- Аналітика

- Новини та інструменти

- Новини ринків

Новини ринків

- EUR/USD trades in positive territory for the third consecutive day on the lower Treasury bond yields.

- European Central Bank (ECB) Vice President Luis de Guindos said Eurozone economic growth will remain weak in the near term.

- Fed Chair Jerome Powell reiterated that the Fed will hike rates again if deemed necessary to bring inflation to the 2% target.

- Investors will closely watch the Eurozone growth numbers, and US inflation data on Tuesday.

The EUR/USD pair climbs to 1.0700 during the early Asian session on Tuesday. The lower US Treasury bond yields weigh on the US Dollar (USD) and lend some support to the pair. However, the fear of recession in the Eurozone might capped the upside of the Euro. The major pair currently trades around 1.0700, up 0.01% on the day.

The European Central Bank (ECB) Vice President Luis de Guindos said that Eurozone economic growth will remain weak in the near term. He further stated that there are signs that the labor market is beginning to weaken. However, it will be in a better position to reassess the inflation outlook and required action in the December meeting. ECB President Christine Lagarde highlighted that inflation remained too high and central bank should bring inflation down to its target while maintaining the current restrictive stance for a longer period.

Market players await the Eurozone Gross Domestic Product (GDP) for the third quarter (Q3). The quarterly growth number is expected to contract by 0.1% while the annual number is forecasted to grow by 0.1%. If the GDP data showed weaker-than-expected results, this could exert some selling pressure on the EUR.

On the USD’s front, the New York Fed’s 1-year and 5-year inflation outlook eased to 3.57% and 2.72%, respectively. The Federal Reserve (Fed) keeps track of inflation expectations data as the policymakers believe that the expected direction of price pressures has a significant impact on where inflation stands now. Fed Chair Jerome Powell reiterated that the Fed will hike rates again if deemed necessary to control inflation. However, Fed tightening expectations remain subdued, as the CME FedWatch Tools shows 11.8% odds of a hike on December 13

Later on Tuesday, Eurostat will release the Eurozone employment, growth data, and ZEW survey. On the US docket, the US Consumer Price Index (CPI) will be due. Traders will take cues from these figures and find a trading opportunity around the EUR/USD pair.

- The AUD/NZD is grinding it out on Monday, testing into higher ground.

- The Aussie is rebounding on a technical basis after declining most of November.

- Resistance is piled up, bulls face uphill battle.

The AUD/NZD has climbed nearly 0.6% as the Aussie (AUD) rallies against the Kiwi (NZD) following two straight weeks of declines.

Hourly candles have the AUD/NZD running straight into the 200-hour Simple Moving Average (SMA) just south of 1.0860. The pair was constrained by the 50-hou SMA following early November's decline from 1.0900, and now the AUD/NZD finds itself trading into the top end of the constraining pattern between the two moving averages.

Monday's clean break upwards from 1.0780 sees the pair pushing through a descending trendline drawn from November's peak bids near 1.0940, and the challenge for bidders will be to keep the momentum going.

On the daily candlesticks, the AUD/NZD looks set to struggle in the midrange after failing to make a firm downside break of the 200-day SMA, and the long-term trend of the AUD/NZD looks set to remain sideways for the foreseeable future.

AUD/NZD Hourly Chart

AUD/NZD Daily Chart

AUD/NZD Technical Levels

- AUD/USD remains capped below the 0.6400 mark in early Tuesday.

- The New York Fed’s 1-year and 5-year inflation outlooks eased to 3.57% and 2.72%, respectively.

- The US Consumer Price Index (CPI) will be the highlight on Tuesday.

The AUD/USD pair recovers some lost ground but remains capped under the 0.6400 psychological mark during the early Asian session on Tuesday. Markets turn cautious ahead of the US Consumer Price Index (CPI), due later on Tuesday. This event could offer hints about the progress of inflation toward its 2% target. At press time, AUD/USD is trading around 0.6375, losing 0.05% on the day.

Meanwhile, the US Dollar Index (DXY), an index of the value of the USD measured against a basket of six world currencies, hovers around 105.65 after retreating from 106.00. The US Treasury bond yields edge lower, with the 10-year yield dropping to 4.63% and the 2-year yield falling to 5.03%.

The New York Fed’s survey of consumer expectations showed the 1-year and 5-year inflation outlooks eased to 3.57% and 2.72%, respectively. Meanwhile, the US government reported a $66 billion budget deficit in October, compared to a deficit of $87 billion during the same month of last year. Tuesday’s spotlight will be the US inflation data. The Consumer Price Index (CPI) is expected to grow by 0.1% in October, and the core inflation measure is estimated to remain at 4.1%. These figures might convince the Federal Reserve (Fed) of additional tightening, as FOMC views are warranted by the data.

On the Aussie front, Reserve Bank of Australia (RBA) Assistant Governor (Economic) Marion Kohler said that a decline in inflation to be slower than previously thought due to the still-high level of domestic demand and strong labor and other cost pressures. Kohler further stated that a tighter policy to counter high inflation is required. The market anticipates that the RBA will hike additional rates in the first half of next year.

Looking ahead, market players will monitor Australia’s Westpac Consumer Confidence and the National Australia Bank's Business surveys. Also, the US CPI data will be due on Tuesday. Later this week, the Australian Q3 Wage Price Index will be due on Wednesday, and the Australian employment report will be released on Thursday.

- AUD/JPY records a slight decline of 0.08% in the Asian trading session, currently positioned at 96.68, following a peak at 96.85.

- Technically, AUD/JPY maintains a neutral stance, though surpassing 96.81 could lead the pair towards 97.00.

- Conversely, inability to break above the Tenkan-Sen might trigger selling pressure, with initial support at Monday’s low of 96.18.

AUD/JPY began the Asian session with minuscule losses of 0.08%, as Wall Street’s turned negative towards the end of Monday’s trading session, ahead of the release of the US CPI data. The pair is trading at 96.68 after hitting a weekly high of 96.85.

From a technical standpoint, the AUD/JPY is neutral biased, facing resistance at the Tenkan-Sen level at 96.81. A breach of that area can open the door to test 97.00, followed by the 2023 high of 97.63m before reaching the 98.00 mark.

On the other hand, failure to conquer the Tenkan-Sen could expose the pair to some selling pressure, with bears targeting Monday’s low of 96.18. Up next would be the psychological 96.00 figure, followed by the Kijun-Sen at 95.83, and the top of the Ichimoku Cloud (Kumo) at 95.00.

AUD/JPY Price Analysis – Daily Chart

AUD/JPY Technical Levels

- The USD/JPY climbed a scant twentyish pips on Monday, closes day towards the midrange.

- Yen markets saw a pop into a hefty expiry on JPY options.

- US CPI inflation numbers in the crosshairs for Tuesday.

The USD/JPY plummeted in Monday's intraday trading, skidding into 151.20 before recovering on the day.

Investors initially feared a market operation by the Bank of Japan (BoJ) to intervene on the Yen's behalf, but a large bundle of options expiries proved to be the culprit. $1.2 billion dollars in Yen options hit the deadline during Monday's US trading session, with an additional $2.2 billion in Yen options coming due in the near future.

The options expiry rallied Yen across the board before sending JPY pairs back into familiar bids.

Tuesday sees the US Consumer Price Index (CPI) inflation figures, and markets are forecasting further cooldown on US inflation.

The Headline CPI reading for October is expected to slip from 0.4% to 0.1%, while the Core CPI (CPI less volatile food and energy prices) is expected to hold steady at -0.1%.

USD/JPY Technical Outlook

The Dollar-Yen hit an intraday high of 151.91, just shy of the 152.00 major handle. The pair is just inches away from clearing 2022's high bids of 151.94. A break of this level would see the USD/JPY trading into its highest prices since 1990, a 33-year high.

Intraday action has been catching bounces from technical support at the 50-hour Simple Moving Average (SMA), and traders will be keeping extra wary of any downside shock towards the 200-hour SMA currently drifting into 150.70.

USD/JPY Hourly Chart

USD/JPY Technical Levels

- The NZD/JPY is seen at 89.15 with 0.15% losses.

- Bulls continue to be on the sidelines after November’s strong start.

- Indicators suggest that the bears are gaining momentum.

The NZD/JPY saw little downward movements on Monday near the 89.15 area as bulls continued consolidating a solid start of the month.

In that sense, according to the daily chart, the NZD/JPY has a neutral to bearish technical outlook, with indicators signalling a short-term pause in the bulls' upward movement as they consolidate after winning more than 3% at the beginning of November. The Relative Strength Index (RSI) exhibits a negative slope above its midline, while the Moving Average Convergence (MACD) presents lower green bars. In the broader context, despite showing a negative outlook in the short-term, the pair is above the 20,100,200-day Simple Moving Average (SMA), suggesting that the bulls are firmly in control of the overall trend.

Zooming in, the four-hour chart shows that the bearish presence is more evident, with the RSI and MACD standing in negative territory. In that sense, the sellers may continue gaining ground as long as the bulls remain asleep.

Support levels: 89.00, 88.75, 88.30 (100-day SMA).

Resistance levels: 89.30 (20-day SMA), 89.50, 90.00.

NZD/JPY daily chart

-638355085356267655.png)

- The EUR/GBP is seeing downside drift ahead of Tuesday's data headliners.

- The Euro is falling back after last week's steady climb.

- Up Next: UK wages & labor, EU labor & GDP.

The EUR/GBP is softening ahead of a key data double-header for both the EU and the UK, with labor, wages, and Gross Domestic Product (GDP) numbers.

The Euro (EUR) is falling back against the Pound Sterling (GBP) heading into the Tuesday market session, declining around 0.4% peak-to-trough on Monday.

UK Average Earnings for the 3rd quarter is expected to decline slightly from 7.8% to 7.7%, while earnings including bonuses is expected to tick downward at a fast pace, from 8.1% to 7.4%.

The UK will also be seeing Employment Change for September, which last showed the UK shed 82 thousand jobs over the month, while Claimant Count Change in October showed an increase in unemployment benefits seekers to the tune of nearly 20.5 thousand.

On the EU side, quarter-on-quarter Employment Change for the 3rd quarter is expected to show a moderate 0.2% gain, while the EU's pan-continental GDP for the quarter is expected to print at a steady reading of -0.1%.

EUR/GBP Technical Outlook

The Euro is falling back into the 200-hour Simple Moving Average (SMA) Against the Pound Sterling, paring back some of the pair's gains from last week.

Monday's decline trims away gains from the swing high into 0.8755, slipping into the bearish side of a rising trendline from last week's low bids near 0.8650.

With the EUR/GBP drifting towards the midrange in the near-term, bidders will be waiting for a downside break of the 0.8700 handle before re-upping positions, while sellers will be considering a trimming below the same level.

EUR/GBP Hourly Chart

EUR/GBP Technical Levels

- EUR/JPY advances for the second consecutive day, trading around 162.27, reflecting a 0.25% rise amid a favorable risk-on market environment.

- The pair shows an upward bias on the daily chart, with a significant resistance level at the August 2008 high of 165.60.

- On the downside, initial support is identified at the Tenkan-Sen level of 160.72, followed by the Senkou Span A at 160.07 and the Kijun-Sen at 159.44.

EUR/JPY continues to advance for the second straight day, gaining traction toward 162.50 in late trading during the North American session, amid a risk-on impulse and despite Japanese authorities' intervention threats. At the time of writing, the EUR/JPY is exchanging hands at 162.27 up 0.25%.

From a daily chart perspective, the EUR/JPY remains upward biased, with the next resistance level emerging at around the August 2008 high of 165.60. A breach of the latter would expose the July 2008 high of 169.97, ahead of challenging the 170.00.

On the opposite flip side, the EUR/JPY first support would be the Tenkan-Sen level at 160.72 before challenging the Senkou Span A at 160.07 and the Kijun-Sen at 159.44.

EUR/JPY Price Analysis – Daily Chart

EUR/JPY Technical Levels

- Silver prices recover, trading at approximately $22.32 an ounce, marking a 0.27% gain after touching five-week lows at $21.88.

- Technical analysis reveals a neutral to downward bias, but a 'hammer' pattern formation on the daily chart suggests potential bullish momentum.

- For a bullish shift, silver needs to surpass the 50-day moving average (DMA) at $22.65, targeting the 200-DMA at $23.25 and the October 20 high at $23.69.

Silver price finds its foot and rises after reaching five-week lows at $21.88 on Monday, and exchanges hands at around $22.32 a troy ounce, late during the North American session, printing gains of 0.27%, at the time of writing.

From a technical standpoint, the grey’s metal is neutral to downward biased, but the daily chart portrays price action is forming a ‘hammer,’ usually a bullish signal, after posting a series of seven successive days registering lower highs and lows, that ended on Monday.

Hence, if XAG/USD would turn bullish, buyers must initially reclaim the 50-day moving average (DMA) at $22.65. A breach of the latter would expose the 200-DMA at $23.25, followed by October 20, the latest cycle high at $23.69. Once cleared, a bullish resumption would be underway.

On the other hand, a drop below the October 13 low of $21.87, would cement a bearish case, with sellers next target being the October 4 swing low of $20.69, followed by the year-to-date (YTD) low of $19.90.

XAG/USD Price Analysis – Daily Chart

XAG/USD Technical Levels

The critical report on Tuesday is the US Consumer Price Index. During the Asian session, the Australian Westpac Consumer Confidence Index and the National Australia Bank's Business Survey are due. Later in the day, the UK will report jobs data, Switzerland will release wholesale inflation data, and the Eurozone will publish Q3 GDP and employment numbers.

Here is what you need to know on Tuesday, November 14:

The US Dollar Index (DXY) fell for the second consecutive day, extending its retreat from the 106.00 area to 105.60. The decline in the Greenback was influenced by lower US Treasury yields and higher commodity prices. The 10-year yield dropped to 4.62%, while the 2-year yield fell to 5.02%.

Market attention is focused on US inflation data scheduled for release on Tuesday. The Consumer Price Index (CPI) is expected to rise by 0.1% in October, with the annual rate slowing from 3.7% in September to 3.36% in October. The core annual rate is forecasted to remain at 4.1%. If the numbers align with expectations, it would reinforce the market's belief that the Federal Reserve has finished raising interest rates.

US CPI Preview: Forecasts from seven major banks, still to the high side of the Fed's target

The EUR/USD held above 1.0650 and climbed to the 1.0700 area, exhibiting sideways movement in the short-term. Eurostat is set to release employment and growth data from the third quarter. Also due is the ZEW survey for November.

The GBP/USD had a bullish bias throughout the day and rose to 1.2280 after staying above the 20-day Simple Moving Average (SMA). The UK will report employment data on Tuesday, including Average Earnings.

The USD/CHF reached weekly highs before retracing towards 0.9000. Switzerland's wholesale inflation data is due on Tuesday, and Swiss National Bank (SNB) Chairman Thomas Jordan is scheduled to deliver a speech.

After a five-day decline, the AUD/USD rose, finding support above 0.6330 and approaching 0.6400. On Tuesday, the Westpac Consumer Confidence and the National Australia Bank's Business surveys will be released. The key report of the week will be the employment figures on Thursday. The Q3 Wage Price Index will be relevant on Wednesday.

The NZD/USD found support around the 0.5865 area at the 20-day SMA and rebounded, but could not reclaim 0.5900. Stats NZ will publish the Food Price Index and will begin releasing other monthly price indexes.

The USD/CAD ended the day flat, hovering around 1.3800. The pair remains sideways without clear signals.

Commerzbank on the Canadian Dollar:

The Bank of Canada (BoC) suspended its rate hike cycle for the second time in early September and has kept its key interest rate stable at 5% since then. At the same time, the Fed is discussing another rate hike. This difference in monetary policy is currently supporting USD-CAD. In the coming weeks, however, it is likely to become clear that there will be no further rate hikes in the US either. As we expect a recession in the US next year, while the Canadian economy is likely to achieve a soft landing, we see CAD recovery potential next year.

Like this article? Help us with some feedback by answering this survey:

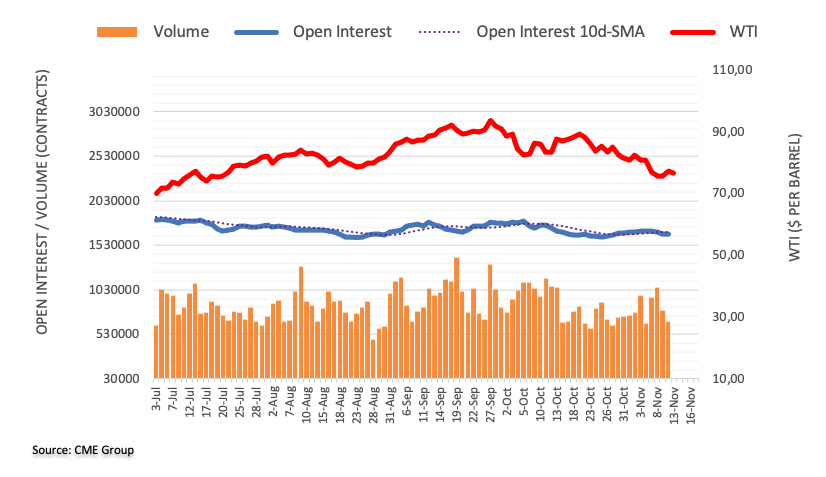

- West Texas Intermediate (WTI) crude oil sees an uptick, buoyed by OPEC+'s revised demand outlook and production shifts.

- OPEC+ report indicates an increase in oil production, particularly from Iran, Angola, and Nigeria, countering concerns over a slowing Chinese economy.

- US Energy Information Administration (EIA) forecasts that a slight decrease in US oil production and Fed hawkish remarks could dent Oil’s demand.

West Texas Intermediate (WTI), the US Crude Oil benchmark, advances more than 1% on Monday, courtesy of an upward revised outlook for Oil’s demand, OPEC+ reported, easing off worries that a global economic outlook could influence prices, amongst less demand woes. WTI is trading at $78.18.

West Texas Intermediate benefits from OPEC+'s optimistic demand forecast and production changes

A report from the Organization of Petroleum Exporting Countries and its allies (OPEC+) upward revised oil production, disregarding fears linked to a weak Chinese economy, which could dent oil demand. OPEC+ added that production rose due to production increases in Iran, Angola, and Nigeria.

On the contrary, a report from the US Energy Information Administration (EIA) said that US oil production would rise slightly less than expected previously, which was blamed on a lower demand. Alongside that, a hawkish stance by the US Federal Reserve (Fed) Chairman Jerome Powell, suggesting that it could raise rates, stroked fears about WTI’s demand outlook.

Another Fed hike could underpin the Greenback (USD), a headwind for US dollar-denominated commodities, which could weigh WTI prices.

Nevertheless, Saudi Arabia and Russia pledge to maintain a 1.3 million barrel cut toward the end of 2023, which would likely keep Oil’s price underpinned and most likely at around current prices.

WTI Price Analysis: Technical outlook

From a technical standpoint, WTI is testing the 200-day moving average (DMA) at $78.19, which would open the door for further upside, like the $80.00 per barrel barrier. A breach of the latter would expose the November 7 high of $81.01, ahead of challenging the 50-DMA at $82.45. On the flipside, if the 200-DMA holds, a WTI dive toward the November 8 swing low of $74.96 is on the cards.

The US government recorded a $66 billion budget deficit in October. The Treasury Department informed that receipts totalled $403 billion and outlays $469 billion. It compares to a deficit of $87 billion during the same month of last year.

- The USD/SEK declined to a low of 10.825.

- The Swedish CPI from October will be reported on Tuesday and is expected to rise to 6.7% YoY.

- US CPI from October is also due on Tuesday.

The USD/SEK fell sharply on Monday to a daily low of 10.825 and then consolidated around 10.830, showing a daily decline of 0.40%, driven a weakening USD, ahead of the report of both country's Consumer Price Indexes (CPI) readings from October.

On Tuesday, the SCB Statistics from Sweden is expected to report that the Consumer Price Index (CPI) from October rose to 6.7% from its previous 6.5%. In that sense, if the reading comes in higher than expected, it may fuel further downside on the pair on the back of hawkish bets on the Riksbank, which left the door open for further tightening.

On the other hand, markets await the US CPI on Tuesday and Producer Price Index (PPI) and Retail Sales figures on Wednesday, which will provide the Federal Reserve (Fed) with fresh evidence on the US inflation outlook. Last week, bank officials and Chair Powell were seen as cautious and stated that the "job wasn’t done", pointing out that they’ll need more evidence to confirm that inflation is coming down. For the upcoming December meeting, markets seem to be confident that the Fed won’t hike, and the USD’s trajectory will likely be set on how long investors will price in rates at restrictive levels based on the outcome of the incoming data.

USD/SEK levels to watch

Based on the daily chart, the USD/SEK holds a bearish bias, with indicators reflecting that the bears are strengthening. The Relative Strength Index (RSI) reveals a downward slope below its middle point, while the Moving Average Convergence (MACD) histogram presents larger red bars. On the broader scale, the pair is also below the 20 and 100-day Simple Moving Averages (SMAs), but above the 200-day SMA, suggesting that the bulls continue to exhibit strength in the overall trend but are seen as weak on the shorter time frames.

Supports: 10.830, 10.770, 10.760

Resistances: 10.862 (100-day SMA), 10.900, 10.980.

USD/SEK daily chart

-638354994147541824.png)

- The GBP/USD is seeing some minor lift ahead of Tuesday's bumper data reading.

- An easy Monday to give way to a bumper economic calendar data docket.

- UK wages & labor, US CPI in the barrel.

The GBP/USD climbed to a Monday high near 1.2280 as markets jockey for position ahead of Tuesday's bumper data prints, with UK wages and labor data hitting markets in the early London session before US Consumer Price Index (CPI) inflation figures drop on investors in the mid-day.

UK Average Earnings (excluding bonuses) for the 3rd quarter is expected to moderate, with the forecast expected to tick down from 7.8% to 7.7%; meanwhile, earnings with bonuses factored in is expected to accelerate towards the low end, forecast to drop from 8.1% to 7.4%.

Investors will be hoping for improvement (or at least a lack of downside) in UK Employment and Claimant Count figures. The UK last saw the labor landscape contract in September, showing a 82 thousand job decline in employed persons, while unemployment benefits seekers increased by almost 20.5 thousand.

US CPI Preview: Forecasts from seven major banks, still to the high side of the Fed’s target

US CPI inflation is broadly expected to hold steady at the annualized level with slight declines in the month-on-month figures. Headline US CPI for the year into October is expected to decline from 3.7% to 3.3%.

Monthly CPI inflation is expected to print at a moderate 0.1% in October compared to September's 0.4%.

GBP/USD Technical Outlook

The Pound Sterling's soft bounce on Monday is continuing last Friday's rebound from a weekly low near 1.2190, breaking through a descending intraday trendline from last week's peak near 1.2425.

The pair is drifting back up into the 200-hour Simple Moving Average (SMA), currently grinding upwards through 1.2260.

The pair is currently setting up a near-term technical support zone near 1.2240, and as long as the low side continues to hold, the topside will be free to crash against the technical resistance barrier baked into the 1.2300 handle.

GBP/USD Hourly Chart

GBP/USD Technical Levels

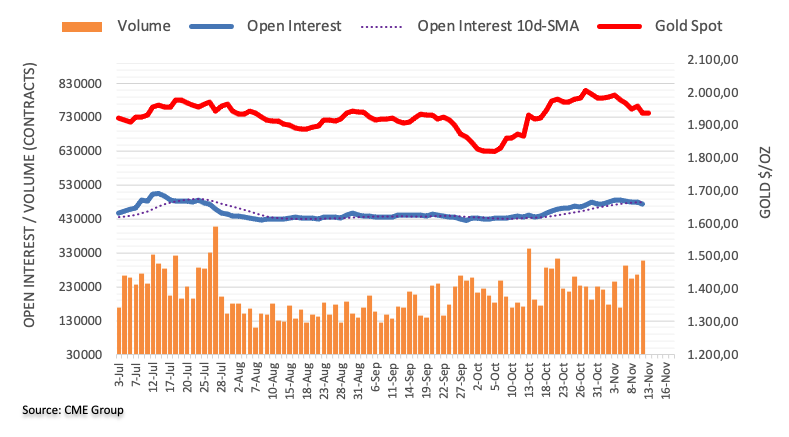

- Gold prices (XAU/USD) see a modest increase of 0.30%, trading at $1944.95, influenced by the weakening US Dollar and declining US Treasury bond yields.

- The market's focus is on the upcoming US Consumer Price Index (CPI) release, with expectations of a slight cooling in inflation rates

- Gold traders are also paying attention to upcoming speeches from Federal Reserve officials.

Gold price encounters some buyers and rises some 0.30% on Monday, late in the New York session, amidst overall US Dollar (USD) weakness, sponsored by a drop in US Treasury bond yields. Therefore, XAU/USD is trading at $1944.95 after hitting a daily low of $1928.10.

XAU/USD gains as market eyes upcoming US inflation data and geopolitical developments

A scarce economic docket in the United States (US), witnessed the majority of traders looking for the release of the Consumer Price Index (CPI) in the US. Before that, a poll from the New York Fed showed that inflation expectations for one year are cooling, while prices in October are expected to drop from 3.7% to 3.3% YoY, revealed forecasts. Core CPI is estimated to lie at 4.1%, unchanged to previously recorded data.

In the meantime, geopolitical risks remain abated according to the market reaction, even though fighting in the Gaza Strip between Israel and Hamas continues. However, an escalation of the conflict remains and could be bullish for the yellow metal.

In the meantime, Gold traders will get some cues from Federal Reserve speakers during the week. On Monday, Governor Lisa Cook failed to provide any headlines in regard to monetary policy, but Tuesday´s agenda would be led by Fed Vice-Chairman Philip Jefferson, John Williams from the New York Fed, and Lisa Cook.

On Wednesday, US President Joe Biden and his Chinese counterpart, President Xi Jinping, will meet at the Asia-Pacific Economic Cooperation (APEC) summit in San Francisco. Remarks are expected regarding military cooperation.

XAU/USD Price Analysis: Technical outlook

XAU/USD is neutral to upward biased; it dipped to a daily low of $1928.10 on Monday, though it resumed its uptrend with buyers eyeing the 20-day moving average (DMA) at $1970.81. On its way toward the latter, buyers must reclaim $1950, followed by the 20-DMA and the $2000 mark. On the other hand, Gold could shift bearish if it drops below key support levels, like the 200-DMA, 100-DMA, and 50-DMA, each at $1935.45, $1927.23, and $1923.11, respectively.

- The DXY index declines to 105.60, still consolidating last week’s gain.

- US October’s headline CPI is expected to have decelerated, and the core measure remains stagnant.

- The economic docket features no relevant high-tier reports on Monday.

The US Dollar (USD) slides on Monday with the DXY index, which measures the value of the US Dollar versus a basket of global currencies, falling to 105.60 on the back of declining US bond yields and investors taking profits from last week’s gains. Focus now shifts to Tuesday’s Consumer Price Index (CPI) data from October and Retail Sales figures from the same month on Wednesday.

Even though the United States labor market has started to show signs of weakness, several Federal Reserve (Fed) officials, including Chair Powell, hinted that the work on inflation isn’t done and opened the door for further monetary tightening. In that sense, as the central bank remains data-dependent, high-tier data will shape the decision of the Fed's last meeting in December. For now, according to the CME FedWatch Tool, the odds of a hike are low, near 10%, but swaps markets seem to be delaying interest rate cuts from May to June.

Daily Digest Market Movers: US Dollar flattens, consolidating weekly gains

- The US Dollar Index stands around 105.60 for a 0.20% loss.

- Markets await next week’s Consumer Price Index (CPI) figures from October in the US.

- Headline CPI is expected to decline to 3.3% YoY, while the core measure is forecasted to remain at 4.1% YoY.

- Retail Sales are expected to have contracted by 0.3% in October.

- US Treasury yields have edged higer on Monday, while the 2-year rate declined to 5.04%.

- According to the CME FedWatch Tool, the odds of a 25-basis-point hike in December are extremely low, below 10%.

Technical Analysis: US Dollar consolidates as bulls take a breath

The daily chart suggests that the DXY Index holds a neutral to bullish technical bias as charts show a brief consolidation period, indicating that the bulls are catching their breath after a gaining week. The Relative Strength Index (RSI) indicates a neutral stance below its midline, displaying a flat slope in negative territory, while the Moving Average Convergence (MACD) displays neutral red bars.

Evaluating the broader scale technical outlook, the pair is below the 20-day Simple Moving Average (SMA) but above the 100 and 200-day SMAs, suggesting that the bulls are in control on the broader time horizon but still need to put in extra effort to assert dominance in the short run.

Support levels: 105.50,105.30, 105.00.

Resistance levels: 106.00, 106.05 (20-day SMA), 106.30.

US Dollar FAQs

What is the US Dollar?

The US Dollar (USD) is the official currency of the United States of America, and the ‘de facto’ currency of a significant number of other countries where it is found in circulation alongside local notes. It is the most heavily traded currency in the world, accounting for over 88% of all global foreign exchange turnover, or an average of $6.6 trillion in transactions per day, according to data from 2022.

Following the second world war, the USD took over from the British Pound as the world’s reserve currency. For most of its history, the US Dollar was backed by Gold, until the Bretton Woods Agreement in 1971 when the Gold Standard went away.

How do the decisions of the Federal Reserve impact the US Dollar?

The most important single factor impacting on the value of the US Dollar is monetary policy, which is shaped by the Federal Reserve (Fed). The Fed has two mandates: to achieve price stability (control inflation) and foster full employment. Its primary tool to achieve these two goals is by adjusting interest rates.

When prices are rising too quickly and inflation is above the Fed’s 2% target, the Fed will raise rates, which helps the USD value. When inflation falls below 2% or the Unemployment Rate is too high, the Fed may lower interest rates, which weighs on the Greenback.

What is Quantitative Easing and how does it influence the US Dollar?

In extreme situations, the Federal Reserve can also print more Dollars and enact quantitative easing (QE). QE is the process by which the Fed substantially increases the flow of credit in a stuck financial system.

It is a non-standard policy measure used when credit has dried up because banks will not lend to each other (out of the fear of counterparty default). It is a last resort when simply lowering interest rates is unlikely to achieve the necessary result. It was the Fed’s weapon of choice to combat the credit crunch that occurred during the Great Financial Crisis in 2008. It involves the Fed printing more Dollars and using them to buy US government bonds predominantly from financial institutions. QE usually leads to a weaker US Dollar.

What is Quantitative Tightening and how does it influence the US Dollar?

Quantitative tightening (QT) is the reverse process whereby the Federal Reserve stops buying bonds from financial institutions and does not reinvest the principal from the bonds it holds maturing in new purchases. It is usually positive for the US Dollar.

- The EUR/USD is cycling, looking for gains ahead of Tuesday's data dump.

- Monday action remains thin, with little on the economic calendar.

- Markets hoping for a flat EU GDP reading, US CPI expected to decline slightly.

The EUR/USD is drifting in light Monday trading ahead of Tuesday's headline data drop featuring EU Gross Domestic Product (GDPO) and US Consumer Price Index (CPI) inflation figures.

The Euro (EUR) ground to an intraday low of 1.0665 before catching a mild rebound into 1.0705 as the pair bounces around familiar levels.

Markets are thin for a relaxed Monday with little of note on the economic calendar, and investors are welcoming the breather before the economic calendar turns hectic this week.

US CPI Preview: Forecasts from seven major banks, still to the high side of the Fed’s target

EU GDP for the 3rd quarter is broadly expected to hold steady at previous readings, with the headline growth measure forecast to print at -0.1%. Decelerating economic growth is expected to be highlighted with the annualized growth figure forecast at 0.1%.

On the US inflation side, headline monthly CPI is expected to decline to 0.1% for October compared to September's 0.4%, and Core CPI (headline CPI less volatile food and energy prices) is forecast to print steady at 0.3% for the same period.

EUR/USD Technical Outlook

The Euro is seeing a near-term rejection from a descending intraday trendline from last week's early peak near 1.0755, and near-term action is seeing technical support from the 1.0670 region.

Hourly candles are seeing further support from the 200-hour Simple Moving Average (SMA) currently rising into 1.0675, and further downside set to see challenges from early November's swing low into 1.0520.

EUR/USD Hourly Chart

EUR/USD Technical Levels

- The GBP/JPY is trading into the high side for Monday.

- Yen options expiries fueled a spike across Yen pairs, but moves proved short-lived.

- UK, Japan data due rounding the corner into the mid-week.

The GBP/JPY is trading back into recent highs after a spike in Yen rates fueled by Yen-based options expiries failed to generate meaningful moves.

Large blocks of Yen options expiries hit markets, sending JPY-based pairs tumbling on reaction, but technical impacts quickly evaporated and pair are now trading back into the top side.

Japanese Finance Minister Shunichi Suzuki hit markets earlier in the day with constantly-reiterated warnings that the Japanese government is "watching currency markets closely", an oft-lofted threat that has essentially become background noise for investors.

UK wages and labor figures are due Tuesday, with Japanese Gross Domestic Product numbers slated for early Wednesday.

UK Average Earnings are expected to slip from 7.8% to 7.7% for the 3rd quarter ending September, while Japan's 3rd quarter GDP is forecast to return to declines, expected to print at -0.1% compared to the 2nd quarter's 1.2% growth.

GBP/JPY Technical Outlook

Monday's options-fueled spike saw the GBP/JPY touch into the 50-hour Simple Moving Average (SMA) near 185.25, but a lack of momentum has the Guppy trading right back into near-term highs at the 186.00 handle.

Near-term chart action remains well-supported by the 200-hour SMA currently rising into 184.75, with a technical floor from a rejection level at 184.65.

Further topside will see the Guppy set to challenge three-month highs near 186.77.

GBP/JPY Hourly Chart

GBP/JPY Technical Levels

- USD/JPY experienced a significant drop, losing 67 pips rapidly, before stabilizing around 151.52, slightly up by 0.03%.

- Japanese Producer Price Index data showed a contraction, justifying the Bank of Japan’s ultra-loose policy.

- Traders are now focusing on the US CPI data release on Tuesday, which is expected to show a slight moderation in inflation rates.

The USD/JPY paired some of its earlier losses after plunging 67 pips in the last hour to a daily low of 151.20 amid the lack of news and reiterating comments of Japanese authorities that FX moves are undesirable and reflect fundamentals. At the time of writing, the USD/JPY hovers at around 151.52, gaining some 0.03%.

USD/JPY sees a sharp but brief drop, recovers as market digests US inflation expectations and Japanese economic data

The US economic docket released the New York Fed Inflation Expectations survey, with data showing American households estimating inflation for one year at 3.6% in October, below last month’s 3.7%, while for a five-year, dipped to 2.7% from 2.8%. After the data, the US Dollar Index (DXY), a gauge of the buck’s value against a basket of six peers, dropped from 105.77 to 105.69, while Wall Street pares some of its earlier losses.

Federal Reserve Governor Lisa Cook crossed the newswires but failed to provide any monetary policy hints. USD/JPY traders brace for Tuesday's November 14 release of inflation figures, with traders expecting the Consumer Price Index (CPI) at 3.3% YoY from a previous 3.7%, and core CPI at 4.1%, from 4.1%.

Meanwhile, the USD/JPY plunged from around 151.88 daily high toward 151.20 at around 15:01 GMT, with the move halting at around 15:07 GMT at 151.20 as buyers entered the markets, lifting the exchange rate towards the current spot price.

During the Asian session, Japanese data showed that the Producer Price Index contracted 0.4% MoM in October, below estimates of a 0% reading and September’s 0.2% shrinkage. Annually-based data dipped to 0.8% from 2.2% in September.

Following the data, Japan Finance Minister Suzuki said that “sudden Forex moves are undesirable,” adding that “should be determined by fundamentals.”

USD/JPY Price Analysis: Technical outlook

Following a probable intervention, the USD/JPY is forming a ‘spinning top,’ and a ‘double top’ chart pattern could be emerging, though a break of the latest cycle low, seen at 149.18, is crucial to pave the way for a pullback. For that outcome, sellers must step in and drag prices below the Tenkan-Sen at 150.55, followed by the Senkou-Span A and the Kijun-Sen, each at 150.25 and 150.00, respectively. Once cleated, up next would be the 149.00 figure and the November 3 cycle low at 149.18.

- The Canadian Dollar is adrift on a thin market at the start of the trading week.

- Canada’s Remembrance Day holiday has most provinces out of the office for Monday.

- The economic calendar is sparse this week, little Canadian data on offer.

The Canadian Dollar (CAD) is finding little momentum in thin holiday markets, with the majority of Canadian provinces and territories taking the day off in observance of Remembrance Day.

There’s little of note on the economic data docket for the CAD this week, and the Loonie will be at the whim of overall market sentiment as the trading week unwinds.

Daily Digest Market Movers: Canadian Dollar shifting around a base of thin bids for Monday

- Monday momentum is limited, capping momentum in either direction to kick off the early trading week.

- There is a notable lack of viable economic data on offer for CAD traders this week.

- Loonie to trade according to market flows with a hefty US data schedule slated for this week.

- Early Tuesday will see Bank of Canada (BoC) Deputy Governor Toni Gravelle deliver talking points while participating in a panel discussion labeled "Challenges for Financial Stability and Financial Regulation amid Heightened Uncertainty".

- BoC Dep Gov Gravelle is participating in the Third High-Level Conference on Global Risk, Uncertainty, and Volatility, in Zurich, Switzerland.

- The BoC’s Council Member is not expected to move markets much, but investors will want to keep an eye out.

Technical Analysis: Canadian Dollar sees thin action for Monday, US Dollar in the driver’s seat

The CAD is seeing thin markets on Monday as it trades against the US Dollar (USD), and shifting sand beneath the Greenback is sending the USD/CAD pair down below the 1.3800 handle for Monday. Thin markets are set to keep the Loonie-Dollar pair constrained for the early part of the week’s trading session.

The USD/CAD is struggling to maintain bullish momentum following last week’s rebound from the 50-day Simple Moving Average (SMA) near 1.3630. A continuation of downside moves will see last Friday’s rejection from 1.3850 firm up into a technical ceiling below November’s early high bids near 1.3900.

On the downside, a bearish extension will see challenges from the 200-day SMA currently pushing upward through 1.3500. A lack of recent directional momentum is seeing technical indicators begin to drift toward the middle, with the Relative Strength Index (RSI) currently heading into the 50.0 median barrier.

USD/CAD Daily Chart

Canadian Dollar price today

The table below shows the percentage change of Canadian Dollar (CAD) against listed major currencies today. Canadian Dollar was the strongest against the New Zealand Dollar.

| USD | EUR | GBP | CAD | AUD | JPY | NZD | CHF | |

| USD | -0.06% | -0.32% | -0.12% | -0.31% | 0.06% | 0.09% | -0.03% | |

| EUR | 0.06% | -0.26% | -0.06% | -0.26% | 0.12% | 0.15% | 0.03% | |

| GBP | 0.30% | 0.26% | 0.18% | 0.00% | 0.35% | 0.39% | 0.28% | |

| CAD | 0.12% | 0.06% | -0.19% | -0.19% | 0.18% | 0.20% | 0.09% | |

| AUD | 0.31% | 0.25% | 0.00% | 0.19% | 0.37% | 0.41% | 0.28% | |

| JPY | -0.07% | -0.13% | -0.35% | -0.19% | -0.33% | 0.04% | -0.09% | |

| NZD | -0.09% | -0.13% | -0.39% | -0.20% | -0.38% | -0.02% | -0.11% | |

| CHF | 0.03% | -0.03% | -0.28% | -0.09% | -0.28% | 0.09% | 0.13% |

The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the Euro from the left column and move along the horizontal line to the Japanese Yen, the percentage change displayed in the box will represent EUR (base)/JPY (quote).

Canadian Dollar FAQs

What key factors drive the Canadian Dollar?

The key factors driving the Canadian Dollar (CAD) are the level of interest rates set by the Bank of Canada (BoC), the price of Oil, Canada’s largest export, the health of its economy, inflation and the Trade Balance, which is the difference between the value of Canada’s exports versus its imports. Other factors include market sentiment – whether investors are taking on more risky assets (risk-on) or seeking safe-havens (risk-off) – with risk-on being CAD-positive. As its largest trading partner, the health of the US economy is also a key factor influencing the Canadian Dollar.

How do the decisions of the Bank of Canada impact the Canadian Dollar?

The Bank of Canada (BoC) has a significant influence on the Canadian Dollar by setting the level of interest rates that banks can lend to one another. This influences the level of interest rates for everyone. The main goal of the BoC is to maintain inflation at 1-3% by adjusting interest rates up or down. Relatively higher interest rates tend to be positive for the CAD. The Bank of Canada can also use quantitative easing and tightening to influence credit conditions, with the former CAD-negative and the latter CAD-positive.

How does the price of Oil impact the Canadian Dollar?

The price of Oil is a key factor impacting the value of the Canadian Dollar. Petroleum is Canada’s biggest export, so Oil price tends to have an immediate impact on the CAD value. Generally, if Oil price rises CAD also goes up, as aggregate demand for the currency increases. The opposite is the case if the price of Oil falls. Higher Oil prices also tend to result in a greater likelihood of a positive Trade Balance, which is also supportive of the CAD.

How does inflation data impact the value of the Canadian Dollar?

While inflation had always traditionally been thought of as a negative factor for a currency since it lowers the value of money, the opposite has actually been the case in modern times with the relaxation of cross-border capital controls. Higher inflation tends to lead central banks to put up interest rates which attracts more capital inflows from global investors seeking a lucrative place to keep their money. This increases demand for the local currency, which in Canada’s case is the Canadian Dollar.

How does economic data influence the value of the Canadian Dollar?

Macroeconomic data releases gauge the health of the economy and can have an impact on the Canadian Dollar. Indicators such as GDP, Manufacturing and Services PMIs, employment, and consumer sentiment surveys can all influence the direction of the CAD. A strong economy is good for the Canadian Dollar. Not only does it attract more foreign investment but it may encourage the Bank of Canada to put up interest rates, leading to a stronger currency. If economic data is weak, however, the CAD is likely to fall.

- The AUD/USD jumped to 0.6375, seeing 0.30% gains

- The US will report US CPI figures from October on Tuesday.

- The Australian Consumer Confidence Index from November is also due on Tuesday.

The AUD/USD gathered momentum on Monday, trading at the 0.6375 level, with 0.30% gains, and the pair's price dynamics were set by a soft US Dollar, which seems to be consolidating last week’s gains.

After the Federal Reserve’s hawkish rhetoric gained relevance last week, the Greenback recovered, and now investors are awaiting inflation figures from October to continue placing bets on the next Fed decisions. The Consumer Price Index (CPI) from the US, is expected to have declined to 3.3% YoY from the previous 3.7%, while the Core measure is expected to have stagnated at 4.1% YoY.

It is worth noticing that Fed officials were seen as not satisfied with the progress made on inflation and claimed to need further evidence to declare that the job is done. In that sense, the outcome of the inflation figures may set the pace for the Greenback’s price dynamics for the next sessions as they will model the expectations for the next December meeting of the Fed. Elsewhere, the US government bond yields are rising. The 2-year rate stands at 5.07%, and the 5 and 10-year yields are seen at 4.70% and 4.67%, respectively, which seems to limit the USD's losses.

AUD/USD levels to watch

The daily chart suggests that the AUD/USD has a neutral to bullish technical bias as the bears step back to consolidate after five consecutive days of losses. The Relative Strength Index (RSI) signals a potential reversal as it exhibits a positive slope below its midline, while the Moving Average Convergence (MACD) presents weaker green bars.

In the larger context, the pair is above the 20-day Simple Moving Average (SMA), but below the 100 and 200-day SMAs, indicating that the bears are still holding some dominance over the bulls on the broader time horizon. However, the short-term outlook will remain positive if the bulls gather further ground and hold above the 20-day SMA.

Supports: 0.6373 (20-day SMA), 0.6350, 0.6300

Resistances: 0.6400, 0.6450, 0.6470.

AUD/USD daily chart

-638354880331849362.png)

- Mexican Peso (MXN) experiences some volatility to start the week, initially rising against the US Dollar (USD) before retreating.

- Banxico's Governor Victoria Rodriguez Ceja's comments on potential rate cuts next year add pressure on the Mexican Peso.

- A risk-off impulse keeps the USD/MXN on positive territory despite overall US Dollar weakness.

Mexican Peso (MXN) loses some ground against the US Dollar (USD) early during the North American session on Monday. The USD/MXN pair reached a low of 17.60 but bounced as buyers regained control, lifting the exchange rate to 17.65, up0.04% on the day.

Mexico's economic docket is empty following last Thursday’s Bank of Mexico – also known as Banxico – decision to hold rates at 11.25% and remove hawkish comments from its statement, which weighed on the Mexican Peso. Nevertheless, the Peso trimmed some losses on Friday, but now, USD/MXN buyers are trying to break the 200-day Simple Moving Average (SMA) at 17.66. On Monday, dovish remarks by Banxico's Governor Victoria Rodriguez Ceja keep the USD/MXN trading with minuscule gains.

Daily digest movers: Mexican Peso remains range bound despite market sentiment shifting sour

- Banxico’s Governor Victoria Rodriguez commented that the easing inflationary outlook could pave the way for discussing possible rate cuts. She said that monetary policy loosening could be gradual but not necessarily imply continuous rate cuts, adding that the board would consider macroeconomic conditions, adopting a data-dependent approach.

- Industrial production in Mexico cooled down, according to data provided by the National Statistics Agency (INEGI) on November 10. The output grew by 3.9% YoY in September, below the 4.4% forecast, trailing August’s 5.2%.

- The latest inflation report in Mexico, published on November 9, showed prices grew by 4.26% YoY in October, below forecasts of 4.28% and prior rate of 4.45%. On a monthly basis, inflation came at 0.39%, slightly above the 0.38% consensus and September’s 0.44%.

- Last Thursday’s hawkish remarks by the US Federal Reserve Chairman Jerome Powell sponsored the USD/MXN a leg up, toward 17.93, before paring some losses.

- Mexico´s economy remains resilient after October’s S&P Global Manufacturing PMI improved to 52.1 from 49.8, and the Gross Domestic Product (GDP) expanded by 3.3% YoY in the third quarter.

- Banxico revised its inflation projections from 3.50% to 3.87% for 2024, which remains above the central bank’s 3.00% target (plus or minus 1%).

Technical Analysis: Mexican Peso remains steady despite Golden Cross surfacing, USD/MXN stays in the green

The USD/MXN remains neutral to upward biased, at a brisk of breaking crucial resistance levels, like the 200-day Simple Moving Average (SMA) at 17.66, followed by the 50-day SMA at 17.70. Once those two levels are breached, the next resistance would emerge at the 20-day SMA at 17.91 before buyers could lift the spot price towards the 18.00 figure.

Conversely, key support levels lie at 17.50, followed by the November 9 low at 17.47 and the 100-day Simple Moving Average (SMA) at 17.33. A loss of the latter will expose the 17.00 psychological level before the pair aims to test the year-to-date (YTD) low of 16.62.

Mexican Peso FAQs

What key factors drive the Mexican Peso?

The Mexican Peso (MXN) is the most traded currency among its Latin American peers. Its value is broadly determined by the performance of the Mexican economy, the country’s central bank’s policy, the amount of foreign investment in the country and even the levels of remittances sent by Mexicans who live abroad, particularly in the United States. Geopolitical trends can also move MXN: for example, the process of nearshoring – or the decision by some firms to relocate manufacturing capacity and supply chains closer to their home countries – is also seen as a catalyst for the Mexican currency as the country is considered a key manufacturing hub in the American continent. Another catalyst for MXN is Oil prices as Mexico is a key exporter of the commodity.

How do decisions of the Banxico impact the Mexican Peso?

The main objective of Mexico’s central bank, also known as Banxico, is to maintain inflation at low and stable levels (at or close to its target of 3%, the midpoint in a tolerance band of between 2% and 4%). To this end, the bank sets an appropriate level of interest rates. When inflation is too high, Banxico will attempt to tame it by raising interest rates, making it more expensive for households and businesses to borrow money, thus cooling demand and the overall economy. Higher interest rates are generally positive for the Mexican Peso (MXN) as they lead to higher yields, making the country a more attractive place for investors. On the contrary, lower interest rates tend to weaken MXN.

How does economic data influence the value of the Mexican Peso?

Macroeconomic data releases are key to assess the state of the economy and can have an impact on the Mexican Peso (MXN) valuation. A strong Mexican economy, based on high economic growth, low unemployment and high confidence is good for MXN. Not only does it attract more foreign investment but it may encourage the Bank of Mexico (Banxico) to increase interest rates, particularly if this strength comes together with elevated inflation. However, if economic data is weak, MXN is likely to depreciate.

How does broader risk sentiment impact the Mexican Peso?

As an emerging-market currency, the Mexican Peso (MXN) tends to strive during risk-on periods, or when investors perceive that broader market risks are low and thus are eager to engage with investments that carry a higher risk. Conversely, MXN tends to weaken at times of market turbulence or economic uncertainty as investors tend to sell higher-risk assets and flee to the more-stable safe havens.

The US Bureau of Labor Statistics (BLS) will release the most important inflation measure, the US Consumer Price Index (CPI) figures, on Tuesday, November 14 at 13:30 GMT. As we get closer to the release time, here are the forecasts by the economists and researchers of seven major banks regarding the upcoming United States inflation print for the month of October.

Headline CPI is set to come out at 0.1% month-on-month in October, a significant retreat from 0.4% in September. The year-on-year number will likely be dragged down from 3.7% to 3.3%. Core CPI is projected to remain at 4.1% YoY and rise by 0.3% MoM, a repeat of last month's increase.

ANZ

We expect core CPI inflation to rise by 0.3% MoM in October. Headline CPI was likely flat on lower energy prices.

TDS

Our forecasts for the October CPI report suggest core inflation gained additional speed for a third month straight: we are projecting an above-consensus 0.36% MoM increase, modestly up from 0.32% in September. We also look for a 0.10% gain for the headline, as inflation will benefit from the sharp retreat in energy prices. Importantly, the report is likely to show that the core goods segment likely added to inflation, while shelter-price gains probably slowed. Note that our unrounded core CPI inflation forecast could easily turn to a 0.3% rounded gain if some of our key assumptions for October don't come to fruition. Our MoM forecasts imply 3.3%/4.2% YoY for total/core prices.

Commerzbank

At first glance, the US consumer prices for October appear to be showing a significant easing of price pressure. This is because consumer prices have probably only risen by 0.1% compared to September. The YoY rate would then fall from 3.7% to 3.3%. However, the main reason for this is that gasoline has become around 5% cheaper. The more important core rate, which excludes the volatile prices for energy and food, is likely to be 0.3%, as in August and September. Overall, there is a risk that the core rate will even trend towards 0.4%. The YoY rate will remain at 4.1% at best anyway, and a decline in October seems very unlikely. The report would not call into question the downward trend in inflation. However, it would remind us that this process is slow and bumpy. In our view, inflation will not fall back to 2% but will stabilize at around 3%.

Deutsche Bank

We expect headline to come in at only +0.1% MoM due to softer energy prices. We think core edges up to +0.4% from +0.3% last month. If we are correct, the YoY rate will be 3.3% and 4.2%, respectively.

NBF

The energy component is likely to have had a negative impact on the headline index, which should translate into a 0.1% increase for headline prices. If we’re right, the YoY rate could fall from 3.7% to a four-month low of 3.3%. The advance in core prices could have been stronger at 0.3%, which should allow core inflation to remain unchanged on a 12-month basis at a two-year low of 4.1%.

CIBC

October CPI will show that core inflation remains just outside of a range consistent with target, coming in at 0.3% MoM. Weaker energy prices will likely result in a softer headline reading around 0.2% MoM. Inflation will continue to reflect a tug-of-war between firming price pressures in demand-sensitive categories such as core services ex. shelter and easing goods prices from the normalization in supply chains. The Fed will be looking for clues about the persistence of these two forces as it assesses the appropriate degree of monetary restraint. Shelter inflation will also be important to watch as it surprised in September and has been somewhat stickier than expected this year.

Wells Fargo

Since the end of September, gas prices have steadily fallen and food inflation has appeared to move sideways. These dynamics underpin our call for the headline CPI to increase only 0.1% in October. If realized, that would be the smallest monthly gain since May. Yet, the modest rise will likely be overshadowed by continued strength in the core CPI, which we expect to increase 0.3% for the third straight month.

Kit Juckes, Chief Global FX Strategist at Société Générale, analyzes USD outlook ahead of US CPI (Tuesday) and Retail Sales (Wednesday) data.

Weak Retail Sales would support the idea that the consumer’s pile of excess savings is getting run down

Tuesday’s US CPI data (we expect a steady core measure at 4.1% while the headline falls to 3.3%) and Wednesday‘s Retail Sales (which are likely to be soft) will attract attention.

Weak Retail Sales would support the idea that the consumer’s pile of excess savings is getting run down and that as demand slows, the labour market will loosen up and the whole economy will slow down too. But Fed Chair Jerome Powell will warn about over-reacting and the market will be wary of over-reacting. I won’t though! A genuinely soft Retail Sales figure would reinforce my view that US yields, and the Dollar have now peaked. Unfortunately, all this caution ensures the Dollar’s fall is very, very slow.

Economists at HSBC still expect a slightly weaker AUD against the USD in the months ahead.

Three factor medium-term bearish view for the AUD

We still maintain our three factor medium-term bearish view for the AUD.

First, slowing US growth would hardly be good news for the AUD, as it would likely combine with weakness in growth elsewhere to heighten global growth concerns and weigh on risk sentiment.

Second, AUD/USD has not benefited much from favourable moves in relative rates recently, but has suffered from unfavourable moves. This asymmetry should last, if markets focus on more dominant negative themes.

Third, our base case remains that China's growth outlook will not be a supportive factor for the currency anytime soon.

USD/CAD is still trading close to its highs for the year. Economists at Commerzbank analyze Loonie’s outlook.

Upward potential in 2024

The Bank of Canada (BoC) suspended its rate hike cycle for the second time in early September and has kept its key interest rate stable at 5% since then. At the same time, the Fed is discussing another rate hike. This difference in monetary policy is currently supporting USD/CAD. In the coming weeks, however, it is likely to become clear that there will be no further rate hikes in the US either.

As we expect a recession in the US next year, while the Canadian economy is likely to achieve a soft landing, we see CAD recovery potential next year.

Kit Juckes, Chief Global FX Strategist at Société Générale, analyzes EUR/USD outlook and how US 10-year yields could impact the pair.

4.5% in US 10s and 1.08 levels in EUR/USD unlikely to be broken today

For Dollar bears, a break of 4.5% in US 10s may be the key signal to look for a break above 1.08 in EUR/USD.

I will be surprised if we can get anywhere close to breaking either level today, but I expect both to break in their own good time.

Economists at UBS expect the US Dollar to remain strong before softening as 2024 progresses.

RBA to keep rates elevated until at least 4Q24

The US Dollar looks likely to stay well supported in the coming months thanks to relatively resilient US economic data. But as 2024 progresses, the USD may weaken slightly in response to slowing US growth and more flexible Fed policy.

We maintain a neutral view on the US Dollar and believe investors should look to sell the Dollar on rallies.

We have a most preferred view on the Australian Dollar, as we see risks of another hike by the Reserve Bank of Australia and expect it to keep rates elevated until at least 4Q24 as it continues to fight inflation.

- The New Zealand Dollar trades little changed on Monday as markets tread water.

- Kiwi remains on the back foot after recent Fedspeak resurrected the chances of a rate hike.

- Hawkish commentary from Fed officials has set the US Dollar trending higher against the Kiwi, NZD/USD declines.

The New Zealand Dollar (NZD) trades flat amid a muted market mood on Monday. Most traders are waiting for bigger macroeconomic data releases scheduled for Tuesday and Wednesday before taking big positions.

The short-term technical situation is precarious, however, threatening deeper losses on the horizon as price edges ever closer to breaking below a key support level at 0.5874.

Daily digest market movers: New Zealand Dollar flat on Monday

- The New Zealand Dollar trades little changed at the start of the week as traders look ahead to more significant data releases later in the week.

- NZD could very well be impacted by Chinese Industrial Production and Retail Sales data on Wednesday morning at 02:00 GMT.

- On Monday, China released figures for New Loans in October, which showed a seasonal slowdown in lending to 738.4B from 2310.0B in September, but still more than the 650.0B expected. It suggests credit remained buoyant during the month.

- China's M2 Money Supply (YoY), showing the amount of money held in most kinds of bank accounts, ticked down to 10.3% in October, compared to 10.4% previously.

- Downbeat Chinese inflation data had dampened the outlook for global growth, weighing on NZD last week, because New Zealand is a major commodity exporter – especially of dairy products – to China.

- NZD fell midweek last week on the back of an inflation report from the RBNZ that showed both one-year-out and two-years-out inflation expectations for New Zealand falling in Q3 compared to the previous quarter.

- The lower inflation expectations imply the RBNZ is less likely to raise interest rates, making the country a less attractive place for global investors to park their capital.

- Inflation expectations have pushed higher in the US after University of Michigan inflation expectations data, released November 10, showed an uptick to 4.4% in November for inflation expected in the year ahead, compared to 4.2% in October and 3.2% in September.

- This reflects the more hawkish commentary that has been coming out of the Federal Reserve (Fed) recently, which suggests a greater probability the Fed may still raise interest rates before it is done with its tightening cycle.

- US Inflation data on Tuesday at 13:30 GMT should shine more light on price rises. A rise of 0.1% MoM and 3.3% YoY is expected for headline inflation in October, whilst core is forecast to increase by 0.3% and 4.1%.

New Zealand Dollar technical analysis: NZD/USD inches lower, threatening more losses

NZD/USD – the number of US Dollars one New Zealand Dollar can buy – edges lower into the 0.5870s on Monday, reaching a key make-or-break level for trend watchers.

-638354821115478975.png)

New Zealand Dollar vs US Dollar: Daily Chart

The pair is a few pips away from breaking below the last major lower high of the previous uptrend, made on November 2, at 0.5874 (visible on the 4-hour chart below), close to the blue 100-4-hour Simple Moving Average (SMA). A break below would probably indicate a short-term bearish trend reversal and deeper losses.

The next target to the downside would probably be at 0.5862, where the 61.8% Fibonacci retracement of the recovery from the year-to-date lows in late October and early November. The main target, however, sits at 0.5790, then 0.5773.

-638354821592748142.png)

New Zealand Dollar vs US Dollar: 4-hour Chart

As long as the November 2 lows stay intact, however, a threat of a recovery and decisive break above the November 3 high at 0.6001 remains, which would reconfirm the short-term bullish bias. The likely target thereafter would be the 0.6055 October high.

The medium and long-term trends are both still bearish, suggesting the potential for more downside is strong.

Bulls would have to push above the 0.6055 October high to change the outlook in the medium term and indicate the possibility of the birth of a new uptrend.

New Zealand Dollar FAQs

What key factors drive the New Zealand Dollar?

The New Zealand Dollar (NZD), also known as the Kiwi, is a well-known traded currency among investors. Its value is broadly determined by the health of the New Zealand economy and the country’s central bank policy. Still, there are some unique particularities that also can make NZD move. The performance of the Chinese economy tends to move the Kiwi because China is New Zealand’s biggest trading partner. Bad news for the Chinese economy likely means less New Zealand exports to the country, hitting the economy and thus its currency. Another factor moving NZD is dairy prices as the dairy industry is New Zealand’s main export. High dairy prices boost export income, contributing positively to the economy and thus to the NZD.

How do decisions of the RBNZ impact the New Zealand Dollar?

The Reserve Bank of New Zealand (RBNZ) aims to achieve and maintain an inflation rate between 1% and 3% over the medium term, with a focus to keep it near the 2% mid-point. To this end, the bank sets an appropriate level of interest rates. When inflation is too high, the RBNZ will increase interest rates to cool the economy, but the move will also make bond yields higher, increasing investors’ appeal to invest in the country and thus boosting NZD. On the contrary, lower interest rates tend to weaken NZD. The so-called rate differential, or how rates in New Zealand are or are expected to be compared to the ones set by the US Federal Reserve, can also play a key role in moving the NZD/USD pair.

How does economic data influence the value of the New Zealand Dollar?

Macroeconomic data releases in New Zealand are key to assess the state of the economy and can impact the New Zealand Dollar’s (NZD) valuation. A strong economy, based on high economic growth, low unemployment and high confidence is good for NZD. High economic growth attracts foreign investment and may encourage the Reserve Bank of New Zealand to increase interest rates, if this economic strength comes together with elevated inflation. Conversely, if economic data is weak, NZD is likely to depreciate.

How does broader risk sentiment impact the New Zealand Dollar?

The New Zealand Dollar (NZD) tends to strengthen during risk-on periods, or when investors perceive that broader market risks are low and are optimistic about growth. This tends to lead to a more favorable outlook for commodities and so-called ‘commodity currencies’ such as the Kiwi. Conversely, NZD tends to weaken at times of market turbulence or economic uncertainty as investors tend to sell higher-risk assets and flee to the more-stable safe havens.

Gold prices briefly hit $2,000 after Hamas’ attack on Israel before retreating recently. Economists at ANZ Bank analyze the yellow metal’s outlook.

Central bank Gold purchases to remain strong

Renewed geopolitical tensions will protect the downside in Gold prices. This is in addition to the conclusion of the US monetary tightening cycle and an imminent peak in the US Dollar.

We expect central bank Gold purchases to remain strong. Based on current pace of purchase, we upgrade our demand estimates to 1,050t from 750t for 2023 and 800t for 2024.

- USD/CAD recovers from 1.3800 ahead of the US CPI data.

- Economists projected that the US core CPI grew at a steady pace in October.

- Fed Powell characterized current interest rates as inadequate to tame price pressures.

The USD/CAD pair rebounds after getting support near 1.3800 ahead of the United States inflation data for October. The Loonie asset recovered amid anxiety as the inflation data would provide further cues about the likely monetary policy action by the Federal Reserve (Fed) in December.

S&P500 futures generated some losses in the London session, portraying a risk-off mood. The US Dollar Index (DXY) is consistently making efforts to break above the immediate resistance of 106.00. 10-year US Treasury yields advance to near 4.66% ahead of US Consumer Price Index (CPI) data.

As per the consensus, the core CPI that excludes volatile food and oil prices grew at a steady pace of 0.3% on a monthly basis. The annual core CPI is also seen to grow by 4.1%. A stubborn US inflation data would elevate risks of further policy-tightening by the Federal Reserve (Fed).

Last week, Fed Chair Jerome Powell characterized current interest rates as inadequate to tame price pressures. Powell said that the Fed will not hesitate to raise interest rates further if inflation remains stubborn.

Meanwhile, the oil price attempts recovery after discovering buying interest near $75.00 as OPEC sees steady demand by China in 2024. It is worth noting that Canada is the leading exporter of oil to the United States and higher oil prices support the Canadian Dollar.

Wide yield differentials have driven USD/JPY to revisit its 2022 high near 152. Economists at TD Securities analyze the pair’s outlook.

FX intervention warnings may prove too little to mark a turnaround in the JPY

FX intervention warnings have intensified but may prove too little to mark a turnaround in the JPY.

Without the BoJ exiting NIRP, it's hard to make a bullish case for the JPY given fundamentals. Likely, MoF officials are buying time for the BoJ and may choose to ease off the pressure on USD/JPY through FX interventions as a weak JPY has become a political issue for the government amid rising cost-of-living pressures.

Position for a trading range 145-150 from now until Q1'24.

Economists at Rabobank analyze GBP outlook against USD and EUR.

Potential for further downside risks to Cable

In view of downside risks to global growth, we expect the USD to remain well supported in the coming months as subdued levels of risk appetite underpin safe-haven assets. This suggests potential for further downside risks to Cable.

However, we see scope for EUR/GBP to move back below the 0.87 level on the back of weak German economic data and our house view that the Eurozone may already be in a technical recession.

- EUR/USD trades in an inconclusive fashion below 1.0700.

- Bouts of selling pressure could revisit 1.0640.

EUR/USD trades in an inconclusive fashion below the 1.0700 mark at the beginning of the week.

If bears regain the initiative, they could initially drag the pair to the interim 55-day SMA, today at 1.0639. The loss of this region could open the door to a probable visit to the weekly low of 1.0495 (October 13) ahead of the 2023 bottom of 1.0448 (October 3).

In the meantime, while below the 200-day SMA at 1.0800, the pair’s outlook should remain negative.

EUR/USD daily chart

Economists at TD Securities do not think the USD is breaking out, and continue to forecast a notable pullback throughout 2024.

US economy slowing through 2024

The regime shift for a weaker USD is evident, and we expect it to continue into next year especially as we see the US economy entering a modest recession with the Fed cutting steeply whereas the rest of the world is still muddling along.

We see the USD correcting lower from over-valued and stretched levels where it aligns more with macro drivers.

A reversion in US curve dynamics from bear to bull steepening will also be very bearish for the USD. Another theme to keep an eye out for in 2024 is the deteriorating fiscal position of the US where growing concern can lead to higher rates but a weaker USD (especially versus JPY).

- The Greenback retreats a touch and starts the week on the backfoot.

- Traders will keep their powder dry for Wednesday and Thursday.

- The US Dollar Index is expected not to make any big moves with a light Monday calendar.

The US Dollar (USD) is easing a touch, with the Australian Dollar (AUD/USD) and the Polish Zloty (USD/PLN) as biggest winners against the Greenback. Markets experience a very calm start to the week with traders keeping their powder dry as this Monday holds no important data events whatsoever when it comes to the US macroeconomic agenda. Traders rather will try to assess and preposition towards Thursday and Friday.

On the economic data front traders will be using today’s empty docket to assess the uptick in Friday’s University of Michigan expectations regarding the inflation outlook, and assess if the US Consumer Price Index on Wednesday and the Producer Price Index on Thursday will already reflect that assumption of an uptick in inflationary pressures.

Seeing from the very choppy and nervous price action on Friday on the back of the Michigan numbers, traders are best to brace for a very nervous and volatile week in the Greenback and in the US Dollar Index.

Daily digest: US Dollar easing ahead of fireworks

- China is weighing unfreezing Boeing 737 orders.

- European Central Bank Vice-President Luis de Guindos issues says he expects a temporary inflation rebound in the coming months. This falls in line with what US Federal Reserve Chairman Jerome Powell said last week.

- Reserve Bank of Australia Assistant Governor (Economic) Marion Kohler said that more hikes could be needed in Australia as the RBA rates are not restrictive enough.

- The Pentagon has confirmed that over the weekend it has hit Iran-linked targets in Syria.

- Equities are still awakening this Monday with the Japanese Topix and Nikkei closing flat. In China the Hang Seng is soaring over 1%, while European and US equities are trading flat for this Monday.

- The CME Group’s FedWatch Tool shows that markets are pricing in a 91.2% chance that the Federal Reserve will keep interest rates unchanged at its meeting in December.

- The benchmark 10-year US Treasury yield trades at 4.65%, and is slowly making its way up again.

US Dollar Index technical analysis: US Dollar wait-and-see

The US Dollar entered a nervous patch on Friday on the back of the University of Michigan inflation expectations survey showed an uptick in inflation expectations. The data confirmed what Fed Chairman Powell was warning about in his most recent statement last week. If the Fed is right and a rise in inflation is noticed this week in both the Consumer Price Index and Producer Price Index numbers, markets might need to factor in another rate hike, which means some more US Dollar strength to come into the DXY.

The DXY was looking for support near 105.00, and was able to bounce ahead of it earlier last week. Any shock events in global markets could spark a sudden turnaround and favour safe-haven flows into the US Dollar. A rebound first to 105.85 would make sense, a pivotal level from March 2023. A break above could mean a revisit to near 107.00 and recent peaks printed there.

On the downside, 105.10 is still acting as a line in the sand. Once the DXY slides back below that, a big air pocket is opening up with only 104.00 as the first big level, where the 100-day Simple Moving Average (SMA) can bring some support. Just beneath that, near 103.50, the 200-day SMA should provide similar underpinning.

US Dollar FAQs

What is the US Dollar?

The US Dollar (USD) is the official currency of the United States of America, and the ‘de facto’ currency of a significant number of other countries where it is found in circulation alongside local notes. It is the most heavily traded currency in the world, accounting for over 88% of all global foreign exchange turnover, or an average of $6.6 trillion in transactions per day, according to data from 2022.

Following the second world war, the USD took over from the British Pound as the world’s reserve currency. For most of its history, the US Dollar was backed by Gold, until the Bretton Woods Agreement in 1971 when the Gold Standard went away.

How do the decisions of the Federal Reserve impact the US Dollar?

The most important single factor impacting on the value of the US Dollar is monetary policy, which is shaped by the Federal Reserve (Fed). The Fed has two mandates: to achieve price stability (control inflation) and foster full employment. Its primary tool to achieve these two goals is by adjusting interest rates.

When prices are rising too quickly and inflation is above the Fed’s 2% target, the Fed will raise rates, which helps the USD value. When inflation falls below 2% or the Unemployment Rate is too high, the Fed may lower interest rates, which weighs on the Greenback.

What is Quantitative Easing and how does it influence the US Dollar?

In extreme situations, the Federal Reserve can also print more Dollars and enact quantitative easing (QE). QE is the process by which the Fed substantially increases the flow of credit in a stuck financial system.

It is a non-standard policy measure used when credit has dried up because banks will not lend to each other (out of the fear of counterparty default). It is a last resort when simply lowering interest rates is unlikely to achieve the necessary result. It was the Fed’s weapon of choice to combat the credit crunch that occurred during the Great Financial Crisis in 2008. It involves the Fed printing more Dollars and using them to buy US government bonds predominantly from financial institutions. QE usually leads to a weaker US Dollar.

What is Quantitative Tightening and how does it influence the US Dollar?