- Analytics

- News and Tools

- Market News

Новини ринків

“Must continue current easy policy given uncertainty over global outlook,” per the latest Summary of Opinions for Bank of Japan’s (BoJ) monetary policy meeting held in April.

Additional details

Must support wage hike momentum through monetary easing.

Achievement of price target appears to have come into sight but must maintain easy policy for time being given downside, upside risks.

Must ensure that tweak to interest rate forward guidance is not interpreted as sign BoJ would allow future rate hikes.

BoJ must be not too quick nor late in policy shift, to avoid causing sharp volatility in interest rate moves.

Closely watching outcome of BoJ’s bond market survey as YCC is causing distortion in smooth finance.

BoJ can get input that may prove useful for future conduct of monetary policy by conducting review of past 25-years of its monetary policy.

BoJ should not target specific monetary policy change when guiding policy review to ensure it would be neutral and convincing.

USD/JPY remains pressured

The dovish Summary of Opinions fail to push back USD/JPY bears as the yen pair stays depressed around 134.00 as Tokyo opens for Thursday. That said, the risk-barometer pair dropped the most in a week the previous day amid broad US Dollar weakness.

- AUD/USD grinds higher after rising to the highest level in 11 weeks.

- Market sentiment remains mildly positive amid softer US inflation, China-linked mixed clues.

- Aussie, China data can entertain intraday traders, risk catalysts are more important for clear directions.

AUD/USD resumes run-up to prod the 0.6800 round figure for the fourth time since early March as markets turn cautiously optimistic after downbeat US inflation and positive vibes from China. However, anxiety ahead of the inflation clues from Australia and China, up for publishing around 01:00 and 01:30 AM GMT, can challenge the Aussie pair buyers during early Thursday.

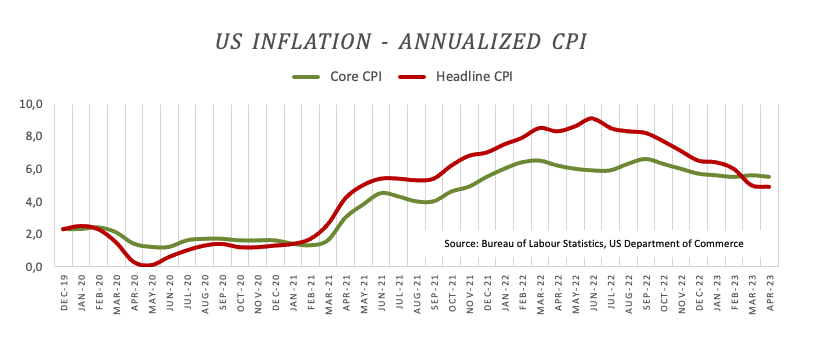

That said, the US inflation per the Consumer Price Index (CPI) eased to 4.9% YoY for April versus market expectations of reprinting 5.0% inflation mark, marking the first below 5.0% print in two years. The MoM figures, however, matched the upbeat 0.4% forecasts compared to 0.1% previous readings. Further, the CPI ex Food & Energy, known as the core CPI, matched 5.5% and 0.4% market consensus on a yearly and monthly basis respectively versus 5.6% and 0.4% priors in that order.

Following the data, Fed funds futures traders are pricing in a pause before expected rate cuts in September, per Reuters.

Elsewhere, US policymakers failed to seal the debt-ceiling deal in their first attempt but let the ball rolling by allowing office members to discuss the details and try again on Friday, which in turn prod the market sentiment. “Detailed talks on raising the US government's $31.4 trillion debt ceiling kicked off on Wednesday with Republicans continuing to insist on spending cuts, the day after Democratic President Joe Biden and top congressional Republican Kevin McCarthy's first meeting in three months,” said Reuters.

On a different page, Australian Treasurer Jim Chalmers was quoted showing readiness to establish more cordial relations with China while praising Australia’s latest annual budget released the previous day.

Alternatively, China military was quoted as rejecting a meeting proposal by the US military officials, which in turn joins the banking woes and fears of debt ceiling expiration weighing on the market sentiment and the AUD/USD prices ahead of the key Aussie-China data.

Against this backdrop, S&P 500 Futures print mild gains after Wall Street’s mixed close whereas US Treasury bond yields struggle for clear directions.

Moving on, AUD/USD traders await Australia’s Consumer Inflation Expectations for May and China’s CPI, as well as the Producer Price Index (PPI), for April ahead of the US PPI for the said month. More importantly, risk catalysts and central bankers, like the Bank of England (BoE) may offer an active day moving forward.

Technical analysis

A two-month-old ascending resistance line, around 0.6820 by the press time, restricts the short-term AUD/USD upside. That said, repeated failures to cross the 100-DMA hurdle of around 0.6800 teases the Aussie pair sellers.

“British Prime Minister Rishi Sunak risks missing his goal of halving inflation this year as underlying inflation shows little sign of having peaked in Britain or abroad,” per UK think-tank National Institute of Economic and Social Research (NIESR) reported Reuters on early Thursday in Asia.

Extra details

NIESR estimated annual consumer price inflation will be 5.4% in the final quarter of 2023 - well above forecasts from the Bank of England and the government's budget watchdog.

NIESR projected full-year consumer price inflation would be 7.4% in 2023 and 3.9% in 2024.

NIESR expects the BoE to raise its key interest rate later on Thursday to 4.5% from 4.25%, in what would be its 12th consecutive rate increase.

BoE is unlikely to bring inflation back to its 2% target until late 2025.

Sunak said in January one of his 2023 goals would be to halve inflation, which in December was 10.5% and averaged 10.7% across the final quarter of 2022.

NIESR's forecast for inflation at the end of this year is well above the 2.9% pencilled in by the Office for Budget Responsibility in March or the BoE's 3.9% projection from February, which is due for a quarterly update later on Thursday.

NIESR expects high inflation since the start of the pandemic to leave Britain's poorest fifth of households an average of 4,000 pounds ($5,000) a year worse off.

NIESR is more optimistic about the outlook for economic growth than many forecasters, predicting gross domestic product will rise 0.3% this year and 0.6% in 2024.

Also read: GBP/USD Price Analysis: Cable turns defensive above 1.2600 on BoE “Super Thursday”

- GBP/USD seesaws around the highest levels since April 2022, prods two-day uptrend.

- Clear upside break of five-week-old hurdle, firmer RSI (14) line keeps buyers hopeful.

- Weekly descending resistance line, bearish MACD signals and pre-BoE caution challenge Cable buyers.

- Bulls seek 1.2700 breakout to keep the reins; downside break of 1.2600 can lure intraday sellers.

GBP/USD bulls take a breather around 1.2630 amid the early hours of the Bank of England (BoE) inspired “Super Thursday”. That said, the Cable pair rose to a 13-month high the previous day while bouncing off the resistance-turned-support line stretched from early April.

The Pound Sterling’s recovery from the previous resistance line also gained support from the firmer RSI (14) line, not overbought. However, the bearish MACD signals and a downward-sloping resistance line from Monday, close to 1.2635 by the press time, prod the Cable buyers.

Even if the GBP/USD bulls manage to cross the 1.2635 trend line resistance, the latest high of around 1.2680 and the 1.2700 round figure may challenge the quote’s further upside.

Following that, a run-up towards the early April 2022 low surrounding 1.2975 and then to the 1.3000 psychological magnet can’t be ruled out.

On the flip side, a clear downside break of the aforementioned resistance-turned-support near 1.2600 can trigger intraday selling of the GBP/USD pair.

In that case, a three-week-long ascending trend line and the 200-SMA, respectively near 1.2500 and 1.2460, can act as the final defense of the GBP/USD buyers.

Overall, GBP/USD buyers keep the reins despite the latest inaction. However, the upside momentum needs validation from the BoE.

Also read: Bank of England Preview: A risk event for the GBP/USD rally

GBP/USD: Four-hour chart

Trend: Further upside expected

New Zealand Finance Minister Grant Robertson said on Thursday that the government budget to be released next week would have a focus on fiscal sustainability as the government does its bit to keep inflation under control, reported Reuters.

“Inflation in New Zealand is tracking at 6.7%, well above the central bank's target range of 1% to 3%, and economists have warned that a boost in government spending could mean inflation stays higher for longer,” adds the news.

On a different page, New Zealand's Food Price Index for April eases to 0.5% MoM from 0.8% prior and 0.4% market forecasts.

More comments from NZ FinMin Robertson

We are committed to playing our part in bringing it down, including by reducing our spending as a percentage of the economy over the coming years.

New Zealand's fiscal position remains strong, the country is resilient, and spending was now tracking back toward the low-30% of GDP range.

NZD/USD remains sidelined

NZD/USD edges higher to 0.6365 amid early Thursday in Asia, after refreshing a five-week top the previous day.

Also read: NZD/USD bulls step back in as Wall Street rallies

Financial Times (FT) came out with news suggesting a standoff between the US and China while turning down the hopes of a meeting among the military officials of the world’s top two economies.

“China has told the US there is little chance of a meeting between the countries’ defense ministers at a security forum in Singapore due to a dispute over sanctions, the latest obstacle to top-level dialogue between the two powers,” said FT.

The news cites difficulties in arranging a meeting of US Defense Secretary Lloyd Austin and China’s new Defense Minister Li Shangfu at the Shangri-La Dialogue security forum in Singapore in June. The reason could be linked to China’s Li being sanctioned by the US in 2018 in relation to Chinese imports of Russian arms when he was serving as a general.

Additional quotes from FT

The US has told China that the sanctions do not prevent Austin from meeting Li in a third country. But several people said it would be almost impossible for China to agree to a meeting while they remain in place. Li became Defense Minister in March.

There was no prospect of the Biden administration removing the sanctions, some of the people said.

Presidents Joe Biden and Xi Jinping agreed that the countries needed to stabilize relations when they met at the G20 in Bali in November. But early efforts to kick-start high-level engagement were derailed after a suspected Chinese spy balloon flew over North America in early February.

The countries are negotiating visits to China by Secretary of State Antony Blinken, Treasury Secretary Janet Yellen and commerce secretary Gina Raimondo.

The Pentagon said it wanted ‘open lines of communication’ with Chinese military leaders but blamed China for the impasse.

Market implications

The news challenges market sentiment and weighs on the risk-barometer pair like AUD/USD. That said, the quote remains pressured around 0.6775 after posting multiple failures to cross the 0.6800 mark.

Also read: AUD/USD bulls move in as US Dollar softens on US CPI

- EUR/JPY is down 0.45%, influenced by lackluster EUR/USD gains amidst the Japanese Yen strength.

- Technical outlook shows an evening-star pattern, suggesting potential for further downside.

- Key levels to watch: Downside support at 147.04, 145.99, and 145.67; upside resistance at 148.00 and 148.40.

The EUR/JPY weakened on Wednesday by 0.45%, dropped below the 20-day Exponential Moving Average (EMA), influenced by the EUR/USD pair, which finished up, but did not convincingly register solid gains aimed to extend the pair’s rally toward 1.1000. That and the Japanese Yen (JPY) strength were the perfect storms that weighed on the Euro (EUR). Hence, the EUR/JPY is trading at 147.49, down by 0.04% as the Asian session begins.

EUR/JPY Price Analysis: Technical outlook

The EUR/JPY printed back-to-back bearish sessions that cracked last year’s high of 148.40, extending its losses past the 20-day Exponential Moving Average (EMA). An evening-star three-candlestick pattern suggests that further downside is expected. But the Relative Strength Index (RSI) indicator remains bullish, while the 3-day Rate of Change (RoC) depicts sellers gathering momentum.

If EUR/JPY drops below the current week’s low of 147.04 and the RSI pierces the 50-midline, that will exacerbate a decline to the 50-day EMA at 145.99. A decisive break will expose the March 31 high-turned support at 145.67 before retracing to the 100-day EMA at 144.56.

Conversely, if EUR/JPY rallies and claims the 20-day EMA, it could climb above the 148.00 mark. Once cleared, the next stop would be the last year’s high of 148.40, followed by the 150.00 figure.

EUR/JPY Price Action – Daily chart

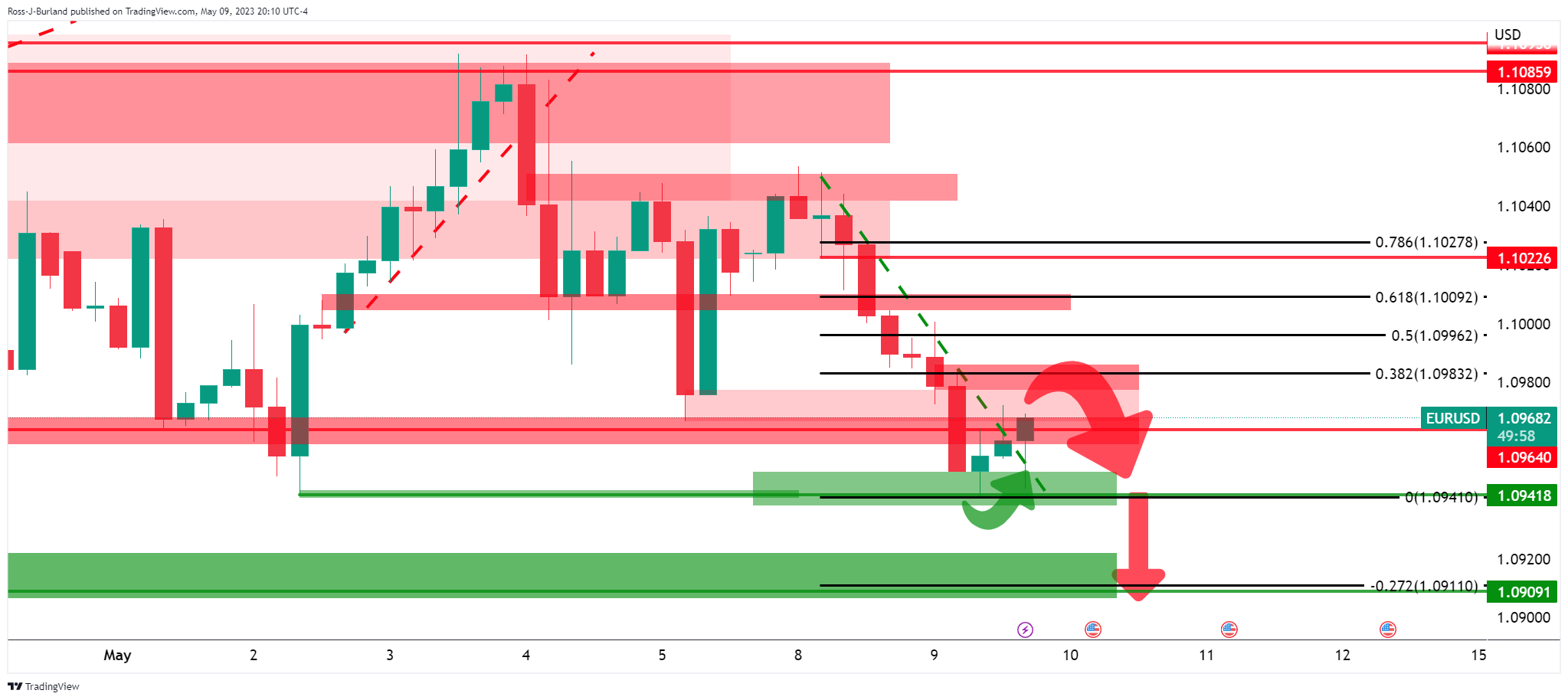

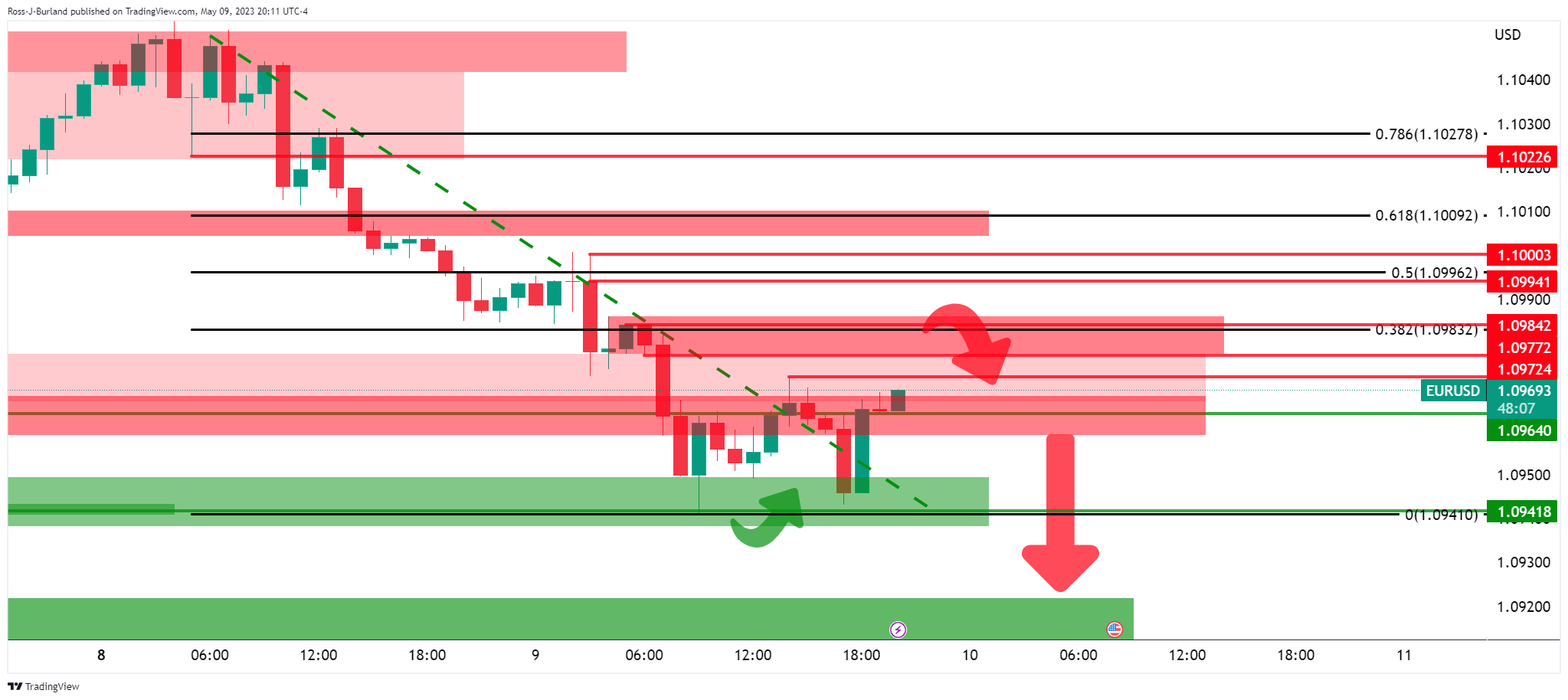

- EUR/USD bounces off three-week low amid broad US Dollar weakness, grinds higher of late.

- US inflation softens to 4.9% YoY in April, matches market forecasts and prod Fed hawks.

- ECB policymakers defend rate hikes, German inflation confirms initial estimations for April.

- More clues of US inflation, ECB policymakers’ comments and US debt ceiling updates eyed for intraday moves.

EUR/USD holds onto Wednesday’s recovery from the lowest levels in three weeks while picking up bids to 1.0985 during early Thursday morning in Asia. In doing so, the Euro pair cheers broadly softer US Dollar amid easy inflation numbers from the US, as well as the European Central Bank (ECB) officials’ hawkish comments. However, looming fears of the US default and the anxiety ahead of a few more clues of the US inflation, as well as banking woes, challenge the pair buyers amid generally inactive trading hours of the day.

On Wednesday, the US inflation per the Consumer Price Index (CPI) eased to 4.9% YoY for April versus market expectations of reprinting 5.0% inflation mark. The MoM figures, however, matched the upbeat 0.4% forecasts compared to 0.1% previous readings. Further, the CPI ex Food & Energy, known as the core CPI, matched 5.5% and 0.4% market consensus on a yearly and monthly basis respectively versus 5.6% and 0.4% priors in that order.

Considering the data, Analysts at the ANZ favored recently easing hawkish Fed bets while saying, “We think the combination of the April CPI and labor market report argue strongly against an early Fed pivot. Core monthly CPI has now been sticky at 0.4% m/m or a touch higher for the past five months and the 3m annualized pace is running in excess of 5.0%. Jobs growth is strong and the evident momentum contrasts with the much-needed slackening that is needed if the unemployment rate is to start moving towards the FOMC’s year-end forecast of 4.5%.”

On the other hand, European Central Bank (ECB) President Christine Lagarde said on Wednesday, “We still have more ground to cover in the fight against inflation.” However, ECB Governing Council member Yannis Stournaras told a Greek newspaper, “As things stand now, we can say that interest rate hikes will be over in 2023.” On the same line, ECB policymaker and Bundesbank Chief Joachim Nagel also said, “We might be approaching the final stretch of rate hikes.” Furthermore, ECB policymaker Mario Centeno was among the first to speak about rate cuts “at some point during 2024”.

Elsewhere, US policymakers failed to seal the debt-ceiling deal in their first attempt but let the ball rolling by allowing office members to discuss the details and try again on Friday, which in turn prod the market sentiment. “Detailed talks on raising the US government's $31.4 trillion debt ceiling kicked off on Wednesday with Republicans continuing to insist on spending cuts, the day after Democratic President Joe Biden and top congressional Republican Kevin McCarthy's first meeting in three months,” said Reuters.

Amid these plays, Wall Street benchmarks closed mixed while the US Treasury bond yields snapped a four-day uptrend. Further, the US Dollar Index (DXY) also printed the first daily loss in three, pressured of late.

Moving on, EUR/USD traders may seek more clues about the US inflation and hence the monthly Producer Price Index (PPI) for April, expected to ease to 2.4% YoY but the Core PPI may improve to 0.2% on MoM, will be important for intraday directions. Additionally, ECB talks and risk catalysts like US default woes and banking fallout fears can also direct the pair’s moves.

Technical analysis

Despite the latest rebound, a convergence of the 21-DMA and a one-week-old descending resistance line, around the 1.1000 round figure, restricts the short-term upside of the Euro pair.

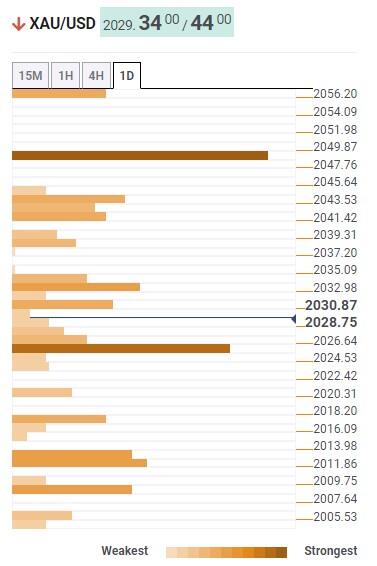

- Gold price rallies on US CPI and soft US dollar, but bears are lurking.

- Gold price is eating into the support structure on the backside of the counter-trendline.

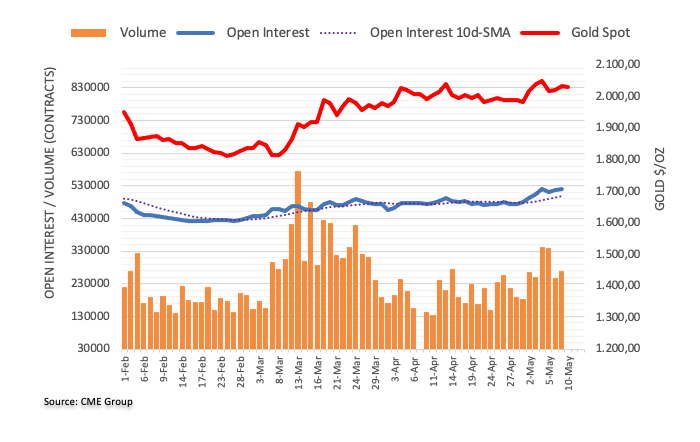

Gold price rallied towards new all-time highs with there not being any surprise in the US Consumer Price Index. XAU/USD traveled from a low of $2,025 and reached a high of $2,048 on the day.

The US Dollar ended the day lower amid lower US yields. The US Dollar Index (DXY), which measures the greenback vs. a basket of currencies, including the Aussie, ended around 101.40, as it remains above the key support of 101.00. The US 10-year Treasury yield settled at 3.43% and the 2-year at 3.90%, after reversing from near 4.10%.

Consumer inflation in the US measured by the Consumer Price Index (CPI) ticked lower in April to 4.9% from 5% in March. The Core CPI slowed down from 5.6% in March to 5.5% in April. Numbers came mostly in line with expectations. The Fed Funds rate at 5.00%-5.25% is now above the annual CPI.

´´The gravitational pull in gold markets should continue to support higher prices over the coming months,´´ analysts at TD Securities argued.

´´While CTA trend followers remain 'max long', discretionary trader interest has just started to kick off. However, given positioning within this cohort tends to lag rates market expectations for Fed funds pricing, we expect discretionary traders to deploy their hoard of dry powder in support of new all-time highs.´´

With respect to the sentiment surrounding the Fed, analysts at Brown Brothers Harriman noted that the ´´easing expectations are starting to get pared back.´´

´´At the start of last week, swaps market was pricing in a Fed Funds range between 4.0-4.25% in 12 months. Earlier, it was as low as 3.5-3.75% but now it's back in the 3.75-4.0% range in 12 months. Three cuts by year-end were fully priced in at the start of this week but the odds of a third hike have fallen to around 60% currently,´´ the analysts explained.

´´That said, market expectations of a Fed pivot are misguided and must be repriced. Fed officials are likely to continue pushing back against this dovish take but it will really be up to the data.´´

Meanwhile, markets are also concerned over the ongoing banking stress and the debt ceiling debacle. Analysts at TD Securities argued that there ´´will remain in focus, and continue to generate headwinds for the USD, especially as the global growth outlook dusts off last year’s stagflationary conditions.´´

´´Overall,´´ the analysts explained, ´´ the data continue to support our view that a new bull market in gold may have just kicked off.´´

Gold technical analysis

The Gold price 4-hour chart´s tweezer top and placement below the prior micro trendline supports, on the backside of those trends, leaves the outlook bearish for a run towards the bullish trendline support:

The hourly chart, above, shows that the price is penetrating the structure around $2,025 and the correction is decelerating. This could lead to further commitments from the bears in the coming sessions.

- US inflation data disappoints, with CPI at 4.9% YoY, below 5% projections; USD/CHF slides towards 0.8890

- SNB Governor Thomas Jordan’s hawkish comments emphasize the need for tighter monetary policy

- Federal Reserve expected to hold rates unchanged in June, with a 93.6% probability, according to CME FedWatch Tool

USD/CHF extends its bearish downtrend, though it appears to consolidate around the year-to-date (YTD) lows at around the 0.8800 handle after US data showed that prices are edging lower. In addition, hawkish rhetoric from the Swiss National Bank (SNB) Governor was cheered by USD/CHF bears. The USD/CHF is trading at around the 0.8890s area.

Swiss National Bank’s Stance on Inflation Curbs USD/CHF Rally, Pair Consolidates Near YTD Lows

Inflation has been the main narrative of Wednesday’s session. The US Bureau of Labor Statistics (BLS) revealed the Consumer Price Index (CPI) in April expanded as expected by 0.4% MoM, while annually based, the data showed an improvement with prices edging below estimates—figures came at 4.9%, below projections of 5%.

The core CPI data, which the US Federal Reserve (Fed) monitors closely to assess inflation without the volatile items, jumped by 0.4% MoM. Year-over-year (YoY) core inflation rose by 5.5%, unchanged from the last reading and aligned with the market’s consensus.

Although inflation remains high, it hurt the USD/CHF prospects of higher prices, as the major dropped from the daily highs of 0.8927 back towards the 0.8890 area. On the upside, the USD/CHF rally was capped by the 20-day EMA at 0.8892 and the psychological 0.8900 figure.

Regarding news from Switzerland, SNB Governor Thomas Jordan commented that inflation remains above average for price stability and higher than the central bank wants. Jordan added that they don’t anticipate a wage-price spiral and emphasized that monetary policy “at the moment” is not restrictive enough. He said that the Swiss Franc (CHF) nominal appreciation was sparked by inflation abroad.

Given the backdrop, the Federal Reserve is expected to hold rates unchanged at their meeting in mid-June, as shown by the CME FedWatch Tool, with odds at 93.6%. A reflection of that is US Treasury bond yields, namely the 2-year note, the most sensitive to changes in monetary policy, dropping 11 bps to 3.910%.

The SNB’s hawkish rhetoric might refrain USD/CHF bulls from entering the market. The SNB is expected to continue tightening monetary conditions as inflation in Switzerland remains above the central bank’s target.

USD/CHF Technical Levels

- AUD/USD pops higher on Wednesday on the back of improved risk appetite.

- US CPI was welcomed by markets and helped to support AUD/USD higher on the day.

AUD/USD is higher on the day by some 0.2% after traveling from a low of 0.6778 to reach a high of 0.6818 so far. Risk has bounced again in late Wall Street and that has taken the high beta currencies higher.

´´Markets reacted positively to the April CPI report, as the continued moderation in shelter inflation left the market unconvinced the FOMC will raise rates again in June,´´ analysts at ANZ Bank explained.

Consumer inflation in the US measured by the Consumer Price Index (CPI) ticked lower in April to 4.9% from 5% in March. The Core CPI slowed down from 5.6% in March to 5.5% in April. Numbers came mostly in line with expectations. The Fed Funds rate at 5.00%-5.25% is now above the annual CPI.

The US Dollar ended the day lower amid lower US yields. The US Dollar Index (DXY), which measures the greenback vs. a basket of currencies, including the Aussie, ended around 101.40, as it remains above the key support of 101.00. The US 10-year Treasury yield settled at 3.43% and the 2-year at 3.90%, after reversing from near 4.10%.

Looking ahead, domestic inflation expectations and Consumer Confidence data are due on Thursday. Traders will also pay close attention to Chinese inflation numbers (Consumer Price Index and Producer Price Index for April).

In regard to the Reserve Bank of Australia, the central bank reversed its April pause, hiking by 25 bps in May and leaving the door open to further increases. This makes for uncertainty but markets are generally of the mind that the RBA will be on hold from here.

With respect to the expectations surrounding the Federal Reserve, analysts at Brown Brothers Harriman noted that the ´´Federal Reserve easing expectations are starting to get pared back.´´

´´At the start of last week, swaps market was pricing in a Fed Funds range between 4.0-4.25% in 12 months. Earlier, it was as low as 3.5-3.75% but now it's back in the 3.75-4.0% range in 12 months. Three cuts by year-end were fully priced in at the start of this week but the odds of a third hike have fallen to around 60% currently,´´ the analysts said.

´´That said, market expectations of a Fed pivot are misguided and must be repriced. Fed officials are likely to continue pushing back against this dovish take but it will really be up to the data.´´

On Thursday, the Bank of Japan will release their summary of opinion from Ueda's first meeting. New Zealand will release the Food Price Index for April, in Australia attention would be on Melbourne Institute's Inflation Expectations survey and Westpac's Consumer Confidence. China will release April's inflation data. Markets will continue to digest US inflation data ahead of the PPI. The Bank of England will announce its decision on monetary policy.

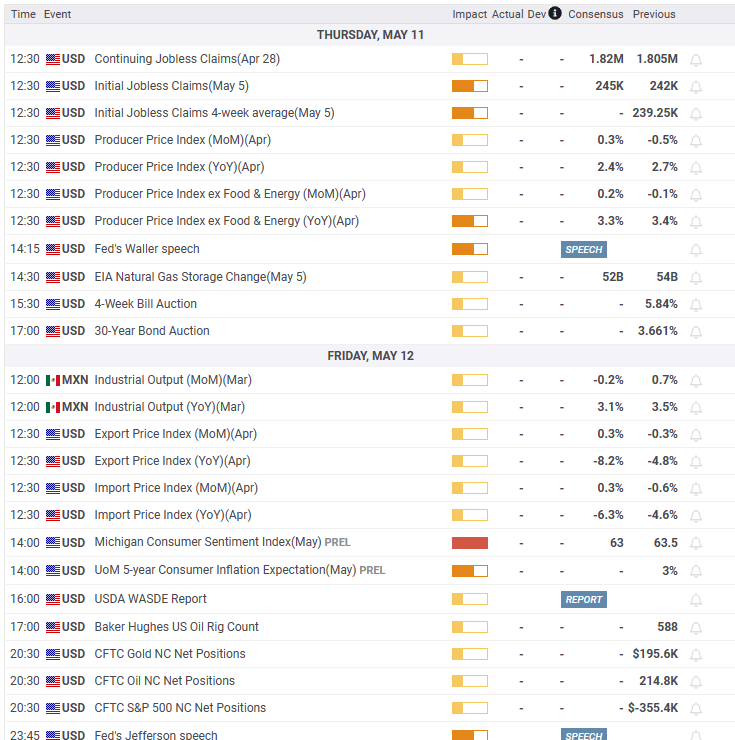

Here is what you need to know on Thursday, May 11:

Consumer inflation in the US measured by the Consumer Price Index (CPI) ticked lower in April to 4.9% from 5% in March. The Core CPI slowed down from 5.6% in March to 5.5% in April. Numbers came mostly in line with expectations. The Fed Funds rate at 5.00%-5.25% is now above the annual CPI.

Analysts at RBC commented on US CPI:

Inflation trends in the U.S. continue to head the right direction, but still have a long way to go before they reach the Fed's 2% target. Labour market conditions still look strong, but are showing cracks under the surface, and tension remains among regional banking credit markets. Increasingly, we expect the Federal Reserve will have to balance risks between sticky inflation, and slowing growth momentum / tighter financial conditions. We continue to expect the move last week to be the last one this cycle, leaving the Fed on hold until later this year.

The US Dollar initially dropped but then trimmed losses, ending the day lower amid lower US yields. The US Dollar Index (DXY) closed around 101.40, as it remains above the key support of 101.00. The US 10-year Treasury yield settled at 3.43% and the 2-year at 3.90%, after reversing from near 4.10%.

More US inflation data is due on Thursday with the Producer Price Index (PPI). Also, the weekly Jobless Claims report is due. The debt ceiling impasse continues despite everybody warning about the situation and its unnecessary costs.

EUR/USD peaked above 1.1000 but then pulled back. It continues to move sideways, above the 1.0940 support area. European Central Bank (ECB) members continue to talk about the need to raise rates further. On Wednesday, Mario Centeno was among the first to speak about rate cuts “at some point during 2024”.

GBP/USD hit fresh multi-month highs and then retreated toward 1.2600. The Bank of England (BoE) will announce its decision on monetary policy on Thursday. A 25 basis points rate hike is priced in.

USD/JPY tumbled from above 105.00 to 104.05, following US inflation data. The Bank of Japan will release the Summary of Opinions, covering Kazuo Ueda's first meeting as governor.

AUD/USD tested levels above 0.6800 but failed to hold. It continues to move with an upside bias, but limited. Inflation expectations and Consumer Confidence data is due on Thursday in Australia. Market participants will also pay close attention to Chinese inflation numbers (Consumer Price Index and Producer Price Index for April).

USD/CAD finished flat around 1.3370, as it continues to consolidate last week's losses. In Canada, Building Permits jumped 11.3% in March. The Kiwi outperformed on Wednesday. NZD/USD posted its highest daily close since early February, above 0.6350. The Food Price Index is due in New Zealand.

Gold spiked after US CPI but then pulled back, stabilizing around $2,030. Silver reversed from five-day highs near $26.00, falling under $25.50. Crude oil prices dropped 1% amid a mixed market sentiment. In Wall Street, the Nasdaq rose 1.04% while the Dow Jones lost 0.09%.

Like this article? Help us with some feedback by answering this survey:

- NZD/USD rallies as risk appetite picks up again.

- US CPI has been taken positively by the markets.

NZD/USD is higher on the day by some 0.5% after traveling from a low of 0.6324 to reach a high of 0.6381 so far. Risk has bounced again in late Wall Street and that has taken the high beta currencies higher.

´´Markets reacted positively to the April CPI report, as the continued moderation in shelter inflation left the market unconvinced the FOMC will raise rates again in June,´´ analysts at ANZ Bank explained.

´´The Kiwi put in another reasonable performance overnight, on crosses (see below) and against the USD, and according to Bloomberg, it remains the best-performing G10 currency week to date. As-expected US CPI data came as a relief to markets, and while it was enough to see US bond yields fall, the subsequent fall in equities and commodities dimmed the impact on risk currencies, with the USD DXY paring losses quickly´´ the analysts added and said further:

´´With global markets clearly in no mood to entertain the idea of more Fed hikes, the risk is we see more USD weakness, but with “Fedspeak” likely to have a hawkish bent, expect volatility. The Budget will be key for NZ next week, and today we have food prices, which might surprise some.´´

As for the Federal Reserve, analysts at Brown Brothers Harriman noted that the ´´Federal Reserve easing expectations are starting to get pared back.´´

´´At the start of last week, swaps market was pricing in a Fed Funds range between 4.0-4.25% in 12 months. Earlier, it was as low as 3.5-3.75% but now it's back in the 3.75-4.0% range in 12 months. Three cuts by year-end were fully priced in at the start of this week but the odds of a third hike have fallen to around 60% currently,´´ the analysts said.

´´That said, market expectations of a Fed pivot are misguided and must be repriced. Fed officials are likely to continue pushing back against this dovish take but it will really be up to the data.´´

Meanwhile, the Reserve Bank of New Zealand, Chrisitan Hawkesby explained at the end of April that the full impact of tightening is yet to be fully seen.

Key notes

- Early signs growth starting to slow.

- Extent of moderation will determine policy.

- Inflation too high and persisten.

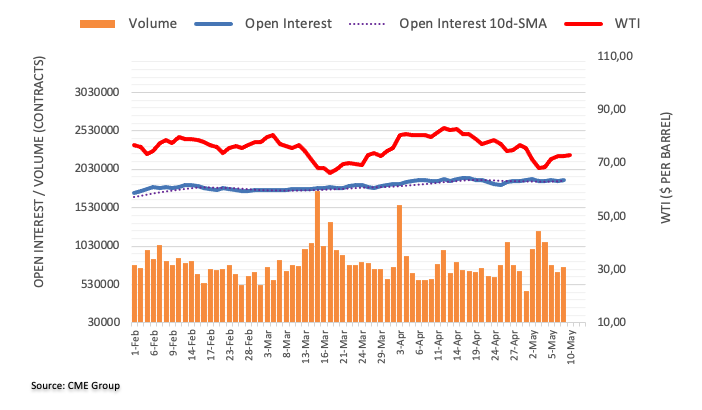

- WTI is in consolidation following a series of news events that have pressured crude prices.

- A combination of risk-off and industry data sees crude lower by over 1%.

West Texas Intermediate, WTI, crude oil is down on the day by some 1.28% after the United States reported inflation in April fell for a tenth straight month. A separate industry-related report also showed US inventories are on the rise. WTI has traveled between a high of $73.83 and a low of $71.86bbls.

Firstly, the US Consumer Price index climbed by 4.9% on an annualized basis in April, under the consensus forecast for a 5% rise, helping to lift spirits in financial markets initially. Core inflation, which excludes volatile food and fuel prices rose 5.5% from 5.6%, matching estimates. However, there was a bout of risk-off that came through late r in the day as the data shows that inflation is still well above the Federal Reserve's target.

´´Increasingly, we expect the Federal Reserve will have to balance risks between sticky inflation, and slowing growth momentum / tighter financial conditions. We continue to expect the move last week to be the last one this cycle, leaving the Fed on hold until later this year,´´ analysts at RBC Economics argued.

In other news, the United States suspended further sales from its Strategic Petroleum Reserve, and Crude oil inventories for the current week showed a build of 2.951M versus -0.917M draw.

- Following the US inflation data release, GBP/JPY sinks more than 100 pips to the 169.00 area.

- A bearish technical outlook emerges as RSI aims lower and the 3-day RoC turns negative.

The GBP/JPY slips after hitting a daily high of 171.17 after safe-haven peers advanced following the release of US inflation data. The GBP/JPY slumped more than 100 pips toward the 169.00 handle as traders anticipate another interest rate hike from the Bank of England (BoE) as it scrambles to curb inflation from around 10%.

GBP/JPY Price Analysis: Technical outlook

After snapping three days of gains, the GBP/JPY dropped toward the 169.50 region as the cross-currency pair formed a bearish-engulfing candle pattern. Although the Relative Strength Index (RSI) indicator remains in bullish territory, it continues to aim lower, suggesting buyers are losing steam ahead of the BoE’s decision. The 3-day Rate of Change (RoC) turned negative, allowing sellers to enter new positions.

If GBP/JPY drops below the 169.00 figure, the next support would be the 20-day Exponential Moving Average (EMA) at 168.33, followed by the April 19 high at 167.97. Once cleared, the GBP/JPY next demand area would be the December 20 high turned support at 167.01.

On the flip side, if GBP/JPY reclaimed the 170.00 figure, the next resistance would be May 9 daily high at 170.71. A breach of the latter will expose the May 10 daily high of 171.17, which once cleared, could pave the way to test the YTD high at 172.13.

GBP/JPY Price Action – Daily Chart

- EUR/USD sits in limbo as the US Dollar creeps higher.

- ECB and Fed sentiment is the driving force.

EUR/USD rallied on the back of the US Consumer Price Index and reached a high of 1.1006 on the day from a low of 1.0941.

US CPI and Fed implications

Headline CPI growth in the US ended lower to 4.9% in April from 5% in March. 'Core' inflation excluding food and energy products also moderated, to 5.5% from 5.6% in March. ´´April core CPI prices suggest underlying inflation is likely to remain sticky as we head into the June Federal Open Market Committee meeting, supporting our view that a final 25bp rate increase to 5.25%-5.50% remains on the table,´´ analysts at TD Securities argued. ´´However, we also acknowledge that the FOMC's decision has become especially data-dependent, with activity/banking related data gaining more prominence on the Fed's dashboard post-SVB.´´

´´Bottom line,´´ analysts at RBC Economics said, ´´inflation trends in the US continue to head the right direction, but still have a long way to go before they reach the Fed's 2% target.´´

´´Labour market conditions still look strong, but are showing cracks under the surface, and tension remains among regional banking credit markets.´´

´´Increasingly, we expect the Federal Reserve will have to balance risks between sticky inflation, and slowing growth momentum / tighter financial conditions. We continue to expect the move last week to be the last one this cycle, leaving the Fed on hold until later this year,´´ the analysts argued.

In this regard, analysts at Brown Brothers Harriman noted that the ´´Federal Reserve easing expectations are starting to get pared back.´´

´´At the start of last week, swaps market was pricing in a Fed Funds range between 4.0-4.25% in 12 months. Earlier, it was as low as 3.5-3.75% but now it's back in the 3.75-4.0% range in 12 months. Three cuts by year-end were fully priced in at the start of this week but the odds of a third hike have fallen to around 60% currently,´´ the analysts explained.

´´That said, market expectations of a Fed pivot are misguided and must be repriced. Fed officials are likely to continue pushing back against this dovish take but it will really be up to the data.´´

ECB in view

Meanwhile, the European Central Bank was later to start hiking so there is the consensus that the ECB should be later to pause. The ECB dialed back to a 25 bp hike in May but suggested further rate increases should be expected. ´´We continue to look for two more 25 bp hikes with a terminal deposit rate of 3.75%,´´ the analysts at RBC Economics argued.

´´A further slowdown in bank lending is expected to weigh on business investment in particular and we’ve lowered our euro area growth forecasts for the second half of this year and 2024,´´ the analysts said, adding:

´´But that isn’t expected to keep the ECB from delivering further rate increases in the near term. The central bank’s May policy statement implied multiple further rate hikes are needed to ensure monetary policy is sufficiently restrictive, consistent with our call for another 50 bps of tightening.´´

- USD/JPY slides 0.73% after three days of bullish action as US inflation cools down.

- The pair drops below key daily moving averages, signaling the potential for further downside.

The USD/JPY snaps three days of gains, slides below the 135.00 figure, and distanced from the 20 and 100-day Exponential Moving Average (EMA) at 134.53 and 134.24, respectively, after US inflation cooled down. The fall of the US 10-year Treasury bond yield weighed on the USD/JPY pair due to its close correlation. At the time of writing, the USD/JPY is trading at 134.22, down 0.73%.

USD/JPY Price Analysis: Technical outlook

Given that the USD/JPY dropped below crucial daily moving averages, the USD/JPY bias shifted neutral. On its way south, the USD/JPY pair fell below dynamic support levels, like the 20 and 100-day EMAs, opening the door to test the 134.00 psychological price level.

If USD/JPY breaks below the latter, the USD/JPY pair would challenge the 50-day EMA at 133.97 before testing the 200-day EMA at 133.87. A breach of the latter will expose the May 4 swing low of 133.49.

Conversely, if USD/JPY reclaims the 20-day EMA at 134.53, the next resistance would be the 135.00 figure, followed by the May 10 high of 135.47. Once cleared, the next demand area would be the May 2 high at 137.77.

Oscillators turned bearish, as the Relative Strength Index (RSI) indicator crossed below the 50-mid line, while the 3-day Rate of Change (RoC) records negative readings.

Trend: Below 135.00, further downside expected.

USD/JPY Price Chart – Daily chart

The US Treasury Department has announced that the government recorded a $178 billion surplus in April, which was below the expected $235 billion. Total receipts in April amounted $638 billion, while outlays were $426 billion.

In the same month last year, the surplus was $308 billion. So far during the fiscal year 2023, the fiscal deficit has reached $924 billion, which is $564 billion higher than the comparable period last year. The total deficit in fiscal year 2022 was $1.3 trillion.

- GBP/USD bulls are struggling in the wake of a US Dollar comeback.

- All eyes now turn to the BoE after the US CPI event on Wednesday.

GBP/USD is flat on the day after a turbulent time with the pair trading between a low of 1.2602 and a high of 1.2679. The volatility has been sparked by the US Consumer Price Index, CPI, in the New York open.

Headline CPI growth in the US ended lower to 4.9% in April from 5% in March. 'Core' inflation excluding food and energy products also moderated, to 5.5% from 5.6% in March.

´´Inflation trends in the US continue to head the right direction, but still have a long way to go before they reach the Fed's 2% target. Labour market conditions still look strong, but are showing cracks under the surface, and tension remains among regional banking credit markets,´´ analysts at RBC Economics said.

´´Increasingly, we expect the Federal Reserve will have to balance risks between sticky inflation, and slowing growth momentum / tighter financial conditions. We continue to expect the move last week to be the last one this cycle, leaving the Fed on hold until later this year.´´

Consequently, the US dollar has found a bid after the initial sell-off and this is weighing on GBP/USD in late trade in the New York session. Meanwhile, eyes will now turn to

Meanwhile, we have the next key event for GBP with the Bank of England. ´´We expect another 25bps hike in Bank Rate to 4.50%, with guidance left unchanged, meaning that the MPC will hike rates again should data justify it,´´ analysts at TD Securities said.

´´We think it will, and expect one final 25bps hike in June to a terminal of 4.75%.´´

´´Much will hinge on the US CPI report in the near-term, but keep in mind that GBP has a propensity sell-off on BoE meetings since they started to hike last year,´´ the analysts explained.

- Gold slips 0.33% as US inflation data fuels uncertainty over Fed tightening cycle.

- US Treasury bond yields drop while Biden and lawmakers continue debt ceiling discussions.

- China’s expanding gold reserves cushion XAU/USD’s fall; the market awaits Thursday’s PPI release.

Gold price slumps following the release of April’s inflation in the United States (US), which initially sent the XAU/USD to its daily high of $2048.15, though it retraced even though the US Dollar (USD) weakened on the news. Hence, the XAU/USD is trading at $2027.54, down 0.33%.

Investors eye PPI data, fed speculations, and debt ceiling talks amid market volatility

US Treasury bond yields dropped, with 2s and 10s, down eight and seven and a half bps, each at 3.935% and 3.446%, respectively. The greenback, which has an inverse correlation with Gold prices, slips 0.14%, down to 101.514.

The US Labor Department revealed the Consumer Price Index (CPI) for April continued to decelerate, as the CPI rose 0.4% MoM, aligned with estimates, while the year-over-year (YoY) came at 4.9%, below forecasts of 5%. Excluding volatile items like food and energy, the core CPI advanced 0.4% MoM, while annually based stood at around the 5.5% threshold.

Meanwhile, speculations that the US Federal Reserve (Fed) will pause its tightening cycle have increased, as shown by the CME FedWatch Tool, with odds at 95%.

On Tuesday, President Biden met with House Speaker Kevin McCarthy and other congressional leaders to discuss a possible increase or temporary stopping of the US debt ceiling. Even though there was no agreement, discussions would be held on Friday. On Monday, the US Treasury Secretary, Janet Yellen, has warned that if the debt ceiling is not raised, the government could run out of money by June 1.

As May comes to a close and if no extension is agreed upon, there will likely be an increase in overall market unease.

In other data, news that China is expanding its Gold reserves and may be abandoning the US Dollar cushioned XAU/USD’s fall. Sources cited by Kitco commented that China’s reserves increased by 8.09 tons in April.

XAU/USD Price Forecast: Technical outlook

The XAU/USD is still upward biased, though price action is forming a spinning top around the week’s highs. If XAU/USD achieves a daily close below the May 9 close of $2034.15, that could exacerbate a fall toward the day’s low at $2021.67 before testing the $2000 psychological level.

Of note, albeit at bullish territory, the Relative Strength Index (RSI) indicator aims toward a neutral level, suggesting that profit-taking took place as investors eye the release of Thursday’s Producer Price Index (PPI) release. The 3-day Rate of Change (RoC) shifted above the neutral level. Therefore, mixed signals by oscillators could refrain traders from opening fresh bets.

Data from the US released on Wednesday showed a decline in the annual Consumer Price Index in April in line with expectations. Analysts at TD Securities point out that April core CPI still suggests underlying inflation is likely to remain sticky ahead of the June FOMC meeting; they are of the view that a final 25bp rate increase to 5.25%-5.50% remains on the table.

Key Quotes:

“Consumer price inflation matched consensus expectations in April, with headline CPI rebounding 0.4% m/m. Prices in the core segment stayed firm, also advancing at a firm 0.4% m/m pace for a second consecutive month. In our view, the path for core inflation over the next few months will continue to be determined by the tug-of-war between the newfound momentum in goods prices and slowing services inflation.”

“With April core CPI prices still suggesting underlying inflation is likely to remain sticky as we head into the June FOMC meeting, we are of the view that a final 25bp rate increase to 5.25%-5.50% remains on the table. However, we also acknowledge that the FOMC's decision has become especially data-dependent, with activity/banking related data gaining more prominence on the Fed's dashboard post-SVB.”

- Silver price slides from a daily high of nearly $26.00, down nearly 1%.

- Disinflationary trends in the US economy persist, but core readings hold at 5.5% YoY.

- XAG/USD technical outlook suggests the potential for further decline, testing key support levels.

Silver price slides after hitting a daily high of $25.91, following the release of US inflation figures continued to show that the economy is in a disinflationary process. Nevertheless, core readings are clinging to the 5.5% YoY barrier, which could warrant further tightening by the Fed. The XAG/USD is trading at around $25.30s, surprisingly down almost 1%, even though the US T-bond yields and the US Dollar (USD) remained down.

XAG/USD Price Analysis: Technical outlook

The XAG/USD daily chart suggests that sellers are gathering momentum, even though the uptrend remains intact. The Relative Strength Index (RSI) indicator flashes the previously mentioned, with the RSI edging towards its neutral level, while the 3-day Rate of Change (RoC) registers volatility in negative readings.

If XAG/USD continued to trend lower would test the 20-day Exponential Moving Average (EMA) at $25.17. In a decisive break, XAG/USD sellers will target the $25.00 figure, followed by the confluence of the 15-day upslope trendline and the February 2 high, turning support at around $24.60/70. A breach of the latter, XAG would slide toward the confluence of a five-month-old previous resistance trendline now support and the 50-day EMA at 24.29/40.

Conversely, the XAG/USD could resume its uptrend once buyers step in and reclaim the May 9 daily low of $25.33. In that outcome, the first resistance would be the May 9 high of $25.67, followed by the $26.00 figure.

XAG/USD Price Action – Daily Chart

European Central Bank (ECB) Governing Council member Mario Centeno said on Wednesday that the policy will remain tight for some more time but oted that rates should start to come down at some point during 2024, as reported by Reuters.

"Monetary policy in terms of fixing key rates is at the maximum of this cycle," Centeno added.

Market reaction

These comments don't seem to be having a significant impact on the Euro's performance against its rivals. As of writing, EUR/USD was up 0.15% on the day at 1.0975.

- US Dollar regains momentum after selling off following the US CPI.

- Data shows that inflation in the US continued to slow down in April.

- USD/CAD is back at 1.3380 after hitting two-day lows at 1.3333.

The USD/CAD dropped to 1.3334 after the release of US inflation data and then bounced sharply, erasing all losses. The pair is hovering around 1.3370, flat for the day.

Focus on US inflation

In April, the Consumer Price Index (CPI) experienced a slight decline to 4.9% from its previous reading of 5% in March. Similarly, the Core rate exhibited a modest deceleration from 5.6% to 5.5%. These figures closely aligned with market expectations. Initially, the release of the US inflation data prompted a decline in the US Dollar Index, that then recovered notably, largely mitigating the post-CPI losses.

On Thursday more US inflation data is due with the Producer Price Index (PPI). Should there be further indications of inflationary pressures easing, the US Dollar could face additional downward pressure.

In Canada, Wednesday's data release revealed a remarkable surge in Building Permits for March, surpassing expectations of a 2.9% decline with a noteworthy increase of 11.3%; February's figures were revised from 8.6% to a more modest 5.5%.

Resistance at 1.3400

The USD/CAD peaked during the European session at 1.3397, but then started to move to the downside. After US data, the pair tumbled driven by the US Dollar's weakness. Later, it rebounded as the Greenback recovered ground.

Equity prices on Wall Street have receded from their recent highs, with the Dow Jones slipping by 0.39%, while the Nasdaq manages to secure a gain of 0.40%. The US 10-year Treasury yield stands at 3.45%, while the 2-year yield is falling 2% at 3.93%.

If the rebound continues, the USD/CAD will likely encounter resistance at the 1.3400 area. A successful breakthrough above this level would indicate further potential for gains. On the other hand, if it drops below 1.3350, the Loonie will likely strengthen, suggesting a test of the daily low at 1.3333 and then the May low at 1.3312.

Technical levels

- USD/MXN nosedives to levels last seen in September 2017, printing a YTD low of 17.6017.

- US inflation data triggers speculations of a pause in the Fed’s tightening cycle.

- The Mexican economy is also showing disinflation, opening the door for Banxico to maintain interest rates.

USD/MXN dives to new six-year lows last seen in September 2017, after US inflation slowed down, as shown by data revealed, triggering speculations that the US Federal Reserve (Fed) can pause its tightening cycle. At the time of writing, the USD/MXN is trading at 17.6279, down 0.81%.

US Dollar weakens against Mexican Peso amid slowing inflation and expectations of unchanged interest rates

The USD/MXN fell below its previous year-to-date (YTD) low of 17.7392 on May 8, as the news hit the screens. The US Bureau of Labor Statistics (BLS) revealed April’s data with the Consumer Price Index (CPI) rising 0.4% MoM, and 4.9% YoY, the monthly figure aligned with estimates, while annually based, edged a tick lower. Excluding volatile items, the so-called core CPI rose by 0.4% MoM as expected, while annually based, it stood at 5.5%, unchanged.

US equities are climbing as investors have begun to price in a less aggressive Fed. The CME FedWatcth Tool shows odds of almost 87% chance that Powell and Co. will hold rates unchanged at the 5.00%-5.25% range.

Therefore, US Treasury bond yields are falling sharply, with 2s down eight bps at 3.941%, while the 10-year benchmark note rate sits at 3.458%, six bps lower than the open.

On the Mexican front, data revealed on Tuesday showed that the economy is also in a disinflation process, as INEGI reported that April’s CPI rose to 6.25% from 6.85% YoY. Headline inflation shrank 0.02% MoM, while core CPI advanced 0.39% MoM, and YoY remained at 7.67%.

That opens the door for the Bank of Mexico (Banxico) to keep rates unchanged after increasing 25 bps to the TIIE, which stands at 11.25%. A poll by the local branch of Citi in Mexico, the Citibanamex poll, showed that most analysts estimate Banxico’s to keep rates unchanged.

In the meantime, discussion around the debt ceiling in the US commenced on Tuesday. According to US Senate Majority Leader Schummer, he said that Staff-level talks on the ceiling are starting today, as of May 10.

USD/MXN Price Analysis: Technical outlook

From a weekly chart perspective, the USD/MXN is headed for a continuation to lower levels, as shown by the chart. The next support would be the psychological 17.50 figure, followed by the July 2017 low of 17.4498. On the other hand, USD/MXN buyers would need to reclaim the April 2018 swing low, which turned resistance at 17.9388, ahead of the psychological 18.00 figure. A decisive break would expose the 20-week EMA at 18.4021.

Upcoming events

Economists at UBS forecast further US Dollar weakness – which could lift Gold to $2,200 by March 2024.

Position for Dollar weakness

“With the Fed opening the door to pausing rate hikes, while other central banks-including the ECB-continue tightening, we expect the US Dollar to weaken further this year as the US interest rate and growth premium erodes. The Fed is likely to cut rates sooner than other major central banks.”

“We maintain a preference for the Australian Dollar and Japanese Yen, and we see relative value in the Euro, Swiss Franc, and British Pound.”

“A weakening Dollar should also support Gold, and we forecast the yellow metal’s price rising to $2,200 by March 2024.”

EUR/GBP is already below key support from its lows for the year and 200-Day Moving Average (DMA) to suggest a top is already in place here, analysts at Credit Suisse report.

Resistance at 0.8770 set to cap

“EUR/GBP has broken key support from the series of lows for the year at 0.8729/18 as well as its 200-DMA to mark a top. We look for this to act as the catalyst for a more concerted downturn with support seen initially at 0.8648/40 ahead of the uptrend from early 2022, now at 0.8603. Whilst we would look for this to hold initially, we look for a break in due course for the ‘measured top objective’ at 0.8455.”

“Resistance at 0.8770 now ideally caps.”

- Pound Sterling vs US Dollar surges after US CPI data.

- US headline inflation numbers came out at a lower-than-expected 4.9% pace on a YoY basis.

- The data gives the broader long-term GBP/USD uptrend impetus to extend.

The Pound Sterling (GBP) rallies sharply versus the US Dollar (USD) after the release of US Consumer Price Index (CPI) data for April on Wednesday. At the time of writing, it has risen to new year-to-date highs in the 1.2670s.

The post-release surge adds fuel to the bullish long-term technical uptrend, advantaging long over short holders.

GBP/USD market movers

- US CPI inflation dips to 4.9% YoY in April, missing expectations of 5.0%. This reflects slowing inflationary pressures, and counter-intuitively weakens the US Dollar (strengthening the GBP/USD), as it makes it even more likely the Federal Reserve (Fed) will leave interest rates unchanged.

- The Pound gains versus the US Dollar due to a widening monetary policy divergence since in the UK interest rates are still expected to rise substantially higher, and currencies that have higher interest rates to benefit from greater demand.

- Apart from the headline YoY figure, the CPI release came out as expected: rising by a faster 0.4% rate MoM in April, and for Core CPI rising 0.4% MoM and 5.5% YoY.

- The Pound Sterling will be impacted by the outcome of the Bank of England (BoE) policy meeting on Thursday. A 25 bps interest rate hike is now expected with almost 100% certainty. What is less certain is the bank’s forward guidance, BoE Chairman Andrew Bailey’s comments in the press conference, and the distribution of member votes.

- The distribution of voting at the BoE’s last meeting was 7-2, with seven policymakers voting for a 25 bps rate hike and two voting for no change. If the distribution changes either way that will impact GBP with a decrease in the ‘no-change’ camp lifting GBP/USD and vice versa for an increase.

- US Treasury bond yields have risen for four consecutive days, providing the US Dollar with some support, but yields are pulling back slightly on Tuesday, which could be a slight headwind for the USD.

GBP/USD technical analysis: New leg in uptrend unfolds

GBP/USD broadly keeps extending its established uptrend making progressively higher highs and higher lows, and this is likely to continue favoring Pound Sterling longs over shorts.

-638193254332793749.png)

GBP/USD: Daily Chart

The shooting star Japanese candlestick reversal pattern on GBP/USD that formed on Monday at the new year-to-date (YTD) highs has failed to obtain confirmation. Tuesday’s bullish close shows a lack of bearish follow-through and severely reduces the validity of the reversal. The surge post-CPI has now almost reclaimed the YTD highs and further invalidated the pattern.

Given the overall trend is bullish, the exchange rate is likely to continue rallying. The May 2022 highs at 1.2665 provide the first resistance level, but once breached it opens the way to the 100-week Simple Moving Average (SMA) situated at 1.2713, and finally at the 61.8% Fibonacci retracement of the 2021-22 bear market, at 1.2758. All provide potential upside targets for the pair. Each level will need to be decisively breached to open the door to the next.

Decisive bearish breaks are characterized by long daily candles that break through key resistance levels in question and close near their highs or lows of the day (depending on whether the break is bullish or bearish). Alternatively, three consecutive candles that break through the level can also be decisive. Such insignia provide confirmation that the break is not a ‘false break’ or bull/bear trap.

It would require a decisive break below the 1.2435 May 2 lows to challenge the dominance of the uptrend and suggest the chance of a bear reversal.

The Relative Strength Index (RSI) is in the mid 60s at the time of writing after peaking in the upper 60s on May 5. This suggests a mild bearish divergence may be developing. If RSI remains below 68 at Wednesday’s close it will confirm a bearish divergence and indicate some underlying weakness. This alone, however, would not be enough evidence to conclude a reversal was in the making.

Pound Sterling FAQs

What is the Pound Sterling?

The Pound Sterling (GBP) is the oldest currency in the world (886 AD) and the official currency of the United Kingdom. It is the fourth most traded unit for foreign exchange (FX) in the world, accounting for 12% of all transactions, averaging $630 billion a day, according to 2022 data.

Its key trading pairs are GBP/USD, aka ‘Cable’, which < href="https://fxssi.com/the-most-traded-currency-pairs">accounts for 11% of FX, GBP/JPY, or the ‘Dragon’ as it is known by traders (3%), and EUR/GBP (2%). The Pound Sterling is issued by the Bank of England (BoE).

How do the decisions of the Bank of England impact on the Pound Sterling?

The single most important factor influencing the value of the Pound Sterling is monetary policy decided by the Bank of England. The BoE bases its decisions on whether it has achieved its primary goal of “price stability” – a steady inflation rate of around 2%. Its primary tool for achieving this is the adjustment of interest rates.

When inflation is too high, the BoE will try to rein it in by raising interest rates, making it more expensive for people and businesses to access credit. This is generally positive for GBP, as higher interest rates make the UK a more attractive place for global investors to park their money.

When inflation falls too low it is a sign economic growth is slowing. In this scenario, the BoE will consider lowering interest rates to cheapen credit so businesses will borrow more to invest in growth-generating projects.

How does economic data influence the value of the Pound?

Data releases gauge the health of the economy and can impact the value of the Pound Sterling. Indicators such as GDP, Manufacturing and Services PMIs, and employment can all influence the direction of the GBP.

A strong economy is good for Sterling. Not only does it attract more foreign investment but it may encourage the BoE to put up interest rates, which will directly strengthen GBP. Otherwise, if economic data is weak, the Pound Sterling is likely to fall.

How does the Trade Balance impact the Pound?

Another significant data release for the Pound Sterling is the Trade Balance. This indicator measures the difference between what a country earns from its exports and what it spends on imports over a given period.

If a country produces highly sought-after exports, its currency will benefit purely from the extra demand created from foreign buyers seeking to purchase these goods. Therefore, a positive net Trade Balance strengthens a currency and vice versa for a negative balance.

Economists at TD Securities discuss the Bank of England interest rate decision and its implications for the GBP/USD pair.

Hawkish (10%)

“The MPC hikes 25 bps but in light of the notably strong wages and inflation data, the Committee reintroduces the guidance that it expects ‘further increases in Bank Rate’ will be required if the economy evolves as expected. While the forecasts will likely show inflation being revised down in the long-term, the MPC emphasizes that the upside skew has increased further – necessitating a more aggressive policy response. GBP/USD +0.30%”

Base Case (70%)

“The MPC hikes 25 bps and leaves guidance essentially unchanged, though the language around financial and banking sector instability might be a bit softer. In doing this, the MPC essentially leaves another 25 bps hike in June on the table. The vote is likely 6/3 for 25/0, with Cunliffe joining Dhingra and Tenreyro in voting for a hold. Inflation projections will probably be tweaked slightly, though this should have limited policy implications given the substantial uncertainty bands around the projections. GBP/USD -0.15%”

Dovish (20%)

“The MPC hikes 25bps but signals a BoC-style ‘conditional pause’. Forward guidance is softened to ‘If there were to be evidence of more persistent pressures, further tightening in monetary policy would may be required’. While the latest wages and inflation data came in notably hot, the Committee emphasizes lower inflation expectation, further declines in commodity prices, and uncertainty about financial and banking sector stability as reasons why further rate hikes probably are not required. GBP/USD -0.60%”

Ahead of highly consequential presidential and parliamentary elections coming up on 14 May, and possibly extending to 28 May, Commerzbank’s FX forecasts are only symbolic for now.

Lira to ultimately break out of its recent low-volatility state if Erdogan wins

“If Erdogan wins, we expect the Lira exchange rate to ultimately break out of its recent low-volatility state produced using regulations and numerous capital controls.”

“If the opposition Nation’s Alliance wins, the market reaction will likely be sharply positive initially. But the coalition is made up of smaller parties, which came together only to oust Erdogan. The market’s enthusiasm could fade if the coalition were to run into cooperation or policy implementation challenges, which would remind markets that Erdogan can return to power.”

“Ahead of this outcome and in view of potential market dislocation, our forecasts are symbolic for now.”

Source: Commerzbank Research

- The index comes under renewed pressure on softer CPI.

- US yields reverse the multi-day recovery across the curve.

- US headline, core inflation eased further in April.

The greenback sets aside two daily gains in a row and returns to the 101.40/30 band when tracked by the USD Index (DXY) on Wednesday.

USD Index appears offered post-CPI

The index rapidly gives away earlier gains and recedes to the negative territory soon after US inflation figures printed another soft readings in April.

Indeed, inflation measured by the headline CPI rose at annualized 4.9% in April and the Core CPI climbed 5.5% over the last twelve months. On a monthly basis, both gauges rose 0.4%.

The continuation of the disinflationary way in US consumer prices sabotages the new bounce back in the greenback and motivates the USD Index (DXY) to switch ongoing increases, as the probability of a respite in the Fed's standardization cycle accumulates further footing.

Earlier in the session, MBA Mortgage Applications expanded 6.3% in the week to May 5. Later in the NA session, April’s Monthly Budget Statement will close the daily calendar.

What to look for around USD

The index now loses momentum, as earlier gains evaporate on the back of softer-than-expected US inflation prints for the month of April.

The index seems to be facing downward pressure in light of the recent indication that the Fed will probably pause its normalization process in the near future. That said, the future direction of monetary policy will be determined by the performance of key fundamentals (employment and prices mainly).

Favouring an impasse by the Fed appears the persevering disinflation – despite consumer prices remain well above the target – incipient cracks in the labour market, the loss of momentum in the economy and rising uncertainty surrounding the US banking sector.

Key events in the US this week: MBA Mortgage Applications, Inflation Rate, Monthly Budget Statement (Wednesday) – Producer Prices, Jobless Claims (Thursday) – Flash Michigan Consumer Sentiment (Friday).

Eminent issues on the back boiler: Persistent debate over a soft/hard landing of the US economy. Terminal Interest rate near the peak vs. speculation of rate cuts in 2024. Fed’s pivot. Geopolitical effervescence vs. Russia and China. US-China trade conflict. Debt ceiling issue.

USD Index relevant levels

Now, the index is down 0.21% at 101.43 and faces initial contention at 101.01 (weekly low April 26) prior to 100.78 (2023 low April 14) and finally 100.00 (psychological level). On the other hand, the break above 101.83 (weekly high May 9) would open the door to 102.40 (monthly high May 2) and then 102.80 (weekly high April 10).

- NZD/USD gains strong positive traction on Wednesday and jumps to a nearly three-month top.

- The US CPI-inspired broad-based USD weakness turns out to be a key factor boosting the pair.

- A slightly overstretched RSI on hourly/daily charts is holding back bulls from placing fresh bets.

The NZD/USD pair catches fresh bids on Wednesday, following the previous day's modest downtick, and resumes its recent upward trajectory witnessed over the past two weeks or so. The momentum picks up pace following the release of the latest US consumer inflation figures and lifts spot prices to a nearly three-month high, around the 0.6380 region during the early North American session.

The US Dollar (USD) weakens across the board after the US Bureau of Labor Statistics reported that inflation in the US, as measured by the Consumer Price Index (CPI) rose 0.4% in April and the yearly rate eased to 4.9% from 5%. Meanwhile, the Core CPI, which excludes volatile food and energy prices, came in at 0.4% and 5.5% on monthly and yearly basis, respectively. In the absence of any upside surprise, the data reaffirms expectations for an imminent pause in the Federal Reserve's (Fed) year-long rate-hiking cycle, which, in turn, weighs heavily on the buck and provides a strong boost to the NZD/USD pair.

The markets, meanwhile, have also started pricing in the possibility that the US central bank will start cutting interest rates later this year, which, along with concerns about the US debt ceiling, leads to a fresh leg down in the US Treasury bond yields. It is worth recalling that US President Joe Biden and House of Representatives Speaker Kevin McCarthy remained divided over raising the $31.4 trillion US debt limit, though agreed to continue talks aimed at breaking the deadlock. Apart from this, a positive risk tone is seen undermining the safe-haven Greenback and benefitting the risk-sensitive Kiwi.

The New Zealand Dollar (NZD) draws additional support from expectations for further rate hikes by the Reserve Bank of New Zealand (RBNZ). This, in turn, suggests that the path of least resistance for the NZD/USD pair is to the upside. That said, the Relative Strength Index (RSI) on hourly and daily charts has moved on the verge of breaking into the overbought territory. This, in turn, prompts some profit-taking and leads to a modest pullback of around 30 pips in the last hour. Nevertheless, the aforementioned supportive fundamental backdrop should limit any meaningful corrective decline.

Technical levels to watch

- US Consumer Price Index rises 0.4% in April, in line with market estimates.

- US Dollar tumbles across the board after the report.

- AUD/USD jumps to 0.6817 and then trims gains.

The AUD/USD pair jumped to 0.6817 after US April inflation data. The pair then pulled back and after Wall Street’s opening bell, it is hovering around 0.6790, up almost 40 pips for the day.

USD tumbles after US inflation

Data release in the US revealed that the US Consumer Price Index (CPI) rose 0.4% in April, in line with expectations, and 4.9% YoY, slightly below the 5% of market consensus. The Core CPI rose 0.4% and the annual rate edged lower from 5.6% to 5.5%, both matching market consensus. On Thursday, the April Producer Price Index (PPI) is due. More evidence of slowing inflation could weigh further on the US Dollar.

The US Dollar Index dropped to 101.21 and then rebounded to 101.40 as US yields moved off lows. Commodity prices soared and then pulled back. In Wall Street, the Dow Jones is up by 0.29% and the Nasdaq gains 1.03%.

The AUD/USD holds a bullish tone, however it is pulling back after being rejected again from above 0.6800. The Aussie needs to hold firm above that area to open the doors to more gains. On the flip side, support emerges at 0.6770 followed by 0.6745.

Technical levels

Economists at TD Securities expect Gold price to trend higher toward new all-time records after the US inflation report came in line with expectations.

No surprises from the inflation report

“With no surprises from the inflation report, the countdown towards new all-time highs in Gold markets continues.”

“The gravitational pull in Gold markets should continue to support higher prices over the coming months.”

“Ongoing banking stress and the debt ceiling debacle will remain in focus, and continue to generate headwinds for the USD, especially as the global growth outlook dusts off last year’s stagflationary conditions.”

- GBP/USD gains strong positive traction on Wednesday and spikes to a fresh one-year top.

- The USD weakens following the release of the US CPI report and provides a goodish boost.

- Traders now await the key BoE decision on Thursday before placing fresh directional bets.

The GBP/USD pair catches aggressive bids during the early North American session and rallies to a fresh one-year high, around the 1.2675 region following the release of the latest US consumer inflation figures.

The US Bureau of Labor Statistics reported that inflation in the US, as measured by the Consumer Price Index (CPI) rose 0.4% in April and the yearly rate eased from 5% to 4.9% - the smallest rise since April 2021. Meanwhile, the Core CPI, which excludes volatile food and energy prices, came in at 0.4% MoM and 5.5% YoY, down from 5.6% previous and matching expectations. This further points to signs of easing inflationary pressures and reaffirms market bets for an imminent pause in the Federal Reserve's (Fed) rate-hiking cycle, which, in turn, weighs on the US Dollar (USD) and provides a goodish lift to the GBP/USD pair.

The markets, meanwhile, have also started pricing in the possibility that the US central bank will start cutting interest rates later this year. This is evident from a fresh leg down in the US Treasury bond yields, which, along with a generally positive tone around the equity markets, undermines the safe-haven Greenback. The British Pound, on the other hand, continues to draw support from rising bets for another 25 bps lift-off by the Bank of England (BoE) on Thursday. This is seen as another factor that boosts the GBP/USD pair and contributes to the strong intraday rally to its highest level since April 2022.

It, however, remains to be seen if bulls can capitalize on the move or opt to take some profits off the table ahead of the central bank even risk - the highly-anticipated BoE monetary policy meeting scheduled on Thursday. Even from a technical perspective, any subsequent move is more likely to confront some resistance near the top boundary of over a one-month-old ascending trend channel, currently pegged just ahead of the 1.2700 round-figure mark. Nevertheless, the aforementioned fundamental backdrop suggests that the path of least resistance for spot prices is to the upside and supports prospects for further gains.

Technical levels to watch

Alvin Liew, Senior Economist at UOB Group, assesses the latest publication of US Nonfarm Payrolls.

Key Takeaways

“US job creation again exceeded expectations with 253,000 jobs added in Apr while the jobless rate receded to the multi-decade low of 3.4% (Mar: 3.5%), as the unemployed numbers fell by 182,000 to 5.7 million and participation rate held at 62.6%. Wage growth pace was also above forecast, and faster than the previous month, at 0.5% m/m, 4.4% y/y.”

“After the 25-bps hike in the May FOMC, we had assigned a high probability the Fed will pause thereafter. We continue to expect no rate cuts in 2023, with the FFTR terminal rate at 5.25% lasting through this year.”

“Admittedly, the US Apr job creation, unemployment rate and wage growth were stronger than expected, which highlight the resilience of US labor market despite the aggressive Fed rate hikes and put doubts on the call that the Fed have reached a pause.”

- EUR/USD regains upside traction and looks at 1.1000.

- Final CPI in Germany rose 7.2 YoY, 0.4% MoM in April.

- US headline CPI dropped more than expected in April.

Sellers now hit the Greenback and help EUR/USD regain upside traction and re-shift the focus to the key barrier at 1.1000 the figure on Wednesday.

EUR/USD picks up pace on soft US CPI

EUR/USD reclaims ground lost earlier in the European session and returns to the positive territory near the key 1.1000 barrier.

Indeed, the pair manages to gather extra steam on the back of the bout of selling pressure in the Buck after US inflation figures showed disinflationary pressures continue to build in the economy.

On the latter, inflation tracked by the headline CPI rose 4.9% in the year to April and held steady at 5.5% when it comes to the Core CPI, which excludes food and energy costs.

Earlier in the domestic calendar, final inflation figures in Germany saw the CPI rise 7.2% in the year to April and 0.4% vs. the previous month. In addition, Industrial Production in Italy contracted 0.6% MoM in March and 3.2% from a year earlier.

What to look for around EUR

EUR/USD looks to regain some fresh buying interest following CPI-led weakness in the US dollar on Wednesday.

The movement of the euro's value is expected to closely mirror the behaviour of the US Dollar and will likely be impacted by any differences in approach between the Fed and the ECB with regards to their plans for adjusting interest rates.

Moving forward, hawkish ECB-speak continue to favour further rate hikes, although this view appears in contrast to some loss of momentum in economic fundamentals in the region.

Key events in the euro area this week: Germany Final Inflation Rate (Wednesday).

Eminent issues on the back boiler: Continuation (or not) of the ECB hiking cycle. Impact of the Russia-Ukraine war on the growth prospects and inflation outlook in the region. Risks of inflation becoming entrenched.

EUR/USD levels to watch

So far, the pair is gaining 0.28% at 1.0989 and faces the next up-barrier at 1.1095 (2023 high April 26) would target 1.1100 (round level) en route to 1.1184 (weekly high March 21 2022). On the other hand, the next contention level aligns at 1.0941 (monthly low May 2) followed by 1.0909 (weekly low April 17) and finally 1.0831 (monthly low April 10).

- US Consumer Price Index rises 0.4% in April, matching market consensus.

- US Dollar Index tumbles after the report as US yields decline.

- XAU/USD jumps to highest since Friday, looking at $2,050.

Gold Price jumped following the release of US consumer inflation and the US Dollar dropped sharply across the board. XAU/USD rose from $2,030/oz to $2,045, reaching the highest level since Friday. Silver also soared, approaching $26.00.

The US Consumer Price Index (CPI) showed inflation rate was 0.4% in April, in line with expectations, and 4.9% YoY, slightly below the 5% of market consensus. The Core CPI rose 0.4% and the annual rate edged lower from 5.6% to 5.5%, both matching market consensus.

Following the numbers, the US Dollar Index turned negative, falling under 101.50. US Treasury bond yields also collapsed, with the 10-year falling to 3.45% from 3.50% and the 2-year to 3.94%.

XAU/USD is trading near the highs, looking at the $2,050 area, boosted by the weaker Dollar and also lower US yields. Above $2,050, attention would turn to the record highs in the $2,075/80 area. The immediate resistance now stands at $2,035.

Technical levels

- USD/JPY retreats sharply from a one-week high amid the emergence of fresh USD selling.

- The softer headline US CPI print reaffirms dovish Fed expectations and weighs on the USD.

- A positive risk tone could undermine the safe-haven JPY and help limit losses for the pair.

The USD/JPY pair attracts some sellers in the vicinity of mid-135.00s, or a one-week high touched this Wednesday and the intraday descent picks up pace following the release of the US consumer inflation figures. Spot prices drop to a fresh daily low during the early North American session and currently trade just above the mid-134.00s, down over 0.50% for the day.

The US Dollar (USD) weakens across the board after the US Bureau of Labor Statistics reported that inflation in the US, as measured by the Consumer Price Index (CPI) rose 0.4% in April and the yearly rate eased to 4.9% from 5%. Meanwhile, the Core CPI, which excludes volatile food and energy prices, matched expectations, coming in at 0.4% and 5.5%, respectively, Nevertheless, the data reaffirms market bets for an imminent pause in the Federal Reserve's (Fed) year-long rate-hiking cycle, which weighs heavily on the Greenback and exerts downward pressure on the USD/JPY pair.

That said, the Bank of Japan's (BoJ) dovish stance, along with a generally positive tone around the equity markets, could undermine the safe-haven Japanese Yen (JPY) and help limit losses for the USD/JPY pair. It is worth recalling that BoJ Governor Kazuo Ueda, speaking in parliament earlier today, said that it was too early to discuss specific plans for an exit from the massive stimulus programme. This, in turn, might hold back bearish traders from placing aggressive bets and act as a tailwind for spot prices, making it prudent to wait for strong follow-through selling before positioning for further losses.

Technical levels to watch