- Аналітика

- Новини та інструменти

- Новини ринків

Новини ринків

- US Dollar Index (DXY), which measures the US Dollar’s performance against a basket of six currencies, shows slight gains after reaching a fresh 15-month low of 99.578.

- June’s US CPI grew 3.0% YoY, underperforming the 3.1% forecast, while Core CPI fell by 0.5%. Concurrently, June’s PPI rose less than the expected 0.1% YoY.

- Considering these conditions, markets now expect fewer Fed rate hikes post-July FOMC, forecasting a stable Federal Funds Rate around 5.25%-5.50% in 2023.

The US Dollar Index (DXY), which measures the US Dollar (USD) performance against a basket of six currencies, recovers some ground, as the DXY prints gains of 0.18% after hitting a fresh 15-month low of 99.578. At the time of writing, the DXY exchanges hands at 99.959, shy of reclaiming the 100.000 figure.

DXY faces pressure from lower consumer and producer price indices, leading to huge losses in the week

The greenback stood under a lot of stress in a busy economic docket., mainly driven by inflation figures, with consumer prices and producer prices edging lower, weakening the US Dollar (USD).

The June US Consumer Price Index (CPI) expanded by 3.0% YoY, falling below the estimated 3.1%. Furthermore, the Core CPI, which excludes volatile items such as food and energy, decreased by 0.5%, dropping from 5.3% in May to 4.8% last month. Meanwhile, the release of the Producer Price Index (PPI) for the same period expanded by 0.1%, YoY below forecasts of 0%, while the so-called Core PPI, on a yearly basis cooled down compared to expectations of 2.6% and came at 2.4%.

Given the backdrop, market participants trimmed their bets the US Federal Reserve (Fed) would hike rates past July’s Federal Open Market Committee (FOMC) meeting on 25-26, with investors pricing in a 25 basis points (bps) increase. Hence, the Federal Funds Rates (FFR) is expected to remain through 2023 at around the 5.25%-5.50% range, as shown by the CME FedWatch Tool.

Consequently, US Treasury bond yields extended their losses. The US 2-year Treasury bond yield finished the week at 4.772%, almost 18 basis points lower than Monday’s open, while the 10-year plunged a quarter of percentage points lower, to 3.834%. That was a heavy burden for the greenback, as shown by the DXY, finishing the week with hefty losses of 2.26%.

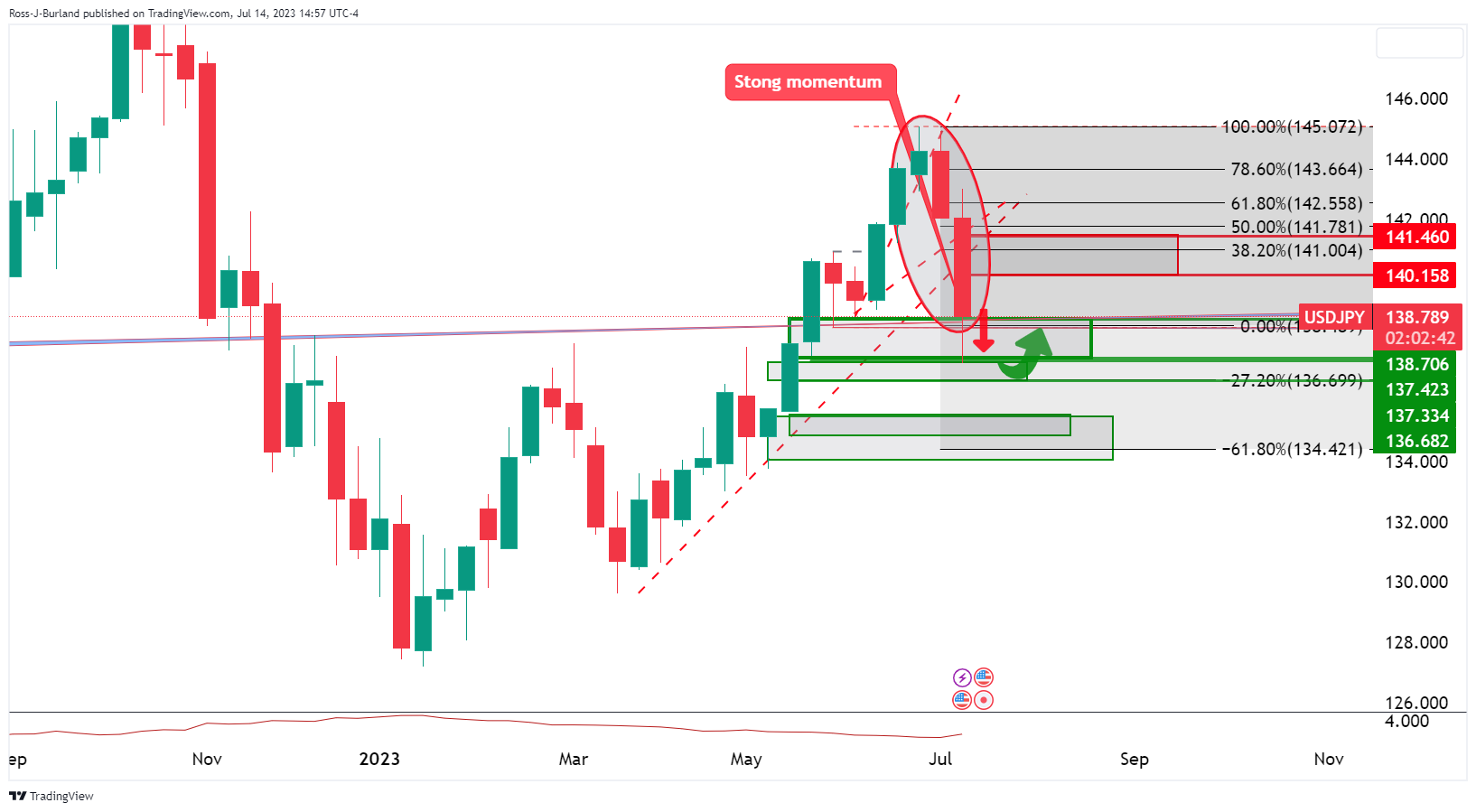

US Dollar Index (DXY): Technical outlook

From a technical standpoint, once the DXY extended its losses past the February 2 daily low of 100.820, it opened the door for further losses. As of writing, DXY’s first support emerged on April 14, 2022, daily low of 99.571. Once cleared, the buck could edge toward the March 30, 2022, low of 97.685 before challenging the 2021 yearly low of 96.938. On the flip side, the DXY first supply area would be the February 2 low-turned resistance at 100.820, followed by the 20-day EMA at 102.037.

- EUR/USD may have run its course and bulls are laying the table.

- A break of key support structures could be on the cards for the week ahead.

EUR/USD is stalling on the bid but underlying momentum is undeniable. At the time of writing the Single Currency is probing key resistance as the following illustrates, However, bears are planning their gameplay as the following charts will lean towards. Meanwhile, the US Dollar has bounced in a correction as markets crystallised the sentiment on the charts that the Federal Reserve is near the end of its rate hike cycle amid softening inflation.

EUR/USD analysis

Zooming in, bears are eyeing the deceleration and prospects of a significant correct as shown in the above top-down analysis.

- EUR/GBP consolidates within a tilted downward bias, with key support at 0.8504.

- The pair’s bullish turn hinges on a 0.8600 breach, testing 50-day EMA.

- RSI is nearing bullish zone; RoC indicates a potential uptrend.

EUR/GBP reverses Thursday’s losses and is set to print weekly gains of 0.40% after Pound Sterling (GBP) bulls emerged yesterday, trimming some of its Wednesday losses. Nevertheless, selling pressure waned, and the EUR/GBP sits above a technical support level. At the time of writing, the EUR/GBP exchanges hands at 0.8573, up 0.32%.

EUR/GBP Price Analysis: Technical outlook

The EUR/GBP daily chart portrays the pair in consolidation, with a downward bias, which could extend if sellers drag prices past the year-to-date (YTD) low of 0.8504. In that event, the next support would be the 0.8450 psychological level before the EUR/GBP dives towards the August 24 swing low of 0.8408.

Conversely, the EUR/GBP could threaten to turn bullish, above the 50-day Exponential Moving Average (EMA) at 0.8616, which would be tested once the Eur/GBP passes the 0.8600 mark. A breach of the latter will expose the June 28 swing high at 0.8658, ahead of the 100-day EMA a 0.8668, followed by the 200-day EMA at 0.8681.

Oscillator-wise, the Relative Strength Index (RSI) is at the brisk of turning bullish, which could exacerbate the EUR bulls’ reaction. The three-day Rate of Change (RoC) portrays the cross as having an upward biased.

Hence, the EUR/GBP could be ready for a bullish resumption in the near term.

EUR/GBP Price Action

- GBP/USD is tiring in the bid and bears are moving in for the kill.

- The week ahead holds a bearish bias, but there ios work to do.

GBP/USD ramped up a sixth consecutive day of gains after data showed the UK economy swung in the red by less than expected. the following shows the bias from the top-down analysis:

GBP/USD moving in on the lower time frames

A correction is underway for the week ahead.

GBPUSD H1 chart

Bears are monitoring for a break of trendline support. 1.3000 is eyed!

- GBP/JPY cleared most of its weekly losses trading near 181.80 tractioned by rising British yields.

- Investors continue to look for clues regarding a potential BoJ YCC policy tweak.

- BoE’s tightening expectations have fallen, and markets now see rates peaking at 6.25%.

On Friday, the Sterling traded with gains agains the JPY, but it is still poised to close a weekly decline. However, the GBP/JPY downside potential may be limited while investors are looking for clues on whether the Bank of Japan (BoJ) will tweak its monetary policy in July.

As for now, markets have already largely discounted a 50 basis point (bps) hike in the August 3 Bank of England (BoE) meeting and foresee 25 bps hikes in September, November and in Q1 2024, which would see the policy rate peaking at 6.25% vs the 6.50% terminal rate expected at the beginning of the week.

Despite tightening expectations falling, British bond yields are on the rise and lend support to the GBP. The 2-year bond yield rose more than 1% to 5.19% while the 5-year rate to 4.58%, up by more than 1.50%, while the 10-year rate stands at 4.44%, seeing 0.80% increases.

On the other hand, investors are looking for clues regarding the next Bank of Japan (BoJ) meeting in July. Former bank official Hideo Hayakawa commented that “it is highly probable” that the bank will adjust the Yield Control Curve policy and that if they don’t, “it doesn’t make sense”. Economic data will continue modelling expectations, so traders will eye next week's Trade Balance data from Japan from June to be reported on Thursday.

GBP/JPY Levels to watch

Despite two consecutive gains days, the outlook is still negative for the pair. Indicators gained some ground but still show weakness with the Relative Strength Index (RSI) near its midline while the Moving Average Convergence Divergence (MACD) prints red bars. To confirm a recovery, the bulls must retake the 20-day Simple Moving Average (SMA) at 182.25.

Support Levels: 181.00, 180.50, 179.00.

Resistance Levels: 182.25 (20-day SMA), 182.50, 183.00.

GBP/JPY Daily chart

-638249613116016619.png)

Bank of Canada (BoC) Governor Tiff Macklem expects inflation to be around 3% for next year and then gradually move back to the 2% target. In an interview with The Globe and Mail, he mentioned that the labor market has eased a bit but still remains very tight. He explained they need to see a better balance in the labor market and a moderation in wage growth.

He is surprised by the ongoing strength in demand in the economy. Regarding inflation, Macklem mentioned that he is amazed by the persistence of underlying inflationary pressures.

“It’s not working as quickly or as powerfully as we thought”, said Macklem explaining why the central restarted interest rate hikes.

Market reaction:

USD/CAD rose further above 1.3220 following Macklem's comments. The Loonie was among the worst performers on Friday.

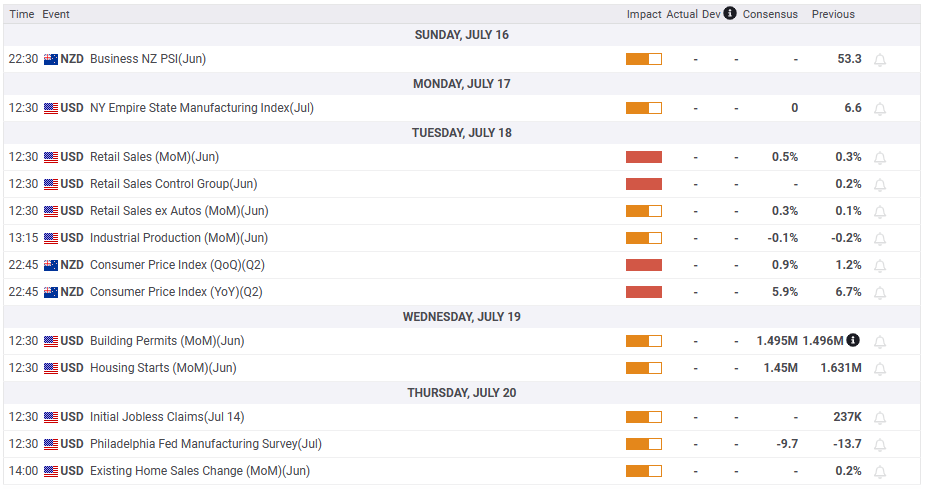

After an intense week across financial markets, volatility is unlikely to ease quickly. Market participants will continue to digest the latest round of US inflation data with a focus on the upcoming FOMC meetings. The Fed enters its blackout period ahead of the July 25-26 meeting. Next week, inflation data from Japan, New Zealand, and the UK is due along with US June Retail Sales and Australian jobs data.

Here is what you need to know for next week:

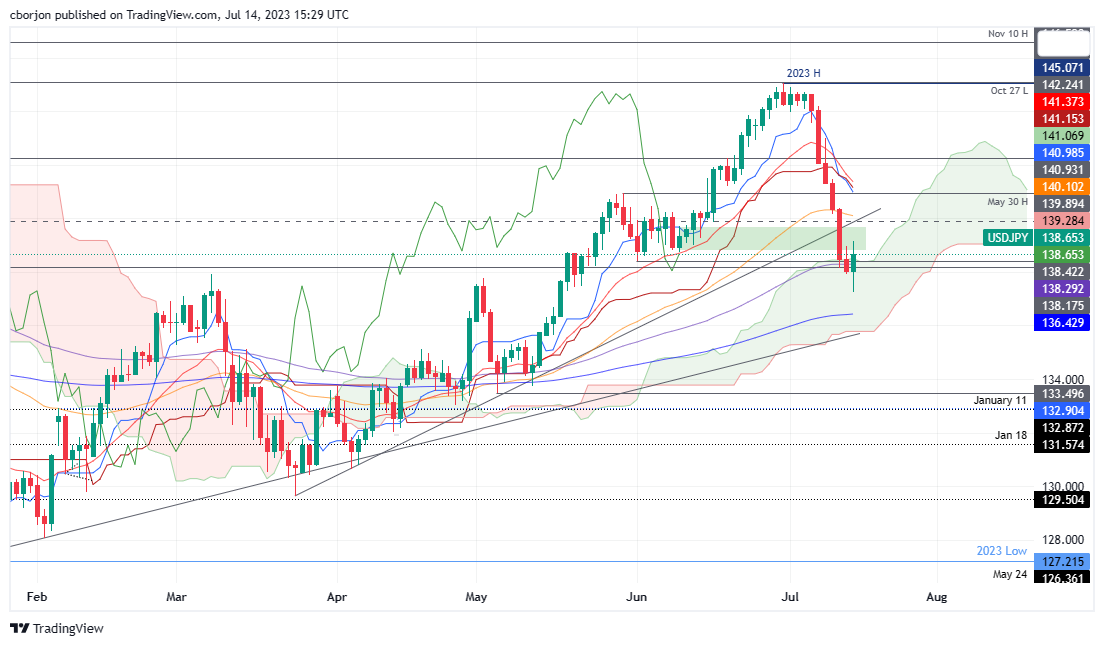

The US Dollar, measured by the DXY, suffered its worst weekly loss since November of last year, falling below 100.00, to the lowest since April 2022. The Greenback remains vulnerable in the context of risk appetite and lower Treasury yields.

US bonds rallied during the week on signals from the US Consumer Price Index (CPI) and the Producer Price Index (PPI) of slowing price pressures. The US 10-year yield dropped to 3.80%, after hitting last week a multi-month high above 4%; the 2-year yield ended a five-week upside run, retreating to 4.70%%. Wall Street cheered the latest inflation numbers and the fact that the next rate hike from the Fed in July could be the last one. US stocks rose more than 2% during the week. Commodities also climbed significantly.

Expectations for another Fed rate hike after July have softened. However, for the September meeting, there will be two more inflation reports, so there is still a long way to go. The most relevant report in the US economic calendar next week is June Retail Sales. Markets won't be hearing from Federal Reserve officials as they enter the blackout period ahead of the July 27-28 meeting. The debate is centered on what the Fed will do after July. At this point, the Fed has not provided clear indications of what its next moves will be.

EUR/USD rose above the 200-week Simple Moving Average (SMA) for the first time in more than a year, and closed above 1.1800, having the best weekly performance since November 2022.

Analysts at Rabobank:

Signs of disinflation in the US and a high level of scepticism about the ability of the Fed to hike rates beyond the July meeting, suggest that a soft USD is likely to prevail in the near-term. That said, signs that the ECB’s rate hike cycle is moving towards its peak suggests that EUR/USD could struggle to make further gains beyond the summer season.

GBP/USD also rose above the 200-week SMA and also broke 1.3100. The positive momentum will be challenged next week with key data from the UK that includes on Wednesday, the Consumer Price Index (CPI) for June, with a decline expected in the annual rate from 2.1% to 1.9% and the Core seen holding at 1.8%. Later on Friday, the June Retail Sales report is due.

Analysts at Commerzbank:

Inflation proved to be more stubborn than expected also in May, whereupon the BoE surprisingly raised its key interest rate by 50 bp. The market now expects a much longer rate hike cycle, which should support the pound in the short term. We have therefore adjusted our forecast. In the medium term, however, we continue to see a weaker pound, as the BoE is likely to act too hesitantly overall.

USD/JPY dropped for the second week in a row and found support above 137.00, on the 20 and 55-week SMA. The yen rose sharply versus the dollar but posted mixed results versus its other rivals as the positive impact from lower yields was offset by risk appetite. The divergence between the Bank of Japan and other central banks remains present, even as the tightening cycle becomes closer. Japan will release the Consumer Price Index on Friday, with the annual rate expected to remain at 0.2% from a year earlier.

USD/CAD rebounded sharply on Friday, trimming weekly losses and retaking 1.3200. The Bank of Canada hiked interest rates to 5.0%, its highest level in 11 years. Canada will report inflation data next Tuesday and Retail Sales on Friday.

AUD/USD broke its range, surpassing 0.6700 and jumped to test the 0.6900 area and June highs. It holds a bullish tone. The Reserve Bank of Australia (RBA) will release the minutes of its latest meeting on Tuesday. Australia will release employment data on Thursday.

NZD/USD broke the resistance area at 0.6300 and briefly reached levels above 0.6400, and then pulled back modestly. As expected, the Reserve Bank of New Zealand (RBNZ) kept interest rates unchanged at 5.5%. On Wednesday, New Zealand will release inflation data, with a slowdown in the annual rate expected from 6.7% to 5.9%.

The Chinese Yuan recovered with USD/CNH falling from 7.22 to 7.11. Data continues to point to weak domestic demand. China will report Q2 GDP on Monday.

Optimism that the Federal Reserve will soon end the tightening cycle boosted emerging market and higher beta currencies. USD/MXN posted its first weekly close under 17.00 since November 2015. The Mexican peso continues to be among the top performers so far during 2023.

The Swedish Krona and the South African Rand were the top performers during the week. USD/ZAR bottomed at 17.90, the lowest since April, while USD/SEK tumbled from 10.800 to 10.180, slightly above YTD lows. The Chilean Peso lagged and failed to rise versus the US Dollar.

Buying Silver was the best trade of the week with XAG/USD gaining more than 8% during the week. Gold rose from $1,925 to $1,960.

Like this article? Help us with some feedback by answering this survey:

- EUR/JPY bears lurking for the open next week.

- EUR has remained firm and bulls stay in control, but the focus is on the Yen.

EUR/JPY is higher on Friday but that not tells the entire story as the following technical analysis illustrates. It has traded between a low of 155.92 and a high of 156.13 but there is a bearish bias:

EUR/USD technical analysis

While the Euro has upside potential, the EUR/JPY chart is bearish as the Yen is flying:

USD/JPY analysis

DXY analysis

EUR/JPY, possibility

If the Yen continues and US Dollar bears remain reluctant to commit, we could see the above scenario play out.

- The XAG/USD closes the week with slight gains near the $25.00 area, tallying a six-day winning streak.

- The metal is set to close an 8% winning week.

- USD sell-off stalled amid positive UoM data and a slight US yield recovery.

In Friday’s session, the XAG/USD stands with gains near the $25.00 psychological resistance. Despite US Treasury yields recovering, the precious metal stays resilient while the USD managed to stop the bleeding, still closing its worst week in 2023.

The XAG/USD gained interest due to falling yields during the week. As the US reported that the Core Consumer Price Index (CPI) from the US from June, dropped to 4.8% YoY in June, while the Core Producer Price Index (PPI) slid to 2.6% YoY in the same period, investors started to bet on a less-aggressive Federal Reserve.

As for now, according to the CME FedWatch tool, markets have priced in a 25 basis point (bps) hike in the next Fed meeting in July, but the odds of another hike in 2023 lowered to around 20% vs 40% at the start of the week. In that sense, US yields sharply declined, and as they could be seen as the opportunity cost of holding the non-yielding grey metal, the price rallied.

To close the week, the US yields recovered with more than 1% increases, but the 2, 5 and 10-year yields are set to close a week of more than 3% declines.

XAG/USD Levels to watch

The daily chart suggests a positive outlook for the XAG/USD, but after six consecutive days of losses, the price will eventually correct downwards. As for now, the Relative Strength Index (RSI) stands flat near overbought levels, while the Moving Average Convergence Divergence (MACD) seem to be running out of steam.

Resistance Levels: $25.10, $25.40, $26.00.

Support Levels: $23.95, $23.55 (100-day Simple Moving Average), $23.15 (20-day Simple Moving Average).

XAG/USD Daily chart

-638249565235285059.png)

- USD/CHF drops 3%, RSI suggests potential recovery, past 0.8700, as a bullish-engulfing pattern could form.

- USD/CHF’s bearish extension hinges on breaking 0.8566 support.

USDH/CHF regains some composture after plummeting more than 3% in the week, breaking technical support levels due to overall US Dollar (USD) weakness across the Forex (FX) board. Slow inflation in the United States (US) triggered market players to pare bets the US Federal Reserve (Fed) will tighten monetary conditions past the Fed July meeting. Hence, the greenback weakened and, against the Swiss Franc (CHF), lost more than 250 pips. The USD/CHF is trading at 0.8622 after reaching a new eight-year low of 0.8566.

USD/CHF Price Analysis: Technical outlook

From a technical standpoint, the USD/CHF is suggested to continue downwards. Still, the Relative Strength Index (RSI) indicator, hitting an extreme 21.47 reading, jumped and is about to cross above the 30 line. That, along with the three-day Rate of Change (RoC) portraying sellers are beginning to lose momentum, could pave the way for the USD/CHF to recover some ground.

If USD/CHF buyers reclaim the 0.8700 figure, that could form a bullish-engulfing candlestick pattern, opening the door for an upward correction. Still, the USD/CHF will remain downward biased unless traders push prices past the 200-day EMA at 0.9179.

A bearish continuation will resume once USD/CHF sellers drag prices below 0.8566, exposing the 0.8500 mark, followed by the 0.8400 figure, ahead of diving towards the 2015 yearly low of 0.8300.

USD/CHF Price Action – Daily chart

- NZD/USD retreats from five-month highs amid profit-taking ahead of the weekend and the backdrop of easing US inflation.

- US economic data for the week revealed a disinflation process in progress, impacting investor anticipation of further rate hikes beyond the expected July FOMC decision.

- Reserve Bank of New Zealand’s decision to hold rates steady has not weakened the Kiwi, which is set to finish the week with gains of over 2.70%.

NZD/USD retreats from five-month highs reached at 0.6411 earlier, drops 0.31%, as traders square off their positions ahead of the weekend. US economic data revealed on Friday portrays inflation is easing, while a University of Michigan (UoM) poll showed consumer sentiment improved. The NZD/USD is trading at 0.6372.

NZD set to end the week with solid gains vs. the USD despite pullback

During the week, the US economic agenda showcased the Consumer Price Index (CPI) and the Producer Price Index (PPI) June figures, showed the disinflation process is gathering momentum. Hence, investors trimmed a possible rate hike past the July FOMC’s decision, in which the Federal Reserve is expected to lift rates by 25 bps to leave rates at 5.25%-5.50%.

Consequently, US Treasury bond yields plunged, while the greenback holds one of its most significant weekly losses since November 2022, as shown by the US Dollar Index (DXY). As of writing, the DXY, which portrays the US Dollar’s performance against a basket of six currencies, gains 0.17%, up at 99.943.

Data-wise, Friday’s US agenda witnessed Import and Export prices slowing down for the second consecutive month, with figures coming below May’s and analysts’ forecasts. That reinforced US CPI, and PPI data revealed during the week a headwind for the US Dollar.

The University of Michigan (UoM) revealed an improvement in US Consumer Sentiment, which was expected to print 65.5 but came at 72.6m at a two-year high. Further data showed that inflation expectations for one year were upward revised to 3.4% from 3.3% in June, while for five years, it edged high to 3.1%, up from 3%.

Joanne Jsu, the UoM Surveys of Consumers Director, said, “The sharp rise in sentiment was largely attributable to the continued slowdown in inflation along with stability in labor markets.”

On the New Zealand front, the latest Reserve Bank of New Zealand (RBNZ) monetary policy decision to hold rates unchanged didn’t weaken the Kiwi (NZD), which is set to finish the week with solid gains of more than 2.70% against the US Dollar (USD).

Upcoming events

NZD/USD Price Analysis: Technical outlook

The NZD/USD daily chart portrays the pair as upward biased, though it should be said that it is trading below the May 23 daily high of 0.6385, opening the door for further losses. Traders should note the Relative Strength Index (RSI) indicator is exiting overbought territory, which could pave the way for deeper correction while keeping the bias intact.

NZD/USD’s support emerges at a five-month-old broken resistance trendline turned support at around 0.6350/60. A breach of that area, the NZD/USD could dive toward the May 23 high-turned support at 0.6302 before extending its losses to June’s 16 swing high-turned support at 0.6247

- WTI bulls are taking profits ahead of the weekend and the price retreated near $75.50.

- The price was rejected twice this week by the 200-day SMA at $77.17, and indicators show some weakness.

- USD weakness and dovish bets to limit the WTI losses.

On Friday, the West Texas Intermediate (WTI) barrel lost some ground as investors did some profit-taking ahead of the weekend after a three-day winning streak. Still, the black gold is set to close a 2.90% winning week amid USD weakness.

That said, the USD somewhat recovered on Friday but is still vulnerable. The Greenback gained some ground following positive University of Michigan (UoM) Consumer Confidence figures. Still, the soft inflation figures reported on Wednesday and Thursday, adding dovish bets on the Federal Reserve (Fed), should limit the USD upside potential.

As for now, investors continue to discount a 25 basis point (bps) hike for the next July Fed meeting but refrain from betting on an additional hike in the rest of 2023. Its worth noticing that higher rates cool down the economy and hence lower the Oil’s demand adding selling pressure to its price.

On the other hand, traders should monitor China’s economic situation, the world’s biggest Oil importer. As economic activity and trade balance data should recently some weakness, it is expected the Chinese government to announce more stimulus measures to support the weakening domestic economy. In that sense, a stronger Chinese economy could boost Oil prices.

WTI Levels to watch

According to the daily chart, the WTI showed a bullish outlook, but indicators show signs of exhaustion. The Relative Strength Index (RSI) got rejected at the overbought threshold and prints a negative slope, while the Moving Average Convergence Divergence (MACD) printed a decreasing green bar.

Resistance Levels: $77.17 (200-day SMA), $78.00,$81.00.

Support Levels: $74.70, 73.55 (100-day SMA), $71.76 (20-day SMA).

WTI Daily chart

-638249514529207101.png)

- USD/MXN extends its losses, falling past the 16.80 mark, as the Mexican Peso benefits from easing US inflation.

- US Bureau of Labor Statistics shows import and export prices trending down, reinforcing previous reports of easing consumer and producer prices.

- Despite this, the US Federal Reserve is expected to lift rates 25 bps at July’s meeting.

USD/MXN extended its losses past the 16.80 mark, with the Mexican Peso (MXN) eyeing additional gains as inflation in the United States (US) subsides, as revealed during the week. The USD/MXN is exchanging hands at 16.8000, down 0.23%, and set to finish the week with losses of almost 1.90%.

US Inflation downtrend favors Mexican Peso; pair loses 1.90% over the week

The last week witnessed inflation figures easing in the US. The US Bureau of Labor Statistics (BLS) revealed that Import and Export prices continued their downtrend, falling below May’s and estimate numbers, aligning recent consumer prices and producer prices reports previously showcased on Wednesday and Thursday, respectively. Although the data could be used by the US Federal Reserve (Fed) to pause its tightening cycle, officials remain focused on bringing inflation towards its 2% goal.

Traders expect the US central bank to hike rates 25 bps at the upcoming July Federal Open Market Committee (FOMC) on 25-26, with odds at 96.1%. However, contrary to Fed policymakers saying that an additional increase is needed past the July meeting, the swaps market shows US rates peaking at 5.25%-5.50%.

The University of Michigan (UoM) revealed an improvement in US Consumer Sentiment, which was expected to print 65.5 but came at 72.6m at a two-year high. Further data showed that inflation expectations for one year were upward revised to 3.4% from 3.3% in June, while for five years, it edged high to 3.1%, up from 3%.

Joanne Jsu, the UoM Surveys of Consumers Director, said, “The sharp rise in sentiment was largely attributable to the continued slowdown in inflation along with stability in labor markets.”

US Treasury bond yields are recovering some ground, as the 10-year Treasury note rate sits at 3.816%, gaining four and a half basis points, while the US Dollar Index, a measure of the dollar’s performance against a basket of peers, stopped its drop at 99.887, gaining 0.10%.

Across the border, a light economic calendar in Mexico left USD/MXN traders leaning into the interest rate differential between both countries and recent US inflation data, which could warrant the Fed could finish its tightening cycle.

USD/MXN Price Analysis: Technical outlook

The USD/MXN monthly chart depicts that the pair might continue to trend lower as the next support emerges at the October 2015 swing low of 16.3267 and the 200-month Exponential Moving Average (EMA) at 16.3138. But firstly, a psychological 16.50 barrier must be taken out by sellers, which should be said, they had no issues taking psychological support levels out of the way, to the downside. Conversely, USD/MXN buyers must claim the July 2017 swing low of 17.4498, so they can have a chance, to lift exchange rates, to the 61.8% Fibonacci retracement at 17.7697, before rallyings toward the 18.0000 figure.

- AUD/USD retreats below 0.6850, still poised to make a 2.40% weekly gain, its highest in 2023.

- UoM US Confidence data provided some support to the USD.

- DXY Index stabilised below 100.00 but remains vulnerable.

At the end of the week, the Aussie lost some ground agains the Greenback as US Treasury yields somewhat recovered, lending the USD support. However, the pair is set to see further upside as it is expected the Federal Reserve (Fed) will tilt more dovish following soft inflation data from June.

In a tough week for the USD it was reported that the Core Consumer Price Index (CPI) from the US from June, dropped to 4.8% YoY in June, while the Core Producer Price Index (PPI) slid to 2.6% YoY in the same period. As markets seem to be taking off the table another rate hike past the July meeting, US Treasury yields declined, making the USD face severe selling pressure.

On the data front, the University of Michigan (UoM) reported that its Consumer Confidence Index increased to 72.6 in July from it previous 65.5 and provided some support for the USD.

On the Aussie’s side, investors await labor market data next week, including the Employment Change and Unemployment rate figures from June to be released next Thursday. In addition, investors should keep an eye on China’s situation as it is expected that the Chinese government will announce stimulus measures to bolster the economy. Regarding the Reserve Bank of Australia (RBA), Deputy Governor Bullock was appointed as the new Governor to replace Governor Lowe and her term is set to begin in September 18.

AUD/USD Levels to watch

Despite Friday’s downside movements, the AUD/USD’s outlook is bullish for the short term. The Relative Strength Index (RSI) and Moving Average Convergence Divergence (MACD) stand strong in positive territory while the pair trades above the 20, 100 and 200-day Simple Moving Averages.

Resistance Levels: 0.6900 (June high), 0.6950,0.6980.

Support Levels: 0.6785, 0.6750, 0.6715 (20-day Simple Moving Average).

AUD/USD Daily chart

-638249468263994885.png)

- USD/JPY recovered some ground but remained in danger of losing its early gains due to the slowing pace of inflation in the United States.

- The pair saw a brief uplift as a report from the University of Michigan indicated improved Consumer Sentiment, posting a two-year high.

- Rising household inflation expectations and speculation on adjustments to Yield Curve Control put pressure on the Bank of Japan.

USD/JPY recovers some ground but remains at the brisk of erasing most of its earlier gains after data from the United States (US) continued to show inflation is decelerating. At the same time, an improvement in US consumer sentiment lifted the pair towards its daily high of 139.15 before reversing its curse. The USD/JPY is trading at 138.47 after hitting a daily low of 137.21, up 0.31%.

USD/JPY trims losses on upbeat US data but inflation data on the US warrants less Fed tightening needed

The USD/JPY jumped during the latest hour after a report from the University of Michigan (UoM) saw an improvement in Consumer Sentiment, which was expected to print 65.5 but came at 72.6m at a two-year high. Joanne Jsu, the UoM Surveys of Consumers Director, said, “The sharp rise in sentiment was largely attributable to the continued slowdown in inflation along with stability in labor markets.” Additional data showed that inflation expectations for one year were upward revised to 3.4% from 3.3% in June, while for a five-year period, they were 3.1%, up from 3%.

Other data the US Department of Labor revealed showed US Import and Export prices slowed down, falling below the estimates in annual and yearly figures for June. The report aligned with the recent inflation data on the consumer and producer side, with numbers justifying the case for the US Federal Reserve (Fed) to keep rates unchanged if they want to, as prices are accelerating towards the Fed’s 2% goal. Nevertheless, Fed policymakers stressed that the battle against inflation has not been won, suggesting further tightening is needed.

US Treasury bond yields are recovering some ground, as the 10-year Treasury note rate sits at 3.793%, up two basis points, a tailwind for the greenback. The US Dollar Index, a measure of the dollar’s performance against a basket of peers, stopped its drop at 99.809, gaining 0.03%.

On the Japanese front, a Bank of Japan (BoJ) survey showed that households’ inflation expectations had risen, keeping the BoJ pressured. Also, expectations of the BoJ tweaking its Yield Curve Control (YCC) have been the main driver behind the Japanese Yen (JPY) strong week against most G8 FX currencies.

USD/JPY Price Analysis: Technical outlook

As of writing, the USD/JPY is struggling to decisively break the top of the Ichimoku Cloud (Kumo), which could pave the way for consolidation. USD/JPY’s sellers are eyeing the bottom of the Kumo at around 135.80/90, but the 200-day Exponential Moving Average (EMA) at 136.43 is expected to cushion the USD/JPY fall. On the upside, if USD/JPY buyers lift the pair past the top of the Kumo at around 138.50/60, it would exacerbate a challenge of the 139.00 psychological level.

The Gold price gained significantly following the publication of US inflation data on Wednesday. Economists at Commerzbank analyze XAU/USD outlook.

The market now only expects one more rate hike by the Fed

The Gold price has gained considerably, primarily thanks to the declining US inflation figures. After all, this makes it appear likely that the (US) rate hike cycle will soon come to an end: the market now envisages only one last rate increase at the end of July.

We agree and therefore expect prices to trend sideways in the coming weeks. They are likely to continue rising if the market begins discussing the subject of rate cuts.

The emergence of an El Niño weather event threatens to disrupt the already uncertain outlook for commodity markets, economists at ANZ Bank report.

El Niño is expected to increase demand for electricity

An El Niño typically brings drought to the western Pacific, rains to the equatorial coast of South America, and storms and hurricanes to the central Pacific. As such, we are likely to see warmer and drier weather in Europe and Asia. This will put further pressure on energy markets in the short term. Coal and Gas consumption is expected to rise.

We expect an increased level of disruptions to supply in the metals markets. Copper from South America is the most exposed. Aluminium supply in China is also at increased risk of disruption. On the flip side, demand for Gold could be impacted as lower revenue from reduced crops keeps India’s farmers hands in their pockets.

We could also see increase levels of carbon emissions brought about by increased fires and higher power consumption. Any potential pick-up in demand for carbon credits from industrial users and consumers could be offset by stronger renewable energy generation.

EUR/USD has had very little difficulty pushing through its spring high – just below 1.11. Economists at Rabobank analyze the pair’s outlook.

A soft USD is likely to prevail in the near-term

Signs of disinflation in the US and a high level of scepticism about the ability of the Fed to hike rates beyond the July meeting suggest that a soft USD is likely to prevail in the near-term. That said, signs that the ECB’s rate hike cycle is moving towards its peak suggest that EUR/USD could struggle to make further gains beyond the summer season. Additionally, if US recession fears strengthen into the end of the year, the USD could benefit from broad-based support.

We have revised down our USD forecasts across the board on a one-month view in response to the disinflationary signals in the US. However, in view of our house forecasts surrounding US recession risks, and in consideration of the economic headwinds facing the Eurozone, we see EUR/USD trading lower into year-end and through the early part of 2024.

Misery – defined as the unemployment rate plus inflation – is falling sharply in the US and more slowly in Europe. Kit Juckes, Chief Global FX Strategist at Société Générale, analyzes the implications for financial markets.

Can beating inflation be painless?

Risky assets would clearly benefit from a recession-free escape from inflation. The Dollar wouldn’t. Nor would the Dollar benefit from a mild recession that allowed European misery to melt away without too much pain (and the ECB to go on hiking after the Fed was finished).

But the tail risk that the Fed is encouraged to pause then pivot and stop raising rates, only to see tight labour markets drive a fresh upturn in underlying inflation next year, is now a real risk. That outcome, scuppering European recoveries and forcing the Fed to drive the economy in a late 2024 recession, may be a tail risk but it’s a big enough one to underpin FX volatility going forwards.

We think the volatility downtrend is over and bumpier markets are likely.

- UoM Consumer Confidence Index rose more than expected in July.

- US Dollar Index clings to modest recovery gains at around 100.00.

Consumer sentiment in the US continued to improve in early July, with the University of Michigan's (UoM) Consumer Confidence Index rising to 72.6 from 64.4 in June. This reading came in better than the market expectation of 65.5.

Further details of the publication revealed that the Current Conditions Index rose to 77.5 from 69.0 and the Expectations Index climbed to 69.4 from 61.5.

The one-year inflation outlook edged higher to 3.4% from 3.3% while the 5-year inflation outlook ticked up to 3.1% from 3%.

Market reaction

The US Dollar Index extended its daily recovery after the data and was last seen rising 0.23% on the day at 100.00.

With inflation receding faster in the US than Europe, economists at UBS expect the Dollar to weaken.

More investors to seek yield in Europe rather than the US

One key consequence of the steady retreat in global inflation will be a weaker US Dollar as price pressures ease faster in the US than in Europe.

Consumer energy subsidies in Europe meant inflation was slower to rise but will also be slower to fall. In turn, this should mean that interest rate differentials with the US will narrow – leading more investors to seek yield in Europe rather than the US.

We forecast EUR/USD to rise to 1.18 by June 2024.

- EUR/USD advances to new highs in the 1.1240/45 band.

- The next up-barrier emerges not before 1.1495.

EUR/USD’s intense upside seems to have met an initial barrier around 1.1240, or 2023 peaks, so far on Friday.

While the continuation of the upside momentum appears favoured in the very near term, the pair’s current overbought conditions might spark a corrective knee-jerk. Further upside is then expected to meet the next resistance level of note at the 2022 high of 1.1495 recorded on February 10.

Looking at the longer run, the positive view remains unchanged while above the 200-day SMA, today at 1.0651.

EUR/USD daily chart

The CAD has participated in the broader rally against the USD this week but gains have come grudgingly. Economists at Scotiabank analyze Loonie's outlook.

CAD set to gain a little at least relative to the USD coming months

The CAD is perhaps catching some of the spillover from the USD, with investors believing that the Fed and BoC will follow similar policy cycles. That may be true in a broad sense but there are other factors that should help the CAD gain a little at least relative to the USD coming months.

If the Fed rate cycle is peaking, which looks very likely, risk assets should improve somewhat, providing the CAD with some additional support. A softer USD should also be supportive for commodity prices. An array of factors already suggests the CAD should be somewhat stronger.

- Gold price has remained subdued around $1,960.00 as the US Dollar Index has attempted a recovery.

- In spite of a decline in price pressures, Fed Waller delivered a hawkish commentary.

- Gold price is gathering strength for further upside after a stalwart rally.

Gold price (XAU/USD) is demonstrating a subdued performance around $1,960.00 in the early New York session. The precious metal is struggling to deliver a decisive move as investors are hoping that the Federal Reserve (Fed) might skip the policy-tightening regime one more time this month.

After recognizing a consistent decline in inflationary pressures, Fed chair Jerome Powell skipped its policy-tightening spell in May but remained doors open for more rate hikes. June’s inflation report conveyed that price pressures have softened more than expected as prices of second-hand automobiles have dropped sharply.

Meanwhile, S&P500 is expected to open on a mildly bullish note amid a risk-on mood. The US Dollar Index (DXY) has delivered a short-lived pullback to near 100.00, however, the downside bias is still favored as fundamentals are still not supporting. The yields offered on 10-year US Treasury bonds have rebounded to near 3.79%.

In spite of the decline in price pressures, Fed Governor Christopher Waller delivered a hawkish commentary. Fed Waller is confident that two more interest rate hikes are appropriate this year to bring down inflation to 2%.

Gold technical analysis

Gold price is gathering strength for further upside after a stalwart rally on a two-hour scale. An inventory adjustment is under process as inventory is exchanged between institutional investors and retail participants. Potential resistance is plotted from June 07 high around $1,966.70.

Upward-sloping 20-period Exponential Moving Average (EMA) at $1,956.33 is providing support to the Gold bulls.

The Relative Strength Index (RSI) (14) has slipped below 60.00, which indicates exhaustion in the upside momentum.

Gold two-hour chart

- DXY bounces off 15-month lows in the 99.60/55 band.

- Extra downside appears favoured for the time being.

DXY manages to regain some composure and leaves behind recent lows in the vicinity of 99.60 on Friday.

The continuation of the decline of the dollar looks the most likely scenario for the time being. Against that, the breach of the current 2023 low at 99.57 (July 14) could spark a deeper pullback to the weekly low of 97.68 (March 30 2022).

Looking at the broader picture, while below the 200-day SMA at 104.37, the outlook for the index is expected to remain negative.

DXY daily chart

The price of a barrel of Brent Oil has been trading below $80 since the beginning of May but has recently approached this level again after an interim drop in June to $72. Economists at Commerzbank analyze Oil outlook.

Oil price set to rise due to tighter market

Demand concerns still stand in the way of a stronger price increase. For example, the economic recovery in China has noticeably lost momentum. Rising interest rates in the USA and Europe are likely to curb Oil demand there.

We have lowered our price forecast for a barrel of Brent Oil at the end of the year to $85. However, we are sticking to the expected price recovery.

Gold climbed by some 1.3 percent on Wednesday and Thursday as inflation eases, but a sustained rally is unlikely for now, Bart Melek, Head of Commodity Strategy at TD Securities, reports.

Rallies may soon run out of steam

For Gold, rising real rates as inflation eases and policy rates stay at the terminal level for a prolonged period may again drive specs away. In addition, the high rate environment, weak Chinese economic performance and a pending recession in the US will no doubt weaken the demand for more industrial metals like Copper and Silver for many months to come. While industrial demand is on the wane into 2023, the unplugging of COVID inspired bottlenecks in the supply chain will likely see mine and smelter production make more metal available.

This may well mean that the Gold, Silver and Copper rallies, which to a large degree have been short covering driven, may soon run out of steam as high opportunity and carry costs prevent any additional meaningful increase in long exposure. New longs are needed to move these markets past resistance, into bull territory.

This rally is vulnerable to reversals, should the Fed's policy rhetoric remain hawkish and if US data surprises to the upside.

Momentum will continue into the third quarter. The max analysts at Société Générale would expect is an S&P 500 of 4,750.

Momentum mania to build further before it breaks

Our tactical indicators also suggest a risk to the upside in Q3 before the lag effect of the rate-hiking cycle appears in early 2024 in the S&P 500.

Momentum mania in Q3 with the S&P 500 reaching 4,750 but likely ending the year at 4,300.

We believe the profit margin reversal, credit weakness and sharply rising recession risk will most likely be visible in 1H24, bringing the S&P 500 back to 3,800.

- USD/CAD has turned sideways above 1.3100 as investors await key triggers for further guidance.

- In June, US inflation grew at a nominal pace as a decline in prices of second-hand automobiles offset a marginal rise in gasoline prices.

- BoC Macklem cited that higher interest rates are needed to slow the growth of demand in the economy and relieve price pressures.

The USD/CAD pair is demonstrating signs of a squeeze in volatility above the immediate support of 1.3100 in the European session. The Loonie asset has turned choppy as the US Dollar Index (DXY) has found an intermediate support around 99.60.

S&P500 futures have recovered their entire losses and have turned positive in London, portraying a recovery in the risk appetite of the market participants.

The US Dollar Index (DXY) has gauged temporary support, however, the downside bias is still solid as investors are hoping that the Federal Reserve (Fed) will pause the policy-tightening spell after hiking interest rates by 25 basis points (bps) to 5.25-5.50% this month. Contrary to the USD Index, the 10-year US Treasury yields have rebounded to near 3.77%.

This week, June’s inflation report conveyed that price pressures grew at a nominal pace as a decline in prices of second-hand automobiles offset the marginal rise in gasoline prices. Core Consumer Price Index (CPI) also posted a nominal pace as demand for big-ticket items remained extremely weak. No doubt, at least one more interest rate hike by the Fed this year is in the pipeline, July’s interest rate hike can be skipped.

Going forward, preliminary Michigan’s Consumer Sentiment Index data (June) will be keenly watched. As per the consensus, the economic data is seen improved to 65.5 vs. the former release of 64.4.

On the Canadian Dollar front, the Bank of Canada (BoC) raised interest rates by 25 basis points (bps) to 5% this week. BoC Governor Tiff Macklem cited "Higher interest rates are needed to slow growth of demand in the economy and relieve price pressures."

Meanwhile, oil prices are expected to extend losses to near $76.00 as global central banks are preparing for a fresh interest rate hike cycle. It is worth noting that Canada is the leading exporter of oil to the United States and a decline in oil prices would impact the Canadian Dollar.

- EUR/JPY reclaims the area above 155.00 on Friday.

- Next on the upside comes the YTD high near 158.00.

EUR/JPY climbs to 4-day highs north of the 155.00 hurdle at the end of the week.

In the meantime, the cross keeps the recovery mode in place and the continuation of the uptrend carries the potential to challenge the so far 2023 peak in the boundaries of 158.00 the figure (June 29).

So far, the longer term positive outlook for the cross appears favoured while above the 200-day SMA, today at 145.88.

EUR/JPY daily chart

USD consolidates in light trade but hefty loss on the week takes a toll, economists at Scotiabank report.

BBDXY breakdown suggests losses of around 4%

While marginally higher on the day overall, the USD is heading for a soft close on the week, a signal that momentum traders are likely to try and exploit further in the coming days and weeks.

Both the DXY and the broader BBDXY have broken below the lows seen earlier this year. After a period of slack, low conviction range trading, a more dynamic phase of market movement might be about to unfold.

The DXY breakdown suggests USD losses may extend 2-3% or perhaps as much as 5% in the next few months. The BBDXY suggests losses of around 4% potentially from a technical point of view.

Considering the ongoing price action, Markets Strategist at UOB Group Quek Ser Leang assesses the outlook for GBP/USD.

Key Quotes

In our 3Q23 Quarterly Global Outlook published on 16 June 2023, when GBP/USD was trading at 1.2785, we highlighted that the crossover of the 21- and 55-week exponential moving averages in GBP/USD. We noted, “This could lead to GBP/USD rising to 1.3100 before the risk of a pullback increases”.

After trading below the short-term resistance level of 1.2850 for a few weeks, GBP/USD lifted off earlier this week, and yesterday (13 July 2023), it surged past our objective of 1.3100 (high of 1.3144). The strong boost in momentum suggests GBP/USD is unlikely to pullback. Instead, it is likely to continue to head higher towards the top of the weekly exponential moving average envelope. This major resistance level is currently at 1.3335.

In order to maintain the strong buildup in momentum, GBP/USD should not break below the ‘breakout’ level of 1.2850 in the next month or so. However, the key support level is at the rising trendline, now at 1.2730. From the perspective of several months, the 55week exponential moving average (now at 1.2400) is unlikely to come under threat.

USD/CAD is trading marginally higher on the day. Shaun Osborne, Chief FX Strategist at Scotiabank, analyzes the pair’s outlook.

There is some support in the 1.3075 area

Intraday gains suggest some mild upside risk for the USD in the short run but gains are liable to remain limited to the upper 1.31/1.3200 area.

Trend signals are tilting a little more bearishly for the USD now, with the daily DMI more aligned with negative intraday and weekly signals.

There is some support for the USD in the 1.3075 area (200-week MA) but a push to test 1.30 (50% Fibonacci retracement of the 2021/22 move up at 1.2992) remains my target.

Shaun Osborne, Chief FX Strategist at Scotiabank, analyzes GBP/USD technical outlook.

Pullbacks to the 1.29/1.30 range likely to be well-supported

The Pound’s powerful rally has stalled against resistance at 1.3145 (tested four times in the past 24 hours). This does not appear to be a major technical point for Cable, according to my read of the charts, however. In fact, there is little – obvious – resistance to GBP gains extending until the 1.33 area at this point.

Some consolidation in this week’s strong GBP gains should perhaps be expected in the short run.

Pullbacks to the 1.29/1.30 range are likely to be well-supported.

EUR/SD holds above 1.12. Economists at Scotiabank analyze the pair’s technical outlook.

Some consolidation would not surprise

Price action looks mildly negative on the day and short-term gains are stretched. Some consolidation in spot gains would not surprise.

The broader trend higher remains strong and bullish momentum suggests limited losses in the short run and more gains ahead.

EUR/USD closing out the week above 1.1183 (200-Week Moving Average) will be an added plus.

See: EUR/USD could correct lower back to the 1.1170-80 area – ING

Economist at UOB Group Ho Woei Chen, CFA, comments on the recently published trade balance figures in the Chinese economy.

Key Takeaways

China’s exports and imports (both USD and CNY terms) contracted by a sharper pace in Jun in further signs of fading recovery momentum in its economy. Declining export and import prices could also have contributed to the weak data which are reported in nominal values.

Only a handful of products recorded y/y increase in exports including motor vehicles, LCD panels and refined petroleum products. Meanwhile, shipments of high-tech products continued to contract, by -16.8% y/y in Jun compared to 13.9% y/y in May.

In volume terms, China’s imports of commodities including crude oil and coal strengthened in Jun. Copper and iron ore imports also held up well above the same period in 2022 despite slowing economic activities.

In 1H23, China’s exports and imports contracted by -3.2% y/y and -6.7% y/y respectively. The weaker than expected June trade data suggests downside risk for our forecast for China’s export and import which are currently at -3.0% and -2.0% for 2023 respectively.

Recent data had turned out to be weaker than expected, suggesting downside risk to our 2Q23 GDP forecast of 7.8% y/y, 0.9% q/q. The 2Q23 GDP report is due next Mon (17 Jul). We expect more measures to stimulate growth in 2H23 to be announced soon after.

The US Dollar Index (DXY) is returning to the 90-100 range, economists at MUFG Bank report.

DXY close to fully reversing the surge fuelled by the Fed’s dramatic hawkish shift last year

DXY fell back below the 100 level on Thursday for the first time since April 2022 and we are now close to fully reversing the USD surge fuelled by the Fed’s dramatic hawkish shift last year when central bank officials and investors realised the scale of the inflation shock at hand.

Over the last 10 years, DXY has tended to remain within a 90-100 range and we suspect we are returning back into that more normal trading range as the global inflation shock recedes.

- GBP/JPY is aiming to recapture 182.00 as investors are shifting their focus on the UK inflation data.

- Catalysts that have been propelling severe inflation in the UK economy are labor shortages and significantly higher food inflation.

- The BoJ might continue its decade-long ultra-dovish interest rate policy this month to elevate wage pressures further.

The GBP/JPY pair is marching towards the crucial resistance of 182.00 in the European session. The cross has picked strength after overstepping the previous day’s high of 181.45 as expectations of a tweak in the Bank of Japan’s (BoJ) ultra-dovish monetary policy by BoJ Governor Kazuo Ueda have lost their impact.

The contribution of higher domestic demand to inflationary pressures in Japan is increasing but is still far from the impact of higher prices of imported products. Wages have shown little promising signs of recovery but the journey towards a 2% stable inflation target is still far. The BoJ might continue its decade-long ultra-dovish interest rate policy this month to elevate wage pressures further.

Meanwhile, the Pound Sterling has hogged the limelight as investors are assured that more interest rate hikes by the Bank of England are in the pipeline so that inflation could return to 2%. After bleak employment reports, stable wage pressures, and weak factory activities, investors are shifting their focus toward inflation data, which will release on Wednesday at 06.00 GMT.

In May, annual headline inflation rebounded to 8.7% and core CPI that excludes volatile oil and food prices printed a fresh high of 7.1%. Catalysts that have been propelling severe inflation in the UK economy are labor shortages and significantly higher food inflation. For labor shortages, the entire blame goes to the Brexit event and early retirements by UK individuals. While food price inflation in the Britain economy dropped to 18.3% in May from its 45-year high of 19.1 and has not peaked yet.

Investors are questioning the relevance of the current level of share prices. Economists at Natixis highlight the two conditions which, if met, imply that – US and Eurozone – equity markets are not overvalued.

There are two conditions that, if met, imply that current share prices are not overvalued

The first condition is that real long-term interest rates (currently 1% in the US and 0.5% in the Eurozone) do not rise significantly. This condition is difficult to meet: the increase in public and private investment linked to the energy transition, water management and industrial reshoring is likely to lead to a shortage of savings and therefore a rise in real long-term interest rates.

The second condition, particularly in the US, is that artificial intelligence generates additional productivity gains. Opinions differ on this question, but it can only be said that the internet has been associated with a marked decline in productivity gains, whereas the opposite was initially believed (in the late 1990s).

UOB Group’s Economist Ho Woei Chen, CFA, assesses the recent interest rate decision by the Bank of Korea (BoK).

Key Takeaways

In line with consensus and our expectation, Bank of Korea (BOK) extended its interest rate pause to the fourth straight meeting today with the benchmark 7day repo rate staying at 3.50%.

It also continued to maintain a tightening stance with all the board members open to a further 25-bps hike to bring the terminal rate to 3.75%. Although inflation is on a downtrend, the risk factors on prices and household debt still exist.

The central bank maintained its GDP growth and headline inflation forecasts for 2023 at 1.4% and 3.5% respectively. Core inflation is projected to continue its slowing trend but may turn out to be slightly higher than the May forecast of 3.3%.

Considering the soft economic outlook and the general slowdown in inflation, we continue to expect the BOK to stay on hold for the rest of 2023. We think a rate cut could come into view in 1Q24. The next monetary policy meeting will be held on 24 Aug.

- US Dollar tries to snap losing streak as Greenback trades in the green.

- All eyes on Michigan Consumer Sentiment to see if the US Dollar can close this week off the lows.

- The US Dollar Index consolidates below 100.00, a weekly close above there would offer relief.

The US Dollar (USD) is trying to claw back a bit after a hectic week where the Greenback did not get any relief at all. At one point it appeared that everything was against the USD, with several inverse correlations kicking into gear. Most notable element is that the stock market has rallied throughout the week which puts a goldilocks scenario on the table where US rates will keep abating, stocks keep rallying and the Greenback will be left behind paying the bill for it all by devaluing even more.

On the economic front, just one really important element to look for which could make or break the small recovery seen in the US Dollar in the European trading session. The University of Michigan Consumer Sentiment could either offer some relief or trigger another round of US Dollar selling and could push the US Dollar Index further below 100.00, making it the worst week since November 2022. The inflation expectations component in the Michigan survey will be crucial as a possible catalyst.

Daily digest: US Dollar pays the bill for the equity rally

- Early on Friday, Christopher Waller from the Federal Reserve Board of Governors reiterated that the Fed needs to keep on fighting inflation and needs to keep policy restrictive for some time.

- The Japanese Yen deserves a moment in the spotlight as the Japanese tiger roars back by hitting an eight-week high against the Greenback.

- At 14:00 GMT, the only important datapoint for this Friday to keep an eye on as the Michigan Consumer Sentiment Index for July will be published. The index itself is expected to rise from 64.4 to 65.5. As such, that number should not have that much market-moving effect. Traders will rather look for the inflation expectations on both short and long term to be more impactful for the US Dollar Index to move higher or to make a new low for this week.

- Equities across the globe are taking it easy this Friday with some very mild losses at -0.17% for the Japanese Topix and the Chinese Hang Seng closed at +0.33%. For the latter, some negative news came as China vows to only provide support packages for specific segments and in the global economy, but no real large support package or quantitative easing is to be in place.

- European and US equity futures are flat for this Friday halfway through the European session. Although the goldilocks scenario might be the talk of the town, the earnings season could throw a spanner in the works for that straight line up to a new all time high.

- The CME Group FedWatch Tool shows that markets are pricing in a 94.9% chance of a 25 basis points (bps) interest-rate hike on July 26. A second rate hike looks to be out of the question judged on the very low percentages that scenario receives for the last Fed meetings later this year.

- The benchmark 10-year US Treasury bond yield trades at 3.97% and is continuing its relentless slide lower from 4.09% last week. Traders are going all-in on the goldilocks scenario where the Fed is done hiking and might even cut rates earlier as foreseen, which would see a massive boom in the economy and stock market.

US Dollar Index technical analysis: 100.00 still in reach

The US Dollar is having its worst week since its sharp correction in November last year. With substantial losses against the Japanese Yen (USD/JPY), Euro (EUR/USD) and Swiss Franc (USD/CHF), the US Dollar Index has lost nearly 2.5% of its value this week. As the DXY has retreated below 100.00, a weekly close above the big figure could spark hopes for the Greenback to still be able to pair back some of the losses.

In such an upside case, look for 102.73 to provide resistance at the 55-day Simple Moving Average (SMA) that will partially re-gain its importance after having been chopped up that much a few weeks ago. Only a few inches above the 55-day SMA, the 100-day SMA comes in at 102.82 and could create a firm area of resistance in between both moving averages. In case the DXY makes its way through that region, the high of July at 103.57 will be the level to watch for a further breakout.

On the downside, the US Dollar bears will look to take price action toward 99.42 as the next important technical support and once tested, that would mean a new 18-month low for the DXY. Just below there, on the weekly chart, we can find the 200-day SMA at 98.25, which is the next vital level to halt any selloffs. Although the price action resides below 100.00, a small turnaround could still be in the cards.

US Dollar FAQs

What is the US Dollar?

The US Dollar (USD) is the official currency of the United States of America, and the ‘de facto’ currency of a significant number of other countries where it is found in circulation alongside local notes. It is the most heavily traded currency in the world, accounting for over 88% of all global foreign exchange turnover, or an average of $6.6 trillion in transactions per day, according to data from 2022.

Following the second world war, the USD took over from the British Pound as the world’s reserve currency. For most of its history, the US Dollar was backed by Gold, until the Bretton Woods Agreement in 1971 when the Gold Standard went away.

How do the decisions of the Federal Reserve impact the US Dollar?

The most important single factor impacting on the value of the US Dollar is monetary policy, which is shaped by the Federal Reserve (Fed). The Fed has two mandates: to achieve price stability (control inflation) and foster full employment. Its primary tool to achieve these two goals is by adjusting interest rates.

When prices are rising too quickly and inflation is above the Fed’s 2% target, the Fed will raise rates, which helps the USD value. When inflation falls below 2% or the Unemployment Rate is too high, the Fed may lower interest rates, which weighs on the Greenback.

What is Quantitative Easing and how does it influence the US Dollar?

In extreme situations, the Federal Reserve can also print more Dollars and enact quantitative easing (QE). QE is the process by which the Fed substantially increases the flow of credit in a stuck financial system.

It is a non-standard policy measure used when credit has dried up because banks will not lend to each other (out of the fear of counterparty default). It is a last resort when simply lowering interest rates is unlikely to achieve the necessary result. It was the Fed’s weapon of choice to combat the credit crunch that occurred during the Great Financial Crisis in 2008. It involves the Fed printing more Dollars and using them to buy US government bonds predominantly from financial institutions. QE usually leads to a weaker US Dollar.

What is Quantitative Tightening and how does it influence the US Dollar?

Quantitative tightening (QT) is the reverse process whereby the Federal Reserve stops buying bonds from financial institutions and does not reinvest the principal from the bonds it holds maturing in new purchases. It is usually positive for the US Dollar.

After the US inflation data surprised so much on Wednesday the market is likely to pay even closer attention to the price and economic data. Antje Praefcke, FX Analyst at Commerzbank, analyzes USD outlook.

Only the precursor?

The inflation data on Wednesday might only have been a precursor for further Dollar weakness. Just imagine what would happen if the next price data surprises to the downside while the economic data also illustrates increasingly clearly that the past rate hikes are having a dampening effect on the US economy – albeit with the expected delay.

In case of an increasingly rapid fall in inflation and weakening economic data the market might increasingly rely on key rates not remaining at high levels for a long time whereas rate cuts before the end of the year are becoming increasingly likely. That would cause the USD to ease further.

It makes sense in my view to also pay attention to second-tier data now, such as US import prices and the US Michigan Index today. Simply in an effort not to miss the trigger for the next downward push in the Dollar.

- USD/CHF is building a base after a sheer correction to near 0.8570.

- It would be early calling the recovery move in the USD Index a reversal amid an absence of supportive economic indicators.

- Michigan Consumer Sentiment Index (June) data is expected to improve to 65.5 vs. the former release of 64.4.

The USD/CHF has found temporary support after a perpendicular sell-off to near 0.8570 in the London session. The Swiss Franc asset is still prone to more losses as fundamentals are still unfavorable and fresh shorts could be built ahead.

S&P500 futures have generated nominal losses in Europe. The US-500 stock basket has remained in the bullish trajectory in the past four-trading sessions but caution among market participants has appeared ahead of quarterly result season.

The US Dollar Index (DXY) is gatherings strength to extend its recovery move made after dropping to near 99.50. It would be early calling the recovery move a reversal amid an absence of supportive economic indicators. This week, the consumer and producer prices report for June month confirmed that the United States is set on track to achieving the 2% inflation target.

Demand for big-ticket items has dropped and gasoline prices have been squeezed, which has released some heat from red-hot inflation. However, labor market conditions are still tight and the core Consumer Price Index (CPI) which doesn’t include volatile oil and food prices is still at 4.8%. Therefore, fears of high inflation are still persistent and the Federal Reserve (Fed) has no chance than to raise interest rates further.

On Friday, investors will focus on preliminary Michigan Consumer Sentiment Index (CSI) (June) data. As per the consensus, the sentiment data is expected to improve to 65.5 vs. the former release of 64.4. Improvement in the market sentiment could be the outcome of a significant decline in inflationary pressures.

Meanwhile, the Swiss Franc is expected to remain solid as the Swiss National Bank (SNB) is expected to raise interest rates further despite inflation data has shown figures below 2% for once. For keeping inflation below 2% steadily, more interest rate hikes are warranted.

The Canadian Dollar may see further gains, economists at Société Générale report.

USD/CAD could repeat a move down to 1.26

The USD/CAD pair should continue to fall (very slowly).

USD/CAD peaked above 1.36 just after the end of the last Federal Reserve hiking cycle in December 2018.

The US Dollar traded down to CAD 1.26 as the Fed eased in 2019. A repeat is possible.

See – USD/CAD: A downside overshoot to 1.28 through Q3 looks to be a growing risk – Scotiabank

Senior Economist at UOB Group Alvin Liew reviews the latest release of US inflation figures (July 12).

Key Takeaways

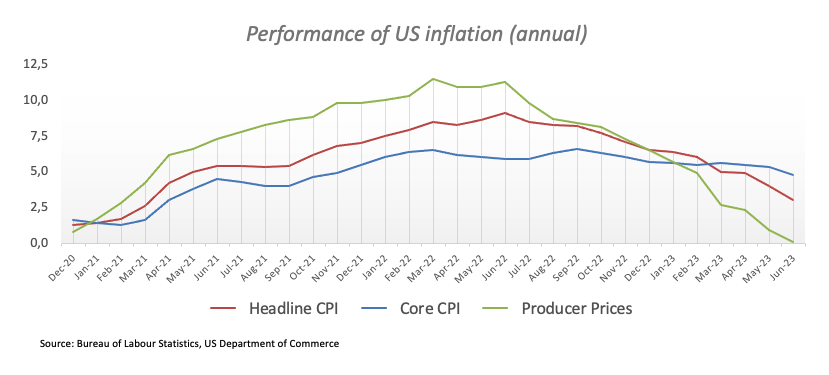

US headline consumer price index (CPI) increased by 0.2% m/m, 3.0% y/y in Jun (from 0.1% m/m, 4.0% y/y in May), below Bloomberg estimates (0.3% m/m, 3.1% y/y) and the lowest headline inflation reading since Mar 2021 (2.6%) and the third below 5% print in a row. Core CPI (which excludes food and energy) also rose at a slower than expected pace, coming in at 0.2% m/m, 4.8% y/y in Jun (versus Bloomberg estimate of 0.3% m/m, 5.0% y/y), compared to 0.4% m/m, 5.3% y/y in May. This was the smallest m/m increase for core CPI since Aug 2021, while the y/y print of 4.8% was the first sub-5% print since Nov 2021.

US Inflation Outlook – Taking stock of the price trajectory to date, we now expect headline inflation to potentially head to sub-1% by end 2023 (in part due to base effects) and to average about 3.2% for 2023. In comparison, while core inflation continues to ease, the pace is clearly slower than the headline, so we now expect core inflation ease to 3.0% y/y by end-2023, still above the Fed’s 2% objective. For the full year, we expect core inflation to average 4.6%. That said, we think that a clear disinflation trend has set in for US CPI, and we expect accommodation costs to ease more visibly in 2H 2023. We also note that core and services inflation remain elevated (y/y) and still rising (m/m), while the continued wage growth may still add to services cost pressure.

- Silver price has shown signs of a loss in the upside momentum while rallying towards $29.00.

- June’s Retail Sales data is seen expanding at a pace of 0.5% vs. the former pace of 0.3%.

- Silver price has delivered a break above the horizontal resistance plotted from $24.59, which has turned into support now.

Silver price (XAG/USD) has sensed selling pressure while attempting to capture the crucial resistance of $29.00 in the London session. The upside momentum in the white metal is losing strength as the US Dollar Index (DXY) has attempted a recovery, however, the upside bias is still intact.

S&P500 futures are showing choppy moves portraying caution among market participants as companies are ready to report second-quarter earnings. Mixed earnings are expected from corporate as the Federal Reserve (Fed) remained aggressive while hiking interest rates from last year’s winter. Also, United States commercial banks deployed more filters on the credit distribution process to maintain asset quality.

The US Dollar Index has rebounded after a straight six-day decline to near 99.50. Price pressures in the United States economy have dropped as gasoline prices have softened sharply and individuals have surrendered spending on big-ticket items to cater to necessities. Households’ real income has slimmed due to higher inflationary pressures.

Going forward, investors will focus on the monthly US Retail Sales data (June), which will release on Tuesday at 12:30 GMT. As per the consensus, the economic data is seen expanding at a pace of 0.5% vs. the former pace of 0.3%.

Silver technical analysis

Silver price has delivered a break above the horizontal resistance plotted from June 09 high at $24.59 on a daily scale, which has turned into support now. The asset is approaching its next stoppage, which is placed from 10 March 2022 high at $26.07.

Upward-sloping 10-period Exponential Moving Average (EMA) at $23.74 is providing support to the Silver bulls.

The Relative Strength Index (RSI) (14) has jumped above 60.00, showing no signs of divergence and any signal of overbought.

Silver daily chart

-638249238846447123.png)

Strategists at UBS are neutral on broad commodities but continue to like both Oil and Gold.

Brent Crude Oil to rise to $90/bbl by year-end

We see balanced risk and reward in broad commodity indexes. Weaker-than-expected growth in China means that concerns about industrial metal demand remain elevated. That said, secular demand drivers (such as the net-zero carbon transition) should provide longer-term support, and in energy, supply discipline means that inventories remain at structurally low levels.

The Oil market is likely to tighten further in the second half, and we forecast Brent Crude prices rising to $90/bbl by year-end.

Gold prices should be supported by a resumption of the US Dollar's downtrend and we like the yellow metal as a diversifier and a hedge within portfolios.

FX option expiries for July 14 NY cut at 10:00 Eastern Time, via DTCC, can be found below.

- EUR/USD: EUR amounts

- 1.0900 1.3b

- 1.0925 486m

- 1.0960 1.8b

- 1.1000 2.4b

- 1.1075 460m

- 1.1120 818m

- 1.1165 545m

- 1.1200 971m

- USD/JPY: USD amounts

- 140.00 780m

- 141.00 570m

- 141.25 550m

- 141.50 439m

- 144.00 450m

- USD/CHF: USD amounts

- 0.9750 1.3b

- AUD/USD: AUD amounts

- 0.6700 990m

- 0.6900 804m

- USD/CAD: USD amounts

- 1.3040795m

- 1.3100 700m

- 1.3225 502m

- 1.3265 368m

- 1.3440 316m

Economists at ING analyze US Dollar Index (DXY) outlook.

A pause or upside correction in the Dollar could come at any time

DXY broke below the 100.00 barrier on Thursday, and the next logical support would likely be at 99.00.

A pause or upside correction in the Dollar could come at any time given the large swings of the past couple of days.

Friday’s moves suggest we could see some re-adjustment/stabilisation happen today with a quiet calendar. However, downside risks will keep prevailing for the Dollar in the near term.

- AUD/USD edges lower on Friday and snaps a three-day winning streak to a nearly one-month high.

- Rebounding US bond yields helps ease the USD bearish pressure and acts as a headwind for the pair.

- Bets that the Fed will soon end its rate-hiking cycle to cap the upside for the USD and lend support.

The AUD/USD pair pulls back from the vicinity of the 0.6900 mark on Friday and eroded a part of the previous day's strong rally to a nearly one-month peak. Spot prices drop to a fresh daily low, around the 0.6860 region during the early part of the European session and for now, seem to have snapped a three-day winning streak, though the near-term bias still seems tilted in favour of bullish traders.

A modest pickup in the US Treasury bond yields assists the US Dollar (USD) to stall its recent sharp downfall to the lowest level since April 2022, which, in turn, is seen as a key factor acting as a headwind for the AUD/USD pair. Apart from this, a slightly negative tone around the US equity futures further contributes to capping the upside for the risk-sensitive Aussie. That said, growing acceptance that the Federal Reserve (Fed) is nearing the end of its policy tightening cycle should limit any meaningful USD recovery and validate the near-term positive outlook for the major.

The US economic data released this week pointed to a further moderation in inflationary pressures and should allow the Fed to soften its hawkish stance. In fact, the headline US CPI slowed to the 3% yearly rate - marking the smallest rise since March 2021, while the monthly rise in core prices was the smallest since August 2021. Moreover, the US PPI for June registered the smallest year-on-year rise since August 2020. This, in turn, reaffirmed market bets that the US central bank will keep interest rates steady after the widely anticipated 25 bps lift-off at its July monetary policy meeting.

Apart from this, hopes that China will announce more stimulus measures to support the fragile domestic economy might also lend some support to the China-proxy Australian Dollar (AUD). Adding to this, optimistic remarks by China's Foreign Minister Wang Yi, saying that China-Australia relations have stabilised, improved and developed, supports prospects for the emergence of some dip-buying around the AUD/USD pair. Bulls, however, might wait for a sustained breakout through the 0.6900 round-figure mark before placing fresh bets and positioning for any further gains.

Market participants now look forward to the release of the Preliminary Michigan US Consumer Sentiment Index. This, along with the US bond yields and the broader risk sentiment, might influence the USD and provide some impetus to the AUD/USD pair on the last trading day of the week. Nevertheless, spot prices remain on track to register strong weekly gains as the focus now shifts to important Chinese macro data due during the Asian session on Monday.

Technical levels to watch

Economists at Commerzbank analyze EUR outlook as the stubborn inflation continues to cause grave concerns for the ECB.

ECB rate cuts are being priced in only very cautiously, but quite convincingly for the US

The market is still pricing in a few more rate hikes for the ECB and what is probably more decisive: ECB rate cuts are being priced in only very cautiously, but quite convincingly for the US.

No doubt we could argue whether the market’s view on the Fed is exaggerated, but the most recent inflation data illustrated that the ECB will have to do more or will have to maintain a restrictive monetary policy for longer. Even if a few doves amongst the ECB board members have recently commented the data is pointing in another direction (for now). And as the ECB will certainly not want to give cause to doubts that it is doing its job properly that is positive for EUR.

- Pound Sterling has slipped modestly as investors are awaiting key inflation data for a fresh trigger.

- United Kingdom’s inflation is set to remain sticky as labor shortages are still a major issue.

- Food price inflation is expected to decelerate to 9% by December.

Pound Sterling has sensed light profit booking after printing a fresh annual high at 1.3140. The GBP/USD pair will likely resume its north-side rally amid an absence of evidence that the United Kingdom’s inflation will cool down. To return inflation to 2%, the Bank of England (BoE) has already raised interest rates to 5% and further policy-tightening is in the pipeline.

United Kingdom’s labor market data missed estimates this week but wage pressures remained elevated as firms are offering higher salaries to bring fresh talent in-house considering labor shortages. No doubt, higher disposable income equipped with households would propel inflationary pressures, which would threaten the economic outlook. Investors will keep an eye on next week’s inflation data as a stubborn report could trigger fears of recession.

Daily Digest Market Movers: Pound Sterling senses pressure as risk appetite eases

- Pound Sterling has dropped to near 1.3100 as the US Dollar Index (DXY) has attempted a recovery move after a five-day losing streak.

- After United Kingdom’s weak labor market report, rising wage pressures, and bleak factory activities, investors need guidance on interest rates peak from the Bank of England.