- Analytics

- News and Tools

- Market News

CFD Markets News and Forecasts — 31-05-2011

U.S. equities continue to hold gains. Strength in technology helped the Nasdaq holding a gain of 0.9% while the Dow and S&P trail with 0.6% gains.

Conglomerate Siemens (SI 133.36, +5.17) is trading higher by 4.1% on word that Germany will discontinue the use of nuclear energy by 2022. The co is a large producer of wind turbines, and is seeing gains on the heels of that announcement.

First Solar (FSLR 123.22, +1.85) and other alternative energy plays are also seeing strength attributable to the news.

USD/JPY currently holds around Y81.33 after posting a high of Y81.77 earlier (55-day moving average at Y81.89). As to supports, rate held above Y80.69/Y80.72 (strong support) for 3 straight days. Bids are seen at Y80.95/Y81.00 and at Y80.70/75.

Stocks have climbed off their lowest levels of the session, and have broken through mid-morning resistance levels.

The S&P 500 Industrials Index is posting a gain of 0.5%. General Dynamics (GD 74.47, +3.21) is the top performing stock in the S&P 500 as it trades higher by 4.5% following a broker upgrade after the company received a $744 million contract from the U.S. Navy, with an option upping the contract to $1.3 billion.

EUR/JPY earlier broke over Y117.20/25 resistance and its 55-day moving average at Y117.40 as well as the May 6 peak at Y117.58, to post a new 3-week high around Y117.80, before retreating. The 100-day (around Y115.30 today) is the initial support. Soc Gen technical analysts say that the cross will need to see a clear cut break above the declining resistance line, which comes in at Y119.20 today before the focus will be turned to the April high of Y123.35. Cross

holds currently at Y117.03.

The euro rose to a three-week high against the dollar on speculation European officials will approve additional aid to Greece next month, dimming the prospects of a sovereign-debt restructuring.

Today the Luxembourg Prime Minister Jean-Claude Juncker said the region’s leaders will decide on a new aid package by the end of June and have ruled out a “total restructuring” of Greece’s debt. Germany may stop demanding an early rescheduling of bonds, according to a report.

The euro stayed higher after a report showed German retail sales rose in April as unemployment fell below 3 million for the first time in almost 19 years, fueling bets the European Central Bank will signal next week that it may raise interest rates for a second time this year.

Data showed sales increased 0.6% from March, when they fell 2.7%. Economists had a forecast a 1.8 percent gain. Sales increased 3.6 percent from a year earlier.

A separate European Union report showed euro-region inflation slowed in May to 2.7% from April’s 2.8%, the fastest pace since October 2008.

Inspectors from the EU, the International Monetary Fund and the European Central Bank are set to conclude a review of Greece’s progress in meeting the terms of last year’s 110 billion-euro ($158 billion) bailout in coming days. The EU will then formulate its plan for additional aid.

The yen pared losses versus the dollar and euro after a report showed U.S. consumer confidence unexpectedly fell in May to a six-month low, and other data showed a drop in home prices and weakening manufacturing.

The Canadian dollar gained the most this year versus its U.S. counterpart after the Bank of Canada kept its benchmark interest rate at 1%, where it has been since September.

AUD/USD holds at $1.0662, on the low side of the day's $1.0637 to $1.0756 range. Earlier the pair broke above $1.0724 (50% retracement of the slide from $1.1011 to May 25 low on $1.0437), but stalled ahead of the 61.8% retrace (at $1.0792). The focus is on Wednesday's Q1 GDP release (median estimate at -1.1% vs 0.7% in Q4).

- prices paid 78.6;

- new orders 53.5;

- employment 60.8,

- inventories 61.6;

- supplier deliveries 63.8;

- production 56.0.

U.S. stocks are poised to start the week in the black Tuesday, after a Wall Street Journal article stirred up hopes of a fresh bailout for Greece.

World markets rallied after the Journal reported Germany is shifting its stance to consider lending more money to Greece.

Economy: According to the closely watched S&P Case-Shiller Index, home prices recently fell to their lowest levels since the housing bubble burst. Prices tumbled 4.2% in the first quarter, sending home prices back to levels not seen since mid-2002.

Investors will also received data from the Chicago Purchasing Managers index at 13:45 GMT, followed by the Conference Board's consumer sentiment data at 14:00 GMT.

Economists expect the Chicago PMI index fell to a reading of 62.5 from April's 67.6, while consumer confidence rose to 66.3 versus April's 65.4.

World markets:

EUR/USD

Offers: $1.4410, $1.4420/25, $1.4440/55, $1.4480, $1.4500/10

Bids: $1.4390/80, $1.4365/50, $1.4335, $1.4325/15

USD/JPY

Offers: Y81.90/95, Y82.05/10, Y82.20/25

Bids: Y81.10/00, Y80.95/00, Y80.75/70

Overnight rate target remains at 1.00%, bank rate 1.25%

WTI July Crude continues to make gains with a move to $102.57. resistance ahead seen at $103.22 with a break there allowing a move to $105.85. Oil currently trades around $102.30

- ECB won't be distracted by debt crisis,dependent banks

- Greater need now for monetary policy normalization

- Inflation risk rising, cites 30% rise in food/energy

- Debt crisis, dependent banks won't distract ecb

- EMU faced with most difficult test since its creation

- No shortcut out of eurozone debt crisis

- National govts must completely implement adjustments

- Return to fin. health possible, cites italy in 1990s

- Global current account imbalances rising again

- Rigid fx, savings&demand differences behind imbalances

- Systemically important banks must be allowed to fai

The euro rose to a three-week high against the dollar on speculation European officials will approve additional assistance for Greece as part of efforts to counter the region’s debt crisis.

The euro pared its first monthly loss since November after Luxembourg Prime Minister Jean-Claude Juncker said European leaders will decide on a new aid package by the end of next month and have ruled out a “total restructuring” of the nation’s debt. The yen fell versus all 16 of its major counterparts as stocks surged and after Moody’s Investors Service placed Japan’s credit ratings on review for possible downgrade. New Zealand’s dollar rose to a record after a report showed business confidence increased.

“The news that European leaders are not going to demand restructuring is making a difference as it simply means they will throw money at the problem to stay off the day of reckoning,” said Geoffrey Yu, a currency strategist at UBS AG in London. “We can see the euro move higher to $1.45.”

The euro stayed higher after a report showed German retail sales rose in April as unemployment fell below 3 million for the first time in almost 19 years, fueling bets that the European Central Bank will signal next week that it may raise interest rates for a second time this year.

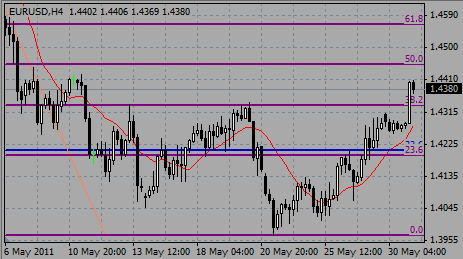

EUR/USD gained above $1.4400.

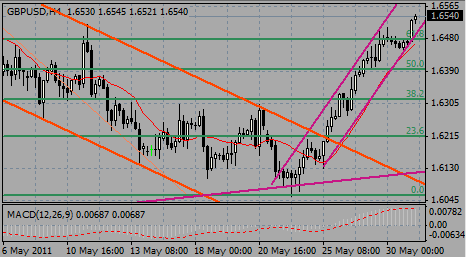

GBP/USD followed the euro and reachd $1.6545, before eased back to $1.6500.

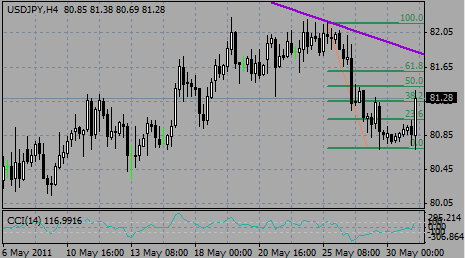

USD/JPY got support at Y80.70, before on the back of rising stocks gained to 81.70.

Today's main event is Bank of Canada's rate decision at 13:00 GMT before Chicago PMI is due to come at 14:00 GMT.

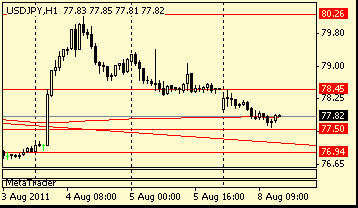

Comments: the pair gained on risk on trade. The nearest resistance - Y81.75. Above growth is possible to Y81.90. The nearest support - Y80.70. Below losses are possible to Y80.20.

Comments: the pair remains under pressure and trades near its historical low. The nearest support - Chf0.8465. Below loss may widen to Chf0.8400. The nearest resistance Chf0.8540. ahead of Chf0.8650.

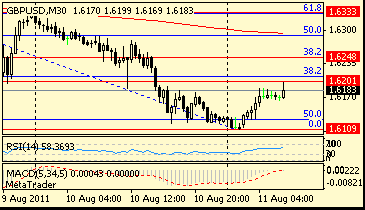

Comments: the pair remains around session high. The nearest resistance - $1.6510/20. Above growth is possible to $1.6575. The nearest support $1.6470. Below decrease is possible to $1.6400.

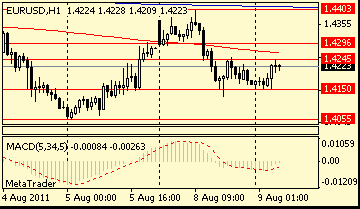

Comments: the pair is on the rise. The nearest resistance $1.4405. ahead of $1.4425. The nearest support $1.4255. Below losses are possible to $1.4200.

EUR/USD

Offers: $1.4410, $1.4420/25, $1.4440/55

Bids: $1.4365/50

USD/JPY

Offers: Y81.45/50, Y82.00/10

Bids: Y81.10/00

Gold traded quietly Monday as the US and UK markets were closed because of holidays. Today gold opened at $1538.75. The metal picked up to $1540.80 before easing back to $1534.70. Support is seen at $1522.75 with resistance at $1551.30.

Silver traded a $37.80-38.41 range yesterday and has today traded a $38.04-36 range in Asia this morning. Support now seen towards 37.45 with resistance at $38.87.

Majors close:

Nikkei 225 -16.97 -0.18% 9,504.97

CAC 40 -12.61 -0.32% 3,938.37

DAX -5.07 -0.07% 7,158.40

Japanese stocks swung between gains and losses amid speculation shares are oversold, and as comments by the Group of Eight nations tempered concern that a U.S. economic recovery is slowing.

Sony Corp. fell 2.1% after a report showed U.S. home-buying plunged more than forecast and the yen advanced against the dollar.

Honda Motor Co., Japan’s No. 2 automaker, dropped 1.3% after hackers accessed personal data of customers in Canada.

Sumitomo Realty & Development Co. rallied 1.2% after being raised to “overweight” from “equal- weight” at Barclays Capital.

European stocks were little changed after four straight weeks of losses for the benchmark Stoxx Europe 600 Index, as chemical makers and renewable-energy companies gained while banks declined.

BASF SE (BAS), the world’s biggest maker of chemicals, rose 1.2%.

Renewable Energy Corp. ASA and Vestas Wind Systems A/S climbed more than 3% as Germany set 2022 as the final date to close its nuclear reactors.

Alpha Bank SA tumbled 9.1% as the International Monetary Fund reviewed Greece’s efforts toward meeting fiscal targets.

Speculation that Greece will restructure its debt and concern the outlook for other economies in the region is worsening has weighed on stocks since February.

Greek Prime Minister George Papandreou said he’ll press ahead with new austerity measures after failing to win backing from the main opposition parties. An international panel of inspectors has concluded that the debt-laden country has missed all the fiscal targets agreed in its rescue plan, Der Spiegel reported May 29.

Markets in the U.K. were closed to observe the Spring Bank Holiday.

U.S. markets were Monday for the Memorial Day holiday.

The euro weakened for the first time in three days Monday against the dollar on concern euro-area leaders will struggle to resolve the debt crisis, damping demand for the region’s assets.

The shared currency weakened after Greek Prime Minister George Papandreou said he’ll press ahead with additional austerity measures even as he failed to win backing from opposition parties.

Greece’s Antonis Samaras, leader of the biggest opposition party, New Democracy, rejected Papandreou’s plan at a meeting with him and other opposition leaders in Athens, saying his party wouldn’t be blackmailed.

European Union officials have called for consensus on the package, which includes an extra 6 billion euros ($8.6 billion) of budget cuts and a plan to speed 50 billion euros of state-asset sales.

New Zealand has recorded its biggest monthly trade surplus on the back of higher prices for dairy products, the country’s top export earner, in a positive sign for a nation hit hard by two recent earthquakes and years of weak economic growth.

The NZ$1.11bn ($908m) trade surplus for April was nearly double economists’ forecasts and helped push the New Zealand dollar to its highest level against its US counterpart since the currency was floated in 1985.

Fonterra, the dairy farmer’s co-operative that accounts for about a fifth of the nation’s exports, recently said that March was its best month for export volumes thanks to rising demand from China, south-east Asia and the Middle East.

Strengthening trade links with China have also helped drive the record trade surplus. Exports to China have risen by nearly 40% in the 12 months ended in March.

New Zealand’s gross domestic product rose 0.2% in the final quarter of 2010 compared with the three months ended September.

However, the devastation caused by February’s earthquake in Christchurch, the second seismic event within six months, is expected to see the economy shrink by about 0.2% in the three months ended in March.

Nevertheless, the economy is expected to strengthen as 2011 continues with growth of about 1.3% for the year, rising to 3.7% in 2012.

EUR/USD fell from Asian high on $1.4305 to the lows near $1.4255 before recovered a bit to current $1.4284. Resistance between $1.4285/90 capped the bulls' attemps to break above.

GBP/USD was under pressure, thus above support at $1.6460/50.

USD/JPY held within the Y80.75/90 before tested Y81.00.

Today's main event is Bank of Canada's rate decision at 13:00 GMT before Chicago PMI is due to come at 14:00 GMT.

05:00 Japan Housing starts (April) Y/Y -3.9% -2.4%

05:00 Japan Construction orders (April) Y/Y - 11.0%

06:00 Germany Retail sales (April) real adjusted 1.8% -2.1%

06:00 Germany Retail sales (April) real unadjusted Y/Y 1.5% -3.5%

06:45 France PPI (April) 0.8% 0.9%

06:45 France PPI (April) Y/Y 6.4% 6.6%

06:45 France Consumer spending (April) 0.0% -0.7%

06:45 France Consumer spending (April) Y/Y 4.4% 2.6%

07:55 Germany Unemployment (May) seasonally adjusted -30K -37K

07:55 Germany Unemployment (May) seasonally adjusted, mln - 2.970

07:55 Germany Unemployment rate (May) seasonally adjusted 7.0% 7.1%

07:55 Germany Unemployment (May) seasonally unadjusted, mln - 3.078

07:55 Germany Unemployment rate (May) seasonally unadjusted - 7.3%

09:00 Italy CPI (May) preliminary 0.2% 0.5%

09:00 Italy CPI (May) preliminary Y/Y 2.7% 2.6%

09:00 Italy HICP (May) preliminary Y/Y 3.0% 2.9%

09:00 EU(17) Harmonized CPI (May) Y/Y preliminary 2.8% 2.8%

09:00 EU(17) Unemployment (April) 9.9% 9.9%

10:00 Italy PPI (April) 0.9% 0.7%

10:00 Italy PPI (April) Y/Y 5.5% 5.7%

12:55 USA Redbook (28.05)

13:00 Canada BOC meeting announcement 1.00% 1.00%

13:45 USA Chicago PMI (May) 63.0 67.6

14:00 USA Consumer confidence (May) 66.4 65.4

© 2000-2026. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers