УВАГА: Матеріал у cтрічці новин та аналітики оновлюєтьcя автоматично, перезавантаження cторінки може уповільнити процеc появи нового матеріалу. Для оперативного отримання матеріалів рекомендуємо тримати cтрічку новин поcтійно відкритою.

Silver's surge to multi-year highs reflects strong precious metals momentum, undeterred by US job market.

Technical outlook hints at more gains, with resistances at $27.50, $28.00.

RSI dip may prompt support tests at $27.00, $26.12 for future direction clues.

Silver soared sharply and finished the week with gains of close to 10%, hitting three-year highs after reaching levels last seen in June 2021. At the time of writing, XAG/USD trades at $27.45 a troy ounce, gaining more than 2%.

The precious metals segment ignored an upbeat US jobs report that might delay the Federal Reserve from slashing rates in the June meeting. According to the CME FedWatch Tool, market participants decreased their bets on a quarter-percentage-point rate cut in June, though July remains in play. Silver followed Gold’s path, though the latter is trading at all-time highs.

XAG/USD Price Analysis: Technical outlook

The grey metal daily chart shows Silver dipped as low as $26.29 after the US NFP release but, in the aftermath, rallied to multi-year highs. The Relative Strength Index (RSI) despite being at overbought conditions, aims up, an indication that buyers are gathering momentum. That said, XAG/USD next resistance would be $27.50, followed by the $28.00 psychological mark. Key resistance lies at June 10, 2021, high at $28.28.

On the other hand, if the RSI punches below the 70 level, that could sponsor a pullback, toward the $27.00 figure. The next support would be the May 5, 2023 high turned support at $26.12, followed by the $26.00 figure.

The daily MACD shows a slight positive momentum, despite the overall bearish bias.

The daily RSI indicates that the sellers are dominating, though the indicator's flat trajectory suggests that the bearish momentum may be slowing.

On the hourly chart, the RSI oscillated near the neutral zone, showing inconsistent bearish-bullish signals.

The NZD/USD pair is trading at 0.6013, indicating a drop of 0.26% in Friday's session but will close a winning week. The prolonged downward trend suggests that sellers command the current market. However, the short-term outlook reveals a slight bullish momentum, which could lead to a period of sideways trading in the next sessions.

The daily Relative Strength Index (RSI) resides in negative territory, with a slightly flat slope, indicating sellers dominate this market but seem to be taking a breather. Moreover, the Moving Average Convergence Divergence (MACD) histogram has registered a green bar, pointing to a slight emergence of positive momentum.

NZD/USD daily chart

On the hourly chart, the most recent RSI reading of 47 hovers close to the neutral zone while the MACD histogram draws flat green bars, which can be interpreted as somewhat positive short-term momentum.

NZD/USD hourly chart

Regarding the overall trend, the NZD/USD remains under the 20,100 and 200-day SMA indicating that the overall trend favors the bears. So in case the buyers manage to gain ground, any movement below these levels wouldn’t be considered a serious buying signal.

Support at 190.96, resistance at 192.00 mark pivot points.

Market eyes technical indicators, global economy for future direction.

The GBP/JPY posted decent gains of 0.17% on Friday amid a risk-on impulse following the release of market-moving economic data from the United States. Nonfarm Payrolls for March exceeded estimates, though they barely benefitted the US Dollar as witnessed by the GBP/USD. At the time of writing, the pair exchanges hands at 191.60 after hitting a low of 190.67.

GBP/JPY Price Analysis: Technical outlook

The pair finished the session near the mid-highs of the week but below the 192.00 figure. With he GBP/JPY achieving a lower high and low, the pair is slightly tilted to the downside, despite standing above the Ichimoku Cloud (Kumo).

Hence, the GBP/JPY first support would be the Senkou Span A at 190.96. A breach of the latter will expose the Kijun-Sen at 190.74, followed b the April 2 low of 190.03. Further downside is seen at the Senkou Span B at 189.38.

On the other hand, the first resistance would be the 192.00 mark. A breach of the latter will expose the 193.00 figure, followed by the year-to-date (YTD) high at 193.54.

The daily chart reveals an encouraging picture for the bulls, with the RSI close to 60.

On the hourly chart, the indicators are weakening, but remain in a positive area.

The cross operating above main SMAs, suggests a maintained bullish bias in both short-term and long-term contexts.

The EUR/JPY pair is currently exchanging hands at 164.24, registering a minor gain of 0.16%. Trading dynamics are steadily bullish, with buyers having a dominant influence over market actions. However, indicators are losing steam in the hourly chart.

The daily Relative Strength Index (RSI) reading, residing near 60, places the market in a positive territory and its consistent positive trend in the RSI, indicates that buyers maintain control over the market. Consistently, the Moving Average Convergence Divergence (MACD) presents an encouraging picture with decreasing red bars suggesting weak negative momentum.

EUR/JPY daily chart

Taking a look at the hourly chart, a similar tone of bullish dominance resounds but with indicators losing traction. The RSI values show a positive terrain, position between 40 and 60 during the most recent hours but point south. The MACD on the other hand, prints flat green bars, indicating a steady buying momentum.

EUR/JPY hourly chart

In the broader perspective, EUR/JPY maintains a significant bullish stance. Notably, the EUR/JPY stands above both the 20,100 and 200-day SMA, reaffirming a solid long-term bullish position and confirming the dominant upward movement shown by the RSI.

In conclusion, the comprehensive examination of EUR/JPY, considering both the daily and hourly charts, delivers a dual message. Buyers generally command the market, as illustrated by the upward RSI trend and the presence of green MACD bars. However, minor dips and slowdowns on the hourly chart imply occasional shifts in market dynamics toward sellers.

EUR/JPY

Overview

Today last price

164.27

Today Daily Change

0.23

Today Daily Change %

0.14

Today daily open

164.04

Trends

Daily SMA20

163.04

Daily SMA50

162.1

Daily SMA100

160.52

Daily SMA200

159.24

Levels

Previous Daily High

164.92

Previous Daily Low

163.79

Previous Weekly High

164.42

Previous Weekly Low

162.94

Previous Monthly High

165.36

Previous Monthly Low

160.22

Daily Fibonacci 38.2%

164.22

Daily Fibonacci 61.8%

164.49

Daily Pivot Point S1

163.59

Daily Pivot Point S2

163.13

Daily Pivot Point S3

162.47

Daily Pivot Point R1

164.71

Daily Pivot Point R2

165.37

Daily Pivot Point R3

165.83

19:32

United States CFTC Oil NC Net Positions climbed from previous 278K to 300.9K

19:32

United States CFTC Gold NC Net Positions climbed from previous $199.3K to $207.3K

19:32

United Kingdom CFTC GBP NC Net Positions rose from previous £35.2K to £43.4K

19:32

Japan CFTC JPY NC Net Positions: ¥-143.2K vs previous ¥-129.1K

19:32

United States CFTC S&P 500 NC Net Positions up to $-78.1K from previous $-169.4K

19:32

Eurozone CFTC EUR NC Net Positions: €16.8K vs previous €31.2K

19:32

Australia CFTC AUD NC Net Positions increased to $-102.7K from previous $-105.5K

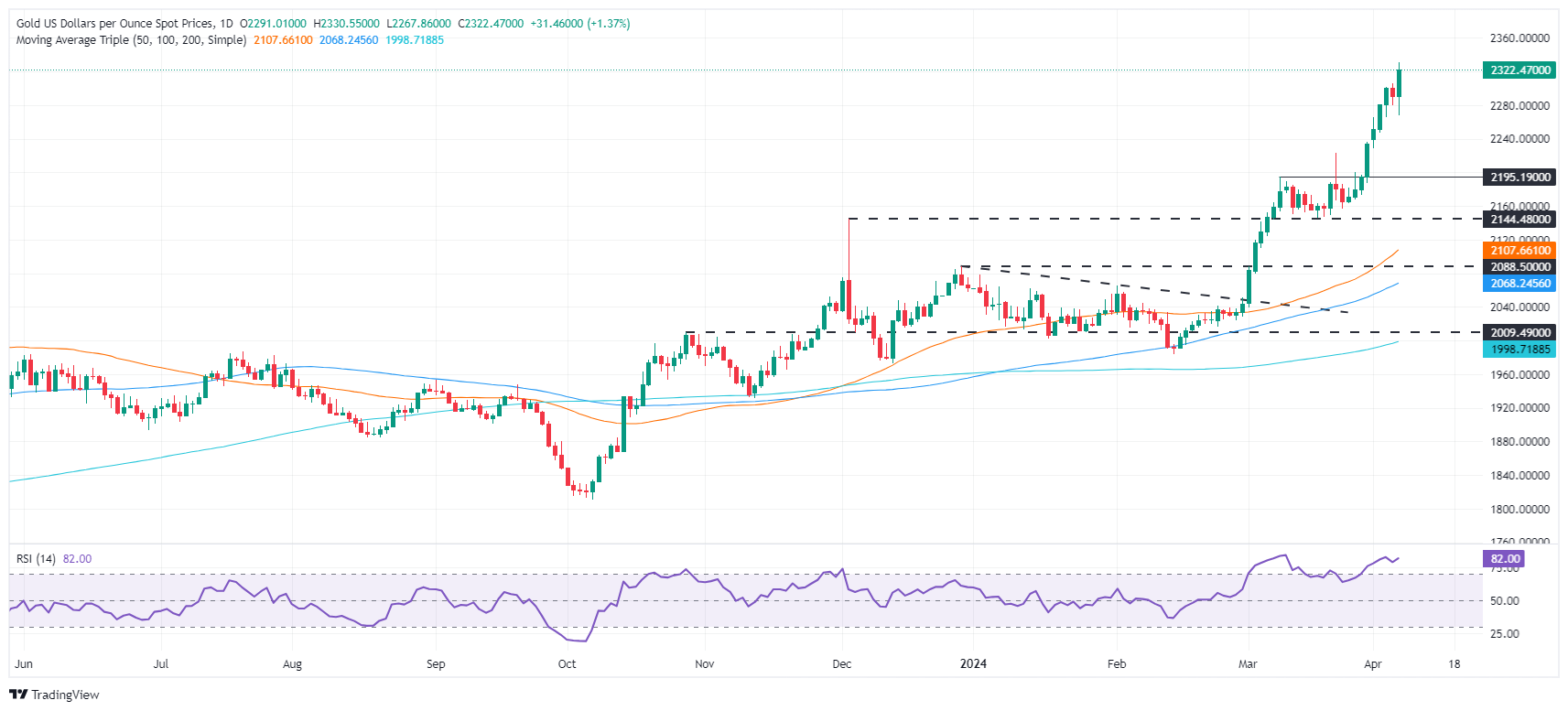

Gold hits record highs, defying US Nonfarm Payrolls spike and US Dollar gains, highlighting safe-haven status.

Fed rate cut outlook adjusted after employment data, central bank remarks.

Geopolitical tensions and strong demand from China bolster Gold's market strength.

Gold rallied to a new all-time high, ignoring a strong March Nonfarm Payrolls report in the United States (US), which could prevent the Federal Reserve (Fed) from slashing rates sooner than the market expects. In achieving its milestone, the yellow metal ignored the rise in US Treasury yields and the Greenback, which clings to modest gains of 0.09%.

XAU/USD trades at $2,324 after reaching $2,330 earlier in Friday’s North American session. Gold’s price continued to be driven by fundamentals linked to the US Dollar, geopolitical risks and physical demand.

Focusing on data, US Nonfarm Payrolls figures for March crushed estimates and February’s numbers as new hirings rose to 303,000. Consequently, the Unemployment Rate fell, while Average Hourly Earnings were mixed, rising on monthly figures but diving on an annual basis.

Following the data, bets that the Fed would cut rates in June fell further, from around 70% a week ago to 53.4%, according to the CME FedWatch Tool.

The employment report reinforced Fed Chair Jerome Powell’s words on Wednesday. He said they’re in no rush to cut rates, and his words echoed throughout the week. On Friday, officials crossed the wires led by Richmond’s Fed Barkin, Dallas Fed Logan and Governor Bowman.

Daily digest market movers: Gold underpinned by strong physical demand, ignores US data

US Department of Labor announces that Nonfarm Payrolls increased by 303,000 in March, higher than the anticipated 200,000 and the previous 270,000.

Further details revealed that the Unemployment Rate decreased modestly to 3.8% from 3.9%, with Average Hourly Earnings meeting consensus predictions. Average Hourly Earnings rose by 0.3% MoM, up from 0.2%. In the twelve months to March, earnings rose by 4.1% as expected, down from 4.3%.

Following these figures, the US Dollar strengthened, evidenced by a 0.15% rise in the US Dollar Index (DXY) to 104.36. US Treasury bond yields increased by about 5 basis points, with the 10-year rate reaching 4.365%.

Recently, Fed Governor Michelle Bowman stated that cutting rates too soon risks a rebound in inflation. She said that eventually, the bank would cut rates, yet inflationary risks are tilted to the upside. Earlier, Richmond Fed President Thomas Barkin described the NFP report as robust but noted that inflation reduction has been inconsistent.

Dallas Fed President Lorie Logan said there’s “no urgency” to cut borrowing costs, adding the risk of cutting too soon is higher than being late.

Geopolitical risks loom following Israel’s attack on Iran’s embassy in Syria. Iran pledged to retaliate against Israel after seven officers were killed. A further escalation could pressure Gold prices upward, with traders looking at the $2,350 figure.

World Gold Consortium reveals that the People’s Bank of China was the largest buyer of the yellow metal, increasing its reserves by 12 tonnes to 2,257 tonnes.

Technical analysis: Gold’s upside set to continue despite RSI’s overbought condition

Gold’s rally is set to continue, with buyers gathering momentum. The Relative Strength Index (RSI), although at overbought conditions past the 70.00 level, aims north. Usually when an asset has a strong uptrend, the 80 reading is seen as the overbought extreme. However, as price action doesn’t show signs of exhaustion, the $2,350 mark is up for grabs.

On the flip side, the first support level would be $2,300. A breach of the latter will expose $2,250, followed by the $2,200 mark.

Gold FAQs

Gold has played a key role in human’s history as it has been widely used as a store of value and medium of exchange. Currently, apart from its shine and usage for jewelry, the precious metal is widely seen as a safe-haven asset, meaning that it is considered a good investment during turbulent times. Gold is also widely seen as a hedge against inflation and against depreciating currencies as it doesn’t rely on any specific issuer or government.

Central banks are the biggest Gold holders. In their aim to support their currencies in turbulent times, central banks tend to diversify their reserves and buy Gold to improve the perceived strength of the economy and the currency. High Gold reserves can be a source of trust for a country’s solvency. Central banks added 1,136 tonnes of Gold worth around $70 billion to their reserves in 2022, according to data from the World Gold Council. This is the highest yearly purchase since records began. Central banks from emerging economies such as China, India and Turkey are quickly increasing their Gold reserves.

Gold has an inverse correlation with the US Dollar and US Treasuries, which are both major reserve and safe-haven assets. When the Dollar depreciates, Gold tends to rise, enabling investors and central banks to diversify their assets in turbulent times. Gold is also inversely correlated with risk assets. A rally in the stock market tends to weaken Gold price, while sell-offs in riskier markets tend to favor the precious metal.

The price can move due to a wide range of factors. Geopolitical instability or fears of a deep recession can quickly make Gold price escalate due to its safe-haven status. As a yield-less asset, Gold tends to rise with lower interest rates, while higher cost of money usually weighs down on the yellow metal. Still, most moves depend on how the US Dollar (USD) behaves as the asset is priced in dollars (XAU/USD). A strong Dollar tends to keep the price of Gold controlled, whereas a weaker Dollar is likely to push Gold prices up.

19:01

United States Consumer Credit Change below expectations ($15B) in February: Actual ($14.12B)

Aussie's reversal has been contained above 0.6555, which leaves the positive momentum intact.

The pair withstood the bullish US Dollar reaction after the NFP release.

A clear break of the 0.6620-0.6630 resistance area would confirm a trend shift.

Australian Dollar’s reversal from Thursday’s highs has been contained above the 0.6555 support area, despite the strong US Dollar reaction to the upbeat US employment data. This keeps bulls hopeful of a deeper recovery, with their focus on the resistance area above 0.6600.

US Nonfarm Payrolls increased beyond expectations in March to close a strong first quarter, although a certain moderation observed in the yearly wage growth maintains hopes of Fed cuts alive. This has put a lid on the USD rally which leaves the pair’s bullish momentum intact.

The weekly chart is forming a large bullish candle which signals a potential change in the broader bearish trend. A break of the 0.6620-0.663030 resistance area would confirm the trend change and expose the 0.6670 top. Support levels remain at 0.6555 and 0.6500.

The NZD/JPY settled at 91.12 mild losses in the Friday session.

The daily RSI reveals a steady bullish momentum.

Hourly chart indicators show a rising bullish sentiment despite some variability.

The NZD/JPY pair, with a slight decline, is currently trading at 91.12 in Friday's session.On the daily chart, the bullish momentum remains steady while the buyers are more present on the hourly timeframes.

The daily chart reveals that the Relative Strength Index (RSI) for the pair is displaying a broadly favorable trend, with a recent rise from the negative zone into positive territory. Meanwhile, the Moving Average Convergence Divergence (MACD) is producing green bars, indicating positive ascending momentum.

NZD/JPY daily chart

Turning attention to the hourly chart a similar pattern is observed in the RSI values. Despite some variability, in recent hours, the RSI remains in the positive sector, rendering the momentum chiefly bullish. The MACD supports this bullish inclination as it illustrates ascending green bars, implying intensified upward momentum on an hourly timeline.

NZD/JPY hourly chart

As for the overall trend, NZD/JPY sits above its 20,100 and 200-day Simple Moving Average (SMA), indicating a bullish stance in the long run.

In summary, as the daily and hourly RSI indicators, in conjunction with the MACD's green bars, the momentum favors the buyers. However, some flatness was seen in the daily indicators but as long as the pair remains above its main SMAs, the outlook will be positive.

Mexican Peso strengthens against US Dollar, with USD/MXN dropping to 16.48 in reaction to upbeat US labor market figures.

Despite a robust US jobs report, increased risk appetite drives equity gains, a tailwind for the Mexican currency.

Fed officials maintain a cautious stance on rate adjustments, influencing market expectations for future monetary policy direction.

The Mexican Peso rallied sharply to a nine-year high on Friday after the release of a stronger-than-expected jobs report in the United States (US). Although the USD/MXN trimmed some of its losses at the release, the Peso’s resilience pressured the US Dollar. The exotic pair is currently trading at 16.48 after hitting a daily high of 16.60.

The USD/MXN main driver is an improvement in risk appetite even though US Nonfarm Payrolls (NFP) for March exceeded estimates and the previous month's data. That didn’t stop traders from pushing US equities higher amid a rise in US Treasury bond yields and the US Dollar. Digging deep into the report, unemployment figures dipped, while Average Hourly Earnings were mixed. Monthly figures increased, but in the twelve months to the data, they dipped.

Given the fundamental backdrop, the swaps market suggests the US Federal Reserve will likely cut rates in July 2024. Still, the first “fully” priced-in rate cut is expected in September.

Elsewhere, Federal Reserve officials continued to emphasize that patience is needed and that they’re not in a rush to ease policy. Dallas Fed President Lorie Logan said there’s “no urgency” to cut borrowing costs, adding the risks of cutting too soon are higher than of those being late.

Daily digest market movers: Mexican Peso soars, ignoring upbeat US economic data

The National Statistics Agency (INEGI) revealed that Mexico’s Auto Exports decreased from 22.6% in January to 4.9% in March. Additionally, Automobile Production in March plunged to a -12.8% reading from a previous 7.8% expansion, fueled by the impact of higher interest rates set by the Bank of Mexico (Banxico).

Banxico’s minutes highlighted that Deputy Governor Irene Espinosa dissented based on inflation expectations being above the central bank’s target. The central bank lowered rates by 25 bps in March to 11.00%. Despite that, the Governing Council stated that it would remain vigilant about inflation and remain data-dependent in upcoming meetings.

The US Bureau of Labor Statistics announced March's Nonfarm Payrolls exceeded expectations, with a significant increase of 303K jobs compared to the anticipated 200K and the previous 270K.

The Unemployment Rate decreased slightly to 3.8% from 3.9% with Average Hourly Earnings meeting consensus predictions.

Following these figures, the US Dollar strengthened, evidenced by a 0.155% rise in the US Dollar Index (DXY) to 104.36. US Treasury bond yields increased by about 5 basis points, with the 10-year rate reaching 4.365%.

Recently, Fed Governor Michelle Bowman stated that cutting rates too soon risks a rebound in inflation. She said that eventually, the bank would cut rates, yet inflationary risks are tilted to the upside. Earlier, Richmond Fed President Thomas Barkin described the NFP report as robust but noted that inflation's reduction has been inconsistent.

Technical analysis: Mexican Peso eyes October’s 2015 high

The USD/MXN extended its losses toward the 16.40 region, though bears are gathering momentum with the Relative Strength Index (RSI) moving back below the 35.00 area, opening the door for further gains in the Peso. A breach of 16.43 would expose October’s 2015 low of 16.32, ahead of the 16.00 mark.

On the flip side, If USD/MXN bulls stepped in, they must reclaim 16.70. Once cleared, the next resistance would be the 50-day Simple Moving Average (SMA) at 16.89, with further upside seen at the 100-day SMA at 17.01, ahead of the 200-day SMA at 17.17.

Mexican Peso FAQs

The Mexican Peso (MXN) is the most traded currency among its Latin American peers. Its value is broadly determined by the performance of the Mexican economy, the country’s central bank’s policy, the amount of foreign investment in the country and even the levels of remittances sent by Mexicans who live abroad, particularly in the United States. Geopolitical trends can also move MXN: for example, the process of nearshoring – or the decision by some firms to relocate manufacturing capacity and supply chains closer to their home countries – is also seen as a catalyst for the Mexican currency as the country is considered a key manufacturing hub in the American continent. Another catalyst for MXN is Oil prices as Mexico is a key exporter of the commodity.

The main objective of Mexico’s central bank, also known as Banxico, is to maintain inflation at low and stable levels (at or close to its target of 3%, the midpoint in a tolerance band of between 2% and 4%). To this end, the bank sets an appropriate level of interest rates. When inflation is too high, Banxico will attempt to tame it by raising interest rates, making it more expensive for households and businesses to borrow money, thus cooling demand and the overall economy. Higher interest rates are generally positive for the Mexican Peso (MXN) as they lead to higher yields, making the country a more attractive place for investors. On the contrary, lower interest rates tend to weaken MXN.

Macroeconomic data releases are key to assess the state of the economy and can have an impact on the Mexican Peso (MXN) valuation. A strong Mexican economy, based on high economic growth, low unemployment and high confidence is good for MXN. Not only does it attract more foreign investment but it may encourage the Bank of Mexico (Banxico) to increase interest rates, particularly if this strength comes together with elevated inflation. However, if economic data is weak, MXN is likely to depreciate.

As an emerging-market currency, the Mexican Peso (MXN) tends to strive during risk-on periods, or when investors perceive that broader market risks are low and thus are eager to engage with investments that carry a higher risk. Conversely, MXN tends to weaken at times of market turbulence or economic uncertainty as investors tend to sell higher-risk assets and flee to the more-stable safe havens.

17:14

United States Baker Hughes US Oil Rig Count: 508 vs 506

The Pound has trimmed retraced post-NFP lows and is practically flat on the daily chart.

Nonfarm Payrolls data shows that the US economy remains creating employment at a strong pace.

A frail economic outlook and softer inflationary pressures are weighing on the Pound.

The Sterling is regaining lost ground on Friday’s US session following a significant reversal, with a strong US employment report sending the Dollar soaring. The pair, however, remains practically flat in the weekly chat after having whipsawed over the last few days.

US Nonfarm Payrolls increased by 303K in March beating expectations of a 200K increase to close a stellar quarter for employment. Wage inflation has continued growing, although the moderation observed in the yearly rate, which has eased to 4.1% from 4.3% in the previous month has eased concerns about a hawkish steer by the Federal Reserve.

In the UK the weak services sector activity data seen this week adds to the evidence of an uncertain economic outlook. The weak GDP and the slowing price pressures boosted speculation that the BoE might anticipate the first rate cuts, which is weighing on the Pound.

The technical picture remains bearish, with resistance at 1.2675 holding buyers ahead of 1.2755. support levels are 1.2575 and 1.2535.

The DXY Index rallied to 104.60 and then stabilized at 104.30.

The BLS reported higher-than-expected NFP employment figures from March.

US Treasury yields soared after the release of the labor data.

The US Dollar Index (DXY) is currently trading at 104.30, trimming steep initial gains on Friday following a surprising beat from the Nonfarm Payrolls (NFP) report. The strong labor market scene, underscored by the better-than-anticipated NFP report for March, solidifies the Dollar's bullish outlook. That being said, the odds of a rate cut in June from the Federal Reserve (Fed) remain high and steady.

US Economic data will continue to guide the timing of the Fed's easing cycle, with consensus still pointing to a June initiation. Next week, markets will eye Consumer Price Index (CPI) figures for March.

Daily digest market movers: DXY soars as labor market data exceeds expectations

The US Bureau of Labor Statistics (BLS) announced an increase of 303K in March jobs, which greatly surpassed the expected 200K.

February's previous NFP growth of 275K was revised downward to 200K.

There was a minor drop in the Unemployment Rate from 3.9% to 3.8%.

The Labor Force Participation Rate witnessed a slight bump from 62.5% to 62.7%.

The annual rate of wage inflation, illustrated by Average Hourly Earnings, was adjusted down to 4.1%, aligning with forecasts.

Regarding the Fed’s stance, officials from the Fed are advising patience before decreasing rates, delivering a mild reinforcement for the USD.

Regardless of this, the market continues to project a June rate cut at around a 70% likelihood, followed by an approximated total easing of roughly 75bps this year.

US Treasury yields are rising with the 2-year yield at 4.70%, the 5-year yield at 4.35%, and the 10-year yield at 4.36%.

DXY technical analysis: DXY manifests bullish momentum domination in short-term outlook

As the indicators on the daily chart reflect, the DXY indicates a positive inclination with a favorable tilt on the Relative Strength Index (RSI). The RSI is currently exhibiting a positive slope in positive territory, which echoes the bullish force’s dominance over selling pressure in the immediate scenario. Meanwhile, the Moving Average Convergence Divergence (MACD), despite having flat green bars, still supports the bullish prospects.

Furthermore, the index position concerning its Simple Moving Averages (SMAs) further corroborates this assertion. The DXY positioning above the 20, 100, and 200-day Simple Moving Averages (SMAs) suggests the bulls are asserting their control. As long as the index remains above these levels, the buyers have reason to remain optimistic.

US Dollar FAQs

The US Dollar (USD) is the official currency of the United States of America, and the ‘de facto’ currency of a significant number of other countries where it is found in circulation alongside local notes. It is the most heavily traded currency in the world, accounting for over 88% of all global foreign exchange turnover, or an average of $6.6 trillion in transactions per day, according to data from 2022. Following the second world war, the USD took over from the British Pound as the world’s reserve currency. For most of its history, the US Dollar was backed by Gold, until the Bretton Woods Agreement in 1971 when the Gold Standard went away.

The most important single factor impacting on the value of the US Dollar is monetary policy, which is shaped by the Federal Reserve (Fed). The Fed has two mandates: to achieve price stability (control inflation) and foster full employment. Its primary tool to achieve these two goals is by adjusting interest rates. When prices are rising too quickly and inflation is above the Fed’s 2% target, the Fed will raise rates, which helps the USD value. When inflation falls below 2% or the Unemployment Rate is too high, the Fed may lower interest rates, which weighs on the Greenback.

In extreme situations, the Federal Reserve can also print more Dollars and enact quantitative easing (QE). QE is the process by which the Fed substantially increases the flow of credit in a stuck financial system. It is a non-standard policy measure used when credit has dried up because banks will not lend to each other (out of the fear of counterparty default). It is a last resort when simply lowering interest rates is unlikely to achieve the necessary result. It was the Fed’s weapon of choice to combat the credit crunch that occurred during the Great Financial Crisis in 2008. It involves the Fed printing more Dollars and using them to buy US government bonds predominantly from financial institutions. QE usually leads to a weaker US Dollar.

Quantitative tightening (QT) is the reverse process whereby the Federal Reserve stops buying bonds from financial institutions and does not reinvest the principal from the bonds it holds maturing in new purchases. It is usually positive for the US Dollar.

Dow Jones trims losses following upbeat US employment data.

A moderate slowdown in the yearly wage growth has eased investors’ concerns about the strong employment reading.

The sharp reversal in the weekly chart suggests that a deeper correction might be in progress.

The Dow Jones Industrial Average (DJIA) traded higher in Friday’s morning session, following upbeat US employment figures. The index, however, is on track for its worst week in the last year as the strong US economic data has put the Federal Reserve’s (Fed) easing plans into question.

Net employment increased in March by 303K, following a 270,000 increment in February and beating expectations of about a 200K rise. Wage figures revealed that salaries keep rising although the moderation in the annual rate seems to have eased investors’ concerns.

On Thursday, Minneapolis Fed President Neel Kashkari suggested that with inflation steady at high levels the bank might refrain from cutting rates this year, which sent equity markets tumbling.

The main Wall Street indices are all positive on Friday. The NASDAQ is leading with a 1.38% advance to 16,271, followed by the S&P 500, up 1.17% at 5,207, and the Dow Jones, which adds 0.9% to 38,943.

Dow Jones news

All sectors are posting gains with Communication Services leading thanks to a 1.94% advance, followed by the Technology sector with a 1.64% gain. Industrials has gained 1.41%. The Utilities sector is the worst performer with a 0.31% advance.

Amazon (AMZN) is leading gains on Friday with a 3.17% rally to $185.66, followed by Salesforce (CRM), which advances 2.57% to $301.68. On the losing end, Intel (INTC) drops 2.16% to $38.87, still weighed down by the hefty losses reported for 2023. Next is McDonald’s (MCD) with a 0.86% decline to $267.777.

Dow Jones technical outlook

The index is trimming some losses on Friday, but the sharp reversal printed in the previous four trading days is forming a bearish engulfing candle on the weekly chart.

This formation often anticipates a major reversal. Price action has found demand above 38,500 to bounce up, but buyers might be challenged at the 39,265 resistance, which closes the path to the 40,000 top.

On the downside, a break of the 34,452 level would confirm a trend reversal and increase bearish pressure toward 38,035.

Dow Jones 4-Hour Chart

Employment FAQs

Labor market conditions are a key element to assess the health of an economy and thus a key driver for currency valuation. High employment, or low unemployment, has positive implications for consumer spending and thus economic growth, boosting the value of the local currency. Moreover, a very tight labor market – a situation in which there is a shortage of workers to fill open positions – can also have implications on inflation levels and thus monetary policy as low labor supply and high demand leads to higher wages.

The pace at which salaries are growing in an economy is key for policymakers. High wage growth means that households have more money to spend, usually leading to price increases in consumer goods. In contrast to more volatile sources of inflation such as energy prices, wage growth is seen as a key component of underlying and persisting inflation as salary increases are unlikely to be undone. Central banks around the world pay close attention to wage growth data when deciding on monetary policy.

The weight that each central bank assigns to labor market conditions depends on its objectives. Some central banks explicitly have mandates related to the labor market beyond controlling inflation levels. The US Federal Reserve (Fed), for example, has the dual mandate of promoting maximum employment and stable prices. Meanwhile, the European Central Bank’s (ECB) sole mandate is to keep inflation under control. Still, and despite whatever mandates they have, labor market conditions are an important factor for policymakers given its significance as a gauge of the health of the economy and their direct relationship to inflation.

Another positive week saw the Greenback reclaim the area beyond the 104.00 hurdle, advancing modestly on a weekly basis against the backdrop of the mixed performance in US yields and Fedspeak supporting a tighter-for-longer Fed’s stance.

Stronger-than-expected NFP readings lent support to the Greenback at the end of the week. The RCM/TIPP Economic Optimism Index is due on April 9, seconded by the Inflation Rate, Wholesale Inventories, and FOMC Minutes, all expected on April 10. On the next day, Producer Prices are due, and the preliminary Michigan Consumer Sentiment will close the week on April 12.

EUR/USD managed to reclaim the area above 1.0800, mostly on the back of Dollar weakness and risk appetite trends in the first part of the week. Germany’s Balance of Trade results are due on April 8, followed by the ECB meeting on April 11, and the final German Inflation Rate on April 12.

GBP/USD ended Friday’s session on the defensive, coming under pressure in the second half of the week on the back of the late bounce in the Greenback. The UK docket will see the BRC Retail Sales Monitor on April 9 ahead of GDP readings, Balance of Trade, Construction Output, and Industrial and Manufacturing Production, all due on April 12.

USD/JPY maintained its consolidation range below the 152.00 region once again this past week, always amidst persistent FX intervention fears. On April 8, the Eco Watchers Survey is due, along with Consumer Confidence on April 9. Additionally, Bank Lending figures and Producer Prices are expected on April 10, while Foreign Bond Investment and final Industrial Production are due on April 11 and April 12, respectively.

In quite a volatile week, AUD/USD revisited the area above 0.6600 the figure, although it ran out of some upside impetus towards the end of the week. On April 8, Home Loans are due ahead of the Westpac Consumer Confidence Index on April 9. Additionally, consumer inflation expectations come on April 11.

Anticipating Economic Perspectives: Voices on the Horizon

BoE’s Breeden speaks on April 8.

Fed’s Kashkari speak on April 9.

Fed’s Goolsbee is due to speak on April 10.

Fed’s Williams, Collins and Bostic speak on April 11 along with BoE’s Greene.

BoE’s Greene, Fed’s Bostic and Daly all speak on April 12.

Central Banks: Upcoming Meetings to Shape Monetary Policies

Canadian Dollar drops for second consecutive day amid higher US Dollar.

Strong US employment data boosts US Treasury yields, US Dollar.

In Canada, strong Ivey PMI data eases downside pressure on Canadian Dollar after disappointing labour figures.

The Canadian Dollar (CAD) extends its losses on Friday following Thursday’s pullback to test fresh year-to-date lows. A combination of a stellar US employment report and weak Canadian labor figures have undermined investors’ confidence in an already weak Loonie.

Data released by the US Labor Department on Friday shows the US economy created employment well above expectations in March. Beyond that, wages continued growing at a steady pace, well above levels consistent with the Federal Reserve’s (Fed) 2% inflation target.

These figures pour cold water on market hopes of interest rate cuts in June and endorse the hawkish party of the central bank, which advocates for delaying and downsizing the easing cycle. This has sent US yields higher, dragging the US Dollar up with them.

In Canada, net employment levels have declined against expectations in March. The negative impact, however, has been offset by the strong improvement of March’s Ivey PMI, which has given some support to an ailing Canadian Dollar.

Daily digest market movers: USD/CAD dips further as US NFP beat expectations

The Canadian Dollar has lost more than 0.5% over the last two days, retracing last week’s gains and reaching its lowest price since December 2023.

US Nonfarm Payrolls increased by 303K in March from 270K in February, well above the 200K forecasted by market experts.

Average Hourly Earnings have increased at a 0.3% monthly pace and 4.1% year on year from 0.2% and 4.3% respectively in February.

Canadian Ivey Purchasing Managers’ Index has improved to 57.7, its best reading over the last 12 months, from 53.9 in February.

Somewhat earlier, Canadian employment data disappointed investors with a 2.2K decline in March after a 40.7K increase in February. The market was expecting a 25K increase.

On Thursday, Fed Powell reiterated that the central bank needs more time to decide on rate cuts, while Fed Kashkhari warned that there might not be any rate cut this year, which sent the USD higher.

Canadian Dollar price today

The table below shows the percentage change of Canadian Dollar (CAD) against listed major currencies today. Canadian Dollar was the strongest against the Japanese Yen.

USD

EUR

GBP

CAD

AUD

JPY

NZD

CHF

USD

-0.06%

0.08%

0.32%

0.10%

0.21%

0.16%

-0.15%

EUR

0.05%

0.10%

0.36%

0.15%

0.26%

0.21%

-0.11%

GBP

-0.08%

-0.14%

0.23%

0.03%

0.14%

0.08%

-0.24%

CAD

-0.29%

-0.35%

-0.23%

-0.19%

-0.08%

-0.13%

-0.44%

AUD

-0.09%

-0.15%

-0.01%

0.23%

0.12%

0.07%

-0.26%

JPY

-0.22%

-0.27%

-0.15%

0.06%

-0.13%

-0.05%

-0.38%

NZD

-0.17%

-0.21%

-0.09%

0.14%

-0.07%

0.04%

-0.34%

CHF

0.14%

0.09%

0.24%

0.46%

0.25%

0.37%

0.33%

The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the Euro from the left column and move along the horizontal line to the Japanese Yen, the percentage change displayed in the box will represent EUR (base)/JPY (quote).

Technical analysis: USD/CAD has tested resistance at the 1.3640 area

The strong US employment data has sent the USD/CAD to test an important resistance area above 1.3620, which so far remains intact, as positive Canadian PMI data has eased bullish pressure on the pair.=

The overall picture shows the US Dollar trading back and forth within an ascending channel with price action capped below trendline resistance at 1.3640. Above here, the next targets are 2.3710 and 1.3770. The channel’s measured target is 1.3845. Support levels are 1.3560 and 1.3485.

USD/CAD 4-Hour Chart

Employment FAQs

Labor market conditions are a key element to assess the health of an economy and thus a key driver for currency valuation. High employment, or low unemployment, has positive implications for consumer spending and thus economic growth, boosting the value of the local currency. Moreover, a very tight labor market – a situation in which there is a shortage of workers to fill open positions – can also have implications on inflation levels and thus monetary policy as low labor supply and high demand leads to higher wages.

The pace at which salaries are growing in an economy is key for policymakers. High wage growth means that households have more money to spend, usually leading to price increases in consumer goods. In contrast to more volatile sources of inflation such as energy prices, wage growth is seen as a key component of underlying and persisting inflation as salary increases are unlikely to be undone. Central banks around the world pay close attention to wage growth data when deciding on monetary policy.

The weight that each central bank assigns to labor market conditions depends on its objectives. Some central banks explicitly have mandates related to the labor market beyond controlling inflation levels. The US Federal Reserve (Fed), for example, has the dual mandate of promoting maximum employment and stable prices. Meanwhile, the European Central Bank’s (ECB) sole mandate is to keep inflation under control. Still, and despite whatever mandates they have, labor market conditions are an important factor for policymakers given its significance as a gauge of the health of the economy and their direct relationship to inflation.

A robust US Nonfarm Payrolls report for March propels the Greenback higher, impacting the EUR/USD.

The Eurozone's mixed economic indicators, including Germany's Factory Orders and Retail Sales, contrast with the strong US employment landscape.

Further downside seen at EUR/USD as technical suggests potential for declines below the 1.0800 threshold.

The Euro registers minimal losses of 0.13% following the release of a stronger-than-expected jobs report from the United States (US) that boosted the Greenback, sending the EUR/USD lower. At the time of writing, the pair trades at 1.0822 after hitting a daily high of 1.0847.

EUR/USD slides as upbeat US labor market data fuels US Dollar rally

On Friday, the US Bureau of Labor Statistics (BLS) revealed that the economy added more jobs than expected. Nonfarm Payrolls for March rose by 303K, crushing estimates and previous readings of 200K and 270K. Further data showed the Unemployment Rate ticking lower from 3.9% to 3.8%, while Average Hourly Earnings were aligned to the consensus.

After the data, the Greenback strengthens as the US Dollar Index (DXY) rises 0.155%, up at 04.36. US Treasury bond yields are climbing between 4.5 and 5 basis points. The US 10-year Treasury note rate is at 4.365%.

Elsewhere, the Richmond Fed President Thomas Barkin commented the rpoert was quite strong, adding that the reduction in inflation has been uneven. Earlier. Fed’s Boston Susan Collins made comments but not on monetary policy.

Across the pond, Factory Orders in Germany improved in February, to 0.2%, improving from January’s -1.4% plunge. Moreover, Retail Sales from the Eurozone (EU) dived -0.5% MoM, worse than the estimated -0.4% contraction.

Given those factors, the EUR/USD retreated below the 200-day moving average (DMA). Traders' focus shifts to next week's data, with the release of US inflation data and consumer sentiment. On the EU’s front, the European Central Bank (ECB) will feature its monetary policy meeting, which will be the highlight of the week.

EUR/USD Price Analysis: Technical outlook

The formation of an ‘evening star’ chart pattern could pave the way for a drop below the 1.0800 figure. Momentum in the EUR/USD is tilted to the downside as the Relative Strength Index (RSI) aims lower and beneath the 50-midline level. A breach below 1.0800 will expose the April 2 low of 1.0724, ahead of 1.0700. On the other hand, buyers will face stirring resistance at the confluence of the 50 and 200-DMAs at around 1.0828/32.

Euro FAQs

The Euro is the currency for the 20 European Union countries that belong to the Eurozone. It is the second most heavily traded currency in the world behind the US Dollar. In 2022, it accounted for 31% of all foreign exchange transactions, with an average daily turnover of over $2.2 trillion a day. EUR/USD is the most heavily traded currency pair in the world, accounting for an estimated 30% off all transactions, followed by EUR/JPY (4%), EUR/GBP (3%) and EUR/AUD (2%).

The European Central Bank (ECB) in Frankfurt, Germany, is the reserve bank for the Eurozone. The ECB sets interest rates and manages monetary policy. The ECB’s primary mandate is to maintain price stability, which means either controlling inflation or stimulating growth. Its primary tool is the raising or lowering of interest rates. Relatively high interest rates – or the expectation of higher rates – will usually benefit the Euro and vice versa. The ECB Governing Council makes monetary policy decisions at meetings held eight times a year. Decisions are made by heads of the Eurozone national banks and six permanent members, including the President of the ECB, Christine Lagarde.

Eurozone inflation data, measured by the Harmonized Index of Consumer Prices (HICP), is an important econometric for the Euro. If inflation rises more than expected, especially if above the ECB’s 2% target, it obliges the ECB to raise interest rates to bring it back under control. Relatively high interest rates compared to its counterparts will usually benefit the Euro, as it makes the region more attractive as a place for global investors to park their money.

Data releases gauge the health of the economy and can impact on the Euro. Indicators such as GDP, Manufacturing and Services PMIs, employment, and consumer sentiment surveys can all influence the direction of the single currency. A strong economy is good for the Euro. Not only does it attract more foreign investment but it may encourage the ECB to put up interest rates, which will directly strengthen the Euro. Otherwise, if economic data is weak, the Euro is likely to fall. Economic data for the four largest economies in the euro area (Germany, France, Italy and Spain) are especially significant, as they account for 75% of the Eurozone’s economy.

Another significant data release for the Euro is the Trade Balance. This indicator measures the difference between what a country earns from its exports and what it spends on imports over a given period. If a country produces highly sought after exports then its currency will gain in value purely from the extra demand created from foreign buyers seeking to purchase these goods. Therefore, a positive net Trade Balance strengthens a currency and vice versa for a negative balance.

“I believe it’s much too soon to think about cutting interest rates,” Federal Reserve Bank of Dallas President Lorie Logan said on Friday, citing upside risks to inflation.

Key takeaways

"Need to see more of the uncertainty resolved about which economic path we’re on."

"Increasingly concerned about upside risk to the inflation outlook."

"FOMC should remain prepared to respond appropriately if inflation stops falling."

"Difficult to predict exactly when overnight reverse repo balances will be depleted."

"Believe it will soon be appropriate for the FOMC to decide when to slow - not stop - the runoff of our asset holdings."

"Slower but still meaningful run-off pace will provide more time for banks and money market participants to redistribute liquidity and for the Fed to assess liquidity conditions."

"Taper will also reduce the risk of going too far."

"Taper should not have much effect on broader financial conditions."

"Taper is unrelated to considerations of the appropriate degree of policy restriction."

"Not ready to put higher trend productivity in my baseline outlook."

Market reaction

The US Dollar Index clings to modest daily gains near 104.40 following these comments.

GBP/JPY fades as UK-Japan interest rates are expected to converge.

In the UK, falling inflation is expected to lead to lower interest rates.

In Japan rising inflation is increasingly expected to lead to higher interest rates.

GBP/JPY trades a tenth of a percent lower on Friday, at just above 191.000, as converging UK-Japan interest rate expectations reduce the advantage for investors of holding the Pound Sterling (GBP) over the Japanese Yen (JPY), weighing on the exchange rate.

Easing inflation expectations in the UK have led investors to speculate that the Bank of England (BoE) will cut interest rates in June. This has weakened the Pound Sterling since lower interest rates tend to reduce foreign capital inflows.

Conversely in Japan, the Bank of Japan increased interest rates from an extraordinarily low, negative 0.1% level, at the bank’s March meeting. The move had many investors speculating as to whether the increase was a one-off or the start of a cycle of rate hikes that could strengthen the Yen over the longer run.

In a recent interview with the Asahi Shimbun, Bank of Japan (BoJ) Governor Ueda seemed to suggest more interest rate hikes could be down the road given accelerating inflation.

Ueda said the positive results of the Shunto spring wage negotiations will be reflected in wages through the summer, and then reflected in higher consumer prices later in the year.

"Given annual wage talks outcome so far, trend inflation is likely to gradually accelerate," said Ueda.

Survey shows UK inflation cooling

In the UK meanwhile, the latest Bank of England (BoE) Decision Maker Panel (DMP) survey for February showed that most firms see selling prices and wage inflation cooling over the next year.

According to the DMP survey, selling price expectations decelerated to 4.1% from 4.3%, the lowest reading in over two years. Wage growth expectations softened to 4.9% on a three-month moving average basis from 5.2% in February.

Bank of England Governor Andrew Bailey recently said that market expectations for two or three rate cuts this year are “reasonable”, further increasing speculation the BoE will pull the trigger and cut rates in June.

Soft Services PMI data for March, released on Thursday, impacted the economic outlook for the UK, adding to the reasons for the BoE to cut interest rates.

The UK Services PMI fell to 53.1, missing expectations and the prior reading of 53.4.

Nevertheless, not all UK data was negative. A recent report by the UK’s largest building society Nationwide showed the first rise in house prices since January 2023, according to the Guardian.

This comes after BoE lending data showed a surprise rise in Mortgage Approvals rising to their highest level since September 2022 in February.

14:32

Turkey Treasury Cash Balance up to -166.78B in March from previous -198.34B

USD/CAD rallies on strong US NFP, weak Canadian labor market data.

The speculation for Fed to begin rate cuts could be shifted to the second half of this year.

Canadian labors were fired over March. The jobless rate rose to 6.1%.

The USD/CAD pair prints a fresh four-month high at 1.3640 in Friday’s early American session. The Loonie asset rallies as the United States Bureau of Labor Statistics (BLS) has reported upbeat Nonfarm Payrolls and the Statistics Canada has showed poor Employment data for March.

The US NFP reported that the labor market witnessed 303K fresh payrolls, significantly better than expectations of 200K and the prior reading of 270K. The Unemployment Rate falls to 3.8% from the consensus and the prior reading of 3.9%. Strong labor demand has dented market expectations for the Federal Reserve (Fed) to begin reducing interest rates, which is currently expected from the June meeting.

Robust labor demand is generally followed by strong wage growth as employers are forced to offer higher pay due to shortage of workers. Higher wage growth boosts consumer spending, which keeps inflation stubbornly higher.

On Thursday, Minneapolis Fed Bank President Neel Kashkari said rate cuts won’t be required this year if inflation remains stall. Neel Kashkari forecasted two rate cuts by 2024 in the latest Fed’s dot plot.

Upbeat labor demand has boosted the US Dollar’s appeal. The US Dollar Index (DXY), which tracks the US Dollar’s value against six major currencies, extends its upside to 104.65.

Meanwhile, the Canadian Dollar weakens as workers were laid-off over month. Canada’s labor market witnessed drawdown of 2.2K workers, which investors forecasted fresh recruitment of 25K jobs. The Unemployment Rate rose strongly to 6.1% from expectations of 5.9% and the prior reading of 5.8%. However, annual Average Hourly Earnings grew at a higher pace of 5.0% from 4.9% in February.

Weak labor demand will boost expectations for the Bank of Canada (BoC) pivoting to rate cuts sooner.

USD/CAD

Overview

Today last price

1.3625

Today Daily Change

0.0083

Today Daily Change %

0.61

Today daily open

1.3542

Trends

Daily SMA20

1.3539

Daily SMA50

1.3513

Daily SMA100

1.3487

Daily SMA200

1.3503

Levels

Previous Daily High

1.3559

Previous Daily Low

1.3478

Previous Weekly High

1.3614

Previous Weekly Low

1.3525

Previous Monthly High

1.3614

Previous Monthly Low

1.342

Daily Fibonacci 38.2%

1.3528

Daily Fibonacci 61.8%

1.3509

Daily Pivot Point S1

1.3494

Daily Pivot Point S2

1.3445

Daily Pivot Point S3

1.3413

Daily Pivot Point R1

1.3575

Daily Pivot Point R2

1.3608

Daily Pivot Point R3

1.3656

14:00

Canada Ivey Purchasing Managers Index s.a came in at 57.5, above expectations (54.2) in March

The release of stronger-than-expected Nonfarm Payrolls data has not changed the view of economists at RBC that the Federal Reserve will start cutting interest rates in June.

Risks are, however, now tilted in favor of a delay.

Robust hiring means risks tilting to a delay

“Robust hiring in US labor markets has yet to let up with payroll employment growth accelerating to 303k in March from already solid readings in the months before.”

“Despite solid headline numbers, the Fed has been pointing to other indicators such as lower quit rate, falling job openings and moderating wage growth as signs of tight labor market conditions unwinding, and has maintained the assessment that risks with its dual mandate are coming into better balance.”

“The choppier the progress with inflation (as it has been in early 2024), the longer the Fed will need to hold rates steady.”

“Our own base-case assumption is that the first rate cut will come in June, with risks tilting to a delay.”

The release of more stellar US jobs data in the form of March Nonfarm Payrolls (NFP), has further reduced the chances of the Federal Reserve (Fed) making a first interest-rate cut in June, according to economists at Commerzbank.

Rate cut in first half of 2024 increasingly unlikely

“The US labor market has once again exceeded expectations.”

“The downright astonishing strength of the labor market makes a first rate cut by the Fed already in the first half of the year increasingly unlikely.”

“Fed Chair Powell regularly points out that the imbalance between supply and demand in the labor market is gradually reducing, which lowers the risk of inflation. However, the new figures do not really support this theory, as job growth has been on the rise again since fall 2023. This indicates that the economy remains very robust. There is therefore no need to rush to cut key interest rates - a narrow majority of Fed members recently still expected three rate cuts later in the year.”

“Consumer price data for March will be published next week. Once again, we expect prices to rise a little too strongly for the Fed's liking.”

“All in all, a first rate cut at the June meeting, which we still expect, is becoming less likely. The timing of the first cut is likely to be determined primarily by the further development of inflation.”

12:32

United States Labor Force Participation Rate climbed from previous 62.5% to 62.7% in March

12:32

United States Unemployment Rate came in at 3.8%, below expectations (3.9%) in March

12:32

United States Average Hourly Earnings (MoM) in line with expectations (0.3%) in March

12:32

Canada Net Change in Employment below forecasts (25K) in March: Actual (-2.2K)

12:31

Canada Unemployment Rate came in at 6.1%, above forecasts (5.9%) in March

12:31

United States Nonfarm Payrolls came in at 303K, above expectations (200K) in March

12:31

Canada Participation Rate remains unchanged at 65.3% in March

12:30

United States Average Hourly Earnings (YoY) in line with expectations (4.1%) in March

12:30

United States Average Weekly Hours came in at 34.4, above expectations (34.3) in March

12:30

United States U6 Underemployment Rate: 7.3% (March)

USD/JPY is expected to rally above its current range in the 151.000s, according to Strategists at BBH.

A combination of very gradual BoJ tightening and a more muted than currently priced-in Federal Reserve (Fed) easing cycle are the fundamental catalysts.

USD/JPY falls due to Ueda – will rise eventually

“USD/JPY fell by over 0.50% to an intra-day low around 150.80 following hawkish comments from BOJ Governor Ueda.”

“Verbal defense on the Yen continues as Japanese Finance Minister Suzuki and Prime Minister Kishida both warned against excessive yen moves.”

“It’s only a matter of time before USD/JPY breaks higher because we anticipate a gradual BOJ tightening process and a more muted than currently priced-in Fed easing cycle.”

GBP/USD bounced off a key support level and rose up strongly this week.

Resistance from two major Moving Averages, however, prevented the trend from going higher.

A clear break above this resistance barrier would be required to confirm a move up to the range highs.

GBP/USD has just bounced off the bottom of a medium-term consolidation range after forming a bullish Tweezer Bottom Japanese candlestick pattern.

The pair rose up strongly on Wednesday and Thursday but then hit stubborn resistance at the intersection of two major moving averages – the red 50-day and blue 100-day Simple Moving Averages (SMA) – and stalled.

Pound Sterling versus US Dollar: Daily chart

The pair formed a bearish Shooting Star candlestick pattern on Thursday and is now trading just beneath it in the 1.2630s.

Given the firm floor of support at the 1.2550s, which has shown itself able to prop up price on at least three occasions since November 2023 it is likely to hold again, and the pair could be at the start of another move back up inside the range.

However, the Moving Average Convergence/ Divergence (MACD) indicator, which is an especially useful confirmation tool for turning points in a range-bound market, has still not crossed its signal line to offer a buy signal.

The 50 and 100 SMAs are also still providing a formidable resistance blockade above price, and ideally need to be penetrated decisively before a more bullish outlook can be adopted.

A decisive breakthrough above the two SMAs – by which is meant a long green candlestick that breaches the resistance and closes near its high, or three green candlesticks that break through the level – would be required to confirm more upside.

The March 21 high at 1.2804 presents as a possible target for such a revolution.

Alternatively, a decisive break below the range low at 1.2550 would lead to a volatile move lower, since support that has been retested on several occasions, when finally broken, usually ends up giving way in a dramatic fashion.

12:01

India Bank Loan Growth declined to 20.2% in March 18 from previous 20.4%

12:01

India FX Reserves, USD up to $645.58B in March 25 from previous $642.63B

The US Dollar Index trades slow and steady as traders step aside to wait for key US data.

The US Labor Report could inject some volatility into DXY if it changes inflation expectations.

Recent commentary from Fed officials has shown vacillation and delay in deciding on whether to cut interest rates.

The US Dollar Index (DXY) seesaws between tepid gains and losses on Friday as traders sit on the sidelines prior to the release of market moving data from the US.

If the key Labor Market metric paints a positive picture for the labor market it should support the US Dollar, pushing up the DXY.

Alternatively a weak showing in the report would have the opposite effect, pushing down the Dollar Index.

Pay-roll day

Economists expect the headline figure to show the US economy added 200,000 jobs in the month of March after adding 275,000 in February. If the real figure is substantially above this – by a margin of more than 10%, say – it is likely to pressure the DXY higher.

Positive employment growth in the US, which already has a relatively tight labor market, will suggest upward pressure on wages and higher inflation. Higher inflation means the US Federal Reserve (Fed) will have to keep its main interest rate, the Fed Funds Rate, at its current relatively high (5.5%) level for longer. Higher interest rates are positive for the US Dollar since they attract greater inflows of foreign capital.

Another important metric within the NFP report is Average Hourly Wages, since this more directly impacts inflation expectations. If this metric rises more than forecast it will push up DXY and the opposite if it falls. In the last report wages rose 4.3% YoY and expectations are for a drop to 4.1%.

Fickle rate-setters

The US Dollar Index has been broadly supported during March by a shift in the commentary coming from interest-rate-setters in the US Federal Reserve.

From previously expecting to cut the key interest rate in the US – the Fed Funds Rate – by a total of 0.75% in 2024, in three 0.25% tranches, some members of the decision-making council have changed their opinion and now see less need to cut interest rates.

Their change in view is as a result of inflation remaining higher-than-expected, especially services sector inflation and robust economic growth in the US, which has continued to show dynamism even in the face of higher borrowing costs.

The DXY recovered after a dip on Thursday after Minneapolis Federal Reserve (Fed) Bank President Neel Kashkari raised the prospect the Fed might not cut interest rates at all in 2024 if inflation remained at current levels.

“If inflation continues to move sideways, it makes me wonder if we should cut rates at all this year,” Kashkari said, despite admitting to previously penciling in two rate cuts this year.

European certainty

DXY is a trade-weighted index measuring the strength of the US Dollar versus its main counterparts. The Euro is the main contributor.

In contrast to the vacillation observed at the Fed, there appears to be more of a consensus amongst rate-setters at the European Central Bank (ECB). They are more unanimous in their desire to go ahead with a proposed interest-rate cut in June, a factor supporting DXY and weighing on the Euro (EUR).

The ECB decision, however, is likely to be dependent on whether wage data released prior to the June meeting shows a decline in wage inflation.

WTI is stuck in a tight range but is poised to close the week on a bullish note.

Supply concerns and an improved demand outlook have boosted Oil’s appeal.

US Biden criticized Ukraine for targeting Russia’s oil infrastructure.

West Texas Intermediate (WTI), futures on NYMEX, consolidate in a tight range around $86.80 in the European session on Friday. The Oil prices are set to conclude the week on a bullish time for the second straight time. The black gold sees a strong bull run in two weeks due to deepening supply concerns and expectations of a sharp revival in the global oil demand.

Escalating tensions in Eastern Europe and the Middle East have reinforced fears of oil supply risks. This week, Ukraine’s drone attacks on Russian oil refineries prompted upside risks to lower oil production, resulting in a fresh escalation in geopolitical tensions. US President Joe Biden criticized the event of Ukraine targeting Russia’s oil infrastructure as it could have drastic consequences to global oil prices.

In the Middle East region, air strikes by Israeli forces on the Iranian embassy in Damascus, resulting in the deaths of Iran's high-rank commanders, have deepened fears of Iran’s direct participation in the war in Gaza. Geopolitical tensions disrupt the supply chain, which increases the prices of various raw materials.

Meanwhile, a sharp recovery in the Manufacturing PMI in the Eurozone, the United Kingdom, and the United States has strengthened the outlook for oil demand. In the UK and the US, the Manufacturing PMI surprisingly returned to growth after contracting for more than a year. In the Eurozone, the Manufacturing PMI outperformed expectations but remains below the 50.0 threshold, which separates contraction from expansion. The oil prices have a direct relationship with the outlook of the manufacturing sector.

Going forward, investors will focus on the United States Nonfarm Payrolls (NFP) data for March, which will be published at 12:30 GMT. The labor market data will influence market expectations for the Federal Reserve (Fed) pivoting to rate cuts, which are currently expected in the June meeting.

Gold price turns sideways near all-time highs as focus shifts to the US NFP report.

The US Dollar rises as Fed Kashkari said he sees no rate cuts if inflation remains stubborn.

Escalating Middle East tensions keep safe-haven bids strong.

Gold price’s (XAU/USD) rally pauses after refreshing all-time highs near $2,305 amid uncertainty ahead of the release of the United States Nonfarm Payrolls (NFP) data for March. The labor market data is expected to influence market expectations for the Federal Reserve (Fed) rate cuts, which financial markets are currently anticipating for June.

The CME FedWatch Tool shows that traders are pricing in a 61% chance that the Fed will trim interest rates in June, an inch higher from 60% a week ago. Traders bets for Fed rate cuts remain broadly unchanged as surprisingly weak US Services PMI for March offset the negative impact of hawkish commentary from a slew of Fed policymakers. Meanwhile, 10-year US Treasury yields are up at 4.34%.

Surprisingly, the Services PMI fell to 51.4 in March, from expectations of 52.7, and the former reading was 52.6.

Meanwhile, the near-term appeal of Gold remains strong due to escalating Middle East tensions. Air strikes from Israeli forces on the Iranian embassy in Damascus, situated near Syria’s capital, have deepened fears of Iran’s participation in the Israel-Palestine war. Rising geopolitical tensions lead investors towards safe-haven assets such as Gold.

Daily digest market movers: Gold price awaits US NFP for fresh guidance

Gold price takes a breather as investors turn cautious ahead of the United States NFP report for March, which will be published at 12:30 GMT. It is anticipated that the United States employers recruited 200K jobs, lower than the robust hiring of 275K seen in February. The Unemployment Rate is anticipated to remain unchanged at 3.9%.

Investors will also focus on March's Average Hourly Earnings data to gain more insights about the inflation outlook. Economists expect monthly wage growth to have grown at a higher pace of 0.3% from 0.1% in February. Annual wage growth is forecasted to have grown by 4.1%, decelerating from the prior reading of 4.3%.

Higher wage growth could slow the progress in inflation declining towards 2%, which could negatively influence market expectations for the Federal Reserve (Fed) to begin reducing interest rates in June. If this happens, the opportunity cost of holding an investment in non-yielding assets such as Gold will increase, weighing on its price. On the contrary, slowing wage growth will strengthen Gold’s appeal.

Meanwhile, the stabilization in the US Dollar’s valuation after the Fed’s hawkish guidance on interest rates has also put slight pressure on the Gold price. The US Dollar Index (DXY) finds support from a two-week low of 103.90 after Minneapolis Fed Bank President Neel Kashkari said rate cuts won’t be required this year if inflation stalls.

Kashkari said he forecasted two rate cuts by 2024 in the latest Fed dot plot. “The Fed needs to keep interest rates higher in the range of 5.25%-5.50% if inflation remains stronger than hoped,” Kashkari warned. He added that if that still did not work, further rate increases are not off the table, but they are also not a likely scenario given what we know right now," Reuters reports.

Technical Analysis: Gold price trades near all-time highs around $2,300

Gold price falls slightly after achieving the $2,300 milestone. The near-term demand remains unabated as all short-to-long term Exponential Moving Averages (EMAs) are sloping higher. On the downside, March 21 high at $2,223 will be a major support area for the Gold price bulls.

The 14-period Relative Strength Index (RSI) near 80.00 indicates that a bullish momentum is still active. However, overbought signals have emerged.

Gold FAQs

Gold has played a key role in human’s history as it has been widely used as a store of value and medium of exchange. Currently, apart from its shine and usage for jewelry, the precious metal is widely seen as a safe-haven asset, meaning that it is considered a good investment during turbulent times. Gold is also widely seen as a hedge against inflation and against depreciating currencies as it doesn’t rely on any specific issuer or government.

Central banks are the biggest Gold holders. In their aim to support their currencies in turbulent times, central banks tend to diversify their reserves and buy Gold to improve the perceived strength of the economy and the currency. High Gold reserves can be a source of trust for a country’s solvency. Central banks added 1,136 tonnes of Gold worth around $70 billion to their reserves in 2022, according to data from the World Gold Council. This is the highest yearly purchase since records began. Central banks from emerging economies such as China, India and Turkey are quickly increasing their Gold reserves.

Gold has an inverse correlation with the US Dollar and US Treasuries, which are both major reserve and safe-haven assets. When the Dollar depreciates, Gold tends to rise, enabling investors and central banks to diversify their assets in turbulent times. Gold is also inversely correlated with risk assets. A rally in the stock market tends to weaken Gold price, while sell-offs in riskier markets tend to favor the precious metal.

The price can move due to a wide range of factors. Geopolitical instability or fears of a deep recession can quickly make Gold price escalate due to its safe-haven status. As a yield-less asset, Gold tends to rise with lower interest rates, while higher cost of money usually weighs down on the yellow metal. Still, most moves depend on how the US Dollar (USD) behaves as the asset is priced in dollars (XAU/USD). A strong Dollar tends to keep the price of Gold controlled, whereas a weaker Dollar is likely to push Gold prices up.

AUD/USD briefly broke out of a descending channel and rallied.

The rally was cut short, however, and the pair retreated back inside the channel.

If AUD/USD rebreaks above the previous high of the initial breakout rally, it will be a bullish sign.

AUD/USD has been falling in a descending channel since the March 8 high at 0.6667.

Over the last three days the pair has risen up from the base of the channel to the highs and briefly broke upper borderline on Thursday before retreating back inside.

Australian Dollar versus US Dollar: 4-hour chart

A move back above the post-breakout rally peak, at 0.6620, however, would confirm two things.

First, that the breakout from the channel was a valid bullish breakout, likely to extend higher.

Second, that the short-term trend had probably reversed from bearish to bullish.

Such a move would probably lead to a move up to a conservative target at 0.6670, calculated as the 0.618 Fibonacci extension of the height of the channel extrapolated from the breakout point higher.

Further strength could lead to the achievement of the second target at 0.6715, which is the full height (Fib. 1.000) of the channel extrapolated higher.

The Mexican Peso is edging higher on Friday after the release of the March meeting minutes.

Higher Crude Oil prices, a key Mexican export, could also be supporting the Peso.

Technically the USD/MXN pair remains in a long-term downtrend.

The Mexican Peso (MXN) trades marginally higher against the US Dollar (USD) on Friday, after the release of the Banco de Mexico’s (Banxico) March meeting minutes and amid a rise in Crude Oil prices, a key export for Mexico.

The Banxico minutes revealed a reluctance on the part of policymakers to embrace a cycle of easing, including a commitment to lowering interest rates in the future, due to continued stubborn inflation.

The prospect of interest rates remaining high in Mexico – they are currently at 11.00% – supports the Mexican Peso as it leads to higher foreign capital inflows.

Higher Crude Oil prices, with Brent Crude Oil pushing above $90 a barrel on Friday, may also have helped the Mexican Peso, given its importance as an export.

Mexican Peso supported by hawk found in Banxico

The Mexican Peso finds support and recovers after the release of the minutes of the Banxico March meeting.

Although the majority of members voted to cut interest rates by 0.25% to 11.00%, one policymaker, Irene Espinosa, voted against the cut.

Key takeaways:

In summary, the minutes highlighted how inflation, particularly in the services sector, remained stubbornly high and interest rates would therefore need to remain elevated to bring it back down to the bank’s 3.0% target.

Members considered that the balance of risks for the trajectory of inflation within the forecast horizon remains biased to the upside.

It was acknowledged that although inflation remained sticky the current environment was less adverse than that faced in 2022 and the first months of 2023.

Members observed that long-term inflation expectations drawn from the survey conducted by Banco de México remain anchored at 3.5% – above Banxico's 3.0% target.

It was agreed that monetary policy should remain restrictive and therefore conducive to the convergence of inflation to the 3% target in the forecast horizon.

Future decisions will be data-dependent.

One member noted that “despite monetary restriction, domestic economic activity continues showing resilience and that demand related pressures may slow down or even reverse the fall in inflation.

Further, it was noted that “economic activity continues exhibiting dynamism despite the historical increase in the real interest rate.”

Mexican Peso sensitivity to risk aversion

The Mexican Peso is biased to depreciate according to data from the foreign exchange derivatives market, according to commentary from one member of the Banxico. MXN is also particularly sensitive to depreciating during periods of high risk aversion, the Banxico meeting minutes said.

“The reduction in exchange rate volatility and in the implied skew in foreign exchange options suggest a lower demand for hedging amid a possible depreciation of the Mexican peso, which contrasts with other election years,” said the member, who was not named.

“Lower demand, as well as the positioning observed in short-term foreign exchange derivatives markets, could magnify a depreciation of the Mexican peso in the event of an episode of high-risk aversion, and thus periods of volatility cannot be ruled out,” the member added.

Technical Analysis: USD/MXN in long trend lower

USD/MXN is in a long-term downtrend that is exhibiting signs of waning pressure. The bear trend started after the pair peaked at 25.76 in April 2020 – we are now in the 16.50s.

It is possible the pair is unfolding a very large three-wave pattern called a Measured Move. Such patterns are composed of an A, B, and C wave, with wave C extending to a similar length to wave A, or a Fibonacci 0.618 ratio of A.

USD/MXN Weekly Chart

If this is the case, price has almost reached the point at which C will equal A, calculated as lying at 15.89.

It has also by now surpassed the conservative target for the end of C at the 0.618 Fibonacci extension of A (at 18.24).

Once the pattern is complete the market usually reverses or undergoes a substantial correction.

The Relative Strength Index (RSI) is converging acutely with price – a sign the downtrend could be losing momentum. In 2024 price has pushed below the level of the 2023 lows but RSI has not followed suit. This non-correlation between price and momentum is a bullish indication. It could lead to a correction higher eventually.

There has been no reaction from price yet, however, so the expectation of upside remains speculatory and unconfirmed.

An actual turnaround in the price would be required to support the view a change is on the horizon, and that is still lacking.

Mexican Peso FAQs

The Mexican Peso (MXN) is the most traded currency among its Latin American peers. Its value is broadly determined by the performance of the Mexican economy, the country’s central bank’s policy, the amount of foreign investment in the country and even the levels of remittances sent by Mexicans who live abroad, particularly in the United States. Geopolitical trends can also move MXN: for example, the process of nearshoring – or the decision by some firms to relocate manufacturing capacity and supply chains closer to their home countries – is also seen as a catalyst for the Mexican currency as the country is considered a key manufacturing hub in the American continent. Another catalyst for MXN is Oil prices as Mexico is a key exporter of the commodity.