- Аналітика

- Новини та інструменти

- Новини ринків

Новини ринків

- US Producer Price Index (PPI) surpasses estimates, bolstering the US Dollar as Treasury yields soar.

- Reserve Bank of New Zealand (RBNZ) is expected to maintain rates at 5.50%, adding pressure on the NZD.

- NZD/USD’s future hinges on US economic data and potential RBNZ rate surprises; 0.5900 level in sight.

NZD/USD plunges below 0.6000, set to finish the week with losses of 1.86% after inflation data in the United States (US), although mixed, weighed on the NZD/USD pair. Furthermore, the Reserve Bank of New Zealand (RBNZ) adopting a dovish stance was the last nail in the coffin for the Kiwi dollar (NZD). The NZD/USD exchanges hands at 0.5981, down 0.65%.

Kiwi dollar faces headwinds from mixed US inflation data and RBNZ’s anticipated rate hold

During the week, the NZD/USD extended its losses courtesy of fundamental news, with US inflation data in the spotlight. Data was mixed, with consumer inflation ticking a little up, but stood below estimates, confirming US disinflationary process. Still, not everything was positive news, as factory prices, known as the Producer Price Index (PPI) for July, exceeded estimates and the prior’s month data. Hence, traders bought the US Dollar (USD) underpinned by soaring US Treasury bond yields, to the detriment of the New Zealand Dollar (NZD).

US Treasury bond yields advanced sharply as traders turned nervous after the data reignited fears of price pressures, which could influence the US Federal Reserve (Fed) to tighten monetary conditions. The US 10-year yields rose nine basis points to 4.168%, while the most sensitive to interest rates, the US 2-year yield, climbed nine basis points to 4.90%.

Consequently, the US Dollar Index (DXY), which measures the buck’s performance vs. its peers, advances 0.32%, at 102.853, printed solid gains during the week.

On the New Zealand (NZ) front, weakness in business activity weighed on the NZD. Worth mentioning that a Reuters poll said that most analysts estimate the Reserve Bank of New Zealand (RBNZ) will keep rates unchanged at 5.50%, at a 14-year high, for the second straight meeting, on August 16. Only two of 29 analysts said that rates would need to rise to 5.75%.

Given the backdrop, the NZD/USD could extend its downtrend, favored by the RBNZ’z stance. If US economic data becomes weaker than expected and the RBNZ surprises the market with a rate hike, the NZD/USD could reclaim the 0.6000 figure. Otherwise, look for a break below 0.5900, with sellers eyeing last year’s October lows of 0.5512.

NZD/USD Price Analysis: Technical outlook

From a technical perspective, the NZD/USD is set to extend its losses, as the weekly chart portrays a ‘broadening formation’, suggesting that further downside is expected. The break of the pair below the 50-week moving average accelerated the NZD/USD’s fall, and a daily close below the May 2023 lows of 0.5985 could put into play a fall towards the bottom of the ‘broadening formation’ at around 0.5875/0.5900. A drop below that level would put last year’s October low at 0.5512 in play.

- The EUR/JPY traded in the red below the 159.00 area after five consecutive days of gains.

- The cross closed Friday with 1.65% weekly gains, trading in highs since 2008.

- Focus shifts to the Eurozone and Japan's GDP for Q2, which will be released the following week.

In Friday's session, the EUR/JPY traded with losses, closed negative below the 159.00 area, and corrected after five consecutive days of gains. On the Euro’s side, France's Consumer Price Index (CPI) figures slightly surprised to the upside but failed to significantly impact the pair, while no relevant reports featured on the Japanese economic calendar. All eyes are now on the Gross Domestic Product (GDP) for Q2, which will be released next week, for both the Eurozone and Japan region will help investors to place their bets on the European Central Bank (ECB) and Bank of Japan (BoJ) following decisions.

EUR/JPY Levels to watch

The daily chart analysis indicates a bullish outlook for the EUR/JPY in the short term despite Friday’s losses. The Relative Strength Index (RSI) is above its midline in positive territory aligning with the positive signal from the Moving Average Convergence Divergence (MACD), which displays green bars, reinforcing the strong bullish sentiment. Additionally, the pair is comfortably above the 20,100,200-day Simple Moving Averages (SMAs), indicating that the bulls are clearly in command on the broader picture.

Support levels: 157.60, 157.00, 156.00.

Resistance levels: 159.00, 159.50, 160.00.

EUR/JPY Daily chart

-638273853941414482.png)

- The pair trades green for a fifth consecutive day, around the critical 145.00 zone.

- The USD continues to strengthen after higher-than-expected US PPI data from July.

- Investors continue to bet on a less aggressive stance by the BoJ causing the Yen to lose interest.

On the last day of the week, the USD/JPY rose near the 145.00 zone, showing more than 2% of weekly gains. This movement was driven by a vital Producer Price Index (PPI) from the US for July and optimistic personal consumer confidence data released by the University of Michigan (UoM). The US treasury bond yields are increasing and show more than 1% of daily gains from this. On the Japanese side, Yen continues to trade weak as investors continue to place bets on a dovish stance by the Bank of Japan (BoJ).

Hawkish bets on the Fed after inflation data favoured the USD

PPI data on Friday saw the headline figure jumping to 2.4% YoY in July, slightly higher than expected. This comes with the US releasing this week that the headline and core Consumer Price Index (CPI) decelerated in the same month, so overall, the US inflation outlook is mixed.

That being said, the US bond yields are seeing gains across the curve driven by hawkish bets on the Federal Reserve. The 10-year bond yield rose to 4.18%, while the 2-year yield stands at 4.90% and the 5-year yielding 4.31%, respectively. In line with that, the CME FedWatch tool indicates that the odds of a 25 basis point (bps) hike in the November meeting rose to nearly 30% but remain low for the upcoming September decision.

On the JPY’s side, no relevant data was released, and the focus shifted to next week's Gross Domestic Product (GDP) data from Q2 from Japan.

USD/JPY Levels to watch

Considering the daily chart, the USD/JPY shows a bullish outlook for the short term. The Relative Strength Index (RSI), positioned above its midline in positive territory with a northward slope, supports this view along with the positive indication from the Moving Average Convergence Divergence (MACD), which is displaying green bars, pointing towards a strengthening bullish trend. On the other hand, the pair is above the 20,100,200-day Simple Moving Averages (SMAs), indicating that the bulls are in command of the broader picture.

Support levels: 143.70, 143.00, 142.00.

Resistance levels: 145.00, 145.50, 146.00.

USD/JPY Daily chart

-638273807969935913.png)

- US Producer Price Index (PPI) outpaces June, driving a temporary Greenback rally and GBP/USD dip.

- University of Michigan poll indicates optimism on inflation’s decline post-Fed’s 525 bps rate hike.

- UK’s economy outperforms forecasts, bolstering Bank of England’s rate hike stance amidst looming recession fears.

Late in the New York session, the Pound Sterling (GBP) continued to hold its ground against the US Dollar (USD) after UK’s economy grew more than expected, despite US elevated inflation on the producer side. Hence, the GBP/USD trades at 1.2697, gaining 0.16%.

Wall Street wavers as mixed US inflation data clashes with UK’s unexpected economic surge

Wall Street is set to finish the session with losses after the United States (US) inflation data posted mixed results. Consumers’ inflation climbed above the prior’s month but below estimates, sparking speculations on the Federal Reserve (Fed) ending its tightening cycle, but data on Friday changed investors’ minds.

The US Department of Labor showed the prices paid by producers, known as the Producer Price Index (PPI), exceeded June’s readings, spurring a Greenback rally; consequently, the GBP/USD weakened.

The University of Michigan Consumer Sentiment poll, revealed that US consumer sentiment slightly deteriorated. Still, Americans remained positive on inflation lowering after the US Federal Reserve (Fed) increased 525 bps its borrowing costs, with inflation expected to dive below 3% on a five-year horizon.

Across the Atlantic, UK’s economy surprisingly grew above estimates, justifying the Bank of England’s (BoE) need to raise rates amidst stubbornly high inflation. Nevertheless, next week’s inflation data can lend a lifeline to the BoE if it shows signs of slowing down as the UK’s economy is still at the brisk of a recession.

GBP/USD Price Analysis: Technical outlook

The GBP/USD breaking to a new weekly high, above 1.2800 but reversing its gains on soft US inflation data, has exacerbated GBP/USD’s pullback, extending beneath the 1.2700 figure. If GBP/USD remains below the latter and achieves a daily close, that would cement Sterling’s (GBP) faith. That said, the GBP/USD first support would emerge at 1.2666, followed by the August 3 daily low of 1.2620, ahead of sliding towards 1.2500. Conversely, if GBP/USD’s buyers reclaim 1.2700, it would be cheered by buyers, which could remain hopeful of targeting 1.2800, ahead of challenging the July 27 daily high at 1.2995.

Analysts at Rabobank, see the USD/JPY pair at 145 on a 3-month view and then pulling back to 140 and 135 in 9 and 12 months, respectively, on the back of expectations of softer Federal Reserve policy.

Key quotes:

“The messages contained within the BoJ’s July policy adjustment have not been easy to decipher. The BoJ may have been attempting to give itself more flexibility around YCC. However, Governor Ueda’s comments on the exchange rate may have encouraged speculation that JPY weakness will result in more upside in 10 yr yields.”

“This week’s softer than expected Japanese economic data support the view that the BoJ will maintain accommodative policy settings, and we have revised higher our USD/JPY forecasts.”

“We have revised down our forecasts for the JPY. We now see USD/JPY at 145 on a 3-month view, recovering to USD/JPY140 and USD/JPY 135 in 9 and 12 months respectively on the back of expectations of softer Fed policy.”

The University of Michigan's Consumer Confidence data for August offered little change. Analysts at Wells Fargo point out that consumers anticipate prices to decline overall, despite their expectations of rising interest rates.

Key quotes:

“Consumers are becoming more convinced that inflation is cooling. Whether or not they fully understand the Federal Reserve's role in that is not completely clear, but they are yet to be convinced that we have seen the last of rising interest rates.”

“A majority of consumer still expects interest rates to rise over the next year. In fact, the index value for this measure, or the share of consumers expecting interest rates to go up less the share expecting them to come down in the next year, sits at 50. Though this is a slight decline from 52 in July, it is still above any other point since February 2021.”

Next week, key events in the US include Retail Sales data and the release of the FOMC minutes. Market participants will also closely listen to comments from Fed officials as they prepare for the Jackson Hole Symposium. In the UK, inflation and employment data will be reported. The RBNZ will have its monetary policy meeting. The RBA will release its meeting minutes, and Australia will report employment figures. Canada's inflation data is also expected to be released.

Here is what you need to know for next week:

Next week, the US is scheduled to release several important economic indicators. On Tuesday, Retail Sales data will be published, followed by Building Permits and Industrial Production on Wednesday and Jobless Claims on Thursday. From China, upcoming data includes Retail Sales and Industrial Production figures for July. However, the most significant event is likely to be the release of the FOMC meeting minutes on Wednesday. Additionally, market participants will closely monitor comments from Federal Reserve members as they prepare for the Jackson Hole Symposium, which is scheduled to begin on August 24th.

The US Dollar Index continued its rally and gained ground for the four week in a row. It closed the week at the highest level since June, approaching the 103.00 level. Stock markets showed little change as caution prevailed. Crude oil extended its seven-week upward trend but retraced slightly after reaching the highest level since November. WTI crude settled above $82.00 per barrel.

US Treasury yields climbed higher, with the 10-year yield surpassing 4.15%. Gold experienced a $30 loss and closed near $1,910, while Silver declined by 4.2% to around $22.60 per ounce.

EUR/USD had a negative week but found support above the 200-week Simple Moving Average (SMA) around 1.0940. Several European countries will observe a holiday on Monday. Germany is expected to report a moderation in the annual Wholesale Price Index from -2.9% to -2.6% for July. The ZEW Survey is scheduled for release on Tuesday. The Eurozone will report Q2 growth data, employment change, and the final CPI on Wednesday and Friday, respectively.

GBP/USD ended in negative territory for the fourth consecutive week. The bias remains bearish, with key support around the 1.2600 level. Following Friday's positive surprise in UK growth figures, the upcoming week will be busy with the employment report on Tuesday, inflation data on Wednesday, and retail sales figures on Friday.

USD/CHF rose during the week but failed to reach three-month highs. Upside remains capped around 0.8800. Switzerland will release the Producer and Import Price Index for July on Tuesday.

USD/JPY surged towards the 145.00 level, marking the highest weekly close since November. The Japanese Yen underperformed, influenced by divergent monetary policies and higher government bond yields. Japan will release Q2 growth data, Industrial Production figures on Tuesday, trade data and Machinery Orders for June on Thursday, and the National CPI on Friday.

AUD/USD ended the week testing levels below 0.6500 and remains under pressure. The pair is approaching 2023 lows. The Reserve Bank of Australia (RBA) will release the minutes of its latest meeting on Tuesday. In terms of economic data, the Q2 Wage Price Index is due on Thursday, expected to show a 1% increase, which will be important for the RBA. The July employment report will be released on Thursday, with an expected positive change in jobs of 21,500.

USD/CAD climbed above the 20-week SMA and encountered resistance at 1.3500. Despite another negative week against the US Dollar, the Canadian Dollar outperformed the Australian Dollar and the New Zealand Dollar. Canada will report consumer inflation on Tuesday.

NZD/USD maintains a negative tone and broke below 0.6000 on Friday, marking the lowest weekly close since November of the previous year. The Reserve Bank of New Zealand (RBNZ) will announce its decision on Wednesday, with the rate expected to remain unchanged at 5.5%. On Thursday, New Zealand will release the Producer Price Index.

The Colombian Peso and the Mexican Peso were among the top performers in the currency market during the week, while the South African Rand experienced the most significant decline.

Like this article? Help us with some feedback by answering this survey:

- XAG/USD fell below $22.70 and is poised for a 3.8% weekly loss.

- July’s PPI from the US rose to 2.4%.

- Rising yields don't allow the metal to gain traction.

On Friday, the XAG/USD saw mild losses and will post its fourth consecutive weekly loss, having lost more than 7% since mid-July. At the end of the week, the US reported hot Producer Price Index (PPI) data and positive University of Michigan (UoM) Sentiment and inflation expectations, which fueled a rise in US bond yields.

After the release of key inflation data throughout the week, American rates are rising. The 10-year bond yield reached 4.16%, up by 1.34%. The 2-year yield stands at 4.89% with a 1% increase, while the 5-year yield is at 4.30% with 1.75 % gains. It's worth noting that American yields tend to be negatively correlated with non-yielding precious metals, so they may limit the XAG/USD’s upside for the rest of the session.

Overall, inflation saw this week the headline and core Consumer Price Index (CPI) coming lower than expected in July, while the PPI rose to 2.4% higher than expectations. The pace for the metal and bond markets in the next session will be determined by the market's assessments of the economic situation in the US and how it will affect the next Federal Reserve (Fed) decisions. As for now, the stronger case is that more hikes will be seen in this tightening cycle, but as Jerome Powell stated, it will all depend on the incoming data.

XAG/USD levels to watch

The technical analysis of the daily chart points to a neutral to a bearish outlook for XAG/USD, indicating the potential for further bearish movement. The Relative Strength Index (RSI) displays a flat slope below the 50 middle points, while the Moving Average Convergence (MACD) lays out weaker red bars. Furthermore, the pair is below the 20,100 and 200-day Simple Moving Averages (SMAs), highlighting the continued dominance of bears on the broader scale, requiring the buyers to take action. Traders should eye the 20 and 100-day averages as they are about to perform a bearish cross which could exacerbate the downside in the near term.

Support levels: $22.50, $22.30, $22.00.

Resistance levels: $23.25 (200-day SMA), $23.50, $23.70, $24.05 (a bearish cross between the 20 and 100-day SMA).

XAG/USD Daily chart

-638273757221757119.png)

- US crude oil benchmark, WTI, rises for the third consecutive day, trading at $83.48, up by 0.80%.

- Oil demand is predicted to grow by 2.25 million bpd in 2024, down from 2024’s 2.44 million bpd, according to OPEC+.

- Weakness in China’s economy could dent oil demand.

Western Texas Intermediate (WTI), the US crude oil benchmark advances for the third day in the week, trims some of its Thursday’s losses, as it tracks an upslope support trendline since mid-July. At the time of writing, WTI is exchanging hands at $83.48, above its opening price by 0.80%.

OPEC+ output reductions and weakening US dollar support crude’s upward trajectory, despite potential demand concerns from China

Oil prices rose on several factors weighing on the market, like Saudi Arabia and Russia’s 1.3 million of crude oil output cuts, while the International Energy Agency (IEA) stated supply cuts by the Organization of Petroleum Exporting Countries and its allies (OPEC+), could drive prices higher before economic headwinds dent global demand growth.

In the meantime, OPEC+ noted that Oil’s demand would increase by 2.25 million bpd in 2024, below this year’s 2.44 million bpd.

Meanwhile, the United States (US) inflation figures on the consumer side witnessed a dip, which weakened the greenback, and underpinned WTI’s towards its new year-to-date (YTD) high above $84.00 per barrel. Nevertheless, Friday’s US PPI data bolstered the US Dollar (USD) as shown by the US Dollar Index (DXY), gaining 0.24% at 102.870, while WTI’s prices drifted lower.

Mixed economic data from China would keep WII’s gains capped on fears the country has been hit by deflation, suggesting the Covid-19 recovery would remain losing steam, weighing on oil demand,

WTI Price Analysis: Technical outlook

WTI’s daily chart portrays the pair as upward biased, thought at the brisk of a support trendline break, which could see WTI’s diving towards the 20-day Exponential Moving Average (EMA) at $80.18, followed by the $80.00 figure. On the upside, WTI’s first supply zone to test would be the $84.00, ahead of challenging the $85.00 a barrel.

- EUR/GBP retreated near 0.8630 after being rejected by the 100-day SMA at 0.8670.

- Q2 GDP data from the UK avoided stagnation, surpassing market expectations.

- Higher British yields help the Pound trade stronger against most of its rivals.

In Friday’s session, the GBP traded with gains agains most of its rivals as the UK reported strong Q2 economic activity figures, which faded recession fears. On the other hand, the EUR is trading mixed, while no relevant data was released during Friday’s session.

Investors assess British solid economic data

The UK's second-quarter Gross Domestic Product (GDP) data revealed robust performance. In terms of the yearly measurement, it surged by 0.4%, surpassing both the anticipated and previous 0.2% figures. The quarter-on-quarter (QoQ) growth also stood at 0.2%, avoiding the predicted stagnation and beating the earlier 0.1% reading. In addition, Manufacturing and Industrial Production came in strong in June, seeing monthly increases of 2.4% and 1.8%, respectively, above expectations.

Reacting to the data, the British yields are seeing gains across the curve, making the GBP gain interest. The 10-year bond yield rose to 4.57% while the 2-year yield stands at 5.05% and the 5-year yielding 4.58%, respectively. In that sense, they reflect that markets expect the Bank of England (BoE) to continue hiking. According to the World Interest Rate Possibilities (WIRP) tool, investors are pricing 50 bps of additional tightening this cycle which would see the terminal rate peak at 5.75%.

EUR/GBP Levels to watch

According to the daily chart, the technical outlook for the EUR/GBP remains neutral to bearish as the bulls show signs of exhaustion and are losing traction. The Relative Strength Index (RSI) shows a weakening bullish trend with a negative slope above its midline, while the Moving Average Convergence (MACD) presents lower green bars. Furthermore, the pair is above the 20-day Simple Moving Average (SMA) but below the 100 and 200-day SMAs, indicating that the bulls aren't done yet and have some gas left in the tank.

Support levels: 0.8615, 0.8600 (20-day SMA), 0.8570.

Resistance levels: 0.8670 (100-day SMA), 0.8700, 0.8723 (200-day SMA).

EUR/GBP Daily chart

-638273711974184676.png)

- The Mexican Peso (MXN) advances against the US Dollar, despite overall US Dollar strength.

- Banxico’s decision to hold rates at 11.25% boosted the Mexican Peso.

- USD/MXN may stabilize near current levels, potentially reaching 17.5000 if surpassing 17.4100. A daily close below 17.0000 could indicate an extended downward trend.

The Mexican Peso (MXN) appreciates against the US Dollar (USD), bucking the trend of Latin American currencies weakening on Friday after the Bank of Mexico (Banxico) kept rates unchanged, even though an uptick in US factory inflation boosted the USD. Nevertheless, the USD/MXN extends its losses and trades above the 17.0000 figure for seven straight days.

Banxico’s decision to maintain rates propels the MXN as it defies the Latin American currency trend on Friday

A risk-off impulse keeps the Greenback in the driver’s seat except for the MXN, with the emerging market currency posting solid gains of 0.87% as the USD/MXN extends its losses past 17.0000. On Thursday, Banxico decided unanimously to hold rates at 11.25%, as the central bank underscored the inflationary outlook as remaining “very complex” and suggested a similar approach as the Federal Reserve, keeping rates higher for longer. Although inflation is converging towards Banxico’s 3% plus or minus 1% range, with July CPI at 4.79%, the central bank continues to display a hawkish message. Meanwhile, analysts estimate Banxico’s first rate cut towards the end of the year.

That favored USD/MXN downside, accelerated by soft US consumer inflation data. USD/MXN gained some traction above 17.0000 after the US Department of Labor reported on the Producer Price Index (PPI) for July came at 0.3% MoM above forecasts of 0.2%, while annual numbers increased from 0.2% to 0.8%. Core PPI readings which exclude volatile items to gather a better reading of inflation, climbed 0.3% MoM, exceeding estimates and the prior’s month -0.1% slide, while annually based, exceeded estimates but was unchanged, compared to June’s 2.4%.

The University of Michigan Consumer Sentiment poll, revealed that US consumer sentiment slightly deteriorated. Still, Americans remain optimistic that inflation would get lowered after the US Federal Reserve (Fed) increased 525 bps its borrowing costs, with inflation expected to dive below 3% on a five-year horizon.

In the meantime, the US Dollar Index (DXY), which measures the buck’s performance against a basket of six currencies, rises 0.20%, at 102.866, underpinned by US Treasury bond yields climbing, with the US 10-year benchmark note sitting at 4.160%, gains five basis point.

Given the backdrop, the USD/MXN would remain subdued, at around current exchange rates, unless the pair breaks above 17.4100, which could see the pair finding acceptance at around 17.5000. Otherwise, further downside is expected, if USD/MXN prints a daily close below 17.0000.

USD/MXN Price Analysis: Technical outlook

From a technical standpoint, the USD/MXN is trading within the 17.00-17.30 range, with neither buyers nor sellers taking control of the USD/MXN pair direction. The USD/MXN spot price remains above the 20-day Exponential Moving Average (EMA) at 16.9946, which could pave the way for further upside, but buyers must lift the exchange rate above the May 17 swing low of 17.4039 to challenge the 100-day EMA at 17.4746, and the 17.5000 mark. Conversely, a daily close below 17.00 could expose the USD/MXN to further selling pressure, with sellers eyeing 16.6238, the YTD low.

- USD/CAD bulls got rejected at the 200-day SMA and retreated near the 1.3420 area, still poised for a weekly gain

- US PPI rose to 2.4% YoY in July, higher than expected.

- Higher Oil prices help the CAD trade strong against most of its rivals.

At the end of the week, the USD/CAD was rejected by the 200-day Simple Moving Average (SMA) at 1.3450 and settled near 1.3430. On the one hand, the USD is trading mildly stronger after hot Producer Price Index (PPI) from July figures which fueled a rise in American bond yields, while the CAD got a boost on the back of rising Oil prices.

Markets asses US inflation data and start to place bets on a hike by the Fed in November

US Producer Price Index from July came in higher than expected. The headline figure rose by 0.3% MoM to 0.8% YoY while the core measure advanced 0.3% MoM vs 0.2% expected to a yearly measure of 2.4%.

As a reaction, the US bond yields are seeing gains across the curve. The 10-year bond yield rose to 4.13%, while the 2-year yield stands at 4.87% and the 5-year yielding 4.25%, respectively. In that sense, higher yields can be attributed to investors placing higher bets on a 25 basis point (bps) hike in November’s Federal Reserve (Fed) meeting. As for now, and according to the CME FedWatch tool, those odds stand at 64% in favour of a no hike and nearly 30% in favour of a hike, vs last week's 25%. For the September meeting, the stronger case continues to be the Fed not hiking.

Other data released by the US by the University of Michigan indicated that its Sentiment index rose to 71.2, better than the 71 expected, while 5-year Consumer Inflation Expectations dropped to 2.9%.

On the other hand, Oil prices resumed their upwards path and as it is one of Canada’s main exports, higher energy prices strengthened the CAD. Data-wise, nothing relevant will be released on Friday for the Canadian economy.

USD/CAD Levels to watch

Analysing the daily chart, indicators point at a neutral to the bearish technical outlook for the USD/CAD, suggesting that the bulls are starting to give up. The Relative Strength Index (RSI) points downwards in the bullish territory, suggesting a possible trend reversal, while the Moving Average Convergence (MACD) prints lower green bars. On the weekly chart, the bullish outlook is more evident as the pair will record its fourth-consecutive weekly gain at the end of this session.

Support levels: 1.3350 (100-day SMA),1.3350, 1.3300.

Resistance levels: 1.3450 (200-day SMA), 1.3500,1.3550.

USD/CAD Daily chart

-638273673290295860.png)

- EUR/USD experienced losses during Friday’s North American session, reaching 1.0975 from a daily high of 1.1000.

- US Department of Labor report indicated Producer Price Index (PPI) growth of 0.3% MoM, exceeding expectations, with annual PPI at 0.8%. Core PPI rose by 0.3% MoM.

- University of Michigan’s survey displayed a slight drop in consumer sentiment to 71.2, while inflation outlooks for one and five years remained optimistic.

EUR/USD registered losses during Friday’s North American session after reaching a daily high of 1.1000, but an uptick in wholesale inflation in the United States (US) increased appetite for the safe-haven status of the Greenback. Hence, the EUR/USD reversed its course and trades at 1.0958, down 0.20%.

Despite touching a high of 1.1000, the Euro retreats against the strengthening US Dollar amid risk-aversion and concerns about inflation

Risk-aversion keeps flows toward the US Dollar (USD) even though consumer inflation in July cooled down, as the US Department of Labor reported on Thursday. Nevertheless, an early report but the same institution witnessed a jump in the Producer Price Index (PPI) of 0.3% MoM above estimates of 0.2%, while annually based ticked up from 0.2% to 0.8%. Core PPI readings which exclude volatile items to gather a better reading about inflation, rose by 0.3% MoM, exceeding estimates and the prior’s month -0.1% slide, while annually based, exceeded estimates but was unchanged, compared to June’s 2.4%.

Following the data, the EUR/USD plunged from around 1.1000 toward the 1.0960 region, extending its drop toward the daily lows of 1.0954 before finding bids and recovering some ground.

The University of Michigan recently revealed that consumer sentiment has deteriorated compared to July 71.6, coming at 71.2, while inflation expectations improved. Americans think inflation in the one and five years horizon would ease, from 3.4% to 3.3% and from 3% to 2.9%, respectively.

In the meantime, the US Dollar Index (DXY), a basket of six currencies vs. the Greenback, stands flat at 102.619, although higher US Treasury bond yields would suggest a stronger US Dollar. The US 10-year benchmark note sits at 4.125%, gains one basis point.

Across the pond, the Eurozone (EU) docket featured inflation data in France and Spain, which showed mixed readings, as France’s inflation was below June’s figures, while Spain’s inflation was above the prior’s month but as expected. In the meantime, a Reuters poll showed that 37 of 70 economists expect the European Central Bank (ECB) to keep rates unchanged in September. Suppose the ECB raises borrowing costs past 4%. It would be the highest deposit rate since the Euro’s introduction in 1999.

Although the interest rates differential favors the US Dollar, uncertainty in the US and the Eurozone could keep choppy trading conditions. Nevertheless, the next week’s EU docket would be busy compared to the US, and if inflation figures show an improvement, that could be bearish for the EUR.

EUR/USD Price Analysis: Technical outlook

After reaching a weekly high of 1.1065 after the release of US consumer inflation, the pair failed to regain the 1.1000 mark, opening the door for further losses. On the upside, EUR/USD price action is capped by the 20-day Exponential Moving Average (EMA) at 1.1003, followed by a two-month-old resistance turned trendline, previous support at around 1.1030/50. With the Relative Strength Index (RSI) remaining at bearish territory and price action failing to achieve a higher peak, the EUR/USD could dip lower, with support emerging at 1.0950, before falling to its month-to-date (MTD) low of 1.0912.

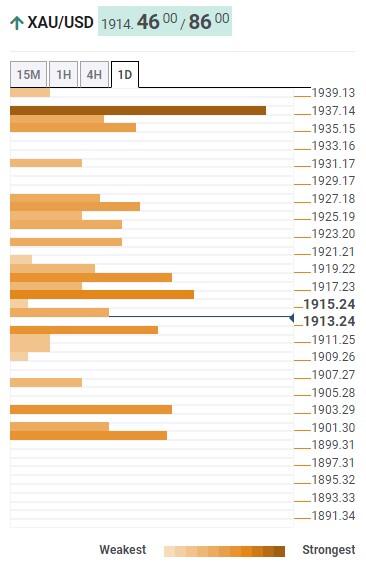

Gold weakness has extended back to key support at $1,898/1,893 but strategists at Credit Suisse continue to look for a floor here.

Weekly close below $1,893 would reinforce the longer-term sideways range

We look for key support and the 38.2% retracement of the 2022/2023 uptrend, 200-DMA and June low at $1,900/$1,891 to hold again and we maintain our long-held view for a major floor here and for an eventual retest of major resistance at the $2,063/$2,075 record highs to be seen.

We still stay biased to an eventual break to new record highs later in the year, which would then be seen to open the door to a move to $2,150 next, then $2,355/$2,365.

A weekly close below $1,893 though would be seen to reinforce the longer-term sideways range, and a fall to support next at $1,810/$1,805.

Is the Oil supercycle still on? Economists at TD Securities analyze crude prices outlook.

Oil markets to remain range-bound at elevated prices for some time

Recent energy supply trends are still corroborating our view that the West is losing control over commodity supply, but developments to global spare capacity have likely flattened the right tail for energy markets over the coming year. Initially, this is likely to cap the upside to long-dated Brent prices but also decreases the risks of a sustained runaway rally in spot crude prices above $100/bbl over the medium-term.

The supercycle may not be off, but the outlook is constrained by ongoing additions to global spare capacity, such that substantial price gains are likely to unleash additional supply. However, Gulf nations have managed to increase their control on global spare capacity, suggesting that the group of producers can continue to engineer a tighter market without fear of significantly losing market share to competitors.

Instead of offering structural tailwinds to prices from an evaporating pool of spare capacity, oil markets are more likely to remain range-bound at elevated prices for some time.

- Silver price juggles in a narrow range below $23.00 despite strength in the US Dollar.

- The US Dollar Index strengthens as US PPI grew at a healthy pace in July.

- US five-year Consumer Inflation Expectations for August softened marginally to 2.9%

Silver price (XAG/USD) continues to oscillate in a narrow range around $22.70 despite the United States Producer Price Index (PPI) growing at a higher pace than expected in July. The white metal looks vulnerable as the US Dollar jumps swiftly to near 102.80 despite hopes that the Federal Reserve (Fed) will keep interest rates steady in its September monetary policy.

S&P500 opened on a bearish note as a rise in US PPI could elevate the burden on households. Also, investors anticipating retaliation from Beijing as US President Joe Biden prohibits investments in some Chinese sensitive technologies.

US Bureau of Labor Statistics reported that monthly PPI grew at a healthy pace of 0.3% against expectations of 0.2%. The higher pace in the price elevation of goods and services at factory gates is due to a rebound in the cost of services at the fastest pace in nearly a year.

On Thursday, US inflation grew at a modest pace in July amid higher house rentals but was aligned with the Fed’s desired rate of 2%. Meanwhile, five-year Consumer Inflation Expectations for August softened marginally to 2.9% against the estimates and the former release of 3.0%.

Silver technical analysis

Silver price consolidates in a narrow range of 22.60-23.00 on an hourly scale. The white metal struggles to find a direction despite the strength of the US Dollar. The 100-period Exponential Moving Average (EMA) at $22.90 is consistently acting as a barricade for the Silver bulls.

A 40.00-60.00 range oscillation by the Relative Strength Index (RSI) indicates a volatility contraction.

Silver hourly chart

-638273603901735529.png)

Commodity markets have become a popular asset class for portfolio investors, just like stocks and bonds. Strategists at ANZ bank analyze commodities outlook.

Falling inventories point to market tightness

Commodity markets have been under pressure in recent time amid a weak economic backdrop. Despite this, there are signs of tightness.

Inventories have always been a good guide to demand; and after a shaky start to the year, are showing signs of tightness across most markets.

There has been a clear drawdown across commodity exchanges and the broader supply chain. However, the trends are more discrete across the energy market. Industrial metals are now at multi-decade low levels which could trigger price rallies amid supply shocks.

- UoM Consumer Confidence Index declined slightly in August.

- US Dollar Index clings to modest daily gains above 102.60.

Consumer sentiment in the US weakened slightly in August, with the University of Michigan's (UoM) Consumer Confidence Index declining to 71.2 from 71.6 in July. This reading came in better than the market expectation of 71.

Further details of the publication revealed that the Current Conditions Index rose to 77.4 from 76.6 and the Expectations Index retreated to 67.3 from 68.3.

The one-year inflation outlook edged lower to 3.3% from 3.4%, while the 5-year inflation outlook ticked down to 2.9% from 3%.

Market reaction

The US Dollar Index stays in positive territory above 102.60 after this report.

Economists at Commerzbank share their ECB and Fed forecasts and their implications for the EUR/USD pair.

The ECB, unlike the Fed, should not cut its key rates

Because the ECB, unlike the Fed, should not cut its key rates, there is still some upside potential for EUR/USD over the next two or three quarters.

As long as inflation in the Euro area is falling, the ECB with its rates on hold appears to be a more credible inflation fighter, from which EUR/USD will probably benefit. However, this perception will be reversed, if Eurozone inflation starts to rise again in the middle of next year. EUR/USD will then tend to weaken again.

Following the publication of the US inflation figures, Gold price briefly climbed to $1,930 but then dropped back to $1,915. Economists at Commerzbank analyze XAU/USD outlook.

Gold faces continuing headwind

The MoM change rates indicate that the inflation rate is moving towards the Fed’s target figure, which points to an end to the rate hike cycle. That said, the US real interest rate is already significantly positive if the market-based inflation expectations are used, which is bad news for Gold.

Gold is also facing headwind from the continuing ETF selling. For the outflows to stop, the market’s remaining rate hike expectations need to disappear and give way to rate cut expectations. We expect this to happen in the fourth quarter.

- USD/JPY is looking to capture the 145.00 resistance as US PPI grew stronger than expected.

- The US Dollar Index climbs above 102.60 as producers elevated the prices of goods and services at factory gates by 0.3%.

- The Japanese Yen remains under pressure amid an absence of a supportive BoJ policy.

The USD/JPY pair is marching towards the critical resistance of 145.00 in the London session. The asset rallies due to underperformance from the Japanese Yen. The major struggles to continue its four-day winning streak as investors await the United States Producer Price Index (PPI) data for further guidance.

S&P500 futures post some losses in Europe amid caution due to robust US PPI and US President Joe Biden’s ban on some investment in Chinese sensitive technologies. US equities ended on a mixed note on Thursday after US Biden’s prohibition of investment in China offsets the impact of slower-inflation growth.

The US Dollar Index (DXY) climbs above 102.60 as producers elevate the prices of goods and services at factory gates by 0.3% while analysts forecasted a pace of 0.2%. Annual headline PPI rose to 0.8% against surprisingly higher expectations of 0.7%. Headline PPI rose beyond expectations due to a recovery in gasoline prices in July. Also, monthly core PPI grew at a 0.3% pace, higher than estimates of 0.2%.

Investors hope that the Federal Reserve (Fed) could pause the policy tightening spell and keep interest rates steady. Monthly inflation grew at a 0.1% pace in July, which were in line with the Fed’s desired rate of 2%.

On the Tokyo front, the Japanese Yen remains under pressure amid an absence of support from the Bank of Japan (BoJ) policy. Analysts at Commerzbank stated even if the BoJ wanted to start a slow exit from its yield curve control with its current monetary policy that cannot be positive for the Yen due to the lack of transparency.

Economists at Nordea expect the EUR/USD pair to lose ground toward 1.07 before bouncing back higher.

USD hurt by soft landing outlook

Disinflation has hurt the USD with US interest rate expectations tilting towards interest rate cuts rather than interest rate hikes. Falling inflation has also lifted risk sentiment. That has not been supportive for the USD, a traditional safe haven, that benefits when there is risk-off.

The USD is likely to perform again when the probability of a soft landing fades and risks of higher interest rates for longer prevail.

Our three-month forecast has EUR/USD trading back down at 1.07 before pulling higher.

- Australian Dollar finds a floor in the lower 0.65s after selling off on fears of a credit crunch in the Chinese property sector.

- Hawkish commentary from the Governor of the RBA, Philip Lowe, helps staunch the bleeding from China property sector woes.

- US factory gate inflation comes out higher than expected, supporting the US Dollar.

The Australian Dollar (AUD) finds a floor against the US Dollar (USD) after selling off during the Asian session on fears of a credit crunch in the Chinese property sector triggered by the default of a private property developer, Country Garden.

The Australian Dollar comes under pressure again, however, following the release of higher-than-expected US factory gate inflation with the release of Producer Price Index data (PPI) for July.

AUD/USD trades in the 0.65s at the start of the US session.

Australian Dollar news and market movers

- The Australian Dollar reverses the substantial gains made on Thursday as a result of positive market sentiment and a weaker US Dollar, caused by the release of lower-than-expected US inflation data for July.

- Fresh China economy woes may have contributed to the Australian Dollar’s turn lower.

- During Friday’s Asian session, the news surfaced that Chinese private property developer Country Garden defaulted on its debt, spreading fear of a meltdown in the country’s fragile property sector.

- Given Australia’s reliance on exporting raw materials such as Iron Ore for Chinese building projects, the news weighed heavily on the Australian Dollar.

- The Aussie found support during the Asian session after comments from Governor Lowe that the market interpreted as hawkish and, therefore, positive for AUD. Lowe reiterated the Reserve Bank of Australia’s (RBA) commitment to fighting inflation and did not rule out the need for further rate hikes.

- Headline PPI shows a 0.8% rise in July YoY versus the 0.7% forecast and 0.3% MoM versus the 0.2% anticipated.

- Core PPI shows a 2.4% rise versus the 2.3% YoY forecast, and 0.3% against the 0.2% estimated on a MoM basis.

Australian Dollar technical analysis

AUD/USD is in a sideways trend on both the long and medium-term charts. The February high at 0.7158 is a key hurdle, which if vaulted, will give the longer-term charts a more bullish tone.

The 0.6458 low established in June is a key level for bears. If this is breached decisively, it would color the charts more bearish. Price is currently closer to this key low.

-638273549308493818.png)

Australian Dollar vs US Dollar: Weekly Chart

Price has now broken cleanly below the confluence of moving averages (MA) close to 0.6700, made up of most of the major SMAs – the 50-week, 50-day and 100-day. The breaching of this key support and resistance level was a bearish sign.

-638273549724929664.png)

Australian Dollar vs US Dollar: Daily Chart

AUD/USD has broken below the 0.6600 June lows, and a continuation down to the key May lows at 0.6460, is quite possible. A decisive break below them would open the way for a move down to 0.6170 and the 2022 lows.

Because the pair is in a sideways trend overall, it is unpredictable, and the probabilities do not favor either bears or bulls overall – nor is the Relative Strength Index (RSI) providing much insight on either timeframe.

For bulls, a decisive break back above the skein of MAs in the upper 0.66s and then through 0.6750 would be a prerequisite for a more optimistic outlook.

In technical terms, a ‘decisive break’ consists of a long daily candlestick, which pierces cleanly above or below the critical level in question and then closes near to the high or low of the day. It can also mean three up or down days in a row that break cleanly above or below the level, with the final day closing near its high or low and a decent distance away from the level.

Australian Dollar FAQs

What key factors drive the Australian Dollar?

One of the most significant factors for the Australian Dollar (AUD) is the level of interest rates set by the Reserve Bank of Australia (RBA). Because Australia is a resource-rich country another key driver is the price of its biggest export, Iron Ore. The health of the Chinese economy, its largest trading partner, is a factor, as well as inflation in Australia, its growth rate and Trade Balance. Market sentiment – whether investors are taking on more risky assets (risk-on) or seeking safe-havens (risk-off) – is also a factor, with risk-on positive for AUD.

How do the decisions of the Reserve Bank of Australia impact the Australian Dollar?

The Reserve Bank of Australia (RBA) influences the Australian Dollar (AUD) by setting the level of interest rates that Australian banks can lend to each other. This influences the level of interest rates in the economy as a whole. The main goal of the RBA is to maintain a stable inflation rate of 2-3% by adjusting interest rates up or down. Relatively high interest rates compared to other major central banks support the AUD, and the opposite for relatively low. The RBA can also use quantitative easing and tightening to influence credit conditions, with the former AUD-negative and the latter AUD-positive.

How does the health of the Chinese Economy impact the Australian Dollar?

China is Australia’s largest trading partner so the health of the Chinese economy is a major influence on the value of the Australian Dollar (AUD). When the Chinese economy is doing well it purchases more raw materials, goods and services from Australia, lifting demand for the AUD, and pushing up its value. The opposite is the case when the Chinese economy is not growing as fast as expected. Positive or negative surprises in Chinese growth data, therefore, often have a direct impact on the Australian Dollar and its pairs.

How does the price of Iron Ore impact the Australian Dollar?

Iron Ore is Australia’s largest export, accounting for $118 billion a year according to data from 2021, with China as its primary destination. The price of Iron Ore, therefore, can be a driver of the Australian Dollar. Generally, if the price of Iron Ore rises, AUD also goes up, as aggregate demand for the currency increases. The opposite is the case if the price of Iron Ore falls. Higher Iron Ore prices also tend to result in a greater likelihood of a positive Trade Balance for Australia, which is also positive of the AUD.

How does the Trade Balance impact the Australian Dollar?

The Trade Balance, which is the difference between what a country earns from its exports versus what it pays for its imports, is another factor that can influence the value of the Australian Dollar. If Australia produces highly sought after exports, then its currency will gain in value purely from the surplus demand created from foreign buyers seeking to purchase its exports versus what it spends to purchase imports. Therefore, a positive net Trade Balance strengthens the AUD, with the opposite effect if the Trade Balance is negative.

Economists at Commerzbank analyze MXN outlook following Banxico’s monetary policy meeting.

Banxico maintains underlying hawkish approach

The Mexican central bank’s (Banxico) unchanged approach constitutes the foundation for the continued Peso strength around 17.00 in USD/MXN.

As expected, Banxico left its key rate unchanged at 11.25% and continued to point out the upside risks for inflation. That makes it clear that it wants to avoid any speculation about the start of rate cuts in view of a significant fall in inflation to 4.8% recently (core inflation at 6.5%). Instead, it underlined in its statement that it is necessary to keep the key rate at the current levels for a prolonged period of time.

We continue to see a chance for a first rate cut at the end of the year. The expected fall in inflation will continue to improve real interest rates until then, which fundamentally supports the MXN's strength.

- Producer inflation in the US increased 0.8% on a yearly basis in July.

- US Dollar Index hold steady slightly above 102.50 after PPI data.

The Producer Price Index (PPI) for final demand in the US rose 0.8% on a yearly basis in July, up sharply from 0.1% increase recorded in June, the data published by the US Bureau of Labor Statistics revealed on Friday. This reading came in slightly higher than the market expectation of 0.7%.

The annual Core PPI increased 2.4% in the same period, matching June's reading. On a monthly basis, the PPI and the Core PPI both rose 0.3%.

Market reaction

The US Dollar Index edged slightly higher after this data and was last seen posting small gains at 102.65.

Economists at Scotiabank analyze GBP/USD technical outlook.

Cable could retest resistance at 1.2800/1.2810

The daily GBP/USD chart reflects heavy price action overall Thursday but the intraday pattern of trade shows the Pound rebounding from trend support just under 1.27 in a constructive manner – the 6-hour candle chart shows a bullish ‘morning star’ signal developing today.

The GBP may be able to strengthen somewhat in the short run to retest resistance at 1.2800/1.2810.

See – GBP/USD: Head and Shoulders pattern points towards potential downside – SocGen

Gold price fell to $1,920 after rising towards $1,980 in July. Economists at ANZ Bank analyze XAU/USD technical outlook.

In a bearish trend

The technical chart shows a broad bearish trend is continuing, with Relative Strength Index (RSI) moving towards oversold territory.

Consolidation near $1,900 forms a key support level. A breach of this support could possibly trigger a fresh sell-off. Nevertheless, we see little possibility of the price falling back to the $1,800 range.

On the upside, it needs to break the resistance of recent highs near $1,980. If Gold trades above this level, this could add a fresh bullish tinge to market sentiment. We expect Gold to trade in the range of $1,900-$1,980 until the Fed confirms its monetary path.

USD/CAD little changed but continues to pressure 200-Day Moving Average. Economists at Scotiabank analyze the pair’s outlook.

Support is 1.3375/1.3400

There is little incentive for investors to push the CAD higher while the risk environment remains challenging.

Price signals are very mixed on the intraday and daily charts but the broader track high in the USD over the past month is evident and is generating bullish trend momentum signals on the shorter-term DMI signals.

Spot has found some resistance around the 200-DMA (1.3450) – in that the USD has failed to close above 1.3450 on a daily basis this week – but that barrier remains under pressure today.

There is some developing resistance above the 200-DMA at 1.3490/1.3500. Support is 1.3375/1.3400.

EUR/USD holds in tight range around the 1.10 level. Economists at Scotiabank analyze the pair’s outlook.

The outlook for the EUR remains positive in the longer run

The outlook for the EUR remains positive in the longer run but recent positioning/sentiment data has highlighted the fact that the long EUR trade is already a little crowded which may be retraining the EUR’s ability to advance without stronger incentives.

Technical pointers provide some conflicting signals for the EUR. The short-term pattern of trade looks bearish after the EUR’s strong reversal from the intraday high on Thursday. However, losses failed to develop in a meaningful way, with spot still (relatively) well-supported against rising trend and MA support in around 1.0925.

The US Dollar Index (DXY) rebound stays seen as corrective whilst below its 200-Day Moving Average (DMA), economists at Credit Suisse report.

Weekly close above 103.57 would turn the core trend neutral again

We continue to view the recent strength as temporary and corrective whilst below 200-DMA and July high at 103.47/103.57.

Below near-term support at 101.74 is needed to see the immediate risk turn lower again for a fall back to 100.55, then the 99.58/99.50 current cycle lows. Beneath here can see a test of support at the 61.8% retracement of the 2021/2022 bull trend and 200-week average at 98.98/98.30.

A weekly close above 103.57 though would be seen to turn the core trend neutral again, with resistance then seen next at 104.70 ahead of the 38.2% retracement of the 2022/2023 downtrend and YTD high from March, seen at 105.38 and 105.88 respectively.

Economists at Société Générale analyze GBP/USD technical outlook.

Support 1.2590, resistance 1.2820

GBP/USD has pulled back towards the trend line drawn since last November and is near intermittent support of 1.2590 representing the low of June. Interestingly, it has formed a Head and Shoulders pattern which generally points towards potential downside.

If the pair fails to defend the neckline at 1.2590, there could be risk of a deeper down move towards 1.2480, the 23.6% retracement from last year and 1.2300.

Left shoulder at 1.2820/1.2870 must be overcome for negating the pattern.

The recent price action denotes a reluctance to rotate away from the USD, in the view of economists at ING.

Disinflation not enough for the bears

The US remains on an encouraging disinflation track, but the Dollar is not turning lower. This is, in our view, due to a lack of attractive alternatives given warning growth signals in other parts of the world (such as the Eurozone and China).

Evidence of a US economic slowdown is needed to bring USD substantially lower.

DXY may consolidate above 102.00 over the next few days.

- USD/CHF oscillates in a wide range and fails to find a decisive move despite the US inflation data release.

- US monthly inflation grew at a 0.2% pace, in alignment with the Fed’s desired rate of 2%.

- The market mood turns cautious as US President authorized a ban on some investments in China in some sensitive technologies.

The USD/CHF pair stays in a sideways profile below the round-level resistance of 0.8800 in the European session. The Swiss Franc asset struggles to find direction despite lower-than-expected growth in the United States Consumer Price Index (CPI) data for July.

Monthly inflation grew at a 0.2% pace, in alignment with Federal Reserve’s (Fed) desired rate of 2%. The US Dollar Index (DXY) is aiming to resume its upside journey after a sideways performance ahead of US Producer Price Index (PPI) data.

The market mood turns cautious as US President Joe Biden authorized to ban some investments in China in some sensitive technologies in three sectors: semiconductors and microelectronics, quantum information technologies, and certain artificial intelligence systems.

USD/CHF traded directionless from the past week despite slower growth in the US inflation. The major turned sideways after a firmer rally after climbing above the horizontal resistance plotted from July 24 high at 0.8700, which turned into support now. The asset oscillates in a range of 0.8700-0.8783, which indicates volatility contraction.

The pair makes efforts to maintain an auction above the 20-period Exponential Moving Average (EMA) at 0.8760.

Momentum oscillator Relative Strength Index (RSI) (14) trades inside the 40.00-60.00, indicating a volatility squeeze.

Going forward, a decisive break above August 2 high at 0.8806 will drive the asset towards April 26 low at 0.8852, followed by June 16 low around 0.8900.

In an alternate scenario, a downside move below August 10 low at 0.8690 would drag the asset toward July 17 high at 0.8630 and July 27 low at 0.8552.

USD/CHF two-hour chart

The latest CPI print was a bit of a head fake for Gold markets, initially generating a rally than a drop back to the daily lows. Economists at TD Securities analyze XAU/USD outlook.

Gold to move into $2,100 territory in late 2023-early-2024

We think that Gold runs below $1,900 support from here should data remain firm and inflation edge higher due to energy.

Longer-term, however, positioning and likely aggressive action on the easing front, once data turns convincingly negative, should catalyze a robust rally that could take the yellow metal into $2,100 territory in late 2023-early-2024.

The Pound is stronger after upbeat UK GDP data. Economists at ING analyze GBP outlook.

Good GDP numbers no game-changer for the BoE

June’s growth numbers in the UK beat expectations, helping to cement a 0.2% QoQ figure for the second quarter. We believe that the implications for the Bank of England are probably quite limited, given the numbers are not far from its forecasts and the focus is firmly on services inflation and wage growth, which are both out next week.

Next week is a key one for the Pound, expect some pre-CPI positioning to dominate in GBP trading and volatility to pick up.

- The US Dollar holds on to gains for the week.

- Another batch of US inflation data is due.

- The US Dollar Index is expected to steady or advance this Friday.

The US Dollar (USD) digested a firm bearish move on Thursday after markets deemed the latest US Consumer Price Index (CPI) numbers as a clear cut case for the US Federal Reserve (Fed) to keep rates unchanged at its September meeting. The market reaction triggered weakness in the Greenback against all major currencies. As the dust settled, the US Dollar Index (DXY) recouped its losses and closed nearly unchanged, backed by some tail risks on the geopolitical front.

Yet again 12:30 GMT is the hour to watch for this Friday as another inflation gauge is set to be released: the US Producer Price Index (PPI) in monthly and yearly performances for both overall and core measures. Expectations overall are for an uptick on every measure, which could support a stronger US Dollar. Last data points of importance for the week will be at 14:00 GMT, with the Michigan Consumer Sentiment Index and inflation expectations. Interesting to see in this last number if consumers are expecting inflation to abate further.

Daily digest: US Dollar faces winds from both sides

- On the geopolitical front, there is some renewed tit-for-tat between the US and China. Torn in the eye for China was the trade deal the US and Taiwan signed, while the US issued a tech-ban on US investments towards China. Meanwhile, US president Joe Biden called China a “ticking time bomb” amidst warnings from China calling out the US to uphold current outstanding agreements and trade conditions.

- At 12:30 GMT the US Producer Price Index (PPI) data for July is to be released: On the monthly performance, both the overall and core gauge are expected to jump from 0.1% to 0.2%. On a yearly performance, the core is expected to take a small step back from 2.4% to 2.3%, and the overall to accelerate from 0.1% to 0.7%.

- At 14:00 GMT, the preliminary Michigan Consumer Sentiment Index for August is expected to stay broadly steady at 71.0 from 71.6 a month earlier. Consumers’ inflation expectations for the next five years are expected to remain unchanged at 3%.

- The US treasury is heading back to the markets to refinance some debt with a 4-week bill and a 30-year bond auction.

- A very mixed picture to close off the week on the stock markets: the Japanese Topix index closed up nearly 1%, while the Chinese Hang Seng is down 1%. European equities are all done over 0.5% and US equity futures are flat.

- The CME Group FedWatch Tool shows that markets are pricing in a 90.5% chance that the Federal Reserve will pause interest rate hikes at its meeting in September. The probability jumped from 85% on Thursday after the latest US CPI print showed inflation grew at a steady pace.

- The benchmark 10-year US Treasury bond yield trades at 4.08%, consolidating the area above 4%. Bonds are a bit less in favor, and thus require a higher yield for investors to buy as markets are baking in the end of the hiking cycle for the Fed.

US Dollar Index technical analysis: Hold the door

The US Dollar had a very volatile day on Wednesday, though saw the US Dollar bulls prevail at the US closing bell. The US Dollar rally for this summer is not over just yet and could still try to make a new high for August, depending on the Producer Price Index numbers later this Friday. Watch out for 102.80 as a line in the sand on the topside on the US Dollar Index (DXY) for more US Dollar strength next week.

For the upside, 102.80 – Tuesday’s peak – is the level to test and break in order to see some more stronger US Dollar moves. This level needs to be broken should the DXY want to try to head to 103.00. Although a bit far off still, the 200-day Simple Moving Average (SMA) at 103.41 could become the new target for next week if the DXY can continue trending higher.

On the downside, a floor is building with the 55-day and the 100-day SMA at 102.40 and 102.30, respectively. However, these levels have been chopped out quite heavily already throughout the week and could become less relevant. Should the Greenback weaken on the back of the PPI or Michigan data, the 102.00 level could come back under more downside pressure.

US Dollar FAQs

What is the US Dollar?

The US Dollar (USD) is the official currency of the United States of America, and the ‘de facto’ currency of a significant number of other countries where it is found in circulation alongside local notes. It is the most heavily traded currency in the world, accounting for over 88% of all global foreign exchange turnover, or an average of $6.6 trillion in transactions per day, according to data from 2022.

Following the second world war, the USD took over from the British Pound as the world’s reserve currency. For most of its history, the US Dollar was backed by Gold, until the Bretton Woods Agreement in 1971 when the Gold Standard went away.

How do the decisions of the Federal Reserve impact the US Dollar?

The most important single factor impacting on the value of the US Dollar is monetary policy, which is shaped by the Federal Reserve (Fed). The Fed has two mandates: to achieve price stability (control inflation) and foster full employment. Its primary tool to achieve these two goals is by adjusting interest rates.

When prices are rising too quickly and inflation is above the Fed’s 2% target, the Fed will raise rates, which helps the USD value. When inflation falls below 2% or the Unemployment Rate is too high, the Fed may lower interest rates, which weighs on the Greenback.

What is Quantitative Easing and how does it influence the US Dollar?

In extreme situations, the Federal Reserve can also print more Dollars and enact quantitative easing (QE). QE is the process by which the Fed substantially increases the flow of credit in a stuck financial system.

It is a non-standard policy measure used when credit has dried up because banks will not lend to each other (out of the fear of counterparty default). It is a last resort when simply lowering interest rates is unlikely to achieve the necessary result. It was the Fed’s weapon of choice to combat the credit crunch that occurred during the Great Financial Crisis in 2008. It involves the Fed printing more Dollars and using them to buy US government bonds predominantly from financial institutions. QE usually leads to a weaker US Dollar.

What is Quantitative Tightening and how does it influence the US Dollar?

Quantitative tightening (QT) is the reverse process whereby the Federal Reserve stops buying bonds from financial institutions and does not reinvest the principal from the bonds it holds maturing in new purchases. It is usually positive for the US Dollar.

Oil price is clearly on the rise. Economists at Société Générale analyze Brent Crude technical outlook.

200-DMA near $81 expected to be a support near term

Brent has extended its rebound after breakout from a multi-month base and has achieved the objective of $87.50 representing April high. An initial pullback can’t be ruled out however the 200-DMA near $81 is expected to be a support near term.

Daily MACD has been posting divergence and has crossed above equilibrium line denoting regain of upward momentum.

Once Brent establishes beyond $87.50, the phase of uptrend could extend towards $93 and $96.50/97.00, the 38.2% retracement from 2022.

- Gold price looks supported but needs to pass through more filters for a confident reversal.

- US inflation grew slower than forecasted in July as lower second-hand automobile prices offset rising rentals.

- US President Biden restricts some new investment in China in sensitive technologies.

Gold price (XAU/USD) is on a temporary cushion after an intense sell-off as investors hope that the modest pickup in the United States Consumer Price Index (CPI) for July is insufficient to force the Federal Reserve (Fed) to raise interest rates further in September. The precious metal attempts a recovery, but an upside isn’t warranted as investors are worried that inflation remains sticky amid rising rental prices.

US inflation rose at a steady pace of 0.2%, as expected by investors and aligned with the Fed’s required inflation rate of 2%. The recovery move in the Gold price is supported by a restricted upside in the US Dollar as chances of a rate cut in 2024 increase. San Francisco Fed President Mary Daly joined policymakers Patrick Harker and John Williams to open the door for rate cut discussions in 2024 depending on the evolution of the inflation economy.

Daily Digest Market Movers: Gold price awaits PPI data

- Gold price gauges support near $1,912.00 after a sheer sell-off. Still, the downside seems favored as United States CPI data for July showed inflation remains sticky.

- The US Consumer Price Index rose at a slower-than-forecasted pace in July. Higher rentals and a modest recovery in gasoline prices were broadly offset by the lower cost of second-hand automobiles.

- The monthly headline and core inflation grew by 0.2%, as expected by analysts.

- Core annual CPI softened to 4.7% from estimates and the prior release of 4.8%, while headline inflation accelerated modestly to 3.2% against the former release of 3.0% but remained marginally below the consensus of 3.3%.

- The 0.2% monthly increase is consistent with the Federal Reserve’s desired inflation rate of 2%.

- A modest rise in US inflation supports the Fed to keep interest rates unchanged in September’s monetary policy.

- As per the CME Group Fedwatch tool, traders see less than a 10% chance that the US will raise interest rates next month.

- The scenario of limited inflation and a historically low Unemployment Rate suggests that the US economy will manage to avoid a recession.

- On Thursday, San Francisco Fed Bank President Mary Daly joined Philadelphia Fed Bank President Patrick Harker and New York Fed President John Williams, saying that discussions about rate cuts would take place next year but will largely depend on the economy and inflation.

- The US Dollar Index (DXY) turns sideways around 102.60 after a sharp rally and awaits the July Producer Price Index (PPI) data for further direction. The PPI headline figure could show a rebound due to the recovery in gasoline prices.

- On Thursday, the US Department of Labor reported that individuals applying for jobless claims for the first time rose to 248K for the week ending August 4, higher than the 230K expected and the prior week's figure of 227K.

- The market mood remains cautious as US President Joe Biden announced restrictions on some new investments in China in sensitive technologies. Investors are worried that Beijing could retaliate.

- The long-awaited order authorizes the U.S. Treasury Secretary to prohibit or restrict U.S. investments in Chinese entities in three sectors: semiconductors and microelectronics, quantum information technologies, and certain artificial intelligence systems, Reuters reports.

- Commercial banks borrowing from the Fed’s emergency lending programs rose slightly for the week through August 9. Total lending from the two Fed backstop programs rose to $108.78 billion from $107.58B the prior week.

Technical Analysis: Gold price finds support near $1,910

Gold price rebounds after momentum oscillators on a lower timeframe reported that the bearish impulse weakened due to a decline in selling pressure. Still, for a confident reversal, the yellow metal has to pass through plenty of filters. Gold price is on tenterhooks as it has corrected to near the 200-day Exponential Moving Average (EMA) around $1,907.68. Failure to sustain above this level would likely push the precious metal into bearish territory.

Inflation FAQs

What is inflation?

Inflation measures the rise in the price of a representative basket of goods and services. Headline inflation is usually expressed as a percentage change on a month-on-month (MoM) and year-on-year (YoY) basis. Core inflation excludes more volatile elements such as food and fuel which can fluctuate because of geopolitical and seasonal factors. Core inflation is the figure economists focus on and is the level targeted by central banks, which are mandated to keep inflation at a manageable level, usually around 2%.

What is the Consumer Price Index (CPI)?

The Consumer Price Index (CPI) measures the change in prices of a basket of goods and services over a period of time. It is usually expressed as a percentage change on a month-on-month (MoM) and year-on-year (YoY) basis. Core CPI is the figure targeted by central banks as it excludes volatile food and fuel inputs. When Core CPI rises above 2% it usually results in higher interest rates and vice versa when it falls below 2%. Since higher interest rates are positive for a currency, higher inflation usually results in a stronger currency. The opposite is true when inflation falls.

What is the impact of inflation on foreign exchange?

Although it may seem counter-intuitive, high inflation in a country pushes up the value of its currency and vice versa for lower inflation. This is because the central bank will normally raise interest rates to combat the higher inflation, which attract more global capital inflows from investors looking for a lucrative place to park their money.

How does inflation influence the price of Gold?

Formerly, Gold was the asset investors turned to in times of high inflation because it preserved its value, and whilst investors will often still buy Gold for its safe-haven properties in times of extreme market turmoil, this is not the case most of the time. This is because when inflation is high, central banks will put up interest rates to combat it.

Higher interest rates are negative for Gold because they increase the opportunity-cost of holding Gold vis-a-vis an interest-bearing asset or placing the money in a cash deposit account. On the flipside, lower inflation tends to be positive for Gold as it brings interest rates down, making the bright metal a more viable investment alternative.

Economists at ING expect the EUR/USD pair to trade between 1.09 and 1.11.

Range-bound for now

Despite the benign US disinflation story, it is no surprise that markets are not flooding long EUR/USD positions. That has been an already relatively crowded trade, and the recent re-pricing of growth expectations of both growth and rate expectations in the Eurozone is weighing on the Euro’s attractiveness.

EUR/USD looks likely to keep trading range-bound (1.09-1.11) until signs of a US economic slowdown move the rate differentials back in the Euro’s favour.

USD/RUB has weakened notably in recent quarters. Currently, the Russian exchange rate is solely driven by the current-account balance. Economists at Commerzbank share their USD/RUB forecast.

Rate hikes do not have direct FX implications

Due to the sanctions, the RUB exchange rate now only reflects current account flows. Hence, the Ruble is likely to depreciate medium-term due to the declining current account surplus.

Russia’s central bank (CBR) continues to be orthodox and cautious, maintaining its former credible style of monetary policy. At least one more rate hike appears quite likely. Rate hikes, however, do not have direct FX implications at this time around.

Source: Commerzbank Research

FX option expiries for Aug 11 NY cut at 10:00 Eastern Time, via DTCC, can be found below.

- EUR/USD: EUR amounts

- 1.0800 593m

- 1.0900 1.2b

- 1.0950 1.9b

- 1.0980 1.3b

- 1.1000 1b

- 1.1025 733m

- 1.1100 995m

- GBP/USD: GBP amounts

- 1.2530 311m

- 1.2700 472m

- 1.2850 404m

- USD/JPY: USD amounts

- 141.30 1.1b

- 142.25 1.1b

- 143.00 517m

- 144.00 850m

- 145.00 755m

USD/CHF: USD amounts

- 0.8560 500m

- 0.8825 463m

- AUD/USD: AUD amounts

- 0.6530 590m

- 0.6600 882m

- 0.6675 1.5b

- 0.6700 363m

- 0.6750 1.5b

- 0.6800 1.1b

- USD/CAD: USD amounts

- 1.3320 3.8b

- 1.3400 516m

- EUR/GBP: EUR amounts

- 0.8700 400m

- EUR/JPY refreshes multi-year peak on Friday, albeit struggles to capitalize on the move.

- Intervention fears benefit the JPY and hold back traders from placing fresh bullish bets.

- The BoJ-ECB policy divergence suggests that the path of least resistance is to the upside.

The EUR/JPY cross enters a bullish consolidation phase and oscillates in a narrow trading band just below its highest level since September 2008 touched earlier this Friday. Spot prices currently trade around the 159.00 mark during the first half of the European session, nearly unchanged for the day.

Speculations that Japanese authorities might intervene in the foreign exchange markets to prop up the domestic currency hold back traders from placing fresh bullish bets around the EUR/JPY cross. Apart from this, speculations that the European Central Bank (ECB) will halt its streak of nine consecutive rate hikes in September, in the wake of easing inflationary pressures and mounting recession fears, contribute to capping the upside for the cross.

That said, a more dovish stance adopted by the Bank of Japan (BoJ), which is the only central bank in the world to maintain a negative benchmark interest rate, helps limit the downside for the EUR/JPY cross. Even the BoJ's recent policy adjustment in July, making the Yield Curve Control (YCC) policy more flexible and allowing yield on the 10-year Japanese government bond to move up toward 1%, has failed to lend support to the Japanese Yen (JPY).

Moreover, policymakers have stressed that the move was a technical tweak aimed at extending the shelf life of stimulus. Adding to this, weaker Japanese wage data released this week reaffirmed market bets that the BoJ will maintain ultra-low interest rates for the rest of the year. This marks a big divergence in comparison to a relatively hawkish ECB, which has raised borrowing costs by a combined 425 bps since last July and favours the EUR/JPY bulls.

The aforementioned supportive fundamental backdrop suggests that the path of least resistance for spot prices is to the upside. Hence, any meaningful corrective decline might be seen as a buying opportunity and is more likely to remain limited. Nevertheless, the EUR/JPY cross remains on track in the green for the second successive week and seems poised to prolong the recent appreciating move witnessed over the past two weeks or so.

Technical levels to watch

The US Dollar weakened modestly on Thursday – which is consistent with the fact that the CPI data reinforced the prospect of monetary easing in 2024, in the view of economists at MUFG Bank.

Inflation data underlines favourable outlook

We certainly saw enough in this CPI report to remain of the view that inflation is set to continue slowly drifting lower and backs up our view that it is likely at this stage that the Fed has finished its tightening cycle.

So we suspect this data will just reinforce the current range trading for the Dollar. We have in fact oscillated mostly between 100-104 in DXY since April and this CPI report is enough to maintain current market pricing on Fed rate cuts next year. That will limit the upside for the Dollar while weak growth abroad will likely limit the USD downside scope for now as well.

In its monthly oil market report, the International Energy Agency (IEA) lowers the 2024 global oil demand growth forecast to 1 million barrels per day (bpd), down 150,000 bpd from the previous forecast.

Additional takeaways

World oil demand hit a record 103 million bpd in June and August could see yet another peak.

Global oil demand is set to expand by 2.2 million bpd in 2023, steady from previous forecast.

Global oil supply plunged by 910,000 bpd July in part due to sharp reduction in saudi output.

Russian oil exports held steady at around 7.3 mbpd in July.