- Analytics

- News and Tools

- Market News

CFD Markets News and Forecasts — 29-07-2011

The markets remain trendless.

Rating agancy

Country S&P Fitch Moody's

Portugal BBB-(neg) BBB- (RWN) Ba2 (neg)

Ireland BBB+(stb) BBB+ (neg) Ba1 (neg)

Italy A+ (neg) AA- (stb) Aa2 (review)

Greece CC (neg) CCC (---) Ca (develp)

Spain AA (neg) AA+ (neg) Aa2 (neg)

Austria AAA(stb) AAA (stb) Aaa (stb)

Belgium AA+(neg) AA+ (neg) Aa1 (stb)

Finland AAA(stb) AAA (stb) Aaa (stb)

Germany AAA(stb) AAA (stb) Aaa (stb)

France AAA(stb) AAA (stb) Aaa (stb)

Netherlands AAA(stb) AAA (stb) Aaa (stb)

US dollar bounces back versus a basket of currencies after the huge drop amid release of weak US data. Before the opening bell the data on U.S. preliminary Q2 GDP showed the U.S. economy grew only by 1.3% while average forecast was at 1.6%. First-quarter GDP was revesed to +0.4% from +1.9%.

The dollar received some support from slight progress in solving the problem of US debt ceiling.

The euro is under pressure as today an international rating agency Moody's placed Spain's AA2 credit rating under review for a possible downgrade. IMF said that a moderate recovery of Spain faces potentially 'severe' risks and noted that spread of debt crisis to Spain would have global impact

Canadian dollar goes up versus the US dollar. Earlier the loonie sharply fell versus major currencies amid reports that showed decline in GDP and raw material price index.

The Swiss frank sheds against the dollar after Swiss central bank saw its first-half loss nearly quadruple from a year earlier on the declining value of its international reserves.

Japan yen begins to retreat versus the dollar amid the rise of the latter.

- Moderate recovery faces potentially 'severe' risks

- Spread of debt crisis to Spain would have global impact

- France, Germany to be hardest hit if contagion hits Spain

- Spain's GDP growth seen 0.8% in 2011, 1.6% in 2012

- Inflation seen 3% in 2011, 1.7% in 2012

- 2011 public sector deficit 6% of GDP

Currently all 8 of 9 major sectors suffer losses. The Basil Materials declined more that others (-1.3%). Industrial Goods holds in green zone (+0.1%).

- Sen Reid said he is willing to take suggestions from Senate GOP and is confident that Sen. McConnell will come back with suggestions. Talks again about compromise.

- Sen Reid said he would be happy to look at alternatives and will give Senate GOP all the time they need.

- Democrats' plan is said to be on standby.

- Key vote in Senate is sheduled to be about midnight ET on Saturday.

- S&P says the US needs to keep its AAA.

- Steve Barrow of Standard Bank puts the odds of a downgrade at about 80%-90% and looksfor the dollar to suffer accordingly.

- Pres Obama said that Boehner plan does not resolve the problem and has no chance of passage.

- He also urged Democrats to find common ground, saying there is rough agreement on spending cuts.

- Obama urged American people to call Congress, keep up pressure and ask for a debt bill.

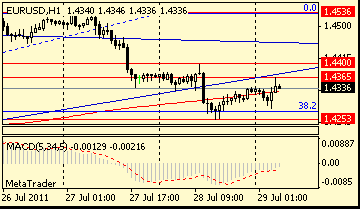

EUR/USD printed session highs on $1.4392. But rate failed to break above the figure and retreated to current $1.4366. Offers mentioned at $1.4400, extending to $1.4410 with stops above.

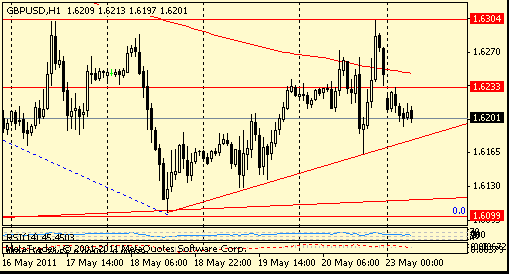

GBP/USD printed session highs on $1.6430 before retreated to figure. Rate earlier rallied from session lows around $1.6261 following the weak US GDP release. Offers placed at $1.6440, extending to $1.6450 with stops above. A break here to open a move toward $1.6470/80 ahead of $1.6495/00.

The majors recovered a bit off their worst levels of the session, but still hold large losses with all three trade down 0.8%.

The Nasdaq is pacing today’s decline with a loss of 1.1%.

The final July Consumer Sentiment Survey from the University of Michigan came in at 63.7, down slighlty from the preliminary reading of 63.8.

EUR/USD $1.4075, $1.4400, $1.4450

USD/JPY Y77.10, Y78.00, Y78.30, Y79.00

EUR/JPY Y112.60

AUD/USD $1.0800, $1.0850, $1.0965, $1.1000

U.S. stocks were headed for an early sell-off Friday after the government said economic growth slowed sharply in the second quarter.

U.S. stocks lost steam late in Thursday's session, pushing the Dow lower for the fifth straight session. It's all about the debt ceiling, which must be raised by Aug. 2, when the Treasury will no longer be able to pay all its bills.

Even if Boehner's plan does pass the House, Senate Majority Leader Harry Reid has promised the Democratic-controlled Senate will block it, and President Obama has threatened a veto.

Moody's said it may downgrade Spanish debt.

Economy: The government reported that second-quarter GDP growth was only 1.3%, up from a revised 0.4% rate in the previous three months. That was far worse than expected.

After the opening bell, the Chicago purchasing managers index and the University of Michigan consumer sentiment survey will be released.

Companies: Drugmaker Merck (MRK, Fortune 500) reported earnings of 95 cents per share - in line with analyst expectations. The company said it that it would reduce its workforce by 12% to 13% from 2009 levels by the end of 2015 as the next phase of a restructuring program.

Shares of Starbucks (SBUX, Fortune 500) were up 2.4% in premarket trading after the company beat earnings expectations on Thursday.

Dow member and oil giant Chevron (CVX, Fortune 500) will also report before the bell. Analysts are looking for Chevron to earn $3.56 a share.

EUR/USD takes some pause around $1.4345 and retreats a bit. Rate earlier rocketed after the dissapointing US GDP data. Offers in place at $1.4350/60. Rate currently holds around $1.4320.

Much weaker than expected US GDP report sends stock futures into dip red with the Dow futures down more then 100 points.

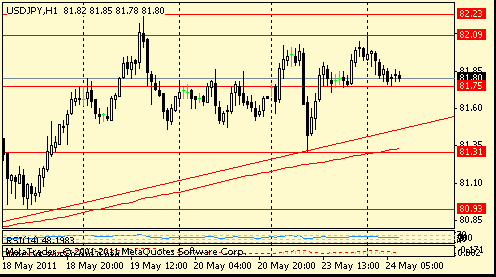

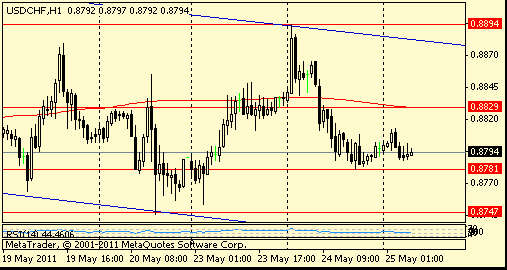

Dollar collapced and curently USD/CHF holds at a new record lows on Chf0.7910, while USD/JPY - at Y77.11.

Data released:

06:00 UK Nationwide house price index (July) 0.2% -0.2% 0.0%

06:00 UK Nationwide house price index (July) Y/Y -0.4% -0.8% -1.1%

06:00 Germany Retail sales (June) real adjusted 6.3% - -2.8%

06:00 Germany Retail sales (June) real unadjusted Y/Y -1.0% - 2.2%

06:45 France PPI (June) -0.1% -0.2% -0.5%

06:45 France PPI (June) Y/Y 6.1% 5.8% 6.0%

06:45 France Consumer spending (June) 1.2% 0.5% -0.8%

06:45 France Consumer spending (June) Y/Y 1.8% 0.4% -1.8%

08:30 UK M4 money supply (June) final -0.5% - 0.1%

08:30 UK M4 money supply (June) final Y/Y -0.7% - -0.2%

08:30 UK Consumer credit (June), bln 0.4 0.3 0.2

09:00 EU(17) Harmonized CPI (July) Y/Y preliminary 2.5% 2.7% 2.7%

The yen and Swiss franc rose as Moody’s Investors Service said it may cut Spain’s credit ranking and U.S. lawmakers delayed voting on a plan to raise the debt limit to avert a default.

The franc headed for an eighth monthly advance versus the greenback, the longest streak of gains in 17 years, while the Australian and New Zealand currencies declined.

The dollar headed for a fourth weekly loss versus the yen before a government report today that economists said will show growth slowed last quarter.

Gross domestic product expanded 1.8% in the three months ended June 30, compared with 1.9% in the previous quarter.

Spain’s Aa2 ratings were placed on review for possible downgrade by Moody’s.

EUR/USD printed a new session lows on $1.4228 before recovered to $1.4257.

GBP/USD initially fell to $1.6260 before back to $1.6290.

USD/JPY under pressure below session highs on Y77.80.

US data starts with the much-awaited GDP data at 1230GMT.

Data continues at 1345GMT when the Chicago PMI is forecast to hold steady at 61.1 in July. At 1355GMT, the preliminary Michigan Sentiment Index is expected to revised up to a reading of 64.0 in July.

USD/JPY declines and currently holds around Y77.55. Initial bids at Y77.35/30 a break to open barrier interest at Y77.25 and a combination of barrier/stops through Y77.00.

AUD/USD holds around $1.0944 as euro recovers off lows. Support on $1.0930/20 with a break under opens the way to $1.0870/60. Offers around $1.1000/10, larger offers at $1.1080.

- sees Irish GDP growth of 0.8% in 2011, 2.1% in 2012

- estimates HICP inflation at 1.0% in 2011, 0.6% in 2012

EUR/USD $1.4075, $1.4400, $1.4450

USD/JPY Y77.10, Y78.00, Y78.30, Y79.00

EUR/JPY Y112.60

AUD/USD $1.0800, $1.0850, $1.0965, $1.1000

The Employment Cost Index is expected to rise 0.5% in second quarter after the 0.6% rise in the previous quarter.

The Employment Cost Index is expected to rise 0.5% in second quarter after the 0.6% rise in the previous quarter.

Nikkei 9,833 -68.32 -0.69%

Hang Seng 22,420 -150.58 -0.67%

S&P/ASX 4,425 -39.13 -0.88%

Shanghai Composite 2,702 -7.05 -0.26%

Resistance 3: Y78.70 (area of Jul 22 and 26 high)

Resistance 2: Chf0.8180 (close price of the last week)

Resistance 3: $ 1.6470 (Jun 7 high)

Resistance 3: $ 1.4540 (Jul 26-27 high)

05:00 Japan Construction orders (June) Y/Y - 25.5%

06:00 UK Nationwide house price index (July) -0.2% 0.0%

06:00 UK Nationwide house price index (July) Y/Y -0.8% -1.1%

08:30 UK Consumer credit (June), bln 0.3 0.2

09:00 EU(17) Harmonized CPI (July) Y/Y preliminary 2.7% 2.7%

12:30 USA PCE price index (Q2) advance - 3.9%

12:30 USA PCE price index ex food, energy (Q2) advance - 1.6%

13:45 USA Chicago PMI (July) 60.6 61.1

13:55 USA Michigan sentiment index (July) final 64.0 63.8

© 2000-2026. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers