- Analytics

- News and Tools

- Market News

CFD Markets News and Forecasts — 19-03-2024

- The Office for National Statistics will publish the UK CPI data for February on Wednesday.

- United Kingdom’s headline and core annual inflation are likely to fall; monthly CPI is set to jump.

- The UK CPI report could significantly impact the BoE’s interest rate outlook and the Pound Sterling.

The United Kingdom’s (UK) Office for National Statistics (ONS) will publish the Consumer Price Index (CPI) data at 07:00 GMT on Wednesday, just a day before the Bank of England (BoE) monetary policy announcement.

Pound Sterling traders will eagerly look forward to the UK CPI inflation report for fresh cues on whether the BoE will signal its first interest rate cut or retain its “higher rate for longer” stance.

What to expect from the next UK inflation report?

The headline annual UK Consumer Price Index is seen rising 3.6% in February, slowing from a 4.0% increase registered in January. The reading would be at its lowest since September 2021 but still much above the BoE’s 2.0% target.

The Core CPI inflation is set to fall to 4.6% YoY in February after reporting a 5.1% growth in January. Meanwhile, the British monthly CPI is likely to rebound 0.7%, following January’s 0.6% drop.

Despite the UK economy tipping into a technical recession at the end of 2023, the BoE’s brighter economic outlook for this year has dissuaded it from leaning towards a dovish pivot.

At its February policy meeting, the BoE maintained the key rate at 5.25%. Governor Andrew Bailey remained non-committal on what will be the Bank’s next interest rate moves in the upcoming meetings. However, he said that "we need to keep policy sufficiently restrictive for sufficiently long, nothing more, nothing less,” depending on the incoming data.

The policy statement said that the “BoE sees upward risks to CPI from geopolitical factors including the Red Sea, while domestic price and wage risks now "more evenly balanced."

While testifying before the UK Treasury Select Committee (TSC) last month, Bailey explained that “we are looking beyond the temporary period when we expect CPI to return to target this year," adding that he is looking for more sustained progress on the reduction of more persistent elements of inflation.

Therefore, the details of the CPI report, including food prices and the sticky services inflation, will grab markets’ attention in the run-up to the BoE policy announcements.

Previewing the UK inflation data, analysts at TD Securities (TDS) noted that “inflation likely took a decent step down across the board in Feb, largely on the back of base effects. Restaurant prices are the main risk to this print due to uncertainty around the scope for a rebound after sales weighed on prices in Jan.”

“Services remain the key focus for the MPC, and here we look for the y/y rate to come down to 6.0% y/y (BoE: 6.1%),” the TDS analysts said.

When will the UK Consumer Price Index report be released and how could it affect GBP/USD?

The UK CPI data is due for release on Wednesday at 07:00 GMT. The Pound Sterling has been losing ground against the US Dollar in the lead-up to the United Kingdom’s inflation showdown. The US Dollar stays supported at one-week highs ahead of Wednesday’s US Federal Reserve (Fed) monetary policy decision.

A higher-than-expected headline and core inflation data could reverberate the BoE’s “higher rates for longer” view, providing a fresh lift to the Pound Sterling. In such a case, GBP/USD could stage an upswing toward the 1.2800 level. On the other hand, GBP/USD could resume its correction toward 1.2600 if the UK CPI data show a notable slowdown in inflationary pressures, as expectations of a second-quarter BoE rate cut could be back on the table.

Markets are pricing in the first BoE rate cut this year at the August 1 policy meeting.

Dhwani Mehta, Asian Session Lead Analyst at FXStreet, offers a brief technical outlook for the major and explains: “The GBP/USD pair is on a corrective decline from seven-month highs of 1.2893. The 14-day Relative Strength Index (RSI) has fallen below the midline, suggesting that the downside risks remain intact for the Pound Sterling.”

Dhwani adds: “A decisive break below the horizontal 50-day Simple Moving Average (SMA) at 1.2687 is needed to challenge the upward-pointing 100-day SMA of 1.2626. Further south, the 200-day SMA at 1.2595 could be retested. Alternatively, acceptance above the 1.2800 level on a daily closing basis is critical for GBP/USD to initiate a meaningful uptrend toward the multi-month high of 1.2893,” Dhwani adds.

Economic Indicator

United Kingdom Consumer Price Index (YoY)

The United Kingdom (UK) Consumer Price Index (CPI), released by the Office for National Statistics on a monthly basis, is a measure of consumer price inflation – the rate at which the prices of goods and services bought by households rise or fall – produced to international standards. It is the inflation measure used in the government’s target. The YoY reading compares prices in the reference month to a year earlier. Generally, a high reading is seen as bullish for the Pound Sterling (GBP), while a low reading is seen as bearish.

Read more.Why it matters to traders

The Bank of England is tasked with keeping inflation, as measured by the headline Consumer Price Index (CPI) at around 2%, giving the monthly release its importance. An increase in inflation implies a quicker and sooner increase of interest rates or the reduction of bond-buying by the BOE, which means squeezing the supply of pounds. Conversely, a drop in the pace of price rises indicates looser monetary policy. A higher-than-expected result tends to be GBP bullish.

Inflation FAQs

Inflation measures the rise in the price of a representative basket of goods and services. Headline inflation is usually expressed as a percentage change on a month-on-month (MoM) and year-on-year (YoY) basis. Core inflation excludes more volatile elements such as food and fuel which can fluctuate because of geopolitical and seasonal factors. Core inflation is the figure economists focus on and is the level targeted by central banks, which are mandated to keep inflation at a manageable level, usually around 2%.

The Consumer Price Index (CPI) measures the change in prices of a basket of goods and services over a period of time. It is usually expressed as a percentage change on a month-on-month (MoM) and year-on-year (YoY) basis. Core CPI is the figure targeted by central banks as it excludes volatile food and fuel inputs. When Core CPI rises above 2% it usually results in higher interest rates and vice versa when it falls below 2%. Since higher interest rates are positive for a currency, higher inflation usually results in a stronger currency. The opposite is true when inflation falls.

Although it may seem counter-intuitive, high inflation in a country pushes up the value of its currency and vice versa for lower inflation. This is because the central bank will normally raise interest rates to combat the higher inflation, which attract more global capital inflows from investors looking for a lucrative place to park their money.

Formerly, Gold was the asset investors turned to in times of high inflation because it preserved its value, and whilst investors will often still buy Gold for its safe-haven properties in times of extreme market turmoil, this is not the case most of the time. This is because when inflation is high, central banks will put up interest rates to combat it. Higher interest rates are negative for Gold because they increase the opportunity-cost of holding Gold vis-a-vis an interest-bearing asset or placing the money in a cash deposit account. On the flipside, lower inflation tends to be positive for Gold as it brings interest rates down, making the bright metal a more viable investment alternative.

- EUR/USD trades flat around 1.0865 near multi-week lows amid the consolidation of the USD.

- The FOMC is expected to hold the interest rate and maintain macroeconomic projections at its March meeting on Wednesday.

- The Eurozone ZEW Economic Sentiment came in at 33.5 in March vs. 25.0 prior, better than expected.

- The FOMC monetary policy meeting will be in the spotlight on Wednesday.

The EUR/USD pair trades on a flat note above the mid-1.0800s during the early Asian session on Wednesday. Meanwhile, the USD Index (DXY) consolidates its gains near three-week highs of 103.80. Traders await the Federal Open Market Committee's (FOMC) monetary policy meeting later in the day and will take more cues from Chairman Jerome Powell’s press conference and economic projections after the meeting. At press time, the major pair is trading at 1.0865, unchanged for the day.

The Federal Open Market Committee (FOMC) is widely expected to keep its key federal funds interest rate unchanged in a range of 5.25% to 5.5%.and maintain macroeconomic projections at its March meeting on Wednesday. Analysts anticipate FOMC’s Powell to reiterate that the central bank wants to see evidence of inflation data in its battle against inflation before cutting rates. Financial markets expect a 25 basis points (bps) rate cut in July and total cuts of 100 bps this year. The US Dollar (USD) has attracted some buyers in the last sessions as the market’s expectations for rate cuts have been dialed back.

Across the pond, the ZEW Economic Sentiment for the Eurozone rose to 33.5 in March from the previous reading of 25.0, above the market consensus of 25.4. Meanwhile, the Economic expectations for Germany improved to 31.7 versus 19.9 prior. The reports suggested a more optimistic outlook for the Eurozone and Germany. However, the survey failed to boost the Euro (EUR) as traders prefer to wait on the sidelines ahead of the FOMC interest rate decision.

The European Central Bank (ECB) President Christine Lagarde is set to speak on Wednesday, and the European Commission will release its flash Consumer Confidence report for March. The FOMC monetary policy meeting will take center stage later on Wednesday. After the meeting, the attention will turn to Powell’s press conference, which might provide information on the central bank's outlook.

- AUD/USD steady post-RBA's dovish stance and static rates.

- US housing data boosts optimism pre-FOMC decision.

- Fed policy update awaited, with eyes on interest rate forecasts.

The Australian Dollar begins Wednesday’s Asian session virtually unchanged against the US Dollar, following Tuesday’s loss of 0.41%, after the Reserve Bank of Australia (RBA) decision. The RBA kept rates unchanged, tilting more dovish than expected. That said, the AUD/USD trades at 0.6532, almost flat.

Aussie Dollar stays firm following the central bank decision

On Tuesday, the Bank of Japan (BoJ) and the RBA announced their March monetary policy decisions. The BoJ hiked rates by ten basis points, the first in 17 years, ending the era of negative interest rates. In addition, it ended the Yield Curve Control (YCC) and its ETF buying program. The RBA softened its tone while keeping the door open for additional tightening if needed.

In the meantime, US equities ended the session in the green as the Federal Open Market Committee (FOMC) decisions loom. Data-wise, the US economic docket revealed housing data. Building Permits increased by 1.9% from 1.489 M to 1.518M, improving sharply compared to January’s data. Housing Starts rose 10.7% from 1.425M to 1.521 M.

An absent economic docket in Australia keeps AUD/USD traders waiting for the Fed’s decision. ANZ analysts commented that they expect the Fed to make no major changes to the Summary of Economic Projections (SEP). Regarding rate cuts, they noted, “We think it will cut in 25bp increments through the second half of the year, reducing the nominal Fed funds corridor by 100bp this year.”

AUD/USD Price Analysis: Technical outlook

The AUD/USD fell below the 200-day moving average (DMA) of 0.6556, opening the door for further losses. This comes after the RBA decision, and with speculations for a Fed “hawkish” tilt, that would exacerbate a dip to 0.6500. Further losses are seen below March 5 swing low of 0.6477, and the February 13 low of 0.6442. On the upside, the 200-DMA would be the first resistance, followed by the 50-DMA at 0.6558 and the 100-DMA at 0.6586.

- The daily chart of NZD/USD presents a bearish outlook with the RSI and MACD deep in the red zone.

- On the hourly chart, the selling pressure is easing.

- The NZD/USD is operating below the main SMAs, indicating a persisting bearish bias.

The NZD/USD pair registered a decline of 0.54%, falling towards 0.6050 in Tuesday's session. Earlier in the session, indicators reached oversold conditions on the hourly chart, and ahead of the Asian session, the pair seems to be consolidating

On the daily chart, the pair is facing intense selling pressure, as indicated by the declining Relative Strength Index (RSI). The latest reading stands at 36, situated in the negative territory and nearing the oversold threshold, suggesting that sellers currently dominate the market. The Moving Average Convergence Divergence (MACD) also confirms this bearish sentiment, with its rising red bars indicating mounting negative momentum.

NZD/USD daily chart

On the hourly chart, however, the picture differs. The RSI readings appear to fluctuate within the negative territory, with the last reading measured at 42, slightly higher than the reading on the daily chart, denoting tempered selling pressure after bottoming at a low of 22 earlier in the session. Here, the MACD shows a declining selling pressure.

NZD/USD hourly chart

On a broader scale, the trend is still bearish as the pair continues to trade below its 20, 100, and 200-day Simple Moving Averages (SMAs).

- Gold is subdued amid a robust US Dollar in anticipation of the Fed's monetary policy announcement.

- Traders are waiting for the Federal Reserve's statement and economic forecasts.

- Concerns over potential adjustments in the Federal Funds Rate projections keep market sentiment cautious.

Gold prices fell late in the North American session on Tuesday amid a strong US Dollar but despite falling US Treasury bond yields. Market participants await the US Federal Reserve’s (Fed) monetary policy announcement on Wednesday, followed by a press conference by Fed Chair Jerome Powell. Meanwhile, XAU/USD prices are set to remain near $2,150 as traders remain uncommitted to posting fresh bets in favor or against the yellow metal.

The non-yielding metal remains subdued as traders await the Federal Open Market Committee (FOMC) decision. In addition to delivering its monetary policy statement, policymakers are expected to update their projections about the United States economy. Growing concerns that the Fed will reduce its estimates for the Federal Funds Rate (FFR) keep traders on edge.

Daily digest market movers: Gold holds to modest gains as US yields drop

- Tuesday’s US economic docket featured the release of Building Permits in February, which rose by 1.9% MoM from 1.489 million to 1.496 million. Meanwhile, Housing Starts for the same period saw a significant increase of 10.7%, surpassing the expected 8.2%.

- The US 10-year Treasury bond yield has fallen two-and-a-half basis points to 4.296%.

- The latest US economic data witnessed mixed readings in business activity, making it challenging to predict the pace of economic deceleration in the US. The labor market has shown signs of cooling, though the economy added more people to the workforce than expected while fewer people applied for unemployment benefits.

- Recent inflation data in the US showed that inflation on the consumer and producer side surprised to the upside, suggesting that inflation is stickier than expected, failing to break below the 3% threshold.

- Given the backdrop, Fed Chair Jerome Powell’s testimony at the US Congress earlier this month, suggesting the Fed would begin to cut borrowing costs, were justified. However, last week’s inflation figures and Retail Sales data triggered a repricing of Fed rate cut bets, aligning with the US central bank's view of 75 basis points of easing toward the end of 2024.

- According to the CME FedWatch Tool, expectations for a June rate cut stand at 58%, down from 72% a week ago.

Technical analysis: Gold buyers take a breather below $2,170

XAU/USD price has stabilized ahead of the FOMC decision, sitting above the December 4 high of $2,146.79, the first support level. A dovish tilt by the Fed could pave the way for a recovery toward the March 8 high of $2,195.15, followed by the $2,200 mark.

On the other hand, if Gold spot price tumbles below $2,150, look for a breach below December’s 3 high, exposing the March 6 low of $2,123.80, followed by $2,100.

Gold FAQs

Gold has played a key role in human’s history as it has been widely used as a store of value and medium of exchange. Currently, apart from its shine and usage for jewelry, the precious metal is widely seen as a safe-haven asset, meaning that it is considered a good investment during turbulent times. Gold is also widely seen as a hedge against inflation and against depreciating currencies as it doesn’t rely on any specific issuer or government.

Central banks are the biggest Gold holders. In their aim to support their currencies in turbulent times, central banks tend to diversify their reserves and buy Gold to improve the perceived strength of the economy and the currency. High Gold reserves can be a source of trust for a country’s solvency. Central banks added 1,136 tonnes of Gold worth around $70 billion to their reserves in 2022, according to data from the World Gold Council. This is the highest yearly purchase since records began. Central banks from emerging economies such as China, India and Turkey are quickly increasing their Gold reserves.

Gold has an inverse correlation with the US Dollar and US Treasuries, which are both major reserve and safe-haven assets. When the Dollar depreciates, Gold tends to rise, enabling investors and central banks to diversify their assets in turbulent times. Gold is also inversely correlated with risk assets. A rally in the stock market tends to weaken Gold price, while sell-offs in riskier markets tend to favor the precious metal.

The price can move due to a wide range of factors. Geopolitical instability or fears of a deep recession can quickly make Gold price escalate due to its safe-haven status. As a yield-less asset, Gold tends to rise with lower interest rates, while higher cost of money usually weighs down on the yellow metal. Still, most moves depend on how the US Dollar (USD) behaves as the asset is priced in dollars (XAU/USD). A strong Dollar tends to keep the price of Gold controlled, whereas a weaker Dollar is likely to push Gold prices up.

- The positive outlook on the daily chart improved but bulls aren’t yet in command.

- the RSI was seen above 70 in recent hours, which may lead to a consolidation.

- To prevent any potential losses, the bulls must defend the key SMAs.

In Tuesday's session, NZD/JPY is trading at 91.36, registering an uptick of 0.74%. Despite some signals of a consolidation incoming, the market sees dominance by buyers, which leads to a broader bullish outlook. Ahead of the Asian session, the pair may correct overbought conditions on the hourly chart and see some red.

On the daily chart, the NZD/JPY pair posts positive momentum following a shift from the negative territory. The Relative Strength Index (RSI) now sits in the positive territory at 52 while the Moving Average Convergence Divergence (MACD) red bars recede, signaling a potential decrease in negative momentum.

