- Аналітика

- Новини та інструменти

- Новини ринків

Новини ринків

- USD/CAD remains flat around 1.3595 following the US and Canada Labor Day holiday.

- Market players speculate on a less aggressive Federal Reserve (Fed) stance following the mixed economic data results.

- BoC is expected to maintain its key interest rate unchanged at 5.00% on Wednesday.

The USD/CAD pair consolidates its losses below the 1.3600 mark during the early Asian trading hours on Tuesday. The major pair currently trades near 1.3595, up 0.03% for the day. The pair’s move is limited following the US and Canada Labor Day holiday. Investors await the Bank of Canada (BoC) interest rate decision and markets anticipate an unchanged in policy.

Last week, US economic data displayed mixed results. August's Nonfarm Payrolls (NFP) came in at 187K, exceeding expectations of 170K and the previous reading of 157K. Nevertheless, the unemployment rate fell substantially to 3.8%, compared to the market consensus and the previous rate of 3.5%. The US Manufacturing PMI came in at 47.6 versus 46.4 previously and exceeded market expectations of 47.0.

Fed Chairman Jerome Powell stated at the Jackson Hole Symposium that a potential additional rate hike would be depending on incoming data. However, Market players bet on a less aggressive Federal Reserve (Fed) stance following the mixed economic data results. The odds of holding an interest rate at the September meeting remain at 93%, according to the CME FedWatch Tool. This, in turn, might cap the upside in the USD and act as a headwind in the USD/CAD pair.

About the data last week, Canadian real Gross Domestic Product (GDP) Annualized for the second quarter contracted at 0.2% YoY against the previous reading of 2.6%. The growth number was worse-than-expected of a 1.2% expansion. The downbeat Canadian data exerted some selling pressure on the Canadian Dollar (CAD).

The markets will shift their attention to the BoC interest rate decision on Wednesday. BoC is expected to maintain its key interest rate unchanged at 5.00% on Wednesday and hold at that level until at least the end of March 2024, according to a Reuters poll. Meanwhile, a rise in oil price lifts the Canadian Dollar against its rivals as Canada is the largest exporter of crude to the US.

Looking ahead, the BoC interest rate decision will be in the spotlight. Later this week, the US ISM Services PMI for August will be released on Wednesday with an expectation to grow to 52.6. On Friday, BoC's Governor Tiff Macklem's speech and the Canadian Unemployment rate might offer some hints about the further monetary policy for the entire year and the data could give a clear direction for the USD/CAD pair.

- USD/MXN prods 15-week-old falling resistance line after a three-day-long winning streak.

- Monthly horizontal resistance area adds to the upside filters.

- Mexican Peso sellers cheer sustained trading beyond 50-DMA, bullish MACD signals.

- Rising trend line from early July acts as the last defense of Mexican Peso bulls.

USD/MXN bulls attack the key upside hurdle surrounding 17.20, close to 17.17 by the press time of early Tuesday morning in Asia.

The Mexican Peso (MXN) pair rose in the last three consecutive days before poking a downward-sloping resistance line from May 31, close to 17.20 at the latest.

The upside momentum takes clues from the bullish MACD signals and the USD/MXN pair’s ability to stay firmer past the 50-DMA, around 16.97 by the press time.

It’s worth noting, however, that a one-month-old horizontal area adds strength to the 17.18–20 hurdle for the USD/MXN bulls.

Following that, a quick run-up towards the ascending resistance line stretched from early July, surrounding 17.46 at the latest, can’t be ruled out.

On the flip side, the USD/MXN pullback remains elusive unless it stays beyond the 50-DMA support of 16.97. That said, the 17.00 round figure restricts the nearby downside of the quote.

In a case where the Mexican Peso (MXN) pair remains bearish past 16.97, a seven-week-long horizontal area surrounding 16.68–70 will be in the spotlight.

Overall, the USD/MXN pair is likely to remain firmer but the immediate resistance line and the presence of the US Factory Orders, as well as Mexican Consumer Confidence, for August test the pair buyers.

USD/MXN: Daily chart

Trend: Limited upside expected

- US Dollar Index remains dicey after a downbeat start to the week that snapped two-day winning streak.

- Mixed US data, unimpressive Fed talks confirms September inaction, odds of witnessing one rate hike in 2023 defend DXY bulls.

- US Labor Day holiday, China-inspired risk-on mood allowed Greenback buyers to take a breather.

- US Factory Orders, yields eyed for fresh impulse.

The US Dollar Index (DXY) remains sidelined around 104.10-15 as bulls and bears jostle amid a light calendar in Tuesday’s Asian session. Also challenging the DXY traders are mixed concerns about the US Federal Reserve (Fed) and China, as well as the cautious mood ahead of the full markets’ reaction to the latest developments, as well as the mid-tier US data and risk catalysts.

That said, the market’s bets on the Federal Reserve’s (Fed) status quo in September contrasts with a recent improvement in the odds favoring a rate hike during late 2023 seems to prod the US Dollar moves. That said, Federal Reserve Bank of Cleveland President Loretta J. Mester defended the US central bank’s hawkish move and ruled out the rate cut bias in her speech on Friday.

On Friday, Nonfarm Payrolls (NFP), the August numbers initially renewed hawkish bias about the Fed, even if the Unemployment Rate and Average Hourly Earnings kept the policy pivot concerns on the table afterward. Following that, the global rating agency Moody’s revised up the US Gross Domestic Product (GDP) predictions for 2023 to 1.9% versus 1.1% expected in May.

It’s worth noting that China’s readiness for opening up the services industry, as well as developments of the manufacturing activities, joins a slew of measures to cut mortgage rates and infuse more liquidity to weigh on the DXY. Further, the optimism about China’s struggling reality firm Country Garden, after it managed to gain approval from creditors to delay the debt payments of around 3.9 billion Yuan ($536 million), also exerts downside pressure on the US Dollar Index.

With the recent improvement in the German bund yields and reassessment of the Fed concerns, especially as the full markets return, the DXY pares the previous day’s losses but seeks more clues to recall the buyers.

Looking forward, China’s Caixin Services PMI for August, as well as the US Factory Orders for the said month, will be important to watch for clear directions. Above all, the risk catalysts and the bond moves should be watched carefully for clear directions.

Technical analysis

Although the US Dollar Index (DXY) bulls remain hopeful beyond the 21-DMA support of 103.45, a downward-sloping resistance line from late May, close to 104.45 by the press time, restricts the immediate upside of the Greenback’s gauge versus the six major currencies.

- GBP/USD edges higher after snapping two-day losing streak the previous day.

- Clear rebound from multi-day-old ascending support line, impending bull cross on MACD favor Cable buyers.

- 50-SMA, five-week-old descending trend line restrict Pound Sterling’s immediate upside.

- Full markets return after a long weekend in the US, mid-tier data eyed for fresh impulse.

GBP/USD struggles to defend the week-start rebound while making rounds to 1.2625-30 amid the early hours of Tuesday’s Asian session. In doing so, the Cable pair jostles with the 50-SMA as full markets return after the US Labor Day Holiday. Apart from the 50-SMA, cautious mood ahead of the final readings of the UK S&P Global/CIPS PMIs for August and the US Factory Orders for the said month also prods the Pound Sterling.

It’s worth noting, however, that the GBP/USD pair’s successful rebound from an ascending trend line stretched from late May, around 1.2580 by the press time, joins the looming bull cross on the MACD indicator to keep the buyers hopeful.

With this, the quote is likely to overcome the immediate SMA hurdle surrounding 1.2630. The same will allow the Cable pair to prod a five-week-long falling resistance line near the 1.2700 threshold.

However, the Pound Sterling’s upside past 1.2700 will be decisive as it will then have only one hurdle, namely the 200-SMA level of around 1.2740, to cross before inviting buyers home.

Alternatively, the GBP/USD pair’s downside appears elusive unless it stays beyond the aforementioned support line stretched from May, close to 1.2580.

Following that, a three-month-old horizontal support line of around 1.2550 will be important as it holds the key to the Pound Sterling’s slump toward the sub-1.2500 zone.

Overall, the GBP/USD pair is likely to keep the latest gains but the road towards the north appears bumpy.

GBP/USD: Four-hour chart

Trend: Limited upside expected

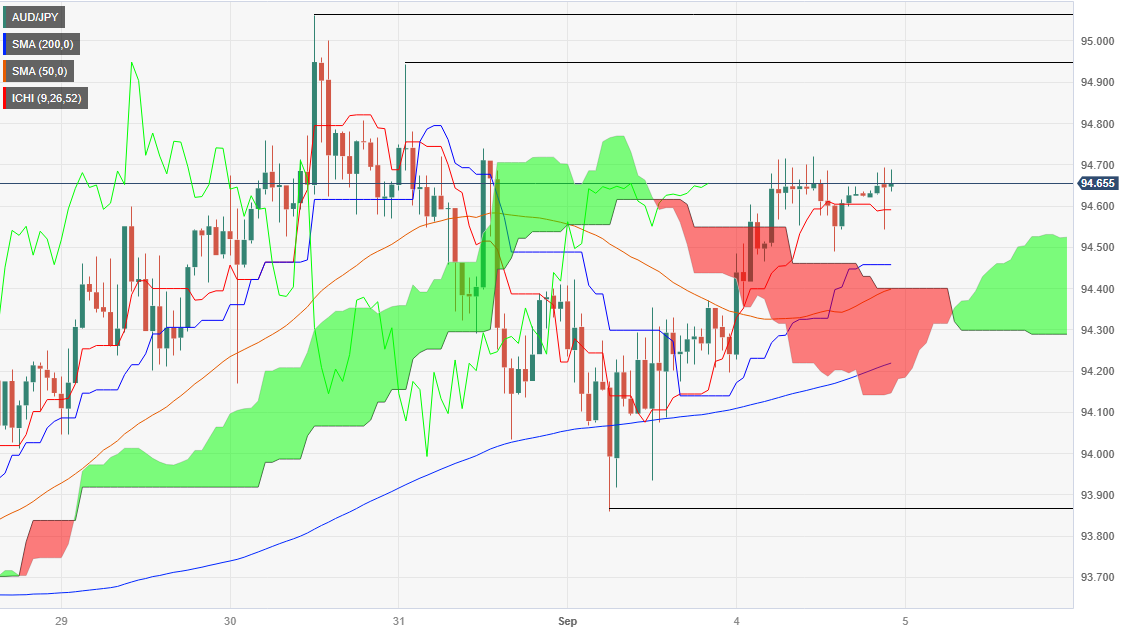

- AUD/JPY pair inches up 0.04% to trade at 94.65, following a 0.30% gain on Monday, as it approaches a key resistance trendline at 94.90/95.00.

- The pair remains neutral/upwards, with significant resistance at a July 25 high of 95.85 and the psychological 96.00 figure.

- Short-term, the AUD/JPY 1-hour chart indicates consolidation around the daily pivot, with first support and resistance levels identified at 94.50/51 and 94.84, respectively.

As Tuesday’s Asian session begins, the Aussie Dollar (AUD) climbs a minuscule 0.04% against the Japanese Yen (JPY), following Monday’s upbeat session, the AUD/JPY gained more than 0.30%. The cross-currency pair exchanges hands at 94.65, ahead of the Reserve Bank of Australia’s (RBA) monetary policy decision.

AUD/JPY Price Analysis: Technical outlook

From a daily chart perspective, the AUD/JPY remains neutral to upward biased, with the cross above the Ichimoku cloud, but about to face solid resistance at a downslope resistance trendline at around 94.90/95.00. A breach of that area would expose the July 25 high at 95.85 before the pair edges toward the psychological 96.00 mark. Downside risks emerge at around the top of the Ichimoku Cloud (Kumo) at 94.08, followed by an upslope support trendline at 93.50/60.

In the short term, the 1-hour chart depicts the pair consolidating art around the daily pivot, with upside risks seen above yesterday’s high of 94.72. Next, resistance emerges at the R1 daily pivot at 94.84, followed by the August 30 high at 5.06, confluence with the R2 daily pivot. Conversely, the AUD/JPY first support emerges at the Senkou-Span A and the daily pivot at 94.50/51. The break below will expose the confluence of the Senkou Span B and the S1 pivot at 94.28.

AUD/JPY Price Action – Hourly chart

- NZD/USD remains flat around 0.5943 amid the quiet trading session.

- Market players bet on a less aggressive Federal Reserve (Fed) stance.

- Chinese authorities plan to introduce more stimulus measures, which lift the Kiwi.

- Investors await Chinese Services PMI, US ISM Services PMI.

The NZD/USD pair trades sideways below the crucial 0.6000 barrier during the early Asian session on Tuesday. The US Dollar (USD) posts modest losses near a monthly high of around 104.10 on a quiet session as Wall Street closed for Labor Day. The pair currently trades around 0.5943, gaining 0.05% on the day.

The US economic data showed a mixed result last week. The US Nonfarm Payrolls (NFP) for August came in at 187K, beating the expectation of 170K and 157K in the previous reading. While, The Unemployment Rate dropped significantly to 3.8%, compared to the market consensus of 3.5% and 3.5% prior. The US Manufacturing PMI came in at 47.6 versus 46.4 prior and better than 47.0 expected.

Market players bet on a less aggressive Federal Reserve (Fed) stance. According to the CME FedWatch Tool, the possibility of an interest rate hold at the September meeting remains at 93%, which might cap the upside in the USD.

The New Zealand economic docket is quite empty this week and the headline surrounding the China stimulus plan might influence the Kiwi dynamic. On Monday, Chinese authorities plan to introduce more measures, including the easing of restrictions on the purchase of homes, to stimulate China's faltering economy, according to Reuters. In response to the news, the Greenback is weakened against its rivals due to risk appetite. This, in turn, lifts the China-proxy New Zealand Dollar (NZD).

About the data, the New Zealand Terms of Trade Index improved to 0.4% in the second quarter, compared to a decline of 1.5% in the previous reading and an expected drop of 1.3%. The ANZ – Roy Morgan Consumer Confidence for August revealed last week that consumer confidence in New Zealand increased marginally to 85 in August from 83.7 in July, but remained subdued.

Looking ahead, the Chinese Caixin Services PMI for August will be released on Tuesday. The US ISM Services PMI will be due on Wednesday while Fed officials enter their blackout period ahead of the September’s Federal Open Market Committee (FOMC) meeting Traders will take cues from the data and find trading opportunities around the NZD/USD pair.

- AUD/USD struggles to defend the week-start gains ahead of Reserve Bank of Australia Interest Rate Decision.

- Country Garden news, China stimulus put a floor under Aussie price despite mixed data at home.

- US holiday offered a dull start to the week comprising RBA, Australia Q2 GDP.

- RBA is expected to keep interest rates unchanged but Lowe’s last speech as Governor will be important to watch.

AUD/USD portrays the pre-event anxiety as it stays defensive around the mid-0.6400s during the early hours of Tuesday’s Asian session. In doing so, the Aussie pair fails to extend the week-start gains backed by headlines from China, as well as surrounding Country Garden, as market players braces for the key Reserve Bank of Australia (RBA) Interest Rate Decision. The event becomes more important as it is the last ruling from Governor Philip Lowe before he hands over the control to Michele Bullock. Apart from the RBA, China Caixin Services PMI and the US Factory Orders also become important to watch for clear directions.

The risk-barometer pair witnessed an upbeat start to the week, despite posting mild gains, after marking the first positive weekly close in seven, as market players cheer the receding odds of the Federal Reserve’s (Fed) hawkish move together with China stimulus. Adding strength to the optimism could be the news from China’s biggest private reality firm Country Garden.

China’s readiness for opening up the services industry, as well as developments of the manufacturing activities, joins a slew of measures to cut mortgage rates and infuse more liquidity to underpin the AUD/USD upside. Further, the optimism about China’s struggling reality firm Country Garden, after it managed to gain approval from creditors to delay the debt payments of around 3.9 billion Yuan ($536 million), also keeps the AUD/USD buyers hopeful.

Further, the market’s bets on the Federal Reserve’s (Fed) status quo in September contrasts with a recent improvement in the odds favoring a rate hike during late 2023 seems to prod the AUDUSD Price even as the US Dollar remains depressed. That said, Federal Reserve Bank of Cleveland President Loretta J. Mester defended the US central bank’s hawkish move and ruled out the rate cut bias in her speech on Friday.

On Friday, Nonfarm Payrolls (NFP), the August numbers initially renewed hawkish bias about the Fed, even if the Unemployment Rate and Average Hourly Earnings kept the policy pivot concerns on the table afterward. Following that, the global rating agency Moody’s revised up the US Gross Domestic Product (GDP) predictions for 2023 to 1.9% versus 1.1% expected in May.

At home, Australia’s TD Securities Index slide to 0.2% MoM from 0.8% prior but improved to 6.1% YoY versus 5.4% previous readings. Further, the ANZ Job Advertisements rose to 1.9% from 0.4% but the Company Gross Operating Profits for the second-quarter (Q2) of 2023 slumped to -13.1% compared to 0.5% previous gains.

Amid these plays, the market sentiment remained mildly positive and put a floor under the AUD/USD pair. However, the cautious mood ahead of the RBA Interest Rate Decision and tomorrow’s Australia Q2 Gross Domestic Product (GDP) challenge the pair traders.

As per the latest Reuters poll, , “The Reserve Bank of Australia will keep its key interest rate unchanged at 4.10% on Tuesday as inflation shows signs of easing,” per the August 30 – September 1 poll of 35 economist by Reuters. The survey finding also mentioned that the respondents largely expect a final hike next quarter.

While the Aussie central bank is mostly certain to keep the rates unchanged at 4.10%, attention will be on the RBA Statement’s tone for clear directions of future rate hikes, which in turn may help the AUD/USD to stay firmer.

Following that, China’s Caixin Services PMI for August, as well as the US Factory Orders for the said month, will be important to watch for clear directions.

Technical analysis

AUD/USD remains on the bear’s radar unless providing a clear upside break of the 0.6500 hurdle comprising multiple levels marked in late June and early July, which in turn highlights a 13-day-old rising support line of around 0.6430 to watch during the quote’s pullback.

- EUR/USD pair gains a modest 0.19% to trade at 1.0792, as US markets remain closed for Labor Day and ECB President Lagarde’s comments fail to stir volatility.

- Mixed US employment data and a higher manufacturing PMI of 47.6 led to reduced expectations for US interest rate hikes, keeping September odds at 93%.

- For further directional cues, investors see upcoming economic indicators, including the Eurozone’s S&P Global Services, Composite PMIs, and US Factory Orders.

A quiet session at the beginning of the week saw the Euro (EUR) gaining 0.19% versus the US Dollar (USD), as the US cash markets were closed on a Labor Day holiday. European Central Bank (ECB) officials failed to boost significantly the EUR, as the EUR/USD pair trades at 1.0792, almost flat as Tuesday’s Asian session begins.

EUR/USD Sees Limited Movement as ECB President Stays Mum on Monetary Policy; U.S. Jobs Data and Chinese Stimulus in Focus

During the European session, ECB’s President Christine Lagarde said that decisive action in high inflationary scenarios was “crucial.” Even though she spoke about inflation in a seminar in London, she failed to trigger volatility in the EUR/USD, as Lagarde was muted in talking about the ECB’s current monetary policy.

In the meantime, the additional stimulus the Chinese Government provides on its property markets boosts the economy and improves investors’ mood.

Last week’s US employment data was mixed as the economy added 187K jobs, above estimates and July’s data. Nonetheless, an uptick in the Unemployment Rate, from 3.5% to 3.8% YoY, kept most currency pairs within familiar levels, though spurred a reaction on the US bond market.

Investors slashed their bets of higher interest rates in the United States (US), which is also bad news for the USD. The odds for September’s meeting stay at around 93%, as shown by the CME FedWatch Tool, while the chances for November diminished further. Additionally, the first-rate reduction is projected for May 1, with traders anticipating rate cut odds around 5.14%, 19 basis points lower than the current effective Federal Funds Rate (FFR) of 5.33%.

Other data, depicted by the Institute for Supply Management (ISM), reported that US business activity, as indicated by the manufacturing PMI, scored 47.6, exceeding analysts’ estimates of 47.0 and the previous reading of 46.4.

What to watch?

The Eurozone (EU) economic docket will feature S&P Global Services and Composite PMIs and the Produce Price Index (PIP) by Eurostat. On the US front, the agenda will review Factory Orders.

EUR/USD Technical Levels

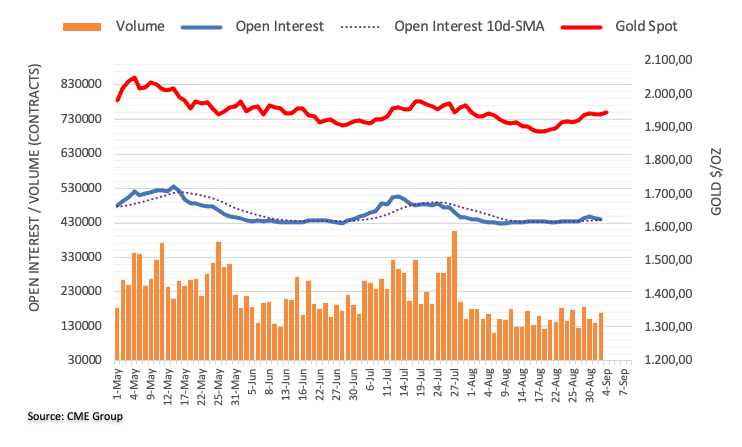

- Gold Price fades bullish bias as full markets return after long weekend in the United States.

- Mixed sentiment about China, Federal Reserve prod XAU/USD buyers.

- China Caixin Services PMI, US Factory Orders will decorate calendar.

- Updates about Sino-American ties, stimulus from Beijing could act as extra catalysts.

Gold Price remains depressed around $1,938, extending Friday’s pullback from the monthly high after a downbeat start to the week. The yellow metal marked a dull performance the previous day amid the United States Labor Day Holiday. However, the uncertainty about the Federal Reserve’s (Fed) next move and a lack of confidence in China’s efforts to defend the world’s second-largest economy seems to weigh on the XAU/USD of late.

Moving on, the full markets return to the table on Tuesday and may offer an active day amid a slew of data/events scheduled for publishing. Among them, China Caixin Services PMI and the US Factory Orders will be eyed for clear directions.

Gold Price retreats amid indecision

Gold Price fails to defend the two-week uptrend amid mixed clues about China and the Federal Reserve (Fed).

Starting with the upbeat United States Nonfarm Payrolls (NFP), the August numbers initially renewed hawkish bias about the Fed, even if the Unemployment Rate and Average Hourly Earnings kept the policy pivot concerns on the table afterward. Following that, the global rating agency Moody’s revised up the US Gross Domestic Product (GDP) predictions for 2023 to 1.9% versus 1.1% expected in May.

It’s worth noting that the market’s bets on the Federal Reserve’s (Fed) status quo in September contrasts with a recent improvement in the odds favoring a rate hike during late 2023 seems to weigh on the Gold Price even as the US Dollar remains depressed. That said, Federal Reserve Bank of Cleveland President Loretta J. Mester defended the US central bank’s hawkish move and ruled out the rate cut bias in her speech on Friday, which in turn prod the Gold buyers.

On the other hand, China’s readiness for opening up the services industry, as well as developments of the manufacturing activities, joins a slew of measures to cut mortgage rates and infuse more liquidity to underpin the XAU/USD upside.

Furthermore, optimism about China’s struggling reality firm Country Garden and the upbeat growth numbers from India, one of the world’s biggest Gold customers, also keep the Gold buyers hopeful.

However, the market’s lack of confidence in the Chinese measures to defend the economy, as well as the Sino-American tension, recently over Taiwan and the US businesses’ discomfort in Beijing, prod the optimism, which in turn challenges the Gold buyers.

Amid these plays, the US Dollar Index (DXY) began the week on a negative note while posting the first daily loss in three.

Federal Reserve, China clues eyed for XAU/USD directions

Looking ahead, the return of the United States traders after a long weekend and the market’s reaction to China’s Caixin Services PMI for August, as well as the US Factory Orders for the said, will be important to watch for clear directions. Above all, updates about the Federal Reserve’s (Fed) next moves and clues about China’s economic recovery, as well as the stimulus measures, will be important for Gold traders to watch for fresh impulse.

Also read: Gold Price Forecast: XAU/USD steady at around $1,938

Gold Price Technical Analysis

Gold Price remains pressured after reversing from a six-week-old descending resistance line, around $1,950 by the press time.

Adding credence to the downside bias are the bearish signals on the Moving Average Convergence and Divergence (MACD) indicator, as well as the Relative Strength Index (RSI) line, placed at 14, retreat to the 50.0 level from an overbought territory.

It’s worth noting, however, that a fortnight-old rising support line and the 200-Simple Moving Average (SMA), around $1,933 and $1,930 in that order, restrict the short-term downside of the Gold Price.

Following that, nine-week-long horizontal support of around $1,903 and the $1,900 round figure may prod the XAU/USD bears before directing the sellers toward the previous monthly low of around $1,885.

Meanwhile, the 61.8% Fibonacci retracement of the Gold Price declines from July to August, around $1,948, restricts immediate upside ahead of the stated resistance from late July 19, close to $1,951 at the latest.

Following that, July’s peak of around $1,985 will act as the final defense of the Gold bears.

Gold Price: Four-hour chart

Trend: Pullback expected

- USD/JPY traded with mild losses in a narrow range on Monday and closed at 146.40.

- The USD was one of the session's worst performers, with the JPY being the weakest.

- Investors turned their focus to ISM Services PMI for fresh catalysts.

At the start of the week, the USD/JPY saw little movement, with both currencies trading weak against most of their rivals. The USD traded soft after last week's key events. Nonfarm Payrolls showed a mixed picture, while the ISM Manufacturing PMI rose higher than expected and the Core Personal Consumption Expenditures came in hot. Focus now shifts to Service sector PMI surveys from the ISM to be released on Wednesday, which will help investors to continue modelling their expectations regarding the next Federal Reserve (Fed) decisions.

The USD is trading soft on Monday after last week's key events. Nonfarm Payrolls showed a mixed picture, while the August ISM Manufacturing PMI rose higher than expected as well as the Core Personal Consumption Expenditures from July. Focus now shifts to Service sector PMI surveys from the ISM to be released on Wednesday, which will help investors to continue modelling their expectations regarding the next Federal Reserve (Fed) decisions.

According to the CME FedWatch tool, the odds of an extra 0.25% tightening throughout the period leading to the December meeting had somewhat eased, but investors are still placing some bets on it. If the Fed opts for another hike, it would lift rates to 5.75%.

On the Yen’s side, local wage and inflation data will play a pivotal role in the Bank of Japan’s (BoJ) considerations for potential adjustments to monetary policy. In that sense, at the early Asian session on Thursday, Japan will report household spending and earnings figures from July, and their outcome will influence the expectations of the following BoJ decisions.

USD/JPY Levels to watch

Analysing the daily chart, the USD/JPY technical outlook is bullish in the short term. The Relative Strength Index (RSI) is positioned above its midline in positive territory. It has a northward slope, indicating a favourable buying momentum. It is further supported by the positive signal from the Moving Average Convergence Divergence (MACD), which displays green bars, underscoring the growing bullish momentum. Also, the pair is above the 20,100,200-day Simple Moving Average (SMA), indicating a favourable position for the bulls in the bigger picture.

Support levels: 145.72 (20-day SMA), 145.00, 144.00.

Resistance levels: 146.80, 147.00, 147.40.

USD/JPY Daily Chart

-638294604806512018.png)

- USD/CHF trades at the 0.8845 zone with mild losses.

- The bulls are having a hard time consolidating above 0.8850.

- 20-day SMA en route to perform a bullish cross with the 100-day SMA.

The USD/CHF has traded sideways since early August in the 0.8700 - 0.88450 range, with bulls failing to gather momentum and seeming to await fresh catalysts.

According to the daily chart, the technical outlook for the USD/CHF remains neutral. The Relative Strength Index (RSI) indicates a stagnant bullish momentum with a flat slope above its midline, while the Moving Average Convergence (MACD) prints unchanged green bars. The four-hour chart also shows a clear neutral bias with no clear dominance and indicators having turned flat.

On the bigger picture, the pair is above the 20-day Simple Moving Average (SMA) but below the 100 and 200-day SMAs, suggesting that despite the recent bearish sentiment, the bulls are still resilient, holding some momentum but that for the longer term, the bears have the upperhand. Traders should eye the convergence of the 20 and 100-day SMA towards the 0.8850 - 0.8880 range as they are about to perform a bullish cross. It's worth mentioning that when a shorter-term SMA crosses above a longer-term SMA, it's usually considered bullish for the pair in the short term.

For this week, a fundamental catalyst is the release of the ISM Services PMI from the US which could influence the bets of the markets on the next Federal Reserve (Fed) decisions and, hence, the USD price dynamics.

Support levels: 0.8800 (20-day SMA), 0.8750, 0.8700.

Resistance levels: 0.8850, 0.8880 (100-day SMA), 0.8900.

USD/CHF Daily Chart

-638294568139617630.png)

The key event during the Asian session will be the Reserve Bank of Australia meeting. No change is expected in interest rates. Additionally, the final reading of Services PMIs will be released. Later in the day, Eurozone wholesale inflation and US Factory Orders data are due.

Here is what you need to know on Tuesday, September 5:

On a quiet session, the US Dollar Index fell modestly and held above 104.00, near monthly highs on a quiet session with Wall Street closed due to Labor Day. US stock futures fell marginally. On Tuesday, July Factory Orders are due.

European Central Bank (ECB) President Christine Lagarde did not provide any new information in her speech on Monday. German trade data came in better than expected, while Eurozone Sentix Investor Confidence dropped further in September to -21.5. EUR/USD moderately rose but was unable to consolidate above 1.0800. The bias remains to the downside, with support at 1.0760. On Tuesday, Lagarde will speak again, Eurostat will release the August Producer Price Index, and the final Service PMIs are due.

GBP/USD rose from below 1.2600 to the 1.2630 area. The Pound outperformed with EUR/GBP falling below 0.8550. The final Service PMI from the UK is due on Tuesday.

USD/JPY continued to rise and climbed to the 146.50 area. A consolidation above that level would strengthen the bullish outlook.

AUD/USD closed around the 20-day Simple Moving Average (SMA) around 0.6460, with modestly gains amid a weaker US Dollar. The Reserve Bank of Australia (RBA) is scheduled to announce its monetary policy decision on Tuesday. It is widely anticipated that the RBA will maintain its key interest rate at 4.1%. This meeting will mark the final one with Philip Lowe serving as governor of the RBA.

NZD/USD continued to trade sideways, with a crucial support level at 0.5900 and trading below the 20-day SMA at 0.5970. To indicate a more sustainable recovery, the Kiwi needs to achieve a daily close above 0.6000.

USD/CAD maintained its gains from Friday but struggled to decisively break above 1.3600. The Bank of Canada will have its monetary policy meeting on Wednesday.

Gold closed near the $1,940 area for the third consecutive day. It continues to trade sideways after failing to break above $1,950 and the 100-day SMA. Silver experienced its fourth consecutive day of losses, slipping slightly below $24.00.

Crude oil prices maintained their recent gains, with the WTI barrel hovering around $85.00. These gains were supported by output cuts from Russia and Saudi Arabia, as well as hopes for additional stimulus measures from China.

Like this article? Help us with some feedback by answering this survey:

- GBP/USD pair rebounds to 1.2630, recovering from last Friday’s low of 1.2580s, as Wall Street observes Labor Day and liquidity thins.

- Mixed US jobs data and a higher-than-expected manufacturing PMI of 47.6 dampen prospects for further Fed tightening, keeping September rate hike odds at 92%.

- High expectations for a 25 bps rate hike by the Bank of England in September contrast with deteriorating economic conditions, adding uncertainty to the currency pair’s direction.

The British Pound (GBP) rebounds at around last Friday’s low of 1.2580s against the Greenback (GBP) and recovered the 1.2600 figure on Monday amid thin liquidity conditions in observance of the US Labor Day. The GBP/USD is trading at 1.2630

British Pound recovers as investors reassess Fed tightening; eyes on upcoming BoE decision and economic indicators

Wall Street is closed today in observance of Labor Day. Last week’s US job data presented a mixed picture, with Nonfarm Payrolls reaching 187,000, surpassing the projected 177,000 in August. However, this didn’t bolster the US Dollar, as the Unemployment Rate also ticked higher as anticipated. Subsequently, the Institute for Supply Management (ISM) reported that US business activity, as indicated by the manufacturing PMI, scored 47.6, exceeding analysts’ estimates of 47.0 and the previous reading of 46.4.

As a result, investors significantly reduced their expectations for the US Federal Reserve’s further tightening of monetary policy. The likelihood of interest rate increases staying unchanged for the September meeting remains at 92%. Additionally, the first-rate reduction is projected for May 1, with traders anticipating rate cut odds around 5.14%, 19 basis points lower than the current effective Federal Funds Rate (FFR) of 5.33%.

In addition, news from China improved investors’ sentiment as the country established measures to boost its property market, which is at the brisk of a crisis. As the Government easied measures, home sales rose, as reported by Bloomberg.

Across the Atlantic, expectations of the Bank of England (BoE) to raise rates by 25 bps remained high at 90% for the September 21 meeting. Nevertheless, traders remain cautious about the approach the BoE could make regarding future tightening as economic conditions continue to deteriorate, suggesting that growth could decelerate.

GBP/USD traders would take direction from economic activity in the agenda. The UK would reveal their BRC Retail Sales, S&P Global/CIPS Services, and Composite PMIs. On the US front, the calendar would feature the ISM Non-Manufacturing PMI, Initial Jobless Claims, and Fed speakers.

GBP/USD Price Analysis: Technical outlook

From a daily chart perspective, the GBP/USD is neutral to downward biased, even though it remains above its 200-day Moving Average (DMA), at 1.2417. Nevertheless, the pair has achieved successive series of lower highs and lows, as shown by market structure, with the major seeing testing the 1.2500 figure if growth economic conditions in the UK faltered. The next support emerges at the 200-DMA at 1.2417 before testing May’s low of 1.2308. Conversely, the major would test 1.2700 if the exchange rate stays above the 1.26 handle.

Analysts at MUFG Bank forecast the EUR/SEK to edge modestly higher to 11.900 by the end of the third quarter, and to drop later to 11.500 by the first quarter of 2024.

Riksbank to step up pace of QT to provide more support for SEK

The krona has re-weakened in August giving back all of the gains recorded in July. It has resulted in EUR/SEK hitting a new record high of 11.963 in August as it moved above the Global Financial Crisis high at 11.790 from March 2009. The krone has been undermined by the recent deterioration in global investor risk sentiment.

The krona would benefit more from a softer landing for the global economy which allows major central banks to begin lowering rates in response to the ongoing slowdown in inflation. The weaker krona if sustained will make it more challenging for the Riksbank to bring down inflation closer to their target.

The krona remains vulnerable to further weakness in the near-term, but we still expect a rebound in the year ahead.

- EUR/GBP pair drops to a new seven-day low of 0.8546, influenced by market expectations of a BoE rate hike and ECB's unchanged stance.

- Technical analysis shows the pair struggling to break the 50-day SMA at 0.8582, maintaining a downtrend with a year-to-date low of 0.8492 in sight.

- Despite the downtrend, a falling wedge pattern suggests an upside potential, with key resistance levels at 0.8572 and 0.8600 to watch.

The Euro (EUR) loses ground against the Pound Sterling (GBP) amid a risk-on impulse, as well as expectations for interest rates staying unchanged by the European Central Bank (ECB). At the same time, the Bank of England (BoE) is seen by market analysts as the only one to raise rates by 25 bps in September. That, alongside technical resistance, dragged the EUR/GBP to a new seven-day low, as the pair trades at 0.8546 after hitting a high of 0.8559.

EUR/GBP Price Analysis: Technical outlook

The daily chart portrays the pair tested the 50-day Simple Moving Average (SMA) at 0.8582, but buyers failed to pierce it on the upside, so the cross extended its losses toward current exchange rates. Due to the pair registering a successive series of lower highs and lows, the downtrend is intact, and if the pair breaches the year-to-date (YTD) low of 0.8492, August 24, 2022, would be tested at 0.8408.

On an intraday bias, the EUR/GBP is trending down but is forming a falling wedge, a bullish chart pattern, that could pave the way for further upside. If the cross breaks to the upside, the first resistance would be the 200-hour SMA (HSMA) at 0.8572, followed by the psychological 0.8600 figure and last week’s high of 0.8610.

If the pair manages to remain within the chart pattern, further downside is seen at the bottom of the falling wedge at around 0.8530/20, which, if broken, the EUR/GBP could plunge towards the YTD low of 0.8492.

EUR/GBP Price Action – Hourly chart

- EUR/JPY trades with gains, and jumped back above 158.00.

- Higher German yields and monetary policy divergences favour the EUR.

- Investors await wage and spending figures from July from Japan this week.

In Monday’s session, the EUR/JPY cross gained ground and marched towards the 158.15 area, tallying nearly 0.35% daily gains. The Euro trades strong against most of its rivals, while the JPY is one of the worst performers in the session, mainly driven by the Bank of Japan’s (BoJ) ultra-dovish stance.

Christine Lagarde, president of the European Central Bank (ECB), delivered a speech on Monday but refrained from commenting about the upcoming September decision. Joachim Nagel was also on the wires but didn’t give any detailed clues regarding the next monetary policy decisions, and he only showed himself concerned with inflation being too high. Meanwhile, German yields are sharply rising, with the 2,5 and 10-year rates increasing by more than 1%, making the Euro gain interest.

In that sense, the World Interest Rates Probabilities (WIRP) indicates that markets are discounting 25% odds of a 25bps hike in the upcoming Sep 14, 2023 meeting while the chances of a similar hike stand at 45% in October, and at 60% in December. This rate hike path would leave the target rate at 5%.

On the JPY’s side, as the Bank of Japan (BoJ) has stated, changes to monetary policy will only be entertained once local wage and inflation indicators match their projections. Japan will report July household spending figures on Tuesday and cash earnings on Friday, which investors will closely monitor to place their bets on the next BoJ decisions.

EUR/JPY Levels to watch

Observing the daily chart, EUR/JPY displays a neutral to bullish technical outlook for the short term as the bulls gain momentum. The Relative Strength Index (RSI) points north above its middle point while the Moving Average Convergence (MACD) lays out decreasing red bars. Moreover, the pair is below the 20-day Simple Moving Average (SMA) but above the 100 and 200-day SMAs, indicating a favourable position for the bulls in the bigger picture.

Support levels: 158.00, 157.00, 156.00.

Resistance levels: 158.30 (20-day SMA), 159.00, 160.00.

EUR/JPY Daily Chart

-638294486790776329.png)

- AUD/USD pair recovers to 0.6460s, up 0.26%, as investors anticipate the Reserve Bank of Australia’s upcoming monetary policy decision.

- Mixed US jobs data and a closed Wall Street for Labor Day contribute to a softer US Dollar, with Fed rate hike probabilities for September holding at 92%.

- Positive news from China’s property market and hawkish remarks from Cleveland’s Fed President Loretta Mester add complexity to the currency landscape.

The Australian Dollar (AUD) pared some of its last Friday’s losses against the US Dollar (USD) ahead of the upcoming Reserve Bank of Australia’s (RBA) monetary policy decision amid a risk-on impulse. The pair reversed its course after reaching a daily low of 0.6440 and is trading at around 0.6460s, above its opening price by 0.26%.

Risk-on sentiment and mixedUS jobs data fuel Aussie Dollar’s recovery; eyes on upcoming RBA monetary policy

Wall Street remains closed in the observance of the Labor Day. Last week’s jobs data from the United States (US) was mixed with Nonfarm Payrolls coming at 187K above estimates of 177K in August, which failed to underpin the Greenback, as the Unemployment Rate ticked higher as estimates. Later, the Institute for Supply Management (ISM) revealed that business activity in the US, as shown by the manufacturing PMI, came at 47.6 figures versus analysts’ estimation of 47.0 versus 46.4 previous readings.

Consequently, investors slashed their bets about the US Federal Reserve continuing to tighten monetary policy. Interest rate probabilities for the September meeting remain at 92%, with the first-rate cut seen on May 1. On that date, traders foresee rates at around 5.14%, 19 basis points below the effective Federal Funds Rate (FFR) of 5.33%.

In the meantime, the Australian Dollar was bolstered ahead of the RBA’s decision, with the cash rate expected to stay unchanged at 4.10%. Yet, traders are not foreseeing any additional hikes until early February 2024, though with a slim chance for a nine-bps rate hike, as shown in the bottom picture.

RBA’s Interest Rates Expectations

Source: Financialsource

In addition, news from China improved investors’ sentiment as the country established measures to boost its property market, which is at the brisk of a crisis. As the Government easied measures, home sales rose, as reported by Bloomberg.

In the central bank action, Cleveland’s Fed President Loretta Mester states that the Unemployment Rate remains low, and she still sees the jobs market as quite strong. However, the policymaker remains hawkish and has seen higher rates for longer.

AUD/USD Price Analysis: Technical outlook

The AUD/USD remains downward biased, yet so far, unable to extend its losses below the August 17 daily low at 0.6364, the current year’s low, which would warrant further losses. Intermediate support levels emerge at November 22 and October 21 lows, each at 0.6272 and 0.6210, before the pair challenges a much more important support level at the October 13 swing low at 0.6169. Conversely, upside risks emerge if the pair cracks the 0.6500 mark.

- GBP/JPY jumped to 185.00, seeing nearly 0.50% daily gains, recovering the 20-day SMA.

- BoE tightening expectations remain steady, and BoJ will likely maintain its dovish outlook.

- Monetary policy divergences drive the pair upwards.

At the start of the week, the GBP/JPY cross jumped towards 185.00 and recovered the 20-day Simple Moving Average (SMA) of 184.60. No relevant economic data will be released on the session for either country, and monetary policy divergences favour the GBP over the JPY.

On the Pound’s side, the UK will have a quiet week, with the final revisions of PMIs on Tuesday being the only highlight. As for now, World Interest Rates Probabilities (WIRP) shows that market participants are discounting higher odds of the Bank of England (BoE) increasing rates by an additional 0.50% of tightening beyond the December meeting, resulting in a total increase to the 5.75%- 6% range. In line with that, the expectations of a more aggressive BoE may limit the GBP’s losses against its rivals.

On the other hand, the BoJ's recent statements underline their commitment to aligning monetary policy with local wage and inflation trends. In that sense, Japan will report household spending figures from July on Tuesday and cash earnings data from July on Friday, which will give further insights to market participants and the BoJ into the current situation of the Japanese economy. Unless the bank does not see the required wage growth, it will likely maintain its dovish approach, leaving the JPY vulnerable.

GBP/JPY Levels to watch

The technical analysis of the daily chart suggests a neutral to bullish stance for GBP/JPY as the bulls work on recovering their ground. The Relative Strength Index (RSI) exhibits a bullish inclination with a positive slope above the 50 threshold, while the Moving Average Convergence (MACD) prints weaker red bars. Additionally, the pair is above the 20,100,200-day Simple Moving Average (SMA), pointing towards the prevailing strength of the bulls in the larger context.

Support levels: 183.50, 183.00, 182.00.

Resistance levels: 185.00, 186.00, 187.00.

GBP/JPY Daily Chart

-638294441171674635.png)

- Banxico’s decision to reduce its currency hedging program sends the pair higher.

- US Nonfarm Payrolls beat expectations but rising Unemployment Rate stalls USD rally.

- Cleveland’s Fed President Loretta Mester remains hawkish on US interest rates.

The Mexican Peso (MXN) prolonged its losses by more than 0.50% versus the US Dollar (USD) after the Bank of Mexico (Banxico) decided to slash its hedging program due to stabilizing the USD/MXN exchange rate amid geopolitical and Covid-19 uncertainty. Hence, the pair trades at 17.1792 after hitting a daily low of 17.0430.

Mexican Peso weakens further after the Bank of Mexico’s decision to cut hedging, despite mixed US employment figures

Last week’s news that Banxico would reduce its currency hedging program sent the USD/MXN pair into a tailspin, as the program was designed to tame volatility, seen by traders as an exit signal from its long positions. On August 31, the USD/MXN posted more than 1.70% gains after Banxico’s decision.

On Friday, the latest US employment figures revealed the US Nonfarm Payrolls (NFP) rose to 187K in August versus 170K expected and 157K prior (revised). Nevertheless, the Unemployment Rate rising to 3.8% from the 3.5% market forecasts and previous readings stalled the Greenback rally, as the data was seen as a justification for the Fed to keep interest rates unchanged at the September meeting.

Other data The US ISM Manufacturing PMI also impressed the US Dollar buyers with the 47.6 figures versus analysts’ estimation of 47.0 versus 46.4 previous readings.

In the central bank action, Cleveland’s Fed President Loretta Mester states that the Unemployment Rate remains low, and she still sees the jobs market as quite strong. However, the policymaker remains hawkish and has seen higher rates for longer.

On the Mexican front, Banxico’s Governor Victoria Rodriguez Ceja took off from the table rate cuts, as she added, “The outlook ahead continues to be complex and uncertain. It’s important to remember that disinflation periods are not linear.”

Upcoming data will see the release of Mexican inflation figures for August, and the US ISM Non-Manufacturing PMI will give direction to the USD/MXN pair. Nevertheless, expect further Mexican Peso weakness after Banxico’s hedge cuts.

USD/MXN Price Analysis: Technical outlook

The USD/MXN is consolidating, with the pair unable to crack to new year-to-date (YTD) lows while reversing its course, threatening to edge higher if it reclaims a mult-month downslope resistance trendline and the 50-day Moving Average (DMA) at around 17.20/17.2900. If that area is reclaimed, look for buyers to test the May 17 daily low turned resistance at 17.4038, seen as a crucial level to overcome, before testing the confluence of the 200-DMA and the psychological 18.0000 figure. On the downside, risks emerge below the confluence of the 20 and 50-DMA at around 16.98/96.

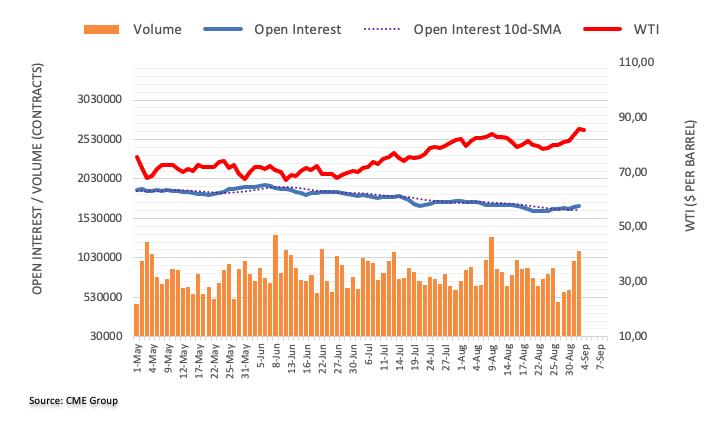

- WTI found support at $85.32 and then settled around $85.50.

- Investors continue to asses the US’s August NFPs released on Friday.

- OPEC expected to extend its voluntary production cuts.

The West Texas Intermediate (WTI) barrel cleared daily losses and traded neutral in the $85.50 - $86.00 zone near multi-month highs, benefited by a softer USD. The Greenback is trading weak against most of its rivals while investors digest Friday’s Nonfarm Payroll (NFP) figures. No relevant economic data will be released during the session, and the focus will shift to Wednesday’s ISM Services PMI figures from August.

NFPs revealed that headline employment grew, but so did the unemployment rate, and wage inflation measured by the Average Hourly Earnings decelerated. Signs of the labour market cooling may ease the pressure on the Federal Reserve (Fed) to continue hiking, and markets started to price in a less aggressive stance for the remainder of the year. As for now, the CME FedWatch tool indicates that the odds of a pause in September remain high while the probabilities of a hike in November and December decreased to nearly 35%, and those dovish bets explain the USD weakness. Interest rates and Oil prices tend to be negatively correlated, so as the Fed approaches the end of its tightening cycle, the WTI may gain further traction.

In addition, the Organization of the Petroleum Exporting Countries (OPEC) and its allies, including Russia, are expected to extend their voluntary production cuts into October, which could contribute to a tighter global supply. Oil prices may get an additional boost.

WTI Levels to watch

Based on the daily chart assessment, a bullish outlook is noted for WTI in the near future. The Relative Strength Index (RSI) resides above its midline in the positive territory near the overbought threshold. It is further validated by the green bars on the Moving Average Convergence Divergence (MACD), indicating a robust bullish momentum. Moreover, the pair is above the 20,100,200-day Simple Moving Average (SMA), pointing towards the prevailing strength of the bulls in the larger context.

Support levels: $85.30, $84.00, $83.00.

Resistance levels: $87.00, $88.00, $89.00

WTI Daily Chart

-638294399089740976.png)

- China’s measures to boost its property market initially lifted investor sentiment.

- Traders price in a less aggressive Federal Reserve; first-rate cut expected in May.

- The upcoming week features sparse New Zealand economic data but includes the RBA monetary policy meeting.

The New Zealand Dollar (NZD) losses some traction against the Greenback (USD) on thin liquidity conditions due to the observance of Labor Day in the United States (US). Even though China’s measures to boost its economy and a risk-on impulse, the pair is under stress after hitting a daily high of 0.5961. The NZD/USD is trading at 0.5935, down 0.04%.

The NZD lost ground despite positive news from China and the Fed’s less aggressive outlook

Price action remains subdued as volume remains scarce. Overnight news from China improved investors’ mood as the country established measures to boost its property market, which is at the brisk of a crisis. As the Government easied measures, home sales rose, as reported by Bloomberg.

Aside from this, traders have begun to price in a less aggressive Federal Reserve (Fed) in the US. Interest rate probabilities for the September meeting remain at 92%, with the first-rate cut seen on May 1, as shown by the bottom picture. On that date, traders foresee rates at around 5.14%, 19 basis points below the effective Federal Funds Rate (FFR) of 5.33%.

Source: Financialsource

The latest round of US data witnessed Nonfarm Payrolls for August at 187K above estimates, which warranted a US Dollar upside in other conditions. Still, it wasn’t the case as the Unemployment Rate rose by 3.8% YoY, above estimates of 3.5%. Analysts at TDS Securities noted, “We think this week’s labor-market and consumer prices data should be judged as positive news by Fed officials, and we continue to view July as the last hike of the Fed’s tightening cycle.”

In the week ahead, the New Zealand economic docket is empty, except for the Global Dairy Trade Price Index release. Nevertheless, one of its largest trading partners, Australia, has scheduled the Reserve Bank of Australia’s (RBA) monetary policy meeting, in which the central bank is expected to keep rates unchanged. In that outcome, the NZD/USD could continue to resume lower unless an upbeat market mood keeps flows going toward riskier assets.

On the US front, a slew of Fed officials would keep traders entertained before policymakers enter their blackout period ahead of September’s monetary policy meeting.

NZD/USD Price Analysis: Technical outlook

From a technical standpoint, the NZD/USD is downward biased, but in the short-term, it’s sideways, in the middle of the August 25-September 1 swing low/high at 0.5886-0.6015, waiting for a clear direction to resume a larger correction. However, if the pair tumbles below 0.5900, expected sellers to pile up and drive prices toward the year-to-date (YTD) low of 0.5886, with further downside seen at the November 3 low of 0.5740. Conversely, a rally to 0.6000 could pave the way for an upward correction, with the 50-day Moving Average (DMA) targeted at 0.6098.

- Silver price corrects further as the US Dollar remains firm due to stable job growth.

- Fed Mester that demand and supply in the labor market is coming into a better balance.

- Silver price demonstrates a Broadening Triangle chart formation.

Silver price (XAG/USD) extends its correction to near the crucial support of $24.00 even though investors hope that the Federal Reserve (Fed) is done with hiking interest rates. The white metal remained offered from Thursday but the broader trend is still positive as the tight United States labor market starts cooling down.

S&P500 futures remain lackluster as US markets are closed on account of Labor Day. Due to the extended weekend, weak volume is expected in the FX domain too. Also, the market mood is quiet due to an extended weekend.

The US Dollar Index (DXY) looks set to extend recovery above the immediate resistance of 104.20 as job growth remains solid in August.

Cleveland Fed Bank President Loretta Mester said on Friday that demand and supply in the labor market is coming into a better balance but the job market is still strong. She further added that while job growth has slowed and job openings are down, the Unemployment Rate is low.

Also, US Manufacturing PMI for August increased to 47.6 from 46.4 in July but remained below the 50.0 mark, which itself shows a contraction in activities. After factory activities, investors shift focus to the Services PMI for August, which will be published on Wednesday.

Silver technical analysis

Silver price demonstrates a Broadening Triangle chart formation on a two-hour scale. The downside is supported near the horizontal resistance plotted from August 25 low around $23.92. A declining 20-period Exponential Moving Average (EMA) indicates that the mid-term trend is bearish. The Relative Strength Index (RSI) (14) shifts into the bearish range of 20.00-40.00, which indicates that a bearish impulse is already active.

Silver two-hour chart

-638294339190992924.png)

Analysts at MUFG Bank forecast the USD/INR at 82.70 by the end of the third quarter and at 81.50 by the end of the first quarter of next year. They have a neutral view of the Indian Ruppe in the short term.

Neutral on INR near-term

We recently turned neutral on INR, and further raise our USD/INR forecast to 82.700 in 3m and 81.000 in 12m with our global team now calling for a shallower and delayed path for US dollar weakness.

There are some headwinds for INR in the nearterm, with inflation spiking more than we initially anticipated in July, albeit mainly driven by food prices so far.

The RBI should remain hawkish for longer. We still expect the next move to be a rate cut but see this happening in June 2024 at the earliest.

The structural reforms over the past decade put India in a good place to benefit from FDI flows, in part to tap the domestic market, but also in line with broader trends to diversify companies’ supply chains.

- EUR/USD makes a U-turn and regains the 1.0800 zone.

- Further decline could revisit the August low near 1.0760

EUR/USD manages to pick up some traction and reclaims the area above 1.0800 the figure at the beginning of the week.

The sharp retracement seen in the latter part of last week seems to have shifted the attention to the downside. Against that, the next contention area aligns at the August low of 1.0765 (August 25) prior to the May low of 1.0635 (May 31).

In the meantime, further losses remain in the pipeline while below the key 200-day SMA, today at 1.0817.

EUR/USD daily chart

- USD/JPY prepares for a fresh rally amid strength in the US Dollar Index.

- The US Dollar remains firm US Dollar due to steady labor growth in August despite higher interest rates by the Fed.

- USD/JPY has been consolidating in a narrow range of 145.58-147.38 for the past three weeks.

The USD/JPY pair gathers strength to extend the V-shape recovery above the immediate resistance of 146.50. The asset remains solid due to a firmer US Dollar amid steady labor growth in August despite higher interest rates by the Federal Reserve (Fed).

The market mood remained majorly quiet on Monday due to an extended weekend in the US on account of Labor Day. The US Dollar Index (DXY) corrects gradually to near 104.00 from the four-day high of 104.20 as investors await the ISM Services PMI for August, which will be published on Wednesday.

Meanwhile, hopes that the Fed will keep interest rates unchanged in the remaining year rose as labor market conditions cool down further. The Unemployment Rate rose and wage growth slowed in August.

USD/JPY has been consolidating in a narrow range of 145.58-147.38 for the past three weeks. The asset is demonstrating a volatility contraction and is expected to deliver a decisive action after a consolidation break.

The asset continues to find support from the upward-sloping 20-day Exponential Moving Average (EMA), which trades around 145.31. Also, advancing 50-EMA indicates that the short-term trend is extremely bullish. Potential resistance is plotted from 21 October 2022 high at around 152.00.

The Relative Strength Index (RSI) (14) aims to stabilize into the bullish range of 60.00-40.00. An occurrence of the same will activate the upside momentum.

Going forward, a decisive break above August 29 high at 147.38 will expose the asset to the psychological resistance of 150.00, followed by 21 October 2022 high at around 152.00.

In an alternate scenario, a breakdown below September 1 low at 144.44 would drag the asset toward the 50-DEMA around 143.50 and July 21 high around 142.00.

USD/JPY daily chart

-638294319240410186.png)

"It will be critical for central banks to keep inflation expectations firmly anchored while these relative price changes play out," Christine Lagarde, President of the European Central Bank (ECB), said on Monday.

"It is exactly when people are paying most attention that central banks should deliver their key communication to ensure that those expectations remain firmly anchored," she added while speaking at the Distinguished Speakers Seminar organised by the European Economics & Financial Centre.

Market reaction

These comments failed to trigger a noticeable market reaction and EUR/USD was last seen trading in positive territory near 1.0800.

- DXY gives away part of the recent two-day advance on Monday.

- Bulls continue to target the 104.50 region in the near term.

DXY partially surrenders the sharp uptick seen in the second half of last week and challenges the key 104.00 neighbourhood on Monday.

If bulls regain the upper hand, the index should shift its focus to another visit to the monthly peak of 104.44 (August 25) just before the May top of 104.69 (May 31). The breakout of this level could prompt a probable test of the 2023 high at 105.88 (March 8) to re-emerge on the horizon.

While above the key 200-day SMA, today at 103.04, the outlook for the index is expected to remain constructive.

DXY daily chart

- EUR/JPY sets aside two daily pullbacks in a row and retests 158.00.

- There seems to be a decent contention area around 157.00.

EUR/JPY regains some upside traction and reverses two straight sessions of losses at the beginning of the week.

The continuation of the uptrend could see the cross challenging the recent 2023 peak at near 159.76 (August 30) ahead of the key round level at 160.00. The surpass of the latter should not see any resistance level of note until the 2008 high at 169.96 (July 23).

In the meantime, the resumption of the selling pressure is expected to meet initial support at the weekly low around 157.00 (September 1), an area reinforced by the temporary 55-day SMA.

So far, the longer term positive outlook for the cross appears favoured while above the 200-day SMA, today at 148.05.

EUR/JPY daily chart

There is still scope for USD/IDR to keep navigating within a 15,185-15,300 range for the time being, suggests Markets Strategist Quek Ser Leang at UOB Group.

Key Quotes

Last week, we expected USD/IDR to trade sideways between 15,240 and 15,340. However, it traded in a lower range of 15,210/15.298.

There is no clear increase in downward momentum and we continue to expect USD/IDR to trade sideways, probably between 15,185 and 15,300.

- USD/CAD remains sideways around 1.3600 as the US and Canadian markets will remain closed on Monday on account of Labor Day.

- The US Dollar maintains its bullish mainstay as job growth remained steady in August.

- The BoC is expected to keep interest rates unchanged at 5% on Wednesday.

The USD/CAD pair remains sideways after a vertical rally near the round-level resistance of 1.3600 in the late European session. The Loonie asset is expected to remain lackluster on Monday as the US and Canadian markets will remain closed on account of Labor Day.

S&P500 futures generate some gains in Europe, portraying strength in the risk-appetite theme. The US Dollar Index (DXY) faces nominal selling pressure near a four-day high at 104.20 while the upside is still favored as investors remain cautious that the Federal Reserve (Fed) will keep interest rates higher for a longer period.

The US Dollar maintains its bullish mainstay as hiring momentum remained steady in August despite restrictive interest rate policy by the Fed. As per the US Nonfarm Payrolls (NFP) report, the job market witnessed a fresh addition of 187K new employees, which was higher than expectations of 170K and July's reading of 157K. However, the higher Unemployment Rate and slower wage growth boost hopes of the Fed announcing a pause in its current tightening spell.

Meanwhile, oil prices turn sideways after a massive rally near $85.50 as Saudi Arabia is expected to extend supply cut by one million barrels per day from October. In an already shrinking oil market, tight supply expectations keep oil prices on fire.

It is worth noting that Canada is the leading exporter of oil to the United States and higher oil prices will support the Canadian Dollar.

This week, the major trigger will be the interest rate decision by the Bank of Canada (BoC), which will be announced on Wednesday. BoC Governor Tiff Macklem is expected to keep interest rates unchanged at 5% as job growth remains slow.

Markets Strategist Quek Ser Leang at UOB Group expects USD/MYR to extend the current side-lined trading in the next few sessions.

Key Quotes

Last week, we highlighted that USD/MYR “could continue to trade in a range this week, likely between 4.6200 and 4.6700.” USD/MYR then traded in a narrower range of 4.6270/4.6540.

The quiet price actions offer no fresh clues, and we continue to expect USD/MYR to trade in a range, likely between 4.6250 and 4.6660.

- US Dollar price action expected to head sideways at the start of the week.

- No real outliers or data points to monitor at the start of the week.

- The US Dollar Index is likely to hold above 104.00.

The US Dollar (USD) steadies on Monday, in a mixed bag against most major currencies. No real outliers to notice as US traders are enjoying the US Labor Day bank holiday. Expect low volumes this Monday as several futures markets are closed.

The focal point this week will be on Wednesday, when the Institute of Supply Management (ISM) will publish the key Services Purchasing Managers Index (PMI) survey for August. Additionally, nearly eight central bank speakers are due to make an appearance and might guide the market towards the next US Federal Reserve meeting on September 20.

Daily digest: US Dollar steadies while enjoying a break

- A very calm calendar ahead with US markets closed for the US Labor Day holiday.

- Germany July Machinery orders fell 11% on a yearly basis.

- Italy is set to prepare for raising its 2023 budget deficit targets, according to Reuters.

- Chinese president Xi Jinping will not attend the G-20 summit in India after reports that Chinese banks are distributing billions of loans to Russia.

- China issues more stimulus measures, which makes the property stocks gauge jump 2.8%.

- Markets will be on edge to hear if the biggest property developer of China, Country Garden, can afford its bond payments, which are already in an extended grace period. Non-payment would trigger a default.

- A similar picture to Friday unfolds in the equity markets with the Japanese Topix index closes at +1.02%. The Hong Kong Hang Seng is about to close higher after its emergency close on Friday due to a typhoon. The index caught up, jumping 2.50% near its closing bell. European equities are trading higher over 0.50% and US equity futures are mildly in the green.

- The CME Group’s FedWatch Tool shows that markets are pricing in a 93% chance that the Federal Reserve will keep interest rates unchanged at its meeting in September.

- The benchmark 10-year US Treasury bond yield trades at 4.18% and will not move this Monday as bond markets are closed for US Labor Day.

- US Dollar Index technical analysis: left or right

- The US Dollar is steady, with no real outliers to report on this Monday. Volumes are usually lower on Mondays, and even more today with the US markets closed for US Labor Day. No big moves to takeaway for the US Dollar Index (DXY), which looks to be consolidating above 104.00.

In case pace picks up again on Tuesday in the same direction asFriday, a surge towards 104.00 is likely. In this region, 104.35 (the peak of August 29) is an ideal candidate for a double top. Should the Greenback go on a tear, expect a test at 104.47 – the six-month high. From there, 104.70 from May 31 will be the next target.

On the downside, the summer rally of the DXY will be the key element to track for any change in sentiment. That is the 200-day Simple Moving Average (SMA) at 103.06, which could bring substantially more weakness once the DXY starts trading further below it. The double belt of support at 102.42, with both the 100-day and the 55-day SMA, are the last lines of defence before the US Dollar sees substantial and longer-term depreciation.

US Dollar FAQs

What is the US Dollar?

The US Dollar (USD) is the official currency of the United States of America, and the ‘de facto’ currency of a significant number of other countries where it is found in circulation alongside local notes. It is the most heavily traded currency in the world, accounting for over 88% of all global foreign exchange turnover, or an average of $6.6 trillion in transactions per day, according to data from 2022.

Following the second world war, the USD took over from the British Pound as the world’s reserve currency. For most of its history, the US Dollar was backed by Gold, until the Bretton Woods Agreement in 1971 when the Gold Standard went away.

How do the decisions of the Federal Reserve impact the US Dollar?

The most important single factor impacting on the value of the US Dollar is monetary policy, which is shaped by the Federal Reserve (Fed). The Fed has two mandates: to achieve price stability (control inflation) and foster full employment. Its primary tool to achieve these two goals is by adjusting interest rates.

When prices are rising too quickly and inflation is above the Fed’s 2% target, the Fed will raise rates, which helps the USD value. When inflation falls below 2% or the Unemployment Rate is too high, the Fed may lower interest rates, which weighs on the Greenback.

What is Quantitative Easing and how does it influence the US Dollar?

In extreme situations, the Federal Reserve can also print more Dollars and enact quantitative easing (QE). QE is the process by which the Fed substantially increases the flow of credit in a stuck financial system.

It is a non-standard policy measure used when credit has dried up because banks will not lend to each other (out of the fear of counterparty default). It is a last resort when simply lowering interest rates is unlikely to achieve the necessary result. It was the Fed’s weapon of choice to combat the credit crunch that occurred during the Great Financial Crisis in 2008. It involves the Fed printing more Dollars and using them to buy US government bonds predominantly from financial institutions. QE usually leads to a weaker US Dollar.

What is Quantitative Tightening and how does it influence the US Dollar?

Quantitative tightening (QT) is the reverse process whereby the Federal Reserve stops buying bonds from financial institutions and does not reinvest the principal from the bonds it holds maturing in new purchases. It is usually positive for the US Dollar.

"Dollar consolidates gains, bonds maintain losses after break-out in oil prices overshadowed the rise in US unemployment rate to 3.8% in August," note analysts at Société Générale.

US markets are closed today

"Decline in payrolls growth confirms labour market loosening, cements Fed pause. US markets are closed today."

"Week ahead: ECB’s Lagarde speaks today, ECB inflation expectations tomorrow and US ISM services on Wednesday. RBA and BoC forecast to keep rates on hold Tuesday/Wednesday. SG house view: Chile CB to cut 100bp tomorrow and Poland to launch easing cycle on Wednesday with a 25bp cut to 6.50%. CPI from Mexico, Chile, Hungary also on agenda."

"China: existing home sales in Beijing jumped 100% to 1,200 units on Saturday from a week before according to Security Journal following lower minimum down payment and easing mortgage restrictions."

Analysts at Rabobank assess the latest CFTC Commitment of Traders report:

Forecasters are confident BoC rates will remain on hold this week

"USD net long positions decreased slightly. This was driven by an increase in short positions. Lower than anticipated JOLTS printed on Tuesday and may act as support for the Fed to pause future rate hikes."

"EUR net long positions have decreased. This was driven by an increase in short positions as the market evaluates recent weak Eurozone economic data and doubts spread as to the ability of the ECB to hike rates further."

"GBP net speculators’ long positions increased for the third consecutive week. This was driven by an increase in long positions. The market continues to price in further BoE rate hikes."

"JPY net short positions have increased for the second consecutive week. This was driven by a contraction in long positions, and an increase in short positions, given shifting expectations that the BoJ may not prove more dovish than previously thought."

"CHF net shorts have fallen for the fourth consecutive week. Short positions decreased slightly as the SNB remains hawkish."

"CAD net shorts have increased slightly. This was driven by a contraction in long positions. Surveys suggest forecasters are confident that BoC rates will remain on hold this week."

"AUD net short positions have increased for the second consecutive week. This was driven by an increase in short positions and has driven the volume of short positions to an all-time high. Weak Chinese data is impacting the AUD, although Australian fundamentals are holding up relatively well."

Analysts at TD Securities thinks that the Reserve Bank of Australia will leave its policy rate unchanged following the September policy meeting.

Governor Lowe's last RBA meeting

We expect the RBA to leave the cash rate unchanged at 4.1% (cons: 4.1%) at the September meeting after the encouraging July CPI print. The economic data hasn't provided much impetus for the RBA to restart its hiking cycle since the Bank transited to a fine-tuning phase in this cycle, emphasising that the Board will take decision month-by-month based on incoming data.

"July CPI inflation continued to decelerate to 4.8% y/y while the job losses of -14.6k in July cements the case for another pause from the Bank. As such, we doubt there will be any distinct shift in the RBA's messaging at the September meeting and expect Governor Lowe's last RBA meeting to go without much fanfare."

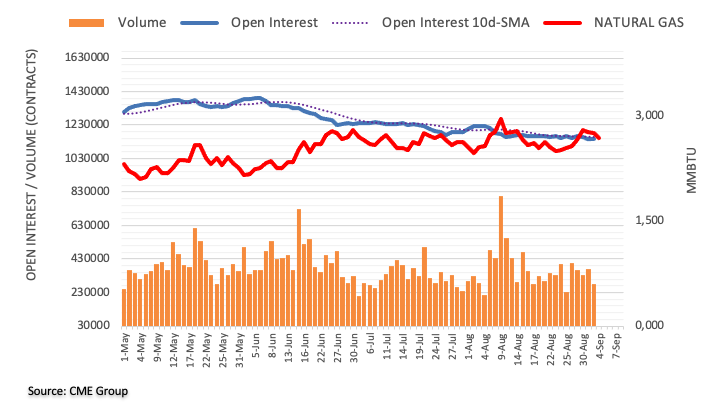

- Natural Gas takes a small step back as US markets close due to the Labor Day Holiday.

- The US Dollar weakens slightly after Friday’s knee-jerk reaction on Nonfarm Payrolls data.

- Support at $2.80 likely to hold before the rally picks up again.

Natural Gas falls slightly in European trading hours as US markets are closed for Labor Day. Substantial declines aren’t expected as European gas supply is under pressure. Over the weekend, supply from three Norwegian gas fields was halted, sending Norwegian gas exports to the EU to its lowest level since 2015.

Meanwhile, the US Dollar trades mixed after a US Jobs report that delivered a knee-jerk reaction. The US Dollar Index first weakened on the initial headlines, and reversed an hour later as markets digested the report’s content, which pointed to still strong labour market conditions. With the US on holiday, no big moves are expected in either Natural Gas futures or in the Greenback.

At the time of writing, Natural Gas is trading at $2.844 per MMBtu.

Natural Gas news and market movers

- The European Natural Gas price jumped 5.3% due to surprise outages in Norway.

- The risk of strikes inAustralia remains high, an outcome that could hit Natural Gas supply going forward.

- Japan’s spot power price climbed 5.5% for the week as bad weather hurts the solar-power supply and puts higher pressure on LNG supplies. Reports of regional costs soaring on LNG supply are being factored into the price as well.

- Further unplanned curbs in Norway are projected due to unforeseen maintenance at the Aasta Hansteen field. The Dvalin field is also impacted, while planned works at Oseberg are being extended due to unforeseen delays.

Natural Gas Technical Analysis: steady during US holiday

Natural Gas was on a tear last week, together with Crude Oil prices. Though the European bloc has its gas stockpiles filled up over more than 90%, it looks like it will need to scramble for any further needs..

On the upside, $3 is the level to watch after the double top formation from Friday and Thursday. Just above there, the 200-day Simple Moving Average (SMA) is present as a cap and has not been tested in the past few months. Keep an eye on $3.03 before targeting $3.18 and testing the upper side of the trend channel.

On the downside, the trend channel has done a massive job underpinning the price action. Aside from one small false break, ample support was provided near $2.71. The 55-daySMA needs to give that much needed support at $2.71 ahead of the ascending trend channel at $2.63. Any falling knives can still be caught by the 100-day SMA near $2.58.

-638294212984860896.png)

Natural Gas FAQs

What fundamental factors drive the price of Natural Gas?

Supply and demand dynamics are a key factor influencing Natural Gas prices, and are themselves influenced by global economic growth, industrial activity, population growth, production levels, and inventories. The weather impacts Natural Gas prices because more Gas is used during cold winters and hot summers for heating and cooling. Competition from other energy sources impacts prices as consumers may switch to cheaper sources. Geopolitical events are factors as exemplified by the war in Ukraine. Government policies relating to extraction, transportation, and environmental issues also impact prices.

What are the main macroeconomic releases that impact on Natural Gas Prices?

The main economic release influencing Natural Gas prices is the weekly inventory bulletin from the Energy Information Administration (EIA), a US government agency that produces US gas market data. The EIA Gas bulletin usually comes out on Thursday at 14:30 GMT, a day after the EIA publishes its weekly Oil bulletin. Economic data from large consumers of Natural Gas can impact supply and demand, the largest of which include China, Germany and Japan. Natural Gas is primarily priced and traded in US Dollars, thus economic releases impacting the US Dollar are also factors.

How does the US Dollar influence Natural Gas prices?

The US Dollar is the world’s reserve currency and most commodities, including Natural Gas are priced and traded on international markets in US Dollars. As such, the value of the US Dollar is a factor in the price of Natural Gas, because if the Dollar strengthens it means less Dollars are required to buy the same volume of Gas (the price falls), and vice versa if USD strengthens.

According to Markets Strategist Quek Ser Leang at UOB Group, USD/THB is now seen trading within the 34.90-35.35 range.

Key Quotes