- Аналітика

- Новини та інструменти

- Новини ринків

Новини ринків

According to Reuters on Tuesday, China will tighten monitoring on several thousand local government financial vehicles (LGFVs), barring new LGFVs from selling bonds publicly, to close loopholes in a strategy to handle municipal debt difficulties. two people with knowledge of the topic said.

Market reaction

With the positive development news in China, AUD/USD climbs above 0.6400, and NZD/USD edges higher to 0.5917 at the press time

The US Deputy Treasury Secretary Wally Adeyemo, expressed optimism on Monday that US banks had not curtailed lending as much as expected since financial issues were seen earlier this year, per Reuters.

Adeyemo said at an Economic Club of New York event that the US banking industry had undergone considerable consolidation following the bankruptcy of numerous banks in late winter and early spring, but there had been no significant pullback in credit.

Market Reaction

The US Dollar Index (DXY) is trading at 104.50, unchanged on the day amid the improvement in risk sentiment.

- Strong Chinese data and hawkish comments by BoJ Governor Ueda underpinned the JPY.

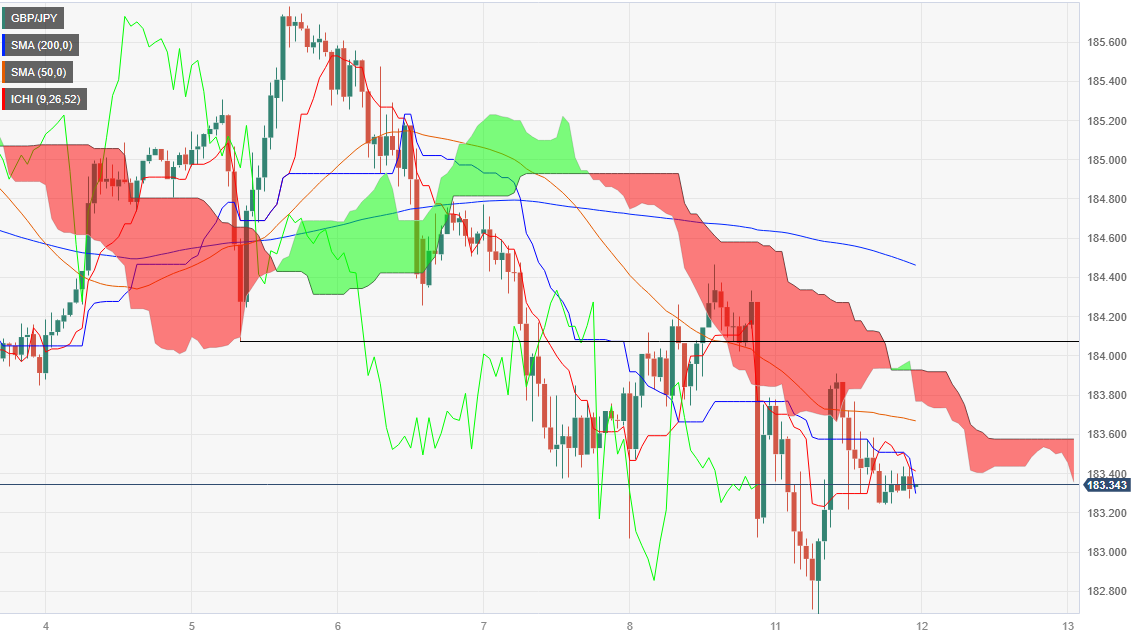

- The pair is neutral to upward biased from a daily chart, at the brisk of breaching the Ichimoku cloud.

- Short term, the GBP/JPY is downward biased, set to test the 183.00 area.

The Pound Sterling (GBP) stops its decline vs. the Japanese Yen (JPY) as Tuesday’s Asian session begins, following Monday’s session that witnessed a 0.47% loss for the cross-currency pair. The reasons behind the move were good Chinese data and some hawkish comments by the Bank of Japan (BoJ) Governor Kazuo Ueda. The GBP/JPY is trading at 183.38, a gain 0.06%.

GBP/JPY Price Analysis: Technical outlook

From a daily chart perspective, the pair is neutral to upward biased, remaining above the Ichimoku Cloud (Kumo). Nevertheless, since the cross printed the yearly high, the GBP/JPY achieved successive series of lower highs and lows, keeping that neutral stance on the cross. Also, an upslope support trendline, drawn from March 2023 lows, passes around 183.00. That said, a decisive break below the latter could open the door for further downside.

Short term, the GBP/JPY is set to extend its losses, capped on the upside by the Senkou Span B at 183.57. Once cleared, the pair’s next stop would be the bottom of the Ichimoku Cloud (Kumo) at around the 183.70 area, followed by a challenge of the 184.00 figure. Conversely, and the path of least resistance, the first support would be the 183.20 area. Once cleared, the cross would dive towards the 183.00 figure, followed by the September 11 daily low at 182.67.

GBP/JPY Price Action – Hourly chart

- AUD/USD takes a breather after surging from 0.6370 to 0.6430 amid the improvement in risk sentiment.

- The Australian Dollar benefited from the upbeat China's inflation data.

- Traders will monitor the Australian Confidence survey, US Consumer Price Index (CPI) data.

The AUD/USD pair edges higher and consolidates its recent gains around 0.6430 during the early Asian session on Tuesday. The rebound of the pair is bolstered by the weaker US Dollar (USD) and improvement in risk sentiment. Meanwhile, the US Dollar Index (DXY) hovers around 104.50 after retracing from the 105.00 area.

The China-proxy Australian dollar (AUD) benefited from China's inflation data. The Chinese Consumer Price Index (CPI) rose 0.1% YoY, from a 0.3% drop in the previous month, compared to the 0.2% rise anticipated. The monthly figure was 0.3% as expected. The improvement in Chinese inflation figures boosted the risk-on mood and dragged the safe-haven US Dollar lower.

On the US Dollar front, investors await the highly-anticipated US Consumer Price Index (CPI) data which might convince the Federal Reserve (Fed) interest rate expectation. The upbeat data would suggest the Federal Reserve needs to tighten monetary policy. This, in turn, might lift the Greenback against its rivals.

After the G20 Summit, US Treasury Secretary Janet Yellen conveyed more optimism that the US could control inflation without damaging the employment market. Yellen also said on Sunday that every gauge of inflation is declining and there were no massive wave of layoffs. Chicago Fed President Austan Goolsbee outlined the central bank's goal of leading the economy into a "golden path." This route represents a scenario in which inflation falls without causing a recession. Furthermore, Fed New York President John Williams said last week that highlighted the decline in inflation and an improving economic balance.

Looking ahead, market participants await the Australian Confidence surveys due later on Tuesday. The Westpac Consumer Confidence is expected at 0.6%. The NAB Business Confidence Index is expected to drop to 1 in August, up from -2 in July. Later this week, the US Consumer Price Index (CPI) on Wednesday and the Producer Price Index (PPI) on Thursday will be released. Traders will take cues from these figures and find the trading opportunity around the AUD/USD pair.

- The USD/JPY inverts currency flows as the Yen rises and the greenback steps down.

- The BoJ could be on track to reverse negative rates, sending JPY back up the charts.

- USD traders will be looking towards US CPI figures on Wednesday.

The USD/JPY saw declines in one of the worst-closing trading days since July, finishing Monday near 146.50 after opening the new trading week on the high side near 147.85. The Japanese Yen (JPY) is seeing fresh bidding in the market on the back of bullish comments from the Bank of Japan (BoJ), and the Greenback (USD) is sliding across the board as profit-taking from the recent bull run saps momentum for the US Dollar.

Yen gaining ground on BoJ hints of future rate policy reversal

Weekend comments from the BoJ’s Governor Kazuo Ueda hinted that the Japanese central bank is inching closer to reversing its negative rate policy. In an interview with the Yomiuri Shimbun newspaper on the weekend, BoJ Governor Ueda expressed that the end of the year could see a shift in negative rates from the Japanese central bank, as long as data supports the view that the BoJ is on track to achieve their 2% annual inflation target.

Markets seized upon the statements, sending the Yen to fresh highs across the board in anticipation of the beginning of a long-awaited rate hike cycle from the BoJ. On the US Dollar side, Greenback traders are taking a step back ahead of key US inflation figures due in the midweek.

US Consumer Price Index (CPI) figures are due on Wednesday, with market forecasts calling for the headline CPI to print at 0.5% MoM, an uptick from the previous period’s 0.2%. Core CPI numbers are expected to hold steady at 0.2%, and deviations in inflation figures could see rapid changes in the market’s USD bias to close out the trading week.

USD/JPY technical outlook

The Dollar-Yen pairing swooned below the 146.00 handle in early Monday trading, recovering to 147.00 before settling at the midpoint near 146.50. Last week saw the pair knocking on the ceiling just above 147.80, but fresh JPY bidding coupled with the USD step back has taken the pair off the highs, and a technical recovery will need to first gather steam from the resistance-turned-support barrier near 146.40.

A new rising trendline on daily candles will see dynamic support if current consolidation continues, and bulls will be looking for an upshot from US CPI data on Wednesday.

USD/JPY daily chart

- XAU/USD secured daily gains on Monday and closed above $1,920.

- The daily chart flashes mixed signals, and there is not a clear dominant for the short term.

- As long as the price remains above $1,920, the outlook will be bright.

The Gold Spot price closed at $1,922 in Monday's session, tallying a 0.18% daily increase. Thanks to weaker US Dollar, precious metals were allowed to gain some traction, but the US Treasury yields, which remain high, halted all attempts to make a significant upward movement.

On the technical front, the daily chart indicates a neutral, with a slight bullish bias in favour of the Gold's buyers. The Relative Strength Index (RSI) displays an ascending slope in the bearish territory, hinting at a potential trend reversal of the recent bearish movements. At the same time, the Moving Average Convergence (MACD) prints lower green bars, which signifies that despite bulls gaining some ground, their momentum is relatively weak. In addition, on the bright side, the pair is holding above the 20 and 200-day Simple Moving Average (SMA) convergence at the $1,915-1,920 and as long as the buyers keep this level, the downside will be limited. However, the bulls still have more work to do and must target the 100-day SMA at $1,950 to gather momentum and continue breaking resistances. Above the 100-day average, the following targets are $1,970 and $1,990.

XAU/USD Daily chart

-638300663119776961.png)

}

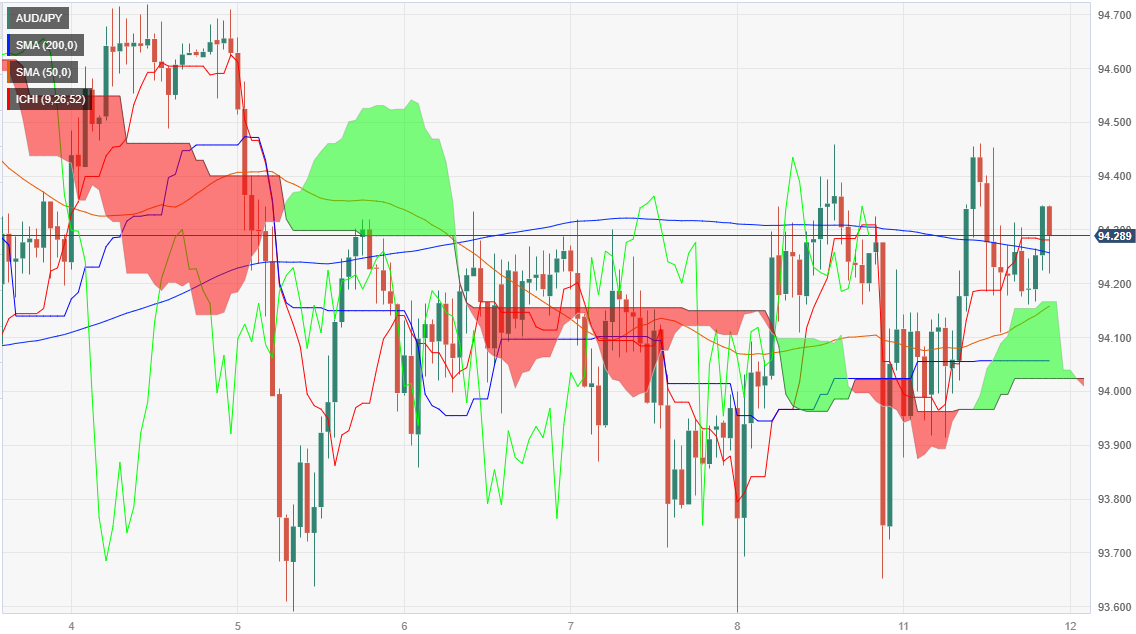

- AUD/JPY trades at 94.22, almost flat as Tuesday's session begins.

- BoJ Governor Kazuo Ueda hints at the end of negative interest rates, sparking short-lived gains in JPY.

- Technical indicators suggest a neutral bias, with both buyers and sellers awaiting a fresh catalyst.

The Australian Dollar (AUD) posted minuscule gains on Monday versus the Japanese Yen (JPY), after the Bank of Japan (BoJ) Governor Kazuo Ueda made comments that the end of negative interest rates is possible if data warrants it. Hence, market participants priced in a possible monetary policy normalization as the JPY registered solid gains. Nevertheless, they were short-lived, as shown by the AUD/JPY pair. At the time of writing, the cross trades at 94.22, almost flat, as Tuesday’s session begins.

AUD/JPY Price Analysis: Technical outlook

The daily chart portrays the pair as neutral biased, with no clear bias, as the pair forms a symmetrical triangle preceded by a downtrend. Also, the Senkou Span A and B lines that form the Ichimoku Clous (Kumo) and the Tenkan and Kijun-Sen are flat. That said, neither buyers nor sellers are in charge, awaiting a fresh catalyst that directs the AUD/JPY pair.

From an hourly chart perspective, the pair finished Monday’s session near the session’s highs, suggesting an upward bias. Hence, the AUD/JPY first resistance would be the September 11 high at 94.45, followed by the September 4 swing high at 94.70, before challenging 95.00. Conversely, the first support would be the top of the Kumo at 94.10, followed by the 94.00 figure. A breach of that area would shift the bias downwards.

AUD/JPY Price Action – Hourly chart

- US equities broadly caught a bid during Monday trading.

- Tesla price target, Hostess deal highlights of US trading.

- Cars and junk food keep the major index in the green as Raytheon sees unexpected costs accumulate.

The Standard & Poor’s (S&P) 500 US mega index is seeing moderate gains to close out Monday’s trading, up around 0.35% near $4,490.00. The major US index is seeing the beginnings of a potential recovery after backsliding from $4,540.00 to last week’s low of $4,430.00.

US equities are getting a lift from the tech sector in Monday’s trading as market investors await key Consumer Price Index (CPI) inflation figures due in the midweek, where headline consumer inflation is expected to tick upwards to 0.5% MoM, compared to the previous period’s 0.2%. Meanwhile, Core CPI data is forecast to hold steady at 0.2%.

S&P juiced by tech stocks, limited losers help bolster index

The S&P was led higher by a few notable performers, including Tesla and Hostess, the maker of Twinkies.

Tesla (TSLA) shares lifted 9.3% after the stock saw its stock upgraded from equal weight to overweight by Morgan Stanley, who also raised their price target for the electric carmaker’s stock from $250 per share to $400.

Hostess Brands gapped higher by 19% when equity markets discovered that the company famous for Twinkies would be acquired by JM Smucker (SJM), with the jellies manufacturer acquiring the mass-produced pastries company in a cash and stock deal that values the company at $34.25 per share.

Stocks holding the back include the stock ticker RTX (RTX) formerly known as Raytheon Technologies, which tumbled 7% after it was revealed it would cost the company around $3 billion dollars to fix metal powdercoats used in the fabrication of engine parts for the Airbus A320 jetliner.

S&P 500 technical outlook

In the near term, the S&P equity index is somewhat hamstrung, floating between the latest turning points between $4,530.00 and $4,430.00, but long-term momentum rests firmly in the hands of the bulls. The index has steadily lifted the year’s opening prices of $3,845.00, but a significant downturn will see a notable lack of technical support levels on its way down to $4,360.00.

S&P 500 daily chart

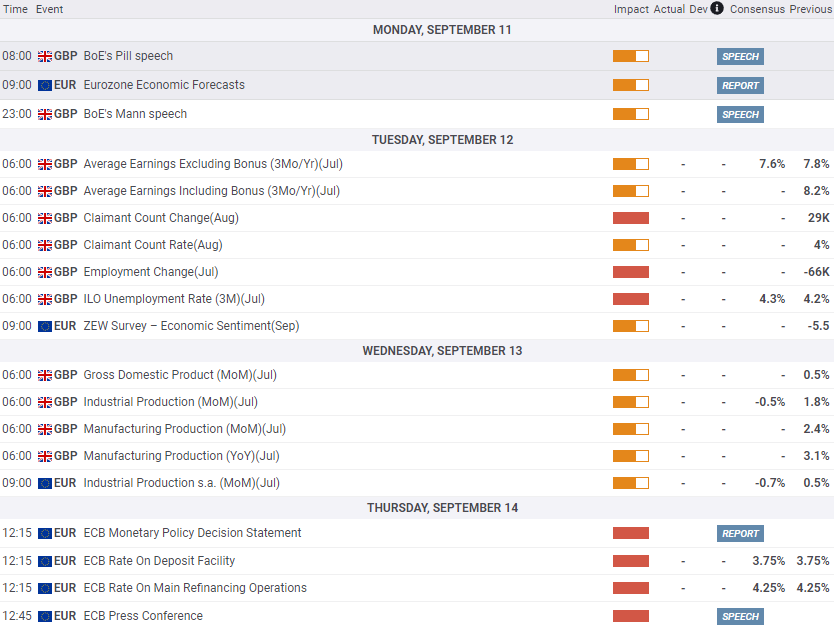

During the Asian session, New Zealand will report Electronic Card Retails Sales data and Australian Confidence surveys are due. Later in the day, the key reports will be the UK employment data and the German ZEW survey.

Here is what you need to know on Tuesday, September 12:

The positive streak of the US Dollar Index (DXY) finally ended after several consecutive days of gains. The pullback was triggered by some improvement in risk sentiment. The Nasdaq increased by 1.14%, while the S&P 500 climbed 0.67%. As a result, the DXY retreated from above 105.00 to 104.55. US Treasury yields moved sideways, with the 10-year yield hovering around 4.28%.

The US Dollar's direction could remain uncertain as key US economic reports are awaited. The Consumer Price Index (CPI) on Wednesday and the Producer Price Index (PPI) on Thursday will provide more inflation data. These figures will be crucial in shaping expectations for the September 19-20 Federal Open Market Committee (FOMC) meeting.

Analysts at TD Securities on US CPI inflation:

Our forecasts for the CPI report suggest core price inflation likely remained subdued in August: We expect it to print 0.2% m/m for a third consecutive month. We also look for a larger 0.6% gain for the headline, as gasoline prices surged. Importantly, the report is likely to show that the core goods segment stayed deflationary, while shelter-price gains probably slowed. Note that our unrounded core CPI inflation forecast is 0.20%, so we see balanced risks around any surprises in August.

EUR/USD reached a six-day high and is currently consolidating around 1.0750. The bias for the upcoming Asian session is tilted towards the upside, but the overall trend still remains to the downside. The German ZEW survey will be released on Tuesday. The focus is on the European Central Bank (ECB), which will have its monetary policy meeting on Thursday.

"I would rather err on the side of over-tightening, " said Catherine Mann from the Bank of England on Monday. GBP/USD rose for the second time in the past eight days, reaching the 1.2550 area. The rebound occurred near the 200-day Simple Moving Average (SMA). On Tuesday, the UK will release employment data, followed by monthly GDP figures on Wednesday.

The Japanese Yen soared during the Asian session following Bank of Japan's Governor Ueda's comments, stating that interest rates could rise by year-end if wages rise enough. USD/JPY dropped below the 146.00 level and reached levels under the 20-day SMA but then rebounded to the 146.50 area.

USD/CAD declined for the second consecutive day, reaching weekly lows near 1.3550. The outlook could turn bearish in the short term if prices stay below the 20-day SMA, which stands at 1.3575.

AUD/USD rose above 0.6400, boosted by the weaker Dollar and a rebound in commodity prices. NZD/USD climbed above 0.5900, extending its recovery from multi-month lows. The outlook for Antipodean currencies has improved, and positive market sentiment suggests further gains are likely.

Metals experienced a pullback during the American session but finished higher. Silver closed above $23.00, and Gold finished near $1,920, far from the daily high of $1,931.

Like this article? Help us with some feedback by answering this survey:

- EUR/JPY fell to a low near 156.60, it lowest since early August.

- Governor Ueda pointed out that a pivot may come by year’s end.

- Markets are still deciding whether the ECB will hike on Thursday or not.

On Monday, the EUR/JPY traded in the 156.60 - 157.55 range. On the one hand, the Japanese Yen is trading with gains against most of its rivals, including the USD, GBP, AUD, etc., mainly driven by a rise in Japanese Government Bond yields after Bank of Japan (BoJ) comments on monetary policy. On the other hand, the Euro is trading soft as investors gear up for the European Central Bank (ECB) decision on Thursday.

The Japanese Yen is one of the top performers in the session, mainly driven by Governor Ueda’s comments during the Asian session. He pointed out that the Bank of Japan (BoJ) may gather enough evidence by the year's end to know whether the economy is ready to pivot to a contractive monetary policy. That being said, he still believes wages and inflations are not meeting the bank’s forecasts. However, if they sustainably grow for the rest of this year, the bank would consider leaving behind the negative interest rates policy.

The 2- and 5-year JGB yields rose to their highest level since January, while the 10-year JGB rate broke above the 0.70% level.

On the EUR side, markets await the ECB’s decisions on Thursday. The expectations are mixed as the World Interest Rates Probabilities (WIRP) tool suggests that markets discount nearly 40% odds of a 25 basis point hike and analysts predict that the decision will be a close call. In addition, Lagarde’s tone and the ECB’s statement will be closely watched for investors to look for clues regarding forward guidance.

EUR/JPY Levels to watch

The technical analysis of the daily chart points to a neutral to bearish outlook for EUR/JPY, indicating the potential for further bearish movement. The Relative Strength Index (RSI) signals a bearish sentiment with a negative slope below its midline, while the Moving Average Convergence (MACD) histogram presents larger red bars. Furthermore, the pair is below the 20-day Simple Moving Average (SMA) but above the 100 and 200-day SMAs, indicating that the buyers still hold momentum on the bigger picture, dominating the sellers.

Support levels: 156.60, 156.00, 155.00.

Resistance levels: 157.00, 158.25 (20-day SMA), 159.00.

EUR/JPY Daily Chart

-638300629341746898.png)

- BoE MPC member Catherine Mann suggests it’s too soon to end the tightening cycle.

- Upcoming UK employment report and US inflation data could be key drivers for the pair.

- BoJ Governor Kazuo Ueda’s hawkish comments also influence the market sentiment.

The Pound Sterling (GBP) posts modest gains versus the US Dollar (USD) late on Monday’s North American session after seesawing in an 80-pip range, though it stays afloat above the 1.2500 figure. The GBP/USD is trading at 1.2510, gains 0.37%.

Pound gains modestly against the US Dollar, buoyed by improved market sentiment and comments from BoE's Catherine Mann

The GBP/USD recovered some ground amidst an improvement in market sentiment spurred by upbeat economic data from China and hawkish comments by the Bank of Japan (BoJ) Governor Kazuo Ueda. Ueda stated the BoJ would look to end its ultra-loose monetary policy quietly and added the BoJ would end the period of negative rates if there’s a shift in data.

In the meantime, the Bank of England (BoE) MPC member Catherine Mann stressed that it’s too soon for the BoE to end its tightening cycle and added that she “would rather err on the side of over-tightening” than the opposite. Mann said she wouldn’t hesitate to cut rates if the BoE overshoots.

Interest rate probabilities show the BoE’s chances for a 25 bps rate hike at 79%, ten days before Andrew Bailey and Co. release their decision. Following their decision in September, money market futures expect no more rate increases compared to last week’s projections, with swaps pricing in 20 bps of increases for March 2024.

Although it should be positive for the GBP/USD exchange rate, the August UK employment report on Tuesday could shift the pair’s direction. The projections foresee a mixed report, with the labor market expected to contract by -80Kj obs, while the Unemployment rate would tick higher.

Recently, a New York Fed Poll showed that Americans are seeing inflation a year from now at 3.6%., up from July 3.5%, while forecasts for three years dropped to 2.8% vs. 2.9% on the previous poll. The same survey indicated that households struggle to access credit, and predicted it would be more challenging in the months ahead. Given that backdrop, it could be a prelude to retail sales, which would be revealed late in the week.

On the US front, the US economic agenda would feature inflation data, which is expected to climb above July’s numbers, except for the core Consumer Price Index (CPI), at 4.3% YoY, down from 4.7%. Any upward surprises in the data could trigger a reaction by the US Federal Reserve, which is expected to keep rates on hold for the September meeting.

GBP/USD Price Analysis: Technical outlook

From a technical standpoint, the GBP/USD reversed its downtrend shy of challenging the 200-day Moving Average (DMA) at 1.2426 and rose above the 1.2500 figure. However, the lack of strength to lift prices toward the June 20 daily low turned resistance at 1.2590, leaving the pair at a brisk for further downside. A drop below 1.2500 could expose the 200-DMA, followed by the 1.2400 figure.

- The USD/CAD is seeing a sell-off on possible profit-taking volumes.

- Resistance is being provided by a rising trendline on daily candles.

- Rising oil prices on supply constraint worries providing a floor on extended Loonie losses.

The USD/CAD pair has taken a step lower for Monday, slipping from 1.3640 into the 1.3580 level, with the Greenback (USD) on the back foot as the USD gives up some of its recent gains across the broader market.

Monday has been a light day for major market catalysts on the US Dollar side, but recent bouts of risk-off market sentiment that sent investors scurrying into the Greenback on global economy concerns could be seeing some profit-taking.

The week is far from over, however, and Wednesday will see US Consumer Price Index (CPI) data dropping on mid-week markets. Headline CPI for the month of August is forecast to come in higher at 0.5% compared to the previous read of 0.2%, representing an uptick in inflationary pressures, while the core CPI figure for the same figure is forecast to hold steady at 0.2%.

Oil prices rise as supply concerns evolve, could support CAD as trading week continues

The Loonie (CAD) has been supported by bolstered crude oil prices of late, with extended oil production cuts from both Russia and Saudi Arabia extended into the end of the year, and continued oil supply constraint concerns are building a hard floor underneath the CAD.

Despite this, the USD/CAD pairing is holding on the upside for September, still well above the month’s opening prices near 1.3510. The Dollar-Loonie rate saw a firm lift into the 1.3690 region on soured risk appetite, but action is steadily declining into a comfortable zone near 1.3580.

USD/CAD technical outlook

Further upside will be capped by firm resistance from the 1.3600 major handle, while any extensions to the downside will see a bit of a support vacuum until facing a near-term floor at 1.3500.

USD/CAD 4-hour chart

- USD/NOK fell below the 20-day SMA towards the 10.6150 area.

- Norwegian CPI from August came in soft.

- Investors await US inflation figures on Wednesday.

At the start of the week, the USD/NOK lost the 20-day Simple Moving Average (SMA) near 10.6150 and then settled around 10.6470. Despite Norway reporting soft inflation data, the pair movements are explained by a US Dollar (USD), which is experiencing weakness across the board.

After last week’s sharp gains, the US is tallying losses against most of its rivals, including the USD, JPY, EUR and GBP, and investors seem to be taking profits. No relevant data will be released during the session, and all eyes are on Wednesday’s Consumer Price Index (CPI) from August, which is expected to have accelerated. Regarding expectations on the Federal Reserve (Fed), markets already priced in a pause in next week’s meeting. However, the odds of one last hike remain high in November and December, according to the CME FedWatch tool.

On the NOK’s side, August’s CPI from Norway came in at 4.8% YoY, lower than the expected and previous figure of 5.4%. The Norges Bank stated in its last meeting that it still has more ground to cover and will likely hike in the September meeting and a hawkish stance may provide further cushioning to the Norwegian currency.

USD/NOK Levels to watch

Analysing the daily chart, it is apparent that the USD/NOK has a neutral to bearish technical stance, with the bears gradually recovering. The Relative Strength Index (RSI) points downwards in the bullish territory, suggesting a possible trend reversal, while the Moving Average Convergence (MACD) histogram presents rising red bars. Moreover, the pair is below the 20-day Simple Moving Average (SMA), but above the 100 and 200-day SMAs, indicating that the buyers still hold momentum on the bigger picture, dominating the sellers.

Support levels: 10.5900 (100-day SMA), 10.5000, 10.4000 (200-day SMA).

Resistance levels: 10.6500 (20-day SMA), 10.7000, 10.7500.

USD/NOK Daily Chart

- European equity markets see slight gains on Monday as risk appetite improves cautiously.

- London's FTSE index lags behind its European counterparts but manages to eke out a green printing.

- Mixed economic data continues to plague European risk sentiment, and the economic calendar represents an uphill climb.

European indexes are closing off their Monday trading sessions broadly higher on the day, though recent swings in risk sentiment have soured the potential for upside momentum.

FTSE lags European indexes, but chalks in a slight gain

London’s Financial Times Stock Exchange (FTSE) 100 index is mostly flat for Monday, ending the trading day near £7,513.00, only a few points above the day’s opening bids of £7,505.00. The day saw back and forth action that failed to generate meaningful moves in either direction as United Kingdom (UK) equities grapple with a dovish Bank of England (BoE) mired in softening economic data for the UK economy.

Across the Channel, European markets were notably firmer, with the Eurostoxx 50 blue chip index and Germany’s DAX index both closing higher for the day. The Eurostoxx 50 opened the day near €4.240.00, reaching an intraday high of €4,279.00 before ending the trading day nearby at €4,264.00.

Germany’s DAX saw similar upside momentum, opening at €15,743.00 and reaching a peak of €15, 851.00 in early Monday trading before giving up half the day’s gains to settle near the €15,800.00 level.

European equities will be looking to establish a foothold and mount moves higher after succumbing to declines in broader market sentiment in recent weeks. However, the upside sees increasing difficulties as resistance levels consolidate just above.

Eurostoxx 50 technical outlook

The Eurostoxx 50 index sees a grouping of resistance levels from late August’s peak near €4,340.00, and risk-off flows saw the index slump to familiar lows near €4,180.00. Things are currently hung in the middle as bulls and bears fight to a standstill at familiar levels that have plagued the index for seven months.

Eurostoxx 50 chart

- USD/CHF trades at 0.8908, unable to break the 0.9000 level.

- 50 and 200-day Moving Averages (DMAs) indicate a lack of trend, staying flat at 0.8774 and 0.9048, respectively.

- Short-term, technical outlook suggests a neutral to bearish bias, with key support level at around 0.8900.

The Greenback (USD) losses ground versus the Swiss Franc (CHF) after developments during the Asian session weakened the former. China’s positive data, mainly inflation back at positive territory, and hawkish words from the Bank of Japan (BoJ) Governor Kazuo Ueda spurred USD weakness. Hence, the USD/CHF is trading at 0.8908 after hitting a daily high of 0.8926.

USD/CHF Price Analysis: Technical outlook

During the last four trading days, the USD/CHF has remained at around the 0.8900 figure, unable to threaten the 0.9000 figure, as volatility keeps the pair consolidating at around a 40 pip range. It should be said the 50 and 200-day Moving Averages (DMAs) turned flat, with the former below price action at 0.8774, while the latter stays at a bearish position at 0.9048, indicating the lack of a trend. However, price action shows a higher series of peaks and throughs but at the expense of an increase in volatility that could break the trading range.

The USD/CHF one-hour chart portrays the pair as neutral to bearish biased, as price action sits below the 50-hour Simple Moving Average (SMA) at 0.8916. However, to reinforce the bias, sellers must crack the September 8 daily low of 0.8895 to challenge the next support area, seen at the September 6 daily low of 0.8881. Once cleared, the next stop would be the 200-hour SMA at 0.8871, followed by the September 5 low of 0.8819. Contrarily, the first resistance is seen at the 50-hour SMA at 0.8916, followed by the September 8 daily high of 0.8936.

USD/CHF Price Action – Hourly chart

- The Aussie is shifting higher after China bullies markets on CNY speculation.

- Upside capped by recent downswings, but there's room to run if sentiment holds.

- Australian unemployment data in the mid-week could help or hurt depending on market sentiment.

The AUD/NZD caught a bump on Monday, trading into the 1.0870 region after kicking the trading week off near 1.0840. The Aussie (AUD) has caught a minor lift back into familiar territory after drifting to a medium-term low near 1.0820 late last week, getting bolstered by improving risk sentiment from China.

Chinese authorities are hitting markets with strong talking points early in the week, essentially warning market participants that they should “voluntarily maintain a stable market” and avoid excessive speculation trading.

Aussie getting dragged higher by up-step from China

The Renminbi (CNY) saw a much stronger fix than usual, and the upside momentum for the Chinese currency is dragging the Aussie higher, with Australia taking pride of place as China’s largest trading partner.

Things are light on the Kiwi (NZD) side, and changes in market dynamics will rest firmly in the hands of AUD traders for the week. The data point of note for the Aussie this week will be unemployment figures due on Wednesday, which markets are broadly expecting to hold steady at 3.7%.

AUD/NZD technical outlook

The Aussie-Kiwi pairing is holding steady in consolidation territory just below the 1.0880 level, but the floor has been sagging in recent days, and each downturn for the AUD sees fresh lows. Chart action is now tapping into a declining trendline baked into the 4-hour candles, and a turnaround from this region will see new bearish challenges of the 1.0820 handle.

On the bullish side, a fresh break to the high side will see significant action around the 1.1000 major psychological level, a region from which the Aussie faced rejection seven weeks ago. Meanwhile, a rough wedge on the daily candles is running aground of consolidating support from the constrained 50-day EMA and 100-day SMA.

AUD/NZD 4-hour chart

- Positive inflation data from China, Australia’s largest trading partner, lifts the Aussie Dollar.”

- Bank of Japan Governor Kazuo Ueda hints at ending negative interest rates, weakening the US Dollar and boosting the AUD.

- Upcoming Australian economic data includes Westpac Consumer Confidence and NAB Business Confidence.

The Australian Dollar (AUD) climbs sharply against the US Dollar (USD) during the North American session on positive news from China ahead of Aussie’s economic data release. That, alongside a risk-on impulse, keeps the AUD/USD trading with gains of 0.97%, exchanging hands at 0.6436 after hitting a daily low of 0.6376.

Australian Dollar gains nearly 1% against the US Dollar as upbeat Chinese inflation data and a risk-on market mood boost the currency

The Greenback retraces on Monday due to an upbeat market mood, but also on comments from a top official of the Bank of Japan (BoJ). That and China’s data portraying the economy as exiting from a deflationary scenario spurred a rally in global equities.

BoJ Governor Kazuo Ueda hinted the BoJ could finish its era of negative interest rates, spurring a reaction on Japanese Yen (JPY) shorts, weakening the US Dollar, and sparking JPY gains by close to 1%.

Aside from this, the Aussie Dollar (AUD) was bolstered by China’s inflation report, with the Consumer Price Index (CPI) for August expanding by 0.1% YoY following a -0.3% number in July, while on a monthly basis, raised more than July’s data.

It should be said that amid the lack of economic data revealed by Australia and the United States (US), China is Australia’s largest trading partner and usually weighs on the former due to that condition. Even though Chinese authorities increased stimulus, the People’s Bank of China. (PBoC) cut interest rates; the economy remains weaker as the services sector continues deteriorating.

Therefore, upbeat developments in China could underpin the Australian Dollar (AUD), which is sensitive to the former economic developments.

The Australian economic agenda would feature consumer and business confidence. The Westpac Consumer Confidence is expected at 0.6% in September. The NAB Business Confidence is foreseen to dip to 1 in August, up from a -2 contraction in July. On the US front, the release of the Consumer Price Index (CPI) for Wednesday, August, would be crucial. Headline inflation is expected to rise above July’s numbers, contrary to core CPI, which is expected to contract further.

If US inflation comes hotter than expected, that would be positive for the USD and negative for the AUD, as it would suggest the Federal Reserve needs to tighten monetary policy. Estimates for the upcoming September meeting remain unchanged, but for the November meeting, chances for higher interest rate increases.

AUD/USD Price Analysis: Technical outlook

From a daily chart perspective, the AUD/USD is ongoing an upward correction after diving toward a year-to-date (YTD) low of 0.6357, but it would need a daily close above the prior week’s high of 0.6521 if buyers would like to remain hopeful of higher prices. A breach of the latter would expose the confluence of the March 10 low and the 50-day Moving Average (DMA) at around 0.6564/74, followed by the 0.6600 figure. Conversely, sellers would extend their losses once they challenge the YTD lows.

- EUR/USD rose to a four-day high of 1.0755.

- ECB’s tightening expectations remain steady ahead of Thursday’s ECB decision.

- Eyes are set on Wednesday’s CPI figures from August from the US.

At the start of the week, the EUR/USD soared towards the 1.0755 area, seeing more than 0.50% gains and then settled near 1.0745. On the one hand, the USD is retreating and trades with losses against most of its rivals while investors are gearing up for Wednesday's Consumer Price Index (CPI) figures from August. On the Euro’s side, investors await Thursday’s European Central Bank (ECB) decisions, where markets discount low odds of a hike.

Recent data from the US showed a mixed labour market outlook with accelerating job creation but wage inflation declining. In contrast, economic activity has shown weakness in the manufacturing sector but a strength in the services area. In addition, despite investors already warranting a pause in next week's Federal Reserve (Fed) meeting, inflation figures from August will be crucial for investors to continue modelling their expectations. The headline CPI is expected to have increased by 0.2% MoM while the Core measure by 0.5%, and hot inflation reading may boost hawkish bets for the November and December meetings.

On the other hand, the Euro is trading soft against most of its rivals ahead of Thursday’s ECB decisions. According to a Bloomberg report, a slight majority of 55 analysts polled are seeing a pause, with 25 seeing a 25 basis point hike. Looking ahead, the chances of a 25 bps increase stand at 60% in the October meeting, followed by a 70% likelihood of a similar increase in December. Investors will closely watch Christine Lagarde’s tone on Thursday and the bank’s statement to look for clues on the next decisions.

EUR/USD Levels to watch

Based on the daily chart, EUR/USD maintains a neutral to bearish technical perspective, suggesting that despite the bulls gaining momentum, the bears are in control. The Relative Strength Index (RSI) holds a positive slope deep in negative territory, while the Moving Average Convergence (MACD) presents stagnant red bars. Moreover, the pair is below the 20,100 and 200-day Simple Moving Averages (SMAs), indicating that the bears are still in command of the broader picture.

Support levels: 1.0700, 1.0680, 1.0650.

Resistance levels: 1.0800, 1.0810-20 (200 and 20-day SMA convergence), 1.0850.

EUR/USD Daily Chart

-638300491564815187.png)

- The EUR/GBP sees recovery from early Monday’s slide, but progress remains limited.

- UK wages, unemployment data to pluck away at the GBP for the early week.

- ECB rate call on the cards will cap the week off with volatility if comments or actions surprise.

The EUR/GBP pairing continues to look for a foothold on the charts, but this week brings key United Kingdom (UK) data and a critical rate call from the European Central Bank (ECB). Showings for both currencies threaten to keep the EUR/GBP pair hamstrung as sentiment drifts back and forth between the two.

UK data coming into view, ECB rate call ahead

The UK faces wage growth, unemployment, and industrial activity figures for the first half of the trading week. Wage figures, while slowly declining, remain elevated. The UK’s Chancellor of the Exchequer Jeremy Hunt noted over the weekend that the Bank of England (BoE) is facing stickier inflation than they previously forecast.

Stubborn inflation issues are partly driven by elevated wage growth, and if figures remain too high for too long it could mire the BoE, making an outright dovish or hawkish stance difficult to maintain.

On the Euro side of the data calendar, the ECB is slated to publish its latest rate call during Thursday’s market session. Market participants are increasingly convinced that the rate hike cycle has peaked in Europe, despite hawkish jawboning from ECB officials recently.

Market forecasts broadly anticipate the ECB to stand pat on rates for September’s meeting, though any nasty surprises from the ECB could throw markets for a loop.

UK-EU economic calendar, Monday through Thursday. All times GMT.

EUR/GBP technical outlook

The Euro (EUR) is looking for a leg up against the Pound Sterling (GBP) in the markets today, trading into a session high of 0.8587. The pair started the trading week on a decidedly softer tone, with the Euro declining to 0.8558 before facing a rally on the back of a waffling GBP.

Longer-term, the pair is looking decidedly constrained, with the EUR/GBP trading into familiar territory for the past three months. The pair refuses to decline any further, marking its territory above the 0.8500 handle, but resistance from a declining 50-day EMA at 0.8585 is capping upside momentum.

EUR/GBP daily chart

- The GBP/JPY sees challenges as the Pound Sterling and Yen play tug-of-war on the charts.

- GBP to feature heavily on the economic calendar for this week, BoJ comments keeping the Yen strung up.

- Market reactions to data will set the direction for the Guppy after weekend BoJ policy statements rile things up.

The GBP/JPY pairing is set to finish the day nearly where it started after Monday market flows saw the Guppy trade back-and-forth on shifting sentiment.

Pound Sterling (GBP) traders are positioning themselves ahead of a United Kingdom (UK) data-heavy economic calendar for the first half of the week, and the Yen (JPY) is finding broad-market support following weekend comments from Bank of Japan (BoJ) officials hinting at the end of negative rates for Japan.

UK data to feature heavily through Wednesday

The GBP will be facing off against the economic calendar through Tuesday and Wednesday; economic data has struggled to meet market expectations as of late, prompting routine sell-offs for the Pound Sterling across the board as data points for the UK’s economy continue to wallow on the low end, prompting particularly dovish showings from the Bank of England (BoE) of late.

Tuesday will see wage growth and unemployment figures, with Wednesday bringing Gross Domestic Product (GDP) numbers, alongside manufacturing and industrial performance.

The UK’s Chancellor of the Exchequer Jeremy Hunt hit the wires on Monday, noting that the UK faces stickier inflation than previously forecast. Due in no small part to still-high wage growth figures, which are expected to show only mild declines this week.

Elsewhere on the docket, Unemployment Rate and Manufacturing figures are expected to worsen, albeit slightly.

GBP economic calendar events, Monday through Wednesday. All times GMT.

The BoJ’s Governor Kazuo Ueda paved the way for speculation about the end of the Japanese central bank’s negative interest rate policy while making comments over the weekend.

During an interview with Yomiuri Shimbun newspaper, Governor Ueda made it very clear that any changes in the BoJ’s rate policy will depend on data showing the BoJ is approaching its 2% inflation target.

This follows soft comments from other BoJ officials last week, meant to target the Yen and discourage further declines in the Japanese currency in an echo of similar activities around this time last year that saw the Japanese central bank conducting open market operations to defend the declining Yen. Prior to that, the BoJ had not conducted open currency market operations since the late 90s.

GBP/JPY technical outlook

Current action sees the Guppy trading into the middle where markets kicked off on Monday, reaching an intraday low of 182.68 before recovering to make a run to 183.90, and is currently settling somewhere in the middle ground.

The Pound Sterling may have finally slipped the 184.00 major handle, a significant psychological level in recent trading history, and a continued slide down will see the GBP/JPY pair challenging old support levels from 181.00 to 180.00. On the bullish side, a fresh break upwards will see challenges from 185.60 to 186.60.

GBP/JPY Daily chart

- WTI trades at $86.62, bolstered by Saudi Arabia and Russia’s commitment to cut production by 1.3 million barrels until year-end.

- Positive economic data from China and potential end of negative interest rates in Japan support oil prices.

- Upcoming US CPI data could influence WTI prices, as they may signal further rate hikes.

Western Texas Intermediate (WTI), the US crude oil benchmark, remains steady at around yearly highs on supply oil cuts, while recent data from China painted a positive outlook in the global second largest economy. WTI is trading at $86.62 after hitting a daily high of $87.61.

US crude oil benchmark remains buoyant as Saudi-Russian supply cuts and upbeat Chinese economic outlook offset potential headwinds from central banks

Oil prices will likely remain underpinned by the supply cuts established by Saudi Arabia and Russia, which committed to slashing production by 1.3 million barrens combined until the end of the year.

Meanwhile, upbeat economic data from China from a deflationary scenario improved investors’ sentiment toward its economic recovery, a tailwind for global oil prices. That, alongside words from the Bank of Japan (BoJ) Governor Kazuo Ueda mentioning a possible end for negative interest rates, underpinned the US Dollar, which is downward pressured, changing hands below the 105.00 figure, as reported by the US Dollar Index (DXY).

Another factor that keeps the WTI price afloat is storms and floods in Eastern Lybia, which triggered the closure of four major oil export ports since Saturday.

In the meantime, a tranche of macroeconomic data could dent oil’s demand, as a major central bank and inflationary data from the US could warrant further tightening is needed. The European Central Bank (ECB) will announce its monetary policy decision on Thursday. A day earlier, the US would reveal the Consumer Price Index (CPI), which could undermine WTI price on expectations for additional rate hikes by the US Federal Reserve if it comes above estimates.

Aside from this, data from the International Energy Agency (IEA) and the Organization of the Petroleum Exporting Countries (OPEC) is due this week. Last month, the former cut its 2024 oil demand growth to 1 million barrels per day, while OPEC kept its 2.25 million barrels per day demand growth projection unchanged.

WTI Price Action – Daily chart

WTI Key Technical Levels

- XAG/USD jumped back above $23.000 and hit a daily high of $23.15

- The USD is trading softer, but US yields remain high.

- All eyes are now on Wednesday’s US CPI from August.

On Monday, precious metals are recovering ground after seeing sharp losses last week, with the Gold and Silver prices seeing daily gains. The XAG/USD stands at $23.00 and failed to maintain its momentum, which took the price to $23.15, depicting that the bears have the upperhand and limit any attempt of the buyers to make a significant upward movement.

A softer USD consolidating last week’s gains could explain the daily advance. However, US Treasury bond yields, often seen as the opportunity cost of holding non-yielding metals, are rising ahead of Wednesday’s inflation figures from the US and limiting the upside for the grey metal. Markets expect that inflation accelerated in August, with the Headline and Core Consumer Price Index (CPI) advancing by 0.5% and 0.2% MoM, respectively.

In line with this, the 10-year bond yield reached 4.29%, up by 0.87%. The 2-year yield stands neutral at 4.99%, while the 5-year yield rose to 4.42%, seeing 0.48% gains. It's worth noticing that US yields remain high as, according to the CME FedWatch tool, markets are discounting high odds of one last hike by the Federal Reserve (Fed), and as long as hawkish bets are high, the upside potential for metals is limited.

XAG/USD Levels to watch

Based on the daily chart, a bearish stance is noted for XAG/USD in the short term. The Relative Strength Index (RSI) is comfortably situated in negative territory below its midline, displaying a southward slope. In addition, the presence of red bars on the Moving Average Convergence Divergence's (MACD) histogram further reinforces the strengthening bearish sentiment. On the other hand, the pair is below the 20,100 and 200-day Simple Moving Averages (SMAs), and cofirms the continued dominance of bears on a broader scale.

Support levels: $22.60, $22.30, $22.00

Resistance levels: $23.50 (20 and 200-day SMA convergence), $23.70, $24.00.

XAG/USD Daily Chart

-638300437923837729.png)

The recent decline of the GBP/USD pair was driven mostly by US Dollar strength rather than the decline in Bank of England rate hike expectations, noted analysts at Rabobank. They see scope for the pair to slide toward 1.23 on a three month perspective.

Key quotes:

While GBP was impacted last week by the decline in rate hike expectations, we would argue that it is USD strength which has been the real force behind the softer tone in cable in recent weeks. The USD is the best performing currency on a 1-month view on the back of the resilience of the US economy and the suspicion that the Fed will have to maintain higher rates for longer.

Slower growth in China and in Europe is bad news for risk appetite. This too is USD supportive. We expect the USD to remain well positioned on a 3-to-6-month view until the market begins to look ahead to Fed rate hikes. This suggests that cable is likely to struggle to regain recovery lost ground. We forecast cable at 1.23 in 3 month and at 1.24 in 6 months.

- USD/MXN drops 0.71% to 17.4624, influenced by a softer US Dollar Index, which declines 0.49% to 104.530 despite rising US bond yields.

- Mexican Industrial Production shows modest growth, while Finance Ministry’s optimistic GDP projections draw skepticism.

- US CPI data for August in focus, expected to rise YoY, potentially reinforcing the Fed’s ‘higher for longer’ rate stance.

The Mexican Peso (MXN) took advantage of a softer US Dollar (USD) on Monday, ahead of the release of inflation figures in the United States (US). The exchange rate traveled as high as 17.5927 before retracing on investors seeking risk. That and Asian central banks propelling their local currencies weakened the USD. The USD/MXN is trading at 17.4624, down 0.71%.

Mexican Peso gains ground against a weakening US Dollar as investors await key US inflation data and weigh Mexico’s economic outlook

Comments by the Bank of Japan (BoJ) Governor Kazuo Ueda prompted investors to close short positions on the Japanese Yen (JPY), spurring weakness on the Greenback. Also, China’s strict scrutiny on US Dollar buying by domestic companies was capped under $50 million, with purchases at or above that amount requiring approval by the People’s Bank of China (PBoC) central bank.

Consequently, the US Dollar Index (DXY), which measures the buck’s performance against a basket of peers, drops 0.49% and sits at 104.530, a headwind for the USD/MXN. This is despite the recent uptick in US bond yields, with the 10-year benchmark note rate gaining three basis points at 4.296%.

Meanwhile, data from Mexico showed that Industrial Production rose by 4.8% in July, a tick lower than the upward revised June figures at 4.9% YoY, while on a monthly basis, decelerated to 0.5% from 0.6% in June.

In other news, the Mexican Finance Ministry projects Mexico to grow between 2.5% and 3.5%, seen as optimistic by analysts. Sources quoted by El Financiero said the forecast is far from the 1.7% consensus and 1% above the Bank of Mexico (Banxico) 2.1% projection.

The economic package in Mexico for 2024 proposes an increase in the fiscal deficit from 3.3% to 4.9% of GDP in 2023, the largest negative balance in 36 years. An analyst cited by El Financiero said, “It is irresponsible to project a deficit, especially when the economy is growing.”

Aside from this, the US economic agenda is scarce on Monday, but it would gather pace on Wednesday with the release of the Consumer Price Index (CPI) for August. Data is expected to rise compared to July’s numbers, meaning the US Federal Reserve (Fed) would need to keep rates higher for longer. The consensus estimates the CPI to rise 3.6% YoY from 3.2% in July. Core CPI is foreseen to slow from 4.7% to 4.3%

USD/MXN Price Analysis: Technical outlook

After printing three consecutive sessions failing to crack above 17.8000, the USD/MXN is retreating toward the September 8 low of 17.4380, which could pave the way for further losses once broken. The 100-day Moving Average (DMA) at 17.2658 emerges as the next support, followed by the 20-DMA at 17.0967 and the 50-DMA at 17.0084. Conversely, if the pair stays above 17.4400, expect further consolidation within the 17.3912-17.7074 before fundamental news triggers a range break.

Catherine Mann, member of the Bank of England’s Monetary Policy Committee, said on Monday that overtightening is easier to fix than not moving interest rates. She added that underestimating the persistence of inflation will lead to overshoot.

Mann delivered a speech at the Canadian Association for Business Economics. She explained that the idea that 3% inflation is close enough can not be the guide for the BoE.

Key takeaways from the speech:

To pause or to hold the policy rate lower for longer risks inflation becoming more deeply embedded, which would then require more tightening in total, to both change inflation itself and to wring-out the embedded inflation that comes from the sustained duration above target. This is why I would rather err on the side of over-tightening. But, if I am wrong, and inflation decelerates more quickly and activity deteriorates more significantly, I will not hesitate to cut rates.

It’s a risky bet that inflation expectations are sufficiently well-anchored and to wait for core inflation to ease down, as this extends the duration way above the target-consistent rate. We need to prepare for a world where inflation is more likely to be volatile in the future, and the neutral nominal rate is likely to be higher than in the past. While these might support a “3% inflation is close enough”, popular in some circles, it cannot be our guide. We need to communicate and act on our commitment to do what is necessary to achieve the 2% target, sooner rather than later.

Market reaction

GPB/USD is trading at the highest level in five days above 1.2500, supported by a weaker US Dollar across the board.

- EUR/USD defends the immediate support of 1.0700 amid a risk-on mood.

- The ECB is expected to keep interest rates unchanged this month due to a weak economy and declining inflation.

- EUR/USD trades in a Symmetrical Triangle chart pattern, which indicates a volatility squeeze.

The EUR/USD pair managed to defend the round-level support of 1.0700 on Monday. The major currency pair broadly struggles for a decisive move as investors await the United States Consumer Price Index (CPI) data for August, which will be published on Wednesday at 12:30 GMT.

S&P500 opens on a bullish note amid a cheerful market mood as investors shift focus to the context that the Federal Reserve (Fed) would not raise interest rates in the remaining year. The US Dollar Index remains under pressure after a nominal improvement in China’s inflation.

On the Eurozone front, investors remain uncertain about the interest rate decision by the European Central Bank (ECB) for September monetary policy. Analysts at Commerzbank a majority of the ECB council members will probably vote for unchanged key rates due to the weak economy and the downward trend in the inflation rate.

EUR/USD trades in a Symmetrical Triangle chart pattern on an hourly scale, which indicates a volatility squeeze. The downward-sloping trendline is plotted from September 6 high at 1.0749 while the upward-sloping trendline is placed from September 7 low at 1.0686.

The shared currency pair remains closer to the 20-period Exponential Moving Average (EMA) at 1.0725 for the past three trading sessions, portraying a sideways performance.

Meanwhile, the Relative Strength Index (RSI) (14) oscillates in the 40.00-60.00, demonstrating a directionless performance ahead of the US inflation data.

Fresh upside bias would appear if the asset delivers a breakout of the neutral triangle September 8 high at 1.0744. A decisive break would send the major toward the horizontal resistances plotted from September 4 high at 1.0809 and September 1 high at 1.0882.

In an alternate scenario, a breakdown below September 7 low at 1.0686 would expose the asset to May low at 1.0635. A slippage below the latter would expose the asset to the round-level support of 1.0600.

EUR/USD hourly chart

-638300382001887116.png)

Analysts at Rabobank see the Brazilian Real depreciating versus the US Dollar over the next months. The forecast USD/BRL at 5.05 by year-end.

Key quotes:

The gains of the BRL and other EM currencies start to dwindle as local central banks start their easing cycle while global interest rates are kept in restrictive mode. A market repricing of looming Fed cuts could erode carry-trade gains even further.

We see the USDBRL trading at 5.05 by end-2023 and 5.15 by end-2024.

IGP-DI accelerates and deflation period ends. IGP-DI general inflation advanced by 0.05% m/m in August, below our and the market's projections (market: 0.13%; Rabobank: 0.19%). Producer inflation back up after seven months. The producer inflation (IPA) component rose by 0.10% m/m (from -0.61% m/m in July). It is the first time IGP-DI posted a positive number in the year.

Next week, the Federal Reserve will have its monetary policy meeting. Market participants anticipate that the central bank will keep rates unchanged. Analysts at Wells Fargo also expect rates to remain unchanged, and they see the economic projections from FOMC members reflecting a more optimistic outlook for the US economy.

Key quotes:

We look for the FOMC to keep its target range for the federal funds rate unchanged at 5.25-5.50% at its meeting on September 20. Most market participants expect rates to remain on hold as well.

The FOMC will release its quarterly Summary of Economic Projections (SEP) at the conclusion of the meeting. We expect that the September SEP will portray a more optimistic outlook for the U.S. economy than the last SEP did in June. Specifically, we look for the FOMC to raise its forecast for real GDP growth this year while also nudging down its outlook for inflation.

We do not think the median dots for 2024 and 2025 will change much, if at all, though some of the highest dots may be reined in a bit.

- NZD/USD shifts auction comfortably above 0.5900 amid improved market sentiment.

- There is a nominal improvement in China’s inflation data but the overall outlook is still vulnerable.

- Investors anticipate that US headline CPI grew at a pace of 0.5% due to a rebound in gasoline prices.

The NZD/USD pair stabilized the auction above the round-level resistance of 0.5900 in the late European session. The Kiwi asset aims to extend upside as the market mood improves amid an ease in China’s deflation risks.

The monthly Consumer Price Index (CPI) expanded by 0.3% in August as expected by the market participants. The expansion pace remained higher than July’s reading of 0.2%. Annual inflation rose to 0.1% from the prior print of 0.3% contraction while investors projected acceleration to 0.2%. Prices of goods and services at factory gates remained in the deflationary phase at -3.0% as projected by investors but improved from July’s figure of -4.4%.

There is a nominal improvement in inflation data but the overall outlook is still vulnerable as households’ demand is quite slim due to slow job growth. Investors hope a series of economic stimulus support from the administration and the People’s Bank of China to boost growth prospects. Premier Li Qiang said this week that China is expected to achieve its 2023 growth target of around 5%.

Meanwhile, the S&P500 is expected to open on a bullish note, following positive cues from overnight futures. The appeal for risk-perceived assets improved while the US Dollar Index (DXY) faced selling pressure. The USD Index finds an intermediate cushion near 104.60 as investors shift focus to the United States inflation data for August, which will be published at 12:30 GMT.

Investors anticipate that US headline CPI grew at a pace of 0.5% due to a rebound in gasoline prices. While core inflation expanded at a steady pace of 0.2%. A surprise upside in the US inflation pace could elevate the odds of one more interest rate hike from the Fed in the remaining year.

- USD/CAD slips below 1.3600 despite nominal recovery in the US Dollar.

- Investors underpinned loonie against the greenback due to surprisingly upbeat Canadian labor market data.

- The market mood could turn cautious ahead of US inflation data, which will be published on Wednesday.

The USD/CAD pair corrects further below the round-level support of 1.3600 in the European session. The Loonie asset weakens despite a recovery attempt in the US Dollar Index (DXY). This demonstrates strength in the Canadian Dollar after upbeat Employment data for August and strength in the oil price due to the tight market.

S&P500 futures have added significant gains in the London session, portraying strength in the appeal for the risk-sensitive assets. Investors’ risk-taking ability improved after inflation in China for August month showed signs of stabilization.

The US Dollar Index (DXY) rebounds after discovering support near 104.50 as investors turn cautious ahead of the Consumer Price Index (CPI) for August, which is scheduled for Wednesday. Headline CPI is seen expanding at a higher pace of 0.5% vs. 0.2% pace, being recorded for July. Core inflation that strips off volatile food and oil prices is seen steady at 0.2%.

A surprise upside in the inflation pace could spoil the market mood and strengthen the US Dollar. Meanwhile, New York Federal Reserve (Fed) Bank President John Williams said last week that inflation is falling and the economy is better balanced, which indicates there is no urgency for an interest-rate increase this month.

The Canadian Dollar strengthened as the labor market data surprisingly outperformed expectations. The Canadian labor market witnessed 39.9K new payrolls in the overall laborforce in August, more than double the expectations of 15K. In July, the labor force witnessed a reduction of 6.4K payrolls. The Unemployment Rate remains unchanged at 5.5% while investors forecasted a higher jobless rate at 5.6%.

Annual Average Hourly Wages rose to 5.2% vs. the former release of 5.0%. Decent wage growth could elevate consumer spending momentum and keep inflationary pressures sticky. This could force the Bank of Canada (BoC) to raise interest rates one more time after pausing them in the last two policy meetings.

- The US Dollar tumbles, portrays a sea of red crosses against all major currencies.

- No focal data points on Monday, which means no catalysts for a turnaround.

- The US Dollar Index falls off its pedestal, finding support momentarily at 104.50.

The US Dollar (USD) tumbles lower this Monday after a surprise intervention from the People’s Bank of China (PBoC). The PBoC held a meeting in Beijing on FX markets and confirmed that it will prevent any “over-adjustment” risk in the Yuan. It fixed its Yuan at 7.2148 USD/CNY where 7.3391 USD/CNY was expected.

Although it will be a very calm Monday in terms of the calendar and no US Federal Reserve speakers scheduled, keep an eye on the US bond market. This Monday three different tenures are set to be auctioned. With plenty of supply to be issued in the markets, US yields might rise again. Remember that bonds are quoted in prices, while yields move inversely to that price. With more supply issued in the markets, prices can drop and yields rise, supporting a stronger US Dollar.

Daily digest: US Dollar two-faced

- Plenty of rumours in the FX markets abound on Monday on the possibility for the Japanese Central Bank (BoJ) to loosen its Yield Curve Control (YCC), which would see its bond yields soaring higher.

- The G20 meeting has not brought any significant headlines or breakthroughs, as most news outlets are focusing on the absence of Russia and China as a telling sign.

- The People's Bank of China (PBoC) has issued again a strong peg for its Yuan against the US Dollar. Additionally, it held a meeting in Beijing to outline an FX strategy in order to avoid speculation on a weakening Yuan. The comments spooked speculators and saw the Yuan strengthening near 1% against the US Dollar.

- In the fallout of those earlier PBoC comments, meeting and fixing, the Greenback lost over 1% as well against the Australian Dollar (AUD/USD) and the Japanese Yen (USD/JPY).

- Equities are looking for direction with no real notable outliers to mention. The only element to mention are the US Nasdaq futures, which are up over 50% in pre-trading.

- The CME Group FedWatch Tool shows that markets are pricing in a 93% chance that the Federal Reserve will keep interest rates unchanged at its meeting in September.

- The benchmark 10-year US Treasury bond yield trades at 4.28% and is steeping again. The same story looks to continue this week with the US Treasury issuing a lot more debt, which causes prices to drop and yields to soar.

US Dollar Index technical analysis: Soft landing

The Greenback is taking a firm step back after falling over 1% against the Yuan, Yen and Australian Dollar. The overall cross for the Greenback is blood red for all its G20 major peers. Nonetheless, the sell-off in the US Dollar Index is notable but remains contained and might ease once the US session opens this week.

The new high to watch is at 105.16, both the high from last Thursday and the six-month high. The US Dollar Index first needs to gain back its lost territory from this Monday and break above the peak of Thursday mentioned here before. From there, the next high is at 105.88, the high of 2023.

On the downside, the 104.50 level already provided support ahead of 104.44. That is the high of August 25th and should act as a pivotal level. Once that gives way, a substantial downturn could take place to 103.03, where the 200-day SMA comes into play for support.

US Dollar FAQs

What is the US Dollar?

The US Dollar (USD) is the official currency of the United States of America, and the ‘de facto’ currency of a significant number of other countries where it is found in circulation alongside local notes. It is the most heavily traded currency in the world, accounting for over 88% of all global foreign exchange turnover, or an average of $6.6 trillion in transactions per day, according to data from 2022.

Following the second world war, the USD took over from the British Pound as the world’s reserve currency. For most of its history, the US Dollar was backed by Gold, until the Bretton Woods Agreement in 1971 when the Gold Standard went away.

How do the decisions of the Federal Reserve impact the US Dollar?

The most important single factor impacting on the value of the US Dollar is monetary policy, which is shaped by the Federal Reserve (Fed). The Fed has two mandates: to achieve price stability (control inflation) and foster full employment. Its primary tool to achieve these two goals is by adjusting interest rates.

When prices are rising too quickly and inflation is above the Fed’s 2% target, the Fed will raise rates, which helps the USD value. When inflation falls below 2% or the Unemployment Rate is too high, the Fed may lower interest rates, which weighs on the Greenback.

What is Quantitative Easing and how does it influence the US Dollar?

In extreme situations, the Federal Reserve can also print more Dollars and enact quantitative easing (QE). QE is the process by which the Fed substantially increases the flow of credit in a stuck financial system.

It is a non-standard policy measure used when credit has dried up because banks will not lend to each other (out of the fear of counterparty default). It is a last resort when simply lowering interest rates is unlikely to achieve the necessary result. It was the Fed’s weapon of choice to combat the credit crunch that occurred during the Great Financial Crisis in 2008. It involves the Fed printing more Dollars and using them to buy US government bonds predominantly from financial institutions. QE usually leads to a weaker US Dollar.

What is Quantitative Tightening and how does it influence the US Dollar?

Quantitative tightening (QT) is the reverse process whereby the Federal Reserve stops buying bonds from financial institutions and does not reinvest the principal from the bonds it holds maturing in new purchases. It is usually positive for the US Dollar.

- Natural Gas rallies in Europe over 8%, while US gas prices lag.

- The US Dollar takes it on the chin as the Chinese Yuan appreciates firmly against the Greenback.

- US Natural gas prices might see spillover from European gas futures and rally higher.

Natural Gas prices are squeezing higher as workers in Australia have started their partial strikes on Friday. The volatility is peaking on the European gas market with European gas futures up over 10% at one point in European trading hours. Prices are set to rally further as from Thursday a full walkout could take place if no accord is being formed.

At the time of writing, Natural Gas is trading at $2.806per MMBtu.

Natural Gas news and market movers

- A big divergence in gas prices from a geographic point of view has emerged with European gas futures rallying nearly 10% to $93.29. It is a fresh monthly high for the month of September.

- Meanwhile, US gas futures were unfazed by the sudden spike in prices on the other side of the Atlantic Ocean. Though traders might see some catch up later this Monday once the US markets opens.

- On Friday, the Baker Hughes Rig Count printed a steady number, residing near an 18-month low. US gas prices might spiral higher as well if the US gas production starts to fall short of demand.

- Several weather projections are pointing to a harsh winter to come for both the US and Europe.

- Norwegian outages are yet again extended with the biggest one, the Troll gas field, extended until September 14th.

- European gas storage is expected to survive the winter and end the season with 44% supply left. Currently, European storage is filled to 93% capacity.

Natural Gas Technical Analysis: Consolidates

Natural Gas is starting to fall in a consolidation pattern where buyers and sellers are being pushed toward each other. Several technical elements such as the 200-day Simple Moving Average (SMA), the ascending trendline and the 55-day SMA are moving toward each other. Once both buyers and sellers have reached their consolidation point, a breakout is due. In this case, it could mean Natural Gas prices rally higher with the Australian strikes creating a shortage of supply.

On the upside, $2.83 needs to be taken out in order for this bounce to gain momentum. Once this rebound materialises, look for the the 200-day Simple Moving Average (SMA) near $2.93. In case price starts to break above there and head higher, $3 will be crucial with the high of September at stake.

On the downside, the trend channel has done a massive job underpinning the price action. The 55-day SMA near $2.72 already provided support ahead of any test on the lower end of the trend channel. In case the 55-day SMA breaks, look for support near $2.66.

-638300236458140745.png)

XNG/USD (Daily Chart)

Natural Gas FAQs

What fundamental factors drive the price of Natural Gas?

Supply and demand dynamics are a key factor influencing Natural Gas prices, and are themselves influenced by global economic growth, industrial activity, population growth, production levels, and inventories. The weather impacts Natural Gas prices because more Gas is used during cold winters and hot summers for heating and cooling. Competition from other energy sources impacts prices as consumers may switch to cheaper sources. Geopolitical events are factors as exemplified by the war in Ukraine. Government policies relating to extraction, transportation, and environmental issues also impact prices.

What are the main macroeconomic releases that impact on Natural Gas Prices?

The main economic release influencing Natural Gas prices is the weekly inventory bulletin from the Energy Information Administration (EIA), a US government agency that produces US gas market data. The EIA Gas bulletin usually comes out on Thursday at 14:30 GMT, a day after the EIA publishes its weekly Oil bulletin. Economic data from large consumers of Natural Gas can impact supply and demand, the largest of which include China, Germany and Japan. Natural Gas is primarily priced and traded in US Dollars, thus economic releases impacting the US Dollar are also factors.

How does the US Dollar influence Natural Gas prices?

The US Dollar is the world’s reserve currency and most commodities, including Natural Gas are priced and traded on international markets in US Dollars. As such, the value of the US Dollar is a factor in the price of Natural Gas, because if the Dollar strengthens it means less Dollars are required to buy the same volume of Gas (the price falls), and vice versa if USD strengthens.

- USD/JPY finds an intermediate support near 146.00 as the impact the BoJ Ueda’s hawkish remark starts easing.

- The USD index corrected from a fresh six-month high near 105.00 Fed policymakers supported keeping the interest rate policy steady.

- Fed Goolsbee said the central bank is aiming to push the economy to a “golden path,”.

The USD/JPY pair discovers support near 146.00 after a vertical sell-off that was inspired by hawkish remarks from Bank of Japan (BoJ) Governor Kazuo Ueda this weekend. The asset finds intermediate support as the impact of discussions about an exit from a negative interest rate stance starts fading.

S&P500 futures generated decent gains in the London session, portraying an improvement in the risk appetite of the market participants. The appeal for risk-sensitive assets improved on Monday as China’s Consumer Price Index (CPI) for August accelerated.

BoJ Ueda said in an interview with Yomiuri newspaper that the BOJ could have enough data by year-end to determine whether it can end negative rates. The achievement of a sustainable inflation target of 2% could allow the BoJ to exit from the decade-long ultra-loose interest rates.

Meanwhile, the US Dollar Index (DXY) corrected a bit after a fresh six-month high near 105.00 on Monday as Federal Reserve (Fed) policymakers supported for keeping the current interest rate policy unchanged for September due to falling inflation and a bleak economic outlook.

Broadly, the US Dollar remains resilient as Chicago Fed Bank President Austan Goolsbee said the central bank is aiming to push the economy to a “golden path,” meaning a situation where inflation recedes without triggering a recession.

Going forward, investors will focus on the US Consumer Price Index (CPI) data for August, which will be released on Wednesday at 12:30 GMT. As per the consensus, headline inflation expanded at a significantly higher pace of 0.5% while core CPI that excludes volatile oil and food prices remained steady against the July pace of 0.2% in both segments.

- Gold price remains sideways as the market awaits US inflation data for further action.

- The US Dollar corrects marginally, while the broader bias remains bullish due to US economic resilience.

- Fed policymakers are expected to maintain the status quo on September 20 as US inflation is falling and the economy is better balanced.

Gold price (XAU/USD) struggles to find a direction as investors await the US Consumer Price Index (CPI) data for August. The precious metal remains sideways despite the US Dollar delivering a corrective move, while investors digest global slowdown fears. US inflation data for August carries significance as it is the last one before the September monetary policy by the Federal Reserve (Fed), which is widely expected to remain unchanged.

Last week, Fed policymakers vocally supported maintaining the status quo on September 20 as inflation is falling and the labor market is loosening up. The appeal for the Gold price could be dampened ahead due to expectations of a healthy performance from the US Dollar. In comparison with other G7 economies, the US economy is better absorbing the impact of higher interest rates. The nation is demonstrating itself as resilient, which should heighten demand for the US Dollar.

Daily Digest Market Movers: Gold price consolidates ahead of US CPI data

- Gold price continues to consolidate inside the $1,924 to $1,931 range from the past three trading sessions as investors await the United States inflation data for August, which will be published on Wednesday at 12:30 GMT.

- Investors will stay focused on the inflation data for August. Headline inflation is seen expanding at a significantly higher pace of 0.5%, while core CPI that excludes volatile oil and food prices is seen steady against July’s pace of 0.2% in both segments.

- US headline inflation is seen growing at a higher pace due to the recovery in gasoline prices, which squeezes households’ income.

- The release of the August CPI data will build a base for September’s monetary policy.

- The precious metal remains sideways amid uncertainty over the interest rate peak for the remaining year, while the September monetary policy is expected to remain unchanged amid supportive economic data.

- As per the CME Fedwatch Tool, traders see a 57.6% chance of interest rates remaining unchanged at 5.25% to 5.50% by year-end.

- Labor growth remained stable in August, while the Unemployment Rate rose to 3.8%. Wage growth slowed, which could slim consumer spending momentum ahead. This could ease additional inflationary pressure.

- Fed policymakers: Dallas Fed Bank President Lorie Logan and New York Fed Bank President John Williams supported an unchanged interest rate decision for September monetary policy last week but kept doors open for further policy tightening in the future.

- Fed Williams said there is no urgency for an interest-rate increase this month as inflation is falling and the economy is better balanced.

- The yellow metal remained lackluster despite some correction in the US Dollar Index (DXY) from its six-month high of 105.00. The USD Index dropped to near 104.60 as deflation risks in China eased in August due to a nominal recovery in inflationary pressures.

- One month of nominal recovery in China’s inflation data is sufficient to warrant economic growth, which will keep the overall trend for the US Dollar bullish.

- Investors are keenly watching whether the central bank pushes the US economy to the “golden path”, meaning a situation where inflation recedes without triggering a recession.

- US Treasury Secretary Janet Yellen said she is confident that the central bank will contain inflation without damaging the job market. She doesn’t see China-led BRICS expansion as a major threat to the economy.