NZD/JPY daily chart

Transitioning to the hourly chart, the NZD/JPY pair displays a stronger positive trend. The RSI enters the overbought territory due to consistent readings above 70. Sharp green bars in the MACD histogram signify strong positive momentum over the past few hours, suggesting buyers dominate the market for now. An RSI above 70 suggests an overextended buying momentum which typically leads to a downward consolidation

NZD/JPY hourly chart

In conclusion, both daily and hourly analyses point to a bullish outlook for the NZD/JPY pair. Traders should monitor the MACD for continued red bar reduction or a shift to green bars, and the RSI to see if it remains within or moves away from the overbought territory in the hourly chart. These data points would suggest a potential price reversal or continuation, respectively.

Regarding a Simple Moving Average (SMA) analysis, despite the bears gaining ground and pushing the pair below the 20-day Simple Moving Average (SMA), the pair remains above the 100 and 200-day SMAs. This pattern suggests that the bulls maintain control of the overall trend.

The Greenback managed to maintain its multi-session constructive bias well and sound and propel the USD Index (DXY) back above 104.00, albeit ephemerally. Sustaining the rally in the Dollar emerged the sharp depreciation of the Japanese yen in the wake of the well-telegraphed rate hike by the BoJ, while it will be all about the Federal Reserve on March 20.

Here is what you need to know on Wednesday, March 20:

Further gains saw the USD Index (DXY) advance to three-week highs past the 104.00 hurdle despite the corrective decline in US yields. The Fed interest rate decision, along with the FOMC Economic Projections and Chair Powell’s press conference, will take centre stage across the pond on March 20.

EUR/USD added to Monday’s pessimism and dropped to multi-week lows near the 1.0830 region, putting the critical 200-day SMA to the test at the same time. On March 20, the ECB’s C. Lagarde will speak, and the European Commission will release its flash Consumer Confidence gauge.

GBP/USD managed to reverse the earlier pullback to the 1.2670 zone and reclaim the area beyond 1.2700 the figure towards the end of the NA session. The UK docket will see the Inflation Rate on March 20.

USD/JPY climbed markedly and traded just pips away from the key 151.00 mark, or 2024 highs, as the selling pressure around the yen picked up strongly following the BoJ rate hike.

AUD/USD extended its leg lower for the fourth session in a row and approached the key support at the 0.6500 neighbourhood in response to the upside bias in the Greenback and the dovish hold from the RBA. On March 20, the RBA’s Consumer Inflation Expectations are due.

Prices of WTI advanced past the $83.00 mark per barrel, or four-month highs, on the back of geopolitics and prospects of stronger demand.

Prices of Gold faded Monday’s small gains and traded with humble losses around the $2,150 zone per troy ounce amidst further advance in the Dollar and lower US yields. Silver prices followed suit and dropped for the second session in a row following Friday’s tops near the $25.50 region per ounce.

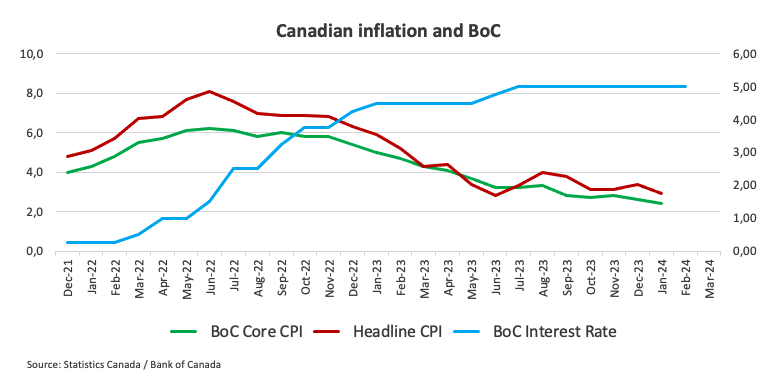

- USD/CAD slips to 1.3565 following Canadian CPI report showing inflation cooling more than expected.

- Disinflationary trend boosts speculation of an upcoming Bank of Canada rate cut, with June odds at 73%.

- US housing data indicates market resilience, adding a positive backdrop to the currency dynamics.

The USD/CAD climbed during the North American session, though it slipped below the 1.3600 figure after data from Canada suggested the disinflationary process continued. At the time of writing, the pair exchanges hands at 1.3565 after hitting a new year-to-date (YTD) high of 1.3613.

The Loonie on the defensive as market participants eye first BoC cut in June

Canada’s economic docket featured the release of inflation data, which decreased below the 3% threshold on annual figures. On a monthly basis, the Consumer Price Index (CPI) saw a 0.3% rise, below the consensus of 0.6%. The Bank of Canada’s (BoC) preferred measure of inflation, the core CPI, slowed in the 12 months to February, from 2.4% to 2.1%.

The data sent the USD/CAD rallying amid speculations that the BoC might cut rates sooner than expected. In the meantime, money market futures data suggest that the odds for the first rate cut by the BoC in the June meeting lie at 73.0%, according to Capital Edge and Refinitiv data.

The US housing sector shows signs of strengthening according to recent economic data. Building Permits in February rose by 1.9% month-over-month, from 1.489 million to 1.496 million. Meanwhile, Housing Starts for the same period saw a significant increase of 10.7%, surpassing the expected 8.2%.

USD/CAD traders brace for Wednesday’s Federal Open Market Committee (FOMC) decision. Futures data shows that the Fed holding rates are unchanged, though uncertainty lies in the update of their Summary of Economic Projections (SEP). Some analysts suggest Fed policymakers could disregard one rate cut, keeping rates higher for longer.

USD/CAD Price Analysis: Technical outlook

After reaching a new YTD high, the USD/CAD retreated below the 1.3600 mark. If the pair closes below the 1.3550 area, that will form an ‘inverted hammer’ opening the door for further losses, but the 100-day moving average (DMA) at 1.3520, a dynamic support level, could cap the losses. Further downside is seen at 1.3500 and at the confluence of the 200 and 50-DMA at 1.3481/87. On the other hand, if buyers come back and reclaim 1.3600, look for a challenge of the November 24 high at 1.3711.

- The EUR/JPY rallied in Tuesday’s session, seeing more than 1% gains.

- The daily RSI reveals growing buying momentum, deep in positive territory.

- The hourly chart hints at overbought conditions, and the RSI staying above 70 signals the potential for profit-taking sell-offs.

In Tuesday's session, the EUR/JPY pair is trading around the 164.00 region, marking a strong rally of 1.14%. The daily outlook is tilting in favor of the buyers while overbought conditions seen on the hourly chart suggest that consolidation is on the horizon.

On the daily chart, the pair exhibits increasing momentum, as indicated by the latest Relative Strength Index (RSI) values. Moving from negative territory, the recent RSI trajectory consolidated in positive territory, lately peaking at 65 which is approaching overbought status. Currently, buyers dominate the market, leading to the possibility of the pair moving into overbought conditions soon.

EUR/JPY daily chart

When examining the hourly chart, the EUR/JPY pair displays persistent overbought conditions. The RSI values consistently stay strong and above 70 which suggests intense buying pressure. The Moving Average Convergence Divergence (MACD) reinforces this bullish momentum with its rising green bars. However, these overbought conditions might soon provoke a downward correction as overbuying could lead to profit-taking sell-offs.

EUR/JPY hourly chart

Conclusively, both the daily and hourly charts indicate robust buying momentum. The positive outlook is further corroborated by the pair trading above the main Simple Moving Averages (SMAs) of 20, 100, and 200 days. Any downward correction which keeps the pair above these levels, won’t affect the overall bullish trend.

- Euro losses a step vs US Dollar, eyes on Fed decision.

- US housing gains, Building Permits, and Housing Starts rise.

- Germany’s ZEW and EU surveys beat expectations, uplifting investor sentiment.

The Euro remains on the defensive against the US Dollar as market participants await March’s monetary policy decision by the Federal Open Market Committee (FOMC) on Wednesday. Therefore, the EUR/USD trades at 1.0859 and loses 0.12%.

EUR/USD dips amid central bank movement, positive US housing data

Tuesday’s session witnessed two major central banks' decisions. The Bank of Japan (BOJ) exited from negative interest rates, though delivered a dovish hike, which weakened the Japanese Yen (JPY) against most G8 currencies. The Reserve Bank of Australia (RBA) holds rates unchanged at 4.35%, with the RBA still considering a rate hike if inflation reaccelerates.

Aside from this, Wall Street prints decent gains as global bond yields drop. The US economic docket showed the housing sector is gathering steam. US Building Permits in February grew 1.9%, MoM, up from 1.489 million to 1.496 million. At the same time, Housing Starts for the same period exceeded estimates of 8.2%, increasing by 10.7%.

In the meantime, the US 10-year Treasury bond yield retreats two basis points, down to 4.034%. The US Dollar Index (DXY), a gauge of the buck’s value against a basket of other currencies, gains 0.23%, up at 103.82.

On the Eurozone’s (EU) front, Germany published the March ZEW Survey, which improved the country to 31.7, while the EU one surged to 33.5, beating estimates.

EUR/USD Price Analysis: Technical outlook

The EUR/USD daily chart suggests the pair is neutral to downward biased, though dynamic support levels like the 200, 100, and 50-day moving averages (DMAs) capped the Euro’s losses, opening the door for a recovery. If buyers lift the exchange rate above 1.0900, it could expose the March 13 high at 1.0964. followed by the year-to-date (YTD) high at 1.0981. On the other hand, sellers need to push prices below the 200-DMA at 1.0838, so they could threaten to challenge 1.0800.

- Mexican Peso weakens in early North American trading as US Dollar gains strength.

- Mexican data is mixed though the economy finished 2023 on a higher note.

- Central bank divergence between Fed and Banxico could bolster USD/MXN pair.

The Mexican Peso depreciated in early trading during the North American session as the US Dollar climbed some 0.25%, based on the US Dollar Index (DXY). Speculation that the Bank of Mexico (Banxico) would ease policy on Thursday grew, while traders continued to trim odds for the Federal Reserve’s first rate cut. The USD/MXN trades at 16.87, clocking a gain of 0.28%.

Mexico’s economic docket featured the release of Aggregate Demand and Private Spending, with both figures exceeding Q3 2023 readings, suggesting the economy ended the year on a higher note. Across the border, US housing data exceeded estimates and improved compared to January’s data, and now all heads turn toward the Federal Open Market Committee (FOMC) decision on Wednesday.

Daily digest market movers: Mexican Peso on defensive amid dovish Banxico

- Estimates that Banxico will lower the interest rate from 11.25% to 11% puts “some” pressure on the Mexican currency, which could lift the USD/MXN toward the 17.00 mark.

- Mexico’s economic data released on Tuesday:

- Aggregate Demand rose by 0.3% QoQ in Q4, up from 0%. On an annual basis decelerated from 2.7% to 2.6%.

- Private Spending on a quarterly basis slowed from 1.2% to 0.9%. On a yearly basis, it improved from 4.3% to 5.1%.

- The USD/MXN is being driven by the reduction of interest rate spreads between Mexico and the United States. This could bolster and set the USD/MXN direction toward the 17.00 figure.

- On March 21, Banxico is expected to decrease interest rates, even though it could feature a 3-2 vote split. Recent speeches and media appearances show that Banxico’s Governing Council is divided, with Governor Victoria Rodriguez Ceja, Omar Mejia Castelazo and Galia Borja Gomez leaning dovish. On the hawkish front lie Jonathan Heath and Irene Espinosa Cantellano.

- An economic slowdown in Mexico is the main event that could spark Banxico’s first rate cut as the central bank has adjusted its economic projections to the downside. Mexico’s central bank expects the economy to grow 2.8% YoY in 2024, down from 3% and maintaining at 1.5% for 2025.

- US Building Permits in February rose 1.9% from 1.495 million to 1.518 million, suggesting that demand continues to increase.

- Housing Starts increased by 10.7% compared to January’s data as starts jumped from 1.425 million to 1.521 million.

- The latest inflation figures in the United States prompted investors to price in a less dovish stance. Money market futures had adjusted their rate cut expectations more in line with the Fed as they foresee the Federal Funds Rate (FFR) at 4.71% toward year end. The next Fed meeting is scheduled for March 19-20 next week, and analysts estimate no change to its Federal Funds Rates (FFR).

Technical analysis: Mexican Peso begins to weaken as USD/MXN aims above 16.80

The USD/MXN has shifted to a neutral bias as buyers stepped in and lifted the exchange rate above the January 8 swing low of 16.78. After breaching that level, the pair clocked a new two-week high of 16.94, though buyers are taking a breather before launching an assault toward 17.00. Once that hurdle is overcome, the next resistance would be the 50-day Simple Moving Average (SMA) at 17.02, followed by the 100-day SMA at 17.16 and the 200-day SMA at 17.21.

On the flip side, the exotic pair must drop below 16.80, which could pave the way for a test of last year’s low of 16.62, followed by October 2015’s low of 16.32 and the 16.00 psychological level.

USD/MXN Price Action – Daily Chart

Mexican Peso FAQs

The Mexican Peso (MXN) is the most traded currency among its Latin American peers. Its value is broadly determined by the performance of the Mexican economy, the country’s central bank’s policy, the amount of foreign investment in the country and even the levels of remittances sent by Mexicans who live abroad, particularly in the United States. Geopolitical trends can also move MXN: for example, the process of nearshoring – or the decision by some firms to relocate manufacturing capacity and supply chains closer to their home countries – is also seen as a catalyst for the Mexican currency as the country is considered a key manufacturing hub in the American continent. Another catalyst for MXN is Oil prices as Mexico is a key exporter of the commodity.

The main objective of Mexico’s central bank, also known as Banxico, is to maintain inflation at low and stable levels (at or close to its target of 3%, the midpoint in a tolerance band of between 2% and 4%). To this end, the bank sets an appropriate level of interest rates. When inflation is too high, Banxico will attempt to tame it by raising interest rates, making it more expensive for households and businesses to borrow money, thus cooling demand and the overall economy. Higher interest rates are generally positive for the Mexican Peso (MXN) as they lead to higher yields, making the country a more attractive place for investors. On the contrary, lower interest rates tend to weaken MXN.

Macroeconomic data releases are key to assess the state of the economy and can have an impact on the Mexican Peso (MXN) valuation. A strong Mexican economy, based on high economic growth, low unemployment and high confidence is good for MXN. Not only does it attract more foreign investment but it may encourage the Bank of Mexico (Banxico) to increase interest rates, particularly if this strength comes together with elevated inflation. However, if economic data is weak, MXN is likely to depreciate.

As an emerging-market currency, the Mexican Peso (MXN) tends to strive during risk-on periods, or when investors perceive that broader market risks are low and thus are eager to engage with investments that carry a higher risk. Conversely, MXN tends to weaken at times of market turbulence or economic uncertainty as investors tend to sell higher-risk assets and flee to the more-stable safe havens.

- US Housing Starts and Building Permits from February beat expectations.

- All eyes are now on the Fed’s updated Dot Plot on Wednesday, an interest rate pause is already priced in.

- US Treasuries are edging downward but remain at multi-week highs.

The US Dollar Index (DXY) is fluctuating around 104.00, registering gains ahead of the impending Federal Open Market Committee (FOMC) meeting on Wednesday. This marks the highest level since March 1. Markets await fresh guidance, and if the Federal Reserve’s (Fed) updated Dot Plot or Chair Jerome Powell provides any dovish signals, the USD may resume its downside action.

In the meantime, Fed officials remain cautious about rushing too soon to start cutting as inflation remains sticky, which seems to also provide a cushion to the USD. The fresh guidance from Wednesday and incoming data will continue dictating the pace of the Greenback for the short term.

Daily digest market movers: DXY extends gains on strong housing data ahead of Fed decision

- Housing Starts in February reported by the US Census Bureau demonstrated a 10.7% MoM increase, rebounding from a -12.3% reading in the previous report.

- Building Permits (Feb) came in at 1.521M, higher than the 1.425M expected.

- The market currently anticipates the Fed remaining on its hawkish path, factoring in a 10% likelihood of a rate cut in May and a 65% chance in June. However, those odds may change after Wednesday’s FOMC decision.

- The 2-year yield is currently trading at 4.70%, while the 5-year yield stands at 4.31% and the 10-year yield at 4.30%.

DXY technical analysis: DXY sees bullish momentum dominate market

The technical indicators on the daily chart reflect a positive bias. The Relative Strength Index (RSI), bearing a positive slope in positive territory, signals an augmenting bullish strength. Simultaneously, the histogram of the Moving Average Convergence Divergence (MACD) is showcasing rising green bars, further affirming the dominance of buying momentum.

The Simple Moving Averages (SMAs) further bolster this bullish outlook. The DXY is now positioned above the convergence of 20,100 and 200-day Simple Moving Averages (SMAs) near the 103.50-70 area, which suggests that bulls are controlling the broader outlook.

Considering these signals, a snapshot of the current technical outlook implies that overall, bulls are gaining ground. However, bulls must build strong support above the mentioned SMAs to consolidate their movements.

Central banks FAQs

Central Banks have a key mandate which is making sure that there is price stability in a country or region. Economies are constantly facing inflation or deflation when prices for certain goods and services are fluctuating. Constant rising prices for the same goods means inflation, constant lowered prices for the same goods means deflation. It is the task of the central bank to keep the demand in line by tweaking its policy rate. For the biggest central banks like the US Federal Reserve (Fed), the European Central Bank (ECB) or the Bank of England (BoE), the mandate is to keep inflation close to 2%.

A central bank has one important tool at its disposal to get inflation higher or lower, and that is by tweaking its benchmark policy rate, commonly known as interest rate. On pre-communicated moments, the central bank will issue a statement with its policy rate and provide additional reasoning on why it is either remaining or changing (cutting or hiking) it. Local banks will adjust their savings and lending rates accordingly, which in turn will make it either harder or easier for people to earn on their savings or for companies to take out loans and make investments in their businesses. When the central bank hikes interest rates substantially, this is called monetary tightening. When it is cutting its benchmark rate, it is called monetary easing.

A central bank is often politically independent. Members of the central bank policy board are passing through a series of panels and hearings before being appointed to a policy board seat. Each member in that board often has a certain conviction on how the central bank should control inflation and the subsequent monetary policy. Members that want a very loose monetary policy, with low rates and cheap lending, to boost the economy substantially while being content to see inflation slightly above 2%, are called ‘doves’. Members that rather want to see higher rates to reward savings and want to keep a lit on inflation at all time are called ‘hawks’ and will not rest until inflation is at or just below 2%.

Normally, there is a chairman or president who leads each meeting, needs to create a consensus between the hawks or doves and has his or her final say when it would come down to a vote split to avoid a 50-50 tie on whether the current policy should be adjusted. The chairman will deliver speeches which often can be followed live, where the current monetary stance and outlook is being communicated. A central bank will try to push forward its monetary policy without triggering violent swings in rates, equities, or its currency. All members of the central bank will channel their stance toward the markets in advance of a policy meeting event. A few days before a policy meeting takes place until the new policy has been communicated, members are forbidden to talk publicly. This is called the blackout period.

The US Federal Reserve (Fed) will announce its Interest Rate Decision on Wednesday, March 20 at 18:00 GMT and as we get closer to the release time, here are the expectations as forecast by analysts and researchers of 15 major banks.

The Fed is expected to keep rates unchanged in the range of 5.25%-5.50% for the fifth time in a row. Investors are eagerly awaiting the quarterly dot plot. The Fed’s last dot plot suggested a median forecast of three rate cuts through 2024. The Summary of Economic Projections (SEP) and Fed Chair Jerome Powell’s post-meeting press conference will also garner attention.

ANZ

We expect the FOMC will leave the target rate for fed funds (FFR) unchanged. Despite a relatively brisk start to 2024, we aren’t expecting any material changes to the FOMC’s current profile of moderating growth, gently rising unemployment and a gradual yet persistent return to target inflation. We acknowledge the possibility of a modest up shift in the dot plot. Discussions on what to do with quantitative tightening (QT) will begin. Recent Fed rhetoric suggests it’s unlikely any specific announcement will come. We think that could come from the May meeting onwards.

Commerzbank

The Fed is unlikely to change its key interest rates, leaving the target range for Fed Funds at 5.25%-5.50% (where it has been since July 2023). The Fed is also likely to reiterate that it does not consider a rate cut appropriate until it has gained greater confidence that inflation is moving sustainably towards 2%. We assume that the dot plot will provide for three rate cuts in 2024, as in the last update in December.

Nordea

We expect no changes to the Fed Funds rate or QT at this meeting. However, the Fed will likely need to revise its growth and inflation projections higher for 2024. This could lead to a median FOMC dot plot that shows only two rate cuts this year compared to the latest projection for three rate cuts, made in December 2023.

Danske Bank

We do not expect the Fed to make monetary policy changes in its March meeting. Besides the obvious focus on rate cut timing cues, we will keep an eye on the updated rate and economic projections as well as more detailed discussion on QT. We think the Fed will cut rates for the first time in May and start to gradually phase out QT only from September. 2024 GDP forecast is set to be revised higher, but we think ‘dots’ will still signal three rate cuts for this year as a whole.

ABN Amro

We expect the Fed to keep policy on hold at the March FOMC meeting. The Committee will also update its quarterly projections, and we expect this to show the median FOMC member still expecting three rate cuts this year. Chair Powell is likely to maintain the cautiously hawkish tone of recent remarks and not seek to rock the boat, as the Fed is likely comfortable with current market pricing for rate cuts. Powell signalled at the January meeting that the FOMC would discuss the winddown of QT at the March meeting. Given that use of the Overnight Repo Facility has stabilised recently, it is probably too soon for the Fed to announce a winddown plan at this meeting, but Powell is likely to confirm that this is now being actively worked on.

ING

Some people think the Fed may need to hike rates further, but we don’t see this happening. We think the next move is a cut, most likely in June. At the December forecast update, the Fed signalled they felt three 25 bps rate cuts would be the most likely path forward for 2024 with a further 100 bps of cuts pencilled in for 2025. We expect a similar set of projections at the March FOMC meeting with the messaging indicating that the Fed is inclined to cut rates later this year, but they need to see more evidence to justify that action. We expect 125 bps of cuts this year, starting in June, with a further 100 bps in 2025 as hopes rise for a soft landing for the economy.

TDS

The FOMC is widely expected to keep the Fed funds target range unchanged at 5.25%-5.50%, with Chair Powell likely continuing to argue for patience regarding the Committee's next policy steps amid the recent firming of inflation. We also look for the Fed to maintain its median projection for three cuts this year and for the release of preliminary details about QT plans. Risk-reward under our baseline of the Fed's 2024 dot remaining unchanged in a market that is net long the dollar is for USD weakness.

Rabobank

The FOMC needs to see more data to gain confidence that inflation is heading sustainably toward its 2% target. We continue to pencil in the first rate cut in June. However, the risk that the Fed will start later than June, rather than before June (= May), has increased. Once started, we expect the Fed to continue with one cut of 25 bps per quarter. However, since our new economic forecasts assume a Trump victory in November, leading to a universal import tariff, we expect inflation to rebound in 2025. This is likely to cause a pause in the Fed’s cutting cycle during the course of next year.

Deutsche Bank

We expect only minor revisions to the meeting statement that saw an overhaul last meeting. With regards to the SEP, the growth and unemployment forecasts are unlikely to change but the 2024 inflation forecasts potentially could. We expect the Fed to revise up their 2024 core PCE inflation forecast by a tenth to 2.5%, although they see meaningful risks that it gets revised up even higher to 2.6%. A 2.5% core PCE reading would allow just enough wiggle room to keep the 2024 fed funds rate at 4.6% (75 bps of cuts). However, if core PCE inflation were revised up to 2.6%, it would likely entail the Fed moving their base case back to 50 bps of cuts, as this would essentially reflect the same forecasts as the September 2023 SEP.

Wells Fargo

We do not expect any policy changes at this meeting. We now believe the Committee will wait until its June 12 meeting before reducing its target range for the federal funds rate by 25 bps. We then look for the FOMC to cut rates by 25 bps at each of its meetings in July, September and December.

RBC Economics

The Fed is widely expected to stand pat on the fed funds range for a fifth consecutive meeting on Wednesday. But any shift in the monetary policy statement language will be closely watched after two straight months of upside surprises on inflation.

NBF

The FOMC is widely expected to leave its key policy rates unchanged for the fifth straight meeting. Since January, policymakers have been waiting for ‘greater confidence that inflation is moving sustainably toward 2 percent’ and recent data is unlikely to have provided the FOMC much assurance. As such, don’t expect the easing bias in the rate statement to become any more pronounced. Markets will be most closely watching the ‘dot plot’ to see whether policymakers dial back the amount of expected easing for 2024. In December, 75 bps of cuts were signaled but the distribution was skewed towards less easing. Given recent inflation developments, there’s a reasonable chance some dots could move higher, bringing the median up with it.

Citi

While markets are increasingly pricing a more hawkish Fed following stronger-than-expected inflation, Chair Powell is likely to emphasize slowing YoY core PCE inflation and restate that the Fed is ‘not far’ from achieving the level of confidence necessary to begin lowering rates. We expect a largely unchanged SEP. Core PCE at the end of 2024 could be nudged higher to 2.5% from 2.4%. Most importantly, median dots are likely to remain unchanged. The FOMC will also discuss balance sheet reduction in depth which might result in some principles being published on how the Fed plans to taper and then eventually end balance sheet reduction.

SocGen

The FOMC convenes this week against the backdrop of mounting inflation pressures and rising concerns over the feasibility and timing of interest rate reductions. The Fed has ample time to assess the situation, and we expect no policy change in March. Economic indicators in the coming months will play a decisive role in determining whether mid-year rate cuts are a viable option. The Fed's new dot plot may prove less dovish than the 75 bps in rate cuts suggested in December.

CIBC

The funds rate will be left unchanged, and Powell ought to avoid giving any definitive signal on when the first cuts will arrive. We’ll concede that recent data on inflation hasn’t been friendly to our forecast for 100 bps of cuts in the latter half of the year, and we’ll need to see some softening in jobs, wages and underlying inflation in the coming months to stick with that view. While it’s a close call, with some risk of a more hawkish turn to only 50 bps of easing, we see the Fed just hanging on to its median projection for three cuts in 2024, and the median call for 2025 also looks likely to be little changed, with the individual dots still widely dispersed. Median forecasts for growth, inflation and unemployment for this year could shift by a decimal place or two here and there, which won’t be material. If so, the biggest change could be in the ‘long term’ outlook for rates, typically viewed as the Fed’s assessment of where neutral will lie. With the economy showing resilience to rates above 5%, the long-term projection will likely move higher, with 2.75% or even 3% now looking like more plausible outcomes.

The United Kingdom will release the Consumer Price Index (CPI) report on Wednesday, March 20 at 07:00 GMT and as we get closer to the release time, here are the forecasts by the economists and researchers of four major banks regarding the upcoming UK inflation print.

The annual headline inflation is forecast to have grown at a slower pace of 3.6% against 4.0% in January. In the same period, core inflation – which excludes volatile food and energy prices – is forecast to have decelerated to 4.6% from 5.1%. If so, headline would be the lowest since September 2021 but still well above the 2% target.

TDS

We expect UK headline inflation to take another step down in February to 3.4% YoY, thus leaving it a touch below the Bank of England's forecast of 3.5% YoY. Core inflation will likely also fall quite a bit this month, we forecast a 0.6ppts decline to 4.5% YoY, which would be the lowest year-on-year rate since January 2022. We expect services inflation at 6.0%, 0.1ppts below the MPC's forecast. Our unrounded forecasts for headline/core are 3.43%/4.46%, so we see risks skewed to the upside for headline inflation but to the downside for core. Overall, barring any major surprises to this month's data, headline inflation is still set to fall below target in April and remain below target for the rest of the year.

Deutsche Bank

We expect a sizeable move lower, including the headline CPI slowing to 3.4% (vs. 4% in January) and core to 4.5% (5.1%).

SocGen

After a three-month period of core being stuck at 5.1%, we expect a sharp 0.6pp decline in February to 4.5% YoY, its lowest rate in two years. This decline should contribute to a 0.6pp fall in headline inflation to 3.4% YoY.

Citi

CPI Inflation, February – Citi Forecast 3.4% YoY, Prior 4.0% YoY; CPI Core, February – Citi Forecast 4.4% YoY, Prior 5.1% YoY (goods prices still subdued).

USD/JPY has risen back above the 150.00 level after the BoJ finally ended its negative interest rate policy. Economists at Rabobank analyze the pair’s outlook.

BoJ prospects of hiking rates again this year remain highly uncertain

In today’s policy statement, the BoJ remarked that as ‘indicated by the results of this year's annual spring labour-management wage negotiations to date, it is highly likely that wages will continue to increase steadily this year’. This has supported the Bank’s confidence that its price stability target is in sight.

Assuming the strong pay deals awarded to unionised workers spread out to the 70% of employees who are not in a union, Japan’s real wage growth could soon be turning higher. Policymakers will be hoping that this boosts consumption which in turns supports corporate profitability. This would indicate that the BoJ’s virtuous cycle is complete. So, while the BoJ may be able to hike rates again this year, this prospect currently remains highly uncertain.

Our three-month USD/JPY forecast of 146.00 assumes a first Fed rate cut in June and an improvement in Japanese real wage data. Our 12-month USD/JPY target is 140.00.

Economists at ING expect the Federal Reserve to start cutting rates in June.

125 bps of cuts this year, starting in June

Given the Fed doesn’t want to cause a recession if it can avoid it, we believe they will be in a position to start moving monetary policy from restrictive territory to a more neutral footing before the summer.

We expect 125 bps of cuts this year, starting in June, with a further 100 bps in 2025 as they seek a soft landing for the economy.

- USD/CAD jumps above 1.3600 as Canadian consumer inflation surprisingly eases in February.

- BoC’s preferred inflation measure decelerated to 2.1% from 2.4% in January on a year-on-year basis.

- The market sentiment remains downbeat amid uncertainty ahead of Fed policy.

The USD/CAD pair soars above the round-level resistance of 1.3600 in the early New York session on Tuesday. The Loonie asset strengthens as the Canadian Consumer Price Index (CPI) for February turns out surprisingly softer than expected.

The annual headline CPI grew at a slower pace of 2.8% than expectations of 3.1% and the former reading of 2.9%. On a monthly basis, the headline CPI rose by 0.3% against the expectation of 0.6%. The Bank of Canada’s (BoC) preferred inflation measure, which strips of eight volatile items grew at a steady pace of 0.1% monthly. The underlying inflation decelerated to 2.1% from 2.4% in January.

The soft inflation data could prompt expectations that the BoC will reduce interest rates sooner than expected. When the BoC considers reducing interest rates, the Canadian dollar faces liquidity outflows.

Meanwhile, the Canadian Dollar has also been weighed down by dismal market sentiment. The appeal for risk-perceived assets weakens amid uncertainty ahead of the Federal Reserve’s (Fed) interest rate decision, which will be announced on Wednesday. The Fed is expected to keep interest rates unchanged in the range of 5.25%-5.50%. The US Dollar Index (DXY) rises to 103.85 as demand for safe-haven assets improves.

Apart from the Fed’s policy decision, investors will focus on the dot plot and economic projections. The dot plot shows policymakers' interest rate projections for different timeframes.

The Australian Dollar (AUD) has weakened following the RBA’s latest policy meeting. Economists at MUFG Bank analyze Aussie’s outlook.

RBA to begin cutting rates during the second half of this year

The RBA left their policy rate unchanged for the third consecutive meeting at 4.35%. However, the RBA softened their guidance over the likelihood of further rate hikes in the updated policy statement.

The updated guidance from the RBA has made us more confident that the RBA has reached the end of their rate hike cycle although the risk of one final hike can’t be completely ruled out.

We expect the RBA to begin cutting rates during the second half of this year. Unlike other major central banks like the Fed, the RBA is expected to be slower to lower rates.

In contrast, one less supportive development for the Aussie has been the recent sharp decline in the price of iron ore which has continued to plunge so far this month. After peaking at the start of this year, the price of iron ore has since declined by almost 30% which continues to pose downside risks for the Aussie in the near term.

After a brief dip just below $2,150, Gold started to recover at the start of the new week. Strategists at Commerzbank analyze the yellow metal’s outlook.

US data has been mixed of late

The so-called ‘dot plot’, i.e. the interest rate forecasts of the individual FOMC members, is likely to attract particular attention at this week's Fed meeting.

US data has been mixed of late. While economic data has been rather disappointing, price data has pointed to ongoing inflationary pressures. Against this backdrop, we believe that the central bankers are unlikely to change their assessment, leaving the ‘dots’ more or less unchanged. This would probably be positive for Gold, as some market participants are likely to expect an upward revision of interest rate expectations following the US inflation data.

USD/JPY rose back above 150.00 after the Bank of Japan abolished negative interest rates and yield curve control. Kit Juckes, Chief Global FX Strategist at Société Générale, analyzes the pair’s outlook.

A well-flagged BoJ move has emboldened Yen bears

The BoJ brought the age of negative rates and yield curve control to an end.

I’m disappointed by the market reaction to the BoJ because there’s a good chance this eventually proves to be a pivotal moment for Japan and the BoJ.

USD/JPY 152.00 now becomes a big psychological level going into Wednesday’s FOMC.

Economists at MUFG Bank analyze Japanese Yen (JPY) outlook after the Bank of Japan (BoJ) policy announcement.

Will Yen selling persist after BoJ policy changes?

We see limits to the extent of Yen selling that can take place from here. Of course, there are greater USD/JPY upside risks over the very short term given this risk event has now passed without any major hawkish surprise and if the FOMC on Wednesday were to drop a DOT in its policy rate profile, US yields will likely jump further and potentially drag USD/JPY to intervention levels.

But over the medium term, we view today’s announcements as hugely significant that is consistent with higher yields and a stronger Yen.

- The US Dollar soars on Tuesday after Asian markets set the scene for a stronger Greenback.

- Traders are letting the dust settle over the BoJ rate decision ahead of US housing data.

- The US Dollar Index briefly hit 104.00 before retreating a touch.

The US Dollar (USD) jumped firmly in the green on Tuesday, giving a big thank you to the Japanese Yen. The Yen, which accounts for roughly 13% of the US Dollar Index (DXY), depreciated nearly 1% against the Greenback after the Bank of Japan (BoJ) delivered a dovish interest-rate hike. The move away from negative interest rates was well communicated months in advance and came as no surprise to markets, resulting in a weaker Yen.

Meanwhile, the US economic data front was all about housing data on Tuesday. Both Building Permits and Housing Starts were better than expected ahead of the US Federal Reserve (Fed) rate decision on Wednesday. The Federal Open Market Committee (FOMC) starts its two-day meeting this Tuesday, and some further contraction in the US housing market could put June back on the table for that eagerly anticipated rate cut.

Daily digest market movers: Ahead of Fed

- In Asia overnight, the BoJ has hiked interest rates for the first time in almost two decades, to 0% from -0.10%. However, markets sent the Japanese Yen weaker after comments from BoJ Governor Kazuo Ueda that the BoJ will keep its monetary easing in place and that this is probably a one-and-done hike.

- In the aftermath of the BoJ rate decision, the Greenback and the Chinese Yuan benefited the most from the devaluing Yen.

- In Europe, European Central Bank Vice President Luis De Guindos said that June will be pivotal for the ECB rate decision. An initial rate cut is already a possibility at the June meeting.

- At 12:30 GMT, US Housing data was released:

- Housing Starts for February came in at 1.521 million, above the estimate of 1.425 million and beating the January number at 1.374 million.

- Building Permits for February jumped to 1.518 million, substantially higher than the 1.489 million from January.

- The US Treasury will be placing a 52-week bill in the market at 15:30 GMT.

- Equities are not reacting well to the dovish hike from the BoJ, with Europe and US indexes trading in the red ahead of the US opening bell.

- According to the CME Group’s FedWatch Tool, expectations for a Fed pause in the March 20 meeting are at 99%, while chances of a rate cut stand at 1%.

- The benchmark 10-year US Treasury Note trades around 4.30%, continuing its ascent from last week.

US Dollar Index Technical Analysis: Stronger due to outside forces

The US Dollar Index (DXY) is fading a touch after it briefly hit the 104.00 mark. Ahead of the US Federal Reserve meeting, this does not look the ideal place to be as markets will be looking for any dovish clues from Chairman Jerome Powell. Any dovish hint could mean that Tuesday’s move will be quickly pared back, with the DXY dropping back deep into 103.00 territory.

On the upside,104.96 remains the first level in sight. Once above there, the peak at 104.97 from February comes into play, ahead of the 105.00 region with 105.12 as the first resistance.

Expect some easing as the dust settles on the BoJ and ahead of the Fed meeting on Wednesday. Some support should come in from the 200-day Simple Moving Average (SMA) at 103.70, the 100-day SMA at 103.60 and the 55-day SMA at 103.50. The 103-area, thus, looks well equipped and covered with support levels to catch any retreats in the DXY.

- Housing Starts and Building Permits in the US increased in February.

- The US Dollar Index clings to daily gains near 104.00.

Housing Starts in the US rose 10.7% in February to 1.52 million units, the monthly data published by the US Census Bureau revealed on Tuesday. This reading followed the 12.3% decrease recorded in January.

In the same period, Building Permits increased 1.9% after falling 0.3% in January.

Market reaction

The US Dollar Index preserves its bullish momentum after the data and was last seen rising 0.32% on the day at 103.92.

- AUD/USD falls sharply to 0.6500 on multiple headwinds.

- The RBA kept interest rates unchanged at 4.35% and delivered neutral guidance on interest rates.

- Investors await the Fed’s dot plot for fresh guidance on interest rates.

The AUD/USD pair faces an intense sell-off as downbeat market sentiment has weakened the appeal of risk-perceived assets. The Aussie asset falls to the psychological support of 0.6500 in Tuesday’s late European session as the US Dollar strengthens amid uncertainty ahead of the Federal Reserve’s (Fed) monetary policy decision, which will be announced on Wednesday.

S&P 500 futures have posted significant losses in the London session, portraying a decline in investors’ risk appetite. The US Dollar Index (DXY) continues its winning streak for the fourth trading session, rises to 104.00 amid upbeat safe-haven bid. 10-year US Treasury yields have come down slightly to 4.32%. Broadly, US bond yields exhibit strength as Fed rate cut expectations for the June policy meeting have dropped due to hot inflation data for February.

The Fed’s interest rate decision will guide the next move in the US Dollar. The CME FedWatch tool shows that the central bank will keep interest rates unchanged in the range of 5.25%-5.50% for the fifth time in a row. Therefore, investors will focus mainly on the release of the dot plot and economic projections. The dot plot, updated every quarter, shows interest rate projections from Fed officials for various timeframes.

Meanwhile, the Australian Dollar weakens as the Reserve Bank of Australia (RBA) delivers neutral guidance on the Official Cash rate (OCR) after keeping it unchanged at 4.35%. RBA Governor Michele Bullock said in his policy statement that a victory on inflation cannot be announced yet. The RBA needs to be more confident that inflation is coming down to consider a rate cut.

GBP/USD trades weaker below support in the low 1.2700s. Economists at Scotiabank analyze the pair’s outlook.

Resistance is 1.2745/1.2750

UK CPI data due on Wednesday and Thursday’s BoE decision may help limit near-term losses.

Sterling’s extended run lower from its early March peak pushed below minor support in the low 1.2700 zone to test the 40-DMA at 1.2680. Short-term price action suggests a potentially positive response to that test in the form of a bullish ‘hammer’ pattern, however.

Resistance is 1.2745/1.2750.

Support below 1.2675/1.2680 sits at 1.2600/1.2610.

EUR/USD finds support in the low 1.0800s. Economists at Scotiabank analyze the pair’s outlook.

EUR may be trying to rebound from the low 1.0800s

Soft price action on Monday and a pickup in intraday bear momentum suggest downside risks remain for the EUR but early Tuesday price signals suggest the EUR may be trying to base/rebound from the low 1.0800s via an intraday bullish ‘hammer’ signal.

Intraday gains back above 1.0875 would give the EUR a little more technical strength intraday.

Support is 1.0835/1.0840 and 1.0800.

- Natural Gas prices are trying to test the $1.90 resistance.

- A mix of geopolitical pressure, ESG, and unforeseen outages are the main drivers supporting prices.

- The US Dollar Index rallies to 104.00 after the BoJ delivered a dovish hike.

Natural Gas prices (XNG/USD) are rallying for a second consecutive day on Tuesday towards the key $1.90 resistance level. When overlooking the charts, gas prices have jumped actually near 20% in five days combined on all gas contracts with near 6% on XNG/USD alone. Traders are seeing a mixture of reasons to keep Gas prices supported, from the current geopolitical tensions in the Middle East and Ukraine to the push for green energy and ESG costs adding a premium to Gas prices. Adding to these, unforeseen outages in the US and Norway are also hitting production.

Meanwhile, the US Dollar is trading firmly in the green. The DXY US Dollar Index, which gauges the Greenback against a basket of currencies, rallies towards 104.00. The inflow in the Greenback comes after the Bank of Japan (BoJ) hiked interest rates for the first time in nearly two decades . However, the main takeaway for markets is that it was a one-and-done deal that was very well communicated.

Natural Gas is trading at $1.86 per MMBtu at the time of writing.

Natural Gas news and market movers: A mix of rocket fuel

- Shipments from Australia last week dropped due to severe weather and storms, making it unsafe for big Gas shipments to take place, according to Bloomberg.

- US LNG exports dropped nearly 10% last week, with the Freeport outage as the main driver. This adds to the several unscheduled maintenance in Norwegian Gas fields.

- Ukraine's attacks on Russian infrastructure are creating an issue for Gas flows towards Asia.

- The European Union has committed to asking importers of Russian LNG to reduce purchases this year, according to Energy Commissioner Kadri Simson.

Natural Gas Technical Analysis: Healing from the downside

Natural Gas prices are starting to heal from their steep decline since February. With traders seeing a mixture of elements supporting prices, this makes the rally more healthy and less dependent on just one driver. Look for $2 on the topside, should more supply issues or a surge in demand occur.

On the upside, the key $2.00 level needs to be regained first. The next key level is the historic pivotal point at $2.12, which falls broadly in line with the 55-day Simple Moving Average (SMA) at $2.08. Should Gas prices pop up in that region, a broad area opens up with the first cap at the red descending trend line near $2.27.

On the downside, multi-year lows are still nearby with $1.65 as the first line in the sand. This year’s low at $1.60 needs to be kept an eye on as well. Once a new low for the year is printed, traders should look at $1.53 as the next supportive area.

Natural Gas: Daily Chart

Natural Gas FAQs

Supply and demand dynamics are a key factor influencing Natural Gas prices, and are themselves influenced by global economic growth, industrial activity, population growth, production levels, and inventories. The weather impacts Natural Gas prices because more Gas is used during cold winters and hot summers for heating and cooling. Competition from other energy sources impacts prices as consumers may switch to cheaper sources. Geopolitical events are factors as exemplified by the war in Ukraine. Government policies relating to extraction, transportation, and environmental issues also impact prices.

The main economic release influencing Natural Gas prices is the weekly inventory bulletin from the Energy Information Administration (EIA), a US government agency that produces US gas market data. The EIA Gas bulletin usually comes out on Thursday at 14:30 GMT, a day after the EIA publishes its weekly Oil bulletin. Economic data from large consumers of Natural Gas can impact supply and demand, the largest of which include China, Germany and Japan. Natural Gas is primarily priced and traded in US Dollars, thus economic releases impacting the US Dollar are also factors.

The US Dollar is the world’s reserve currency and most commodities, including Natural Gas are priced and traded on international markets in US Dollars. As such, the value of the US Dollar is a factor in the price of Natural Gas, because if the Dollar strengthens it means less Dollars are required to buy the same volume of Gas (the price falls), and vice versa if USD strengthens.

USD/JPY traded back above 150.00 after the BoJ exited its Negative Interest Rate Policy (NIRP). Economists at TD Securities analyze the pair’s outlook.

BoJ exited NIRP and YCC simultaneously

BoJ exited NIRP and YCC simultaneously and revamped its monetary policy framework around short-term interest rates. The Bank kept its QE program and signalled that it will make nimble responses to any spike in long-run interest rates. Our confidence around an October hike has lessened after Governor Ueda's dovish comments and the recent economic data.

USD/JPY is now hostage to the FOMC decision on Wednesday and any big hawkish surprise from Powell could push USD/JPY beyond its 2022 high at 151.90 which may invoke some strong verbal interventions from the MoF.

The new Canadian inflation figures for February will be released today. Economists at Commerzbank analyze how the Consumer Price Index (CPI) report could impact the Loonie.

Bloomberg consensus is currently subject to considerable uncertainty

Economists surveyed by Bloomberg are looking for a non-seasonally adjusted increase of 0.6% MoM, which should translate into a seasonally adjusted increase of around 0.26%.

If today's figures confirm the ongoing inflationary risks, the market may push back its rate cut expectations a bit. This would certainly be positive for the CAD.

However, it should also be noted that the Bloomberg consensus is currently subject to considerable uncertainty. The number of participants in the survey for Canadian inflation data has fallen significantly in recent years. And even last month, the survey was expecting a solid increase, and in the end, prices actually fell. This is something to keep in mind for today.

- EUR/GBP rebounds to 0.8550 amid uncertainty over the Pound Sterling outlook ahead of the BoE policy meeting.

- The UK inflation data will influence expectations for the BoE to reduce interest rates from August.

- Eurozone ZEW Survey- Economic Sentiment improves sharply to 33.5 in March.

The EUR/GBP pair jumps to 0.8550 in the European session on Tuesday. The asset rises ahead of key United Kingdom economic events this week. The Pound Sterling will be influenced by the Bank of England’s (BoE) interest rate decision, which will be announced on Thursday.

The BoE is widely anticipated to keep interest rates unchanged at 5.25% as inflation is far from the desired rate of 2%. Investors await fresh cues about when the BoE could begin reducing interest rates. Currently, market participants anticipate that the BoE will announce their first rate cut in the August policy meeting after maintaining a hawkish stance for more than two years.

BoE policymakers have been reiterating that rate cuts would be appropriate only if they are convinced that inflation will return sustainably to the desired target of 2%.

Before the BoE policy, investors will focus on the UK Consumer Price Index (CPI) data for February, which will be published on Wednesday. The annual headline inflation is forecast to have grown at a slower pace of 3.6% against 4.0% in January. In the same period, core inflation that excludes volatile food and energy prices is forecast to have decelerated to 4.6% from 5.1%.

Meanwhile, the Euro rises on upbeat Eurozone ZEW Survey—Economic Sentiment. The economic data showcases institutional investors' sentiment towards the economic outlook improving significantly to 33.5 from expectations of 25.4 and the former reading of 25.0.

Going forward, the Euro will be guided by market expectations for the European Central Bank's (ECB) rate cuts. Investors expect the ECB to start reducing interest rates by summer.

- Gold price dips to $2,150 as investors turn cautious ahead of Fed’s interest rate decision.

- The US Dollar advances on hopes that the Fed could delay rate-cut plans.

- 10-year US yields fall moderately but hold strength on lower expectations for the Fed reducing interest rates in June.

Gold price (XAU/USD) drops to $2,150 in Tuesday’s European session as a strong US Dollar weighs heavily on the precious metal. The appeal for Gold remains subdued amid uncertainty ahead of the Federal Reserve’s monetary policy decision and the release of the quarterly dot plot on Wednesday.

The Fed is widely expected to keep interest rates unchanged in the range of 5.25%-5.50% for the fifth time in a row, but uncertainty over rate-cut projections keeps the Gold price on the tenterhooks. Investors are scaling back bets that the Fed could begin reducing interest rates in June, putting further downside pressure on Gold.

Meanwhile, 10-year US Treasury yields have fallen slightly to 4.32% but remain broadly strong on hopes that the first Fed rate cut, which is currently anticipated in June, will be delayed. Higher-than-expected consumer and producer inflation data are casting doubts among investors that this policy pivot will indeed occur in June or will be further postponed.

Daily digest market movers: Gold, bond yields fall while US Dollar rallies

- Gold price falls sharply to the crucial support of $2,150. Investors turn risk-averse towards bullions ahead of the interest rate decision by the Federal Reserve, which will be announced on Wednesday.

- The CME FedWatch tool shows that after the conclusion of the two-day meeting, the Fed will keep interest rates unchanged. Investors are eagerly awaiting the quarterly dot plot, which shows projections for interest rates over time by Chair Jerome Powell and other officials. The dot plot will signal any change in projections for rate cuts this year.

- December’s dot plot indicated that Fed officials are anticipating three rate cuts in 2024. If the Fed dials down rate-cut projections, the Gold price could face significant downside pressure. Currently, the CME FedWatch tool shows a 60% chance that at least three rate cuts will be announced by 2024. The chances for at least three rate cuts were slightly below 80% before the release of the hot consumer and producer inflation data for February.

- In addition to the dot plot, the Fed will also release economic projections for inflation and economic growth. An upbeat economic outlook would strengthen the appeal of the US Dollar. The United States economy has been performing better on the grounds of consumer spending and labor market than any other country in the Group of Seven (G-7) economies.

- The US Dollar Index (DXY), which measures the US Dollar’s value against six rival currencies, rises to 104.00 amid improvement in safe-haven bid.

Technical Analysis: Gold price ranges between $2,145-$2,165

Gold price faces pressure as the upside remains limited amid caution ahead of the Fed’s decision on interest rates. The precious metal trades broadly sideways, ranging between $2,145 and $2,165, and it is likely to break the consolidating trend after the Fed’s policy meeting.

The precious metal may continue its downside towards the 20-day Exponential Moving Average (EMA) at $2,097. After a wide divergence, the asset tends to face a mean-reversion move, which results in a price or a time correction.

On the downside, December 4 high near $2,145 and December 28 high at $2,088 will act as major support levels.

The 14-Relative Strength Index (RSI) retraces from its peak near 84.50, although the upside momentum is still active.

Gold FAQs

Gold has played a key role in human’s history as it has been widely used as a store of value and medium of exchange. Currently, apart from its shine and usage for jewelry, the precious metal is widely seen as a safe-haven asset, meaning that it is considered a good investment during turbulent times. Gold is also widely seen as a hedge against inflation and against depreciating currencies as it doesn’t rely on any specific issuer or government.