- Analytics

- News and Tools

- Market News

CFD Markets News and Forecasts — 19-11-2021

- XAG/USD finishes the week on the wrong foot, despite falling US bond yields.

- XAG/USD plummeted in the day as risk-off market mood boosts the greenback.

- Fed’s Waller and Clarida would like a faster bond taper.

- XAG/USD Technical outlook: An inverted head and shoulders target the $28.20-30 range.

As Wall Street closes, silver (XAG/USD) finished the session in the red, down almost 1%, at $24.58 at the time of writing. Friday’s session witnessed a downbeat market sentiment in the equity markets. The S&P 500 and the Dow Jones Industrial printed losses between 0.11% and 0.74%. The outlier was the Nasdaq 100, gaining 0.56%. Safe-haven currencies finished the day in the green in the FX market, while risk-sensitive currencies, like the AUD, the NZD, and the GBP, fell.

In the overnight session, silver remained subdued, trendless trading around the $24.75-93 region. However, some fed speakers spurred demand for the greenback throughout the American session, ultimately affecting the white metal, which plunged to the $24.50 area.

Fed’s Waller and Clarida would like a faster bond taper

On Friday, Fed Governor Christopher Waller indicated that the Federal Reserve may double the pace of its QE to $30 billion per month to end by April of 2022. Waller added that accelerating the rhythm would give the US central bank space for rate hikes as soon as Q2 of 2022.

Later during the day, Fed’s Vice Chairman Richard Clarida said that it “may very well be appropriate” to discuss accelerating the pace of the bond tapering, in line with St. Louis President James Bullard. Further noted that he sees upside risks to inflation and added that the economy is very strong position at that it looks as though Q4 is going to be very good.

The 10-year Treasury yield closed at 1.55% in the bond market, down three and a half basis points.

XAG/USD Price Forecast: Technical outlook

-637729570768222399.png)

Silver (XAG/USD) portrays that an inverted head-and-shoulders in the daily chart just formed. However, it would need a confirmation above the neckline, though Friday’s price action witnessed a daily close below the neckline. Despite the abovementioned, the non-yielding metal has an upward bias in the near term, with the 50 and 100-day moving averages (DMA’s) residing below the spot price.

Nevertheless, to accelerate the uptrend, silver bulls would need to reclaim the 200-DMA at $25.26. That outcome would open the door for further gains, though XAG/USD bulls would find some hurdles on the way north.

The first resistance would be the August 4 high at $26.00. A sustained breach of the latter would expose July 14 high $26.44, followed by the psychological $27.00.

On the flip side, failure the first support would be the 100-DMA at $24.06

- GBP/JPY pulled back sharply on Friday amid a broader downturn in risk sentiment, but found good support in the mid-152.00s.

- The pair may well struggle next week if risk appetite continues to worsen and it breaks key support.

GBP/JPY came under pressure on Friday, dropping back from Asia Pacific levels close to 154.50 to as low as 152.50 in the late European morning and in doing so dropped below its 50-day moving average at 153.47. The pair dropped back sharply as a result of a broad deterioration in risk appetite due to lockdown concerns in Europe that saw risk-sensitive currencies (like GBP) dumped in favour of safe-haven currencies (like JPY).

But the pair found decent support just above 152.50, given that this level also coincides with the prior monthly lows set last Thursday and Friday. Buying interest in the mid-152.00s was likely heightened given the proximity to the pair’s 200DMA, which resides at 152.30. Ahead of Friday FX market close and as trading conditions die down, the pair has managed to recover back to the north of the 153.00 level to trade in the 153.20s, with the 50DMA for now acting as resistance. At current levels, the pair trades with losses of about 0.6% on the day.

If the European Covid-19/lockdown news continues to worsen over the weekend, there is every chance that the broader market’s bid for havens may continue into next week. In this scenario, GBP/JPY could well be at risk of breaking below support in the mid-152.00s and its 200DMA. From a technical standpoint, this would be bearish, as there are no further key areas of resistance for the pair all the way down to the 149.00s.

While GBP is vulnerable to a downturn in sentiment, domestic UK fundamentals, for now, do not seem to provide too much reason to be bearish GBP. It seems highly likely that in December, the BoE will become the first major central bank to start hiking interest rates post-Covid-19. On Friday, BoE Chief Economist Huw Pill said that the burden of proof was on those who wanted to wait to hike rates, not on those who wanted to get the hiking cycle started. Central bank policy divergence, thus, leans in favour of a higher GBP/JPY.

Meanwhile, the Covid-19 situation in the UK is nowhere near as dire as it is in mainland Europe. Infection rates in the UK have been broadly stable over the past few months and the country’s booster vaccine rollout, which has already now more than covered the most vulnerable categories, has already been hailed a success. While lockdowns might be a story for the EU, they may not be for the UK this winter.

- NZD/USD drops below the figure, amid broad US dollar strength across the board.

- COVID-19 cases increase in Europe, spurred demand for safe-haven assets.

- Fed’s Waller and Clarida: Aims for a faster QE pace so that the US central bank could have some space to maneuver.

- Money market futures have priced in a 25 basis point increase by the RBNZ on its November 24 Monetary Policy Meeting.

The NZD/USD slumps for the third week in a row, trading at 0.6996 during the New York session at the time of writing. Dismal market sentiment in the financial markets spurred demand for safe-haven currencies, like the US dollar, the Japanese yen, and the Swiss franc. Further, major US equity indices fall, except for the tech-heavy Nasdaq 100, gaining 0.56%.

COVID-19 cases increase in Europe, dent the market sentiment

As the weekend looms, a COVID-19 fourth wave in Europe clouds the economic outlook. Higher cases in Eastern Europe threaten that an economic slowdown is around the corner. Austria reimposed coronavirus restrictions, with a lockdown of 20 days for vaccinated and unvaccinated people. Meanwhile, in Germany, the situation is no better, as some parts of the country closed non-essential business, while the Netherlands has already ordered shops and bars to close early.

Moving back to the NZD/USD pair, the overnight session witnessed a 50-pip drop in just three hours. It broke some pivot-points support levels on its way down, but the move was capped around the 0.6990 area, in the vicinity of Thursday’s low. Further, as market liquidity evaporated as European traders head into the weekend, the pair remains subdued within the 0.6990-0.7020 range.

In the macroeconomic docket, it was light for New Zealand. In the US, Fed speakers crossed the wires.

On Friday, Fed Governor Christopher Waller suggested that the US central bank might double the pace of its QE to $30 billion per month to end by April of 2022. Further added that accelerating the rhythm would give space to the Fed for rate hikes as soon as Q2 of 2022.

After Walles spoke, Fed’s Vice Chairman Richard Clarida said that it “may very well be appropriate” to discuss accelerating the pace of the bond tapering, in line with other Fed policymakers. Further added that he sees upside risks to inflation and added that the economy is very strong position at that it looks as though Q4 is going to be very good.

NZD/USD traders’ focus will turn on the New Zealand Retail Sales and the Reserve Bank of New Zealand Monetary Policy Meeting in the upcoming week. Meanwhile, in the US economic docket, Durable Good Orders, GDP for Q3, the Federal Reserve favorite gauge for inflation the PCE and FOMC minutes, would entertain traders.

- EUR/USD is set to close out the week below 1.1300, a potentially bearish signal for next week.

- The pair was weighed heavily by European lockdown concerns and later hawkish Fed commentary.

Things are not looking good for EUR/USD, with the currency pulling back beneath the psychologically important 1.1300 level as FX volumes thin and the weekend approaches. Technicians may well view failure to close to the north of 1.1300 as a bearish signal heading into next week. Since EUR/USD broke below a long-term descending trend channel, its not particularly surprising to have seen the pace of the sell-off pick up in recent days. Bearish technicians will have their sights firmly set on a test of the next key area of support around the 1.1150-1.1180 area.

Recapping the day's action then: EUR/USD started the session off above 1.1370, but as the news hit on Friday morning that Austria was to implement a full lockdown and that Germany soon follows, the pair dropped like a stone. Analysts unanimously agree that widespread lockdowns in Europe over the coming months will deliver a significant blow to the Eurozone growth (meaning negative revisions to forecasts), giving the ECB more reason to be dovish in the face of high inflation. By the late European morning, the pair had printed a fresh 16-month lows at 1.12501. Some profit-taking then allowed it to recover back as high as 1.1320 as the US session began, but hawkish vibes from key Fed members which injected upside into short-end and real US bond yields gave USD a boost.

For reference, Governor Christopher Waller called for an accelerated QE taper and said that rate increases could be appropriate as soon as Q2 2022. This followed a similar message from St Louis Fed President James Bullard, who earlier in the week urged the Fed to double the pace of its QE taper to $30B per month in January. Shortly after Waller had finished orating, it was influential Vice Chairman of the FOMC Richard Clarida’s turn. He didn’t speak much on policy but did say that it may be appropriate to discuss an accelerated QE taper in December. Plenty more FOMC members will hit the wires next week market participants will be eager to assess the appetite on the Committee for an accelerated QE taper and earlier rate hikes.

Looking back on the week in its entirety, it’s been an ugly one. At present levels, the pair is set to close with weekly losses of about 1.4%, its worst performance since mid-June. Strong US Retail Sales, NY and Philly Fed survey, Weekly Jobless Claims and Building Permits data, as well as on Friday all helped the dollar push on. Meanwhile, the resolutely dovish tone of core ECB members and the escalating Covid-19 crisis in Europe hurt the single currency.

- USD/CHF advance on risk-off market sentiment amid falling US bond yields.

- Monetary policy divergence between the Fed and the SNB favors the US dollar.

- USD/CHF Technical outlook: Mild-bullish but would need to break above 0.9291 to cement the upward bias.

The USD/CHF rebounds from two days of consecutive losses, rises 0.39%, trading at 0.9289 during the New York session at the time of writing. The greenback benefits from the safe-haven status, which also has the Swiss Franc. However, central bank policy divergence, with the Fed reducing its QE program and looking forward to hiking rates, while the Swiss National Bank would maintain its loose monetary policy.

Broad US Dollar strength depreciates the Swiss franc

In the meantime, the US Dollar Index, which tracks the greenback’s performance against a basket of six rivals, advances 0.52%, reclaiming the 96 figure at 96.03, acting as a tailwind for the USD/CHF pair.

In the overnight session, the USD/CHF reached a daily low at 0.9242, attributed to risk-off market sentiment and falling US T-bond yields. When the European session began, COVID-19 news from Austria reimposing lockdowns for 20 days to vaccinated and unvaccinated people worsened the market sentiment. Additionally, Germany’s coronavirus cases increased the infection rate pace, reporting 52,970 new cases on Friday, threatening to slow down the largest economy of Europe.

That propelled investors toward US dollar-denominated assets, boosting the buck. Nevertheless, as the New York session progresses, the US T-bond yields keep falling with the 10-year benchmark note rate at 1.534%, down five basis points.

USD/CHF Price Forecast: Technical outlook

The USD/CHF has an upward bias, as depicted by the daily chart, with the daily moving averages (DMA’s) located below the spot price, acting as support. However, the uptrend seems weaker than USD bulls expected because the spot price remains short of the November 18 high at 0.9291.

To further cement an upward bias in the USD/CHF pair, USD bulls need a daily close above the former. That outcome would expose 2021 swing high at 0.9473, but it would find some hurdles on the way north. The first resistance would be the November 17 high at 0.9330, followed by the September 30 high at 0.9368.

- Spot gold has slipped in recent trade amid a risk in short-end yields prompted by hawkish Fed speak.

- XAU/USD broke out to fresh two-week lows under $1850.

Spot gold (XAU/USD) prices have come under pressure in recent trade having broken below key support and amid a rise in short-end US yields. Prices, which shot up last week amid demand for inflation protection in wake of a much hotter than expected US inflation report, had been consolidating within a pennant structure. However, on Friday, spot gold broke to the south of this pennant, triggering a bout of technical selling that even pushed XAU/USD prices below last week’s lows at $1850. Having carved out fresh weekly lows around $1844, prices are now consolidating just to the south of the $1850 mark. Gold bears may now target a move down to the next key area of resistance around $1833.

-637729430339211593.png)

Hawkish Fed

The technical break to the downside coincided with a sharp uptick in short-end US yields (as well as a pickup from lows across the US yield curve), which was itself triggered by hawkish Fed commentary. 2-year yields were down as much as 5bps at 0.45% on Friday, but are now back to flat around 0.50%. Short-end real yields are also higher on Wednesday, with the 5-year TIPS yield up 6bps to -1.85%. Higher yields increase the opportunity cost of holding non-yielding precious metals, thus weighing on the demand for gold.

In terms of the latest from the Fed; Governor Christopher Waller called for an accelerated QE taper and said that rate increases could be appropriate as soon as Q2 2022. Shortly thereafter, influential Vice Chairman of the FOMC Richard Clarida said that it could be appropriate to discuss an accelerated QE taper in December. Plenty more FOMC members will hit the wires next week market participants will be eager to assess the appetite on the Committee for an accelerated QE taper and earlier rate hikes.

- AUD/USD slumps during the New York session, down almost half percent.

- Increasing COVID-19 cases in Eastern Europe, Austria's lockdowns, and Germany's possibility of reimposing restrictions dampened investors' mood.

- AUD/USD Technical outlook: Negative below the downtrend at 0.7577 – Commerzbank.

The AUD/USD extends its three-week slump, a 300pip slump, trading at 0.7243 during the New York session at press time. In the overnight session, the Australian dollar tried to pare some of its weekly losses. However, it failed to break the robust resistance area near the R1 daily pivot point level, retracing down to 0.7228, breaking support levels on the way down.

The risk-off mood in the market dampened the prospects of risk-sensitive currencies like the AUD, the NZD, and the GBP. Contrarily, safe-haven peers like the Japanese yen and the greenback are the winners of the day. Factors like the fourth-wave COVID-19 cases spike in Eastern Europe, alongside Germany, spurred demand for the US dollar.

Meanwhile, the US Dollar Index advances at press time, closing to the 96.00 figure, on Federal Reserve Vice-Chairman Richard Clarida's comments that may be appropriate in December to discuss speeding QE taper. He added that there are upside risks to inflation, that the economy is in a very strong position at that it looks as though Q4 is going to be very good.

AUD/USD Price Forecast: Negative below the downtrend at 0.7577 – Commerzbank

According to Karen Jones, Team Head FICC Technical Analysis at Commerzbank, the aussie would decline towards the August low at 0.7106 on a break below 0.7250.

She added, "failure at 0.7250 will target the 29th September low at 0.7171 and the August low at 0.7106." Further noted that "Initial resistance is the 55-day ma at 0.7348 then 0.7430 the 9th November high and the 20-day ma at 0.7409. Above here lies the 0.7477 3rd September high, and we look for the market to fail in this vicinity." Jones further noted that long-term bearish pressure would be maintained below the 0.7534/77 area.

- XAU/EUR is back to flat in the EUR 1630 region having hit 14-month highs earlier in the session.

- Gold has been broadly weighed in recent trade amid hawkish vibes from Fed policymakers.

Euro-denominated spot gold (XAU/EUR) printed fresh 14-month highs on Friday at EUR 1653, but has since pulled back to the EUR 1630 area. On the day, prices are now flat versus more being up more than 1.0% when at highs. However, on the month, euro-denominated gold’s price gains still stand at close to 6.0%.

The pair was boosted early during Friday’s European session amid a ramp-up in Covid-19 fears on the continent after Austria announced a lockdown to start on Monday and German officials refused to rule out that they could follow suit. The euro weakened broadly as a result and is still the underperforming G10 currency on the day.

But gold prices have broadly weakened over the last few hours amid what has turned out to be quite a sharp pick up in short-end US real and nominal yields. The yield on the US 5-year TIPS bond is up 8bps on Friday, while in recent trade the nominal 2Y yield has eroded earlier losses of as much as 5bps to trade flat on the day around 0.50%.

The move higher in yields that has weighed on gold followed a succession of hawkish Fed commentary. Governor Christopher Waller called for an accelerated QE taper and said that rate increases could be appropriate as soon as Q2 2022. Shortly thereafter, influential Vice Chairman of the FOMC Richard Clarida said that it could be appropriate to discuss an accelerated QE taper in December. Plenty more FOMC members will hit the wires next week market participants will be eager to assess the appetite on the Committee for an accelerated QE taper and earlier rate hikes.

Vice Chair of the FOMC Richard Clarida said on Friday that it "may very well be appropriate" to discuss accelerating the pace at which the Fed is winding down its bond-buying programme at the December policy meeting. Speaking at the San Francisco Fed's 2021 Asia Economic Policy Conference, he added that there are upside risks to inflation, that the economy is in a very strong position at that it looks as though Q4 is going to be very good.

Market Reaction

The Dollar has seen some modest strength in recent trade after Clarida alluded to an accelerated pace of QE taper. Clarida is seen as the Fed's most important "thought leader" given that he is actually an economist by trade, versus Fed Chair Jerome Powell being a lawyer. If he is open to the idea of an accelerated QE taper, it is much more likely to actually happen. Fed Governor Christopher Waller called for an accelerated QE taper earlier in the session and St Louis Fed President, who is a 2022 voter, called for the same earlier in the week.

Bost suggested doubling the pace of QE taper to $30B per month, meaning the taper would end in April. An earlier end to the QE taper would bring forward when the Fed would be able to lift interest rates. Hence, short-end US yields have risen in recent trade; US 2-year yields are now flat on the day at 1.50% having been as low as 0.45% earlier in the session.

- USD/CAD advances for the fifth consecutive week, up some 0.25%.

- The US dollar advances firmly, despite falling US bond yields.

- USD/CAD Technical outlook: A break above 1.2654 would expose the 1.2800 figure.

The USD/CAD climbs during the day, looking to close on the upside for the fifth week in a row, trading at 1.2632 at the time of writing. As the weekend approaches, the USD/CAD bulls keep pushing the pair towards higher prices, despite the Bank of Canada (BoC) hawkishness in the last two months. USD bulls benefitted from the Fed’s announcement of a bond tapering in the November 3 monetary policy meeting, which spurred a US 10-year Treasury yield spike above 1.60%.

However, US bond yields are plummeting in the day, with the 10-year at 1.528%, falling almost six basis points, at press time. Further, the greenback gains 0.30% with its US Dollar Index, sitting at 95.82, well below the weekly tops, around 96.00. Then how is it possible that the USD/CAD pair is edging higher? The answer lies in falling crude oil prices.

Developments in the last three days in the oil market that involved the White House and Asian allies accorded to “intervene” in the crude oil market, as high energy prices threaten to weaken the global economic growth. Authorities in China have already said that they plan to tap some of their oil reserves.

Goldman Sachs commodity strategists noted that the market has priced in the supply of 100M barrels. They added that it might limit the scope for further downside due to the reserve release news. At press time, Western Texas Intermediate (WTI) is trading at $75.31, down some 3.71%.

USD/CAD Price Forecast: Technical outlook

-637729384145428832.png)

As the weekend approaches, the USD/CAD bulls keep pushing the pair towards higher prices, though they found strong resistance at the October 3 high, at 1.2654. Worth noticing that swing high is also a weekly resistance that USD bulls fail to break. However, a breach of the latter would expose the confluence of a downslope resistance trendline and the September 29 high around the 1.2770-85 area. A sustained break above the former would expose September 20 high at 1.2895.

On the flip side, failure of a daily close above the October 3 high would add additional pressure on the pair. The first demand zone on the way south would be the 100-day moving average (DMA) at 1.2549, followed by the 50-DMA at 1.2528. A breach of the latter could send the USD/CAD tumbling towards the November 15 low at 1.2492.

How much stronger can the Swiss franc get?, asks analysts at MUFG Bank. The Swiss franc reached levels not seen since 2015 versus the euro. According to them, if EUR/CHF breaks under 1.0500, it could spark a flurry of buying and a surge stronger.

Key Quotes:

“The Swiss franc has continued to perform well and is in focus today after EUR/CHF broke notably below the 1.0500 level for the first time since July 2015 – not even through the worst point of turmoil last year did EUR/CHF break the 1.0500 level. So this is significant and highlights underlying and persistent CHF strength. This strength in 2021 has been since March. The rise in global yields in Q1 helped fuel CHF selling but since the narrative changed to focusing on inflation concerns and supply constraint issues, CHF has trended stronger versus EUR.”

“While global inflation may ease SNB concerns and offer the prospect of a less active fight against CHF appreciation, we suspect at some point the markets may force the hand of the SNB to intervene and limit CHF strength from a move beyond parity.”

Federal Reserve Board of Governors member Christopher Waller on Friday suggested that if the bank was to double the pace of its QE taper (to $30B per month), then the taper could conclude by the start of April. That, he added, would give the Fed more policy space for rate hikes as early as Q2. St Louis Fed President James Bullard has recently also suggested doubling the pace of QE taper to $30B per month, though Bullard said this could make way for hikes as soon as Q1, earlier than what Waller said.

Waller said that he would rather end the QE taper before raising interest rates, a preference so far espoused by all other Fed policymakers. Waller added that he was concerned that markets don't believe that the Fed can get inflation under control in the next three to five year and that it is very important that the Fed maintains its credibility on inflation.

For reference, 5-year break-even inflation expectations (the difference between the nominal five-year yields and the inflation-protected five-year yield) went above 3.0% in November for the first time ever. The 5-year inflation-protected bond only started trading in 2004, meaning this measure of inflation expectations cannot be calculated any further back. Some have argued a rise this far from the Fed's 2.0% target constitutes the de-anchoring of inflation expectations.

Market Reaction

FX markets have not seen any notable reaction to these comments. Traders await a speech from Fed Vice Chair Richard Clarida at 1715GMT.

Despite falling sharply and reaching levels under 1.1300 (EUR/USD), analyst at MUFG Bank consider there remain factors that could encourage further declines going forward for the euro. They see the negative momentum around the euro likely to persist.

Key Quotes:

“Our FX forecasts have shown EUR as the laggard over the forecast horizon given the scope for the ECB to remain well behind most other G10 central banks in hiking rates. In October, there was a notable shift in rate expectations higher that dragged even EUR rates higher. The 3-year forward OIS for EUR turned positive in October but economic developments in the euro-zone lately and ECB communications have driven rates back into negative territory.”

“The economic risks have certainly deteriorated and while those risks may be better priced now, things can still get worse. Austria today announced a full lockdown with covid risks elevated across numerous euro-zone countries. The shifting economic risk profile could quickly change what markets expect from the ECB at its December policy meeting. Suddenly, the ECB may have strong justification for maintaining a more dovish stance through a larger or longer APP program. Developments in the coming days will be key. Secondly, we have the minutes from the last FOMC meeting next week.”

“The September BoP data released today from the ECB highlighted negative portfolio flows at that point. Euro-zone investors bought EUR 27.7bn worth of foreign long-term debt securities and foreign investors sold EUR 30.8bn. With global yields set to rise notably further relative to the euro-zone this is a factor that could further weigh on EUR performance over the coming months.”

“While we have already seen a sharp drop in EUR/USD, there remains scope for this to continue over the short-term at least.”

- The S&P 500 is trading flat and is resilient to global risk off amid strength in the tech sector.

- Passage of Biden’s $1.75T BBB spending package in the House failed to lift the mood for cyclical stocks.

US equity markets have so far proven broadly resilient despite a downturn in global risk appetite triggered by fears about Europe heading back into lockdown. While major European equity bourses nurse losses of anywhere between 0.2-1.7% on the session, the S&P 500 is currently trading flat at the 4710 mark, only a few points away from record highs printed at the start of the month at 4718.50.

The resilience of the S&P 500 owes to its much heavier weighting towards the technology sector than in European indices. The Nasdaq 100 (a proxy for the Tech sector) is currently trading higher by 0.7% on the session amid notable gains in big tech names who all did very well out of the pandemic. The Nasdaq 100 index on Friday rose above the 16.5K level for the first time and is has even managed to clinch the 16.6K mark. “Stay-at-home names” like Netflix, which benefit from increased engagement when people spend more time at home during lockdowns, gained on Friday.

A sharp drop in long-term US bond yields amid a heightened demand for safe-haven assets is helping the duration-sensitive tech sector. Lower bond yields reduce the opportunity cost of owning “growth stocks” (which tech stocks normally are), which are stocks whose valuation is disproportionately based on expectations for future earnings growth rather than current earnings.

The Dow, which is less weighted towards big tech, fell 0.5% on Friday. The news that the US House of Representatives had passed US President Joe Biden’s $1.75T “Build Back Better” social spending package failed to boost cyclical stocks (stocks whose performance is more closely correlated to the economy). That’s probably because there is no guarantee the bill will pass the Senate; moderate Democrat Senator Joe Manchin is worried about inflation and reportedly wants to delay further fiscal stimulus into 2022.

The drop in earnings weighed on bank stocks, with the S&P 500 financials index dropping more than 1.0%, weighing on the Dow. Energy stocks also performed poorly amid sharp downside in crude oil prices, also weighing on the Dow. The S&P 500 energy sector was down nearly 4.0%.

Hawkish Fed?

Equity investors have also been keeping an eye on commentary from Federal Reserve policymakers. Fed Board of Governors member Christopher Waller gave a speech at the Center for Financial Stability in New York earlier and called for the Fed to accelerate the pace of the QE taper and subsequent rate hikes. These are the most hawkish remarks so far from a “core” Fed member (i.e. a member of the Fed’s Board of Governors). Market participants are now wary that Fed Vice Chair Richard Clarida could offer similarly hawkish sentiments in a speech scheduled for release at 1715GMT. For now, the hawkish vibes from Waller have not affected equity sentiment. As long as markets perceive that the Fed isn't making a “hawkish mistake” – i.e. tightening policy too quickly and hurting growth as a result – more hawkish signals from Fed policymakers can be tolerated.

- US dollar pullback late on Friday as market sentiment recovers.

- Pound is set to end the week higher versus the US dollar and above 1.3400.

- Charts continue to show weakness in GBP/USD.

The GBP/USD pair rose during the American session and recovered from 1.3406 to the 1.3470 area, trimming losses. The recovery pushed the weekly result back into positive ground.

Again cable found support at the 1.3400 area that has become a critical level. A break lower could trigger more losses, exposing the November low at 1.3351. The recovery faced resistance around 1.3500/10. The bearish bias will likely remain intact while under 1.3600.

Thanksgiving ahead

Next week economic data to be released includes the PMIs across the globe. It will be the preliminary reading of November. Also GDP data is due in Germany and the US. “The Thanksgiving holiday in the US means a short week with the data flow concentrated on Wednesday. The highlight may well be the minutes to the November 3rd FOMC meeting when the Federal Reserve announced the start of QE tapering”, explained analysts at ING.

Also market participants await news regarding the next Fed Chair. President Biden is set to announce a new term for Powell or Brainard as his replacement. In the UK, Brexit concerns are on the rise and will likely keep creating headlines next week.

Technical levels

Federal Reserve Board of Governors member Christopher Waller said on Friday that the rapid improvement seen in the labour market and high inflation makes him favour a faster pace of QE taper and sooner rate lift-off, according to Reuters. Inflationary pressures are becoming more widespread, Waller continued and will last longer into 2022 than expected.

Waller added that the labour market is rapidly approaching full employment and that supply chain disruptions were having a larger and more persistent effect on the economy. Nonetheless, Waller said he expects growth in Q4 2021 and Q1 2022 to be "robust". Finally, Waller said that he would support a reduction in the balance sheet, which he thinks might help smooth market functioning, and would support a similar process of balance sheet reduction to last time.

Market Reaction

Waller's comments are the most hawkish yet from a core Fed member (i.e. a member of the permanent voting Board of Governors). But for now, FX markets are not seeing any reaction. Fed Vice Chari Richard Clarida is scheduled to speak later in the session. If his remarks follow a similarly hawkish tone, that would be more likely to provoke USD strength.

- Bond yields have moved sharply lower on Friday amid a bid for haven assets as Europe heads for lockdown.

- The US 10-year Treasury yield is now back to the low 1.50s%.

US bond yields saw a sharp drop on Friday, the primary catalyst for which was a continued ramp up in concerns about lockdowns in Europe where Covid-19 infection/hospitalisation rates continue to surge. The drop in bond yields/rally in bond prices reflects a broader outperformance of safe-haven assets on Friday. The US 10-year Treasury yield dropped more than 6bps to 1.52%, now more than 13bps below earlier weekly highs at 1.65%. Declines of a similar magnitude were witnessed across the treasury curve. The 2-year yield fell 5bps to 0.45%, nearly 10bps below earlier weekly highs, the 7-year fell 7bps to 1.40% and the 30-year fell 5bps to 1.92%.

Austria on Friday become the first major western European nation to announce the reimposition of strict lockdown measures since early 2021, which will begin on Monday and last at least 20 days. Germany’s health minister refused to rule out that Germany could follow suit, saying that the pandemic situation there was becoming increasingly severe.

Some market participants voiced fears that the US could be headed down a similar path. The seven-day moving average number of Covid-19 infections reported per day in the US has been trending higher in November. Having fallen to the low 70Ks in late October/early November, the seven-day moving average is now approaching 100K.

Analysts at Reuters said recent rate volatility is “likely exaggerated by impaired liquidity that has plagued the market for the past few weeks” that, it said, is “in part because hedge funds burned by volatile moves in October and November have pulled back from the market”. Reuters warned that “liquidity is also expected to worsen next week before the market will close on Thursday for Thanksgiving”.

- Yen holds onto daily gains on the back of a deterioration in market sentiment.

- US yields decline significantly while US stocks are mixed.

- USD/JPY remains in the weekly consolidation range.

The USD/JPY is falling on Friday, extending the retreat from the multi-year high it reached on Wednesday near 115.00. Hours ago it bottomed at 113.58, the lowest level since November 10. It then bounced to the upside, but it was unable to regain 114.00.

The yen is among the top performers on Friday. It pulled back during the American session but still remains strong supported by lower US yields and falling equity prices. The US 10-year yield stands at 1.52%, down 4%. Investors’ sentiment is mixed in US markets while European stocks are all in red. The cautions tone following the announcement of a national lockdown in Austria weighed on risk appetite.

The USD/JPY dropped sharply from 114.50 and bottomed at 113.58. In the short term it holds a negative tone. The weekly chart shows the current consolidation range intact, between 113.20 and 114.40. A close above the last one or below 113.20 should provide fresh signs.

The decline of USD/JPY was limited thanks to a stronger greenback. The demand for the dollar also rose amid a run to safety. The DXY trades at 95.80, up 0.31% for the day. It tested the YTD high and pulled back.

Technical levels

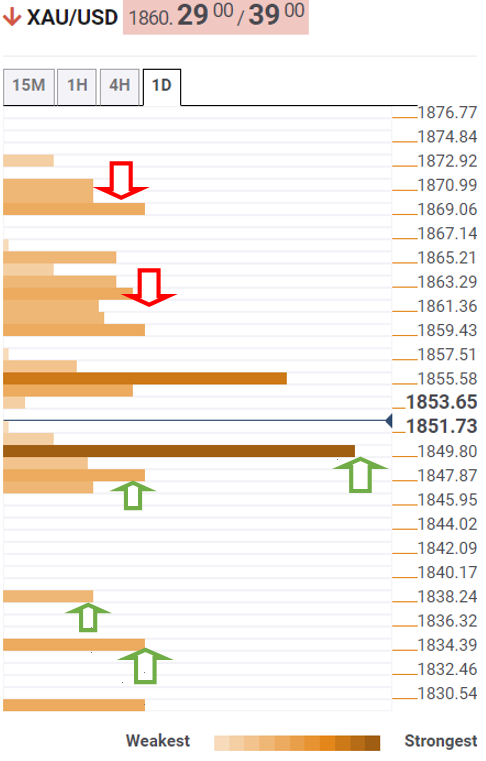

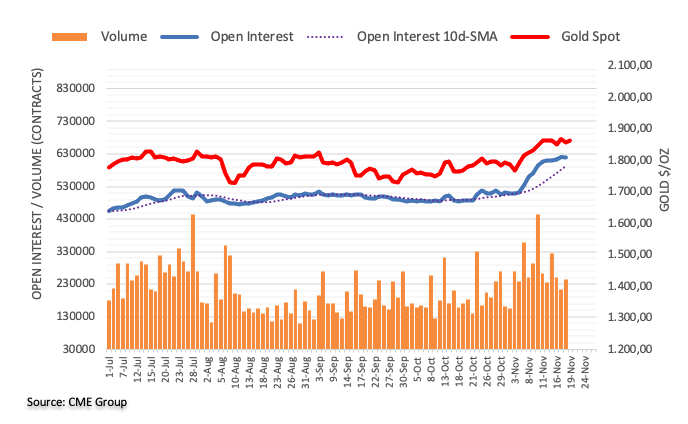

- XAU/USD remains in a choppy trading range, within the $1,850-65 range.

- US T-bond yields plummet six basis points, though gold fails to react according to the drop in yields.

- The US Dollar Index clings to the 95.90 amid falling US bond yields.

Gold (XAUUSD) barely advance during the New York session, up 0.04%, trading at $1,861 at the time of writing. The non-yielding metal remained subdued in the overnight session, within the $1,850-68 range, despite US bond yields drifting lower with the 10-year benchmark note down almost six basis points, at 1.529%. Contrarily, the US Dollar Index, which measures the buck’s performance against a basket of its peers, is advancing 0.45%, sitting at 95.98, after briefly piercing the 96.00 figure.

The market sentiment is downbeat at press time, with most US equity indices in the red, except for the heavy-tech Nasdaq Composite up 0.62%. Factors like increasing COVID-19 cases in Eastern Europe like Austria in a lockdown for 20 days, and Germany’s coronavirus cases spiking above March 2020 high, dented investors mood. Further, the health minister said he could not rule out another lockdown in Germany as infections surge aggressively in the largest Eurozone economy.

Indeed, gold seems to be trading on US inflation expectations, heavily influenced by real yields, leaving nominal on the side. As of November 18 data, real yields sit at -1.89%, one basis point higher than November 15.

XAU/USD Price Forecast: Technical outlook

-637729332106540135.png)

The daily chart shows that gold is in consolidation, after retreating from weekly tops around $1,877, around the $1,860 area. Despite the abovementioned, XAU/USD keeps tilted to the upside, with the daily moving averages (DMA’s) located well below the spot price, with the 100-DMA above the 200 and the 50-DMA, respectively. However, the latter has a steeper upward slope, suggesting it is near a crossing over the 200-DMA.

In the abovementioned outcome, a golden cross would be formed, viewed as a strong bullish signal that could spur a rally towards $1,900. Nevertheless, it would find some hurdles on the way north. The first resistance level would be the November 16 high at 1877. A sustained breach of the latter would expose $1,900, a level that was last seen in June 11 of this year.

On the downside, the XAU/USD next support area would be, according to Dhwani Mehta, Analyst at FX Street, would be the “$1,857, the intersection of the Fibonacci 61.8% one-day and Fibonacci 23.6% one-week.”. Further, a break below the abovementioned level could send gold tumbling towards the confluence of the pivot point one-month R2 and the November 17 low around $1,849, which would be the last line of defense for gold buyers.

French President Emmanuel Macron said that the UK is playing with France's nerves over fishing licenses on Friday, according to Reuters. The French President reaffirmed that the UK is not respecting post-Brexit fishing arrangements and reiterated that his government would continue to support the fishermen until they get their licenses.

Macron added that the situation is progressing too slowly and with not enough firmness. He said that the European Commission needs to do more to help.

Market Reaction

GBP has not reacted to the latest remarks from Macron, but traders should remain cognizant that France may soon revert back to threatening retaliatory measures against the UK if it doesn't get what it wants. This weighed on GBP a few weeks back.

- DXY deflates after challenging 2021 highs past 96.20.

- US yields remain depressed, risk-off mood bolsters the dollar.

- FOMC’S Clarida, Waller speaks later in the NA session.

The greenback came under some pressure after challenging 2021 highs past 96.20 when tracked by the US Dollar Index on Friday.

US Dollar Index closes its fourth straight week with gains

The index keeps the bid bias unchanged, as the risk aversion mood dominates the sentiment in the global markets at the end of the week.

The rebound in the greenback after two consecutive daily pullbacks appears exclusively driven by renewed weakness in the risk complex, while US yields extend further the recent bearish move. That said, the index is on the way to close its fourth consecutive week in the positive territory, while it gained more than 4.6% since September lows in the 92.00 neighbourhood.

Later in the session, FOMC’s permanent voters R.Clarida (dovish) and C.Waller (centrist) are due to speak.

US Dollar Index relevant levels

Now, the index is advancing 0.37% at 95.87 and a break above 96.24 (2021 high Nov.17) would open the door to 97.00 (round level) and then 97.80 (high Jun.30 2020). On the flip side, the next down barrier emerges at 94.96 (weekly low Nov.15) followed by 94.56 (monthly high Oct.12) and finally 93.87 (weekly low November 9).

- WTI is sharply down on Friday and on course to lose over 5.0% this week.

- Prices have been battered by lockdown fears in Europe and concerns about a global crude oil reserve release.

Oil prices are down sharply on the final trading day of the week amid fears that European lockdowns will hit demand. Front-month futures for the American benchmark for sweet light crude oil, West Texas Intermediary or WTI, dipped to fresh six-week lows under $76.00 at one point earlier in the session. WTI has since recovered back to the north of the $76.00 level, but that means it is still down by over $2.50 or more than 3.0% on the day. On the week, the losses are closer to $4.50 (over 5.0%).

Austria became the first western European nation to announce a full lockdown on Friday, amid surging Covid-19 infection and hospitalisation rates. The lockdown will apply to all citizens and last for 20 days, whereafter restrictions on the unvaccinated will continue. Other European nations have also been reimposing restrictions on everyday life and commerce (such as the Netherlands) and fears are growing that they could be next inline to enact broader lockdowns. Germany’s health minister on Friday said that the health situation in the country had become so grave that a full lockdown, including on the vaccinated, could not be ruled out. Widespread European lockdowns would deliver a significant blow to European fuel demand.

Elsewhere, crude oil prices have also this week been weighed amid concerns of an imminent crude oil reserve release from major oil-consuming nations. The US, in response to OPEC+’s refusal to increase output at a faster rate earlier in the month, has spent the last few days petitioning major Asian oil importers to release reserves. Authorities in China have already said they plan to do so. According to commodity strategists at Goldman Sachs, additional supplies of 100M barrels (i.e. from a global oil reserve release) has now been priced in by the market. This may limit the scope for further crude oil downside as a result of the reserve release story, which analysts at Goldman called a “short-term fix to a structural deficit”.

Finally, another theme that is likely to have contributed to the recent oil price downside is increasing chatter/concern that oil markets, currently in a large supply deficit, may soon be headed for a supply surplus. OPEC’s Secretary-General thinks markets will be in surplus by December, whilst the UAE’s oil minister saw this occurring in Q1 2022. US oil output is expected to continue to recover amid higher prices and smaller OPEC+ members who have struggled to keep up with rising output quotas are expected to catch up in the months ahead. Moreover, weaker European demand amid lockdowns over the winter months may also make the supply gap easier to close.

UK Brexit Minister Lord David Frost said on Friday that the UK and EU have not yet made substantive progress on the fundamental customs issues relating to goods moving from Great Britain to Northern Ireland. If no solution can be found, he continued in a reiteration of his previously held stance, the UK remains prepared to use the safeguard provisions under Article 16. Frost said that the UK's preference was to secure a solution based on consensus, but any such solution must constitute a significant change from the current situation. Significant gaps remain between the EU and UK on most fronts, he said.

Market Reaction

GBP/USD has been turning a tad lower in recent trade, but continues to trade within the days ranges around the 1.3450 mark.

The US House of Representatives passed US President Joe Biden's $1.75T "Build Back Better" social spending package by a margin of 220-213 on Friday, sending it to be voted on in the Senate.

European Commission Vice President Maros Sefcovic said on Friday that it is essential that the recent change in tone from the UK now leads to tangible solutions in the framework of the Northern Ireland Protocol. Sefcovic continued that there is a genuine sense of urgency related to medical supplies and that he was urging the UK government to make a clear move towards the EU in the area of sanitary and phytosanitary controls. Sefcovic confirmed that he will be meeting with UK Brexit Minister Lord David Frost next week in London.

Market Reaction

There has not been any notable market reaction to these latest remarks on Brexit.

- EUR/GBP is set to end a torrid week at lows amid broad euro underperformance on Friday amid European lockdown fears.

- The pair is back under the 0.8400 level and eyeing 21-month lows.

EUR/GBP has turned sharply lower on the final trading day of the week, dropping from Asia Pacific levels above 0.8420 to back below 0.8400 as it eyes a test of 21-month lows printed earlier in the week in the mid-0.8380s. Euro underperformance is a major driver of the recent downturn in the EUR/GBP currency pair, amid concerns about a rapid deterioration in the Eurozone economy as the pandemic takes hold on the continent.

Austria announced that it will reimpose a full lockdown on all people from Monday for 20 days, with restrictions to then continue afterward on the unvaccinated. Moreover, the country said that all citizens would be required to be vaccinated by 1 February 2022, or else face hefty fines. More concerning from a financial market perspective is that it seems as though Germany will be following closely behind. Germany’s health minister on Friday said that the health situation in the country had become so grave that a full lockdown, including on the vaccinated, could not be ruled out. According to a senior portfolio manager at Swiss asset manager Vontobel, “a total lockdown for Germany would be extremely bad news for the economic recovery”.

Negative news on the pandemic front in Europe has largely overshadowed a much hotter than expected German PPI report for October, as well as hawkish comments from outgoing ECB Governing Council member and Bundesbank President Jens Weidmann. In fairness, Weidmann is a well-known hawk and has spent most of the last decade unable to influence ECB policy, which is dominated by the doves, so his comments usually do not move the needle for the euro. Weidmann is quitting at the end of the year.

The downside on Friday caps off a torrid week for EUR/GBP. The pair has dropped more than 1.5% from above 0.8500 to current levels under 0.8400, its worst weekly performance since March 2020. Aside from the escalation of the severity of the European Covid-19 situation throughout the week, the pair has also been weighed by strong UK macroeconomic data. Earlier in the week, the latest jobs report provided early indications that there was not a spike in joblessness after the end of the UK government’s furlough scheme in late September and October inflation was hotter than expected.

Most recently, the October Retail Sales report released on Friday prior to the European open beat expectations, though economists put this down to consumers bringing forward their Christmas/holiday shopping amid supply chain concerns. FX strategists also touted the ongoing story of BoE/ECB divergence as a negative. The BoE is expected by many to start hiking interest rate as soon as December, while the key ECB policymakers such as President Lagarde have been trying to guide the market against expecting rate hikes as soon as 2022. Comments from hawkish ECB member Jens Weidmann, who leaves the bank at the end of the year, and comments from the BoE’s Chief Economist were ignored by FX markets.

Elsewhere, the tone of Brexit developments has become more positive this week and most market participants seem to expect the UK and EU to eventually bridge their differences regarding the implementation of the Northern Ireland Protocol.

Movements in bond markets, which reflect the deterioration in the European economic sentiment are also likely weighing. German 10-year yields down 7bps this week to their lowest levels since mid-September just above -0.35%, while UK 10-year yields are down less than 5bps and still comfortably above last week’s 0.82% lows.

- EUR/USD dropped to new 16-month lows around 1.1250.

- The greenback briefly tested the boundaries of 2021 highs.

- ECB’s Lagarde said there is no rush to tighten monpol.

Sellers keeps the European currency under pressure and forces EUR/USD to recede to fresh 16-month lows in the 1.1250 region on Friday.

EUR/USD weaker on risk-off sentiment

EUR/USD remains depressed on the back of persevering buying pressure in the greenback and the prevailing risk-off mood among market participants.

Indeed, renewed demand for the buck prompted the US Dollar Index to reverse the recent weakness and challenge once again the area of 2021 highs near 96.20 despite the corrective downside in US yields.

Earlier in the session, Chairwoman C.Lagarde suggested that there is no rush to prematurely tighten the current monetary conditions.

EUR/USD levels to watch

So far, spot is losing 0.73% at 1.1288 and faces the next up barrier at 1.1422 (10-day SMA) followed by 1.1464 (weekly high Nov.15) and finally 1.1509 (20-day SMA). On the other hand, a break below 1.1250 (2021 low Nov.17) would target 1.1185 (monthly low Jul.1 2020) en route to 1.1168 (low Jun.19 2020).

Bank of England Chief Economist Huw Pill said on Friday that markets should not assume that the BoE's first rate hike will be a 15bps move, according to Reuters. Speaking at an economics conference in Bristol, the BoE's Chief Economist added that "there is an attraction at some point to getting back to a multiple of 0.25 ... but we are not under pressure to do that immediately."

Market Reaction

FX markets have not seen any notable reaction to Pill's latest remarks.

According to the latest figures from Statistics Canada released on Friday, Canadian Retail Sales fell by 0.6% MoM in September, less than the 1.7% expected decline. In August, Retail Sales increased at a MoM pace of 1.8%. Excluding autos, Retail Sales fell by 0.2% MoM in September, less than the 1.0% expected drop, after rising 2.6% MoM in August.

Market Reaction

The loonie has not seen any market reaction to the latest Canadian data and continues to trade on the back foot amid sharply lower crude oil prices and a risk-off market tone.

Bank of England Chief Economist Huw Pill said on Friday that, on the back of recent data, the burden of proof at the bank had shifted onto those not wanting to raise interest rates.

Market Reaction

FX markets do not seem to have reacted to the latest comments from Pill, who earlier also alluded to the fact that he wasn't yet sure how he would vote at the December policy meeting.

There has been an interesting development in GBP Short-Term Interest Rate (STIR) markets on Friday. December 2021 Sterling libor futures have rallied 5bps to 99.80 from previously around 99.75, implying that markets are revising lower their expected probability of the BoE hiking interest rates by 15bps in December (see the chart below).

Source: Reuters Eikon

USD/JPY is set to gold support at 113.87/76. With a major base in place, analysts at Credit Suisse look for an eventual clear break above key resistance at 114.73/92 for strength to the long-term downtrend from April 1990 at 117.00/01.

Support at 113.87/76 to hold

“With a major base in place, we continue to look for a clear and sustained break in due course above key resistance at 114.70/92. This should then see a resumption of the core uptrend with resistance then seen next at 115.51 and then the long-term downtrend from April 1990 at 117.00/01.”

“Whilst we would expect a fresh phase of consolidation to emerge from the 117.00 level, big picture we continue to look for an eventual move to 122.90/123.00.”

“Near-term support from the 13-day exponential average and price support at 113.87/76 ideally still holds. A break would warn of a retreat back to 112.76/40, but with fresh buyers expected here.”

EUR/GBP extends its aggressive rejection from its 200-day average at 0.8575 for a move to a new low for the year. Analysts at Credit Suisse look for a test of long-term support at the 2019 and 2020 lows at 0.8281/39.

Resistance at 0.8463/68 set to cap

“EUR/GBP keeps the immediate risk lower for a test of 0.8339/32 next and eventually pivotal long-term support from the 2019 and 2020 lows and the 50% retracement of the upmove from 2015 at 0.8281/39.”

“Whilst we would look for a fresh hold at 0.8281/39, for now, an eventual break would see a multi-year top established to open the door to what we believe would be a significant fall, with support then seen next and initially at 0.8118.”

“Near-term resistance remains at 0.8430/38, above which can ease the immediate downside bias for a recovery back to the 13-day exponential average and price resistance at 0.8463/68, but with fresh sellers expected to show here.”

See: EUR/GBP to race higher towards 0.88 if Article 16 is triggered – Nordea

ECB Governing Council Member and Bundesbank President Jens Weidmann said in a speech on Friday that the bank should not ignore the risk of too high inflation, and must remain watchful, according to Reuters. Monetary policy should not commit to its current very expansionary stance for too long, he added, before continuing that if required to safeguard price stability, monetary policy as a whole will have to be normalised.

Weidmann said that elevated inflation rates will probably take longer than previously projected to recede and that the pandemic could have a marked impact on inflation setting. That could mean that inflation won't fall back below the ECB's 2.0% symmetric target in the medium-term, he added.

Market Reaction

Weidmann is a well-known ECB hawk, and thus the euro has not reacted to his comments. Weidmann is set to leave his post as Bundesbank head at the end of the year.

Irish Prime Minister Michael Martin said on Friday that he detects genuine desire from all sides to solve issues relating to the Northern Ireland Protocol (NIP). His comments follow comments from influential UK Minister Michael Gove, who said that he was confident that we will be able to make progress in discussions relating to the NIP without triggering Article 16.

However, earlier in the session, UK Brexit Minister Lord David Frost said that significant gaps still remain between the UK and EU and that a triggering of Article 16 remained on the table. Meanwhile, European Commission Vice President confirmed to the press that the EU was offering to the UK a permanent 50% cut in customs-related paperwork.

Market Reaction

GBP has not seen any notable reaction to the latest Brexit-related updates.

BoE Chief Economist Huw Pill said on Friday that he genuinely does not yet know how he is going to vote at the December monetary policy meeting. For reference, markets are fully priced for the BoE to implement a 15bps rate hike to 0.25%. Pill added that the direction of travel for interest rates over the medium-term is pretty clear (i.e. hinting strongly that the BoE will be hiking over the next 12 months), but that the long-term outlook for rates is too uncertain to give a specific forecast three of five years ahead.

Additional remarks

“It does matter if markets misunderstand BoE, but maybe less than markets think.”

“The BoE should not get caught up in minute-by-minute market and media-driven dynamics, should instead focus on the medium-term”.

“The BoE wants to train people to think the right way about monetary policy.”

“The past few weeks have not been a good example of a common understanding of monetary policy between the BoE and markets.”

“No policymaker wants to create unnecessary volatility.”

“The BoE should not artificially suppress volatility caused by genuine uncertainty.”

“Two-sided risks make communication more complex than in the past.”

“Fed-style dot plots would probably add to confusion in BoE communications.”

“The direction of travel for interest rates over the medium-term is pretty clear”.

“The long-term outlook for rates is too uncertain to give a specific forecast 3 or 5 years ahead.”

Market Reaction

GBP did not react to these latest remarks from BoE's Pill.

- USD/TRY adds to the rally above the 11.00 mark

- The lira remains under heavy fire following the CBRT rate cut.

- The resumption of the dollar buying pushes spot higher.

The lira extends its march south and now pushes USD/TRY to daily tops near 11.2000, where some resistance appears to have turned up for the time being.

USD/TRY up on lira weakness, dollar uptrend

USD/TRY advances for the ninth consecutive session on Friday, always on the back of the indefatigable lira selloff although this time the strong upside in the greenback also helps the pair extending the rally.

Indeed, the ongoing context favours the risk aversion and therefore lends extra legs to the buck despite US yields trade on the defensive so far on Friday.

The pair, in the meantime, trades a tad below Thursday’s all-time highs near 11.2800, recorded in the aftermath of another reduction of the One-Week Repo Rate by the Turkish central bank (CBRT) at its meeting. Losses in TRY has been also exacerbated after the central bank left the door (wide) open to another interest rate cut at the December event.

The lira has so far shed more than 33% vs. the US dollar and remains the worst performing EM currency by far this year. The last time the pair advanced for ten sessions in a row was back in 2019, from April 18th until May 1st. We’re just there… about to break another record.

USD/TRY key levels

So far, the pair is gaining 0.35% at 11.1152 and a drop below 10.2276 (10-day SMA) would expose 9.8325 (high Oct.25) and finally 9.4722 (monthly low Nov.2). On the other hand, the next up barrier lines up at 11.2792 (all-time high Nov.18) followed by 12.0000 (round level).

Bank of England Chief Economist Huw Pill said on Friday that some patience would be required before inflation comes back to 2.0%, according to Reuters. Pill said that he and the BoE's Monetary Policy Committee (MPC) are committed to achieving 2.0% inflation, but that there would be no quick fix. It is a pretty uncomfortable time to join a central bank, Pill continued. He joined the BoE as Chief Economist at the start of September.

Market Reaction

GBP/USD has not seen a notable reaction to the latest comments from the BoE's Chief Economists. His concern about inflation supports the case for a 15bps rate hike from the BoE in December, which is now the market's base case assumption.

- EUR/USD resumes the downside and breaks below 1.1300.

- Another visit to YTD low at 1.1263 seems to be shaping up.

EUR/USD trades well on the defensive and puts the 1.1300 mark once again to the test at the end of the week.

The continuation of the downtrend appears favoured in the short-term horizon. That said, bets remain on the rise for another test of the so far 2021 low at 1.1263 (November 17). The loss of this area could drag spot to the round level at 1.1200 before the July 2020 low at 1.1185 ahead of 1.1168 (low June 19 2020).

In the meantime, extra losses remain on the cards as long as the pair trades below the immediate resistance line (off September’s high) today near 1.1600. In the longer run, the negative outlook persists while below the 200-day SMA, today at 1.1857.

EUR/USD daily chart

- DXY reverses two straight daily pullbacks and flirts with 96.00.

- Next of note comes the YTD peak past 96.20.

DXY advances to 2-day highs above the key barrier at 96.00 the figure on Friday.

Further upside targets the so far 2021 high at 96.24 (November 17), while a breakout of this level is expected to shift the attention to the June 2020 low at 95.71 before 97.80 (high June 30 2020).

Looking at the broader picture, the constructive stance on the index is seen intact above the 200-day SMA at 92.26.

DXY daily chart

- EUR/JPY resumes the downtrend and breaches 129.00.

- Next of note on the downside comes the 128.30 region.

EUR/JPY accelerates losses and drops below the key support at 129.00 the figure on Friday.

A deeper pullback looks likely with the immediate support now emerging at October’s low at 128.33 (October 6). If cleared, then a move to the YTD low at 127.93 (September 22) should return to the radar in the short-term horizon.

Below the 200-day SMA, today at 130.51, the outlook for the cross is seen as negative.

EUR/JPY daily chart

- USD/CAD is posting strong gains ahead of the American session on Friday.

- WTI is trading at its lowest level since early October below $77.

- Broad-based dollar strength is providing an additional boost to USD/CAD.

After closing virtually unchanged near 1.2600 on Thursday, the USD/CAD pair regained its traction and reached its strongest level in six weeks at 1.2657. As of writing, the pair was up 0.4% on a daily basis at 1.2650.

WTI slumps below $77

Falling crude oil prices seem to be weighing on the commodity-sensitive loonie on Friday. Prospects of increasing global oil supply and renewed concerns over resurging coronavirus cases hurting the energy demand is dragging oil prices lower. Currently, the barrel of West Texas Intermediate is trading at its lowest level since early October at $76.20, losing more than 3% on the day.

On the other hand, the risk-averse market environment is helping the greenback outperform its rivals and allowing USD/CAD to continue to push higher.

Following a two-day correction, the US Dollar Index (DXY) is back above 96.00 ahead of the American session. In case Wall Street's main indexes edge lower after the opening bell, the DXY could preserve its bullish momentum.

Meanwhile, the Canadian economic docket will feature September Retail Sales data, which is expected to reveal a monthly contraction of 1.7% and October Housing Price Index.

Technical levels to watch for

EUR/USD is similarly holding at the 61.8% retracement of the 2020/2021 uptrend at 1.1290. Economists at Credit Suisse view this as a temporary pause and look for a sustained break in due course for a move to 1.1020.

Resistance at 1.1428/38 to cap for an eventual sustained move below 1.1290

“EUR/USD has found a floor for now at the 61.8% retracement of the 2020/2021 uptrend at 1.1290. With a major ‘head and shoulders’ top in place, our core outlook stays bearish and we view this pause as temporary and healthy before the core downtrend resumes.”

“Resistance is seen at 1.1375/76 initially, then 1.1387, above which can see the recovery extend to our corrective objective and what we look to be tougher resistance at the 13-day exponential average and 38.2% retracement of the October/November fall at 1.1428/38. We look for this to then cap and for the trend to turn lower again.”

“Support moves to 1.1327 initially, then 1.1313. An eventual sustained move below 1.1290 should clear the way for a fall back to 1.1264/55 ahead of 1.1185, then the ‘measured objective’ from the top at 1.1075 and eventually our main objective of the 78.6% retracement and price support at 1.1019/02.”

- AUD/USD came under stong bearish pressure in the European session on Friday.

- US Dollar Index tests 96.00 supported by safe-haven flows.

- There won't be any high-impact data releases from the US.

Following a consolidation phase below 0.7300 during the Asian trading hours, the AUD/USD pair lost its traction and dropped to its weakest level since early October at 0.7232. As of writing, the pair was down 0.52% on the day at 0.7252.

Dollar capitalizes on safe-haven flows

The renewed USD strength seems to be causing AUD/USD to fall sharply on Friday. The US Dollar Index (DXY), which closed the previous two trading days in the negative territory, is currently rising 0.5% on a daily basis at 96.00. The souring market mood amid concerning coronavirus headlines coming from Europe seems to be helping the greenback find demand as a safe haven.

The S&P Futures are trading in the red, suggesting that Wall Street's main indexes could stay on the back foot ahead of the weekend.

Later in the session, there won't be any data releases from the US but Federal Reserve Governor Christopher Waller and Federal Reserve Vice Chair Richard Clarida will be delivering speeches. Investors will keep a close eye on comments regarding the Fed's policy outlook in the face of persistently high inflation.

Technical levels to watch for

- GBP/USD turned south after trading above 1.3500 earlier in the day.

- British pound is struggling to find demand despite the upbeat Retail Sales data.

- US Dollar Index is testing 96.00 as market mood sours.

The GBP/USD pair spent the Asian session in a relatively tight range near 1.3500 but came under strong bearish pressure during the European trading hours. As of writing, the pair was down 0.5% on a daily basis at 1.3420.

Earlier in the day, the data published by the UK's Offıce for National Statistics revealed that Retail Sales in October rose by 0.8% on a monthly basis. This reading came in higher than the market expectation for an increase of 0.5%. Although the initial market reaction helped the British pound gather strength, the negative shift witnessed in market sentiment forced the pair to reverse its direction.

DXY gains traction ahead of the American session

Reports of Austria going into a full lockdown due to the rising number of coronavirus cases revived concerns over the global economic activity slowing down in winter. US stock index futures turned south and the US Dollar Index climbed to 96.00 area, reflecting the dismal market mood.

There won't be any high-tier macroeconomic data releases featured in the US economic docket in the remainder of the day and the risk perception is likely to continue to drive the financial markets.

Meanwhile, Northern Ireland protocol negotiations are set to continue in Brussels on Friday and investors will keep a close eye on fresh Brexit headlines ahead of the weekend.

Key technical levels to watch for

- USD/JPY is back in the red amid a renewed risk-off wave.

- Rejection above 21-SMA calls for a retest of 100-SMA on the 4H chart.

- RSI has pierced through the midline, more downside likely?

USD/JPY is trading below 114.00, having witnessed a sharp 60-pips drop in the last hour after a renewed risk-aversion wave gripped markets on the covid resurgence in the Euro area.

Austria announced a nationwide lockdown from Monday while Germany stated that it is in a national emergency state, due to the resurgence of the coronavirus in the bloc, which has triggered a flight to safety in the Japanese yen.

Although the downside remains cushioned amid a broadly strong US dollar, which also attracts the safe-haven flows.

Looking ahead, the covid updates and Fedspeak will be closely eyed for fresh trading impetus on the major.

Looking at USD/JPY’s four-hour chart, the price came under massive selling pressure after it ran into strong offers once again just above the ascending 21-Simple Moving Average (SMA) at 114.38.

The latest sell-off has taken out the bullish 50-SMA support at 114.00, as bears now challenge the critical horizontal 100-SMA at 113.87.

A four-hourly candlestick closing below the latter will expose the upward-sloping 200-SMA support at 113.64.

The Relative Strength Index (RSI) has pierced through the midline, currently pointing south and allowing more room for declines.

USD/JPY: Daily chart

Any rebound will challenge the 50-SMA support-turned-resistance, above which the 21-SMA barrier will be back in play.

If the bulls succeed in recapturing the 21-SMA, then a retest of the daily highs at 114.54 could be in the offing.

USD/JPY: Additional levels to consider

- EUR/USD gives away Thursday’s advance and resumes the downside.

- German Producer Prices surprised to the upside in October.

- ECB’s Lagarde sees inflation picking up pace by year end.

The optimism around the single currency was short-lived. Indeed, EUR/USD resumes the prevailing downtrend on Friday, only interrupted by the positive price action witnessed on the previous session.

EUR/USD looks to Lagarde, dollar

EUR/USD hovers round the 1.1300 neighbourhood after a brief test of daily lows near 1.1280 during early trade.

The resumption of the upside pressure in the dollar despite the soft note in US yields along the curve allows the US Dollar Index (DXY) to regain traction and flirt once again with the 96.00 zone, or 2-day tops.

On the ECB’s front, Chairwoman Lagarde now sees inflation gathering further pace by year end, while factors pushing consumer prices higher are expected to fade over the medium term. She also said that inflation needs to clinch the bank’s 2% goal on a durable basis.

In the euro docket, German Producer Prices rose more than expected in October at a monthly 3.8% and 18.4% over the last twelve months. Additionally, the EMU’s Current Account surplus rose to €26.9 in September (from €17.6B).

What to look for around EUR

EUR/USD quickly faded Thursday’s bullish attempt and now remains focused on the downside, where the 2021 low near 1.1260 emerges as the next magnet for bears. As usual, the pair’s price action is predicted to mainly track the dynamics around the buck, while bouts of intermittent strength are expected to come from the improvement in the risk complex. On the more macro view, the loss of momentum in the economic recovery in the region - as per some weakness observed in key fundamentals – coupled with rising cases of COVID-19 is also seen pouring cold water over investors’ optimism. Further out, the euro should remain under scrutiny amidst the implicit debate between investors’ speculations of a probable lift-off sooner than anticipated and the ECB’s so far steady hand, all amidst the tenacious elevated inflation in the bloc and increasing conviction that it could last longer than previously anticipated.

Key events in the euro area this week: ECB Lagarde (Friday).

Eminent issues on the back boiler: Asymmetric economic recovery post-pandemic in the region. Sustainability of the pick-up in inflation figures. Pick-up in the political effervescence around the EU Recovery Fund in light of the rising conflict between the EU, Poland and Hungary on the rule of law. ECB tapering speculations.

EUR/USD levels to watch

So far, spot is losing 0.62% at 1.1301 and faces the next up barrier at 1.1422 (10-day SMA) followed by 1.1464 (weekly high Nov.15) and finally 1.1509 (20-day SMA). On the other hand, a break below 1.1263 (2021 low Nov.17) would target 1.1185 (monthly low Jul.1 2020) en route to 1.1168 (low Jun.19 2020).

Brexit-risks are back in the limelight as Boris Johnson considers invoking article 16 in the Northern Irish protocol. In the view of economists at Nordea, EUR/GBP is probably headed towards higher levels, if Brexit risks are reintroduced.

Triggering of Article 16 will likely lead the BoE towards fewer hikes than priced

“We judge that EUR/GBP is headed back towards 0.88 should the Brexit-uncertainty be re-introduced and it will likely also at least partly wreak havoc with Bank of Englands hiking plans.”

“We continue to forecast two hikes (2x 25 bps) from Bank of England during 2022, and we expect them to refrain from hiking in December should the triggering of Article 16 happen before then, which we consider to be the base case now.”

- Gold price rebounds as yields pare gains, DXY rally could limit the upside.

- Gold bulls remain motivated as long as the key $1,850 support holds.

- Gold capitalizes on inflation fears, buyers look to retain control.

Having failed several attempts to resist above the $1,870 threshold, gold price continues to hover in a familiar range above the critical $1,850 support. The latest uptick in gold price can be attributed to a sharp sell-off in the US Treasury yields, as the risk sentiment sour amid inflation and coronavirus concerns. However, strengthening US economic recovery calls for earlier Fed’s tightening, boosting the US dollar, which could limit gold’s upside.

Read: Investors expect high inflation, golden inquisition ahead?

Gold Price: Key levels to watch

The Technical Confluences Detector shows that gold price staged a solid rebound from ahead of the key $1,850 support, which is the convergence of the pivot point one-month R2 and SMA10 one-day.

If that cap is taken out on a sustained basis, then gold bears will test minor support at $1,847, the Fibonacci 38.2% one-week.

A steep drop towards the pivot point one-day S3 at $1,839 cannot be ruled out should the abovementioned support fail to hold.

The Fibonacci 61.8% one-week at $1,834 will be the line in the sand for gold bulls.

Alternatively, gold buyers need to find a strong foothold above a dense cluster of resistance levels around the $1,863-$1,865 region.

That level is the intersection of the SMA100 one-hour, Fibonacci 38.2% one-day and SMA10 four-hour.

Further up, the previous week’s high of $1,869 will get retested.

Here is how it looks on the tool

About Technical Confluences Detector

The TCD (Technical Confluences Detector) is a tool to locate and point out those price levels where there is a congestion of indicators, moving averages, Fibonacci levels, Pivot Points, etc. If you are a short-term trader, you will find entry points for counter-trend strategies and hunt a few points at a time. If you are a medium-to-long-term trader, this tool will allow you to know in advance the price levels where a medium-to-long-term trend may stop and rest, where to unwind positions, or where to increase your position size.

German Health Minister Jens Spahn expressed his concerns over the covid resurgence, citing that “we are in a national emergency.”

Additional quotes

Vaccinations won't cut it at this point to stop the COVID-19 spread.

The COVID-19 situation is more serious than last week.

Vaccinations won't be enough.

Controls are needed to stop the rise in COVID-19 cases.

Market reaction

EUR/USD remains pressured amid dovish comments from ECB President Lagarde, the US dollar’s strength and renewed covid concerns.

At the time of writing, the pair sheds 0.30% on a daily basis to trade at 1.1334.

GBP/USD has bounced back to return to 1.35. Economists at Société Générale notes that the cable could rise as high as 1.3910 on a breach of the 1.3600 hurdle.

Next hurdle at 1.3600

“GBP/USD bounce has persisted since last week and the pair is heading towards daily Kijun line at 1.3600.”

“If the 1.3600 level is reclaimed, the rebound is expected to extend towards 200-DMA near 1.3850/1.3910.”

S&P 500 up move has developed a brief pause after reaching the upper band of an ascending channel near 4720 (now at 4750). As the index stays above the 4630/15 support, economists at Société Générale expect the S&P 500 to head back higher towards 4780.

Signals of trend reversal are still not visible

“Signals of trend reversal are still not visible. A break below 4630/4615, the 23.6% retracement from October will be essential to denote a deeper pullback.”

“Holding above the 4630/4615 support, the uptrend is likely to persist.”

“Beyond 4720, the index is expected to head higher towards 4750 and next projections of 4780.”

USD/CAD recently reclaimed the 200-day moving average (DMA) at 1.2465 extending its rebound towards the daily Ichimoku cloud near 1.2650. A break above would clear the way for a potential rise towards the 1.2950/1.3020 area, economists at Société Générale report.

Consolidation above the 200-DMA near 1.2465 is crucial to extend the advance

“Daily MACD has entered positive territory which denotes potential upside.”

“A break above 1.2650 can take the pair towards 1.2795 and perhaps even towards the graphical levels of 1.2950/1.3020.”

“Consolidation above the 200-DMA near 1.2465 will be crucial for persistence in up move.”

- DXY regains upside traction and surpasses 95.80.

- US yields tick higher and support the upside in the index.

- FOMC’s Waller, Clarida scheduled to speak later in the session.

The US Dollar Index (DXY), which gauges the greenback vs. a bundle of its main competitors, manages to regain buying interest and returns to the area above 95.80 on Friday.

US Dollar Index up on US yields

After two consecutive daily pullbacks, the index finally manages to regain the smile and revisit the upper-95.00s at the end of the week. So far, the 95.50 area have emerged as quite a firm contention.

The recovery in the dollar comes amidst a better tone in the US money markets, where yields now attempt a mild recovery along the curve.

In the meantime, inflation concerns continue to dominate the FX scenario in the global markets, as well as prospects of an anticipated start of the tightening cycle by the Federal Reserve. On the latter, FOMC’s J.Williams suggested on Thursday than expectations for future increases of consumer prices remain on the rise while US inflation appears more broad-based.

No data releases in the US calendar on Friday should leave the attention to speeches by FOMC’s permanent voters R.Clarida (dovish) and C.Waller (centrist).

What to look for around USD