- Analytics

- News and Tools

- Market News

CFD Markets News and Forecasts — 21-06-2011

EUR/USD quite volatile tosay ahead of the Greek confidence vote this evening. Rate currently holds around $1.4408. Session highs were earlier printed at $1.4420.

The Dow has drifted off of its session high. Among losers are just Boeing (BA 74.16, -0.36), Procter & Gamble (PG 64.79, -0.29) and United Tech (UTX 85.37, -0.18).

The dollar fell as stocks and commodities rose, reducing demand for a refuge as the Federal Reserve begins a two-day policy meeting.

The greenback weakened to the lowest versus the euro in almost a week. The shared currency rose as European leaders said a Greek default can be avoided amid speculation Prime Minister George Papandreou will win a confidence vote today.

The euro rose as Greece’s Papandreou seeks to secure multiparty support for his government’s austerity measures. That is a condition for receiving aid needed to avoid a default.

Greece needs parliamentary approval of a 78 billion-euro ($112 billion) package of budget cuts and asset sales.

The greenback remained weaker as National Association of Realtors data showed sales of existing homes decreased in May to the lowest level in six months. Purchases of existing U.S. homes fell 3.8% to a 4.81 million annual pace last month, in line with estimates.

Meanwhile, economists forecast the Federal Open Market Committee will keep the benchmark interest rate at zero to 0.25 percent tomorrow, where it’s been since December 2008.

Australia’s dollar declined after the nation’s central bank said domestic data had not added “any urgency” to the need for policy adjustment and it may be “prudent” to keep rates unchanged, according to minutes released today of a June 7 policy meeting.

The pound weakened as Bank of England Markets Director Paul Fisher said further bond purchases to stimulate the economy are possible.

Resistance 1: Y80.60

Resistance 1: Y80.40

Current price: Y80.11

Comments: Rate remains within the range, holding above strong support at Y80.00 (chsnnel line from Jun 08). Break under opens the way to Jun 08 lows around Y79.65/70 (Y79.60 - May 05 lows) and then - to Y79.10/00 (Mar 18 lows). Resistance comes at recent highs on Y80.40. Next band of resistance is around Y80.60 (61.8% Fibo of Y81.10 - Y80.00 decline).

Resistance 1: Chf0.8450

Current price: Chf0.8420

Support 1: Chf0.8370

Support 2: Chf0.8320

Support 3: Chf0.8080

Comments: Dollar weakens, heading to support channel from Jun 07 at Chf0.8370. Break under opens the way down to Chf0.8320 (record lows seen Jun 07 lows). Below support is near channel line from Feb on Chf0.8080. Resistance comes at recens highs on Chf0.8450, then - at Chf0.8520. Stronger level - at Chf0.8560/65 (channel line).

Comments: rate tries to recover with strong resistance remains at $1.6260 (50% Fibo of $1.6440 - $1.6080 decline). Clear break above $1.6260 opens the way up to $1.6300 (61.8%). Further band of resistance is around $1.6380 (recent highs). Minor support is around $1.6180, then - at $1.6120. Stronger support remains near $1.6080 (Jun 16 lows).

Resistance 2:$1.4460

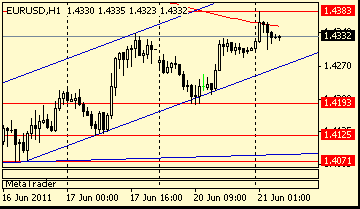

Comments: Rate challenges resistance at $1.4400 with a break above targets $1.4460/70 (channel line from Jun 16). Key level - at $1.4500 (Jun 14 high). Back under channel support line at $1.4280 to open the way down to $1.4200 and then - to support at $1.4120.

Strength in the tech sector lifted the Nasdaq to a gain of 2%. As a reminder, last week the Nasdaq was at its lowest level in six months. Heavyweights like Apple (AAPL 323.31, +7.99) have been the biggest drivers of the move.

Strength in the broader equity market has the S&P 500 up 1%.

EUR/USD holds around $1.4383 after it printed hourly high on $1.4388. Traders still remind about the semi-official supply ahead of $1.4400. Break above opens the way up to a tech resistance around $1.4415.

USD/JPY still holds within the narrow range, limited by Y80.13-Y80.23. Rate remains vulnerable to Greek comments. The market focus is on confidence vote for Greek Prime Minister George Papandreou. Bids mentioned at Y80.10/00 (Y80.02 - June 17/20 lows), further bids at Y79.95/90. Offers placed between Y80.30/35, with stops through Y80.40. A break here opens Y80.50/55 (also offers/stops). The rate currently trades Y80.10.

Natural resource plays have sprinted out to an impressive lead over the broad market, which is currently up with a solid gain of its own. Strength in the materials space has the sector up 1.2%. As for energy stocks, they are up 1.1%, as a group.

Meanwhile, financials and tech stocks continue to struggle to attract meaningful support. In turn, both sectors are up with gains of only 0.3%. The two, which are frequently regarded as broad market drivers for their relative market weight and pervasiveness in the economy, have mostly traded in lackluster fashion in recent weeks.

Economists expect the pace of existing home buying to slow to 4.79 million annualized units, down from 5.05 million units in April.

U.S. stocks were set to extend gains Tuesday, following world markets higher, as investors awaited a confidence vote for Greek Prime Minister George Papandreou.

The vote of confidence, held by the Greek parliament, may determine whether Papandreou's government has the strength to avoid a default and secure a rescue package.

Despite ongoing anti-government protests, investors are largely expecting Papandreou to win the vote, said Mark Luschini, chief investment strategist, Janney Montgomery Scott.

U.S. stocks managed gains Monday, even as investors remained cautious about Greece's debt crisis.

World markets:

Economy: Wall Street will get May existing home sales data from the National Association of Realtors at 14:00 GMT. Economists expect the pace of existing home buying to slow to 4.79 million annualized units, down from 5.05 million units in April.

Companies: Credit union regulators sued JPMorgan (JPM, Fortune 500) and Royal Bank of Scotland (RBS) for selling mortgage bonds that were designed to fail -- leading federal credit unions to lose more than $800 million. Shares of JPMorgan rose 0.8%, while Royal Bank of Scotland's stock edged lower.

Shares of Bed Bath & Beyond (BBBY, Fortune 500) jumped more than 4% after Jefferies reaffirmed its "buy" rating and $62 price target for the company's stock -- expecting Bed Bath & Beyond to beat earnings estimates in the first quarter.

Best Buy Inc. (BBY, Fortune 500)'s board authorized a new $5 billion share repurchase program to replace its previous $5.5 billion share repurchase program. Shares of the company rose 4.3% in premarket trading.

Shares of Renren (RENN) gained 2.5% before the market open, after the Chinese social-networking site reported a narrower loss in the first quarter, as sales increased 47%.

Drugstore chain Walgreens (WAG, Fortune 500) reported third-quarter results before the opening bell that beat expectations, posting record earnings and revenue.

Oil for July delivery gained $1.08 to $94.34 a barrel.

Gold futures for August delivery rose $3.10 to $1,545.10 an ounce.

Bonds: The price on the benchmark 10-year U.S. Treasury edged lower, pushing the yield up to 2.98% from 2.96% late Monday.

The dollar fell against most of its major peers before a report that’s predicted to show new home sales in the U.S. slumped in May, bolstering the case for the Federal Reserve to keep interest rates at a record low.

Purchases of existing U.S. homes decreased 5% to a 4.8 million annual rate in May, the weakest since November, according to the median forecast of economists. April home prices fell 0.3%, the Federal Housing Finance Agency will say tomorrow, according to projections in a separate survey.

Fed Vice Chairman Janet Yellen said June 9 that a “long, drawn-out recovery” was likely for the U.S. housing market. “For its part, the Federal Reserve will continue to use its policy tools to support the economic recovery,” she said.

The dollar weakened to an almost one-week low versus the euro before Fed policy makers begin a two-day meeting amid signs the U.S. economy is slowing. The 17-nation currency rose as European leaders said a Greek default can be avoided and before Prime Minister George Papandreou faces a confidence vote today. It pared gains after a report showed German investor confidence fell.

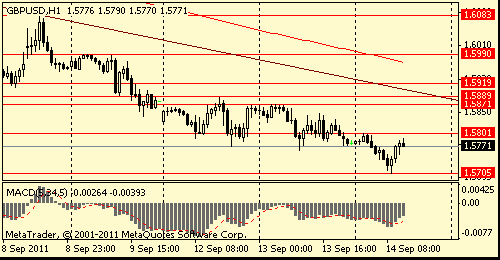

The pound weakened 0.3 percent to 88.58 pence per euro and was little changed at $1.6195 as Bank of England Markets Director Paul Fisher said further bond purchases to stimulate the economy are possible.

- Privatisation is essential from Greece

Aussie is trading on a bid tone tracking EUR/USD higher. Support remains at $1.0540/30, ahead of bids behind at $1.0500/1.0490. Closest resistance at session high $1.0615/20, a break here opens $1.0675/80.

European shares rose early on Tuesday on expectations that euro zone policymakers can come up with a solution to save Greece from missing its July debt payment and avoid short-term contagion risk to the peripherals.

One in three chance rating may be downgraded in next 3-years.

Rate slips back to retest recent ZEW react lows at $1.4315. Next support seen into $1.4300, ahead of $1.4270. Offers spotted at $1.4335/40 and on approach to $1.4375/80.

Cross has triggered stops through Y114.95 as the euro loses ground. Closest support eyed at Y114.70/65 (5-DMA/session low). A break here to open Y114.30 area. Offers remain at Y115.20/25.

EUR/USD $1.4350, $1.4300, $1.4275, $1.4230

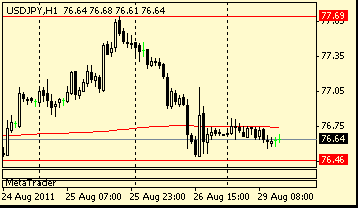

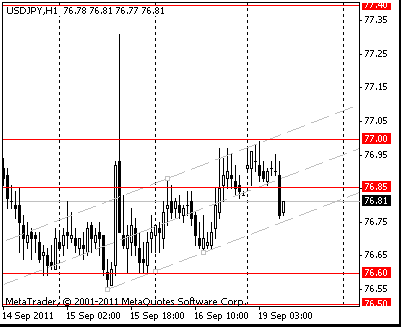

USD/JPY Y80.00, Y80.50, Y80.75, Y81.00, Y81.15

GBP/USD $1.6230, $1.6170

EUR/GBP stg0.8800

USD/CHF Chf0.8420

AUD/USD $1.0420, $1.0550, $1.0605, $1.0675

NZD/USD $0.8000

Data:

The main core-European release for Tuesday will be the German ZEW data, which is expected to weaken to readings of 90.0 for the current assessment and -3.0 for the economic sentiment index.

Events in the UK start at 0810GMT, when Bank of England MPC member Paul Fisher delivers a speech, followed at 0830GMT by the May Public

Sector Finances are due.

The euro rose against the majority its most-traded counterparts after European leaders reassured investors a Greek default on its debts can be avoided, easing concern about a spreading regional credit crisis.

The common currency erased its decline versus the yen and dollar, as Luxembourg’s Jean-Claude Juncker said Italy was not in danger amid the euro area’s debt crisis. The Swiss franc remained higher against all its most-traded counterparts as Juncker said Greek Prime Minister George Papandreou had assured him the government would do everything ensure financial aid before the Greek parliament takes no confidence vote in his government tomorrow.

Greece needs parliamentary approval of a 78 billion-euro package ($111.6 billion) of budget cuts to ensure the payment of a fifth loan under last year’s 110 billion-euro bailout.

The new Greek finance minister, Evangelos Venizelos, who was named in Papandreou’s cabinet overhaul three days ago, came to Luxembourg with a “strong commitment” to the planned cuts that provoked street protests last week.

The main core-European release for Tuesday will be the German ZEW data, which is expected to weaken to readings of 90.0 for the current assessment and -3.0 for the economic sentiment index.

Events in the UK start at 0810GMT, when Bank of England MPC member Paul Fisher delivers a speech, followed at 0830GMT by the May Public

Sector Finances are due.

Resistance 2: Y81.00 (Jun 3, 15 and 16 high)

Resistance 3: Chf0.8550 (Jun 15-16 high)

Resistance 3: $ 1.6410 (resistance line from May 2)

Resistance 3: $ 1.4500 (area of Jun 14 high)

04:30 Japan All industry index (April) 1.6% -6.3%

© 2000-2026. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers