- Аналітика

- Новини та інструменти

- Новини ринків

Новини ринків

- WTI gains momentum above the $83.00 mark, the highest level since November 2022.

- Crude oil stockpiles came in at 5.85M (Aug. 4), higher than the market consensus of 0.567M.

- Oil traders will monitor July’s Consumer Price Index (CPI), due on Thursday.

Western Texas Intermediate (WTI), the US crude oil benchmark, is trading around the $83.60 mark so far on Thursday, the highest level since November 2022. An unanticipated increase in EIA crude oil inventories alleviated concerns about China's sluggish demand.

That said, the concern about the economic slowdown in China exerts pressure on WTI prices as China is the major oil consumer in the world. The Chinese inflation data on Wednesday showed the Chinese Consumer Price Index (CPI) YoY fell 0.3% in July from 0% prior, and the market consensus anticipated a -0.4% decline. Meanwhile, the Producer Price Index (PPI) declined 4.4% YoY, compared to the 4.1% decrease YoY expected and a 5.4% drop prior. Additionally, China's crude oil imports in July decreased 18.8% from the previous month to the lowest daily rate since January.

However, a steep drawdown in US crude oil inventories boosts WTI prices. The Energy Information Administration (EIA) showed on Wednesday that crude oil stockpiles came in at 5.85M for the week ending August 4, higher than the market consensus of 0.567M. Meanwhile, Baker Hughes reported that the number of US rigs decreased to 525 for the week of August 4, 2023, from 623 in the week ending January 13, 2023.

Furthermore, the recent recovery in WTI is driven by prolonged voluntary limits in Saudi Arabian output as well as increased global demand. Last week, Saudi Arabia announced it would extend its voluntary oil output cut of one million barrels per day (bpd) through September. In the meantime, Russia's oil exports will also decrease by 300,000 bps in September.

Oil traders will closely watch July’s Consumer Price Index (CPI), due on Thursday. The inflation figure is expected to rise from 3% to 3.3%, and the core inflation figure is expected to stay at 4.8%. These events could significantly impact the USD-denominated WTI price. Oil traders will take cues from the data and find trading opportunities around the WTI price.

- GBP/USD remains on the back foot inside one-week-old symmetrical triangle.

- Sustained trading below 50-SMA, short-term bearish trend channel and steady RSI lure Cable sellers.

- Pound Sterling bulls need upside break of 1.2785, backed by softer US inflation, firmer UK Q2 GDP, to retake control.

GBP/USD seesaws around 1.2720 while portraying the pre-data anxiety on early Thursday, after declining in the last two consecutive days.

Apart from the cautious mood ahead of the US Consumer Price Index (CPI) for August, the preliminary readings of the UK’s second quarter (Q2) Gross Domestic Product (GDP), the Cable pair also justifies an absence of major data/events during the Asian session. With this, the Pound Sterling stays within a one-week-old symmetrical triangle, currently between 1.2700 and 1.2785.

Also read: GBP/USD slumps below 50-DMA ahead of US inflation, UK’s GDP figures

Even if the aforementioned catalysts restrict the GBP/USD pair’s immediate moves, the quote’s sustained trading below the 50-SMA, as well as within a three-week-old bearish channel, joins the steady RSI (14) to keep sellers hopeful.

However, a clear break of 1.2700 becomes necessary for the Cable bears to visit June’s bottom of around 1.2590.

Following that, the stated channel’s bottom line, close to 1.2550 at the latest, could challenge the Pound Sterling sellers.

Meanwhile, the 50-SMA surrounding 1.2760 restricts the immediate upside of the GBP/USD pair ahead of the 1.2780-85 resistance confluence including the top lines of the stated triangle and the channel.

In a case where the GBP/USD manages to cross the 1.2785 hurdle, the odds of witnessing a rally towards the late July swing high of around 1.3000 can’t be ruled out.

GBP/USD: Four-hour chart

Trend: Further downside expected

Late Wednesday, US President Joe Biden signed the much-awaited bill that allows the US Treasury Department to prohibit or restrict certain US investments in Chinese entities, per Reuters.

The three key technology sectors mentioned in the executive order are semiconductors and microelectronics, quantum information technologies, and certain Artificial Intelligence (AI) systems.

The news also cites US President Biden as declaring a national emergency to deal with countries like China "in sensitive technologies and products critical to the military, intelligence, surveillance, or cyber-enabled capabilities."

It’s worth noting that the bill was edited to soften the restrictions for China technology companies on a revenue generation basis. Bloomberg previously came out with the news suggesting the hardships for only those Chinese companies that get more than 50% of revenue from the sectors including quantum computing and artificial intelligence (AI) to be included in the list.

Market reaction

Trading sentiment remains mostly unchanged on the news as most market players were aware of the outcome. Also restricting the reaction to the news could be the trader’s wait for the US inflation data.

Also read: AUD/USD stays depressed below 0.6550 ahead of Australia/US inflation clues

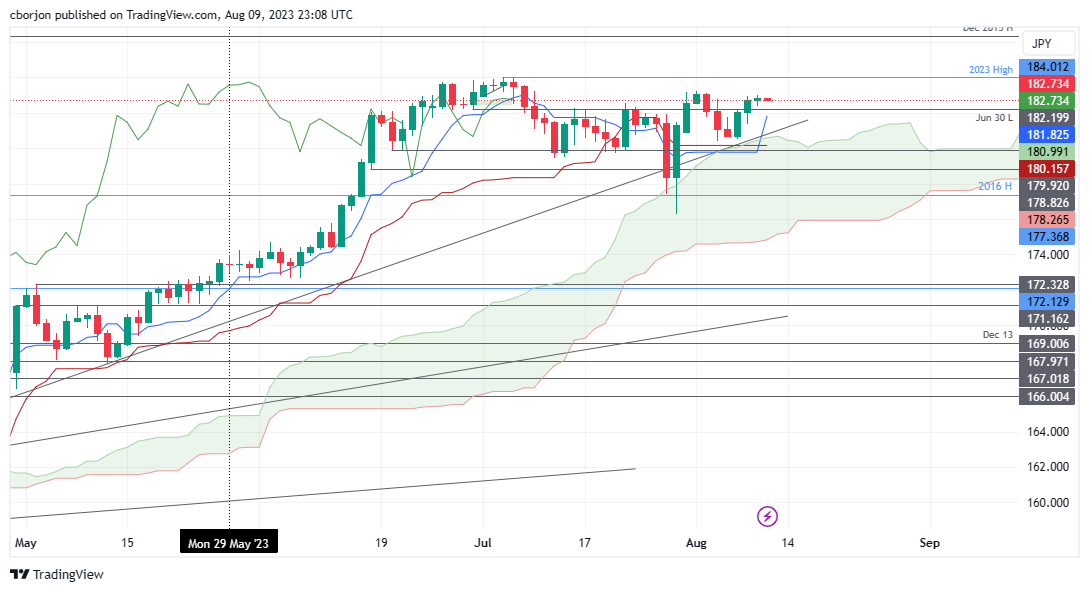

- Despite a brief touch at 183.01, the GBP/JPY remains anchored below the 183.00 psychological resistance.

- Key resistance lies at last week’s high of 183.24, and surpassing this could put YTD high of 184.01 into focus.

- Support levels to watch include the August 9 low at 182.36, Tenkan-Sen at 181.82, and an established support trendline from April's lows around 180.80/95.

GBP/JPY consolidates around the weekly highs of 182.70s and prints a small candlestick, suggesting the uptrend is losing steam, despite reaching a fresh weekly high of 183.01. However, as the Asian session began, the GBP/JPY exchanged hands at 182.69, well below 183.00, after the Tenkan-Sen crossed above the Kijun-Sen level.

GBP/JPY Price Analysis: Technical outlook

From a technical perspective, the GBP/JPY remains neutral to upward bias but must reclaim the last week’s high of 183.24 to threaten the year-to-date (YTD) high of 184.01. Even though the bullish cross of the Tenkan-Sen above the Kijun-Sen portrays the GBP/JPY as bullish, further confirmation is expected.

Otherwise, if GBP/JPY dives below the August 9 low of 182.36, it would exacerbate a pullback towards the top of the Ichimoku Cloud (Kumo). The GBP/JPY’s first support would be the Tenkan-Sen at 181.82, followed by a support trendline drawn from the lows of April, at 180.80/95, before slumping towards the Kijun-Sen at 180.15, inside the Kumo.

GBP/JPY Price Action – Daily chart

- EUR/USD remains sidelined after snapping a two-day losing streak the previous day.

- US Dollar prints corrective pullback amid market’s preparations for the key data/events, as well as due to downbeat yields.

- Downbeat US mortgage applications, increasing bets on Fed policy pivot tame fears about German recession, Italy tax woes.

- ECB’s monthly bulletin will clarify bloc’s economic conditions, upbeat US inflation eyed to recall Fed hawks.

EUR/USD aptly portrays the pre-data anxiety as it seesaws around 1.0975-80 during the early hours of Thursday’s Asian session, struggling to extend the previous day’s corrective bounce from the weekly low. In doing so, the Euro pair justifies the mixed catalysts surrounding the US and Eurozone amid the looming fears of softer US inflation and the bloc’s recession woes, not to forget China deflation. Furthermore, the downbeat concerns about the European Central Bank (ECB) and the Federal Reserve (Fed) and prod the major currency pair, especially when the US Dollar retreats.

US Dollar Index (DXY) marked the first daily loss in three despite witnessing a corrective bounce by the end of Wednesday’s North American session to around 102.50. In doing so, the greenback’s gauge consolidates the weekly gains amid downbeat US MBA Mortgage Applications, as well as softer US Treasury bond yields.

On Wednesday, the US MBA Mortgage Applications dropped for the third consecutive week by posting -3.1% fall for the week ended on August 04, versus -3.0% prior. It’s worth noting that the solid mortgages previously fuelled the housing market and inflation, which in turn allowed the Fed to defend its hawkish bias.

Apart from the likely challenges to the Fed hawks, Biden Administration’s relief to China technology companies also helped ease the fears surrounding the Dragon Nation, joined by unimpressive China inflation data, to weigh on the US Dollar. “The US plans to target only those Chinese companies that get more than 50% of revenue from the sectors including quantum computing and artificial intelligence (AI),” said the news.

That said, an improvement in China’s Producer Price Index (PPI) for July superseded negative readings of the Consumer Price Index (CPI) for the said month. That said, CPI declines to -0.3% YoY versus -0.4% YoY expected and 0.0% prior whereas the PPI improves to -4.4% YoY compared to -4.1% YoY market forecasts and -5.4% previous readings.

Elsewhere, the CME Group FedWatch Tool shows that markets are pricing in an 86.5% chance that the Federal Reserve will pause interest rate hikes at its meeting in September.

At home, Italy’s surprise tax on windfall profits of banks joined previously released German statistics to suggest the looming recession in the bloc’s powerhouse. Further, the global rating agencies’ downward revision to the US banks and financial institutions weighs on the risk sentiment and the EUR/USD price despite the latest corrective bounce. On the same line could be fears of the UK recession and slowing economic growth in China, not to forget the Dragon Nation’s geopolitical tension with the US and Japan about Taiwan.

Against this backdrop, Wall Street closed on the negative side despite the downbeat performance of the US Treasury bond yields.

Moving on, the ECB’s monthly Economic Bulletin will be eyed closely amid economic fears surrounding the old continent, which if confirmed can recall the Euro bears. However, the reaction might be limited as traders are more interested in the United States inflation data, per the Consumer Price Index (CPI) for July. Market forecasts suggest an improvement in the headline CPI to 3.3% YoY versus 3.0% prior while the Core CPI, namely the CPI ex Food & Energy, may remain unchanged at 4.8%.

Also read: US CPI Preview: Forecasts from 10 major banks, monthly pace should hold at 0.2%

Technical analysis

EUR/USD bulls need a clear upside break of a one-month-old descending resistance line surrounding 1.0970, as well as the 10-DMA level of around 1.0980, to keep the reins.

- USD/CHF remains confined in a narrow range below the 0.8800 mark on Thursday.

- Money market futures do not anticipate higher borrowing rates.

- Investors will closely watch the US Consumer Price Index (CPI) for July.

The USD/CHF pair remains range-bound around 0.8770 in the early Asian session. Meanwhile, the US Dollar Index (DXY), a measure of the value of USD against six other major currencies, trades mixed and remains above 102.40 on Thursday. Market participants await key US inflation data for fresh impetus.

On Tuesday, US trade data showed a sluggish economic rebound and subdued global demand in the country. The US trade deficit narrowed sharply in June, with the figure coming in at $65.5 billion, higher than expectations of $65 billion and below the $68.3 billion prior.

Additionally, Imports fell 1.0% to $313 billion from $316.1 billion the previous month, the lowest level since November 2021. The Commerce Department reported that a drop in Imports on Tuesday might indicate a slowdown in company investment and domestic demand despite the Federal Reserve's significant interest rate rises. Meanwhile, Exports dropped 0.1% to $247.5 billion, a 15-month low.

According to the CME FedWatch Tool, the odds for a rate hike in September are 13.5%. Money market futures do not anticipate higher borrowing rates. Nevertheless, the dovish stance from Fed officials might cap the upside in the US Dollar and act as a headwind for the USD/CHF pair.

On the Swiss front, the State Secretariat for Economic Affairs (SECO) revealed on Monday that the Swiss Unemployment Rate came in at 1.9% in July, matching expectations. The figure remained unchanged compared to the June reading and marked its lowest level since October 2022.

In the absence of the economic data release from Switzerland, the US Consumer Price Index (CPI) for July will be in the spotlight this week. The figure is expected to rise from 3% to 3.3%, and the core rate is forecast to stay at 4.8%. Also, the weekly Jobless Claims will be due on Thursday. Market participants will keep an eye on the data and find trading opportunities around the USD/CHF pair.

- AUD/USD holds lower ground at multi-day bottom after declining in the last two consecutive days.

- Sour sentiment, fears about China weigh on Aussie despite US Dollar’s retreat.

- Australia Consumer Inflation Expectations for August, US CPI for July will be crucial to recall RBA, Fed hawks.

AUD/USD bears take a breather at the lowest level in two months, marked earlier in the week, as markets brace for the all-important Australia and US inflation clues during early Thursday morning in Canberra. In doing so, the Aussie pair licks its wounds near 0.6530 after declining in the last two consecutive days to refresh the 10-week low. It’s worth noting that the pre-data anxiety prods the momentum traders but the fears about China, Australia’s biggest customer, to exert downside pressure on the quote.

Markets remained mostly downbeat on Wednesday, despite the initial improvement, as fresh geopolitical and banking sector fears contrast with an intermediate relief to China. Even so, the traders’ rush towards the bonds could be witnessed and the same drowned the yields, as well as other riskier assets like equities, Gold and Antipodeans like AUD/USD.

Additionally, looming fears about the Aussie economy also weigh on the AUD/USD price. The S&P Global came out with its economic assessment of the Pacific major on Wednesday and said, “It is possible, but not certain, that the Australian economy can manage a ‘soft landing’ with inflation decreasing to the RBA’s target range.” “The key risk is that inflation in Australia is more sticky than expected and the RBA has to hike interest rates more strongly,” added the global rating and research house.

Further, the looming bankruptcy of the Dragon Nation’s biggest private real estate company, namely the Country Garden, as it has less than 30 days after the initial default on paying the bond coupons in early August, also weighs on the AUD/USD. Further, the recent China deflation and receding activity data join the nation’s geopolitical tussles with the US, and recently with Japan, to weigh on the economic outlook for China and weigh on the Aussie pair.

Even so, better-than-forecast China inflation data, despite marking the deflation, and the US Dollar Index (DXY) pullback from a one-month high can’t be cheered by the AUD/USD traders. An improvement in China’s Producer Price Index (PPI) for July superseded negative readings of the Consumer Price Index (CPI) for the said month. That said, CPI declines to -0.3% YoY versus -0.4% YoY expected and 0.0% prior whereas the PPI improves to -4.4% YoY compared to -4.1% YoY market forecasts and -5.4% previous readings.

Apart from China’s economic issues, Biden Administration also signaled relief to China technology companies and tamed the previous risk-off mood initially on Wednesday. “The US plans to target only those Chinese companies that get more than 50% of revenue from the sectors including quantum computing and artificial intelligence (AI),” said Bloomberg News.

Furthermore, the increasing odds of witnessing the US Federal Reserve’s (Fed) policy pivot challenges the US Dollar bulls and should have favored the Gold Price, but could not. That said, the CME Group FedWatch Tool shows that markets are pricing in an 86.5% chance that the Fed will pause interest rate hikes at its meeting in September.

Looking ahead, Australia’s Consumer Inflation Expectations for August will offer immediate directions to the AUD/USD pair ahead of the US inflation data, per the Consumer Price Index (CPI) for July to gain clear directions. Market forecasts suggest an improvement in the headline CPI to 3.3% YoY versus 3.0% prior while the Core CPI, namely the CPI ex Food & Energy, may remain unchanged at 4.8%.

Technical analysis

A nine-month-old rising support line, around 0.6480 by the press time, challenges the AUD/USD bears amid the nearly oversold RSI conditions.

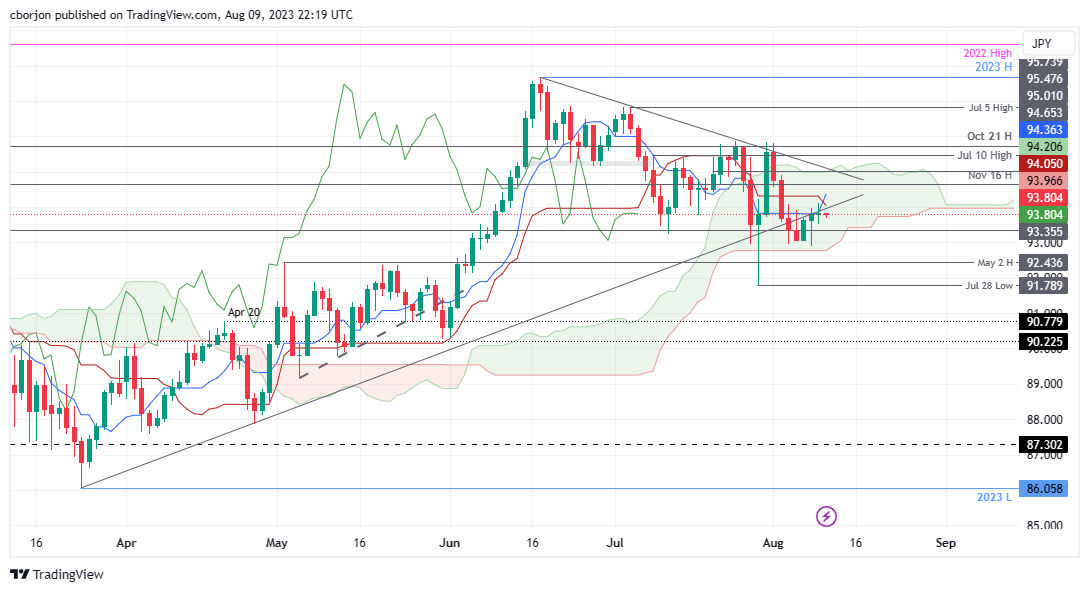

- AUD/JPY support levels to watch are the August 9 low at 93.52, the August 8 low at 92.89, and Kumo’s bottom edge at 92.78.

- AUD/JPY upside barriers include the 94.00 psychological level, Kijun-Sen at 94.05, Tenkan-Sen at 94.36, and Kumo’s upper edge around 94.90/98.

AUD/JPY remains undecisive as Wednesday’s price action printed a doji; simultaneously, the Tenkan-Sen crossed above the Kijun-Sen, a bullish signal that warrants further upside. Nevertheless, price action inside the Ichimoku Cloud (Kumo) would cap AUD/JPY movement. The AUD/JPY changes hands at 93.80, almost flat as the Asian session begins.

AUD/JPY Price Analysis: Technical outlook

From a technical perspective, the AUD/JPY is set to remain sideways, as price action lies inside the Kumo. But after three days of consecutive gains, the last one formed a doji, suggesting that neither buyers nor sellers are in charge, after breaking a support trendline drawn from year-to-date (YTD) lows of 86.06.

Given the backdrop, the AUD/JPY could test the lows of the Kumo, despite upside risks remaining. The AUD/JPY would test the August 9 daily low of 93.52. A breach of the latter would expose the August 8 daily low of 92.89, followed by the bottom of the Kumo at 92.78.

On the other hand, if AUD/JPY reclaims 94.00, the pair could test the top of the Kumo, but first, it would need to clear key resistance levels. The first resistance would be the Kijun-Sen and Tenkan-Sen levels, each at 94.05 and 94.36, followed by the top of the Kumo at 94.90/98.

AUD/JPY Price Action – Daily chart

- Gold Price stays pressured at the lowest level in a month ahead of United States Consumer Price Index for July.

- XAU/USD traces firmer sentiment as China-linked fears recedes, concerns about Federal Reserve policy pivot gain acceptance.

- Economic fears surrounding China, Europe and the UK may prod XAU/USD bulls as US Dollar resists declining further.

- Upbeat US inflation can join tight labor market to recall Fed hawks and weigh on Gold Price.

Gold Price (XAU/USD) refreshes the lowest level in a month as it drops to $1,914 during the early hours of Thursday’s Asian session. In doing so, the precious metal fails to cheer positive news from China, as well as a retreat in the US Dollar ahead of the United States inflation data. The reason could be linked to the market’s fears about the global economic and banking sector's health.

Gold Price falls despite mixed concerns about China, dovish Fed bets

Gold Price remains on the back foot after declining in the last three consecutive days. In doing so, the XAU/USD justifies the market’s lack of confidence and the positioning for the United States inflation data.

It’s worth noting that Italy’s surprise tax on windfall profits of banks joined the global rating agencies’ downward revision to the US banks and financial institutions to weigh on the risk sentiment and the Gold Price the previous day. On the same line could be fears of the UK recession and slowing economic growth in China, not to forget the Dragon Nation’s geopolitical tension with the US and Japan about Taiwan.

With this, a better-than-forecast China inflation data, despite making the deflation, and the US Dollar Index (DXY) pullback from a one-month high can’t be cheered by the XAU/USD traders. An improvement in China’s Producer Price Index (PPI) for July superseded negative readings of the Consumer Price Index (CPI) for the said month. That said, CPI declines to -0.3% YoY versus -0.4% YoY expected and 0.0% prior whereas the PPI improves to -4.4% YoY compared to -4.1% YoY market forecasts and -5.4% previous readings.

The reason could be linked to the looming bankruptcy of the Dragon Nation’s biggest private real estate company, namely the Country Garden, as it has less than 30 days after initial default on paying the bond coupons in early August. Further, the recent China deflation and receding activity data join the nation’s geopolitical tussles with the US, and recently with Japan, to weigh on the economic outlook for one of the world’s biggest XAU/USD customers.

Apart from China’s economic issues, Biden Administration also signaled relief to China technology companies and tamed the previous risk-off mood initially on Wednesday. “The US plans to target only those Chinese companies that get more than 50% of revenue from the sectors including quantum computing and artificial intelligence (AI),” said Bloomberg News.

Furthermore, the increasing odds of witnessing the US Federal Reserve’s (Fed) policy pivot challenges the US Dollar bulls and should have favored the Gold Price, but could not. That said, the CME Group FedWatch Tool shows that markets are pricing in an 86.5% chance that the Fed will pause interest rate hikes at its meeting in September.

US inflation will be more important for XAU/USD after softer NFP

Given the market’s recent indecision about China and the XAU/USD’s sustained downside, the traders will closely observe the United States inflation data, per the Consumer Price Index (CPI) for July to gain clear directions. Market forecasts suggest an improvement in the headline CPI to 3.3% YoY versus 3.0% prior while the Core CPI, namely the CPI ex Food & Energy, may remain unchanged at 4.8%. Should the US inflation data print upbeat figures, the Gold Price may break the immediate key support and slide beneath the $1,900 support while downbeat outcomes could trigger the much-awaited corrective bounce.

Also read: US CPI Preview: Forecasts from 10 major banks, monthly pace should hold at 0.2%

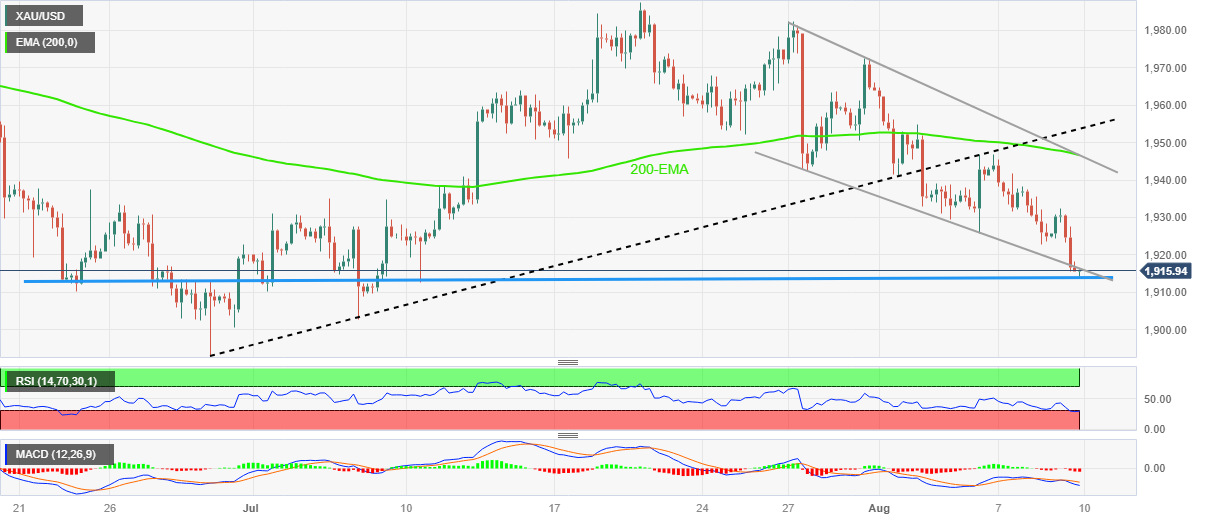

Gold Price Technical Analysis

Gold Price remains on the back foot after recently breaking the bottom line of a two-week-old falling trend channel, poking a seven-week-old horizontal support zone of late.

It’s worth noting that the nearly oversold conditions of the Relative Strength Index (RSI) line, placed at 14, join the sluggish signals from the Moving Average Convergence and Divergence (MACD) indicator to challenge further downside of the XAU/USD price.

The same highlights the immediate support comprising multiple levels marked since June 22 around $1,915, which in turn could challenge the bears ahead of the pre-event consolidation.

However, a clear downside break of $1,915 won’t hesitate to direct the XAU/USD price toward June’s low of around $1,893, with the $1,900 threshold likely acting as a buffer.

Meanwhile, an upside break of the stated channel’s bottom line, close to $1,917 by the press time can propel the Gold Price towards a descending resistance line stretched from August 31, close to $1,930 by the press time.

Following that, a convergence of the 200-bar Exponential Moving Average (EMA) and the previously stated channel’s top line, close to $1,948, will be important to watch for the XAU/USD buyer’s entry.

In a case where the Gold Price crosses the $1,948 hurdle, a six-week-old previous support line surrounding $1,955 will act as the final defense of the bears.

Overall, the Gold Price hits rock bottom and may witness a dead cat bounce but the recovery hinges on the key US inflation data and the $1,955 breakout.

Gold Price: Four-hour chart

Trend: Limited downside expected

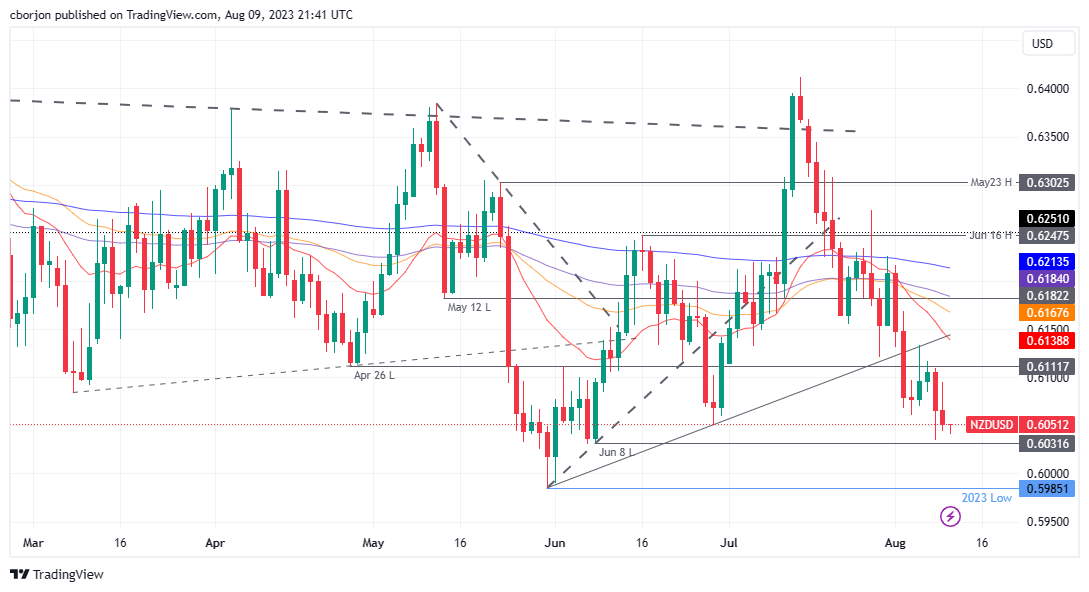

- NZD/USD dips 0.24% following economic slowdown fears in China, trading cautiously at 0.6050 ahead of US inflation data.

- US CPI expectations: Forecasts suggest a MoM rate of 0.2% and a YoY decrease from 3.3% to 3%. Core CPI might slightly decline to 4.7% YoY.

- RBNZ anticipation: With no significant NZ data releases, the market focus shifts to the potential RBNZ stance, expected to maintain rates at 5.50%.

NZD/USD extended its losses for two straight days on Wednesday, losing 0.24% after hitting a daily high of 0.6094, but deflation in China spurred fears of an economic slowdown. That, alongside the release of inflation in the United States (US), would keep the NZD/USD trading within narrow ranges. The NZD/USD changes hands at 0.6050 as the Asian session commences.

Kiwi dollar on the defensive, as traders brace for US inflation report, anticipate next RBNZ’s move

The lack of economic news turned market sentiment sour, but the greenback, as shown by the US Dollar Index (DXY) failed to gain traction ahead of an important US inflation report. The Consumer Price Index (CPI) for July is estimated to dip to 0.2% on MoM, while annually based to dip to 3% from 3.3% in June. Regarding core CPI, which strips out volatile items, is estimated to remain at 0.2%, unchanged, while Year-over-year is estimated to slow from 4.8% to 4.7%.

Aside from data in the calendar, Federal Reserve officials remain focused on data, which has shown that monetary policy is lagging, but the deflationary process started. Additional policymakers are turning neutral, while Michelle Bowman commented that further tightening is needed.

The CME FedWatch Tool shows odds for a rate hike in September at 13.5%, as money market futures do not expect more borrowing costs to increase. Nonetheless, if Fed officials begin to pile into the dovish stance, any rate cut signals would weaken the greenback; hence further NZD/USD upside is expected.

An absent docket on the New Zealand (NZ) front will keep traders focused on US Dollar dynamics. ANZ analysts expect the Reserve Bank of New Zealand (RBNZ) to hold rates at 5.50% at its next monetary policy meeting next Wednesday. “The RBNZ is expected to reiterate their “watch, worry and wait” stance.

NZD/USD Price Analysis: Technical outlook

The NZD/USD downtrend remains intact after dropping below the daily Exponential Moving Averages (EMAs). Also, successive series of lower peaks and throughs open the door to test yearly lows. It the NZD/USD dives below the current week’s low of 0.6034, the next support would emerge at the July 8 low of 0.6031. Once cleared, the next demand area would be the 0.6000 mark, below testing the year-to-date (YTD) low of 0.5985.

- The USD/CAD reached the 200-day SMA but then fell to 1.3420.

- Better-than-expected Building data from Canada and rising Oil prices limit the CAD’s downside.

- Markets remain cautious, awaiting Thursday´s inflation data for more guidance.

The USD/CAD traded flat near the 1.3420 area on Wednesday. On the US side, no relevant data was released, while investor remains cautious ahead of Thursday's Consumer Price Index (CPI) data from July. However, the Loonie gained strength from robust Canadian Building Permits for July, and Oil prices rising to highs since November 2022.

After two days of trading strong, the USD backed off somewhat, with the DXY index consolidating at 102.50. As the American economic calendar remains empty, the focus is on inflation data on Thursday which projections see the headline CPI slightly accelerating to 3.3% YoY and the Core CPI coming in at 4.8%.

On the CAD’s side, Building Permits from Canada from July unexpectedly rose by 6.1% MoM in July, while markets expected a 3.5% decline and boosted the Loonie. In addition, the West Texas Intermediate (WTI) barrel jumped above $84.00 for the first time since November 2022 and helped the CAD to trade resilient against its rivals.

USD/CAD Levels to watch

According to the daily chart, the technical outlook remains neutral to bullish for the short term as the bulls gain momentum. The Relative Strength Index (RSI) points north above its middle point, while the Moving Average Convergence (MACD) histogram displays larger green bars. Plus, the pair is above the 20 and 100-day Simple Moving Averages (SMA) but below the 200-day SMA, suggesting that on the bigger picture, the bulls are still in command over the bears but still need to overcome the 1.3500 level to confirm to upside.

Support levels: 1.3450, 1.3400,1.3320.

Resistance levels: 1.3500 (200-day SMA), 1.3550, 1.3570.

USD/CAD Daily chart

-638272137412243655.png)

The key event of the day will be the US CPI report for July. During the Asian session, wholesale inflation data is due in Japan, and in Australia, the Melbourne Institute Inflation Expectations report.

Here is what you need to know on Thursday, August 10:

Thursday is the key day in a relatively quiet week in terms of economic data, with the focus on US inflation data. The Consumer Price Index (CPI) is expected to show a rebound in the annual rate from 3% to 3.3%, while the Core rate is anticipated to remain at 4.8%. The weekly Jobless Claims report will also be relevant.

US CPI Preview: Forecasts from 10 major banks, monthly pace should hold at 0.2%

The inflation figures in the US are likely to trigger volatility, and market participants are eagerly awaiting the data. Prior to the report, the US Dollar posted mixed results on Wednesday, maintaining relative strength overall.

US stocks experienced a decline, with the Nasdaq falling 1.17% and the Dow Jones losing 0.54%. Crude oil prices, on the other hand, rose to fresh multi-month highs, with the WTI barrel climbing 1.60% and breaking above $84.00.

The US 10-year Treasury auction received decent demand. Its yield fell modestly to 4.01%, while the 2-year rebounded to 4.80%.

In a quiet session for currencies, the US Dollar Index experienced a marginal decline, consolidating around 102.50 as market participants await US inflation data.

EUR/USD modestly rose to 1.0970 as the Euro outperformed following the Italian government's decision to water down its windfall tax on banks by implementing caps on payouts. The European Central Bank (ECB) will release its Economic Bulletin, and Italy will report the final reading of July inflation.

USD/CHF rose for the second consecutive day but remains below 0.88000. EUR/CHF rebounded from 0.9580 to 0.9630 on Wednesday after the clarification regarding Italy's new windfall tax on banks.

GBP/USD remains range-bound around 1.2750. On Friday, the UK will report GDP and Industrial Production data.

USD/CAD marginally rose, closing slightly above 1.3420 but still far from its highs.

Analysts at Commerzbank on the Loonie:

The Bank of Canada surprisingly ended its interest rate pause at the beginning of June. It has since raised the key interest rate in two steps to 5%. Market expectations that it would raise rates further by the end of the year crumbled recently, which weighed on the CAD at the beginning of August, as did global factors. However, we maintain our outlook and see moderate CAD recovery potential in the medium term.

AUD/USD traded within Tuesday's range, remaining stagnant near 0.6540. The bias continues to favor the downside, influenced by cautious market sentiment and declining commodity prices. On Thursday, the Melbourne Institute is set to release the inflation expectations report.

NZD/USD recorded its lowest daily close in two months around 0.6050 but managed to hold above the key support level of 0.6030.

Gold prices continued to decline, marking the third consecutive day of losses and recording the lowest daily close in a month at $1,914. Similarly, Silver also lost ground, falling to $22.65. Precious metals remain under pressure, struggling to initiate a sustainable recovery and showing no signs of a correction.

Like this article? Help us with some feedback by answering this survey:

- EUR/JPY consolidates above 157.00 and threatens the cycle high at 158.00.

- The EUR is one of the best-performing currencies on Tuesday, driven by higher German yields.

- Weak Japanese data favours a more dovish stance of the BoJ.

In Wednesday’s session, the EUR/JPY rose near the 157.70 area on the back of a stronger EUR. On the other hand, the JPY weakened after weak economic activity data, which makes investors foresee the Bank of Japan (BoJ) not hurrying to pivot its monetary policy.

Considering this, the German yields are seeing gains across the curve, helping the European currency trade strong against most of its rivals. The 10-year bond yield rose to 2.47%, while the 2-year yield stands at 3.12% and the 5-year yielding 2.52%, respectively with all three seeing gains of more than 1%.

Moreover, no relevant data will be released from the European block this week, and regarding the next European Central Bank (ECB) decisions expectations, investors await the next set of data. Considering that Christine Lagarde is “open-minded” and that the decision will depend on incoming data regarding the September resolution, markets will closely monitor next week’s Q2 Gross Domestic Product (GDP) and inflation data from July from the European Union.

On the Japanese front, Machine Tool Orders came in at -19.8% YoY in July vs the -21.1% expected and its previous figure in May, tallying a contraction for seven straight months. In that sense, weak economic data supports a more dovish stance of the Bank of Japan (BoJ) which could apply further pressure on the JPY.

EUR/JPY Levels to watch

Considering the daily chart, the EUR/JPY shows a bullish sentiment for the short term. The Relative Strength Index (RSI), positioned above its midline in positive territory with a northward slope, supports this view along with the positive indication from the Moving Average Convergence Divergence (MACD), which is displaying green bars, pointing towards a strengthening bullish trend. Also, the pair is above the 20,100,200-day SMAs, pointing towards the prevailing strength of the bulls in the larger context.

Support levels: 157.00, 156.00, 155.00.

Resistance levels: 158.00, 158.50, 159.00.

EUR/JPY Daily chart

-638272097407482087.png)

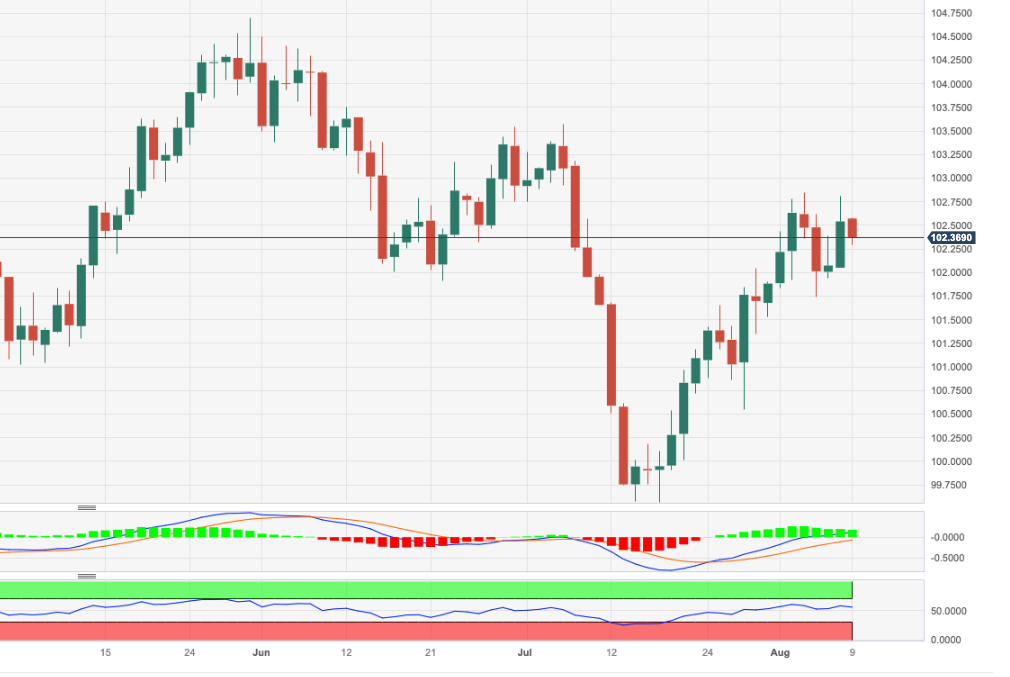

- GBP sees narrow trade: Lingers below the 50-day EMA, trading at 1.2724, with significant UK GDP data due Friday.

- Bank of England’s stance: Market odds suggest a September rate hike at 85%, potentially peaking the Bank Rate at 5.75% by December.

- Awaiting July US CPI numbers, expectations stand at 0.2% MoM; annual inflation is estimated at 4.8%, guiding Fed’s future decisions.

GBP/USD modestly dives during the North American session, below the 50-day Exponential Moving Average (EMA) even though the US Dollar (USD) remains soft across the board as speculators prepare for the release of inflation data in the United States (US). The GBP/USD is trading at 1.2724, down 0.18%

GBP/USD trend uncertain as market players must diggest US and UK inflation and growth data

The Pound Sterling (GBP) remains trading within a narrow range amid the lack of catalyst during the first part of the week, as UK’s economic docket will reveal its first part of market moving data on Friday, with Gross Domestic Product (GDP) for Q2 on its preliminary reading expected to decelerate to 0%, below the prior’s quarter 0.1% growth, on QoQ data. On a yearly basis, Q2 is estimated to remain unchanged at 0.2%, while MoM data from June is estimated to improve from May’s contraction. If the UK economy shows further weakness, the GBP/USD could accelerate its downtrend, as data could refrain the Bank of England (BoE) from aggressively tightening policy.

Regarding that theme, money market futures odds for a quarter of a percentage point increase by the BoE in September lie at an 85% chance, while for December is fully priced in, suggesting the Bank Rate would peak at 5.75%, against 6.5% at the beginning of August.

Across the pond, the US Department of Labor would release the July inflation report, which is expected to show the US economy deflationary process remains underway, but not as fast as Fed officials expected. The Consumer Price Index, monthly and annually, is foreseen to hit 0.2% and 3%, respectively. Monthly data would remain unchanged from June’s, while year-over-year (YoY) would show an improvement from 3.3%. Excluding volatile items, the so-called core CPI is projected to remain at 0.2% MoM, with annual inflation estimated to be 4.8%, the same as in June.

US central bank officials had begun to split between dovish and hawkish stances. Still, GBP/USD traders must wait for tomorrow’s data, which could shed some light on the US Federal Reserve’s (Fed) forward path on monetary policy.

The CME FedWatch Tool shows odds for a rate hike in September at 13.5%, as money market futures do not expect more borrowing costs to increase. Nonetheless, if Fed officials begin to pile into the dovish stance, any rate cut signals would weaken the greenback; hence further GBP/USD upside is expected.

Given the backdrop, the GBP/USD could remain subdued ahead of US data. After that, an uptick could weigh on the GBP/USD, but UK’s GDP data could rock the boat and shift the pair upwards. Therefore, caution is warranted for GBP/USD traders.

GBP/USD Price Analysis: Technical outlook

GBP/USD is neutral to downward biased, as it has achieved successive series of lower peaks and throughs, but it remains shy of taking a decisive direction ahead of fundamental news from the US and the UK. As the GBP/USD drops below the 50-day EMA, the next support level to challenge is the current week’s low of 1.2684. A breach of the latter will expose the August 3 low of 1.2620, followed by the 100-day EMA at 1.2603. On the other hand, if GBP/USD reclaims the 20-day EMA at 1.2800, that could pave the way to test a downslope resistance trendline at around 1.2830/40.

- EUR/GBP recovered the 20-day SMA rising near 0.8630, seeing nearly 0.40% gains.

- EUR is one of Wednesday’s top performers amongst its rivals.

- No relevant data will be released for either economy. Tightening expectations of BoE and ECB to dictate the pace.

At the middle of the week, the EUR/GBP recovered ground and jumped above the 20-day Simple Moving Average (SMA) of 0.8600. The EUR trades with gains against the USD, CHF, JPY, and AUD on higher German yields while the Pound trades soft.

On a quiet week, tightening expectations dictate the pace of the EUR/GBP cross, and rising German yields are pushing the pair higher. The 10-year bond yield rose to 2.47%, while the 2-year yield stands at 3.09% and the 5-year yielding 2.53%, respectively, making the EUR gain interest against its rivals. The focus now shifts to next week’s Q2 Gross Domestic Product (GDP) and inflation data from July from the European Union, which will help investors to model the next data-dependant European Central Bank (ECB) decision.

On the Pound’s side, GDP data on Friday will be key. The Bank of England reported in it last monetary policy statement that it no longer expects a recession, so the economic outlook in the UK will have an impact on the bets of market participants on the next BoE’s decision. As for now, they still bet, according to the World Interest Rate Possibilities (WIRP), a terminal rate of 5.75%, meaning an additional 50 basis point tightening for the rest of this cycle.

EUR/GBP Levels to watch

The daily chart suggests that the technical outlook is neutral to bullish for the short term as the bulls gain momentum, but buyers still have some work to do. The Relative Strength Index (RSI) has a positive slope in the bullish territory just above its midline, while the Moving Average Convergence (MACD) histogram displays increasing green bars. On the other hand, the pair is above the 20-day Simple Moving Average (SMA) but below the 100 and 200-day SMAs, indicating that there is still some light for the bulls but that the bears have the upperhand on the bigger picture.

Support levels: 0.8600 (20-day SMA), 0.8570, 0.8530.

Resistance levels: 0.8670 (100-day SMA), 0.8680, 0.8700

EUR/GBP Daily chart

-638272022139112620.png)

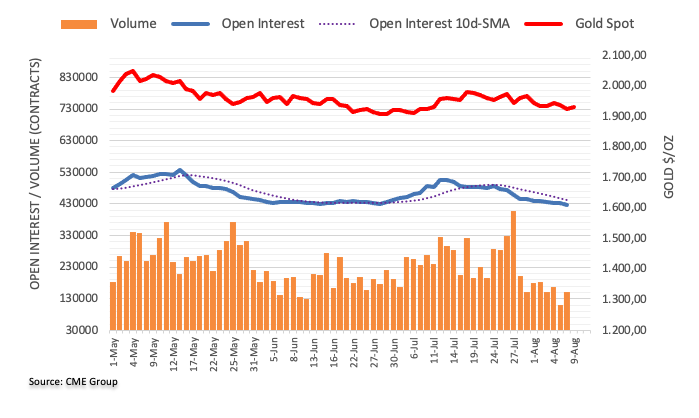

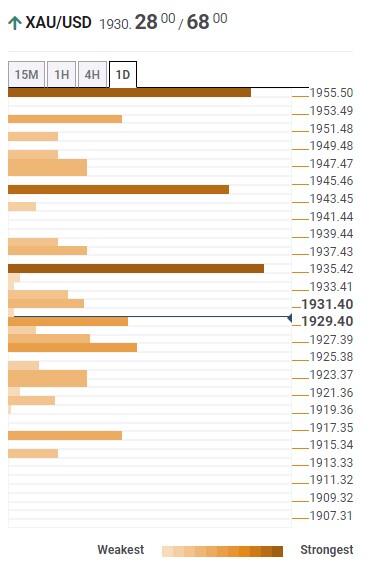

- XAU/USD dips 0.39%, targeting the 200-day EMA as traders anxiously await US inflation numbers.

- Fed’s varying tone: While Harker hints at steady rates, Bowman pushes for hikes to control inflation, impacting Gold’s momentum.

- US 10-year Treasury bond yield hovers at 4%, while the DXY index drops slightly, failing to increase appetite for Gold.

Gold price losses traction for the third straight day in the week tumbles 0.39% below its opening price as sellers eye a test of the 200-day Exponential Moving Average (EMA) at $1,908.12. Traders bracing for US inflation data release keep the yellow metal price depressed, exchanging hands at XAU/USD changes hands at $1,917.54.

Gold traders weigh US inflation projections and mixed Federal Reserve signals; eyes set on September rate hike odds

The XAU/USD treads water ahead of the release of the July inflation report, which is expected to show the deflationary process remains intact. Estimates for the Consumer Price Index monthly and annually stand at 0.2% and 3%, respectively. Monthly data would remain unchanged from June’s, while year-over-year (YoY) would show an improvement from 3.3%. Excluding volatile items, the so-called core CPI is foreseen to remain at 0.2% MoM, with annual inflation estimated to be 4.8%, the same as in June.

However, XAU/USD buyers could remain hopeful for higher prices, as most Federal Reserve (Fed) officials have begun to turn neutral or even dovish, as shown by Philadelphia Fed President Patrick Harker stating that rates could remain at current levels, barring any deterioration on US economic data, said on Tuesday. Contrarily, Fed Governor Michelle Bowman stated the Fed needs to keep the pedal to the metal, lifting rates to curb inflation.

Expectations for a rate hike in September remained depressed, with odds at a 13.5% chance, as shown by the CME FedWatch Tool. Any Fed signals for rate cuts in 2024 could increase the appetite for the non-yielding metal, which is suffering from high US Treasury bond yields.

The US 10-year Treasury bond yield dives two basis points to 4.00% but remains above the figure, a headwind for XAU/USD, while the US Dollar Index (DXY), a measure of the greenback’s performance against its peers, loses traction, edges to 102.436, down 0.10%.

XAU/USD Price Analysis: Technical outlook

XAU/USD price is depressed after testing the lows of June at around $1,893.12, extended its gains toward the July 20 swing high at $1,987.42, though buyers’ failure to crack the latter exacerbated a pullback toward current gold price. On its way south, XAU/USD breached the 20, 50, and 100-day EMAs and as of writing, is breaking below a five-month-old support trendline that passes at around $1,922/$1,930. A daily close would expose the 200-day EMA, followed by the $1,900 figure.

From an oscillator’s view, the Relative Strength Index (RSI) and the three-day Rate of Change (RoC) suggest further downside expected as sellers remain in charge.

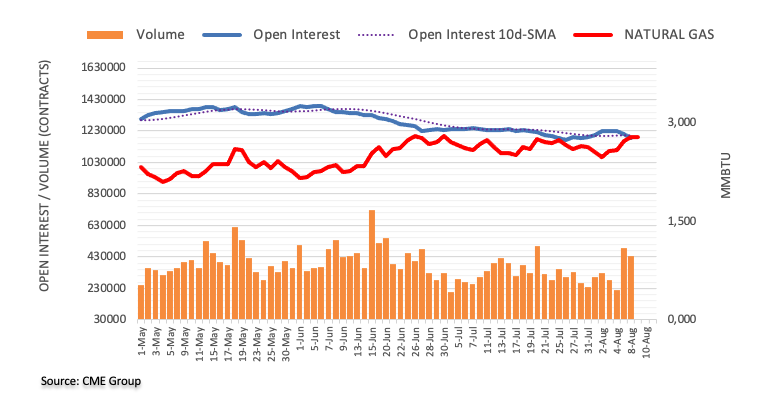

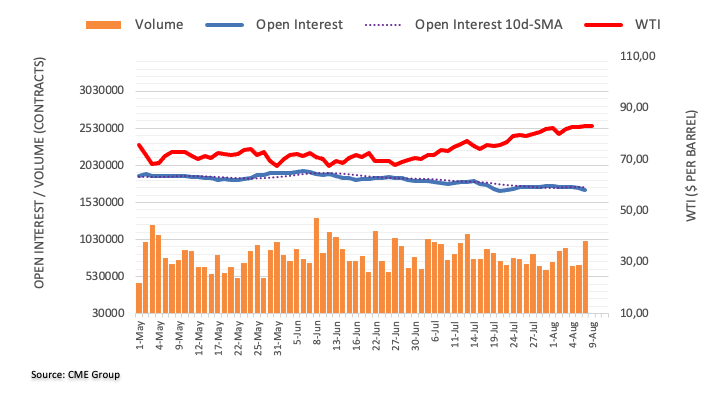

- WTI jumped to its highest level since November 2022 above $84.00.

- Tighter global supply and Chinese inflation data are fuelling Oil prices.

- EIA Oil stocks data came in higher than expected.

On Wednesday, the West Texas Intermediate (WTI) rose to a high of $84.15, it highest level since mid-November 2022 and then settled around $83.00. Tighter global supplies on the prospects of further Saudi production cuts and deflation evidence in China, which sparked expectations of more aggressive Chinese fiscal policies, explain those upwards movements.

China reported that the Consumer Price Index (CPI) from July came in at -0.3% YoY vs -0.4% expected, while the Producer Price Index (PPI) set a 4.4% yearly decrease in the same month, higher than the 4.1% expected. According to TD Securities analysts, evidence of deflation in the Asian gigant fueled hopes of “bazooka-like” fiscal stimulus packages to bolster the local economy. In that sense, further stimulus would raise Oil demand, and as China is the largest importer in the world, the prices rise.

In addition, Saudi’s voluntary production cuts and Russia's export curtailment contribute to a tighter global supply, favouring black gold’s price.

On the data front, the EIA (Energy Information Administration) Crude Oil stockpiles report, which gives a weekly measure of the change in the number of barrels in stock of crude Oil and its derivates, came in at 5.85M in the first week of August, higher than the 0.567M expected.

WTI Levels to watch

The technical outlook for the WTI is bullish for the short term, but indicators flash overbought conditions, suggesting that a technical correction may be on the horizon. The Relative Strength Index (RSI) indicates overbought conditions as it points north above the 70 threshold, while the Moving Average Convergence (MACD) histogram displays increasing green bars. Additionally, the pair is above the 20,100,200-day SMAs, highlighting the continued dominance of bulls on the broader scale.

Support levels: $82.00,$80.00, $79.20 (20-day SMA).

Resistance levels: $84.00, $85.00, $87.00.

WTI Daily chart

-638271980844858843.png)

- XAG/USD stands near $22.70, while bears still have the upperhand.

- The USD weakened following two consecutive sessions of strength.

- US Treasury yields stand mixed ahead of inflation data from the US from July.

In Wednesday's session, the Silver spot price XAG/USD traded with mild losses, while the USD traded weaker and corrected after two days of strength. Markets remain quiet ahead of crucial Consumer Price Index (CPI) data from the US from July, which will impact bond and metal price dynamics.

Considering this, the US bond yields showed a mixed performance on Wednesday. The 10-year bond yield trades at 4.01%, seeing 0.23 % losses on the day, while the 2-year yield stands at 4.76% with 0.12 % gains and the 5-year yielding 4.10%, seeing mild losses.

In terms of the next Federal Reserve (Fed) following monetary policy decisions, tightening expectations have risen. According to World Interest Rate Possibilities (WIRP) tool, the markets are currently pricing in a 15% chance of a 25 bps hike in the September meeting, while those odds rise to 30% in November. It will all come down to the incoming data, as Jerome Powell stated during the press conference after the last Fed decision.

It's worth noticing that higher interest rates tend to be negatively correlated with non-yielding precious metal prices, so traders will keep a close eye on Thursday’s CPI data from the US.

XAG/USD Levels to watch

The daily chart analysis indicates a bearish outlook for the XAG/USD in the short term. The Relative Strength Index (RSI) is below its midline in negative territory, with a negative slope, aligning with the negative signal from the Moving Average Convergence Divergence (MACD), displaying red bars, reinforcing the strong bearish sentiment. Moreover, the pair is below the 20,100 and 200-day Simple Moving Averages (SMAs), supporting the idea that the bears are in command in the bigger picture.

Support levels: $22.50, $22.30, $22.00.

Resistance levels: $23.25 (200-day SMA), $23.50, $23.70, $24.00.

XAG/USD Daily chart

-638271939048292227.png)

- Mexico’s inflation progress, as INEGI reports, CPI continuing its downtrend.

- Following CPI data, most analysts expect Banxico to keep rates unchanged at 11.25%, with potential rate cuts in Q4 2023.

- Federal Reserve policymakers showed mixed signals as traders eye US CPI on August 10.

The Mexican Peso (MXN) gains some traction as the USD/MXN pair edges lower after inflation data from Mexico portrays the deflationary process continues with success, ahead of Thursday’s monetary policy by the Bank of Mexico (Banxico). At the time of writing, the USD/MXN trades at 17.0830, down 0.14%.

USD/MXN dips as traders wait for US inflation data and Banxico’s decision

The Instituto National of Estadistica Geografia e Informatica (INEGI) revealed the Consumer Price Index for July came below estimates of 0.49% MoM, at 0.48%, while annually based, hit 4.79%, as foreseen and a quarter of percentage below June’s figures. Nevertheless, as in most developed economies, core CPI is showing some stickiness, coming at 6.64% YoY, below estimates of 6.68%, and 0.25% beneath June’s 6.89%.

Following the inflation release, most analysts foresee Banxico’s holding rates unchanged at 11.25% on the August 10 monetary policy reunion. Pantheon Economics expects the first rate cut by Q4 2023.

Meanwhile, an absent US economic agenda would keep traders awaiting the release of the US inflation data. The Consumer Price Index (CPI) is expected to remain unchanged compared to June’s 0.2% MoM, while market analysts foresee a dip to 3% from 3.3% YoY. Core CPI is estimated to print 0.2% MoM as the prior month’s release, and YoY is projected to stay at 4.8% as June’s.

In the meantime, Federal Reserve officials begin to shift towards a neutral stance, led by Philadelphia Fed President Patrick Harker, saying the Fed is at a stage where it could keep rates unchanged unless data suggests the opposite. Contrarily, Fed Governor Michelle Bowman stated the Fed needs to keep the pedal to the metal, lifting rates to curb inflation.

Expectations for a rate hike in September remained depressed, with odds at a 15% chance, as shown by the CME FedWatch Tool.

The US Dollar Index (DXY), a gauge of the buck’s value against a basket of six currencies, is losing some traction, down by 0.11%, at 102.430, undermined by falling UST bond yields. The US 10-year benchmark note rate is 4.00%, down two basis points.

USD/MXN Price Analysis: Technical outlook

The USD/MXN is trading sideways above the 17.0000 figure for the fifth straight day, capped on the upside by the 50-day Exponential Moving Average (EMA) at 17.1308, while the figure and the 20-day EMA at 16.9849 act as support levels for the US Dollar bulls. If USD/MXN clears the 50-day EMA, that could exacerbate a move toward the crucial May 17 low of 17.4038, turned resistance. A daily close above the latter could pave the way to test the 100-day EMA at 17.4922. Conversely, if USD/MXN drops below the 20-day EMA, the pair could challenge the year-to-date (YTD) low of 16.6238.

- USD/JPY climbs to 143.53 despite weakening US Dollar across FX and declining US Treasury bond yields.

- Inflation anticipation: Wall Street is on standby for July’s CPI, expected to remain steady at 0.2% MoM.

- Mixed Fed signals stir the market, with officials hinting at tightening and others suggesting a steady rate path.

USD/JPY advances for three straight days, climbing 0.11%, despite falling US Treasury bond yields and overall US Dollar (USD) weakness across the FX board, ahead of inflation data release from the United States (US). At the time of writing, the USD/JPY exchanges hands at 143.53 after hitting a low of 142.98.

Uncertainty over the Federal Reserve’s stance and Japanese monetary policy dynamics to dictate USD/JPY direction

Wall Street trades with minuscule losses amidst a light US economic docket as traders brace for July’s inflation data. The Consumer Price Index (CPI) is expected to remain unchanged compared to June’s 0.2% MoM, while market analysts foresee a dip to 3% from 3.3% YoY. Core CPI is estimated to print 0.2% MoM as the prior month’s release, and YoY is projected to stay at 4.8% as June’s.

Aside from this, the shrinkage of the trade deficit slightly boosted the greenback, but mixed messages from US Federal Reserve (Fed) officials, keep investors uncertain about the Fed’s forward path. Even though Fed Governor Michelle Bowman stressed the need for additional tightening, more policymakers are taking a more cautious or neutral approach, as Philadelphia Fed President Patrick Harker. He commented the Fed is at a stage where it could leave rates unchanged, barring an abrupt change in the direction of recent economic data.

Monetary policy expectations on the Fed show money market traders expect no change to the Federal Funds Rate (FFR), with odds at 86.5%, as shown by the CME FedWatch Tool.

The US Dollar Index (DXY), a gauge of the buck’s value against a basket of six currencies, is losing some traction, down by 0.11%, at 102.430, undermined by falling UST bond yields. The US 10-year benchmark note rate is 4.00%, down two basis points.

The lack of economic data in Japan would keep traders leaning toward US Dollar dynamics, as well as recent data from the Bank of Japan (BoJ), as most members of the BoJ expressed an opinion about the Yield Curve Control (YCC). Even though there was some chatter about normalizing monetary policy, most BoJ’s members remain on the dovish side of the spectrum.

USD/JPY Price Analysis: Technical outlook

The USD/JPY found support around the top of the Ichimoku Cloud (Kumo), briefly pierced on Monday. However, a ‘tweezers bottom and harami’ pattern exacerbated a recovery toward current exchange rates. In addition, the Tenkan-Sen is about to cross above the Kijun-Sen line, seen as a bullish signal, while the Chikou Span is still below the price action. That said, the USD/JPY is bullishly biased, and it might test the year-to-date (YTD) high at 145.07, but firstly it would need to surpass key resistance levels, like the psychological 144.00 figure. Conversely, if the major drops inside the Kumo, it could test the current week’s low of 141.50.

The US Bureau of Labor Statistics (BLS) will release the most important inflation measure, the US Consumer Price Index (CPI) figures, on Thursday, August 10 at 12:30 GMT. As we get closer to the release time, here are the forecasts by the economists and researchers of 10 major banks regarding the upcoming United States inflation print for the month of July.

Headline and core CPI, which excludes volatile food and oil prices, are seen coming in at 0.2% month-on-month, same as in June. Annual headline CPI is expected to rebound to 3.3% vs. June’s print of 3.0% and core is seen steady at 4.8% YoY.

Commerzbank

We expect the core rate to remain at just 0.2% in July. The headline inflation rate is also likely to be 0.2%. As this would be largely in line with the Fed's inflation target of 2%, such a result would support our view that the Fed is unlikely to raise rates again.

Credit Suisse

We expect core CPI inflation to remain at 0.2% MoM in July, maintaining a more modest run rate after stepping lower in June. The YoY reading of core inflation is likely to decline to 4.7%. On the other hand, unfavorable base effects and modestly higher gas prices are likely to lead headline inflation higher to 3.3% YoY. A reading in-line with our expectations would represent the second consecutive month that monthly core inflation has been broadly in-line with the Fed’s target.

TDS

Core-price inflation likely remained the same in July, printing a second straight 0.2% MoM gain (0.23% unrounded). Goods inflation was likely a big factor to the downside, with shelter prices remaining a key wildcard (we expect modest acceleration). Rising gas prices will also help to keep headline inflation steady. Our MoM forecasts imply 3.3%/4.8% YoY for total/core prices.

ANZ

We expect both headline and core CPI inflation to rise by 0.2% MoM in July. Falling used car prices are again expected to see a decline in core goods prices. Some one-off factors are expected to keep core services ex-rent subdued, while rent inflation should continue to cool from a heady pace. Our diffusion and dispersion indices suggest inflation pressures are abating and normalising. The Fed is wary of upside risks to elevated inflation given demand for labour remains excessive. Most policymakers think the policy rate will need to be kept restrictive for some time to get inflation back to target. The risks remain that the Fed’s work is not yet done.

NBF

The energy component is likely to have had a sizeable positive impact on the headline index given the sharp rise in gasoline prices during the month. This, combined with another healthy gain in shelter costs, should result in a 0.4% increase in headline prices. If we’re right, the year-on-year rate could move up from 3.0% to 3.4%, marking the first increase in 13 months for this indicator. The advance in core prices could have been more subdued in July thanks in part to a decline in the price of used vehicles. But a rise of 0.3% in the month will still be too large to allow a drop in the annual rate. The latter should instead remain unchanged at 4.9%.

RBC Economics

YoY growth in US consumer prices likely ticked slightly higher for the first time in a year in July – gasoline prices didn’t move much this July but a larger 8% drop in July a year ago will fall out of the 12-month growth rate. YoY growth in core (ex-food & energy) prices will still be high (we expect +4.7%) in July, but we expect a moderate 0.2% MoM increase to match the June gain. Slower growth in core CPI has come alongside a pullback in home rent inflation as earlier slowing in market asking rent growth feed through to lower rent CPI with a lag as contracts get renewed. Absent a reacceleration in core inflation, we expect the Fed to step to and stay on the sideline and maintain the Fed Funds at 5.25% – 5% range until 2024.

CIBC

After some relief in core prices in June, price pressures likely maintained a 0.2% monthly pace in July for both headline and core (ex. food/energy) CPI. Unfavorable base effects will have propped up annual CPI inflation to 3.2%, while annual core inflation likely subsided to 4.7%. Within core categories, shelter prices could have decelerated, reflecting the typical lag associated with softer rents seen last year, but the Fed will be focused on core services outside of rent of shelter, as that’s a better gauge of underlying price pressures tied to demand. That measure was flat on a monthly basis in June, but that partly reflected a sizable drop in airfares that may not have extended into July. Still, even a bounce in core services ex. shelter to 0.3% MoM would leave the three-month annualized change at a tame 2.1%.

Citi

We expect a 0.196% MoM increase in core CPI in July, a modestly stronger increase than in June but clearly a much more favorable monthly pace of inflation for the Fed than over much of the last few years. Shelter prices are likely to continue to slow overall this year, though the July data may see a somewhat stronger 0.47% MoM increase in each of primary rents and owners’ equivalent rent. More negative seasonal factors after July could mean shelter prices slow further in the fall. Meanwhile, headline CPI should rise 0.3% MoM and rebound from a near-term bottom of 3.0% YoY to 3.3% YoY.

Westpac

The June CPI report was pivotal for the current cycle as a modest 0.2% monthly print brought annual headline inflation down to 3.0%, a third of its peak level. A similar outcome is expected by Westpac, though the annual rate will lift slightly owing to an adverse base effect. The composition of US inflation remains problematic, however. Goods inflation is benign and services ex. shelter increasingly constructive for a return to target well before the medium term. But, because of its weight and scale, by itself, shelter inflation has the capacity to hold inflation above the 2.0% YoY target for the foreseeable future. It is also worth recognising that, while shelter inflation should abate to year-end and through early-2024, capacity in the sector will remain a concern for years, and with it shelter inflation.

Wells Fargo

We expect the disinflationary trend to continue in July and estimate a 0.2% bump in both the headline and core measures over the month. Looking under the hood, we expect faster deflation for vehicles and other goods in July, counteracted by slightly firmer services prices for travel and medical care. If realized, these prints would translate to a 3.3% annual headline rate and a 4.7% annual core rate. Through the monthly noise, inflation appears set on a downward path. However, progress in the coming months is likely to be slower and noisier than June’s print alone would suggest. We expect monthly gains in core inflation to pick up slightly in Q4 as the disinflationary momentum from waning goods prices fades and health insurance prices rebound toward the end of the year.

Economists at Commerzbank expect the Brazilian Real to defend its strong level against the US Dollar this year. However, monetary policy support for BRL is likely to gradually weaken in 2024.

A somewhat weaker Real next year

Attractive real interest rates should continue to support the Brazilian Real even after the start of the rate-cutting cycle.

In the longer term, however, we see depreciation risks for the BRL, mainly due to our concerns about a less hawkish monetary policy.

Source: Commerzbank Research

See: USD/BRL set to trade in a 4.70-5.00 range in the month ahead – SocGen

The Australian Dollar has been the worst-performing G10 currency in the past month. Nonetheless, economists at ING see ample room for recovery.

Markets are underestimating risks of more RBA tightening

We think the domestic picture will improve for AUD, as the RBA may well have to hike again despite market’s flat rate expectations.

The monetary policy story could potentially come through as a positive factor at a time (September, for example) when USD resilience hasn’t abated yet, meaning an RBA-driven bullish pocket for AUD could initially be mostly mirrored in relative strength against other pro-cyclical currencies rather than on AUD/USD.

In line with our bearish USD call for later in the year, we expect AUD/USD to rebound back to the June and July 0.69 peaks before year-end, and then find more support above 0.70 in the first half of 2024.

The Swiss Franc was the second best performing currency in July lagging behind only the Norwegian Krone.

SNB unlikely to hike rates further this year

While recent Franc gains have not been as extreme as back in early 2015, we do believe that the strength of the CHF is currently overshooting somewhat and expect it to correct lower in the coming months.

The Swiss Franc has been benefitting from the relatively hawkish policy stance of the SNB who have actively been encouraging a stronger CHF to dampen upside risks to their inflation outlook. With inflation likely to slow further below the SNB’s 2.0% target in the coming months, we do not expect the SNB to hike rates further this year.

EUR/CHF – Q3 2023 0.9650 Q4 2023 0.9700 Q1 2024 0.9800 Q2 2024 0.9800

USD/CHF – Q3 2023 0.8770 Q4 2023 0.8660 Q1 2024 0.8670 Q2 2024 0.8820

Why is not the Euro weaker? Kit Juckes, Chief Global FX Strategist at Société Générale, analyzes the shared currency outlook.

Positions are holding Euro up, but for how long?

We can see EUR/USD trade in a range for a while longer, as long as positions stay where they are.

But if the economic data don’t start providing support, and relative expectations about Fed and ECB policy don’t move in the Euro’s favour this month, we’re going to see long Euro positions capitulate in September.

- The US Dollar is unchanged near the New York opening bell.

- Very light data calendar points to a rather uneventful day in the wake of US inflation data on Thursday.

- The US Dollar Index nudges lower, eyes key support test.

The US Dollar (USD) is trading sideways to slightly lower as markets are currently positioned within the eye of the data storm that will see wind speed peaking on Thursday with the US Consumer Price Index (CPI) numbers. A mix of events on Tuesday – with lackluster import/export data out China together with resparked recession fears, and the 40% tax on profits for Italian banks – served a risk averse cocktail which fueled the rally in the Greenback across the board in every major G10 pair. The very light economic calendar and the US Consumer Price Index (CPI) numbers on Thursday will see traders sitting on their hands for Wednesday in order to keep their powder dry for the main event.

On the economic front, a light release calendar is on the cards, with only the weekly Mortgage Applications numbers expected. From the commodity side, the US Energy Information Administration (EIA) will release Crude Oil and derivatives numbers. This release will get some additional attention as Western Texas Intermediate (WTI) crude price went on a wild ride on Tuesday, by first dropping 3.10% during the European session and then rallying 4% during the US trading session.

Daily digest: US Dollar calmness before the storm of Thursday

- Markets faced the first and only piece of macroeconomic data out of the US at 11:00 GMT with the weekly Mortgage Bankers Association (MBA) Mortgage Applications dropping to -3.1% from -3.0% previous week.

- The US Treasury Department is about to tap the markets for a 10-year note auction. As the 10-year tenor acts as an important benchmark, expect some additional attention to any bid/cover ratios and demanded yields.

- Expect a bit of fireworks from the US Energy Information Administration (EIA) Crude Oil numbers. Western Texas Intermediate (WTI) crude price moved over 7% in intraday volatility on Tuesday, and as recession fears are fading on Wednesday, a drop in stockpile could fuel a pop higher in the Crude Oil price.

- Stocks are rebounding a bit with the Hang Seng unchanged and European equities on the front foot. Both the German DAX and the European Stoxx 50 are paring back losses from Tuesday. US equity futures head slightly lower after a green opening after some disappointing earnings.

- The CME Group FedWatch Tool shows that markets are pricing in an 86.5% chance that the Federal Reserve will pause interest rate hikes at its meeting in September.

- The benchmark 10-year US Treasury bond yield trades at 4.01% and is trading higher after the drop below 4% intraday on Tuesday. The risk aversion from Tuesday seems to be in the rear mirror and US bonds are no longer heavily bid.

US Dollar Index technical analysis: nothing to see here

The US Dollar made it through a very difficult area on the US Dollar Index (DXY) chart. The region with both the 100-day and the 55-day Simple Moving Average (SMA) has been broken to the upside and must have hurt quite a few US Dollar bears in the process. With the US Dollar retracing a little bit on Wednesday, it will be important to see if the 100-day SMA at 102.31 will be able to refrain the DXY from paring back all gains from Tuesday.

For the upside, 102.45 – where the 55-day SMA is located – is the next key level to have a daily close above in order to advance in a solid way. The fact this technical indicator already got breached below means that it misses buying-interest. In case the US Dollar Index is able to head back above it, look for 103 and a new monthly high to be at hand.

On the downside, the US Dollar bulls will want to defend that earlier mentioned 100-day SMA at 102.31, in order to avoid a full paring back of earlier gains for this week. If bulls fail to do so, expect to see a nosedive move toward 102.00. The low of past Friday at 101.74 could be a line in the sand to predict if more downside is to come, once it is being tested.

Central banks FAQs

What does a central bank do?

Central Banks have a key mandate which is making sure that there is price stability in a country or region. Economies are constantly facing inflation or deflation when prices for certain goods and services are fluctuating. Constant rising prices for the same goods means inflation, constant lowered prices for the same goods means deflation. It is the task of the central bank to keep the demand in line by tweaking its policy rate. For the biggest central banks like the US Federal Reserve (Fed), the European Central Bank (ECB) or the Bank of England (BoE), the mandate is to keep inflation close to 2%.

What does a central bank do when inflation undershoots or overshoots its projected target?

A central bank has one important tool at its disposal to get inflation higher or lower, and that is by tweaking its benchmark policy rate, commonly known as interest rate. On pre-communicated moments, the central bank will issue a statement with its policy rate and provide additional reasoning on why it is either remaining or changing (cutting or hiking) it. Local banks will adjust their savings and lending rates accordingly, which in turn will make it either harder or easier for people to earn on their savings or for companies to take out loans and make investments in their businesses. When the central bank hikes interest rates substantially, this is called monetary tightening. When it is cutting its benchmark rate, it is called monetary easing.

Who decides on monetary policy and interest rates?

A central bank is often politically independent. Members of the central bank policy board are passing through a series of panels and hearings before being appointed to a policy board seat. Each member in that board often has a certain conviction on how the central bank should control inflation and the subsequent monetary policy. Members that want a very loose monetary policy, with low rates and cheap lending, to boost the economy substantially while being content to see inflation slightly above 2%, are called ‘doves’. Members that rather want to see higher rates to reward savings and want to keep a lit on inflation at all time are called ‘hawks’ and will not rest until inflation is at or just below 2%.

Is there a president or head of a central bank?

Normally, there is a chairman or president who leads each meeting, needs to create a consensus between the hawks or doves and has his or her final say when it would come down to a vote split to avoid a 50-50 tie on whether the current policy should be adjusted. The chairman will deliver speeches which often can be followed live, where the current monetary stance and outlook is being communicated. A central bank will try to push forward its monetary policy without triggering violent swings in rates, equities, or its currency. All members of the central bank will channel their stance toward the markets in advance of a policy meeting event. A few days before a policy meeting takes place until the new policy has been communicated, members are forbidden to talk publicly. This is called the blackout period.

- EUR/USD reverses part of the weekly leg lower on Wednesday.

- Initial support emerges at the monthly low of 1.0912.

EUR/USD regains some composure and bounces to the 1.0990 region on Wednesday.

In case losses accelerate, spot should face interim contention at the 55-day and 100-day SMAs at 1.0930 and 1.0924, respectively, ahead of the so far August low at 1.0912 (August 3). In case the latter is breached on a sustainable way, the pair could embark on a move to the July low of 1.0833 (July 6).

In the meantime, while below the weekly high of 1.1149 (July 27), the pair risks further retracements for the time being.

Looking at the longer run, the positive view remains unchanged while above the 200-day SMA, today at 1.0760.

EUR/USD daily chart

- DXY comes under pressure following two consecutive daily gains.

- Further north emerges the monthly high at 102.84.

DXY faces some renewed selling pressure and retreats from Tuesday’s weekly peaks in the 102.75/80 band on Wednesday.

The index extends the upbeat tone seen at the beginning of the week and seems ready to challenge the so far monthly top of 102.84 (August 3) sooner rather than later. The breakout of this level exposes a probable move to the July high of 103.57 (July 3), which appears underpinned by the proximity of the key 200-day SMA.

Looking at the broader picture, while below the 200-day SMA (103.43) the outlook for the index is expected to remain negative.

DXY daily chart

The Mexican Peso has been on a roller coaster ride. Economists at Commerzbank analyze USD/MXN outlook.

USD/MXN to remain around 17 for the time being

Last week's fairly significant period of Peso weakness confirms our view that much of the upside is already priced into the MXN and that further appreciation potential is likely to be limited.

Although Mexico's real interest rate will continue to improve as inflation continues to decline, as long as Banxico leaves interest rates unchanged, this is not a fundamental shift in monetary policy that would justify a revaluation of the Peso.

Analysts do not expect the first rate cuts until the end of the year. As long as there is no significant change, we expect the USD/MXN to remain around 17 for the time being, thanks to the still attractive real interest rate.

- EUR/JPY extends the upside to the mid-157.00s.

- Extra advance is expected to target the YTD top past 158.00.

EUR/JPY advances further and leaves behind the 157.00 hurdle on Wednesday.

So far, the continuation of the upside momentum appears likely with the initial target still at the 2023 high at 158.04 (July 21). The breakout of this level exposes a move to the round level of 160.00.

So far, the longer term positive outlook for the cross appears favoured while above the 200-day SMA, today at 146.84.

EUR/JPY daily chart

- EUR/JPY extends the upside to the mid-157.00s.

- Extra advance is expected to target the YTD top past 158.00.

EUR/JPY advances further and leaves behind the 157.00 hurdle on Wednesday.

So far, the continuation of the upside momentum appears likely with the initial target still at the 2023 high at 158.04 (July 21). The breakout of this level exposes a move to the round level of 160.00.

So far, the longer term positive outlook for the cross appears favoured while above the 200-day SMA, today at 146.84.

EUR/JPY daily chart

Economists at CIBC Capital Markets expect NZD/USD to remain under pressure in the short term. However, the pair is set to bounce back higher in the fourth quarter.

Short term headwinds

The on-hold RBNZ should enable NZD/USD to depreciate in the short term, as the Fed appears underpriced for a final hike. This dynamic should drive NZD/USD through Q3, but we then see the pair rising to 0.63 by Q4.

The weak Chinese economy is likely to continue weighing on the NZD through Q3, but when stimulus eventually arrives, NZD/USD should move higher.

Ultimately, NZD/USD faces short term headwinds from an on-hold RBA and weak Chinese economy, but over the longer term, the major drivers of the currency appear to be lining up for a NZD rally.

Economists at CIBC Capital Markets expect NZD/USD to remain under pressure in the short term. However, the pair is set to bounce back higher in the fourth quarter.

Short term headwinds

The on-hold RBNZ should enable NZD/USD to depreciate in the short term, as the Fed appears underpriced for a final hike. This dynamic should drive NZD/USD through Q3, but we then see the pair rising to 0.63 by Q4.

The weak Chinese economy is likely to continue weighing on the NZD through Q3, but when stimulus eventually arrives, NZD/USD should move higher.

Ultimately, NZD/USD faces short term headwinds from an on-hold RBA and weak Chinese economy, but over the longer term, the major drivers of the currency appear to be lining up for a NZD rally.

- USD/CAD rebounds after building a base around 1.3400 as the market mood turns cautious.

- US headline inflation for July is expected to rebound as oil prices recovered sharply last month.

- USD/CAD shifts auction above the 1.3387 resistance, which turns into a support for the US Dollar bulls.

The USD/CAD pair attempts to break the consolidation above the round-level support of 1.3400 in the European session. The Loonie asset finds strength as the US Dollar rebounds after discovering a cushion near 102.30.

Bearish sentiment revives as investors turn cautious ahead of the United States inflation data, which will be released on Thursday at 12:30 GMT. US headline inflation for July is expected to rebound as oil prices recovered sharply last month.

July’s inflation data is expected to build a base for Federal Reserve’s (Fed) September monetary policy as sticky price pressures would force policymakers to consider an extension of policy-tightening.

USD/CAD shifts auction above the horizontal resistance plotted from July 07 high at 1.3387 on a four-hour scale, which turns into a support for the US Dollar bulls. The Loonie asset is approaching the next resistance plotted around 1.3650. Upward-sloping 20-period Exponential Moving Average (EMA) at 1.3400 provides support to the US Dollar.

The Relative Strength Index (RSI) (14) oscillates in a 40.00-60.00 range, which indicates a consolidation ahead.

Mean-reversion move to near 1.3400 would be a buying opportunity for the US Dollar bulls. This would drive the asset toward June 05 high at 1.3462 followed by the psychological resistance at 1.3500.

In an alternate scenario, a downside move below July 18 high at 1.3288 would drag the asset toward July 27 low around 1.3160 and July 14 low marginally below 1.3100.

USD/CAD four-hour chart

-638271826616214793.png)

EUR had little to oppose the USD move on Tuesday. Economists at Commerzbank analyze EUR/USD outlook.

Little momentum for EUR

The ECB is likely to remain concerned regarding inflation in the Eurozone, while also being hopeful that the positive development will continue.

Contrary to the situation in the US, the economy in the Eurozone is weakening, which is likely to put pressure on EUR. If inflation then continues to move in the right direction, rate cut speculation for the Eurozone might be re-fuelled.

Once again market participants have to be patient though as there will be no significant new data from the Eurozone this week. Next week’s GDP data might provide more momentum again.

GBP/USD has found decent support on dips over the past week but gains have been capped below 1.28. Economists at Scotiabank analyze the pair’s outlook.

GBP should remain well-supported on dips