- Analytics

- News and Tools

- Market News

CFD Markets News and Forecasts — 10-03-2011

Gainers:

TRR.N 4.87 +0.07 +1.46

AEO.N 15.66 +0.10 +0.64

AHD.N 20.90 +0.04 +0.19

JCP.N 37.00 +0.06 +0.16

NAV.N 63.13 +0.04 +0.06

Loosers:

PRM.N 4.35 -0.19 -4.19

WRE.N 29.48 -0.42 -1.39

PRGN.N 3.08 -0.03 -0.96

MER_pm.N 23.22 -0.21 -0.88

MER_pk.N 23.45 -0.13 -0.54

Stocks extended their recent pullback to fresh session lows. The move took the S&P 500 down to the 1294 line, which matches the monthly low that was set two weeks ago. Support there has helped stocks make a modest rebound effort, though.

Finally cracked the residual bids around $1.3790, nudges to $1.3784 as initial flush of stops runs its course. Further stops sub $1.3780, ahad of $1.3740, 50% of the latest rally.

European shares fell to the lowest closing level so far this year on Thursday, on economic recovery and sovereign debt concerns that could see a key technical level challenged in the short term.

Stocks have slipped a bit in recent trade. Buyers had been defending many of the market's dips during the past couple of hours. Treasuries have eased back in recent trade, too. They are still up with slight gains ahead of results from an auction of 30-year Bonds at the top of the hour.

The euro fell to the lowest level in a week against the dollar after Moody’s Investors Service lowered Spain’s credit rating, increasing pressure on European leaders to find a solution to the region’s debt crisis.

The shared currency weakened against most of its major peers as Spanish debt was downgraded to Aa2 by Moody’s, which also cut Greece’s ranking this week. Currencies of commodity- exporting countries weakened after China reported an unexpected trade deficit and crude oil prices fell. The pound stayed lower versus the greenback after the Bank of England left interest rates at a record low.

“The euro has been hobbled by negative risk flows,” said Boris Schlossberg, director of research at online currency trader GFT Forex in New York. “The greatest risk that the market is starting to fear is that the spate of downgrades within the euro zone and the expansion of the periphery credit risks could force the European Central Bank to possibly delay the rate hike, which is already priced into the currency.”

The euro may decline to as low as $1.3538 should it break below the key support level of $1.3978, the 78.6 percent Fibonacci retracement from its November peak, according to Karen Jones, head of fixed-income, commodity and currency technical analysis at Commerzbank AG in London.

“A break below support at the 20-day moving average at $1.3752 targets a move down toward $1.3538, the 55-day moving average,” she said.

European leaders are due to meet tomorrow having set a March 25 deadline to approve a “comprehensive” package of measures to end the sovereign-debt crisis. Moody’s said the outlook for the Spanish rating is “negative,” meaning the next change is most likely to be another cut.

- EFSF needs larger volume, more flexibility;

- Banks need adequate capitalization;

- ECB rate hike pre-announcement in line with mandate;

- Markets awaiting decisions on EMU debt crisis;

- Uncertainty especially high ahead of EU decisions

- EFSF needs larger volume, more flexibility;

- Banks need adequate capitalization;

- ECB rate hike pre-announcement in line with mandate;

- Markets awaiting decisions on EMU debt crisis;

- Uncertainty especially high ahead of EU decisions

Stocks are attempting to stabilize after suffering a precipitous drop at the open. Losses remain deep and broad, though. In fact, 95% of the issues in the S&P 500 are in the red.

Amid the bloodshed, airline stocks have actually put together a 0.1% gain, as measured by the Amex Airline Index. The bid for airline shares comes as oil prices push down to $102 per barrel, which makes for a 2.3% loss.

JPM notes jobless claims remain "more than 25,000 lower than that reported for the February payroll survey week. The claims data may be bounce around somewhat, but we believe the overall trend is consistent with healing in the labor market."

U.S. stocks were poised to follow overseas markets lower Thursday, after China reported a surprise trade deficit and Spain's credit rating was lowered one notch.

A wider U.S. trade gap and a slightly worse-than-expected jobless claims report pressured futures but analysts expect that to ease as investors digest the data.

The U.S. trade balance for January widened to $46.3 billion, a five-month high. This was much wider than the $41.5 billion gap forecast, according to a consensus estimate.

The U.S. Department of Labor released the latest weekly initial unemployment claims data, which totaled 397,000. Economists expected the number of people filing for first-time benefits to have risen to 382,000 last week from 368,000 the previous week.

In addition, the European debt crisis has returned to the forefront this week, with Moody's lowering Spain's credit rating Thursday, after downgrading Greece earlier this week. Moody's cut Spain's government bond rating to Aa2 with a negative outlook from Aa1, and said further downgrades are possible.

China reported a $7.3 billion trade deficit in February, as imports soared and exports rose only slightly. Government officials attributed the cooling exports to Chinese New Year, when the country's manufacturing output slowed dramatically.

World markets:

Companies: Starbucks (SBUX) and Green Mountain Coffee (GMCR) announced a deal that will put Starbucks coffee into Green Mountain's K-Cup single-cup brewing packets.

Shares of Green Mountain were up 9% in premarket trading, Starbucks stock was up more than 1% on the deal.

Hospital chain HCA (HCA) raised its public offering to 126.2 million shares at a price of $30 per share, according to published reports. It is considered to be the largest private-equity backed IPO in U.S. history, according to Renaissance Capital, raising an estimated $3.8 billion for both the company and existing shareholders.

Oil for April delivery slipped $1.02 to $103.36 a barrel.

Gold futures for April delivery fell $10.10 to $1,419.50 an ounce.

The price on the benchmark 10-year U.S. Treasury rose, pushing the yield down to 3.46% from 3.47% late Wednesday.

Stops below $1.6210 targeted and triggered, as rate drops back to $1.6108, with rate retaining a heavy tone as recovery efforts remains very shallow. Next support seen at $1.6104, the level corresponding to the 76.4% retrace of the move up from $1.6030 to $1.6344. More stops noted on a break of $1.6100, which if triggered to open a deeper move toward $1.6075/70.

Keeps Bank rate unchanged, as widely expected.

Bank rate remains at 0.5%

Offers at $1.3850 so far able to counter rate's recovery efforts, though corrective pullbacks remain shallow and keeps hopes alive for a stronger recovery. Intraday stops said to begin above $1.3850, more through $1.3860. Rate currently trades around $1.3845. Support remains in place at $1.3830, stronger on approach to $1.3800

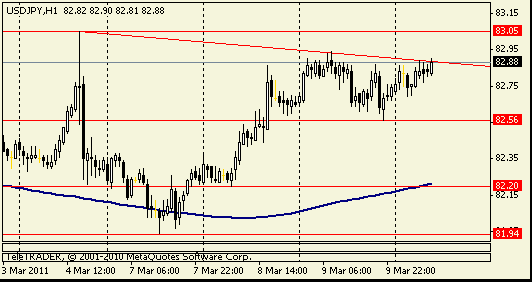

EUR/JPY Y115.90, Y113.00, Y112.00

GBP/USD $1.6000, $1.6365

USD/CHF Chf0.9275

AUD/USD $1.0200, $1.0130, $1.0100, $1.0060, $1.0050, $1.0000

NZD/USD $0.7425, $0.7470, $0.7480

AUD/NZD NZ$1.3800

Nikkei -1.46% 10,434.38

majority for a move in May. Recent CIPS PMIs did not provide much comfort on the growth front, showing an overall 'flattish' picture although cost and price pressures remain strong.

The 17-nation currency rose earlier on speculation the European Central Bank asked for prices to purchase the securities of the region’s most indebted nations. The central bank inquired about prices for Irish bonds and didn’t buy, according to two traders with knowledge of the matter.

The Swiss franc rose against all of its 16 most-traded counterparts as crude oil prices increased on concern turmoil in North Africa and the Mideast will disrupt supply, encouraging investors to seek refuge.

Crude oil gained 0.3 percent to $105.33 a barrel in New York. It reached a two and a half year high of $106.95 earlier this week.

Currencies of commodity-exporting countries strengthened against the dollar as raw materials rose for an eight day in nine.

majority for a move in May. Recent CIPS PMIs did not provide much comfort on the growth front, showing an overall 'flattish' picture although cost and price pressures remain strong.

© 2000-2026. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers