- Аналітика

- Новини та інструменти

- Новини ринків

Новини ринків

- GBP/JPY's descent under the 190.00 mark aligns with a broader downward trend, eyeing further technical levels.

- A pivotal close below the February 29 low could open paths towards 188.73 Kijun-Sen and beyond.

- Recovery hinges on reclaiming ground above 189.00, with resistances waiting at 189.71 and the early March highs.

The GBP/JPY fell for the fourth straight day late in the North American session, set to finish the week with losses of 0.44%, below the 190.00 threshold. At the time of writing, the cross trades at 188.98, down 0.31%.

GBP/JPY Price Analysis: Technical outlook

After diving below February 29 low of 189.04, the GBP/JPY has tilted to the downside, but sellers need to achieve a daily close below that level, so they test the Kijun-Sen at 188.73. Further losses are seen at 188.00, followed by the 50-day moving average (DMA) at 187.47.

On the other hand, if buyers move in and the pair prints a close above 189.00, that could sponsor a leg up. The first resistance would be the Tenkan-Sen at 189.71, followed by the March 7 high at 190.14. the next ceiling level would be the March 4 high at 191.18.

GBP/JPY Price Action – Daily Chart

Chicago Federal Reserve (Fed) President Austan Goolsbee stated that he expects the Fed to begin lowering interest rates later this year as inflation cools off. The head of the Chicago Fed gave his outlook on the Fed's rate stance during an interview with Fox News on Friday.

Chicago President Goolsbee's comments were the last scheduled speaking engagement from Fed officials before the US central bank enters the media blackout period before the March 19-20 policy meeting.

Key highlights

The Fed remains focused on inflation, not price levels.

It is unrealistic to expect price levels to return to pre-COVID levels immediately.

Higher rates have definitely contributed to housing costs.

Fed's Goolsbee expects rates to come down as inflation falls this year.

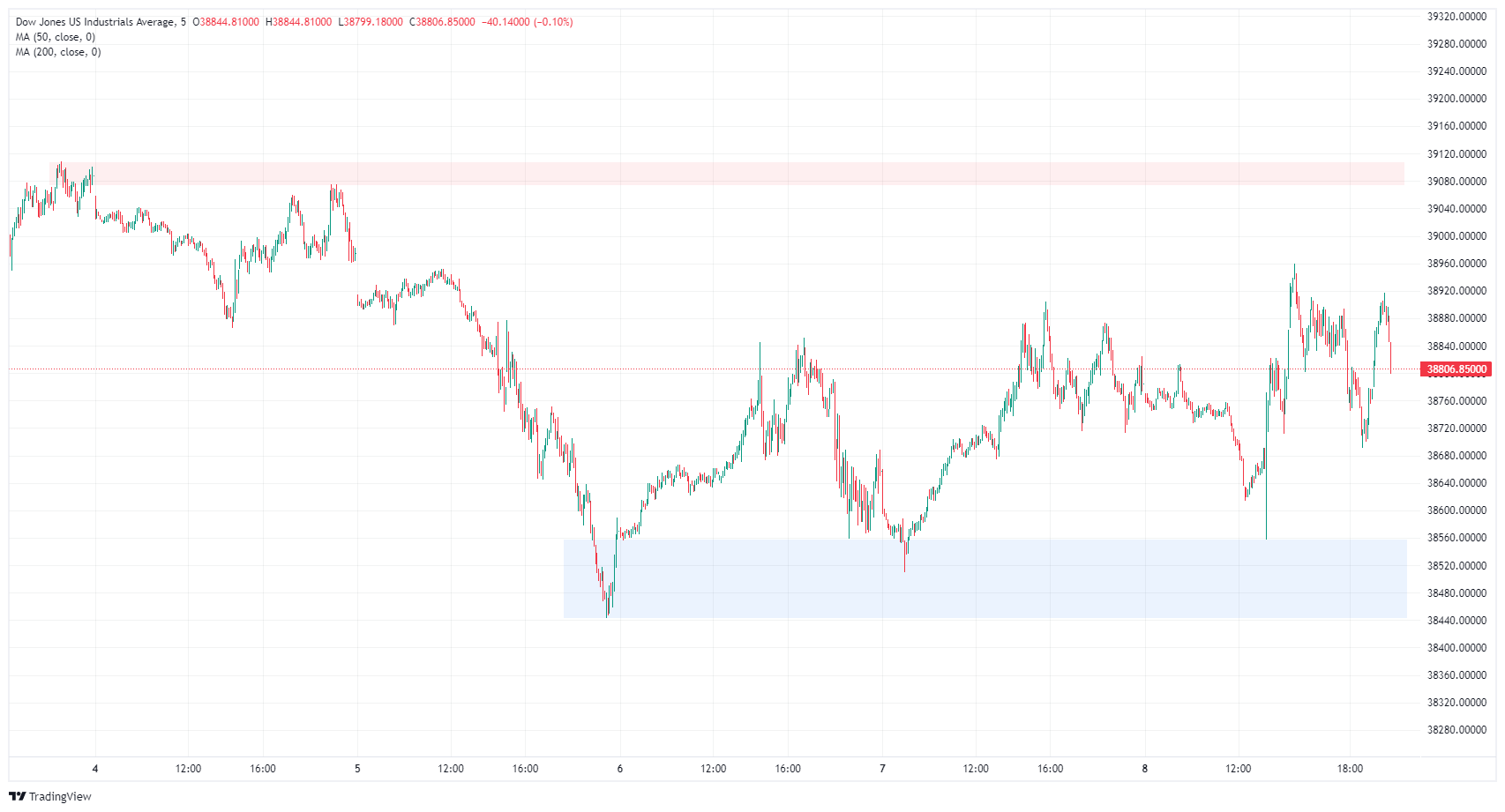

- Dow Jones is in the green on Friday after a mixed US NFP print.

- The S&P 500 and NASDAQ indexes are in the red on the day.

- US NFP jobs data came in better than expected, but with steep revisions.

The Dow Jones Industrial Average (DJIA) is up around a quarter of a percent after US Nonfarm Payrolls (NFP) came in wildly mixed, sending broader markets into a confused tailspin. Equities gave a mixed performance as investors grapple with a still-firm US labor market and deep revising cuts to previous data.

Friday’s NFP print showed the US added 275K net new jobs in February, well above the forecast 200K, but January’s print saw a steep revision to 229K. The previous NFP print initially showed an 11-month high of 353K additions, and the large revision is hobbling the market’s ability to pick a direction to wrap up the trading week.

Dow Jones news: Markets reprice rate cut bets, Apple gains pare Intel losses

Friday’s mixed NFP print increased rate market bets that the Federal Reserve (Fed) will trim interest rates at the Federal Open Market Committee’s June rate call. According to the CME’s FedWatch Tool, rate futures are pricing in 75% of at least a 25 basis point trim in June. Investors are shrugging off warnings from Fed Chairman Jerome Powell this week that inflation is still not at a satisfactory level for the US central bank to begin weighing action on interest rates. Markets are hoping that the Fed will get bullied into rate cuts before the end of H1 2024 with not-as-good-as-expected economic figures.

The DJIA’s worst-performing stock on Friday was Intel Corp. (INTC), down nearly 4% in active trading as investors pull back from a recent tech stock splurge fueled by expectations that Intel will be able to capitalize on the recent popularity of Intel’s services dedicated to AI applications. Apple Inc. (AAPL) is the DJIA’s best performer, paring away some of Intel’s declines and gaining around 2.25% on Friday. Apple is snapping a seven-day losing streak as investors scoop up the tech darling.

Other Friday gainers listed on the Dow Jones include 3M Co. (MMM) and Cisco Systems Inc. (CSCO), gaining around 1.7% apiece. On the down side, Boeing Co. (BA) shed 1.4% on the day, declining to $200.21. The airline stock is down significantly from December’s peak at $267.54.

Dow Jones FAQs

What is the Dow Jones?

The Dow Jones Industrial Average, one of the oldest stock market indices in the world, is compiled of the 30 most traded stocks in the US. The index is price-weighted rather than weighted by capitalization. It is calculated by summing the prices of the constituent stocks and dividing them by a factor, currently 0.152. The index was founded by Charles Dow, who also founded the Wall Street Journal. In later years it has been criticized for not being broadly representative enough because it only tracks 30 conglomerates, unlike broader indices such as the S&P 500.

What factors impact the Dow Jones Industrial Average?

Many different factors drive the Dow Jones Industrial Average (DJIA). The aggregate performance of the component companies revealed in quarterly company earnings reports is the main one. US and global macroeconomic data also contributes as it impacts on investor sentiment. The level of interest rates, set by the Federal Reserve (Fed), also influences the DJIA as it affects the cost of credit, on which many corporations are heavily reliant. Therefore, inflation can be a major driver as well as other metrics which impact the Fed decisions.

What is Dow Theory?

Dow Theory is a method for identifying the primary trend of the stock market developed by Charles Dow. A key step is to compare the direction of the Dow Jones Industrial Average (DJIA) and the Dow Jones Transportation Average (DJTA) and only follow trends where both are moving in the same direction. Volume is a confirmatory criteria. The theory uses elements of peak and trough analysis. Dow’s theory posits three trend phases: accumulation, when smart money starts buying or selling; public participation, when the wider public joins in; and distribution, when the smart money exits.

How can I trade the DJIA?

There are a number of ways to trade the DJIA. One is to use ETFs which allow investors to trade the DJIA as a single security, rather than having to buy shares in all 30 constituent companies. A leading example is the SPDR Dow Jones Industrial Average ETF (DIA). DJIA futures contracts enable traders to speculate on the future value of the index and Options provide the right, but not the obligation, to buy or sell the index at a predetermined price in the future. Mutual funds enable investors to buy a share of a diversified portfolio of DJIA stocks thus providing exposure to the overall index.

Dow Jones Industrial Average forecast

The Down Jones ticked into a new high on Friday, testing 38,960.00 before falling back into range, but the major equity index is on the green side of the day’s opening bids as markets wind down ahead of the week’s closing bell. The DJIA is on pace to close bullish for a third straight day as the index recovers from a near-term decline from Friday’s all-time highs of 39,281.86.

The DJIA recovered from the week’s bottom bids near 38,440.00, but buyers were unable to recover the week’s early peak at 39,075.61.

Dow Jones Industrial Average, 5-minute chart

Nonfarm Payrolls FAQs

What are Nonfarm Payrolls?

Nonfarm Payrolls (NFP) are part of the US Bureau of Labor Statistics monthly jobs report. The Nonfarm Payrolls component specifically measures the change in the number of people employed in the US during the previous month, excluding the farming industry.

How does Nonfarm Payrolls influence the Federal Reserve monetary policy decisions?

The Nonfarm Payrolls figure can influence the decisions of the Federal Reserve by providing a measure of how successfully the Fed is meeting its mandate of fostering full employment and 2% inflation.

A relatively high NFP figure means more people are in employment, earning more money and therefore probably spending more. A relatively low Nonfarm Payrolls’ result, on the either hand, could mean people are struggling to find work.

The Fed will typically raise interest rates to combat high inflation triggered by low unemployment, and lower them to stimulate a stagnant labor market.

How does Nonfarm Payrolls affect the US Dollar?

Nonfarm Payrolls generally have a positive correlation with the US Dollar. This means when payrolls’ figures come out higher-than-expected the USD tends to rally and vice versa when they are lower.

NFPs influence the US Dollar by virtue of their impact on inflation, monetary policy expectations and interest rates. A higher NFP usually means the Federal Reserve will be more tight in its monetary policy, supporting the USD.

How does Nonfarm Payrolls affect Gold?

Nonfarm Payrolls are generally negatively-correlated with the price of Gold. This means a higher-than-expected payrolls’ figure will have a depressing effect on the Gold price and vice versa.

Higher NFP generally has a positive effect on the value of the USD, and like most major commodities Gold is priced in US Dollars. If the USD gains in value, therefore, it requires less Dollars to buy an ounce of Gold.

Also, higher interest rates (typically helped higher NFPs) also lessen the attractiveness of Gold as an investment compared to staying in cash, where the money will at least earn interest.

Sometimes Nonfarm Payrolls trigger an opposite reaction than what the market expects. Why is that?

Nonfarm Payrolls is only one component within a bigger jobs report and it can be overshadowed by the other components.

At times, when NFP come out higher-than-forecast, but the Average Weekly Earnings is lower than expected, the market has ignored the potentially inflationary effect of the headline result and interpreted the fall in earnings as deflationary.

The Participation Rate and the Average Weekly Hours components can also influence the market reaction, but only in seldom events like the “Great Resignation” or the Global Financial Crisis.

- Indications from the daily chart imply a dominance by sellers for the short term.

- The same indicators on the hourly chart also imply a bearish momentum, although depicting potential signs of diminishing selling traction.

- The hourly RSI is recovering after hitting oversold conditions earlier in the session.

In Friday's session, the NZD/JPY pair is currently changing hands at 90.84, down 0.50%. The technical outlook for the pair points to strong control from sellers. Even though the market has been under a selling spree, recent conditions hint at a potential weakening of this selling pressure.

Based on the indicators of the daily chart, the NZD/JPY pair appears to be dominated by sellers. The Relative Strength Index (RSI) remains within negative territory. Additionally, the rising red bars on the Moving Average Convergence Divergence (MACD), which suggest negative momentum, strengthen the belief of ongoing bearish sentiment.

NZD/JPY daily chart

Shifting attention to the hourly chart, the RSI oscillates near the oversold territory, indicating heavy selling pressure. However, the recent uptick in the RSI value might suggest seller fatigue. Combined with the decreasing red bars in the MACD histogram, this demonstrates a possible loss in the pace of negative momentum.

NZD/JPY hourly chart

In conclusion, there is consistency between the daily and hourly charts, both implying bearish momentum in NZD/JPY. However, the latest hourly indicators hint towards a possible slowdown in the selling pressure – a divergence that traders should keep an eye on. In addition, the overall trend continues to favor the buyers as the cross remains above the 100 and 200-day Simple Moving Averages (SMAs). The fact that it sits below the 20-day Average adds negativity to the short-term outlook.

- EUR/USD spiked after the US NFP print, but mixed numbers confounded markets.

- US NFP showed more jobs added, but steep revisions crimp risk appetite.

- Next week: US and EU CPI inflation on Tuesday.

EUR/USD found some room on the top end on Friday, climbing to a fresh high for the week near 1.0980. Bullish momentum got pulled down after investors realized the US Nonfarm Payrolls (NFP) print was more complicated than the initial reaction.

US NFP job additions came in above expectations, but the previous print was steeply revised lower, taking it down from an 11-month high. European final Gross Domestic Product (GDP) figures broadly came in at expectations, and markets will be pivoting to face next Tuesday’s Consumer Price Index (CPI) inflation prints for both the US and the euro area.

Daily digest market movers: Mixed US NFP confounds markets

- February’s US NFP showed that 275K new jobs were added during the month, well above the forecast 200 K.

- The figure is now higher than January’s print, which was revised sharply lower to 229K from the initial 11-month high of 353K.

- US Average Hourly Earnings growth in February slowed more than expected to 0.1% MoM, below the expected 0.3% and down from the previous month’s 0.5%.

- Annualized Average Hourly Earnings eased to 4.3%, missing the forecast of 4.4%. The previous period also saw a slight downside revision to 4.4% from 4.5%.

- The EU’s final Gross Domestic Product (GDP) did not change from the preliminary release, with Q4’s QoQ GDP staying flat at 0.0%.

- Germany’s YoY Producer Price Index (PPI) unexpectedly recovered ground in January, coming in at -4.4% compared to the forecast decline to -6.6% versus the previous month’s -5.1%.

Euro price today

The table below shows the percentage change of Euro (EUR) against listed major currencies today. Euro was the weakest against the Japanese Yen.

| USD | EUR | GBP | CAD | AUD | JPY | NZD | CHF | |

| USD | 0.13% | -0.23% | 0.29% | 0.04% | -0.58% | 0.10% | 0.00% | |

| EUR | -0.13% | -0.38% | 0.17% | -0.09% | -0.72% | -0.04% | -0.16% | |

| GBP | 0.24% | 0.37% | 0.54% | 0.28% | -0.34% | 0.34% | 0.23% | |

| CAD | -0.29% | -0.17% | -0.54% | -0.26% | -0.88% | -0.21% | -0.33% | |

| AUD | -0.04% | 0.09% | -0.28% | 0.26% | -0.62% | 0.04% | -0.06% | |

| JPY | 0.58% | 0.72% | 0.33% | 0.87% | 0.61% | 0.69% | 0.56% | |

| NZD | -0.10% | 0.04% | -0.34% | 0.21% | -0.06% | -0.67% | -0.12% | |

| CHF | 0.04% | 0.16% | -0.21% | 0.32% | 0.07% | -0.56% | 0.13% |

The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the Euro from the left column and move along the horizontal line to the Japanese Yen, the percentage change displayed in the box will represent EUR (base)/JPY (quote).

Technical Analysis: EUR/USD finds a new high before slumping back

EUR/USD rose to a new eight-week high on Friday, climbing to 1.0981 before settling into the day’s range near 1.0930. The pair is on pace to finish in the green for a third straight week, and the Fiber is up over 2.2% from the last swing low into the 1.0700 handle.

EUR/USD has closed bullish for all but three of the last 17 straight trading days, but that run will be threatened if the pair closes below 1.0951. The Euro is trading well above the 200-day Simple Moving Average (SMA) at 1.0833, extending a bullish recovery after catching a firm bounce from a pullback to 1.0800.

EUR/USD hourly chart

EUR/USD daily chart

Euro FAQs

What is the Euro?

The Euro is the currency for the 20 European Union countries that belong to the Eurozone. It is the second most heavily traded currency in the world behind the US Dollar. In 2022, it accounted for 31% of all foreign exchange transactions, with an average daily turnover of over $2.2 trillion a day.

EUR/USD is the most heavily traded currency pair in the world, accounting for an estimated 30% off all transactions, followed by EUR/JPY (4%), EUR/GBP (3%) and EUR/AUD (2%).

What is the ECB and how does it impact the Euro?

The European Central Bank (ECB) in Frankfurt, Germany, is the reserve bank for the Eurozone. The ECB sets interest rates and manages monetary policy.

The ECB’s primary mandate is to maintain price stability, which means either controlling inflation or stimulating growth. Its primary tool is the raising or lowering of interest rates. Relatively high interest rates – or the expectation of higher rates – will usually benefit the Euro and vice versa.

The ECB Governing Council makes monetary policy decisions at meetings held eight times a year. Decisions are made by heads of the Eurozone national banks and six permanent members, including the President of the ECB, Christine Lagarde.

How does inflation data impact the value of the Euro?

Eurozone inflation data, measured by the Harmonized Index of Consumer Prices (HICP), is an important econometric for the Euro. If inflation rises more than expected, especially if above the ECB’s 2% target, it obliges the ECB to raise interest rates to bring it back under control.

Relatively high interest rates compared to its counterparts will usually benefit the Euro, as it makes the region more attractive as a place for global investors to park their money.

How does economic data influence the value of the Euro?

Data releases gauge the health of the economy and can impact on the Euro. Indicators such as GDP, Manufacturing and Services PMIs, employment, and consumer sentiment surveys can all influence the direction of the single currency.

A strong economy is good for the Euro. Not only does it attract more foreign investment but it may encourage the ECB to put up interest rates, which will directly strengthen the Euro. Otherwise, if economic data is weak, the Euro is likely to fall.

Economic data for the four largest economies in the euro area (Germany, France, Italy and Spain) are especially significant, as they account for 75% of the Eurozone’s economy.

How does the Trade Balance impact the Euro?

Another significant data release for the Euro is the Trade Balance. This indicator measures the difference between what a country earns from its exports and what it spends on imports over a given period.

If a country produces highly sought after exports then its currency will gain in value purely from the extra demand created from foreign buyers seeking to purchase these goods. Therefore, a positive net Trade Balance strengthens a currency and vice versa for a negative balance.

- The hourly chart portrays the RSI in the oversold territory, signaling a potential short-term rebound.

- On a broader perspective, the AUD/JPY remains above the main SMAs, indicating long-term bullish sentiment.

- The daily RSI is also in negative territory, showing increasing selling pressure.

- In the next sessions, the sellers may take a step back to consolidate their movements.

In Friday's session, the AUD/JPY pair is now trading at 97.49, demonstrating a loss of 0.38%. While the pair is currently dominated by sellers, oversold conditions seen on the hourly chart suggest that the pair may see some upside in the short term to consolidate.

Analyzing the daily chart, the pair's Relative Strength Index (RSI) sits in negative territory, showcasing stronger selling momentum. In line with that, the Moving Average Convergence Divergence (MACD) histogram shows increasing negative momentum with rising red bars. Despite the ongoing bearish tendency, the pair manages to stay above the 100 and 200-day Simple Moving Averages (SMAs), which signifies a favorable condition for the bulls overall.

AUD/JPY daily chart

Zooming to the hourly chart, the RSI is currently located in the oversold territory, contrasting sharply with the daily chart, suggesting a possible short-term rebound due to oversold conditions. Likewise, the MACD illustrates increasing negative momentum on the hourly chart, aligning with the daily analysis. Despite differing conditions outlined in the hourly and daily charts, both depict dominant bearish forces, with bulls maintaining their stance in the broader spectrum and with the possibility of a bullish rebound in the short term.

AUD/JPY hourly chart

- Silver inches closer to retesting its year-to-date high of $24.63, after marking a 0.86% increase.

- Technical dynamics suggest potential for further gains if silver surpasses the $24.50 resistance.

- Downside risks loom if silver falls below $24.31, targeting supports at $24.00 and the March 6 low of $23.57.

Silver's price rallies, but it remains below the new year-to-date (YTD) high of $24.63. It reached earlier, post gains of 0.86%, and trades at around $24.50 during the mid-North American session.

XAG/USD Price Analysis: Technical outlook

Silver retreated during the day, below the March 7 daily close of $24.31, which could sponsor a leg down if sellers push the prices lower. However, buyers are keeping Silver’s price above the latter, and if they reclaim the $24.50 level, that could push XAG/USD to re-test $24.63, ahead of $25.00.

On the flip side, if sellers drag Silver’s prices below $24.31, XAG/USD could dive to $24.00. A breach of the latter will expose the March 6 low of $23.57, followed by the confluence of the 100 and 200-day moving average (DMA) at $23.27.

XAG/USD Price Action – Daily Chart

- US NFP on Friday prints big upswing to expectations but steep revisions.

- Canada also mixed, adding more jobs than expected but softer wages.

- Next week: US CPI inflation, strictly low-tier Canadian data.

The Canadian Dollar (CAD) roiled against the US Dollar (USD) on Friday after US Nonfarm Payrolls (NFP) figures came in mixed, and Canadian employment figures were broadly overshadowed by US data. The CAD is broadly softer on the day, shedding weight against all of its major currency peers.

Canada added more jobs than expected in February, but wage growth slowed slightly while the Unemployment Rate ticked a bit higher. On the US side, a big beat on NFP forecasts was overshadowed by a massive downside revision to January’s jobs figure, leaving market sentiment hamstrung. Next week’s economic calendar is notably light on Canadian releases, and markets will be getting the next update on US inflation when February’s Consumer Price Index (CPI) prints next Tuesday.

Daily digest market movers: Split NFP print leaves markets churning on Friday

- The US NFP for February added 275K new jobs during the month versus the forecast of 200K.

- January’s NFP print saw a steep correction, revised down to 229K from the previous 11-month peak of 353K.

- Annualized Hourly Earnings growth for the year ended February eased to 4.3% versus the expected 4.4%, and the previous print saw a slight downside revision from 4.5%.

- The US Unemployment Rate also rose in February, ticking up to 3.9% compared to the expected steady print at 3.7%.

- Canada added 40.7K jobs in February, over double the forecast of 20K and rising slightly from the previous month’s 37.2K.

- The Canadian Unemployment Rate also ticked higher to 5.8% in February from 5.7%, in-line with expectations.

- Canadian Average Hourly Wages printed at 4.9% YoY, easing back from the previous period’s 5.3%.

Canadian Dollar price today

The table below shows the percentage change of Canadian Dollar (CAD) against listed major currencies today. Canadian Dollar was the weakest against the Japanese Yen.

| USD | EUR | GBP | CAD | AUD | JPY | NZD | CHF | |

| USD | 0.04% | -0.29% | 0.10% | -0.08% | -0.43% | 0.00% | -0.11% | |

| EUR | -0.06% | -0.36% | 0.05% | -0.13% | -0.51% | -0.06% | -0.18% | |

| GBP | 0.31% | 0.36% | 0.41% | 0.22% | -0.12% | 0.30% | 0.18% | |

| CAD | -0.10% | -0.06% | -0.41% | -0.19% | -0.53% | -0.09% | -0.23% | |

| AUD | 0.09% | 0.13% | -0.24% | 0.20% | -0.33% | 0.08% | -0.02% | |

| JPY | 0.45% | 0.52% | 0.15% | 0.55% | 0.36% | 0.47% | 0.32% | |

| NZD | -0.01% | 0.04% | -0.30% | 0.11% | -0.08% | -0.43% | -0.17% | |

| CHF | 0.13% | 0.18% | -0.18% | 0.22% | 0.05% | -0.31% | 0.13% |

The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the Euro from the left column and move along the horizontal line to the Japanese Yen, the percentage change displayed in the box will represent EUR (base)/JPY (quote).

Technical analysis: Canadian Dollar softens on Friday, leaks recent gains against Greenback

The Canadian Dollar (CAD) is broadly softer on Friday heading into the trading week’s close, shedding around half a percent against the Japanese Yen (JPY) and the Pound Sterling (GBP). The CAD is also down about a fifth of a percent against the Australian Dollar (AUD), as well as down a tenth of a percent against the Euro (EUR) and the US Dollar.

The USD/CAD roiled during the US trading session, sending the pair down to 1.3420 before recovering into the 1.3475 region. The Loonie is still sharply down from the week’s highs near 1.3605, but it is recovering toward the midrange as Friday markets take aim at the weekend.

Friday’s post-dip recovery sends USD/CAD back into the 200-day Simple Moving Average (SMA) at 1.3477. The long-term moving average has flatlined just below the 1.3800 handle for most of 2024, and the pair is set to continue struggling in the near term as it churns within a rough range between 1.3600 and 1.3400.

USD/CAD hourly chart

USD/CAD daily chart

Canadian Dollar FAQs

What key factors drive the Canadian Dollar?

The key factors driving the Canadian Dollar (CAD) are the level of interest rates set by the Bank of Canada (BoC), the price of Oil, Canada’s largest export, the health of its economy, inflation and the Trade Balance, which is the difference between the value of Canada’s exports versus its imports. Other factors include market sentiment – whether investors are taking on more risky assets (risk-on) or seeking safe-havens (risk-off) – with risk-on being CAD-positive. As its largest trading partner, the health of the US economy is also a key factor influencing the Canadian Dollar.

How do the decisions of the Bank of Canada impact the Canadian Dollar?

The Bank of Canada (BoC) has a significant influence on the Canadian Dollar by setting the level of interest rates that banks can lend to one another. This influences the level of interest rates for everyone. The main goal of the BoC is to maintain inflation at 1-3% by adjusting interest rates up or down. Relatively higher interest rates tend to be positive for the CAD. The Bank of Canada can also use quantitative easing and tightening to influence credit conditions, with the former CAD-negative and the latter CAD-positive.

How does the price of Oil impact the Canadian Dollar?

The price of Oil is a key factor impacting the value of the Canadian Dollar. Petroleum is Canada’s biggest export, so Oil price tends to have an immediate impact on the CAD value. Generally, if Oil price rises CAD also goes up, as aggregate demand for the currency increases. The opposite is the case if the price of Oil falls. Higher Oil prices also tend to result in a greater likelihood of a positive Trade Balance, which is also supportive of the CAD.

How does inflation data impact the value of the Canadian Dollar?

While inflation had always traditionally been thought of as a negative factor for a currency since it lowers the value of money, the opposite has actually been the case in modern times with the relaxation of cross-border capital controls. Higher inflation tends to lead central banks to put up interest rates which attracts more capital inflows from global investors seeking a lucrative place to keep their money. This increases demand for the local currency, which in Canada’s case is the Canadian Dollar.

How does economic data influence the value of the Canadian Dollar?

Macroeconomic data releases gauge the health of the economy and can have an impact on the Canadian Dollar. Indicators such as GDP, Manufacturing and Services PMIs, employment, and consumer sentiment surveys can all influence the direction of the CAD. A strong economy is good for the Canadian Dollar. Not only does it attract more foreign investment but it may encourage the Bank of Canada to put up interest rates, leading to a stronger currency. If economic data is weak, however, the CAD is likely to fall.

- Nonfarm Payrolls data reported by the US Bureau of Labor Statistics came in higher than expected.

- Average Hourly Earnings for February unveiled a lower figure than expected, while the Unemployment Rate increased.

- Markets are still seeing the first cut in June.

- The index will close out a 1% losing week, its worst performance since December.

The US Dollar Index (DXY) is trading near 102.60 on Friday, recording a loss. The driving factors for these movements largely include the dovish stance of the Federal Reserve (Fed) Chair, Jerome Powell, and the weak performance of the US labor market in February.

Despite the Nonfarm Payrolls (NFP) report for February showing that the US Unemployment rate increased while Earnings mildly eased, markets are still betting that the easing cycle will begin in June. For the next session, the USD may suffer additional losses as investors fear an economic slowdown.

Daily digest market movers: DXY falls to lows after NFPs figures

- February's Nonfarm Payrolls reported by the US Bureau of Labor Statistics exceeded expectations, coming in at 275,000, remarkably higher than the predicted 200,000, indicating robust employment growth.

- On the negative side, the Unemployment rate for February saw an increase to 3.9%, higher than expectations of 3.7%.

- Wage inflation measured by the Average Hourly Earnings missed the consensus to rise by 4.3% YoY.

- US Treasury yields show a mixed performance with the 2-year yield at 4.48%, the 5-year yield at 4.06%, and the 10-year yield at 4.09%.

- According to the CME FedWatch Tool, the odds of Fed interest rate cuts in March and May remain low. Markets are bracing for the first cut to come in June.

DXY technical analysis: DXY bears seize control, oversold signals loom

The DXY's outlook is predominantly bearish despite the Relative Strength Index (RSI) nearing oversold conditions. The RSI's position near 30 often signals the potential for a price reversal. With the Moving Average Convergence Divergence (MACD) presenting rising red bars, the momentum is currently pointing toward the bears.

Further compounding this bearish notion, DXY resides below its 20, 100 and 200-day Simple Moving Averages (SMAs), contributing to an overall downward trend. These SMAs are pivotal technical markers, and their placement below current prices typically strengthens the sellers’ grip.

The bearish price action in recent trading sessions allies with the technical indicators to forge a negative short-term outlook. However, the RSI's near-oversold position may provide some potential for buyers to contest the bear’s hold, but they will struggle against the prevailing negative momentum.

US Dollar FAQs

What is the US Dollar?

The US Dollar (USD) is the official currency of the United States of America, and the ‘de facto’ currency of a significant number of other countries where it is found in circulation alongside local notes. It is the most heavily traded currency in the world, accounting for over 88% of all global foreign exchange turnover, or an average of $6.6 trillion in transactions per day, according to data from 2022.

Following the second world war, the USD took over from the British Pound as the world’s reserve currency. For most of its history, the US Dollar was backed by Gold, until the Bretton Woods Agreement in 1971 when the Gold Standard went away.

How do the decisions of the Federal Reserve impact the US Dollar?

The most important single factor impacting on the value of the US Dollar is monetary policy, which is shaped by the Federal Reserve (Fed). The Fed has two mandates: to achieve price stability (control inflation) and foster full employment. Its primary tool to achieve these two goals is by adjusting interest rates.

When prices are rising too quickly and inflation is above the Fed’s 2% target, the Fed will raise rates, which helps the USD value. When inflation falls below 2% or the Unemployment Rate is too high, the Fed may lower interest rates, which weighs on the Greenback.

What is Quantitative Easing and how does it influence the US Dollar?

In extreme situations, the Federal Reserve can also print more Dollars and enact quantitative easing (QE). QE is the process by which the Fed substantially increases the flow of credit in a stuck financial system.

It is a non-standard policy measure used when credit has dried up because banks will not lend to each other (out of the fear of counterparty default). It is a last resort when simply lowering interest rates is unlikely to achieve the necessary result. It was the Fed’s weapon of choice to combat the credit crunch that occurred during the Great Financial Crisis in 2008. It involves the Fed printing more Dollars and using them to buy US government bonds predominantly from financial institutions. QE usually leads to a weaker US Dollar.

What is Quantitative Tightening and how does it influence the US Dollar?

Quantitative tightening (QT) is the reverse process whereby the Federal Reserve stops buying bonds from financial institutions and does not reinvest the principal from the bonds it holds maturing in new purchases. It is usually positive for the US Dollar.

- Mexican Peso appreciates for the seventh consecutive day, buoyed by soft US Dollar following mixed US jobs report.

- Banxico's upcoming rate decision eyed closely after subdued Mexican inflation figures.

- US Nonfarm Payrolls exceed expectations, but revisions and higher Unemployment Rate fuel speculation of June Fed rate cut.

The Mexican Peso appreciated for the seventh straight day on Friday against the US Dollar following a mixed jobs report from the United States that increased speculation that the US Federal Reserve (Fed) would cut interest rates in June. The data helped the Greenback tumble to refresh seven-week lows, a tailwind for the emerging market currency that is set to finish the week with gains of more than 0.20%. The USD/MXN trades at 16.78, down 0.52%.

Mexico’s economic docket is empty on Friday, but data revealed during the week could influence the Bank of Mexico (Banxico) decision on March 21. Gross Fixed Investment remained flat on monthly figures but contracted for the 12 months to December, while Consumer Confidence was unchanged. However, Thursday’s inflation data was the main spotlight, with the Consumer Price Index (CPI) lower than expected on monthly and annual figures, while core CPI was mixed.

On the other side of the border, the US Bureau of Labor Statistics (BLS) revealed a mixed US Nonfarm Payrolls (NFP) report. Although the US economy added more jobs than expected, the BLS downwardly revised January’s figures, while the Unemployment Rate jumped close to the 4% threshold.

Daily digest market movers: Mexican Peso boosted by broad US Dollar weakness

- US Nonfarm Payrolls in February were higher than the consensus of 200K and rose by 275K. January’s figures were revised down to 229K from 353K. Further data underscored that the jobs market is cooling as the Unemployment Rate increased from 3.7% to 3.9%, while Average Hourly Earnings edged lower in monthly and annual figures.

- Earlier, New York Fed President John Williams said that the Fed's tight monetary policy has moderated demand, emphasizing the Fed's dedication to price stability. He stressed that the Fed's decisions are independent of politics and remarked on the economy's strong performance in 2023.

- Mexican economic data released in the week:

- Mexico’s inflation was 4.40% YoY, below estimates of 4.42% and January’s 4.88%. On a monthly basis, CPI was down from 0.11% to 0.09%.

- The Core CPI rose by 4.64% above forecasts but lower than the previous reading of 4.76%, while monthly figures were aligned with estimates of 0.49%, up from 0.40%.

- Mexico’s consumer confidence index was 47.0 in February when adjusted for seasonal factors. The unadjusted index was 47.1.

- Mexico’s Gross Fixed Investment remained flat in December. Nevertheless, on an annual basis, it dipped from 19.2% to 13.4%.

- A Reuters poll sees the Mexican Peso depreciating 7% to 18.24 in 12 months from 16.96 on Monday, according to the median of 20 FX strategists polled between March 1-4. The forecast ranged from 15.50 to 19.00.

- A Reuters poll shows 15 analysts estimate that inflation will slow down in February, corroborating bets that the Bank of Mexico (Banxico) could cut rates as soon as the March 21 meeting.

- Banxico’s private analysts' poll projections for February were revealed. They expect inflation at 4.10%, core CPI at 4.06%, and the economy to grow by 2.40%, unchanged from January. Regarding monetary policy, they see Banxico lowering rates to 9.50% and the USD/MXN exchange rate at 18.31, down from 18.50.

- During Banxico’s quarterly report, policymakers acknowledged the progress on inflation and urged caution against premature interest rate cuts. Governor Victoria Rodriguez Ceja said adjustments would be gradual, while Deputy Governors Galia Borja and Jonathan Heath called for prudence. The latter specifically warned against the risks of an early rate cut.

- Banxico updated its economic growth projections for 2024 from 3.0% to 2.8% YoY and maintained 1.5% for 2025. The slowdown is blamed on higher interest rates at 11.25%, which sparked a shift in three of the five governors of the Mexican Central Bank, who are eyeing the first rate cut at the March 21 meeting.

- The political race is almost defined in the United States after Super Tuesday. Former President Donald Trump leads the Republicans with 995 delegates, shy of the 1,215 needed. On the Democratic side, US President Joe Biden leads with 1,497 delegates, short of the 1,968 needed.

- The CME FedWatch Tool shows traders increased their bets for a 25-basis-point rate cut in June from 52.7% a week ago to 78%.

Technical analysis: Mexican Peso posts solid rally as USD/MXN hovers around 16.80

The USD/MXN downtrend remains in play after breaching below 17.90, printing a new yearly low of 16.76. However, sellers need to achieve a daily close below 16.80 if they would like to test the 2023 yearly low of 16.62. Once that barrier is surpassed, look for October 2015’s low of 16.32 and the 16.00 threshold.

On the other hand, if buyers reclaim the 17.00 figure, that could open the door to testing the 50-day Simple Moving Average (SMA) at 17.05, followed by the 200-day SMA at 17.23 and the 100-SMA at 17.24.

USD/MXN Price Action – Daily Chart

Mexican Peso FAQs

What key factors drive the Mexican Peso?

The Mexican Peso (MXN) is the most traded currency among its Latin American peers. Its value is broadly determined by the performance of the Mexican economy, the country’s central bank’s policy, the amount of foreign investment in the country and even the levels of remittances sent by Mexicans who live abroad, particularly in the United States. Geopolitical trends can also move MXN: for example, the process of nearshoring – or the decision by some firms to relocate manufacturing capacity and supply chains closer to their home countries – is also seen as a catalyst for the Mexican currency as the country is considered a key manufacturing hub in the American continent. Another catalyst for MXN is Oil prices as Mexico is a key exporter of the commodity.

How do decisions of the Banxico impact the Mexican Peso?

The main objective of Mexico’s central bank, also known as Banxico, is to maintain inflation at low and stable levels (at or close to its target of 3%, the midpoint in a tolerance band of between 2% and 4%). To this end, the bank sets an appropriate level of interest rates. When inflation is too high, Banxico will attempt to tame it by raising interest rates, making it more expensive for households and businesses to borrow money, thus cooling demand and the overall economy. Higher interest rates are generally positive for the Mexican Peso (MXN) as they lead to higher yields, making the country a more attractive place for investors. On the contrary, lower interest rates tend to weaken MXN.

How does economic data influence the value of the Mexican Peso?

Macroeconomic data releases are key to assess the state of the economy and can have an impact on the Mexican Peso (MXN) valuation. A strong Mexican economy, based on high economic growth, low unemployment and high confidence is good for MXN. Not only does it attract more foreign investment but it may encourage the Bank of Mexico (Banxico) to increase interest rates, particularly if this strength comes together with elevated inflation. However, if economic data is weak, MXN is likely to depreciate.

How does broader risk sentiment impact the Mexican Peso?

As an emerging-market currency, the Mexican Peso (MXN) tends to strive during risk-on periods, or when investors perceive that broader market risks are low and thus are eager to engage with investments that carry a higher risk. Conversely, MXN tends to weaken at times of market turbulence or economic uncertainty as investors tend to sell higher-risk assets and flee to the more-stable safe havens.

A dreadful week for the Greenback ended with the USD Index (DXY) retreating to two-month lows near 102.30 as investors continued to price in a rate cut in June, while the move lower in US yields also accompanied the downside in the Dollar. Closer to home, the ECB left its policy rates unchanged, as expected, while investors also see the central bank starting its easing cycle in June.

The USD Index (DXY) navigated a “sea of red” this week, accelerating its losses to the low-102.00s in the wake of a firmer US NFP on Friday. Next week, the US Inflation Rate is due on March 12 and is expected to remain at the centre of the debate. On March 14, Producer Prices are also due, along with Retail Sales, weekly Initial Jobless Claims, and Business Inventories. Closing the week emerges Industrial Production and the advanced Michigan Consumer Sentiment.

EUR/USD gathered extra upside traction and finally left behind the 1.0900 hurdle in quite convincing fashion amidst rising bets for an ECB rate cut in June. On the domestic calendar, the final Inflation Rate in Germany is due on March 12, while Industrial Production in the broader Euroland will be published on March 13.

The continuation of the upward trend lifted GBP/USD to multi-month peaks at levels just shy of 1.2900 the figure. An interesting UK calendar next week will see the release of the labour market report on March 12, seconded by GDP figures, Construction Output, Goods Trade Balance, Industrial and Manufacturing Production, and the NIESR Monthly GDP Tracker, all due on March 13.

USD/JPY increased its weekly decline to fresh five-week lows near 146.50 on the back of the deep sell-off in the Greenback and investors’ speculations of a potential BoJ lift-off later in the month. Next week kicks in with the final Q4 GDP Growth Rate, while Producer Prices and the BSI Large Manufacturing index are due on March 12. Additionally, the usual weekly Foreign Bond Investment figures are due on March 14, and the Tertiary Industry Index is expected at the end of the week.

AUD/USD managed to surpass the key 0.6600 barrier and rise to two-month peaks exclusively on the back of Dollar dynamics. In Australia, Consumer Inflation Expectations are due on March 15.

In China, Inflation Rate and Producer Prices come on March 9 prior to New Yuan Loans on March 12 and the House Price Index on March 15. USD/CNH navigated a side-lined range throughout the week, slipping back below the 7.2000 region on Friday.

Anticipating Economic Perspectives: Voices on the Horizon

- RBA S. Hunter speaks on March 11.

- BoE C. Mann speaks on March 12.

After a lacklustre start to the year, Oil prices are starting to come to life. Economists at MUFG Bank analyze Brent’s outlook.

Oil bulls are quietly winning the narrative

Oil bulls are quietly winning the narrative as prices are working their way higher, with a breakout of the $10 range that Brent crude has been confined to so far in 2024, now imminent. Granted, the steady climb is not remarkable, but economic exceptionalism, tightening fundamentals and prompt oil time spreads in backwardation (signalling supply tightness) is reinforcing the constructive narrative.

We maintain our Brent call that prices will hover within a $80.00-$90.00 range this year and view that Oil markets will remain supported by tight micro fundamentals (moderate deficits), OPEC+ driven carry and effective hedging value against negative geopolitical supply shocks.

The Japanese Yen (JPY) has depreciated considerably against the US Dollar (USD) and the Euro (EUR) since the start of 2021. Analysts at Natixis explain why a weak Yen is good for Japan.

The Bank of Japan has little incentive to obtain an appreciation of the Yen

Japan's expansionary monetary policy, while the other OECD countries have adopted a restrictive monetary policy since 2022, has caused the Yen to depreciate sharply. But in reality, the depreciation of the yen is good for Japan's economy: It is helping to bring inflation back towards the 2% target; It stimulates exports; Since Japan has very substantial net external assets, mainly in Dollars and Euros, the depreciation of the Yen generates a capital gain on the yen value of these external assets.

As a result of these positive effects of a weak Yen on Japan, we should not expect Japan to switch to a much more restrictive monetary policy. At most, we should expect a symbolic hike in the Bank of Japan’s base rate.

- New Zealand Dollar rises versus the US Dollar following the release of US employment data.

- US Nonfarm Payrolls rose higher than expected in February, but gains were offset by wage and unemployment data.

- Hourly Earnings fell from what was expected, and the Unemployment Rate unexpectedly rose, suggesting underlying labor market weakness.

The New Zealand Dollar rises against the US Dollar on Friday, after the release of US Nonfarm Payrolls data suggests disinflationary tendencies that could bring forward the time of the Federal Reserve’s (Fed) first expected interest rate cut.

NZD/USD – the number of US Dollars that one New Zealand Dollar can buy – rose to day’s high of 0.6218 on Friday, during the US session, following the release of the Bureau of Labor Statistics (BLS) report. If the data prompts an earlier rate cut from the Fed, it will be negative for the US Dollar as lower rates attract less foreign capital inflows.

New Zealand Dollar prints new high after Nonfarm Payrolls

Whilst the headline NFP figure showed the economy adding 275K jobs in February, which was higher than the 200K expected, the other data in the BLS report suggested weaknesses in the labor market.

Average Hourly Earnings, which are a key component of inflation, rose by a lower-than-expected 4.3% YoY and 0.1% MoM. Both were below the 4.4% and 0.3% predicted. The Unemployment Rate, meanwhile, rose to a higher-than-expected 3.9% when it had been projected to stay put at 3.7%.

The data suggests less inflationary pressure from wages and low unemployment, which could prompt the Fed to bring forward interest rate cuts to earlier in the year. Lower interest rates are negative for the US Dollar as they reduce foreign capital inflows.

New Zealand Dollar supported by Brighter outlook for China

The New Zealand Dollar (NZD) has been further supported by the release of better-than-expected trade data from its largest export partner, China, on Thursday.

The Chinese Trade Balance data showed an unexpected rise in the country’s trade surplus to $125.16 billion in February, according to data from the General Administration of Customs for the People’s Republic of China.

Economists had expected the Trade Balance to come out at only $103.70 billion, from a lower $75.34 billion in the previous month of January.

The higher surplus is a sign of economic health and suggests greater prosperity, leading to increased demand for New Zealand exports, primarily milk and dairy products. This, in turn, is likely to result in an increase in demand for New Zealand’s currency.

Technical analysis: NZD/USD rising in a range

NZD/USD is trading plum in the middle of a sideways consolidation that has lasted for over a year. The long-term trend is too opaque to guess, suggesting little overall directional bias.

New Zealand Dollar vs US Dollar: Daily chart

The top of the range lies at 0.6400, with only a break above indicating a bullish trend developing. The range bottom – if one can be deduced amongst all the ups and downs – lies near 0.5800. Price would need to sink to below this level to turn the trend bearish.

Since Wednesday, price has bounced back from support at the level of the 100 and 200-day Simple Moving Averages (SMA) acting in concert near 0.6090. Although the recovery has been strong, it is not enough to deduce that a short-term uptrend is in play.

If Friday (today) ends as a green up day, a bullish Three White Soldier Japanese candlestick pattern will have formed, suggesting a greater chance of a bullish continuation. However, given the generally sideways nature of the pair, even such a pattern might not be so reliable unless accompanied by a key shift in fundamentals.

New Zealand Dollar FAQs

The New Zealand Dollar (NZD), also known as the Kiwi, is a well-known traded currency among investors. Its value is broadly determined by the health of the New Zealand economy and the country’s central bank policy. Still, there are some unique particularities that also can make NZD move. The performance of the Chinese economy tends to move the Kiwi because China is New Zealand’s biggest trading partner. Bad news for the Chinese economy likely means less New Zealand exports to the country, hitting the economy and thus its currency. Another factor moving NZD is dairy prices as the dairy industry is New Zealand’s main export. High dairy prices boost export income, contributing positively to the economy and thus to the NZD.

The Reserve Bank of New Zealand (RBNZ) aims to achieve and maintain an inflation rate between 1% and 3% over the medium term, with a focus to keep it near the 2% mid-point. To this end, the bank sets an appropriate level of interest rates. When inflation is too high, the RBNZ will increase interest rates to cool the economy, but the move will also make bond yields higher, increasing investors’ appeal to invest in the country and thus boosting NZD. On the contrary, lower interest rates tend to weaken NZD. The so-called rate differential, or how rates in New Zealand are or are expected to be compared to the ones set by the US Federal Reserve, can also play a key role in moving the NZD/USD pair.

Macroeconomic data releases in New Zealand are key to assess the state of the economy and can impact the New Zealand Dollar’s (NZD) valuation. A strong economy, based on high economic growth, low unemployment and high confidence is good for NZD. High economic growth attracts foreign investment and may encourage the Reserve Bank of New Zealand to increase interest rates, if this economic strength comes together with elevated inflation. Conversely, if economic data is weak, NZD is likely to depreciate.

The New Zealand Dollar (NZD) tends to strengthen during risk-on periods, or when investors perceive that broader market risks are low and are optimistic about growth. This tends to lead to a more favorable outlook for commodities and so-called ‘commodity currencies’ such as the Kiwi. Conversely, NZD tends to weaken at times of market turbulence or economic uncertainty as investors tend to sell higher-risk assets and flee to the more-stable safe havens.

Citing three sources familiar with the matter, Reuters reported on Friday that European Central Bank (ECB) policymakers overwhelmingly back June for a reduction in key rates.

Some policymakers floated the idea on the sidelines of Thursday's ECB meeting of a second cut in July, to win over a small group still pushing for an April start, sources further told Reuters.

Market reaction

This headline failed to trigger a noticeable reaction in EUR/USD. At the time of press, the pair was up 0.1% on the day at 1.0960.

The Cocoa price has reached a new record high due to a shortage of supply. A further increase in prices is quite possible, strategists at Commerzbank say.

Cocoa more expensive than ever

The Cocoa price reached a new record high at the beginning of March due to a shortage of supply. This is due to poorer harvests in the two most important producing countries, Ivory Coast and Ghana. The Cocoa market is therefore likely to post a record supply deficit this crop year, with stocks falling to their lowest level for decades.

No relief is expected in the short term, meaning that a further increase in prices is quite possible.

- EUR/JPY falls to 160.86, reacting to rumors of Bank of Japan possibly ending negative interest rates.

- Technical analysis indicates potential for further pullback if pair closes below the 161.31 Kijun-Sen level.

- Recovery above 161.00 could signal a rebound towards the 162.00 mark, with eyes on the March 7 high.

The EUR/JPY dives for the second consecutive day, losing 0.64% in early trading during the North American session. Rumors that the Bank of Japan (BoJ) could end negative rates are growing, hence sponsoring a leg-up in the Japanese Yen (JPY) against most G7 currencies. At the time of writing, the pair exchanges hands at 160.86.

EUR/JPY Price Analysis: Technical outlook

Despite posting a three-week low, the EUR/JPY is slightly tilted to the upside. Nevertheless, if sellers achieve a daily close below the Kijun-Sen at 161.31, that could pave the way for a deeper pullback. The next support would be the 160.00 psychological figures, followed by the Senkou Span B at 159.39 and the top of the Ichimoku Cloud (Kumo) at around 159.00/15.

On the other hand, if buyers lift the exchange rate above 161.00 and reclaim the Kijun-Sen, a leg-up toward 162.00 is on the cards. Once cleared, look for a test of the March 7 high at 162.81.

EUR/JPY Price Action – Daily Chart

USD/MXN fell in February from 17.17 to 17.06. Economists at MUFG Bank analyze Mexican Peso’s outlook.

MXN weakening path ahead

The MXN might weaken in the next few months on the back of a dovish tone of Banxico minutes and weaker-than-expected industrial production and retail sales that could drive a Banxico rate cut coming earlier than the Fed, although some Banxico members are willing to synchronize its decision with the Fed.

From June onwards, the MXN tends to be more strongly influenced by expectations regarding the new government and its policies. Eurasia judges that Ms. Claudia Sheinbaum has an 80% chance to become the next president after the 2nd June election. Morena party tends to maintain the majority at both Lower House and Senate, as well as the majority of state governors. However, the government coalition might not get a two-thirds majority in Congress, thus having to negotiate with the opposition to pass key reforms.

The US election in November and potential immigration and trade policy changes could weigh on Mexico’s economy. In light of those risks, we expect a gradually weaker MXN.

- Australian Dollar rises and marks its third consecutive day of gains.

- US Nonfarm Payrolls outperform expectations at 275K, but rising unemployment and lower wage growth hint at a cooling job market.

- AUD/USD's rally supported by dipping US 10-year Treasury yields and a weakening Dollar Index, amid global monetary policy recalibrations.

The Australian Dollar advanced for the third straight trading day, early in the North American session, edges up 0.35% and exchanges hands at 0.6654.

Aussie Dollar’s strengthens as US Dollar extends its weekly losses

Recently released data by the US Department of Labor revealed the US Nonfarm Payrolls for February exceeded estimates of 200K, came at 275K, and was higher than January’s downward revised 353K reading to 229K. Further data underscored that the jobs market is cooling as the Unemployment Rate increased from 3.7% to 3.9%, while Average Hourly Earnings edged lower in monthly and annual figures.

The AUD/USD extended its rally toward a daily high of 0.6664, while US Treasury bond yields edged lower. The US 10-year benchmark note rate is down to 4.044%, the lowest level since February 2.

At the same time, the US Dollar Index (DXY) is tumbling 0.25%, sitting at 102.52, threatening to drop to an eight-week low.

New York Fed Williams: Neutral interest rates “still quite low”

Earlier, the New York Fed President John Williams said the restrictive monetary stance has cooled demand, adding that the Fed is responsible for achieving price stability. He said the Fed doesn’t consider politics in deliberations and stated the economy in 2023 was remarkable.

Aside from this, Australian data revealed during the week showed a surplus in the Trade Balance, while the economy grew 0.2% QoQ in Q4 2023, below estimates of 0.3%. On a yearly basis, the economy expanded 1.5% YoY, above estimates but shy of the previous reading of 2.1%.

AUD/USD Price Analysis: Technical outlook

The AUD/USD sitting above the 0.6600 figure, has opened the door for further upside, as confirmed by Relative Strength Index (RSI) studies at bullish territory. If buyers extend the rally toward 0.6700, that could open the door for testing the January 5 high at 0.6747, before challenging the 0.6800 mark. On the other hand, a pullback below the January 5 low of 0.6640, could exacerbate a test of the 0.6600 figure.

Economists at HSBC analyze the Swiss Franc (CHF) outlook.

EUR/CHF is likely to track sideways

The CHF’s bad performance is in part due to its safe-haven status, as global equity markets gain. The Swiss Franc has also been hit by the Swiss National Bank’s (SNB) shift in tone around the currency, with FX strength no longer a policy tool or aspiration it seems.

We continue to look for a higher USD/CHF over the near term, while the EUR/CHF pair is likely to track sideways.

- GBP/JPY finds an intermediate support near 188.60. More downside likely on BoJ rate hike bets.

- BoJ policymakers see a positive cycle for wage growth, able to keep inflation above 2%.

- The Pound Sterling will be guided by the UK’s labor market data, scheduled for next week.

The GBP/JPY pair discovers temporary support near 188.60 after sharply correcting from 191.00 in the last three trading sessions. The asset is expected to witness more downside as market expectations for the Bank of Japan (BoJ) abandoning negative interest rates have improved.

A few BoJ policymakers expect a positive cycle in wage growth, improving the odds of inflation remaining above the 2% target sustainable. The BoJ had been reluctant to exit the expansionary policy stance as policymakers were not convinced that wage growth would continue to grow steadily. Investors hope the BoJ will shift to policy normalization in the March monetary policy meeting.

The Japanese Yen would witness strong buying interest if the BoJ delivers a hawkish interest rate decision, as its monetary policy has remained extremely dovish for more than a decade.

Meanwhile, the Pound Sterling awaits fresh guidance on interest rates. The United Kingdom's economic calendar remained light this week. Going forward, investors will focus on the labor market data for three months ending in January, which will be published early next week. Investors will keenly focus on the Average Earnings data, which will provide a fresh outlook on inflation.

The UK’s wage growth has remained almost double what is required to be consistent with the return of inflation to 2%. Strong wage growth momentum would dampen market expectations for rate cuts, which could result in higher investment in the Pound Sterling.

AUD/USD is testing the water above the 0.6600 level for the first time since early February. Economists at Rabobank analyze the pair’s outlook.

Potential for further dips back to 0.6500 in the one-to-three-month horizon

The Aussie should continue to draw support from a relatively hawkish central bank and, compared with various other major economies, a strong set of fundamentals which include both a balanced budget and positive current account position.

We see scope for AUD/USD to move to 0.7000 on a 12-month horizon. That said, we also see the potential for further dips back to 0.6500 in the one-to-three-month horizon on further bouts of USD strength.

Federal Reserve Bank of New York President John Williams noted on Friday that demand has cooled amid the restrictive monetary policy stance, per Reuters.

Key takeaways

"Fed is responsible for achieving price stability."

"Understanding price-wage dynamics is key research topic."

"Inflation expectations have come down quite a bit."

"Neutral interest rate is likely still quite low."

"Nobody thinks high inflation is a good thing."

"Fed focuses on mission, does not consider politics in deliberations."

Market reaction

These comments failed to trigger a noticeable market reaction. At the time of press, the US Dollar Index was unchanged on the day at 102.80.

- The US Dollar extends losses to levels not seen since mid-January.

- US Federal Reserve Chairman Jerome Powell triggered the sell-off by confirming that rate cuts will come this year.

- The US Dollar Index trades below 103.00, and might snap 102.00 if NFP data disappoints.

The US Dollar (USD) is entering on Friday what could become a sixth consecutive day of losses after Thursday ended with the longest red candle of the week. In the showdown between the US Federal Reserve (Fed) and the European Central Bank (ECB), the Fed sounded more dovish as Chairman Jerome Powell committed to rate cuts this year, while ECB’s President Christine Lagarde did not even mention cuts in her statement after the ECB rate decision. Meanwhile, data out of the US that signals losing momentum gives markets the sense of urgency that the Fed will need to move quickly to salvage a soft landing.

On the economic calendar front, only one real data point will be important this Friday. The US EmploymentReport will release its monthly change in Nonfarm Payrolls, with expectations at 200,000, coming from 353,000 a month earlier. The lowest estimate among economists is around 110,000 and the highest at 286,000, which means that any print below the lowest estimate will likely see another leg of US Dollar weakness. In contrast, an upbeat number above 286,000 will probably see the DXY pare back Thursday’s losses.

Daily digest market movers: Fed is ready to pull the trigger on cuts

- The US Jobs Report for February will be published at 13:30 GMT:

- Nonfarm Payrolls growth is expected to decline from 353,000 to 200,000.

- Growth in Yearly Average Hourly Earnings is expected to fall slightly from 4.5% to 4.4%.

- Monthly Average Hourly Earnings growth should also decrease from 0.6% to 0.3%.

- The Unemployment Rate should remain stable at 3.7%.

- Equities are flat to mildly in the green after the Asia closing. Equities were on fire on Thursday after Powell commented that the Fed is ready to cut once data falls in line.

- According to the CME Group’s FedWatch Tool, expectations for a Fed pause in the March 20 meeting are at 95%, while chances of a rate cut stand at 5%.

- The benchmark 10-year US Treasury Note trades around 4.07%, the lowest level in over a week.

US Dollar Index Technical Analysis: Thursday’s nosedive

The US Dollar Index (DXY) broke below 103.00 on Thursday after a string of events with both the ECB and the Fed firing up markets on possible rate cuts to come. The US Jobs Report this afternoon could make it a full week of losses for the DXY, or have it salvage the situation by pushing it back up above 103.00. One thing remains clear: the road to recovery back to 105.00 will be long and hard, with King Dollar going away for a longer time.

On the upside, the first reclaiming ground is at 103.28, the 55-day Simple Moving Average (SMA), and at the 200-day SMA near 103.72. Once broken through, the 100-day SMA is popping up at 103.81, so a bit of a double cap in that region. Depending on the catalyst that pushes the DXY upwards, 104.60 remains the key level on the topside.

The DXY is trading a bit in nomad's land, with not really any significant support levels nearby. More downside looks inevitable with 101.75 up next, which bears some pivotal relevance. Once through there, the road is open for another leg lower to 100.61, the low of 2023.

Nonfarm Payrolls FAQs

Nonfarm Payrolls (NFP) are part of the US Bureau of Labor Statistics monthly jobs report. The Nonfarm Payrolls component specifically measures the change in the number of people employed in the US during the previous month, excluding the farming industry.

The Nonfarm Payrolls figure can influence the decisions of the Federal Reserve by providing a measure of how successfully the Fed is meeting its mandate of fostering full employment and 2% inflation. A relatively high NFP figure means more people are in employment, earning more money and therefore probably spending more. A relatively low Nonfarm Payrolls’ result, on the either hand, could mean people are struggling to find work. The Fed will typically raise interest rates to combat high inflation triggered by low unemployment, and lower them to stimulate a stagnant labor market.

Nonfarm Payrolls generally have a positive correlation with the US Dollar. This means when payrolls’ figures come out higher-than-expected the USD tends to rally and vice versa when they are lower. NFPs influence the US Dollar by virtue of their impact on inflation, monetary policy expectations and interest rates. A higher NFP usually means the Federal Reserve will be more tight in its monetary policy, supporting the USD.

Nonfarm Payrolls are generally negatively-correlated with the price of Gold. This means a higher-than-expected payrolls’ figure will have a depressing effect on the Gold price and vice versa. Higher NFP generally has a positive effect on the value of the USD, and like most major commodities Gold is priced in US Dollars. If the USD gains in value, therefore, it requires less Dollars to buy an ounce of Gold. Also, higher interest rates (typically helped higher NFPs) also lessen the attractiveness of Gold as an investment compared to staying in cash, where the money will at least earn interest.

Nonfarm Payrolls is only one component within a bigger jobs report and it can be overshadowed by the other components. At times, when NFP come out higher-than-forecast, but the Average Weekly Earnings is lower than expected, the market has ignored the potentially inflationary effect of the headline result and interpreted the fall in earnings as deflationary. The Participation Rate and the Average Weekly Hours components can also influence the market reaction, but only in seldom events like the “Great Resignation” or the Global Financial Crisis.

The new all-time highs for Gold are noteworthy. Strategists at Commerzbank think there is too much interest rate optimism on the Gold market and see the sharp rise as an exaggeration.

Lasting upside potential only when interest rate cuts in the US begin

The market is mostly pointing to increasing hopes of Fed interest rate cuts, as the latest US economic indicators have been rather disappointing.

The new all-time highs on the Gold market are driven by short-term speculation. We therefore expect a correction in the coming days and weeks.

Only when the cycle of interest rate cuts in the US actually begins there is likely to be lasting upside potential.

ANZ Bank’s analysis concludes that normalising inflation is sustainable, and the ECB will cut interest rates in the second quarter (Q2).

ECB readying to cut in Q2, rate setters focused on June

We expect that the ECB will begin cutting interest rates in Q2.

We believe that the improvement in inflation is sustainable and that below trend growth and restrictive monetary transmission will drive further weakness in inflation in coming months.

Real policy rates have risen sharply, and we estimate they will make record highs during the first half of this year.

The ECB wants to be doubly sure that inflation is sustainably trending towards 2.0%. It is therefore proceeding with caution.

Our assessment of current guidance from ECB officials is that hawks are in the ascendancy and there is a preference to wait for more data on wage growth before starting to cut. We think there is a consensus building around June.

- WTI Oil recovers on Friday towards $80 on a positive demand outlook.

- Oil traders are betting on a pickup in demand as interest-rate cuts should spur economic growth.

- The US Dollar Index fell below the 103.00 level, trading in the mid-102.00s ahead of NFP.

Oil prices are increasing on Friday, looking again at the $80 level, as investors seem to bet on an improved demand outlook. The move comes after dovish comments from US Federal Reserve Chairman Jerome Powell, who said in a two-day hearing in Congress that the Fed is ready to cut interest rates. Lower rates are likely to spur economic growth, and this could mean more demand for Oil.

The US Dollar, however, didn’t like this message. The US Dollar Index (DXY), which tracks the Greenback against a basket of foreign currencies, fell sharply on Thursday. . With the US Dollar weakening, Oil prices have room to rise in the correlation between the Greenback and the commodity. Should the US Nonfarm Payrolls (NFP) number this afternoon trigger another round of US Dollar weakness, Crude could close off this week above $80.

Crude Oil (WTI) trades at $78.91 per barrel, and Brent Oil trades at $83.04 per barrel at the time of writing.

Oil news and market movers: Demand is already underway

- Oil traders are back to placing bullish bets on Oil with the underlying idea that rate interest-rate cuts in both Europe and the US would spur economic growth and thus see a pickup in demand again.

- An increase in demand is already underway inAsia, with India and China buying up every cheap contract in sight as their industrial and travel demand picks up pace. These two sectors are very Oil-consuming.

- The failed ceasefire talks are keeping tensions high in Gaza.

- This Friday, the Baker Hughes Oil Rig Count is set to be released at 18:00 GMT. The previous count was at 506 rigs.

Oil Technical Analysis: Back to 2013

Oil prices are entering dynamics not seen since 2013, when a substantially weaker US Dollar opened up space for Oil prices to rise towards $100. Seeing the current rate cuts and dovish stance by the Fed, more upside could be at hand.. Although $100 is still far off, chances are growing.

Oil bulls still clearly see more upside potential. The break above $80 though does not seem to be taking place that quickly, and $85 is appearing as the next cap. Further up, $86.90 follows suit before targeting $89.64 and $90.00 as top levels.

On the downside, the 200-day Simple Moving average (SMA) near $77.93 is the first point of contact to provide some support. Quite close behind are the 100-day and the 55-day SMAs near $75.81 and $75.26, respectively. Add the pivotal level near $75.27, and it looks like the downside is very limited and well-equipped to resist the selling pressure.

US WTI Crude Oil: Daily Chart

WTI Oil FAQs

WTI Oil is a type of Crude Oil sold on international markets. The WTI stands for West Texas Intermediate, one of three major types including Brent and Dubai Crude. WTI is also referred to as “light” and “sweet” because of its relatively low gravity and sulfur content respectively. It is considered a high quality Oil that is easily refined. It is sourced in the United States and distributed via the Cushing hub, which is considered “The Pipeline Crossroads of the World”. It is a benchmark for the Oil market and WTI price is frequently quoted in the media.

Like all assets, supply and demand are the key drivers of WTI Oil price. As such, global growth can be a driver of increased demand and vice versa for weak global growth. Political instability, wars, and sanctions can disrupt supply and impact prices. The decisions of OPEC, a group of major Oil-producing countries, is another key driver of price. The value of the US Dollar influences the price of WTI Crude Oil, since Oil is predominantly traded in US Dollars, thus a weaker US Dollar can make Oil more affordable and vice versa.

The weekly Oil inventory reports published by the American Petroleum Institute (API) and the Energy Information Agency (EIA) impact the price of WTI Oil. Changes in inventories reflect fluctuating supply and demand. If the data shows a drop in inventories it can indicate increased demand, pushing up Oil price. Higher inventories can reflect increased supply, pushing down prices. API’s report is published every Tuesday and EIA’s the day after. Their results are usually similar, falling within 1% of each other 75% of the time. The EIA data is considered more reliable, since it is a government agency.

OPEC (Organization of the Petroleum Exporting Countries) is a group of 13 Oil-producing nations who collectively decide production quotas for member countries at twice-yearly meetings. Their decisions often impact WTI Oil prices. When OPEC decides to lower quotas, it can tighten supply, pushing up Oil prices. When OPEC increases production, it has the opposite effect. OPEC+ refers to an expanded group that includes ten extra non-OPEC members, the most notable of which is Russia.

- EUR/GBP weakens after several ECB officials talk up the possibility of an early rate cut.

- Francois Villeroy de Galua and Joachim Nagel talk of spring rate cut, putting April back on the table.

- The technical outlook turns more bearish as price sinks back down towards February’s lows.

The Euro (EUR) is sinking, trading in the 0.8510s against the Pound Sterling (GBP) on Friday, after two leading members of the European Central Bank's (ECB) Governing Council (GC) voiced approval for a spring rate cut.

Their dovish views clash with the more cautious stance of the ECB President Christine Lagarde, who said on Thursday, that June would be the next key date for reviewing policy on interest rates.

Spring can be anytime from “April to June” says De Galau

Francois Villeroy de Galau, Governor of the Bank of France and GC member, said a rate cut in spring was now “very likely” on Friday, adding, “spring goes from April to June.”

His ECB colleague, Bundesbank President Joachim Nagel, said "The probability is increasing that we could see an interest-rate cut before the summer break," adding, "This will be data dependent, but the prospects have brightened." According to a report on Poundsterlinglive.com.

The comments led to broad based weakness for the Euro as lower interest rates reduce the attractiveness of a currency as a place for foreign investors to park their capital.

Technical Analysis: Price sinking to key support

EUR/GBP’s long-term technical outlook is sideways with a slight bearish bias in the intermediate and short-term.

Given the overall bearish theme of the charts the price will probably continue sinking to the key support level at 0.8493. A break below that would turn the picture much more bearish.

Euro vs Pound Sterling: Daily chart

There are some signs of a possible recovery, however, if price stabilizes.

The Moving Average Convergence/ Divergence (MACD) is converging bullishly with price action suggesting the downtrend may be losing momentum. .

An Inverse Head and Shoulders pattern could be forming, although the chances are diminishing as the market continues falling. For confirmation of the pattern, price would have to break above what is known as “the neckline” which is drawn as a resistance line at the highs. On EUR/GBP the neckline is at 0.8750. Such a break could be followed by a rise of either the same length as the height of the pattern extrapolated higher, or a Fibonacci 61.8%.

Given the confluence of resistance from the 100 and 200-day Simple Moving Averages (SMA) at around 0.8615, as well as resistance from the trendline nearby, this zone provides a potential conservative estimate for the pattern.

- USD/JPY extends its losing spell as the Japanese Yen strengthens on hawkish BoJ bets.

- The US Dollar weakens on firm expectations for the Fed reducing interest rates in June.

- Investors await the US NFP for fresh guidance.

The USD/JPY pair continues its losing spell for the fourth trading session on Friday. The asset falls vertically to 147.00 on firm expectations that the Bank of Japan (BoJ) will pivot to raising interest rates after keeping them in the negative territory for more than a decade.

S&P 500 futures are positive in the European session, indicating a higher risk appetite of the market participants. The 10-year US Treasury yields have dropped significantly to 4.07% as Federal Reserve (Fed) Chair Jerome Powell has recognized the need to dial back the restrictive monetary policy stance to prevent the economy from falling into a recession.

Market expectations for the BoJ exiting the ultra-dovish policy stance increase after a few policymakers said a positive wage cycle is in sight. This has convinced investors that steady wage growth would keep inflation above the 2% target. Investors hope that the BoJ will quit the expansionary policy stance itself in the March policy meeting.