- Аналітика

- Новини та інструменти

- Новини ринків

Новини ринків

- The AUD/USD caught a much-needed bid in Friday trading after the US NFP report clobbered forecasts.

- The Aussie still remains buried deep in bear country after falling to fresh lows for 2023 in the early week.

- Market focus is set to crystallize on US inflation expectations next week.

The AUD/USD etched in a new high for Friday at the 0.6400 level after catching a broad-market risk appetite bid that sent the US Dollar (USD) lower across the FX marketscape as market risk appetite flipped risk-on to close out the trading week.

US Nonfarm Payrolls soar by 336,000 in September vs. 170,000 forecast

Despite Friday's much-needed reprieve for the Aussie (AUD), which remains down nearly 11% against the USD for the year, market sentiment is due to turn back to US inflationary pressure next week, with US Producer Price Index (PPI) numbers and the Federal Reserve's (Fed) latest meeting minutes slated for next Wednesday, to be followed by the latest US Consumer Price Index (CPI) inflation reading later in the week.

US: All eyes will be on inflation data – RBC

AUD/USD technical outlook

The Aussie rode a wave of market risk appetite higher on Friday close the daily session in the green, but the AUD/USD is still down 0.75% on the week's opening prices near 0.6433.

Despite the late-week bullish push, the AUD/USD remains firmly entrenched in bearish territory, with current price action trading well below the 200-day Simple Moving Average (SMA) at 0.6675, with near-term moves capped by the 50-day SMA near 0.6450.

AUD/USD daily chart

AUD/USD technical levels

- US equities caught a firm bid on Friday after a bumper NFP beat.

- The S&P 500 has pinged a new high for the week as investors pile out of safe havens to close out the trading week.

- Inflation data for the US will be the key focus moving forward as markets watch the Fed carefully.

The Standard & Poor's (S&P) 500 soared late Friday into $4,305 after markets yanked out the stopper and went full risk-on after US Non-Farm Payrolls handily beat the street, printing at a forecast-clobbering 336K against the anticipated 170K, and the previous figure was also revised higher to 227K from 187K.

US Nonfarm Payrolls soar by 336,000 in September vs. 170,000 forecast

US equities have been knocked lower as of late, crushed underfoot by rising US Treasury yields. Investors, fearing that still-high inflationary pressures will keep the Federal Reserve (Fed) stuck in a higher-for-longer rate cycle.

Next week sees US Producer Price Index (PPI) numbers and the latest draft of the Fed's meeting minutes, and investors will be turning an eye towards next week's Consumer Price Index (CPI) to re-focus on inflation pressures after Friday's focus shift.

US: All eyes will be on inflation data – RBC

S&P 500 technical outlook

The S&P 500 closed out the trading week at $4,305 after tapping a new weekly high of $4,321.94. The major US equity index fell to an intraday low of $4,208.68 on reaction to the bumper NFP reading, before market sentiment shifted into high gear and giving the S&P a much-needed rebound into a new high for the week.

On the daily candlesticks the S&P 500 is in desperate need of a bullish extension after seeing a bullish rejection from the 200-day Simple Moving Average (SMA) near $4,220, but the index still remains firmly bearish, still down 6.5% from July's peak of $4,607, and is still stuck below technical resistance from the 50-day SMA at $4,421.78.

S&P 500 daily chart

S&P 500 technical levels

- EUR/JPY touches a four-day high of 158.26, buoyed by a sharp rally in EUR/USD, before settling around 158.05.

- Despite breaching the Ichimoku Cloud, immediate resistances at 158.47 and 158.65 cap further upward momentum.

- Potential downside could see the pair target 156.45, with further declines possibly testing the October 3 low of 154.34.

EUR/JPY prints solid gains of more than 0.90% on Friday after the EUR/USD rallied sharply towards a daily high of 1.0600, which lifted the cross-currency pair towards a four-day high of 158.26 before reversing toward current exchange rates at around 158.05.

From a technical perspective, the EUR/JPY remains consolidated in the daily chart despite breaking above the Ichimoku Cloud (Kumo), which is usually seen as a bullish signal, but immediate resistance would cap the Euro’s intentions of higher prices. If the pair aims higher, the first resistance is seen at the October 2 high of 158.47, followed by the September 13 daily high of 158.65, before challenging 159.00

On the flip side, if EUR/JPY drops inside the Kumo, it could dive towards the Senkou Span A at 156.45 before challenging the bottom of the Kumo at 156.49. Once those two levels are cleared, the pair could aim towards the October 3 daily/weekly low of 154.34.

EUR/JPY Price Action – Daily chart

EUR/JPY Technical Levels

Data released on Friday showed employment rose by 63,800 in September in Canada, surpassing expectations. Analysts at CIBC point out that weakness under the hood should limit its implications for the Bank of Canada.

Weakness under the hood

While the headline increase in employment was a surprise, the weaker detail and decline in hours worked point to a still sluggish economy to end Q3.

With GDP having basically stalled in Q2 and Q3, and without a clear indication that it was accelerating again heading towards the final quarter, we still see the Bank of Canada remaining on hold despite the stronger-than-anticipated inflation readings recently.

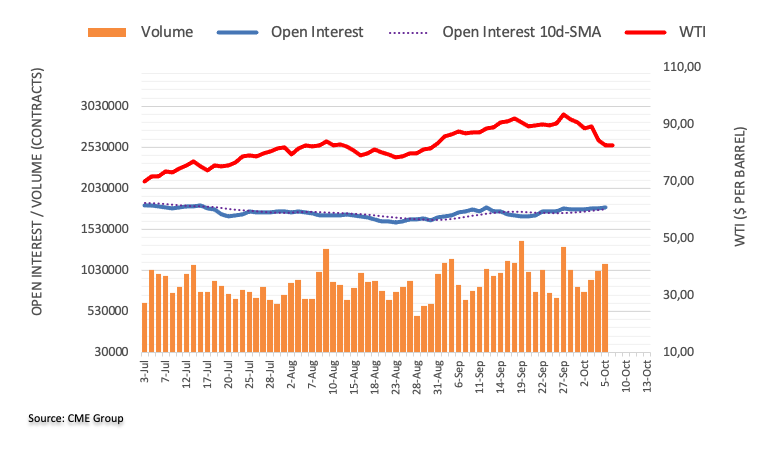

- WTI nudges up to $82.85 per barrel, gaining 0.40%, as the USD experiences a pullback, ending a 12-week rally.

- US job growth impresses with a 336K rise, yet Federal Reserve officials hint at a potential pause on rate hikes.

- Russia’s lifted diesel export ban and a dip in US oil rigs introduce new variables into WTI’s supply-demand equation.

West Texas Intermediate (WTI), the US crude oil benchmark, snaps two days of losses and climbs 0.55% late in the New York session. News that Russia’s lifted a fuel export ban capped the ongoing fally, while global economic headwinds threaten to dent demand.

Oil prices find respite as Russia lifts export bans, US Dollar retreats.

At the time of writing, WTI is trading at $82.85 per barrel and posting minimal gains of 0.40%. Oil’s uptick is attributed to broad US Dollar (USD) weakness, sparked after Greenback’s buyers booked profits ahead of the weekend. Consequently, the US Dollar Index (DXY), which measures the buck’s performance against its rival, posts weekly losses of -12% halting its 12-week rally.

Although the latest raft of US economic data was US Dollar-supportive, an overextended uptrend suggested the buck was headed for a mean reversion move. US job growth rose by 336K in September, as revealed by the Department of Labor, smashing estimates and the previous month’s data.

Meanwhile, Federal Reserve officials remain muted regarding the US Nonfarm Payrolls report, which justifies the need for higher rates. But San Francisco’s Fed President Mary Daly said, “The recent rise in Treasury yields is doing some of the work for the Fed, and if that doesn't reverse and inflation continues to cool, the Fed can leave rates on hold.”

In the meantime, Russia’s lifted its ban on diesel exports for supplies delivered to ports by pipeline, cushioning WTI’s advance as supply increases.

On the oil data front, US oil rigs fell five to 497 this week, the lowest level since February 2022, according to the energy services firm Baker Hughes.

WTI Technical Levels

- The US Dollar Index has gone full reverse in Friday trading following a forecast-busting NFP release.

- The DXY pegged a new low for the week after dropping away from 107.00.

- Market sentiment has twisted the throttle on risk appetite to close out the trading week, piling out of safe havens.

The US Dollar Index (DXY) tumbled in Friday trading after briefly reclaiming the 107.00 handle, sagging into a fresh low for the week at 105.95.

US Non-Farm Payrolls (NFP) figures on Friday handily beat forecasts, adding 336K jobs in September, well above the forecast decline to 170K and surging above the previous month's reading of 227K (revised upwards from 178K).

US Nonfarm Payrolls soar by 336,000 in September vs. 170,000 forecast

Inflation remains a firmly sticky thorn in the Federal Reserve's (Fed) side, and ongoing inflationary pressure is making market participants nervous that the Fed will have no choice but to keep interest rates higher for longer.

US: All eyes will be on inflation data – RBC

Forex Today: US data sustains Dollar strength, focus shifts to inflation

Dollar Index technical outlook

The US Dollar Index spiked to an intraday high just shy of the 107.00 level in Friday's trading on reaction to the better-than-expected NFP report, but broader markets quickly turned risk-on, sending the DXY into a fresh low for the week at 105.95.

The US Dollar is trapped on the low end to close out the trading week after Friday's nearly-1% plunge top-to-bottom, and the DXY is set for a showdown on daily candlesticks with a rising trendline from July's lows at 99.56.

Dollar Index daily chart

Dollar Index technical levels

Nathan Janzen, Assistant Chief Economist at Royal Bank of Canada points out that next week the crucial report in the US will be on Thursday with the Consumer Price Index (CPI). They see a slowdown in inflation, the headline and the core.

US inflation growth to edge lower in September

All eyes will be on U.S. inflation data in an otherwise quiet week of economic data releases. CPI growth likely looked a little better in September – we look for a slowing to a 3.5% year-over-year rate from 3.7% in August.

Fed policymakers will be more focused on ‘core’ measures that are more likely to be impacted by domestic economic conditions than global factors like energy price movements. Those measures have also slowed substantially. We look for price growth excluding food & energy products to edge down to a 4.0% year-over-year rate in September from 4.3% in August.

The Fed won’t hesitate to respond with higher interest rates to cool the economy and keep inflation in check. Although our own base-case assumes that won’t be necessary with the recent run of economic resilience not expected to last.

- GBP/USD rebounds from multi-month lows, climbing to 1.2240s amidst a backdrop of positive US labor market data.

- US Treasury bond yields echo a 'higher-for-longer' sentiment, while Fed officials present a somewhat moderated stance.

- Upcoming data, including US inflation figures and UK GDP, will influence the pair’s trajectory in the coming week.

The Pound Sterling (GBP) rallied for the third consecutive day against the US Dollar (USD) on Friday as the North American session began to wind down ahead of the weekend. Although September’s Nonfarm Payrolls report was positive, the GBP/USD recovered after reaching multi-month lows of 1.2037 and has risen more than 1.70% towards 1.2240s.

Pound Sterling leaps vs. USD amid central bank divergence between the BoE and the Fed

During the week, the GBP/USD pair was driven by expectations of further tightening by the US Federal Reserve (Fed). Even though most Fed speakers moderated their tone, US Treasury bond yields reflected the higher-for-longer mantra after reaching highs last seen in 2007. Michelle Bowman was the only Fed official who stated she would like to see another rate hike.

On the data front, the JOLTs Job Openings data was a prelude to today’s US Nonfarm Payrolls, which crushed estimates and the prior month's numbers. However, a moderate deceleration is business activity linked to the services sector portrays the slowing economy, but it remains expanding.

On the UK front, the S&P Global/CIPS Services PMI, although it exceeded estimates, deteriorated a tick. Speculations about a stagnating economy have trimmed the odds for additional tightening by the Bank of England (BoE), even though its Governor, Andrew Bailey, commented that inflation at around 6.7% would continue to fall amidst rates staying at around 5.25%.

Next week, the US economic docket will feature Fed speakers, producer and consumer price inflation figures, unemployment claims, and consumer sentiment. On the UK front, the Gross Domestic Product (GDP) would dictate the future direction for the Pound Sterling, along with the Goods Trade Balance and Industrial Production.

GBP/USD Price Analysis: Technical outlook

After printing a two-candlestick ‘bullis-engulfing’ chart pattern on Wednesday, price action exploded to the upside, but it has remained volatile, as Friday’s low pierced October 5 daily low of 1.2105. Buyers stepped in around the latter; consequently, the major reacted upwards of more than 100 pips. If the GBP/USD breaks above the September 29 latest swing high at 1.2271, the pair could rally towards 1.2300 and challenge the 1.2400 figure. Conversely, the Cable would remain subject to further selling pressure below 1.2271.

- Gold spot prices are catching a late-week lift out of the week's lows following a bumper NFP report.

- XAU/USD is still in bearish territory for the week after draining from $1,850.

- The US NFP firmly beat market expectations, sending risk appetite into the ceiling for Friday.

Gold spot prices have climbed into $1,833.00 in late Friday trading after a bumper US Non-Farm Payrolls (NFP) printing, and risk-on market flows are sending XAU/USD bids into fresh highs despite still remaining notably lower than Monday's opening prices.

The US economy added an unexpected 26K jobs to the employment landscape, handily beating the forecast 170K and rising even further from the previous reading of 227K, which was revised upwards from 178K.

Market sentiment has pinned firmly bullish following the NFP beat, taking XAU/USD back up the charts after most of the week saw spot Gold prices firmly on the low end.

US Nonfarm Payrolls soar by 336,000 in September vs. 170,000 forecast

Gold prices have been under immense pressure with US Treasury yields pinning into 17-year highs, pushing investors into safe-haven tunnels and sending the US Dollar soaring.

Markets are catching a brief breather from high-side Treasury yields, but next week will see renewed pressure from US Producer Price Index (PPI) figures and the Federal Reserve's (Fed) latest meeting minutes, where investors will be keeping a close eye on the Fed's internal dialogues, looking for hints about the US central bank's path forward on interest rates.

XAU/USD technical outlook

Despite Friday's bump-and-run in Gold prices, the XAU/USD remains deeply buried in bearish territory, down nearly 6% from mid-September's peak near $1,950.00.

The XAU/USD is set for a bullish relief rally with price action trading far below the 200-day Simple Moving Average (SMA) near $1,930.00, and it will be a challenge for Gold bulls to push spot prices back into near-term bullish territory with the 50-day SMA confirming a bearish cross of the longer moving average.

XAU/USD daily chart

XAU/USD technical levels

After the release of US labor data, the focus turns to inflation data and the FOMC minutes. These upcoming data points are expected to spur movements in the bond market and potentially challenge the dollar's strength.

Here is what you need to know for next week:

The US Dollar Index (DXY) continued its correction on Friday, despite the better-than-expected US employment report. The numbers triggered a rally in the Greenback, which was short-lived, suggesting some exhaustion of the rally. The DXY is set to end the week around 106.00, posting marginal losses and ending an 11-week positive streak. Although the trend remains upward, it has softened. Fundamentals still favor the Dollar, and the slide appears to be corrective in nature.

On Monday, the US market will be closed due to Columbus Day; it will also be a holiday in Canada.

The US will release wholesale inflation data on Wednesday. The Producer Price Index (PPI) is expected to rise by 0.4% in September. Later in the day, the Federal Reserve will release the minutes of its latest meeting, which will be closely watched.

Thursday will be a key day with the release of the US Consumer Price Index (CPI). The headline and core rates are expected to show a 0.3% monthly increase. A surprise with higher inflation would increase expectations of further tightening from the Federal Reserve and could lead to a stronger US Dollar and higher yields, potentially causing market concerns. Conversely, numbers below estimates could fuel risk appetite and weigh on the US Dollar. The weekly Jobless Claims report will also be closely watched, especially after the upbeat Nonfarm Payrolls.

Several Fed officials are scheduled to deliver remarks, including Vice Chair Jefferson and Logan on Monday, and Waller on Tuesday. The next FOMC decision is on November 1.

EUR/USD rose after falling for 11 consecutive weeks, gaining ground after the Nonfarm Payrolls release on Friday. The pair appears to be stabilizing, and a break above 1.0630 could strengthen the rebound. The European Central Bank (ECB) will release the minutes of its latest meeting on Thursday.

GBP/USD rose on Friday for the third day, approaching the 20-day Simple Moving Average (SMA) at 1.2260. The pair had its best week since early July. The UK's monthly GDP and Manufacturing Production data are due on Thursday.

USD/JPY remains near the critical area of 150.00, which is suspected of having triggered intervention from Japanese authorities to curb the yen's strength on Tuesday. The pair posted its highest weekly close in decades around 149.35 and remains supported by the divergence between US and Japanese bond yields.

Commodity-linked currencies were the worst performers during the week. Declines in crude oil prices, metals, and deteriorating market sentiment weighed on these currencies. However, they ended the week on a positive note, with a move that could continue into next week.

China will release trade data on Friday, which will be important for market sentiment and Antipodean currencies. The economic calendar for Australia and New Zealand is quiet for the week ahead.

AUD/USD finished the week slightly lower, hovering around 0.6390 but far from the monthly low it reached earlier. The pair returned to the previous range, and the recovery signals positive momentum for the Aussie. However, it needs to rise above 0.6500 to change the short-term outlook.

NZD/USD ended the week flat, slightly below 0.6000. It remains below the 20-day Simple Moving Average at 0.6050, an area that could be challenged next week.

Canadian data and the reversal in crude oil prices brought volatility to the Loonie. While the sharp decline in crude oil prices weighed on the currency, positive Canadian employment data boosted it. USD/CAD posted its highest weekly close since March, around 1.3660. The pair peaked at 1.3785 and pulled back sharply, increasing the risk of an extension to the downside.

Gold rebounded at the 200-week SMA and managed to stay above $1,800. On Friday, it staged a recovery, surging above $1,830. The trend is downward, but short-term momentum favors the yellow metal.

Like this article? Help us with some feedback by answering this survey:

- The GBP/JPY is catching a late-week lift as investors jump back into risk assets.

- Market sentiment has flipped positive to close out the trading week.

- The US NFP printing has sent the entire market broadly risk-on and most pairs are recovering the week's downside action.

The GBP/JPY is tapping into the week's highs near 182.80 after catching a firm lift on rebounding investor market sentiment, climbing a full 1% from the day's lows just past the 181.00 handle and is now testing 182.75 after a 180-pip climb.

Broader markets went firmly risk-on following the US Non-Farm Payrolls (NFP) data beat, with the NFP showing 336K jobs added to the US economy, well above the forecast 170K. Market sentiment has turned firmly bullish on the bumper reading, sending risk assets back into weekly highs, sending markets broadly into the green for the Friday trading session.

The GBP/JPY tapped into 182.80 on the post-NFP market run-up, and is currently trading into 182.70 as the trading week wraps up another Friday session.

Japanese Labor Cash Earnings missed expectations in the early Friday trading session, holding flat at the previous printing of 1.1% and flubbing market expectations of a rise to 1.5%, and Guppy traders will be looking ahead to Monday's UK BRC Like-For-Like Retail Sales on Monday, which last showed similar retail sales rising 4.3% for the annualized period into August.

GBP/JPY technical outlook

The GBP/JPY is set to close out Friday's trading session firmly bid, testing the week's highs near 182.80 after rising from Friday's early lows near the 181.00 psychological level.

The GBP/JPY is catching a near-term bullish bounce on the daily candles, climbing from Tuesday's low near 178.00 and lifting into the 50-day Simple Moving Average (SMA) just north of current price action at 183.36.

The Guppy has been treading water in firmly bullish territory in the long-term, with candlesticks still trading well above the 200-day SMA at 172.00, and the tricky challenge for GBP/JPY bidders will be pushing the pair back above August's highs past the 186.00 handle.

GBP/JPY daily chart

GBP/JPY technical levels

- Canadian Dollar market flows turn bullish following US & Canada labor data prints.

- Canada Unemployment Rate flat at 5.5%, US unemployment holds at 3.8%.

- US NFP handily beats expectations with slightly softer earnings.

The Canadian Dollar (CAD) is climbing to fresh highs, set to challenge Monday’s trading range following a bumper labor data release, with a firm US Nonfarm Payrolls (NFP) reading for the US Dollar (USD) mixing with misses on hourly wages and unemployment.

Canada labor markets continue to improve, with the Canadian economy adding more jobs than expected, but a bumper NFP reading is seeing mixed results for the USD on lethargic US unemployment rate and wages figures.

Daily Digest Market Movers: Canadian Dollar staggers on labor data, US NFP

- US NFP broadly beat expectations, printing 336K against the expected 170K, and handily vaulting over the previous 227K (revised upwards from 187K).

- US data came in mixed despite the broad NFP beat, with hourly wages holding steady at 0.2% for September against the expected uptick to 0.3%.

- US Unemployment Rate also failed to meet expectations, flat at 3.8% versus the forecast 3.7%.

- Canadian Unemployment Rate held at 5.5% against the forecast 5.6%.

- Canadian jobs change shows a bumper 63.8K change in net employment against the forecast 20K and clearing the previous 39.9K.

- The data-beat for the Loonie was a clean beat for the CAD against the US Dollar, and the USD/CAD pair is dropping back after spending most of the week on the high end.

- US 10-year Treasury yields shot back up to 4.88% for the day, but the Loonie is holding surprisingly resilient.

- Little meaningful data remains until Wednesday’s US Producer Price Index (PPI) figures.

Technical Analysis: Canadian Dollar catches a rise on labor data beats, sending USD/CAD back to 1.3660

The USD/CAD clipped into an intraday high of 1.3746 before getting forced back down the charts into 1.3660, losing contact with the 50-hour Simple Moving Average (SMA) near 1.3720 and making a run for support at the 200-hour SMA near 1.3620.

Despite Friday’s reprieve, the USD/CAD remains firmly bullish on the charts, trading well above the 200-day SMA near 1.3450 and the 50-day SMA confirming a bullish cross of the longer moving average.

The Relative Strength Index (RSI) has pulled back from overbought conditions on the daily chart, and USD/CAD short interest will want a bearish confirmation before following the indicator lower.

Nonfarm Payrolls FAQs

What are Nonfarm Payrolls?

Nonfarm Payrolls (NFP) are part of the US Bureau of Labor Statistics monthly jobs report. The Nonfarm Payrolls component specifically measures the change in the number of people employed in the US during the previous month, excluding the farming industry.

How does Nonfarm Payrolls influence the Federal Reserve monetary policy decisions?

The Nonfarm Payrolls figure can influence the decisions of the Federal Reserve by providing a measure of how successfully the Fed is meeting its mandate of fostering full employment and 2% inflation.

A relatively high NFP figure means more people are in employment, earning more money and therefore probably spending more. A relatively low Nonfarm Payrolls’ result, on the either hand, could mean people are struggling to find work.

The Fed will typically raise interest rates to combat high inflation triggered by low unemployment, and lower them to stimulate a stagnant labor market.

How does Nonfarm Payrolls affect the US Dollar?

Nonfarm Payrolls generally have a positive correlation with the US Dollar. This means when payrolls’ figures come out higher-than-expected the USD tends to rally and vice versa when they are lower.

NFPs influence the US Dollar by virtue of their impact on inflation, monetary policy expectations and interest rates. A higher NFP usually means the Federal Reserve will be more tight in its monetary policy, supporting the USD.

How does Nonfarm Payrolls affect Gold?

Nonfarm Payrolls are generally negatively-correlated with the price of Gold. This means a higher-than-expected payrolls’ figure will have a depressing effect on the Gold price and vice versa.

Higher NFP generally has a positive effect on the value of the USD, and like most major commodities Gold is priced in US Dollars. If the USD gains in value, therefore, it requires less Dollars to buy an ounce of Gold.

Also, higher interest rates (typically helped higher NFPs) also lessen the attractiveness of Gold as an investment compared to staying in cash, where the money will at least earn interest.

Sometimes Nonfarm Payrolls trigger an opposite reaction than what the market expects. Why is that?

Nonfarm Payrolls is only one component within a bigger jobs report and it can be overshadowed by the other components.

At times, when NFP come out higher-than-forecast, but the Average Weekly Earnings is lower than expected, the market has ignored the potentially inflationary effect of the headline result and interpreted the fall in earnings as deflationary.

The Participation Rate and the Average Weekly Hours components can also influence the market reaction, but only in seldom events like the “Great Resignation” or the Global Financial Crisis.

- USD/JPY ascends to 149.50, rebounding from lows, driven by a US jobs report that eclipsed market expectations.

- Despite a surge, USD/JPY retraces slightly, settling around 149.20, with US 10-year note yielding at a sturdy 4.780%.

- Japanese officials express concerns over Yen volatility, while a rise in the 10-year JGB coupon hints at potential BoJ intervention.

USD/JPY climbs during the North American session courtesy of solid US jobs data, which spurred a jump from the last two days' lows of 148.26. On its way north, buyers reclaimed the 149.00 mark and hit a three-day high of 149.50, underpinned by high US bond yields.

US bond yields and employment data boost the USD/JPY, though caution is warranted as Japanese authorities watch volatility

The latest US jobs market data revealed by the US Bureau of Labor Statistics (BLS) witnessed the creation of more than 336K employees in the economy, smashing estimates of 170K and 100K more than the 227K August upward revised data. The report shows the labor market remains hot, though it could be influenced by seasonality adjustments.

On the wage front, Average Hourly Earnings rose by 4.2% below the consensus and August’s 4.3%, and the Unemployment Rate was unchanged at 3.8%, higher than the consensus of 3.7%.

The USD/JPY increased towards a high of 149.53 before reversing its course and stabilizing at around 149.20. the US 10-year benchmark note retreated from 2007 highs of 4.887%, but it remains up six basis points at 4.780%.

On the Japanese front, authorities remain vocal in regard to “excessive” Japanese Yen (JPY) volatility in the FX markets. Masato Kanda said on Wednesday, “If currencies move too much on a single day or, say, a week, that's judged as excess volatility.”

“Even if that's not the case, if we see one-sided moves accumulate into very big moves in a certain period of time, that's also excess volatility,” he said.

Although there was no official statement regarding last Tuesday’s 200 plus pip fall of the USD/JPY from around 150.00, the exchange rate remains well-suited below the latter. Of note, it should be said that the 10-year Japanese Government Bond (JGB) coupon has risen to 0.80%, opening the door for the Bank of Japan (BoJ) to intervene and cap the recent rise in yields.

USD/JPY Technical Levels

- EUR/USD catches a firm lift post-US NFP release, climbing 1.12% from the day's bottom.

- Broad-market flows have gone firmly risk-on following a bumper NFP reading for the USD.

- Euro traders will be looking ahead to Monday's investor confidence indicator for October.

The EUR/USD climbed 117 pips from Friday's bottom bids of 1.0482 to tap into the 1.0600 handle as Friday's US Non-Farm Payrolls (NFP) sends investors piling out of the US Dollar and back into risk assets to close out the trading week. The EUR/USD is now trading back slightly, testing the waters around 1.0580 as investors settle into the Friday close.

US Nonfarm Payrolls soar by 336,000 in September vs. 170,000 forecast

The Euro (EUR) is now back into green territory for the trading week, but only just, after hitting a weekly low near 1.0448. The US added 336K jobs last month, a clean beat of the forecast 170K and a step above the previous print of 176K (revised upwards to 227K).

The economic calendar is looking notably thin for the opening half of next week, with the EU's Sentix Investor Confidence reading for October, which last printed at -21.5.

Next Wednesday will bring US Producer Price Index (PPI) figures, as well as the Federal Reserve's latest meeting minutes.

EUR/USD technical outlook

The EUR/USD is trading just south of 1.0600 after climbing from Friday's bottom, turning the trading day green and erasing the week's downside losses as Euro bulls look to keep the pair trading in positive territory into the closing bell.

The Euro is set to close bullish against the US Dollar for the third straight trading day, but the pair remains steeply in bearish territory with daily candlesticks still trading far below the 200-day Simple Moving Average (SMA) near 1.0825.

A descending trendline from July's peak of 1.1275 remains the target to beat for bidders, and the 50-day SMA will pose an additional technical challenge as it confirms a bearish crossover of the longer moving average.

Technical indicators are moving broadly out of oversold territory, and bidders could use the reversal signals to gain a foothold into higher territory. The Relative Strength Index (RSI) and Moving Average Convergence-Divergence (MACD) indicators are both rolling over from oversold to bidding phases, giving the EUR/USD room to run if investor confidence manages to hold steady.

EUR/USD hourly chart

EUR/USD daily chart

EUR/USD technical levels

- The NZD/USD is bounding higher as the US Dollar falls back on NFP data beats.

- Kiwi catches enough lift to tap the 0.6000 major level post-NFP.

- The Kiwi is now grasping to stay flat on the week.

Friday markets are seeing a broad reversal of the week's flows after the US Non-Farm Payrolls (NFP) figures came ion well above expectations, with the US economy adding 336K jobs, well above the forecast decline to 170K and easily beating the previous figure which was revised from 187K to 220K.

US Nonfarm Payrolls soar by 336,000 in September vs. 170,000 forecast

With the US NFP barrelshot out of the way, markets are stepping away from the US Dollar (USD) to close out the trading week, and the NZD/USD has rebounded from Friday's low of 0.5923 and is now trading back slightly into 0.5980 after briefly tipping into the 0.6000 major handle.

Markets will be rounding the corner into a sedate trading window next week, and meaningful data isn't expected until Wednesday's US Producer Price Index (PPI) figures as well as the Federal Reserve's (Fed) Federal Open Market Committee (FOMC) which will be dropping their latest meeting minutes for investors to review.

NZD/USD technical outlook

The NZD/USD pinged 0.6000 following the US Dollar's broad-market fallback, sending the pair back into the week's opening bids. The pair has climbed 2.2% from the week's bottom near 0.5870, and the Kiwi is set to fall back heading into the Friday close.

On the daily candlesticks the NZD/USD still remains firmly planted in consolidation territory, trading into the 50-day Simple Moving Average (SMA) with the 200-day SMA firmly entrenched just north of 0.6150.

September's bottom of 0.5846 still remains a key technical floor, but the pair is still well off recent highs, down 6.7% from July's peak into 0.6415.

NZD/USD hourly chart

NZD/USD daily chart

NZD/USD technical levels

- Silver rebounds from a near $20.80 low, surging above $21.50, undeterred by positive US economic reports.

- A critical resistance at $21.60/70 looms, with a breakthrough potentially paving the way to $22.00.

- Downward path highlights supports at $21.00 and a 7-month low of $20.69, with a possible dip to $19.90

Silver price (XAG/USD) stages a recovery after bottoming at around the $20.80 area during the last three days, rising back above $21.50, posting gains of 2.81%. An upbeat report from the United States (US) was not a reason to stop Silver’s climb on Friday.

The daily chart portrays the XAG/USD as neutral to downward biased despite registering solid gains. At the time of writing, Silver is testing the bottom of an upslope support trendline turned resistance, which passes at around $21.60/70, which, if broken, could sponsor another leg-up for XAG/USD towards the $22.00 mark. Once cleared, the next stop would be the 20-day Exponential Moving Average (EMA) at $22.50.

Conversely, and the path of least resistance, the XAG/USD first support would be $21.00, followed by the recent 7-month low of $20.69. A decisive break, Silver’s could test the year-to-date (YTD) low reached on March 2023 at around $19.90.

XAG/USD Price Action – Daily chart

XAG/USD Technical Levels

- USD/CHF spirals to a weekly low of 0.9074, even as US hiring surges to a robust 336K.

- Greenback’s rally falters, with the DXY index retracting 0.34%, slipping back beneath the pivotal 106.00.

- Market eyes on Fed officials, upcoming meeting minutes, and crucial inflation data to discern future USD/CHF dynamics.

The Swiss Franc (CHF) extended its gains versus the US Dollar (USD) as the pair dropped past the 0.9100 figure, which briefly halted the downward pullback, but selling pressure outpaced buyers struggling to cap the downtrend. The USD/CHF is trading at around 0.9080s, hitting a new weekly low of 0.9074.

Despite robust US Nonfarm Payrolls, USD/CHF slumped to a new weekly low

The US Department of Labor revealed the latest Nonfarm Payrolls report, which crushed forecasts as hiring in September rose by 336K, crushed the 170K, and exceeded the upward revised figures for August to 227 K. Digging a little deep into the data, Average Hourly Earnings aimed down from 4.3% to 4.2% below estimates, and the Unemployment Rate stood at 3.8%, unchanged from August.

Even though the data released lifted the USD/CHF toward a daily high of 0.9175, the major has reversed that leg-up and tumbled, as the Greenback rally was overextended. The US Dollar Index (DXY) , which measures the buck’s value against a basket of six currencies, drops 0.34%, below the 106.00 mark.

Meanwhile, market participants had increased the US Federal Reserve’s (Fed) odds for 25 bps for the December meeting, standing at 42.04% according to the CME FedWatch Tool.

For the next week, USD/CHF traders would take some clues from Federal Reserve officials, the Fed's last meeting minutes, and inflation data.

USD/CHF Price Analysis: Technical outlook

From a technical standpoint, the USD/CHF daily chart portrays the pair forming a ‘double-top’, confirmed by price action falling below the last cycle low of 0.9091. That said, the chart pattern price objective would be 0.8960, but on its way south, the major must reclaim the 200-day moving average (DMA) at 0.9025, followed by the 0.9000 mark.

- Mexican Peso is marking over 5% weekly losses as US Nonfarm Payrolls outperform analysts' estimates.

- Mexico's encouraging data fails to lift the Peso’s amid government regulatory changes.

- Rumors of Tesla’s Giga factory cancellation and airport tariff changes amplify investor apprehension in Mexico.

Mexican Peso (MXN) selling pressure continues, with the emerging market currency losing ground against the US Dollar (USD) early in the North American session. The USD/MXN pair climbed to a seven-month high of 18.48, shy of testing the psychological 18.50 price level. Solid economic data from the United States (US) underpins the USD/MXN, which is posting substantial gains of more than 5% in the week.

The US Bureau of Labor Statistics (BLS) revealed the Nonfarm Payrolls report for September, which crushed estimates as job creation was almost twice expectations, with figures coming at 336K vs. 170K forecasts by analysts. Further data showed the Participation Rate was unchanged, while the Unemployment Rate was aligned with August’s figures at 3.8%. Average Hourly Earnings growth, seen as an equivalent of inflation linked to wages, was 4.2% YoY, a tick lower than foreseen.

Daily Digest Market Movers: Mexican Peso weakens further; economists lift estimates for USD/MXN

- US Nonfarm Payrolls for September came at 336K, exceeding forecasts of 170K, and crushed last month’s 227K (upwardly revised from 187K).

- The Unemployment Rate in the US stood at 3.8% above estimates but flat compared with August, while the Participation Rate stood at 62.8%.

- Average Hourly Earnings eased from 4.3% to 4.2% YoY.

- Auto Exports in Mexico rose 16% YoY in September, above the prior month’s 15.7%.

- Mexico’s September auto Production soared 24%, smashing August’s minuscule 2.8% growth.

- According to Reuters, “Rohan Patel, Tesla's senior public policy and business development executive, in a post on the platform X, formerly Twitter, rejected a Mexican media report saying Tesla had canceled its plans and thanked local, state and federal officials.”

- The Mexican Stock Exchange continues to feel the effects of the government’s decision to change airport tariffs, while rumors of Tesla’s canceling its Giga factory plant spooked investors.

- A Citi Banamex poll showed economists estimate headline inflation at 4.70% and core at 5.09% for the year’s end.

- Analysts polled by Citi Banamex foresee the USD/MXN to end 2023 at 17.80, up from 17.60, and for 2024 at 18.86, up from 18.70 two weeks ago.

- On Wednesday, the IMF raised Mexico’s growth projection in 2023 from 2.6% to 3.2% and from 1.5% foreseen in July to 2.1% for 2024.

- Banxico’s September poll amongst economists reported that interest rates are expected to remain at 11.25% while inflation would dip to 4.66%.

- The same poll shows the exchange rate is set to finish at around 17.64, down from 17.75.

- Mexico’s S&P Global Manufacturing PMI for September came at 49.8, sliding to contractionary territory and below August’s 51.2, as the economy loses steam.

- The Bank of Mexico (Banxico) held rates at 11.25% in September and revised its inflation projections from 3.5% to 3.87% for 2024, above the central bank’s 3% target (plus or minus 1%).

- Banxico’s Government Board highlighted Mexico’s economic resilience and the strong labor market as the main drivers to keep inflation at the current interest rate level.

Technical Analysis: Mexican peso at the brisk of testing 18.50

The daily chart shows that the Mexican Peso is set to extend its losses. The USD/MXN pair has hit a new cycle high at 18.48, putting into play a challenge of the psychological 18.50 figure, which could extend towards the April 2018 yearly low of 18.60. With those levels cleared, the next stop would be the March 24 high at 18.79, followed by the psychological 19.00 figure.

Mexican Peso FAQs

What key factors drive the Mexican Peso?

The Mexican Peso (MXN) is the most traded currency among its Latin American peers. Its value is broadly determined by the performance of the Mexican economy, the country’s central bank’s policy, the amount of foreign investment in the country and even the levels of remittances sent by Mexicans who live abroad, particularly in the United States. Geopolitical trends can also move MXN: for example, the process of nearshoring – or the decision by some firms to relocate manufacturing capacity and supply chains closer to their home countries – is also seen as a catalyst for the Mexican currency as the country is considered a key manufacturing hub in the American continent. Another catalyst for MXN is Oil prices as Mexico is a key exporter of the commodity.

How do decisions of the Banxico impact the Mexican Peso?

The main objective of Mexico’s central bank, also known as Banxico, is to maintain inflation at low and stable levels (at or close to its target of 3%, the midpoint in a tolerance band of between 2% and 4%). To this end, the bank sets an appropriate level of interest rates. When inflation is too high, Banxico will attempt to tame it by raising interest rates, making it more expensive for households and businesses to borrow money, thus cooling demand and the overall economy. Higher interest rates are generally positive for the Mexican Peso (MXN) as they lead to higher yields, making the country a more attractive place for investors. On the contrary, lower interest rates tend to weaken MXN.

How does economic data influence the value of the Mexican Peso?

Macroeconomic data releases are key to assess the state of the economy and can have an impact on the Mexican Peso (MXN) valuation. A strong Mexican economy, based on high economic growth, low unemployment and high confidence is good for MXN. Not only does it attract more foreign investment but it may encourage the Bank of Mexico (Banxico) to increase interest rates, particularly if this strength comes together with elevated inflation. However, if economic data is weak, MXN is likely to depreciate.

How does broader risk sentiment impact the Mexican Peso?

As an emerging-market currency, the Mexican Peso (MXN) tends to strive during risk-on periods, or when investors perceive that broader market risks are low and thus are eager to engage with investments that carry a higher risk. Conversely, MXN tends to weaken at times of market turbulence or economic uncertainty as investors tend to sell higher-risk assets and flee to the more-stable safe havens.

US treasury yields have risen substantially in recent weeks. The question is how far yields could rise in the coming years. Another is how far they could fall. Economists at Rabobank address these questions.

Still upward potential in the 10-year US treasury yield in the FOMC scenario

We find that if the economy evolves in line with the FOMC projections, the 10-year yield will rise to over 5% in 2024, followed by a gradual decline to the 3-4% range in the coming years.

In a scenario with inflation rebounding to 5%, the 10-year yield peaks at almost 6.1% in December 2024 and then slides back slowly to about 4.5%.

In a scenario of economic stagnation, the 10-year yield starts to fall in 2024 and continues to decline toward 1% in the following years.

US job growth blew past expectations in September. After NFP, FOMC is watching the Consumer Price Index (CPI ) and Employment Cost Index (ECI) closely, economists at Wells Fargo report.

FOMC to remain on hold at its upcoming November 1 meeting

Today's report drove yet another increase in Treasury yields and fanned the flames that the FOMC may hike the federal funds rate one more time at one of its two remaining meetings of the year.

Another rate hike before the end of the year is a possibility, but for now, our base case remains that the last rate hike of the tightening cycle occurred in July.

The earnings data from the employment report are a somewhat crude measure of wages, so the Employment Cost Index (ECI) to be released on October 31 will be critical to confirming that labor costs are indeed decelerating. If the CPI and ECI data cooperate, we would expect the FOMC to remain on hold at its upcoming November 1 meeting.

In September, the Philippine Peso was volatile against the US Dollar. Economists at MUFG Bank analyze USD/PHP outlook.

Risks PHP come from oil, rice and the US Dollar

We forecast gradual weakness in PHP against the US Dollar at 57.30 in 3M and 57.50 in 12M.

While we continue to note upside risks on global oil and rice prices, we do see some areas of support for PHP, which is reflected in our forecast for gradual weakness in the FX. First, BSP has intervened more aggressively and turned more hawkish. Second, the current account deficit should narrow slightly. Third, FDI flows should also pick up in 2024. Lastly, we still expect inflation to trend lower.

Risks to our PHP forecasts come from oil, rice and the US Dollar.

USD/PHP – Q4 2023 57.30 Q1 2024 57.50 Q2 2024 57.50 Q3 2024 57.50

The Taiwan Dollar extended losses to the lowest against the US Dollar since November 2022. Economists at MUFG Bank analyze USD/TWD outlook.

USD/TWD to range-bound

While overall external demand remains weak and USD remains strong, the marginal recovery of semiconductor sector and potential upside on CNY likely lend some support for the currency.

Net, we expect USD/TWD to range-bound but with a upside bias for TWD against the Dollar in near term, before TWD’s strengthening in medium term on the rebound of AI investment.

USD/TWD – Q4 2023 32.00 Q1 2024 31.80 Q2 2024 31.40 Q3 2024 31.00

- AUD/USD has dropped to near 0.6300 after robust US job data.

- The US laborforce witnessed 336K fresh payrolls, much higher than estimates of 170K.

- Fed Mester was ‘loud and clear’ that the central bank is not done with hiking interest rates.

The AUD/USD pair has faced an intense sell-off to near 0.6300 after the better-than-projected United States Nonfarm Payrolls (NFP) report. The Aussie asset shifted into a bearish trajectory as the market mood has turned cautious as the expectations of one more interest-rate hike from the Federal Reserve (Fed) has accelerated.

The S&P500 opened on a bearish note after the upbeat US job growth in September. The US laborforce witnessed 336K fresh payrolls, much higher than estimates of 170K and the former release of 227K. The jobless rate remains steady at 3.8%, nominally higher than expectations of 3.7%. The monthly wage rate grew by 0.2% but was lower than expectations of 0.3%. The annualized wage rate decelerated to 4.2% vs. the estimates and the former release of 4.3%.

Meanwhile, the US Dollar Index (DXY) jumps to near 106.80 as the odds of one more rate hike from the Fed has increased. As per the CME Fedwatch tool, the chances for interest rates remaining unchanged at 5.25-5.50% have dropped to 70% from 81% after the NFP data release. Also, trades see a 39% chance for Fed increasing rates to 5.50-5.75% by the year-end.

This week, Cleveland Fed Bank President Loretta Mester was ‘loud and clear’ that the Fed is not done with hiking interest rates. Fed Mester said that one more interest rate hike is well-needed this year and they are required to remain high for a longer period. Interest rates should remain high for long enough until the central bank assess the impact of policy-tightening yet done.

On the Aussie front, the Australian Dollar remained under pressure as the Reserve Bank of Australia (RBA) kept the interest rates unchanged at 4.1% as expected by the market participants. The RBA kept monetary policy steady for the fourth time in a row.

The Hong Kong Dollar (HKD) has been a symbol of globalisation since the opening of China’s economy 40 years ago. Economists at ANZ Bank analyze the HKD outlook.

A weak HKD is a market reality

As the US Federal Reserve quantitatively tightens and financial demand in Hong Kong remains lacklustre, the HKD is likely to stay at the weaker side of the band over the next few years.

A weak HKD is a market reality rather than a phenomenon caused by geopolitical pressure.

Economists at ING analyze EUR/USD outlook for the next year.

EUR/USD currently contains a 2% risk premium

Our calculations point to EUR/USD still heading up towards the 1.18 area in the second half of 2024 based solely on our house calls for the Fed and European Central Bank policy trajectories. Yet, as we have seen repeatedly, policy rate differentials are not the sole driver of EUR/USD.

Currently, we estimate that EUR/USD contains a 2% risk premium – a risk premium that can extend to 6% during times of extreme stress in the Eurozone.

A low growth environment in the Eurozone and political uncertainty over the re-introduction of the Stability and Growth Pact will keep that risk premium in the Euro and means that EUR/USD ends this year near 1.06 and that its best levels of 2024 may be closer to 1.15 rather than 1.18.

"For the moment, we are fine with the current level of rates," European Central Bank's (ECB) policymaker Peter Kazimir said on Friday, as reported by Reuters.

On a separate note, ECB policymaker Boštjan Vasle argued that it was impossible to tell today whether more tightening will be needed and said that it was possible to get to the inflation target without a recession.

Market reaction

The EUR/USD pair showed no immediate reaction to these comments and was last seen losing 0.40% on the day at 1.0505.

- USD/JPY prints a fresh three-day high at 149.50 on the robust US NFP report.

- Fresh payrolls in September were higher at 336K than expectations of 170K and 227K reading from August.

- The resilient US labor market data may elevate hopes of one more interest rate increase from the Fed.

The USD/JPY pair prints a fresh three-day high at 149.50 after the release of the better-than-anticipated United States Nonfarm Payrolls (NFP) report. The asset strengthens as resilient labor market conditions are expected to set a hawkish undertone for the Federal Reserve’s (Fed) monetary policy meeting in November.

As per the US NFP report, 336K individuals were hired by US employers in September, which was notably higher than expectations of 170K and 227K reading from August. The Unemployment Rate remained unchanged at 3.8%, a tick higher than expectations of 3.7%.

On the wage front, monthly Average Hourly Earnings grew steadily at a 0.2% pace while investors forecasted a higher pace of 0.3%. The annualized wage data edged down to 4.2% against the consensus and the former release of 4.3%.

The US Dollar Index (DXY) climbs to near 107.00 as the resilient US labor market data is expected to elevate hopes of one more interest rate increase from the Fed. Also, 10-year US Treasury yields jumped to near 4.84%. This week, Fed Bank President Loretta Mester said that interest rates should rise again in November if the economy continues to remain the way it is. Fed’s interest rates could remain unchanged if labor demand turns weak.

On the Japanese Yen front, the clarification from Bank of Japan’s (BoJ) money market data that Tuesday’s flash crash was not due to the central bank’s intervention in the FX domain has impacted the Japanese Yen’s appeal. Things have come back to square, investors continue to await the BoJ’s stealth intervention.

- EUR/USD reverses initial gains and refocuses on 1.0500.

- There is still scope for another visit to the YTD low near 1.0450.

EUR/USD gives away the initial advance to the 1.0570 region and shifts its attention back to the 1.0500 neighbourhood on Friday.

The continuation of the rebound should initially retarget the minor barrier at 1.0617 (September 29) ahead of the weekly peak of 1.0767 (September 12). On the flip side, if bears regain the upper hand, the pair could slip back to the area of yearly lows around 1.0450 (October 3).

Meanwhile, further losses remain on the table as long as the pair navigates the area below the key 200-day SMA, today at 1.0823.

EUR/USD daily chart

- DXY now reverses two daily pullbacks in a row on Friday.

- Further recovery targets the YTD top near 107.30.

DXY stages quite a marked comeback and sets aside two consecutive sessions of losses on Friday.

Considering the ongoing price action, extra gains appear likely in the dollar for the time being. Once the index clears the 2023 top of 107.34 (October 3), it could encourage bulls to challenge the weekly peak at 107.99 (November 21 2022) just ahead of the round level at 108.00.

In the meantime, while above the key 200-day SMA, today at 103.16, the outlook for the index is expected to remain constructive.

DXY daily chart

The US labor market held up surprisingly well in September. Pressure for another rate hike is rising, economists at Commerzbank report.

Data for the previous months were revised significantly upward

In September, job growth in the US amounted to 336K, which was significantly more than expected. The continued strong employment growth – which has been revised significantly upward for the previous months – does not suggest that the labor market is moving into a better balance of supply and demand. This raises questions as to whether the easing in wages is permanent. Pressure is mounting on the Fed to hike rates once again.

No further employment report is due before the next FOMC meeting on October 31/November 1, which could make it clearer whether job growth has re-accelerated, against the Fed's wishes. Thus, the inflation figures scheduled for next week could be the deciding factor as to whether the Fed hikes or prefers to wait for more data.

- The US economy adds 336K jobs in September, surpassing expectations of 170K.

- Canadian employment rose by 64K, also surpassing expectations.

- USD/CAD remains near the 1.3720 area as the Loonie outperforms.

The USD/CAD rose to 1.3745 after the release of US and Canadian labor market data and then reversed, pulling back toward the 1.3700 area. The positive impact of the US figures was offset by the Canadian report.

Upbeat jobs reports

The Unemployment Rate in Canada held steady at 5.5% in September, better than the market consensus of a modest increase to 5.6%. Employment rose by 63,800, above the 20,000 expected.

In the US, Nonfarm payrolls jumped by 336K, largely above the 170K of market consensus. August numbers were revised higher from 187K to 227K. The Unemployment rate remained steady at 3.8%.

The numbers boosted both the US Dollar and the Canadian Dollar, resulting in the USD/CAD remaining in a familiar range around 1.3720. The Loonie is outperforming while the US Dollar Index is up by 0.45%, approaching the 107.00 level.

Kit Juckes, Chief Global FX Strategist at Société Générale, analyzes EUR/USD and USD/JPY outlooks on three scenarios

Hard, soft, or no landing at all?

The base case assumption, which assumes a mild US recession in the middle of next year, looks for 10-year Treasury yields to fall to 3.7% by the middle of next year.

USD/JPY could be just below 150 in mid-2024 on a US no landing, below 130 on a hard landing and just below 140 on our base case.

Our rates forecasts imply EUR/USD reaching 1.15 by mid-2024 on our base case for the economic outlook (mild recession), and 1.02 on the ‘no-recession’ forecast. A hard landing clouds the outlook because the initial reaction is for the relationship between EUR/USD and interest rates to break down, temporarily.

- Canada Unemployment Rate holds steady at 5.5% in September.

- Employment increases by 63,800, above expectations of 20,000.

- USD/CAD remains hovering around 1.3720, modestly higher for the day.

The Unemployment Rate in Canada held steady at 5.5% in September, Statistics Canada reported on Friday, better than the market consensus of a modest increase to 5.6%. Employment rose by 63,800 following an increase of 39,900 in August, and above expectations of 20,000.

"Employment growth in September was concentrated in part-time work, which rose by 48,000 (+1.3%). Since the beginning of the year, growth in part-time work (+1.9%) has outpaced growth in full-time work (+1.0%)," informed Statistics Canada.

Further details of the publication revealed that on a year-over-year basis, average hourly wages rose 5.0% in September, following an increase of 4.9% in August.

Market reaction

The USD/CAD rose after the release of employment reports in the US and Canada, and then pulled back toward 1.3730. While the Loonie outperformed after the data, it was offset by a stronger US Dollar on the back of US data.

- GBP/JPY climbs to near 182.00 as the impact of expectations of BoJ’s intervention starts fading.

- BoJ’s money market data cleared that Tuesday’s flash crash move was not the by-product of stealth intervention.

- GBP/JPY delivers a breakout of the Symmetrical Triangle chart pattern.

The GBP/JPY pair delivered a sharp upside move to near 182.00 in the London session. The asset picks strength as the market sentiment improves. The cross has extended its upside significantly after Tuesday’s ‘flash crash’, which resulted in a huge buying for the Japanese Yen.

Earlier, investors misunderstood the crack in the GBP/JPY pair as a stealth intervention by the Bank of Japan (BoJ) but the BoJ’s money market data showed that it was not the by-product of official intervention. This weakened the appeal for the Japanese Yen again as the BoJ is expected to maintain the expansionary policy stance for a longer period.

Meanwhile, the appeal for the Pound Sterling improves as Bank of England (BoE) Governor Andrew Bailey sees inflation easing to 5% or below by the year-end. If the BoE manages to do so, the promise made by the UK Prime Minister of halving the inflation to 5.2% by the end of 2023 would be fulfilled.

GBP/JPY delivers a breakout of the Symmetrical Triangle chart pattern on an hourly scale, which results in wider ticks and heavy volume. The 20-period Exponential Moving Average (EMA) around 181.40 will continue to provide support to the Pound Sterling bulls.

The Relative Strength Index (RSI) (14) shifts into the bullish range of 60.00-80.00, which indicates that the bullish impulse is already active.

A mean-reversion move to near October 3 high at 181.38 would be a buying opportunity for the market participants. This would drive the asset toward September 28 high at 182.43 followed by September 29 high around 183.00.

In an alternate scenario, a breakdown below October 4 low at 179.47 would expose the asset to October 3 low at 178.00.

GBP/JPY hourly chart

-638321918582509092.png)

The USD is mixed overall against the majors ahead of the US Nonfarm Payrolls report. Economists at Scotiabank analyze Greenack’s outlook.

Extended bull run appears vulnerable

Price action is endangering the bullish run in the DXY that has so far secured eleven, consecutive weekly gains. Double-digit runs like this are rare and it is even rarer for the run of net gains to extend much further. As things stand, the weekly pattern of price action is shaping up bearishly, forming a potential ‘shooting star’ candle pattern which might call time on the trend higher.

If there is anything that is going to stop the USD from notching up a twelfth, consecutive weekly gain, it might well be overblown job expectations.

With a long weekend ahead in North America, trade might fizzle out pretty quickly unless the number produces a major surprise.

EUR/USD grinds higher through mid-1.05s. Economists at Scotiabank analyze the pair’s outlook.

Price moves continue to lean bullish

Price moves continue to lean bullish after the EUR developed a ‘morning star’ reversal pattern through mid-week.

Solid EUR gains on Thursday serve as ‘confirmation’ of the reversal but there is clearly a lot of work ahead for the EUR to build on this development.

Last Friday’s high at 1.0617 is the key, short-term barrier for the EUR to clear if gains are to develop a little more towards 1.0650/1.0750.

Support is 1.0530.

USD/CAD has rallied on the back of USD strength and the spike in US treasury yields. Economists at Société Générale analyze the pair’s outlook.

Prevalence of upward momentum

Daily MACD remains anchored within positive territory denoting prevalence of upward momentum.

Defence of the 50-DMA near 1.3510 could lead to persistence in up move.

The pair has faced interim hurdle at 1.3770, the 76.4% retracement from 2022. Beyond 1.3770, next potential objectives are located at 1.3860 and 2022 high of 1.3980.

See: USD/CAD to slip a little more obviously on losses through 1.3695 – Scotiabank

GBP/USD regains 1.22. Economists at Scotiabank analyze the pair’s outlook.

Technical rebound gathers momentum

Sterling’s solid rebound from its mid-week low via a big, bullish key reversal/outside range signal has extended a little further to reach the low 1.22s.

Late day gains on Thursday through 1.2175/80 added to the GBP’s bullish credentials on the short-term charts and supported the case for some additional progress in the near term towards the 1.23 level.

Support is 1.2185/1.2195.

See – GBP/USD: 1.20 remains a real possibility – ING

- The Greenback holds on to weekly gains despite a three-day losing streak.

- Traders are front running expectations of a weaker US Dollar after the US jobs report as rumours point to a disappointing print.

- US Dollar Index retreats but could still eke out twelfth week of gains.

The US Dollar (USD) sees traders bracing for that final moment that has been keeping every trading desk on edge throughout the week. The monthly US jobs report is due this Friday and will finally confirm or contradict what earlier numbers this week have been suggesting: the US economy and its job market are starting to slow down. There is a very fine nuance here between slowing down instead of contracting: expectations are that numbers will still be positive, pointing to economic growth, though in a less convincing way than previous months.

Expect to see nearly every asset class being locked until 12:30 GMT when the US Nonfarm Payrolls (NFP) report will be released. Markets have already punished the Greenback throughout the week with a less than expected Institute of Supply Management’s (ISM) Purchasing Managers Index (PMI) print for the Service sector and a miss on expectations for the ADP jobs number. The last few trading hours will be crucial to see if the US Dollar Index (DXY) can still eke out that twelfth week of gains. The US jobs number could just as easily supply more Greenback weakness and end the DXY winning streak.

Daily digest: US Dollar under pressure

- The entire market is focused on 12:30 GMT. Nonfarm Payrolls for September are expected to head from 187,000 to 170,000. The Average Hourly Earnings monthly print is expected to marginally tick up from 0.2% to 0.3%. The US Unemployment Rate is expected to head from 3.8% to 3.7%.

- The Change in Nonfarm Payrolls has an estimation range from 90,000 to 250,000. So to have a firm market moving number, it either needs to be firmly below 90,000 or higher than 250,000. Everything within the range could mean that market movements remain short-lived and retract just hours after the initial move occurs.

- Equities are near flat with only Hong Kong’s Hang Seng index up over 1.5%. All other indices and futures are less than 0.5% in the green or red.

- The CME Group FedWatch Tool shows that markets are pricing in a 81.5% chance that the Federal Reserve will keep interest rates unchanged at its meeting in November. The combination of economic numbers this week has erased nearly every probability of another hike.

- The benchmark 10-year US Treasury yield is trading near 4.74% and is off this week’s high from 4.88%.

US Dollar Index technical analysis: End of the line with NFP

The US Dollar sees its engine stuttering: the US economy is starting to show some signs of less growth. In the past week, traders have punished the Greenback three days in a row on disappointing ISM PMI numbers, lower than expected ADP job numbers and rumours that the US Jobs report this Friday might be a big miss. The US Dollar Index is still clinging on to its twelfth straight weekly gain, though any substantial miss in this Friday’s NFP reading might mean the end of the line for the DXY rally.

The US Dollar Index opened around 106.33, though the overheated Relative Strength Index (RSI) is acting as a cap as it trades into an overbought region. With 107.19 – the high of November 30, 2022 – tested on Wednesday, it will be important to see if DXY can get a daily close above that level. If that is the case, 109.30 is the next level to watch.

On the downside, the recent resistance at 105.88 should be seen as first support. Still, that barrier has just been broken to the upside, so it isn’t likely to be strong. Instead, look for 105.12 to do the trick and keep the DXY above 105.00.

Nonfarm Payrolls FAQs

What are Nonfarm Payrolls?

Nonfarm Payrolls (NFP) are part of the US Bureau of Labor Statistics monthly jobs report. The Nonfarm Payrolls component specifically measures the change in the number of people employed in the US during the previous month, excluding the farming industry.

How does Nonfarm Payrolls influence the Federal Reserve monetary policy decisions?

The Nonfarm Payrolls figure can influence the decisions of the Federal Reserve by providing a measure of how successfully the Fed is meeting its mandate of fostering full employment and 2% inflation.

A relatively high NFP figure means more people are in employment, earning more money and therefore probably spending more. A relatively low Nonfarm Payrolls’ result, on the either hand, could mean people are struggling to find work.

The Fed will typically raise interest rates to combat high inflation triggered by low unemployment, and lower them to stimulate a stagnant labor market.

How does Nonfarm Payrolls affect the US Dollar?

Nonfarm Payrolls generally have a positive correlation with the US Dollar. This means when payrolls’ figures come out higher-than-expected the USD tends to rally and vice versa when they are lower.

NFPs influence the US Dollar by virtue of their impact on inflation, monetary policy expectations and interest rates. A higher NFP usually means the Federal Reserve will be more tight in its monetary policy, supporting the USD.

How does Nonfarm Payrolls affect Gold?

Nonfarm Payrolls are generally negatively-correlated with the price of Gold. This means a higher-than-expected payrolls’ figure will have a depressing effect on the Gold price and vice versa.

Higher NFP generally has a positive effect on the value of the USD, and like most major commodities Gold is priced in US Dollars. If the USD gains in value, therefore, it requires less Dollars to buy an ounce of Gold.

Also, higher interest rates (typically helped higher NFPs) also lessen the attractiveness of Gold as an investment compared to staying in cash, where the money will at least earn interest.

Sometimes Nonfarm Payrolls trigger an opposite reaction than what the market expects. Why is that?

Nonfarm Payrolls is only one component within a bigger jobs report and it can be overshadowed by the other components.

At times, when NFP come out higher-than-forecast, but the Average Weekly Earnings is lower than expected, the market has ignored the potentially inflationary effect of the headline result and interpreted the fall in earnings as deflationary.

The Participation Rate and the Average Weekly Hours components can also influence the market reaction, but only in seldom events like the “Great Resignation” or the Global Financial Crisis.

- EUR/JPY regains the upside and surpasses 157.00.

- The ongoing consolidation is expected to persist near term.

EUR/JPY quickly leaves behind Thursday’s inconclusive price action and resumes the upside bias beyond the 157.00 barrier at the end of the week.

In the meantime, the cross remains stuck within the consolidative range and the breakout of it exposes a visit to the so far monthly high of 158.65 (September 13) prior to the 2023 top at 159.76 (August 30), which precedes the key round level at 160.00.

On the downside, the so far monthly low of 154.34 (October 3) emerges as the initial contention in case of bearish attempts.

So far, the longer term positive outlook for the cross appears favoured while above the 200-day SMA, today at 149.81.

EUR/JPY daily chart

All eyes are on the US Nonfarm Payrolls report. Economists at MUFG Bank discuss how employment data could impact yields and the Dollar.

An in-line print could allow the Dollar to adjust a little further weaker

If today’s NFP data was to reveal an acceleration in payrolls it would certainly push further back the expectations on the timing of a downturn, reinforce the ‘higher for longer’ mantra and fuel renewed UST bond selling and Dollar buying.

An in-line print may be greeted with some relief that extends the correction in yields a little further lower from here which would allow the Dollar to adjust a little further weaker too.

The Fed’s Summary of Economic Projections in September revealed expectations of the labour market being stronger (unemployment rate revised down from 4.1% to 3.8% for Q4 2023 – the current level) which means any disappointment in the data like another jump in the unemployment rate has the potential to influence rate expectations that bit more.

See – NFP Preview: Forecasts from seven major banks, losing momentum

USD/CAD trades sideways around 1.3700. Economists at Scotiabank analyze the pair’s technical outlook.

Resistance is 1.3785

The USD’s push through resistance in the low 1.37 area earlier this week has not stuck, giving the impression of a ‘false break’ but the USD’s retreat has not yet been significant enough to ease upward pressure on funds more clearly from a technical point of view.

Intraday losses through 1.3695 should see the USD slip a little more obviously but perhaps only to 1.3600/1.3650 in the short run.

Resistance is 1.3785.

Markets are twiddling their thumbs ahead of the US labour market data. Kit Juckes, Chief Global, FX Strategist at Société Générale, analyzes the outlook for bonds and the Dollar.

Hard, soft, or no landing at all?

The ADP report, which barely correlates at all with the official data on a month-to-month basis, came in weak and that may mean the soft consensus is a little lower than the 160K NFP increase that forecasters are looking for.

I have a bias to think it could be a bad day for bonds, with US politics, debt supply, and strong payrolls all potentially supporting the Dollar as we look ahead to next week’s auctions and CPI data; but I’m biased because I’ve caught, and a cold and it’s darkened my mood!

See – NFP Preview: Forecasts from seven major banks, losing momentum

USD/JPY is trading near 149. Economists at MUFG Bank analyze the pair’s outlook ahead of the US Nonfarm Payrolls report.

USD/JPY to see a clear break higher well through 150.00 before the MoF intervenes

One of the key measures monitored by the BoJ that we track – contractual pay for full-time employees (so ex-bonus and ex-overtime) – slowed from 2.0% to 1.5%, the weakest reading since April. Given that wages will be such a key determinant in assessing whether price stability has been achieved, this data certainly lowers the probability of any near-term surprise removal of NIRP or another change in YCC.

It seems therefore more likely that we will see USD/JPY grind higher and retest that level just above the 150 mark that prompted a sharp reversal. That of course could come as soon as this afternoon if the US jobs report was to prove stronger-than-expected.

We’d still expect a clearer break higher well through 150.00 before the MoF would intervene.

See – NFP Preview: Forecasts from seven major banks, losing momentum

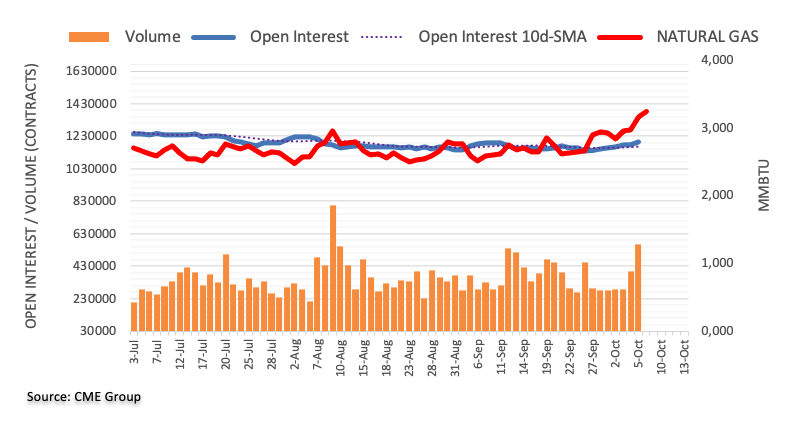

- Natural Gas prices jump to $3.404.

- The US Dollar trades directionless ahead of the US jobs report.

- US Natural Gas prices could head higher on the possibility of a cold front coming in sooner than expected.

Natural Gas prices are increasing to new year-to-date highs as Australian union workers are discussing the possibility to resume strikes. The resurge in strike risk comes after Chevron reneged earlier commitments on pay and conditions to workers. Expectations are that at the earliest Monday, a notice will be given that in seven days industrial action will take place, again risking a 10% supply shortage in the LNG market in the near term.

Meanwhile, the US Dollar (USD) sees traders bracing for the datapoint that has been keeping every trading desk on edge throughout the week. The monthly US jobs report is due later on Friday and will finally confirm or contradict what earlier numbers this week have been suggesting: the US economy and its job market are starting to slow down. There is a very fine nuance between slowing down instead of contracting.Expectations are that the US economy will continue to add jobs, pointing to economic growth, though in a less convincing way than previous months.

Natural Gas is trading at $3.4040 per MMBtu at the time of writing.

Natural Gas news and market movers

- Chevron appears to be backtracking on earlier commitments given to LNG union workers in order to resolve the strikes that took place at the beginning of September.

- On Thursday, workers discussed and endorsed restarting strike actions.

- Expectations are that at the earliest, the legal binding seven-day notice will be delivered by Monday, which means strikes will start in roughly ten days' time.

- Ports in Wheatstone and Gorgon account for nearly 10% of the world’s supply in LNG.

- Shell reported that its earnings from gas trading have rebounded in the third quarter.

- Pakistan is open to sign a long-term liquefied natural gas purchase agreement to make up for an expected shortfall in domestic fuel production.

Natural Gas Technical Analysis: dreaming of $4

Natural Gas peaks to a new year-to-date high with $3.4080 as a new level to pencil in the books. The move comes after Australian union workers are considering going back to strike as Chevron is backtracking on earlier concessions in order to resolve the stalemate between the Union and the energy company. With market supply facing the possibility of a short squeeze of near 10% in the near term, together with a substantial drop in temperature forecasted for Europe in the coming weeks, Natural Gas prices could reach $4.

With the firm peak and breakthrough out of the trend channel on Thursday, it will be crucial going forward that the upper band of that same trend channel acts as support. There aren’t any significant resistance levels except for $3.65, the peak of January 17. From there, the high of 2023 near $4.3080 comes into play as the next level on the upside.

On the downside, the trend channel needs to act as support now, near $3.30. In case that breaks down again, Natural gas prices could sink lower to $.3.07, with that orange line identified from the double top around mid-August. Should the drop become a broader sell-off, prices could sink below $3 towards $2.85, near the 55-day Simple Moving Average.

-638321801805314848.png)

XNG/USD (Daily Chart)

Natural Gas FAQs

What fundamental factors drive the price of Natural Gas?

Supply and demand dynamics are a key factor influencing Natural Gas prices, and are themselves influenced by global economic growth, industrial activity, population growth, production levels, and inventories. The weather impacts Natural Gas prices because more Gas is used during cold winters and hot summers for heating and cooling. Competition from other energy sources impacts prices as consumers may switch to cheaper sources. Geopolitical events are factors as exemplified by the war in Ukraine. Government policies relating to extraction, transportation, and environmental issues also impact prices.

What are the main macroeconomic releases that impact on Natural Gas Prices?

The main economic release influencing Natural Gas prices is the weekly inventory bulletin from the Energy Information Administration (EIA), a US government agency that produces US gas market data. The EIA Gas bulletin usually comes out on Thursday at 14:30 GMT, a day after the EIA publishes its weekly Oil bulletin. Economic data from large consumers of Natural Gas can impact supply and demand, the largest of which include China, Germany and Japan. Natural Gas is primarily priced and traded in US Dollars, thus economic releases impacting the US Dollar are also factors.

How does the US Dollar influence Natural Gas prices?

The US Dollar is the world’s reserve currency and most commodities, including Natural Gas are priced and traded on international markets in US Dollars. As such, the value of the US Dollar is a factor in the price of Natural Gas, because if the Dollar strengthens it means less Dollars are required to buy the same volume of Gas (the price falls), and vice versa if USD strengthens.