- Аналітика

- Новини та інструменти

- Новини ринків

Новини ринків

- AUD/USD remains on the defensive near 0.6491 amid the firmer USD.

- US Initial Jobless Claims rose by 218K from a week earlier, stronger than expected.

- RBA’s Bullock said the board is focused on bringing inflation down, and the evidence of inflation is encouraging.

The AUD/USD pair extends its downside and holds below the 0.6500 mark during the early Asian session on Friday. The hawkish comments from Federal Reserve (Fed) officials and a stronger US Dollar (USD) weigh on the pair. AUD/USD currently trades around 0.6491, losing 0.01% on the day.

On Thursday, the US weekly Initial Jobless Claims fell to 218K for the week ended February 3 from the previous week of 227K, better than the estimation of 220K. The report indicated ongoing labor market resilience. Continuing Claims decreased by 23K to 1.891M in the week ended January 27. Finally, Wholesale inventories of merchant wholesalers lifted 0.4% MoM and were down 2.7% YoY.

Many Fed officials signaled that they were in no rush to lower borrowing costs until they were confident that inflation would return to the 2% target. On Thursday, Fed Richmond President Thomas Barkin reiterated that policymakers have time to be patient about the timing of rate cuts due to a solid labor market and ongoing disinflation. The US central bank has raised its policy rate by 525 basis points (bps) to the current 5.25% to 5.50% range since March 2022.

Late Thursday, Reserve Bank of Australia (RBA) Governor Michele Bullock stated that the central bank is focused on bringing inflation down, and the evidence of inflation is encouraging. Bullock emphasized that the board hasn’t ruled out a further interest rate hike but neither has it ruled it in.

Dallas Fed L. Logan is set to speak later on Friday. In the absence of top-tier economic data from the US and Australia, risk sentiment will likely play a crucial role in the AUD/USD pair.

The Reserve Bank of Australia (RBA) Governor Michele Bullock spoke in parliament on Thursday after leaving rates on hold earlier this week.

Key quotes

“RBA Board is focused on bringing inflation down.”

“Remain acutely aware that the cost of living is rising much faster than it has over recent decades.”

“Recent developments in inflation are encouraging.”

“We have some way to go to meet our target.”

“Recent developments in inflation are encouraging.”

“We have some way to go to meet our inflation target.”

“Even if the economy evolves along the central path, inflation will still have been outside the target range for four years.”

“While there are some encouraging signs, Australia's inflation challenge is not over.”

“The longer inflation remains high and outside the target range, the greater is the risk that inflation expectations of households and businesses adjust higher.”

“At this stage, the board hasn’t ruled out a further increase in interest rates but neither has it ruled it in.”

“Given the substantial costs to the economy and the Australian people of continued high inflation, the board is committed to bringing inflation back to target in a reasonable time frame.”

“Trying to bring inflation back to target without slowing the economy more than necessary on the one hand or risking high inflation for longer.”

Market reaction

At the press time, the AUD/USD pair was up 0.03% on the day to trade at 0.6495.

- The NZD/JPY rose to 91.05 on Thursday, registering a 0.70% rally.

- The Yen was one of the worst-performing currencies due to dovish BoJ comments.

- On the four-hour chart, overbought conditions suggest a possible correction in the near term.

In Thursday's session, the NZD/JPY staged a rally to land at 91.05, buoyed by steady a softening Yen due to the Bank of Japan’s (BoJ) dovish stance. With the daily chart painting a bullish picture, the pair is tipped in favor of the Kiwi as the pair stands at its highest level since November. However, a potential correction looms on the horizon as the four-hour chart indicators strayed into overbought territory.

In line with that, Deputy Governor Uchida highlighted the unlikelihood of sudden rate hikes which drove markets to bet on a more dovish approach of the BoJ regarding its pivot to a more hawkish policy. For the next sessions, incoming data will be key to dictate the pace of the cross but in case Japan reports negative data, the cross could see further upside as the BoJ won't have incentives to leave its ultra-loose policy.

NZD/JPY technical analysis

The technical indicators on the daily chart reflect bullish dominance. Despite a consolidation looming in the immediate term, the cross is trending above its 20, 100, and 200-day Simple Moving Averages (SMAs), indicative of the buyers' stronghold on larger time frames. The rising slope and placement in the upper region of the Relative Strength Index (RSI) also reinforces the continued bullishness. Moreover, the Moving Average Convergence Divergence (MACD) histogram is demonstrating an uptick with the green bars becoming longer, further empowering the buying momentum.

NZD/JPY daily chart

-638430267362004855.png)

On the shorter four-hour chart, however, a temporary pullback seems likely. The technical indicators have reached the overbought zone suggesting the possibility of an imminent correction. In this context, the Relative Strength Index (RSI) rose above 70 while the Moving Average Convergence Divergence (MACD) displays rising green bars. Given the intense buying pressure in the shorter time frame, a brief retreat in prices aligns with usual asset behavior after bouts of aggressive purchasing momentum.

- Investors kept their eyes on government bond yields and stocks for direction.

- Reserve Bank of Australia Governor Michele Bullock will hit the wires early on Friday.

- NZD/USD could accelerate its slump on a break through 0.6078.

The NZD/USD pair trades just below the 0.6100 mark ahead of the Asian opening, ending Thursday with modest losses. The pair hit 0.6123 at the beginning of the day, but quickly turned south as the US Dollar found legs on strong American data and the soft tone of stock markets. It is worth adding, however, that after spending most of the day in the red, Wall Street has managed to trim early losses, with the Dow Jones Industrial Average and the Nasdaq Composite posting modest gains and the S&P500 poised to end the day little changed just below the 5,000 mark.

Focus on equities and yields

The focus was not only on equities. Investors were also paying attention to US Treasury yields, up on the day on the back of signs the Federal Reserve (Fed) has no reason to rush into cutting interest rates. Multiple policymakers hit the wires these days and backed Chairman Jerome Powell’s concepts, expressed in the aftermath of the latest monetary policy. The main idea is that interest rates will remain at current levels until officials are more certain inflation will stabilize around their 2% goal.

In the meantime, solid US employment-related data took out pressure from policymakers. The country reported that weekly unemployment claims rose to 218K in the week finished February 2, beating the 220K expected.

The macroeconomic calendar will remain scarce in Asia on Friday, with only a speech from the Reserve Bank of Australia (RBA) Governor Michele Bullock in the docket.

NZD/USD Technical Outlook

The NZD/USD pair held within familiar levels, maintaining a technically neutral stance. The daily chart shows sellers are aligned around a bearish 20 Simple Moving Average (SMA), while intraday buying interest surged around a flat 200 SMA, the latter at around 0.6080.

The same chart shows technical indicators have lost momentum within negative levels, lacking enough directional strength to anticipate a new leg south.

The case for another leg lower should be stronger on a break through the daily low, at 0.6078. Speculative interest will then look to test buyers´ determination at 0.6028, the February monthly low.

Alternating risk appetite trends dominated the sentiment in the FX universe amidst steady speculation of a Fed rate cut in May, rising geopolitical concerns, and some remarks hinting at the idea that the ECB is in no rush to start cutting rates.

Here is what you need to know on Friday, February 9:

The greenback regained some poise and encouraged the USD Index (DXY) to stay afloat above the 104.00 mark amidst further repricing of an interest rate cut by the Fed in May. On Friday, Dallas Fed L. Logan will be the only spot on the US docket.

EUR/USD advanced marginally and managed to keep the trade in the upper end of the weekly range in the 1.0770/80 band. In the domestic calendar, the final Inflation Rate in Germany will be in the spotlight on Friday.

GBP/USD reversed its two-day advance and retreated modestly on Thursday, although it managed well to maintain the region above 1.2600 the figure.

Dovish comments from BoJ’s Uchida weighed heavily on the Japanese yen and boosted USD/JPY to new yearly highs north of the 149.00 barrier, amidst humble gains in the US Dollar and higher yields.

AUD/USD added to Wednesday’s losses and dropped markedly to the sub-0.6500 zone, as further deflationary forces in China, negative price action in the commodity complex, and the somewhat stronger dollar were all too much for the Aussie Dollar.

In China, the flash Q4 Current Account will be in the pipeline on Friday. In the meantime, USD/CNH extended the weekly bounce and flirted with the 7.2200 zone.

Unabated geopolitical concerns and the positive weekly report from the EIA sustained the intense march north in prices of the WTI past the $76.00 mark per barrel.

Gold prices declined modestly to the $2030 region per troy ounce, while Silver prices rebounded sharply to three-day highs around $22.60 per ounce.

- The GBP/USD currently trades at 1.2615, recording mild losses.

- Broad-spectrum technical indicators reveal a bullish hold for larger time-frames but the short term is somewhat negative.

- The USD is getting traction thanks to positive labor market figures and markets pushing the Fed’s easing cycle to May.

On Thursday, the GBP/USD pair declined towards the 1.2615 level showing slight losses with upbeat US labor market figures benefiting the Greenback with Jobless claims from the week ending on February 3 coming in lower than expected. However, the Bank of England (BoE) holds a somewhat similar stance as the Federal Reserve (Fed) in delaying rate cuts so the losses may be limited.

Moreover, markets are predicting 100 bps rate cuts over the next 12 months, starting in June while investors are seeing higher 125 bps of easing in 2024 from the Fed indicating that the losses from the Pound may be limited. However, it will all come down to the incoming data as they will shape the expectations of the next decisions. Next in line, next Tuesday, the US will release January’s inflation figures while the UK will reveal key labor market figures which may likely set the pace for the pair for the next sessions.

GBP/USD daily chart

The indicators on the daily chart reflect a somewhat bearish bias for the short term. The Relative Strength Index (RSI) is on a downward slope and in negative territory. This gives clear evidence that market sentiment is favoring the sellers. Concurrently, the Moving Average Convergence Divergence (MACD) is throwing out red bars, indicating the selling pressure is not diminishing. That being said, on the broader market outlook, the pair is below the 20-day Simple Moving Averages (SMAs), but above the 200 and 100-day SMA. This suggests that the overall uptrend prevails, despite the recent downward movements, but as long as the buyers fail to reconquer the 20-day average, more downside may be on the horizon.

GBP/USD daily chart

- The DXY stabilized at 104.15 on Thursday after reaching a daily high of 104.40.

- Weekly Jobless Claims came in higher than expected in the week ended in February 3.

- Markets digest Fed official Barkin's words.

The US Dollar (USD) steadily rose on Thursday, initially to 103.45 and then stabilizing at 104.15 on the back of positive Initial Jobless Claims figures. However, bulls seem to be running out of steam due to a lack of fresh drivers, while Federal Reserve (Fed) speakers refuse to give additional guidance on the bank’s next steps.

The US Federal Reserve's Chair, Jerome Powell, commented that he considered a cut in March “unlikely”, adding that the bank needs more evidence on inflation coming down to gain confidence for cutting rates. Several officials were on the wires this week but didn’t give new guidance, basically confirming that the Fed awaits more data and disregards cuts in March.

Daily digest market movers: US Dollar gains some ground on positive Jobless Claims

- Initial Jobless Claims for the week ended on February 3 fell short of the consensus. The US Department of Labor reported that the claims came in at 218K, lower than the predicted 220K and a slight reduction from the previous week's 227K claims.

- According to the CME FedWatch Tool, the possibility of rate cuts in March dropped to 20%. Those odds rise to 50% for the May meeting, where the probability of a hold is also high.

- An ascent in US Treasury bond yields also supports the US Dollar. The 2-year yield is at 4.45%, the 5-year yield is at 4.11%, and the 10-year yield is at 4.16%.

Technical analysis: DXY fails to regain the 100-day SMA, bulls still present

The daily Relative Strength Index (RSI) shows a flat slope, albeit in positive territory, hinting at a gradual slowdown in buying momentum. However, it is too soon to anticipate a bearish reversal as positive territory generally denotes a bullish bias.

The Moving Average Convergence Divergence (MACD) presents flat green bars, illustrating a slowdown in bullish momentum but without a bearish crossover. The MACD indicates that buying pressure is still present, albeit reduced.

Regarding the Simple Moving Averages (SMAs), the index is anchored above the 20-day and 200-day SMAs, signaling a bullish bias in the longer framework, yet it is trading below the 100-day SMA, demonstrating some bearish pressure in the intermediate term. In conclusion, the short-term technical outlook seems to be tilted in favor of the bulls, albeit with weakening momentum.

US Dollar FAQs

What is the US Dollar?

The US Dollar (USD) is the official currency of the United States of America, and the ‘de facto’ currency of a significant number of other countries where it is found in circulation alongside local notes. It is the most heavily traded currency in the world, accounting for over 88% of all global foreign exchange turnover, or an average of $6.6 trillion in transactions per day, according to data from 2022.

Following the second world war, the USD took over from the British Pound as the world’s reserve currency. For most of its history, the US Dollar was backed by Gold, until the Bretton Woods Agreement in 1971 when the Gold Standard went away.

How do the decisions of the Federal Reserve impact the US Dollar?

The most important single factor impacting on the value of the US Dollar is monetary policy, which is shaped by the Federal Reserve (Fed). The Fed has two mandates: to achieve price stability (control inflation) and foster full employment. Its primary tool to achieve these two goals is by adjusting interest rates.

When prices are rising too quickly and inflation is above the Fed’s 2% target, the Fed will raise rates, which helps the USD value. When inflation falls below 2% or the Unemployment Rate is too high, the Fed may lower interest rates, which weighs on the Greenback.

What is Quantitative Easing and how does it influence the US Dollar?

In extreme situations, the Federal Reserve can also print more Dollars and enact quantitative easing (QE). QE is the process by which the Fed substantially increases the flow of credit in a stuck financial system.

It is a non-standard policy measure used when credit has dried up because banks will not lend to each other (out of the fear of counterparty default). It is a last resort when simply lowering interest rates is unlikely to achieve the necessary result. It was the Fed’s weapon of choice to combat the credit crunch that occurred during the Great Financial Crisis in 2008. It involves the Fed printing more Dollars and using them to buy US government bonds predominantly from financial institutions. QE usually leads to a weaker US Dollar.

What is Quantitative Tightening and how does it influence the US Dollar?

Quantitative tightening (QT) is the reverse process whereby the Federal Reserve stops buying bonds from financial institutions and does not reinvest the principal from the bonds it holds maturing in new purchases. It is usually positive for the US Dollar.

- BoJ Deputy Shinichi Uchida cooled hopes for an upcoming tightening cycle in Japan.

- The Nikkei 225 posted its highest close since February 1990, adding roughly 750 points.

- USD/JPY on its way to test the 150.00 level, according to the daily chart.

The US Dollar struggles for direction on Thursday, but not against its Japanese rival. The USD/JPY pair trades in the 149.30 region, its highest since last November. Dovish comments from Bank of Japan (BoJ) Deputy Governor Shinichi Uchida, stating policy tightening would be gradual and that a rate adjustment would not necessarily trigger a tightening cycle, weighed on the Japanese Yen.

Such comments underpinned local equities. The Nikkei 225 added roughly 750 points or 2% on the day, outperforming its Asian counterparts. The index closed the day at 36,863.28, the highest close since February 1990.

Meanwhile, higher United States (US) government bond yields gave USD/JPY an additional boost. Solid US employment figures pushed the 10-year Treasury yield to a fresh weekly high of 4.16%, as Initial Jobless Claims further blurred the odds for a Federal Reserve’s (Fed) rate cut.

USD/JPY Technical Outlook

The USD/JPY pair trades a handful of pips below its intraday high, paring its run amid the poor performance of Wall Street, reflecting a souring mood. Still, the pair retains substantial gains and has room to test the 150.00 mark in the upcoming sessions.

The USD/JPY pair trades a handful of pips below its intraday high, paring its run amid the poor performance of Wall Street, reflecting a souring mood. Still, the pair retains substantial gains and has room to test the 150.00 mark in the upcoming sessions.

In the daily chart, the pair bottomed around a directionless 100 Simple Moving Average (SMA) for the week, providing dynamic support at around 147.50. The initial bounce turned into a firmer rally, and the 20 SMA is currently crossing the mentioned 100 SMA, reinforcing the support area. As long as above it, bulls will likely retain control.

Finally, the Momentum indicator recovered from around its 100 level, while the Relative Strength Index (RSI) indicator accelerated north and approaches overbought readings, both reflecting strong buying interest.

- AUD/USD resumed the decline and retreats below 0.6500.

- The recovery in the greenback put the AUD under pressure.

- Inflation Rate in China surprised to the downside.

The Australian dollar came under renewed selling pressure amidst the solid performance in the Greenback on Thursday.

Indeed, the greenback set aside two daily declines in a row and reclaimed the area north of 104.00 the figure when gauged by the USD Index (DXY). This rebound occurred amid steady investor speculation about a potential interest rate cut by the Federal Reserve (Fed) in either May or June.

Turning to domestic factors, the AUD’s weakness remained propped up by the generalized bearish trend in the commodity complex, where copper prices and iron ore extended further their retracements.

Also weighing on the Aussie Dollar emerged another lower-than-expected inflation figures in China in the first month of the year.

In the meantime, market participants continued to evaluate the Reserve Bank of Australia's (RBA) latest interest rate decision, which kept rates unchanged at 4.35% while delivering a hawkish message that left a potential future rate hike in the pipeline for the time being.

Still around the RBA and its Statement on Monetary Policy (SoMP), the bank slightly lowered its inflation forecasts, anticipating both metrics to remain below 3% by the fourth quarter of 2025. Additionally, the RBA revised down its GDP growth projections, reflecting a less optimistic outlook for consumer spending and housing investments in the near term.

Governor Bullock's departure from the expected move towards a dovish stance further tempered the pair's upward potential. She emphasized the incomplete nature of addressing inflation and highlighted the current inflation rate as unacceptably high.

AUD/USD daily chart

AUD/USD short-term technical outlook

Further losses in the AUD/USD should pass its 2024 level of 0.6468 (February 5), setting up a potential test of the 2023 low of 0.6270 (Oct 26). The breach of the latter may result in a move to the round level of 0.6200 before the 2022 low of 0.6169 (October 13).

On the upside, the key 200-day SMA at 0.6571 is ahead of the intermediate 55-day SMA at 0.6642. The breakout of this zone may push the pair to attempt the December 2023 top of 0.6871 (December 28), followed by the July 2023 peak of 0.6894 (July 14) and the June 2023 high of 0.6899 (June 16), all right before the key 0.7000 threshold.

The 4-hour chart turned bearish, paving the way for a dip to 0.6452 once 0.6468 is cleared. On the bullish side, 0.6610 is an immediate hurdle ahead of the 200-SMA at 0.6650. The surpassing of this zone indicates a possible progress to 0.6728. The MACD remains well in the negative zone, and the RSI deflated to the 36 zone.

View Live Chart for the AUD/USD

Richmond Fed Thomas Barkin spoke at the Economic Club of New York on Thursday:

In aggregate, past rate hikes are still working their way into the economy.

It's hard to determine the appropriate course of action for rates based solely on economic models.

I would like to see a broader range of factors contributing to lower inflation.

Specifically, I would like to see rents and service prices cooling down further.

The decision to cut rates will depend on the extent to which inflation is being mitigated.

We will gain valuable insights into inflation trends over the next six months.

If inflation returns to 2% alongside strong demand, it would indicate a higher neutral rate.

The January jobs data indicates an incredibly vibrant job market. However, while the job market is tight, it may not be as tight as the data suggests."

- EUR/USD found little support from ECB Economic Bulletin.

- US Initial Jobless Claims provided little spark for markets.

- Euro traders look to Friday’s Germany HICP inflation.

EUR/USD tested into a near-term low of 1.0741 on Thursday as the latest Economic Bulletin from the European Central Bank (ECB) provided little new information for investors looking for guidance on when to expect rate cuts. The ECB continues to grapple with a lopsided European economy. Euro area price pressures remain higher than the ECB would like to see despite an ongoing softening in broad economic figures and faltering growth for the European economy.

US Initial Jobless Claims came in slightly better than expected, but a mid-tier data schedule for the US this week is keeping broad-market risk appetite hanging relatively in the middle.

Daily Digest Market Movers: EUR/USD remains caught in near-term cycle

- ECB’s Economic Bulletin reveals little new, peels back the layers on hampered ECB.

- Inflation continues to decline.

- Rates will remain sufficiently restrictive.

- Inflation is expected to keep easing through 2024.

- Economic risks remain tilted to the downside.

- Elevated wage growth, declining labor productivity keeps price pressure high.

- US Initial Jobless Claims printed at 218K for the week ended February 2, markets expected 220K.

- Four-week average Initial Jobless Claims ticked higher to 212.25K from 208.5K (revised up from 207.75K).

- Richmond Federal Reserve (Fed) President Thomas Barkin on Thursday:

- Fed Chairman Jerome Powell speaks for the Federal Open Market Committee, will not undercut or explain the Chairman’s statements.

- Fed remains focused on inflation and unemployment, not US government debt.

- An economic downturn would be a case for a rate cut.

- The Fed has plenty of time to remain patient on rate changes.

- Fed is in no rush to cut rates.

- Barkin won’t take too much signal from single-month data.

- Remains cautious regarding the accuracy of economic numbers at the start of the year, but data remains remarkable.

- Friday’s YoY German Harmonized Index of Consumer Prices (HICP) inflation report is expected to hold steady at 3.1% for January, with the MoM figure likewise forecast to hold steady at -0.2%.

Euro price today

The table below shows the percentage change of Euro (EUR) against listed major currencies today. Euro was the strongest against the Japanese Yen.

| USD | EUR | GBP | CAD | AUD | JPY | NZD | CHF | |

| USD | 0.03% | 0.09% | 0.01% | 0.49% | 0.82% | 0.29% | -0.05% | |

| EUR | -0.03% | 0.06% | 0.00% | 0.47% | 0.79% | 0.26% | -0.09% | |

| GBP | -0.09% | -0.05% | -0.06% | 0.41% | 0.74% | 0.20% | -0.16% | |

| CAD | -0.02% | 0.01% | 0.06% | 0.47% | 0.80% | 0.27% | -0.09% | |

| AUD | -0.50% | -0.47% | -0.41% | -0.47% | 0.33% | -0.20% | -0.57% | |

| JPY | -0.83% | -0.81% | -0.75% | -0.81% | -0.33% | -0.54% | -0.89% | |

| NZD | -0.29% | -0.26% | -0.20% | -0.27% | 0.21% | 0.53% | -0.36% | |

| CHF | 0.07% | 0.09% | 0.15% | 0.09% | 0.57% | 0.88% | 0.36% |

The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the Euro from the left column and move along the horizontal line to the Japanese Yen, the percentage change displayed in the box will represent EUR (base)/JPY (quote).

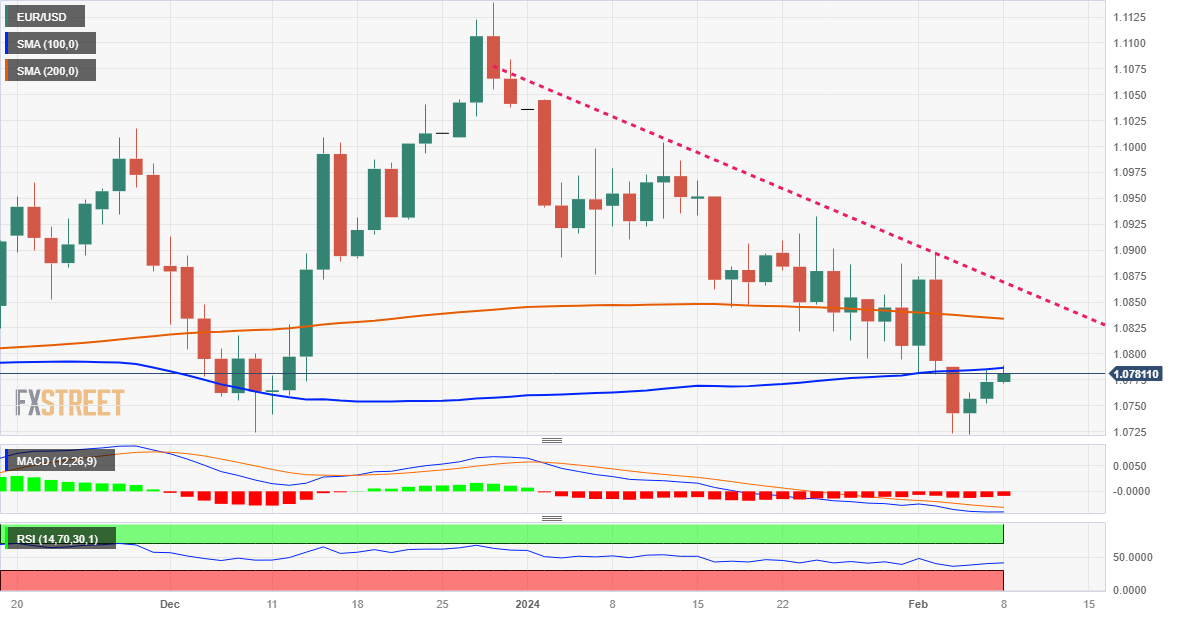

Technical analysis: EUR/USD cycles on Thursday as pair remains mired in low-side technical trap

EUR/USD dipped on Thursday, falling toward 1.0740 before seeing a brief pullback in the US market session, but the pair remains hamstrung below the 200-hour Simple Moving Average (SMA) at 1.0800.

Daily candlesticks have EUR/USD stuck on a near-term technical support level from 1.0750, and bidders will be tempted to drive the pair back into the bullish side of the 200-day SMA at 1.0835. The EUR/USD remains down over 3% from December’s peak bids at 1.1140.

EUR/USD hourly chart

EUR/USD daily chart

Euro FAQs

What is the Euro?

The Euro is the currency for the 20 European Union countries that belong to the Eurozone. It is the second most heavily traded currency in the world behind the US Dollar. In 2022, it accounted for 31% of all foreign exchange transactions, with an average daily turnover of over $2.2 trillion a day.

EUR/USD is the most heavily traded currency pair in the world, accounting for an estimated 30% off all transactions, followed by EUR/JPY (4%), EUR/GBP (3%) and EUR/AUD (2%).

What is the ECB and how does it impact the Euro?

The European Central Bank (ECB) in Frankfurt, Germany, is the reserve bank for the Eurozone. The ECB sets interest rates and manages monetary policy.

The ECB’s primary mandate is to maintain price stability, which means either controlling inflation or stimulating growth. Its primary tool is the raising or lowering of interest rates. Relatively high interest rates – or the expectation of higher rates – will usually benefit the Euro and vice versa.

The ECB Governing Council makes monetary policy decisions at meetings held eight times a year. Decisions are made by heads of the Eurozone national banks and six permanent members, including the President of the ECB, Christine Lagarde.

How does inflation data impact the value of the Euro?

Eurozone inflation data, measured by the Harmonized Index of Consumer Prices (HICP), is an important econometric for the Euro. If inflation rises more than expected, especially if above the ECB’s 2% target, it obliges the ECB to raise interest rates to bring it back under control.

Relatively high interest rates compared to its counterparts will usually benefit the Euro, as it makes the region more attractive as a place for global investors to park their money.

How does economic data influence the value of the Euro?

Data releases gauge the health of the economy and can impact on the Euro. Indicators such as GDP, Manufacturing and Services PMIs, employment, and consumer sentiment surveys can all influence the direction of the single currency.

A strong economy is good for the Euro. Not only does it attract more foreign investment but it may encourage the ECB to put up interest rates, which will directly strengthen the Euro. Otherwise, if economic data is weak, the Euro is likely to fall.

Economic data for the four largest economies in the euro area (Germany, France, Italy and Spain) are especially significant, as they account for 75% of the Eurozone’s economy.

How does the Trade Balance impact the Euro?

Another significant data release for the Euro is the Trade Balance. This indicator measures the difference between what a country earns from its exports and what it spends on imports over a given period.

If a country produces highly sought after exports then its currency will gain in value purely from the extra demand created from foreign buyers seeking to purchase these goods. Therefore, a positive net Trade Balance strengthens a currency and vice versa for a negative balance.

- Canadian Dollar is broadly higher in calm markets.

- Canada Unemployment, Average Hourly Wages due on Friday.

- Canadian Dollar in tight race with recovering US Dollar.

The Canadian Dollar (CAD) has stepped broadly higher against the majority of its major currency peers on Thursday, though the CAD is battling a recovering US Dollar (USD) as the two currencies are on pace to settle the day as the top performers. US Initial Jobless Claims came in lower than expected, driving investors back into the Greenback as the US economy continues to outperform.

Canada sees a clear economic docket on Thursday as investors gear up for Friday’s Canadian labor and wages figures. Markets are forecasting a slight uptick in the Canadian January Unemployment Rate, as well as a smaller-than-usual Net Change in Employment for January, though the number is still projected to be positive.

Daily digest market movers: Canadian Dollar fighting for second place on Thursday

- US Initial Jobless claims beat expectations, coming in at 218K for the week ended February 2 compared to the forecast of 220K.

- The previous week’s Initial Jobless Claims saw an upside revision from 224K to 227K.

- The 4-week average for US Initial Jobless Claims climbed to 212.25K from 208.5K (revised up from 207.75K).

- President of the Federal Reserve (Fed) Bank of Richmond, Thomas Barkin, noted on Thursday that Fed Chairman Jerome Powell speaks for the Federal Open Market Committee (FOMC).

- Fed’s Barkin won’t prejudice the outcome of the March FOMC meeting, deferring to Fed head Powell’s statements.

- More Barkin:

- The Fed is focused on inflation and unemployment, not US government debt.

- If the US economy takes a turn for the worse, that would be a rate cut scenario.

- The Fed has time to be patient on rate cuts.

- Economic data remains remarkable, but Barkin is cautious regarding accuracy.

- It’s entirely possible that the neutral rate has risen.

- Need to see good inflation numbers being sustained and broadening.

- Canada’s Friday Unemployment Rate for January is forecast to tick upward to 5.9% from December’s 5.8%.

- Net Change in Employment forecast to add 15K net job gains through January, a thin number but still positive.

- Canadian annualized Average Hourly Wages in January will also print on Friday, last annualized wage growth figure showed YoY hourly wage gains of 5.7%.

Canadian Dollar price today

The table below shows the percentage change of Canadian Dollar (CAD) against listed major currencies today. Canadian Dollar was the strongest against the Japanese Yen.

| USD | EUR | GBP | CAD | AUD | JPY | NZD | CHF | |

| USD | 0.12% | 0.15% | 0.00% | 0.55% | 0.91% | 0.38% | 0.05% | |

| EUR | -0.12% | 0.03% | -0.11% | 0.43% | 0.78% | 0.26% | -0.09% | |

| GBP | -0.15% | -0.03% | -0.14% | 0.40% | 0.76% | 0.23% | -0.12% | |

| CAD | -0.01% | 0.10% | 0.14% | 0.54% | 0.89% | 0.37% | -0.02% | |

| AUD | -0.56% | -0.44% | -0.41% | -0.54% | 0.36% | -0.17% | -0.53% | |

| JPY | -0.90% | -0.81% | -0.76% | -0.91% | -0.38% | -0.52% | -0.87% | |

| NZD | -0.37% | -0.27% | -0.24% | -0.37% | 0.18% | 0.53% | -0.36% | |

| CHF | -0.03% | 0.09% | 0.10% | -0.02% | 0.53% | 0.87% | 0.35% |

The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the Euro from the left column and move along the horizontal line to the Japanese Yen, the percentage change displayed in the box will represent EUR (base)/JPY (quote).

Technical analysis: Canadian Dollar rebounds against US Dollar on Thursday

The Canadian Dollar is broadly higher on Thursday, gaining nine-tenths of a percent against the Japanese Yen (JPY) and over half a percent against the Australian Dollar (AUD). On the low end, the CAD is mostly flat against the US Dollar after recovering from an early dip, and it is up a scant tenth of a percent against the Euro (EUR).

The USD/CAD saw a sharp turnaround just below 1.3500 on Thursday as investors aren’t ready to push the pair back over the key price handle. The pair is currently finding technical support from the 200-hour Simple Moving Average (SMA) near 1.3450, and an extended breakdown puts the USD/CAD on the road to re-challenging early February’s swing lows into 1.3370.

Daily candles remain caught in the midrange of a consolidation zone between the 50-day and 200-day SMAs at 1.3423 and 1.3476, respectively, but the USD/CAD is still up over 2% from December’s bottom bids of 1.3177.

USD/CAD hourly chart

USD/CAD daily chart

Canadian Dollar FAQs

What key factors drive the Canadian Dollar?

The key factors driving the Canadian Dollar (CAD) are the level of interest rates set by the Bank of Canada (BoC), the price of Oil, Canada’s largest export, the health of its economy, inflation and the Trade Balance, which is the difference between the value of Canada’s exports versus its imports. Other factors include market sentiment – whether investors are taking on more risky assets (risk-on) or seeking safe-havens (risk-off) – with risk-on being CAD-positive. As its largest trading partner, the health of the US economy is also a key factor influencing the Canadian Dollar.

How do the decisions of the Bank of Canada impact the Canadian Dollar?

The Bank of Canada (BoC) has a significant influence on the Canadian Dollar by setting the level of interest rates that banks can lend to one another. This influences the level of interest rates for everyone. The main goal of the BoC is to maintain inflation at 1-3% by adjusting interest rates up or down. Relatively higher interest rates tend to be positive for the CAD. The Bank of Canada can also use quantitative easing and tightening to influence credit conditions, with the former CAD-negative and the latter CAD-positive.

How does the price of Oil impact the Canadian Dollar?

The price of Oil is a key factor impacting the value of the Canadian Dollar. Petroleum is Canada’s biggest export, so Oil price tends to have an immediate impact on the CAD value. Generally, if Oil price rises CAD also goes up, as aggregate demand for the currency increases. The opposite is the case if the price of Oil falls. Higher Oil prices also tend to result in a greater likelihood of a positive Trade Balance, which is also supportive of the CAD.

How does inflation data impact the value of the Canadian Dollar?

While inflation had always traditionally been thought of as a negative factor for a currency since it lowers the value of money, the opposite has actually been the case in modern times with the relaxation of cross-border capital controls. Higher inflation tends to lead central banks to put up interest rates which attracts more capital inflows from global investors seeking a lucrative place to keep their money. This increases demand for the local currency, which in Canada’s case is the Canadian Dollar.

How does economic data influence the value of the Canadian Dollar?

Macroeconomic data releases gauge the health of the economy and can have an impact on the Canadian Dollar. Indicators such as GDP, Manufacturing and Services PMIs, employment, and consumer sentiment surveys can all influence the direction of the CAD. A strong economy is good for the Canadian Dollar. Not only does it attract more foreign investment but it may encourage the Bank of Canada to put up interest rates, leading to a stronger currency. If economic data is weak, however, the CAD is likely to fall.

- The EUR/GBP currently trades at 0.8540, recording a 0.10% on Thursday.

- Monetary policy divergences between the BoE and ECB will eventually benefit the GBP.

- Markets are leaning toward a rate cut by the ECB in April while the BoE is seen starting in June.

In Thursday's session, the EUR/GBP pair is seen at 0.8540, posting modest gains. The pair is receiving pressure from a dovish stance by the European Central Bank (ECB), tipping rate cut odds for April. Meanwhile, GBP maintains its undercurrent due to the Bank of England (BoE) monetary policy which seems to be pushing the easing cycle to June.

Adding to that, markets currently price in about 65% odds for rate cuts to commence in April, predicting 125 bp worth of easing this year, despite ongoing resistance from ECB officials. On the other hand, for the BoE, investors anticipate about 100 bp of rate cuts in the next 12 months, beginning in June due to the recent economic figures which suggest that the British economy remains resilient. Moreover, as long as the UK's economy continues to show strength and markets delay the BoE's interest rate cuts, the cross may see further downside.

EUR/GBP technical analysis

The daily chart indicators indicate a possible dominance of buying momentum. The Relative Strength Index (RSI) is on a positive slope but in negative territory, revealing an increasing strength of the buying force. Concurrently, the Moving Average Convergence Divergence (MACD) shows rising green bars, suggesting that the bullish sentiment is taking hold. However, it's crucial to note that the pair is currently trading under the 20, 100, and 200-day Simple Moving Averages (SMAs), pointing towards the prevailing strength of the bears in a broader perspective. This situation proposes a challenging scenario for the buyers, despite the recent signs of a bullish recovery.

EUR/GBP daily chart

-638430060156548811.png)

Canada’s employment data for January will be reported by Statistics Canada on Friday, February 9 at 13:30 GMT and as we get closer to the release time, here are forecasts from economists and researchers at five major banks regarding the upcoming jobs figures.

The North American economy is expected to have added 15K vs. 0.1K in December, while the unemployment rate is expected to rise a tick to 5.9%.

TDS

We look for employment to rise by 30K in January, slightly above the recent trend, although this will not be enough to keep the UE rate from rising 0.1pp to 5.9%. This reflects a recent pickup in hiring intentions while stronger growth momentum into year-end will also provide a tailwind to job growth, although we see limited scope for softer wage growth (0.1pp to 5.6%).

NBF

Job creation may have remained tepid in January (+10K), reflecting an economy operating below its potential. This modest gain, combined with another significant expansion of the labour force and an unchanged participation rate (65.5%), should translate into a two-tenth increase in the unemployment rate, to 6.0%.

RBC Economics

We expect Canada’s unemployment rate likely hit 5.9% in January – up almost a full percentage point from 5% a year earlier. That’s the highest rate since the pandemic – January 2022. We expect to see another 10K jobs added from December, but that’s not fast enough to keep up with the country’s record pace of population growth.

Citi

After essentially zero job growth in December, we expect employment to rise by a solid 40K jobs to start the year in January. This would be stronger than the trend over the last few months and stronger than a typical pre-pandemic pace around ~25K/month. But with substantially stronger population growth and an expectation that the labor force participation rate will rebound to 65.6% after falling in December, a 40K increase in employment would still imply the unemployment rate rises to 5.9%. Wages will be one of the most important factors to watch. After a large jump to 5.7% YoY in December, we expect average hourly wages to fall to 5.3% YoY in January.

CIBC

Canada’s labour market likely weakened in January, with a modest 10K gain in jobs leading the unemployment rate to tick up to 5.9%. That would reflect a deterioration in domestic demand, with consumers becoming more cautious with spending as mortgages renew, and the rise in business insolvencies portending layoffs in some sectors. Hours worked could have picked up, but that will likely be a one-time impact owing to the end of public sector strikes in Quebec. With a strong year-ago monthly wage growth figure falling out of the annual calculation, wage growth for permanent employees could have subsided by a few ticks, but that would still leave it above 5.0% YoY.

The S&P 500 came close to rising above 5,000 for the first time on Wednesday. Economists at UBS see the potential for further gains.

Potential for a period of continued stronger growth, tame inflation, and swifter monetary easing

Our base case remains for a soft landing for the US economy, with the S&P 500 ending the year around current levels. However, recent economic data have highlighted the potential for a period of continued stronger growth, tame inflation, and swifter monetary easing. In this event, we believe the S&P 500 has the potential to rise to around 5,300 this year.

We believe this would be a particularly positive outcome for small-cap stocks, which benefit more from Fed easing given their greater reliance on floating-rate debt.

Economists at ANZ Bank expect the USD/JPY exchange rate to trade at 136.00 by the end of 2024.

Shifts in anticipation of a Fed rate cut in the first half of 2024 could slightly tilt USD/JPY downward within the range

Current dynamics, including higher US Treasury yields and the Fed's stance against early rate cuts, are expected to keep USD/JPY within a narrow range in the near term. We anticipate limited near-term recovery for the JPY against the USD, with the currency pair expected to remain rangebound between 146 and 148.50.

Market speculation about a potential Fed rate cut in early 2024 could influence USD/JPY, potentially pushing it slightly lower within the established range.

The March and April BoJ policy meetings are anticipated to induce significant volatility in JPY crosses, with the market closely watching for signals on ending negative rates and easing policies.

We project the USD/JPY pair to reach 136.00 by the end of the year.

Gold’s prospects in Q1 are losing some shine as expectations for a near-term Fed rate cut have ebbed, economists at MUFG Bank say.

Phase of range-bound to extend

Gold extends decline as rate-cut bets fade. While this development is likely to extend the current phase of range-bound Gold prices, with short-term moves tied to data potentially influencing Fed decision-making, we believe downside to the price will be limited by robust support from the other two channels, namely, supportive central bank demand and bullion’s role as the geopolitical hedge of last resort .

Gold is our most bullish call this year. Bullion is set to hit record levels on a trifecta of Fed cuts, supportive central bank demand and bullion’s role as the geopolitical hedge of last resort.

Bank of England (BoE) policymaker Catherine Mann, who voted in favor of a rate hike in the last policy meeting, said on Thursday that she is not convinced that the near-term declaration in headline inflation will continue, per Reuters.

Mann noted that she is worried that a Red Sea price shock could be incorporated into corporate pricing swiftly and argued that financial conditions in the UK eased "too much."

Market reaction

These comments failed to trigger a noticeable reaction in GBP/USD. As of writing, the pair was down 0.25% on the day at 1.2593.

The FX market’s sensitivity to central bank policy continues to amaze Kit Juckes, Chief Global FX Strategist at Société Générale.

Dollar could be in for 2-3% more upside from here

If the market embraces the idea that the Fed’s projection of three cuts this year is what’s going to happen, then the Dollar’s in for 2-3% more upside from here, and EUR/USD could test 1.0500 at some point.

In practise, of course, there are two sides to the argument and the ECB’s pushing back at rate cut expectations every bit as hard as the Fed is. So too, are most central bank policymakers, except for the BoJ, whose Deputy Governor is stressing that an end to YCC and negative rates would not signal the start of a series of policy moves.

I doubt the end of YCC and negative rates can be achieved without some upward pressure on the Yen, but clearly, the move from USD/JPY 152.00 to 127.00 in late 2022/early 2023 has left scars.

Banxico meets to set interest rates today. The Mexican Peso (MXN) has been one of the very few currencies to appreciate against the dollar on a total return basis this year. Economists at ING analyze MXN outlook ahead of the decision.

Strong demand to emerge for the Peso on any dips

We think the Peso would not sell off too aggressively if Banxico did surprise and cut its 11.25% policy rate today. For reference, four of thirty economists polled by Bloomberg are looking for a cut.

And even if rates were cut, we think 10%+ implied yields, backed by supportive fiscal policy in an election year, should see strong demand emerge for the Peso on any dips.

We think USD/MXN will be trading in the 16.50-17.00 area later this year when the Dollar trend turns broadly lower.

USD/CAD has settled in the mid/upper 1.3400s. Economists at the Bank of Montreal analyze the pair’s outlook.

CAD is unlikely to take flight

The Canadian Dollar (CAD) remains boxed in a narrow, depressed range.

Given the country's poor economic and productivity performance, CAD is unlikely to take flight. However, assuming the trade-weighted Greenback continues to retreat from earlier record highs, the Loonie could strengthen modestly to 1.3200 by year-end.

See – USD/CAD: A final leg of Loonie weakness in the coming quarter – CIBC

The US Dollar Index (DXY) rebounds from the 104.00 area. Economists at Scotiabank analyze Greenback’s outlook.

DXY is showing some signs of short-term technical strength

The DXY is showing some signs of short-term technical strength, with the index basing around the 104.00 area on Wednesday; gains today may be setting the index up for a retest of the 104.55/104.60 peaks seen at the start of the week.

Markets may be giving the USD a bit of a lift ahead of Friday’s annual US CPI revisions – not usually a big issue for markets until last year’s surprising and quite significant upward revisions.

- AUD/USD slumps below 0.6500 on cautious market mood.

- The Australian Dollar weakens as upside risks to China’s deflation deepen.

- The outlook for the Aussie asset weakens after an H&S breakdown.

The AUD/USD pair falls sharply below the psychological support of 0.6500 in the early New York session. The Aussie asset faces a sharp sell-off as investors turn anxious amid an absence of potential economic triggers.

The US Dollar Index (DXY) delivers a sharp recovery after consolidating near 104.00 as Federal Reserve (Fed) policymakers avoid speculating over the timing of rate cuts. Policymakers said they need more evidence indicating that inflation will sustainably return to the 2% target.

As per the CME Fedwatch tool, a rate-cut decision in March is unlikely. For May, chances in favor of a 25-basis point (bp) are stable at 54%.

Meanwhile, the Australian Dollar weakens against the US Dollar as upside risks to deflation in the Chinese economy have prompted the need for more stimulus from the People’s Bank of China (PBoC).

Annual consumer prices were deflated at a robust pace of 0.8% against expectations of 0.5% and the prior reading of 0.3%. Producers at factory gates slash prices at factory gates significantly due to poor aggregate demand. Being a proxy to China’s economy, the appeal for the Australian Dollar weakens.

AUD/USD witnesses a steep fall after a breakdown of the Head and Shoulder chart pattern formed on a daily time frame. The necklines of the aforementioned chart pattern is plotted from December 7 low at 0.6525. A bear cross, represented by the 20 and 50-day Exponential Moving Averages (EMAs) at 0.6625, indicates more weakness ahead.

The 14-period Relative Strength Index (RSI) has shifted into the bearish range of 20.00-40.00, which indicates momentum has leaned towards the downside.

Selling pressure would accelerate if the Aussie asset will drop below February 6 low of 0.6478, which will expose the asset to October 11 high at 0.6445. A downside move below the latter would drag the asset towards the round-level support of 0.6400.

In an alternate scenario, a recovery move above January 25 low at 0.6566 would drive the asset toward the round-level resistance of 0.6600, followed by January 30 high at 0.6625.

AUD/USD daily chart

-638429973897761526.png)

Federal Reserve (Fed) Bank of Richmond President Thomas Barkin told Bloomberg on Thursday that economic data has been remarkable across the board but noted that he is cautious about the accuracy of numbers at the turn of the year.

Barkin added that they have time to be patient on rate changes and said that he needs to see good inflation numbers being sustained and broadening.

Market reaction

The US Dollar Index edged higher following these comments and was last seen rising 0.35% on the day at 104.40.

- Initial Jobless Claims rose by 218K from a week earlier.

- Continuing Jobless Claims surprised to the upside.

US citizens that applied for unemployment insurance benefits increased by 218K in the week ending February 3 according to the US Department of Labor (DoL) on Thursday. Once again, the prints surpassed consensus and follow a 227K gain in the previous week.

Further details of the publication revealed that the advance seasonally adjusted insured unemployment rate was 1.2% (from 1.3%) and the 4-week moving average stood at 212.25, a decrease of 3.750K from the previous week's revised average.

In addition, Continuing Claims decreased by 23K to 1.894M in the week ended January 27.

Market reaction

The US Dollar Index kept the weekly advance in place and flirts with yearly highs near 104.40 soon after the publication of weekly labour market data.

USD/JPY has surged above the 149.00 level. Economists at Rabobank analyze the pair’s outlook.

USD/JPY seen at 135.00 on a 12-month view

While the market is facing up to the reality that BoJ policy adjustment this year will likely be carefully paced, we view levels at USD/JPY 149.00 as overdone and look for the JPY to strengthen ahead of the March 19 policy meeting.

We view the chances of an April rate hike as strong and maintain a 12-month USD/JPY forecast of 135.00.

GBP/USD drops back to 1.2600. Economists at Scotiabank analyze the pair’s outlook.

Move higher has stalled in the short run

Sterling has struggled to exploit regaining 1.2600 – formerly strong support – this week.

Trend signals have retained a bearish undertone on the intraday and daily studies through the GBP’s mini-rebound this week, underscoring a soft undertone for the Pound after losing key support.

Short-term price signals do suggest the move higher has stalled in the short run. Weakness through 1.2600 may see losses extend back to the low/mid 1.2500s again.

Resistance is 1.2640/1.2650.

European Central Bank (ECB) policymaker Pierre Wunsch said on Thursday that they have some indications, not strong ones, that wage growth in the Euro area is softening, as reported by Reuters.

"There is value in waiting to get more comforting wage data," Wunsch added.

Market reaction to ECB commentary

These comments don't seem to be having a noticeable impact on the Euro's performance against its major rivals. At the time of press, EUR/USD was trading at 1.0756, losing 0.15% on a daily basis.

EUR/USD drifts back from the upper 1.0700s. Economists at Scotiabank analyze the pair’s outlook.

Support is 1.0720/1.0725

Grinding gains in the EUR/USD pair from the low 1.0700s appear to have stalled via a likely bearish ‘evening star’ signal on the intraday (6-hour) chart.

Trend momentum is flat and losses may be slow in developing from here but the EUR’s stall around 1.0790 coincides with a test of the 100-Day Moving Average (1.0787) which has effectively served as resistance this week.

Support is at 1.0720/1.0725.

- US stock index futures trade modestly lower on Thursday.

- S&P 500 set a new all-time high on Wednesday.

- Market participants continue to assess quarterly earnings reports.

S&P 500 futures fall 0.17%, Dow Jones futures are unchanged and Nasdaq futures are down 0.17% ahead of the opening bell on Thursday.

S&P 500 (SPX), Dow Jones (DJIA), and Nasdaq (IXIC) indexes closed on Wednesday with a 0.82% gain, a 0.40% increase, and a 0.95% rise, respectively.

What to know before stock market opens

- The Technology Sector was the best-performing S&P 500 major sector on Wednesday, with a daily gain of nearly 1.5%. The Real Estate Sector and the Consumer Staples Sector declined less than 0.1% as the only major sectors closing the day in negative territory.

- Emerson Electric Co.(EMR) was the top gainer in the S&P 500 on Wednesday, rising 10.4% to $104.11. V.F. Corp. (VFC) fell nearly 10% to $15.31 as the biggest decliner of the day.

- The data from the US showed that the goods and services deficit was $62.2 billion in December, up $0.3 billion from $61.9 billion in November.

- The Federal Reserve (Fed) reported late Wednesday that consumers added $1.56 billion in additional borrowing, far below the $16 billion forecast and declining steeply from the previous month's $23.75 billion.

- In an interview with CNBC on Wednesday, Minneapolis Fed President Neel Kashkari argued they can dial back the policy rate quite slowly if the labor market continues to be strong. "At the moment, two to three rate cuts this year seems appropriate," he added.

- Federal Reserve Board of Governor member Adriana Kugler noted on Wednesday that she is pleased with the great progress on inflation and added that she is optimistic that the progress will continue. "Some measures of financial conditions have eased but remain relatively tight and are consistent with continued progress on inflation,” Kugler elaborated.

- “The data point to continued disinflation, to labor markets coming into better balance, and to resilient consumer spending—three elements necessary for us to stick to the soft landing we remain optimistic to achieve,” Philadelphia Fed President Patrick Harker said on Tuesday.

Disney and PayPal reported earnings

- Walt Disney Co. (DIS) reported a quarterly revenue of $23.5 billion, slightly below the market projection of $23.6 billion, per Reuters. Disney's board of directors authorized a $3 billion share repurchase program for the current fiscal year, and declared a dividend of 45 cents a share. “Our strong performance this past quarter demonstrates we have turned the corner and entered a new era of growth for our company,” Disney CEO Bob Iger said in a statement.

- PayPal Holdings Inc. (PYPL) said revenue rose 8.7% to $8.03 billion from a year ago, surpassing the market forecast of $7.87 billion. Quarterly adjusted earnings were $1.48 per share for the quarter ended in December, and quarterly net income was $1.4 billion. "We're doing a lot of things to drive change internally and externally,” CEO Alex Chriss said in a post-earnings conference call, according to Reuters. “However, nothing happens overnight. It will take time for some of our initiatives to scale and move the needle," Chriss added.

- Alibaba Group Holdings Ltd. (BABA) reported Q3 adjusted net income of RMB 47,951 million and Q3 revenue of RMB 260,348 million before the opening bell on Wednesday. In its earnings report, the company said that the board of directors approved an increase of $25 billion to the share repurchase program. “Our top priority is to reignite the growth of our core businesses, e-commerce and cloud computing,” Alibaba said, per Reuters.

- Uber Technologies Inc. (UBER) announced Q4 net income of $1.4 billion and Q4 gross bookings of $37.6 billion. Net revenue for that period was $9.94 billion. "Uber's platform advantages and disciplined investment in new growth opportunities resulted in record engagement and accelerating Gross Bookings in Q4," Chief Financial Officer Prashanth Mahendra-Rajah said, per Reuters.

- Motorola Solutions Inc. (MSI), DexCom Inc. (DXCM), Take-Two Interactive Software, Inc. (TTWO) and Pinterest Inc. (PINS) are among the noteworthy companies that will release earnings reports after the closing bell on Thursday.

S&P and Nasdaq futures are presented by CME e-minis and Dow Jones futures are presented by CBOT e-mini.

S&P 500 FAQs

What is the S&P 500?

The S&P 500 is a widely followed stock price index which measures the performance of 500 publicly owned companies, and is seen as a broad measure of the US stock market. Each company’s influence on the computation of the index is weighted based on market capitalization. This is calculated by multiplying the number of publicly traded shares of the company by the share price. The S&P 500 index has achieved impressive returns – $1.00 invested in 1970 would have yielded a return of almost $192.00 in 2022. The average annual return since its inception in 1957 has been 11.9%.

How are companies chosen to be included in the S&P 500?

Companies are selected by committee, unlike some other indexes where they are included based on set rules. Still, they must meet certain eligibility criteria, the most important of which is market capitalization, which must be greater than or equal to $12.7 billion. Other criteria include liquidity, domicile, public float, sector, financial viability, length of time publicly traded, and representation of the industries in the economy of the United States. The nine largest companies in the index account for 27.8% of the market capitalization of the index.

How can I trade the S&P 500?

There are a number of ways to trade the S&P 500. Most retail brokers and spread betting platforms allow traders to use Contracts for Difference (CFD) to place bets on the direction of the price. In addition, that can buy into Index, Mutual and Exchange Traded Funds (ETF) that track the price of the S&P 500. The most liquid of the ETFs is State Street Corporation’s SPY. The Chicago Mercantile Exchange (CME) offers futures contracts in the index and the Chicago Board of Options (CMOE) offers options as well as ETFs, inverse ETFs and leveraged ETFs.

What factors drive the S&P 500?

Many different factors drive the S&P 500 but mainly it is the aggregate performance of the component companies revealed in their quarterly and annual company earnings reports. US and global macroeconomic data also contributes as it impacts on investor sentiment, which if positive drives gains. The level of interest rates, set by the Federal Reserve (Fed), also influences the S&P 500 as it affects the cost of credit, on which many corporations are heavily reliant. Therefore, inflation can be a major driver as well as other metrics which impact the Fed decisions.

- The US Dollar prints small gains against most major G20 peers.

- Traders are getting ready for the weekly US Jobless Claims.

- The US Dollar Index pops back above 104 in a very calm market for now.

The US Dollar (USD) is back in the green after a stalemate session on Wednesday. Initially hopes of a ceasefire breakthrough between Israel and Hamas made the safety-linked US Dollar retreat a touch. After Israel’s Prime Minister Benjamin Netanyahu came out late Wednesday evening with a statement rejecting the plan, however, the USD gained a bid. According to Netanyahu the complete destruction of Hamas would only take a few more months anyway.

On the economic front, traders are getting ready for the weekly US Jobless Claims. The Wholesale Inventories are due as well later this Thursday, though expect not much movement in the Greenback on the back of that.

Traders looking for a longer term trade or strategy, or analysts that want to better assess the longer term inflation risks might consider taking a look at the US crop report: The United States Department of Agriculture (USDA) releases every month the World Agricultural Supply and Demand Estimates report (WASDE) where insights are given on supply, demand, bad harvests on all sorts of crops, and thus on possible weak spots that might attribute to the food inflation basket.

Daily digest market movers: At a drift

- This Thursday Nevada and the Virgin Islands are up for Republican Caucus elections. Another landslide victory for former US President Donald Trump would almost guarantee him the nomination as Republican Presidential Candidate for the November elections.

- At 13:30 GMT the weekly US Jobless Claims are due to be released. Expectations are for a decline in the numbers after the strong upbeat US Jobs report from past Friday.

- Initial Jobless Claims are expected to head from 224,000 to 220,000.

- Continuing Jobless Claims are seen heading from 1,898 million to 1,878 million.

- Wholesale Inventories for December are expected to stay steady near 0.4%.

- At 16:30, a 4-week Note will be auctioned by the US Treasury Department.

- Richmond’s Federal Reserve President Thomas Barkin is due to speak at 17:05. A 30-year bond auction will take place around 18:00.

- Around 17:00, the United States Department of Agriculture (USDA) will release its monthly World Agricultural Supply and Demand Estimates report (WASDE).

- Equity markets are mixed this Thursday. Japanese indices have closed off this Thursday in the green with the Nikkeai up over 2%. Quite a different picture in China where the Hang Seng is down 1.3%. European equities are looking for direction while US equity futures are rather flat.

- The CME Group’s FedWatch Tool is now looking at the March 20th meeting. Expectations for a pause are 81.5%, while 18.5% for a rate cut.

- The benchmark 10-year US Treasury Note trades near 4.12%,and trades in the middle of this week’s range.

US Dollar Index Technical Analysis: Steady awaiting confirmation

The US Dollar Index (DXY) is slowly but surely advancing higher again with markets digesting the failed ceasefire plan that was put on the table by Hamas. The harsh rhetoric from Prime Minister Benjamin Netanyahu could mean some lingering US Dollar strength in the coming weeks. Meanwhile markets will be looking for next Republican state Caucus elections, which could lock in Trump as a favorite for November.

Should the US Dollar Index move higher again, first look for a test at the peak of Monday, near 104.60. That level needs to be broken and is more important than the 100-day SImple Moving Average snap at 104.30. Once broken above that Monday high, the road is open for a jump to 105.00 with 105.12 as key levels to keep an eye on.

The 100-day SMA (104.29) is clearly the unreliable boyfriend in the rally at the moment. A false break on Monday and no support provided on Tuesday from the moving average opens the door for a bit of a squeeze lower. The first ideal candidate for support is the 200-day SMA near 103.60. Should that give way, look for support from the 55-day SMA near 103.00 itself.

US Dollar FAQs

What is the US Dollar?

The US Dollar (USD) is the official currency of the United States of America, and the ‘de facto’ currency of a significant number of other countries where it is found in circulation alongside local notes. It is the most heavily traded currency in the world, accounting for over 88% of all global foreign exchange turnover, or an average of $6.6 trillion in transactions per day, according to data from 2022.

Following the second world war, the USD took over from the British Pound as the world’s reserve currency. For most of its history, the US Dollar was backed by Gold, until the Bretton Woods Agreement in 1971 when the Gold Standard went away.

How do the decisions of the Federal Reserve impact the US Dollar?

The most important single factor impacting on the value of the US Dollar is monetary policy, which is shaped by the Federal Reserve (Fed). The Fed has two mandates: to achieve price stability (control inflation) and foster full employment. Its primary tool to achieve these two goals is by adjusting interest rates.

When prices are rising too quickly and inflation is above the Fed’s 2% target, the Fed will raise rates, which helps the USD value. When inflation falls below 2% or the Unemployment Rate is too high, the Fed may lower interest rates, which weighs on the Greenback.

What is Quantitative Easing and how does it influence the US Dollar?

In extreme situations, the Federal Reserve can also print more Dollars and enact quantitative easing (QE). QE is the process by which the Fed substantially increases the flow of credit in a stuck financial system.

It is a non-standard policy measure used when credit has dried up because banks will not lend to each other (out of the fear of counterparty default). It is a last resort when simply lowering interest rates is unlikely to achieve the necessary result. It was the Fed’s weapon of choice to combat the credit crunch that occurred during the Great Financial Crisis in 2008. It involves the Fed printing more Dollars and using them to buy US government bonds predominantly from financial institutions. QE usually leads to a weaker US Dollar.

What is Quantitative Tightening and how does it influence the US Dollar?

Quantitative tightening (QT) is the reverse process whereby the Federal Reserve stops buying bonds from financial institutions and does not reinvest the principal from the bonds it holds maturing in new purchases. It is usually positive for the US Dollar.

Market repricing of a less aggressive global easing path has seen the US Dollar (USD) outperform in the G10 space so far this year. Economists at HSBC analyze Greenback’s outlook.

Geopolitical uncertainty might provide support to the USD in the weeks and months ahead

Geopolitical uncertainty might also provide support to the ‘safe-haven’ USD in the weeks and months ahead.

Over the medium term, we expect the USD to strengthen modestly against the EUR and GBP amid the US economy’s continued outperformance against the Eurozone and the UK.

The USD could also be supported by its ongoing yield advantage.

Bank of Mexico's monetary policy decision is due out today. Will the Banxico signal a turnaround? Economists at Commerzbank analyze how the Mexican Peso (MXN) could react to Banxico’s announcement.

Banxico is likely to take a wait-and-see approach

Banxico is likely to take a wait-and-see approach today. After all, it is unlikely that it would have delayed the first rate cut for all these months to bring inflation under control in the long term and then initiate a turnaround at a time when the overall rate is rising again. Even if this is not a general exclusion, I can't imagine that Banxico would want to do this. It would also put pressure on the Peso.

The more important question is whether it will hint at a first rate cut in March. After all, the real economy is now showing clear signs of the impact of high interest rates. Depending on whether there is more or less evidence today that rate cuts are imminent, the Peso could come under pressure.

But even if there are no hints, a first rate cut in March does not seem unlikely at the moment, given the developments in core inflation and the slowdown in economic growth. Unless, of course, inflation gets out of control again.

The Japanese Yen (JPY) has weakened resulting in USD/JPY surpassing the year-to-date high of 148.89 from 5th February. Economists at MUFG Bank analyze the pair’s outlook.

JPY to rebound heading into Q2

The BoJ is preparing market participants for an exit from negative rates but there was no urgency expressed to indicate that the first hike will be delivered in March. It remains consistent with our base case outlook for the first hike to be delivered in April, but we acknowledge that the risk of earlier exit in March has increased recently in light of the change in BoJ communication since their last meeting in January.

We remain unconvinced that the Yen can weaken much further in the near term and still expect the JPY to rebound heading into Q2 as the BoJ finally moves to exit negative rates based on the assumption that the upcoming wage negotiations do not disappoint.

- Natural Gas hits rock bottom and enters an area not seen since August 2020.

- Traders are following the ongoing probe by the House into Biden’s LNG export ban.

- The US Dollar Index steadies at 104 and is supported with some risk-off tone after ceasefire talks hit a dead end in the Middle East.

Natural Gas (XNG/USD) is trading sub-$2, and flirting with lower levels, not seen since August 2020. The move comes on the back of a probe by the House Committee on the action US President Joe Biden put in place to halt any developments on new LNG export terminals. The administration had said it would not issue approvals on new studies and plans earlier than after one year. The probe will be heading into its second day this Thursday with a hearing on the issue with Deputy Secretary of Energy David Turk.

The US Dollar (USD), which is negatively correlated to Natural Gas, is steady after some profit taking from its earlier peak performance on Monday and past Friday. The geopolitical element helps the Greenback a bit with Israel Prime Minister Benjamin Netanyahu rejecting the recent ceasefire proposal from Hamas and rather committing to fully infiltrating the Gaza region and liquidating Hamas. The breakdown of the ceasefire talks is triggering some risk off and is providing support for the Greenback.

Natural Gas is trading at $1.98 per MMBtu at the time of writing.

Natural Gas market movers: More downside headlines

- Europe sees Norway coming back online in full, delivering Natural Gas, after some brief supply hiccups and technical maintenance.

- Mild weather is forecasted for Europe, meaning that current Gas reserves are enough to see the current situation through until early summer.

- Japan is set to decrease its demand for Natural Gas with the nation boosting its nuclear power output, and will result in an 8% decline by the summer for its LNG needs.

- Germany and Algeria have signed a deal for Algeria to deliver pipeline Gas to Germany.

Natural Gas Technical Analysis: Ceasefire talks off the table

Natural Gas is facing a more substantial downturn and could be on its way to hit pre-Covid lows. Although the ceasefire plans are off the table now in the Middle East, markets have gotten time to grow accustomed to the tensions, and since the tensions escalated, Gas transit has not been distorted whatsoever. Overall, with spring coming closer, it does not look like Gas will be able to sprint substantially higher anytime soon under these conditions.

On the upside, Natural Gas is facing some pivotal technical levels to get back to. First, the low of January at $2.10 needs to be reclaimed again. Next is the intermediary level near $2.48. Once that area gets hit, expect to see a test near $2.57 at the purple line.

Once the current low at $2.04 gets tested, or broken again, expect the $2.00 big figure to crack under pressure as well. The first level to look for on the downside is near $1.95 (orange level) which goes back to August 2020. Next is the red line near $1.51, the low of June 2020.

-638429850316897688.png)

XNG/USD (Daily Chart)

Natural Gas FAQs

What fundamental factors drive the price of Natural Gas?

Supply and demand dynamics are a key factor influencing Natural Gas prices, and are themselves influenced by global economic growth, industrial activity, population growth, production levels, and inventories. The weather impacts Natural Gas prices because more Gas is used during cold winters and hot summers for heating and cooling. Competition from other energy sources impacts prices as consumers may switch to cheaper sources. Geopolitical events are factors as exemplified by the war in Ukraine. Government policies relating to extraction, transportation, and environmental issues also impact prices.

What are the main macroeconomic releases that impact on Natural Gas Prices?

The main economic release influencing Natural Gas prices is the weekly inventory bulletin from the Energy Information Administration (EIA), a US government agency that produces US gas market data. The EIA Gas bulletin usually comes out on Thursday at 14:30 GMT, a day after the EIA publishes its weekly Oil bulletin. Economic data from large consumers of Natural Gas can impact supply and demand, the largest of which include China, Germany and Japan. Natural Gas is primarily priced and traded in US Dollars, thus economic releases impacting the US Dollar are also factors.

How does the US Dollar influence Natural Gas prices?

The US Dollar is the world’s reserve currency and most commodities, including Natural Gas are priced and traded on international markets in US Dollars. As such, the value of the US Dollar is a factor in the price of Natural Gas, because if the Dollar strengthens it means less Dollars are required to buy the same volume of Gas (the price falls), and vice versa if USD strengthens.

Despite a progressively more restrictive monetary policy environment since early 2022, Gold recorded a surprisingly strong performance. It hovered above $2,000 for a significant part of the last twelve months. Economists at TD Securities analyze the yellow metal’s outlook.

XAU/USD to average $2,200 next quarter

The Fed's dovish pivot, along with another year of record official sector buying are set to feed a Gold bull run later in the year.

The combination of pending Fed rate cuts in the months to come should prompt traders to grow long exposure, and along with very strong physical demand and official sector buying are projected to lift prices to an average of $2,200 next quarter.

We expect Gold to average $2,081 for all of 2024.

- EUR/JPY refreshes weekly high near 160.50 on BoJ Shinichi’s dovish commentary.

- The BoJ may exit from its expansionary policy stance only after the wage cycle heightens.

- The Eurozone economy might remain stagnant in the fourth quarter of 2023.

The EUR/JPY prints a fresh weekly high near 160.50 in the European session on Thursday after dovish commentary from Bank of Japan (BoJ) Deputy Governor Uchida Shinichi. BoJ Shinichi said the central bank would be reluctant to raise interest rates aggressively despite exiting the decade-long ultra-dovish monetary policy.

Uchida Shinichi added that monetary policy conditions in the Japanese economy are in a deep negative trajectory, which is not expected to get blown up aggressively.

The Japanese Yen has been under pressure as BoJ policymakers run behind the market’s expectations of adopting a neutral stance. Slower wage growth momentum has been limiting hopes of exiting from an easy policy stance, limiting the sustainability of price pressures above 2%. Meanwhile, deepening geopolitical tensions have escalated uncertainty over restrictive policy stance.

On the Eurozone front, a vulnerable economic outlook has prompted expectations of early rate cuts by the European Central Bank (ECB). ECB policymaker Pablo Hernandez de Cos said this week, "it is already very important for European citizens to know that we are confident the next move will be a cut.” ECB Cos remains confident about inflation declining towards the 2% target.

On the contrary, the ECB Economic Bulletin released in early London indicated that Governing Council (GC) members will ensure that key rates remain sufficiently restrictive as long as price stability is ensured. Over the economic outlook, GC members anticipate a stagnant performance for the final quarter of 2023.

The Euro has rebounded against the US Dollar in recent days after hitting a year-to-date low at the start of this week at 1.0723. Economists at MUFG Bank analyze EUR/USD outlook.

Rising likelihood of ECB cutting ahead of Fed weighing on EUR/USD