- Analytics

- News and Tools

- Market News

CFD Markets News and Forecasts — 31-03-2011

- Move on Irish debt applies to outstanding, new securities;

- Assess progress in Irish EU-IMF program "positively";

- To review risk control measures on Irish debt regularly;

- Irish debt rating requirement suspended until further notice;

- Welcome rigorous capital assessments needs of irish banks;

- Welcome Irish government commitment to ensure capital needs met;

- E24 billion in new capital to substantially strengthen Irish banks;

- Banks must be solvent for continued eurosystem refinancing access;

- Eurosystem to continue providing liquidity to Irish banks.

Energy stocks were early leaders, but the sector has pared its gains over the past few hours. The sector is now up only 0.3% after it had been up 1% this morning.

Materials stocks have maintained their strength, though. The sector is up 0.7%, which makes it today's strongest sector.

Financials and consumer discretionary stocks make up this session's worst performers. Both sectors are down 0.3%.

The euro strengthened against the dollar and the yen after euro-region inflation unexpectedly accelerated in March, bolstering the case for the European Central Bank to raise interest rates next week.

Inflation in the 17-nation euro region quickened to 2.6% in March from 2.4% in February, European Union estimates showed today. That’s the fastest pace since October 2008, and exceeds the ECB’s 2% limit for a fourth month. Economists had forecast inflation to hold steady.

“As risk is being put back on, the euro is benefitting as the market looks forward to interest-rate expectation, regardless of what their economy is doing, the Irish stress test or any banking issues,” said Brian Taylor, chief currency trader a Manufacturers & Traders Trust in Buffalo New York. “Not only is the euro resilient against the dollar, it’s kicking everyone’s tail.”

The 17-nation currency remained higher against most its major counterparts after Ireland announced that four of the country’s banks need to raise 24 billion euros ($34 billion) of additional capital. The dollar weakened as fewer Americans filed jobless benefits applications last week before the March employment report tomorrow.

The shared currency earlier pared gains against the greenback after Anglo Irish Bank Corp. Chief Executive Officer Mike Aynsley said he’s “not sure we’ll get details” of plans for a funding facility for Irish banks after results of the stress tests.

“Consumer price data is outweighing Portugal and Ireland,” said Stephen Gallo, head of market analysis at Schneider Foreign Exchange in London. “It adds supports to the euro.”

Results from Ireland's bank stress tests were just released. The report indicates that four banks, including Allied Irish Banks (AIB) and Bank of Ireland (IRE), need a total of 24 billion euros of additional capital.

Semiconductor stocks are caught in a spell of selling pressure. The group is currently down 0.7% after it butted up against its 50-day average in the prior session. Although its lack of direction in the past few sessions has made for a lackluster finish to the first quarter, the Philadelphia Semiconductor Index is on pace for a 6.5% quarterly gain. That compares favorably to the S&P 500's first quarter gain of 5.5%.

"Chicago PMI came in at an extremely robust 70.6 in March. The production and new orders figures remained in the mid-70s. All of the major components of this report 60 or higher. On an ISM weighted basis, the figure was virtually unchanged at 67.5. This report shows no sign of any weakness in the motor vehicle industry."

The major equity averages are currently mired near the neutral line as underlying stocks trade in mixed fashion.

However, energy stocks have made a strong bounce in the early going. The sector's early sprint to a 1.0% gain has been helped by oil's rally in early pit trade. Oil prices were last quoted with a 2% gain at $106.30 per barrel.

- Prices Paid 83.4;

- New orders 74.5;

- Employment 65.6 vs 59.8;

- Inventories 60.5;

- Production 74.2.

EUR/USD holds a bit higher session low on $1.4262. Rate currently holds around $1.4169. Bids at $1.4160/50 area remain intact. Stops remain in place below $1.4140 but traders then suggesting that the Wednesday breakout area at $1.4120 should offer some support.

U.S. stocks were poised to open slightly lower Thursday, after a weekly report on jobless claims that was a bit higher than expected.

U.S. stocks ended Wednesday with solid gains, after two upbeat reports on job growth. One report from outplacement consulting firm Challenger, Gray & Christmas said private employers announced fewer planned job cuts in March - even as government layoffs mounted.

A second report, from payroll processor ADP, showed private sector employment rose by 201,000 in March. Investors view the ADP report as a guide for what's coming in Friday's employment report from the Labor Department.

Economy: The government's weekly jobless claims report showed a decline of 6,000 claims to 388,000 in the week ended March 26, which was slightly more than expected.

Economists had expected new claims to total 383,000 last week.

The Chicago-area purchasing managers' index for March is due at 13:45 GMT.

Companies: Warren Buffett's heir apparent, David Sokol, quit Berkshire Hathaway (BRKA, Fortune 500). In a press release Wednesday, Buffett said the resignation was a "total surprise," but he also revealed that Sokol had purchased shares of Lubrizol (LZ, Fortune 500) before pushing him to buy the company in March for $9.7 billion.

"I'd like to do what [Buffett] did in 1965: invest my own money," he said.

Dollar mostly ignored the weekly jobless claims data. Currently EUR/USD still weakening, holding around $1.4195, the GBP/USD - at $1.6069 and the USD/JPY - on Y82.78.

Data released

06:00 UK Nationwide house price index (March) 0.5% 0.0% 0.3%

06:00 UK Nationwide house price index (March) Y/Y 0.1% -0.6% -0.1%

06:00 Germany Retail sales (February) real adjusted -0.3% 0.3% 1.4%

06:00 Germany Retail sales (February) real unadjusted Y/Y 1.1% 1.1% 2.6%

06:45 France PPI (February) 0.8% 0.7% 0.9%

06:45 France PPI (February) Y/Y 6.3% 6.2% 5.6%

07:55 Germany Unemployment (March) seasonally adjusted -55K -22K -52K

07:55 Germany Unemployment (March) seasonally adjusted, mln - 3.069

07:55 Germany Unemployment rate (March) seasonally adjusted 7.1% 7.2% 7.3%

07:55 Germany Unemployment (March) seasonally unadjusted, mln 3.210 - 3.317

07:55 Germany Unemployment rate (March) seasonally unadjusted 7.6% - 7.9%

08:00 Italy PPI (February) 0.5% 0.6% 1.1%

08:00 Italy PPI (February) Y/Y 5.3% - 5.1%

09:00 Italy CPI (March) preliminary 0.4% 0.3% 0.3%

09:00 Italy CPI (March) preliminary Y/Y 2.5% 2.2% 2.4%

09:00 Italy HICP (March) preliminary Y/Y 2.6% 2.1% 2.1%

09:00 EU(17) Harmonized CPI (March) Y/Y preliminary 2.6% 2.3% 2.4%

The euro strengthened against the dollar and the yen as data showed euro-region inflation unexpectedly accelerated in March, bolstering the case for tighter monetary policy.

German unemployment fell sharply for a second straight month in March, pushing the jobless rate down to 7.1%, its lowest level since figures for a unified Germany were first published two decades ago.

In a sign that demand for labour remains robust in Europe's largest economy, the Federal Labour Office said unemployment fell by 55,000 in March after a drop of 54,000 in February.

Data from the Federal Statistics Office showed an unexpected 0.3% drop in real retail sales for the month of February in a sign rising prices, driven by high oil, may be tempering consumer demand.

Annual inflation in Germany has pushed up to 2.2%, when harmonised according to EU standards, and consumer prices in the broader 17-nation euro zone jumped 2.6% in March compared to the year before, data on Thursday showed.

The European Central Bank is expected to respond to rising price risks next week by raising its benchmark interest rate from a record low 1.0%.

“The market is expecting the ECB to hike interest rates,” said Jane Foley, a senior foreign-exchange strategist at Rabobank International. “There has been decent buying of the euro. Ultimately it underscores that investors are still not that fazed by the crisis in Portugal or the Irish stress tests.”

Australia’s dollar climbed to a record after the nation’s retail sales grew more than estimated.

Sales rose 0.5% last month, the Bureau of Statistics said today, surpassing the 0.4% increase projected by economists. The number of permits granted to build or renovate houses and apartments dropped 7.4%, while economists had estimated a 4% increase.

EUR/USD rose from $1.4125 to $1.4235 in EU before retreated to $1.4200. In general rate looks bullish.

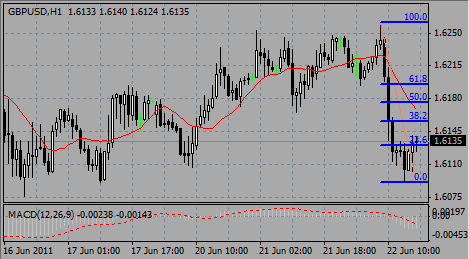

GBP/USD challenged resistance at $1.6150 but failed to break above and retreated to $1.6060. Later rate rebounded to $1.6088.

USD/JPY remains within the Y82.60/90 range.

US data starts at 1230GMT with the weekly jobless claims. Initial jobless claims are expected to fall 2,000 to 380,000 in the March 26 week after falling in four of the last five weeks.

US data continues at 1345GMT with the the March Chicago Purchasers Index. The Chicago PMI is expected to fall to a reading of 70.0 in March.

At 1400GMT, factory new orders are expected to rise 0.5% in February after being lifted by aircraft orders and energy prices in January.

EUR/GBP refresed session highs and 2011 highs at stg0.8844, after breaking above previous high at stg0.8836 (Mar 29). Next band of resistance is around stg0.8860/65.

Oil breaks through the 5-DMA resistance level despite daily studies suggesting a weakening. Overall, the double-top pattern at $106.69/95 remains in play. Initial resistance now seen as the Mar 7 high at $106.95.

Euro rose strongly Thursday after German unemployment fell sharply for a second straight month in March, pushing the jobless rate down to 7.1%, its lowest level since figures for a unified Germany were first published two decades ago.

In a sign that demand for labour remains robust in Europe's largest economy, the Federal Labour Office said unemployment fell by 55,000 in March after a drop of 54,000 in February.

Data from the Federal Statistics Office showed an unexpected 0.3% drop in real retail sales for the month of February in a sign rising prices, driven by high oil, may be tempering consumer demand.

Annual inflation in Germany has pushed up to 2.2%, when harmonised according to EU standards, and consumer prices in the broader 17-nation euro zone jumped 2.6% in March compared to the year before, data on Thursday showed.

The European Central Bank is expected to respond to rising price risks next week by raising its benchmark interest rate from a record low 1.0%.

Today's focus will be on Jobless Claims report after a strong ADT data yesterday.

On Wednesday a private report showed U.S. companies added 201,000 jobs in March, fueling speculation the Federal Reserve may curtail its debt buying.

The private report precedes the Labor Department’s nonfarm payroll numbers to be released April 1. U.S. payrolls added 190,000 in March, according to the median estimate of economists.

Gold pushing higher despite mixed daily studies. However, a key supp level which gold failed to close below for three sessions remains at $1414.60 (23.6% Fibonacci of $1308.5/1447.4). For now, initial res seen as the Dec 7 reversal high at $1430.80 and further res seen as the daily Boll top and Mar 24 record high at $1447.40.

AUD/USD refreshed 30 year high of $1.0363 following the flushing of the $1.0350 barrier. But rate quickly eases back to $1.0345. Some technical resistance seen towards $1.0380 and talk of a further barrier at $1.0400.

GBP/USD retreats after rising up to session highs on $1.6152. Currently rate holds around $1.6121. Some pick up on the wire report of UK Treasury comment that they are to top up currency reserves by stg6bln.

Hang Seng +0.32% 23,527.52

Shanghai Composite -0.94% 2,928.11

Nikkei +0.48% 9755.10

The yen fell to almost a three-week low versus the dollar amid demand for higher-yielding assets.

The Japanese currency weakened for a fifth straight day against the dollar as a private report showed U.S. companies added 201,000 jobs in March, fueling speculation the Federal Reserve may curtail its debt buying.

The private report precedes the Labor Department’s nonfarm payroll numbers to be released April 1. U.S. payrolls added 190,000 in March, according to the median estimate of economists.

Japan’s currency has weakened 2.3% against the dollar in the first quarter and 7% against the euro. Those declines accelerated in March with the yen losing 2.6% against the dollar and 1.6% to the euro in the past nine days.

Europe’s common currency has strengthened 5.2% versus the dollar this year as euro-region policy makers stiffened their anti-inflation views. The ECB will increase its main refinancing rate by a quarter-percentage point to 1.25% at its April 7 meeting, according to the median forecast of economists.

US data starts at 1230GMT with the weekly jobless claims as well as the ISM-NY Business Index for March. Initial jobless claims are expected to fall 2,000 to 380,000 in the March 26 week after falling in four of the last five weeks. US data continues at 1345GMT with the the March Chicago Purchasers Index and also the weekly Bloomberg Comfort Index. The Chicago PMI is expected to fall to a reading of 70.0 in March. Other regional data already released have suggested stronger expansion. At 1400GMT, factory new orders are expected to rise 0.5% in February after being lifted by aircraft orders and energy prices in January. Durable goods orders were already reported down 0.9% in the month, but non-durable goods orders are expected to get a lift from rising energy prices.

31/03/2011

© 2000-2026. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers