- Аналітика

- Новини та інструменти

- Новини ринків

Новини ринків

- AUD/USD steadies after snapping four-day uptrend, holding lower ground of late.

- China housing jitters, rush to buy Hong Kong insurance and Sino-American tussles weigh on Aussie pair due to Canberra-Beijing ties.

- Hawkish FOMC Minutes supersede mixed comments from NY Fed President Williams, softer US data.

- RBA’s hawkish halt may tease AUD/USD buyers if US ADP Employment Change, ISM Services PMI disappoint.

AUD/USD licks its wounds around mid-0.6600s amid a sluggish start to Thursday’s Asian session, after posting the first daily loss in five. In doing so, the Aussie pair portrays the cautious mood ahead of Australian trade numbers for May, as well as recently mixed catalysts surrounding the Fed. Even so, pessimism about Canberra’s biggest customer Beijing, as well as broad recession woes, keeps the risk-barometer pair depressed.

A jump in Chinese investor buying Hong Kong and Macau wealth products join pessimism about China’s top-tier housing players like Shimao Group, as well as the government-backed Sino-Ocean Group, to amplify economic fears about the world’s biggest industrial player China.

The same joins the ongoing Sino-American tension and softer China data to exert additional downside pressure on the AUD/USD price. On Wednesday, downbeat prints of China’s Caixin Services PMI for June, to 53.9 versus 57.1 prior, joined the escalating fears of the US-China tension amid fresh warnings of further trade restrictions from Beijing to weigh on the sentiment and prices of the riskier assets like AUD/USD.

That said, China’s Global Times and former Vice Commerce Minister flagged hardships for the US IT companies, as well as metal players. Earlier on Wednesday, China announced abrupt controls on exports of some gallium and germanium products, effective from August 1. The dragon nation’s latest retaliation is in reaction to the US curb on AI chips’ shipments to Beijing.

It should be noted that the Federal Open Market Committee (FOMC) Minutes for the June meeting stated that almost all members agreed to a pause in the rate hike trajectory while some policymakers showed an inclination for a July rate hike of around 0.25%. The same highlights hawkish bias at the US central bank, versus the Reserve Bank of Australia’s (RBA) pause in the rate hike, to weigh on the Aussie pair.

Even so, softer US data and fears of recession, as signaled by the US Treasury bond yields curve inversion, put a floor under the AUD/USD. That said, US Factory Orders reprints 0.3% MoM growth for May versus 0.8% expected. The official publication also mentioned that the new orders for manufactured durable goods in May rose for the third consecutive month. Earlier in the week, the US ISM Manufacturing PMI and S&P Manufacturing PMI came in softer and propelled the Gold Price.

While portraying the mood, the markets almost priced in the June Fed rate hike by 0.25% and weighed on the Gold Price while the Wall Street benchmarks closed in the red and the US Treasury bond yields joined the US Dollar Index (DXY) to rise.

Moving on, Australia’s Imports, Exports and Trade Balance for May will be the immediate catalyst to watch for the AUD/USD pair traders. Following that, the US ISM Services PMI and ADP Employment Change for June will be crucial as both of them will help determine Friday’s all-important Nonfarm Payrolls (NFP) and affect the AUD/USD prices. Above all, the risk catalysts, namely China headlines and recession woes, will be crucial to watch for clear directions.

Technical analysis

A clear U-turn from the 200-DMA, around 0.6700 by the press time, directs AUD/USD sellers toward a six-week-old rising support line, close to 0.6630 at the latest.

- EUR/USD remains depressed at the lowest level in a week after breaking the key DMA support.

- Bearish MACD signals, steady RSI line add strength to downside bias.

- Convergence of 100-DMA, fortnight-old descending trend line appears short-term key support.

- Euro bulls should remain cautious below two-week-long resistance line.

EUR/USD holds lower grounds at the weekly bottom surrounding 1.0850 amid the early hours of Thursday in Asia. In doing so, the Euro pair justifies the previous day’s closing beneath the 50-DMA, the first clear break in three weeks, while also keeping the bears on the table after a three-day downtrend.

Not only the 50-DMA break but the bearish MACD signals and a near-50.0 RSI (14) line also suggests further downside of the EUR/USD pair.

However, a convergence of the 100-DMA and a fortnight-old descending trend line, around 1.0825 by the press time, becomes a tough nut to crack for the Euro bears.

Following that, an ascending support line from May 31, near 1.0800, becomes the last defense of the EUR/USD buyers before directing the quote toward the 50% and 61.8% Fibonacci retracements of January-April upside, respectively near 1.0790 and 1.0715.

Alternatively, the 50-DMA and 38.2% Fibonacci retracement together guard the EUR/USD recovery around 1.0865.

Even if the major currency pair crosses the 1.0865 hurdle, a downward-sloping resistance line from June 23, close to 1.0900 at the latest, will be in the spotlight.

Overall, EUR/USD remains on the back foot but the downside room appears limited.

EUR/USD: Daily chart

Trend: Limited downside expected

Federal Reserve (Fed) Bank of New York President, as well as Vice Fed Chair, John Williams crossed wires via Reuters late Wednesday when he unveiled support for slowing down on the rate hike trajectory. The policymaker also showed his data dependency for future Fed decisions.

The voting member of the Federal Open Market Committee (FOMC) also unveiled his support for no rate change in June monetary policy meeting but marked surprise from the stable natural rate level.

It should be noted that the Fed Vice Chair Williams quoted remarkably “well-anchored” inflation expectations but cited that fate of inflation is up to the Fed.

Even so, Fed’s Williams marked the need for the US central bank to balance the demand and supply flow, indirectly suggesting higher rates ahead.

Key statements

I’m not content with where inflation is right now.

I see progress on inflation but price pressures still too high.

Economy still has strong demand for labor.

FX implications

Being the statements from one of the key Fed members, the markets reacted to the mostly hawkish comments by supporting the US Dollar, in hopes of higher rates from the US central bank. The same joins the upbeat FOMC Minutes to weigh on the EUR/USD, pressured at a weekly low of around 1.0850.

Also read: EUR/USD bears move closer to the edge of the abyss after FOMC minutes and ahead of a slew of key US data

- GBP/USD bounces off 200-HMA to pare Wednesday’s losses, lacks clear directions of late.

- UK/US PMIs, US ADP Employment Change decorate the calendar.

- Steady RSI, sluggish MACD signals keep Cable buyers on the table.

- Three-week-long horizontal region appears strong upside hurdle; Pound Sterling bears aim for 1.2660 after 200-HMA break.

GBP/USD picks up bids to reverse the latest daily losses while defending the 1.2700 round figure as it prints the 1.2705 mark amid the early hours of Thursday’s Asian session. In doing so, the Cable pair bounces off the 200-Hour Moving Average (HMA).

Also read: GBP/USD drops below 1.2700 post FOMC minutes release

It’s worth noting that the Pound Sterling’s latest rebound from the key moving average justifies the steady RSI (14) line, as well as sluggish MACD, which in turn suggests the pair’s another attempt to cross a downward-sloping resistance line from June 27, at 1.2735 by the press time.

Following that, the 61.8% Fibonacci retracement of June 16-29 fall, at 1.2750, can challenge the Cable buyers before directing them to a three-week-old horizontal resistance area surrounding 1.2805-10.

In a case where the GBP/USD price remains firmer past 1.2810, the odds of witnessing a tough fight to cross the previous monthly high of around 1.2850, which is also the yearly peak, can’t be ruled out.

On the flip side, a clear break of the 200-HMA level of 1.2690 can quickly fetch the Cable pair towards the late June swing high of around 1.2660. However, the June 29 bottom surrounding 1.2590 can challenge the GBP/USD bears afterward.

Should the Pound Sterling bears smash the 1.2590 level, they will aim for the previous monthly low of 1.2368.

GBP/USD: Hourly chart

Trend: Limited recovery expected

- BoJ intervention prospects raise prospects for a bearish correction in USD/JPY.

- USD/JPY bears are lurking at resistance and eye a significant correction.

USD/JPY edged higher on Wednesday with the US Dollar finding support ahead of a slew of key US events that included Wednesday's hawkish Federal Open Market Committee minutes that reinforced market expectations of another interest rate hike at the end of July.

Most Fed officials expected that the policymakers would eventually need to tighten policy further.

As a consequence, the US Treasury yields moved higher and added to earlier gains in the Greenback. ''Fed funds futures showed expectations of a 25 basis point hike at the end of a two-day policy meeting on July 26 rose to 88.7%, according to CME Group's FedWatch Tool,'' Reuters reported.

Indeed, USD/JPY has broadly moved higher in sync with the US 10-year Treasury yield. However, the market is also paying attention to the potential risk of intervention from the Bank of Japan. This opens the risk of a move lower in USD/JPY and the following illustrates a bearish technical scenario.

USD/JPY monthly chart

The monthly W-formation is compelling. This is a reversion pattern and if there is resistance here, then there is the possibility of a retracement back to the neckline that meets the 61.8% Fibonacci near 134 the figure.

USD/JPY weekly charts

On a weekly chart, this might play out as follows, allowing for the ebbs and flows on the way down as bears take on the dynamic trendline support towards 140.50 and 50 pips below the weekly 61.8% ratio near 141.50

(Overall bearish trajectory bias, resistance and support levels).

USD/JPY bullish weekly outlook

However, while on the front side of the trendline, the bulls are in charge and that leaves 145.10 and space to 152.00 technically up for grabs.

- Gold Price drops back towards multi-month-old horizontal support amid risk-off mood.

- Sour sentiment, hawkish Federal Reserve Minutes propel US Dollar and weigh on XAU/USD.

- United States ADP Employment Change, ISM Services PMI eyed for clear directions.

Gold Price (XAU/USD) remains pressured around $1,915 amid early Thursday morning in Asia, after fading the four-day uptrend, reversing from 21-DMA. In doing so, the XAU/USD not only braces for the key horizontal support but also takes clues from China concerns, as well as hawkish expectations from the Federal Reserve (Fed). That said, the XAU/USD pullback ignores softer United States data while tracing upbeat US Treasury bond yields.

Gold Price retreats amid China, Federal Reserve concerns

Gold Price bears the burden of China-inflicted fears while posting the first daily loss in five. That said, China’s top-tier housing players like Shimao Group, as well as the government-backed Sino-Ocean Group, feel the heat of the first fall in housing sales after four-month advances. Further, the headlines surrounding the US-China ties and fresh trade sanctions, as well as the downbeat Chinese PMIs, weigh on the risk appetite and the XAU/USD price.

On Wednesday, downbeat prints of China’s Caixin Services PMI for June, to 53.9 versus 57.1 prior, joined the escalating fears of the US-China tension amid fresh warnings of further trade restrictions from Beijing to weigh on the sentiment and prices of the riskier assets.

That said, China’s Global Times and former Vice Commerce Minister flagged hardships for the US IT companies, as well as metal players. Earlier on Wednesday, China announced abrupt controls on exports of some gallium and germanium products, effective from August 1. The dragon nation’s latest retaliation is in reaction to the US curb on AI chips’ shipments to Beijing.

Elsewhere, the Federal Open Market Committee (FOMC) Minutes for the June meeting stated that almost all members agreed to a pause in the rate hike trajectory while some policymakers showed an inclination for a July rate hike of around 0.25%. The Fed members also noted a reduction in bank stress, improvement in economic conditions and substantial improvement in bond issuance.

Talking about the data, US Factory Orders reprints 0.3% MoM growth for May versus 0.8% expected. The official publication also mentioned that the new orders for manufactured durable goods in May rose for the third consecutive month. Earlier in the week, the US ISM Manufacturing PMI and S&P Manufacturing PMI came in softer and propelled the Gold Price.

Amid these plays, the markets almost priced in the June Fed rate hike by 0.25% and weighed on the Gold Price while the Wall Street benchmarks closed in the red and the US Treasury bond yields, as well as the US Dollar Index (DXY) rose.

Looking ahead, the risk catalysts will be crucial to watch for clear directions of the Gold Price. Among them, China headlines and recession woes will be in the spotlight. Additionally, the US ISM Services PMI and ADP Employment Change for June will be crucial as both of them will help determine Friday’s all-important Nonfarm Payrolls (NFP) and affect the XAU/USD prices.

Gold Price Technical analysis

Gold Price retreats from the 21-DMA, around $1,934 by the press time, to pare the first weekly gain in four.

Adding strength to the pullback move are the sluggish signals from the Moving Average Convergence and Divergence (MACD) indicator, as well as the below-50 conditions of the Relative Strength Index (RSI), placed at 14.

With this, the XAU/USD appears well-set to prod the $1,900 round figure but a six-month-old horizontal area, around $1,890-85, appears a tough nut to crack for the Gold bears.

In a case where the Gold Price drops below $1,985, the 200-DMA support of around $1,863 and early March swing high near $1,858 may act as the final defenses of the buyers.

On the contrary, a daily closing beyond the 21-DMA hurdle of $1,934 isn’t an open ticket to the Gold buyers as a downward-sloping resistance line from June 02, close to $1,945 at the latest, can challenge the XAU/USD upside.

Even if the Gold Price crosses the $1,945 hurdle, bulls need to remain cautious below the previous monthly high of around $1,985.

Overall, the Gold price is likely to witness a short-term downside ahead of the top-tier United States data.

Gold Price: Daily chart

Trend: Limited downside expected

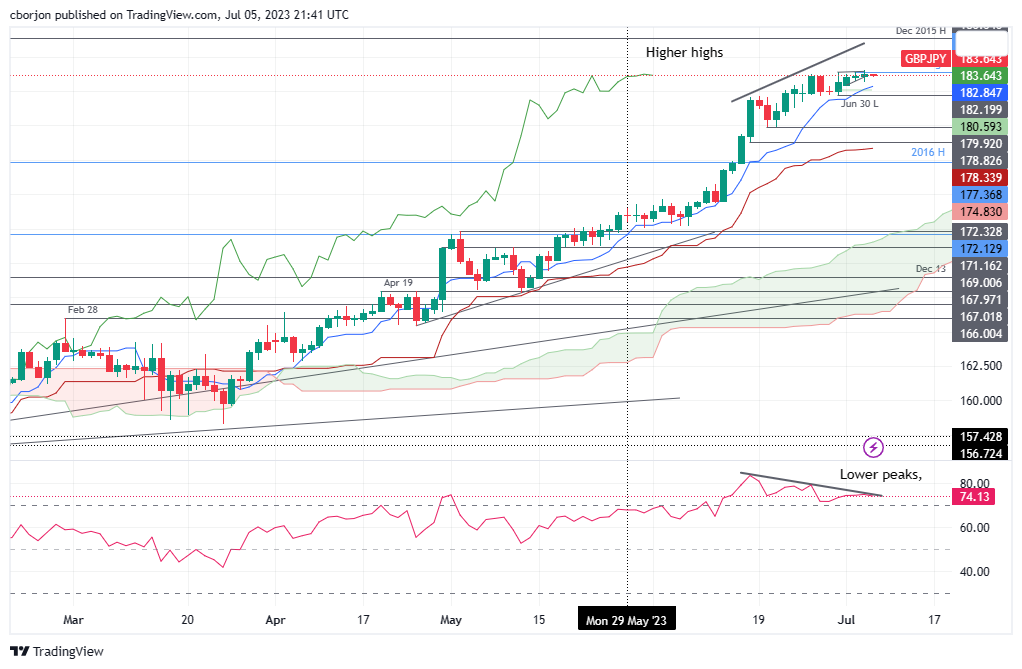

- GBP/JPY wavers around 184.00, with intervention from Japanese authorities limiting a further upward push.

- Negative divergence in the Relative Strength Index (RSI) indicates potential downward movement for the GBP/JPY.

- Key support and resistance levels lie in wait, with an immediate downside target at 183.00 and an upside potential at 185.00.

GBP/JPY begins the Asian session on a lower note. The GBP/JPY finished Wednesday's session extending its gains to four straight days but failed to decisively break stubborn resistance at 184.00, near the year-to-date (YTD) high. At the time of writing, the GBP/JPY is trading at 183.70, losses a minuscule 0.01%.

GBP/JPY Price Analysis: Technical outlook

The GBP/JPY uptrend remains capped at around the 184.00 figure. Japanese authorities' language intervention in the Forex markets keeps the Japanese Yen (JPY) from weakening, putting a lid on GBP/JPY buyers' attempt to crack 184.00. As the GBP/JPY reaches a higher-high, the Relative Strength Index (RSI) prints lower peaks, suggesting a negative divergence formed, suggesting further GBP/JPY downside is expected.

Nevertheless, the GBP/JPY must drop below 183.00, so it can expose the Tenkan-Sen line at 182.84. A breach of the latter will expose the June 30 daily low at 182.19, followed by the 182.00 figure. Once broken, the GBP/JPY next support would be the Senkou Span A, at 180.59.

Conversely, a rally above the year-to-date (YTD) high of 184.01 would expose the 185.00 figure, followed by the December 2015 daily high at 186.34.

GBP/JPY Price Action – Daily chart

- The USD/CAD jumped above the 20-day SMA for the first time since early June to 1.3285.

- Rising yields following hawkish FOMC minutes benefitted the USD.

- Rising Oil prices to limit falling CAD losses.

Following the release of hawkish FOMC minutes, the USD/CAD pair surged above the 20-day simple moving average (SMA), reaching 1.3285. The increase in yields, driven by members of the Committee supporting a 25 bps hike in the June meeting, favoured the US Dollar, contributing to the pair's upward momentum. However, the West Texas Intermediate Crude Oil (WTI) is seeing more than 1% gains on the day and limits the CAD’s downside potential.

Based on the minutes of the FOMC meeting in June, it was revealed that while some members of the Committee supported a 25 basis point increase despite agreeing to pause the hike temporarily. These members were concerned that tightening the labour market could lead to inflationary pressures. Therefore, they decided to pause and assess the impact of monetary policy on the US economy before making any further decisions. The Committee also reached a consensus to maintain rates in a restrictive stance.

Following this development, there was a general increase in US yields. Specifically, the 2-year yield rose to 4.95%, a 0.78% increase, while the rates for the 5-year and 10-year bonds reached 4.24% and 3.93%, rising by 1.81% and 1.90%, respectively.

Regarding the next Federal Reserve (Fed) meeting in July, markets anticipate a 25 basis points hike. However, investors await crucial labour market data for the US from June on Thursday. The employment figures, to be released by the ADP Research Institute on Thursday, are expected to be around 228k, indicating a deceleration from the previous figure of 278k. Additionally, the US Department of Labor Jobless Claims is projected to rise to 245k on a weekly basis.

USD/CAD levels to watch

On the daily chart, the USD/CAD appears neutral to bullish in the short term. Despite standing in negative territory, the Relative Strength Index (RSI) and the Moving Average Convergence Divergence (MACD) are gaining momentum, suggesting that the buyers are gearing up for another upwards leg.

Support Levels to watch: 1.2345 (20-day Simple Moving Average), 1.2320, 1.3190.

Resistance Levels to watch: 1.3300, 1.3320, 1.3350.

USD/CAD Daily chart

- AUD/USD are moving in and testing the bull's commitments in key weekly support area.

- Bears eye a break towards the 0.6640s while below 0.6670 near term.

AUD/USD is lower on the day, down some 0.57% at the time of writing after falling from a high of 0.6698 to a low of 0.6652. The currency has been better offered following the Reserve Bank of Australia which kept interest rates at 4.10%. Markets, however, expect that September will most likely be the timing for the next rate increase, and this has been reflected in the price over the last weeks.

Meanwhile, from a technical perspective, AUD/USD bulls have moved aside and the bears are taking control into a key support area on the charts as the following multi-time-frame analysis will illustrate

AUD/USD weekly charts

Zoomed in, we can see that the price broke a key 0.6710 resistance to recently form a fresh daily high which has changed the bearish character to bullish after a sweep of stops below the prior 0.6450 channel support. If bulls commit in the area between the 50%, 61.8% and 78.6% ratios, the neckline of the bullish W-formation, then there are firm possibilities of a retest of the trendline resistance in the build-up to higher highs with eyes set on the 0.7150s.

AUD/USD daily chart

However, this current price action is bearish and risks a test of below 0.6640 and then 0.6600. A break there will leave 0.6537 vulnerable and then the swing low in the 0.6450s.

AUD/USD H1 chart

This leaves near-term prospects bearish while below the hourly resistance of the M-formation's neckline and resistance 0.6670 above as follows:

The 0.6640s are vulnerable for a test in the session ahead that guards a run to 0.6620 and in-the-money long positions below the weekly 61.8% Fibonacci ratio as drawn on thew weekly chart above.

- WTI surged 1.28%, buoyed by high US crude exports and OPEC+’s commitment to output cuts.

- Extension of production cuts into August is expected to tighten the oil market further, analysts report.

- Potential rate hikes by the Federal Reserve and global economic slowdown threaten the upward momentum.

Western Texas Intermediate (WTI), the US crude oil benchmark, rose on Wednesday after Tuesday’s holiday in the United States (US), keeping prices almost unchanged due to thin volumes amidst US traders’ absence. Hence, WTI is trading at $71.86 per barrel, up by 1.28%, after hitting a daily low of $70.40.

WTI surges on supply tightening measures, but macro-economic factors cast a shadow

Government data revealed that US crude shipments for the week ending June 23 finished at or near record highs with a daily volume of 5.338 million barrels. The week before was 4.543 million, being the June 16 week, while for the week ended June 9, exports were at 3.27 million daily. Therefore, WTI exports have doubled over the last three weeks.

That keeps WTI underpinned, alongside crude oil output cuts by Saudi Arabia and Russia, which extended its 1 million and 500,000 barrels per day cut to August.

Analysts quoted by Reuters said, “The July voluntary cuts and the extension into August should considerably tighten the oil market, but investors will stay on the sidelines until oil inventories show substantial draws.”

The Organization of Petroleum Exporting Countries and its allies, known as OPEC+, gathered at an industry event on Wednesday and commented the cartel will keep its efforts to support a “stable and balanced oil market.”

In the meantime, a global economic slowdown, seen after the release of the Manufacturing and Services PMI, could cap WTI prices. That and higher interest rates in the United States (US) can keep US crude oil prices meandering around the $70.00 per barrel price after June’s Federal Reserve (Fed) meetings showed divisions amongst policy markets pausing on increasing interest rates. It should be noted that a July rate hike is almost certainly, which could boost the greenback, a headwind for US Dollar (USD) denominated commodities.

WTI Technical Levels

- NZD/USD failed to consolidate above the 100-day SMA at 0.6190 and retreated towards the 0.6180 zone.

- FOMC minutes revealed that some members wanted to hike by 25 bps in the last meeting.

- The USD gained interest on the back of hawkish bets on the Fed and rising US yields.

On Wednesday, the Kiwi failed to hold gains that took the NZD/USD pair above the 100-day Simple Moving Average (SMA) and turned south towards 0.6180. Following the minutes, US Treasury yields rose, benefiting the greenback while investors eagerly await labour market data.

US yields rise after hawkish FOMC minutes. Eyes on labour market data

According to the FOMC minutes from the latest June meeting, despite anonymously agreeing to pause, some members of the Committee supported the case of hiking by 25 basis points. In that sense, driven by a tight labour market, members worried that it might fuel inflationary pressures but considered pausing to assess the effects of monetary policy on the US economy. In addition, members agreed that it would be appropriate to maintain rates in a restrictive stance.

As a reaction, the US yields rallied across the board. The 2-year yield rose to 4.95% while the 5 and 10-year bond rates to 4.24% and 3.93%, respectively. As bond yields tend to favour the local currency's value, the USD gained interest.

That being said, the focus now turns to June's crucial US labour market data. On Thursday, the ADP Research Institute will release employment figures expected to come in at 228k and decelerate from its previous 278k and the US Department of Labor Jobless Claims is expected to accelerate to 245k on a weekly basis.

NZD/USD Levels to watch

According to the daily chart, the technical outlook for the NZD/USD has turned neutral for the short term as there is no clear dominance between buyers and sellers. In addition, the 20, 100 and 200-day SMA converge towards the 0.6200 area, awaiting a fundamental catalyst.

Support Levels to watch: 0.6170 (200-day SMA), 0.6160(20-day SMA), 0.6130.

Resistance Levels to watch: 0.6190 (100-day SMA), 0.6200, 0.6210.

NZD/USD Daily chart

Market participants will continue to digest the FOMC minutes and prepare for the upcoming economic reports about the US labor market. During the Asian session, Australia will report trade data, and later in Europe, Eurozone Retail Sales are due.

Here is what you need to know on Thursday, July 6:

US markets dropped moderately on Wednesday on the back of tensions between China and the US, as well as following reports of softer economic activity. The Chinese Caixin Services dropped more than expected, and Japanese, Australian, and Eurozone PMIs were revised lower. Additionally, US Factory Orders rose below expectations.

Data from the US on Wednesday showed an increase in Factory Orders in May of 0.3%, below the market consensus of 0.8%. On Thursday, the focus will turn to labor market data with the ADP private employment report, Jobless Claims, and JOLTS. These numbers will be followed on Friday by the Nonfarm Payrolls report. Also on Thursday, the ISM Services PMI is due.

The FOMC minutes of the June meeting, when the central bank skipped, showed no major surprises. Some members "favored" a 25 basis points rate hike. The message continues to be that members see more rate hikes ahead, and the markets are finally believing the Fed.

US yields rose, supporting the US Dollar. The 10-year yield climbed to 3.95%, the highest level since mid-March. The DXY rose for the third day, rising above 103.30 but remains under the critical level of 103.50. The short-term direction of the US Dollar will likely be US labor data dependent.

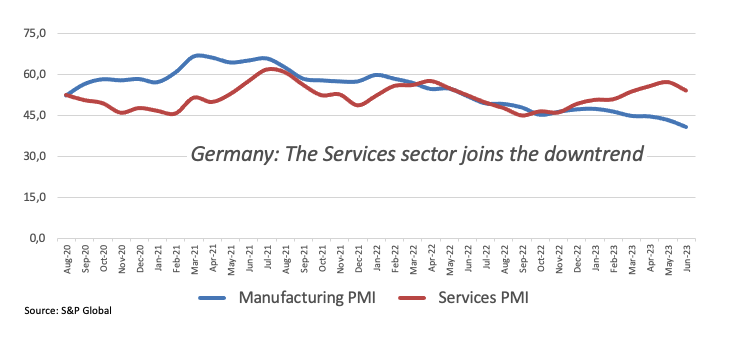

The final June Services PMI from the Eurozone was revised modestly lower, and also the Composite PMI, which dropped below 50 for the first time since December. The Eurozone Producer Price Index declined in May by more than expected, with a monthly slide of 1.9% and the annual rate falling from 0.9% to -1.5%. On Thursday, Germany will report Factory Orders, and Eurozone Retail Sales.

EUR/USD failed to retake 1.0900 and dropped toward 1.0850, as the Euro lagged and the Dollar outperformed. EUR/GBP fell to one-week lows under 0.8550. GBP/USD remained sideways around 1.2700, supported by the 20-day Simple Moving Average.

USD/JPY continued to move in the recent range around 144.50, with the focus on the 145.00 potential intervention level. Higher government bond yields and the divergence between the Bank of Japan and other central banks supports the uptrend.

NZD/USD dropped marginally after being unable to hold above 0.6200. The Kiwi outperformed among commodity currencies. AUD/USD ended a four-day positive streak after failing to retake 0.6700. The pair dropped to 0.6650, the day after the Reserve Bank of Australia (RBA) kept rates on hold. AUD/NZD fell for the fourth day in a row, reaching the weakest level since late May at 1.0760.

USD/CAD rose from 1.3220, approaching 1.3300, hitting the strongest level in two weeks. The Loonie failed to benefit from higher crude oil prices. The WTI barrel rose 1.25%, hitting weekly highs near $72.00.

Gold spiked to $1,935 but later reversed, falling below $1,920 and ending the day looking vulnerable. On the contrary, Silver rose 0.70% and finished above $23.00. Cryptocurrencies declined, with Bitcoin falling 1.05% to $30,465, and Ethereum dropping to $1,910.

Like this article? Help us with some feedback by answering this survey:

- USD/JPY jumped above 144.60 after hitting a daily low of 144.07 earlier in the session.

- Minutes from the June FOMC meeting revealed that most participants supported a 25 bps hike.

- Rising yields made the USD gain traction.

On Wednesday, the USD/JPY trades higher as the USD gains interest after the Federal Open Market Committee (FOMC) minutes from the June meeting revealed a hawkish stance from its members, with most supporting future rate hikes. In response, the shorter-term US Treasury bond yields rose as markets expect a more aggressive Federal Reserve (Fed) moving forward.

FOMC minutes from June’s meeting reveal a hawkish stance from members

Committee members support the case for hiking interest rates by 25 basis points in the future, according to the FOMC minutes from the latest June meeting – their view shapped predominantly by a tight labour market. The board's ultimate decision was to pause rate hikes, as Jerome Powell considered it necessary to first assess the effects of monetary policy so far on the US economy.

In addition, the minutes revealed that all participants agreed that maintaining a restrictive stance would be appropriate. It's worth noticing that the dot plots in the last monetary policy statement showed that most members see the terminal rate peaking at 5.50% this year, meaning that they foresee an additional 25 bps hike. As a reaction, the reassurance of an aggressive stance by the Fed members fueled the US bond yields, with the 2, 5 and 10-year yields showing gains of 0.50-2% following the release of the minutes.

That being said, investors will eye the release of ADP Employment change data on Thursday and Non-Farm Payrolls on Friday to continue modelling their expectations regarding the next Fed meeting.

USD/JPY Levels to watch

According to the daily chart, the technical outlook for the USD/JPY is bullish in the short term. However, indicators are losing steam, with the Relative Strengh Index (RSI) correcting overbought conditions and the Moving Average Convergence Divergence (MACD) printing decreasing green bars.

Support Levels to watch: 144.00, 143.70,143.30

Resistance Levels to watch: 144.90, 145.00 (psychological mark), 145.07 (June 30 high).

USD/JPY Daily chart

- EUR/USD is breaking down technically as we head into key US data events.

- FOMC minutes prop up the hawkish sentiment and the US Dollar.

EUR/USD fell by some 0.25% on Wednesday, weighed by a weaker-than-forecast eurozone PMI and PPI, risk-off tones surrounding China noise and by the Federal Open Market Committee minutes that have cemented the current hawkish sentiment.

The US Dollar has been climbing of late and jolted higher in late trade in New York ahead of more critical US data releases Thursday and Friday. Firstly, worries that trade frictions between China and the US could escalate kickstarted a move up in the Greenback this week. China made an abrupt announcement on Monday of controls from Aug. 1 on exports of some gallium and germanium products which has ramped up a trade war with the United States and could potentially cause more disruption to global supply chains. ''Analysts have described Monday's move as China's second - and bigger - countermeasure in the long-running US-China tech fight, coming after it banned some key domestic industries from purchasing from US memory chipmaker Micron (MU.O) in May,'' Reuters wrote on the matter.

Eurozone inflation expected to fall

Domestically, eurozone data disappointed and follows a mixed inflation report that was released at the end of June whereby the headline beat expectations, but while the data accelerated 5.5% in June it was lower than May’s 6.1% increase. The Core HICP inflation rose to 5.4% YoY in June, compared with May’s figure of 5.3%. But markets had forecasted a 5.5% clip. On Wednesday, the eurozone reported soft final June services and composite PMIs.:

Both headline services and composite PMIs fell four ticks from the preliminary to 52.0 and 49.9, respectively. ''This was the first sub-50 reading for the composite since December and confirms our view that the eurozone is slipping into recession,'' analysts at Brown Brothers Harriman explained.

''Looking at the country composite readings, Germany fell two ticks from the preliminary to 50.6 and France fell one tick to 47.2. Italy and Spain reported for the first time and their composites came in at 49.7 and 52.6, respectively. Both fell more than two full points from May. Italy has joined France below the key 50 boom-bust line and it’s only a matter of time before other nations do as well,'' the analysts added and explained that eurozone inflation expectations continue to fall:

''The monthly ECB survey showed inflation expectations for the next 12 months fell to 3.9% in May vs. 4.1% in April and 5.0% in March. For three years ahead, inflation expectations remained steady at 2.5% vs. 2.9% in March. The ECB will be happy to see the drop and should allow the doves to retain control of the narrative at the July 27 meeting''

Markets are expecting the ECB to hike 25bp two more times and World Interest Rate Probability, WIRP, suggests odds of a 25 bp hike are near 90% this month.

Hawkish FOMC minutes props up the US Dollar

Meanwhile, in the US, the Federal Open Market Committee (FOMC) released the minutes of its June meeting, triggering a rise in the Greenback. According to the document, some officials favoured a rate hike at the meeting but went along with a pause. The minutes showed a division among FOMC members. “Most participants observed that uncertainty about the outlook for the economy and inflation remained elevated and that additional information would be valuable for considering the appropriate stance of monetary policy”, the minutes noted.

More here: FOMC minutes: Some officials favoured a 25bps hike at the June meeting

Now, the focus is on the US jobs data where the nation will report on layoffs on Thursday, Jobless Claims, ISM Services and JOLTS ahead of Friday's Nonfarm Payrolls report. This slew of fresh data would be expected to overshadow today's FOMC minutes and offer clues as to the next move from the Fed where there is a possibility of two more hikes this year.

''US payrolls likely remained above-trend in June, but still representing slowing after ~300k expansions in Apr-May. We also look for the UE rate to drop a tenth to 3.6% and for wage growth to print 0.3% MoM,'' analysts at TD Securities said.

Other than this week's events, traders will then be looking ahead to next Wednesday's Consumer Price Index.

EUR/USD and US Dollar charts

The DXY index, as illustrated above, has seen a move higher on the FOMC minutes into an area of potential resistance. The Euro bulls will want to see the 103.30s support and trendlines break to the downside in the coming sessions which could help prop the Single Currency around the US data events:

On the other hand, EUR/USD is headed to the edge of the abyss around what could prove to be daily weak lows that guard a move below 1.0850 in a broken-down market that leaves the 1.07 area vulnerable for the days ahead.

- Gold prices take a hit, dropping below the 20-day EMA, after the Federal Reserve hints at a potential rate hike in July.

- The resurgent US Dollar and soaring Treasury bond yields further tighten the screws on the precious metal’s bullish momentum.

- Despite a unanimous decision for a June pause, officials’ concerns over a tight labor market point to a looming rate increase.

- Market expectations for July rate hikes remained high, with odds at 88.7%, according to the CME FedWatch Tool.

Gold price snaps three days of gains, tumble below the 20-day Exponential Moving Average (EMA), after the US Federal Reserve (Fed) release of June’s monetary policy meeting minutes, which were tilted hawkish, with officials worried about the tightness of the labor market. Although most officials agreed to a June pause, a July rate hike is almost inevitable. At the time of writing, the XAU/USD exchanges hands at $1916.80, down 0.44% after reaching a high of $1934.97

The greenback is staging a comeback, a headwind for Gold. The US Dollar Index (DXY) rises 0.29%, at around 103.370, while US Treasury bond yields are soaring, with the 10-year benchmark note rate at 3.945%, gaining eight and a half basis points (bps). Money market futures speculate the Fed will raise rates in July, with odds of a 25 bps rate hike at 88.7%, as shown by the CME FedWatch Tool.

Summary of the FOMC’s June meeting minutes

The minutes from the Federal Open Market Committee (FOMC) meeting revealed a unanimous agreement among all participants to maintain unchanged interest rates to assess the cumulative impact of previous tightening measures. However, some Fed officials advocated for a 25 basis point rate hike, citing the tightness of the labor market as their justification. Despite differing opinions on specific rate adjustments, all participants concurred on the necessity of maintaining a restrictive monetary policy stance.

Similarly, the May minutes showed that the Federal Reserve staff forecasts a mild recession towards the end of the year. Additionally, the minutes emphasized that the policy outlook hinged on the presence of upside risks to the inflation trajectory and the potential for inflation expectations to become unanchored. These factors remain crucial considerations for the Federal Reserve’s decision-making process.

XAU/USD Price Analysis: Technical outlook

XAU/USD remains neutral to downward biased, unable to break above solid resistance at the 20-day EMA at $1930.93, seen as the first resistance level by Gold buyers. In addition, a Wednesday’s daily close below Tuesday’s low of $1919.89 can open the door for further downside, with XAU/USD sellers eyeing the $1900 figure, followed by the 200-day EMA a $1896.80. Once that level is cleared, the next support would be June’s 29 swing low and three-month-low of $1893.12. Conversely, if XAU/USD reclaims the 20-day EMA, followed by the 50-day EMA at $1835.34, XAU buyers would remain hopeful to test $1950.

- GBP/USD stands at 1.2705, reflecting a slight decrease by 0.02%, amid the FOMC minutes release.

- The FOMC minutes revealed that some Fed officials called for a 25 bps rate hike, citing labor market tightness as the main reason.

- The Federal Reserve staff forecasted a mild recession towards the end of the year.

- Market expectations for two rate hikes remained unchanged, with odds for November at 31%, while for July, chances stand at 88.7%, according to the CME FedWatch Tool.

GBP/USD hovers around the 1.2700 mark as the latest Federal Reserve Open Market Committee (FOMC) minutes showed that some Fed officials wanted to raise rates. Still, they agreed to pause to assess the impact of the Fed’s cumulative tightening amidst maintaining a restrictive stance. The GBP/USD is trading at 1.2692, down 0.12%.

The US Dollar Index (DXY) barely reacted to the data and stayed firm at around 103.290, while US Treasury bond yields continued to climb after the June minutes release. Expectations for two rate hikes remained unchanged, with odds for November at 31%, while for July, chances for a rate hike are at 88.7%, as shown by the CME FedWatch Tool.

Must read: FOMC minutes: Some officials favored a 25bps hike at the June meeting

Summary of the FOMC’s June meeting minutes

FOMC’s minutes showed that all participants judged it appropriate or acceptable to leave rates unchanged to assess the impact of cumulative tightening. However, Fed officials that wanted to lift rates by 25 bps mentioned the tightness of the labor market as the main reason for a hike. At the same time, all participants agreed to keep a restrictive stance as appropriate.

In the meantime, Fed staff sees a mild recession late in the year, as mentioned in the May minutes, while upside risks to the inflation outlook or the possibility of inflation expectations might become unanchored, remained key to the policy outlook.

GBP/USD Price Analysis: Technical outlook

The GBP/USD failed to react to the data, though it turned negatively but clung above the 1.2700 figure. However, the GBP/USD remains capped by the weekly high of 1.2739 seen last Tuesday but failed to dive beneath the 1.2700 figure. From an oscillator perspective, the Relative Strength Index (RSI) drops toward the 50-midline, while the three-day Rate of Change (RoC) depicts buyers losing momentum. But unless GBP/USD tumbles below 1.2700, upside risks remain. On the downside, key support levels lie at the 20-day EMA at 1.2662, followed by the 1.2600 figure and the 50-day EMA at 1.2567. On the upside, resistance lies at 1.2700, followed by 1.2736 and 1.2750.

- Federal Reserve released the minutes from its June 13-14 meeting.

- The minutes showed some policymakers favored a rate hike, but went with a pause.

- US Dollar pulls back modestly after the minutes.

The Federal Open Market Committee (FOMC) released the minutes of its June meeting, triggering a limited reaction across financial markets. According to the document, some officials favored a rate hike at the meeting, but went along with a pause. The minutes showed a division among FOMC members.

In June, the Federal Reserve (Fed) kept the interest rate unchanged at 5.00% - 5.25%, as expected. In the projections, members see more rate hikes before year-end. The minutes show that “almost all participants noted that in their economic projections that they judged that additional increases in the target federal funds rate during 2023 would be appropriate.”

“Most participants observed that uncertainty about the outlook for the economy and inflation remained elevated and that additional information would be valuable for considering the appropriate stance of monetary policy”, the minutes noted.

Key takeaways from the minutes:

“Participants generally noted that banking stresses had receded and conditions in the banking sector were much improved since early March."

“The economy was facing headwinds from tighter credit conditions, including higher interest rates, for households and businesses, which would likely weigh on economic activity, hiring, and inflation, although the extent of these effect remained uncertain. Against this backdrop, and in consideration of the significant cumulative tightening in the stance of monetary policy and the lags with which policy affects economic activity and inflation, almost all participants judged it appropriate or acceptable to maintain the target range for the federal funds rate at 5 to 5-1/4 percent at this meeting. Most of these participants observed that leaving the target range unchanged at this meeting would allow them more time to assess the economy's progress toward the Committee's goals of maximum employment and price stability.”

“Some participants indicated that they favored raising the target range for the federal funds rate 25 basis points at this meeting or that they could have supported such a proposal.”

“The participants favoring a 25 basis point increase noted that the labor market remained very tight, momentum in economic activity had been stronger than earlier anticipated, and there were few clear signs that inflation was on a path to return to the Committee's 2 percent objective over time.”

“Almost all participants noted that in their economic projections that they judged that additional increases in the target federal funds rate during 2023 would be appropriate.”

“Most participants observed that uncertainty about the outlook for the economy and inflation remained elevated and that additional information would be valuable for considering the appropriate stance of monetary policy.”

“Many also noted that, after rapidly tightening the stance of monetary policy last year, the Committee had slowed the pace of tightening and that a further moderation in the pace of policy firming was appropriate in order to provide additional time to observe the effects of cumulative tightening and assess their implications for policy.”

Market reaction:

The US Dollar strengthened after the minutes. The DXY printed fresh weekly highs above 103.30 and EUR/USD fell toward 1.0850.

- EUR/JPY cleared daily gains and fell to the 157.00 area after peaking at 157.72.

- European Services PMIs from June showed disappointing results.

- JPY gains interest as the probabilities of a BoJ intervention rise.

EUR/JPY faced selling pressure, leading to a retreat towards 157.00, erasing earlier gains from its peak at 157.72. Disappointing European Services PMIs for June contributed while the Japanese Yen gained interest as market probabilities of a potential Bank of Japan (BoJ) intervention increase as the USD/JPY approached 145.00.

The Euro faced selling pressure on weak Services PMIs

The recently released PMI data from S&P Global and Hamburg Commercial Bank (HCOB), indicated that French and Spanish Services PMIs for June fell short of expectations, registering at 47.2 and 53.4, respectively. On the other hand, the German and Italian indexes remained unchanged from their previous figures, with readings of 54.1 and 52.2, respectively. Overall, the Eurozone's PMIs came in at 52, slightly below the anticipated 52.4, signalling a slight deceleration but still indicating expansion in the sector.

On the other hand, the Bank of Japan’s (BoJ) dovish stance has significantly weakened the Yen in the previous session as economies entered another tightening cycle and higher interest rates tend to be positively correlated with the value of a currency. As a result, the USD/JPY rose to 145.00 psychological level last Friday, so escalating odds of further intervention by the BoJ to support the Yen may limit its downside potential.

EUR/JPY Levels to watch

The bulls finally gave up. After showing overbought conditions in the daily chart since mid-June, indicators finally show some weakness. The Relative Strength Index (RSI) fell below the 70.00 threshold, while the Moving Average Convergence Divergence shows decreasing green bars suggesting that the bears may take control.

On the downside, support levels to monitor stand at the 156.70 area, followed by 156.00 and 155.00. On the upside, if the bulls regain momentum, resistance levels are seen at 157.50, followed by 158.00 (cycle-high) and 158.50.

EUR/JPY Daily chart

-638241758999443707.png)

On Wednesday, July 5, the US Federal Reserve (FED) will release the latest monetary policy meeting minutes of the Federal Open Market Committee (FOMC) at 18:00 GMT, sought by traders as they would provide insight into the US central bank’s forward path.

On June 13-14, the US Federal Reserve, after raising 500 basis points (bps), decided to keep the Federal Funds Rates (FFR) unchanged at 5.00%-5.25%, as policymakers would like to assess the impact of the cumulative tightening in the economy, which according to the latest round of data, remains resilient.

The Fed’s June meeting witnessed the release of the Summary of Economic Projections (SEP), used by Fed officials to guide the market regarding how they see economic growth, inflation, unemployment, and the FFR. It should be said that twelve of the eighteen Federal Reserve Open Market Committee (FOMC) members expect rates to peak at 5.6%, implying that Fed Chair Jerome Powell and Company foresee two additional rate hikes.

That helped the greenback, which initially witnessed weakness, though the Fed’s hawkish hold limited its losses. OF note, Fed Chair Jerome Powell stuck to the 50 bps of tightening pending to be raised at his public appearances while downplaying a recessionary scenario and emphasizing the tightness of the labor market.

Despite that, money market futures estimate the Federal Reserve would hike just once, as shown by the CME FedWatch Tool, with odds above 85%.

It should be said postures within the Federal Reserve had begun to change, as some hawks are worried about overtightening, like the case of Atlanta’s Fed President Raphael Bostic, who shifted dovish. Nevertheless, most US central bank officials estimate that further monetary firming is needed to tackle inflation at twice the Fed’s 2% goal.

After the FOMC’s June minutes, upcoming US Nonfarm Payrolls data and inflation figures would help the Fed to figure out the next move at the July 25-26 FOMC meeting.

How Could It Affect EUR/USD?

Given that the EUR/USD is trading with a bearish tone in the week, if the FOMC’s minutes area tilted hawkish could motivate EUR/USD sellers to decisively break support at the 50-day Exponential Moving Average (EMA) at 1.0857 and exacerbate a test of the 1.0800 mark. Nonetheless, the EUR/USD will need to hurdle the 100-day EMA at 1.0806 before cracking the 1.0800 figure as US Dollar (USD) bulls eye the 200-day EMA at 1.0722.

Conversely, worse-than-expected Eurozone (EU) growth data and PMI flashing a recession might prevent the European Central Bank (ECB) from hiking twice toward the September meeting. But as ECB officials remained hawkish, any dovish signal by the Fed could pave the way for EUR/USD to reclaim the 1.0900 figure, ahead of challenging 1.1000.

Key Notes

- FOMC Minutes to offer clues about Fed interest rate path

About the Federal Reserve Open Market Committee (FOMC) minutes

FOMC stands for The Federal Open Market Committee that organizes 8 meetings in a year and reviews economic and financial conditions, determines the appropriate stance of monetary policy and assesses the risks to its long-run goals of price stability and sustainable economic growth. FOMC Minutes are released by the Board of Governors of the Federal Reserve and are a clear guide to the future US interest rate policy.

- USD/CHF pair trades in the 0.8934/0.9004 area, showing a neutral to downward bias amidst a lack of strong catalysts.

- The RSI points towards bullish territory, while the RoC indicates buyers are still in control, sending mixed signals to traders.

- Breaking above the 0.9000 mark could challenge current resistance levels, while a fall below 0.8945 may trigger a deeper decline.

USD/CHF advanced steadily on Wednesday after the release of US economic data painted a gloomy economic outlook in the United States (US) as traders prepare for the Federal Reserve’s (Fed) release of the latest monetary policy minutes. The USD/CHF trades at 0.8977 after hitting a daily low of 0.8957 and gains 0.08%.

USD/CHF Price Analysis: Technical outlook

The USD/CHF remains neutral to downward biased, but the lack of catalyst triggered a consolidation during the week in the 0.8934/0.9004 area. Nevertheless, the long-term daily Exponential Moving Averages (EMAs) sitting above the current exchange rate warrants further downside.

Even though the Relative Strength Index (RSI) is in bearish territory, it continues to edge higher, is about to cross above the 50-midline, and will turn bullish, while the three-day Rate of Change (RoC) suggests that buyers remained in charge.

Hence, mixed signals could refrain traders from opening fresh long/short bets on the pair. However, If USD/CHF reclaims 0.9000, the pair could challenge the confluence of the 50-day EMA and the current week’s high at around 0.9003/04. A breach of the latter will expose the USD/CHF June 30 swing high at 0.9016, followed by a one-month-old downslope resistance trendline at 0.9015, followed by the 100-day EMA at 0.9074, and the 0.9100 figure.

On the flip side, if USD/CHF drops below the July 4 daily low of 0.8945, which, once cleared, will expose the June 30 daily low of 0.8935, ahead of diving toward the June 16 low of 0.8901.

USD/CHF Price Action – Daily chart

- EUR/GBP peaked at a daily high of 0.8575 (20-day SMA) and then retreated to 0.8550.

- German, French and Spanish HCOB Services PMIs from June showed disappointing results.

- The British index showed an expansion, just as the markets expected.

Following the release of European Services Purchasing Managers Index (PMI) data, the EUR/GBP relinquished its daily gains. The pair initially reached a high of 0.8575, where the 20-day Simple Moving Average (SMA) stands, but later retreated to 0.8550. Disappointing results from German, French, and Spanish Hamburg Commercial Bank (HCOB) Services PMIs contributed to the reversal, while the British index met expectations by standing in expansion territory.

Euro lost ground after disappointing EZ Services PMIs.

During the European session, the HCOB reported that June's Frech and Spanish Services PMIs were below expectations at 47.2 and 53.4, respectively. In addition, the German and Italian indexes remain unchanged concerning their previous figures at 54.1 and 52.2, respectively. Overall the Eurozone’s figure came in at 52, vs the 52.4 expected reflections of deceleration but remaining in the expansion area.

Conversely, the British Service PMI released by the Chartered Institute of Purchasing & Supply (CIPIS) and the S&P Global came in at 53.7, just as expected.

For the rest of the week, investors will put an eye on Thursday’s release of Retail Sales from the Eurozone from June and European Central Bank’s De Guindos and Lagarde’s speeches on Friday. On the British Calendar, market participants will see the Construction PMI release from June and Housing data on Friday from June.

EUR/GBP Levels to watch

According to the daily chart, the technical outlook favours the bears. Bulls struggle to reignite their momentum as the Moving Average Convergence Divergence (MACD) prints decreasing green bars while the Relative Strength Index (RSI) points south, in negative territory.

Support Levels to watch: 0.8540, 0.8525,0.8520.

Resistance Levels to watch: 0.8575 (20-day SMA), 0.8590, 0.8600.

EUR/GBP Daily chart

- The USD/MXN pair slides to a seven-year low on disappointing US manufacturing data and a weakened USD.

- Mexican economy indicators show mixed signs, with a slight fall in Gross Fixed Investment but a rise in Consumer Confidence.

- Upcoming US labor data, Banxico’s meeting minutes, and Mexican inflation data could significantly impact the USD/MXN movement.

The USD/MXN falls in the North American session reached a new seven-year low of 16.9761 after data from the United States (US) accentuated an ongoing slowdown in manufacturing as orders missed estimates. That, alongside a weak US Dollar (USD) and interest rate differential between the US and Mexico, boosted the Mexican Peso (MXN). At the time of writing, the USD/MXN exchanges hands at 16.9874, slides 0.43%.

Amid disappointing US economic data, interest rate differential benefits the Mexican Peso

US equities remain pressured, as the US Census Bureau showed that Factory Orders in May, failed to grow at the 0.8% pace expected, expanded by 0.3%, unchanged compared to April, while orders that exclude transportation plummeted -0.5%, below the 0.5% growth estimates by the consensus.

The USD/MXN dived before the US Factory Orders release, from around 17.0219, toward its new year-to-date (YTD) low of 17.9761. However, the pair has recovered some ground, hoovers nearby the 17.00 figure.

Today’s data showed that Factory Orders remain unchanged, and weaker readings on the ISM Manufacturing PMI in the last eight months show the US economy could be at the brisk of getting into a recession. Nonetheless, additional data ahead in the current and the following week could give more cues about the US economy’s status.

Aside from this, speculators see the Fed lifting rates In July, as shown by the CME FedWatch Tool. Chances for a 25 bps increase are at 88.7%, while the swaps market sees the Federal Funds Rates (FFR) peaking at 5.25%-5.50%.

Across the border, the Mexican economic docket revealed that Gross Fixed Investment in April fell -0.3% MoM, beneath March’s 0.5% growth. At the same time, Consumer Confidence for June rose by 45.2, above the 44.3 consensus and exceeding the previous month’s 44.5.

Upcoming events

The US agenda will deliver labor market data, the Balance of Trade on Thursday, and the ISM Services PMI. On Friday, the US Nonfarm Payrolls report could dictate what the Fed could do at the next monetary policy meeting. On the Mexican front, the Bank of Mexico (Banxico) will release its last meeting minutes on Thursday, followed by inflation data on Friday.

USD/MXN Price Analysis: Technical outlook

The USD/MXN downtrend is set to continue as the pair is trading well beneath its daily Exponential Moving Averages (EMAs). The Relative Strength Index (RSI) indicator remains in bearish territory, while the three-day Rate of Change (RoC) shows sellers are in charge. That said, the USD/MXN needs to achieve a daily close below 17.00. In that outcome, the next support would be the 16.50 psychological figure, followed by the October 2015 daily low of 16.3267, before testing the 16.00 mark. Conversely, the USD/MXN first resistance is the 20-day EMA at 17.1772, followed by the May 17 daily low-turned resistance at 17.4038.

- Volatile session for metals as the US Dollar remains steady.

- After spiking to the highest level since June 23, XAU/USD turned to the downside.

- Gold is losing momentum, and the reversal could expose $1,900.

The price of Gold surged to $1,935/oz, reaching the highest level since June 23. However, it quickly reversed course and turned lower. XAU/USD dropped to $1,919, hitting a fresh daily low.

The yellow metal climbed to weekly highs and then fell to daily lows in just a few minutes, losing almost $20. Volatility remains elevated, with the price struggling to hold above $1,920. If the price manages to remain above $1,930, the outlook would improve for the bulls. On the contrary, if the price consolidates under $1,920, more losses seem likely. The next support area is seen around $1,910.

Attention on FOMC minutes and US data

Economic data from the US showed Factory Orders in May rose by 0.3%, below the 0.8% expected by the markets. On Thursday, key labor market data is due, including the ADP report, Jobless Claims, and JOLTS. On Friday, it will be the turn of the Nonfarm Payroll report.

Later on Wednesday, at 18:00 GMT, the Federal Reserve will release the minutes of its June meeting, when it decided to hold rates steady for the first time in the tightening cycle. The minutes could show a hawkish bias in the discussion. Since the meeting, Chair Powell and other officials have repeated that the forecasts are for more rate hikes before year-end.

The minutes and the job figures will likely cause volatility across financial markets and will play a key role in shaping Fed monetary policy expectations. If markets see a more hawkish tone from the Fed, it could send US yields higher and weigh on Gold. On the contrary, weak data could be positive for the yellow metal.

Technical levels

Economists at TD Securities analyze how US data this week could impact Gold.

Focus on the ISM services and jobs data

Postponing the looming recession any further threatens a resurgence in real wages that could keep the Fed on its warpath against inflation. However, we expect that data trends will likely sufficiently soften to keep the Fed from further pursuing its warpath against inflation, particularly as the more cyclical components of growth data are already deteriorating at a fast pace.

This places significant attention on the ISM services and jobs data, where Gold's reaction function may be asymmetrically skewed to the upside on misses in the data.

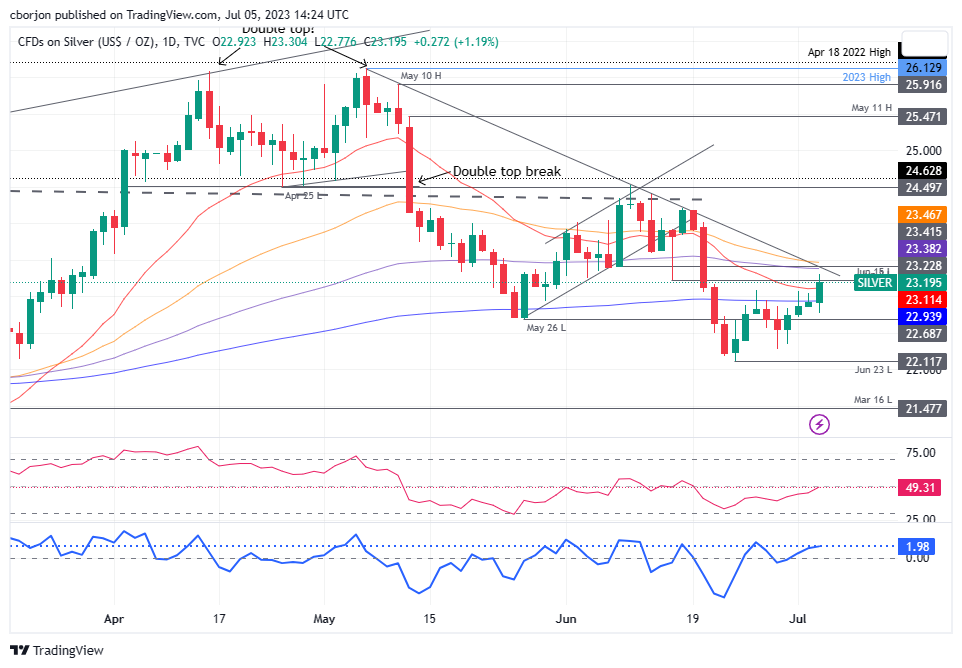

- Silver prices climb for the fourth consecutive day, spurred by a weak USD and expectations of the upcoming Fed meeting minutes.

- Amid disappointing US economic data, China-US trade tensions may further drive XAG’s appeal as a haven asset.

- Market anticipation builds ahead of key US labor market data and Nonfarm Payrolls report, which could shape future Fed actions.

Silver price climbs for the fourth consecutive trading day as the US Dollar (USD) weakened ahead of the release of June’s Federal Reserve (Fed) last meeting minutes, which would give some cues about the US central bank’s forward path on monetary policy. The XAG/USD trades above the $23.00 figure after hitting a daily low of $22.77.

Slowdown in the US economy and geopolitical tensions bolster Silver prices

Wall Street is back though operating with losses ahead of the release of the Fed’s minutes. Data from the US Census Bureau revealed that Factory Orders for May came at 0.3%, unchanged compared to April’s data, but missed estimates of a 0.8% increase. Excluding transports, orders plunged -0.5%, less than the prior’s month downward revised metric of -0.6% and below the 0.5% expansion projected by the consensus.

XAG/USD reacted upwards to the data, as it shows the US economy is slowing down, as data revealed on Monday showed June’s ISM Manufacturing PMI plummeting into the recessionary territory at 46.0, below April’s 46.9. US Treasury bond yields are almost unchanged, while US real yields, calculated with the nominal yield minus inflation, stay at 1.630%, capping XAG/USD’s rally.

Regarding monetary policy, futures traders see the Fed raising rates just once, contrary to what Fed Chair Powell said on his last two public appearances, as shown by the CME FedWatcth Tool odds for a 25 bps rate hike in July, at 88.7%. The minutes could cement the Fed’s dot-plot case for two rate increases, which market participants do not project.

Meanwhile, China-US tussles could augment appetite for precious metals as tension around IT, technology, and raw materials exports from China to the US to produce chips could shift sentiment sour and bolster precious metals. In that regard, US Treasury Secretary Janet Yellen travels to China Thursday for meetings with Chinese officials.

Upcoming events

The US agenda will deliver labor market data on Thursday and the ISM Services PMI. On Friday, the US Nonfarm Payrolls report could dictate what the Fed could do at the next monetary policy meeting.

XAG/USD Price Analysis: Technical outlook

The XAG/USD extended its recovery, though it remains below technical resistance levels, which, once cleared, could pave the way for further upside. The first resistance is the 20-day Exponential Moving Average (EMA) at $23.10, followed by the confluence of a downslope resistance trendline and the 50-day EMA at around $23.46. Break above will expose the June 16 daily high at $24.20. Conversely, a drop below $23.00 would keep sellers in charge and exacerbate a fall to the June 23 swing low of $22.11.

EUR/GBP has been driven by short-term rate differentials for the majority of the recent past. Economists at Société Générale analyze GBP outlook.

Supported by rates, vulnerable when they peak and as growth slows

Random recurrent crises notwithstanding, Sterling is being supported by a faster pace of rate hikes than elsewhere, and markets are now pricing a higher peak in the UK than in the eurozone or US. That will support GBP for as long as this unusually close correlation between currencies and short-term rates persists and until the rate outlook changes.

The UK has a less attractive growth/inflation trade-off than other major economies, something which has been exacerbated by Brexit. The upshot of that will be weaker growth and higher inflation over 2023-2024 than in the Eurozone.

Sterling can only expect support from higher rates for so long before the growth outlook (and the longer-term interest rate implications of weak growth) takes over. We think that will start to happen in 2H23 as rates approach their peak.

- Factory Orders in the US rose less than expected in May.

- US Dollar Index continues to fluctuate near 103.00.

The data published by the US Census Bureau revealed on Wednesday that new orders for manufactured goods, Factory Orders, increased $1.6 billion, or 0.3%, to $578 billion in May. This print followed April's increase of 0.3% and came in worse than the market expectation for an increase of 0.8%.

"New orders for manufactured durable goods in May, up three consecutive months, increased $5.0 billion, or 1.8%, to $288.4 billion, up from the previously published 1.7%," the publication further read.

Market reaction

The US Dollar Index stays in its daily range near 103.00 after this report.

Economists at MUFG Bank see EUR/USD higher but lower than previously forecast.

Some upside scope from here

We have nudged our peak EUR/USD level of 1.1500 a little lower.

Weaker-than-expected data from the Eurozone, a rate hike by the Fed in July and continued global growth concerns will take some of the modest upward momentum away from EUR/USD.

Still, assuming no notable worsening of growth in the Eurozone and some pick-up in China optimism, we still see some upside scope from here.

EUR/USD – Q3 2023 1.10 Q4 2023 1.12 Q1 2024 1.13 Q2 2024 1.10

- EUR/USD keeps hovering around the 1.0900 region on Wednesday.

- Immediately to the downside emerges the 1.0830 contention zone.

EUR/USD maintains the choppiness well in place around the 1.0900 yardstick on midweek.

Price action around the pair looks vacillating for the time being. Against that, spot needs to clear the June peak at 1.1012 (June 22), ideally in the near term, to allow for the resumption of the uptrend and a potential challenge of the 2023 top just below 1.1100 (April 26).

However, failing to do so, could spark the resurgence of the selling pressure, which could open the door to another visit to the weekly low at 1.0835 (June 30) prior to the transitory 100-day SMA, today at 1.0823.

Looking at the longer run, the positive view remains unchanged while above the 200-day SMA, today at 1.0608.

EUR/USD daily chart

Lee Sue Ann, Economist at UOB Group, reviews the latest interest rate decision by the RBA (July 4).

Key Takeaways

The Reserve Bank of Australia (RBA) decided to leave the cash rate target unchanged at 4.10%, stating that the latest decision to hold will provide some time to assess the impact of the increase in interest rates to date and the economic outlook

We were anticipating a 25bps hike at this meeting but had acknowledged that it would be a close call. While the slump in the latest headline inflation was positive, two key components – electricity and rents – of the CPI basket could delay the return of inflation to the RBA’s 2-3% target band.

The next batch of quarterly CPI data (2Q23) will be released on 26 Jul. Before that, labour market data for Jun will be rolled out on 20 Jul. We think the RBA will likely push for a 25bps rate hike at the 1 Aug monetary policy meeting. It will also be when the RBA updates growth and inflation forecasts.

- USD/CAD has sensed sheer selling pressure around 1.3300 amid strength in the oil price.

- S&P500 is expected to open on a negative note as investors are cautious ahead of second-quarter corporate earnings.

- Although Fed has voted for two more interest rate hikes, the investing community is expecting only one rate hike by the year-end.

The USD/CAD pair has faced stiff barricades near the round-level resistance of 1.3300 in the early New York session. The Loonie asset is expected to remain on the tenterhooks as the market mood has turned risk-off ahead of the United States opening after a holiday.

S&P500 is expected to open on a negative note as investors are cautious ahead of second-quarter corporate earnings. Subdued earnings are expected from US firms amid higher interest rates from the Federal Reserve (Fed) and tight credit conditions by commercial banks. US commercial banks tightened their credit-disbursement process to avoid maintaining asset quality in a turbulent environment.

The US Dollar Index (DXY) has dropped after facing selling pressure around 103.20 despite investors shifting their focus to the release of the Federal Open Market Committee (FOMC) minutes. Although Fed chair Jerome Powell has voted for two more interest rate hikes, the investing community is expecting only one rate hike by the year-end.

About USD Index guidance, economists at MUFG expect Even if the FOMC does hike in July, with the market close to fully priced and with most other G10 central banks priced to hike further, the scope for the Dollar to strengthen over the second half of the year remains limited.

Meanwhile, the Canadian Dollar has picked strength amid upbeat oil prices. West Texas Intermediate (WTI), futures on NYMEX, have climbed to near $72.00 as buying interest inspired by the announcement of production cuts by Saudi are outperforming the bleak global outlook.

It is worth noting that Canada is the leading exporter of oil to the United States and higher oil prices support the Canadian Dollar.

- DXY extends the weekly consolidative mood around 103.00.

- The resumption of the buying interest could challenge 103.50.

DXY alternates gains with losses amidst the weekly range bound theme around the 103.00 zone on Wednesday.

While further consolidation seems probable in the very near term, the continuation of the uptrend in place since mid-June could challenge the weekly high at 103.54 (June 30) prior to the May high at 104.69 (May 31), which appears reinforced by the 200-day SMA.

Looking at the broader picture, while below the 200-day SMA at 104.74, the outlook for the index is expected to remain negative.

DXY daily chart

Economists at Société Générale analyze CAD outlook and expect the USD/CAD pair to tick down below the 1.30 level.

Slow gains as Fed turn approaches

The peak level of US-Canadian relative rates is now probably in the rear-view mirror for the rest of the current economic cycle, and that should support the CAD from now on.

We’re unlikely to see a rapid move from here given that there is a possibility that the Fed tightens a little more (the Bank of Canada seems very likely to raise rates at least one more time), but we think we have seen the peak in USD/CAD and will see a return back to a 1.25-1.30 trading range during the back end of this year.

There is uncertainty about the impact on the Canadian economy of this spring/summer’s wildfires, and success in getting inflation down in Canada will translate into reduced urgency about further policy tightening, but that means the pace and extent of the downtrend in USD/CAD is likely to be slow rather than suggesting levels below USD/CAD 1.30 can’t be sustained.

-

Canadian Dollar loses ground as higher interest rates in the US and expectations of more hikes favor the US Dollar.

-

A triennial OPEC conference of Oil bigwigs gets underway though media coverage is limited.

-

The longer-term uptrend may be experiencing the start of a new upcycle if the daily highs can be held.

Canadian Dollar (CAD) is weakening versus the US Dollar (USD) on Wednesday, depressed by the view that interest rates will rise further in the US compared to Canada.

According to predictions from Trading Economics, base interest rates – set by each nation's central banks – are likely to rise by 0.25% in Canada compared to 0.50% in its Southern neighbor. Since relatively higher interest rates attract greater capital inflows, USD is set to benefit more than CAD.

A major Organization of the Petroleum Exporting Countries (OPEC) conference is underway, which could affect Oil prices, whilst Crude traders will also be keenly awaiting American Petroleum Institute (API) data. Both could impact the Canadian Dollar (CAD).

USD/CAD is trading in the upper 1.32s on Wednesday during the US session.

Canadian Dollar news and market movers

-

The Canadian Dollar (CAD) is falling versus the US Dollar (USD) on the back of predictions of greater interest rate hikes in the US compared to Canada.

-

The US Federal Reserve (Fed) has already raised its base lending rate, the Fed Funds Rate, to a higher level of 5.25%, compared to the Bank of Canada’s (BoC) Policy Interest Rate of 4.75%.

-

According to Trading Economics, the Fed is expected to hike rates by 0.25% in both Q3 and Q4 before peak rate is reached. This compares with only one 0.25% hike in Q3 in the case of the BoC.

-

US Treasury Bond yields, the return investors can expect from holding bonds, are generally higher than their Canadian counterparts, further drawing investor capital and supporting the currency. The benchmark 10-year US Treasury Bond yield is at 3.859% compared to the 10-year Canadian Government Bond’s 3.352%.

-

Both countries’ yield curves are showing inversion, suggesting rates will peak in the near-term before falling, which is in line with Trading Economics’ forecasts. Yield curve inversion is also potentially a warning of impending recession.

-

OPEC’s triennial get-together, the 8th International Seminar, is underway in Vienna and will last till the end of July 6. Oil Ministers from member states will meet other key players in the field of global energy. Reporters’ access to the event has been limited, but there is a possibility of news leaks impacting Oil prices and therefore CAD, since Crude is Canada’s largest export.

-

The most recent issue to have come under the spotlight for the Oil market is concern regarding Saudi and Russian supply, so any news regarding this could impact markets.

-

Weekly inventory figures from the American Petroleum Institute (API) are scheduled for release at 14:30 GMT and may impact Oil prices and therefore USD/CAD if they show an unexpected change in inventories.

Canadian Dollar Technical Analysis: Signs of a reversal in line with longer-term uptrend

USD/CAD has been in a long-term uptrend on the weekly chart since the 2021 lows. Since October 2022, it has been in a sideways consolidation within the uptrend and currently sits at the bottom of that range. Given that the trend has a tendency to extend, the probabilities overall favor longs over shorts.

The USD/CAD appears to have completed a measured move price pattern since the March 2023 highs. The measured move is a 3-wave zig-zag-like price pattern, much like an ABC correction in which the first and third waves are of a similar length (waves A and C on the chart below).

The measured move on USD/CAD looks like it has probably completed since waves A and C are of a similar length. If so, price has probably bottomed and is about to begin a cycle higher.

-638241589027422930.png)

US Dollar vs Canadian Dollar: Weekly Chart

There is also a confluence of support just under the June lows in the late 1.30s, made up of several longer moving averages and a major trendline. This is likely to underpin price at this level and reduces the chances of a breakdown. Only a decisive break below 1.3050 would provide evidence this thick band of weighty support has been definitively broken. A decisive bearish break is one that is accompanied by a longer-than-average red candlestick or three red candlesticks in a row.

-638241588399388130.png)

US Dollar vs Canadian Dollar: Daily Chart

The daily chart further suggests the potential for a bullish recovery. The move up from the June 27 bottom has been accompanied by strong momentum, as shown by the high reading on the Relative Strength Index (RSI) momentum indicator, which is higher than it was when prices were more elevated prior to the market bottom.

The price is currently breaking above the 1.3270 key lower high, potentially confirming a short-term bullish reversal. The move could see a rise up to possibly as high as 1.3400 and the 50-day Simple Moving Average, bringing the short-term trend in line with the longer-term uptrend.

Much depends on Wednesday’s close. If it is strongly bullish with the day closing near its elevated highs of 1.3293 then the breakout higher can be classed as decisive and likely to extend. If price drops back down, however, and ends the day below 1.3270, the break may have been false and prices could move lower or go sideways in the short time.

Canadian Dollar FAQs

What key factors drive the Canadian Dollar?

The key factors driving the Canadian Dollar (CAD) are the level of interest rates set by the Bank of Canada (BoC), the price of Oil, Canada’s largest export, the health of its economy, inflation and the Trade Balance, which is the difference between the value of Canada’s exports versus its imports. Other factors include market sentiment – whether investors are taking on more risky assets (risk-on) or seeking safe-havens (risk-off) – with risk-on being CAD-positive. As its largest trading partner, the health of the US economy is also a key factor influencing the Canadian Dollar.

How do the decisions of the Bank of Canada impact the Canadian Dollar?

The Bank of Canada (BoC) has a significant influence on the Canadian Dollar by setting the level of interest rates that banks can lend to one another. This influences the level of interest rates for everyone. The main goal of the BoC is to maintain inflation at 1-3% by adjusting interest rates up or down. Relatively higher interest rates tend to be positive for the CAD. The Bank of Canada can also use quantitative easing and tightening to influence credit conditions, with the former CAD-negative and the latter CAD-positive.

How does the price of Oil impact the Canadian Dollar?

The price of Oil is a key factor impacting the value of the Canadian Dollar. Petroleum is Canada’s biggest export, so Oil price tends to have an immediate impact on the CAD value. Generally, if Oil price rises CAD also goes up, as aggregate demand for the currency increases. The opposite is the case if the price of Oil falls. Higher Oil prices also tend to result in a greater likelihood of a positive Trade Balance, which is also supportive of the CAD.

How does inflation data impact the value of the Canadian Dollar?