- Analytics

- News and Tools

- Market News

Новини ринків

- USD/JPY has sensed some buying interest around 134.40 as investors are shifting their focus toward US NFP data.

- The market mood seems divided as risk-perceived currencies are enjoying bids while US equities are facing pressure.

- US banking woes have renewed as PanWest Bancorp has come under pressure.

The USD/JPY pair has gauged an intermediate cushion after a perpendicular sell-off to near 134.40 in the Asian session. The asset witnessed massive selling pressure after neutral interest rate guidance came from the Federal Reserve (Fed) post a widely anticipated 25 basis point (bp) rate hike.

S&P500 futures have recovered some losses posted in early Asia, showing signs that investors are digesting uncertainty about the further roadmap of arresting stubborn United States inflation by the Fed. The overall market mood seems divided as risk-perceived currencies are enjoying bids while US equities are facing pressure.

Meanwhile, US banking woes have renewed as another commercial bank has come under pressure. Bloomberg reported that PacWest Bancorp is considering strategic options, including a potential sale. PacWest's shares fell by more than 50% in the post-market, indicating significant investor concern about the bank's situation.

Investors should be aware that Japanese markets are closed today on account of Greenery Day

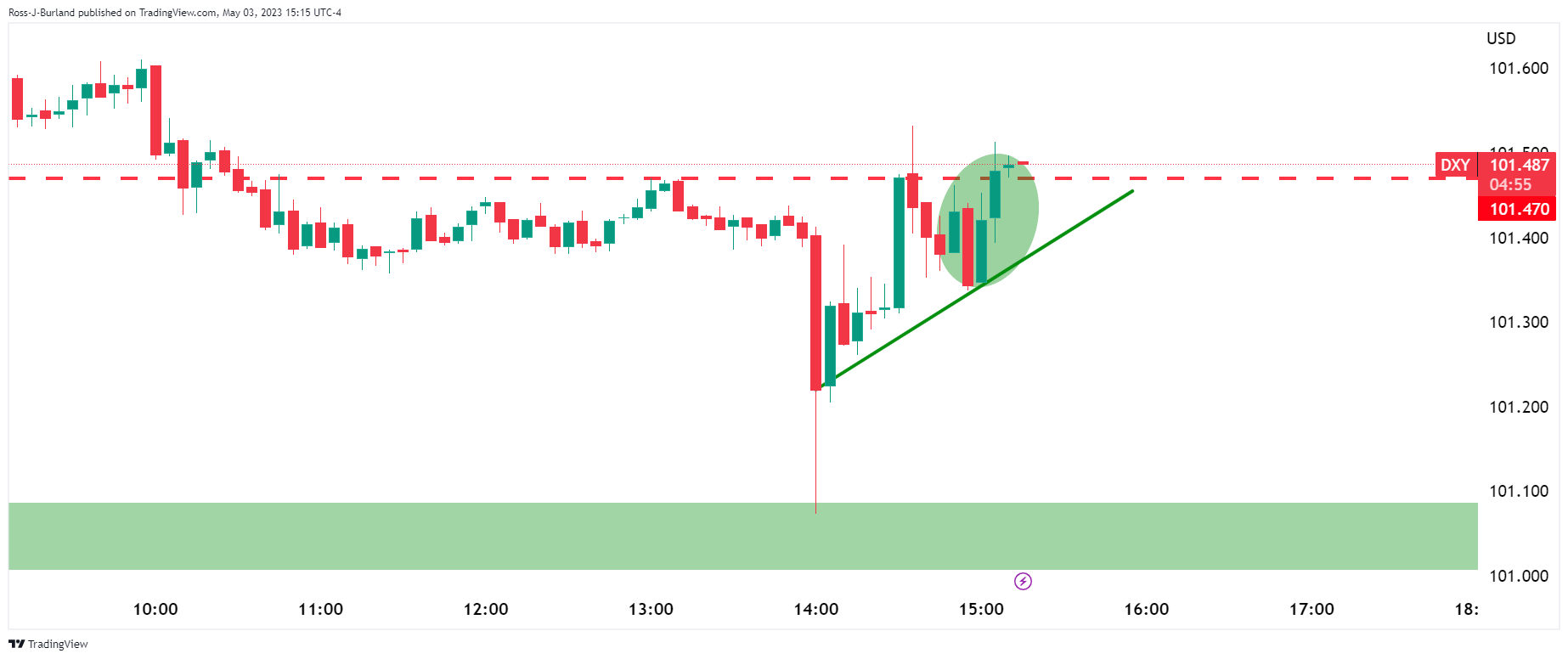

The US Dollar Index (DXY) has dropped to near 101.20 on neutral Fed guidance, renewed US banking jitters, and concerns over the US debt ceiling. Further delay in debt ceiling increase could result in loss of timely payments from the US Treasury.

On Wednesday, the US Automatic Data Processing (ADP) agency reported an addition of fresh 296K jobs in April vs. the estimates of 150K and the former release of 145K. Upbeat US ADP data indicates tight labor market conditions in the US economy.

Going forward, US official Employment data will be of utmost importance. The Unemployment Rate is seen unchanged at 3.5%. According to the consensus for Nonfarm Payrolls (NFP), the US economy added 179K in April lower than the former release of 236K.

Apart from the labor market numbers, Average Hourly Earnings will be keenly watched. The economic indicator is seen unchanged at 0.3% and 4.2% on a monthly and an annual basis.

Silver price (XAG/USD) grinds higher during a three-day uptrend to early Thursday in Asia, near up 0.50% intraday near $25.70 by the press time. In doing so, the bright metal justifies the US Federal Reserve’s (Fed) hesitance in suggesting further rate hikes, despite lifting the benchmark rates by 0.25%, as well as the upbeat options market sentiment.

That said, the one-month risk reversal (RR) of the Silver price, a gauge of the spread between the call and put options, prints the strongest bullish level of 0.1000 in three weeks by the end of Wednesday’s North American session. It’s worth noting that the daily RR dropped the most since April 18 the previous day. Even so, the Silver options market signals remain bearish for May, after a downbeat April.

Given the recently upbeat options market signals, coupled with the US Dollar’s failure to cheer the Fed’s rate hike, the Silver price may witness further advances.

However, today’s European Central Bank (ECB) decision and the risks surrounding the US default and banking crisis will be the key to watch for fresh impulse.

Also read: Forex Today: Dollar slides as Fed delivers as expected

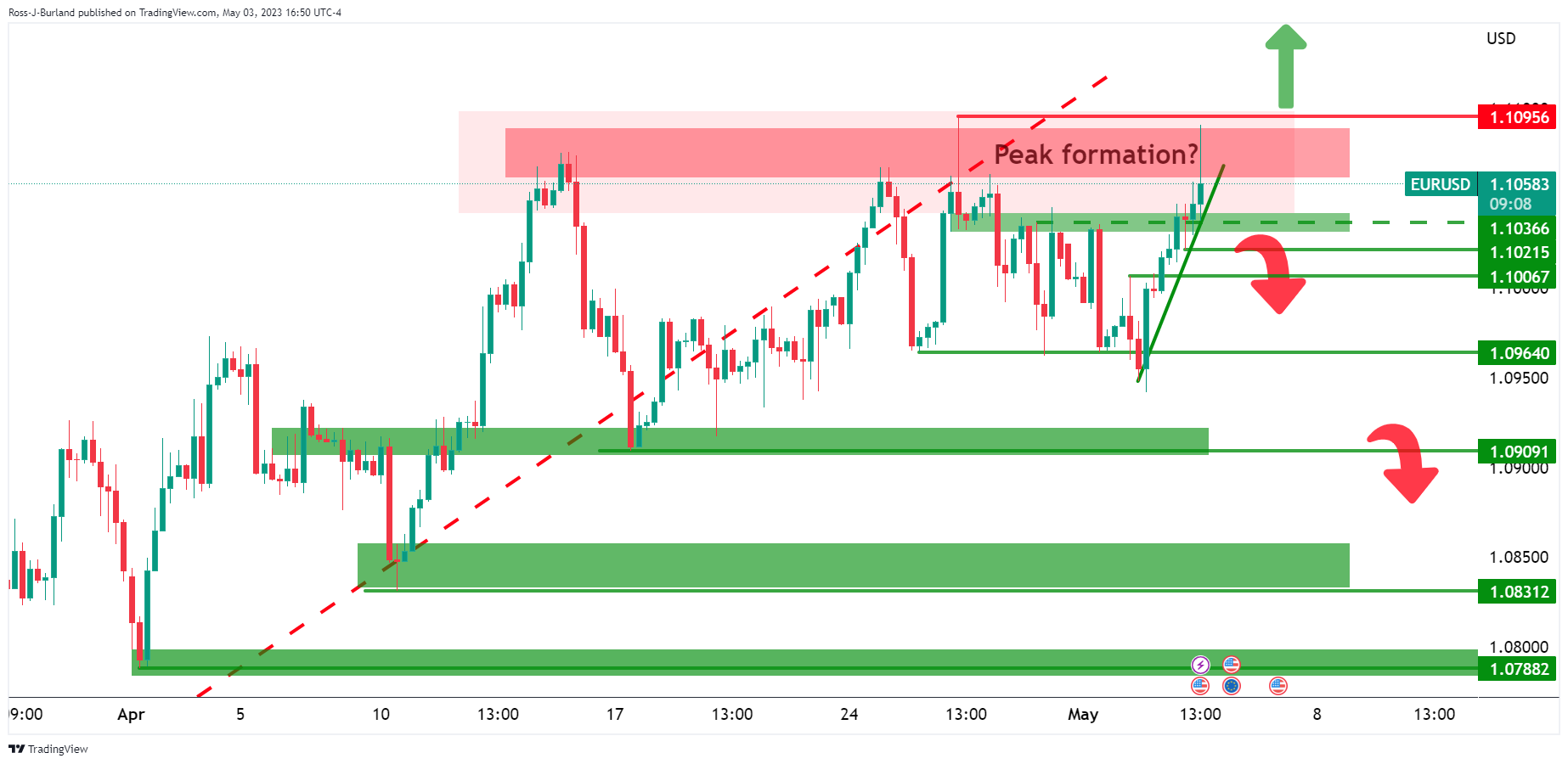

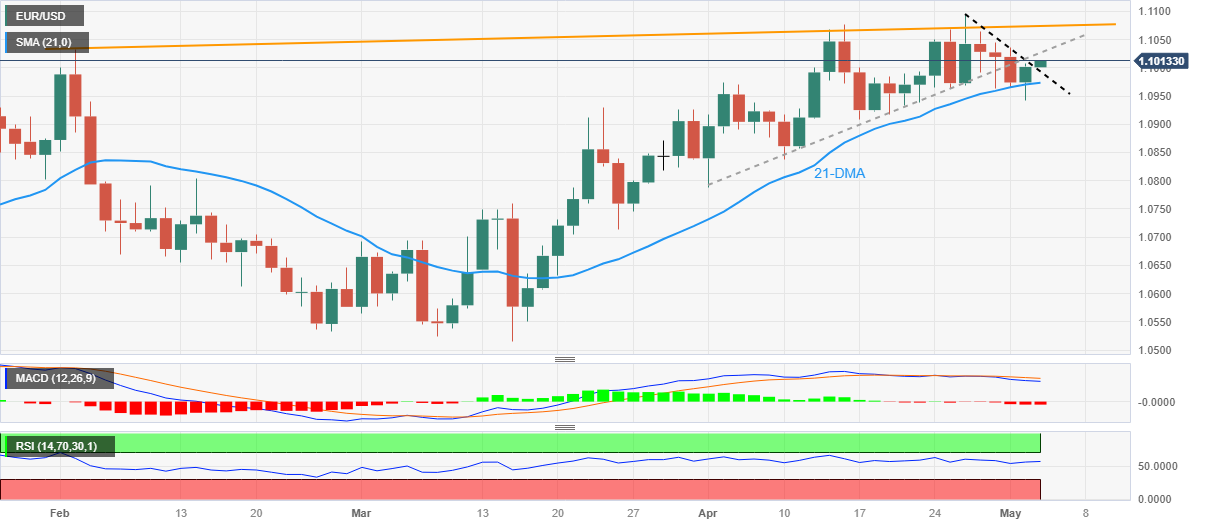

- EUR/USD grinds higher within a three-week-old bullish trend channel.

- Sustained break of weekly resistance line, 100-SMA joins bullish MACD signals to favor Euro buyers.

- RSI prints lower high despite EUR/USD’s gradual increase, challenging further advances.

- Sellers need validation from 200-SMA to retake control.

EUR/USD bulls keep the reins near the highest levels in 13 months by printing mild gains near 1.1070 as Euro traders await Thursday’s European Central Bank (ECB) monetary policy decision.

In doing so, the Euro pair defends the Federal Reserve-inspired gains with a three-week-old ascending trend channel. However, a divergence between the RSI (14) line and the EUR/USD price challenges the pair buyers ahead of the key event.

Also read: European Central Bank Preview: Lagarde set to lift the Euro in two out of three scenarios

It’s worth noting that the RSI (14) line is in a descending formation since April 14 even if the Euro pair grinds higher, which in turn suggests that the bulls are running out of steam.

The same joins the quote’s nearness to the aforementioned trend channel’s resistance line, close to 1.1110, to increase the odds of the EUR/USD pair’s pullback.

In that case, a convergence of the 100-SMA and one-week-old previous resistance line, near 1.0995, could lure the intraday sellers ahead of the stated channel’s bottom line, close to 1.0950 at the latest.

Even so, the EUR/USD bears need to remain cautious ahead of the 200-SMA break, currently around 1.0925.

On the contrary, an upside clearance of the 1.1110 hurdle comprising the channel’s top line could propel the Euro price towards the March 2022 high of near 1.1185.

EUR/USD: Four-hour chart

Trend: Pullback expected

- USD/CAD is preparing for further side as oil prices continue to bleed amid fears of a global economic slowdown.

- Later this week, US/Canada Employment data will be keenly watched.

- USD/CAD is approaching the 61.8% Fibonacci retracement plotted at 1.3648.

The USD/CAD pair has turned sideways after a perpendicular rally to near 1.3630 in the early Asian session. The Loonie asset is gathering strength for further upside as a bloodbath in oil prices amid deepening fears of a global economic slowdown due to higher interest rates from central banks. The street is worried about the oil demand outlook as tight liquidity conditions would force firms to underutilize their production capacities.

Oil prices have refreshed their annual low of $63.60 after the Federal Reserve (Fed) hikes interest rates by 25 basis points (bps) to 5.00-5.25%.

Going forward, the Canadian Dollar will dance to the tunes of Friday’s Employment data (April). The net change in Employment is seen at 20K higher than the former addition of 34.7K. The Unemployment Rate is expected to increase to 5.1%.

Also, the US Employment data (April) will be keenly watched. The US Nonfarm Payrolls (NFP) data is seen at 179K lower than the former release of 236K.

USD/CAD is approaching the 61.8% Fibonacci retracement (placed from March 10 high at 1.3862 to April 14 low at 1.3301) at 1.3648. The downward-sloping trendline from March 10 high at 1.3862 has acted as a major barricade for the US Dollar bulls.

The 20-period Exponential Moving Average (EMA) at 1.3600 is providing cushion to the US Dollar bulls.

Meanwhile, the Relative Strength Index (RSI) (14) is making efforts for shifting into the bullish range of 60.00-80.00. An occurrence of the same will activate the bullish momentum.

An extension in a recovery move above the 61.8% Fibo retracement at 1.3650 will trigger a reversal and will drive the major toward the round-level resistance at 1.3700. A break above the same will expose the asset to March 22 high at 1.3745.

On the flip side, a decisive break below May 02 low at 1.3529 will expose the asset to psychological support at 1.3500 followed by a 23.6% Fibo retracement at 1.3438.

USD/CAD four-hour chart

- US Dollar Index remains depressed after falling the most in seven weeks.

- Fed fails to impress US Dollar bulls despite 0.25% rate hike as policy pivot gains attention.

- Looming fears of US default, banking sector turmoil also weigh on DXY.

- Second-tier US data can entertain traders, risk catalysts are the key ahead of NFP.

US Dollar Index (DXY) remains pressured at the lowest level in a week, recently licking its wounds near 101.30 amid early Thursday in Asia, after falling the most in two months due to the Federal Reserve’s dovish rate hike. Also exerting downside pressure on the greenback’s gauge versus six major currencies are the fears surrounding the US default and baking crisis.

US Federal Reserve (Fed) matched market forecasts on Wednesday by announcing a 0.25% increase in the benchmark Fed rate, making it the highest since 2007. Fed Chairman Jerome Powell also appeared positive while ruling out fears of a banking rout. However, a dropping in the statement suggesting the need for further rate hikes gained major attention and weighed on the US Dollar despite the hawkish move by the Fed.

Apart from the Fed, the looming banking crisis in the US also weighs on the US Dollar as PacWest Bancorp recently became another US bank to witness the heat of excess withdrawal and is on the brink of collapse. That said, Western Alliance Bancorp is also in the line and hence the US banking sector appears in trouble moving forward, which in turn sours the market sentiment and prods the hawkish central banks, as it did to the Fed.

Furthermore, the comments from the White House suggesting debt limit default could cost 8.3 million job losses also weigh on the sentiment and the US Dollar.

It’s worth noting that the upbeat US data also failed to impress the DXY bulls. US ADP Employment Change rose to 296K for April from 142K prior versus 148K market forecast. Additionally, the annual pay growth declined to 13.2% from 14.2%. Further, ISM Services PMI improved to 51.9 in April versus 51.8 market forecasts and 51.2 previous readings. It’s worth noting, however, that the S&P Global Services PMI and Composite PMI for April eased to 53.6 and 53.4 versus 53.7 and 53.5 respective priors.

While portraying the mood, Wall Street closed with minor losses and the yields remain pressured while weighing on the US Dollar Index.

Looking forward, DXY traders will pay close attention to the risk catalysts for fresh impulse amid a dearth of top-tier data. However, European Central Bank (ECB) Monetary Policy Meeting can entertain traders.

Technical analysis

Failure to provide a daily closing below the three-week-old ascending support line, near 101.15 by the press time, joins nearly oversold RSI (14) line to signal corrective bounce in the US Dollar Index price.

- USD/CHF remains pressured at the lowest levels since January 2021 after falling the most in seven weeks.

- Fed announces a dovish rate hike of 0.25%, dumping statement on interest rate lifts gain major attention.

- Bank fallouts, US debt ceiling expiration also weigh on sentiment and Swiss Franc pair.

- Risk catalysts are the key for immediate directions.

USD/CHF holds lower grounds near 0.8830 amid early Thursday, after falling to early 2021 levels on the Federal Reserve’s (Fed) dovish rate hike. The risk-barometer pair also bears the burden of the market’s fears of US default and banking fallouts. With this, the Swiss Franc (CHF) pair prints a three-day downtrend near the multi-month low following the biggest daily slump in nearly seven weeks.

Fed lifted its benchmark rate to the highest levels since 2007 by announcing a 0.25% increase, matching market forecasts. The policymakers including Chairman Jerome Powell appeared positive while ruling out fears of banking rout. However, a dropping of the statement suggesting the need for further rate hikes gained major attention and weighed on the US Dollar despite the hawkish move.

On the other hand, PacWest Bancorp recently became another US bank to witness the heat of excess withdrawal and is on the brink of collapse. That said, Western Alliance Bancorp is also in the line and hence the US banking sector appears in trouble moving forward, which in turn weigh on the market sentiment and prod the hawkish central banks, like it did to the Fed.

Elsewhere, the comments from the White House suggesting debt limit default could cost 8.3 million job losses also weigh n the sentiment and the USD/CHF pair.

Talking about the data, US ADP Employment Change rose to 296K for April from 142K prior versus 148K market forecast. Additionaly, the annual pay growth declined to 13.2% from 14.2%. Further, ISM Services PMI improved to 51.9 in April versus 51.8 market forecasts and 51.2 previous readings. It’s worth noting, however, that the S&P Global Services PMI and Composite PMI for April eased to 53.6 and 53.4 versus 53.7 and 53.5 respective priors.

Amid these plays, Wall Street closed with minor losses and the yields remain pressured while weighing on the US Dollar Index.

Moving on, market players may pay close attention to the risk catalysts for fresh impulse amid a dearth of top-tier data. However, European Central Bank (ECB) Monetary Policy Meeting can entertain traders.

Technical analysis

A clear downside break of a three-week-old descending support line, now immediate resistance near 0.8850, directs USD/CHF bears towards the year 2021 low of around 0.8755.

- Fundamental news, like the US Federal Reserve 25 bps rate hike, spooked Euro buyers; hence the EUR/JPY fell.

- Short term, the EUR/JPY might extend its losses before continuing its uptrend.

The EUR/JPY dropped for the third straight session after hitting a multi-year high of 151.61, collapsing beneath the 149.00 figure on a 100-plus pip fall. A bearish engulfing candle pattern was followed by another bearish candle that dragged prices toward the 148.00 regions. At the time of writing, the EUR/JPY is trading at 148.92, down 0.05%, as the Asian session begins.

Must read: Breaking: Fed hikes policy rate by 25 bps to 5-5.25% as expected

EUR/JPY Price Analysis

Despite the ongoing correction on the pair, the EUR/JPY remains upward biased, which dragged the exchange rate 250 pips lower from its yearly highs. If EUR/JPY sellers would need to extend their gains, the pair must fall and reclaim last year’s high of 148.40, and once cleared, the next support in play would be the 20-day EMA at 147.57. But firstly, the EUR/JPY needs to crack below 148.00.

Conversely, for a bullish continuation, the EUR/JPY must reverse and conquer 149.00. A breach of the latter and the pair could rally towards the 2014 swing high at 149.78 before re-testing the 150.00 figure.

EUR/JPY Daily Chart

- GBP/USD is marching towards 1.2600 as a Fed rate-cycle pause would trim Fed-BoE policy divergence.

- US labor market conditions carry the potential of making inflation persistent.

- S&P500 futures are showing further losses in early Asia, indicating a risk-off mood.

The GBP/USD pair is approaching the round-level resistance of 1.2600 in the early Tokyo session. The Cable is aiming higher as the Federal Reserve (Fed) is following the language of other central banks. Fed chair Jerome Powell has confirmed that further monetary policy decisions will be data-dependent, which indicates that the central bank has reached an intermediate terminal rate for now.

S&P500 futures are showing further losses in early Asia after a bearish settlement. US equities surrendered their entire gains added in the early New York session amid uncertainty over the further path to be followed by the Fed to tame sticky inflation. Negative market sentiment has faded appeal for risk-sensitive assets.

The US Dollar Index (DXY) is declining towards May 03 low around 101.07 amid neutral guidance from the Fed. Also, the US yields are heavily down amid an increase in demand for US government bonds. The 10-year US Treasury yields have dropped to near 3.36%.

Meanwhile, upbeat US labor market conditions are signaling that a hawkish stance from the Fed would not be over soon as labor shortage could propel inflationary pressures. On Wednesday, the US Automatic Data Processing (ADP) agency reported an addition of fresh 296K jobs in April vs. the estimates of 150K and the former release of 145K.

There is no denying the fact that extreme labor shortage would have been offset by offering higher wages, which carries the potential of making inflation persistent.

On the Pound Sterling front, the Bank of England (BoE) is expected to raise interest rates further as United Kingdom inflation is not ready to leave the double-digit territory despite consistent policy tightening. BoE Governor Andrew Bailey is ready to raise interest rates consecutively for the 12th time. An interest rate hike of 25 bps is anticipated by the market participants.

“The New Zealand farming sector faces challenges as interest rates and other costs rise and returns are forecast much lower, with dairy farms the hardest hit,” Reserve Bank of New Zealand (RBNZ) Governor Adrian Orr said on Thursday per Reuters.

RBNZ Governor Orr appeared for a testimony to a parliamentary committee.

The news also spots Senior RBNZ officials noting that debt levels in the sector are down significantly from five years ago when the central bank was highlighting debt as a major vulnerability for the dairy sector.

More comments from Orr

What we observe in the dairy sector in particular, is the structure of the industry - the high leverage nature of the industry - leads to a very high vulnerability to shifts and interest rates up and down.

Cost pressures remain so there's definitely challenges in the sector.

On the same line RBNZ Deputy Governor Christian Hawkesby told the same parliamentary committee, per Reuters, that the central bank was not concerned about New Zealand's growing current account deficit.

"New Zealand government debt is still relatively low compared to other countries, and that puts us in a strong position," Hawkesby said.

Also read: NZD/USD Price Analysis: Pullback moves prod 0.6200 ahead of China Caixin PMI

- NZD/USD takes offers to snap two-day uptrend, reverses from the highest levels in three weeks.

- Weekly support line, one-month-old previous resistance line restrict immediate downside.

- Failure to cross 50% Fibonacci retracement, looming bear cross on MACD favor Kiwi sellers.

NZD/USD takes offers to refresh intraday low near 0.6210 as it reverses the Fed-inspired gains during early Thursday amid a risk-off mood, as well as due to the anxiety ahead of China Caixin Manufacturing PMI for April.

Technically, the Kiwi pair’s inability to cross the 50% Fibonacci retracement of its April 05-26 downside, near 0.6250, joins an impending bear cross on the MACD indicator to lure the sellers.

Adding strength to the bearish bias could be the recent downside break of the 200-SMA, around 0.6215 at the latest.

With this, the Kiwi pair is all set to drop toward the weekly support line of near 0.6200. However, the resistance-turned-support line from early April, near 0.6175 by the press time, could restrict the NZD/USD pair’s further downside.

Should the quote remains weak past 0.6175, the odds of witnessing a fall toward the previous monthly low, also the Year-To-Date (YTD) bottom, near 0.6110 can’t be ruled out.

On the contrary, recovery moves may initially aim for the 200-SMA level of around 0.6215 before challenging the 50% Fibonacci retracement and the recent swing high, respectively near 0.6250 and 0.6260.

Following that, the 61.8% Fibonacci retracement, also known as the golden ratio, of near 0.6280 will precede the 0.6300 round figure and mid-April swing high of 0.6316 to prod the NZD/USD bulls.

To sum up, NZD/USD slips to the bear’s radar but the downside room appears limited.

NZD/USD: Four-hour chart

Trend: Further downside expected

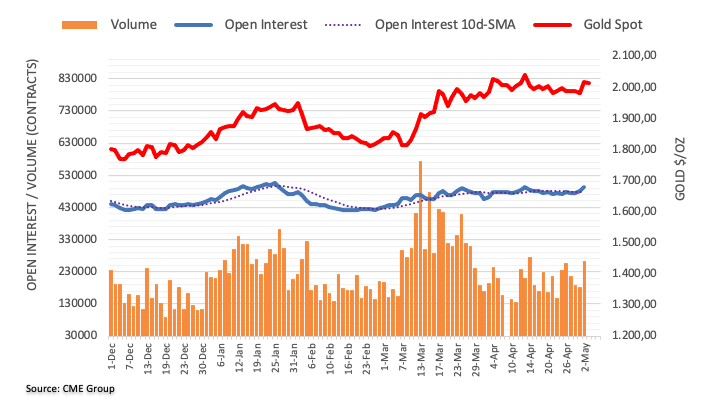

- Gold price has displayed some correction after posting a fresh YTD high at $2,079.76.

- The Fed announced that further monetary policy decisions would be highly dependent on incoming data.

- Investors are worried that US labor market conditions are still tight and could accelerate persistent inflation.

Gold price (XAU/USD) has witnessed a steep fall after printing a fresh year-to-date (YTD) high placed at $2,067.00 in the early Asian session. The yellow metal has attracted significant offers as the US Dollar Index (DXY) has attempted a recovery. Earlier, the precious metal gained immense strength as the Federal Reserve (Fed) signaled a pause in the policy-tightening spell from June after hiking interest rates by 25 basis points (bps) to 5.00-5.25%.

Fed chair Jerome Powell announced that further monetary policy decisions would be highly dependent on incoming data. The Fed is moving from its prior language of ‘some additional policy firmly’ to ‘closely monitoring incoming information’ suggesting that monetary policy is restrictive enough for now to curb sticky inflation.

Meanwhile, S&P500 futures settled Wednesday’s session on a bearish note after surrendering stellar gains amid uncertainty over the further path of arresting sticky inflation, portraying a risk-aversion theme.

The US Dollar Index (DXY) is showing signs of recovery after a steep correction to near 101.26. Investors are worried that the United States labor market conditions are still tight and could accelerate persistent inflation.

On Wednesday, the US Automatic Data Processing (ADP) agency showed an addition of fresh payrolls at 296K vs. the estimates of 150K and the former release of 145K. If incoming information continues to remain expansionary in this way, the Fed won’t have another option than to hike interest rates further.

Gold technical analysis

Gold price has sensed selling pressure after printing a fresh YTD at $2,079.76 as profit-booking kicked in. The precious metal has conquered its prior resistance plotted from 07 August 2020 high at $2,075.22. Intermediate support is placed from April 21 low at $1,969.29.

The 10-period Exponential Moving Average (EMA) at $1,973.73 is providing cushion to the Gold bulls.

Meanwhile, the Relative Strength Index (RSI) (14) is oscillating in the bullish range of 60.00-80.00, indicating a continuation of the upside momentum.

Gold weekly chart

- AUD/USD grinds lower after three-day uptrend, takes offers of late.

- Fed matches 0.25% rate hike expectations but removal of guidance for further rate increase weighs on US Dollar.

- Hawkish surprise from RBA, upbeat Australia Retail Sales help Aussie pair buyers despite firmer US data.

- Australia’s trade numbers for March, China’s Caixin Manufacturing PMI for April eyed for immediate directions.

AUD/USD pauses recent upward trajectory, especially backed by the Fed vs. RBA play, as it takes offers to 0.6660 during early Thursday morning in Asia. The Aussie pair recently benefited from the US Federal Reserve’s (Fed) hesitance in suggesting further rate hikes, despite announced a 25 basis points (bps) of an increase to the benchmark Fed rate. Also favoring the quote could be the Reserve Bank of Australia’s (RBA) hawkish surprise and upbeat Aussie Retail Sales marked previously. However, US banking fallout fears and US debt ceiling expiration woes seem to underpin the latest decline in the AUD/USD prices.

Fresh selling of PacWest Bancorp and Western Alliance Bancorp shares triggered banking fears across the board, which in turn exerts downside pressure on the AUD/USD prices. On the same line could be the comments from the White House suggesting debt limit default could cost 8.3 million job losses. Further, Reuters said that shares of US regional lenders collapsed in extended trade on Wednesday, with PacWest Bancorp losing over half its value after reports the California bank is exploring strategic options, including a sale.

On Wednesday, the US Federal Reserve lifted its benchmark rate to the highest levels since 2007 by announcing a 0.25% increase, matching market forecasts. The policymakers including Chairman Jerome appeared positive while ruling out fears of banking rout. However, a dropping of the guidance signaling further rate hike gained major attention and weighed on the US Dollar despite the hawkish move.

On the other hand, Australia’s seasonally adjusted Retail Sales for March rose 0.4% versus market expectations of witnessing a 0.2% steady growth number. Further, Australia’s AiG Industry Index for March rose to 20.1 versus -6.1 prior whereas the AiG Manufacturing and Construction PMIs for the said month dropped to -20.2 and -12.4 respective levels versus -5.8 and 5.6 priors in that order. Further, S&P Global Services PMI for April improved to 53.7 versus 52.6 initial forecasts while the Composite PMI also rose to 53.0 from 52.2 first estimations for the said month.

Further, the Reserve Bank of Australia (RBA) surprises markets by lifting the Official Cash Rate (OCR) by 25 basis points (bps) to 3.85%. Not only does the RBA announce a 0.25% rate hike but the Aussie central bank also expects further tightening of the monetary policy. That said, the RBA also revised its inflation and Gross Domestic Product (GDP) forecasts in the latest policy document. Additionally, RBA Governor Philip Lowe repeated that some further tightening may be required to bring inflation back to the 2-3% target within a reasonable timeframe.

Technical analysis

Despite a four-day uptrend, AUD/USD repeatedly fails to provide a daily closing beyond the 21-DMA and a three-week-old descending resistance line, respectively near 0.6675 and 0.6685, which in turn teases sellers.

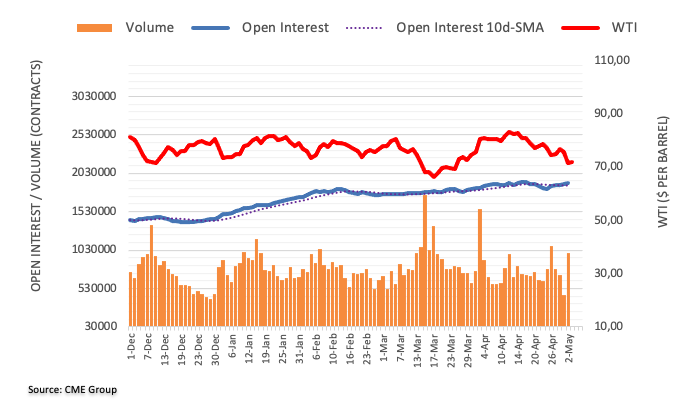

- WTI is pressured and near fresh cycle lows in $68.00.

- US Dollar is lower on the Fed as markets await the ECB.

WTI Crude Oil was heavily down on Wednesday with a drop-kicking in ahead of the Federal Reserve interest rate decision. Crude was posting a 5-week low and has been under pressure on concerns of a global slowdown that would only weigh on energy demand. At the time of writing, Crude prices are trading at $68.08 WTI and have traveled between a high of $71.74 and a low of $68.02bbls.

Among worries in the energy sector, the banking turmoil and the risks of tighter monetary policy from the world's central banks have played their roles. On Wednesday, the Federal Reserve raised interest rates by 25 bp ahead of Thursday´s European Central Bank meeting which is expected to raise rates by +25 bp as well.

Additionally, Crude prices maintained sharp losses following this Wednesday's mixed EIA inventory report. EIA gasoline supplies unexpectedly rose +1.74 million bbl versus expectations of a -1.5 million bbl draw. Also, crude stockpiles at Cushing, the delivery point of WTI futures, rose +541,000 bbl. The EIA report showed that (1) US crude oil inventories as of April 28 were -1.9% below the seasonal 5-year average, (2) gasoline inventories were -6.2% below the seasonal 5-year average, and (3) distillate inventories were -12.5% below the 5-year seasonal average.

Analysts at TD Securities explained that crude oil prices were plummeting in line with the notable deterioration in commodity internals that have soured demand signals. ´´While energy markets have now begun to price in recession risks, prices remain notably more elevated than would be otherwise anticipated in the face of the deteriorating macroeconomic backdrop, given still elevated supply risk premia. ´´

Following the Federal Reserve's decision to raise interest rates to their highest level since 2007, Bloomberg reported that PacWest Bancorp is considering strategic options, including a potential sale.

PacWest's shares are falling by more than 50% in the post-market, indicating significant investor concern about the bank's situation.

After the Fed, the focus now turns to the European Central Bank. During the Asian trading session, New Zealand will report Building Permits, Australia will report Trade Balance figures, and the Chinese Caixin Manufacturing PMI is also due.

Here is what you need to know on Thursday, May 4:

As expected, the Federal Reserve raised interest rates by 25 basis points to 5.00-5.25%, the highest level since 2007. The FOMC also removed forward guidance about further rate hikes but noted that the timing of future rate changes will depend on incoming economic data. The bias still favors further tightening. The currency market saw limited impact.

Analysts at Societe Generale explained:

With the Fed funds target range of 5.00-5.25% the Fed has met its dot-plot guidance from last December and updated as of March. A pause is the next step. A full stop requires confirmation that inflation pressures (rents in particular) subside and employment slows.

Wall Street stocks closed lower and US bond yields declined further, putting pressure on the US Dollar. The US Dollar Index (DXY) closed at its lowest level in a week around 101.35 but remained above recent lows. Meanwhile, the US 10-year yield settled at 3.36%, marking a one-month low.

The US will release data on Q1 Unit Labor Costs and weekly Jobless Claims on Thursday. The ADP Employment report for April showed a surge in private payrolls, rising by 296K and surpassing expectations. However, the market's reaction to the data was muted as investors await Friday's Nonfarm Payrolls report

The focus has now shifted to the upcoming European Central Bank (ECB) meeting, where a 25 basis point rate hike is expected, but a 50 basis point hike is also possible. The outcome of the meeting is likely to trigger reactions in the Euro. The EUR/USD pair approached 1.1100 after the FOMC statement before pulling back to 1.1050. Despite the limited upside, the pair remains bullish.

European Central Bank Preview: Lagarde set to lift the Euro in two out of three scenarios

GBP/USD reached its highest intraday levels since June, approaching 1.2600 before retreating slightly. The bias is to the upside.

USD/JPY extended its slide for the second day in a row, impacted by lower US yields and the decline in equity prices on Wall Street. Over the past two days, it has fallen more than 200 pips, hitting three-day lows at 134.82.

AUD/USD rose for the third consecutive day but failed to hold above 0.6700, indicating that it is not yet ready for a bullish breakout. Nevertheless, it remains far from the recent lows. On Thursday, the Australian trade data and the Caixin China Manufacturing PMI are due.

NZD/USD continued to edge higher, reaching two-week highs at 0.6260. The Kiwi outperformed CAD and AUD following positive labor market data from New Zealand. Market participants expect the Reserve Bank of New Zealand (RBNZ) to raise rates again at the next meeting on May 24. In the Financial Stability Report, the RBNZ stated that the national financial system is well-positioned to deal with rising interest rates and global risks.

Crude oil prices dropped again, falling by more than 4%. WTI posted its lowest close since mid-March near $68.00. Gold continued to rise, holding firm above $2,000; it peaked at $2,036, with the year-to-date high around $2,050 on the radar. Silver also gained but more modestly, rising to $25.50. Cryptocurrencies fell on Wednesday, with BTC/USD down 1% to $28,350

Like this article? Help us with some feedback by answering this survey:

- EUR/USD bulls move back into the peak formation.

- Federal Reserve´s dovish hike weakened the US Dollar.

EUR/USD has been attempting to run higher on Wednesday and reached the 1.1090s and a previous resistance area. The Euro ran higher on the back of what was traded as a dovish 25 basis point hike from the Federal Reserve ahead of tomorrow's European Central Bank meeting.

At the time of writing, EUR/USD is trading at 1.1055 as the US Dollar scrambled back from the edge of the abyss following a balanced press conference from the Federal Reserve´s, Jerome Powell. The following are the key takeaways from the event:

Fed´s statement, key takeaways

- Fed drops language that it anticipates more policy firming may be appropriate to attain a sufficiently restrictive stance.

- Will continue reducing the balance sheet as planned.

- Job gains have been robust and inflation remains elevated.

- Tighter credit conditions are likely to weigh on the economy, hiring, and inflation.

- Fed says the vote in favor of the policy was unanimous.

- Fed repeats us banking system is sound and resilient.

- In determining the extent to which additional policy firming may be appropriate, it will take into account tightening.

The Federal Reserve removed the prior language that signaled more hikes were coming. Instead, the statements say the extent to which more firming is needed hinges on the economy. Consequently, Fed futures are pricing in a pause in June and July and rate cuts in September.

However, Fed´s Chairman Jerome Powell was questioned by the press as to whether rate cuts are on the way, to the contrary, he said it would not be appropriate for us to cut rates when he outlined the conditions of high inflation whereby the Fed would need to stay on its rate hiking course.

´´Rate cuts would be inappropriate given our belief that inflation will take some time to subside,´´ Fed Chairman said.

Consequently, the US Dollar was thrown around as follows:

US Dollar, DXY chart

The eclipsed price action above on the 5min chart was the reaction to Powell´s back peddling when it came to rate cuts. The price to the downside was the market's initial reaction to the prospects of a pivot from the Fed. The line in the sand is around 101.50:

The European Central Bank is the next main highlight for EUR/USD.

´´ It is our view that the ECB will announce three more 25 bps rate hikes in May, June and July,´´ analysts at Rabobank said.

´´While the USD has failed to gain a safe-haven bid this week on concerns about US regional banks. Fresh stresses elsewhere could yet promote a move back to USDs. We see risk of a move back to the EUR/USD 1.06 in H2 this year,´´ the analysts concluded.

EUR/USD technical analysis

The EUR/USD 4-hour chart is pretty messy with the price breaking structures on the downside and coming right back into the peak formations again. With that being said, a break above 1.1100 will be bullish while a break below 1.1020 would be bearish.

- Fed Chair Powell Signals Monetary Policy Meeting by Meeting, Raises Rates by 25bps.

- US Central Bank Ready to Take Action, Including Raising Rates, Says Fed Chair.

- USD/MXN Price Analysis: Likely to break to new multi-year lows below 18.00.

The USD/MXN plummets to fresh six-year lows, last seen in September 2017, after the US Federal Reserve (Fed) raised rates by 25 bps, though it opened the door for pausing. The USD/MXN is trading at 17.8865, down 0.50% at the time of typing.

The US Federal Reserve Chair Powell took the stance after he and his colleagues decided to raise rates by 25 bps and signaled that the US central bank would determine its monetary policy, meeting by meeting. Jerome Powell added that inflation is too high and the labor market is tight.

When asked about rate cuts, he said it “would not be appropriate to cut rates, given our view that inflation will take some time to come down.” Powell added that the US central bank is “prepared to do more,” including rising rates if needed, and that officials did not decide to pause at the upcoming June meeting.

On Wednesday, the US central bank hiked rates by 25 bps to the 5.00% - 5.25% area but tweaked its language regarding additional rate hikes. The Fed shifted to being data-dependent and will asses future decisions based on information about the economy, inflation, and the overall financial markets behavior.

Policymakers added that ongoing tightening of credit conditions could help the Fed to get inflation to its 2% target. Although today’s Fed decision was perceived as dovish, officials reiterated that inflation is elevated and the labor market robust. Regarding the balance sheet reduction, the FOMC decided to continue as planned.

USD/MXN Technical Analysis

As Fed Chair Powell spoke in his press conference, the USD/MXN reached a multi-year low at around 17.8283. Nevertheless, the USD/MXN buyers lifted the exchange rates to the current level. If USD/MXN buyers want to shift the bias to neutral, they must reclaim the 20-day EMA at 18.0566, followed by the 50-day EMA at 18.2511. A breach of the latter will expose the 100-day EMA at 18.5732.

- USD/CAD is mixed during the Fed event on Wednesday.

- USD/CAD is trapped in a box 1.3600 is key.

- A break below 1.3580 tips the bias in favor of the bears.

USD/CAD is down on the day by some 0.2% as the US Dollar plummets on the back of what has been perceived to be a dovish outcome of the Federal Reserve meeting on Wednesday. A dovish hike is being priced into the markets following the Federal Reserve´s rate hike of 25 basis points and accompanying announcements within its statement.

The US Dollar has dropped as the central bank removed the prior language that signaled more hikes were coming. Instead, the statements say the extent to which more firming is needed hinges on the economy. Subsequently, Fed futures are pricing in a pause in June and July and rate cuts in September.

Currently, Federal Reserve´s Chairman, Jerome Powell is being quizzed by the press that are scrutinizing the language in the statement.

Feds statement, key takeaways

- Fed drops language that it anticipates more policy firming may be appropriate to attain a sufficiently restrictive stance.

- Will continue reducing the balance sheet as planned.

- Job gains have been robust and inflation remains elevated.

- Tighter credit conditions are likely to weigh on the economy, hiring, and inflation.

- Fed says the vote in favor of the policy was unanimous.

- Fed repeats us banking system is sound and resilient.

- In determining the extent to which additional policy firming may be appropriate, it will take into account tightening.

´The press are asking whether rate cuts are on the way and Fed´s Powell has dodged to comment anything in concrete. To the contrary, ´´it would not be appropriate for us to cut rates,´´ when he outlined the conditions of high inflation whereby the Fed would need to stay on its rate hiking course. ´´Rate cuts would be inappropriate given our belief that inflation will take some time to subside,´´ Fed Chairman said. Consequently, the US Dollar is finding some support:

DXY chart

USD/CAD technical analysis

The price is trapped in a box 1.3600 is key. If 1.3600 can hold, then the bulls will be in play still. A break below 1.3580 tips the bias in favor of the bears.

FOMC Chairman Jerome Powell comments on the policy outlook after the Federal Reserve's decision to raise the policy rate by 25 basis points to the range of 5-5.25% following the May policy meeting.

Key quotes

"Support for rate hike today was very strong."

"There were a number of policymakers at today's meeting talking about pausing, but not so much at this meeting."

"There is a sense we are much closer to the end than the beginning."

"We feel like we are close, or maybe even there."

"We can afford to look at the data and make a careful assessment."

"Speed of SVB run needs to be reflected in supervision, regulation."

"It's clear we need to strengthen supervision, regulation for large banks."

- NZD/USD stays above 0.6220s in a volatile session as Fed Chair Powell speaks.

- The removal of hawkish language in the monetary policy statement signals a possible Fed pivot.

- Fed Powell: If the US gets tip into a recession, I “hope it would be mild.”

The NZD/USD advances sharply, eyeing the 200-day SMA at 0.6255, after the US Federal Reserve (Fed) decided to raise rates by 25 bps, though it opened the door for a “possible” pause. As Fed Chair Jerome Powell speaks, the NZD/USD is trading volatile within the 0.6220-60 area at the time of writing.

The Fed would be data-dependent at upcoming meetings, including a possible pause

In his press conference, Federal Reserve Chair Jerome Powell said the Fed would take a data-dependent approach, and there are some signs that supply and demand in the labor market are returning to balance. He added that inflation pressures continued to run high, and if the US hits a recession, it would be mild.

Powell added that the US central bank is prepared to do more if warranted and emphasized the Fed’s goal to restore price stability while adding that rates would remain higher “for a while.”

On Wednesday, the Fed Chair Powell and Co. voted to raise rates to the 5.00% - 5.25% area, though tweaked its language regarding additional rate hikes. The Fed shifted to being data-dependent and will asses future decisions based on information about the economy, inflation, and the overall financial markets behavior.

Federal Reserve officials added that ongoing tightening of credit conditions could aid the US central bank to achieve its 2% inflation goal. Despite removing some hawkish language from the monetary policy statement, policymakers reiterated that inflation is high and that the labor market is tight. Therefore, June’s meeting would likely be live, even though the futures markets had begun to price in the first rate cut in September. Concerning the balance sheet reduction, the Quantitative Tightening (QT) would continue as planned.

NZD/USD Technical Levels

FOMC Chairman Jerome Powell comments on the policy outlook after the Federal Reserve's decision to raise the policy rate by 25 basis points to the range of 5-5.25% following the May policy meeting.

Key quotes

"There are no promises, but it's possible we can continue to have labor market cooling without big increases in unemployment."

"Case of avoiding recession is more likely than having a recession."

"If we have recession, would hope it would be mild."

"Do not think wages are principle driver of inflation."

"As goods pipelines get back to normal, will see prices, corporate margins coming down."

"A particular focus now and going forward is what's happening with credit tightening."

"Need to factor credit tightening into whether our policy stance is sufficiently restrictive."

"Would not be appropriate to cut rates, given our view that inflation will take some time to come down

"Non-housing services inflation hasn't moved much."

FOMC Chairman Jerome Powell comments on the policy outlook after the Federal Reserve's decision to raise the policy rate by 25 basis points to the range of 5-5.25% following the May policy meeting.

Key quotes

"We are trying to reach and then stay at for an extended period a sufficiently restrictive stance to bring down inflation."

"We have to balance risk of not doing enough against risk of slowing economic activity too much."

"Felt that this rate hike and change in statement was the right way to balance that."

"Will be an ongoing process to assess appropriate level of rates."

"Policy is tight."

"Real rates are around 2%, meaningfully above neutral rate."

"We might possibly be at sufficiently restrictive level, may not be far off."

"We have a goal of getting to 2%, will take some time and will not be a smooth process."

"We think we will need to stay on this for a while."

"Wages still above level consistent with 2% inflation over time."

"Labor market is very very strong, inflation is running high and well above goal."

"Right now we need to focus on bringing inflation down."

FOMC Chairman Jerome Powell comments on the policy outlook after the Federal Reserve's decision to raise the policy rate by 25 basis points to the range of 5-5.25% following the May policy meeting.

Key quotes

"Don't have an agenda for further bank consolidation."

"Bank consolidation has been going on for a while."

"Have long felt that having small, medium and large banks is a great part of our banking system."

"Hard to predict how much credit tightening will replace need for any further rate hikes."

"Assessing the extent to which firmer policy will be needed will be ongoing, and meeting by meeting."

"Credit tightening complicates that assessment, adds uncertainty."

"Will be an ongoing assessment whether Fed has reached sufficiently restrictive."

"Not possible to say with confidence if we have reached sufficiently restrictive level."

"Will revisit that at June meeting."

"Before declaring we've reached sufficiently restrictive stands will need more data."

FOMC Chairman Jerome Powell comments on the policy outlook after the Federal Reserve's decision to raise the policy rate by 25 basis points to the range of 5-5.25% following the May policy meeting.

Key quotes

"No one should assume the Fed can protect the economy from a failure to pay bills on time."

"Debt ceiling did come up in discussions."

"Talked about debt limit issue as a risk to the outlook."

"Debt limit issue was not important in today's monetary policy decision."

"Was raised by some as a risk but not critical to today's decision."

"The feFebruary 14 presentation was a general presentation on interest rate risks."

"There was one page on Silicon Valley Bank."

"Nothing in the February 14 briefing about the risk of a bank run."

"Staff was going to do a horizontal assessment of banks, not presented as urgent or alarming."

"Many banks are now attending to liquidity."

"Financial stability tools and monetary policy tools are working well together."

- US Dollar bears are lurking below 101.50 while Fed Powell talks.

- Fed's Powell´s comments will be scrutinized for a possible hawkish tone to flip the script.

The US Dollar is volatile in the session surrounding the Federal Reserve. DXY, which is an index that measures the Greenback vs.. a basket of major currencies, was initially sold off but has since recovered the losses and is heading a touch higher.

The Federal Reserve rate hike of 25 basis points and accompanying announcements within its statement. The central bank removed the prior language that signaled more hikes were coming. Instead, the statements say the extent to which more firming is needed hinges on the economy. Consequently, Fed futures are pricing in a pause in June and July and rate cuts in September.

Feds statement, key takeaways

- Fed drops language that it anticipates more policy firming may be appropriate to attain a sufficiently restrictive stance.

- Will continue reducing the balance sheet as planned.

- Job gains have been robust and inflation remains elevated.

- Tighter credit conditions are likely to weigh on the economy, hiring, and inflation.

- Fed says the vote in favor of the policy was unanimous.

- Fed repeats us banking system is sound and resilient.

- In determining the extent to which additional policy firming may be appropriate, it will take into account tightening.

All in all, the Fed has opened the door to a rate-hike pause, and Gold price is reacting in kind.

Markets will now await the Chairman, Jerome Powell who will be speaking in the press conference.

Watch live: Fed Chair Jerome Powell

US Dollar technical analysis

The price is bearish while below 101.50.

- GBP/USD stays positive following the Federal Reserve’s “dovish” interest rate hike.

- Federal Reserve officials voted unanimously for a 25 bps rate hike.

- Policymakers dropped some hawkish language, perceived as a signal that the Fed could pause.

The GBP/USD rallied sharply to a fresh YTD high at 1.2589 on the back of a 25 bps interest rate increase by the Federal Reserve (Fed), which dropped “hawkish” language, adopting a more neutral stance. At the time of writing, the GBP/USD remains volatile, trading at around 1.2560-1.2590, with gains close to 0.80%.

Review of the Fed’s May meeting monetary policy statement

To highlight, Federal Reserve officials voted unanimously for a quarter of a percent increase to the Federal Funds Rate (FFR). They switched the language from “anticipating that some additional policy firm may be appropriate…” to “determining the extent to which additional policy firming may be appropriate,” policymakers would assess their decisions based on the economy, inflation, and the financial markets behavior.

Powell and Co. added that tightening credit conditions would help the Fed to achieve its goal. They emphasized the resilience and soundness of the banking system and added that inflation remains high and the labor market tight. Concerning the QT, the balance sheet reduction would continue as planned.

After the Federal Reserve’s decision, US rate futures show traders are pricing in rate cuts in September, according to Reuters.

GBP/USD’s pair reaction to the headline

The GBP/USD climbed sharply but has retraced some gains as the Federal Reserve Chai Jerome Powell’s press conference begins. The 1-hour chart portrays the GBP/USD as forming a gravestone doji, which could suggest further downside estimates. Nevertheless, GBP/USD traders better buckled up; as volatility increases, it could trigger some action.

GBP/USD key resistance levels lie at 1.2550, 1.2589, and 1.2600. On the flip side, the GBP/USD would find support at 1.2510, the 20-hour SMA, followed by the 1.25 figure, ahead of dropping towards the 50-hour SMA at 1.2492.

GBP/USD Technical Levels

FOMC Chairman Jerome Powell comments on the policy outlook after the Federal Reserve's decision to raise the policy rate by 25 basis points to the range of 5-5.25% following the May policy meeting.

Key quotes

"A decision on a pause was not made today."

"Statement change was meaningful."

"It is a meaningful change to no longer say we anticipate more firming of policy."

"Staff forecast is independent of Fed policymakers."

"Broadly the staff forecast was for a mild recession."

"Staff forecast for this meeting was broadly similar to march forecast."

"Debt limit is a fiscal policy matter for elected officials to deal with."

"It is essential for debt limit to raised in timely way."

"Consequences of a default would be quite adverse."

FOMC Chairman Jerome Powell comments on the policy outlook after the Federal Reserve's decision to raise the policy rate by 25 basis points to the range of 5-5.25% following the May policy meeting.

Key quotes

"Highly attentive to risks of inflation to both sides of mandate."

"We are seeing the effects of policy tightening, particularly in housing and investment."

"Will take time for full effects of monetary restraint to be realize."

"Economy is likely to face headwinds from credit conditions."

"Strains from banking sector resulting in tighter conditions."

"Extent of effects is uncertain."

"Strains from banking system in March is resulting in even tighter conditions."

"Our future policy actions will depend on how events unfold."

"We will make rate determination meeting by meeting."

"We are prepared to do more if more is warranted."

"Reducing inflation likely to require period of below trend growth, softer labor market."

"Restoring price stability is essential."

FOMC Chairman Jerome Powell comments on the policy outlook after the Federal Reserve's decision to raise the policy rate by 25 basis points to the range of 5-5.25% following the May policy meeting.

Key quotes

"Conditions in banking sector have broadly improved."

"US banking system is sound and resilient."

"Committed to learning right lessons."

"Focus remains on dual mandate."

"Strongly committed to bringing inflation back down to 2%."

"Without price stability will not achieve sustained strong labor market."

"We will take a data-dependent approach from here."

"Activity in housing sector remains weak."

"Labor market remains very tight."

"Some signs that supply and demand in labor market coming back into better balance."

"Nominal wage growth has shown signs of easing."

"Inflation has moderated somewhat."

Inflation pressures continue to run high."

"Have a long way to go to bring down inflation."

- Federal Reserve raises rates and signals potential pause.

- US Dollar weakens after FOMC statement.

- AUD/USD testing 0.6700 amid volatility.

The AUD/USD jumped to 0.6702 after the Federal Reserve’s decision due to broad-based dollar weakness. It then pulled back modestly, trimming some gains. The pair still holds a bullish tone ahead of Chair Powell's press conference.

Fed raises, probably for the last time in a while

The Fed raised rates to 5.00% - 5.25%, the highest level since 2007, as expected. In the statement, the central bank signaled a potential pause. Chair Powell will offer a press conference and answer questions. He is unlikely to declare 'mission accomplished' and will probably highlight that what happens next is 'data-dependent'.

The US Dollar Index (DXY) dropped to 101.07 before returning to 101.35. It is still down for the day but off its lows. US yields printed fresh lows after the decision but then bounced, and are now slightly above the level they were at before the statement. US stocks hit new daily highs but then pulled back to prior levels.

The AUD/USD pair jumped to 0.6702, hitting a fresh daily high before pulling back under 0.6700. It still holds bullish momentum amid elevated volatility. Above 0.6705, the next resistance is seen at Tuesday's high of 0.6717, followed by 0.6745/50. On the flip side, 0.6675 is the immediate support, followed by 0.6650.

Technical levels

- Gold Price rallies and drops back on the Federal Reserve rate hike and statement.

- Markets now await Fed´s Jerome Powell for clarity and direction.

The Gold price jumped to a high of $2,036.15 and counting on the back of the initial reaction to the Federal Reserve rate hike of 25 basis points and accompanying announcements within its statement.

The US Dollar has dumped and is down some 0.8% at the time of writing as the central bank removes the prior language that signaled more hikes were coming. Instead, the statements say the extent to which more firming is needed hinges on the economy. Consequently, Fed futures are pricing in a pause in June and July and rate cuts in September.

Feds statement, key takeaways

- Fed drops language that it anticipates more policy firming may be appropriate to attain a sufficiently restrictive stance.

- Will continue reducing the balance sheet as planned.

- Job gains have been robust and inflation remains elevated.

- Tighter credit conditions are likely to weigh on the economy, hiring, and inflation.

- Fed says the vote in favor of the policy was unanimous.

- Fed repeats us banking system is sound and resilient.

- In determining the extent to which additional policy firming may be appropriate, it will take into account tightening.

All in all, the Fed has opened the door to a rate-hike pause, and Gold price is reacting in kind.

Markets will now await the Chairman, Jerome Powell who will be speaking in the press conference.

Watch live: Fed chair Jerome Powell

Gold technical analysis

The bulls are in the market but the volatility is rife and there are prospects of a move lower into the in-the-money longs from the start of the US session if the bears can get below $2,021 on hawkish rhetoric from Jerome Powell:

- USD/JPY fell to a new daily low of 134.83 after the Fed’s dovish hike.

- Federal Reserve officials voted unanimously for a 25 bps rate hike.

- Policymakers dropped some hawkish language, perceived as a signal that the Fed could pause.

The USD/JPY extended its losses past the prior’s day low of 135.07, collapsing down the 135 figure, as the US Federal Reserve (Fed) decided to raise rates by 25 bps, though it signaled that it would pause its cycle. At the time of writing, the USD/JPY is trading volatile at around the 134.80-135.40 area.

Summary of the Fed’s monetary policy statement

Federal Reserve officials voted unanimously to raise rates by 25 bps, as shown by its monetary policy statement. Policymakers dropped the “some additional policy firming may be appropriate in order to attain a stance of monetary policy that is sufficiently restrictive to return inflation to 2% over time” language and instead mentioned that “in determining the extent to which additional policy firming may be appropriate,” policymakers would study incoming data.

Fed officials said that tightened credit conditions would likely weigh on the economy and reiterate the soundness of the banking system. Furthermore, policymakers emphasized that the labor market remains robust, and inflation is elevated. Regarding the balance sheet reduction, it will continue as planned since May 2022.

After the Federal Reserve’s decision, US rate futures show traders are pricing in rate cuts in September, according to Reuters.

USD/JPY Market’s Reaction

-638187345625496687.png)

The USD/JPY 1-hour chart portrays that the pair fell below its prior low of 135.07 and printed a new one at 134.83. From there, the USD/JPY pair bounced off, with USD/JPY buyers eyeing a test of the 20-hour SMA at 135.72. But firstly, the buyers must conquer 135.50.

USD/JPY Technical Levels

- Federal Reserve raises rates as expected by 25bps to 5.00%-5.25%.

- US Dollar tumbles across the board, US yields hits fresh lows.

- EUR/USD soars above 1.1050, tests multi-month highs.

The EUR/USD pair jumped from 1.1045 to 1.1091, reaching a one-week high after the Federal Reserve announced, as expected, a 25 basis points rate hike, and suggested a potential pause.

Fed delivers as expected

The US central bank raised rates with a dovish twist, which weighed on the US Dollar. As a result, the DXY dropped to 101.08, hitting a fresh weekly low, while at the same time, US 2-year yields fell below 3.90%. At 18:30 GMT, Chair Powell will deliver a press conference.

The EUR/USD pair rose towards the key area of 1.1100 and then pulled back modestly, holding above the 1.1050 area with a bullish impulse. A break above 1.1100 could trigger an acceleration and open the doors to the highest level since March 2022.

On the contrary, a retreat below 1.1050 should keep the pair in the recent range. Below the key support, the next level of support is seen at 1.0950, with a slide below exposing 1.0900/10.

Technical levels

March 22May 03, 2023

Recent indicators point to Economic activity expanded at a modest growthpace in spending and production.the first quarter. Job gains have picked upbeen robust in recent months and are running at a robust pace;, and the unemployment rate has remained low. Inflation remains elevated.

The U.S. banking system is sound and resilient. Recent developments are likely to result in tighterTighter credit conditions for households and businesses andare likely to weigh on economic activity, hiring, and inflation. The extent of these effects isremains uncertain. The Committee remains highly attentive to inflation risks.

The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. In support of these goals, the Committee decided to raise the target range for the federal funds rate to 4-3/45 to 5-1/4 percent. The Committee will closely monitor incoming information and assess the implications for monetary policy. The Committee anticipates that someIn determining the extent to which additional policy firming may be appropriate in order to attain a stance of monetary policy that is sufficiently restrictive to return inflation to 2 percent over time. In determining the extent of future increases in the target range, the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments. In addition, the Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage-backed securities, as described in its previously announced plans. The Committee is strongly committed to returning inflation to its 2 percent objective.

In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook. The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee's goals. The Committee's assessments will take into account a wide range of information, including readings on labor market conditions, inflation pressures and inflation expectations, and financial and international developments.

Voting for the monetary policy action were Jerome H. Powell, Chair; John C. Williams, Vice Chair; Michael S. Barr; Michelle W. Bowman; Lisa D. Cook; Austan D. Goolsbee; Patrick Harker; Philip N. Jefferson; Neel Kashkari; Lorie K. Logan; and Christopher J. Waller.

.

The US Federal Reserve (Fed) announced on Wednesday that it raised the policy rate, federal funds rate, by 25 basis points to the range of 5-5.25% following the May policy meeting. This decision came in line with the market expectation.

In its policy statement, the Fed dropped language that it 'anticipates' more policy firming may be appropriate to attain 'sufficiently restrictive' stance.

Follow our live coverage of the Fed's policy announcements and the market reaction.

Market reaction

With the initial reaction, the US Dollar came under renewed bearish pressure and the US Dollar Index declined toward 101.00.

Key takeaways from the policy statement

"In determining the extent to which additional policy firming may be appropriate, will take into account tightening to date, policy lags and other developments."

"US banking system is sound and resilient."

"Tighter credit conditions likely to weigh on economy, hiring and inflation."

"Job gains have been robust, inflation remains elevated."

"Will continue reducing balance sheet as planned."

"Vote in favor of policy was unanimous."

- Gold recovered its bright after a drop toward its weekly low at $2007.79.

- ADP Employment Change report surprises with huge hiring increase, though failed to underpin the US Dollar.

- ISM’s Non-Manufacturing PMI for April shows hiring moderation and lower input prices.

Gold price advances to two-week highs as the Federal Reserve Open Market Committee (FOMC) decision looms. Estimates are that the Federal Reserve will hike rates by 25 bps, though uncertainty around the Fed Chair Jerome Powell’s press conference keeps investors uneasy. The XAU/USD is trading at $2026.76.

Gold is steady around $2020, ahead of Fed’s decision and Powell’s press conference

Sentiment remains upbeat as Wall Street post gains, ahead of the FOMC’s decision. The latest round of data from the United States was positive, though it gave the Fed the green light to continue tightening monetary conditions.

Firstly, the April ADP Employment Change report showed that private hiring rose by 296K, crushing estimates of 148K, though it did little to weigh on the Gold price, which continues to trend higher. However, on the data release, it dipped toward 2007, though it offered buyers a better entry price to lift prices to fresh two-week highs.

Later, the ISM revealed April’s Non-Manufacturing PMI, which came at 51.9 above the prior’s month data. The report highlights that hiring continued though it moderated, while the price subcomponent remained nearby the lowest levels since 2020.

Ahead of the FOMC’s decision, traders seemed convinced of the Fed’s 25 bps rate hike, as the CME FedWatch Tool shows an 88.2% chance.

Furthermore, the fall of US Treasury bond yields has been another reason for the XAU/USD’s gains throughout the session. The US 10-year Treasury bond yield is dropping 5 bps, yielding 3.386%.

Most analysts speculate that today’s decision could be the latest hike of the current tightening cycle of the Federal Reserve. It should be said that May’s decision would not update Fed officials’ projections regarding the economy’s general health. The June meeting will unveil the Summary of Economic Projections (SEP).

XAU/USD Technical Levels

- GBP/USD bulls are in the market ahead of the Fed.

- Bulls are above support in the right-hand shoulder.

It´s Federal Reserve day and that spells volatility and technicals tend to be hard to go by as navigating the fundamentals does not stick to what is seen on the charts. Nevertheless, GBP/USD is above water and there is a bullish bias as the following illustrates:

GBP/USD daily charts

As illustrated, GBP/USD is trading above support and within the right-hand shoulder of the inverse head and shoulders.

GBP/USD M15 chart

On the lower timeframes, the bulls will be in the clear while above the1.2540s with a first target in the 1.2570s.

- EUR/USD stays firm at around 1.1050 ahead of the FOMC’s decision.

- The US ADP Employment report for April almost doubled the forecasts, as private hiring increased to almost 300K.

- The US Federal Reserve is expected to raise rates b 25 bps, though Powell’s message is still uncertain.

The EUR/USD extends its gains after hitting a weekly low of 1.0942 on Tuesday, as traders brace for the Federal Reserve (Fed) and the European Central Bank (ECB) monetary policy decisions today and on May 4. At the time of writing, the EUR/USD is trading around 1.1050, above its opening price by 0.44%.

EUR/USD is steady as US ADP Employment report surpasses expectations ahead of uncertain Fed decision

A risk-on impulse took over, despite renewing banking concerns in the United States (US). Wall Street is trading with gains, though lower US Treasury bond yields undermined the US Dollar (USD), hence the EUR/USD advanced.

Therefore, the US Dollar Index (DXY), a measure of the buck’s value against six currencies, drops 0.54%, down to 101.41.

The latest data in the US economic agenda revealed that private hiring increased above estimates, but wages eased. April’s ADP Employment Change report showed that the economy added 296K jobs, exceeding forecasts of 148K. That triggered a reaction in the pair, as the EUR/USD dived to the 1.1020s region before bouncing and climbing to its daily high at 1.1060.

Of late, the ISM revealed the Non-Manufacturing PMI for April, also known as the Services, which rode by 51.9 above March’s 51.2. digging into the data, the price subcomponent held close to its lowest levels since 2020, while the employment index showed moderation.

Across the pond, the Eurozone (EU) docket featured the Unemployment Rate for March, which dipped to 6.5%, beneath the estimates and the prior’s month reading of 6.6%.

In the meantime, the EUR/USD traders prepare for the Federal Reserve decision. Odds for a 25 bps hike lie at 86.8%, as shown by the swaps markets. Notably, according to the futures market, this is the last increase expected by investors, as they are already pricing in 75 bps of rate cuts by year’s end.

On the Europan Central Bank front, estimates are lingering between a 50 or 25 bps increase. Although a 25 bps rate hike is already priced in, going twice is likely possible after the latest EU inflation data report. That has been the reason that underpinned the EUR/USD pair during the last couple of months.

EUR/USD Technical Levels

- Jerome Powell will answer questions from the press after the Fed Interest Rate Decision.

- Any hints on the future monetary policy can trigger significant market moves on US Dollar and other asset classes.

Jerome Powell, Chairman of the Federal Reserve System (Fed), will speak in a press conference on Wednesday at 18:30 GMT, 30 minutes after the Fed Interest Rate decision is announced. Powell’s speech will reflect the current views of the Federal Open Market Committee (FOMC) on monetary policy.

The Federal Reserve is widely expected to deliver a 25 basis points interest rate hike, setting the Fed funds rate in the 5%-5.25% range. Powell’s press conference will provide hints on whether this might be the last interest rate hike of this cycle, or if rather the monetary policy tightening might continue in the coming months.

Jerome Powell will face tough questions by the press on whether the Federal Reserve can keep going with its interest rate hikes, considering the financial stress that the banking system has suffered recently, with First Republic Bank having been taken over by JP Morgan in the past week. Powell’s words will carry enormous importance for the market, with the US Dollar and the US Treasury bonds being the most-affected assets, and in turn, triggering volatility in most asset classes.

According to Yohay Elam, Senior Analyst at FXStreet, Jerome Powell will keep the door open to both tightening and easing policy scenarios, exerting caution. Elam expects Powell’s press conference to support the US Dollar, weighing down on Gold price and the stock markets:

Uncertainty means keeping all options on the table. Fed Chair Powell is set to reject any notion that the bank is done hiking in his press conference. He will go beyond token remarks of "doing what is needed" and firmly place another 25 bps hikes on the table.

In response to such remarks – and sticking to the bank's projections of refraining from cuts until year-end, markets may reverse course. Stocks and Gold would stumble, while the US Dollar would advance on such developments.

About Jerome Powell

Jerome H. Powell first took office as Chair of the Board of Governors of the Federal Reserve System on February 5, 2018, for a four-year term. He was reappointed to the office and sworn in for a second four-year term on May 23, 2022. Powell also serves as Chairman of the Federal Open Market Committee, the System's principal monetary policymaking body.

Powell has served as a member of the Board of Governors since taking office on May 25, 2012, to fill an unexpired term. He was reappointed to the Board and sworn in on June 16, 2014, for a term ending January 31, 2028.

- US private hiring surged above estimates; the USD/JPY seesawed but later slipped.

- ISM Non-Manufacturing PMI climbs in April, despite hiring moderation.

- Traders focus on the US Federal Reserve decision and Powell’s press conference.

The USD/JPY tumbled for the second day in a row, influenced by the fall in the US 10-year Treasury bond yield amidst a mixed market sentiment spurred by the Federal Reserve’s (Fed) monetary policy decision looming. Therefore, US Treasury bond yields are falling, particularly the 10-year, which correlates closely to the USD/JPY pair. At the time of writing, the USD/JPY is trading at 135.14, losing 1.03%.

USD/JPY pressured on falling US bond yields, risk-off mood

US equities are fluctuating ahead of the Fed’s decision. The US ADP Employment Change report, which reveals how private hiring is going in the country, jumped surprisingly by 296K exceeding estimates of 148K and March’s data of 142K. In addition, data showed that albeit hiring rose, wages cooled down from 14.2% to 13.2%, according to the ADP Research Institute report.

After the report, the USD/JPY edged towards 136.00 before making a U-Turn and plunged 60 pips, towards the 135.40 area, before extending its losses.

Of late, the US ISM Non-Manufacturing PMI in April climbed to 51.9 from 51.2 in March, as shown by data. The report showed that a measure of prices paid held close to its lowest level while hiring moderated.

Due to its Golden Week holidays, an absent Japanese economic agenda keeps investors leaning toward US Dollar (USD) dynamics and market sentiment.

The Federal Reserve would unveil its decision ahead of the session, followed by Chair Powell’s press conference, which USD/JPY traders widely expect.

USD/JPY Technical Analysis

The USD/JPY daily chart portrays the pair as neutral to downward biased after failing to crack the March 8 high of 137.91, exacerbating a fall below the 200-day SMA at 137.43. In addition, a dark-cloud cover candlestick chart pattern, formed during the last two previous days from today, opened the door for the 1% plus drop, with sellers testing previous the April 19 swing high at 135.14; previous resistance turned support. A breach of the latter will expose 135.00, followed by the 20-day SMA at 134.17. Conversely, if USD/JPY buyers hold the spot above April 19 high, the pair could rally to the 136.00 figure.

Economists at Rabobank see risk of a move lower in EUR/USD in the latter half of this year.

USD likely to find support if the market prices out 2023 rate cuts

“In the months ahead, the EUR is likely to be adjusting to a softening Eurozone economy. This implies that the upside momentum in EUR/USD that has persisted since Q4 last year, may be nearing a peak.”

“If inflation remains sticky, it follows that Fed policy will have to work harder than in previous cycles to push inflation back to the 2% target. The USD is likely to find support if the market prices out 2023 rate cuts.”

“We see risk of a move back to the EUR/USD 1.06 in H2 this year.”

Gold price has once again managed to exceed the $2,000 mark ahead of the US Federal Reserve interest rate decision. Economists at Commerzbank analyze how the policy announcement could impact the yellow metal.

Today’s rate hike will not turn out to be the last

“In view of the recent fall in inflation and initial signs of weakness on the US labour market, many market participants now expect the Fed to signal a pause in rate hikes. According to our experts, such hopes could prove premature.”

“We are confident that today’s rate hike will not turn out to be the last. This, in turn, is likely to undermine any expectations of a rapid interest rate turnaround – the market envisages the first rate cuts in the second half year. All of this points to an upward correction of interest rate expectations and thus to a weaker Gold price. That said, it is by no means certain that the Fed will be able to convince the market of its hawkish stance.”

“It is equally conceivable that the market will regard any further rate hikes as a mistake that could exacerbate a potential recession in the US and force the Fed to implement an even more pronounced interest rate U-turn at a later date. This could then offset any negative impact of the rate hikes on the Gold price.”

USD/CAD’s bull trend is yet to be nullified, econmists at Rabobank report.

USD/CAD to fluctuate in the 1.34-1.36 range over the coming months

“The main driver of FX markets remains carry and risk sentiment, both of which are likely to drive some upside for USD/CAD. On the flip side, higher energy prices in the second half of the year should provide some support for CAD.”

“We expect the former drivers to dominate upside from oil prices but the pair is unlikely to break out of the 1.3280 to 1.3880 range this year and we see the primarily fluctuating in the 1.34-1.36 range over the coming months, with the risk skewed to an upside break.”

“The long term bull trend won’t be nullified until we see a confirmed close below 1.3260 and we see little chance of that happening this year.”

GBP/USD is consolidating in the low 1.25 area. Economists at Scotiabank expect the pair to enjoy further gains.

Short-term price patterns are mildly bullish

“The fact that Cable is trading on a 1.25 handle remains a broader positive for the Pound, given it has struggled mightily to extend gains through the mid-1.24 area this year.”

“Short-term price patterns are mildly bullish, given the steady uptrend in spot since the mid-Apr test and rejection of key support at 1.2350/60.”

“Friday’s drop from the intraday high is a setback from a technical point of view but trend momentum remains bullish and losses should remain limited.”

“New cycle highs would be bullish and reaffirm potential for gains to extend to 1.27/1.28.”

- US ISM Services PMI improved modestly in April.

- US Dollar Index stays deep in negative territory near 101.50.

The business activity in the US service sector continued to expand at a modest pace in April with the ISM Services PMI edging higher to 51.9 from 51.2 in March. This reading came in slightly better than the market expectation of 51.8.

Further details of the publication revealed that the Prices Paid Index ticked up to 59.6 from 59.5 and the Employment Index declined to 50.8 from 51.3.

Assessing the survey's findings, “there has been a slight uptick in the rate of growth for the services sector, due mostly to the increase in new orders and ongoing improvements in both capacity and supply logistics," noted Anthony Nieves, Chair of the Institute for Supply Management (ISM) Services Business Survey Committee. "The majority of respondents are mostly positive about business conditions; however, some respondents are wary of potential headwinds associated with inflation and an economic slowdown.”

Market reaction

The US Dollar stays under selling pressure after this report and the US Dollar Index was last seen losing 0.45% on the day at 101.50.

Economists at Nordea answer some questions that keep reappearing when discussing the Norwegian Krone and Norges Bank.

At what level will Norges Bank intervene?

“If EUR/NOK rises from 12 to 14 over the duration of a month no intervention will come, but if EUR/NOK rises from 12 to 14 in one day, then it is likely that Norges Bank will step in.”

What is most likely to happen with the NOK after Norges Bank’s May meeting?

“We believe that talk and speculation of a 50 bps rate hike from Norges Bank this week could leave some participants wrong-footed. If Norges Bank hikes by 25 bps, as we expect, the NOK will likely weaken further.”

What is Nordea’s base case for the NOK?

“We expect the NOK to weaken further until the summer, with EUR/NOK coming above 12. However, after the summer, the NOK sales will be wound down and most central banks will pause their rate hikes. We see a lower EUR/NOK towards year-end, closer to 11.00, but the NOK will likely remain weak in a historic context for some time.”

- USD/CAD reverses an intraday dip and climbs to a fresh weekly high on Wednesday.

- Tumbling Crude Oil prices undermines the Loonie and acts as a tailwind for the major.

- Broad-based USD weakness keeps a lid on the pair ahead of the crucial FOMC decision.