- Analytics

- News and Tools

- Market News

CFD Markets News and Forecasts — 28-04-2011

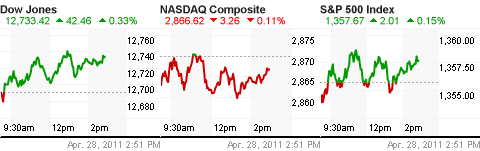

Stocks recently returned to session highs, but they have been unable to build on the move.

Despite the number of headlines for traders to act on, share volume remains unimpressive with hardly 600 million shares traded, so far, on the NYSE.

More than 100 companies are scheduled to report earnings after today's close. Another 40 or so are scheduled for tomorrow morning.

Trade is still choppy, but the Dow is on pace for its sixth gain in seven sessions. General Electric (GE 20.54, -0.11), a leader in the prior session, is down today, but Boeing (BA 78.01, +1.89) has been a source of strength as it bounces to its highest level in almost three years following positive analyst commentary.

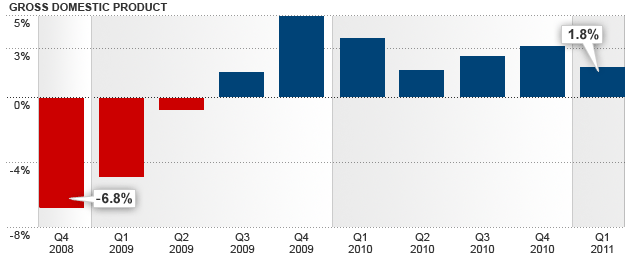

The Dollar Index fell to its lowest level in more than two years as the U.S. economy expanded in the first quarter at a slower rate than forecast, encouraging the Federal Reserve to keep borrowing costs low.

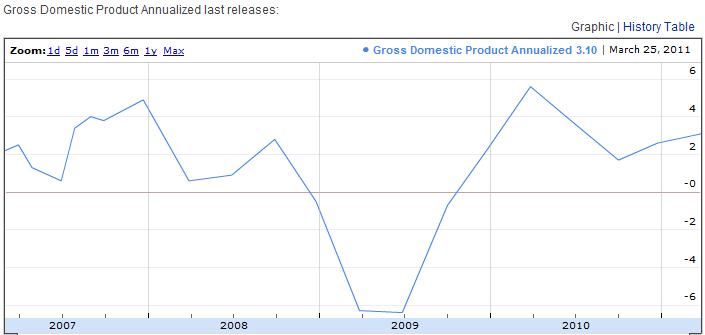

The U.S. currency fell against the euro and yen after the Commerce Department reported that gross domestic product rose at a 1.8 percent annual pace in the first quarter after a 3.1 percent rate of expansion in the last three months of 2010. The median forecast of economists was for a 2 percent pace of growth.

The yen appreciated versus most of its major counterparts after a report showed Japanese investors sold foreign assets last week.

The yen rallied today as Japanese investors were net sellers of foreign bonds during the week ended April 22. They sold 171.8 billion yen ($2.1 billion) in overseas bonds and notes and 5.6 billion yen in overseas stocks, according to figures based on reports from designated major investors released by the Ministry of Finance in Tokyo. They bought 14.6 billion yen in overseas short-term securities. The total net sale was 162.8 billion yen.

“The data is accelerating dollar weakness,” said Mark McCormick, a currency strategist at Brown Brothers Harriman & Co. in New York. “The yen is firmer today because it now seems that there is more of a potential for repatriation back into the economy, which would drive up demand.”

New Zealand’s dollar was one of the worst performers against the greenback after Reserve Bank Governor Alan Bollard called the currency’s recent advance “unwelcome.” The dollar sank a day after Fed Chairman Ben S. Bernanke said he was unsure when monetary stimulus will unwind.

A sudden flurry of selling recently backed down stocks. The move actually put the Nasdaq at a session low.

BMO says Q1 GDP shows "The U.S. economy has lost what little upward momentum it had, partly because of temporary factors like bad weather, lower defense spending and auto shutdowns related to Japan's crises, and partly because of not-so transitory factors like rising gasoline prices and state & local budget cuts."

Energy stocks are under stiff pressure this morning. Their collective slide of 0.9% comes amid a negative response to the latest report from Exxon Mobil (XOM 87.05, -0.73), which actually featured a better-than-expected bottom line. Fellow integrated play ConocoPhillips (COP 77.81, -2.02) has extended its prior session slide following its downgrade by analysts at Deutsche Bank.

In contrast, telecom is outperforming for the second straight session. The sector is up 0.6%. Sprint Nextel (S 4.93, +0.14) is a top performer in its space following its latest quarterly report, which featured stronger-than-expected results on both the top and bottom line.

EUR/USD $1.4810, $1.4700, $1.4660, $1.4615, $1.4600

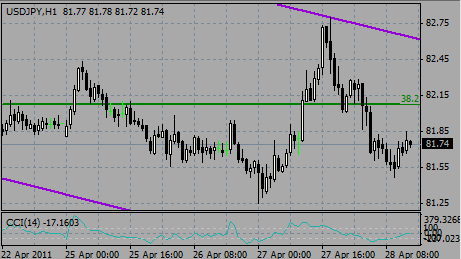

USD/JPY Y81.50, Y82.00, Y82.55, Y83.00

EUR/JPY Y120.00, Y121.95, Y122.60

GBP/USD $1.6550, $1.6500

USD/CHF Chf0.8755

EUR/CHF Chf1.3000

AUD/USD $1.0750

U.S. stock futures slumped after the government released data on gross domestic product and jobless claims before Thursday's opening bell.

Exxon Mobil reported a 69% jump in first-quarter profit of $10.7 billion. Investors weren't all that impressed.

Investors sent all three indexes to fresh multi-year highs Wednesday after Fed chief Ben Bernanke's first press conference.

Economy: On Thursday, the Department of Commerce released its report on first-quarter gross domestic product, showing that GDP expanded at an annual rate of 1.8% during the first quarter.

The government also reported its weekly initial jobless claims data. The Labor Department reported that jobless claims totaled 429,000 last week. Economists expected them to fall to 390,000. It also marked the third week in a row that jobless claims came in above the key 400,000 level.

Later in the morning, a report from the National Association of Realtors is expected to show a 1.7% rise in pending home sales for the month of March.

Companies: Procter & Gamble (PG, Fortune 500) reported an increase in quarterly net profits and sales but still disappointed investors. The company's stock slipped nearly 2% in premarket trading.

PepsiCo (PEP, Fortune 500) and Sprint Nextel (S, Fortune 500) also reported quarterly results before the market open. Pepsi's stock was flat in premarket trading while Sprint's stock rose about 3%.

After the closing bell, analysts expect Microsoft to post a quarterly profit of $4.8 billion, up 20% from a year earlier, on sales of $16.2 billion.

EUR/GBP tries to recover after earlier it fell from highs on stg0.8915. Offers still between stg0.8920/25 with options on stg0.8925 and stops above stg0.8930. Rate currently trades around stg0.8875 after it broke support at stg0.8880.

AUD/USD slid back below $1.0900, as rate extends its corrective pullback off overnight highs of $1.0948. The stall ahead of $1.0950 has prompted speculation that the level holds option barrier interest.

As GDP data came in expected, the weekly claims data higher than expected. Currently EUR/USD holds around $1.4811 after falling to a session low around $1.4785.

Median estimate for the first publication of GDP for Q1 is +1.8% y/y after +3.1% in Q2, wit promising employment numbers on the one hand and underlying weakness in the housing market on the other that has led a number of prominent institutions to downgrade their economic growth forecasts for Q1 and 2011 as a whole.

As a reminder, yesterday Bernanke said in the press conference that he believes GDP growth will be less than 2% as slower consumer spending and a wider trade deficit slowered economic activity at the start of the year.

Possible outcome:

Above estimates: A strong reading above 1.8% should give the USD some strength to correct the selling pressure. Data should ideally breach the psichological 2% band, this could trigger a strong rebound in the Dollar, aiming to set under $1.4800. Below this achievable break, not much support is seen until $1.4700, stronger support, ahead of $1.4650.

Below estimates: Should the number fall short of 1.8%, then the Dollar is poised to extend gains towards the next area of resistance at $1.4900. Upon the touch of this new high, the doors for $1.5000 big round number will get widely opened. From a weekly perspective, the chart does not show much resistance until $1.5120/30 area.

In line with expectations: Data in line with estimates may not be good enough for the Dollar. However, Euro may find it hard to overstrech much further. For these reasons, we favour quotes to consolidate near highs with the potential to see a pullback to $1.4700.

Data released:

06:00 Germany Import prices (March) 1.1% 1.1% 1.1%

06:00 Germany Import prices (March) Y/Y 11.3% 11.3% 11.9%

06:00 Germany Import prices excluding oil (March) Y/Y - 8.8%

06:45 France Consumer spending (March) -0.7% 0.3% 0.9%

06:45 France Consumer spending (March) Y/Y 2.6% 3.7% 5.5%

07:55 Germany Unemployment (April) seasonally adjusted -37K -32K -55K

07:55 Germany Unemployment (April) seasonally adjusted, mln - -

07:55 Germany Unemployment rate (April) seasonally adjusted 7.1% 7.0% 7.1%

The Dollar Index fell to its lowest level since 2008 as the Federal Reserve’s pledge to keep interest rates near zero to stimulate growth spurred investors to buy higher-yielding assets.

The Australian dollar climbed to a record against its U.S. counterpart amid speculation the South Pacific nation will raise rates to contain inflation.

“It’s still a broadly negative dollar story,” said Lee Hardman, a currency strategist at Bank of Tokyo-Mitsubishi UFJ Ltd.. “There’s not much change to the outlook for Fed policy. The downtrend for aggressive dollar selling is firmly entrenched.”

The dollar has lost 1.1% in the past week, extending this year’s decline to 6.9%. The yen has fallen 0.9% this week, and has lost 7.6% this year.

The Dollar Index fell for an eighth day, its longest losing run since March 2009, after Fed Chairman Ben S. Bernanke signaled yesterday in his first press conference following a policy decision that the central bank intends to maintain monetary stimulus.

Fed policy makers kept the target rate for overnight lending between banks at zero to 0.25%. The rate has remained at that level since December 2008.

Australia’s dollar appreciated as traders boosted bets that the central bank will increase borrowing costs. The Reserve Bank of Australia will raise its target rate of 4.75% by 25 basis points over the next 12 months, up from 19 basis points a week earlier.

EUR/USD corrected to $1.4795 before it rose to 17-months highs around $1.4880 earlier.

GBP/USD back to $1.6660 after rising up to highs near $1.6740.

USD/JPY fell to a session low on Y81.50 before back to Y81.82.

In the US, also at 1230GMT, the main release is the Q1 US GDP data and the April 23 week jobless claims data. The advance estimate for first quarter GDP is expected to be at a 1.8% rate of growth, down from the 3.1% gain in the previous quarter.

Jefferies: "Bernanke is in no hurry to remove accommodation".

HSBC: "The press conf gave the same message as before".

Gold continues to push higher and reached another all-time high today at $1534.05. Daily studies maintain bullish while in overbought territory with momentum reaching a 5-month high. Resistance seen at $1539.10 (the daily Bollinger band top), followed by a 4-week resistance line at $1562.30 and then a 12-month trend line at $1565.80.

The dollar sank to a three-year low against a basket of currencies and was at risk of a drop to $1.50 versus the euro.

The dollar slid across the board, with the Australian dollar challenging previous highs to a 29-year peak above $1.0900. Both the euro and sterling scaled 17-month highs.

Analysts said more dollar weakness was likely after the Federal Reserve said overnight that it would end its bond-buying programme in June as planned and appeared in no rush to tighten monetary policy further.

The dollar index has slid nearly 4 percent this month, on track for the biggest monthly decline since Sept. 2010 and bringing it closer to a record low of 70.698 hit in March 2008.

The euro hit a 17-month high above $1.48, its rise having gained steam after triggering stop-loss bids around that level and after breaching resistance around $1.4850.

The dollar gained no traction from a news conference by Federal Reserve Chairman Ben Bernanke on Wednesday where he forecast weaker U.S. growth in the first three months of 2011, though he attributed it to transitory factors. It was the first regularly scheduled briefing by a Fed chief in the central bank's 97-year history.

Sterling also hit a 17-month peak near $1.6750. Possible upside targets include the November 2009 high at $1.6879 and then the August 2009 peak of $1.7044. The 200-week moving average at $1.7005 may also serve as resistance.

The Australian dollar scaled a fresh 29-year high near $1.0950 and was last up 0.8 percent at $1.0943.

- Price pressures from whole range of sources

- Sterling aggravating UK price pressures

- Global price pressures will persist for some time

- Shouldn't wait for 'red' signal before rate hike

- Price pressures from whole range of sources

- Sterling aggravating UK price pressures

- Global price pressures will persist for some time

- Shouldn't wait for 'red' signal before rate hike

EUR/GBP breaks above resistance at stg0.8905 on the reported German name buys, with strong euro demand. Cross printed session high on stg0.8916. Resistance/offers seen between stg0.8920/25, with stops noted on a break of stg0.8930.

EUR/JPY Y120.00, Y121.95, Y122.60

GBP/USD $1.6550, $1.6500

USD/CHF Chf0.8755

EUR/CHF Chf1.3000

AUD/USD $1.0750

- Quake Rebuilding Efforts to Create New Demand;

- Japan Can Lead World in Energy, Ecology Saving;

- 1% Price Stability Reset After Board Shuffled;

- Need More Than Cost Cuts to Raise Productivity.

Hang Seng -0.37% 23,805.63

Shanghai Composite -1.31% 2,887.04

Nikkei +1.63% 9849.74

The yen touched the lowest in two weeks versus the euro as Asian stocks extended a rally in shares around the world.

Across the Atlantic, the Canadian February employment data is released at 1230GMT. In the US, also at 1230GMT, the main release is the Q1 US GDP data and the April 23 week jobless claims data. The advance estimate for first quarter GDP is expected to be at a 1.8% rate of growth, down from the 3.1% gain in the previous quarter.

The greenback earlier touched its lowest level since December 2009 on speculation the Fed will keep borrowing costs low.

Fed Chairman Ben S. Bernanke is due today to give his first press conference after a policy meeting.

The central bank held its target rate for overnight lending between banks at zero to 0.25%, as forecast. The benchmark has stayed at that level since December 2008.

“The economic recovery is proceeding at a moderate pace and overall conditions in the labor market are improving gradually,” the Federal Open Market Committee said in its statement after a two-day meeting.

The Fed announced in November it would buy $600 billion in Treasuries in an effort to stabilize the U.S. economy under the second round of quantitative easing.

Consumer prices increased in March for a ninth consecutive month, led by gains in food and fuel costs, according to the Labor Department. The U.S. unemployment rate dropped last month to a two-year low of 8.8%.

The economy grew at a 2% annual pace in the first quarter after a 3.1% rate of expansion in the last three months of 2010, according to the median forecast of economists before tomorrow’s report from the Commerce Department.

The outlook on Japan’s AA- local-currency government debt rating, the fourth-highest grade, was lowered to “negative” from “stable,” S&P said today, citing costs for rebuilding after the nation’s record earthquake on March 11.

The yen has weakened 5.2% over the past month. The dollar has declined 4%.

The Australian dollar touched a record on speculation the Reserve Bank of Australia will raise borrowing costs to contain accelerating inflation.

© 2000-2026. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers