- Analytics

- News and Tools

- Market News

CFD Markets News and Forecasts — 11-07-2011

"Already Moody's put Italy's AA2 rating on review for downgrade. S&P recently put Italy's A+ rating on negative outlook, which in light of its deteriorating score was not a surprise. Moody's Aa2 rating is most out of line, and we believe several cuts there are justified. Fitch's AA- rating is also too high and may also reexamine Italy in the coming weeks."

The euro tumbled to a seven-week low against the dollar and slid versus the yen as rising Italian bond yields stoked concern Europe’s sovereign-debt crisis in deepening.

- will not consider temp budget/debt limit, we do not manage our affairs in 3m increments.

- said he agreed spending cuts in defense, healthcare; econ as a whole will benefit.

- will meet every day until debt ceiling deal is reached, unacceptable to not hike debt ceiling.

Models and algos said to be ongoing sellers of euro-dollar, and cable for that matter, euro pressing to marginal fresh lows for the day as residual demand interest is erased. Bids ahead of $1.4000, stops in place below and order books described as very thin. Euro last around $1.4015.

The Nasdaq is quickly cutting its opening loss. The move comes amid help from tech stocks, which have managed to work their way higher so that the overall tech sector is now down 0.7% after it had been down by about 1% at the open.

Among tech stocks, Google (GOOG 533.71, +1.72) is a leader. Its strength comes after it suffered an outsized loss last Friday in response to an analyst downgrade. Meanwhile, Apple (AAPL 358.63, -1.08) has made a charge toward the neutral line, but remains in the red with only a narrow loss.

Stocks are down sharply in the opening minutes of the session. Weakness is widespread, but materials stocks, energy stocks, and financial stocks are in the worst shape; their losses currently range from 1.5% to 1.7%. Only tech, consumer discretionary, and consumer staples have managed to limit their losses to less than 1%.

Amid such sharp selling pressure, Treasuries have attracted plenty of safety seekers. In turn, the yield on the benchmark 10-year Note is back below 3.0% to trade near its one-week low.

U.S. stocks were headed for an early sell-off Monday, as investors fret over weak domestic economic data and Europe's debt crisis, while bracing for second-quarter corporate results.

The three major indexes posted modest gains last week. Positive reports on initial claims and hiring initially boosted optimism about the labor market. But when the government's June jobs data came in far worse than expected, stocks ended Friday's session with a thud.

The U.S. economy created only 18,000 jobs last month -- a fraction of the 120,000 new jobs that a CNNMoney survey of 27 economists had forecast.

Investors will be keeping a close watch on the eurozone debt crisis, and especially Italy, the region's latest problem child.

In Washington, lawmakers will resume talks to raise the debt ceiling, and President Obama is scheduled to hold a news conference on the issue Monday

Companies: Dow component Alcoa (AA, Fortune 500) will be the first major company to release quarterly results, due out after the closing bell Monday. Analysts polled by Thomson Reuters expect the aluminum maker to post earnings per share of 32 cents on revenue of $6.31 billion.

World markets:

Gold futures for August delivery rose $2.60 to $1,544.10 an ounce.

Bonds: The price on the benchmark 10-year U.S. Treasury fell, pushing the yield down to 3.02% from 3.15% late Friday.

The euro tumbled to a more than three-week low against the dollar and slid versus the yen as rising Italian bond yields stoked concern Europe’s sovereign- debt crisis in deepening.

The euro fell to a record low against the Swiss franc as Austria’s Finance Minister Maria Fekter said Italy will be discussed at today’s monthly gathering of euro-area finance ministers. Australia’s dollar weakened on speculation China will take further steps to cool growth, while Norway’s krone fell after inflation in June was less than economists estimated.

“It’s really a story of independent euro weakness,” said Adam Cole, head of global currency strategy at Royal Bank of Canada in London. “We are seeing contagion spreading to Italy. The bailout facility as it stands would be nowhere near big enough to deal with Italy.”

The euro has fallen in four of the past five days after Moody’s Investors Service downgraded Portugal to below investment grade, reigniting concern the region’s debt crisis will spread beyond Greece as officials remain divided over a solution to the crisis.

The yield on Italy’s 10-year bond rose as much as 19 basis points today to 5.47 percent, driving the premium over German bunds to a euro-lifetime record of 268 basis points. The difference in yield, or spread, between Spanish and German 10- year securities also reached the highest in the euro era, widening to 308 basis points.

A European bailout fund may have to be doubled to 1.5 trillion euros to cover a crisis in Italy, according to the European Central Bank, German newspaper Die Welt reported, citing unidentified “high-ranking” people at central banks. The Financial Times cited unidentified senior officials as saying European leaders are prepared to accept that Greece should default on some of its bonds as part of a new bailout plan for the country that would put its total debt levels on a sustainable footing.

European government calls for banks to share in bailing out Greece are a “credit negative” for nations unable to access market funding, Moody’s Investors Service said today.

Continued weakness in the euro as the rate hits the key level of Y113.50/40 a break here opensY112.80. Resistance reverts to Y113.95/00.

- Confident Italy to decide on budget consolidation;

- Need new Greek aid program quickly;

- Euro is stable; some countries have debt problem

Extends lows to $1.4110, with recovery efforts remaining very shallow. Strong demand seen into $1.4100. A break below the figure to expose next strong support between $1.4070. Resistance now seen at $1.4135.

- Slowdown seen in Canada, France, Germany, Italy, UK, Brazil, China, India;

- Tenative signs of turning point in growth cycle in US, Japan, Russia;

- OECD leading indicator down 0.3 point in May;Growth rate -0.2% m/m

- Italy not topic at EU-ECB meeting today;

- Need to agree swiftly on new Greece aid package;

- Greece is main topic at EU-ECB meeting

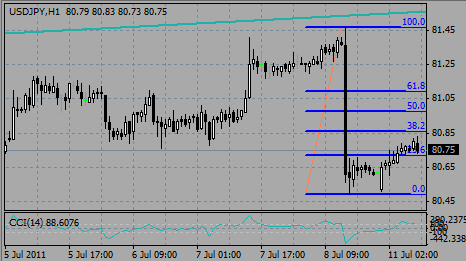

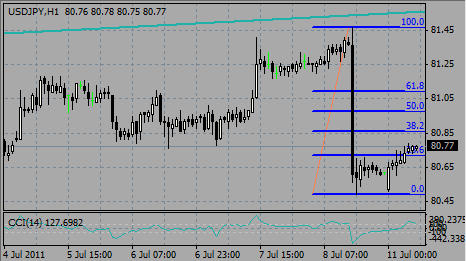

USD/JPY is contained in a tight Y80.72-83 range. On the topside offers at Y80.80/90 (Y80.87 - 08 Jul high). On the downside bids at Y80.60/55, larger at Y80.50/40 and Y80.30/25.

AUD/USD holds around $1.0700 where large Australian Corporates are noted on the bid. Demand remains at $1.0680, stops through $1.0650 and corporate bids noted at $1.0635/30. Offers at $1.0760/65 and $1.0790/00 ahead of stops through $1.0820.

EUR/USD remains under pressure, holding around session lows on $1.4134. Options at $1.4125 may attract some buyers. Stops on a break below $1.4125/20 with stronger demand seen placed toward $1.4100 ($1.4102 Jun 28 low).

EUR/USD: $1.4000, $1.4050, $1.4125, $1.4300

USD/JPY: Y80.00, Y80.50, Y81.00, Y81.25, Y81.50, Y82.00

EUR/JPY: Y115.00, Y113.00

GBP/USD: $1.6020

EUR/GBP: stg0.8720

USD/CHF: Chf0.8400

AUD/USD: $1.0550, $1.0770, $1.0800

01:30 Australia Home Loans (May) 4.4% 4.5% 4.6%

05:00 Japan Consumer Confidence Index (Jun) 35.3 35.5 34.2

The euro fell to a two-week low against the dollar and yen on concern that Europe’s sovereign- debt crisis may spread to Italy as policy makers remain divided on how to structure aid for Greece.

The euro dropped against most major peers after Die Welt reported that the European Central Bank is seeking to expand a fund to include help for Italy, following a coordinated rescue for Greece by the European Union and International Monetary Fund.

A bailout fund may have to be doubled to 1.5 trillion euros ($2.13 trillion) to cover a crisis in Italy, the ECB said, according to the German newspaper Die Welt. The Financial Times cited unidentified senior officials as saying European leaders are prepared to accept that Greece should default on some of its bonds.

“Italy is a very large economy, and if indeed we do see contagion spread toward Italy, then the ECB, EU and IMF will need to come up with a totally different plan to deal with it,” said Khoon Goh at ANZ National Bank Ltd.. “Ongoing concerns are proving to be a real drag on the euro.”

Alcoa Inc., the largest aluminum producer in America, will become the first company on the Dow Jones Industrial Average to report second-quarter earnings today. Corporate profits are forecast to have grown by 13% in the period, according to analyst estimates.

