- Analytics

- News and Tools

- Market News

CFD Markets News and Forecasts — 14-07-2011

At its session high, the Dow was up about 90 points.

JPMorgan Chase (JPM 40.72, +1.10) has supported for the Dow today. Its upside earnings surprise has put the stock at a weekly high, but it has struggled to get other blue chips and financial plays to follow it higher. For instance, Bank of America (BAC 10.16, -0.03) has spent the entire afternoon in the red.

Today the U.S. dollar significantly dropped as late Wednesday Moody's and Chinese ratings agency Dagong both put the US AAA credit rating on negative watch.

“The fear of the U.S. downgrade has led to a swift move to the safe haven currency,” said Sebastien Galy, a foreign-exchange analyst at Societe Generale in London.

Euro strengthened versus US dollar amid the weakness of the latter. Despite Greece's credit rating was cut three levels by Fitch Ratings from B+ to CCC, any downgrade in the eurozone has increasingly less impact than debt problems in the US.

It should be noted that yesterday Federal Reserve chairman Ben Bernanke, raised the possibility of a third bout of quantitative easing – or “QE3”, that the central bank is ready to provide additional economic stimulus if needed.

Japan’s currency, shedding in the beginning of the session against dollar amid speculation the nation will intervene in markets to limit its gains, retreated but declining again.

The Swiss franc reached to record highs against the dollar, euro and the pound amid concerns about credit ratings of U.S and Greece. Today Fitch Ratings has affirmed Switzerland's ratings at 'AAA'. Its outlook remains stable.

New Zealand’s dollar strengthened to a record after a government report showed the economy grew faster than expected. The New Zealand economy has released today its house price index for the month of June which increased 1.3%, compared with a previous drop by 1.8% in May. This fact signaled the nation is recovering from a deadly earthquake in February.

Despite yesterday the yellow metal rallied to a new high around $1,600 per troy ounce and silver approached $40 per troy ounce and today continued theirs rally on fiscal and economic problems in the US, currently the precious metals are slightly above yesterday’s closing price.

Oil weakens after Wednesday's gains with Aug crude down $2.20 at $95.84 and in the lower reaches of the day's $95.76/98.88 range.

USD/CAD holds around C$0.9588, recovered from lows around C$0.9550 area. Offers likely in place ahead of the overnight high at C$0.9610 to slow gains from here.

- need to define housing finances for future;

- Fannie/Freddie own about half of a million of empty homes;

- housing is an "epicenter" of economic problems;

- default could potentially throw finaces into chaos;

- danger to create even the possibility of default;

- 1H weakness comes from temporary factors;

- recovery is slow due to housing;

- unemployment also a drag;

- EU problems do affect US and trade;

- don'y expect bif direct impacts of any Europe default;

- but indirect effects of Europe default could be big;

- can only conclude default is "very bad for jobs";

- US fiscal problems not the same with EU.

- don'y expect bif direct impacts of any Europe default;

- but indirect effects of Europe default could be big;

- can only conclude default is "very bad for jobs";

- US fiscal problems not the same with EU.

- need to define housing finances for future;

- Fannie/Freddie own about half of a million of empty homes;

- housing is an "epicenter" of economic problems;

- default could potentially throw finaces into chaos;

- danger to create even the possibility of default;

- 1H weakness comes from temporary factors;

- recovery is slow due to housing;

- unemployment also a drag.

Nomura says downward trend in unemploy claims "evident in the decline in the 4-week average -- suggests the job market is relatively stable if not improving a bit after weakening markedly in May and June."

Early trade is rather choppy, but the major equity averages have managed to remain in positive territory with modest gains.

Energy is an early leader. The sector has sprinted ahead to a 1.2% gain as ConocoPhillips (COP 9.70, +5.30) shares spike more than 7% in response to news that the company will split itself into two publicly traded entities, one which will focus on refining and marketing, the other will take over exploration and production operations.

In the backdrop, oil prices are up 0.6% to $98.70 per barrel.

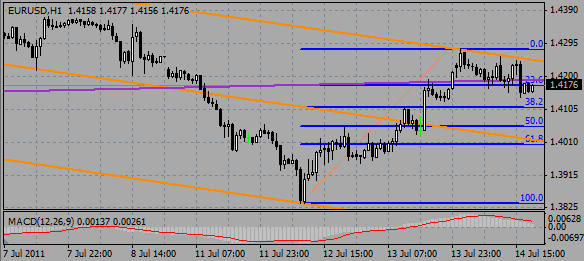

EUR/USD $1.4200, $1.4250, $1.4270, $1.4285/90

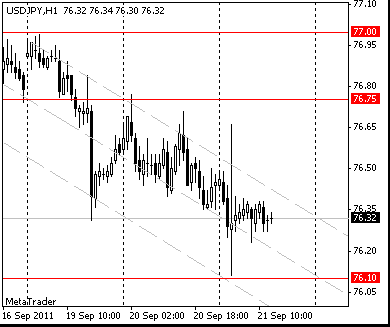

USD/JPY Y79.00, Y79.50

EUR/JPY Y111.00, Y114.30

GBP/USD $1.6150

AUD/USD $1.0750, $1.0800

AUD/CAD C$1.0300, C$1.0325

U.S. stocks were headed for slight gains at Thursday's open, despite a warning from Moody's of a possible downgrade to U.S. debt that is sure to weigh on markets.

A strong earnings report from JPMorgan Chase (JPM, Fortune 500), the first of the big banks to report, and better-than-expected economic data were lending some support.

U.S. stocks snapped a three-session losing streak Wednesday, after Federal Reserve chairman Ben Bernanke reiterated that the central bank remains ready to provide additional stimulus.

After the bell Wednesday, Moody's Investors Services said it would put the sterling bond rating of the United States on review for possible downgrade.

Moody's initiated the review, because of the "rising possibility" that Congress will fail to raise the debt ceiling in time -- something that could lead to a U.S. default on its debt.

Economy: The Labor Department said jobless claims fell 22,000 to 405,000. Economists were expecting weekly claims to decrease to 410,000 claims. It was the 14th straight week filings came in above the key level of 400,000.

The June producer price index, a reading of wholesale inflation, fell 0.4% in June, after rising 0.2% the prior month. Economists were expecting the measure to have fallen 0.2%.

The Commerce Department said June retail sales rose 0.1%. Sales were expected to have fallen 0.2% last month.

Bernanke's testimony to Congress will continue Thursday, with the Fed chairman appearing before the Senate's Committee on Banking, Housing and Urban Affairs.

Companies: Conoco Phillips (COP, Fortune 500) said that it is splitting its operations into two distinct publicly traded corporations, sending its stock up 7%.

In a tax-free spin to shareholders, ConocoPhillips will separate its oil refining and marketing business from its exploration and production operations.

JPMorgan Chase (JPM, Fortune 500) reported quarterly income of $5.4 billion, or $1.27 a share, on revenue of $27.4 billion. Both figures topped estimates. But the bank also said that it sees additional costs for resolving mortgage issues. Shares of JPMorgan edged up 1%.

Shares of Yum! Brands (YUM, Fortune 500) were almost 3% higher in premarket trading after the fast food operator posted better-than-expected earnings after the market close on Wednesday.

A day after a poor preliminary results report for the second quarter, shares of Hartford Financial Services Group (HIG, Fortune 500) fell almost 4% before the market open.

After the bell, Google (GOOG, Fortune 500) will report its quarterly results. Analysts expect that Google earned $7.86 a share.

World markets:

Oil for August delivery gained 20 cents to $98.25 a barrel.

Gold futures for August delivery rose $5.70 to $1591.20. Earlier in the trading session, gold set a new intraday record of $1,594.00 an ounce.

Bonds: The price on the benchmark 10-year U.S. Treasury dropped, pushing the yield up to 2.91% from 2.89% late Wednesday.

Cable reached $1.6150, a break to open a move toward $1.6170/80 ahead of earlier highs at $1.6195, with offers noted between $1.6195/00.

US data calendar, including jobless claims, retail sales and PPI, which are all due at 1230GMT.

At 1400GMT, Federal Reserve Chairman Ben Bernanke delivers the semi-annual monetary policy report to the Senate Banking Committee. At the same time, May business inventories are expected to increase 0.9% in May, reflecting the already announced 0.8% increase in factory inventories and the 1.8% increase in wholesale inventories. The weekly EIA Natural Gas Stocks data follows at 1430GMT

EUR/USD $1.4000, $1.4015, $1.4200, $1.4270, $1.4285-90,

USD/JPY Y79.50, Y79.75, Y80.00, Y80.20, Y81.00

EUR/JPY Y111.00, Y114.30, Y115.75

GBP/USD$1.6000, $1.6150, $1.6240

AUD/USD $1.0600, $1.0640, $1.0650, $1.0750, $1.0800, $1.0850, $1.0930, $1.0950

AUD/CAD C$1.0300, C$1.0325

NZD/USD $0.8225

The dollar held yesterday’s loss against the euro after Moody’s Investors Service put the U.S. under review for a credit rating downgrade, damping demand for the nation’s currency.

US data calendar, including jobless claims, retail sales and PPI, which are all due at 1230GMT.

At 1400GMT, Federal Reserve Chairman Ben Bernanke delivers the semi-annual monetary policy report to the Senate Banking Committee. At the same time, May business inventories are expected to increase 0.9% in May, reflecting the already announced 0.8% increase in factory inventories and the 1.8% increase in wholesale inventories. The weekly EIA Natural Gas Stocks data follows at 1430GMT

Nikkei 9,936 -27.02 -0.27%

Hang Seng 21,918 -8.57 -0.04%

S&P/ASX 4,491 -24.07 -0.53%

Shanghai Composite 2,810 +14.97 +0.54%

The dollar weakened against all major currencies after Federal Reserve Chairman Ben Bernanke reiterated that the central bank is ready to provide additional economic stimulus if needed and investor demand for higher-yielding assets increased.

Earlier the Australian and New Zealand dollars advanced against the greenback after better-than-expected economic data on China. The GDP growth of China, Australia's first largest and New Zealand's second-largest trading partner, rose at an annual pace by 9.5% between April and June, down from 9.7% in the previous quarter. But its data on industrial production (act. 15.1% vs. con.13.2% and prev. 13.3%) and retail sales (act. 17.7% vs. con.17.0% and prev. 16.39) appeared to be well above median forecasts.

The euro also found support from positive data from China’s National Bureau of Statistics as it weighed on haven demand for the dollar and on speculation that China’s foreign exchange reserves had reached a record $3,179bn.

Italian bonds gains for the second day, pushing the yield on the 10-year security down 12 basis points, weakening concern that EU debt crisis may spread to Italy.

US data calendar, including jobless claims, retail sales and PPI, which are all due at 1230GMT.

At 1400GMT, Federal Reserve Chairman Ben Bernanke delivers the semi-annual monetary policy report to the Senate Banking Committee. At the same time, May business inventories are expected to increase 0.9% in May, reflecting the already announced 0.8% increase in factory inventories and the 1.8% increase in wholesale inventories. The weekly EIA Natural Gas Stocks data follows at 1430GMT

Resistance 3: $ 1.6370 (61.8 % FIBO $1.6750-$ 1.5780)

Resistance 3: $ 1.4470 (Jul 6 high)

© 2000-2026. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers