- Analytics

- News and Tools

- Market News

CFD Markets News and Forecasts — 08-10-2020

| Time | Country | Event | Period | Previous value | Forecast |

|---|---|---|---|---|---|

| 00:30 (GMT) | Australia | Home Loans | August | 10.7% | |

| 00:30 (GMT) | Australia | RBA Financial Stability Review | |||

| 01:45 (GMT) | China | Markit/Caixin Services PMI | September | 54 | |

| 06:00 (GMT) | Japan | Prelim Machine Tool Orders, y/y | September | -23.3% | |

| 06:00 (GMT) | United Kingdom | Manufacturing Production (YoY) | August | -9.4% | -5.9% |

| 06:00 (GMT) | United Kingdom | Industrial Production (YoY) | August | -7.8% | -4.6% |

| 06:00 (GMT) | United Kingdom | Industrial Production (MoM) | August | 5.2% | 2.5% |

| 06:00 (GMT) | United Kingdom | Manufacturing Production (MoM) | August | 6.3% | 3% |

| 06:00 (GMT) | United Kingdom | GDP, y/y | August | -11.7% | |

| 06:00 (GMT) | United Kingdom | GDP m/m | August | 6.6% | 4.6% |

| 06:00 (GMT) | United Kingdom | Total Trade Balance | August | 1.1 | |

| 06:45 (GMT) | France | Industrial Production, m/m | August | 3.8% | 1.7% |

| 12:30 (GMT) | Canada | Employment | September | 245.8 | 156.6 |

| 12:30 (GMT) | Canada | Unemployment rate | September | 10.2% | 9.7% |

| 13:00 (GMT) | United Kingdom | NIESR GDP Estimate | Quarter III | 7% | 8.7% |

| 14:00 (GMT) | U.S. | Wholesale Inventories | August | -0.1% | 0.5% |

| 17:00 (GMT) | U.S. | Baker Hughes Oil Rig Count | October | 189 | |

| 23:50 (GMT) | Japan | Core Machinery Orders, y/y | August | -16.2% | |

| 23:50 (GMT) | Japan | Core Machinery Orders | August | 6.3% |

FXStreet reports that Mazen Issa, Senior FX Strategist at TD Securities is biased to NZD weakness on the crosses, particularly AUD/NZD, following comments from the Reserve Bank of new Zealand (RBNZ) that suggest more easing is in the pipeline.

“On the one hand, the RBNZ has signaled that a ‘least regrets approach to thinking how much stimulus to deliver’ is a clear indication that the central bank is readying the stimulus canon. On the other hand, the NZD is also a beneficiary of the reflation trade in a Biden/blue wave administration.”

“We think AUDNZD topside makes sense and we look for a run towards 1.1050. In our FX monthly, we highlighted that we would engage in AUDNZD longs on a dip towards 1.0750. Admittedly, that position may have run away from us in the last couple of days. Nonetheless, we think AUD/NZD dips should be faded from here in anticipation of the RBNZ decision next month.”

- Growth is significantly better than expected

- Home sales and autos are "booming"

- Administration is pushing for targeted relief to airlines, small business, and stimulus checks

- Other side needs to meet White House "halfway"

- Canada came into the pandemic with a number of vulnerabilities and it “seems certain” the country would exit with higher levels of government debt

- As much as bold policy response was needed, it will inevitably make economy and financial system more vulnerable to economic shocks down the road

- Without fiscal and monetary policy actions, economic devastation of the pandemic could have been much, much worse

- Full recovery will take long time; many risks remain

- Nobody wants to return to lockdown, but second wave could test our resolve to practice physical distancing and keep the pandemic from spreading uncontrollably again

- BoC is keeping a close eye on household debt levels and Canada’s housing market, both of which were vulnerabilities coming into the pandemic

- BoC will continue to assess the risk that credit losses could become large enough that banks need to tighten credit conditions; if this happens, our banking system would go from being a tailwind that supports recovery to being a headwind

- BoC is not discussing negative interest rates, but "never say never"

The Canada

Mortgage and Housing Corp. (CMHC) reported on Thursday the seasonally adjusted

annual rate of housing starts was at 208,980 units in September, down 20.1

percent from a downwardly revised 261,547 units in August (originally 262,396 units).

This was the highest reading since September 2007.

Economists had

forecast an annual pace of 240,000 for September.

According to the report, urban starts plunged by 21.1

percent m-o-m last month to 195,909 units, as multiple urban starts tumbled by 27.0

percent m-o-m to 146,005 units, while single-detached urban starts rose by 3.4

percent m-o-m 49,904 units. At the same time, rural starts were estimated at a

seasonally adjusted annual rate of 13,071 units.

- Says he wants standalone bills because the bigger package has too much for state and local governments

- Wants targeted assistance in key areas

- September statement was a message of patients on rates

- New inflation framework is a tolerance for modest overshoot above 2%; it is less so a promise to engineer it

- Inflation moderately above 2% unlikely to warrant a policy response if economy is otherwise doing well

- While the new statement reflects patience in awaiting inflation, not yet clear how much patience given uncertainty over how pandemic will impact prices

- It is important to provide guidance on Fed's QE

U.S. stock-index futures rose on Thursday, as expectations of more fiscal stimulus being approved in the U.S. outweighed disappointing weekly jobless claims.

Global Stocks:

Index/commodity | Last | Today's Change, points | Today's Change, % |

Nikkei | 23,647.07 | +224.25 | +0.96% |

Hang Seng | 24,193.35 | -49.51 | -0.20% |

Shanghai | - | - | - |

S&P/ASX | 6,102.00 | +65.60 | +1.09% |

FTSE | 5,983.61 | +37.36 | +0.63% |

CAC | 4,908.47 | +26.47 | +0.54% |

DAX | 13,023.19 | +94.62 | +0.73% |

Crude oil | $40.81 | +2.15% | |

Gold | $1,904.20 | +0.71% |

FXStreet reports that according to the Credit Suisse analyst team, the EUR/JPY pair is expected to see a sustained move above its 55-day average to reinforce its base for an eventual move back to the 127.08 September high.

“EUR/JPY remains well supported at 123.86/84 as expected and is seeing a fresh and concerted challenge on its 55-day average and 50% retracement of the September fall at 124.72/74. With a base in place, we continue to look for a clear and sustained move above here to reinforce the base and resumption of the broader uptrend resumed.”

“We see the next resistance at the 61.8% retracement and price resistance at 125.28/32, ahead of 126.46 and eventually the 127.08/11 high and long-term downtrend from late 2014, where we would expect fresh sellers to show.”

(company / ticker / price / change ($/%) / volume)

3M Co | MMM | 167.5 | 1.01(0.61%) | 2519 |

ALCOA INC. | AA | 12.39 | 0.15(1.23%) | 14376 |

ALTRIA GROUP INC. | MO | 40.7 | 0.17(0.42%) | 9578 |

Amazon.com Inc., NASDAQ | AMZN | 3,224.36 | 28.67(0.90%) | 61981 |

American Express Co | AXP | 103.41 | 0.46(0.45%) | 4941 |

AMERICAN INTERNATIONAL GROUP | AIG | 29.8 | 0.24(0.81%) | 693 |

Apple Inc. | AAPL | 116.25 | 1.17(1.02%) | 1383164 |

AT&T Inc | T | 28.32 | 0.04(0.14%) | 440068 |

Boeing Co | BA | 166.28 | 1.67(1.01%) | 161085 |

Caterpillar Inc | CAT | 155.5 | 0.73(0.47%) | 4206 |

Chevron Corp | CVX | 74.45 | 0.67(0.91%) | 10988 |

Cisco Systems Inc | CSCO | 39.78 | 0.38(0.96%) | 58694 |

Citigroup Inc., NYSE | C | 44.92 | 0.08(0.18%) | 136955 |

E. I. du Pont de Nemours and Co | DD | 58.05 | 0.39(0.68%) | 931 |

Exxon Mobil Corp | XOM | 33.89 | 0.39(1.16%) | 57141 |

Facebook, Inc. | FB | 260.16 | 2.04(0.79%) | 108635 |

FedEx Corporation, NYSE | FDX | 271.57 | 3.31(1.23%) | 12858 |

Ford Motor Co. | F | 7.3 | 0.07(0.97%) | 113375 |

Freeport-McMoRan Copper & Gold Inc., NYSE | FCX | 17.19 | 0.31(1.84%) | 59678 |

General Electric Co | GE | 6.36 | 0.05(0.79%) | 902567 |

General Motors Company, NYSE | GM | 31.86 | 0.24(0.76%) | 18212 |

Goldman Sachs | GS | 205 | 1.40(0.69%) | 11247 |

Home Depot Inc | HD | 285 | 2.21(0.78%) | 5664 |

HONEYWELL INTERNATIONAL INC. | HON | 172 | 0.45(0.26%) | 2077 |

Intel Corp | INTC | 52.96 | 0.29(0.55%) | 81302 |

International Business Machines Co... | IBM | 135 | 10.93(8.81%) | 2151825 |

Johnson & Johnson | JNJ | 148.55 | 0.67(0.45%) | 17483 |

JPMorgan Chase and Co | JPM | 100.4 | 0.67(0.67%) | 102678 |

McDonald's Corp | MCD | 227.22 | 0.74(0.33%) | 107671 |

Merck & Co Inc | MRK | 80.12 | 0.08(0.10%) | 9419 |

Microsoft Corp | MSFT | 210.6 | 0.77(0.37%) | 158031 |

Nike | NKE | 130.7 | 0.64(0.49%) | 5266 |

Pfizer Inc | PFE | 36.58 | 0.11(0.30%) | 50987 |

Procter & Gamble Co | PG | 140.99 | 0.29(0.21%) | 2484 |

Starbucks Corporation, NASDAQ | SBUX | 88.8 | 0.35(0.40%) | 6984 |

Tesla Motors, Inc., NASDAQ | TSLA | 437.8 | 12.50(2.94%) | 1119516 |

The Coca-Cola Co | KO | 49.73 | 0.17(0.34%) | 6959 |

Travelers Companies Inc | TRV | 114.83 | 1.03(0.91%) | 935 |

Twitter, Inc., NYSE | TWTR | 46.35 | 0.48(1.05%) | 24220 |

Verizon Communications Inc | VZ | 59.09 | 0.11(0.18%) | 48616 |

Visa | V | 203.12 | 0.65(0.32%) | 6147 |

Wal-Mart Stores Inc | WMT | 141.55 | 0.66(0.47%) | 15979 |

Walt Disney Co | DIS | 123.59 | 0.68(0.55%) | 19688 |

Yandex N.V., NASDAQ | YNDX | 61.79 | 0.94(1.54%) | 33671 |

Tesla (TSLA) upgraded to Buy from Neutral at New Street; tgt $578

- Covid-19 aid talks are starting to work out; really good chance to reach a deal

- House Speaker Nancy Pelosi wants to make a deal on COVID-19 aid

- Both sides discussing deal for airlines, individual stimulus checks

- Says he is feeling really good, ready to go except for quarantine

- It is not acceptable to do next presidential debate virtually

The data from

the Labor Department revealed on Thursday the number of applications for

unemployment exceeded economists’ forecast last week, as the U.S. labor market

struggles to recover from its biggest shock in history, caused by the

COVID-19 pandemic.

According to

the report, the initial claims for unemployment benefits totaled 840,000 for

the week ended October 3.

Economists had

expected 820,000 new claims last week.

Claims for the

prior week were revised upwardly to 849,000 from the initial estimate of 837,000.

Meanwhile, the

four-week moving average of claims dropped to 857,000 from an upwardly revised

870,250 in the previous week.

Continuing

claims declined to 10,976,000 million from an upwardly revised 11,979,000 in

the previous week.

| Time | Country | Event | Period | Previous value | Forecast | Actual |

|---|---|---|---|---|---|---|

| 09:30 | Switzerland | SNB Chairman Jordan Speaks | ||||

| 10:15 | Eurozone | ECB's Yves Mersch Speaks | ||||

| 11:30 | Eurozone | ECB Monetary Policy Meeting Accounts | ||||

| 12:15 | Canada | Housing Starts | September | 261.5 | 240 | 209 |

| 12:30 | U.S. | Continuing Jobless Claims | September | 11979 | 11400 | 10976 |

| 12:30 | U.S. | Initial Jobless Claims | October | 849 | 820 | 840 |

| 12:30 | Canada | BOC Gov Tiff Macklem Speaks |

USD edged down against most other major currencies in the European session on Thursday as investors grew more optimistic that the U.S. lawmakers could approve more fiscal stimulus for the U.S. economy, even if it comes in the form of smaller, targeted aid bills.

The U.S. Dollar Index (DXY), measuring the U.S. currency's value relative to a basket of foreign currencies, dropped 0.03% to 93.60.

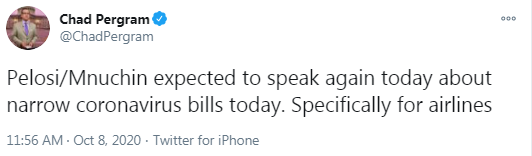

FOX News' congressional correspondent reported that House Speaker Nancy Pelosi and Treasury Secretary Steve Mnuchin expected to speak again today about narrow coronavirus bills, specifically for airlines.

In addition, market participants continued to digest the minutes of the September meeting of the U.S. Federal Reserve, released on Wednesday, which hinted at the central bank's willingness to provide deeper monetary support in the form of accelerated monthly bond purchases and years of near-zero interest rates.

Investors also bet that Joe Biden, the Democratic candidate for U.S. president, if elected, would quickly spend money to stimulate economic recovery.

The ECB

released account of its September 9-10 monetary policy meeting. It noted that:

- Recovery was asymmetric, being further advanced in manufacturing sector than in services sector;

- On the basis of the current information, PEPP envelope would likely have to be used in full to provide necessary accommodation to offset downward impact of pandemic on path of inflation;

- Point was made that pace of monthly purchases could be reduced as tensions in financial markets subsided;

- Further cuts in policy rates and changes to conditions of TLTROs are also part of the toolkit for providing additional monetary policy accommodation, if necessary;

- Recent appreciation of euro exchange rate had had a material impact on the inflation outlook in the September ECB staff projections;

- There was broad agreement among members that there was no room for complacency;

- There had been a marked appreciation of the euro exchange rate since July; while the appreciation to some extent reflected improvements in global risk sentiment, as well as euro area factors such as NGEU recovery plan, it also reflected developments in monetary conditions in euro area relative to the rest of the world;

- Market positioning remained tilted towards further euro appreciation, with net speculative US dollar positions against advanced economy currencies, including the euro, remaining sizeable;

- Inflation was expected to remain persistently low over the medium term, notwithstanding gradual pick-up over projection horizon;

- Underlying dynamics of the pandemic, developments in negotiations on post-transition Brexit arrangement, outcome of US presidential election and decisions on fiscal plans at individual country level as well as at euro area level had to be closely monitored.

FXStreet reports that analysts at Credit Suisse note that upward pressure continues to build in the S&P 500 Index with a break above 3429/44 seen marking the completion of a “head & shoulders” base for a resumption of the broader core uptrend.

“The S&P 500 has for now essentially ignored the bearish ‘reversal day’ from Tuesday and this leaves the focus firmly on the mid-September highs and 61.8% retracement of the fall from September at 3429/44.”

“With a clear ‘head & shoulders’ base forming and with daily MACD momentum having already turned higher our bias leans higher for an eventual clear and sustained move above 3444. This would then see a more important base established to mark a resumption of the core uptrend. We would then see resistance at 3495 initially ahead of 3565 and eventually the 3588 high. Immediate support moves to 3396/94, with 3385/81 now ideally holding to keep the immediate risk higher.”

- Crisis measures are justified by pandemic but should not be taken beyond crisis without deepening institutional functioning of democracy at the union level

FXStreet notes that NZD/USD has held above the potential uptrend from August at 0.6521 to reinforce the view of the Credit Suisse analyst team of further sideways trading. Resistance moves initially to 0.6601 while support is seen at 0.6568.

“NZD/USD corrective weakness has come to a halt for a rebound higher just ahead of the potential uptrend from August, currently at 0.6521. This reinforces the view that we could see further sideways trading before an eventual resumption of the core bull trend, with resistance seen initially at 0.6601, ahead of 0.6657/58, where we would expect to see a pause at first.”

“Removal of 0.6657/58 would subsequently open the door to the cluster of resistances at 0.6778/6806 – the recent and current year highs as well as the 78.6% retracement of the December 2018/March 2020 fall – where we would expect to see a more concerted effort to cap at first.”

“Support moves to 0.6568, then 0.6547/40, beneath which would see a move back to 0.6521/12.

FXStreet reports that economist at UOB Group Lee Sue Ann reviewed the recent fiscal measures announced by the Australian government.

“Australia PM Scott Morrison’s conservative government, on Tuesday (6 October), unleashed further emergency stimulus to prop up economic growth, backpedalling on a previous promise to return the budget to surplus. The 2020/21 Budget brings the Government's overall support to A$507bn, including A$257bn in direct economic support.”

“Australia delayed the release of this year’s federal budget, which usually takes place in May, as the COVID-19 pandemic upended most of the economic assumptions underlying its projections... The latest measures are forecast to push the budget deficit out to a record A$213.7bn (around 11% of GDP).”

“The government’s highly expansionary budget came shortly after the Reserve Bank of Australia (RBA)’s policy decision on Tuesday, at which it kept interest rates at a record-low and flagged reducing high unemployment rate as a national priority. Further monetary expansion is likely, but we think the impact will be modest.”

- Supply of money can be reduced at any time if demand for Swiss franc weakens

FXStreet reports that Brexit deal optimism is helping to lift the GBP/USD pair back towards the 1.3000-level. However, the sharp rise in UK COVID-19 cases is set to trigger renewed restrictions, dampening the good mood, as per MUFG Bank.

“Bloomberg has reported that in private, officials are more upbeat over the likelihood of reaching a trade deal despite the UK government’s continued public threats to walk away from talks if a deal is not reached by the 15th October while the EU has dared Boris Johnson to walk away if he views a deal as impossible. The upcoming EU Summit on 15th and 16th October is viewed as more of a ‘stock-taking exercise’ which won’t get in the way of negotiations.”

“The improving mood music surrounding the Brexit talks is encouraging a stronger pound. However, the upside potential for the pound from Brexit developments is being dampened by negative COVID-19 developments in the UK. The sharp rise in COVID-19 cases particularly in the North of England and London is increasing the risk of tighter restrictions being re-imposed in the coming weeks and months that could deliver a more significant setback to the economic recovery.”

Reuters reports that ECB vice president Luis de Guindos said on Thursday that the European Central Bank has to use the tools at its disposal as the coronavirus pandemic depresses inflation expectations and an incipient recovery loses steam.

"Inflation expectations are very subdued as a result of the pandemic and some specific factors and we have to act with the tools available to us," de Guindos said in response to a question about the ECB's bond purchases.

FXStreet reports that there is plenty of risk of further equity turbulence on US political headlines, keeping the AUD/USD pair capped at 0.7250 and with scope for a test of the 100-Day Moving Average (DMA) at 0.7064, as per Westpac.

“Australia’s official 2020/21 budget was well flagged as usual, with the delivery of the details not inspiring a noticeable A$ response. This financial year is set to produce a record-smashing deficit“.

“H2 is likely to produce reasonable growth even if Victoria’s restrictions remain harsh and as tensions between New South Wales and Queensland deepen over the latter’s ongoing border closure.”

“AUD/USD continues to follow the swings in US equities, which in turn keeps political news prominent.”

“We switch from up to neutral on the week, with rallies capped around 0.7230/50 and scope for a test of the 100-DMA at 0.7064.”

CNBC reports that with uncertainty looming over the upcoming U.S. elections in November, JPMorgan Asset Management’s Patrik Schowitz says investors should look past the “noise” and focus on the medium term instead.

“On a six month view, you know, we think the cyclical view matters much, much more than … the exact noise and shenanigans around the U.S. election,” Schowitz, global multi-asset strategist at the firm, told CNBC.

“Anything longer than say two or three months, you should be positioned risk-on, you should be overweight risky assets like credit, like equities,” he said.

Still, Schowitz acknowledged that there are “a lot of risks” ahead over the next month or two, with the firm staying more balanced at present.

Commenting on the potential for more U.S. stimulus, Schowitz said: “It’ll be better to get to stimulus now, but as long as we get it early next year we think the economy will be able to get through that,” adding that households that have built a “massive amount of savings.”

Bloomberg reports that Greek bonds yields dropped to a record low as support from the European Central Bank and the European Union quells investor concerns about the health of the region’s most indebted nation in the face of the coronavirus.

Yields on the nation’s 10-year securities fell as much as six basis points to 0.881%, dropping below a previous low set in February, before the height of the pandemic crisis in Europe.

The rally is “consistent with the collapse in credit and term premia across European rates markets, and with rising expectations of ECB easing,” said Antoine Bouvet, senior rates strategist at ING Groep NV in London. “The trend is your friend.”

The Greek government expects public debt-to-GDP will be close to 200% for 2020 before declining again in 2021. The draft budget presented Monday sees growth of as much as 7.5% in 2021 after a sharp decline of 8.2% this year, mainly due to a forecast 30.4% increase in investments.

FXStreet reports that FX Strategists at UOB Group believe USD/CNH is poised for further downside in the next weeks.

24-hour view: “Our expectation for USD to ‘edge higher to 6.7600’ did not quite materialize as it traded in a quiet manner between 6.7276 and 6.7544. The underlying tone has weakened somewhat but while USD could edge lower but Monday’s (05 Oct) low of 6.7135 could be just out of reach (minor support is at 6.7200). Resistance is at 6.7450 but the stronger level is at 6.7550.”

Reuters reports that the French economy rebounded 16% in the third quarter after an unprecedented 13.8% slump in the previous three months, the central bank estimated

The euro zone’s second-biggest economy slumped deep into recession in the second quarter after the country was put under one of the strictest coronavirus lockdowns in Europe for two months.

Since the lockdown lifted on May 11, business activity has sprung back to life and the economy was operating down 5% from pre-crisis levels as of September, the central bank said.

FXStreet reports that Bart Melek, Head of Commodity Strategy at TD Securities, notes that WTI Oil tough support is seen at $37 while stubborn resistance awaits at $42.

“Given that the US and global demand recovery is likely to be somewhat slower than previously thought and considering that OPEC+ is not firmly signaling that it will postpone (or promise additional cuts if needed) its planned increase in shipments starting in January, crude oil will likely be under pressure. However, since investors are already positioned short and given there will be a vaccine, new fiscal spending after the election on the horizon and considering that there is a storm raging in the US Gulf, the downside is likely to be limited.”

“The upside is also well constrained. We judge there is good technical support near $37/bbl, with strong resistance near $42/bbl.”

| Time | Country | Event | Period | Previous value | Forecast | Actual |

|---|---|---|---|---|---|---|

| 05:00 | Japan | Eco Watchers Survey: Current | September | 43.9 | 49.3 | |

| 05:00 | Japan | Eco Watchers Survey: Outlook | September | 42.4 | 48.3 | |

| 05:45 | Switzerland | Unemployment Rate (non s.a.) | September | 3.3% | 3.3% | 3.2% |

| 06:00 | Germany | Current Account | August | 21.0 | 16.5 | |

| 06:00 | Germany | Trade Balance (non s.a.), bln | August | 19.2 | 12.8 |

During today's Asian trading, the US dollar declined against the euro and was almost unchanged against the yen.

Traders are assessing the prospects for the US authorities to take new stimulus measures against the background of the controversial actions of US President Donald Trump. On Tuesday, Trump announced the termination of negotiations with Congress on a new package of incentives before the presidential election, which will be held on November 3, but a few hours later called on lawmakers to approve the allocation of additional assistance to airlines, as well as funds for small business support programs and direct payments to Americans.

House speaker Nancy Pelosi said Wednesday that Democrats oppose passing several bills to target certain segments of the economy outside of a large-scale stimulus package. "It's hard to see a clear, reasonable line in what he's doing," Pelosi said, commenting on Trump's actions.

The ICE index, which tracks the US dollar against six currencies (the Euro, Swiss franc, yen, canadian dollar, pound sterling and Swedish Krona), fell 0.08%.

Traders are closely monitoring the dynamics of US - China relations after Bloomberg reported yesterday that Washington is considering imposing restrictions on China's Ant Group and Tencent Holdings Ltd. due to concerns that the payment platforms of these companies may pose a threat to US national security.

Reuters reports that financial services firms in Britain turned more optimistic for the first time this year as a drop in business bottomed out, but big uncertainties remained about COVID-19 and a post-Brexit trade deal.

Quarterly survey by the Confederation of British Industry showed that a drop in profits for banks, finance companies and building societies was partly offset by growth in earnings from insurance and investment management.

"While it is reassuring to see business volumes begin to stabilise in a sector so vital for the UK's recovery, financial services isn't out of the woods just yet," Rain Newton-Smith, the CBI's chief economist, said.

Staff numbers fell less severely than in the previous three-month period and the decline was expected to slow again.

The survey was conducted between Sept. 1 and Sept. 19 and 133 firms replied.

Coronavirus second wave will obviously add to economic uncertainty

Some sectors of the economy need further support for the recovery

Some parts of the economy will face structural change due to the pandemic

It is in the interests of UK and EU to get a Brexit deal

FXStreet reports that FX Strategists at UOB Group expect EUR/USD to navigate within the 1.1640-1.1820 range in the next weeks.

Next 1-3 weeks: “Yesterday, we highlighted that ‘as EUR approaches 1.1830, upward momentum has improved, albeit not by much’. We added, ‘there is room for EUR to edge above 1.1830 and move towards the next resistance at 1.1870’. EUR subsequently rose to a high of 1.1807 before dropping suddenly to an overnight low of 1.1730. While our ‘strong support’ level at 1.1715 is still intact, the rapid loss in momentum indicates that our expectation for a higher EUR is incorrect. From here, it seems that EUR has lapsed back into a consolidation phase and is likely trade between 1.1640 and 1.1820 for now.”

According to the latest KPMG and REC, UK Report on Jobs survey, a further recovery in hiring activity was seen during September, with both permanent placements and temp billings rising at steeper rates.

Panel members indicated that the easing of lockdown measures to contain the coronavirus disease 2019 (COVID-19) outbreak had led clients to take on more staff. At the same time, overall vacancies rose for the first time since February, albeit only slightly. Nonetheless, redundancies stemming from the pandemic led to a further substantial increase in staff supply, which dampened pay trends for both permanent and temporary workers.

UK recruitment consultancies signalled a further increase in overall recruitment activity during September. Notably, permanent placement growth was the strongest for nearly two years, while temp billings expanded at the quickest rate since the end of 2018. The upturns were widely linked to the reopening of the UK economy and the recommencement of projects following the easing of coronavirus disease 2019 (COVID-19) lockdown measures.

Starting salaries awarded to permanent workers continued to fall solidly in September, with the rate of decline accelerating slightly since August. Meanwhile, temp wages fell only modestly. In both cases, rising candidate numbers, subdued demand for workers and greater pressure on clients' budgets were linked to reduced pay.

According to the report from the Federal Statistical Office (Destatis), in August 2020, German exports were up 2.4% and imports 5.8% on July 2020 after calendar and seasonal adjustment. Destatis also reports that, compared with February 2020, the month before restrictions were imposed due to the corona pandemic, exports were down 9.9%, and imports 6.4% when adjusted for calendar and seasonal variations.

Germany exported goods to the value of 91.2 billion euros and imported goods to the value of 78.5 billion euros in August 2020. Compared with August 2019, exports decreased by 10.2%, and imports by 7.9% in August 2020.

The foreign trade balance showed a surplus of 12.8 billion euros in August 2020. In August 2019, the surplus amounted to 16.4 billion euros. In calendar and seasonally adjusted terms, the foreign trade balance recorded a surplus of 15.7 billion euros in August 2020.

The German current account of the balance of payments showed a surplus of 16.5 billion euros in August 2020, which takes into account the balances of trade in goods (+14.4 billion euros), services (-2.9 billion euros), primary income (+8.2 billion euros) and secondary income (-3.2 billion euros). In August 2019, the German current account showed a surplus of 15.9 billion euros.

EUR/USD

Resistance levels (open interest**, contracts)

$1.1901 (4975)

$1.1854 (3077)

$1.1815 (2499)

Price at time of writing this review: $1.1773

Support levels (open interest**, contracts):

$1.1741 (2091)

$1.1698 (2628)

$1.1649 (2781)

Comments:

- Overall open interest on the CALL options and PUT options with the expiration date October, 9 is 70247 contracts (according to data from October, 7) with the maximum number of contracts with strike price $1,1900 (4975);

GBP/USD

Resistance levels (open interest**, contracts)

$1.3152 (1542)

$1.3056 (379)

$1.2975 (866)

Price at time of writing this review: $1.2936

Support levels (open interest**, contracts):

$1.2890 (975)

$1.2867 (587)

$1.2833 (918)

Comments:

- Overall open interest on the CALL options with the expiration date October, 9 is 16291 contracts, with the maximum number of contracts with strike price $1,3150 (1542);

- Overall open interest on the PUT options with the expiration date October, 9 is 18305 contracts, with the maximum number of contracts with strike price $1,3150 (2526);

- The ratio of PUT/CALL was 1.12 versus 1.14 from the previous trading day according to data from October, 7

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

| Raw materials | Closed | Change, % |

|---|---|---|

| Brent | 41.77 | 0.7 |

| Silver | 23.78 | 3.53 |

| Gold | 1887.615 | 0.54 |

| Palladium | 2350.52 | 0.51 |

| Index | Change, points | Closed | Change, % |

|---|---|---|---|

| NIKKEI 225 | -10.91 | 23422.82 | -0.05 |

| Hang Seng | 262.21 | 24242.86 | 1.09 |

| KOSPI | 21.04 | 2386.94 | 0.89 |

| ASX 200 | 74.3 | 6036.4 | 1.25 |

| FTSE 100 | -3.69 | 5946.25 | -0.06 |

| DAX | 22.55 | 12928.57 | 0.17 |

| CAC 40 | -13.46 | 4882 | -0.27 |

| Dow Jones | 530.7 | 28303.46 | 1.91 |

| S&P 500 | 58.48 | 3419.45 | 1.74 |

| NASDAQ Composite | 210 | 11364.6 | 1.88 |

| Time | Country | Event | Period | Previous value | Forecast |

|---|---|---|---|---|---|

| 05:00 (GMT) | Japan | Eco Watchers Survey: Current | September | 43.9 | |

| 05:00 (GMT) | Japan | Eco Watchers Survey: Outlook | September | 42.4 | |

| 05:45 (GMT) | Switzerland | Unemployment Rate (non s.a.) | September | 3.3% | 3.3% |

| 06:00 (GMT) | Germany | Current Account | August | 20.0 | |

| 06:00 (GMT) | Germany | Trade Balance (non s.a.), bln | August | 19.2 | |

| 09:30 (GMT) | Switzerland | SNB Chairman Jordan Speaks | |||

| 10:15 (GMT) | Eurozone | ECB's Yves Mersch Speaks | |||

| 11:30 (GMT) | Eurozone | ECB Monetary Policy Meeting Accounts | |||

| 12:15 (GMT) | Canada | Housing Starts | September | 262.4 | 240 |

| 12:30 (GMT) | U.S. | Continuing Jobless Claims | September | 11767 | 11400 |

| 12:30 (GMT) | U.S. | Initial Jobless Claims | October | 837 | 820 |

| 12:30 (GMT) | Canada | BOC Gov Tiff Macklem Speaks | |||

| 18:30 (GMT) | U.S. | Fed Barkin Speech | |||

| 22:00 (GMT) | U.S. | FOMC Member Kaplan Speak | |||

| 23:30 (GMT) | Japan | Labor Cash Earnings, YoY | August | -1.3% | |

| 23:30 (GMT) | Japan | Household spending Y/Y | August | -7.6% | -6.9% |

| Pare | Closed | Change, % |

|---|---|---|

| AUDUSD | 0.71364 | 0.51 |

| EURJPY | 124.645 | 0.59 |

| EURUSD | 1.1762 | 0.25 |

| GBPJPY | 136.796 | 0.6 |

| GBPUSD | 1.29083 | 0.27 |

| NZDUSD | 0.65759 | -0.1 |

| USDCAD | 1.32589 | -0.4 |

| USDCHF | 0.91604 | -0.22 |

| USDJPY | 105.971 | 0.34 |

© 2000-2026. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers