- Аналітика

- Новини та інструменти

- Новини ринків

Новини ринків

“Bullock is the right person to lead the RBA into the future and ensure we have the world’s best and most effective central bank,” said the Australian government officials during an emergency press conference held early Friday.

That said, Australian Prime Minister Anthony Albanese and Treasurer Jim Chalmers called an emergency press conference after media reports circulated that Philip Lowe won’t have a chance for reappointment after his term expires in September 2023.

The government update also mentioned that Bullock will be the first woman to lead the RBA while also citing the empty space for RBA Deputy Governor’s place, which will be filled in the next few months. The news also mentioned that the appointment will take place from September 18, 2023.

USD/MXN licks its wounds at the lowest levels since December 2015, making rounds to 16.85 during early Asian session on Friday.

That said, the Mexican Peso (MXN) pair dropped in the last five consecutive days amid broad based US Dollar weakness, mainly driven by the concerns that the downbeat US inflation lcues will prod the US Federal Reserve (Fed) from lifting interest rates past July. Adding strength to the USD/MXN bearish bias are the downbeat options market signals.

That said, the one-month Risk Reversal (RR) of the USD/MXN pair, a measure of the spread between call and put prices, dropped the most in six days to -0.240 by the end of Thursday’s North American trading session.

In doing so, the options market figures defy the hopes of witnessing a corrective bounce in the USD/MXN price. It should be noted that the options market gauge prints the biggest weekly RR slump since early June with -0.327 mark at the latest.

Elsewhere, the US Dollar Index (DXY) remains on the back foot at lowest levels since since April 2022 ahead of the preliminary readings of July’s Michigan Consumer Sentiment Index, as well as the five-year Consumer Inflation Expectations.

Also read: Forex Today: Dollar's downward spiral continues

Fed’s Waler: Jobs, economic strength give Fed space to hike further

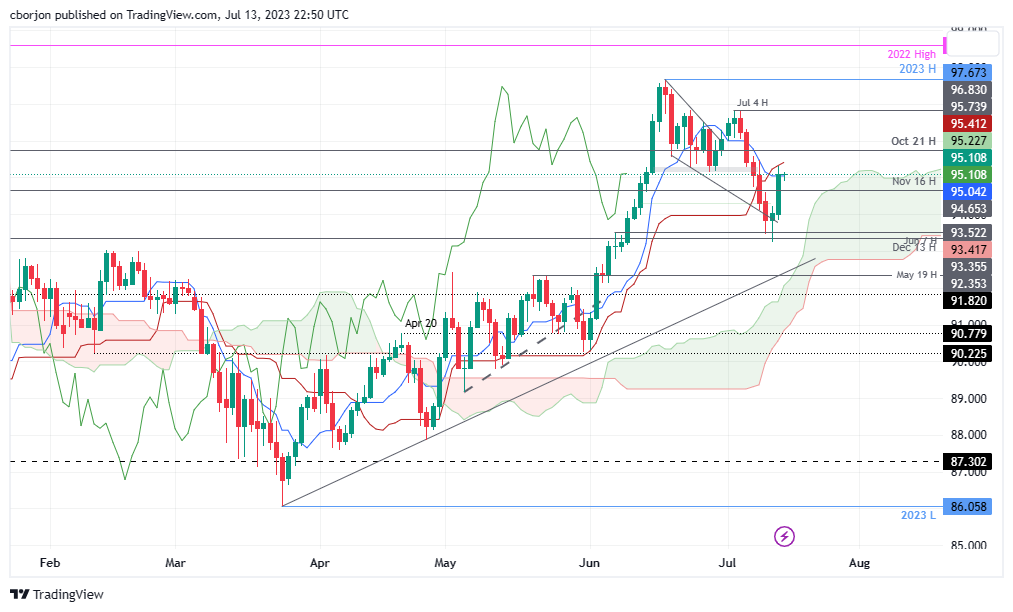

- AUD/JPY gains 1% and breaches the Tenkan-Sen line, exposing the Kijun-Sen.

- A morning star candlestick pattern signals potential AUD/JPY upside.

- The AUD/JPY could turn bearish if demand prices dive below 95.00.

AUD/JPY reversed its downtrend, and rallied sharply on Thursday, gaining more than 1%, or 106 pips, courtesy of a risk-on impulse due to cooling US inflation and a break of a technical resistance level that has turned support. As the Asian session begins, the AUD/JPY is trading at 95.08, almost flat.

AUD/JPY Price Analysis: Technical outlook

The daily chart portrays the AUD/JPY as upward biased but hovering above/below the Tenkan-Sen line at 95.04. Price action witnessed the pair bouncing slightly below the June 7 high of 93.52, a guarded area for Aussie (AUD) bulls, forming a hammer candlestick on Wednesday. That, alongside Thursday’s long bullish and Tuesday’s bearish candles, formed a three-candlestick pattern, ‘morning star,’ indicating that further upside is expected.

AUD/JPY’s next resistance emerges at the Kijun-Sen line at 95.08, followed by the October 21 daily high at 95.74. The 96.00 figure would be up next, followed by the July 4 high at 96.84, before the pair attacks the 97.00 mark.

For a bearish resumption, AUD/JPY sellers need prices to dive below 95.00 as they eye the current week’s low of 93.25.

AUD/JPY Price Action – Daily chart

- GBP/USD seesaws at the highest level since April 2022, pauses six-day uptrend.

- Overbought RSI conditions, late 2021 low challenge Cable buyers.

- Pound Sterling’s upside remains favored unless staying beyond two-month-old previous resistance line.

- Bulls can aim for 1.3300 on breaking immediate upside hurdle.

GBP/USD makes rounds to 1.3130-40 after refreshing a 15-month high as it awaits fresh clues during the early hours of Friday’s Asian session. In doing so, the Cable pair takes clues from the overbought RSI conditions while portraying the trader’s cautious mood at the key upside hurdle.

Also read: GBP/USD rally breaks 1.3100 barrier amid soft US PPI data

That said, December 2021 bottom surrounding 1.3160 restricts the immediate upside of the Pound Sterling pair at the multi-month high, amid the overbought RSI (14) line, suggesting a pullback toward the 78.6% Fibonacci retracement of the January-September 2022 downturn, near 1.3030.

However, the Pound Sterling buyers remain hopeful unless the quote stays beyond the previous resistance line stretched from early May 2023, around 1.2970 by the press time.

Following that, the previous monthly high of around 1.2850 and May’s peak of 1.2680 could lure the GBP/USD sellers.

Meanwhile, the Cable buyer’s ability to cross the 1.3160 hurdle could quickly propel the price toward the March 2022 high surrounding 1.3300.

Though, January 2022 low near 1.3360-55 and multiple tops marked in early 2022 around 1.3650 may prod the GBP/USD bulls before directing them to the previous yearly top of near 1.3750.

GBP/USD: Daily chart

Trend: Limited upside expected

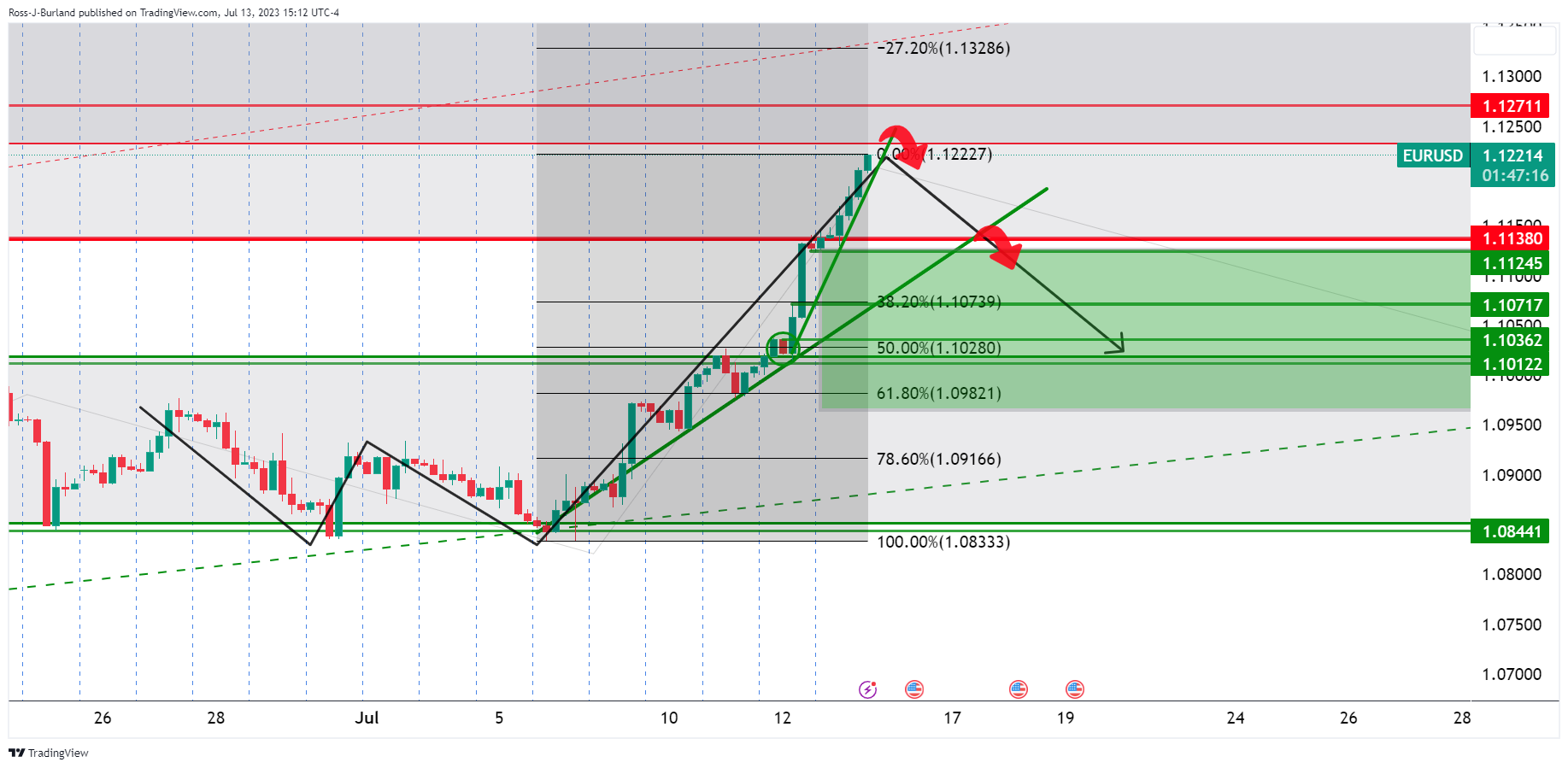

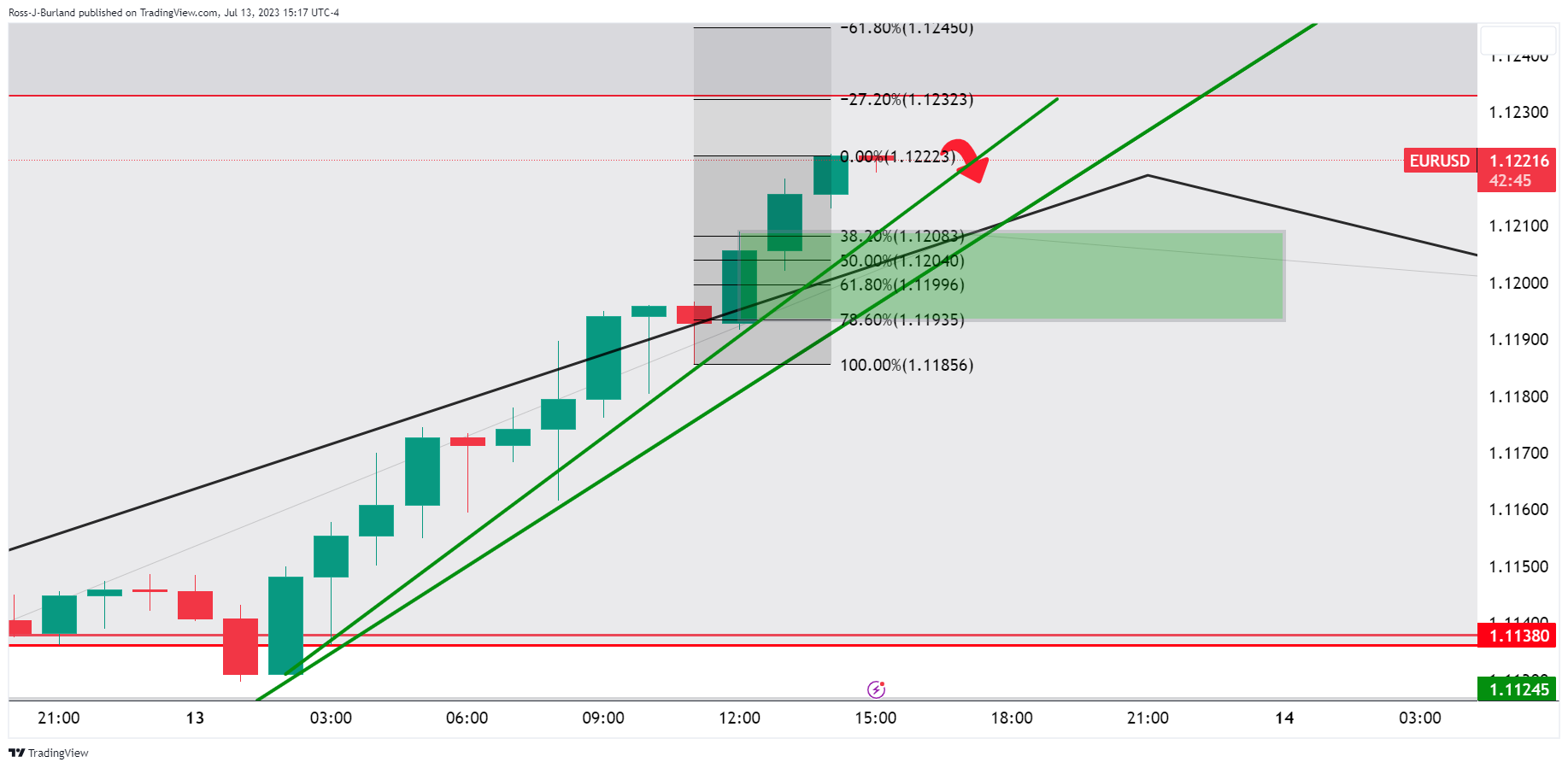

- EUR/USD seesaws at the highest level since March 2022, stabilizing after six-day uptrend.

- US Dollar slumps as US inflation clues suggest limited room for the Fed to lift interest rates past July.

- Mixed EU data at home, unimpressive ECB talks fail to probe Euro buyers.

- EC economic forecasts, US Michigan Consumer Sentiment Index, inflation expectations in focus for clear directions.

EUR/USD bulls take a breather at the highest levels in 16 months, bracing for the biggest weekly gain since November 2022, as it makes rounds to 1.1225-30 amid early Friday morning in Asia. In doing so, the Euro pair cheers the broad-based US Dollar weakness amid concerns that the Federal Reserve has limited scope to increase the interest rates past July. Additionally, downbeat US Treasury bond yields and hawkish clues from the European Central Bank (ECB) officials also propel the major currency pair.

US Dollar Index (DXY) dropped to the lowest level since April 2022 the previous day, down 2.45% on a week so far, as downbeat inflation clues from the US push back the Federal Reserve (Fed) hawks.

On Thursday, US Producer Price Index (PPI) came in as 0.1% YoY for June, versus 0.4% expected and 0.9% prior while the PPI ex Food & Energy, also known as the Core PPI, eased to 2.4% YoY from 2.8% previous reading and 2.6% market forecasts.

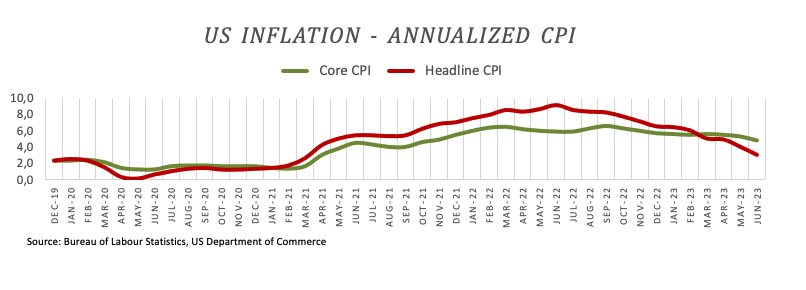

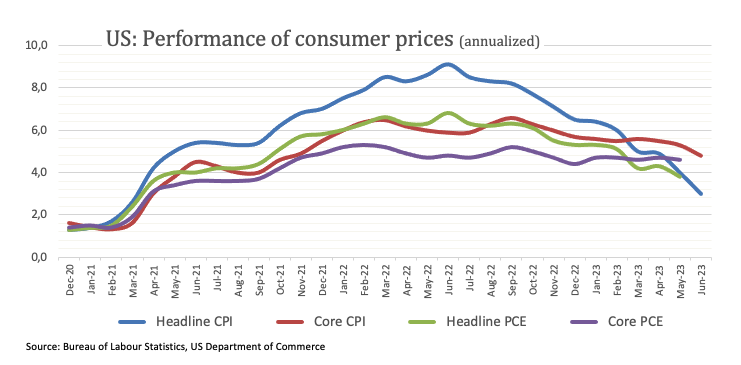

Earlier in the week, the US Consumer Price Index (CPI) registered a 3.0% YoY figure for June versus 3.1% market forecasts and 4.0% reported for May. Further details suggest that the CPI ex Food & Energy, also known as the Core CPI, softened to 4.8% yearly for the said month compared to analysts’ estimations of 5.0% and 5.3% previous readings.

That said, the US Weekly Initial Jobless Claims declined to 237K for the week ended on July 07, from 250K expected and 249K prior (revised).

Following the disappointing inflation data, the market’s expectations of the Fed rate hike past July have sharply deteriorated.

On the other hand, Eurozone Industrial Production eased to 0.2% MoM for May on a seasonally adjusted basis versus 0.3% market forecasts and 1.0% previous readings.

It should be noted, however, that the European Central Bank’s (ECB) June policy meeting revealed on Thursday that minimum of two successive rate hikes needed for inflation projections to materialize.

Alternatively, ECB Governing Council member Ignazio Visco said during an interview with Italy's Sky TG24 news channel, “We are not very far' from peak in interest rates.”

Against this backdrop, Wall Street cheers risk-on mood while the US 10-year and two-year Treasury bond yields plummet.

While the dovish Fed concerns propel the EUR/USD pair, today’s European Commission (EC) Economic Forecasts and trade numbers may direct the traders ahead of the preliminary readings of July’s Michigan Consumer Sentiment Index, as well as the five-day Consumer Inflation Expectations. Should the final clues of the US inflation appear downbeat, the Euro may easily aim for the previous yearly high of around 1.1500.

Technical analysis

A daily closing beyond an ascending resistance line stretched from May 2022, around 1.1190 by the press time, keeps EUR/USD bulls hopeful of visiting the 1.1300 round figure.

- Western Texas Intermediate (WTI), the US crude oil benchmark, rallied more than 1.70% on Thursday, hitting a new three-month high amid easing US inflation data.

- Recent Consumer and Producer Price Indices (CPI and PPI) figures in the United States showed modest climbs, sparking speculation that the US interest rate could be peaking soon.

- Higher US interest rates, which often boost the US Dollar and slow economic growth, typically dampen demand for crude oil.

Western Texas Intermediate (WTI), the US crude oil benchmark, rallied sharply on Thursday, more than 1.70%, and hit a new three-month high, following two inflation reports that could warrant the Fed of overtightening monetary conditions. At the time of writing, WTI exchanges hands at $77.10, slightly down as the Asian session begins.

Rising oil demand forecasts and the soft US Dollar boosted WTI prices

Inflation data in the United States (US) continued its downward trajectory, with Consumer and Producer Price Indices (CPI and PPI) figures climbing modestly, spurring speculations that the US central bank might refrain from lifting rates past the July FOMC’s meeting.

Higher interest rates in the US usually boost the US Dollar (USD) and tend to slow economic growth, denting demand for crude oil. In the meantime, the US Dollar Index (DXY) dropped to its lowest level since April 2022, helping to boost WTI prices, as the DXY sits at 99.778, down 0.80%.

In the meantime, the International Energy Agency (IEA) revealed that oil demand would increase and reach a record high, despite global tightened monetary conditions and economic headwinds.

Despite the current economic weakness, the Organization of Petroleum Exporting Countries (OPEC) updated its oil demand, which remained upbeat. The cartel raised the growth forecast for the rest of 2023 and a slight economic slowdown in the next year.

WTI Price Analysis: Technical outlook

Given the fundamental backdrop, WTI’s price action left oil’s price close to testing the 200-day Exponential Moving Average (EMA) at $77.34, which, once cleared, could open WTI’s path to challenge $80.00 per barrel. Also, a downslope trendline drawn from November highs passes nearby the 200-day EMA, making its break an essential achievement for oil bulls. Once cleared, the next resistance would be the psychological $80.00, followed by the January 23 swing high at $82.60. Failure to conquer the 200-day EMA will leave WTI’s exposed to selling pressure. Key support levels lie at $77.00, the $76.00 figure and the June 5 daily high turned support at $74.92.

- NZD/USD bulls are in the market but a fading opportunity could be on the cards.

- Friday is the end of the three-day cycle that could prove fruitful for the bears.

The New Zealand dollar strengthened for the second straight session as the US dollar continues to slide. An eight-week high was made on fresh selling of the Greenback as further data pointed to disinflation in the US economy signaling the Federal Reserve will need to adopt a less hawkish stance this year. meanwhile, although New Zealand's inflation rate slowed to 6.7% in the first quarter, it is still above the Reserve Bank of New Zealand's target range of 1-3% over the medium term.

On the technical front, we have a topping pattern in play as follows:

NZD/USD H1 chart

It's the end of the week and a three-day cycle that could see the price deteriorate into longs that have been built up since Wednesday's rally. The M-formation is a topping pattern that could offer an opportunity before the week is out as traders take profits into the weekend.

NZD/USD M15 charts

We are seeing signs of deceleration, but there will need to be a break of the 0.6370s to confirm that bearish bias. even still, there are prospects of a move higher to test 0.6400/20:

NZD/USD daily chart

The daily chart is offering prospects of a continuation...traders can look for a fade if the market offers the set up to end the week.

- AUD/USD closed Thursday near 0.6890, recording a 1.47% gain.

- The Aussie held gains despite weak Import and Exports Chinese data reported during the Asian session.

- USD faced severe selling pressure following soft PPI figures.

On Thursday, the AUD/USD tallied a fifth consecutive day of gains and closed near the 0.6890 zone. The broad USD weakness amid dovish bets on the Federal Reserve (Fed) following soft inflation figures allowed the Aussie to gain ground despite weak Trade Balance figures reported from China early in the Asian session.

The Producer Price Index (PPI) from the US from June came in at 0.1% lower than expected at 0.2%, and the Core Figure was 2.4% lower than expected at 2.6%. As a reaction, US Treasury bond yields saw sharp declines across the board, with the 2, 5 and 10-year yields retreating to 4.63%, 3.94% and 3.76%, respectively.

Even though a 25 basis point rate hike is expected at the next FOMC (Federal Open Market Committee) meeting on July 25-26, what is driving the Dollar lower is the belief that it will be the last hike. It's worth noting that several officials deemed “additional” increases necessary but the recent inflation from the US figures released on Wednesday and Thursday made markets refrain from betting on an additional hike past July.

AUD/USD Levels to watch

The daily chart suggests that the pair’s outlook for the short term is bullish. Indicators hold strong in positive territory, with the Relative Strength Index (RSI) nearing overbought conditions and the Moving Average Convergence Divergence (MACD) printing rising green bars, indicating that the bulls have the upper hand.

Resistance Levels: 0.6900 (June's high), 0.6950,0.6980.

Support Levels: 0.6785, 0.6750, 0.6715 (20-day Simple Moving Average).

-638248804518007813.png)

During the Asian session, Japan will release Industrial Production data. Later in Europe, Germany will release wholesale June inflation, the European Commission's economic growth forecast, and trade balance data. Later in the day, US Consumer Confidence and Canadian Manufacturing Sales are due. The US Dollar's decline remains in the spotlight.

Here is what you need to know on Friday, July 14:

The US Dollar dropped sharply again after the release of more inflation data from the US. The figures offer signals that inflation continues to cool, triggering more gains in Wall Street and Treasury bonds.

The US Producer Price Index (PPI), which peaked at 11.2% in June 2022, rose 0.1% in June from a year ago, the lowest reading since August 2020. Labor market data showed Initial Jobless Claims totaled 237K in the week ended July 8, below the 249K of the previous week. Despite inflation cooling, the Federal Reserve (Fed) is on its way to raise interest rates by 25 basis points on July 26. However, market participants are increasing bets that it will be the last hike of the tightening cycle. Those expectations are driving the US Dollar lower. On Friday, the University of Michigan will release its Consumer Confidence report.

The US Dollar Index (DXY) dropped below 100.00, reaching its lowest level since April 2022. The DXY has fallen for six consecutive days and is not showing signs of stabilization. The bearish Dollar's momentum remains strong and could lead to further losses.

Wall Street cheered inflation figures again. The Dow Jones rose 0.14%, the S&P 500 gained 0.85% (highest close since April 2022), and the Nasdaq rose by 1.58%. Commodities also rose further, with Silver extending weekly gains with a 3% gain to $24.85, while Gold remained steady hovering around $1,960.

The upbeat tone across equity markets remained despite weak June trade data reported by China early on Thursday. Exports fell 12.4% YoY (the largest contraction since February 2020) and imports rose 6.8%, both worse than expected. The numbers increase the pressure on Chinese officials to introduce more stimulus.

EUR/USD soared to 1.1225, remains at the highs, as the bullish momentum remains intact. The European Central Bank (ECB) minutes pointed to another rate hike in July. On Friday, the European Commission will release economic growth forecasts and trade balance data.

GBP/USD posted another daily gain, as it has been the case since the beginning of the month. The pair broke above 1.3000 and also 1.3100, to the highest level in 15 months. UK GDP data showed a contraction in May of 0.1%, better than the expected -0.3%. Industrial Production indicators also showed a decline in May, but less than forecasted. The Pound remains strong even as tightening expectations from the Bank of England soften.

USD/JPY fell for the sixth consecutive day, reflecting the weakness of the Dollar and lower government bond yields, falling towards 138.00. The Japanese currency gained ground versus other currencies amid risk appetite.

Antipodean countries continue to benefit from the weaker Dollar and higher equity prices. AUD/USD jumped towards 0.6900, testing June highs and posting the highest daily close since February. NZD/USD climbed to the highest level since early February, just below 0.6400.

USD/CAD closed at 1.3100, the lowest level since August 2022. On Friday, Canada will report May Manufacturing Sales. The Loonie lagged behind AUD and NZD despite the 2% gain in crude oil prices.

Like this article? Help us with some feedback by answering this survey:

- After five days of losses, the GBP/JPY managed to jump above 181.00 on Thursday.

- GDP in the UK contracted in May but was lower than expected.

- BoJ’s policy tweak expectations to limit the JPY’s losses.

The GBP/JPY gains ground despite weak economic figures from the UK. Investors continue to bet on an aggressive Bank of England (BoE), which limits the Pound’s losses, while the expectations of a pivot of the Bank of Japan (BoJ) support the Yen.

The Office for National Statistics (ONS) revealed that the UK's Gross Domestic Product (GDP) declined slower than expected in May at 0.1% MoM vs the expectations of 0.3%. The Manufacturing production saw similar results as they also contracted by 0.2% MoM in the same period but lower than the expectations of 0.5%. Finally, Industrial Production declined, but at a higher pace than expected at 0.6% vs 0.4% MoM in the same period.

The U.K. is undoubtedly moving towards a recession as the Bank of England tightens its monetary policy, and the economy weakens. In addition, the GDP has experienced a monthly contraction for the first time since March 2021.

Despite weak economic data, according to the World Interest Rate Probabilities (WIRP), the markets have already priced in a 50 basis points (bps) interest rate hike for August 3rd. However, the expectations have shifted for the subsequent hikes as a 25 bps increase is currently priced in for September 21st, as opposed to the initial projection of a 50 bps hike earlier in the week.

On the Japanese side, the JPY may limit its losses on the back of a Yield Control Curve (YCC) policy pivot by the Bank of Japan (BoJ). Masato Kanda, a currency diplomat from Japan, acknowledged that the prevailing deflationary trends "might be changing". Its worth noticing that rising wages may contribute to an increase in inflationary pressures, but the Bank shouldn’t disregard China’s economic situation, which is showing signs of weakness, as it could further weaken the local economy.

GBP/JPY Levels to watch

Despite indicators gaining ground, the short-term outlook favours the Yen over the GBP. The Relative Strength Index (RSI) shows strong downward momentum despite standing in positive territory. At the same time, the Moving Average Convergence Divergence (MACD) prints higher red bars indicating that the bears are in command.

Support Levels: 181.00, 180.50, 179.00.

Resistance Levels: 182.25 (20-day SMA), 182.50, 183.00.

GBP/JPY Daily chart

-638248777249918137.png)

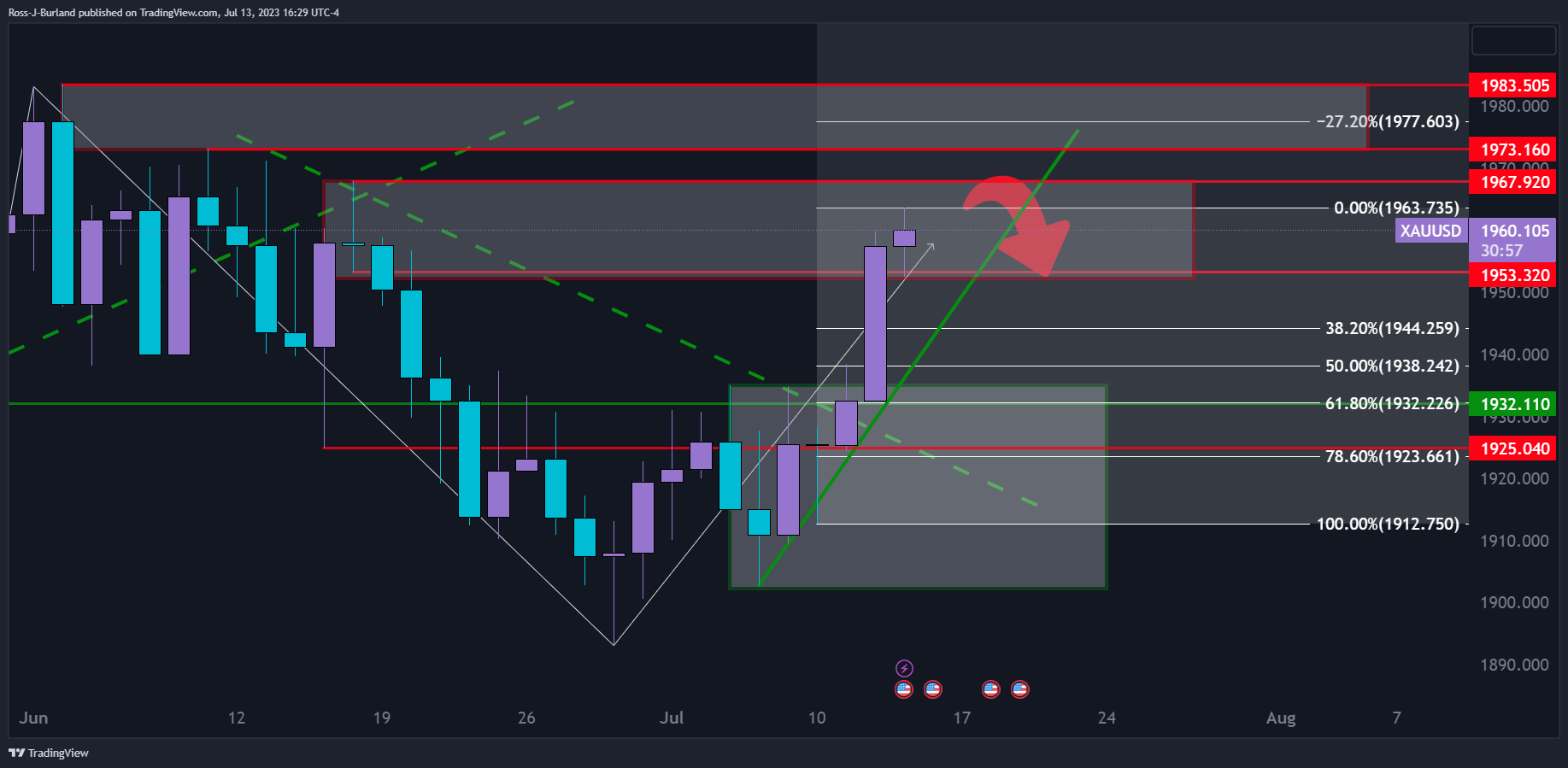

- Gold price could be on the verge of a correction as per resistance, but the bulks are still in control.

- A move through the current resistance of the $1,970s opens risk for a test of the $1,983 highs.

- Gold price bears eye the 61.8% ratio to the downside in line with $1,932 support.

Gold prices edged higher on Thursday while the Greenback continued lower as data continue to dictate the market's sentiment. US Treasury yields were the driver on yet another report that showed slowing US price pressures, pushing investors to add risk.

This benefitted the Gold price that was already glowing on the United States reported inflation report that showed that the Consumer Price Index rose by just 3% annualized in June, which was down from a 4% rate in May. On Thursday, the price pressures were shown to have eased in June, with the Producer Price index rising 0.1% annualized from 1.1% in May.

The DXY is already down for the sixth straight day and traded at its lowest since April 2021 near 99.97. A close below 100.00 will open risk for a test of the late March 2022 low near 97.685. Looking to US Treasury yields, the 2-year traded as low as 4.622% today and has fallen nearly half a percentage point from last week’s peak near 5.12%.

Gold technical analysis

The daily charts show that the price is now in a resistance area and could be on the verge of a correction. The 61.8% Fibonacci retracement area is eyed as support to $1,932.

- US inflation seems to be easing, with June’s Producer Price Index (PPI) missing estimates and the previous month’s data. The Core PPI, excluding volatile items, also showed signs of weakening.

- The Federal Funds Rate (FFR) is expected to peak at 5.25%-5.50% for the remainder of the year, according to money market futures, despite softening inflation data.

- Japanese households expect higher inflation levels, averaging 10.5% for next year, well above the BoJ’s 2% target.

The USD/JPY extended its losses for the sixth consecutive trading session and broke to a new two-month low of 137.92 on speculations the US Federal Reserve would hike in July to reach its peak rates as inflation continued to ease. Hence, the USD/JPY is trading at 137.98, below the psychological 138.00 figure, after hitting a daily high of 138.95.

Yen strengthens as the USD softens, following disappointing US PPI data and low bond yields

Inflation in the United States (US) is edging lower after data revealed that the June Producer Price Index (PPI) missed estimates of the downside following Wednesday’s consumer inflation report. PPI expanded at a 0.1% YoY pace, beneath forecasts of 0.4%, and lower than May 1.1%, while Core PPI, which strips volatile items, showed signs of losing steam and expanded at a 2.4% YoY pace, below estimates of 2.6% and the previous month’s 2.8%.

Although the data would justify a pause on the Fed’s tightening cycle, money market futures think otherwise. According to the CME FedWatcth Tool, odds for a quarter of a percentage increase lie above 90%. Even though Fed Chair Jerome Powell and some of his colleagues expressed that “a couple” of increases are pending, investors pared those bets. That said, the Federal Funds Rate (FFR) is expected to peak at 5.25%-5.50% for the remainder of the year.

That would likely keep the greenback pressured, as shown by the US Dollar Index (DXY). The DXY, which tracks the buck’s performance against other currencies, tumbled to a new 15-month low of 99.741, losing 0.80%. Another factor weighed by lower inflation levels in the US is bond yields, with the US 10-year note rate sitting at 3.767%, down nine basis points.

Therefore, the USD/JPY has dropped 4% since July 6, mainly attributed to a soft US Dollar and lowes US bond yields.

On the Japanese front, households’ expectations for higher inflation levels put pressure on the Bank of Japan (BoJ). According to Reuters, “Households expect inflation to average 10.5% a year from now, the June survey showed, down from 11.1% in the previous survey but well above the BOJ’s 2% target.” That comes at the expense of BoJ Governor Kazuo Ueda’s stance to keep monetary policy loose until the BoJ sees clear evidence that inflation will persist at around 2%.

USD/JPY Price Analysis: Technical outlook

The USD/JPY has tumbled below the 100-day Exponential Moving Average (EMA) of 138.79, extending its downward path past the top of the Ichimoku Cloud. With USD/JPY prices dropping inside the Cloud suggests the trend is still strong. The Tenkan-Sen crossing below the Kijun-Sen, while the Chikou Span standing below the price action, means the USD/JPY shifted bearish and could threaten to edge lower. First support emerges at the 137.00 mark, followed by the 200-day EMA at 136.40. Conversely, if USD/JPY buyers reclaim 138.00, that could pave the way to regain the 100-day EMA, followed by the 139.00 figure.

- EUR/JPY’s bulls gained ground following seven consecutive days of losses and jumped to 154.90.

- ECB’s accounts confirmed two additional hikes in 2023.

- China’s weak data weights on the JPY.

On Thursday, the EUR/JPY managed to stop the bleeding following a seven-day losing streak and jumped towards the 154.90 area. The Euro gained traction following the release of the European’s Central Bank (ECB) accounts from the June meeting, and the Yen lost ground against most of its rivals amid weak Chinese Trade Balance data.

ECB’s monetary policy accounts showed that most of the Governing Council supported a 25 basis points (bps) hike in June and confirmed that a minimum of two additional increases were needed. In addition, the members “could consider” hiking beyond July if necessary. That being said, the ECB’s tightening expectations remain steady. World Interest Rate Probabilities (WIRP) suggests that a 25 basis points (bps) hike is already priced in for the July meeting, and additional hikes of a quarter of a percentage points rise to 60% and 80% in September and October, respectively. The markets foresee no more hikes following December.

During the early Asian trading hours, China released that its trade surplus rose to $70.62 billion from $65.81 billion in June. In addition, Imports and Exports declined by 6.8% and 12.4% YoY respectively in the same period. In that sense, the Bank of Japan (BoJ) should monitor its biggest trading partner situation as it could aggravate the local economic downturn.

In addition, Japan's currency diplomat Masato Kanda cited that deflationary norms “may be changing” and that the BoJ is closely monitoring the FX markets. It's worth noticing that the JPY had gained ground in the previous session thanks to expectations on a Yield Control Curve (YCC) policy tweak by the BoJ, so any hints of a pivot may contribute to limiting the Yen’s losses.

EUR/JPY Levels to watch

According to the daily chart, the EUR/JPY still holds a negative outlook for the short term. Indicators display weakness, with the Relative Strength Index (RSI) and Moving Average Convergence Divergence (MACD) standing in negative territory. However, on the bigger picture the outlook favour the Euro as it holds above the 100 and 200-day Simple Moving Averages (SMAs)

Support Levels: 153.40, 153.00, 152.50.

Resistance Levels: 155.40, 156.17 (20-day SMA), 157.00.

EUR/JPY Daily chart

-638248742970352418.png)

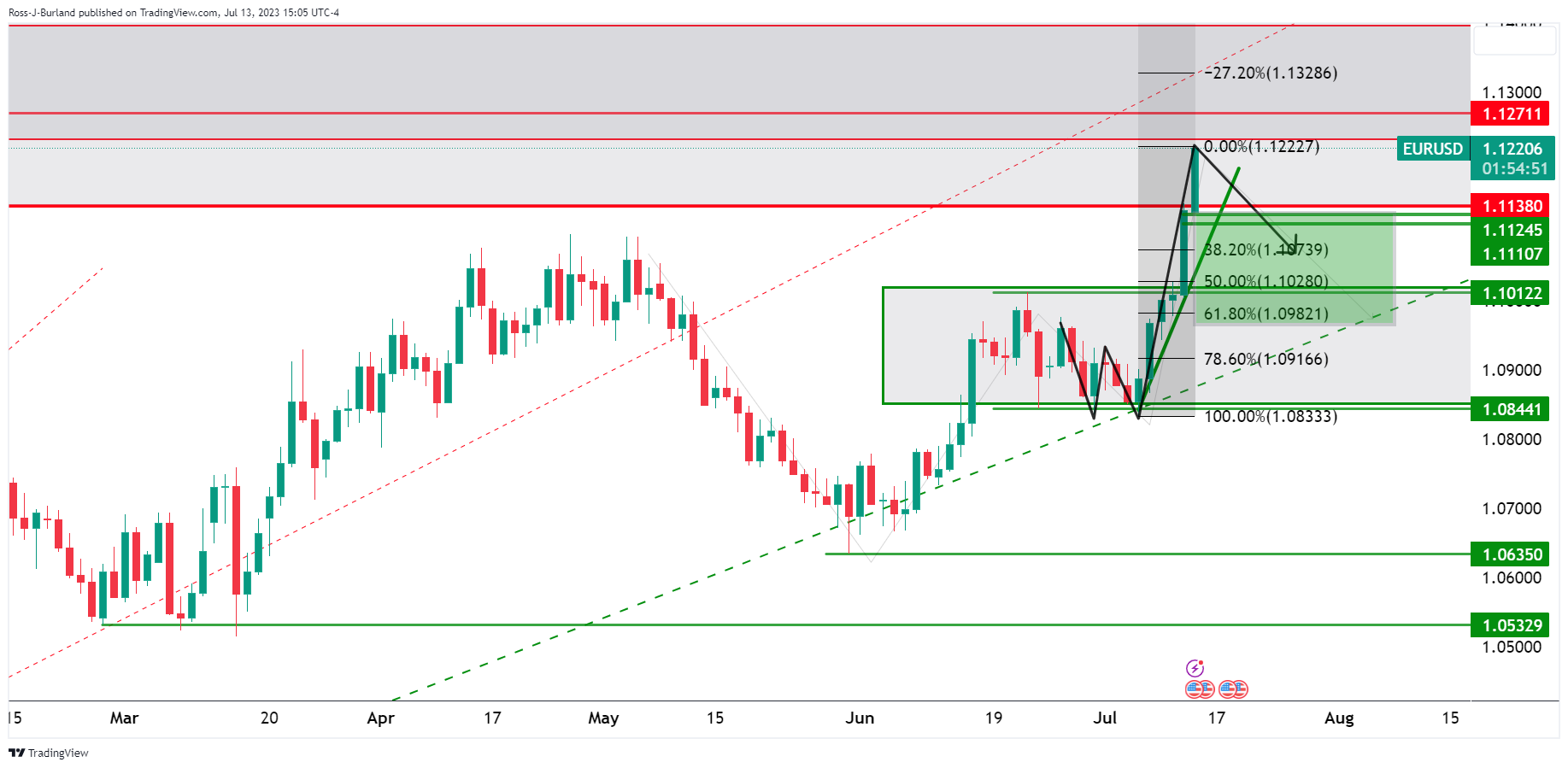

- EUR/USD bulls are in the market, but the trend could be ripening for a correction.

- Longs could face a squeeze into the end of the week and the charts below show the prospect of a correction.

EUR/USD has climbed by over 0.8%, to trade at its highest since April 2022 as markets foresee European Central Bank hiking another 50bp before cutting rates by about 65bp in H2 2024. Sentiment around the Federal Reserve has shifted more dovish further out which is seeing a waterfall slide in the Greenback this week after inflation data came in lower than expected.

EUR/USD weekly chart

The weekly chart's W-formation is still in progress with the right-hand arm heading higher into supply territory.

EUR/USD daily chart

The daily chart's W-formation is over-extended, so there are fewer prospects of a move into the neckline. However, a 50% mean reversion is feasible.

EUR/USD H4 chart

EUR/USD is showing no signs of deceleration on the 4-hour chart at this juncture.

EUR/USD H1 chart

EUR/USD is petering out, perhaps, as per the hourly chart. The 38.2% ratio is in sight and breaking the 50% mean reversion area will likely set the scene for a deeper correction into London and New York.

- The US Producer Price Index (PPI) for June rose below estimates, suggesting a steady deceleration of inflation in the US.

- Initial Jobless Claims in the US were lower than estimated, although the focus remains on the Fed’s inflation targets.

- The UK missed a recession, though fears reignited as the Bank of England is expected to tighten monetary conditions.

GBP/USD rallies past the 1.3100 mark and is gaining close to 1% on Thursday, as overall US Dollar (USD) weakness extended amid speculations the Federal Reserve (Fed) is closing to finishing its tightening cycle after June’s PPI and CPI data was softer than expected. The GBP/USD is exchanging hands at 1.3111 after hitting a daily low of 1.2979.

Rising speculations of Fed’s tightening cycle ending spurs Sterling gains

GBP/USD accelerated its gains after the US Bureau of Labor Statistics (BLS) revealed that prices paid by producers, also known as the Producer Price Index (PPI) in June, rose below estimates, suggesting the deflation process in the US is gathering pace. PPI rose by 0.1% YoY, below forecasts of 0.4%, down ticked from May 1.1%. Core PPI, which strips volatile items, showed signs of losing steam and expanded at a 2.4% YoY pace, below estimates of 2.6% and the previous month’s 2.8%.

At the same time, the BLS informed that Initial Jobless Claims for the week ending July 5 climbed less than estimates of 250K, standing at 237K. Even though the data portrays a tight labor market, investors ignored it, as the Fed’s primary focus remained on inflation.

Despite the inflation downtrend continuing, the Federal Reserve is estimated to raise rates by 25 bps at the upcoming July meeting. However, bets for the rest of the year, paired as shown by November’s odds standing at 21%, according to CME FedWatch Tool.

On the UK front, the UK economy dodged a recession, as UK’s GDP growth for the last 3-months came at 0%, while month-over-month (MoM) figures in May dropped -0.1%, trailing April’s 0.2% expansion. Although the economy didn’t grow, concerns of a recession loom, as the Bank of England (BoE) is set to tighten monetary policy to curb high inflation at 8.6 percent levels.

GBP/USD Price Analysis: Technical outlook

the GBP/USD is set to test the 2021 yearly low of 1.3160 after storming through the 1.3000 figure, which didn’t last long enough, to refrain buyers from committing to open fresh long bets, that Sterling (GBP) would continue to edge higher. A decisive break above the former could put the 1.3200 figure on the table; otherwise, a healthy correction could send the pair dipping towards the 1.3100 psychological level before diving to July 12 daily high at 1.3000. Of note, the Relative Strength Index (RSI) is at overbought conditions, still shy of reaching the 80 levels, usually used as the extreme overbought area, after an asset witnessed a strong uptrend.

The US Treasury Department has announced that the government recorded a $227.8 billion deficit in June, which was larger than the expected deficit of $175 billion. Total receipts in June amounted $418 billion, while outlays were $646 billion.

In the same month last year, the deficit was $88 billion. So far, during the fiscal year 2023 (FY 2023), the fiscal deficit has reached $1,392 billion, which is $17 billion higher than the total deficit of FY 2022. July, August, and September are typically deficit-heavy months, so the final deficit for FY 2023 will likely be larger.

- USD/CHF recorded more than 0.85% losses on the day, falling below the 0.8600 mark.

- Following soft CPI and PPI figures from the US from June, investors take of the table an additional hike by the Fed past July.

- Jobless Claims decelerated in the week ending on July 7.

- Declining US Treasury yields made the DXY dive to lows since April 2022.

On Thursday, the USD/CHF tallied a six-day losing streak, falling below the 0.8600 mark for the first time since January 2015. In that sense, soft Consumer Price Index (CPI) and Produce Price Index (PPI) data from the US fueled a widespread USD weakness as its DXY index fell below the 100.00 level for the first time since April 2022.

The Producer Price Index (PPI) from the US from June came in at 0.1% MoM, less than the 0.2% anticipated, and the Core Figure came in at 2.4%, falling short of the 2.6% forecast. Furthermore, US Jobless Claims for the week ending July 7 slowed down. It was reported that 237K people filed their first state unemployment insurance claims, less than the consensus estimate of 250K and the previous figure of 249K.

The yields on US Treasury bonds are falling in response to the US data. The 2-year yield decreased to 4.62%, the 5-year rate to 3.85%, and the 10-year yield decreased to 3.77% all displaying more than 2% slides.

Despite this, the CME FedWatch tool indicates that investors continue to wager on a 25 basis point increase by the Federal Reserve (Fed) in July. The declining yields reflect a drop in the likelihood of a subsequent hike after July, which is now just about 15%, down from 40% at the beginning of the week.

On the CHF’s side, investors will eye the release of the Producer Price Index from Switzerland from June on Friday, expected to decline 0.2% MoM from the previous 0.3% reading.

USD/CHF Levels to watch

According to the daily chart, the daily chart suggests a bearish outlook for the USD/CHF. However, the Relative Strength Index (RSI) pierced through the oversold threshold of 70.00, suggesting that an upwards correction may be on the horizon to consolidate the latest downward movements.

If there is an upwards correction, short-term resistance levels line up at 0.8665, 0.8700 and 0.8750. In case bears continue to gain momentum, supports are seen at 0.8500, 0.8360 and 0.8300 (January 15, 2015 low).

USD/CHF Daily chart

-638248651410489613.png)

- USD/MXN recovers slightly after touching multi-year lows of 16.8083 but stays below the 17.0000 figure.

- Initial Jobless Claims in the US rose less than expected, while US Producer Price Index (PPI) for June grew by 0.1% MoM, less than estimates.

- With no Mexican economic data, USD/MXN traders are focused on US dynamics.

USD/MXN resumes its downtrend after touching muti-year lows of 16.8083, remains below the 17.0000 figure on Thursday after data from the United States (US) shows the Federal Reserve’s (Fed) job is about to be achieved, as inflation continues to edge lower. At the time of writing, the USD/MXN is trading at 16.8682 after hitting a daily high of 16.9619.

Mexican peso gains ground as US Dollar weakens amid lower-than-expected jobless claims, PPI

The USD/MXN drops due to improved risk appetite, to the detriment of safe-haven peers, like the US Dollar (USD). Data from the US Department of Labor (DoL) revealed that Initial Jobless Claims for the last week climbed less than estimates of 250K, standing at 237K. The Fed’s Beige Book showed that demand for labor “remained healthy” in June, though it noted that hiring “was getting more targeted and selective.”

At the same time, the US Producer Price Index (PPI) for June expanded by 0.1% MoM, exceeding May’s 0.4% plunge but was beneath estimates of 0.2%. On year-over-year (YoY) figures, PPI grew 0.1%, below forecasts of 0.4%, while the Core PPI, which excludes volatile items, increased 0.1% MoM, unchanged from May, accelerating below estimates of 0.2%. Yearly Core PPI cooled down compared to expectations of 2.6% and came at 2.4%. Hence PPI data followed suit with a soft US CPI report that could refrain Fed officials from lifting rates twice, as they previously commented after the FOMC’s June meeting.

An absent Mexican economic docket leaves USD/MXN traders focused on the US dynamics. As long as the interest rate differential between the US and Mexico favors the latter, further downside is expected. However, traders must know that political risks are beginning to boil in Mexico as general elections loom for June 2024.

USD/MXN Price Analysis: Technical outlook

The USD/MXN downtrend would likely continue as the pair remains below the 17.00 mark. Sellers eyeing the October 2015 swing low of 16.3267 keeps the USD/MXN pressured, with the next support eyed at 16.5000 before sellers reclaim the latter. The following support would emerge at 16.00. Conversely, if USD/MXN buyers regain the 17.0000 figure, it could exacerbate a recovery toward the 20-day Exponential Moving Average (EMA) at 17.1073 short term. The USD/MXN must surpass the 17.4038 area to switch the bias to neutral.

- The XAG/USD records more than 2% gains on the day, jumping to the $24.70 area.

- Following soft CPI figures on Wednesday, weak PPI on Thursday applied further pressure on the US Dollar.

- Falling US Treasury yields and dovish bets on the Fed allowed precious metals to advance.

The XAG/USD recorded a fifth consecutive day of gains and jumped to its highest level since mid-May towards the $24.70 area. In that sense, following soft Consumer Price Index (CPI) and Produce Price Index (PPI) data from the US, investors refrained from betting on an additional hike from the Federal Reserve (Fed) past July which made the US yields decline across the board.

The Producer Price Index (PPI) came in at 0.1% MoM, which waslower than the 0.2% expected, while the Core Figure came in at 2.4% YoY, failing to match the expectations of 2.6%. In addition, US Jobless Claims for the week ending on July 7 decelerated. The number of people filing first-time claims for state unemployment insurance came in at 237K, lower than the consensus of 250K and its previous figure of 249K.

The US Treasury yields, which could be seen as the opportunity cost of holding non-yielding metals, continue to decrease following Wednesday’s soft CPI figures. The 2-year yield fell to 4.86%, the 5-year rate to 4%, and the 10-year yield to 3.80%. The 2-year and 5-year rates are displaying a 6% decline on the week, and the 10-year nearly a 3% fall, allowing the XAG/USD to advance.

According to the CME FedWatch tool, investors continue to bet on a 25 basis point hike by the Federal Reserve (Fed) in July. The falling yields reflect the decline in the odds of an additional hike following July which stand near 15% vs 40% at the start of the week.

XAG/USD Levels to watch

The daily chart suggests a (very) bullish outlook for the grey metal for the short term. The price trades above its main Simple Moving Averages (SMAs) of 20, 100 and 200 days while technical indicators hint at a strong bullish momentum. In that sense, the Relative Strength Index (RSI) points north near overbought conditions while the Moving Average Convergence Divergence (MACD) prints rising green bars.

Resistance Levels: $25.00, $25.30, $25.60.

Support Levels: $24.05, $23.50 (100-day SMA), $23.10 (20-day SMA),.

-638248594415611915.png)

In an interview with CNBC on Thursday, San Francisco Federal Reserve President Mary Daly said it was too early to declare victory on inflation, as reported by Reuters.

Additional takeaways

"Hard to say wage growth is going to lead inflation down."

"We still have an economy with a lot of momentum."

"We need to move rates up to restrictive territory."

"Policy effects need to go through the system."

"As inflation starts coming down, we can start lowering the nominal rate to bring real rates down to neutral level."

"We want to start heading towards the neutral rate as we approach 2% on inflation."

"Right now, all of my attention is on decidedly if we need to hike more and how much more we need hike in order to really get inflation heading down to 2%."

Market reaction

These comments failed to help the US Dollar find demand. As of writing, the US Dollar Index was down 0.55% on the day at 100.00.

- NZD/USD trading at 0.6378 extends gains vs. the USD, bolstered by recent US inflation data.

- US Producer Price Index (PPI) for June rose by 0.1% MoM, slightly below estimates of 0.2%, indicating slowing factory inflation in the US.

- Initial Jobless Claims in the US for the week ended July 6 were less than expected, suggesting a tight labor market.

The New Zealand Dollar (NZD) extends its gains vs. the US Dollar (USD), spurred by recent inflation data in the United States (US) on the consumer side, registered a solid deceleration. Also, today’s economic docket prompted speculations the Federal Reserve (Fed) is about to end its tightening cycle. At the time of writing, the NZD/USD is trading at 0.6378.

US inflation data spurs speculation about Fed’s tightening cycle, boosting Kiwi

A risk-on impulse favors risk-perceived Forex currencies like the Kiwi (NZD), contrarily to the safe-haven greenback. On Thursday, the US Bureau of Labor Statistics (BLS) delivered inflation and labor market data, crucial for the Fed, which Is expected to lift rates 25 bps at the July meeting. The US Producer Price Index (PPI) for

US Producer Price Index (PPI) for June rose by 0.1% MoM, exceeding May’s 0.4% plunge but was beneath estimates of 0.2%. Annually based, PPI expanded by 0.1%, below forecasts of 0.%. The so-called Core PPI, which strips out volatile items, rose by 0.1% MoM, unchanged from May, and accelerated below estimates of 0.2%. Yearly Core PPI cooled down compared to expectations of 2.6% and came at 2.4%. The data showed the also called factory inflation is slowing down, in tune with Wednesday’s CPI report, which witnessed a 1% drop in CPI towards the 3% threshold.

In other data, the BLS revealed Initial Jobless Claims for the week ended July 6, jumping 237K, below the estimates of 250K, portraying a tight labor market. The Fed’s Beige Book showed that demand for labor “remained healthy” in June, though it noted that hiring “was getting more targeted and selective.”

The NZD/USD reacted upwards to the data, hitting a daily high of 0.6394, before retracing some pips, to current spot prices.

Data on the New Zealand (NZ) front, even though it was weaker, with the manufacturing sector contracting in June to its lowest level since November 2022, it was ignored by investors. Even the latest monetary policy decision of the Reserve Bank of New Zealand (RBNZ) of keeping rates unchanged does little to cramp NZD/USD uptrend.

NZd/USD Price Analysis: Technical outlook

The NZD/USD daily chart portrays the pair as neutral-upwards, threatening to extend its gains past the February 14 swing high at 0.6389, which could put into play 0.6400 if cleared. Once the figure is reclaimed, the NZD/USD yearly high of 0.6538 would be at the brisk of being challenged. Nonetheless, traders must achieve a daily close above 0.6389 to cement the case for higher prices. Conversely, the NZD/USD first support would be the 0.6300 mark. Sellers would keep a close eye, as they would like to test the 200-day EMA at 0.6223, but firstly they must reclaim June 16 daily high turned support at 0.6248, as they eye the 0.6200 barrier.

A spokesperson for the International Monetary Fund (IMF) said on Thursday that slowing exports and weaker private investment cause China's growth momentum to slow, per Reuters.

"The overall picture of growth in China is one of slowing economy, consistent with the IMF forecasts in April," the spokesperson added. "Subdued inflation in China is due to weaker demand, slack in the economy after strong reopening in the first quarter."

Market reaction

These comments don't seem to be having a noticeable impact on risk mood. As of writing, the S&P 500 Index was up 0.6% on the day.

The Riksbank delivered in June but was unable to convince the market. Economists at Commerzbank analyze the Swedish Krona outlook.

No upside potential for the time being

Although the Riksbank raised the key interest rate in June, it is not acting decisively enough against inflation risks compared to the European Central Bank. Therefore, the SEK will probably not have much upside potential this year.

Only next year, when the tide turns in favour of the Riksbank, should the Krona appreciate again.

Source: Commerzbank Research

Gold price has recovered and is back to $1,950. Economists at Commerzbank analyze the yellow metal’s outlook.

Further upside potential towards the end of the year

The recent weakening of the Gold price is likely to have come to an end, now that the market has significantly scaled back its expectations of further US interest rate hikes.

We even see some further upside potential towards the end of the year. Because by then at the latest it should be clear that the US rate hike cycle is over.

Source: Commerzbank Research

Slowing inflation adds to headwinds for the US Dollar, economists at UBS report.

Inflation continued to soften

US consumer price inflation slowed markedly in June, rekindling hopes that the Fed could soon be able to call an end to its fastest rate-hiking cycle since the 1980s. Annual headline inflation for the month was 3%, down from 4% the prior month and the smallest increase since March 2021.

Core inflation, which excludes volatile food and energy prices, rose 4.8%, decelerating from 5.3% in May and coming in below the consensus forecast of economists. There were even promising signs that services sector inflation, which has been a major concern for policymakers, is cooling. Services excluding housing and energy decelerated to a 4% annual advance, also the smallest increase since late 2021.

Despite the good news on inflation, our view is that the Fed will be reluctant to declare victory just yet. But the data do support our base case that an end to hikes is now in sight, which will add to pressure on the US Dollar.

USD/CAD could now break below 1.3000 quite soon, economists at ING report.

Loonie has the best volatility-adjusted carry in the G10 space

The extra hike by the BoC and no pushback against further moves in the future mean that CAD can keep benefitting from an attractive carry.

It’s worth remembering that the Loonie has the best volatility-adjusted carry in the G10 space. We don’t necessarily see this as the inception of a broader USD downtrend, but the close USD/CAD correlation also means that CAD is more shielded in the event of a USD rebound than other pro-cyclical currencies.

A move below 1.3000 is surely possible in the coming weeks, although we may need to wait the fourth quarter of this year to see USD/CAD sustainably trade around 1.27/1.28.

Economists at Nordea continue to think that the 25 bps hike very likely seen at the July meeting will be the last one in this cycle.

Another 25 bps rate hike in July is close to a done deal

The European Central Bank continues to see more tightening warranted, and another hike in July appears a done deal.

Upside inflation risks need to ease further and the impact of tighter policy to strengthen for the ECB to stop after July, which remains our baseline.

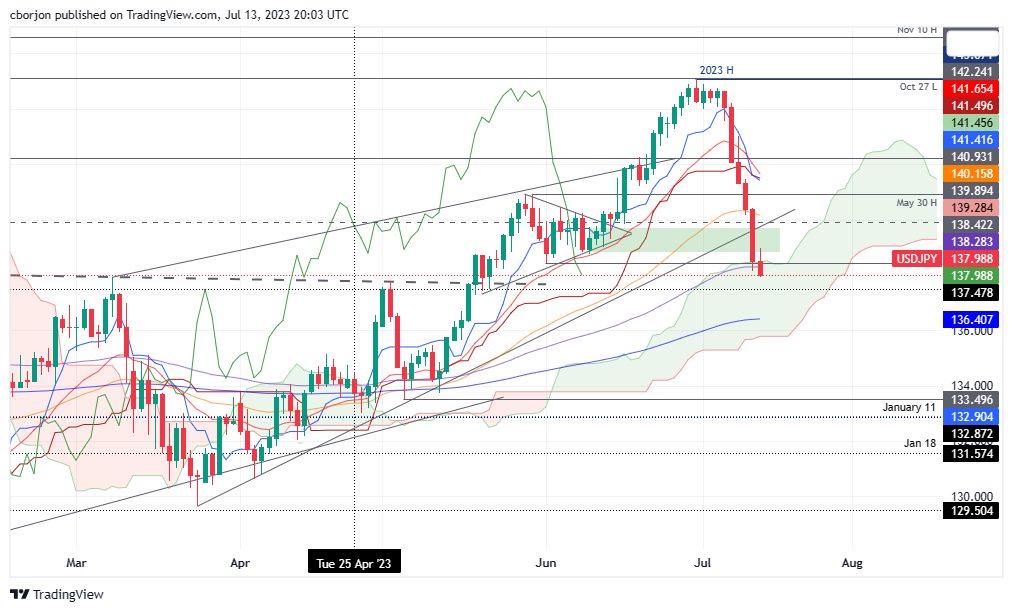

- USD/JPY has found an intermediate cushion near 138.50. More downside is expected as US PPI has softened significantly.

- The monthly headline and core PPI expanded by 0.1% but at a slower pace than the consensus of 0.2%.

- A significant decline in US factory gate prices indicates that household demand has dropped sharply.

The USD/JPY pair has gauged intermediate support near 138.50 in the early European session. The asset has attempted a recovery move after building a base around 138.50, however, more downside seems favored as the United States Producer Price Index (PPI) has softened more than expected.

The monthly headline and core PPI expanded by 0.1% but at a slower pace than expected by the market participants at 0.2%. On an annualized basis, headline prices at factory gates have decelerated dramatically to 0.1% vs. the consensus of 0.4% and the former release of 0.9%. Additionally, core PPI has softened to 2.4% against the estimates of 2.65 and the prior release of 2.8%.

After the soft inflation report, a significant decline in factory gate prices indicates that price pressures are declining broadly. Also, households’ demand has dropped sharply which has forced producers to grip retail prices.

The pace of softening in inflation and the PPI report is going to encourage the Federal Reserve (Fed) to skip the policy-tightening spell for the second time.

Apart from the PPI report, weekly Initial Jobless Claims have also been released for the week ending July 07. The US Department of Labor has reported that first-time claimers were 237K vs. expectations of 250K and the former release of 249K.

S&P500 is expected to open on a bullish note, considering positive gains made in the overnight session. US equities have remained firm as soft inflation has trimmed fears of a recession significantly. The US Dollar Index (DXY) has continued its decline to near 100.15.

On the Japanese Yen front, Japan's top currency diplomat Masato Kanda cited that deflationary norms may be changing. Kanda added the government is closely watching FX market moves.

- EUR/USD prints new 2023 peaks around 1.1190.

- Immediately to the upside emerges the 1.1200 barrier.

EUR/USD extends the monthly bullish performance and approaches the 1.1200 hurdle for the first time since February 2022.

The continuation of the upside momentum is expected to revisit the round level at 1.1200 in the very near term. Once this level is cleared, a probable visit to the 2022 high at 1.1495 (February 10) could start emerging on the horizon.

Looking at the longer run, the positive view remains unchanged while above the 200-day SMA, today at 1.0643.

EUR/USD daily chart

-

Canadian Dollar continues rallying against the US Dollar on Thursday after the BoC’s decision to raise rates at its meeting on the previous day.

-

The Bank of Canada cited Canada’s robust economic growth as the main reason for raising rates as it fears inflationary forces building.

-

USD/CAD falls close to the June lows in 1.31s, threatening a break, but tough support below likely to prevent deeper sell-off.

Canadian Dollar (CAD) continues rising versus the US Dollar (USD), on Thursday, in the aftermath of the Bank of Canada’s (BoC) decision to raise interest rates by 0.25% and its open-ended, data-driven approach to forward guidance.

USD/CAD is trading in the upper 1.31s as the US session gets underway.

Canadian Dollar news and market movers

-

The Canadian Dollar trades higher after the BoC raises interest rates by 0.25%, bringing the overnight rate to 5.00% at its meeting on Wednesday.

-

Higher rates are positive for CAD (negative for USD/CAD) as they attract more foreign capital inflows increasing demand for the currency.

-

Governor Tiff Macklem stressed future policy decisions would be dependent on incoming data, leaving markets unclear on whether this would be the BoC’s last hike in the tightening cycle.

-

The decision to raise rates at the July meeting had only been reached after a discussion by board members on the relative merits of leaving rates unchanged or raising them.

-

“On balance, our assessment was the cost of delaying action was larger,” Macklem concluded.

-

Regarding inflation, the BoC Governor said that whilst it was welcome inflation in Canada had fallen to 3.4% in May – substantially below the 8.1% of last summer – a large number of items in the basket of goods used to calculate the Consumer Price Index (CPI) were still rising strongly.

-

“A little over half the components of the CPI basket,” had seen their prices rising more than 5%, said Macklem in the press conference after the announcement. “If you look across the basket, meat is up 6%, bread is up 13%, coffee is up 8%, baby food is up 9% … rent is up 6%,” he added.

-

Demand and consumption in the Canadian economy were still growing, said Macklem, indicating the possibility of inflation pressures ahead.

-

The sensitive housing market had also defied expectations of a slow-down and was instead showing signs of picking up despite higher interest rates increasing mortgage repayments.

-

Recent labor market stats showed 60K new jobs were filled in Canada in June, more than three times the estimated 20K. Average Hourly wages rose 3.9%, which though lower than the previous month’s 5.1%, was nevertheless buoyant. Despite the strong jobs number, the report also showed the Unemployment Rate unexpectedly rising to 5.4% from 5.2% in the previous month, and higher than the 5.3% forecast.

-

All in all, the overall positive macroeconomic data from the Canadian economy leant the BoC governing council to make their decision to raise rates to stave off incoming inflationary effects rather than wait and see.

-

The BoC does not now see inflation returning to its 2% target until the middle of 2025, about 6 months later than its previous forecast.

-

Although the Canadian Dollar rose on the BoC announcement, a growing number of analysts foresee a harsher climate for the currency in the second half of 2023.

-

Analysts at National Bank of Canada, Macquarie and Nomura Bank all foresee the CAD weakening in H2 of 2023.

-

“Our bearish view for the second half 2023 remains predicated on the prospect that Canada will suffer a more severe slowdown than the U.S.,” said Thierry Wizman, global currencies and interest rate strategist at Macquarie Futures USA.

-

Wizman cites the negative impact higher interest rates will have on the Montreal Housing market as a major driver of a weaker CAD later in the year.

-

“The rise in rates has already happened and households will begin to feel the squeeze as fixed-rate mortgages are rolled over at higher rates,” Wizman said, in a note quoted by the Financial Post.

-

Nomura sees rate differentials and greater growth in the US as driving USD/CAD higher.

-

The negative effect of a global economic slowdown on commodity prices negatively impacting Canada's terms of trade is the main factor dragging CAD down, according to National Bank of Canada in a note cited on Poundsterlinglive.com.

-

The US Federal Reserve is almost certain to raise rates at its July 26 meeting, given the 5.3% Core CPI still prevalent in the US, which will probably boost the US Dollar.

-

Despite Wednesday’s lower-than-expected US inflation data, market gauges of the probability of a further rate hike from the Fed at their July 26 meeting put the chances at above 90%, although any further hikes in 2023 are now less probable than the Fed standing pat.

Canadian Dollar Technical Analysis: June lows threatened

Despite recent weakness, USD/CAD is in a long-term uptrend on the weekly chart, which began at the 2021 lows. Since October 2022, the exchange rate has been in a sideways consolidation within that uptrend. Given the old saying that ‘the trend is your friend’, however, the probabilities of an eventual continuation higher marginally favor longs over shorts.

USD/CAD appears to have completed a large measured move price pattern that began forming at the March 2023 highs. This pattern resembles a 3-wave ABC correction, in which the first and third waves are of a similar length (labeled waves A and C on the chart below).

USD/CAD’s measured move looks like it has completed, given waves A and C are of a similar length. This suggests price probably bottomed at the June 27 lows and is now at the start of a new cycle higher.

-638248499864483916.png)

US Dollar vs Canadian Dollar: Weekly Chart

A confluence of support situated under the June lows in the upper 1.3000s, which is made up of several longer moving averages and a major trendline, provides a backstop to further losses. Only a decisive break below 1.3050 would indicate this thick band of weighty support has been definitively broken, bringing the uptrend into doubt.

-638248499434094636.png)

US Dollar vs Canadian Dollar: Daily Chart

The daily chart shows USD/CAD recovered to just shy of the 1.3400 crossroads where the 50-day Simple Moving Average (SMA) is located, last Thursday, before reversing lower.

It has since declined all through this week and is now threatening the June 27 lows at 1.3117. It is possible that price may break below those lows – however, it is unlikely to go much lower immediately below them is the confluence of support situated between 1.3080-1.3100. Only a clean break below 1.3050 would reverse the trend and suggest a much more bearish picture for USD/CAD.

More likely, the pair will retest the level of the June 27 lows and then recover again as it forms a complex basing pattern before eventually going higher.

It will take a decisive break above the 50-day SMA, however, to reinvigorate the USD/CAD uptrend again. Bulls marginally have the upper hand, with the odds slightly favoring a recovery and a continuation higher.

Bank of Canada FAQs

What is the Bank of Canada and how does it influence the Canadian Dollar?

The Bank of Canada (BoC), based in Ottawa, is the institution that sets interest rates and manages monetary policy for Canada. It does so at eight scheduled meetings a year and ad hoc emergency meetings that are held as required. The BoC primary mandate is to maintain price stability, which means keeping inflation at between 1-3%. Its main tool for achieving this is by raising or lowering interest rates. Relatively high interest rates will usually result in a stronger Canadian Dollar (CAD) and vice versa. Other tools used include quantitative easing and tightening.

What is Quantitative Easing (QE) and how does it affect the Canadian Dollar?

In extreme situations, the Bank of Canada can enact a policy tool called Quantitative Easing. QE is the process by which the BoC prints Canadian Dollars for the purpose of buying assets – usually government or corporate bonds – from financial institutions. QE usually results in a weaker CAD. QE is a last resort when simply lowering interest rates is unlikely to achieve the objective of price stability. The Bank of Canada used the measure during the Great Financial Crisis of 2009-11 when credit froze after banks lost faith in each other’s ability to repay debts.

What is Quantitative tightening (QT) and how does it affect the Canadian Dollar?

Quantitative tightening (QT) is the reverse of QE. It is undertaken after QE when an economic recovery is underway and inflation starts rising. Whilst in QE the Bank of Canada purchases government and corporate bonds from financial institutions to provide them with liquidity, in QT the BoC stops buying more assets, and stops reinvesting the principal maturing on the bonds it already holds. It is usually positive (or bullish) for the Canadian Dollar.

The disinflation trend continued in June. While this will not derail a July Fed hike, it increases ABN Amro’s conviction that this will be the final rate rise.

June disinflation will not derail a July Fed hike

While the Fed will welcome further disinflationary progress, the June CPI report is unlikely to prevent the FOMC from hiking by another 25bp when it meets on 24-25 July, given the stickiness in labour-intensive services inflation and the broader resilience in other macro indicators in the US.

However, the report gives us greater conviction that July will be the last hike of the current cycle, with a September hike looking unlikely assuming current data trends persist. Our base case continues to be for the Fed to start cutting rates next March. Still, we continue to see a risk that stickier services inflation keeps broader price growth above the Fed’s target in the medium term, with the risk therefore tilted towards rates staying restrictive for longer.

- DXY extends the sell-off to the 100.15/10 band, new YTD lows.

- A test of the key 100.00 support looms closer.

Further downside bias drags DXY to new 2023 lows in the 100.15/10 band on Thursday.

The continuation of the decline of the dollar looks the most likely scenario for the time being. Against that, the index now targets the psychological 100.00 yardstick ahead of the weekly low of 99.81 (April 21 2022).

Looking at the broader picture, while below the 200-day SMA at 104.44, the outlook for the index is expected to remain negative.

DXY daily chart

Markets Strategist at UOB Group Quek Ser Leang comments on the recent price action and prospects for EUR/USD.

Key Quotes

While EUR/USD rose above the cloud resistance and reached 1.1010, it then fell back lower. However, EUR/USD did not break below 1.0800 (low of 1.0832 last week). EUR/USD turned around strongly from 1.0832, and yesterday (12 July 2023), it jumped to a fresh year-to-date high of 1.1140.

Weekly MACD appears poised to crossover into positive territory. This bodes well for further EUR/USD strength. On the weekly chart, there are hardly any significant resistance levels until the 2022 high of 1.1495. The top of the weekly exponential moving average envelope is also near 1.1495. However, it remains to be seen if EUR/USD has enough momentum to reach this solid resistance level in the next couple of months. Note that on the daily chart, EUR/USD has already moved above the top of the exponential moving average envelope.

This time around, in order to keep the momentum going, EUR/USD must stay above the trendline support, currently near 1.0880. This level is also near the 55-day exponential moving average. On a short-term note, 1.1010 is already a rather strong support level.

- Producer inflation in the US increased only 0.1% on a yearly basis in June.

- US Dollar Index stays in negative territory below 100.50.

The Producer Price Index (PPI) for final demand in the US rose 0.1% on a yearly basis in June, down from the 0.9% increase recorded in May, the data published by the US Bureau of Labor Statistics revealed on Thursday. This reading came in lower than the market expectation of 0.4%.

The annual Core PPI increased 2.4% in the same period, compared to the market expectation of 2.6%. On a monthly basis, the PPI and the Core PPI both rose 0.1%.

Market reaction

The US Dollar stays under modest bearish pressure after this data and the US Dollar Index was last seen losing 0.25% on the day at 100.30.

- EUR/JPY manages to gather some upside traction on Thursday.

- Initial contention seems to have turned up near around 153.30.

EUR/JPY partially reverses the recent 7-session negative streak on Thursday.

The cross regains some balance and manages to bounce off Wednesday’s 4-week lows near 153.30. In case sellers return to the market, the cross risks a probable decline to the intermediary 55-day SMA, today at 151.91.

So far, the longer term positive outlook for the cross appears favoured while above the 200-day SMA, today at 145.81.

EUR/JPY daily chart

- Initial Jobless Claims decreased by 12,000 in the week ending July 8.

- Continuing Jobless Claims rise by 11,000 in the week ending July 1.

- US Dollar Index hits fresh lows, and then rebounds above 100.30.

Initial Jobless claims totaled 237,000 in the week ending July 8, the weekly data published by the US Department of Labor (DOL) showed on Thursday. The print follows the previous week's 249,000 (revised from 248,000) and came in below market expectations of 250,000.

Further details showed that “the 4-week moving average was 246,750, a decrease of 6,750 from the previous week's revised average.”

Continuing Claims rose by 11,000 in the week ended July 1 to 1.729 million, a reading worse than market estimates of 1.723 million. The four-week moving average was “1,735,250, a decrease of 10,750 from the previous week's revised average.”

Market reaction:

Alongside Jobless Claims, the June Produce Price Index (PPI) was released, showing more evidence of inflation slowing down. The US Dollar Index (DXY) hit fresh monthly lows after the reports at 100.12 and then rebounded, trimming a small fraction of recent losses, rising above 100.30.

- Gold price is trading back-and-forth around $1,960.00 as investors await further triggers.

- As the second-quarter result season is on its way, sheer volatility in US equities cannot be ruled out.

- Gold price has delivered a breakout of the Wyckoff ‘Accumulation’ chart pattern.

Gold price (XAU/USD) is demonstrating a non-directional performance around $1,960.00 as investors are awaiting United States Producer Price Index (PPI) data for further guidance. The US Dollar Index (DXY) is struggling to find any intermediate support as investors are hoping that the Federal Reserve (Fed) could tweak its old commentary of ‘two more rate hikes are appropriate’ after June’s soft inflation report.

S&P500 futures have generated significant gains in the European session, portraying the strong risk appetite of the market participants. As the second-quarter result season is on its way, sheer volatility in US equities cannot be ruled out. The yields offered on 10-year US Treasury bonds have rebounded to near 3.83%.

After soft inflation report, investors have shifted their focus towards the US PPI data, which will release at 12:30 GMT. As per the consensus, monthly headline and core PPI are expected to show a pace of 0.2%. Annual headline PPI is likely to decelerate to 0.4% vs. the former release of 1.1%. Sheer softening of prices of goods and services at factory gates would cool down inflationary pressures. Also, a decline in PPI would convey that the overall demand is in a declining stage.

Minneapolis Fed Bank President Neel Kashkari cited that policy rates needed to raise further and supervisors must ensure that banks are prepared to run new high-inflation stress tests to identify at-risk banks and size individual capital shortfalls.", as reported by Reuters.

Gold technical analysis

Gold price has delivered a breakout of the Wyckoff ‘Accumulation’ formed on a four-hour scale in which inventory is transferred from retail participants to institutional investors. The precious metal is in a ‘mark up’ phase and is expected to find stoppage near the horizontal resistance plotted from May 19 high at $1,984.25.

The Relative Strength Index (RSI) (14) has shifted into the bullish range of 60.00-80.00, indicating strength in the upside momentum.

Gold four-hour chart

USD losses extend. Shaun Osborne, Chief FX Strategist at Scotiabank, analyzes the Greenback’s outlook.

USD to be more susceptible to weak economic data reports moving forward

Economic data this week have cut the odds of the Fed delivering two more hikes this year and history shows markets are quick to discount the prospect of lower Fed rates once the rate cycle peak is in; history also shows that this typically pressures the USD and that feels about where we are in this process, with the USD trading at its lowest since last April. The USD is likely to be more susceptible to weak economic data reports moving forward.

The DXY is down nearly 2% on the week and is trading below the January and April lows at 100.8. This implies (to me) that risks are tilted towards another 2-3% drop at least in the coming weeks and months (which could stretch to a loss of around 5%, based on the charts).

The accounts of the European Central Bank's (ECB) June policy meeting revealed on Thursday that policymakers agreed that it was seen as essential to communicate that monetary policy had still more ground to cover.

Key takeaways as summarized by Reuters

"It was argued that market participants would be surprised by the upward revision of inflation."

"A very broad consensus supported the 25 basis point rate increase."

"Emphasis was put on the merit of sticking to a data-dependent, meeting-by-meeting approach."

"A very broad consensus also prevailed in favour of confirming the end of reinvestments under the APP as of July."

"The level of the peak deposit facility interest rate, as well as its duration, as embodied in the forward curve and reflected in the staff projections, could be judged as insufficient to bring inflation back to the 2% medium-term target."

"Governing Council should stress that fiscal policy needed to be tightened."

"Inflation was still projected to remain too high for too long, calling into question whether it was returning to target in a timely manner."

"Upside risks to the inflation outlook were judged to still prevail."

"For the inflation projections to materialise, the Governing Council had still, as a minimum, to deliver two successive interest rate increases in June and July."

"Bringing inflation down from very high numbers to more moderate levels was easier than achieving a full return to 2%."

"Longer-term market-based measures remained stubbornly high."

"The view was held that the Governing Council could consider increasing interest rates beyond July, if necessary."

Market reaction

EUR/USD trades at fresh 15-month highs on Thursday, clings to strong daily gains at around 1.1170 after the ECB's publication.

USD/CAD is soft but holding within Wednesday’s range. Economists at Scotiabank analyze the pair outlook.

The underlying trend is USD-negative, but…

The underlying trend is USD-negative but trend dynamics are not quite as strong here as in some of the other USD pairs. Trend oscillators are, however, aligned bearishly for the USD across short, medium, and longer-term studies which continues to point to limited scope for USD rebounds and ongoing pressure on the downside towards the 1.31 area in the near term.

Resistance is 1.3200 and 1.3250.

- GBP/JPY has sustained comfortably above 180.00 as BoE is preparing for a consecutive fat rate hike.

- Weak UK factory activity data failed to impact the rally in the Pound Sterling.

- Japan's top currency diplomat Masato Kanda cited that deflationary norms may be changing.

The GBP/JPY pair is holding its auction above the psychological resistance of 180.00 in the London session. The cross picked strength after a five-day losing streak around 179.50 as investors expect that the Bank of England (BoE) is preparing for a consecutive fat rate hike in August.

Headline Consumer Price Index (CPI) in the United Kingdom seems sticky at 8.7% while core inflation that excludes volatile oil and food prices has printed a fresh high of 7.1%. Tight labor market conditions have started releasing heat due to higher interest rates but the journey towards achieving 2% inflation is far from over.

BoE Governor Andrew Bailey has already pushed interest rates to 5% and more interest rate hikes are in the pipeline. Money markets are anticipating that the interest rate peak by the BoE will be around 6.5%.

Meanwhile, weak UK factory activity data failed to impact the rally in the Pound Sterling. Manufacturing Production reported a light pace in contraction at 0.2% vs. the consensus of -0.5%. Meanwhile, the economic indicator remained between the consensus of -1.7% and the prior release of -0.6% at -1.2%. Monthly Gross Domestic Product (GDP) has posted a contraction by 0.1% while investors were anticipating a contraction by 0.3%.

UK Finance Minister Jeremy Hunt said that “while an extra Bank Holiday had an impact on growth in May, high inflation remains a drag anchor on economic growth.”

On the Japanese Yen front, Japan's top currency diplomat Masato Kanda cited that deflationary norms may be changing. This must be the outcome of the rising contribution of demand-driven aspects in inflationary pressures. Kanda added the government is closely watching FX market moves.

EUR/USD makes quick progress through the upper 1.11s. Shaun Osborne, Chief FX Strategist at Scotiabank, analyzes the pair’s outlook.

The 200-Week Moving Average of 1.1183 is a nearby bellwether to monitor

Solid gains and solid trend momentum are bringing my 1.12/1.13 target zone into range a bit more quickly than expected.

The 200-Week Moving Average (1.1183) is a nearby bellwether to monitor. The EUR has not traded above this mark since late 2021 and it has been a pretty good pointer for the EUR tone in recent years. A solid move (a weekly close, perhaps two) above here would suggest the EUR rebound has medium/longer term legs and might put 1.16/1.17 on the radar for the months ahead.

Sterling is strengthening further on Thursday. Economists at Scotiabank analyze GBP/USD outlook.

Spreads support firm gains

Cable is strengthening, with the help of solid yield spreads over the USD.

Sterling is trading higher for a sixth, consecutive daily gain and a 2.8% gain over the period.

GBP/USD is trading well through its 200-Week Moving Average which is support now at 1.2887 and has little ahead of it in terms of resistance until 1.3328 (76.4% retracement of the 2021/22 decline).

See – GBP/USD: Many investors will now be targeting a move to 1.33 assuming a weekly close above 1.30 – ING

Ahead of the summer, G10 volatility has just hit its lowest level since early 2022. Fed tightening cycles kill Dollar volatility until data suggest that the economy will need rate cuts, economists at Société Générale report.

Since 2003, August is clearly the worst month to hold a short vol position

EUR/USD volatility has just hit its lowest level since early 2022. But global monetary tightening comes at the cost of future growth, and investors could feel the pain when the data strike back.

US inflation is decelerating quickly, while historically, Fed tightening cycles suppress Dollar volatility until data suggest that the economy will need rate cuts.

Last but not least, August is generally a month where being short vol is a painful trade. Since 2003, EUR/USD volatility has increased this month in 75% of the years. Even if history is not bound to repeat, investors should not neglect this seasonal effect, especially in an environment where volatility remains under selling pressure and with the imminent threat of thinner summer liquidity.

US inflation came slightly lower than had been expected. Economists at Commerzbank analyze USD outlook after the US CPI report.

A small surprise in US CPI, a giant jump in EUR/USD

The majority of analysts had expected that the core rate would stand at 0.3% (MoM, seasonally adjusted), but it turned out to be just under 0.2%. ‘So what?’ one might wonder. That does not mean that the inflation issue in the US has now been solved. We might see setbacks over the coming months.

Greenback weakened significantly after the data release. One might ask if an inflation surprise of relatively small absolute magnitude can justify such market reaction. But we've seen similar patterns before. At recent levels, USD exchange rates obviously had priced in quite an unrealistic level of Fed tightening. That part of the USD exchange rates had to be corrected quite quickly.

The prospect of a reduced USD carry is putting pressure on a currency. That bit is the simple part of the story. However, there is one complication. As it is not just the terminal rate that matters (i.e. the rate peak) but also a matter of how long interest rates remain at this high level. That means: there is still some scope toward further Dollar weakness. Wednesday’s market move does not have to constitute the end of the USD weakness.

Economists at Scotiabank analyze USD/CAD outlook.

USD/CAD rebounds to remain limited to the 1.33, perhaps 1.34 – at most – area for now

The hot take bottom line from here is that USD/CAD rebounds are likely to remain limited to the 1.33, perhaps 1.34 (at most) area for now.

We have a 1.30 forecast for year-end but the risk of a downside overshoot to 1.28 through Q3 looks to be a growing risk.

See: USD/CAD set to move to 1.30 in the near future – TDS

Lee Sue Ann, Economist at UOB Group, reviews the latest interest rate decision by the RBNZ.

Key Takeaways

As expected, the Reserve Bank of New Zealand (RBNZ) decided to leave its official cash rate (OCR) unchanged at 5.50% at its Jul meeting. Since today’s decision was an interim review rather than a quarterly Monetary Policy Statement, there were no updated forecasts nor press conference with RBNZ Governor Adrian Orr.

New Zealand entered a technical recession in 1Q23, with the economy contracting by 0.1% q/q. Meanwhile, inflation undershot the RBNZ’s projection for two consecutive quarters. Headline CPI growth eased to 6.7% y/y in 1Q23. All eyes will now turn to 2Q23 CPI data due on 19 Jul, which is expected to see a further drop to 6.0% or lower.

We are keeping our OCR forecast at 5.50% for the rest of this year, though bearing in mind that the RBNZ has paused in previous tightening cycles before hiking again. The next monetary policy decision is on 16 Aug.

- US Dollar is near several multi-month lows against major currencies.

- The economic calendar puts the spotlight on the US Producer Price Index release.

- The US Dollar Index said goodbye to 101.00 and is now pulled toward 100.00.

The US Dollar (USD) was in a sea of red on Wednesday when compared to several other major currencies. It was very hard to look for any green print as the Greenback lost substantial ground against all G10 currencies with notable losses against the Japanese Yen extending over 1%. On Thursday, the US Dollar was down nearly 1% against the Australian Dollar (AUD/USD) and the New Zealand Dollar (NZD/USD). The US Dollar Index (DXY) has been unable to catch a breath and is again on the back foot nearing the all important 100.00 line in the sand.