- Analytics

- News and Tools

- Market News

CFD Markets News and Forecasts — 19-05-2011

Stocks have slipped a bit in recent trade. Their wavering action has been going on for more than an hour.

Action in the automotive space has been lackluster this session. Ford (F 15.11, -0.01) is flat after it signed a definitive agreement to sell its automotive fuel tank business. As for General Motors (GM 31.46, -0.06), its shares are down narrowly, even though the company confirmed that it is planning a production boost for its Chevrolet Volt. Meanwhile, Advance Auto Parts (AAP 63.23, -7.43) has dropped precipitously following news of its earnings miss.

Overall gains remain modest. Meanwhile, the industrials sector has managed to reclaim gains from this morning so that it is now up with a 0.9% gain. That's more than double what any other sector has achieved.

Health care stocks have been under pressure all session. The sector's weakness comes amid sharp losses among pharmaceutical plays like Brisol-Myers Squibb (BMY 28.57, -0.29) and Pfizer (PFE 21.01, -0.17). Abbot Labs (ABT 53.35, -0.47) is also under pressure.

JPM says Philly and Empire data were weaker and "other regional surveys could give us a better sense of the impact that auto plant shutdowns have had on manufacturing." JPM points out employment index rose in Philly data, "however, the measure of the workweek (not part of the ISM-weighted composite) declined 13.8 points to 3.9; this index generally follows a similar trajectory as the employment index."

A disappointing batch of economic data brought stocks down from an early advance, but the market has made a modest rebound amid a downturn by the dollar.

LinkedIn (LNKD 104.90, +59.90) has soured in its debut session. The stock issued its Initial Public Offering at $45 per share, but has rallied to well above $100 per share.

Retailers have had a rough session. Sears Holding (SHLD 73.68, -2.17), Limited (LTD 41.00, -1.45), Buckle (BKE 42.00, -5.90), and Hott Topic (HOTT 7.00, -0.66) are all in the red following their quarterly reports. Discount retailer Dollar Tree (DLTR 63.74, +2.41) is up with a solid gain following its upside earnings surprise, but Big Lots (BIG 33.30, -4.44) has dropped sharply following news that the company is not looking to sell itself.

Semiconductor stocks have also lagged this session. The group's 1% loss, as measured by the Philadelphia Semiconductor Index, comes after the equipment space was downgraded by analysts at Goldman Sachs.

The yen dropped against most of its major counterparts as Japan slid into its third recession in a decade and Prime Minister Naoto Kan said he expects the central bank to maintain a flexible monetary policy.

Gross domestic product in Japan contracted an annualized 3.7 percent in the three months through March, following a revised 3 percent drop in the previous quarter, the Cabinet Office said today in Tokyo.

The dollar pared losses against currencies of commodity exporters as data showed Philadelphia-area manufacturing grew at the slowest pace in seven months.

“The market is worried that demand and output in Japan collapsed a lot further than they had thought,” said Steven Englander, head of Group-of-10 currency strategy at Citigroup Inc. in New York. On the U.S. data, “the question is how concerned does this make you that growth is going to disappoint -- and as that concern grows, some of the commodity currencies come under pressure,” he said.

The dollar reversed a loss against New Zealand’s currency after the Federal Reserve Bank of Philadelphia’s general economic index unexpectedly fell to 3.9, the weakest reading since October, from 18.5 a month earlier. Readings greater than zero signal expansion. In another report, the National Associated of Realtors said sales of existing U.S. homes slid 0.8 percent in April to a 5.05 million annual pace.

The franc fell against the euro as Swiss Economy Minister Johann Schneider-Ammann said authorities will consider “appropriate” measures if the currency continues to strengthen.

Stocks have stabilized after descending into negative territory. Leadership is lacking, though.

Industrial stocks continue to post the best gains of any major sector, but their 0.5% gain is only half of what had been sported when the sector was at its session high.

Materials stocks were also strong in the early going, when they put together a gain of roughly 1%. That sector has since rolled over to trade with a fractional loss.

HFE says "The Philly Fed index dropped to just 3.9 from 18.5, well below the consensus, 20.0, and the lowest reading since October. This looks terrible but remember that the Philly index is much more volatile than national indicators like the ISM." HFE says index fell because of high oil "but with more than half the Feb-Apr increase now reversed sentiment should begin to recover soon. In the meantime, though, at least some decline in the ISM looks likely."

Commodities are mostly lower this morning and recent weakness in the dollar index, which fell into the red a short while ago, doesn't seem to be having much of a positive effect currently.

In the energy markets, natural gas has been in negative territory all morning and quickly dropped about 1% just a few minutes before U.S. equity markets opened. Ahead of inventory data, natural gas remained near session lows of $4.20/MMBtu. Following the data, which showed a build of 92 bcf vs. expectations for a build of 90 bcf, natural gas sold off to new session lows of $4.19/MMBtu and remains at those lows currently, down 1.7%

Crude oil has been in positive territory for the majority of this morning's activity. In the last 20 minutes, crude pulled back from ~$100.70 to ~$100.20, but remains in positive territory. Currently, crude is sitting at $100.25/barrel, down 0.3%.

Overnight, agriculture commodities, especially corn and wheat, extended gains as unfavorable weather and flooding continues to delay planting in the U.S. In the last five sessions, corn futures are 12.1% higher and wheat futures are up 14.1% in the last three session.

In the precious metals space, gold has been in negative territory all morning and is currently down 0.3% at $1491.20/oz. Silver, on the other hand, has spent the morning in positive territory and is currently up 0.6% at $35.30/oz. Neither precious metal has displayed much volatility this morning.

Apr exist home sales -0.8% to a SAAR 5.05 mln (5.2 mlnexpected), -12.9% from a year ago

Apr Leading Indicators -0.3% vs Mar +0.7%

May Philly Fed mfg index 3.9 vs 18.5 Apr

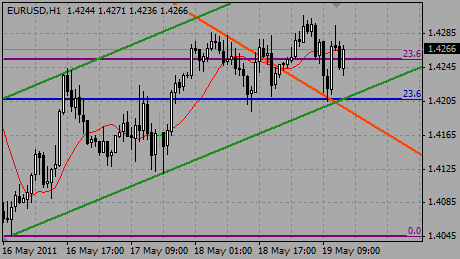

EUR/USD $1.4160, $1.4175, $1.4225, $1.4300, $1.4310

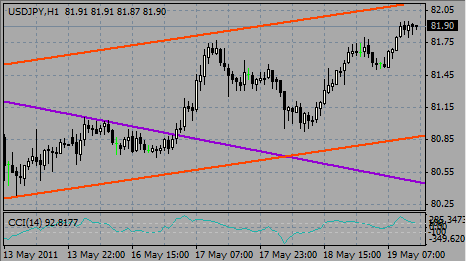

USD/JPY Y81.10, Y81.00, Y80.95

EUR/JPY Y114.70

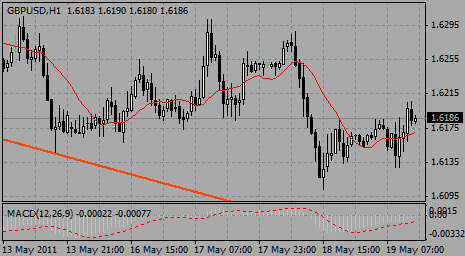

GBP/USD $1.6180, $1.6135, $1.6000, $1.6270

USD/CHF Chf0.8890

CHF/JPY Y91.00

AUD/USD $1.0620, $1.0600

AUD/JPY Y86.20, Y85.90

AUD/USD heading down towards the session lows of $1.0626, holding around $1.0637. Support comes at $1.0630. The move largely on the back of a weaker euro and Gold.

U.S. stocks were set to edge higher at Thursday's open, as investors weigh a slightly better-than-expected report on the labor market, and await additional reports on the housing and manufacturing sectors.

Economy: The number of people filing for first-time unemployment benefits dropped sharply for the second straight week to 409,000, the government said. Economists expected jobless benefits to show a drop to 420,000.

No change is expected from the April index on leading economic indicators, following a 0.4% rise the month before.

Also due Thursday the Philadelphia Fed index for May, a regional reading on manufacturing.

At 14:00 GMT the National Association of Realtors will release its April reading on existing home sales.

Companies: Sears Holdings (SHLD, Fortune 500) announced a net loss for the most recent quarter of $170 million, compared to a profit of $16 million a year ago. The loss per share came in at $1.39 for the quarter. Sears blamed bad weather and the weak economy for their performance. Earnings per share of $1.39 was worse than the $1.22 analysts expected.

Gap (GPS, Fortune 500) will report its company earnings after the close. The clothing retailer is expected to earn 39 cents per share.

Shares of Intel (INTC, Fortune 500) fell more than 1.8%, after Goldman Sachs reportedly downgraded the chipmaker on concerns about oversupply.

USD/JPY breaks above options on Y82.00 and currently holds around Y82.07. But the move further is capped by strong offers from a UK clearer.

Data released:

08:30 UK Retail sales (April) 1.1% 0.6% 0.2%

08:30 UK Retail sales (April) Y/Y 2.8% 2.1% 1.3%

10:00 UK CBI industrial order books balance (May) -2% -7% -11%

The pound fluctuated against the euro and the dollar after data showed retail sales climbed 1.1% from March, when they rose a revised 0.3%. The median forecast of economists was for a 0.8% increase. The pound fell earlier after an index of consumer sentiment declined.

Franc was under pressure as Swiss investor confidence dropped for the first time in three months in May as a worsening European debt crisis and an appreciating franc clouded the economic growth outlook.

An index of investor and analyst expectations fell to minus 11.5 from 8.8 in April.

The yen fell after Japan’s economy fell into recession in the first quarter as production and consumer spending were hit by the March earthquake and tsunami.

Gross domestic product fell by an annualised 3.7% in the first three months, after a revised fall of 3% in last quarter of 2010. Analysts had expected the economy to contract by just 1.9%.

EUR/USD earlier fell to the $1.4202 session lows before later recovered to $1.4295. But bulls failed to breng the rate above the $1.4300 and euro fell to $1.4250/60 on position-adjusting.

GBP/USD rose from $1.6130 to $1.6206 and retreated. Currently rate holds around $1.6184.

USD/JPY rose from Y81.50 to Y81.95, before set stable within the Y81.80/95 range.

Today's focus is on Jobless claims, Existing home sales and Philadelphia Fed index.

Almost as expected, initial jobless claims fell by 44k to 434k in the week ending 7 May. But they have remained elevated, partly because of production disruptions related to the Japanese disaster. We expect initial jobless claims to have fallen to 425k in the week ending 14 May.

Existing home sales rose a stronger than expected 3.7% mom in March, and given that forerunning pending home sales increased by almost 6% in the previous two months, we predict that existing home sales will have gone up again to 5.22m in April. However, the annual rate would still deteriorate from -6.25% to -10%.

Philadelphia Fed index plunged from an extraordinarily high level of 43.4 to a mere 18.5 in April. As manufacturing is still leading the upswing, we expect the index to recover to 22.0 in May.

GBP/USD retreats with offers mantioned from above $1.6200 through to $1.6220. Rate currently trades around $1.6187.

EUR/USD extends recovery to $1.4290 before corrected back. Resistance seen at the overnight Asian high of $1.4308, with stronger offers noted between $1.4310/20. Stops seen placed above. Further offers placed from $1.4330 through to $1.4350.

GBP/USD breaks above $1.6200 to print a high on $1.6208, as EUR/GBP eases to around stg0.8810, off recovery highs of stg0.8825. Next resistance in cable seen at $1.6215/20, a break to open a move on toward $1.6245/50. Rate currently trades around $1.6200.

July WTI Crude sharply higher on the back of earlier comments from the IEA, calling for more oil for refiners to stem market tightening, with a rally to $101.21 from a low of $99.82. Today's resistance is seen $102.93 and $103.90 with support coming in at yesterday's low of $97.97 and $97.22. The Nymex contract currently trades around $101.02.

The yen fell after Japan’s economy fell into recession in the first quarter as production and consumer spending were hit by the March earthquake and tsunami.

Gross domestic product fell by an annualised 3.7% in the first three months, after a revised fall of 3% in last quarter of 2010. Analysts had expected the economy to contract by just 1.9%.

A further contraction is expected in the second quarter before the economy rebounds as reconstruction spending kicks in, although the Japanese economy has suffered more than a decade of low growth and weak consumer spending.

“Encouragingly there have already been signs that supply disruptions are easing and with household confidence set to remain depressed in the near-term, Japanese investor demand for foreign assets should remain weak, helping the yen to remain firm,” said Lee Hardman at Bank of Tokyo Mitsubishi.

The sell-off was tempered by news that China bought Y234.5bn ($2.9bn) in long term Japanese government bonds in April, its biggest single-month purchase of Japanese debt in more than six years.

The pound remained under pressure against both the dollar and the euro as investors continued to rein in their expectations for the next rise in UK interest rates.

Although inflation was shown on Tuesday to have jumped to an annualised 4.5%, investors scaled back their assessment of when the Bank of England was likely to deliver any policy response after minutes from its May meeting were more dovish than expected.

Today's focus is on Jobless claims, Existing home sales and Philadelphia Fed index.

Almost as expected, initial jobless claims fell by 44k to 434k in the week ending 7 May. But they have remained elevated, partly because of production disruptions related to the Japanese disaster. We expect initial jobless claims to have fallen to 425k in the week ending 14 May.

Existing home sales rose a stronger than expected 3.7% mom in March, and given that forerunning pending home sales increased by almost 6% in the previous two months, we predict that existing home sales will have gone up again to 5.22m in April. However, the annual rate would still deteriorate from -6.25% to -10%.

Philadelphia Fed index plunged from an extraordinarily high level of 43.4 to a mere 18.5 in April. As manufacturing is still leading the upswing, we expect the index to recover to 22.0 in May.

Gold is steadily down from earlier highs in Asia of $1499.85, with the metal touching a low of $1489.55, tracking the crude oil move. Gold currently trades around $1491.00.

USD/JPY Y81.10, Y81.00, Y80.95

EUR/JPY Y114.70

GBP/USD $1.6180, $1.6135, $1.6000, $1.6270

USD/CHF Chf0.8890

CHF/JPY Y91.00

AUD/USD $1.0620, $1.0600

AUD/JPY Y86.20, Y85.90

The euro fluctuated against the dollar amid shifting investor appetite for riskier assets as U.S. stocks swung between gains and losses.

Sterling fell against all of its 16 most-traded counterparts as minutes of the British Bank of England’s May 5 meeting showed most policy makers said higher interest rates might hurt the recovery. New Zealand’s dollar was the best performer against the greenback after the nation’s producer prices and consumer confidence increased.

FOMC Minutes show active discussion of exit strategy, with "a range of views" but agreed this "did not mean that the move toward such normalization would necessarily begin soon." Some said need to be prepared to tighten later; a few wanted action later this yr;FOMC agreed no action in the end. Most preferred once asset sales are appropriate, "such sales should be put on a largely predetermined and preannounced path; however, many of those participants noted that the pace of sales could nonetheless be adjusted in response to material changes in the economic outlook. Several other participants preferred instead that the pace of sales be a key policy tool and be varied actively in response to changes in the outlook. A majority of participants preferred that sales of agency securities come after the first increase" in FF target. Many wanted to return SOMA to all Tsys "perhaps over 5 yrs." More gradual asset sales might allow an earlier FF rate hike. Most prefer returning to FF target, talked about a corridor target system of IOER low/DR top.

Shanghai Composite -0.46% 2,859.57

Nikkei -0.43% 9620.82

Hang Seng +0.66% 23,163.38

© 2000-2026. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers