- Аналітика

- Новини та інструменти

- Новини ринків

Новини ринків

- EUR/USD stabilizes at the lowest level in a month as it bounces off 100-DMA to prod three-day downtrend.

- US Dollar surprisingly cheers US credit rating downgrade via risk aversion, strong yields.

- Lack of entertainment from the ‘Old Continent’ allows Greenback bulls to keep the reins.

- Slew of inflation, employment and activity data from Eurozone, US will entertain Euro traders, bears occupy driver’s seat below 1.0985.

EUR/USD seesaws around 1.0940-50 during the early hours of Thursday’s Asia session after declining to the lowest level in a month by posting a three-day downtrend in the last. In doing so, the Euro pair portrays the market’s cautious mood ahead of a slew of data from the Eurozone and the US. It’s worth noting that the risk aversion wave joins upbeat Treasury bond yields and an empty plate to offer from the bloc to underpin the US Dollar’s rally the previous day, which in turn dragged the Euro towards the lowest level since early July.

Fitch Ratings’ downgrade to the US government credit rating flagged fears of the US default and weighed on the sentiment, which in turn bolstered the US Dollar’s haven demand, drowning the EUR/USD pair due to its risk-barometer status. Apart from the haven demand, upbeat prints of the US ADP Employment Change and a run-up in the Treasury bond yields also pleased the Euro bears.

On Wednesday, US ADP Employment Change for July rose past 189K markets forecasts to 324K while the previous readings were revised down to 455K.

That said, US Treasury Secretary Janet Yellen and White House (WH) Economic Adviser Jared Bernstein defended the credibility of the US Treasury bonds and vouched for the US economic strength after Fitch Ratings’ cited such concerns as the catalysts for their downgrade to the US government credit ratings. On the same line, the US Treasury Department raised possibilities of testing demand for the US bonds after the rating cut by fueling the weekly longer-term debt issuance. The same pushed markets to remain worrisome and rush for risk safety.

Amid these plays, US 10-year Treasury bond yields rose to the highest level since November 2022 while the US Dollar Index (DXY) also jumped to a three-week top. Further, the Wall Street benchmarks also closed in the red and portrayed risk aversion.

Looking forward, Eurozone Producer Price Index (PPI) for June will precede the final activity data for July to entertain EUR/USD traders during early Thursday. Should the EU numbers flash upbeat data, the Euro pair may consolidate the latest losses.

Following that, the US ISM Services PMI, Factory Orders, Weekly Initial Jobless Claims and quarterly readings of Nonfarm Productivity and Unit Labor Costs will be crucial to watch for clear directions. It’s worth noting that the EUR/USD bears are more likely to witness further downside but it all depends upon how strongly the scheduled statistics defend the Federal Reserve’s (Fed) September rate hike.

Technical analysis

A daily closing beneath the nine-week-old rising support line, now immediate resistance near 1.0985, keeps EUR/USD sellers hopeful even if the 100-DMA tests further downside around 1.0915.

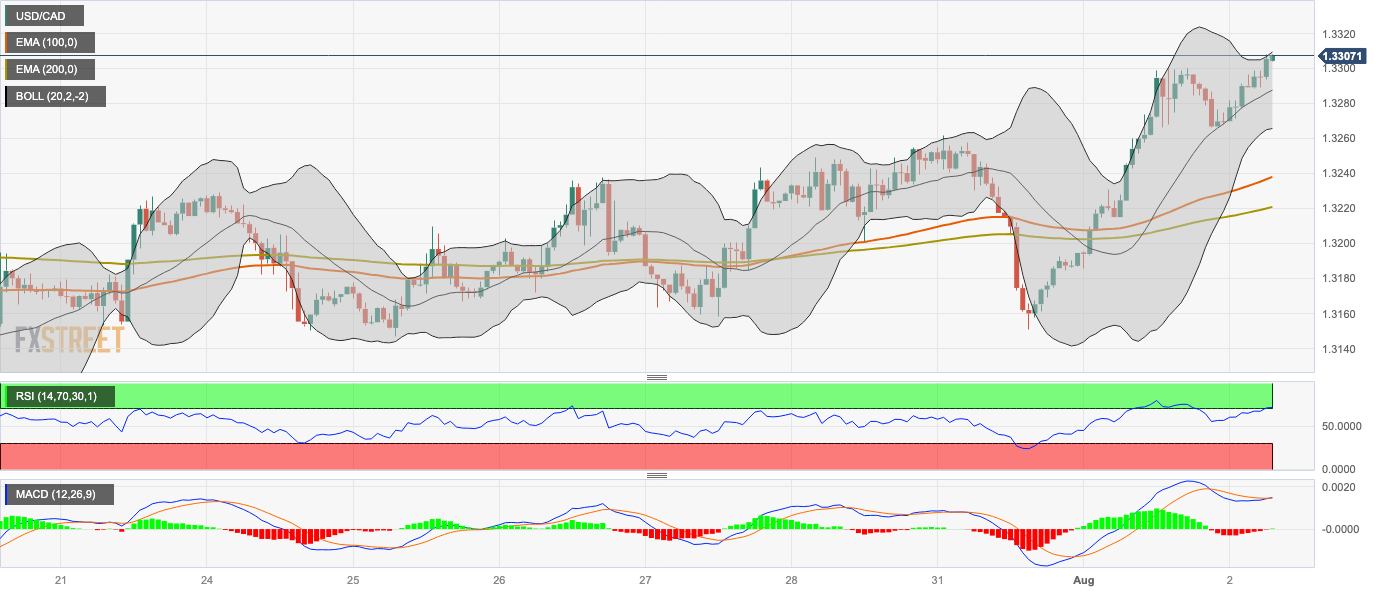

- USD/CAD oscillates in a narrow range near 1.3345, down 0.03% for the day.

- ADP showed that the US economy created 324K jobs in July, above the estimation.

- A decrease in oil prices has undermined the Loonie.

- The key events to monitor are the Canadian Employment Change and Nonfarm Payrolls.

The USD/CAD pair consolidates its recent gains around 1.3345 during the early Asian session on Thursday. The major pair is on track for its sixth weekly close above 1.3200. Lower Oil prices are the main driver of the Canadian Dollar's depreciation.

On Wednesday, Automatic Data Processing Inc. (ADP) revealed that the number of employed people in the US private sector rose by 324K, above estimates of 189K and lower than the revised reading of 455,000 in June. This figure is above the 12-month average. The employment data could convince the Federal Reserve (Fed) to hike additional rates this year, which benefits the US Dollar and acts as a tailwind for the USD/CAD pair.

On the Canadian Dollar front, investors await the Canadian Employment Change on Friday as it could offer hints into the strength of domestic activity and the direction of the BoC's monetary policy.

Earlier this week, Canada’s manufacturing sector declined for the third consecutive month in July. The S&P Global Canada Manufacturing PMI rose to 49.6. This figure followed the previous month's 48.8 and was better than expected at 48.9. A reading below 50 indicates sector contraction. It has been below that level since May. Meanwhile, a decrease in oil prices has undermined the Loonie since Canada is the largest oil exporter to the United States.

Market participants will keep an eye on the US weekly Jobless Claims, Unit Labour Costs and ISM Service PMI later in the American session. On Friday, attention will shift to Canadian Employment Change and Nonfarm payrolls. The US economy is expected to have created 180,000 jobs. While economists forecast that the Canadian economy will create 21,100 jobs in July. The data will be critical for determining a clear movement for the USD/CAD pair.

Technically, the further upside appears favorable for USD/CAD as the Relative Strength Index (RSI) stands above 50 on the one-hour chart. The immediate resistance level is seen at 1.3385 (High of June 6) and the initial support level appears at 1.3300 (a psychological round mark).

- GBP/JPY stays pressured after reversing from three-week-old ascending resistance line.

- Downbeat oscillators, fears of BoE’s dovish hike direct sellers toward previous resistance line.

- Buyers need validation from BoE Governor Andrew Bailey and yearly high marked in July to retake control.

GBP/JPY holds lower grounds near 182.00 after snapping a three-day uptrend the previous day. In doing so, the cross-currency pair keeps Wednesday’s U-turn from a three-week-old rising trend line as market players await the Bank of England (BoE) Interest Rate Decision on Thursday.

Also read: Bank of England Preview: Sell Sterling? Why Bailey may break the Pound, even with a bigger hike

Not only the quote’s pullback from the key resistance line stretched from July 11 but bearish MACD signals and downward-sloping RSI (14), not oversold, also weigh on the GBP/JPY price on a crucial day.

With this, the pair sellers appear well set to test the previous resistance line from July 06, close to 181.30 by the press time.

In a case where the market’s disappointment from the BoE becomes too heavy and breaks the 181.30 support, the 200 Exponential Moving Average (EMA) level of 180.60 and the 180.00 round figure will challenge the GBP/JPY pair’s further downside.

On the flip side, a clear break of the aforementioned resistance line, close to 183.40 by the press time, could convince sellers to stay in the line. However, they may want to wait for a clear upside break of the yearly high marked in July, around 184.00, for further dominance.

To sum up, GBP/JPY stays on the bear’s radar as markets prepare for the BoE’s dovish hike.

GBP/JPY: Four-hour chart

Trend: Further downside expected

- EUR/JPY retraces from the weekly high of 157.50, falling past 157.00, trading at 156.78, failing to test the YTD high of 157.99.

- Japanese Yen’s strength is attributed to the Bank of Japan’s Yield Curve Control flexibility and a downgrade of US creditworthiness from AAA to AA+.

- Technicals show a peak around the 156.80/157.40 area, with bearish signals from the Tenkan-Sen, Kijun-Sen, and Chikou Span.

EUR/JPY retraces from weekly highs of 157.50 and drops below 157.00 as buyers failed to extend their gains and test the year-to-date (YTD) high of 157.99. The reasons behind the Japanese Yen (JPY) strength are the Yield Curve Control (YCC) flexibility imposed by the Bank of Japan (BoJ), as well as the downgrade of US creditworthiness from AAA to AA+. Therefore, the EUR/JPY tumbled and is trading at 156.78.

EUR/JPY Price Analysis: Technical outlook

The EUR/JPY appears to have peaked at around the 156.80/157.40 area, as depicted in the daily chart. The cross-currency pair has failed to decisively clear the 158.00 mark, exacerbating its fall beneath the 157.00 figure. In addition, a two-day candlestick called dark cloud cover looms, but Thursday’s price action must clear Wednesday’s daily low of 156.25 and achieve a daily close below the latter to extend its losses.

Notably, the Tenkan-Sen sits below the Kijun-Sen, at around the top of the Ichimoku Cloud (Kumo) at around 154.59/72, a bearish signal. Furthermore, the Chikou Span is positioned below the price action, suggesting that sellers could regain control in the near term.

The EUR/JPY first support would be 156.25, followed by the figure at 156.00. A breach of the latter will expose the Kijun-Sen at 154.72, followed by the Tenkan-Sen at 154.59, before dipping inside the Kumo. Conversely, if EUR/JPY reclaims 157.00, that could open the door for further upside, with buyers challenging 158.00.

EUR/JPY Price Action – Daily chart

- AUD/USD portrays corrective bounce after falling heavily in the last two consecutive days to refresh a multi-week low.

- US Dollar cheered risk aversion, strong yields after Fitch Ratings’ downgrade to US government credit rating.

- Upbeat US ADP Employment Change, RBA’s surprise pause add strength to downside bias about Aussie pair.

- Australia Retail Sales, Trade Balance and a slew of activity/employment clues from China and US eyed for clear directions.

AUD/USD prints mild gains around 0.6540 amid the initial Asian session on Thursday as it consolidates the recent losses after falling heavily in the last two consecutive days to the lowest levels since early June. In doing so, the Aussie pair braces for a slew of top-tier data from Australia, China and the US after bearing the burden of the Reserve Bank of Australia’s (RBA) rate hike pause and the strong US Dollar.

That said, the Fitch Ratings’ downgrade to the US government credit rating flagged fears of the US default and weighed on the sentiment, which in turn bolstered the US Dollar’s haven demand, drowning the AUD/USD pair due to its risk-barometer status. Apart from the haven demand, upbeat prints of the US ADP Employment Change and a run-up in the Treasury bond yields also pleased the Aussie bears.

It’s worth mentioning that downbeat prints of Australia’s AiG activity numbers for June also weighed on the AUD/USD price.

On Wednesday, Australia’s AiG Industry Index for June slumped to -14.7 from -11.9 whereas AiG Manufacturing PMI for the said month nosedived to -25.6 from -19.8 previous readings. That said, Australia’s S&P Global Composite PMI edges lower to 48.2 for July from 48.3 while the Services PMI eases to 47.9 from 48.0.

On the other hand, US ADP Employment Change for July rose past 189K markets forecasts to 324K while the previous readings were revised down to 455K.

It should be noted that US Treasury Secretary Janet Yellen and White House (WH) Economic Adviser Jared Bernstein defended the credibility of the US Treasury bonds and vouched for the US economic strength after Fitch Ratings’ cited such concerns as the catalysts for their downgrade to the US government credit ratings. On the same line, the US Treasury Department raised possibilities of testing demand for the US bonds after the rating cut by fueling the weekly longer-term debt issuance. The same pushed markets to remain worrisome and rush for risk safety. As a result, US 10-year Treasury bond yields rose to the highest level since November 2022 while the US Dollar Index (DXY) also jumped to a three-week top. Further, the Wall Street benchmarks also closed in the red and portrayed risk aversion.

Looking forward, Australia’s second-quarter (Q2) Retail Sales and Trade Balance for June will join China’s Caixin Services PMI for July to entertain AUD/USD traders during the Asian session. Following that, the US ISM Services PMI, Factory Orders, Weekly Initial Jobless Claims and quarterly readings of Nonfarm Productivity and Unit Labor Costs will be crucial to watch for clear directions. Although the RBA is more likely to have reached the policy pivot, especially after the latest two consecutive pauses, today’s Aussie data and Friday’s RBA Monetary Policy Statement can help confirm the bias and may flag further downside of the AUD/USD pair.

Technical analysis

A daily closing beneath the 10-month-old rising support line, now immediate resistance near 0.6590, directs the AUD/USD bears toward the yearly low marked in May around 0.6460.

- USD/CHF remains confined in a tight range between 0.8770 and 0.8780 ahead of the Swiss inflation data.

- The number of employed people in the US private sector rose by 324K, above estimates of 189K.

- Fitch downgraded the US government's credit rating from AAA to AA+, fueling concern about the US debt ceiling crisis.

- Investors await the Swiss Consumer Price Index (CPI), the US weekly Jobless Claims and Unit Labor Cost.

The USD/CHF pair consolidates in a narrow range above 0.8770 in the early Asian session after retreating from the key barrier around 0.8800. The solid US ADP Employment Change lifts the Greenback. The US Dollar Index (DXY), a measure of the value of USD against six other major currencies, surges to its highest level since July 7 at 102.80 in response to the news.

That said, Automatic Data Processing Inc. (ADP) revealed on Wednesday that the number of employed people in the US private sector rose by 324K, above estimates of 189K and lower than the revised reading of 455,000 in June. This figure is above the 12-month average. Investors speculate on a more aggressive Federal Reserve (Fed) stance, which benefits the US Dollar and acts as a tailwind for the USD/CHF pair.

On the other hand, markets turned cautious after Fitch downgraded the United States government's credit rating from AAA to AA+. The leading rating company cited an expected fiscal deterioration over the next three years and a high general government debt burden as the primary reasons for this drastic action.

US Treasury Secretary Janet Yellen said late Wednesday that Treasury securities remain the world's most secure and liquid asset and that the US economy is fundamentally robust, per Reuters. Additionally, White House (WH) Economic Adviser Jared Bernstein expressed confidence in the US government and Congress to avoid default, and the US Treasury debt remains the safest in the world. However, this headline fuels concern about the US debt ceiling crisis and might cap the upside in the Greenback. This, in turn, might benefit the Swiss Franc, a traditional safe-haven asset.

Looking ahead, market participants await the Swiss Consumer Price Index (CPI) YoY for July. Also, investors will take cues from more US employment data. The US weekly Jobless Claims and Unit Labor Costs are due later in the day. The highlight of the week is the US Nonfarm Payrolls on Friday. The economy is expected to have created 180,000 jobs in July.

- Gold Price remains pressured at three-week low after breaking key support confluence.

- Firmer US Dollar, Treasury bond yields weigh on XAU/USD price ahead of United States activity, employment clues.

- Upbeat US ADP Employment Change, US credit rating woes join likely weak physical Gold demand from Asia to favor sellers.

- Firmer prints of US ISM Services PMI, Factory Orders and Q2 Unit Labor Costs will favor XAU/USD bears before NFP.

Gold Price (XAU/USD) languishes at the lowest level since July 12, making rounds to $1,935 after breaking the $1,945 support confluence, as bears lick their wounds ahead of a slew of United States statistics scheduled for release on Thursday. That said, a jump in the US Treasury bond yields and the US Dollar weighed on the Gold Price the previous day. While tracing the catalysts, the market’s fears emanating from the Fitch Ratings’ downgrade to the US credit rating, the US Treasury’s testing of the market’s acceptance and the upbeat Automatic Data Processing (ADP) Employment Change for July gained major attention.

Gold Price drops as US Dollar cheers upbeat United States employment data, strong yields

Gold Price dropped for the second consecutive day to the lowest level in three weeks as the Firth Ratings’ downgrade to the US government credit rating flagged fears of the US default and weighed on the sentiment, which in turn bolstered the US Dollar’s haven demand and weighed on the Gold Price. Apart from the haven demand, upbeat prints of the US ADP Employment Change and a run-up in the Treasury bond yields also favored the US Dollar, as well as weighed on the XAU/USD.

Late on Wednesday, US Treasury Secretary Janet Yellen and White House (WH) Economic Adviser Jared Bernstein defended the credibility of the US Treasury bonds and vouched for the US economic strength after Fitch Ratings’ cited such concerns as the catalysts for their downgrade to the US government credit ratings.

On the same line, the US Treasury Department raised possibilities of testing demand for the US bonds after the rating cut by fueling the weekly longer-term debt issuance.

Elsewhere, US ADP Employment Change for July rose past 189K markets forecasts to 324K while the previous readings were revised down to 455K.

Amid these plays, US 10-year Treasury bond yields rose to the highest level since November 2022 while the US Dollar Index (DXY) also jumped to a three-week top, which in turn weighed on the Gold Price. It should be noted that the Wall Street benchmarks also closed in the red and portrayed risk aversion while favoring the XAU/USD bears.

Gold sellers seek more clues to confirm Federal Reserve rate hike in September

Although the firmer US Treasury bond yields and the US Dollar keep the Gold sellers hopeful, the Greenback buyers need more clues to defend the latest strength as markets brace for Friday’s United States Nonfarm Payrolls (NFP).

As a result, today’s US ISM Services PMI, Factory Orders, Weekly Initial Jobless Claims and quarterly readings of Nonfarm Productivity and Unit Labor Costs will be crucial to watch for the Gold traders. Should these figures keep coming in firmer, the markets can expect a firmer US NFP and increase their bets on the Federal Reserve (Fed) rate hike in September, which in turn will favor the US Dollar and weigh on the Gold Price.

Also read: Gold Price Forecast: XAU/USD pressuring a critical support level

Gold Price Technical Analysis

Gold Price offered a clear break of the $1,945 support confluence, now resistance, and welcomed bears on Wednesday.

Adding strength to the downside bias for the XAU/USD price is the descending Relative Strength Index (RSI) line, placed at 14, as well as bearish signals from the Moving Average Convergence and Divergence (MACD) indicator.

With this, the Gold sellers prod an ascending support line from late November 2022, close to $1,930 by the press time, a break of which could drag the bullion prices to a five-month-long rising trend line, near $1,918 at the latest.

In a case where the XAU/USD remains weak past $1,918, the 50% Fibonacci retracement of its November 2022 to May 2023 upside, around the $1,900 round figure, will precede the 200-DMA support of $1,892 to offer the last fight to the bears before the bull’s surrender.

On the contrary, a daily closing beyond the $1,945 resistance confluence comprising the 50-DMA and a five-week-old upward-sloping trend line, could direct the Gold Price toward February’s peak of around $1,960.

It’s worth observing, however, that the Gold Price remains on the bear’s radar unless crossing the previous monthly high surrounding $1,988.

Overall, the Gold Price is likely to witness further downside but the road towards the south is long and bumpy.

Gold Price: Daily chart

Trend: Further downside expected

- GBP/USD breaks below the bottom of an ascending channel and the 50-day EMA at 1.2742, trading at 1.2715 with a neutral to downward bias.

- If the pair drops below the 1.2700 psychological level, support may be found at the 100-day EMA at 1.2591, followed by the 200-day EMA at 1.2440.

- A rebound above 1.2700 and reclaiming the 50-day EMA could lead to a rally towards 1.2800, with the next resistance at the 20-day EMA at 1.2827.

- The RSI has turned bearish, while the three-day RoC suggests that the 1.2700 level might hold in the short term amid the BoE monetary policy decision.

GBP/USD breaks below the bottom of an ascending channel, ahead of the Bank of Englan’s (BoE) monetary policy decision on Thursday, as the pair aims toward the 1.2700 psychological figure. As the Asian session commences, the GBP/USD is exchanging hands at 1.2715, posting minuscule gains of 0.04%.

GBP/USD Price Analysis: Technical outlook

The GBP/USD is neutral to downward biased, as the daily chart depicts, as the pair dropped on Wednesday’s session below the 50-day Exponential Moving Average (EMA) at 1.2742. In addition, the GBP/USD extended its fall below the bottom of the ascending channel, opening the door for further losses. That, alongside the Relative Strength Index (RSI) indicator turning bearish, could pave the way for a drop below 1.2700. Nevertheless, the three-day Rate of Change (RoC) portrays a slight divergence with price action, suggesting that the 1.2700 psychological level might hold in the near term.

If GBP/USD drops below 1.2700, next support emerges at the 100-day EMA at 1.2591, followed by the 200-day EMA at 1.2440. Conversely, if GBP/USD stays above 1.2700 and reclaims the 50-day EMA at 1.2742, that could exacerbate a rally towards 1.2800 and beyond. Next resistance emerges at the 20-day EMA at 1.2827, followed by a downslope resistance trendline at 1.2925/40.

GBP/USD Price Action – Daily chart

“Treasury securities remain the world's preeminent safe and liquid asset, and that the American economy is fundamentally strong,” said US Treasury Secretary Janet Yellen on late Wednesday while at an Internal Revenue Service contractor office near Washington, per Reuters.

On the same line, White House (WH) Economic Adviser Jared Bernstein also said that the US Treasury debt remains the safest in the world.

More to come…

- NZD/USD has taken a hit, declining by more than 1%, with a daily high previously at 0.6169.

- The US credit rating was downgraded from AAA to AA+, causing a surge in demand for the US Dollar and the Japanese Yen in the FX market.

- New Zealand’s unemployment rate rose to 3.6%, above expectations, and wage growth was weaker than anticipated, aligning with the RBNZ’s decision to end its tightening cycle.

NZD/USD plunged more than 1% on Wednesday, courtesy of a risk-off impulse as US credit rating was downgraded by Fitch, sparking a jump in US Treasury bond yields. That, alongside a solid July ADP National Employment report, boosted appetite for the US Dollar (USD). Hence, the NZD/USD slumps toward 0.6077 at the time of writing after reaching a daily high of 0.6169.

Risk-off sentiment boosts the US Dollar as Fitch downgrades US credit rating, and soft employment figures in New Zealand weigh on the Kiwi

Market sentiment was dampened after Tuesday’s Fitch Ratings downgraded US creditworthiness from AAA to AA+ “on a perceived deterioration in US governance, which it said gave less confidence in the government’s ability to address fiscal and debt issues,” according to the report. After the release, traders seeking refugee bought the US Dollar (USD) and the Japanese Yen (JPY) in the FX space.

Earlier, data revealed by ADP revealed that private hiring in July improved sharply, with the economy adding 324K jobs smashing 189K estimates, ahead of Friday’s US Nonfarm Payrolls report. According to a Reuters poll, the US economy created 200K jobs, as revealed by analysts. In other data, July’s manufacturing activity continued to improve in the US, as the ISM shows, arriving at 46.4, below 46.8 estimates but exceeding June’s 46.0.

On the New Zealand (NZ) front, labor market data for the second quarter (Q2) of 2023 was soft. The Unemployment rate rose by 3.6% above 3.5% estimates, and wages, including and excluding overtime, came in at 1.1% q/q vs. 1.2% expected and 0.9% in Q1. Regarding Average hourly earnings, they came at 1.9% QoQ below Q1 2.1%, supporting the Reserve Bank of New Zealand’s (RBNZ) decision to finish its tightening cycle. The swaps market suggests the RBNZ would keep rates unchanged for August and October, but November is still open. Nevertheless, if data remains weak, the RBNZ will hold rates at the current level.

NZD/USD Price Analysis: Technical outlook

From a daily chart standpoint, the NZD/USD has turned bearish since the start of the week, dropping below the 200, 100, and 20-day Exponential Moving Averages (EMAs), spurring a 146 pip drop. Also, the NZD/USD breaking below the two-month-old upslope support trendline opened the door to test year-to-date (YTD) lows of 0.5985, but sellers must conquer demand zones on its way down. Firstly the June 29 daily low of 0.6050, followed by June’s 8 low of 0.6045, ahead of 0.6000. On the other hand, if NZD/USD stays above 0.6100, that could pave the way to test the psychological 0.6150, ahead of challenging a busy area with the daily EMAs hovering around 0.6200.

- EUR/USD tallies a third stright daily loss, and fell to the 1.09370 level.

- The Labour market in the US and in the EUR showed positive results this week.

- All eyes are now on Friday’s US NFPs.

The EUR/USD is trading in negative territory after 3 consecutive days of losses, fueled by a stronger USD following robust labour market data. The greenback, measured by the DXY index, gained ground in the middle of the week and jumped to its highest label since July 7.

According to, Automatic Data Processing (ADP), Inc released the US Employment Change for July, which measures the change in the number of employed people in the US, came in at 324k, better than the expected 189k but below the previous 455k. With this in mind, hot labour market data may set the tone for the Federal Reserve (Fed) to consider one additional hike in 2023, and that is what is driving the USD upwards.

That being said, Jobless Claims on Thursday and the Nonfarm Payrolls report on Friday will give additional clues to the markets regarding the labour situation in the US and will continue placing their bets for the next Fed meeting. As for now, according to the CME FedWatch tool, the most likely case is that the Federal Open Market Committee (FOMC) won't hike in September or November.

For the Eurozone’s side, Spain released the Unemployment Change for July, which showed that the number of unemployed workers added during the previous month, came in better than expected. This comes after Germany also reported strong labour figures on Tuesday. Its worth noting that Christine Lagarde highlighted that the labour market remains robust and also mentioned that incoming data will be considered for the following interest rate decisions, so strong data may fuel hawkish bets on the European Central Bank (ECB). For the rest of the week, Services PMIs from European countries will be released on Thursday, giving further guidance to both markets and the ECB regarding the economic activity situation in the zone.

EUR/USD Levels to watch

According to the daily chart, bears are gaining ground as the Relative Strength Index (RSI) is in negative territory and has a slope below its midline. The Moving Average Convergence Divergence (MACD) prints strong growing red bars indicating that bulls are not in the scene.

Resistance levels: 1.0950, 1.1000, 1.1075 (20-day SMA).

Support levels: 1.0913 (100-day SMA), 1.0900, 1.0850.

EUR/USD Daily chart

-638266079408531297.png)

During the Asian session, Australian data includes the final S&P Global Composite PMI, retail sales, and trade data. The Chinese Caixin Services PMI is also due. Later in the day, Switzerland will report inflation, and Eurostat will release the June Producer Price Index. The main event in Europe will be the Bank of England's decision. In the US, the weekly jobless claims, ISM Services PMI, and Unit Labor Costs are due, all ahead of Friday's NFP.

Here is what you need to know on Thursday, August 3:

US stocks dropped on Wednesday following Fitch Ratings' downgrade of the US government credit rating late on Tuesday. The Dow Jones lost 0.98%, and the Nasdaq plummeted 2.17%. US yields peaked after the release of US data and then pulled back, with the 10-year settling around 4.07% and the 2-year at 4.88%.

Market participants will digest earnings results from Apple, Amazon, ConocoPhillips, Airbnb, among others on Thursday.

While on Tuesday, the decline in job openings showed signs of easing, the ADP private employment report came in stronger than expected and above the average of the last 12 months, with private employment rising by 324K, surpassing expectations of 189K.

Nela Richardson Chief Economist, ADP:

“The economy is doing better than expected and a healthy labor market continues to support household spending. We continue to see a slowdown in pay growth without broad-based job loss.”

The combination of risk aversion and soft US data boosted the Greenback. The US Dollar Index (DXY) climbed to 102.80, reaching the highest level since July 7. More US employment data is due on Thursday with jobless claims and unit labor cost. Also due is the Factory Orders report. All of this takes place ahead of Friday's Nonfarm Payrolls (NFP). Early on Thursday, the Chinese Caixin Service PMI will be released.

EUR/USD posted its lowest close in almost four weeks after breaking an uptrend line. It remains under pressure below 1.0960, with the next support level at 1.0900. On Thursday, the final Eurozone PMIs are due, as well as the June Producer Price Index.

GBP/USD dropped for the third consecutive day and tested levels below 1.2700 on the back of a stronger US dollar. The Bank of England (BoE) will announce its monetary policy decision on Thursday, with a rate hike expected.

Analysts at TD Securities:

We expect the MPC to hike Bank Rate by 25bps in a 1-7-1 decision. The risks of a 50bps hike are material. Accompanying projections are likely to show a sizeable downgrade to the inflation outlook.

USD/JPY bounced all the way back from 142.30 to the 143.50 zone. The initial reaction to the US credit downgrade was offset by US jobs data, also helped by higher Treasury yields.

AUD/USD dropped below 0.6600 and accelerated to the downside, closing at 0.6540, the lowest since early June. Risk aversion, lower commodity prices, and the strong US Dollar offer a negative context for the Aussie. The bias is to the downside. Australia will report trade data and retail sales on Thursday.

NZD/USD fell below 0.6100 to 0.6068, a one-month low. Soft employment data from New Zealand supported expectations that the Reserve Bank of New Zealand (RBNZ) has ended its tightening cycle.

USD/CAD edged further higher to the 1.3350 zone and is looking at the June high at 1.3386. The Canadian Dollar hit monthly highs versus the Aussie and the Kiwi.

Crude oil prices ended a positive streak with a 2% slide. The WTI barrel pulled back under $80.00. Cryptocurrencies fell moderately, with Bitcoin at $29,130 and Ethereum at $1,840. Litecoin tumbled 5.85%.

Like this article? Help us with some feedback by answering this survey:

- XAG/USD fell below $24.00, seeing losses of 2.40%.

- US private employment beat estimates in July.

- Higher US yields and a stronger dollar are driving commodities prices lower.

On Wednesday’s session, the XAG/USD Silver spot price fell to its lowest point since July 12 driven by a stronger USD to the $23.70 area. The DXY index is rising for a fifth consecutive day, mainly because the US economy is resilient and may push the Federal Reserve (Fed) not to halt its tightening cycle.

According to Automatic Data Processing Inc. (ADP), there were 324,000 employed people in the US in July, higher than the 189,000 expectations but lower than the revised number of 455,000 in June. As the labour market is still extremely tight, it may push the Fed to consider hiking in September, strengthening the USD.

In response, US bond yields and the opportunity cost of holding Silver are rising. The yields on the 5- and 10-year bonds increased by 4.26% and 4.10%, respectively, each by more than 1%. The 2-year yield increased by 0.60% on the day to 4.92%.

As for now, according to the CME FedWatch tool, markets anticipate that the Fed won't hike in September and bet on a low odd of 20% of a 25 basis point hike, while the chances of a hike in November top out at 30% in November.

XAG/USD Levels to watch

The daily chart analysis indicates a bearish outlook for the XAG/USD in the short term. The Relative Strength Index (RSI) is below its midline in negative territory, with a negative slope, aligning with the negative signal from the Moving Average Convergence Divergence (MACD), which displays red bars, reinforcing the strong bearish sentiment. On the other hand, the pair is below the 20 and 100-day Simple Moving Averages (SMAs), but above the 200-day SMA, indicating that the bulls aren't done yet and that the outlook is still positive, looking at the bigger picture.

Support levels: $23.40,$23.15 (200-day SMA), $23.00.

Resistance levels. $24.00 (100-day SMA), $24.27 (20-day SMA), $24.50.

XAG/USD Daily chart

-638266036123266746.png)

- WTI crude oil benchmark is down 3.24% after hitting a daily high of $82.39.

- Fitch’s revision of US Government debt from AAA to AA+ impacts market sentiment, adding pressure on oil and other US Dollar-denominated commodities.

- A decline in China’s factory activity for the fourth consecutive month hints at slowing economic recovery and potentially reduced oil demand.

Western Texas Intermediate (WTI), the US crude oil benchmark, tumbled more than 3% on Wednesday as risk aversion surfaced, following Fitch’s downgrading US credit rating from AAA to AA+. Furthermore, a drop in US stockpiles weighed on oil prices. WTI is trading at $79.44 per barrel, down 3.24% after hitting a daily high of $82.39.

WTI’s price falls sharply as risk aversion surfaces

Fitch’s revision to US Government debt from AAA to AA+ was blamed “on a perceived deterioration in US governance, which it said gave less confidence in the government’s ability to address fiscal and debt issues,” according to sources cited by Reuters. That said, Wall Street plunged, while most US Dollar denominated commodities, like precious metals and oil, drifted lower.

The US Energy Information Administration (EIA) revealed that stockpiles dropped by 17 million barrels, the largest fall in US crude oil inventories, according to records from 1982. Increased refinery runs and strong US crude exports spurred stockpiles to dip.

In the meantime, weaker PMIs revealed in China showed that factory activity fell for the fourth month in a row in July, suggesting China’s demand for oil would continue to dent as the economic recovery slowdown.

Market players anticipate Saudi Arabia to extend its 1 million barrels per day (bpd) crude output for another month, including September, in a meeting of oil producers on Friday.

WTI Price Analysis: Technical outlook

WTI is trading within the bottom boundaries of an ascending channel, which witnessed the US crude oil benchmark advance from around $67.10 above $82.00 per barrel. However, as sentiment turns negative, WTI is extending its losses past $80.00 a barrel, threatening to extend its losses toward the intersection of the 200 and 20-day EMAs, each at $77.45 and $77.37, respectively. If that area is cleared, WTI’s next stop would be the confluence of the 50 and 100-day EMAs, at $74.91 and $74.88. On the other hand, if WTI stays above $80.00, that could pave the way for a recovery toward higher prices.

- XAU/USD extended its drop as US bond yields, particularly 10s, climbed above 4%.

- The credit rating agency’s downgrade of US Government debt from AAA to AA+ has impacted market sentiment, leading investors towards safety in the US Dollar and Japanese Yen.

- ADP National Employment report showed that private hiring grew by 324K, exceeding estimates, ahead of Friday’s crucial Nonfarm Payrolls data.

Gold price extends its drop to two consecutive days as US bond yield climb due to market sentiment shifting sour. That, alongside US Dollar (USD) strength following an upbeat US jobs report, is the primary driver of XAU/USD’s price action. At the time of writing, the XAU/USD is trading at $1,937.75, down 0.73%.

Gold price dips for the second straight day as US yields rise, boosting the US Dollar

Wall Street treads water as sentiment remains depressed following Fitch’s downgrading of debt of the United States (US). Despite that, US Treasury bond yields rose, led by the US 10-year benchmark note rate at 4.067%, which gains four basis points after reaching 4.126% during the North American session.

Fitch’s revision to US Government debt from AAA to AA+ was blamed “on a perceived deterioration in US governance, which it said gave less confidence in the government’s ability to address fiscal and debt issues,” according to sources cited by Reuters. Hence, market participants sought safety, with the US Dollar and the Japanese Yen (JPY) leaders in Wednesday’s session.

In the meantime, the ADP National Employment report flashed that private hiring grew by 324K exceeding estimates of 189K, ahead of July’s US Nonfarm Payrolls data on Friday, with forecasts circa 200K people added to the workforce.

Regarding Tuesday’s data, the ISM Manufacturing PMI came at recessionary territory below the 50 figure for the ninth straight month, though it continued to improve; compared to June’s 46, it arrived at 46.4. Even though it was an improvement, the trend appears to slow down.

In the meantime, the US Dollar Index (DXY), a measure of the buck’s value against a basket of six currencies, advances 0.54% at 102.514, prolonging its gains to six straight days, with traders eyeing a break above the 100-day EMA at 102.561.

XAU/USD Price Analysis: Technical outlook

Although XAU/USD achieved a higher high on Friday 20 daily high at $1,987.42, the XAU/USD retraced back below the $1,950 area, extending its losses below the 20 and 50-day Exponential Moving Averages (EMAs), at $1,952.02 and $1,951.05, respectively. Additionally, XAU/USD dropped under the 100-day EMA, opening the door for further downside. Nevertheless, the emergence of a ‘bullish flag’ can pave the way for further upside, with prices edging toward $2,000. On the flip side, if XAU/USD falls below $1,933.07, that would exacerbate a dip toward the 200-day EMA at $1,906.99.

- USD/CHF jumped near 0.8800, setting a five-day winning streak.

- The US reported hot ADP figures, which strengthened the USD.

- The USD DXY index is rising and trades at 102.65.

The USD/CHF has risen to its highest level since mid-July, towards 0.8800 and then settled near 0.8770, driven by a stronger USD. In simple terms, the US economy is holding firm, making investors place bets on a more aggressive bet on the Federal Reserve (Fed) which is benefiting the greenback.

The number of employed people in the US was 324,000 in July, according to Automatic Data Processing Inc. (ADP), which was higher than the 189,000 expectations but lower than the revised figure of 455,000 in June.

US bond yields are increasing globally in response to the data. The 5- and 10-year yields increased by 4.26% and 4.10%, respectively, with both seeing more than 1% increases. The 2-year yield rose to 4.92%, with a 0.60% increase on the day.

Regarding Fed expectations, according to the CME FedWatch tool, market participants are betting on low odds of a hike in September, while the probability of a walk in November stands near 30%, and investors foresee low odds of a 50 bps increase. However, the highlight with which the markets will make their projections will be Friday's Nonfarm payrolls (NFPs) report. The unemployment rate is anticipated to stay constant at 3.6%, while consensus for NFP has increased to 200k from 209k in June, while Average Hourly Earnings are expected to have eased.

For the rest of the session, the Swiss and American calendars will have nothing relevant to offer, so market sentiment and Fed bets will set the pace.

USD/CHF Levels to watch

Considering the daily chart, the USD/CHF shows a bullish sentiment for the short term. The Relative Strength Index (RSI), positioned above its midline in positive territory with a northward slope, supports this view along with the positive indication from the Moving Average Convergence Divergence (MACD), which is displaying green bars, pointing towards a strengthening bullish impulse. Plus, is consolidating above the 20-day Simple Moving Average (SMA), indicating that the outlook is still positive for the short term.

Resistance levels: 0.8810, 0.8830, 0.8850.

Support levels: 0.8700 (20-day SMA), 0.8660, 0.8630.

USD/CHF Daily chart

-638265960240503705.png)

- EUR/GBP remains neutral to downward biased, with strong resistance at around 0.8650/75, potentially hindering buyers’ attempts to reach 0.8700.

- If the pair breaks above 0.8675, it may target 0.8700, followed by a seven-month-old downslope resistance trendline around 0.8730/50.

- A daily close below the 50-day EMA at 0.8609 could open the way for a drop toward last week’s low of 0.8544 or the YTD low of 0.8504.

The EUR/GBP extends its gains to two consecutive days but faces solid resistance at around 0.8630, with the EUR/GBP pair dropping below the 50-day Exponential Moving Average (EMA) at 0.8609. At the time of writing, the EUR/GBP exchanges hands at 0.8607, gaining 0.12% after reaching a low of 0.8584.

EUR/GBP Price Analysis: Technical outlook

The EUR/GBP daily chart portrays the pair as neutral to downward biased, despite the recent lower low being above the year-to-date (YTD) low of 0.8504 at 0.8544 but strong resistance at 0.8650/75, which could cap buyers’ attempts to reach the 0.8700 figure in the near term.

If EUR/GBP breaks above 0.8675, the next supply zone would be 0.8700. A breach of the latter will expose a seven-month-old downslope resistance trendline at around 0.8730/50, followed by a rally to 0.8800.

On the other hand, if EUR/GBP prints a daily close below the 50-day EMA at 0.8609, that could open the door for a break below the 0.8600 mark. The following support would be the 20-day EMA at 0.8689, followed by the last week’s low of 0.8544, ahead of the YTD low of 0.8504.

Oscillator-wise, the Relative Strength Index (RSI) turned bullish, while the three-day Rate of Change (RoC) suggests buyers are entering the market. However, they must reclaim solid resistance levels if they would like to extend their gains toward the 0.8700 figure.

EUR/GBP Price Action – Daily chart

- USD/CAD rose near 1.3340, displaying more than 0.40% gains on the day.

- ADP showed that the US created more jobs than expected in July.

- Dropping Oil prices and a negative market sentiment also contribute to the upwards momentum.

On Wednesday’s session, the USD/CAD rose for a second consecutive day, near 1.3340. A stronger Dollar amid hot labour market data from the US and lower Oil prices are the main responsible for the CAD’s weakness.

The US created more jobs than expected in July

The number of employed people in the US was 324,000 in July, according to Automatic Data Processing Inc. (ADP), which was higher than the 189,000 expectations but lower than the revised figure of 455,000 in June. Despite decelerating from its previous reading, it may suggest to the Federal Reserve (Fed) that the sector is still tight and may contribute to inflationary pressures via rising wages. That said, investors will closely look at Nonfarm Payrolls and Average Hourly Earnings data on Friday.

Reacting to the data, the USD strengthened as US yields rose and Wall St indexes dropped. The 2-year yield rose to 4.93% while the S&P 500 (SPX) declined by 1.23% as well as the Dow Jones and the Nasdaq Composite, which are seeing losses of 0.76% and 1.84%, respectively.

In that sense, investors may place bets on a more aggressive Fed. Still, as Chair Powell stated, monetary policy decisions will depend on data, so the labour market on Thursday and Friday will dictate the pace of the markets.

USD/CAD Levels to watch

From a technical standpoint, the USD/CAD maintains a bullish outlook for the short term, as observed on the daily chart. The Relative Strength Index (RSI) is comfortably positioned in the positive territory above its midline. It has a northward slope, complemented by a positive signal from the Moving Average Convergence Divergence (MACD), showing green bars, signalling a growing bullish momentum. Additionally, the pair is above the 20-day Simple Moving Average (SMA) but below the 100 and 200-day SMAs, suggesting that despite the recent bearish sentiment, the bulls are still resilient, holding some momentum.

Resistance levels: 1.3385 (July’s high), 1.3407 (100-day SMA), 1.3455 (200-day SMA).

Support levels: 1.3280, 1.3250, 1.3240.

-638265914308186468.png)

- USD/MXN pair is trading at 17.0378, up from its daily low of 16.8333 and above its 20-day Exponential Moving Average (EMA).

- Banxico’s Heath said interest rate levels are correct, even though the Fed hikes again.

- USD/MXN remains intact but is subject to correction, with significant resistance near the 17.00 mark and the 50-day EMA at 17.1336.

The Mexican Peso (MXN) weakens as the North American session progresses, down 0.82%, as the USD/MXN exchange rate looms around 17.0000 with strength for the first time since July 21, 2023. The USD/MXN is trading at 17.0378, above its 20-day Exponential Moving Average (EMA), bouncing from a daily low of 16.8333.

USD/MXN advances 0.97% on risk-off impulse, Banxico’s Heath dovish comments

A recent downgrade of debt issued by the United States (US) turned market sentiment sour as Wall Street trades with losses. Private hiring in the US rose by 324K, according to figures published by the ADP Research Institute in collaboration with Stanford Digital Economy Lab, exceeding estimates of 189K. Although the data is encouraging, it hasn’t been a prelude to the Nonfarm Payrolls report, which is expected on Friday, to show the economy added just 200K people to the workforce in July.

Regarding Tuesday’s data, the ISM Manufacturing PMI came at recessionary territory below the 50 figure for the ninth straight month, though it continued to improve; compared to June’s 46, it arrived at 46.4. Even though it was an improvement, the trend appears to slow down.

The USD/MXN resumed its uptrend based on the data bolstering the US Dollar (USD) as shown by the US Dollar Index (DXY). The DXY, which tracks the greenback’s performance against a basket of peers, stands at 102.663, gaining 0.69%, underpinned by US Treasury bond yields advance.

On the Mexican front, the Bank of Mexico (Banxico) Deputy Governor Jonathan Heath said, “restrictive monetary policy stance should be held for awhile to wait of it to have effect,” expressed in a Banorte podcast interview. He acknowledged that core inflation is not easing as the headline, adding that “it’s important for the exchange rate to be as flexible as possible with no intervention to manipulate it to a rate where it shouldn’t be.” He added that interest rates are “correct” even if the Fed hikes again.

USD/MXN Price Analysis: Technical outlook

From a technical standpoint, the USD/MXN downtrend remains intact but subject to a correction, as the 20-day EMA at 16.9005 has been left behind, with the exchange rate eyeing higher prices. The USD/MXN would face solid resistance at a three-month-old downslope resistance trendline nearby the 17.00 mark, below the 50-day EMA at 17.1336. Once that area is cleared, the USD/MXN could challenge a crucial resistance area at a May 17 low of 17.4038, which, once cleared, the 100-day EMA at 17.5313 would be up for grabs. On the downside, if USD/MXN drops below 16.9011, the year-to-date (YTD) low at 16.6238 could be tested.

- USD/JPY trades flat at 143.35 after finding support at a low of 142.22.

- According to ADP, the number of employed people rose by 324k in July.

- Rising yields allowed the USD to gain traction.

On Wednesday, the USD gained traction following hot labour market data from the US. The DXY index trades rose above the 100-day Simple Moving Average towards 102.70, its highest level since early July.

Automatic Data Processing Inc. (ADP) revealed that the number of employed people in the US was 324,000 in July, higher than the 189,000 expected but lower than the revised figure of 455,000 in June.

As a reaction, US bond yields are rising across the board. The 2-year yield jumped to 4.92%, while the 5 and 10-year yields to 4.26% and 4.10%, respectively, with the latter increasing by more than 1%. Regarding bets on the Federal Reserve (Fed), according to the CME FedWatch tool, markets are confident that the Federal Open Market Committee (FOMC) won’t hike in September but started low bets on a 50 basis point hike (bps) in the November meeting. In addition, the odds of a lower hike of 25 bps stand around 25%.

Focus now shifts to Jobless Claims data on Thursday and Nonfarm Payrolls on Friday, as Jerome Powell clearly stated that ongoing decisions will depend “solely” on incoming data.

USD/JPY Levels to watch

Based on the daily chart, the USD/JPY exhibits a bullish outlook for the short term. The Relative Strength Index (RSI) and Moving Average Convergence Divergence (MACD) remain in positive territory, with the RSI above its midline with a positive slope. The MACD is also displaying green bars, indicating a strengthening bullish momentum.

Resistance levels: 143.50, 144.00, 144.50.

Support levels: 142.30,140.70 (20-day SMA), 140.00.

USD/JPY Daily chart

-638265865638007581.png)

Gold has been very sensitive to upside and downside economic data surprises. When data starts to come in below expectations, XAU/USD could surge above $2,100, economists at TD Securities report.

Mean reverting nature of economic surprises points to $2,100+ Gold

The cyclicity and mean reverting nature of economic data surprises, along with the Fed's restrictive rate policies, should work in tandem to precipitate a downdrift in US economic surprise indices.

If the Fed Fund futures reaction remains constant, dropping on negative data surprises as it rose in response to positive surprises, the resulting lower yield along the forward curve should see Gold rally. We project that this, along with technical factors, could help the yellow metal move into $2,100+ territory into late-2023.

Central bank policies are set to diverge from the steady hikes characterizing the first half of 2023, contributing to increased market volatility for the remainder of the year, economists at Charles Schwab report.

More volatility in currencies, interest rates and stocks

In the second half of the year, central bank policy is diverging from the steady pace of hikes seen in the first half of the year.

Perhaps most significantly, a potential unwinding of the Yen carry trade could roil markets.

These shifts could mean more volatility in currencies, interest rates and stocks than seen in the first half of the year.

Economists at Rabobank share their USD/JPY and EUR/JPY forecasts.

Fibonacci retracement at EUR/JPY 151.30 is key support

Our forecast of USD/JPY 138 on a three-month view assumes that speculation of further potential tweaks by the BoJ remains, though we expect that progress will be slow on this front.

We see the EUR/JPY pair at 149 in three months. EUR/JPY broke below trendline support on the back of the ECB’s dovish hike in late July. The Fibonacci retracement at EUR/JPY 151.30 is key support.

The US Dollar weakened further in July as it fell to fresh year-to-date lows. Economists at MUFG Bank analyze Greenback’s outlook.

US Dollar to rebound in the H1 of next year

We expect the US Dollar to weaken further through the rest of this year.

The main risk to our view would be if US inflation proves more sticky than expected thereby limiting room for Fed cuts, and/or if the US economy becomes too hot or too cold.

In our forecast profile, we show the US Dollar beginning to rebound in the H1 of next year to reflect the risk of a sharper US/global slowdown in response to tighter monetary policy that boosts demand for safe havens such as the USD.

The Bank of England (BoE) will announce its Interest Rate Decision on Thursday, August 3 at 11:00 GMT and as we get closer to the release time, here are the expectations forecast by the economists and researchers of 10 major banks.

The BoE is expected to hike rates by 25 basis points to 5.25%. Markets flirt with the option of a larger hike to 5.50%. Updated macro forecasts will be released. The central bank's Decision Maker Panel survey will be out as well.

SocGen

We believe the MPC will hike by 25 bps at the August meeting to address the signs of more persistent inflationary pressures that have developed since the previous meeting. Namely, the continued overshoot in pay growth. Nevertheless, the other indicators of persistent services inflation and labour market tightness, have eased since the previous meeting, meaning a 50 bps hike could be avoided. After the August meeting, the data should still point to the need for more tightening but again by 25 bps to 5.5%. Thereafter, softening data are likely to convince the MPC that it has done enough to bring inflation under control, albeit slowly.

ING

There’s just enough in the latest data flow for the Bank to be comfortable reverting back to a 25 bps hike in August. We shouldn’t rule out a 50 bps hike though, especially if the committee concludes they think they’ll hike again in September.

TDS

This meeting is a tricky one: incoming data and projections are likely to support a 25 bps hike, but the MPC may be tempted to repeat a 50 bps hike alongside a dovish lean to speed up their journey to terminal. They've signalled nothing about their intentions in recent weeks, either. Ultimately we think 25 bps will prevail, but it's a very close call.

Danske Bank

We expect the BoE to hike the Bank Rate by 25 bps. We expect a peak in the Bank Rate of 5.50% with risks tilted to the upside. We see current market pricing of a peak in policy rates of 5.90% as too aggressive. EUR/GBP is set to move modestly higher on announcement. We do not expect the press conference to offer much further guidance than the written material.

Nomura

With the inflation data having softened, there being more signs of an easing labour market (albeit from very tight levels in the first place) and some key surveys highlighting downside risks to the growth outlook, we think the Bank will be cautious and hike by a quarter point. Aside from the data, BoE guidance and uncertainties about policy lags also favour a 25 bps hike. We expect the discussion among the MPC to be primarily between 25 bps and 50 bps. The latter remains on the table because of above-normal service inflation, strong wage growth and a general view that inflation might prove stickier in the UK than elsewhere. Despite this, we think the stronger justifications for a smaller move will result in a 1-7-1 vote in favour of the decision for 25 bps (one member voting for no change, seven for 25 bps and one for 50 bps). After the August meeting, we expect further 25 bps hikes in September and November for a peak Bank Rate of 5.75%. We ultimately see rate cuts but not until the very end of 2024.

Credit Suisse

We expect the BoE to vote 8-1 to raise rates 50 bps at its August meeting from 5.0% to 5.5% on the back of elevated services inflation and record-high wage growth. However, given the recent fall in inflation, it is quite possible that the BoE hikes 25 bps, making the August decision a close call. One member (Swati Dhingra) is likely to vote for unchanged rates, but there are risks that if the majority vote is for 50 bps, one or two members vote for 25 bps.

Rabobank

The Bank of England still faces the difficult trade-off between reducing inflation and avoiding an unnecessarily deep recession. Our view remains that the BoE aims for a stance slightly more hawkish than the Fed or the ECB while avoiding any excess hawkishness. Though inflationary pressures persist, signs of slowing economic growth and initial progress on bringing inflation down support scaling back to a 25 bps hike. We expect a 2-6-1 vote split, with the core of the MPC preferring slower hikes while remaining explicitly vigilant on inflation.

Deutsche Bank

We expect a 25 bps hike taking the Bank Rate to 5.25%, although it is a close call between that and 50 bps. Beyond next week's decision, we see two more 25 bps hikes, with rate cuts potentially starting from Q2-24.

BMO

We continue to look for a 50 bps hike to 5.50%, although the market’s conviction is waning after the ECB’s move away from the hawkish door. But remember: Britain’s 7.9% inflation rate is far higher than the Euro area’s 5.5% rate, and Governor Bailey (and Chancellor Hunt) has been under a microscope over his failure to rein inflation in. The BoE’s credibility is at stake, and it was glaringly obvious with the appointment of former Fed Chair Ben Bernanke to head up the review into the BoE’s forecasting. Less polite company would say an outsider was brought in to find out why the Bank was so wrong. It also helps that the MPC’s biggest dove is out and has been replaced with what seems like a hawk. There seem to be few reasons to downshift to 25 bps.

Wells Fargo

After a 7-2 vote to raise interest rates by 50 bps at the June meeting, slowing but still elevated inflation, along with slower activity growth, makes it a closer call as to whether the BoE will raise by 50 bps again in August, or lift rates by a smaller 25 bps increment. We still lean toward a 50 bps increase but acknowledge a 25 bps move is a distinct possibility (indeed, the consensus forecast is for a smaller quarter-point hike). We will also be paying attention to the BoE's updated economic projections for insight in the potential pace and magnitude of further monetary tightening beyond the August meeting.

Brazil's central bank (Banco Central do Brasil, BCB) is ahead of rate cuts. Economists at Commerzbank analyze BRL outlook.

A less hawkish monetary policy could prove to be a drag on the BRL next year

Today's BCB decision is widely expected to result in a rate cut. The big question is whether the interest rate will be cut by 25 bps or 50 bps. Although the latter is seen as more likely by the market, it would certainly be the more dovish signal that could weigh more heavily on the BRL. However, the new inflation forecasts are likely to have a greater impact on the expected overall size of future rate cuts.

We expect the BCB to emphasize a prudent approach in its accompanying statement and to leave no doubt that it will react promptly to any upside risks to inflation. Its track record gives it a high degree of credibility, which is why we expect the Real to trade at strong levels against the USD for the time being, below 5.00 in USD/BRL terms.

The most interesting question is whether the statement will reflect a possible more dovish signature of the two central bankers newly appointed by President Lula da Silva, Gabriel Galipoli and Ailton Aquino. Because I still fear that a less hawkish monetary policy after the end of BCB Governor Roberto Campos Neto's term in December 2024 could prove to be a drag on the BRL next year.

- Silver price drops vertically as US ADP reports fresh additions of 324K payrolls in July vs. estimates of 189K.

- The US Dollar Index climbs above the crucial resistance of 102.40 amid negative market sentiment.

- Silver price is maintaining a lower high formation, which indicates that investors are capitalizing pullbacks as selling opportunities.

Silver price (XAG/USD) falls back swiftly after a short-lived pullback near $24.45 in the early New York session. The white metal faces a significant sell-off as the additions of fresh private payrolls in the United States labor market were higher than expectations in July.

The Automatic Data Processing (ADP) agency of the US economy reported that fresh 324K individuals were recruited in July while investors were anticipating employment of 189K. Strong demand for labor by US private sector indicates that inflationary pressures could rebound ahead. This has also set a positive undertone for the Nonfarm Payrolls (NFP) data, which will be published on Friday at 12:30 GMT.

The Federal Reserve (Fed) said in the monetary policy statement that further policy action will be highly data-dependent. And now, a tight labor market along with stellar Q2 Gross Domestic Product (GDP) performance could consider one more interest rate hike from the Fed.

Meanwhile, the US Dollar Index (DXY) climbs above the crucial resistance of 102.40 amid negative market sentiment. S&P500 is expected to open on a negative note following bearish sentiment from overnight futures. US equities are expected to remain under pressure as Fitch downgraded the US economy amid concerns over rising fiscal spending.

Silver technical analysis

Silver price is maintaining a lower high formation on an hourly scale, which indicates that investors are capitalizing pullbacks as selling opportunities. The asset could deliver further downside if it drops below the horizontal support plotted from July 27 low around $24.00.

The 200-period Exponential Moving Average (EMA) at $24.50 is acting as a barricade for the Silver bulls.

Meanwhile, the Relative Strength Index (RSI) (14) slips into the bearish range of 20.00-40.00m indicating an activation of the downside momentum.

Silver hourly chart

-638265801401784578.png)

Economists at Rabobank are leaving their forecasts for USD/MXN unchanged. Peso is overvalued, it is overbought, but it can stay that way.

Overvalued, overbought but...

We would argue, that there is little reason to expect a significant sell-off in MXN in the coming month. There are a multitude of reasons to expect continued strength. But, at the same time, it is uncomfortable to suggest that a significantly overvalued currency will not just remain overvalued (which is our base case) but will in fact become even more so. This is the position we find ourselves in, however.

Despite these words, we are leaving our forecasts for USD/MXN unchanged. 16.80 by the end of Q3 and 17.60 by the end of Q4. The risk to our mind is skewed to the downside in the short-term, with the potential for USD/MXN to break through support at 16.70 and text 16.40, while the risk toward the end of the year we see skewed to the upside with the potential for USD/MXN to break 18 by year-end.

- EUR/USD adds to the weekly leg lower and revisits 1.0950.

- The weekly high at 1.1150 continues to cap the upside.

EUR/USD comes under intense selling pressure and flirts once again with weekly lows in the mid-1.0900s on Wednesday.

Considering the ongoing price action, spot could see its downside momentum accelerate and retest the weekly low of 1.0943 (July 28). The breakdown of this region could put a test of the 1.0910 zone, where the transitory 55-day and 100-day SMAs coincide, back on the radar.

Looking at the longer run, the positive view remains unchanged while above the 200-day SMA, today at 1.0733.

EUR/USD daily chart

The Pound continued to strengthen in July hitting fresh year-to-date highs against the US Dollar and Euro. Economists at MUFG Bank analyze GBP outlook.

Turning point has not yet been reached

We believe that the Pound’s recent strong rebound is starting to lose some upward momentum.

Evidence of much weaker UK growth in the 2H of this year and/or a faster-than-expected slowdown in inflation will be required to trigger a reversal of Pound gains.

EUR/GBP – Q3 2023 0.8550 Q4 2023 0.8650 Q1 2024 0.8850 Q2 2024 0.8900

GBP/USD – Q3 2023 1.2870 Q4 2023 1.2950 Q1 2024 1.2770 Q2 2024 1.2360

- DXY advances for the fifth straight session on Wednesday.

- The downside pressure should alleviate on a breakout of 102.50.

DXY extends the upside to new four-week peaks around 102.50, an area also coincident with the interim 55-day and 100-day SMAs.

The index appears poised to extend the ongoing multi-session recovery for the time being. Against that, the surpass of the weekly/monthly top of 102.50 (August 1) should prompt the index to rapidly challenge the temporary 55-day SMAs at 102.54.

Once the latter is cleared, it should alleviate the downside bias in the dollar and allow for extra gains to the next target at the July high of 103.57 (July 3), which appears underpinned by the proximity of the key 200-day SMA, today at 103.65.

Looking at the broader picture, while below the 200-day SMA the outlook for the index is expected to remain negative.

DXY daily chart

Fitch lowered the US credit rating to AA+ from AAA. Do downgrades matter? Economists at Rabobank analyze USD outlook.

The resilience of US growth this year is a positive factor

In past periods of stress regarding the US debt ceiling, treasuries have seen buying pressures on the back of safe-haven demand. A negative risk event generally triggers a positive USD response, almost irrespective of its source. This is related to Greenback’s use worldwide as an invoicing currency and its dominance in the global payments system.

While the USD has not shown much initial reaction to Fitch’s announcement, the news should draw attention back to the management of fiscal policies in the US.

The resilience of US growth this year is a positive factor. That said, growth is expected to slow this year and both the budget deficit and the debt/GDP ratios are expected to rise through 2023 and 2024. The Bloomberg survey forecasts the US budget deficit at 5.7% and 5.8% of GDP in 2023 and 2024 respectively from 5.4% in 2022. The survey also forecasts that US debt will stand at 97.3% of GDP this year and 99.8% next year. These numbers are notably higher than in the pre-pandemic years.

It is possible that over the medium-term the USD will be impacted more by the political reactions that the Fitch announcement generates, rather than by the announcement per se.

Economists at Société Générale analyze USD/BRL technical outlook.

Below 4.69; next potential support is at 4.61/4.59

USD/BRL broke through the lower limit of a multi-month range near 5.01 resulting in a steady decline. It has recently tested the lower band of a descending channel at 4.69.

An initial bounce is under way and revisit of 50-DMA near 4.86 can’t be ruled out. Lower limit of previous consolidation at 4.95/5.01 is an important resistance zone near term. Failure to overcome this could lead to continuation in the downtrend.

Below 4.69; next potential support is at last year's low of 4.61/4.59.

- Australian Dollar pierces new lows after the release of strong US labor data for July.

- ADP Employment Change rises by 324K, easily beating the 189K estimate.

- The data follows a run of weakness for the Aussie after a sour market mood turned investors risk averse.

The Australian Dollar (AUD) reaches new two-month lows against the US Dollar (USD) on Wednesday, after the release of US private payrolls data shows a larger-than-expected expansion of the workforce in July.

Data from the US’s largest payroll processor ADP, showed an unexpected rise of 324K jobs in July versus the 189K predicted. The data reinforces the view that the US labor market is rock solid and inflation is likely to remain stubbornly high. The Federal Reserve is more likely to maintain interest rates higher for longer if more people are earning, and higher interest rates are positive for the US Dollar as they attract greater foreign capital inflows.

Australia’s largest export Iron Ore is also in decline, further hitting the Australian Dollar, with Chinese Iron Ore Futures reaching a new low for July in the $108s.

AUD/USD trades in the 0.65s as the US session gets underway.

Australian Dollar news and market movers

- The Australian Dollar loses ground against the USD after ADP payroll data shows a greater-than-expected rise in new employees in July.

- US private sector added 324K new workers in July when only a 189K increase had been forecast by economists, although the figure was still below the 497K in June.

- A risk-off mood permeated markets on Tuesday, weighing on the Australian Dollar after weaker-than-expected US ISM Manufacturing PMIs for July and JOLTS Job Openings in June weighed on animal spirits.

- The market mood was not helped by data from China, showing business activity in the manufacturing sector fell into contractionary territory in July, with the Caixin Manufacturing PMI falling to 49.2 in July from 50.5 in June.

- The Australian Dollar was already on a weak footing after the RBA left the policy rate unchanged at 4.1% on Tuesday morning, against the market expectation for a 25 basis points hike. In the policy statement, the RBA explained that the decision to hold rates unchanged would provide them more time to assess the impact of policy tightening to date and the economic outlook.

- That said, they did not completely rule out the possibility of more rate hikes in the future, "Some further tightening of monetary policy may be required to ensure that inflation returns to target in a reasonable timeframe, but that will depend upon the data and the evolving assessment of risks," the RBA noted.

Australian Dollar technical analysis

AUD/USD is in a sideways trend on both the long and medium-term charts. The February high at 0.7158 is a key hurdle, which if vaulted, will alter the outlook to one that is more bullish longer term.

The 0.6458 low established in June is a key level for bears, which if breached decisively, would give the chart a more bearish overtone. Price is currently moving down nearer to this key low.

-638265776565483304.png)

Australian Dollar vs US Dollar: Weekly Chart

Price has now broken cleanly through the confluence of moving averages (MA) close to 0.6700, made up of most of the major SMAs – the 50-week, 50-day and 100-day. The breaching of this key support and resistance level is a bearish sign.

-638265777037404459.png)

Australian Dollar vs US Dollar: Daily Chart

It is possible price may have completed a Measured Move pattern or three wave ABC correction (see daily chart), in July. If so, there is a chance it may be about to start a short-term upcycle. Given how bearish price action is at the moment, however, the chances of this scenario unfolding are diminishing by the hour.

AUD/USD has now also broken below the 0.6600 June lows on an intraday basis, and a continuation down to the key May lows at 0.6460, is quite possible. A decisive break below them would open the way for a move down to 0.6170 and the 2022 lows.

Because the pair is in a sideways trend on the higher time-frame charts, the probabilities do not favor either bears or bulls overall – nor is the Relative Strength Index (RSI) providing much insight on either timeframe.

In technical terms, a ‘decisive break’ consists of a long daily candlestick, which pierces cleanly above or below the critical level in question and then closes near to the high or low of the day. It can also mean three up or down days in a row that break cleanly above or below the level, with the final day closing near its high or low and a decent distance away from the level.

- AUD/USD is expected to extend its downside below 0.6565 amid the upbeat US ADP employment report.

- The USD Index drives higher as the stellar addition of private payrolls would set a positive undertone for Fed policy.

- RBA Lowe kept doors open for more interest rates as inflation will take time to return to 2% amid the tight labor market.

The AUD/USD pair prepares to extend losses below the immediate support of 0.6565 as the United States Automatic Data Processing (ADP) reports that employment additions were higher than expectations. The US labor market witnessed an addition of fresh 324K private payrolls, significantly higher than the estimates of 189K but lower than the former release of 497K.

The US Dollar Index (DXY) delivers a breakout of the consolidation formed around 102.10 as upbeat labor market conditions have propelled hopes of one more interest rate hike from the Federal Reserve (Fed).

ADP Employment data set a positive undertone for the US Nonfarm Payrolls (NFP) data for July, which will be published on Friday at 12:30 GMT. According to the estimates, the economic data is seen at 200K, slightly lower than the former reading of 209K. The Unemployment Rate is expected to remain steady at 3.6%. Apart from the employment additions, investors will keenly focus on the Average Hourly Earnings.

Expectations state that labor earnings gained at a pace of 0.3% in July, lower than the former pace of 0.4%. The annual data is expected to decelerate to 4.2% against the former release of 4.4%.

On the Australian Dollar front, the Reserve Bank of Australia (RBA) kept interest rates unchanged at 4.1%. RBA Governor Philip Lowe kept doors open for more interest rates as inflation will take time to return to 2% amid a tight labor market. Over the inflation outlook, the central bank forecasted that inflation will return to 2-3% by late 2025.

- The US Dollar outperforms its rivals as markets adopt a cautious stance.

- The US Dollar Index stays in positive territory above 102.00 following Tuesday's choppy action.

- USD benefits from souring market mood after Fitch downgraded US credit rating.

The US Dollar gathered strength against its rivals after Tuesday's indecisive trading. The USD Index – which tracks the USD's valuation against a basket of six major currencies – held above 102.00 despite the pullback seen in the American session on Tuesday and stretched higher on Wednesday.

Global rating agency Fitch announced late Tuesday that it downgraded the US government's credit rating to AA+ from AAA, citing anticipated fiscal deterioration over the next three years and a high and growing general government debt burden. This development caused market participants to stay away from risk-sensitive assets, allowing the USD to find demand as a safe haven.

The US private sector employment rose by 324,000 in July, the data published by Automatic Data Processing (ADP) showed on Wednesday. This reading surpassed the market expectation for an increase of 189,000 and provided further support to the USD. June's figure was revised lower from 497,000 (the highest since February 2022) to 455,000.

“The economy is doing better than expected and a healthy labor market continues to support household spending,” said Nela Richardson, chief economist, ADP. “We continue to see a slowdown in pay growth without broad-based job loss.”

Daily digest market movers: US Dollar benefits from risk aversion

- 10-year US Treasury bond yield holds steady above 4% following Tuesday's upsurge.

- The number of job openings on the last business day of June stood at 9.58 million, the US Bureau of Labor Statistics (BLS) reported in the Job Openings and Labor Turnover Survey (JOLTS) on Tuesday. This reading followed 9.61 million openings in May and came in slightly below the market expectation of 9.62 million.

- US ISM Manufacturing PMI imrpoved modestly to 46.4 in July from 46 in June. This reading came in below the market expectation of 46.8 and showed an ongoing contraction in the manufacturing sector's business activity.

- The Employment component of the ISM PMI survey declined to 44.4 from 48.1.

- “Banks reported that, on balance, levels of standards are currently on the tighter end of the range for all loan categories. Compared with the July 2022 survey, banks reported tighter levels of standards in every loan category," the Fed said in the July 2023 Senior Loan Officer Opinion Survey on Bank Lending Practices (SLOOS).

- The ISM reported on Monday that the Chicago PMI improved to 42.8 in July from 41.5 in June.

- The Federal Reserve Bank of Dallas' Texas Manufacturing Survey revealed that the headline Manufacturing Business Index edged higher to -20 in July from -23.2 in June.

- Inflation in the US, as measured by the change in Personal Consumption Expenditures (PCE) Price Index, fell to 3% on a yearly basis in June from 3.8% in May, the US Bureau of Economic Analysis reported on Friday. This reading came in below the market expectation of 3.1%.

- Core PCE Price Index, the Federal Reserve's preferred gauge of inflation, arrived at 4.1% on a yearly basis, down from 4.6% in May and below the market forecast of 4.2%. Further details of the publication revealed that Personal Income and Personal Spending increased 0.3% and 0.5% on a monthly basis, respectively.

- In an interview with CBS over the weekend, Minneapolis Federal Reserve Bank President Neel Kashkari said that he was not sure whether the Fed was done raising rates. Commenting on the jobs markets, Kashkari noted that it would not surprise him to see the unemployment rate tick up slightly.

- The Fed raised its policy rate by 25 basis points (bps) to the range of 5.25%-5.5% following the July policy meeting as expected. In the post-meeting press conference, Fed Chairman Jerome Powell refrained from confirming another rate hike this year and said that every policy meeting will be live. "If we see inflation coming down credibly, we can move down to a neutral level and then below neutral at some point," Powell told reporters, noting that the policy was already restrictive.

Technical analysis: US Dollar Index trades near key resistance