- Аналітика

- Новини та інструменти

- Новини ринків

Новини ринків

- EUR/USD trimmed near-term gains on Monday, holding above 1.0800 but declining.

- French elections delivered a less-than-solid outcome, coalition minority set for deadlock.

- US Fed Chair Powell due to testify before US federal committees this week.

EUR/USD stumbled on Monday after a muddled election outcome in France leaves policy guidance unclear for the Euro bloc. A coalition minority government win in France kept a financially-disastrous far right party out of the leadership race after a strong upset in earlier European Parliamentary elections. Still, the win was anything but decisive as a hodge-podge of coalition parties with conflicting ideologies is set for policy deadlock in France in the coming months.

Forex Today: All eyes on Powell

Federal Reserve (Fed) Chairman Jerome Powell is set to make the first of two appearances this week as the Fed head delivers the semiannual Monetary Policy Report to the US Senate Banking Committee. This will be followed up by a second appearance on Wednesday to deliver the same report to the US Congressional House Committee on Financial Services.

Later this week, key US inflation data will be released. The US Consumer Price Index (CPI) inflation is due on Thursday, and the Producer Price Index (PPI) wholesale inflation is slated for Friday. Some traders who are hoping for a decrease in inflation to push the Fed into making rate cuts sooner rather than later may be disappointed. Forecasts suggest that both CPI and PPI inflation figures are expected to either remain steady or increase slightly.

Final German inflation figures will be published during the Thursday European market session. German Harmonized Index of Consumer Prices (HCOB) inflation is broadly expected to hold steady 2.5% YoY as inflation pressures continues to vex the Bundestag’s 2% inflation target.

Economic Indicator

Consumer Price Index ex Food & Energy (MoM)

Inflationary or deflationary tendencies are measured by periodically summing the prices of a basket of representative goods and services and presenting the data as the Consumer Price Index (CPI). CPI data is compiled on a monthly basis and released by the US Department of Labor Statistics. The MoM print compares the prices of goods in the reference month to the previous month.The CPI Ex Food & Energy excludes the so-called more volatile food and energy components to give a more accurate measurement of price pressures. Generally speaking, a high reading is seen as bullish for the US Dollar (USD), while a low reading is seen as bearish.

Read more.Next release: Thu Jul 11, 2024 12:30

Frequency: Monthly

Consensus: 0.2%

Previous: 0.2%

Source: US Bureau of Labor Statistics

The US Federal Reserve has a dual mandate of maintaining price stability and maximum employment. According to such mandate, inflation should be at around 2% YoY and has become the weakest pillar of the central bank’s directive ever since the world suffered a pandemic, which extends to these days. Price pressures keep rising amid supply-chain issues and bottlenecks, with the Consumer Price Index (CPI) hanging at multi-decade highs. The Fed has already taken measures to tame inflation and is expected to maintain an aggressive stance in the foreseeable future.

EUR/USD technical levels

Fiber is struggling after repeated near-term failures to breach above 1.0840, and bulls are running out of gas as the 200-hour Exponential Moving Average (EMA) rises into 1.0780, keeping a tight floor under intraday price action.

Daily candles continue to churn in the midrange of a rough descending channel through 2024, and EUR/USD is set to face a drooping technical ceiling as the upper bound eases to 1.0850.

EUR/USD hourly chart

EUR/USD daily chart

Euro FAQs

The Euro is the currency for the 20 European Union countries that belong to the Eurozone. It is the second most heavily traded currency in the world behind the US Dollar. In 2022, it accounted for 31% of all foreign exchange transactions, with an average daily turnover of over $2.2 trillion a day. EUR/USD is the most heavily traded currency pair in the world, accounting for an estimated 30% off all transactions, followed by EUR/JPY (4%), EUR/GBP (3%) and EUR/AUD (2%).

The European Central Bank (ECB) in Frankfurt, Germany, is the reserve bank for the Eurozone. The ECB sets interest rates and manages monetary policy. The ECB’s primary mandate is to maintain price stability, which means either controlling inflation or stimulating growth. Its primary tool is the raising or lowering of interest rates. Relatively high interest rates – or the expectation of higher rates – will usually benefit the Euro and vice versa. The ECB Governing Council makes monetary policy decisions at meetings held eight times a year. Decisions are made by heads of the Eurozone national banks and six permanent members, including the President of the ECB, Christine Lagarde.

Eurozone inflation data, measured by the Harmonized Index of Consumer Prices (HICP), is an important econometric for the Euro. If inflation rises more than expected, especially if above the ECB’s 2% target, it obliges the ECB to raise interest rates to bring it back under control. Relatively high interest rates compared to its counterparts will usually benefit the Euro, as it makes the region more attractive as a place for global investors to park their money.

Data releases gauge the health of the economy and can impact on the Euro. Indicators such as GDP, Manufacturing and Services PMIs, employment, and consumer sentiment surveys can all influence the direction of the single currency. A strong economy is good for the Euro. Not only does it attract more foreign investment but it may encourage the ECB to put up interest rates, which will directly strengthen the Euro. Otherwise, if economic data is weak, the Euro is likely to fall. Economic data for the four largest economies in the euro area (Germany, France, Italy and Spain) are especially significant, as they account for 75% of the Eurozone’s economy.

Another significant data release for the Euro is the Trade Balance. This indicator measures the difference between what a country earns from its exports and what it spends on imports over a given period. If a country produces highly sought after exports then its currency will gain in value purely from the extra demand created from foreign buyers seeking to purchase these goods. Therefore, a positive net Trade Balance strengthens a currency and vice versa for a negative balance.

- GBP/USD briefly found fresh highs above 1.2840 before slumping back on Monday.

- The first of two appearances from Fed Chair Powell is slated for Tuesday.

- Key US consumer and wholesale inflation figures due later this week.

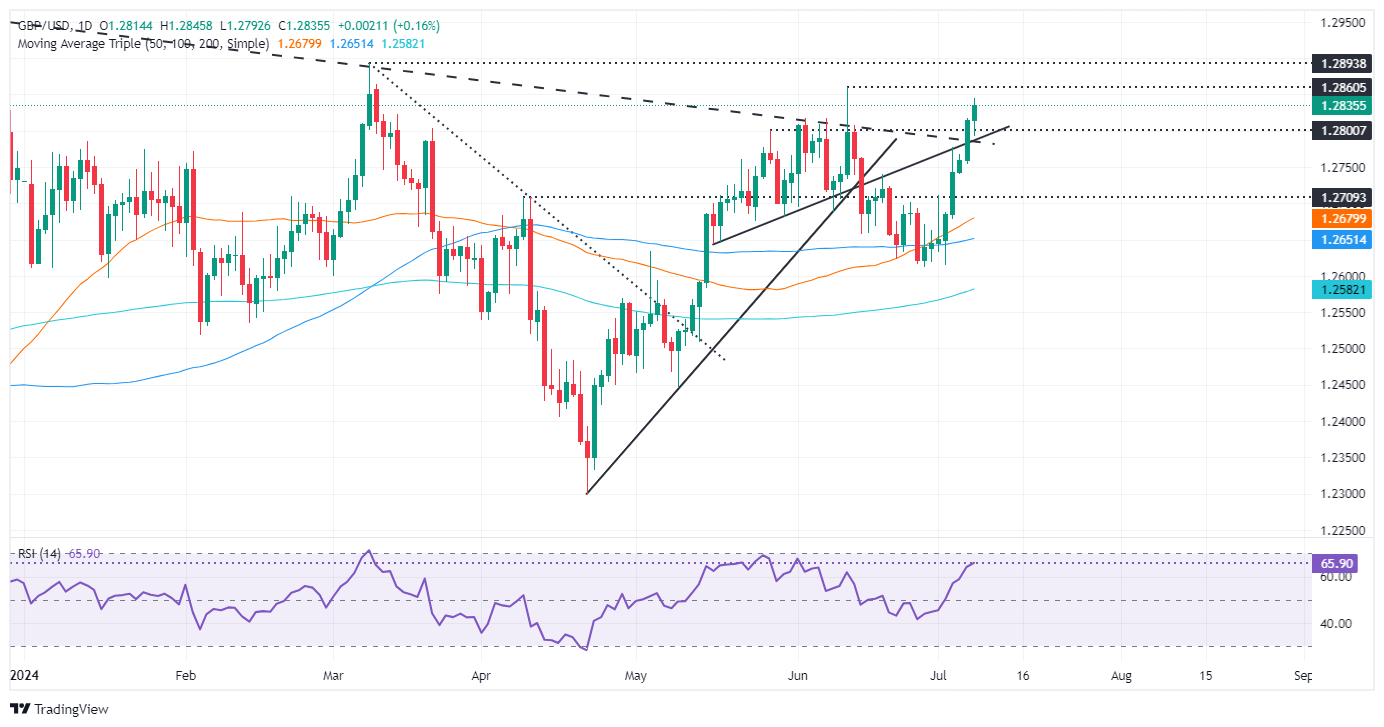

GBP/USD briefly tested a fresh four-week high on Monday, crossing above 1.2840 before broad-market flows dragged Cable back down to the week’s opening bids just north of 1.2800. UK data remains thin this week, leaving traders grappling with peaking rate cut hopes clashing with an overly-cautious Federal Reserve (Fed) that insists on waiting for further signs that US inflation will ease towards the Fed’s 2% annual inflation target.

Forex Today: All eyes on Powell

Fed Chairman Jerome Powell will make the first of two appearances this week when he delivers the Fed’s latest semiannual Monetary Policy Report to the US Senate Banking Committee. Fed Chair Powell will follow up with a repeat performance when testifying before the Congressional House Committee on Financial Services on Wednesday.

Key US inflation data is due later in the week, with US Consumer Price Index (CPI) inflation due on Thursday and Producer Price Index (PPI) wholesale inflation slated for Friday. Traders hoping for further easing in inflation figure to help bully the Fed into rate cuts sooner rather than later may be setting themselves for disappointment later in the week with both CPI and PPI inflation figures forecast to either hold steady or tick upwards slightly.

UK data also remains limited this week, with various appearances from Bank of England (BoE) policymakers slated for Wednesday and industrial and manufacturing activity survey results on the books for Thursday. UK Industrial and Manufacturing Production are both expected to rebound in May after the previous month’s slight contraction.

Economic Indicator

Consumer Price Index (MoM)

Inflationary or deflationary tendencies are measured by periodically summing the prices of a basket of representative goods and services and presenting the data as The Consumer Price Index (CPI). CPI data is compiled on a monthly basis and released by the US Department of Labor Statistics. The MoM figure compares the prices of goods in the reference month to the previous month.The CPI is a key indicator to measure inflation and changes in purchasing trends. Generally, a high reading is seen as bullish for the US Dollar (USD), while a low reading is seen as bearish.

Read more.Next release: Thu Jul 11, 2024 12:30

Frequency: Monthly

Consensus: 0.1%

Previous: 0%

Source: US Bureau of Labor Statistics

The US Federal Reserve has a dual mandate of maintaining price stability and maximum employment. According to such mandate, inflation should be at around 2% YoY and has become the weakest pillar of the central bank’s directive ever since the world suffered a pandemic, which extends to these days. Price pressures keep rising amid supply-chain issues and bottlenecks, with the Consumer Price Index (CPI) hanging at multi-decade highs. The Fed has already taken measures to tame inflation and is expected to maintain an aggressive stance in the foreseeable future.

GBP/USD technical levels

Cable has firmly rallied after recovering from July’s early swing low towards 1.2600, but bullish momentum has stopped short of breaching June’s key peak at 1.2860. The pair is still trading on the high side of the 200-hour Exponential Moving Average (EMA) at 1.2735.

Bullish daily candles are set for a bearish turnaround as bids get set adrift within a heavy supply zone above 1.2800. Price action has so far stayed on the north side of the 200-day EMA at 1.2609.

GBP/USD hourly chart

GBP/USD daily chart

Pound Sterling FAQs

The Pound Sterling (GBP) is the oldest currency in the world (886 AD) and the official currency of the United Kingdom. It is the fourth most traded unit for foreign exchange (FX) in the world, accounting for 12% of all transactions, averaging $630 billion a day, according to 2022 data. Its key trading pairs are GBP/USD, aka ‘Cable’, which accounts for 11% of FX, GBP/JPY, or the ‘Dragon’ as it is known by traders (3%), and EUR/GBP (2%). The Pound Sterling is issued by the Bank of England (BoE).

The single most important factor influencing the value of the Pound Sterling is monetary policy decided by the Bank of England. The BoE bases its decisions on whether it has achieved its primary goal of “price stability” – a steady inflation rate of around 2%. Its primary tool for achieving this is the adjustment of interest rates. When inflation is too high, the BoE will try to rein it in by raising interest rates, making it more expensive for people and businesses to access credit. This is generally positive for GBP, as higher interest rates make the UK a more attractive place for global investors to park their money. When inflation falls too low it is a sign economic growth is slowing. In this scenario, the BoE will consider lowering interest rates to cheapen credit so businesses will borrow more to invest in growth-generating projects.

Data releases gauge the health of the economy and can impact the value of the Pound Sterling. Indicators such as GDP, Manufacturing and Services PMIs, and employment can all influence the direction of the GBP. A strong economy is good for Sterling. Not only does it attract more foreign investment but it may encourage the BoE to put up interest rates, which will directly strengthen GBP. Otherwise, if economic data is weak, the Pound Sterling is likely to fall.

Another significant data release for the Pound Sterling is the Trade Balance. This indicator measures the difference between what a country earns from its exports and what it spends on imports over a given period. If a country produces highly sought-after exports, its currency will benefit purely from the extra demand created from foreign buyers seeking to purchase these goods. Therefore, a positive net Trade Balance strengthens a currency and vice versa for a negative balance.

- USD/CAD remains capped within a trading range near 1.3635 in Tuesday’s early Asian session.

- Loosening US labor market triggered the Fed rate cut expectation this year.

- Lower crude oil prices weigh on the Loonie.

The USD/CAD pair oscillates in a narrow trading range around 1.3635 during the early Asian session on Tuesday. Traders prefer to wait on the sidelines ahead of Powell’s semi-annual testimonies and key US data. Additionally, the Federal Reserve’s (Fed) Michael Barr and Michelle Bowman are set to speak later on Tuesday.

Meanwhile, the USD Index (DXY) hovers around the 105.00 barrier despite lower US bond yields. The recent US employment report for June hinted that the labour market in the United States is cooling sharply, triggering the expectation that the US Fed could lower its borrowing costs sooner than expected this year. This, in turn, is likely to weigh on the Greenback. Investors have priced in nearly 76% odds of a Fed rate cut in September, up from 71% last Friday, according to the CME FedWatch tool.

On the CAD’s front, weakening Canadian employment on Friday raised expectations for rate cuts from the Bank of Canada (BoC). Canada's Unemployment Rate rose to 6.4% in June from 6.2% in May, according to Statistics Canada.

Meanwhile, crude oil prices edge lower in response to growing peace talks in the Middle East, exerting some selling pressure on the commodity-linked Canadian Dollar (CAD) as Canada is the major crude oil exporter to the United States.

Canadian Dollar FAQs

The key factors driving the Canadian Dollar (CAD) are the level of interest rates set by the Bank of Canada (BoC), the price of Oil, Canada’s largest export, the health of its economy, inflation and the Trade Balance, which is the difference between the value of Canada’s exports versus its imports. Other factors include market sentiment – whether investors are taking on more risky assets (risk-on) or seeking safe-havens (risk-off) – with risk-on being CAD-positive. As its largest trading partner, the health of the US economy is also a key factor influencing the Canadian Dollar.

The Bank of Canada (BoC) has a significant influence on the Canadian Dollar by setting the level of interest rates that banks can lend to one another. This influences the level of interest rates for everyone. The main goal of the BoC is to maintain inflation at 1-3% by adjusting interest rates up or down. Relatively higher interest rates tend to be positive for the CAD. The Bank of Canada can also use quantitative easing and tightening to influence credit conditions, with the former CAD-negative and the latter CAD-positive.

The price of Oil is a key factor impacting the value of the Canadian Dollar. Petroleum is Canada’s biggest export, so Oil price tends to have an immediate impact on the CAD value. Generally, if Oil price rises CAD also goes up, as aggregate demand for the currency increases. The opposite is the case if the price of Oil falls. Higher Oil prices also tend to result in a greater likelihood of a positive Trade Balance, which is also supportive of the CAD.

While inflation had always traditionally been thought of as a negative factor for a currency since it lowers the value of money, the opposite has actually been the case in modern times with the relaxation of cross-border capital controls. Higher inflation tends to lead central banks to put up interest rates which attracts more capital inflows from global investors seeking a lucrative place to keep their money. This increases demand for the local currency, which in Canada’s case is the Canadian Dollar.

Macroeconomic data releases gauge the health of the economy and can have an impact on the Canadian Dollar. Indicators such as GDP, Manufacturing and Services PMIs, employment, and consumer sentiment surveys can all influence the direction of the CAD. A strong economy is good for the Canadian Dollar. Not only does it attract more foreign investment but it may encourage the Bank of Canada to put up interest rates, leading to a stronger currency. If economic data is weak, however, the CAD is likely to fall.

- GBP/JPY found yet another new 16-year peak, but momentum is slumping.

- Strictly mid-tier data is on the economic calendar for the Guppy this week.

- GBP/JPY continues to grind out fresh peaks, but topping patterns are growing.

GBP/JPY briefly tested a fresh 16-year peak as the pair continues to grind out years-long high bids. The Guppy touched 206.67 before settling back into Monday’s opening range. Despite setting regular new highs in a one-sided trend, bullish momentum appears to be drying up as the pair begins to hesitate on the top end of a nearly seven-month bull run.

Economic data remains light for both the Pound Sterling (GBP) and the Japanese Yen (JPY) this week. Japanese Labor Cash Earnings, reported early on Monday, rose for the year ended in May, but less than expected. Wages grew 1.9% YoY versus the previous revised 1.6%, missing the forecast of 2.1%. Little else of note remains on the data docket this week for the Yen, leaving JPY traders to struggle at the bottom of a long slide in the currency at the hands of a wide rate differential between the JPY and other major global currencies.

UK data also remains limited this week, with various appearances from Bank of England (BoE) policymakers slated for Wednesday and industrial and manufacturing activity survey results on the books for Thursday.

GBP/JPY technical outlook

GBP/JPY fell away from fresh 16-year highs above 206.50 set on Monday, settling back into familiar intraday territory at the 206.00 handle. Technical pressure is still firmly pinned into the bullish side, but topside momentum is showing signs of petering out, and progress in swing highs is slowly rapidly as bidders run out of gas.

Spinning top daily candles are getting priced into the Guppy charts, and traders should be on the lookout for a retreat to the 50-day Exponential Moving Average (EMA) near 200.00. Despite odds of a near-term pullback, the long-term trend heavily favors the bulls, and a rebound from major technical levels could be on the cards looking forward.

GBP/JPY hourly chart

GBP/JPY daily chart

Pound Sterling FAQs

The Pound Sterling (GBP) is the oldest currency in the world (886 AD) and the official currency of the United Kingdom. It is the fourth most traded unit for foreign exchange (FX) in the world, accounting for 12% of all transactions, averaging $630 billion a day, according to 2022 data. Its key trading pairs are GBP/USD, aka ‘Cable’, which accounts for 11% of FX, GBP/JPY, or the ‘Dragon’ as it is known by traders (3%), and EUR/GBP (2%). The Pound Sterling is issued by the Bank of England (BoE).

The single most important factor influencing the value of the Pound Sterling is monetary policy decided by the Bank of England. The BoE bases its decisions on whether it has achieved its primary goal of “price stability” – a steady inflation rate of around 2%. Its primary tool for achieving this is the adjustment of interest rates. When inflation is too high, the BoE will try to rein it in by raising interest rates, making it more expensive for people and businesses to access credit. This is generally positive for GBP, as higher interest rates make the UK a more attractive place for global investors to park their money. When inflation falls too low it is a sign economic growth is slowing. In this scenario, the BoE will consider lowering interest rates to cheapen credit so businesses will borrow more to invest in growth-generating projects.

Data releases gauge the health of the economy and can impact the value of the Pound Sterling. Indicators such as GDP, Manufacturing and Services PMIs, and employment can all influence the direction of the GBP. A strong economy is good for Sterling. Not only does it attract more foreign investment but it may encourage the BoE to put up interest rates, which will directly strengthen GBP. Otherwise, if economic data is weak, the Pound Sterling is likely to fall.

Another significant data release for the Pound Sterling is the Trade Balance. This indicator measures the difference between what a country earns from its exports and what it spends on imports over a given period. If a country produces highly sought-after exports, its currency will benefit purely from the extra demand created from foreign buyers seeking to purchase these goods. Therefore, a positive net Trade Balance strengthens a currency and vice versa for a negative balance.

- NZD/USD saw slight losses but maintained a position above the crucial 20-day SMA support around 0.6120.

- The technical outlook remains positive, despite Monday's bearish activity.

- Bears are testing the 20-day SMA strength.

On Monday, the NZD/USD struggled, losing 0.30% to 0.6125, erasing its daily gains. Despite this, the pair successfully defended its position above the 20-day Simple Moving Average (SMA) support level at 0.6120, a feat securely achieved in the past week.

As for the daily technical indicators, the Relative Strength Index (RSI) now stands at 53, showing a downward movement, indicating that the bullish momentum took a slight hit. The Moving Average Convergence Divergence (MACD) keeps on printing decreasing red bars, noting the fading bearish strength.

NZD/USD daily chart

From the perspective of resistances, the 0.6170 level is the immediate challenge, which is trailed closely by the significant 0.6200 mark. A firm break above these levels can be viewed as a full confirmation of the recent bullish momentum, taking the pair deeper into bullish territory.

Ahead lies immediate support near the 20-day SMA at 0.6120, with stronger support at the decisive 0.6070 mark. If the sellers manage to lower the price below these supports, it will indicate a developing selling pressure that could lead to a deeper corrective decline.

- Silver retreats beneath $31.00 after hitting a daily high of $31.36, forming a bearish harami pattern.

- Support levels to watch: $30.81 (June 21 high) and $30.18 (July 5 low).

- Bullish targets: $31.49 (July 5 high) and YTD high of $32.51 if upward momentum resumes.

Silver price trims some of its last Friday’s gains. It forms a ‘bearish harami’ candlestick chart pattern, an indication that buyers were unable to capitalize on US Dollar weakness to push the grey metal price above last week’s high of $31.49. Therefore, XAG/USD reversed its course after hitting a daily high of $31.36, trading at $30.79, down more than 1.30%.

XAG/USD Price Analysis: Technical outlook

Silver is upward biased, and as I wrote in an article, XAG “has cleared the ‘double bottom’ neckline at the time of writing, validating the chart pattern.” Nevertheless, today’s formation of a bearish chart pattern could pave the way for a pullback.

If XAG/USD sellers drag the spot price below the June 21 high of $30.81, that will expose the next support at the July 5 low of $30.18. On further weakness, the non-yielding metal would likely drop toward the $30.00 figure, with sellers eyeing a test of the 50-day moving average (DMA).

For a bullish continuation, the XAG/USD must clear the July 5 high at $31.49, clearing the path to challenging the $32.00 figure. Up next would be the year-to-date (YTD) high of $32.51.

XAG/USD Price Action – Daily Chart

Silver FAQs

Silver is a precious metal highly traded among investors. It has been historically used as a store of value and a medium of exchange. Although less popular than Gold, traders may turn to Silver to diversify their investment portfolio, for its intrinsic value or as a potential hedge during high-inflation periods. Investors can buy physical Silver, in coins or in bars, or trade it through vehicles such as Exchange Traded Funds, which track its price on international markets.

Silver prices can move due to a wide range of factors. Geopolitical instability or fears of a deep recession can make Silver price escalate due to its safe-haven status, although to a lesser extent than Gold's. As a yieldless asset, Silver tends to rise with lower interest rates. Its moves also depend on how the US Dollar (USD) behaves as the asset is priced in dollars (XAG/USD). A strong Dollar tends to keep the price of Silver at bay, whereas a weaker Dollar is likely to propel prices up. Other factors such as investment demand, mining supply – Silver is much more abundant than Gold – and recycling rates can also affect prices.

Silver is widely used in industry, particularly in sectors such as electronics or solar energy, as it has one of the highest electric conductivity of all metals – more than Copper and Gold. A surge in demand can increase prices, while a decline tends to lower them. Dynamics in the US, Chinese and Indian economies can also contribute to price swings: for the US and particularly China, their big industrial sectors use Silver in various processes; in India, consumers’ demand for the precious metal for jewellery also plays a key role in setting prices.

Silver prices tend to follow Gold's moves. When Gold prices rise, Silver typically follows suit, as their status as safe-haven assets is similar. The Gold/Silver ratio, which shows the number of ounces of Silver needed to equal the value of one ounce of Gold, may help to determine the relative valuation between both metals. Some investors may consider a high ratio as an indicator that Silver is undervalued, or Gold is overvalued. On the contrary, a low ratio might suggest that Gold is undervalued relative to Silver.

- AUD/NZD opened the week mildly higher at around 1.0990.

- New Zealand's struggling economy still causes worries, as the market awaits the RBNZ meeting later this week.

- The RBA continues its hawkish tone, creating a favorable outlook for the Aussie.

Following a climb to the highest level since mid-May and gaining more than 1.20% since late June, the AUD/NZD buyers stepped back to secure some gains but the pair is poised for some consolidation. The Reserve Bank of New Zealand (RBNZ)'s Wednesday meetup and while New Zealand's economic performance still shows signs of struggle, fundamentals lean in favor of the Aussie.

In New Zealand, the focus is on ongoing concerns such as the sluggish economic outlook and the coming meetings of the RBNZ on Wednesday where a hold is priced in. Other mid-tier data this week include the Consumer Inflation expectations and NZ PMIs on Wednesday and Thursday which might fuel moves on the NZD dynamics.

Despite markets betting on a 60% probability of a rate hike by the end of the year, as shown in the RBNZ’s May rate path projection, the market strongly anticipates a November rate cut. Some even foresee an earlier cut in October, considering New Zealand's slowing growth.

Meanwhile, in Australia, the latest hot inflation data has ramped up market expectations. The market now suggests an almost 40% chance of a 25 bps rate hike on the September 24 meeting of the Reserve Bank of Australia (RBA), rising to around 50% by November 5. The RBA recently has been contemplating raising rates, thus benefiting the Aussie.

AUD/NZD technical analysis

Short-term, the AUD/NZD maintains a bullish stance, though the looming potential for a correction as indicated by nearing overbought conditions warrants caution. The Relative Strength Index (RSI) sits close to 70 and the Moving Average Convergence Divergence (MACD) continues to display rising green bars on the chart.

Support levels lie at 1.0950, 1.0930, and 1.0900. Buyers will be eyeing 1.1000 as the next resistance target. A correction might be on the horizon, but as long as the AUD/NZD stays above the 20, 100, and 200-day Simple Moving Averages (SMA), the outlook remains favorable.

AUD/NZD daily chart

- USD/JPY consolidates with technical indicators suggesting a range-bound movement between 160.00 and 162.00.

- Potential Japanese intervention in FX markets looms, deterring aggressive buyers.

- A break above 161.00 could target YTD high of 161.95, while support lies at 160.22, with further downside risks to 158.25.

The USD/JPY consolidates below the psychological 161.00 figure as US Treasury bond yields edge lower and the Greenback weakens. The traders focus on Fed Chair Jerome Powell's semi-annual testimony at the US Congress and the release of US inflation figures. The major trades at 160.79, virtually unchanged.

USD/JPY Price Analysis: Technical outlook

The USD/JPY daily chart is set to continue to trend higher from a price action standpoint, but fears of intervention by Japanese authorities in the FX markets might dent buyers from pushing the exchange rate higher.

Momentum suggests the pair would consolidate within the 160.00-162.00 range, as the Relative Strength Index (RSI) remains flat in bullish territory.

If USD/JPY buyers reclaim 161.00, that could exacerbate an upward move toward the year-to-date (YTD) high of 161.95. Further gains are seen above 162.00, at around the November 1986 high of 164.87.

Conversely, if the major slumps below the April 29 high at 160.22, the next support would be the Senkou Span A at 159.68. A breach of the latter and the pair will test the Kijun-Sen at 158.25, ahead of the Senkou Span B at 156.91.

USD/JPY Price Action – Daily Chart

Japanese Yen PRICE Today

The table below shows the percentage change of Japanese Yen (JPY) against listed major currencies today. Japanese Yen was the strongest against the US Dollar.

| USD | EUR | GBP | JPY | CAD | AUD | NZD | CHF | |

|---|---|---|---|---|---|---|---|---|

| USD | -0.00% | -0.01% | -0.03% | -0.01% | -0.04% | -0.04% | -0.02% | |

| EUR | 0.00% | -0.04% | -0.02% | -0.02% | -0.03% | -0.01% | -0.02% | |

| GBP | 0.01% | 0.04% | 0.02% | 0.02% | 0.02% | 0.02% | 0.01% | |

| JPY | 0.03% | 0.02% | -0.02% | 0.02% | -0.02% | -0.03% | 0.02% | |

| CAD | 0.01% | 0.02% | -0.02% | -0.02% | -0.04% | -0.01% | -0.02% | |

| AUD | 0.04% | 0.03% | -0.02% | 0.02% | 0.04% | -0.02% | -0.01% | |

| NZD | 0.04% | 0.01% | -0.02% | 0.03% | 0.01% | 0.02% | 0.02% | |

| CHF | 0.02% | 0.02% | -0.01% | -0.02% | 0.02% | 0.00% | -0.02% |

The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the Japanese Yen from the left column and move along the horizontal line to the US Dollar, the percentage change displayed in the box will represent JPY (base)/USD (quote).

- Crude Oil markets chilled on Monday, easing lower as odds of supply constraints drop.

- Fears of supply chain disruptions from Tropical Storm Beryl eased after storm downgrade.

- Barrel traders will be looking for a continuation of last week’s supply declines to bolster prices.

West Texas Intermediate (WTI) eased lower on Monday, bleeding bids as broad-market fears of supply disruptions from Tropical Storm Beryl have receded. The tropical storm, which initially made landfall in Texas as a category 1 hurricane, has been downgraded after wind speeds declined, and looks set to peter out without disrupting US domestic Crude Oil markets.

A risk bid from possible supply chain disruptions from Beryl helped to bolster Crude Oil prices last week. However, Monday’s updates to the storm’s projected dissipation has pulled technical support from beneath Crude bids, extending Friday’s declines and sending WTI down to $81.60.

Crude Oil markets will be looking for a continuation of last week’s sharp supply drawdown after both the American Petroleum Institute (API) and the Energy Information Administration (EIA) both post huge week-on-week contractions in US Crude Oil supplies. Energy investors will be looking for a repeat this week when the API reports Weekly Crude Oil Stocks on Tuesday, followed by EIA barrel counts on Wednesday.

Global energy markets continue to keep Crude Oil prices bid on long-running hopes of a broad uptick in fossil fuel demand, but after a half-year of flubbed sparks in demand upticks, analysts are beginning to express skepticism about the accuracy of demand growth projections from the Organization of the Petroleum Exporting Countries (OPEC). Global Crude Oil demand forecasts were initially built upon a foundation of easing global interest rates, a trend that has failed to materialize through 2024.

WTI technical outlook

WTI US Crude Oil has eased back below the 200-hour Exponential Moving Average (EMA) at $82.14, testing close to a familiar technical inflection point at $81.50. WTI flubbed a bullish push into fresh near-term highs last week, falling just short of reclaiming the $84.00 handle and easing back into recent technical levels.

Daily candlesticks are set to finish an unceremonious end to a recent bullish break north of a near-term congestion zone. An extended backslide will see WTI bids challenging the 200-day EMA at $79.29 once more.

WTI hourly chart

WTI daily chart

WTI Oil FAQs

WTI Oil is a type of Crude Oil sold on international markets. The WTI stands for West Texas Intermediate, one of three major types including Brent and Dubai Crude. WTI is also referred to as “light” and “sweet” because of its relatively low gravity and sulfur content respectively. It is considered a high quality Oil that is easily refined. It is sourced in the United States and distributed via the Cushing hub, which is considered “The Pipeline Crossroads of the World”. It is a benchmark for the Oil market and WTI price is frequently quoted in the media.

Like all assets, supply and demand are the key drivers of WTI Oil price. As such, global growth can be a driver of increased demand and vice versa for weak global growth. Political instability, wars, and sanctions can disrupt supply and impact prices. The decisions of OPEC, a group of major Oil-producing countries, is another key driver of price. The value of the US Dollar influences the price of WTI Crude Oil, since Oil is predominantly traded in US Dollars, thus a weaker US Dollar can make Oil more affordable and vice versa.

The weekly Oil inventory reports published by the American Petroleum Institute (API) and the Energy Information Agency (EIA) impact the price of WTI Oil. Changes in inventories reflect fluctuating supply and demand. If the data shows a drop in inventories it can indicate increased demand, pushing up Oil price. Higher inventories can reflect increased supply, pushing down prices. API’s report is published every Tuesday and EIA’s the day after. Their results are usually similar, falling within 1% of each other 75% of the time. The EIA data is considered more reliable, since it is a government agency.

OPEC (Organization of the Petroleum Exporting Countries) is a group of 13 Oil-producing nations who collectively decide production quotas for member countries at twice-yearly meetings. Their decisions often impact WTI Oil prices. When OPEC decides to lower quotas, it can tighten supply, pushing up Oil prices. When OPEC increases production, it has the opposite effect. OPEC+ refers to an expanded group that includes ten extra non-OPEC members, the most notable of which is Russia.

- USD/CHF rose slightly in the quiet market environment ahead of this week's US CPI data.

- Last week's underwhelming US data weighed on the USD.

- Markets are bracing for the US inflation data due later in the week for directional cues.

On Monday, the USD/CHF traded largely neutral around 0.8970 with some gains. That being said, the pair continues soft, following last week's US data which fueled dovish bets on the Federal Reserve (Fed) which made markets dump the USD. There won't be any highlights on Monday and markets brace for inflation data from the US later in the week.

The US markets are now keenly watching for the release of June's Consumer Price Index (CPI). The data will play a crucial role in determining whether the inflation resurgence is tapering off or if the softer readings in April and May were transitory. The headline CPI for June is predicted to decelerate to 3.1% YoY, down from May's 3.3%, marking a third successive month of slowing growth. In addition, Fed Chair Powell delivers his Semiannual Monetary Policy Report to Congress this week on Tuesday which might also shake the USD dynamics.

On the Swiss side, no major highlights are expected this week, hinting that the pair's movement will be mostly driven by the USD's dynamics. Financial markets see over 50% odds of a third interest-rate cut by the Swiss National Bank (SNB) in September. Likewise, the odds of a cut by the Fed in September have soared to around 80% according to the CME FedWatch tool.

USD/CHF technical analysis

The technical outlook remains somewhat negative in the short term. The pair broke the six-day winning streak and has now recorded losses for three consecutive sessions ending last Friday. Moreover, The Moving Average Convergence Divergence (MACD) and Relative Strength Index (RSI) indicators continue to lose momentum.

The pair's movement now centers around whether the buyers will defend the 20-day Simple Moving Average (SMA) at 0.8950. The 100-day SMA, which sits at 0.8990, is now the immediate resistance level.

USD/CHF daily chart

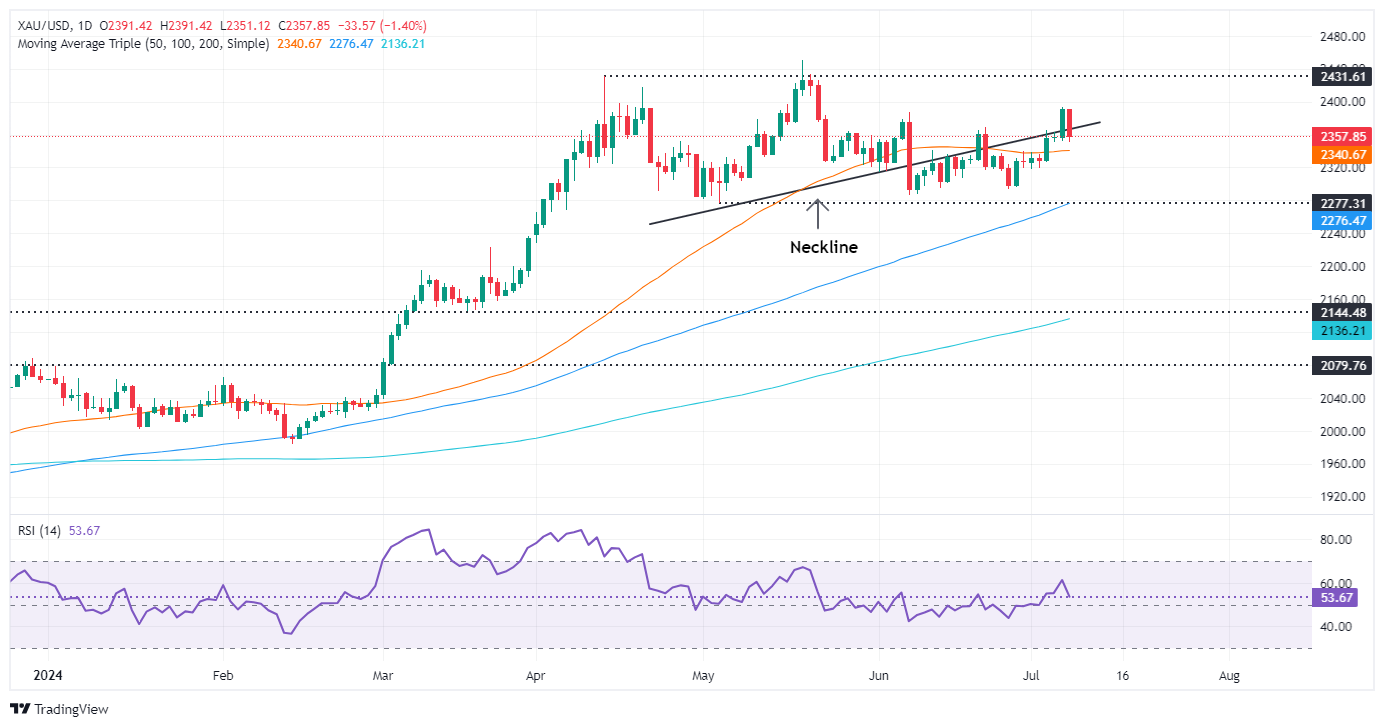

- Gold stumbles after peaking at $2,391 amid revived risk appetite.

- Mixed US jobs data fuel speculation of an imminent Federal Reserve rate cut.

- China's PBoC halts Gold purchases, impacting bullion prices alongside falling Treasury yields.

The Gold price made a U-turn on Monday, trimming some of last Friday's gains and tanking more than 1% as risk appetite returned. US equities posted gains while US Treasury bond yields edged lower. The XAU/USD trades at $2,358 after hitting a daily high of $2,391.

Last week’s US NFP report was mixed. June figures exceeded estimates, but April’s and May’s downward revisions hinted that the US jobs market is cooling sharply. Consequently, the US Unemployment Rate ticked higher, spurring speculation that the Federal Reserve could slash interest rates sooner than expected.

Bullion prices were also hurt by the People Bank of China’s (PBoC) decision not to buy Gold in June, as in May, China held 72.80 million troy ounces of the precious metal at the end of June.

The US 10-year Treasury bond yield fell almost two basis points to 4.27%, reflecting that market players expect the Federal Reserve to lower borrowing costs amid the chances of hurting the labor market.

According to data from the CME FedWatch Tool, investors are pricing in 73% odds of a Fed rate cut in September, up from 71% last Friday.

The US economic docket will feature Fed Chairman Jerome Powell's semi-annual Congressional Testimony and the release of inflation figures on the consumer and producer sides. Initial Jobless Claims and the University of Michigan Consumer Sentiment will also complement the schedule.

Daily digest market movers: Gold price slumps ahead of Fed’s Powell speech

- The US CPI is expected to decrease from 3.3% to 3.1% year-over-year in June, while core inflation is projected to remain steady at 3.4% year-over-year.

- According to the consensus, Initial Jobless Claims for the week ending July 6 are expected to increase from 238K to 240K.

- July Consumer Sentiment is set to improve to 68.5, up from 68.2 in June, according to the consensus.

- Federal Open Market Committee (FOMC) June Meeting Minutes showed that most participants estimated that the current policy is restrictive but had opened the door for rate increases. Policymakers acknowledged the economy is cooling and could react to unexpected economic weakness.

- December 2024 fed funds rate futures contract implies that the Fed will ease policy by 39 basis points (bps) toward the end of the year.

Technical analysis: Gold price retreats below Head-and-Shoulders neckline

Gold price has retreated after decisively breaking the Head-and-Shoulders neckline, which witnessed the XAU/USD price travel to $2,392 before slumping toward $2,357, the current exchange rate, opening the door for a consolidation.

Momentum shows buyers are losing steam, with the Relative Strength Index (RSI) decelerating toward the 50-neutral line, which, if crossed, will hint that sellers are moving in.

If XAU/USD drops below $2,350, further declines could target the $2,300 level. If this support fails, the next demand zone would be the May 3 low of $2,277, followed by the March 21 high of $2,222.

On the other hand, if Gold prices climb above $2,400, further upside is seen, with the next resistance lying at the YTD high of $2,450, ahead of the $2,500 mark.

Gold FAQs

Gold has played a key role in human’s history as it has been widely used as a store of value and medium of exchange. Currently, apart from its shine and usage for jewelry, the precious metal is widely seen as a safe-haven asset, meaning that it is considered a good investment during turbulent times. Gold is also widely seen as a hedge against inflation and against depreciating currencies as it doesn’t rely on any specific issuer or government.

Central banks are the biggest Gold holders. In their aim to support their currencies in turbulent times, central banks tend to diversify their reserves and buy Gold to improve the perceived strength of the economy and the currency. High Gold reserves can be a source of trust for a country’s solvency. Central banks added 1,136 tonnes of Gold worth around $70 billion to their reserves in 2022, according to data from the World Gold Council. This is the highest yearly purchase since records began. Central banks from emerging economies such as China, India and Turkey are quickly increasing their Gold reserves.

Gold has an inverse correlation with the US Dollar and US Treasuries, which are both major reserve and safe-haven assets. When the Dollar depreciates, Gold tends to rise, enabling investors and central banks to diversify their assets in turbulent times. Gold is also inversely correlated with risk assets. A rally in the stock market tends to weaken Gold price, while sell-offs in riskier markets tend to favor the precious metal.

The price can move due to a wide range of factors. Geopolitical instability or fears of a deep recession can quickly make Gold price escalate due to its safe-haven status. As a yield-less asset, Gold tends to rise with lower interest rates, while higher cost of money usually weighs down on the yellow metal. Still, most moves depend on how the US Dollar (USD) behaves as the asset is priced in dollars (XAU/USD). A strong Dollar tends to keep the price of Gold controlled, whereas a weaker Dollar is likely to push Gold prices up.

The Greenback kicked off the week with decent gains, leaving behind some of the NFP-driven weakness and regaining some fresh traction in response to the broad-based knee-jerk in the risk complex. In the meantime, investors continued to digest the French snap elections and gradually shifted their attention to Powell’s semi-annual testimonies and key US data.

Here is what you need to know on Tuesday, July 9:

The USD Index (DXY) reclaimed the 105.00 barrier and above despite the move lower in US yields. The semi-annual testimony by Chair J. Powell to the Congress will be the salient event in the US docket on July 9. In addition, the Fed’s Barr and Bowman are also due to speak.

EUR/USD succumbed to the late rebound in the US Dollar soon after hitting new four-week highs near 1.0850. There are no data releases scheduled for the euro area on July 9.

GBP/USD could not sustain the early move to multi-week tops near 1.2850, eventually ending the session almost unchanged. On July 9, the BRC Retail Sales Monitor is due along with speeches by the BoE’s Cleland and Truran.

USD/JPY alternated gains with losses around the 160.80 region following two daily drops in a row. The Japanese calendar will be empty on July 9.

AUD/USD came under pressure after reaching new six-month peaks in the 0.6760-0.6765 band. The Consumer Confidence gauge tracked by Westpac takes centre stage in Oz on July 9.

WTI prices corrected markedly lower in response to growing peace talks in the Middle East and a stronger US Dollar.

Gold prices retreated from recent peaks near the $2,400 mark per ounce troy on the back of the rebound in the Greenback and some profit taking mood. Silver followed suit and partially left behind the recent robust recovery.

- Despite minimal losses, the AUD/USD remains at its highest level since January, just below 0.6740.

- RBA’s hawkish interest rate stance supports the Aussie.

- Week’s highlight will be inflation figures from the US on Thursday.

The Australian Dollar (AUD) saw some losses on Monday against the USD, which still remains weak after last week's data, which fueled dovish expectations for the Federal Reserve (Fed). With the pair maintaining its highest level since early January, the upside for the Aussie is limited by strong data reported last week along with the Reserve Bank of Australia’s (RBA) hawkish stance.

The RBA appears set to be one of the final G10 countries' central banks to initiate cuts, which should continue to support AUD as it might benefit from monetary policy divergences.

Daily digest market movers: AUD benefited by monetary policy divergences, eyes on US CPI

- US CPI will be reported on Thursday. The headline is expected to decrease slightly to 3.1% YoY, while the core is predicted to remain steady at 3.4% YoY.

- Potential easing by the Fed, juxtaposed with the likely extended restrictive stance of the RBA, could bolster the AUD/USD in coming months.

- Still, concerns about slow momentum of Chinese economy may hinder a sustained recovery of the Australian currency.

- This week doesn't offer any major events on Australia's calendar, and the AUD is forecast to hold its gains against its competitors as long as the RBA maintains its hawkish stance.

- On the Fed's side, there's a 70% chance of a September rate cut, contingent on future data with markets seriously betting on a hike this year by the RBA.

Technical analysis: AUD/USD concedes some ground, further correction possible

The AUD/USD lost ground on Monday, but the overall outlook is positive, backed by deep positive territories on the technical indicators Relative Strength Index (RSI) and Moving Average Convergence Divergence (MACD). With the pair securing a four-day winning streak and reaching its highs since January, the bulls confirmed a bullish outlook last week.

Nevertheless, traders should pay attention to possible overbought conditions, suggesting a slight correction might be imminent.The next bullish targets are at 0.6750 and 0.6780, while support levels to monitor are at 0.6670, 0.6650 and 0.6630.

Australian Dollar FAQs

One of the most significant factors for the Australian Dollar (AUD) is the level of interest rates set by the Reserve Bank of Australia (RBA). Because Australia is a resource-rich country another key driver is the price of its biggest export, Iron Ore. The health of the Chinese economy, its largest trading partner, is a factor, as well as inflation in Australia, its growth rate and Trade Balance. Market sentiment – whether investors are taking on more risky assets (risk-on) or seeking safe-havens (risk-off) – is also a factor, with risk-on positive for AUD.

The Reserve Bank of Australia (RBA) influences the Australian Dollar (AUD) by setting the level of interest rates that Australian banks can lend to each other. This influences the level of interest rates in the economy as a whole. The main goal of the RBA is to maintain a stable inflation rate of 2-3% by adjusting interest rates up or down. Relatively high interest rates compared to other major central banks support the AUD, and the opposite for relatively low. The RBA can also use quantitative easing and tightening to influence credit conditions, with the former AUD-negative and the latter AUD-positive.

China is Australia’s largest trading partner so the health of the Chinese economy is a major influence on the value of the Australian Dollar (AUD). When the Chinese economy is doing well it purchases more raw materials, goods and services from Australia, lifting demand for the AUD, and pushing up its value. The opposite is the case when the Chinese economy is not growing as fast as expected. Positive or negative surprises in Chinese growth data, therefore, often have a direct impact on the Australian Dollar and its pairs.

Iron Ore is Australia’s largest export, accounting for $118 billion a year according to data from 2021, with China as its primary destination. The price of Iron Ore, therefore, can be a driver of the Australian Dollar. Generally, if the price of Iron Ore rises, AUD also goes up, as aggregate demand for the currency increases. The opposite is the case if the price of Iron Ore falls. Higher Iron Ore prices also tend to result in a greater likelihood of a positive Trade Balance for Australia, which is also positive of the AUD.

The Trade Balance, which is the difference between what a country earns from its exports versus what it pays for its imports, is another factor that can influence the value of the Australian Dollar. If Australia produces highly sought after exports, then its currency will gain in value purely from the surplus demand created from foreign buyers seeking to purchase its exports versus what it spends to purchase imports. Therefore, a positive net Trade Balance strengthens the AUD, with the opposite effect if the Trade Balance is negative.

- Dow Jones found early highs before settling back into the low end.

- New trading week kicks things off with a breather after Friday’s NFP.

- US consumer and wholesale inflation figures are due this week.

The Dow Jones Industrial Average (DJIA) whipped on Monday, briefly testing fresh highs and breaking out of Friday’s tight churn before slumping into the red for the new trading week. Federal Reserve (Fed) Chairman Jerome Powell gives the first of a two-day Monetary Policy Report to the US Congress on Tuesday, with key US inflation figures slated for the back half of the trading week.

Fed Chair Powell will deliver the first half of his Monetary Policy Report to the Senate Banking Committee on Tuesday, followed by the same presentation to the House Committee on Financial Services on Wednesday. US Consumer Price Index (CPI) inflation is slated for Thursday, and US Producer Price Index (PPI) wholesale inflation is due Friday.

US inflation figures will be the key data print this week as investors look for signs of rate cuts from the Fed. Despite broad-market hopes for a rate trim, Fed officials have continued to lean into the wait for further evidence that inflation will ease back to the Fed’s 2% annual target. According to the CME’s FedWatch Tool, rate traders are pricing in nearly 80% odds of at least a quarter-point trim to the Fed funds rate on September 18, a little over ten weeks from now.

Waiting for this week’s inflation data will be tense. Core CPI for the year ended June is forecast to hold steady at 3.4% YoY, while core PPI inflation for the same period is expected to tick higher to 2.5% YoY from the previous 2.3% as inflationary pressures remain elevated at the producer-supplier level.

Dow Jones news

The Dow Jones index was mixed on Monday, with roughly half of the equity board’s constituent securities in the green for the day, but overall declines in key goods producers kept headline index prices subdued. Nike Inc. (NKE) fell -2.25% to $73.73 per share, extending into a fresh 52-week low and facing further declines as the shoe manufacturing giant sees growth problems for the year ahead as the footwear giant’s market share gets cannibalized by smaller, more strategic competitors.

Intel Corp. (INTC) surged on Monday, rising 5.3% to $33.72 per share after a note from Melius Research analysts suggested that NVIDIA Corp. (NVDA) competitors like Intel and Advanced Micro Devices Inc. (AMD) could play significant catchup in the AI space with current sector giant NVIDIA.

Dow Jones technical outlook

The Dow Jones Industrial Average (DJIA) rallied in early Monday trading, tapping into a fresh seven-week high of 39,663.30 before a sharp downturn erased the day’s gains. The Dow Jones slid to an intraday low just south of 39,275.00. The major equity index remains down around one-tenth of one percent on Monday.

The Dow Jones has churned in familiar chart territory just above the 50-day Exponential Moving Average (EMA) at 38,983.20 since recovering from late May’s bottom near 38,000.00. Despite holding firmly in the high end, bullish momentum remains limited, and Dow Jones bidders have so far failed to develop the necessary momentum to drag bids back over all-time highs set above the 40,000.00 major price handle.

Dow Jones five minute chart

Dow Jones daily chart

Dow Jones FAQs

The Dow Jones Industrial Average, one of the oldest stock market indices in the world, is compiled of the 30 most traded stocks in the US. The index is price-weighted rather than weighted by capitalization. It is calculated by summing the prices of the constituent stocks and dividing them by a factor, currently 0.152. The index was founded by Charles Dow, who also founded the Wall Street Journal. In later years it has been criticized for not being broadly representative enough because it only tracks 30 conglomerates, unlike broader indices such as the S&P 500.

Many different factors drive the Dow Jones Industrial Average (DJIA). The aggregate performance of the component companies revealed in quarterly company earnings reports is the main one. US and global macroeconomic data also contributes as it impacts on investor sentiment. The level of interest rates, set by the Federal Reserve (Fed), also influences the DJIA as it affects the cost of credit, on which many corporations are heavily reliant. Therefore, inflation can be a major driver as well as other metrics which impact the Fed decisions.

Dow Theory is a method for identifying the primary trend of the stock market developed by Charles Dow. A key step is to compare the direction of the Dow Jones Industrial Average (DJIA) and the Dow Jones Transportation Average (DJTA) and only follow trends where both are moving in the same direction. Volume is a confirmatory criteria. The theory uses elements of peak and trough analysis. Dow’s theory posits three trend phases: accumulation, when smart money starts buying or selling; public participation, when the wider public joins in; and distribution, when the smart money exits.

There are a number of ways to trade the DJIA. One is to use ETFs which allow investors to trade the DJIA as a single security, rather than having to buy shares in all 30 constituent companies. A leading example is the SPDR Dow Jones Industrial Average ETF (DIA). DJIA futures contracts enable traders to speculate on the future value of the index and Options provide the right, but not the obligation, to buy or sell the index at a predetermined price in the future. Mutual funds enable investors to buy a share of a diversified portfolio of DJIA stocks thus providing exposure to the overall index.

- Mexican Peso rallies as USD/MXN drops below 18.00 and hits lowest level since June 25.

- June’s CPI report, Consumer Confidence, and Industrial Production to shape Mexico's economic outlook.

- Banxico minutes likely to signal patience on rate cuts amid steady inflation expectations.

The Mexican Peso rallied sharply against the US Dollar as the USD/MXN fell below the 18.00 psychological figure on Monday, a level last seen on June 25. This signaled that Peso’s buyers remain committed to the so-called “carry trade,” which underpins the Mexican currency. Therefore, the exotic pair exchanged hands at 17.99, down 0.45%.

Mexico’s economic docket will interest traders. The focus is June’s Consumer Price Index (CPI) report, which will be released on July 9. Further data, like Consumer Confidence and Industrial Production, will be released, which will dictate the economic trend and set it to slow down, according to analysts.

On Thursday, the Bank of Mexico (Banxico) will reveal the latest meeting monetary policy minutes, which are expected to show that the central bank will remain patient regarding cutting borrowing costs.

Across the border, the New York Federal Reserve revealed that consumer inflation expectations were lowered from 3.2% to 3% for one year. Besides that, market players will be focused on Federal Reserve (Fed) Chair Jerome Powell's speech at the US Congress on Tuesday and Wednesday and the release of June’s inflation figures.

Last week’s US jobs data sparked speculation that the Fed might ease policy in September, according to the CME FedWatch Tool data. Odds for a September cut stand at 73%, up from 71% last Friday.

Daily digest market movers: Mexican Peso rises further despite firm US Dollar

- Banxico’s survey showed that economists estimate the Gross Domestic Product (GDP) will end the year at 2%, down from 2.1%. They expect Banxico to cut rates from 11.00% to 10.25%, up from 10.00% projected in May.

- Some analysts in Mexico estimate the economy might slow down but dodge a recession, according to the National Statistics Agency (INEGI) Coincident Indicator. Despite that, they said reforms pushed by President Andres Manuel Lopez Obrador (AMLO), particularly the judiciary reform, could affect the country’s creditworthiness.

- Mexico’s CPI is expected to rise from 4.69% YoY to 4.84% in June, while core CPI is estimated to dip from 4.21% to 4.15% annually.

- US CPI is foreseen to drop from 3.3% to 3.1% in the 12 months to June, while underlying inflation is projected to stay firm at 3.4% YoY.

- US Dollar Index (DXY), which tracks the value of a basket of six currencies against the American Dollar, stays firm at 104.94, up 0.06%.

Technical analysis: Mexican Peso stays near weekly highs as USD/MXN hovers around 18.00

The USD/MXN reached a nine-day low of 17.97, though some bids below the 18.00 figure lifted the pair above the latter. The Greenback remains soft against the Peso. The momentum has shifted in the sellers' favor, with the Relative Strength Index (RSI) about to drop below the 50-neutral line.

If USD/MXN achieves a daily close below 18.00, the next support would be the June 24 swing low of 17.87. Further losses lie underneath at the 50-day Simple Moving Average (SMA) at 17.56, followed by the 200-day SMA at 17.26. The next floor level would be the 100-day SMA at 17.17.

For a bullish resumption, the USD/MXN must surpass 18.10, followed by a rally above the June 28 high of 18.59, so buyers can challenge the YTD high at 18.99. Conversely, sellers will need a drop below 18.00, which could extend the pair’s decline toward the December 5 high, which turned support at 17.56, followed by the 50-day Simple Moving Average (SMA) at 17.37.

Mexican Peso FAQs

The Mexican Peso (MXN) is the most traded currency among its Latin American peers. Its value is broadly determined by the performance of the Mexican economy, the country’s central bank’s policy, the amount of foreign investment in the country and even the levels of remittances sent by Mexicans who live abroad, particularly in the United States. Geopolitical trends can also move MXN: for example, the process of nearshoring – or the decision by some firms to relocate manufacturing capacity and supply chains closer to their home countries – is also seen as a catalyst for the Mexican currency as the country is considered a key manufacturing hub in the American continent. Another catalyst for MXN is Oil prices as Mexico is a key exporter of the commodity.

The main objective of Mexico’s central bank, also known as Banxico, is to maintain inflation at low and stable levels (at or close to its target of 3%, the midpoint in a tolerance band of between 2% and 4%). To this end, the bank sets an appropriate level of interest rates. When inflation is too high, Banxico will attempt to tame it by raising interest rates, making it more expensive for households and businesses to borrow money, thus cooling demand and the overall economy. Higher interest rates are generally positive for the Mexican Peso (MXN) as they lead to higher yields, making the country a more attractive place for investors. On the contrary, lower interest rates tend to weaken MXN.

Macroeconomic data releases are key to assess the state of the economy and can have an impact on the Mexican Peso (MXN) valuation. A strong Mexican economy, based on high economic growth, low unemployment and high confidence is good for MXN. Not only does it attract more foreign investment but it may encourage the Bank of Mexico (Banxico) to increase interest rates, particularly if this strength comes together with elevated inflation. However, if economic data is weak, MXN is likely to depreciate.

As an emerging-market currency, the Mexican Peso (MXN) tends to strive during risk-on periods, or when investors perceive that broader market risks are low and thus are eager to engage with investments that carry a higher risk. Conversely, MXN tends to weaken at times of market turbulence or economic uncertainty as investors tend to sell higher-risk assets and flee to the more-stable safe havens.

- Canadian Dollar flows mostly stuck in place on Monday, limiting price momentum.

- Canada has a strictly low-tier showing on the economic calendar this week.

- Markets to keep an eye out for Fed Chair Powell’s Monetary Policy Report.

The Canadian Dollar (CAD) largely churned in familiar territory on Monday, trading softly against the US Dollar (USD) as markets recovered from last Friday’s US jobs data glut. Monday’s sun rises on calmer markets after US labor figures crimped recent gains for the CAD, and USD/CAD is marking out a thin range just below 1.3650.

Canada is almost entirely absent from the economic calendar this week, leaving the CAD adrift against broader market flows. Key US inflation and activity data are due throughout the week, and market participants will be trying to nail down firmer timing on the Federal Reserve’s (Fed) pace of rate cuts moving forward.

Daily digest market movers: Canadian Dollar mostly treads water in Monday kickoff

- Key CAD data is absent this week; CAD traders are forced to wait for the crumbs of Friday’s low-tier Building Permits.

- North American markets will remain tepid until Tuesday’s first of two appearances from Fed Chairman Jerome Powell, who will deliver his two-day Semi-Annual Monetary Policy Report to the US Senate Banking Committee.

- A smattering of appearances from other Fed policymakers are due throughout the first half of the trading week.

- US Consumer Price Index (CPI) inflation is slated for Thursday, with Producer Price Index (PPI) inflation due on Friday.

- Investors will be looking for a further easing in US inflation data to help muscle the Fed closer to a rate cut in September.

Canadian Dollar PRICE Today

The table below shows the percentage change of Canadian Dollar (CAD) against listed major currencies today. Canadian Dollar was the strongest against the Australian Dollar.

| USD | EUR | GBP | JPY | CAD | AUD | NZD | CHF | |

|---|---|---|---|---|---|---|---|---|

| USD | 0.06% | -0.05% | -0.02% | -0.09% | 0.16% | 0.07% | 0.09% | |

| EUR | -0.06% | 0.09% | 0.24% | 0.17% | 0.26% | 0.34% | 0.37% | |

| GBP | 0.05% | -0.09% | 0.10% | 0.09% | 0.16% | 0.25% | 0.27% | |

| JPY | 0.02% | -0.24% | -0.10% | -0.07% | 0.19% | 0.24% | 0.17% | |

| CAD | 0.09% | -0.17% | -0.09% | 0.07% | 0.20% | 0.16% | 0.20% | |

| AUD | -0.16% | -0.26% | -0.16% | -0.19% | -0.20% | 0.09% | 0.10% | |

| NZD | -0.07% | -0.34% | -0.25% | -0.24% | -0.16% | -0.09% | 0.03% | |

| CHF | -0.09% | -0.37% | -0.27% | -0.17% | -0.20% | -0.10% | -0.03% |

The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the Canadian Dollar from the left column and move along the horizontal line to the US Dollar, the percentage change displayed in the box will represent CAD (base)/USD (quote).

Technical analysis: Canadian Dollar spins in place on tepid Monday

The Canadian Dollar (CAD) eased to broadly higher territory on Monday as market focus shifted elsewhere, leaving the CAD to drift in familiar territory. The Canadian Dollar rose around one-quarter of one percent against the New Zealand Dollar (NZD) and the Swiss Franc (CHF), but is trading flatly elsewhere, trading within one-tenth of one percent against the US Dollar, Euro (EUR), Pound Sterling (GBP), and Japanese Yen (JPY).

Last Friday’s NFP-fueled bounce in USD/CAD has run aground of low-volume rocks, and the pair’s recovery from just north of 1.3600 remains within arm’s reach of fresh lows. Further downside is still on the cards if Greenback bulls cannot muscle the pair back above the 200-hour Exponential Moving Average (EMA) at 1.3660.

USD/CAD hourly chart

USD/CAD daily chart

Canadian Dollar FAQs

The key factors driving the Canadian Dollar (CAD) are the level of interest rates set by the Bank of Canada (BoC), the price of Oil, Canada’s largest export, the health of its economy, inflation and the Trade Balance, which is the difference between the value of Canada’s exports versus its imports. Other factors include market sentiment – whether investors are taking on more risky assets (risk-on) or seeking safe-havens (risk-off) – with risk-on being CAD-positive. As its largest trading partner, the health of the US economy is also a key factor influencing the Canadian Dollar.

The Bank of Canada (BoC) has a significant influence on the Canadian Dollar by setting the level of interest rates that banks can lend to one another. This influences the level of interest rates for everyone. The main goal of the BoC is to maintain inflation at 1-3% by adjusting interest rates up or down. Relatively higher interest rates tend to be positive for the CAD. The Bank of Canada can also use quantitative easing and tightening to influence credit conditions, with the former CAD-negative and the latter CAD-positive.

The price of Oil is a key factor impacting the value of the Canadian Dollar. Petroleum is Canada’s biggest export, so Oil price tends to have an immediate impact on the CAD value. Generally, if Oil price rises CAD also goes up, as aggregate demand for the currency increases. The opposite is the case if the price of Oil falls. Higher Oil prices also tend to result in a greater likelihood of a positive Trade Balance, which is also supportive of the CAD.

While inflation had always traditionally been thought of as a negative factor for a currency since it lowers the value of money, the opposite has actually been the case in modern times with the relaxation of cross-border capital controls. Higher inflation tends to lead central banks to put up interest rates which attracts more capital inflows from global investors seeking a lucrative place to keep their money. This increases demand for the local currency, which in Canada’s case is the Canadian Dollar.

Macroeconomic data releases gauge the health of the economy and can have an impact on the Canadian Dollar. Indicators such as GDP, Manufacturing and Services PMIs, employment, and consumer sentiment surveys can all influence the direction of the CAD. A strong economy is good for the Canadian Dollar. Not only does it attract more foreign investment but it may encourage the Bank of Canada to put up interest rates, leading to a stronger currency. If economic data is weak, however, the CAD is likely to fall.

- US Dollar, down 0.80% last week, now at lowest level since mid-June.

- Anticipation builds with the upcoming release of the June inflation figures and Fed talks.

- Market is pricing in less than 10% odds of a cut in July and around 80% in September.

The US Dollar continues to struggle amid signs of disinflation in the US economy, fostering confidence in a potential September rate cut from the Federal Reserve (Fed) among market participants. This week, Fed Chair Jerome Powell and other governors’ words might bail out the USD and limit the losses if they remain cautious.

Despite the trailing softness in the US indicators, Fed officials are still reluctant to embrace cuts, opting to remain data-dependent and might continue asking for patience.

Daily digest market movers: US Dollar continues soft ahead of CPI and Powell’s testimony

- Among the most noteworthy events of the week are Chairman Powell's Semiannual Monetary Policy Report to Congress, multiple Fed members speaking, and the release of inflation data for June.

- On Thursday, the headline Consumer Price Index (CPI) is expected to have dropped two ticks to 3.1% YoY, while the core figure is expected to remain steady at 3.4% YoY.

- As for now, the market predicts less than a 10% chance of a rate cut at the July 31 meeting, with the odds shooting to around 80% for September.

DXY technical outlook: DXY's struggle persists as it resides below 20-day SMA

Following the DXY's slip below the 20-day Simple Moving Average (SMA) and shrinking by 0.80% last week, the technical outlook has shifted for the worst. Both the Relative Strength Index (RSI) and the Moving Average Convergence Divergence (MACD) have slumped into negative territory.

Meanwhile, the 104.70 zone, marked by the 200-day SMA, continues to provide strong support. If the selling pressure continues, the 104.50 and 104.30 areas could potentially put a stop to further losses.

US Dollar FAQs

The US Dollar (USD) is the official currency of the United States of America, and the ‘de facto’ currency of a significant number of other countries where it is found in circulation alongside local notes. It is the most heavily traded currency in the world, accounting for over 88% of all global foreign exchange turnover, or an average of $6.6 trillion in transactions per day, according to data from 2022. Following the second world war, the USD took over from the British Pound as the world’s reserve currency. For most of its history, the US Dollar was backed by Gold, until the Bretton Woods Agreement in 1971 when the Gold Standard went away.

The most important single factor impacting on the value of the US Dollar is monetary policy, which is shaped by the Federal Reserve (Fed). The Fed has two mandates: to achieve price stability (control inflation) and foster full employment. Its primary tool to achieve these two goals is by adjusting interest rates. When prices are rising too quickly and inflation is above the Fed’s 2% target, the Fed will raise rates, which helps the USD value. When inflation falls below 2% or the Unemployment Rate is too high, the Fed may lower interest rates, which weighs on the Greenback.

In extreme situations, the Federal Reserve can also print more Dollars and enact quantitative easing (QE). QE is the process by which the Fed substantially increases the flow of credit in a stuck financial system. It is a non-standard policy measure used when credit has dried up because banks will not lend to each other (out of the fear of counterparty default). It is a last resort when simply lowering interest rates is unlikely to achieve the necessary result. It was the Fed’s weapon of choice to combat the credit crunch that occurred during the Great Financial Crisis in 2008. It involves the Fed printing more Dollars and using them to buy US government bonds predominantly from financial institutions. QE usually leads to a weaker US Dollar.

Quantitative tightening (QT) is the reverse process whereby the Federal Reserve stops buying bonds from financial institutions and does not reinvest the principal from the bonds it holds maturing in new purchases. It is usually positive for the US Dollar.

Economic Indicator

Consumer Price Index (YoY)

Inflationary or deflationary tendencies are measured by periodically summing the prices of a basket of representative goods and services and presenting the data as The Consumer Price Index (CPI). CPI data is compiled on a monthly basis and released by the US Department of Labor Statistics. The YoY reading compares the prices of goods in the reference month to the same month a year earlier.The CPI is a key indicator to measure inflation and changes in purchasing trends. Generally speaking, a high reading is seen as bullish for the US Dollar (USD), while a low reading is seen as bearish.

Read more.Last release: Wed Jun 12, 2024 12:30

Frequency: Monthly

Actual: 3.3%

Consensus: 3.4%

Previous: 3.4%

Source: US Bureau of Labor Statistics

The US Federal Reserve has a dual mandate of maintaining price stability and maximum employment. According to such mandate, inflation should be at around 2% YoY and has become the weakest pillar of the central bank’s directive ever since the world suffered a pandemic, which extends to these days. Price pressures keep rising amid supply-chain issues and bottlenecks, with the Consumer Price Index (CPI) hanging at multi-decade highs. The Fed has already taken measures to tame inflation and is expected to maintain an aggressive stance in the foreseeable future.

USD/CNH traded briefly above 7.31 before turning lower into the week’s close, OCBC FX analysts Frances Cheung and Christopher Wong note.

The pair moves lower tracked broad USD pullback

“Move lower tracked broad US Dollar (USD) pullback while daily fixing reverted to +5pips/day last week (vs. +15 pips/day during 19 – 28 Jun). Today’s fixing came in at -3pips at 7.1286 (vs. 7.1289 on Fri).”

“That said, recent USD/CNY fixings continued to follow a pattern that reinforced our view that authorities are pursuing a measured pace of RMB depreciation, in attempt to let out some depreciation pressure. We believe the Intent is not to pursue a big bang approach so as not to undermine sentiments (for fear of accelerating outflows) – we continue to monitor.”

“But overall, higher USD/CNY fix, wider CNH-CNY spread and worries of escalation in US-China trade tensions may imply some concerns on RMB in the immediate horizon. USDCNH was last at 7.2867 levels. Mild bullish on daily chart eased but decline in RSI moderated. 2-way risks. Resistance at 7.31, 7.3440 (previous high in Oct 2023). Support at 7.28, 7.2770 (21 DMA) and 7.26 (50 DMA).”

The Euro (EUR) started the week on a slightly softer footing after 2nd round election results produced a somewhat surprise outcome, OCBC FX analysts Frances Cheung and Christopher Wong note.

Leftwing government may be a mild negative for EUR

“Leftwing NFP alliance is tops on 182, Macron’s centrists on 163 and the far-right RN and its allies on 143. The outcome shows how elections can be fluid and unpredictable as markets were so fixated on a far-right win. It also shows how tactical dropouts in round 2 elections can affect far-right and swing final outcome.”

“A leftist-dominated government was least expected and most feared as public spending may rise, further putting financial strains on public finance. The only consolation here is that the outcome is a hung parliament, and the left is short of an absolute majority. They will need to find other parties to form a government. A leftist leaning government may be a mild negative for EUR in the interim.”

“EUR was last seen at 1.0833 levels. Mild bullish momentum on daily chart intact but rise in RSI slowed. 2-way risks look more likely. Resistance at 1.0870 (50% fibo). Support at 1.0810 (38.2% fibo retracement of 2024 high to low, 100 DMA). 1.0730/50 levels (23.6% fibo, 21 DMA), 1.0660/ 70 levels (recent low).”

The Dollar Index (DXY) fell last week on softer US data and Fedspeaks, OCBC FX analysts Frances Cheung and Christopher Wong note.

DXY falls on Fedspeaks and softer US data

“While recent headline NFP may have surprised to the upside at +206k vs 190k, the print is now dipping back below the 6month moving average of +222k. 2month payroll downward net revision was also large at -111k while unemployment rate rose to 4.1% (vs. 4% prior). Job vacancy rate is also on a decline. On net, tightness in labour market is easing.”

“This week, we are keeping a close watch on US CPI report (Thu) and Fed Chair Powell’s semi-annual testimony to Banking senate panel (Tue) and House Financial Services Committee (Wed). If there is no change in tune to Powell’s recent remarks and CPI continues to print softer, then the USD slippage may have room to run.”

“DXY was last seen at Last seen at 104.89. Daily momentum turned bearish while RSI fell. Evening star pattern observed on weekly chart. On net, the bearish setup may have room to run. Support at 104.80 (61.8% fibo retracement of Oct high to 2024 low, 100 DMA), 104.50 (200 DMA) and 103.98 (50% fibo). Resistance at 105.10 (50 DMA), 105.80 (76.4% fibo) and 106.20.”

Oil market upside was being driven by supply side risk tied to boiling Middle East tensions, and the rally was extended via Commodity Trading Advisor (CTA) buying flows, TDS Senior Commodity Strategist Ryan McKay notes.

CTAs are set to sell 10% of their max WTI crude position

"Oil market upside was being driven by supply side risk tied to boiling Middle East tensions, and the rally was extended via CTA buying flows."

"However, we highlight that the risk premia associated with Middle East tensions tends to quickly erode without an escalation to a broader conflict, and with systematic flows hitting elevated long levels, the lack of persistent buying is likely to soon weigh on the market. Indeed, CTAs are set to sell roughly 10% of their max WTI crude position, with the $80/bbl region serving as additional key selling levels."