- Analytics

- News and Tools

- Market News

CFD Markets News and Forecasts — 13-04-2011

Stocks are resting only modestly above their session lows. Outside of equities, the Dollar Index is near its session high, although its gain currently stands at less than 0.2%.

- many Districts described the improvements as only moderate

- KC described its economic gains as solid

- mfg continued to lead

- retailers in Boston reported mixed sales results

- retail sales remained weak in Richmond

- all other Districts experienced at least slight gains in consumer spending

- many Districts described the improvements as only moderate

- KC described its economic gains as solid

- mfg continued to lead

- retailers in Boston reported mixed sales results

- retail sales remained weak in Richmond

- all other Districts experienced at least slight gains in consumer spending

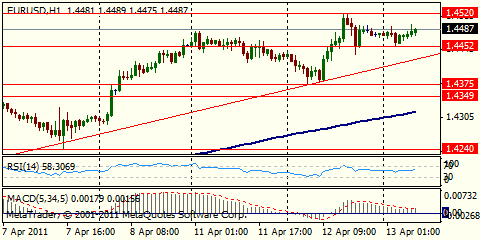

EUR/USD holds under pressure around $1.4435 area as earlier noted bids at $1.4445/60 are filled, then stop interest at $1.4440. Area of $1.4420/25 said to hold demand.

Stocks opened today's trade with solid gains, but the tone of trade has since deteriorated.

Strong gains abroad and a pleasing quarterly report from banking bellwether JPMorgan Chase (JPM 46.29, -0.35) helped stocks push higher in early trade. However, shares of banks have buckled under pressure from sellers. Weakness among bank stocks has taken the financial sector down to a 0.8% loss.

Part of this session's change in sentiment stems from the failure of the S&P 500 to extend its opening gains through near-term resistance in the 1321-1322 zone.

As a reminder, the Fed's Beige Book will be released at 18:00 GMT.

The euro edged to a 15-month high against the dollar.

The euro was lifted by reported demand from sovereign names looking to recycle dollar proceeds as the single currency remained supported by the prospect of further rate rises in the euro zone while policy stays loose in the United States and Japan.

"The European Central Bank's increase of interest rates last week should not be considered as an isolated decision and the ECB president has signalled that it was not a one-off," ECB Governing Council member Luc Coene said on Wednesday.

Commodity-linked currencies such as the Australian and New Zealand dollars also rose, buoyed by a recovery in commodity prices and stocks.

An Australian sentiment index rose 1.2 percent to 105.3 this month from March, according to a Westpac Banking Corp. and Melbourne Institute survey released today. House prices in New Zealand increased 0.5 percent in March, an index published by the Real Estate Institute of New Zealand Inc. showed.

Stocks have extended their recent retreat. The downturn has actually taken the Dow and S&P 500 into negative territory. Although the Nasdaq isn't quite there yet, it is at a session low.

Financials have been a drag on trade today. The sector had attempted to stage an impressive rally yesterday, but broad market weakness undercut the sector that is down 0.4%.

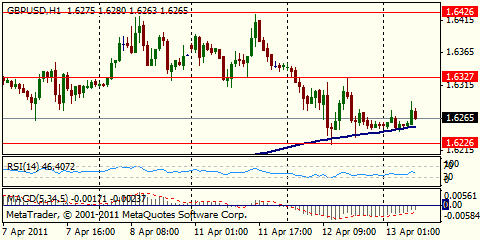

GBP/USD holds around $1.6288. Traders mention stops below $1.6230 ahead of earlier mentioned stops intereast below $1.6210 and $1.6180. Rate earlier fell to hourly lows around $1.6240.

Both the Dow and the S&P 500 have slipped from their opening levels, but the Nasdaq is trying to hold firm near the top end of its early morning trading range. Tech stocks, collectively up 0.7%, are helping to support the Nasdaq.

Although they are usually considered one of the more stodgy sectors, utilities are outperforming this morning. The sector has already run ahead to a 0.9% gain. Duke Energy (DUK 18.19, +0.20) and American Electric (AEP 34.98, +0.39) are primary leaders in the utilities space.

- Must prevent rise of EMU inflation expectations;

- ECB evaluating timing, mode of exit from accommodation;

- Global monetary policies must consider infl. pressures;

- Whole world now has need to end fiscal, monetary support;

- Recovery has not cancelled crisis impact,ended weakness;

- Divergence in growth worldwide can cause fx volatility;

- EMU states must have fiscal rules consistent w/eu rules

U.S. stocks were poised for gains Wednesday after JPMorgan Chase reported solid earnings, but cautioned that mortgage losses would continue.

U.S. stocks finished lower Tuesday, with all three major indexes losing about 1%, as a 3% drop in oil prices sparked a sell-off in energy stocks, and Alcoa's sales disappointment weighed down the Dow.

The first major bank to report quarterly results, JPMorgan Chase (JPM) announced a 70% jump in first-quarter net income to $5.6 billion, or $1.28 per share, beating analysts' forecasts for $1.16 per share.

Revenue slipped to $25.8 billion from a year earlier but still edged above analysts' predictions.

Additionally, bankers from the investment banking giant are in line for a 34% raise this year. JPMorgan Chase shares rose 1.5% following the report.

Economy: Census Bureau reported retail sales rose 0.4% in March. The number was slightly lower than the 0.5% increase economists expected, due to rising gas prices. Stripping out gas, retail sales were only up 0.1% for the month.

The latest business inventory numbers will be released at 14:00 GMT from the Census Bureau. Companies are expected to have boosted their inventories by 0.8% in February.

In the afternoon, the Federal Reserve will release its Beige Book.

Companies: Shares of Tyco International (TYC) fell more than 1.8% in premarket trading, after French company Schneider Electric denied reports that it is trying to buy the Swiss manufacturing conglomerate for $30 billion.

World markets:

Oil for May delivery gained 41 cents to $106.66 a barrel.

Gold futures for June delivery rose $7.60 to $1,461.20 an ounce.

The price on the benchmark 10-year U.S. Treasury fell, pushing the yield up to 3.53% from 3.50% late Tuesday.

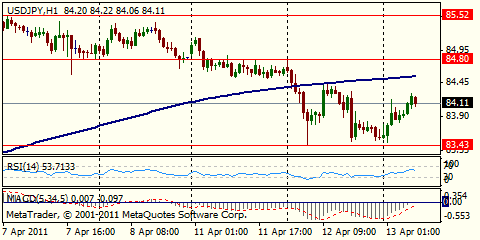

EUR/JPY

Offers: Y122.17/20, Y122.25, Y122.75, Y123.10, Y124.00

Bids: Y121.60/50, Y120.80, Y120.55, Y120.00

The yen was the worst performer among the 17 most-traded currencies as European stocks rebounded and data showed the euro-region economy is improving, boosting demand for higher-yielding assets.

Euro-area industrial output rose for a fifth month in February, stoking bets that the European Central Bank will tighten policy further after last week’s interest-rate increase.

Production in the euro area rose 0.4% in February, European Union statistics showed today.

Commerce Department figures scheduled for release today at 12:30 GMT are expected to show U.S. retail sales gained 0.5% in March.

“The market’s view that the global economy remains on a recovery track is unlikely to push stocks and commodity prices down much further,” said Daisaku Ueno, president of Gaitame.com Research Institute Ltd. in Tokyo, a unit of Japan’s largest currency margin company. “That may reduce demand for the yen as a refuge.”

New Zealand’s dollar rose to best performer against the dollar after the Real Estate Institute said its index of house prices increased for a second month in March. Australian dollar rallied from near a one-week low versus the yen after an industry report showed consumer confidence improved in April.

The pound touched the lowest in almost six months against the euro as a report showed U.K. jobless claims unexpectedly increased in March even as unemployment declined.

Sterling erased earlier gains versus the dollar. Jobless benefit claims rose by 700 from February to 1.451 million, the Office for National Statistics said today in London. That compared with the median forecast of a drop of 3,000. Unemployment fell to 7.8% from 8%.

EUR/USD

Offers: $1.4530/35, $1.4550, $1.4580

Bids: $1.4480, $1.4455/45, $1.4425/20, $1.4400

USD/JPY

Offers: Y84.55/60, Y84.85/90

Bids: Y83.50, Y83.45/40, Y83.25/20, Y82.75/70

The street expects EPS of $1.154 on revenue of $25.3 billion. Analysts note that JPMorgan has topped the consensus view by 12% in each of the past two quarters, and has come above consensus for the past 8 quarters.

EUR/USD $1.4500 (large), $1.4450, $1.4400, $1.4300

USD/JPY Y85.00, Y84.50, Y84.00, Y83.90, Y83.75, Y83.50, Y83.20

EUR/JPY Y120.00

GBP/USD $1.6260, $1.6150, $1.6100

AUD/USD $1.0425

USD/CAD C$0.9550

- Will eliminate monetary factors fueling inflation;

- Says won't relax controls on housing market;

- Overall price stability the top priority;

- Reiterates yuan FX reform goals.

- Inflation spread to advanced from emerging economies;

- Overall price stability 'most urgent task';

- Domestic demand playing bigger role in economy;

- To control price increase in acceptable range.

EUR/JPY Y120.00

GBP/USD $1.6150, $1.6100

AUD/USD $1.0425

The IMF lowered its 2011 forecast for Japanese growth to 1.4 percent from 1.6 percent in its World Economic Outlook report yesterday, citing effects from the disaster.

Canada’s dollar slid versus the U.S. dollar after the Bank of Canada held its target rate for overnight loans between commercial banks at 1 percent, where it has been since September.

The pound slumped to its weakest against the euro in almost six months as the U.K.’s inflation unexpectedly slowed in March, discouraging the Bank of England from raising interest rates.

Consumer prices rose 4 percent from a year earlier, down from a 4.4 percent pace in February.

The U.S. trade deficit narrowed in February from a seven-month high as demand for imports decreased for the first time in four months.

The gap shrank to $45.8 billion from $47 billion in January, Commerce Department figures showed today in Washington.

EMU data continues at 0900GMT with the release of EMU industrial output data for February.

© 2000-2026. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers