indicators provide a more balanced picture, showcasing an equilibrium between buyers and sellers.

- The cross saw a recovery during the American session and managed to clear daily losses.

In Friday's session, the NZD/JPY is trading at 90.70, recording a slight loss of 0.22% after bottoming at a low of 90.35. The positioning of the pair above the key 100 and 200-day Simple Moving Averages (SMAs) might hint at bullish prospects in the overall trend, yet the shorter technical outlook tilts toward the bears as it trades below the 20-day average.

On the daily chart, the NZD/JPY's Relative Strength Index (RSI) has been in negative territory, signaling that sellers have been dominant. The Moving Average Convergence Divergence (MACD) doesn't present any brighter picture either. Its histogram has flat red bars, indicating negative momentum and a lack of buying strength.

NZD/JPY daily chart

Switching to the hourly chart, the RSI recovered towards 50, the neutral level, suggesting a balance between buyers and sellers. On the other hand, the MACD histogram displays flat green bars, indicating a steady positive momentum.

NZD/JPY hourly chart

To conclude, the broader daily analysis paints a reasonably bearish picture, with the RSI and MACD indicating seller dominance and the pair below the 20-day SMA. Yet, the hourly chart presents a somewhat mixed picture, showing a balance between buyers and sellers. Considering the pair's position above the 100 and 200-day SMAs, despite the immediate bearish sentiment, the bulls might still have a chance to regain control.

Firmer US inflation prints lent support to the Dollar and US yields, underpinning at the same time the view of a Fed’s rate cut at the June gathering. On another front, EUR/USD and GBP/USD abandoned the area of recent peaks, and the Japanese yen remained in the limelight ahead of the BoJ’s potential lift-off next week.

The USD Index (DXY) climbed past the 103.00 hurdle with certain conviction, aided by rising speculation over an interest rate cut in June and the increasing likelihood of only two rate cuts (instead of three) for the current year. In the upcoming week, the NAHB Housing Market Index is due on March 18, ahead of Building Permits and Housing Starts on March 19. The Fed meets on March 20 along with the always-relevant press conference by Chair J. Powell. Usual Initial Jobless Claims, the Philly Fed Manufacturing Index, Existing Home Sales, the CB Leading Index, and flash S&P Global Manufacturing and Services PMIs are due on March 21.

EUR/USD picked up some pace after bottoming out in fresh weekly lows near 1.0870, reversing at the same time three consecutive weeks of gains. On March 18, the final Inflation Rate in the broader Euroland is due seconded by the Balance of Trade figures. The ZEW’s Economic Sentiment is expected for both Germany and the euro bloc on March 19, prior to the flash Consumer Sentiment in the euro area on March 20. March 21 will see the release of advanced Manufacturing and Services PMIs in Germany and the broader euro region, while Germany’s Business Climate tracked by the IFO institute is due at the end of the week.

The persistent risk-off mood weighed on the British pound and dragged GBP/USD to new multi-day lows near 1.2520 on Friday, ending the week with marked losses. In the UK, the Inflation Rate is due on March 20 ahead of Public Sector Net Borrowing, flash Manufacturing and Services PMIs, and the BoE interest rate decision, all on March 21. Finally, Retail Sales and the Gfk Consumer Confidence are due on March 22.

USD/JPY advanced for the fourth straight session on Friday, extending the rebound past the 149.00 barrier following lows in the mid-146.00s recorded on Monday. Machinery Orders are due on March 18, while the BoJ meeting and Industrial Production come on March 19. In addition, the Reuters Tankan Index, Balance of Trade figures, and the advanced Jibun Bank Manufacturing and Services PMIs are due on March 21. Ending the week, emerge the Inflation Rate and Foreign Bond Investment readings.

AUD/USD put the key 200-day SMA around the 0.6560 to the test on Friday, adding to Thursday’s losses and extending further the weekly leg lower. On March 18, the RBA’s Consumer Inflation Expectations come on March 18, prior to the RBA meeting on March 19. Additionally, the Q4 GDP Growth Rate and the flash Judo Bank Manufacturing and Services PMIs are scheduled for March 20. The Australian labour market report is due on March 21, ahead of the Balance of Trade results.

In China, Fixed Asset Investment, Retail Sales, Industrial Production, and the Unemployment Rate are all due on March 18. USD/CNH ended the week in a positive tone and beyond the 7.2000 barrier.

Anticipating Economic Perspectives: Voices on the Horizon

- ECB C. Lagarde speaks on March 20 along with BuBa President J. Nagel.

- BoC T. Gravelle and FOMC M. Barr speak on March 21.

- BuBa President J. Nagel, FOMC M. Barr, and Atlanta Fed R. Bostic speak on March 22.

Central Banks: Upcoming Meetings to Shape Monetary Policies

- The RBA and the BoJ will meet on March 19.

- The PBoC, the BI, and the Fed will hold their events on March 20.

- The BoE and the Norges Bank meet on March 21.

- Crude Oil is pinned into the high end to wrap up the trading week.

- WTI holding above $80.00 per barrel.

- Barrel traders pinning hopes on supply constraints looking forward.

West Texas Intermediate (WTI) US Crude Oil was pinned north of $80.00 per barrel on Friday as energy markets continued to price in expectations of a widening gap between global Crude Oil output and a forecast uptick in global Crude Oil demand through the rest of 2024 and into 2025.

The International Energy Agency (IEA) recently adjusted its forecasts, calling for a global Crude Oil deficit assuming the Organization of the Petroleum Exporting Countries (OPEC) maintains its current voluntary production caps. OPEC will meet next on June 1 to discuss output levels for the second half of 2024, and investors are broadly anticipating the Crude Oil cartel to continue squeezing quotas as tight as possible as Saudi Arabia pushes to keep barrel prices bolstered.

Declines in US Crude Oil supplies sparked a bullish lean in energy markets this week after the American Petroleum Institute (API) and the Energy Information Administration (EIA) both printed deeper drawdowns in Crude Oil stocks than expected after capacity demand at US refineries ticked up.

US Crude Oil supplies drawdown sparks risk bid

The API reported on Tuesday that Weekly Crude Oil Stocks for the week ended March 8 declined 5.5 million barrels, well below the forecast uptick of 400K barrels, engulfing the previous week’s buildup of 4423K barrels. The EIA’s Crude Oil Stocks Change for the same period showed a 1.536 million barrel decline, missing the forecast buidup of 1.338 million barrels and wiping out the previous week’s 1.367 million barrel increase.

WTI technical outlook

WTI is trading into the high end of a supply zone near the $80.00 handle after vaulting over the 200-hour Simple Moving Average (SMA) just above $78.00 earlier this week, and the 200-hour SMA is now turning bullish, rising above $78.50.

A near-term demand zone sits nearby to catch any downside moves near the $77.00 handle, and Crude Oil is holding steady after tapping a multi-month high this week.

WTI hourly chart

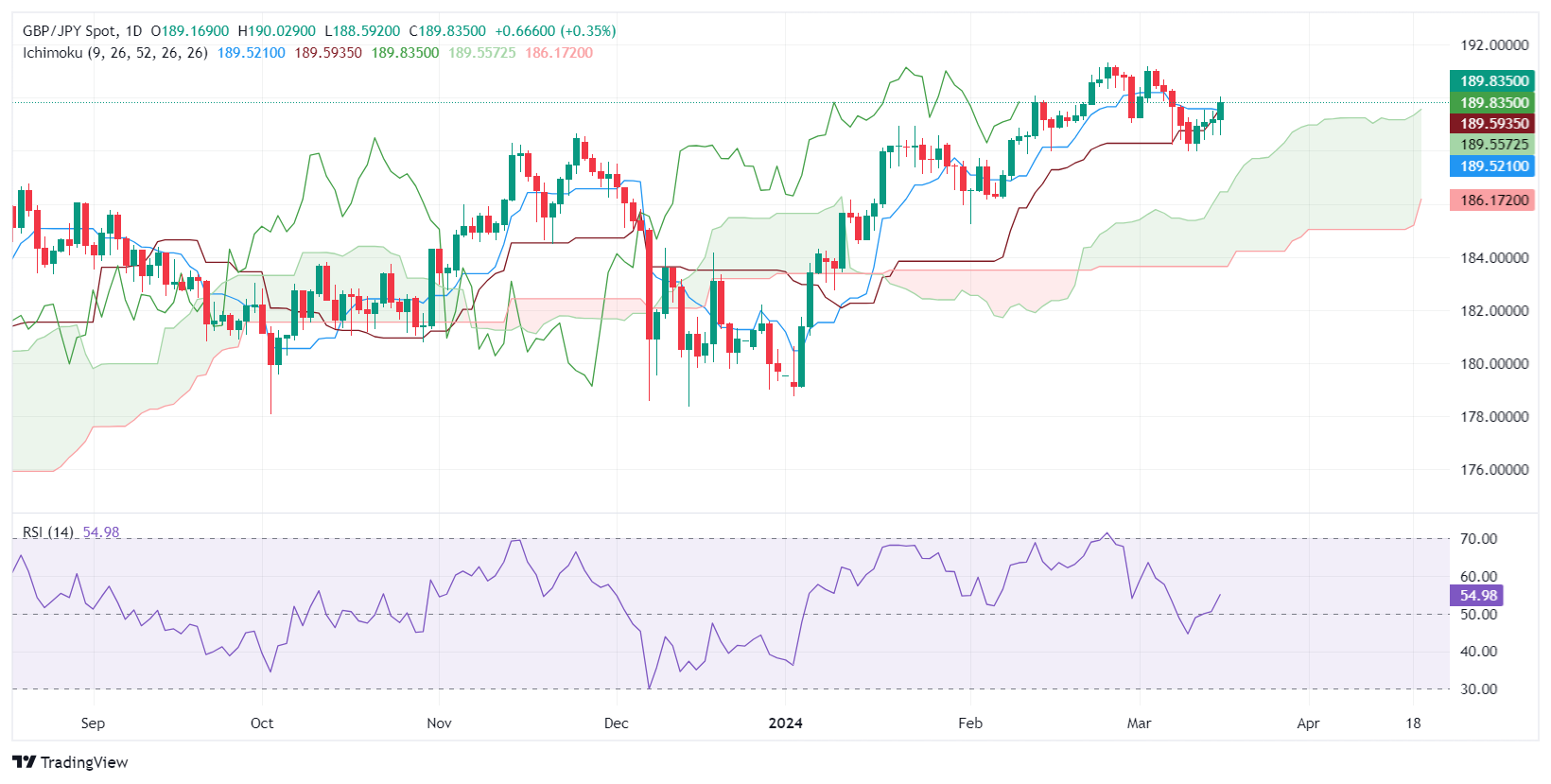

- GBP/JPY rises buoyed by uncertainty over BoJ's interest rate stance, marking a weekly gain.

- Recovery from near the 50-day DMA suggests bullish momentum, with eyes on the 190.00 resistance mark.

- A drop below the Kijun Sen could signal a correction phase, with significant support at the March 11 low.

The Pound Sterling extended its gains versus the Japanese Yen and is set to finish the week with gains, as the GBP/JPY trades at 189.72, gains 0.34%. Bank of Japan (BoJ) officials delivering mixed messages during the week prompted investors to sell the Yen as speculations grew the BoJ would not raise rates.

GBPJPY Price Analysis: Technical outlook

The cross-pair has recovered after dipping near the 50-day moving average (DMA) at 187.84, capping the GBP/JPY slide amid BoJ’s ending negative interest rates. Once those dissipated, a ‘bullish harami’ candle pattern emerged, pushing the spot prices higher. As of writing, the next resistance level would be 190.00. A breach of the latter would expose the March 4 high of 191.18, followed by the year-to-date high of 191.32.

For a bearish scenario, sellers must drag the price below the Kijun Sen o f58, ahead of the Senkou Span A at 189.64. Although this suggests that the pair is in an ongoing correction, a drop below the March 11 low of 187.96 could open the door for a deeper pullback.

GBPJPY Price Action – Daily Chart

- The pair met strong resistance at the 20-day SMA, which in case of conquering it, will confirm a bullish bias.

- The daily chart indicators suggest a strengthening upward momentum with the RSI jumping above 50.

- The hourly RSI hovers in the overbought territory, a potential sign of short-term buyer exhaustion.

In Friday's session, EUR/JPY trades with gains at 162.27, marking a 0.54% rise in attempting to conquer the 20-day Simple Moving Average (SMA). The bulls seemingly hold a strong grip, as the buying momentum appears to intensify. Yet, the sellers might come into action as the indicators flash overbought signs on the hourly signs.

Based on the indicators of the daily chart for the EUR/JPY pair, the Relative Strength Index (RSI) has moved into positive territory, suggesting a stronger upward momentum. Meanwhile, the downturn of the Moving Average Convergence Divergence (MACD) histogram prints shortening red bars, arguing in favor of a stronger bullish grip.

EUR/JPY daily chart

Turning to the hourly chart, the RSI seems to be hovering in the overbought territory. Despite a strong upward trend, this indicates potential exhaustion from the buyers. Similarly, the MACD's decreasing green bars might be signaling a shift in the tide, turning favor towards sellers for the short-term period.

EUR/JPY hourly chart

Given that the pair remains above the 100- and 200-day SMAs, yet below the 20-day SMA, it gives mixed signals regarding the broader market control. Thus, an interplay of daily and hourly charts suggests an uphill battle with the bulls maintaining control in a larger context, albeit facing potential near-term pressures.

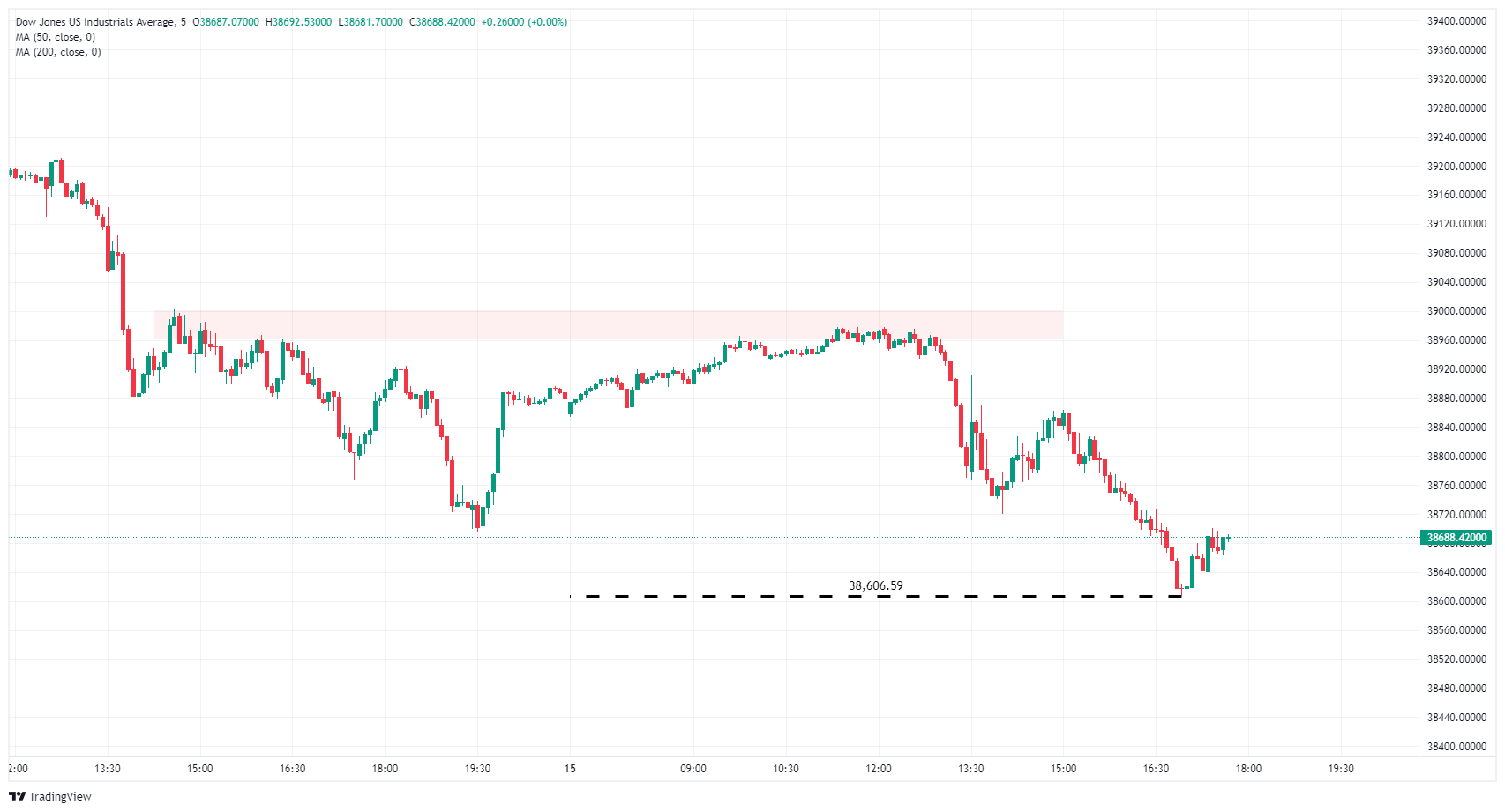

- Dow Jones follows other indices lower on Friday.

- UoM Consumer Sentiment Index ticked lower.

- June rate cut bets have edged down to 60%.

The Dow Jones Industrial Average (DJIA) is down a little over half a percent as markets round the corner into the Friday closing bell with US equities broadly lower on the day. An extended pullback in the tech and telecoms sectors are dragging down the averages, with limited gains to keep the Dow Jones on-balance as markets buckle down for the weekend.

According to the CME’s FedWatch Tool, rate futures are pricing in nearly a 41% chance of no rate movement from the Federal Reserve (Fed) at the US central bank’s June rate call. Money markets see an over 90% chance of no rate cuts from the Fed at both the March and May rate statements. The Fed’s next rate call and update to the Fed’s in-houser Dot Plot summary of rate projections are due next week at 1800 GMT on Wednesday.

The Technology Sector has extended into a four-day pullback after peaking on Monday, shedding an additional 1.4% on Friday. A 1.2% decline in the Communications Services Sector follows closely behind the Tech Sector’s pullback.\

The Materials and Industrials Sectors are in the green on Friday but doing little to counterbalance headline losses, gaining a scant 0.22% and 0.11%, respectively.

Dow Jones news

Most of the equities listed on the Dow Jones Industrial Average (DJIA) were in the red on Friday, with Microsoft Corp. (MSFT) and Salesforce Inc. (CRM) leading the losers, both shedding around 2.5%. Amazon Inc. (AMZN) followed close behind, down around 2.3% on the day.

Boeing Co. (BA) is seeing a brief reprieve from recent hard selling, rebounding 1.3% on Friday as 3M Co. (MMM) climbs around 1%. Of the 30 securities listed on the Dow Jones, over two-thirds are printing on the down side as markets prepare to exit for the weekend.

The Dow Jones Industrial Average is following its peer indices lower on Friday but is drowning slower than the others, falling around 0.6% on the day as the NASDAQ Composite sheds a full percentage point and the S&P 500 slides 0.7%.

Dow Jones Industrial Average technical outlook

The Dow Jones Industrial Average (DJIA) declined after facing an intraday rejection from a supply zone near the 39,000.00 major handle, marking in the day's bottom at 38,606.59. The index is still trading above the week's early low set on Monday near 38,470.00, but is still down 1.4% from the week's peak bids near 39,225.00.

The Dow Jones continues to churn near all-time highs set in February at 39,281.86, and the index is still up over 19% from October's lows near 32,475.00.

Dow Jones Industrial Average, 5-minute chart

Dow Jones FAQs

The Dow Jones Industrial Average, one of the oldest stock market indices in the world, is compiled of the 30 most traded stocks in the US. The index is price-weighted rather than weighted by capitalization. It is calculated by summing the prices of the constituent stocks and dividing them by a factor, currently 0.152. The index was founded by Charles Dow, who also founded the Wall Street Journal. In later years it has been criticized for not being broadly representative enough because it only tracks 30 conglomerates, unlike broader indices such as the S&P 500.

Many different factors drive the Dow Jones Industrial Average (DJIA). The aggregate performance of the component companies revealed in quarterly company earnings reports is the main one. US and global macroeconomic data also contributes as it impacts on investor sentiment. The level of interest rates, set by the Federal Reserve (Fed), also influences the DJIA as it affects the cost of credit, on which many corporations are heavily reliant. Therefore, inflation can be a major driver as well as other metrics which impact the Fed decisions.

Dow Theory is a method for identifying the primary trend of the stock market developed by Charles Dow. A key step is to compare the direction of the Dow Jones Industrial Average (DJIA) and the Dow Jones Transportation Average (DJTA) and only follow trends where both are moving in the same direction. Volume is a confirmatory criteria. The theory uses elements of peak and trough analysis. Dow’s theory posits three trend phases: accumulation, when smart money starts buying or selling; public participation, when the wider public joins in; and distribution, when the smart money exits.

There are a number of ways to trade the DJIA. One is to use ETFs which allow investors to trade the DJIA as a single security, rather than having to buy shares in all 30 constituent companies. A leading example is the SPDR Dow Jones Industrial Average ETF (DIA). DJIA futures contracts enable traders to speculate on the future value of the index and Options provide the right, but not the obligation, to buy or sell the index at a predetermined price in the future. Mutual funds enable investors to buy a share of a diversified portfolio of DJIA stocks thus providing exposure to the overall index.

- GBP/USD falls as US inflation data and retail sales reinforce a less dovish Fed outlook.

- Industrial Production in the US shows signs of recovery, contributing to the US Dollar’s resilience.

- UK labor market report influences BoE rate cut speculations, with attention on June's monetary policy.

- Market anticipation builds for next week’s Fed and BoE meetings, with inflation data set to impact GBP/USD.

The Pound Sterling is set to finish the week with losses, yet extended its downtrend for two straight days after piercing the 1.2800 figure. The GBP/USD exchanges hands at 1.2731, post losses of 0.16%.

GBP/USD retreats below 1.2800, exposing critical support levels after hot US inflation

The Greenback remains bid as traders trimmed their bets of a dovish Federal Reserve. The US Department of Labor revealed February’s consumer and producer inflation data, with figures suggesting that prices remain elevated, unable to break below the 3% threshold. In the meantime, a solid Retail Sales report failed to exceed estimates but showed an improvement compared to the prior month’s reading.

Today, the US economic schedule showed that Industrial Production rebounded on February, snapping two months of consecutive deterioration. Manufacturing output came at 0.1% MoM, up from -0.5% contraction in January, and exceeded the consensus according to data revealed by the Fed. Recently, the University of Michigan Consumer Sentiment on its preliminary reading was 76.5, below estimates and the previous reading of 76.9. Americans expect inflation to remain at 3% in the 12 months from March and for five years at 2.9%.

Across the pond, a softish labor market report weakened the Cable. A rise in the unemployment rate and a dip in Average Earnings excluding Bonuses, a measure of wage inflation, dipped from 6.2% to 6.1%. The data sparked markets to ramp up bets on a Bank of England (BoE) rate cut in June.

In the meantime, traders brace for the next week’s monetary policy decisions by the Fed and the BoE. The consensus expect both institutions to hold rates unchanged, though any dovish hints, could trigger a reaction by the financial markets. Traders would also be looking at the release of inflation figures in the UK

GBP/USD Price Analysis: Technical outlook

GBP/USD buyers failed to cling to gains above 1.2800, exacerbating a drop below the latest cycle high of 1.2827, exacerbating a pullback below the 1.2800 handles. That said, key support levels were exposed, like the 50-day moving average (DMA) at 1.2685, followed by the next cycle low seen on March 1 low at 1.2599. once those levels are cleared, the confluence of the 100 and 200-DMAs around 1.2589/1.2601 would be up next.

Pound Sterling FAQs

The Pound Sterling (GBP) is the oldest currency in the world (886 AD) and the official currency of the United Kingdom. It is the fourth most traded unit for foreign exchange (FX) in the world, accounting for 12% of all transactions, averaging $630 billion a day, according to 2022 data. Its key trading pairs are GBP/USD, aka ‘Cable’, which accounts for 11% of FX, GBP/JPY, or the ‘Dragon’ as it is known by traders (3%), and EUR/GBP (2%). The Pound Sterling is issued by the Bank of England (BoE).

The single most important factor influencing the value of the Pound Sterling is monetary policy decided by the Bank of England. The BoE bases its decisions on whether it has achieved its primary goal of “price stability” – a steady inflation rate of around 2%. Its primary tool for achieving this is the adjustment of interest rates. When inflation is too high, the BoE will try to rein it in by raising interest rates, making it more expensive for people and businesses to access credit. This is generally positive for GBP, as higher interest rates make the UK a more attractive place for global investors to park their money. When inflation falls too low it is a sign economic growth is slowing. In this scenario, the BoE will consider lowering interest rates to cheapen credit so businesses will borrow more to invest in growth-generating projects.

Data releases gauge the health of the economy and can impact the value of the Pound Sterling. Indicators such as GDP, Manufacturing and Services PMIs, and employment can all influence the direction of the GBP. A strong economy is good for Sterling. Not only does it attract more foreign investment but it may encourage the BoE to put up interest rates, which will directly strengthen GBP. Otherwise, if economic data is weak, the Pound Sterling is likely to fall.

Another significant data release for the Pound Sterling is the Trade Balance. This indicator measures the difference between what a country earns from its exports and what it spends on imports over a given period. If a country produces highly sought-after exports, its currency will benefit purely from the extra demand created from foreign buyers seeking to purchase these goods. Therefore, a positive net Trade Balance strengthens a currency and vice versa for a negative balance.

- Canadian Dollar is mostly flat on Friday with limited momentum.

- Housing Starts in Canada since November ticked higher.

- Next week: Canadian CPI inflation, US Fed rate call.

The Canadian Dollar (CAD) was mostly higher on Friday but stuck close to the day’s opening range against the US Dollar (USD) as markets shuffled in place ahead of the weekend. The University of Michigan US Consumer Sentiment Index ticked slightly lower early in the American trading session, and the highest print of Canadian Housing Starts since November sailed by without much notice from investors.

Canada brings February’s Consumer Price Index (CPI) inflation figures next week, slated for Tuesday, and markets will be quickly pivoting to face the latest rate statement from the Federal Reserve (Fed) on Wednesday. The Fed will also be updating its Dot Plot projection of interest rate expectations for the next one to five years.

Next week, the latest US Manufacturing Purchasing Managers Index (PMI) will be released on Thursday, followed by Canadian Retail Sales and the US Services PMI component on Friday. Early median market forecasts expect the US Manufacturing PMI to tick slightly lower, and Canadian Retail Sales are expected to contract.

Daily digest market movers: Data drives little chart movement, investors buckle down for the wait to Fed

- Seasonally-adjusted Canadian Housing Starts for the year ending in February rose to 253.5K, easily clearing the forecast of 230K and the previous period’s 223.2K (revised down from 223.6K).

- Canadian Wholesale Sales in January also recovered to a slim 0.1%, bouncing from the forecast of -0.6%. The previous month’s Wholesale Sales were revised to -0.3% from 0.3%. Next-to-flat prints in the revision-prone indicator are unlikely to drive much investor confidence.

- The University of Michigan’s US Consumer Sentiment Index ticked slightly lower in March down to 76.5 versus the market’s forecast hold at the previous 76.9.

- UoM 5-year Consumer Inflation Expectations in March held steady at 2.9% as US consumers remain skeptical that the Fed will successfully drag inflation below 2%.

- US MoM Industrial Production recovered a slim 0.1% in February, snubbing the market’s forecast of 0.0%, but only slightly. The previous month’s Industrial Production was revised down to -0.5% from the initial print of -0.1%.

- Next Tuesday’s Canadian CPI for the year ended February is expected to increase to 3.1% from the previous 2.9%. The Bank of Canada’s (BoC) Core Consumer Price Index (CPI) last came in at 2.4%.

- Canadian Retail Sales are also forecast to contract, with markets expecting a -0.4% print versus the previous 0.9%.

Canadian Dollar price today

The table below shows the percentage change of Canadian Dollar (CAD) against listed major currencies today. Canadian Dollar was the strongest against the New Zealand Dollar.

| USD | EUR | GBP | CAD | AUD | JPY | NZD | CHF | |

| USD | -0.05% | 0.12% | 0.00% | 0.24% | 0.49% | 0.60% | -0.06% | |

| EUR | 0.04% | 0.15% | 0.03% | 0.27% | 0.52% | 0.63% | -0.03% | |

| GBP | -0.09% | -0.14% | -0.12% | 0.14% | 0.40% | 0.51% | -0.15% | |

| CAD | 0.01% | -0.05% | 0.11% | 0.24% | 0.48% | 0.60% | -0.06% | |

| AUD | -0.24% | -0.28% | -0.11% | -0.23% | 0.24% | 0.37% | -0.30% | |

| JPY | -0.50% | -0.53% | -0.35% | -0.48% | -0.27% | 0.09% | -0.52% | |

| NZD | -0.60% | -0.65% | -0.51% | -0.60% | -0.37% | -0.13% | -0.66% | |

| CHF | 0.04% | -0.01% | 0.15% | 0.04% | 0.27% | 0.53% | 0.64% |

The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the Euro from the left column and move along the horizontal line to the Japanese Yen, the percentage change displayed in the box will represent EUR (base)/JPY (quote).

Technical analysis: Flat Friday trading as Canadian Dollar struggles to pare losses against Greenback

The Canadian Dollar (CAD) was mixed to flat on Friday, staying close to the day’s opening range against the US Dollar, Euro (EUR), and Swiss Franc (CHF). The CAD has climbed around a tenth of a percent against the Pound Sterling (GBP) and is up roughly half a percent against the Japanese Yen (JPY).

Intraday trading in the USD/CAD is stuck on the high side of 1.3500, with the day’s early high near 1.3550 and sellers failing to push the pair back below 1.3510. A near-term supply zone is pricing in a potential pullback floor near 1.3460, and intraday bids are struggling to pierce a support-turned-resistance level near 1.3550.

USD/CAD hourly chart

Canadian Dollar FAQs

The key factors driving the Canadian Dollar (CAD) are the level of interest rates set by the Bank of Canada (BoC), the price of Oil, Canada’s largest export, the health of its economy, inflation and the Trade Balance, which is the difference between the value of Canada’s exports versus its imports. Other factors include market sentiment – whether investors are taking on more risky assets (risk-on) or seeking safe-havens (risk-off) – with risk-on being CAD-positive. As its largest trading partner, the health of the US economy is also a key factor influencing the Canadian Dollar.

The Bank of Canada (BoC) has a significant influence on the Canadian Dollar by setting the level of interest rates that banks can lend to one another. This influences the level of interest rates for everyone. The main goal of the BoC is to maintain inflation at 1-3% by adjusting interest rates up or down. Relatively higher interest rates tend to be positive for the CAD. The Bank of Canada can also use quantitative easing and tightening to influence credit conditions, with the former CAD-negative and the latter CAD-positive.

The price of Oil is a key factor impacting the value of the Canadian Dollar. Petroleum is Canada’s biggest export, so Oil price tends to have an immediate impact on the CAD value. Generally, if Oil price rises CAD also goes up, as aggregate demand for the currency increases. The opposite is the case if the price of Oil falls. Higher Oil prices also tend to result in a greater likelihood of a positive Trade Balance, which is also supportive of the CAD.

While inflation had always traditionally been thought of as a negative factor for a currency since it lowers the value of money, the opposite has actually been the case in modern times with the relaxation of cross-border capital controls. Higher inflation tends to lead central banks to put up interest rates which attracts more capital inflows from global investors seeking a lucrative place to keep their money. This increases demand for the local currency, which in Canada’s case is the Canadian Dollar.

Macroeconomic data releases gauge the health of the economy and can have an impact on the Canadian Dollar. Indicators such as GDP, Manufacturing and Services PMIs, employment, and consumer sentiment surveys can all influence the direction of the CAD. A strong economy is good for the Canadian Dollar. Not only does it attract more foreign investment but it may encourage the Bank of Canada to put up interest rates, leading to a stronger currency. If economic data is weak, however, the CAD is likely to fall.

- The Greenback gears up to hold onto a 0.7% weekly gain.

- Sentiment data from the University of Michigan came in weak.

- On the bright side, Industrial Production data came in stronger than expected.

- The focus will now turn to next week’s FOMC meeting.

The US Dollar Index (DXY) is registering slight gains at the level of 103.40 on Friday, rebounding from December lows amid rising US Treasury yields. This follows the release of hot inflation data this week. The resilience of strong economic indicators and a cautious stance from the Federal Reserve (Fed) against hasty easing offer potential for US Dollar recovery. Next week, all eyes will be on the updated Federal Open Market Committee (FOMC) forecast, which could give additional traction to the USD.

Despite persistent inflation in the US, incoming data will continue to dictate the timing of the easing cycle, expected in June. Investors overlook hot inflation rates as mixed labor market data seems to have overshadowed it. Next week’s FOMC Dot Plot might also recalibrate the market’s expectations.

Daily digest market movers: US Dollar to close the week with mild gains after mid-tier data

- The University of Michigan reported the March Consumer Expectations index at 74.6, down from the previous figure of 75.2.

- The Consumer Sentiment index for March was reported at 76.5, slightly down from 76.9 in the previous period.

- The 5-Year Inflation Expectations remained steady at 2.9%.

- On the positive side, the Industrial Production (MoM) for February came in at 0.1%, which was an improvement from the previous report of -0.5%.

- US Treasury yields rise with the 2-year yield at 4.71%, the 5-year at 4.13%, and the 10-year at 4.29%.

- The market anticipates no rate cuts from the Federal Reserve in the coming week, with eyes on whether the Fed can ensure a smooth landing. Projections for a cut in May stand at 10%, while the likelihood of a June cut is around 65%.

- The market will focus on whether officials still envision three cuts in 2024.

DXY technical analysis: DXY sees a bearish undertone despite the recent bullish gains

The daily chart indicators reveal the dominance of selling momentum in DXY's technical landscape. The Relative Strength Index (RSI) prints a positive slope yet remains in negative terrain, suggesting that bears still hold the reins but with buyers building momentum. On the other hand, the Moving Average Convergence Divergence (MACD) histograms are showing decreasing red bars, highlighting decreasing selling pressure.

Adding to the bearish implications, DXY is trading below its 20, 100, and 200-day Simple Moving Averages (SMAs), pointing to a strong downtrend. This consolidation beneath the SMAs may suggest a short-term bearish outlook, offsetting any bullish attempt. Although bulls are gradually gaining ground, the prevailing selling momentum communicates strong downward pressure. Until the RSI climbs into bullish territory and MACD bars switch to the green zone, the bearish perspective will remain intact.

US Dollar FAQs

What is the US Dollar?

The US Dollar (USD) is the official currency of the United States of America, and the ‘de facto’ currency of a significant number of other countries where it is found in circulation alongside local notes. It is the most heavily traded currency in the world, accounting for over 88% of all global foreign exchange turnover, or an average of $6.6 trillion in transactions per day, according to data from 2022.

Following the second world war, the USD took over from the British Pound as the world’s reserve currency. For most of its history, the US Dollar was backed by Gold, until the Bretton Woods Agreement in 1971 when the Gold Standard went away.

How do the decisions of the Federal Reserve impact the US Dollar?

The most important single factor impacting on the value of the US Dollar is monetary policy, which is shaped by the Federal Reserve (Fed). The Fed has two mandates: to achieve price stability (control inflation) and foster full employment. Its primary tool to achieve these two goals is by adjusting interest rates.

When prices are rising too quickly and inflation is above the Fed’s 2% target, the Fed will raise rates, which helps the USD value. When inflation falls below 2% or the Unemployment Rate is too high, the Fed may lower interest rates, which weighs on the Greenback.

What is Quantitative Easing and how does it influence the US Dollar?

In extreme situations, the Federal Reserve can also print more Dollars and enact quantitative easing (QE). QE is the process by which the Fed substantially increases the flow of credit in a stuck financial system.

It is a non-standard policy measure used when credit has dried up because banks will not lend to each other (out of the fear of counterparty default). It is a last resort when simply lowering interest rates is unlikely to achieve the necessary result. It was the Fed’s weapon of choice to combat the credit crunch that occurred during the Great Financial Crisis in 2008. It involves the Fed printing more Dollars and using them to buy US government bonds predominantly from financial institutions. QE usually leads to a weaker US Dollar.

What is Quantitative Tightening and how does it influence the US Dollar?

Quantitative tightening (QT) is the reverse process whereby the Federal Reserve stops buying bonds from financial institutions and does not reinvest the principal from the bonds it holds maturing in new purchases. It is usually positive for the US Dollar.

- Mexican Peso sees modest uplift as US inflation data tempers Fed easing expectations.

- Industrial Production in Mexico shows resilience, reinforcing views on potential Banxico rate adjustments.

- Deputy Governor Omar Mejia hints at upcoming rate cuts, with a focus on maintaining restrictive monetary policy.

- US Industrial Production recovery and shifts in consumer sentiment barely move the USD/MXN currency pair.

The Mexican Peso (MXN) begins Friday’s session printing minuscule gains against the US Dollar (USD) after hot inflation figures in the United States evaporated traders' hopes for a rate cut by the US Federal Reserve (Fed).

Mexico’s weekly economic docket witnessed the release of Industrial Production data, which showed a slight improvement despite dealing with high-interest rates of 11.25% set by the Bank of Mexico (Banxico). Two days ago, Banxico’s Deputy Governor, Omar Mejia, commented that a rate cut is possible, adding that it’s not premature and that despite decreasing interest rates, it doesn’t mean monetary policy is not restrictive. The Mexican Central Bank's next meeting will be on March 21, and market participants anticipate a 25-basis-point rate cut.

Across the border, the US economic docket is slightly busier. The Fed reported that Industrial Production recovered, snapping two consecutive months of decreases. The University of Michigan recently announced that consumer sentiment slightly deteriorated compared to last month’s figures and the consensus.

Daily digest market movers: Mexican Peso counterattacks ahead of Banxico and Fed decisions

- Banxico’s Mejia commented that they have a long way to go on the disinflationary path, though he acknowledged the stickiness of services inflation. He stresses that the balance of risks for inflation is less adverse.

- Mexico’s economic schedule for the next week will feature Aggregate Demand, Private Spending, Retail Sales, Economic Activity, and inflation figures for the first half of March. Besides all this data, the highlight would be Banxico’s interest rate policy decision.

- Banxico’s private analyst poll projections for February were updated. They expect inflation at 4.10%, core CPI at 4.06%, and the economy to grow by 2.40%, unchanged from January. Regarding monetary policy, they see Banxico lowering rates to 9.50% and the USD/MXN exchange rate at 18.31, down from 18.50.

- During Banxico’s quarterly report, policymakers acknowledged the progress on inflation and urged caution against premature interest rate cuts. Governor Victoria Rodriguez Ceja said adjustments would be gradual, while Deputy Governors Galia Borja and Jonathan Heath called for prudence. The latter specifically warned against the risks of an early rate cut.

- Banxico updated its economic growth projections for 2024 from 3.0% to 2.8% YoY and maintained 1.5% for 2025. The slowdown is blamed on high interest rates at 11.25%, which sparked a shift from three of Banxico’s five governors, who are eyeing the first rate cut at the March 21 meeting.

- A Reuters poll sees the Mexican Peso depreciating 7% to 18.24 in 12 months from 16.96 on Monday, according to the median of 20 FX strategists polled between March 1-4. The forecast ranged from 15.50 to 19.00.

- A Reuters poll shows 15 analysts estimate that inflation will slow down in February, corroborating bets that Banxico could cut rates as soon as the March 21 meeting.

- US Industrial Production was 0.1% MoM, up from -0.5% contraction in January, and exceeded the consensus.

- The University of Michigan Consumer Sentiment on its preliminary reading was 76.5, below estimates and the previous reading of 76.9. Americans expect inflation to remain at 3% in the 12 months from March and for five years at 2.9%.

- Thursday’s data added to the release of the latest Consumer Price Index (CPI) report in the United States, cementing the Federal Reserve’s case for being patient about cutting interest rates. Unless data proves the disinflationary process is sustainably trending toward the 2% goal, they will stick to the “higher for longer” mantra. The next Fed meeting is scheduled for March 19-20 next week.

- Meanwhile, 52 of 108 economists expect the Fed to cut rates by 75 basis points in 2024, with 26 saying 100 bps.

- The CME FedWatch Tool shows traders decreased their bets for a 25-basis-point rate cut in June, down from 72% at the beginning of the week to 58%.

- Next week, the US economic schedule will feature medium and high-impact data.

- March 19: Housing data, led by Building Permits, Housing Starts.

- March 20: The Federal Open Market Committee (FOMC) monetary policy decision and Fed Chair Jerome Powell press conference.

- March 21: Current Account, Initial Jobless Claims, S&P Global PMI and Existing Home Sales.

- March 22: Atlanta Fed President Raphael Bostic speech.

Technical analysis: Mexican Peso stays firm with USD/MXN spot below 16.70

The USD/MXN downtrend remains intact, but after refreshing year-to-date lows of 16.64, the exotic pair seems to be oversold. The Relative Strength Index (RSI) was below the 30.00 level and remains flat, which could open the door for further downside. In that case, the next support would be last year’s low of 16.62, which, once cleared, could exacerbate a fall to challenge October 2015’s low of 16.32, followed by the 16.00 psychological level.

On the other scenario, if buyers lift the USD/MXN exchange rate toward January’s low of 16.78, that could pave the way to challenge the 17.00 figure. Key resistance levels are seen at the 50-day Simple Moving Average (SMA) at 17.03, followed by the 100-day SMA at 17.17 and the 200-day SMA at 17.21.

USD/MXN Price Action – Daily Chart

Mexican Peso FAQs

The Mexican Peso (MXN) is the most traded currency among its Latin American peers. Its value is broadly determined by the performance of the Mexican economy, the country’s central bank’s policy, the amount of foreign investment in the country and even the levels of remittances sent by Mexicans who live abroad, particularly in the United States. Geopolitical trends can also move MXN: for example, the process of nearshoring – or the decision by some firms to relocate manufacturing capacity and supply chains closer to their home countries – is also seen as a catalyst for the Mexican currency as the country is considered a key manufacturing hub in the American continent. Another catalyst for MXN is Oil prices as Mexico is a key exporter of the commodity.

The main objective of Mexico’s central bank, also known as Banxico, is to maintain inflation at low and stable levels (at or close to its target of 3%, the midpoint in a tolerance band of between 2% and 4%). To this end, the bank sets an appropriate level of interest rates. When inflation is too high, Banxico will attempt to tame it by raising interest rates, making it more expensive for households and businesses to borrow money, thus cooling demand and the overall economy. Higher interest rates are generally positive for the Mexican Peso (MXN) as they lead to higher yields, making the country a more attractive place for investors. On the contrary, lower interest rates tend to weaken MXN.

Macroeconomic data releases are key to assess the state of the economy and can have an impact on the Mexican Peso (MXN) valuation. A strong Mexican economy, based on high economic growth, low unemployment and high confidence is good for MXN. Not only does it attract more foreign investment but it may encourage the Bank of Mexico (Banxico) to increase interest rates, particularly if this strength comes together with elevated inflation. However, if economic data is weak, MXN is likely to depreciate.

As an emerging-market currency, the Mexican Peso (MXN) tends to strive during risk-on periods, or when investors perceive that broader market risks are low and thus are eager to engage with investments that carry a higher risk. Conversely, MXN tends to weaken at times of market turbulence or economic uncertainty as investors tend to sell higher-risk assets and flee to the more-stable safe havens.

Gold’s rally has not been deterred by the pushing out of expectations around the timing of Federal Reserve rate cuts. Economists at ANZ Bank analyze the yellow metal’s outlook.

Macroeconomic and geopolitical backdrop remains supportive

The timing and pace of the Federal Reserve’s rate cuts is a long-term driver for Gold. Currently, the FOMC needs more confidence that inflation is returning to 2% before considering cuts. We believe the cuts will commence from July this year. Markets are pricing-in cuts starting from H2 2024. That said, the push back in market expectations from March to June may cap the price rally.

A change in the governing party in the US would present risks around the future of policies. Amid these economic and geopolitical tensions, equity markets are hitting record high. This could potentially make investors more wary about the downside risk than upside potential. Volatility is expected to pick up as we get closer to the US elections. A risk-off scenario in equity markets will lend support to Gold prices.

EUR/USD has seen some movement in the first two months of the year but remains relatively rangebound between the 1.0750 and 1.1000 levels. Economists at the National Bank of Canada analyze the pair’s outlook.

Some volatility for the Euro expected over the next quarters

We expect some volatility for the Euro over the next quarters, especially as both the Federal Reserve and the European Central Bank policy paths become clearer.

Nonetheless, we see the common currency depreciating towards the end of the year.

BoJ hiking could help the Japanese Yen (JPY) somewhat, but for a much stronger JPY the Fed needs to cut rates markedly, economists at Nordea say.

BoJ is at the onset of raising rates after high wage growth

While the USD sets the tone for most currencies, the JPY could finally be in for some slight relief now that the BoJ is at the beginning of its hiking cycle.

We believe that the BoJ will signal next Tuesday that rates will likely be raised at the April meeting after the announcement for wage growth above 5% for the largest workers union. With wage growth the highest in three decades and inflation above 2%, the negative interest rate era in Japa is about to end. However, we don’t expect a massive rate hiking cycle from the BoJ.

The BoJ will take baby steps when hiking rates to ensure that the inflation dynamic is around 2%. As such, no major JPY strengthening will come so long as the Fed and ECB keep rates unchanged.

The recent rise in the Gold price cannot be adequately explained in fundamental terms, which is why a price correction is likely in the short term, strategists at Commerzbank say.

Will XAU/USD rally continue?

In the absence of a convincing explanation for Gold's rally, we are sceptical that the precious metal will be able to sustain its gains in the short term.

In particular, if US interest rate cut expectations take a new blow, as they did on Tuesday following another strong reading on US inflation, many investors could be tempted to take profits and the recent moderate downward correction could continue.

However, it is unlikely that prices will fall back to the levels seen at the end of February as the Fed is expected to cut interest rates from June, which should support Gold. However, further upside potential is likely to be limited in the medium to long term. This is because a pronounced cycle of interest rate cuts in the US is unlikely, given the persistent risks of inflation.

We are therefore ‘only’ raising our Gold price forecast for the end of this year and the end of next year from $2,100 to $2,200.

- Silver nears the top of a range as the bulls push prices higher.

- Long-term fundamentals support, including positive global growth and robust demand.

- US Industrial Production data beats to the upside suggesting increased demand by industry.

Silver price (XAG/USD) pushes higher, trading up over one and a half percentage points in the $25.20s on Friday, on technical buying mainly – and long-term bullish fundamentals.

The precious metal, which is used in industrial processes as well as to store value, sees gains after the release of US Industrial Production data beat estimates with a 0.1% rise in February when economists had expected flat growth. The data, released by the US Federal Reserve (Fed), was also an improvement on the negative 0.5% of the previous month.

A positive outlook for global growth has led analysts such as Macquarie's Marcus Garvey to speculate Silver could be in for more gains as demand increases for its use in the manufacture of Solar Panels, a wide variety of electronic devices and jewelry.

Recent higher-than-expected inflation data from the US has failed to dissuade Silver bulls, despite the data pointing to further delays before the Federal Reserve pushes the button on cutting interest-rates. Usually a higher interest rate outlook would be bearish for Silver in its role as an investment since it is non-yielding so loses out in a high inflation environment, however, this has not been the case this time.

The Silver Institute, a not-for-profit organization based in the US, has forecast robust demand for Silver in 2024, predicting it will see its second best year on record with demand rising to 1.2 billion ounces.

From a technical perspective, XAG/USD remains stuck in a range between $19.00 and $26.00 (thick lines), which itself sits within a broader range between $17.50 and $30.00.

It is rallying in a short-term bullish uptrend within its ranges, and is now quite near the narrower range’s highs. A decisive break above $25.85 would probably indicate a breakout to the upside, further increasing bullish enthusiasm.

Such a breakout would probably see Silver rally to between around $29.50, if using the 0.618 Fibonacci ratio of the range, or just shy of $32.00 if extrapolating the full height of the range higher.

Silver versus US Dollars: Weekly chart

If the latter, then it will mean the pair has also broken out of the top of the broader range, indicating even greater upside, potentially to a target at $37.50.

Alternatively the precious metal could meet tough resistance at the range highs in the $25.80-90s and pullback down.

Traders should watch for a decisive break higher before jumping in. A “decisive” break is one characterized by a long green daily candle piercing clearly above the level and closing near its high, or three green candles in a row, breaching the level.

- NZD/USD tumbles to 0.6100 as market sentiment remains downbeat.

- Hot US CPI and PPI data for February has diminished Fed rate cut expectations for June.

- The NZ Dollar will dance to the tunes of the Q4 GDP data.

The NZD/USD pair falls vertically to the round-level support of 0.6100 in Friday’s early American session. The Kiwi asset weakens as market expectations for the Federal Reserve (Fed) reducing interest rates in the June policy meeting have diminished. This has led to a big dent in the demand for risk-sensitive assets.

The S&P 500 opens on a bearish note as investors rush for safe-haven assets amid uncertainty ahead of the Federal Reserve’s (Fed) monetary policy decision, which will be announced on Wednesday. The Fed is expected to keep interest rates unchanged in the range of 5.25%-5.50% while investors will majorly focus on the dot plot and economic projections. The US Dollar Index (DXY) consolidates in a tight range around 103.80. 10-year US Treasury yields rise to 4.31%.

Expectations for the Fed to cut interest rates are shifting to the July monetary policy meeting as consumer and producer prices remain hotter than expected in February. The situation is not favorable for the Fed to pivot to rate cuts. Fed policymakers have been reiterating that rate cuts would be appropriate only if they get confidence that inflation will sustainably return to the 2% target.

Meanwhile, the New Zealand Dollar will be guided by the Q4 Gross Domestic Product (GDP) data of 2023, which will be published later next week. The NZ economy is forecasted to have remained stagnant. The NZ economy would be considered in a technical recession if the economy contracts in the final quarter of 2023. The economy was contracted by 0.3% in the third quarter of 2023.

The US Dollar (USD) has run out of momentum due to more mixed economic data. Economists at Société Générale analyze the forex market outlook.

Sterling is clearly vulnerable

USD/JPY is likely to fall as the BoJ exits negative rates and yield curve control. A symbolic move still matters if it suggests that higher rates will be seen eventually. The Yen is too cheap.

EUR/USD may be stuck, but GBP/USD could fall as the UK continues to stagnate and the Bank of England finally cuts rates.

- UoM Consumer Sentiment Index edged lower in March's preliminary reading.

- The US Dollar Index stays in daily range above 103.00 after the data.

Consumer confidence in the US weakened slightly in early March, with the University of Michigan's Consumer Sentiment Index edging lower to 76.5 from 76.9 in February. This reading came in below the market expectation of 76.9.

The 5-year Inflation Expectation component of the survey remained unchanged at 2.9%.

Assessing the survey's findings, "small improvements in personal finances were offset by modest declines in expectations for business conditions," said Surveys of Consumers Director Joanne Hsu and continued:

"After strong gains between November 2023 and January 2024, consumer views have stabilized into a holding pattern; consumers perceived few signals that the economy is currently improving or deteriorating. Indeed, many are withholding judgment about the trajectory of the economy, particularly in the long term, pending the results of this November’s election."

Market reaction

This report failed to influence the US Dollar's valuation against its major rivals. At the time of press, the US Dollar Index was virtually unchanged on the day at 103.40.

Speculation around a BoJ monetary policy shift has been building. Economists at TD Securities bring forward their call for an April hike to March.

BoJ to hike next week

Following the positive round of wage increases announced this week and Rengo's announcement today delivering a 5% increase in first round wage negotiations, we believe the BoJ has the information it needs to hike at next week's meeting. Accordingly, we bring forward our call for an April hike to March.

We expect USD/JPY's reaction function to be asymmetric here with a bigger move on delivering a hike (USD/JPY towards 145.00) than on a disappointment (towards 150.00) as even in the latter the BoJ can try to sound hawkish and lay the grounds for an April pivot.

- USD/JPY jumps to 148.80 on hopes that the BoJ will maintain its ultra-loose monetary policy stance on Tuesday.

- The BoJ lacks a significant wage-price spiral to back an exit to negative interest rates.

- Diminished Fed rate cut expectations keep the US Dollar strong near its three-week highs around 103.50.

The USD/JPY climbs to 148.80 in the late European session on Friday as the Japanese Yen weakens on expectations that the Bank of Japan (BoJ) will not end the expansionary policy stance in the meeting on Tuesday.

Plenty of fundamentals favor the BoJ quitting negative interest rates. BoJ’s favourite inflation measure, the Consumer Price Index (CPI), excl. fresh food has remained above the 2% target for a longer period. Meanwhile, Japan's biggest companies agreed with labor unions to raise wages by the highest level in 33 years, reported Reuters.

In addition, Japan's Finance Minister Shunichi Suzuki said early Friday that the economy is no longer in deflation and that the government will mobilize all policy steps available to continue the strong trend of wage hikes this year. However, investors hope the BoJ will not go for exiting the prolonged expansionary policy stance as a full-proof plan for the wage-price spiral remains absent.

Market participants will keenly focus on the BoJ’s press conference about when the central bank will scrap its negative interest rates and Yield Curve Control (YCC). Earlier, BoJ Governor Kazuo Ueda said policymakers will debate whether the outlook is bright enough to phase out the massive monetary stimulus.

Meanwhile, market sentiment remains cautious as stubborn United States inflation has dented expectations for the Federal Reserve (Fed) to reduce interest rates from the June meeting. Surprisingly stubborn US Producer Price Index (PPI) data for February is expected to allow Fed policymakers to argue to keep interest rates higher for a longer period.

The US Dollar Index (DXY) is holding near its three-week high of around 103.50. Ten-year US Treasury yields are extending their upside to 4.31%.

The strength of the Gold price is a little puzzling. Economists at Commerzbank analyze the yellow metal’s outlook.

A Fed rate cut has hardly moved any closer for most market participants

Despite the recent weak US economic data, a Fed rate cut has hardly moved any closer for most market participants. According to Fed Funds Futures, the first rate cut is not expected until June at the earliest.

The Fed meets next week: a rate cut is not expected. But if the Fed's new projections and Fed Chairman Powell's words at the press conference can be interpreted as having increased the chances of faster interest rate cuts, the Gold market could even set new records, before the rally runs out of steam.

- The Australian Dollar is hit by negative Chinese House Price data on Friday.

- A fall in Chinese New Loans and M2 Money Supply add to the narrative of constraint.

- AUD/USD tumbled on Thursday after US data showed inflationary tendencies in the US economy.

AUD/USD is trading almost two tenths of a percent lower on Friday, extending Thursday’s sell-off into the weekend. The pair is feeling pressure from negative Chinese housing and lending data which indicates the property sector of the world’s second largest economy is still in the eye of the storm.

The weak Chinese data is a negative factor for the Australian Dollar which relies heavily on the Chinese market for its exports, particularly Iron Ore, which is Australia’s largest export commodity.

The Chinese House Price Index showed a decline in house prices of minus 1.4% in February from minus 0.7% in the previous month of January, according to data from the National Bureau of Statistics of China, released early Friday. This continues the down trend in Chinese house prices since 2019.

Chinese property market woes have had a direct impact on Iron Ore prices, because the country uses so much of the ore to make the steel girders it uses in its buildings. Iron Ore prices have registered a roughly 25% drop since the start of 2024 alone.

-638461042762640597.png)

Other data out on Friday showed an unexpected fall in New Loans in China, in February. New Loans shrank to ㍐1,450 billion, according to data from The People’s Bank of China (Pboc). This was a decline from the 4,920 billion Yuan in January and below estimates of 1,500 billion. The data indicates less lending, which could be growth limiting, especially for the borrowing intensive property sector.

Data showing lower-than-expected Money Supply M2, which increased by 8.7% YoY in February versus the 8.8% forecast, suggests a brake on liquidity.

US factory gate inflation rises

AUD/USD fell over half a percent on Thursday after the release of US macroeconomic data indicated the US economy was hotter-than-expected.

The US Producer Price Index, which measures factory-gate price inflation, rose to 1.6%, easily beating the 1.1% expected and 1.0% previous, suggesting continued inflationary tendencies.

Core PPI also rose by more than estimated. The data suggests the inflation will be passed on to consumers and turn up later to bug shoppers in the Consumer Price Index.

The higher inflation makes it less likely the Federal Reserve (Fed) will be in a hurry to cut interest rates. Whilst market expectations continue to see the probabilities favor a rate cut in June, the chance of a reduction in May has dwindled to virtually zero.

Higher interest rates for longer are positive for USD because they attract more foreign capital inflows. They are negative for the AUD/USD which measures the number of Australian Dollars purchasable with one US Dollar. As such the data was negative for the pair, which declined substantially after the release on Thursday.

- The US Dollar locks in gains for this week after hotter-than-expected US CPI and PPI figures.

- Traders brace for Import-Export prices and Michigan Consumer Sentiment numbers.

- The US Dollar Index trades at a crucial pivotal level that could unlock 104.00.

The US Dollar (USD) trades firmly in the green on Friday after markets got shaken on Thursday after a badge of US economic data suggested inflation pressures are far from over.. A textbook panic attack took place in markets, with risk assets such as equities and Bitcoin selling off, yields jumping higher with bonds being sold and the US Dollar strengthening against everything. The surprise uptick in the Produce Price Index (PPI) numbers spooked investors, who rushed to reprice the first interest-rate cut by the Federal Reserve (Fed) away from June and towards September.

On Friday’s economic calendar, there are some lighter data set to be released. Still, many investors will be set to square their positions for this week ahead of the US Federal Reserve rate decision next week and the risk event of the Bank of Japan, which could opt for hiking interest rates for the first time in decades. For this Friday, the Import and Export prices data and the preliminary data from the University of Michigan Consumer Sentiment and Inflation Expectations for March could eke out some more gains for the Greenback.

Daily digest market movers: Last data points opportunity

- At 12:30, Import and Export price data for February will be released:

- The monthly Import price Index headed from 0.8% to 0.3%, while the Yearly Import Index fell by 0.8% in January.

- The monthly Export price Index declined from 0.0% to 0.8%. The Yearly Export Index fell by 1.8% in January.

- The New York Empire State Manufacturing Index for March did a nosedive move from -2.4 to -20.9.

- At 13:15 GMT, both Industrial Production and Capacity Utilization data for February will be released. Production is expected to remain roughly stable, from -0.1% to 0.0%. Capacity Utilization is seen unchanged at 78.5%.

- The last data number for this Friday is the University of Michigan release, at 14:00 GMT:

- Consumer Sentiment for March is expected to remain stable at 76.9.

- Inflation expectations were at 2.9% in February, with no forecast available.

- Equities are carefully in the green after the bloodbath on both the European and US equity markets. European indices are though mildly in the green while US futures are flat ahead of the US opening.

- According to the CME Group’s FedWatch Tool, expectations for a Fed pause in the March 20 meeting are at 99%, while chances of a rate cut stand at 1%. The odds of a June rate cut are around 60%, below the above 70% priced in a week ago.

- The benchmark 10-year US Treasury Note trades around 4.28%, the highest level this week.

US Dollar Index Technical Analysis: Brief return of the King

The US Dollar Index (DXY) –not Elvis Presley of course – made its way back to the stage on Thursday after markets got shaken with the US Dollar as the sole winner. Although the PPI numbers might have sparked some worries on the June timing, it is again a mere repricing, by moving the probability for that initial rate cut from June to September. It is the same story we have seen year-to-date, which means that the probability of the DXY falling back to 103.00 is substantially bigger than rallying back up to 104.00.

On the upside, the 55-day Simple Moving Average (SMA) at 103.42 is facing some pressure. Not far above, a double barrier is set to hit with the 100-day SMA near 103.68 and the 200-day SMA near 103.70. Depending on the catalyst that pushes the DXY upwards, 104.96 remains the key level on the topside.

As mentioned in the opening paragraph on technical analysis, the move from Thursday already covers that pushback of a rate cut to September, and a move further down the line to December looks very unlikely. More downside thus, looks inevitable once markets move forward again to the June probability, with 103.00 and 102.00 up next, which bears some pivotal relevance. Once through there, the road is open for another leg lower to 100.61, the low of 2023.

US Dollar FAQs

The US Dollar (USD) is the official currency of the United States of America, and the ‘de facto’ currency of a significant number of other countries where it is found in circulation alongside local notes. It is the most heavily traded currency in the world, accounting for over 88% of all global foreign exchange turnover, or an average of $6.6 trillion in transactions per day, according to data from 2022. Following the second world war, the USD took over from the British Pound as the world’s reserve currency. For most of its history, the US Dollar was backed by Gold, until the Bretton Woods Agreement in 1971 when the Gold Standard went away.

The most important single factor impacting on the value of the US Dollar is monetary policy, which is shaped by the Federal Reserve (Fed). The Fed has two mandates: to achieve price stability (control inflation) and foster full employment. Its primary tool to achieve these two goals is by adjusting interest rates. When prices are rising too quickly and inflation is above the Fed’s 2% target, the Fed will raise rates, which helps the USD value. When inflation falls below 2% or the Unemployment Rate is too high, the Fed may lower interest rates, which weighs on the Greenback.

In extreme situations, the Federal Reserve can also print more Dollars and enact quantitative easing (QE). QE is the process by which the Fed substantially increases the flow of credit in a stuck financial system. It is a non-standard policy measure used when credit has dried up because banks will not lend to each other (out of the fear of counterparty default). It is a last resort when simply lowering interest rates is unlikely to achieve the necessary result. It was the Fed’s weapon of choice to combat the credit crunch that occurred during the Great Financial Crisis in 2008. It involves the Fed printing more Dollars and using them to buy US government bonds predominantly from financial institutions. QE usually leads to a weaker US Dollar.

Quantitative tightening (QT) is the reverse process whereby the Federal Reserve stops buying bonds from financial institutions and does not reinvest the principal from the bonds it holds maturing in new purchases. It is usually positive for the US Dollar.

Economists at ING analyze US Dollar’s outlook ahead of next week’s Fed meeting.

Dollar’s yield position is strong, even without a hawkish Fed

We recently stressed the upside risks for the Dollar given its still strong underlying yield position, and we are finally observing some USD buying across the board. The coming days will tell us where the FX market is positioning itself in the hawkish-dovish surprise spectrum for the Fed meeting.

We believe hawkish bets may be misplaced again this time as the Fed should reiterate a relatively optimistic narrative on disinflation and still hint at monetary easing ahead.

The main upside risk for the Dollar is a revision higher in the dot plots, but even then, we struggle to see this having a prolonged impact on FX if – as it appears likely – the Fed will continue to point to the crucial role of upcoming data releases, which are generally expected to start showing some signs of softening.

Economists at Rabobank analyze the Japanese Yen (JPY) outlook ahead of next week’s BoJ policy meeting.

Risk of a near-term pullback

If the BoJ does exit its negative interest rate policy on March 19, likely, rates will only be raised by 10 or 15 bps. Additionally, at best the tone of the BoJ’s guidance next week is likely to be one of cautious optimism. Importantly, even after the negative policy rate has been consigned to the economic history books, Japan’s monetary policy settings are likely to remain accommodative.

A very guarded tone from the BoJ on the outlook for further policy moves would raise the risk that the JPY could suffer a ‘sell on the fact’ reaction to a BoJ policy change on March 19. That said, despite the risk of a near-term pullback, we continue to see scope for USD/JPY to trend lower to 146.00 on a three-month view.

- Swiss Franc is vulnerable as inflation data continues to undershoot official forecasts.

- The SNB expected inflation to average 1.9% in 2024 in its December forecast, but it currently sits at 1.2%.

- The latest Producer and Import Prices showed the tenth month of deflation in a row.