The Australian dollar fell for a second day against the greenback on speculation China, its largest trading partner, will increase efforts to tame inflation even as growth cools.

China’s consumer price index increased 6.4% in June from a year earlier, the National Bureau of Statistics said on July 9, exceeding the 6.2% median estimate. The government will say on July 13 that gross domestic product rose 9.3% in the second quarter from a year before, according to a separate survey, down from 9.7% the previous quarter.

EUR/USD held within the $1.4190/$1.4230 range before weakening to session lows around $1.4130.

GBP/USD still corrects after Friday's gains. rate retreated from session highs on $1.6040 to $1.5940.

USD/JPY rose strongly from Y80.50 to Y80.80.

There is no major data for today.

The U.S. trade deficit widened in May to $44.1 billion from a revised $43.7 billion gap in the prior month, according to the median before tomorrow’s Commerce Department data.

The Federal Open Market Committee is scheduled to release tomorrow the minutes from its June 21-22 meeting.

Both August WTI and Brent contracts easing back again this morning. WTI is now down over $1 to $95.00 after opening highs around $96.30 and Brent is closing in on Frday's lows of $116.88 with a fall to $116.94 from opening highs of around $117.88.

Gold edge higher again to $1547.10 in Asia today, but Silver has eased off from open highs around $36.81 to $36.52. Gold resistance is noted towards $1558.25 with support rising to $1524.80. Silver resistance is at $37.64 with support moving up to $36.00 .

EUR/USD

Offers: $1.4220б, $1.4250/60

Bids: $1.4150

USD/JPY

Offers: Y80.80, Y81.00

Bids: Y80.50, Y80.00

GBP/USD

Offers: $1.6010, $1.6025, $1.6040/50

Bids: $1.5987, $1.5940/30

AUD/USD

Offers: $1.0760, $1.0800

Bids: $1.0680

Mounting optimism about the outlook for Japan’s economy helped shares in Tokyo return to levels not seen since the March earthquake and tsunami last week.

The Nikkei 225 Average ended at 10,137.73, up 2.7% over the week, after briefly breaking above 10,200 to a four-month high on Friday.

The gain marked a third successive weekly increase for the benchmark indicator. The broader Topix index closed at 874.34, up 2.4% over the week.

Shares in leading Japanese exporters had a strong week on the back of hopes that the global recovery could be back on track.

Canon rose 3.2% over the five-day period while Toyota Motor added 3.3% and Honda Motor climbed 4.8%.

Chinese stocks also enjoyed a third straight week of gains.

The Shanghai Composite rose 1.4% to 2,797.77 while, in Hong Kong, the Hang Seng index climbed 1.5% to 22,726.43.

The People’s Bank of China on Wednesday raised its benchmark lending and deposit rates by 25 basis points.

Investors will now be awaiting the imminent release of Chinese inflation data for any clues about further tightening moves.

European stocks declined last week as concern deepened that the region’s debt crisis will spread and a report showed U.S. employers added fewer workers than forecast, fueling speculation the economic recovery is slowing.

UniCredit SpA, Italy’s biggest lender, and Portugal’s Banco Espirito Santo SA (BES) led declines in banking shares, sliding more than 7 percent. British Sky Broadcasting Plc fell the most since 2008 on speculation its acquisition by News Corp. will be delayed amid a phone-tapping scandal at the News of the World.

CSM NV plummeted 15 percent after the world’s largest maker of bakery ingredients said earnings declined.

The benchmark Stoxx Europe 600 Index slid 0.4 percent to 273.76 this week.

European stocks erased their weekly advance Friday after Labor Department data showed U.S. employers added 18,000 workers in June, the fewest in nine months.

European Central Bank officials increased the key interest rate by 25 basis points to 1.5% this week, matching forecasts by all 55 economists in a Bloomberg survey. President Jean-Claude Trichet said the ECB will suspend its minimum credit-rating threshold on Portuguese bonds after Moody’s Investors Service lowered the country’s debt to junk.

Italy’s FTSE MIB slid 7.2%, the most in 14 months, as UniCredit sank 20% and Intesa Sanpaolo SpA plummeted 14%.

Banco Espirito Santo slumped 7.1% while Banco Comercial Portugues SA retreated 13% to a record low. Moody’s cut Portugal’s credit rating to Ba2 as the nation joined Greece as the second euro-region country with a non-investment grade rating.

Credit Agricole SA (ACA) dropped 12% and National Bank of Greece SA slid 10%.

CSM plunged 15%, the biggest drop since November 2008. The maker of bakery ingredients said earnings came to about 80 million euros ($114 million) in the first half. It reported 102.5 million euros a year earlier.

ThyssenKrupp AG posted the biggest weekly drop in 14 months, falling 6.9%, as Germany’s largest steelmaker sold a 9.6% stake to reduce debt. The company sold 49.5 million shares at 32.95 euros each, raising 1.63 billion euros.

Stocks on Wall Street sank, trimming the Standard & Poor’s 500 Index’s biggest two-week gain since 2009.

The S&P 500 pared the two-week rally to 5.9% last week.

Financial stocks led the way down on Wall Street as weaker-than-expected employment numbers dashed hopes that the “soft patch” in the US economy was coming to an end.

BB&T suffered the most in the financial sector, losing 3.3%.

Bank of America was down 1.9%, despite news that it had reached a deal to sell its Balboa Life Insurance unit to Securian Financial, a US provider of insurance and retirement plans.

In the wider market, the S&P 500 index was still up 0.3% over the week.

In the industrial space, Caterpillar was down 1.1% despite news that China’s regulator had approved its acquisition of mining equipment firm, Bucyrus International.

Elsewhere, Cummins was down 1.9% while the S&P industrial index was 1.2%.

The worst performing stock on the S&P 500 index was JDS Uniphase, which fell 4.6%.

The Dow Jones Industrial Average was up 0.6% at 12,657.05, while the Nasdaq Composite rose 1.6% to 2,859.81 over the week.

In corporate news last week, News Corp was in focus as the furore over allegations of phone hacking at one of its British newspapers escalated. The stock was down 7.3% over the week, as the paper in question was closed down and some speculated that News Corp’s proposed takeover of BSkyB, the satellite broadcaster, could be in jeopardy.

Japan's benchmark stock indices ended Monday's session lower. The Nikkei was down 68.20 points, or 0.67%, to stand at 10069.53. The

broader-based TOPIX was down 3.86 points at 870.48.

The euro fell last week amid the eurozone’s developing debt crisis.

Over the five sessions, investors saw Portugal’s sovereign rating downgraded to junk status by Moody’s; and a sharp sell-off in Italian bonds and credit default swaps which hit the country’s banking stocks.

The ECB also raised interest rates last week, remaining hawkish on inflation, while influential jobs data from the US were much weaker than expected, thwarting any hopes of a near-term normalisation of US interest rates. These two events briefly supported the euro, but over the week it was concerns over the debt crisis that dominated.

Against the dollar, the euro fell 2.1% last week.

Payrolls expanded only by 18,000 in June after a revised increase of 25,000 in the previous month, the Labor Department reported Friday. The median forecast of economists was for 105,000 more jobs. The unemployment rate unexpectedly increased to 9.2%.

The Canadian currency slid versus the greenback. It earlier rose after the government reported that Canada’s employers added more jobs last month than economists forecast.

Nikkei 225 +66.59 +0.66% 10,138

FTSE 100 -63.97 -1.06% 5,991

CAC 40 -66.41 -1.67% 3,914

DAX -68.71 -0.92% 7,403

Dow -62.29 -0.49% 12,657

Nasdaq -12.85 -0.45% 2,860

S&P 500 -9.42 -0.70% 1,344

10 Year Yield -0.13 3.02%

Oil -0.30 -0.31% $95.90

Gold +2.00 +0.13% $1,543.60

Resistance 3: Y82.20

Resistance 1: Y81.00

Current price: Y80.77

Resistance 1: Chf0.8500

Current price: Chf0.8382

Support 1: Chf0.8360

Support 2: Chf0.8250

Support 3: Chf0.8200

Comments: Dollar remains under pressure with support is around session lows on Chf0.8360. Channel support line from Jun 06 comes at Chf0.8250. Below support is around Chf0.8200. Resistance comes at Chf0.8500 (channel lines from Jun06 and Feb16 crossing). Above resistances comes at Chf0.8600 and Chf0.8680.

Comments: Rate holds a bit higher the lower bound of the triangle on the hourly charts, coming today at $1.4170. Further support is near $1.4100 (Jun 27 lows) and $1.3970 (May 23 lows). Resistance is near $1.4320 (channel line from Jul 05). Above there is a room for a rise to $1.4530 (upper bound of triangle), with a break above opens the way to $1.4570 (Jul 04 high).

02:50 Japan (M2+CDs) money supply (June) Y/Y - 2.7%

09:45 France Industrial production (May) - -0.3%

09:45 France Industrial production (May) Y/Y - 3.9%

© 2000-2026. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers