- Analiza

- Novosti i instrumenti

- Vesti sa tržišta

Forex-novosti i prognoze od 03-06-2024

Japan's Monetary Base, or the amount of currency being supplied by the Bank of Japan (BoJ) as measured by combining all notes and coins in circulation in addition to current account balances, eased to 0.9% for the year ended in May as Japanese markets struggle to find uses for additional cash supplied by the BoJ. Investors broadly expected May's annualized Monetary Base to expand by 2.2% YoY, a slight uptick from the previous period's 2.1%.

Market reaction

USD/JPY is battling the 156.00 handle in the early hours of the Pacific market session. The pair is down from the week's early bids near 157.40 and testing into near-term lows as the Greenback falls in a broad-market recovery in risk appetite.

USD/JPY hourly chart

About Japanese Monetary Base

The Monetary Base released by the Bank of Japan is the "Currency Supplied by the BoJ" including all the JPY in circulation, encompassing notes and coins as well as money held in bank accounts. It is considered as an important indicator of inflation, as monetary expansion adds pressure to the exchange rates. An acceleration of monetary base is considered as positive for the JPY, whereas a decline is seen as negative.

- NZD/USD trades flat around 0.6190 in Tuesday’s early Asian session.

- The US Manufacturing PMI dropped to 48.7 in May from 49.2 in April, weaker than expected.

- The improving Chinese Caixin Manufacturing PMI data and the hawkish stance from the RBNZ support the Kiwi.

The NZD/USD pair consolidates its gains near 0.6190 on Tuesday during the early Asian session. The worse-than-expected US ISM Manufacturing PMI data has dragged the Greenback lower and supported the pair. Investors await the US ISM Services PMI, which is due on Wednesday. On Friday, US employment data, including Nonfarm Payrolls, Unemployment Rate, and Average Hourly Earnings will be in the spotlight.

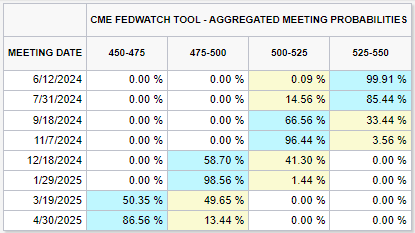

The US manufacturing sector had a second consecutive month of contraction in May and the 18th time in the last 19 months, the Institute for Supply Management (ISM) showed on Monday. The US Manufacturing PMI came in weaker than expected, dropping to 48.7 in May from 49.2 in April. Traders raise their bets on the US Federal Reserve (Fed) rate cuts this year, seeing nearly a 53% odds of a rate cut in September, up from 49% before the inflation report, according to the CME FedWatch tool.

On the Kiwi front, the encouraging Chinese Caixin Manufacturing PMI for May lifted the China-proxy New Zealand Dollar (NZD) as New Zealand is one of China's leading trading partners. Apart from this, the hawkish stance from the Reserve Bank of New Zealand (RBNZ) further boosted the NZD, as RBNZ Deputy Governor Christian Hawkesby said in recent weeks that cutting interest rates is not part of the near-term discussion and the central bank needs to maintain rates for longer to ensure inflation returns to the 1-3% target range.

- EUR/USD vaulted into fresh near-term highs to kick off the new trading week.

- Markets broadly sold off the Greenback after worse-than-expected PMIs.

- Thursday’s ECB rate call, Friday’s US NFP labor print loom ahead.

EUR/USD kicked off another Nonfarm Payrolls (NFP) week looking for higher ground, vaulting the Euro to its highest bids against the US Dollar in almost ten weeks, clipping over the 1.0900 handle. Monday’s one-sided trading leaves the Fiber overextended in bullish chart territory, and it will be several days until meaningful data hits newsfeeds.

Tuesday will carry the week’s momentum into a moderately thin economic calendar. Final German unemployment figures for May are due early during European market hours, and Tuesday’s US market session will follow up with US Factory Orders and JOLTS Job Openings.

Germany’s Unemployment Change in May is expected to hold steady at 10K MoM, with the seasonally-adjusted Unemployment Rate broadly expected to hold flat at 5.9%. On the US side, Tuesday’s upcoming MoM Factory Orders in April are forecast to ease to 0.6% from 1.6%, while JOLTS Job Openings are expected to ease slightly to 8.34 million MoM in April compared to the previous 8.488 million.

Firm early-week bidding set to clash with ECB rate cuts and NFP jobs data

Thursday’s ECB rate call will be closely watched by Fiber traders. The ECB is broadly expected to trim its Main Refinancing Operations Rate by 25 basis points to 4.25%, and with a first rate cut all but priced in, investors will be scrambling to take a look at the ECB’s Monetary Policy Report for signals about when a follow-up rate cut will be forthcoming.

Friday will close out an otherwise mild trading week with a fresh print of US NFP labor data. The US is expected to have added 190K new jobs through May, a tick higher than the previous month’s 175K. Investors desperate for rate cuts, which are currently pricing in a first rate trim from the Federal Reserve (Fed) in November, will be looking for downside revisions to key employment figures in order to knock the Fed into a faster pace of rate cuts.

EUR/USD technical outlook

EUR/USD drove into fresh ten-week highs on Monday, crossing 1.0900 and testing 1.0910 for the first time since late March. The pair has pushed deep into the north side of the 200-day Exponential Moving Average (EMA) at 1.0804, and overbought conditions could set into the pair and drag the Fiber back into consolidation territory.

A long-running pattern of lower highs from 2024’s peak bids near 1.1140 is weighing on continued bullish pressure, though the pair has broken through a descending trendline and could make a leg higher after a brief pullback to the 1.0850-1.0800 region.

EUR/USD hourly chart

EUR/USD daily chart

- AUD/USD rises to 0.6693, buoyed by weaker US business activity data and falling Treasury yields.

- ISM Manufacturing PMI dips to 48.7, signaling contraction, while S&P Global PMI shows slight recovery.

- Upcoming US Nonfarm Payrolls report and Australian economic data could influence AUD/USD direction.

The Australian Dollar registered gains of 0.55% versus the Greenback on Monday and opened Asian Tuesday’s session with renewed strength amid falling US yields. Expectations that the Federal Reserve would ease policy in 2024 were fueled by a weaker-than-expected US business activity report. The AUD/USD trades at 0.6693, virtually unchanged.

Aussie Dollar up as US yields drop and undermine the buck

US data was the driver of the day. The Institute for Supply Management (ISM) reported that business activity in the manufacturing sector slowed in May for the third straight month. The ISM Manufacturing PMI decreased from 49.2 to 48.7 for the second straight reading at contractionary ground and below the consensus of 49.6.

Other data from S&P Global highlighted a recovery for the same sector, with the Manufacturing PMI expanding from 50 to 51.3, which is above estimates of 50.9.

The AUD/USD advanced due to overall US Dollar weakness, undermined by lower US Treasury yields. The US 10-year Treasury bond yields plunged eleven basis points to 4.392%, while the US Dollar Index (DXY) dove 0.5% to 104.07. However, US data ahead could change the pair's direction as the release of the US Nonfarm Payrolls report looms.

Fed funds rate futures estimate just 32 basis points of interest rate cuts in 2024, according to data from the Chicago Board of Trade (CBOT).

On Australia’s front, the schedule will feature Company Gross Profits and Business Inventories for the first quarter of 2024, on QoQ figures, along with the Current Account for the same period and the final Retail Sales report for April. month.

AUD/USD Price Analysis: Technical outlook

From a technical perspective, a ‘double bottom’ chart pattern looms, which could pave the way to test 0.6750 and beyond. However, to confirm its validity, buyers must crack the latest cycle high of 0.6714 before reaching 0.6750 and the 0.6800 figure. Otherwise, if sellers moved in and kept prices below 0.6700, look for a retest of the 0.6600 figure.

- GBP/USD gains ground near 1.2810 amid the weaker USD on Tuesday.

- The US ISM Manufacturing PMI declined to 48.7 in May from 49.2 in April, worse than expected.

- Traders expect that the BoE could start cutting interest rates from August meeting.

The GBP/USD pair attracts some buyers around 1.2810 during the early Asian session on Tuesday. The uptick of the major pair near multi-week highs is bolstered by the softer US dollar (USD) after the weaker-than-expected US Manufacturing PMI data. Later on Tuesday, the US Factory Orders and JOLTs Job Openings will be released.

The manufacturing sector in the United States contracted at an accelerating pace in May, the Institute for Supply Management (ISM) reported on Monday. The US ISM Manufacturing PMI dropped to 48.7 in May from 49.2 in April, below the market consensus of 49.6. The Greenback faced some renewed selling pressure in response to the downbeat data.

Ahead of the blackout period for the FOMC, Minneapolis Fed president Neel Kashkari noted that interest rates need to stay on hold for an “extended” time, adding that lowering borrowing costs before inflation was under control would put the foundations of US prosperity at risk. Nonetheless, the recent cooler US PCE inflation data and weaker US Manufacturing PMI have triggered the expectation that the US Federal Reserve (Fed) will cut the interest rate this year. Traders are now pricing in nearly a 53% possibility of a Fed rate cut in September, up from 49% before the inflation report.

On the other hand, the markets anticipate that the Bank of England (BoE) could start cutting interest rates from the August meeting as UK annual headline inflation eased significantly in April. However, the BoE policymakers remain worried about slower progress in the service disinflation process. In the absence of top-tier economic data releases from the UK, the USD price dynamics will continue to play a key role in influencing the GBP/USD this week.

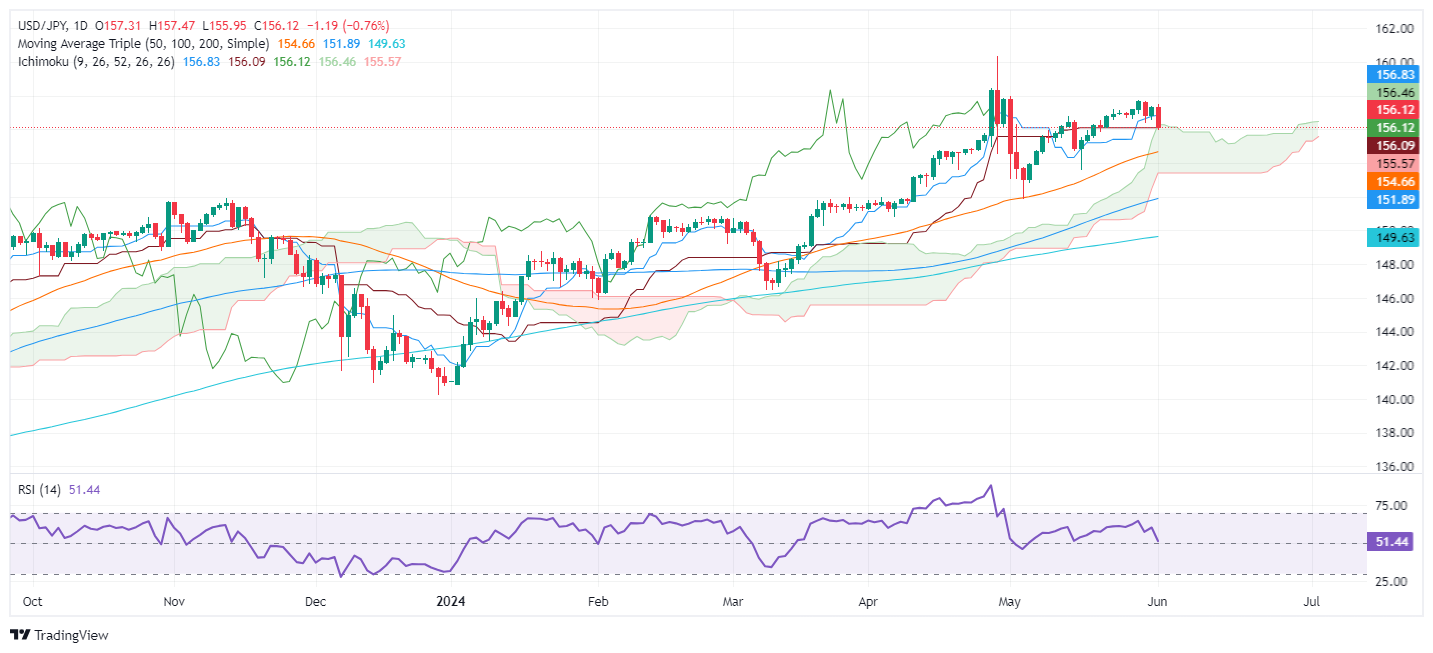

- USD/JPY retreats as it forms a bearish engulfing candle chart pattern.

- Technical outlook: USD/JPY drops below Ichimoku Cloud top at 155.95, hinting at potential further declines.

- Key support levels: Tenkan-Sen at 154.92, 50-DMA at 154.74, and trendline at 154.20; resistance at Kumo top 156.15/20 and May 29 high of 157.71.

The USD/JPY retreated more than 0.70% on Monday following softer-than-expected business activity data in the United States (US). That, along with last Friday’s inflation report, the Fed’s Core PCE, reignited speculation that the US central bank could slash rates toward the end of the year. The pair trades at 156.14.

USD/JPY Price Analysis: Technical outlook

From a daily chart perspective, the USD/JPY failed to pierce the 157.50 resistance level and dived below the 157.00 figure, exacerbating a drop below the top of the Ichimoku Cloud (Kumo) at around 155.95, opening the door for further losses.

Even though momentum favors buyers, as depicted by the Relative Strength Index (RSI), it has turned flat close to the 50 midlines, about to enter bearish territory.

In the short term, the USD/JPY is neutral to downward biased. The first support would be the Tenkan-Sen at 154.92, followed by the 50-day moving average (DMA) at 154.74. Once cleared, the next stop would be an upslope support trendline at 154.20 before testing the bottom of the Kumo at 153.30/40.

Conversely, if USD/JPY climbs above the top of the Kumo at around 156.15/20, that would sponsor an uptick toward the May 29 high at 157.71.

USD/JPY Price Action – Daily Chart

- The daily RSI has shifted downwards and with the MACD showing increasing red bars pointing to a slowdown in upward momentum.

- On the hourly chart, indicators suggest moderate bullish momentum, supported by an increasing RSI and green bars in the MACD.

- The 20-day SMA at 169.22 serves as a critical support level for the pair to consolidate.

In Monday's session, a weak Yen against its rivals caused the EUR/JPY pair to slip to 170.30. Despite this slip, the pair's position remains solid above the key support level of the 20-day SMA at 169.22. However, as the pair currently hovers in overbought territory, the upside appears limited.

The daily Relative Strength Index (RSI) showed a reduction to 61, suggesting a potential slowdown in the pair's upward momentum. The daily MACD, with increasing red bars, agrees with this outlook..

EUR/JPY daily chart

On the hourly chart, the RSI suggests a moderate bullish momentum, standing at 51, marking a positive shift in the session. The hourly MACD, showing rising green bars, supports this short-term bullish sentiment. Nevertheless, because the pair is hovering in the overbought zone, the upward move may be short-lived.

EUR/JPY hourly chart

Meanwhile, the pair continues to trade above the significant support level of the 20-day Simple Moving Average (SMA). Should the position fall below this support level, sellers may meet further resistance at the 100 and 200-day SMAs, providing a safety barrier at around 164.00 and 161.00. As long as these support levels are defended, the overall bullish outlook remains intact, despite the possibility of consolidation. On the upside, the buyers must recapture the 167.00 area to continue moving upwards.

- GBP/JPY cycles 200.00 in rough churn as Yen struggles to hold steady.

- GBP and JPY settle in for a quiet week on the data docket.

- UK Retail Sales and Japanese wages both expected to rebound this week.

GBP/JPY is cycling the 200.00 major handle heading into a quiet week for both currencies, with the economic data calendar almost entirely populated with low-tier data releases through the majority of the trading week. UK BRC Like-For-Like Retail Sales are expected to recover ground in May, while Japanese Labor Cash Earnings are expected to accelerate for the year ended in April.

UK YoY BRC Retail Sales are expected to rebound to 1.2% through May, a healthy recovery but still underperforming the previous period’s -4.4% decline. April’s YoY Retail Sales figures had tumbled to its lowest level since December of 2019, and investors are hoping that May’s annualized figure is able to recover ground. UK BRC Retail Sales are slated to print early Tuesday.

Japanese Labor Cash Earnings are expected to accelerate to 1.7% for the year ended in April, forecast to rise to 1.7% from the previous period’s 0.6% increase. Wage growth remains a key driver in Bank of Japan (BoJ) policymaking as the Japanese central bank remains fearful of Japanese inflation slumping to near-zero growth figures. A firm rebound in wage growth will help bolster the BoJ’s confidence in closing the differential between Japanese monetary policy and other major central banks around the world.

GBP/JPY technical outlook

GBP/JPY has struggled in a rough range after hitting multi-decade highs at 200.75 in May, waffling between bids north of 200.00 and a near-term floor just below 199.00. The Guppy is treading water on the high side, but bulls finally appear to have run out of gas after pushing the pair into higher closes for five consecutive months.

GBP/JPY hourly chart

GBP/JPY daily chart

- Daily chart indicators suggest a downward trend; the decline in RSI is marking a downward momentum

- Signs of bullish exhaustion after the recent gains have strengthened the consolidation outlook.

- The pair currently targets support around the 103.70 area, which aligns with the 20-day SMA.

In Monday's trading session, the AUD/JPY pair slipped to the 104.35 region due to the resumption of a downward momentum. The pair's upward trajectory appears increasingly exhausted, and a consolidation phase seems more probable moving forward.

As per the daily chart, the RSI has descended to 59 from the previous session's reading of 65, suggesting a continued downward momentum. Along with this, the MACD prints rising red bars, indicating an increase in the selling traction

AUD/JPY daily chart

The 20-day SMA has now established a sturdy support base around the 103.70 region, which could potentially halt the ongoing losses. Any breakthrough below the 20-day SMA could prompt a short-term bearish atmosphere.

In the case of a further decline, the 100 and 200-day SMA might act as barriers to cushion losses. On the other hand, the bulls might face resistance in trying to push the pair back above the 105.00 mark. If the pair fails to break through these integral points, traders might witness the pair entering into a consolidation phase.

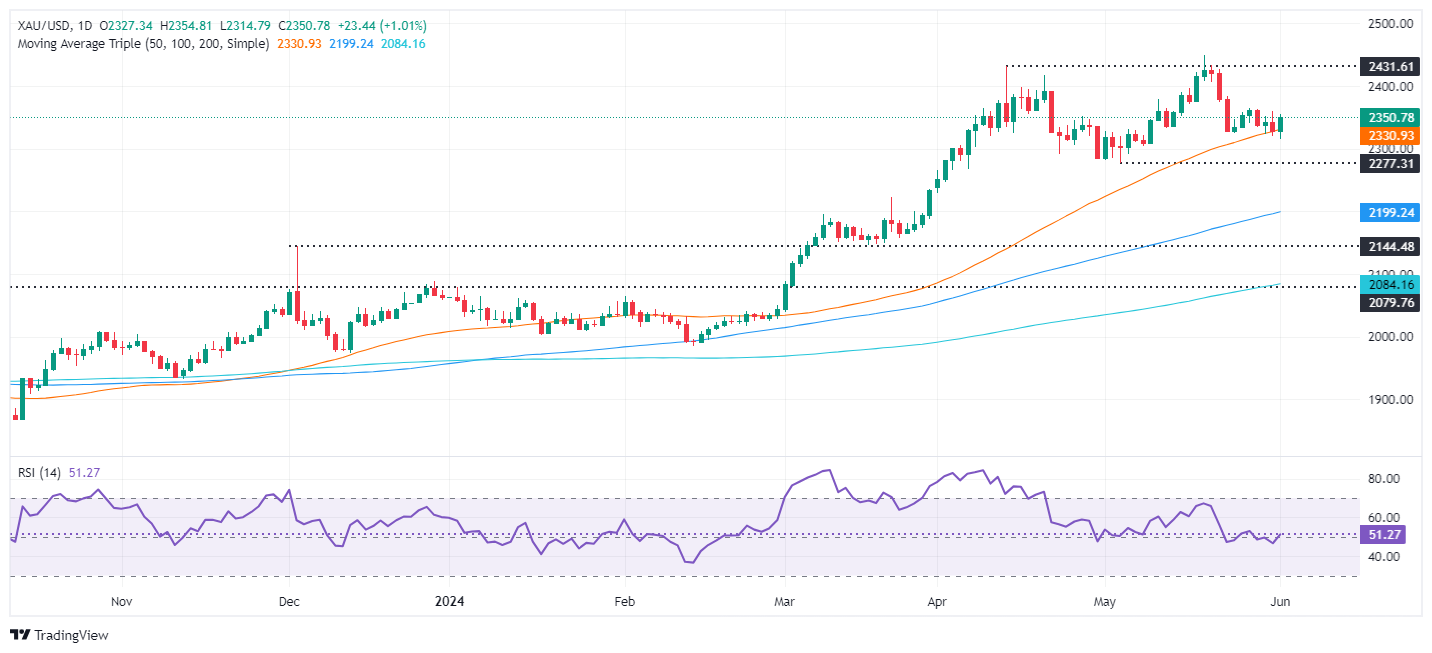

- Gold climbs over 0.80% after hitting a daily low of $2,314.

- Mixed US economic data and stable PCE inflation raise hopes for Fed rate cuts.

- US Treasury yields drop, extending Greenback’s losses for the third consecutive day.

Gold climbed more than 0.80% after US Treasury bond yields dropped following the release of mixed data from the United States (US), increasing hopes that the US Federal Reserve might ease policy. That, along with a risk-off impulse, kept the yellow metal climbing after hitting a daily low of $2,314 and trading at $2,345.

Last week, the Fed’s preferred inflation gauge, the US Core Personal Consumption Expenditure Price Index (PCE), stabilized, augmenting hopes for rate cuts. Meanwhile, business activity was mixed, according to reports from S&P Global and the Institute for Supply Management (ISM) in May, with the latter contracting for the second consecutive month.

Consequently, US Treasury bond yields dropped, and the Greenback extended its losses to three straight days. The US 10-year Treasury bond yields plunged eleven basis points to 4.392%. The US Dollar Index (DXY), which tracks the performance against a basket of six currencies, fell 0.5% to 104.07.

On the geopolitics front, Hamas accepted US President Joe Biden's cease-fire proposal for Gaza. However, Israeli President Benjamin Netanyahu rejected the idea and emphasized Israel’s conditions for ending the war.

Daily Digest Market Movers: Gold price rises as US Treasury yields retreat from multi-week high

- Gold prices advance after bouncing off the 50-day Simple Moving Average (SMA) at $2,324.

- US S&P Global revealed that Manufacturing PMI for May increased from 50 to 51.3, exceeding estimates of 50.9

- The ISM Manufacturing PMI contracted further, from 49.2 to 48.7.

- Traders are currently pricing about a 59% chance of a rate cut, according to the CME FedWatch Tool.

- The US economic docket during the week will feature Factory Orders, JOLTS Job openings, and ADP Employment Change ahead of Friday’s Nonfarm Payrolls.

- Fed funds rate futures estimate just 32 basis points of interest rate cuts in 2024, according to data provided by the Chicago Board of Trade (CBOT).

Technical analysis: Gold price climbs and hovers at $2,350

Gold price uptrend remains intact after bouncing off the 50-day Simple Moving Average (SMA) at $2,331. Momentum shifted in favor of the buyers, as the Relative Strength Index (RSI) remained above the 50 midline, opening the door for further Gold’s upside.

Further gains lie ahead if XAU/USD buyers reclaim the $2,400 level, followed by the year-to-date high of $2,450 and, subsequently, the $2,500 mark.

Conversely, if XAU/USD falls below the 50-day Simple Moving Average (SMA) at $2,331, that could pave the way to challenge the May 8 low of $2,303, followed by the May 3 cycle low of $2,277.

Gold FAQs

Gold has played a key role in human’s history as it has been widely used as a store of value and medium of exchange. Currently, apart from its shine and usage for jewelry, the precious metal is widely seen as a safe-haven asset, meaning that it is considered a good investment during turbulent times. Gold is also widely seen as a hedge against inflation and against depreciating currencies as it doesn’t rely on any specific issuer or government.

Central banks are the biggest Gold holders. In their aim to support their currencies in turbulent times, central banks tend to diversify their reserves and buy Gold to improve the perceived strength of the economy and the currency. High Gold reserves can be a source of trust for a country’s solvency. Central banks added 1,136 tonnes of Gold worth around $70 billion to their reserves in 2022, according to data from the World Gold Council. This is the highest yearly purchase since records began. Central banks from emerging economies such as China, India and Turkey are quickly increasing their Gold reserves.

Gold has an inverse correlation with the US Dollar and US Treasuries, which are both major reserve and safe-haven assets. When the Dollar depreciates, Gold tends to rise, enabling investors and central banks to diversify their assets in turbulent times. Gold is also inversely correlated with risk assets. A rally in the stock market tends to weaken Gold price, while sell-offs in riskier markets tend to favor the precious metal.

The price can move due to a wide range of factors. Geopolitical instability or fears of a deep recession can quickly make Gold price escalate due to its safe-haven status. As a yield-less asset, Gold tends to rise with lower interest rates, while higher cost of money usually weighs down on the yellow metal. Still, most moves depend on how the US Dollar (USD) behaves as the asset is priced in dollars (XAU/USD). A strong Dollar tends to keep the price of Gold controlled, whereas a weaker Dollar is likely to push Gold prices up.

- Negative momentum nudges the NZD/JPY pair into a slight retreat, with consolidation continuing to dominate the trend.

- The sellers face a considerable barrier at the 96.30 area.

- The buying momentum continues to be limited.

During Monday's session, the NZD/JPY pair experienced a slight retreat as the sellers tried pushing past a strong resistance at the 96.30 area. However, the charm offensive from the buyers wasn't entirely diminished, holding the pair in a protracted consolidation phase over the course of the day.

Though still well within positive territory, the Relative Strength Index (RSI) has dropped to 67, from 71. This drop, mild in nature, indicates a reduction in the momentum that characterized the previous session's overbought situation However, on Monday the index managed to jump back near the 70 threshold suggesting that there is still more toom to correct. Concurrently, the Moving Average Convergence Divergence (MACD) continues to register decreasing green bars, suggesting a decline in buying momentum. The combination of these factors implies the potential for a continued period of consolidation, rather than a reversal of the uptrend seen recently.

NZD/JPY daily chart

This retreat is by no means a synonym for reversal. The outlook still remains positive, and the NZD/JPY pair continues to rest well above a healthy support level at 95.50. For the balance to tip in favor of the sellers, they would need to crack this support and break below the 20-day Simple Moving Average (SMA) at 95.20, a level that has provided reliable support for buyers since the beginning of May. Until then, the current pattern is likely to be viewed as corrective and part of the ongoing consolidation phase.

- WTI backslid to $74.00 per barrel after OPEC+ failed to bolster Crude trader hopes.

- Voluntary production cuts are slated to be phased out beginning in October.

- OPEC voluntary cuts have kept 2.2 million bpd off the market since 2022.

Crude Oil prices tumbled on Monday after an update on voluntary production cuts didn’t go how energy traders had hoped last week. The Organization of the Petroleum Exporting Countries (OPEC) and its extended network of non-member allies, OPEC+, announced the beginning of a phase-out of long-running production caps. The phase-out is slated to begin in October.

OPEC+ has been participating in voluntary Crude Oil production cuts that have kept 2.2 million barrels per day off the markets in an attempt to bolster global barrel prices in the face of global Crude Oil output that has grown to outpace demand. However, key members of OPEC+ who rely on selling Crude Oil in order to balance their government budgets have balked at the idea of continuing to support global prices at the expense of their solvency, and are set to begin phasing out currently-standing production limits sometime in October. OPEC+ stipulated that ending production limits will be data-dependent heading closer to October, but energy traders promptly sold off Crude Oil as barrels slated for year-end delivery become an unappealing bet.

US Crude Oil traders will be looking ahead to weekly updates on barrel counts from the American Petroleum Insitute (API) and the Energy Information Administration (EIA), due on Tuesday and Wednesday, respectively. Last week’s updates showed a sharp pullback in Crude Oil supplies, but inventories in upstream refined Crude Oil products spiked after a widely-expected uptick in US Crude Oil demand at the beginning of the Memorial Day driving season failed to materialize, leaving refineries with far more inventory than expected.

WTI technical outlook

WTI tumbled to its lowest prices since February, extending a bearish slide into the $74.00 per barrel handle and declining 8% from last week’s peak near $80.40 per barrel. Intraday short pressure cleanly snapped a technical barrier at $77.00, and a long-standing demand zone from $77.00 to $76.00 could rotate to form a heavy supply zone following any profit-taking from rebound bets.

US Crude Oil is poised for its single worst day in 2024, in the red nearly 4% from the day’s opening bids near $77.00 and testing into lows last set during the first week of February. WTI is down 15% from 2024’s peaks near $87.00.

WTI hourly chart

WTI daily chart

The loss of impetus in the US manufacturing sector sparked a deeper pullback in the Greenback and supported further the recovery of the risk-associated assets at the beginning of a week ruled by the ECB event and US Nonfarm Payrolls.

Here is what you need to know on Tuesday, June 4:

The USD Index (DXY) dropped markedly and flirted with three-week lows near the 104.00 neighbourhood. On June 4, Factory Orders take centre stage seconded by the JOLTs Job Openings and the RCM/TIPP Economic Optimism Index.

EUR/USD advanced for the third session in a row and challenged the key 1.0900 barrier amidst generalized Dollar weakness. The release of Germany’s labour market report and EMU’s Consumer Inflation Expectations will be at the centre of the debate on the domestic docket on June 4.

GBP/USD advanced to just pips away from the key 1.2800 hurdle, or multi-week highs, on Monday. The BRC Retail Sales Monitor is expected across the Channel on June 4.

The weaker Dollar and diminishing US yields prompted USD/JPY to recede to multi-session lows in the sub-156.00 region at the beginning of the week. In Japan, a JGB 10-year Auction is only due on June 4.

The increasing selling pressure in the Greenback motivated AUD/USD to advance to the proximity of the 0.6700 mark. On June 4, Business Inventories, Current Account and final Retail Sales are all due in Oz.

WTI prices receded for the third consecutive week and broke below the $77.00 mark per barrel on Monday, as traders digested the bearish tone from the OPEC+ meeting on Sunday.

Gold prices charted a strong advance to the $2,350 region on the back of the intense sell-off in the Dollar and declining US yields across the curve. By the same token, Silver followed suit and reversed three consecutive sessions of losses.

- On Monday, the AUD/NZD dipped below key technical levels, with the 100 and 200-day SMAs breached.

- Current focus is on GDP data from Australia, expected to remain steady.

- New Zealand’s manufacturing activity Q1 data on Friday will be closely watched.

The AUD/NZD echoed a bearish technical outlook on Monday, falling below key levels towards 1.0805 as markets await mid-tier data from both nations on a quiet economic schedule at the beginning of the week.

In Australia, markets will anticipate Wednesday's Gross Domestic Product (GDP) data. A steady growth of 0.2% QoQ is expected, while a 1.2% YoY rate is projected, a slight dip compared to the Q4 YoY rate of 1.5%. That being said, the AUD’s losses may be limited, thanks to the strong Australian Q1 CPI inflation data and another robust April reading, which hints at the Reserve Bank of Australia (RBA) being one of the last G10 central banks to cut rates in this cycle.

On the other hand, New Zealand will focus on releasing its Q1 manufacturing activity data on Friday. Should the manufacturing output reflect the same upward trend, it might further slow the Reserve Bank of New Zealand’s RBNZ's rate cuts. The market now forecasts a 75% probability of the first cut happening as late as November.

AUD/NZD technical analysis

Technical indicators have turned bearish. On Monday, sellers oversaw the breaching of the 100 and 200-day Simple Moving Averages (SMAs). The RSI heads towards the oversold territory, echoing a similar sentiment, while the MACD histogram continues to confirm this downward momentum with its persistent formation of red bars.

Despite the bearish patterns unfolding, the focus will be whether the downward trend can be sustained or if there will be an upward correction as markets continue to assess the upcoming economic data releases.

AUD/NZD daily chart

- Dow Jones backslides as investors balk at softening US data.

- Markets have shifted to bets of a November Fed rate cut.

- Monday kicks off NFP week with a sharp pullback in equities.

The Dow Jones Industrial Average (DJIA) fell around 300 points on Monday after investors took a backstep after US ISM Manufacturing Purchasing Managers Index (PMI) figures unexpectedly declined in May. Softening US data knocked risk appetite lower as markets rethink their outlook on the US economy.

Despite an uptick in May’s S&P Global Manufacturing PMI, which rose to 51.3 compared to the expected flat hold at 50.9, investors are balking after the ISM Manufacturing PMI for the same period eased lower. May’s ISM Manufacturing PMI eased back to 48.7 from the previous month’s 49.2, falling away from the market forecast increase to 49.6.

According to the CME’s FedWatch Tool, rate markets have fully priced in a first rate cut from the Federal Reserve (Fed) in November, with interest rate traders seeing over 96% odds of an initial 25-basis-point decline in the Fed Funds Rate by the Federal Open Market Committee’s (FOMC) November rate decision.

Dow Jones news

The Dow Jones initially plunged 400 points in early Monday trading, recovering slightly to -300 points on the day as investors try to recover their footing. Around two-thirds of the DJIA’s constituent equities are in the red on Monday, with losses lead by Chevron Corp. (CVX) which fell -3.35% to $156.71 per share. CVX is closely followed by Dow Inc. (DOW), which fell -3% to %55.91 per share on Monday.

Boeing Co. (BA) rebounded 2.34% on Monday, climbing to $181.91 per share. Merch & Co Inc. (MRK) followed closely behind, gaining 1.85% and rising to $127.85 per share.

Dow Jones technical outlook

Monday’s pullback chewed throw a significant portion of last Friday’s much-needed rebound, keeping the Dow Jones pinned below 39,000.00. The major equity index is still down over 4% from record highs set just above 40,000.00.

The Dow Jones is on pace to close down once more on Monday, and the index’s pullback has seen the DJIA close in the red for all but three of the last ten consecutive trading sessions. The Dow Jones still remains firmly in bull territory, but bids are edging closer to the 200-day Exponential Moving Average (EMA) at 37,247.44.

Dow Jones five minute chart

Dow Jones daily chart

Dow Jones FAQs

The Dow Jones Industrial Average, one of the oldest stock market indices in the world, is compiled of the 30 most traded stocks in the US. The index is price-weighted rather than weighted by capitalization. It is calculated by summing the prices of the constituent stocks and dividing them by a factor, currently 0.152. The index was founded by Charles Dow, who also founded the Wall Street Journal. In later years it has been criticized for not being broadly representative enough because it only tracks 30 conglomerates, unlike broader indices such as the S&P 500.

Many different factors drive the Dow Jones Industrial Average (DJIA). The aggregate performance of the component companies revealed in quarterly company earnings reports is the main one. US and global macroeconomic data also contributes as it impacts on investor sentiment. The level of interest rates, set by the Federal Reserve (Fed), also influences the DJIA as it affects the cost of credit, on which many corporations are heavily reliant. Therefore, inflation can be a major driver as well as other metrics which impact the Fed decisions.

Dow Theory is a method for identifying the primary trend of the stock market developed by Charles Dow. A key step is to compare the direction of the Dow Jones Industrial Average (DJIA) and the Dow Jones Transportation Average (DJTA) and only follow trends where both are moving in the same direction. Volume is a confirmatory criteria. The theory uses elements of peak and trough analysis. Dow’s theory posits three trend phases: accumulation, when smart money starts buying or selling; public participation, when the wider public joins in; and distribution, when the smart money exits.

There are a number of ways to trade the DJIA. One is to use ETFs which allow investors to trade the DJIA as a single security, rather than having to buy shares in all 30 constituent companies. A leading example is the SPDR Dow Jones Industrial Average ETF (DIA). DJIA futures contracts enable traders to speculate on the future value of the index and Options provide the right, but not the obligation, to buy or sell the index at a predetermined price in the future. Mutual funds enable investors to buy a share of a diversified portfolio of DJIA stocks thus providing exposure to the overall index.

- Mexican Peso falls sharply after Dr. Claudia Sheinbaum’s victory and Morena’s majority in Congress.

- Concerns rise over potential constitutional changes and market stability, impacting investor sentiment toward the Peso.

- Sheinbaum pledges to maintain financial discipline and Bank of Mexico autonomy, but market remains wary.

The Mexican Peso plunges against the US Dollar during the North American session following Dr. Claudia Sheinbaum’s overwhelming victory in Mexico’s presidential election. Additionally, her party, Morena, won the majority of the Mexican Congress, opening the door to change the Mexican Constitution, which was seen by investors as a threat to the status quo. The USD/MXN trades at 17.66, with more than 4% losses.

The Mexican Peso began its landslide after the Instituto Nacional Electoral (INE) revealed Sheinbaum’s party, Morena, would have the majority in both houses of the legislature. This opens the door to making structural changes that involve reforming the judicial system, which could be greatly influenced by the president.

Following the INE announcement, Sheinbaum compromised to continue the current plant from President Andres Manuel Lopez Obrador’s (AMLO) government. She pledged to maintain financial discipline and emphasized the autonomy of the Bank of Mexico.

Sheinbaum added, “There wouldn’t be real increases to fuels or electricity,” populist promises previously made by AMLO.

Analysts via Reuters commented that a Morena-led congress could be reluctant to “approve the necessary reforms to adopt the measures required to attract investment,” which could leverage the nearshoring opportunity, said Alberto Ramos of Goldman Sachs.

Most analysts were expecting Sheinbaum’s victory but not the overwhelming result in the Mexican Congress.

Andres Abadia of Pantheon Macroeconomics added, “The potentially qualified majority could open the door for (her party) Morena to increase the concentration of power and pose a threat to institutional checks and balances.”

Lastly, Chris Turner of ING added, "The question is whether the Morena party has done so well that it could command a super-majority and try to pursue market non-friendly policies of constitutional reform.”

Daily digest market movers: Mexican Peso remains offered on investors' fears

- Monday’s economic docket in Mexico featured Business Confidence and Foreign Reserves.

- Mexico’s Business Confidence in May worsened compared to April’s, drifting from 54.1 to 53.7.

- Mexico’s Foreign Reserves increased from $220 billion to $221 billion in April, revealed Banxico.

- September would be the crucial month for the Mexican Congress. Morena’s majority could push bills blocked by the opposition, including the reduction of lawmakers and plans for direct election of the Supreme Court members.

- Morgan Stanley noted that if Mexico’s upcoming government and Congress adopted an unorthodox agenda, it would undermine Mexican institutions and be bearish for the Mexican Peso, which could weaken to 19.20.

- That and speculation of another Banxico rate cut in June could pave the way for further upside in the USD/MXN.

- US manufacturing PMIs in May were mixed, as revealed by the Institute for Supply Management (ISM) and S&P Global.

- The US ISM Manufacturing PMI was worse than expected in May, coming at 48.7, down from 49.2 and below estimates of 49.6. Contrarily, the S&P Global Manufacturing PMI expanded by 51.3, up from 50 and exceeding estimates of 50.9.

- The futures markets suggest the Federal Reserve might cut rates by 31 basis points in 2024, according to December’s 2024 fed funds future rate contract.

Technical analysis: Mexican Peso depreciates as USD/MXN rallies above 17.50

The USD/MXN downtrend begins to be threatened due to political uncertainty. That has lifted the exchange rate above the 200-day Simple Moving Average (SMA) of 17.15, opening the door to push the spot prices toward a one-month high of 17.73.

Momentum has shifted strongly in favor of buyers as communicated by the Relative Strength Index (RSI), which has skyrocketed and crushed the 70 overbought level.

That said, if the USD/MXN clears the psychological 18.00 figure, up next would be the year-to-date (YTD) high of 18.15. Further gains are seen above the latter, on October 6, 2023, at a high of 18.48, before the exotic pair trends up toward the 19.00 figure.

On the downside, if sellers push the exchange rate below the 17.00 figure, that could pave the way to test the year-to-date (YTD) low of 16.25.

Mexican Peso FAQs

The Mexican Peso (MXN) is the most traded currency among its Latin American peers. Its value is broadly determined by the performance of the Mexican economy, the country’s central bank’s policy, the amount of foreign investment in the country and even the levels of remittances sent by Mexicans who live abroad, particularly in the United States. Geopolitical trends can also move MXN: for example, the process of nearshoring – or the decision by some firms to relocate manufacturing capacity and supply chains closer to their home countries – is also seen as a catalyst for the Mexican currency as the country is considered a key manufacturing hub in the American continent. Another catalyst for MXN is Oil prices as Mexico is a key exporter of the commodity.

The main objective of Mexico’s central bank, also known as Banxico, is to maintain inflation at low and stable levels (at or close to its target of 3%, the midpoint in a tolerance band of between 2% and 4%). To this end, the bank sets an appropriate level of interest rates. When inflation is too high, Banxico will attempt to tame it by raising interest rates, making it more expensive for households and businesses to borrow money, thus cooling demand and the overall economy. Higher interest rates are generally positive for the Mexican Peso (MXN) as they lead to higher yields, making the country a more attractive place for investors. On the contrary, lower interest rates tend to weaken MXN.

Macroeconomic data releases are key to assess the state of the economy and can have an impact on the Mexican Peso (MXN) valuation. A strong Mexican economy, based on high economic growth, low unemployment and high confidence is good for MXN. Not only does it attract more foreign investment but it may encourage the Bank of Mexico (Banxico) to increase interest rates, particularly if this strength comes together with elevated inflation. However, if economic data is weak, MXN is likely to depreciate.

As an emerging-market currency, the Mexican Peso (MXN) tends to strive during risk-on periods, or when investors perceive that broader market risks are low and thus are eager to engage with investments that carry a higher risk. Conversely, MXN tends to weaken at times of market turbulence or economic uncertainty as investors tend to sell higher-risk assets and flee to the more-stable safe havens.

- Weak ISM PMI report for May and decreasing US Treasury yields weigh on USD.

- ISM Manufacturing PMI report increases odds of Fed rate cut in September.

- Markets awaiting upcoming Nonfarm Payrolls report and wage growth data.

On Monday, the US Dollar Index (DXY) continued its decline toward the 104.15 area mainly due to the Institute of Supply Management (ISM) PMI report for May. The data led to a decline in US Treasury yields and a slight increase in the odds of a Federal Reserve (Fed) rate cut in September.

Market attention has now shifted toward labor market data, specifically the Nonfarm Payrolls report for May, for investors to gather additional data on the US economy.

Daily digest market movers: DXY retreats due to weak ISM data

- Investors are signaling concerns with the ISM PMI report due to indications of a contracting manufacturing sector.

- The ISM Manufacturing PMI for May contracted to 48.7, falling below both the expected 49.6 and April's 49.2, as per the ISM data released on Monday.

- The lower-than-expected PMI data led to an increase in market-based probabilities of a Fed interest rate cut in September.

- Following the release, the probability of a rate cut in September increased to nearly 60%.

- Markets eagerly await the Nonfarm Payrolls report for May, due later this week, which may influence the Fed's future decisions.

- US Treasury yields saw a sharp decline with the 2, 5 and 10-year yields falling more than 2%.

DXY technical analysis: US Dollar struggles as negative indicators resurface

The DXY fell below the 20, 100 and 200-day Simple Moving Averages (SMAs) on Monday due to the disappointing ISM PMI report. This caused the index to enter a bearish phase.

Similarly, the Relative Strength Index (RSI) and Moving Average Convergence Divergence (MACD) fell into negative territory, indicating a rise in bearish sentiment and selling pressure. However, as the pair now tallies a three-day losing streak there are chances that buyers might step in for a slight upwards correction.

US Dollar FAQs

The US Dollar (USD) is the official currency of the United States of America, and the ‘de facto’ currency of a significant number of other countries where it is found in circulation alongside local notes. It is the most heavily traded currency in the world, accounting for over 88% of all global foreign exchange turnover, or an average of $6.6 trillion in transactions per day, according to data from 2022. Following the second world war, the USD took over from the British Pound as the world’s reserve currency. For most of its history, the US Dollar was backed by Gold, until the Bretton Woods Agreement in 1971 when the Gold Standard went away.

The most important single factor impacting on the value of the US Dollar is monetary policy, which is shaped by the Federal Reserve (Fed). The Fed has two mandates: to achieve price stability (control inflation) and foster full employment. Its primary tool to achieve these two goals is by adjusting interest rates. When prices are rising too quickly and inflation is above the Fed’s 2% target, the Fed will raise rates, which helps the USD value. When inflation falls below 2% or the Unemployment Rate is too high, the Fed may lower interest rates, which weighs on the Greenback.

In extreme situations, the Federal Reserve can also print more Dollars and enact quantitative easing (QE). QE is the process by which the Fed substantially increases the flow of credit in a stuck financial system. It is a non-standard policy measure used when credit has dried up because banks will not lend to each other (out of the fear of counterparty default). It is a last resort when simply lowering interest rates is unlikely to achieve the necessary result. It was the Fed’s weapon of choice to combat the credit crunch that occurred during the Great Financial Crisis in 2008. It involves the Fed printing more Dollars and using them to buy US government bonds predominantly from financial institutions. QE usually leads to a weaker US Dollar.

Quantitative tightening (QT) is the reverse process whereby the Federal Reserve stops buying bonds from financial institutions and does not reinvest the principal from the bonds it holds maturing in new purchases. It is usually positive for the US Dollar.

- Markets kick off NFP week pricing in a first Fed rate cut in November.

- Canada reveals unexpected downturn in Manufacturing PMI data.

- CAD traders will be gearing up for a midweek BoC rate call as NFP Friday looms.

The Canadian Dollar (CAD) is broadly lower on Monday after May’s S&P Canadian Global Manufacturing Purchasing Managers Index (PMI) figures missed the mark. A similar miss in ISM US Manufacturing PMIs has left the Canadian Dollar and the US Dollar (USD) battling for second place.

Canada has spent 13 months with manufacturing PMI surveys printing below the key 50.0 level as industry leaders continue to grapple with a mouldering Canadian economy. CAD traders will also be looking ahead to Wednesday’s rate call from the Bank of Canada (BoC) as markets lean further into hopes of a rate trim from the Canadian central bank. According to a recent Reuters poll, 22 of 29 surveyed economists expect a 25-basis-point rate cut from the BoC on June 5.

Daily digest market movers: Canadian Dollar weakens, but Greenback weakens faster

- Canadian S&P Manufacturing PMI in May eased to 49.3 from 49.4, missing the forecasted increase to 50.2.

- Markets broadly ignored the S&P Global US PMI to focus on a miss in the US ISM Manufacturing PMI, which eased to 48.7 from 49.2 in May, down from the forecast increase to 49.6.

- Wednesday looms ahead with the BoC’s latest rate call, where markets are anticipating a quarter-point cut.

- Wednesday also brings ADP Employment Change for May, a common (albeit volatile) preview of Friday’s US Nonfarm Payrolls (NFP) jobs report.

- Canadian labor figures due Friday will be overshadowed by market reactions to US NFP.

Canadian Dollar PRICE Today

The table below shows the percentage change of Canadian Dollar (CAD) against listed major currencies today. Canadian Dollar was the strongest against the US Dollar.

| USD | EUR | GBP | JPY | CAD | AUD | NZD | CHF | |

|---|---|---|---|---|---|---|---|---|

| USD | -0.31% | -0.29% | -0.72% | 0.09% | -0.29% | -0.62% | -0.87% | |

| EUR | 0.31% | 0.05% | -0.39% | 0.40% | -0.10% | -0.33% | -0.56% | |

| GBP | 0.29% | -0.05% | -0.38% | 0.34% | -0.09% | -0.44% | -0.63% | |

| JPY | 0.72% | 0.39% | 0.38% | 0.78% | 0.47% | 0.21% | 0.01% | |

| CAD | -0.09% | -0.40% | -0.34% | -0.78% | -0.41% | -0.73% | -0.97% | |

| AUD | 0.29% | 0.10% | 0.09% | -0.47% | 0.41% | -0.24% | -0.49% | |

| NZD | 0.62% | 0.33% | 0.44% | -0.21% | 0.73% | 0.24% | -0.28% | |

| CHF | 0.87% | 0.56% | 0.63% | -0.01% | 0.97% | 0.49% | 0.28% |

The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the Canadian Dollar from the left column and move along the horizontal line to the US Dollar, the percentage change displayed in the box will represent CAD (base)/USD (quote).

Technical analysis: Canadian Dollar stumbles on Monday despite USD/CAD pumping the brakes

The Canadian Dollar (CAD) is broadly lower on Monday, shedding weight across the board and struggling to hold ground against the US Dollar. The CAD is down three-quarters of a percent against the Japanese Yen (JPY) and the Swiss Franc (CHF). A softening Greenback will have to settle for second place on Monday as the declining US Dollar is struggling to catch up to the weakening CAD.

USD/CAD slumped once more into a familiar demand zone near the 1.3600 handle, but firmer bidding on the Greenback side keeps the pair in range of Monday’s early peak near 1.3660. The pair has been in a rough consolidation pattern since the beginning of May, but highs are drifting lower as CAD strength looks set to fade further.

A long-term technical floor is still priced in at the 200-day Exponential Moving Average (EMA) near 1.3560, and USD/CAD appears mired in congestion at the 50-day EMA near 1.3645. A move higher will see the pair grappling with 2024’s peak bids near 1.3850.

USD/CAD hourly chart

USD/CAD daily chart

Canadian Dollar FAQs

The key factors driving the Canadian Dollar (CAD) are the level of interest rates set by the Bank of Canada (BoC), the price of Oil, Canada’s largest export, the health of its economy, inflation and the Trade Balance, which is the difference between the value of Canada’s exports versus its imports. Other factors include market sentiment – whether investors are taking on more risky assets (risk-on) or seeking safe-havens (risk-off) – with risk-on being CAD-positive. As its largest trading partner, the health of the US economy is also a key factor influencing the Canadian Dollar.

The Bank of Canada (BoC) has a significant influence on the Canadian Dollar by setting the level of interest rates that banks can lend to one another. This influences the level of interest rates for everyone. The main goal of the BoC is to maintain inflation at 1-3% by adjusting interest rates up or down. Relatively higher interest rates tend to be positive for the CAD. The Bank of Canada can also use quantitative easing and tightening to influence credit conditions, with the former CAD-negative and the latter CAD-positive.

The price of Oil is a key factor impacting the value of the Canadian Dollar. Petroleum is Canada’s biggest export, so Oil price tends to have an immediate impact on the CAD value. Generally, if Oil price rises CAD also goes up, as aggregate demand for the currency increases. The opposite is the case if the price of Oil falls. Higher Oil prices also tend to result in a greater likelihood of a positive Trade Balance, which is also supportive of the CAD.

While inflation had always traditionally been thought of as a negative factor for a currency since it lowers the value of money, the opposite has actually been the case in modern times with the relaxation of cross-border capital controls. Higher inflation tends to lead central banks to put up interest rates which attracts more capital inflows from global investors seeking a lucrative place to keep their money. This increases demand for the local currency, which in Canada’s case is the Canadian Dollar.

Macroeconomic data releases gauge the health of the economy and can have an impact on the Canadian Dollar. Indicators such as GDP, Manufacturing and Services PMIs, employment, and consumer sentiment surveys can all influence the direction of the CAD. A strong economy is good for the Canadian Dollar. Not only does it attract more foreign investment but it may encourage the Bank of Canada to put up interest rates, leading to a stronger currency. If economic data is weak, however, the CAD is likely to fall.

- GBP/USD climbs to 1.2772, close to a four-day high of 1.2784.

- Technical outlook shows upward bias with RSI pointing higher but not yet overbought.

- Key resistance at 1.2800; surpassing it could lead to YTD high of 1.2893, while support lies at 1.2643 and 1.2600.

The British Pound rallied for the third straight day against the US Dollar, gaining some 0.37% in early trading during the North American session. The GBP/USD exchanged hands at 1.2785, shy of a four-day high of 1.2787 reached during the European session.

GBP/USD Price Analysis: Technical outlook

From a daily chart perspective, the GBP/USD is upward biased as buyers gain momentum, reflected on the Relative Strength Index (RSI). The RSI aims upwards yet with a room before turning overbought.

That said, buyers need to clear the conglomeration of technical levels, with the 1.2800 figure and a downslope resistance trendline passing around that area. Once surpassed, the next stop would be the year-to-date (YTD) high of 1.2893, which is shy of 1.2900.

On the other hand, if GBP/USD tumbles below 1.2700, that could sponsor a leg down toward the confluence of the May 3 high turned support and the 100-day moving average (DMA) at around 1.2643. Further losses lie at 1.2600.

GBP/USD Price Action - Daily Chart

- NZD/USD jumps to 0.6815 after downbeat US ISM Manufacturing PMI report.

- Weak factory activity report dents the US Dollar’s appeal.

- The RBNZ is less likely to return to the policy normalization process this year.

The NZD/USD pair advances to 0.6185 in Monday’s American session as the United States (US) Institute of Supply Management (ISM) has reported a weak Manufacturing PMI report for May. The agency reported that the Manufacturing PMI, which gauges the factory activity, surprisingly declines to 48.7 from the estimates of 49.8 and the former release of 49.2.

Apart from that, other sub-components such as New Orders and Prices Paid Indexes were also weaker than expectations, weighing on the US Dollar (USD). Weak factory data is expected to boost market speculation for the Federal Reserve (Fed) to begin reducing interest rates from the September meeting. The US Dollar Index (DXY) slumps to 104.25.

Meanwhile, the New Zealand Dollar remains firm as investors expect that the Reserve Bank of New Zealand (RBNZ) will not consider lowering interest rates this year. Also, there is a debate that the RBNZ could hike its Official Cash Rate further. Meanwhile, RBNZ Governor Adrian Orr has already commented that more rate hikes remain off the table as long as inflation expectations remain anchored.

NZD/USD attempts to break the Bullish Flag chart formation in a four-hour timeframe, which exhibits an inventory adjustment process between institutional investors and retail participants. This pattern indicates a consolidation after a sharp upside move and it generally breaks towards the direction of the trend, which in this is upwards.

The 50-period Exponential Moving Average (EMA) near 0.6126 continues to provide support to the New Zealand Dollar bulls.

Meanwhile, the 14-period Relative Strength Index (RSI) has climbed above 60.00. A sustainable move above 60.00 will strengthen Kiwi bulls further.

An upside move above the round-level resistance of 0.6200 will drive the asset January 15 high near 0.6250, followed by January 12 high near 0.6280.

On the contrary, fresh downside would appear if the asset breaks below April 4 high around 0.6050 This would drag the asset towards the psychological support of 0.6000 and April 25 high at 0.5969.

NZD/USD daily chart

- ISM Manufacturing PMI declined in May, pointing to ongoing contraction.

- US Dollar stays under bearish pressure after disappointing PMI data.

The business activity in the US manufacturing sector contracted at an accelerating pace in May, with the ISM Manufacturing PMI dropping to 48.7 from 49.2 in April. This reading came in below the market expectation of 49.6.

The Employment Index of the PMI survey improved to 51.1 in May from 48.6 in April, while the New Orders Index slumped to 45.4 from 49.1. Finally, the Prices Paid Index, the inflation component, retreated to 57 from 60.9 in the same period.

Commenting on the survey's findings, "US manufacturing activity continued in contraction after growing in March, the first expansion for the sector since September 2022. Demand was soft again, output was stable, and inputs stayed accommodative," said Timothy R. Fiore, Chair of the Institute for Supply Management (ISM) Manufacturing Business Survey Committee.

Market reaction

The US Dollar (USD) came under renewed selling pressure following this report. At the time of press, the USD Index was down 0.28% on the day at 104.33.

- GBP/JPY pulls back after retouching multi-year highs.

- The trend is bullish so the pull back is not expected to last before the uptrend resumes.

- Intervention by the Japanese authorities is a risk factor that could push GBP/JPY lower.

GBP/JPY rallies up to 200.65 on Monday just short of multi-year highs (May 29) and then pulls back. Despite correcting back down to the 199.50s the pair remains in an uptrend over a short, intermediate and long-term time horizon, and since “the trend is your friend” more upside it expected.

4-hour Chart

The pair has broken through one – perhaps even two – trendlines underpinning the rally during May. If the correction continues it will probably find support at 198.79 (May 30 swing lows). A break below would suggest further weakness to perhaps the 100 Simple Moving Average (SMA) at 198.40.

Given the dominant uptrend, however, bulls are expected to turn things around once the correction runs out of steam and pushes the pair higher again.

The only sign the pull back may be ending is the formation of a bullish Japanese Hammer candlestick reversal candlestick on the last bar. This occurs when price makes a new low but then recovers to close near the open. If the current period ends as a bullish green candle it will confirm the hammer and could indicate a short-term reversal and resumption of the uptrend.

A break above the 200.75 high will establish a higher high and extend the uptrend. The next targets will probably be at the round numbers – 201.00, 202.00 etc.

Risk of intervention from the Japanese authorities to strengthen the Yen (resulting in a decline of GBP/JPY) could distort the technical picture.

- Silver price revives downside move as US bond yields drop sharply.

- US bond yields weaken as market speculation for Fed reducing interest rates in September improves.

- The next move in the US Dollar will be guided by the US ISM Manufacturing PMI for May.

Silver price (XAG/USD) recovers strongly after discovering buying interest near the crucial support of $30.00 in Monday’s New York session. The white metal bounced back as US Treasury yields plunge du to slight improvement in market speculation for the Federal Reserve (Fed) to begin reducing interest rates from the September meeting.

The CME FedWatch tool shows that the probability of a rate-cut decision in the September meeting has increased to 52% from 49% recorded a week ago. This has weighed heavily on US Treasury yields. 10-year US bond yields have declined to 4.46%. Lower yields on interest-bearing assets reduce the opportunity cost of holding an investment in non-yielding assets, such as Silver.

Some improvement in the Fed rate-cut expectations was driven by downwardly revised Q1 United States (US) Gross Domestic Product (GDP) estimates to 1.3% and weak Personal Spending data for April.

The US Dollar Index (DXY), which tracks the Greenback’s value against six major currencies, retreats to 104.50.

Going forward, investors will focus on the US ISM Manufacturing PMI data for May, which will be published at 14:00 GMT. The PMI is estimated to have improved to 49.8 from the former reading of 49.2. However, a figure below the 50.0 threshold Itself suggests contraction.

Silver technical analysis

Silver price trades in a Rising Channel chart pattern formed on a four-hour timeframe in which each pullback move is considered a buying opportunity by market participants. The white metal comes under pressure as it drops below the 50-period Exponential Moving Average (EMA), which trades around $31.00.

The 14-period Relative Strength Index (RSI) shifts into the bearish range of 20.00-40.00, suggesting that the momentum has leaned towards the downside.

Silver four-hour chart

- EUR/JPY is pulling back within a strong short, intermediate and long-term uptrend.

- If it continues declining the pull back could well find support at the 100 SMA.

- Any weakness will probably be short-lived given the overall bullish bias of the charts.

EUR/JPY is in an uptrend on all major timeframes and trading with a bullish bias over a short, intermediate and long time horizon. Given “the trend is your friend” EUR/JPY is more likely than not to continue rising.

4-hour Chart

The pair has pulled back to the 50 Simple Moving Average (SMA) but the uptrend remains intact in the short-term, and it is expected to find its feet and resume going higher. There are currently no signs of a recovery and reversal in line with the dominant uptrend.

The 100 SMA (blue) at 168.49 has faithfully supported price on previous pull backs, suggesting it may do the same if price pulls back any lower.

A break above 170.89 (June 3 high) would establish a higher high and probably indicate a continuation of the uptrend. The next target to the upside is 171.60, the high of April 29.

The Relative Strength Index (RSI) is in the neutral zone suggests there is more room for upside before the pair becomes overbought.

EUR/JPY would need to fall to 166.62 (50-day SMA) to suggest a reversal of the dominant uptrend. It would need to break below the trendline at circa 164.50 for confirmation of a reversal of the trend.

- The US Dollar trades mixed against its major peers on Monday.

- Markets are in a positive tone after a quiet weekend on the geopolitical front.

- The US Dollar Index trades in the mid-104.00 region, looking for direction.

The US Dollar (USD) trades broadly stable on Monday after a calm weekend without geopolitical headlines setting the tone. The Greenback will not be able to enjoy the calm start for long, because this week is full on the economic front. On Monday, a few important data points are set to be released in the run-up to the ultimate data point right at the end of the week: the US Employment Report, with its Nonfarm Payrolls print for May.

On Monday, all eyes will be on two PMI surveys gauging the health of the US manufacturing sector: the final reading of the S&P Global Manufacturing Purchasing Managers Index (PMI) for May and the more market-moving survey from the Institute for Supply Management (ISM).

Daily digest market movers: Manufacturing PMI on forefront

- Monday’s US calendar kicks off with the release of the final S&P Global Manufacturing PMI for May at 13:45 GMT. The preliminary estimate was at 50.9 and it is expected to remain unchanged.

- At 14:00 GMT, the Institute for Supply Management releases its recent findings from its monthly survey for May:

- The headline Manufacturing PMI index is expected to increase to 49.8 from 49.2.

- The Employment Index was at 48.6 in April, with no forecast available for May.

- The New Orders index came in at 49.1 a month ago, with no consensus view reported.

- The Prices Paid index should remain rather stable, from 60.9 to 60.

- Construction Spending is expected to rise 0.2% in April, swinging from a 0.2% contraction in March.

- Equities are trading in the green across the board, with all major indices from Asia, Europe and US futures up by an average of 1%.

- According to the CME Fedwatch Tool, Fed Fund futures pricing data suggests a 46.1% chance for keeping rates unchanged in September, against a 47.2% chance for a 25 basis points (bps) rate cut and a 6.7% chance for an even 50 bps rate cut. An interest rate hike is no longer considered an option.

- The benchmark 10-year US Treasury Note trades around 4.49%, in the middle of its monthly range between 4.34% and 4.61%.

US Dollar Index Technical Analysis: Tensions building towards NFP

The US Dollar Index (DXY) is hanging a bit in no man's land this Monday after its negative performance last week. When looking at a weekly chart, the DXY is clearly in consolidation, posting with lower highs and higher lows as sellers and buyers are being pushed towards each other. In this context, normally a breakout is then set to take place, something that could happen this week taking into account the very busy economic calendar ahead.

On the upside, the DXY index reclaimed the key 105.00 round level, which broadly aligns with the 55-day Simple Moving Average (SMA). It will be important to see if these levels hold support should the US data weaken. Once that is proven, look for 105.52 and 105.88.

On the downside, the 200-day SMA at 104.44 and the 100-day SMA around 104.42 are the last line of defence. Once that level snaps, an air pocket is placed between 104.30 and 103.00. Should the US Dollar decline persist, the low of March at 102.35 and the low from December at 100.62 are levels to consider.

US Dollar FAQs

The US Dollar (USD) is the official currency of the United States of America, and the ‘de facto’ currency of a significant number of other countries where it is found in circulation alongside local notes. It is the most heavily traded currency in the world, accounting for over 88% of all global foreign exchange turnover, or an average of $6.6 trillion in transactions per day, according to data from 2022. Following the second world war, the USD took over from the British Pound as the world’s reserve currency. For most of its history, the US Dollar was backed by Gold, until the Bretton Woods Agreement in 1971 when the Gold Standard went away.

The most important single factor impacting on the value of the US Dollar is monetary policy, which is shaped by the Federal Reserve (Fed). The Fed has two mandates: to achieve price stability (control inflation) and foster full employment. Its primary tool to achieve these two goals is by adjusting interest rates. When prices are rising too quickly and inflation is above the Fed’s 2% target, the Fed will raise rates, which helps the USD value. When inflation falls below 2% or the Unemployment Rate is too high, the Fed may lower interest rates, which weighs on the Greenback.

In extreme situations, the Federal Reserve can also print more Dollars and enact quantitative easing (QE). QE is the process by which the Fed substantially increases the flow of credit in a stuck financial system. It is a non-standard policy measure used when credit has dried up because banks will not lend to each other (out of the fear of counterparty default). It is a last resort when simply lowering interest rates is unlikely to achieve the necessary result. It was the Fed’s weapon of choice to combat the credit crunch that occurred during the Great Financial Crisis in 2008. It involves the Fed printing more Dollars and using them to buy US government bonds predominantly from financial institutions. QE usually leads to a weaker US Dollar.

Quantitative tightening (QT) is the reverse process whereby the Federal Reserve stops buying bonds from financial institutions and does not reinvest the principal from the bonds it holds maturing in new purchases. It is usually positive for the US Dollar.

- USD/CHF declines to near 0.9000 despite the US Dollar’s recovery.

- The US Dollar rebounds amid uncertainty ahead of US data-packed week.

- The Swiss Franc reflects sheer strength ahead of the Swiss CPI report for May

The USD/CHF pair extends its losing streak for the third trading session on Monday. The Swiss Franc asset weakens even though the US Dollar has rebounded amid uncertainty ahead of the United States data-packed week.

This week, the US economic calendar is full of top-tier events such as the ISM Manufacturing and Services PMI, ADP Employment Change and the Nonfarm Payrolls (NFP) data for May, and the JOLTS Job Openings for April. The economic data will provide significant cues about when the Federal Reserve (Fed) will start lowering its key borrowing rates this year.

Currently, financial markets expect that the Fed will choose the September meeting as the earliest point from when it will start reducing interest rates.

In today’s session, the US Dollar will be impacted by the US ISM manufacturing PMI, which will be published at 12: 30 GMT. The Manufacturing PMI is estimated to have risen to 49.8 from 49.2. However, a figure below the 50.0 threshold is considered as contraction. Investors will also focus on other sub-components such as New Orders and Prices Paid Indexes, which are leading indicators of inflation.

Meanwhile, the Swiss Franc exhibits strength ahead of the Swiss Consumer Price Index (CPI) data for May, which will be published on Tuesday. May’s CPI data will be the latest inflation reading available to Swiss National Bank (SNB) policymakers that will indicate whether a subsequent rate-cut move is required. Monthly CPI data is expected to have grown at a faster pace of 0.4% from the prior reading of 0.3%.

- Oil steadies near $77.00, looking for direction after Sunday’s OPEC+ meeting.

- OPEC+ meeting sets the tone for more downside after the summer season despite the decision to extend production cuts.

- The US Dollar Index trades at mid-104.00 levels and is facing a heavy week full of economic data.

Oil prices trade broadly steady on Monday, ignoring the OPEC+ decision to extend current production cuts into 2025 with the goal to support prices. Despite the broad commitment to keep a tight supply, some Oil producers within the organization will be able to ease some of the voluntary production cuts, which came as a surprise. The biggest winner was the United Arab Emirates, which can head back to markets and sell more barrels. Overall, Saudi Arabia and Russia will still take the bulk part of the effort and maintain that 2 million barrel draw per day, phasing it out from October.

Meanwhile, the US Dollar Index (DXY) is floating around a steady level near 104.63 with markets bracing for a very busy week. Several important data points are set to be released throughout the week in the run-up to the main event on Friday: the US Employment Report. Traders will be looking for clues over whether the US economy has topped out.

At the time of writing, Crude Oil (WTI) trades at $77.08 and Brent Crude at $81.33.

Oil news and market movers: OPEC+ fizzled again

- OPEC+ agreed to extend the cuts of 3.66 million barrels per day by a year until the end of 2025. However, voluntary production cuts, currently at around 2 million barrels per day, will start to be phased out from October after the recent OPEC+ production quota decision, Bloomberg reports.

- Goldman Sachs managing director and head of research Daan Struyven said in a note that the outcome of the OPEC+ meeting is bearish due to the decision to return supply to markets despite the recent surprise increase in inventories. Risks for Oil prices are now skewed to the downside, Bloomberg reports.

- Warren Patterson, head of commodity strategies at ING, sees a possible uptick in crude prices over the summer period. Still, the deficit is expected to widen by the third quarter.

Oil Technical Analysis: Doubling down on Fed cuts

Oil prices are not feeling warm about the recent agreement on output from OPEC+. Despite several bearish headlines from analysts and traders, there might be the consideration that OPEC+ expects a pickup in demand will take place by 2025. After all, sooner or later, the US Federal Reserve will cut interest rates, and it looks like OPEC+ is starting to prepare for this scenario.

First, the Simple Moving Averages (SMA) need to be regained under control. The 100-day SMA at $79.09 and the 200-day SMA at $79.54 are the first levels on the upside. Next, the 55-day Simple Moving Average (SMA) at $81.13 and the descending trendline at $81.45 are an area with a lot of resistance where any recovery rally could pause. Once broken through there, the road looks quite open to head to $87.12.

On the downside, the $76.00 marker is coming back into focus with the $75.27 level playing a crucial role if traders still want to have an option to head back to $80.00. Should that $75.27 pivotal level snap, expect to see a risk-full nosedive move that could sprint all the way down to $68, below $70.00.

US WTI Crude Oil: Daily Chart

WTI Oil FAQs

WTI Oil is a type of Crude Oil sold on international markets. The WTI stands for West Texas Intermediate, one of three major types including Brent and Dubai Crude. WTI is also referred to as “light” and “sweet” because of its relatively low gravity and sulfur content respectively. It is considered a high quality Oil that is easily refined. It is sourced in the United States and distributed via the Cushing hub, which is considered “The Pipeline Crossroads of the World”. It is a benchmark for the Oil market and WTI price is frequently quoted in the media.

Like all assets, supply and demand are the key drivers of WTI Oil price. As such, global growth can be a driver of increased demand and vice versa for weak global growth. Political instability, wars, and sanctions can disrupt supply and impact prices. The decisions of OPEC, a group of major Oil-producing countries, is another key driver of price. The value of the US Dollar influences the price of WTI Crude Oil, since Oil is predominantly traded in US Dollars, thus a weaker US Dollar can make Oil more affordable and vice versa.

The weekly Oil inventory reports published by the American Petroleum Institute (API) and the Energy Information Agency (EIA) impact the price of WTI Oil. Changes in inventories reflect fluctuating supply and demand. If the data shows a drop in inventories it can indicate increased demand, pushing up Oil price. Higher inventories can reflect increased supply, pushing down prices. API’s report is published every Tuesday and EIA’s the day after. Their results are usually similar, falling within 1% of each other 75% of the time. The EIA data is considered more reliable, since it is a government agency.

OPEC (Organization of the Petroleum Exporting Countries) is a group of 13 Oil-producing nations who collectively decide production quotas for member countries at twice-yearly meetings. Their decisions often impact WTI Oil prices. When OPEC decides to lower quotas, it can tighten supply, pushing up Oil prices. When OPEC increases production, it has the opposite effect. OPEC+ refers to an expanded group that includes ten extra non-OPEC members, the most notable of which is Russia.

- AUD/USD slips below 0.6650 amid US Dollar’s recovery.

- The US Dollar rebounds even though the Fed’s rate-cut prospects for September edge higher.

- Market speculation for the RBA tightening policy further has strengthened.

The AUD/USD pair falls to near 0.6635 in Monday’s European session. The Aussie asset is expected to witness more downside as the US Dollar recovers despite slight improvement in expectations that the Federal Reserve (Fed) will start reducing interest rates from the September meeting

The CME FedWatch tool shows that traders see a 52% for the central bank announcing a rate-cut move in September, which has improved from 49% recorded a week ago. Mild recovery in the Fed rate-cut speculation for September is driven by weak revised estimates for Q1 Gross Domestic Product (GDP) and slower Personal Spending growth for April.

The United States Q1 GDP grew by 1.3%, slower than preliminary estimates of 1.6%. US Personal Spending grew at a slower pace of 0.2% from the estimates of 0.3% and the former release of 0.7%. Consumer spending accounts for two-thirds of the US economic activity. Weak data has raised doubts over the US maintaining its strong economic outlook in the long-run.

In today’s session, investors will focus on the US ISM Manufacturing PMI for May, which will be published at 14:00 GMT. The factory data is estimated to have improved to 49.8 from the former reading of 49.2. However, a figure below the 50.0 threshold is considered as contraction.

Meanwhile, the near-term outlook of the Australian Dollar remains strong as investors hope that the Reserve Bank of Australia (RBA) could announce one more interest rate-hike due to stubbornly higher inflation data.

This week, the Australian Dollar will be guided by the Q1 GDP data, which will be published on Wednesday. The Australian economy is estimated to have expanded at a steady pace of 0.2%.

- Gold spikes to a high of $2,359 on Friday after US PCE inflation data undershoots expectations, suggesting interest rates might fall.

- Gold then rolls over and declines to three-week lows, however, as safe-haven demand declines, bulls take flight.

- Asian demand and cooling inflation expectations could put a floor under the rout.

- Technicals remain bearish after a breakout from a Bear Flag.

Gold (XAU/USD) slides lower to trade in the $2,320s on Monday as a positive risk-on environment inherited from the Asian session lowers safe-haven demand for the metal.

Gold rolls over after hitting temporary high

Gold pumped after the release of marginally lower-than-expected US core Personal Consumption Expenditures (PCE) data on Friday, the Federal Reserve’s (Fed) preferred gauge of inflation. Core PCE came out at 0.2% month-over-month in April instead of 0.3% forecast. The data lifted the precious metal temporarily to a peak of $2,359, however, it promptly tumbled back down.

The lower inflation data recalibrated expectations of when the Fed will cut interest rates, increasing the probability of a September cut to 55% from around 50% previously. This is positive for Gold, which as a non yielding asset tends to appreciate when interest rates fall. That said, Gold investors remain cautious about the trajectory of interest rates amid still-high inflation and a Fed that is still hazy about its intentions.

Gold to be supported during the summer