- Analytics

- News and Tools

- Market News

CFD Markets News and Forecasts — 17-06-2011

Stocks continue to drift lower. The downward grind has left the three major equity averages to trade at new session lows.

Amid the stock market's weakening, the Volatility Index is climbing so that it is now down 3% for the session. Just yesterday it set a near three-month high.

Treasuries have started to tick higher in response to the recent action among stocks. In turn, the benchmark 10-year Note is at a session high, although it is still down a single tick.

The euro gained versus the dollar by the most in two weeks after German Chancellor Angela Merkel agreed to compromise and work with the European Central Bank on a debt plan for Greece.

Currencies of commodity-exporting countries rose as stocks advanced, boosting appetite for higher-yielding assets. The MSCI World (MXWO) Index of equities added 0.8 percent as Merkel retreated from German demands that bondholders be forced to shoulder a “substantial” share of a Greek rescue, easing concern the region’s sovereign debt problems will worsen.

“The aim is involvement of the private sector on a voluntary basis, and for that the Vienna Initiative, as it’s called, is a good basis,” Merkel said. “I think we can achieve something on this basis.” A rollover involves reinvesting the proceeds from maturing bonds in new securities.

Adopting the Vienna plan, used during the financial crisis of 2009 for eastern European units of banks to maintain their exposure, would involve encouraging creditors to roll over expiring bonds, buying time for Greece until its austerity program shows results or until a permanent rescue fund kicks in from mid-2013.

Greek bonds rallied and European stocks reversed losses as attention shifted to Athens, where Prime Minister George Papandreou overhauled his Cabinet as he struggles to gain parliamentary approval for a 78 billion euro ($111.5 billion) five-year package of budget cuts and asset sales by July.

“The latest events seem to have eased some of the immediate market stresses concerning Greece and the periphery,” said Robert Lynch, head of currency strategy for HSBC Holdings Plc in New York. “Not only did it relieve downward pressure on the euro, but it’s also allowing some semblance of increased risk appetite back into the market.”

The euro-area’s currency fell earlier on concern a potential Greek debt default may spread to other indebted nations in the 17-member bloc. The euro reversed losses after French President Nicolas Sarkozy said a “breakthrough” had been made on the Greek debt crisis, following a meeting with Merkel, who said she’ll work with the European Central Bank to avoid disrupting markets.

The dollar remained lower after a report showed U.S. consumer sentiment was lower than forecast in June, while an index of leading economic indicators rose in May.

The Thomson Reuters/University of Michigan preliminary index of consumer sentiment decreased to 71.8 from 74.3 in May. Economists forecast a reading of 74.

The Conference Board’s gauge of the outlook for the next three to six months rose 0.8 percent after a revised 0.4 percent decline in April, the New York-based group said today. Economists forecast a 0.3 percent gain.

A flurry of selling pressure has undercut stocks. The effort took the Nasdaq down to the neutral line, but it has yet to cross into the red. Meanwhile, both the Dow and S&P 500 have managed to hold on to modest gains.

Treasuries have had a hard time attracting support this session. That has kept the benchmark 10-year Note stuck in the red with a slight loss; its yield, at 2.95%, is at the mid-point of its weekly range.

- Mon pol is still accommodative; real rates are negative;

- Risks to global and EMU recovery not negligible now;

- See higher input prices moving along production chain;

- Not seen 'excessively large' increase in wage demands

- Stakes are very high for greece,euro area and beyond;

- Greek fallout could be of 'broad geographical scope';

- Default may hit fin systems,have impact on recovery;

- Key to restore confidence in EMU as soon as possible;

- ECB won't take part in debt rollover--even if voluntary;

- Hard to assess what results in credit, rating event;

- ECB exercised mandate very flexibly, must draw line;

- Demands to do more an encroachment on ECB independence;

- Effective counter-measures can be taken only by govts;

- Need reliable backstop; larger EFSF is one option;

- Greek cbank may give ELA to banks even if default

Choppy action has eaten into the broad market's gain. Still, stocks are up a few points for the week. That's something that hasn't happened since April.

The Nasdaq is having a harder time holding on to its gain, however. Sellers have sent the tech-rich index to a session low, where it has been left to cling to a fractional gain. For the week, though, the Nasdaq is still down about 17 points, or less than 1%.

CRT says the softer Jun Michigan confidence reading also had "more benign near-term inflation expectations" as 1y infl expectations slipped 0.1pt to 4.0%. May LEI "came in higher than

forecast at +0.8%... Interest rate spread was the largest contributor at +0.32% and consumer expectations at +0.23%.

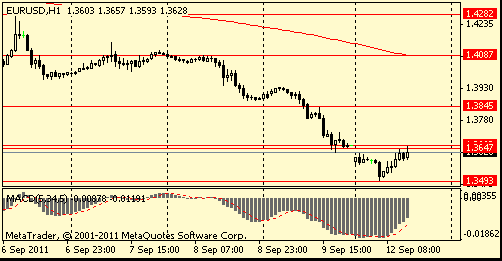

EUR/USD $1.4000, $1.4025, $1.4100, $1.4140, $1.4300

USD/JPY Y80.00, Y81.00, Y82.00

EUR/JPY Y115.00, Y115.40, Y117.00

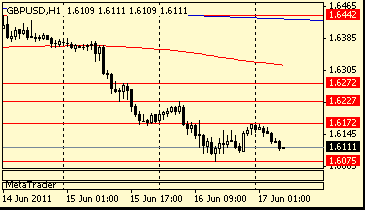

GBP/USD $1.6000, $1.6100, $1.6310

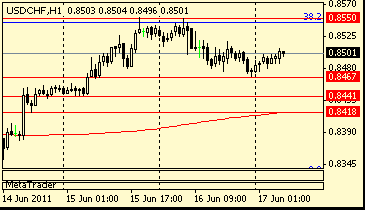

USD/CHF Chf0.8450, Chf0.8500

EUR/CHF Chf1.2100

AUD/USD $1.0450, $1.0500, $1.0625

U.S. stocks futures point for an early rebound Friday, as oil prices slipped and investors awaited another economic data.

Oil prices, which sank 2% in earlier trading, may also give markets a boost Friday.

U.S. stocks closed mixed on Thursday, as weakness in the tech sector countered stronger-than-expected reports on the housing market and unemployment.

Economy: After the market open, the University of Michigan will release its initial June consumer sentiment index at 13:55 GMT. Economists are looking for the index to fall to a reading of 73.5, from May's reading of 74.3.

The Conference Board will release its report on Leading Economic Indicators for May at 14:00 GMT. Economists forecast a decline of 0.4%, following a 0.3% drop in the previous month.

Companies: Shares of Research in Motion (RIMM) tumbled 18% in premarket trading, after the BlackBerry-maker slashed its full-year earnings outlook by 30% and announced layoff plans after the market closed Thursday.

Capital One (COF, Fortune 500) plans to acquire ING Direct. But after the announcement, Moody's warned of a possible downgrade and said it is reviewing Capital One's financial strength and long-term ratings. Shares of the bank fell more than 1% before the market open.

EUR/CHF holds at Chf1.2108 with option for today's NY cut at Chf1.2100. USD/CHF has expiries at Chf0.8450 and Chf0.8500. Rate currently trades around Chf0.8480.

EUR/USD challenged $1.4295/00 before position adjustmen brought the rate down to current $1.4256. Earlier rate was lifted amid speculation the Eurogroup to reach a responsible deal for Greece on Sunday.

Data released:

09:00 EU(17) Trade balance (April) unadjusted, bln -4.1 -2.1 2.8

09:00 EU(17) Trade balance (April) adjusted, bln -2.9 - -2.2 (0.9)

The euro gained for a second day following a meeting of French President Nicolas Sarkozy with German Chancellor Angela Merkel, when Sarkozy said a “breakthrough” had been made on the Greek debt crisis.

Sarkozy told that a solution involving holders of Greek bonds in a new rescue package for the indebted nation has been found. The chancellor said Germany would work with the ECB on the compromise deal.

The euro-area currency fell earlier today on concern a Greek debt default could spread to other indebted nations in the bloc.

EUR/USD rose from $1.4120 to a new session high on $1.4300. Later rate retreated to $1.4277.

GBP/USD increased from $1.6090 to $1.6185 before corrected to $1.6168.

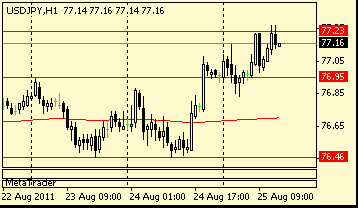

USD/JPY fell to session lows around Y80.20, then recovered to Y80.36.

US data starts at 1355GMT, when the Michigan Sentiment Index is expected to rise to a reading of 74.5 in early-June after rising sharply to 74.3 in May.

EUR/GBP continues продолжает свой рост и сейчас кросс пишет новые сессионные максимумы на stg0.8831 на фоне возобновившегося роста евровалюты. Рост кросса ускорился после преодоления stg0.8800. Ближайшее сопротивление - на stg0.8840 (максимумы 14 июня).

EUR/JPY retreats following the euro weakness. Cross trades at Y114.56 after printed session high on Y114.77. Bids were mentioned at Y114.25/40, stronger - ahead of Y114.00. Further support comes at earlier lows on Y113.70.

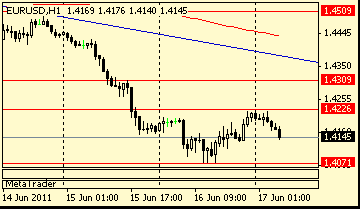

EUR/USD retreats and currently holds under $1.4280. Earlier rate tested resistance/offers between $1.4285/90. Stronge offers come at $1.4300. Initial support is near hourly lows on $1.4210/20.

In Europe euro recovered from 3-week lows amid unconfirmed rumors that a new Greek aid package of E150bln could be agreed. Market talks a new aid includes E80bln of a new money, E40-50bn from privatizations, E30-40bn from rollover of Greek bonds.

But the euro remains under pressure relative to the yen.

But earlier rate fell on concerns how policy makers will tackle Greece's debt crisis with no apparent solution in sight.

Germany's Merkel said today there won't be a decision on Greek aid till September, but she is very optimistic about the Greek problems solution. Also she mentioned that Germany and France will do everything for saving euro.

ECB's Nowotny said there is a need to make Greece decision faster as Greece situation makes economy uncertain.

Friday’s session is likely to be dominated by any further news from talks regarding Greece and also any developments out of Athens on the political manoeuvring.

- supports Greek PM;

- till September there won't be a decision on Greek aid;

- very optimistic about the Greek problems solution.

- Greece situation makes economy uncertain;

- Germany GDP may come at +2.5% in 2012 and +3.4% in 2011;

- Global economy normalizing.

- E80bln new money

- E40-50bln from privatizations

- E30-40bln from Greek bonds

EUR/USD continues to hold higher, printing session high on $1.4244. Rate earlier broke key resistance at $1.4240, but failed to set above. Next resistance seen between $1.4250/60 ahead of stronger area between $1.4280/85.

E80bln new money

E40-50bln from privatizations

E30-40bln from rollover of Greek bonds

EUR/USD $1.4000, $1.4025, $1.4100, $1.4140, $1.4300

USD/JPY Y80.00, Y81.00, Y82.00

EUR/JPY Y115.00, Y115.40, Y117.00

GBP/USD $1.6000, $1.6100, $1.6310

USD/CHF Chf0.8450, Chf0.8500

EUR/CHF Chf1.2100

AUD/USD $1.0450, $1.0500, $1.0625

It is a quiet end to the week - in terms of the European data calendar at least. European data starts at 0600GMT with ACEA May new car registrations, although of more interest will be EMU trade data for April, which isreleased at 0900GMT at the same time as EMU construction output, also for April. At 1300GMT, the International Monetary Fund releases it's quarterly update of the World Economic Outlook.

Resistance 3: Chf0.8680 (61.8 % FIBO Chf0.8890-Chf0.8330)

Resistance 3: $ 1.6270 (high of american session on Jun 15)

Resistance 3: $ 1.4370 (resistance line from Jun 9)

09:00 EU(17) Trade balance (April) unadjusted, bln -2.1 2.8

© 2000-2026. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers