- Analytics

- News and Tools

- Market News

CFD Markets News and Forecasts — 08-02-2022

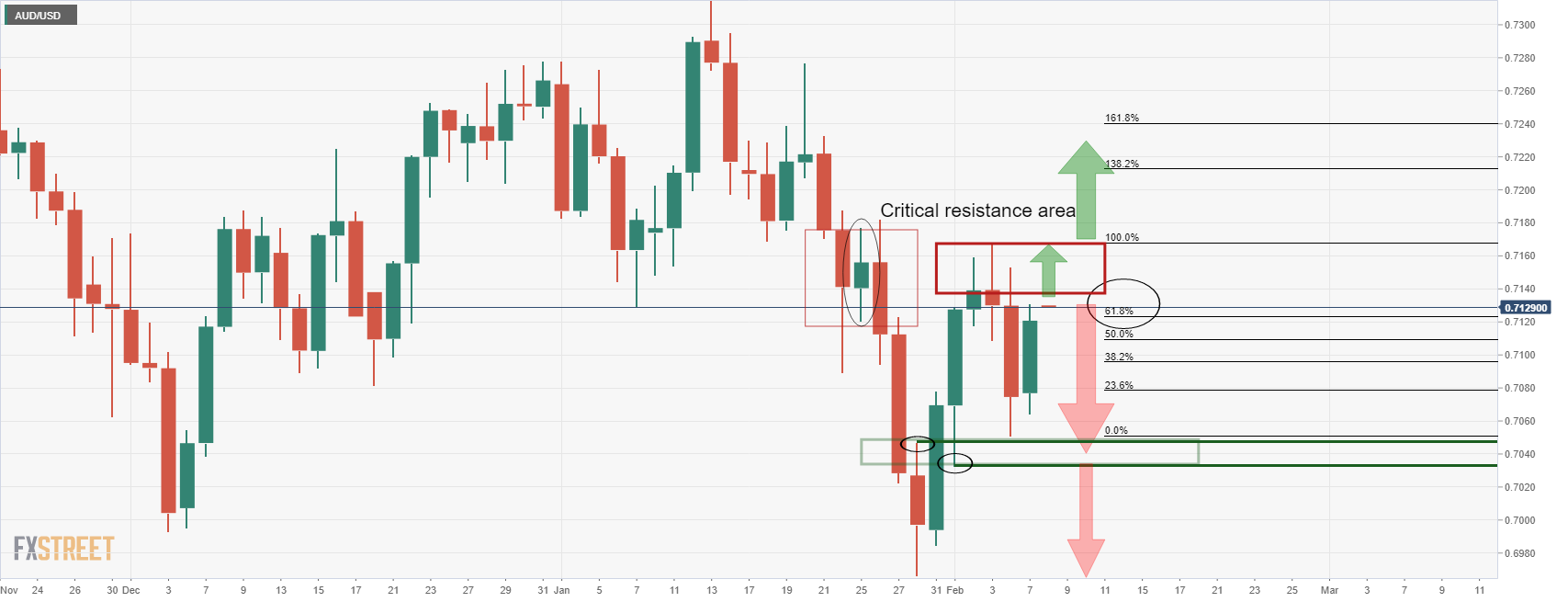

- AUD/USD remains sidelined after two-day uptrend to refresh weekly top.

- Australia Westpac Consumer Confidence improved in February but marked the third monthly negative print.

- Risk appetite stays weak even as equities, gold remain firmer.

- Concerns over US inflation, geopolitics become major catalysts, Aussie Consumer Inflation Expectations are important too.

AUD/USD hovers around 0.7140-50 during the initial Asian session on Wednesday, following a two-day uptrend, as market players search for fresh clues amid cautious optimism.

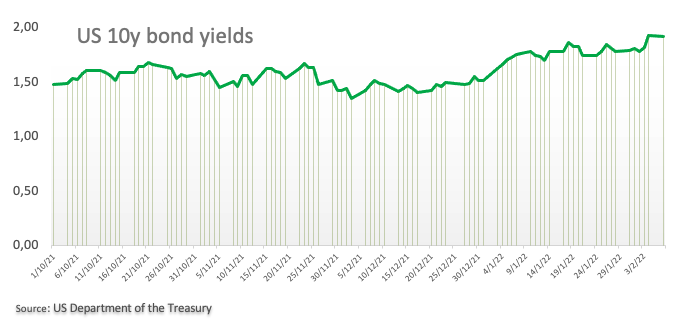

The recently mixed feelings among the traders could be linked to strong US Treasury yields and anxiety ahead of the US Consumer Price Index (CPI) data. Also challenging the pair buyers are the latest headlines conveying the Sino-American trade tussles and China’s readiness to tame disorderly growth of capital.

That said, Australia’s Westpac Consumer Confidence for February improved to -1.3% versus -2.0% previous readouts. Even so, the figures marked a third consecutive monthly fall.

Elsewhere, the Chinese Communist Party (CCP) was quoted in the South China Morning Post (SCMP) as saying, “China should ‘support and guide’ the healthy development of capital, and prevent the ‘barbaric growth of capital.’ The same should challenge the equity buyers as the yields are up.

Concerning the US Treasury yields, Reuters said, “The yield on the 10-year note reached 1.97%, its highest level since Nov 7, 2019, as investors await inflation data on Thursday. Expectations are for the January consumer price index to show a 0.5% increase after a 0.6% rise in the prior month, with the year-over-year reading expected to show a 7.3% climb.”

It’s worth noting that White House Press Secretary Jen Psaki conveyed China’s lack of performance over the Phase 1 deal trade terms, which in turn challenges the AUD/USD bulls due to Australia’s trade links with Beijing.

On the contrary, the US dollar’s downbeat performance, despite the latest rebound, joins firmer Wall Street benchmarks and gold prices to favor the AUD/USD bulls.

Moving on, risk catalysts will direct short-term AUD/USD moves ahead of Thursday’s US inflation and Australia Consumer Inflation Expectations for February, expected 4.5% versus 4.4% prior.

Technical analysis

50-DMA joins a two-week-old descending trend line to highlight 0.7160-65 as the short-term key resistance. However, firmer MACD and RSI conditions hint at further upside until the quote drops below the weekly support line near 0.7095.

- EUR/USD remains on the back foot for the third consecutive day.

- US 10-year Treasury yields rally to three-year high, Wall Street benchmarks closed positive.

- ECB’s Villeroy joins the bear’s league by criticizing hawkish reaction at the latest meeting.

- German trade numbers will entertain traders but US CPI, EC Economic Forecasts are the key.

EUR/USD holds lower ground near 1.1415 during a quiet Asian session on Wednesday, after stepping back from a three-month high in the last two days.

The pair’s latest weakness could be linked to the higher US Treasury yields and downbeat comments from the European Central Bank (ECB) policymakers.

“The yield on the 10-year note reached 1.97%, its highest level since Nov 7, 2019, as investors await inflation data on Thursday. Expectations are for the January consumer price index to show a 0.5% increase after a 0.6% rise in the prior month, with the year-over-year reading expected to show a 7.3% climb,” said Reuters.

On the other hand, European Central Bank (ECB) governing council member and Bank of France's head Francois Villeroy de Galhau said on Tuesday that the market reaction to last week's ECB meeting may have been too strong.

It’s worth noting that an escalation in the risk concerning the Russia-Ukraine war and the market’s anxiety ahead of the US Consumer Price Index (CPI) data for January, as well as the European Commission’s quarterly economic forecasts, up for publishing on Thursday, also weigh on the EUR/USD prices of late.

On the contrary, firmer equities and the US dollar’s failure to track firmer bond yields seem to challenge the EUR/USD sellers ahead of the key day.

Ahead of the crucial catalysts, markets remain bearish on the major currency pair. “On balance, we still expect the risks to be to the downside for EURUSD this year and to the upside next year. We have been forecasting EURUSD at 1.10 this year, 1.15 next year and 1.20 (lower end of long-term equilibrium range) in 2024. Although getting the timing right of such a path will be difficult, we stick with it for now,” said Bank of America (BofA).

For now, German trade numbers for January will join the Fedspeak to direct intraday moves ahead of the key data/events.

Read: Forex Today: Tension mounts ahead of US inflation data

Technical analysis

Failures to cross a three-month-old horizontal hurdle surrounding 1.1485 seem to direct EUR/USD bears towards a 21-DMA level near 1.1340.

- USD/CAD struggles to extend recovery moves from fortnight-long horizontal support.

- Bullish MACD signals keep buyers hopeful to poke the monthly resistance line.

- Convergence of 100-DMA, 50% Fibonacci retracement offers strong support.

USD/CAD buyers flirt with a short-term key hurdle surrounding 1.2700 during Wednesday’s Asian session, following the bounce off a two-week-old horizontal support zone.

A convergence of the 50-DMA and 38.2% Fibonacci retracement (Fibo.) of October-December 2021 upside challenges the USD/CAD pair’s immediate upside around 1.2710.

However, bullish MACD signals and the Loonie pair’s ability to stay beyond 1.2655-50 horizontal area for nearly two weeks keep the buyers hopeful to overcome the immediate hurdle.

Following that, a downward sloping trend line from early January, near 1.2785, will be in focus as a break which will direct USD/CAD bulls towards crossing the 1.2800 threshold.

Meanwhile, a downside break of the 1.2650 support will again highlight the 1.2625-20 support confluence, comprising the 100-DMA and 50% Fibo.

Should the quote’s drop below 1.2620, the mid-January’s swing high near 1.2570 may offer an intermediate halt during the fall targeting the yearly low of 1.2453.

USD/CAD: Daily chart

Trend: Further recovery expected

- The AUD/JPY upside breaks confirm a bullish flag as bulls regain control above the 82.00 mark.

- AUD/JPY Technical Outlook: Despite being upward biased, would need a daily close above the 100-DMA to cement the uptrend.

The AUD/JPY breaks upward, above the 100 and the 200-day moving averages (DMAs), at 82.53 and 82.40, respectively. At the time of writing, the AUD/JPY cross-currency is trading at 82.56.

The market sentiment is upbeat. US equity indices ended in the green, while Asian stock futures point to a higher open. The risk-sensitive AUD was bolstered in the FX complex, while the JPY was the laggard on the Tuesday session, courtesy of the rise in US T-bond yields, with the 10-year yield, at 1.965%.

AUD/JPY Price Forecast: Technical outlook

The AUD/JPY broke a bullish flag to the upside, though the 100-DMA capped the move. However, the long-real body of Tuesday’s price action suggests that the uptrend could accelerate towards fresh daily highs, even opening the door for a challenge of the YTD high.

That said, the AUD/JPY first resistance would be January 20 daily high at 82..97. Breach of the latter would expose a four-month-old downslope trendline around the 83.25-40 range, followed by the psychological 84.00 figure.

Contrarily, failure to reclaim 83.00 could pave the way for further losses in the AUD/JPY pair. The first support would be 82.00, pushing the price below the top-trendline of the bullish flag, viewed as a false breakout. A crackdown of the 82.00 mark would expose January 24 daily low at 80.69, followed by January 28 at 80.36.

Early Wednesday morning in Asia, Reuters came out with the news conveying the passage of intermediate US government funding bill.

“A bipartisan majority of the U.S. House of Representatives on Tuesday voted to extend temporary funding for the federal government through March 11 to avoid agency shutdowns when existing money expires at midnight on Feb. 18,” said the news initially before announcing the final passage.

More to come…

- WTI pares recent losses after a two-day downtrend refreshed weekly bottom.

- Concerns surrounding Abu Dhabi, Russia joined hopes of overcoming virus woes to trigger the rebound in oil prices.

- API Weekly Crude Oil Stock rose dropped below -1.645M prior.

- EIA inventories, risk catalysts will be watched for fresh clues.

WTI crude oil sellers lick their wounds near $88.70 by the end of Tuesday’s settlement, recently bounced off weekly low.

The black gold’s weakness over the last two days could be considered as profit booking moves near the multi-day high, as well as recent trade tussles between the US and China. However, surprise draw in the industry reports of oil stockpile joins escalating fears of Moscow’s attack on Ukraine to underpin the commodity’s latest rebound. On the same line were headlines conveying an explosion in Abu Dhabi and cautious optimism conveyed by US Centers for Disease Control and Prevention (CDC) Director Dr. Rochelle Walensky.

Weekly Crude Oil Stock by the American Petroleum Institute (API) dropped to -2.025M versus -1.645M previous readouts for the week ended on February 04.

Elsewhere, concerns over one or two rocket-fired explosions in Abu Dhabi also helped oil prices to recover before the blast was termed as cylinder-blast by local media.

On the same line were hopes of witnessing easy covid infections by US CDC Director Walensky while extending the mask mandate. “Walensky said she is ‘cautiously optimistic’ COVID-19 cases in the United States will fall below crisis levels, ‘I don't think we're there right now,’” said Reuters.

Furthermore, the US and the UK stay firm to take harsh measures on Russia if it invades Ukraine but Moscow isn’t stepping back. US President Joe Biden will talk to French leader Emmanuel Macron on Wednesday over the issue.

It should be noted that the fears of the Fed’s faster rate hike and cautious mood ahead of the US Consumer Price Index (CPI) also challenged oil prices but firmer equities and gold defended bulls of late.

Moving on, official oil inventory data from the US Energy Information Administration, expected 0.647M versus -1.047M, will be important for the WTI crude oil prices. However, major attention will be given to risk catalysts for fresh impulse.

Technical analysis

WTI crude oil takes a U-turn from a five-week-old ascending trend line, backed by RSI’s pullback from overbought territory, which in turn suggests the oil benchmark’s run-up to regain the $90.00 threshold.

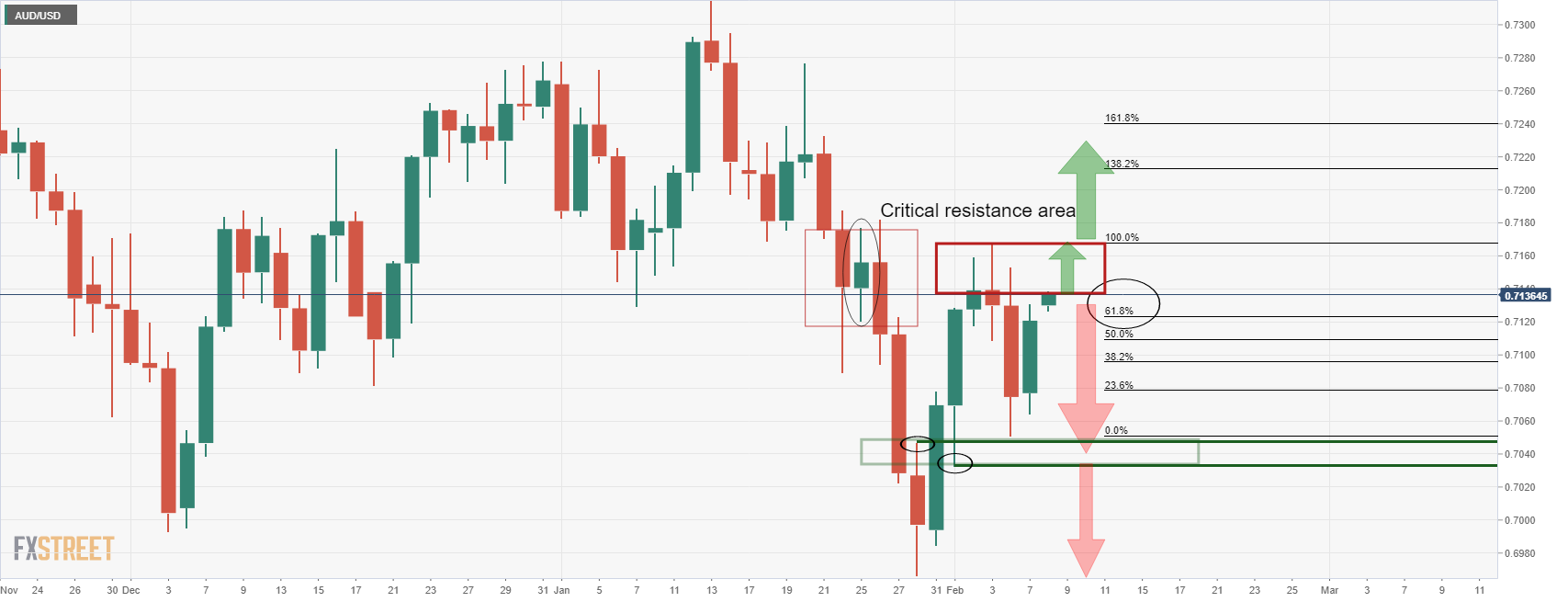

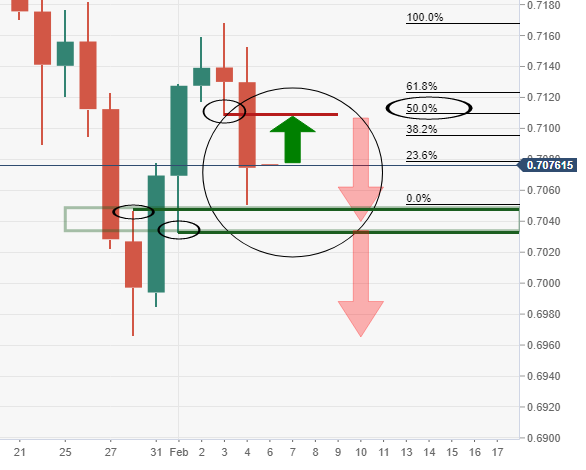

- AUD/USD bulls are challenging the bear's commitments a critical area of resistance.

- The weekly bears are eyeing a break of 0.7105, then 0.7050 for a test to 0.7000.

AUD/USD has continued to chip into the daily resistance ahead of what could now start to shape up to be a more volatile number of days ahead. The US dollar is going to be under scrutiny in the next 72 hours as markets get set for inflation data and start second-guessing the Federal Reserve's moves in Mach. From a technical standpoint, that leaves the downside vulnerable while the price remains below the 0.7180's as follows:

AUD/USD daily chart

The price is fairly bid above the 61.8% ratio but sellers may emerge soon if the bulls fail to take out the critical resistance area near 0.7180. A move lower will likely see 0.7050 in the near future that guards 0.70 the figure as per the weekly chart's downside initial target:

AUD/USD H1 chart

From an hourly perspective, the H1 0.7105 swing lows will be key. Bbelow there, the flood gates could open up for the bears.

- On Tuesday, the GBP/CAD climbs 0.40% as WTI fall below $90.00.

- Central bank divergence between the BoE and BoC bolstered the GBP, as rates increased in the UK.

- GBP/CAD is neutral subject to a breakout either way; caution is warranted.

The GBP/CAD pares some of its Monday’s losses during the North American session, climbing 0.39%. At the time of writing, the GBP/CAD is trading at 1.7208. The British pound recovered some ground vs. the Canadian dollar, courtesy of lower oil prices which weighed on the latter, as US crude oil benchmark WTI slid under the $90.00 per barrel.

Risk-on market mood, keep the British pound in the right, foot alongside some risk-sensitive currencies like the antipodeans and the Canadian dollar. However, the Loonie was hurt by oil prices, while the GBP got a lift-up on the last week, as the Bank of England hiked rates by 25 basis points.

The GBP/CAD narrative lies on the central bank divergence. In the last two meetings, the Bank of England hiked 40 bps and left bank rates at 0.50%. Meanwhile, on its last monetary policy, the Bank of Canada (BoC) chose to keep rates unchanged, even though STIR markets priced in an 80% chance of increasing rates from 0.25% to 0.50%.

Therefore, the GBP/CAD is upward biased, but in the last two days have witnessed a fall from weekly highs, weighed by political issues in the UK that looms the possible resignation of British Prime Minister Boris Johnson.

GBP/CAD Price Forecast: Technical outlook

That said, the GBP/CAD seesawed in the week, between the 1.7130-1.7260 range. On Tuesday, the pair bounced off the weekly lows as the GBP/CAD slide stalled at the 200-day moving average (DMA) at 1.7145.

The GBP/CAD is neutral biased, subject towards a breakout upwards or downwards. However, on the downside lie the 100 and the 50-DMA around 1.7081 and 1.7038, which would be difficult to overcome if crude oil prices keep headed south.

Upwards, the GBP/CAD resistance levels ahead are February 7 daily high at 1.7274, followed by 1.7308. On the flip side, the 1.7200 figure is the first support, which, once broken, would expose the 200-DMA at 1,7145, followed by 1.7100.

- NZD/USD bulls in control and eye significant market structure ahead.

- US dollar could come back into vouge as the US CPI looms.

NZD/USD is heading into the early Asian shift higher by some 0.24% and has travelled from a low of 0.6627 to a high of 0.6653 on the day so far. The bulls are in charge as they take ut a critical level of daily resistance this week with eyes on a run towards the Feb highs near 0.6680 as illustrated below.

Meanwhile, all the action was once again centred on bond markets, with the bellwether US 10yr Treasury bond at yet another post-COVID high, as analysts at ANZ Bank highlighted. The US yields are indeed pushing up key technical levels which, if broken, could send the yields over the key psychological threshold of 2% this week.

The US dollar stands to gain on a correction in the euro as well which is falling under pressure. Sentiment surrounding the European Central Bank was dialled back at the star of the week yet the hawks continue to circle over the Federal Reserve. In the lead up to March's Federal meeting, exceptionally positive US labour data last week, in the form of Nonfarm Payrolls, has put extra focus on this week's Consumer Price Index.

The data could cement expectations on whether the Federal Reserve will raise interest rates by a 25 basis point or a 50 basis point at a March review. Money markets are now pricing in more than a 60% probability of a 50 bps rate hike. As a consequence, the US dollar could be in the running for a significant correction in the forex space with the 96 mark in focus as the DXY index.

However, ''currency markets aren’t really responding to rising bond yields, and one reason for that is they are rising in unison globally. And being a quiet week locally, there is little to differentiate the Kiwi,'' analysts at ANZ Bank explained.

Looking ahead, the markets are going to be looking into the US inflation story on the back of the US Consumer Price Index on Thursday.

''There is genuine nervousness ahead of it, with the street forecasting a pick-up to an incredible 7.3%,'' analysts at ANZ Bank said. ''It all speaks to heavy going, so to speak, and as we noted in our NZD Update yesterday, there are crosscurrents aplenty and volatility looks like it might trump directionality in 2022. Hang on to your hats!''

NZD/USD technical analysis

NZD/USD bulls are looking into the Feb. highs on the daily chart that meet with the weekly 38.2% ratio:

A break there opens the prospects of a run to the M-formation's neckline and through a 50% mean reversion.

- EUR/CHF consolidated in the mid-1.0500s on Tuesday, finding support ahead of the 1.0520 area but unable to test 1.0600 again.

- A more dovish tone to ECB rhetoric this week versus last has taken the sting out of ECB tightening bets.

EUR/CHF consolidated in the mid-1.0500s on Tuesday, with buying interest coming into play upon a dip back towards support in the form of the earlier 2022 highs around 1.0520 mark. Meanwhile, the pair was never able to muster a meaningful push back towards earlier weekly highs at 1.0600 reached in the immediate aftermath of the ECB’s hawkish shift last week. That can likely be explained by the fact that, this week, ECB speakers have sought to strike a more balanced tone in order to push back against what ECB’s Francois Villeroy de Galhau on Tuesday said was an over-the-top market reaction last week.

ECB members, including President Christine Lagarde herself, have sought to emphasise that the bank might be headed towards policy tightening, and that could mean a hike later this year, but would not rush to conclusions. Meanwhile, Lagarde and others were keen to emphasise that while policy normalisation is on the table (i.e. returning rates to “neutral”), policy tightening (raisine rates above “neutral”) most certainly is not. This week’s rhetoric has taken the sting out of market pricing, which was implying the possibility of a rate move as soon as July.

EUR/CHF will be watching a speech from the ECB’s Chief Economist Philip Lane on Thursday, where he will likely echo, or might even take a more dovish line, than Lagarde. Further dovishness may continue to dent the euro and that might mean EUR/CHF continues to pull back from earlier weekly highs and actually tests support at 1.0520.

Longer-term, if the now expected ECB hawkish shift in its inflation forecasts and rate guidance is forthcoming at the March meeting, that might argue for a higher EUR/CHF. That would certainly make the SNB happy. But continued higher inflation in the Eurozone versus low inflation Switzerland means that as the value of each euro is eroded at a faster pace than each Swiss franc, the medium-term direction for the pair may continue to be lower.

- Spot silver has pushed back into the $23.20s as precious metals continue to shrug off the headwind of higher yields.

- As US CPI looms, and may spur fresh Fed tightening bets, silver is trading over 3.0% higher on the week.

Spot silver (XAG/USD) prices pushed convincingly back above the $23.00 level on Tuesday, after attracting buyers amid an earlier session pullback to the 50-Day Moving Average in the $22.80s. At current levels, XAG/USD trades about 0.9% higher on the day in the $23.20s and close to its 21-Day Moving Average, with spot silver prices shrugging off a slightly strong buck and rise in US bond yields. US yields were up by a similar margin across the curve on Tuesday (3-5bps), with the 10-year hitting 1.97% for the first time since August 2019, though not managing a clean break above resistance in the form of Q4 2019 highs in the 1.96% area.

The move higher in nominal yields was in part driven by a rise in real yields that would typically be a negative for non-yielding inflation hedge precious metals like silver. Higher real yields represent 1) a rise in the opportunity cost of holding non-yielding assets and 2) a cheaper alternative form of inflation protection. But the negative correlation between the likes of silver and yields has been weaker as of late, perplexing analysts.

Some have said inflation concerns remain elevated as energy prices continue to surge and amid worries the Fed is “behind the curve”. Others have cited geopolitical concerns as driving safe-haven demand (though certainly not into bonds). Either way, as US Consumer Price Inflation data, which may well push US yields ever higher if it spurs further Fed tightening bets, looms, XAG/USD is trading up over 3.0% higher on the week. That marks a more than 5.5% rebound from last week’s lows at $22.00, which marked a double bottom for the year.

- US inflation data and UK GDP will be key for GBP/USD this week.

- Bears eye the 1.3520 horizontal support that could be the last defence before a test of 1.3490 swing lows.

At 1.3559, GBP/USD is up on the day by 11% and has travelled from a low of 1.3507 to score a high of 1.3564 on the day so far. Nevertheless, the greenback is being eyed for prospects of a bid given the perkiness in US yields and the anticipation of US nfla5ion data this Thursday.

The US dollar stands to gain on a correction in the euro and in continued hawkish sentiment surrounding the Federal Reserve. In the lead up to March's Federal meeting, exceptionally positive US labour data last week, in the form of Nonfarm Payrolls, has put extra focus on this week's Consumer Price Index that has been forecasted at a four-decade high 7.3%.

The data could cement expectations on whether the Federal Reserve will raise interest rates by a 25 basis point or a 50 basis point at a March review. Money markets are now pricing in more than a 60% probability of a 50 bps rate hike. As a consequence, the US dollar could be in the running for a significant correction in the forex space with the 96 mark in focus as the DXY index. This will ultimately weigh on the pound and leave 1.3490 vulnerable in a breakdown of technical structure as illustrated in the technical analysis below.

Meanwhile, however, given the widening interest rate differentials between the pound and other major currencies, such as the euro, GBP bears could be hard pushed to run away with it for the time being. In this regard, this week's UK Gross Domestic Product will be a key event for sterling this Friday.

The data, expected by analysts at TD Securities to contract by 0.8% MoM in December, thus bringing GDP below its pre-COVID level once again, will be the first major event after last week's Bank of England interest rate decision.

While the Bank of England delivered a quarter-point hike last week as widely expected, a split vote came as a surprise, as four of the nine Monetary Policy Committee members wanted a 50 basis points move. This leaves the bulls in good stead for the time being. Money markets are now pricing in another 127 bps of hikes over the remainder of the year.

GBP/USD technical analysis

As the hourly chart illustrates, the bulls are attempting to take on the resistance area but without conviction so far. Should they fail at this juncture, the bears will be encouraged to be involved at a discount and will eye a break of the 1.3520 horizontal support that could be the last defence before a test of 1.3490 swing lows.

- AUD/USD has been ebbing higher but remains capped under 0.7150 and within recent ranges.

- Analysts have cited favourable price action in the base metals space and in global equities as benefitting the Aussie.

- The pair will likely remain fairly subdued, however, ahead of key US CPI data on Thursday.

It’s been a pretty quiet session for AUD/USD, with the pair ebbing higher and remaining support above 0.7100, but unable to test resistance at 0.7150. As things stand, the pair is about 0.2% higher on the day and continues to trade within last Friday’s ranges, though has pared the entirety of last Friday’s post-strong US jobs data drop back to the 0.7050 area.

Analysts have cited favourable price action in the base metals space as benefitting the material export-dependent Aussie, as well as favourable conditions in the global equity space. But any meaningful break, say, above last week’s highs in the 0.7160s, will likely have to wait until after Thursday’s US inflation data, where the YoY rate of Consumer Price Inflation is seen rising 7.3% YoY.

FX strategists have said that even an in line with expectations reading could bolster Fed tightening bets, underpinning the US dollar. That suggests the more likely direction for AUD/USD may instead be a break back under 0.7100 and toward’s last Friday’s lows just above 0.7050. Chatter about the potential timeline of RBA tightening also remains a key theme for AUD/USD, after former RBA board member John Edwards said on Tuesday that he thinks the bank might hike four times this year starting in August.

The RBA is yet to indicate plans to tighten that soon. Analysts at Westpac say they “stick to the view that the A$ should remain capped by the $0.7140/70 level given the very different stance that the RBA is maintaining versus a wide range of other central banks”. However, they continue, “we would look to use weakness towards $0.70 as an opportunity to buy for strength later in the year” he added, noting strong prices for Australia's major commodities.

What you need to know on Wednesday, February 9:

Major pairs continued lacking certain directional strength and held within limited intraday ranges on Tuesday. The greenback found some strength in soaring government bond yields, as that on the US 10-year Treasury note reached 1.97%. However, yields’ strength was barely enough to prevent the dollar from plummeting.

The EUR/USD pair briefly pierced the 1.1400 level but ended the day in the 1.1410 price zone. Comments from the European Central Bank member Francois Villeroy put some pressure on the shared currency by the end of the day, as he noted that the market may have overreacted to President Christine Lagarde’s words last week.

UK Prime Minister Boris Johnson reshuffled its cabinet. Jacob Rees-Mogg has become the new Brexit Minister, while Mark Spencer replaced him as leader of the Commons. Chris Heaton-Harris becomes the new chief whip, while Paymaster General Michael Ellis would take on the additional role of minister for the Cabinet Office. The decision comes in the middle of the lockdown parties’ scandal, which menaces Johnson’s leadership. GBP/USD trades around 1.3550.

The AUD/USD pair is up for a second consecutive day trading in the 0.7140 region. The USD/CAD pair edged higher and currently hovers around 1.2700, as lower oil prices undermined demand for the Canadian dollar. The greenback posted modest gains against safe-haven CHF and JPY.

Gold surged to a fresh two-week high of $1,828.36 a troy ounce, holding nearby at the end of the day. Meanwhile, WTI trades at $89.80 a barrel.

Market players keep waiting for January US inflation figures to be out on Thursday.

Top 3 Price Prediction Bitcoin, Ethereum, XRP: Crypto profit-taking starts before new uptrend

Like this article? Help us with some feedback by answering this survey:

- EUR/USD bears stay in control and eyes are on a significant retracement.

- The daily time frame's 38.2% ratio is located at 1.1345.

As per the prior analysis, EUR/USD: Bulls firming, eyes on M-formation neckline before 1.1410 break, the price remains pressured with a bias to the downside from both the hourly and daily perspectives.

EUR/USD prior analysis, H1 chart

As illustrated, from an hourly time frame basis, the price was expected to remain under pressure following the bull's last attempts into resistance.

EUR/USD live market

As can be seen, the price has respected the forecasted trajectory below resistance and would be expected to continue lower in the coming week. On a daily basis, the 38.2% Fibonacci retracement levels have a confluence with the prior structure on a closing basis as follows:

- The USD/CAD pares Monday’s losses as WTI plunges below $90.00.

- The US 10-year Treasury yield reached a new high at 1.97%.

- USD/CAD Technical Outlook: A daily close above the 50-DMA would expose the YTD high at 1.2813.

In the New York session, the USD/CAD trim Monday’s losses and reclaims the 1.2700 figure as the Canadian dollar weakens, as oil prices fall, a headwind for the Loonie. At the time of writing, the USD/CAD is trading at 1.2702.

Falling oil prices weigh on the CAD

On Tuesday’s, Western Texas Intermediate (WTI), the US crude oil benchmark, falls more than 2%, as it moves beneath $90.00 per barrel. Alongside oil factors, the Canadian Trade Balance for December printed a deficit of C$0.14 billion when expectations were of a surplus of C$2.5 billion, hurt the prospects of the Loonie. Additionally, US T-bond yields skyrocketing in the session, led by the 10-year benchmark note reaching a daily high at 1.97%, boosted the greenback.

Fundamentally speaking, the narrative of the central banks’ worldwide tightening conditions keeps markets trendless. Money markets futures expectations of the Federal Reserve, analysts estimate five hikes to the Federal Funds Rates (FFR) by the end of 2022.

In the meantime, USD/CAD traders get ready for Thursday’s US inflation figures. The Consumer Price Index (CPI) for January is expected at 7.3% while excluding volatile items like energy and food called Core CPI, which is foreseen at 5.5%.

USD/CAD Price Forecast: Technical outlook

The USD/CAD is upward biased but faces resistance at the 50-day moving average (DMA) at 1.2708. The pair consolidated around the 1.2650-1.2760 area, amid the lack of catalyst as market participants assess economic conditions.

However, once USD bulls reclaimed 1.2700, that would open the door for a test of the 50-DMA. A breach of the latter would expose the February 4 daily high at 1.2786. An upward break would send the USD/CAD higher towards the January 6 high at 1.2813.

- EUR/JPY continued to trade within recent intra-day ranges on Tuesday, remaining support above January’s highs in the 131.60 area.

- The euro saw momentary weakness as ECB’s Villeroy pushed back against the post-ECB meeting market reaction.

- Ahead, the pair will be focus on US inflation data on Thursday for any read across to FX markets.

EUR/JPY has continued to trade within recent ranges on Tuesday, undulating between the 131.50-132.00 levels, meaning the price action has remained well contained within Monday’s 131.20-132.20ish ranges. FX markets continue to trade in a broadly subdued manner, with EUR/JPY happy to consolidate recent gains after its big post-hawkish ECB push to multi-month highs in the latter part of last week. For now, support in the form of the early January high at 131.60 continues to prove an attractive long entry point for intra-day speculators.

Recent comments from ECB governing council member and Bank of France head Francois Villeroy de Galhau, who said that last week’s post-ECB rate decision market reaction may have been too strong, resulted in momentary euro weakness. His comments come after a more measured tone on the prospect for monetary policy tightening from ECB President Christine Lagarde and other ECB policymakers this week, undermining the case for further short-term euro upside.

Nonetheless, as Eurozone yields continue to trade with an upside bias in tandem with their US counterparts and broader risk appetite remains resilient in the run-up to Thursday’s US consumer inflation report, EUR/JPY may remain supported in the short-term. Should the upcoming US inflation report surprise to the upside, subsequent Fed tightening fears could weigh on market sentiment and give the yen a boost, which could set EUR/JPY back later this week.

European Central Bank governing council member and Bank of France head Francois Villeroy de Galhau said on Tuesday that the market reaction to last week's ECB meeting may have been too strong.

Market Reaction

This may have been a reference to money market pricing that jumped forward to pricing a possibility of an ECB hike as soon as July, rather than a reference to currency markets. Nonetheless, the euro did see some momentary weakness, with EUR/USD dipping back towards session lows in the 1.1400 area to probe session lows.

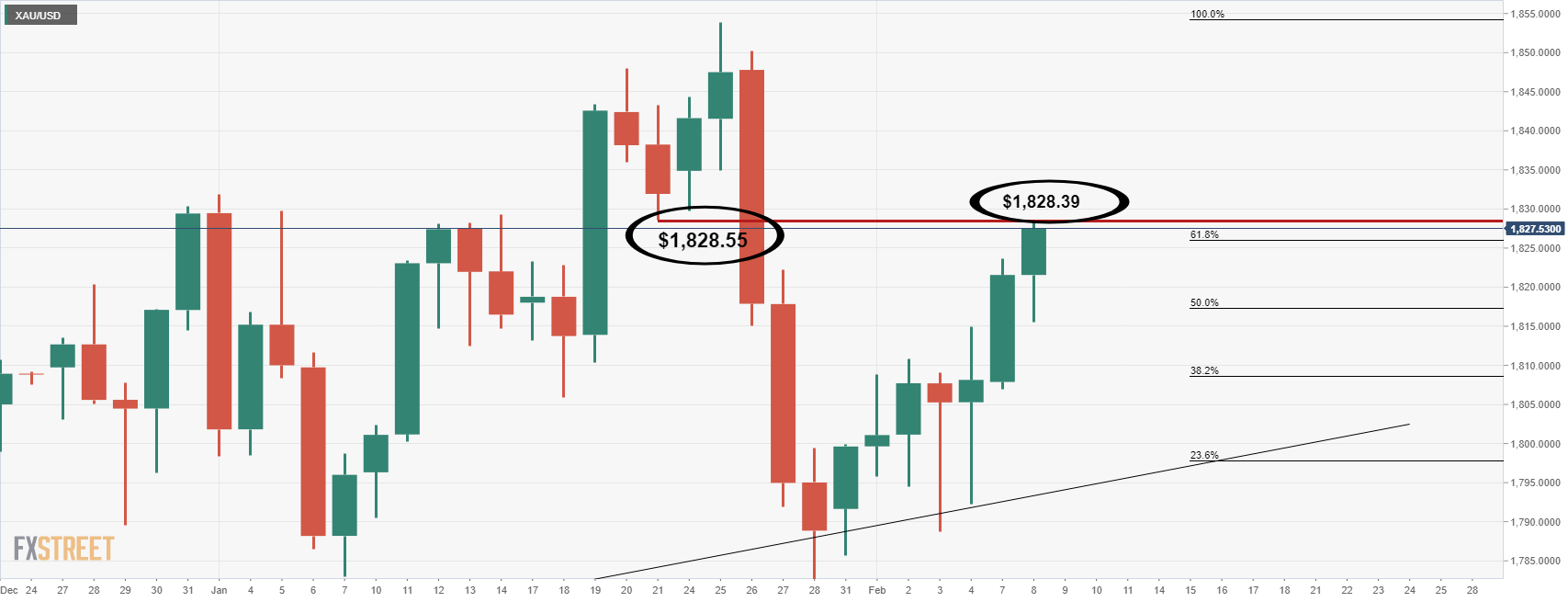

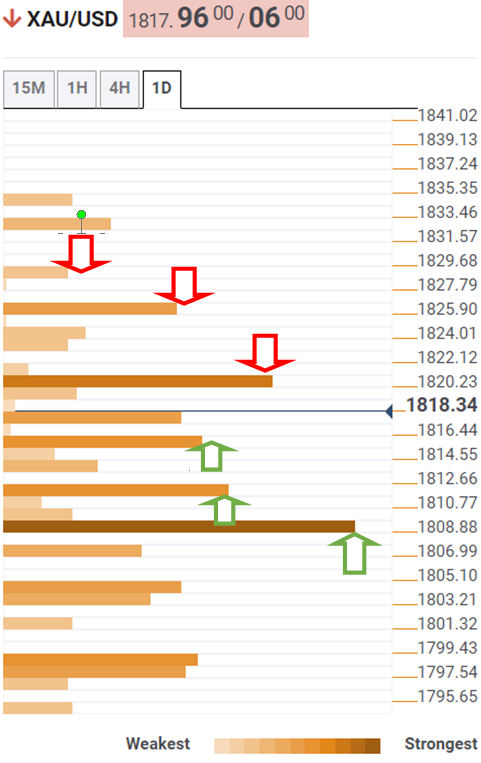

- For gold's next move, all eyes turn to the US dollar and CPI later this week.

- CTA trend followers could add to outflows should prices close below $1800/oz.

At $1,827, gold, XAU/USD is higher on the day by 0.40%. The price has moved from a low of $1,815.49 to reach a high of $1,828.40 so far. Overall, it's a slow start to the week and there is a lack of volatility on the forex space which means the US dollar is stuck around opening levels for the week as traders await key inflation data on Thursday.

However, benchmark US 10-year Treasury yields are pushing up key technical levels which, if broken, could send the yields over the key psychological threshold of 2% this week. This is supporting the greenback on Tuesday. DXY is over 0.2% higher, which is an index that measures the US dollar vs. a basket of rival major currencies. The index has ranged between 95.398 and 95.75.

Looking ahead, with gold at a critical juncture, as illustrated on the charts below, analysts at TD Securities explain, that at first glance, 'the set-up is in gold ripe for another position squeeze, as several participants including TD Securities have established tactical short gold positions.

They explained that this is following the decisively hawkish Fed meeting, only to find substantial volume on the bid keeping prices from breaking below their bull-market-era trendline support. ''This time'', they argue, however, ''the bar is high for a substantial squeeze, suggesting macro headwinds will ultimately weigh on gold.''

''. It remains to be seen whether central bank purchases might be playing a substantial role in keeping gold prices from breaking lower, but shorts are unlikely to feel much pain as the data continues to point to little speculative interest for the yellow metal. Conversely, CTA trend followers could add to outflows should prices close below $1800/oz.''

Gold technical analysis

As per the prior analysis, and this week's, Gold, Chart of the Week: Bulls take on the 38.2% Fibo, now eye the 61.8% golden ratio, the price has finally moved on the 61.8% ratio as follows:

Gold, prior analysis

''While there are no direct confluences at a specific price target between the neckline of the M-formation and the 61.8% ratio, the area between the two mile-stones near $1,830 will be expected to offer firm resistance.''

Gold live market

As illustrated, the bulls have moved in on the 61.8% ratio. What now?

In the chart below, we see that the price has reached the neckline of the M-formation to the rounded down $1,828. This matters because this is an area of liquidity that could lead to supply entering the market which would typically cap the price. This leaves the focus on the downside which leaves the $1,811 vulnerable:

The W-formation's neckline aligns, albeit not perfectly to the US dollar, with a 50% mean reversion of the prior bullish impulse, so this is an ''area'' between $1,811 and $1,808 that the bears could be looking to target.

With all that being said, there is every possibility that the bulls will stay in control which exposes $1,850 on consecutive daily closes above the current highs. On the other hand, the bears will be monitoring for topping formations on both the daily and lower times frame charts at this juncture.

- GBP/JPY bulls break above 156.50, top of the 154.30-156.50 range.

- The market sentiment is upbeat, but the FX market is mixed.

- GBP/JPY Technical Outlook: A daily close above 156.50 would add upward pressure on the pair.

The GBP/JPY eyes to break the 154.30-156.50 range as risk-sentiment improves during the New York session. At the time of writing, the GBP/JPY is trading at 156.58.

In the FX complex, the market mood is mixed. Risk-sensitive currencies rise, led by the AUD, NZD, and GBP, while the safe-haven CHF and USD advance. In the case of the JPY is getting hammered throughout the session.

GBP/JPY Price Forecast: Technical outlook

The GBP/JPY broke above the top of the trading range during the session, but it would need a daily close above to cement its bullish case further. The daily moving averages reside well beneath the spot price, suggesting upward bias.

On Monday’s article, I noted that “GBP/JPY traders may wait on the sidelines, expecting a breakout of the 154.30-156.50 trading range.”

That said, the GBP/JPY first resistance would be January 18 daily high at 156.90. Once the level gives way, the next resistance would be the January 12 daily high at 157.70, followed by the November 2021 swing highs at 158.22.

On the flip side, the GBP/JPY first support would be 156.00. A breach of the latter would expose the February 7 daily low at 155.13, followed by February 3 155.04.

- S&P 500 rose back above 4500 on Tuesday but remains within recent ranges ahead of US CPI later this week.

- Any upside surprise could add further momentum to the recent rise in yields, potentially pressuring big tech/growth names.

The S&P 500 rose back above the 4500 level on Tuesday, up about 0.5% versus Monday’s close in the 4480s, though the index has remained well within the 4470-4540ish ranges that have prevailed since last Thursday. Market commentators cited underwhelming Q4 earnings results from Pfizer, whose year ahead forecast for vaccine and anti-viral pill sales disappointed, and pre-US Consumer Price Inflation data “jitters” as keeping equities locked within recent ranges.

Traders also noted further downside in Meta Platforms (Facebook) as weighing on broad market sentiment, with FB shares down another 1.0% to take losses since last week’s earnings to more than 30%. Billionaire investor Peter Thiel stepped down from the company's board, news which traders said weighed on the share price.

The Nasdaq 100 has seen similar trading conditions, undulating between the 14.5-14.8K levels for a fourth consecutive session. On Tuesday, the index trades about 0.9% higher around 14.7K. The Dow managed to push marginally above its last Friday/Monday ranges and is eyeing a retest of the 35.5K level, up about 0.8% on the day. The CBOE S&P 500 Volatility Index fell below the 22.00 level for the first time since last Wednesday.

Calm trading conditions reflect the fact that investors are nervous to place any big bets ahead of Thursday’s US inflation release, which has been billed as this week’s main event. The headline YoY rate should surpass 7.0% and the risk is that markets interpret this as increasing the likelihood that the Fed hikes rates by 50bps in March and embarks on more aggressive tightening throughout the duration of 2022.

Further Fed tightening bets could add further momentum to the move higher in long-term US bond yields, with the 10-year already nearing 2.0% for the first time since August 2019. This could weigh heavily on tech/growth names, much of whose valuation depends on expectations for future earnings growth rather than present earnings, thus leaving valuations vulnerable to a rise in opportunity cost (for which yields are a proxy).

Beyond March, analysts at Wells Fargo expect the European Central Bank (ECB) to start raising its Deposit Rate shortly after it completes its net bond purchases. They see an initial 25 bps Deposit Rate hike in December 2022 and another 25 bps hike in March 2023. They consider the divergence between the ECB and the Federal Reserve to weigh on EUR/USD over the medium-term.

Key Quotes:

“Beyond March (…), we expect the European Central Bank will take the opportunity to start moving its Deposit Rate away from negative territory by late 2022. Specifically, we now forecast an initial 25 bps Deposit Rate increase to -0.25% at the December 2022 announcement, with another 25 bps hike to 0.00% to follow at the March 2023 announcement. Beyond March next year, we expect the Eurozone economic environment will be one of moderate growth and slowing core CPI inflation, but perhaps still above 2% at that time. Accordingly, we expect the ECB will continue raising interest rates beyond March 2023, though at a reduced pace. Specifically, we also forecast 10 bps Deposit rate increases at each of the June 2023, September 2023 and December 2023 meetings, which would see the Deposit rate end next year at +0.30%.”

“Although we believe the ECB will adjust its interest rate stance more rapidly than we previously forecast, it will lag behind the pace of rate hikes from the Federal Reserve, and also fall slightly short of the pace of ECB rate hikes currently priced in by market participants. Accordingly, we still view this more timely path for ECB interest rate increases as consistent with moderate weakness in the EUR/USD exchange rate over the medium-term.”

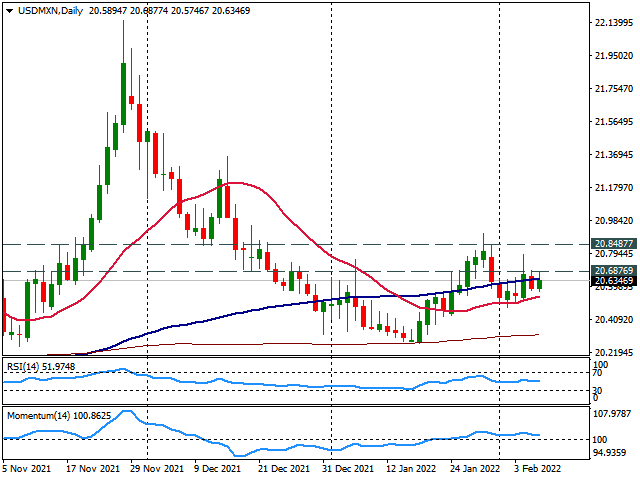

- USD/MXN found support above 20.50 and also at the 20-day SMA.

- Bias skewed to the upside, limited at the moment by 20.70.

- Mexican peso to strengthen with a break under 20.50.

The USD/MXN is rising on Tuesday as it hovers around 20.60. During the last sessions, it has been consolidating after being unable to hold above 20.70.

The bias in the short-term term is biased to the upside but gains seem limited while under 20.70. A close above could open the doors to 20.85/90, the next resistance and last protection to 21.00.

The bullish tone will be negated with a decline under the 20.50/55 support area that contains a horizontal line and also the 20-day simple moving average. A break lower would target 20.40. The next support is seen at 20.35 and the 200-day moving average at 20.30.

USD/MXN daily chart

- The USD/JPY advances sharply during the day some 0.45%.

- A mixed market mood keeps investors uneasy amid global central banks tightening conditions.

- USD/JPY is upward biased as USD bulls get ready to test a 24-year-old downslope trendline.

Tuesday’s price action of USD/JPY appears to be breaking a one-month-old downslope resistance trendline, drawn from January highs, which rejected Monday’s upward move, sending the pair towards its daily low under 115.00. At the time of writing, the USD/JPY is trading at 115.59.

The financial market’s mood seesaws as investors move in turbulent waters. Global central bank tightening monetary policy conditions and rising global bond yields keep market participants nervous.

US Treasury yields keep heading north as the New York session progresses. The US 10-year Treasury yield rises sharply and closes to the 1.97% threshold, weighing on the USD/JPY pair, which is closely correlated to it.

Analysts at Société Générale noted that “if we are going to see 10-year Note yields break 2% and the market price in a higher terminal Fed Funds rate (which seems highly likely) then USD/JPY 116 is going to break again and a move towards 120 will follow.”

USD/JPY Price Forecast: Technical outlook

The USD/JPT daily chart depicts the pair as upward biased. The daily moving averages (DMAs) reside well below the spot price, while the Relative Strength Index R(RSI=

The upward break mentioned in the first paragraph, confirmed by a daily close in those levels, would open the door for a test of the 2022 YTD high at 116.35. Breach of the latter could pave the way for further gains and expose a 24-year-old downslope trendline drawn from August 1998, swing highs which pass around 117.00. An upward break would expose the January 2017 swing high at 118.61.

- GBP/USD continues to trade in subdued fashion in fitting with the broader FX market feel in the 1.3550 area.

- A key fib retracement in the 1.3550s is capping the price action whilst 1.3500 is acting as support.

- FX markets are in wait-and-see mode ahead of this week’s US CPI report.

In fitting with the broadly subdued start to the week in global FX markets as traders await key US Consumer Price Inflation data that could influence Fed tightening expectations on Thursday, GBP/USD has remained contained in the 1.3550 area. Indeed, as was the case on Monday, the presence of the 50% Fibonacci retracement back from the 2022 high at 1.3750 to the 2022 low at 1.3350 in the 1.3550s is again capping the price action. Meanwhile, dips back towards 1.3500 continue to attract buying interest.

Last week’s hawkish BoE surprise, where four out of nine rate-setters voted for a larger 50bps hike (while the majority voted for a 25bps hike) has not given sterling lasting support. GBP/USD was unable to hold above 1.3600 in wake of the BoE’s meeting before then being knocked back into the low 1.3500s by a strong US labour market report that pumped Fed tightening bets.

Focus on the impending cost of living crisis in the UK is likely the main factor keeping sterling capped. Taxes and energy prices are set to rise in Q2 all while inflation continues to eat away at incomes, undermining expectations for how high the BoE’s terminal rate will eventually be. Bank of America said on Tuesday that its measure of UK household confidence in their personal finances fell to its lowest since the bank began its survey in 2017.

The failure to rally post-last week’s hawkish BoE surprise suggests downside risks for GBP/USD going forward, if the US dollar can recover from recent positioning-related weakness. A break below support at 1.3500 could open the door to a drop back towards 1.3400 and the next area of key support in the mid-1.3300s in the form of last month’s lows.

The 10-year US Treasury bond yields are about to break above 2.00%. In this case, the USD/JPY pair is set trend higher towards 116.00 ahead of 120.00 over the coming weeks, economists at Société Générale report.

The yen seems bound to remain cheap and get cheaper

“If we are going to see 10-year Note yields break 2% and the market price in a higher terminal Fed Funds rate (which seems highly likely) then USD/JPY 116 is going to break again and a move towards 120 will follow.”

“For now, and all the more so given the price of oil and other commodities, the yen seems bound to remain cheap and get cheaper. USD/JPY can trundle to 120 and interruptions on days of higher volatility are likely to be temporary.”

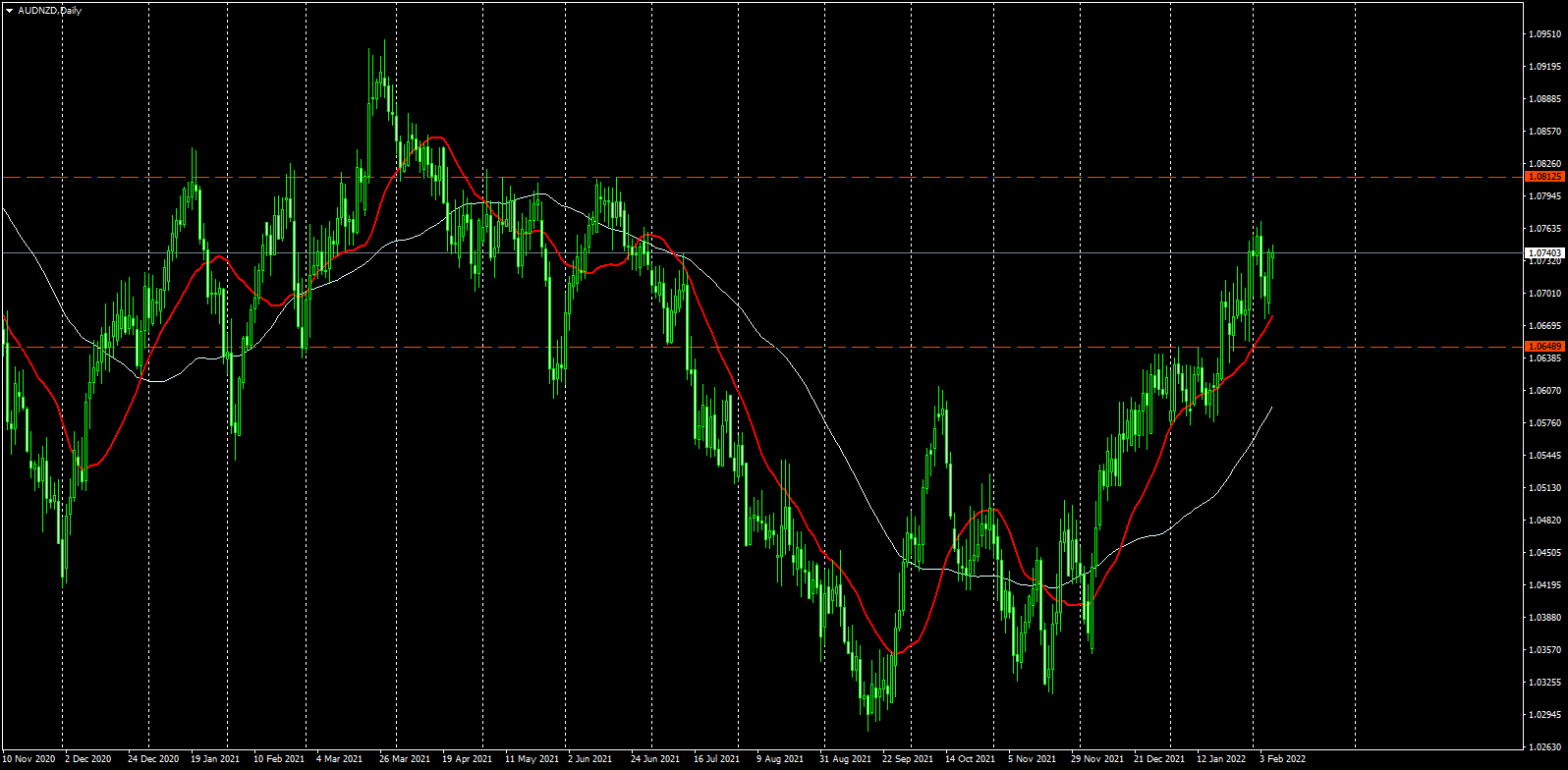

- The aussie holds a bullish bias virus the kiwi.

- The next target of AUD/NZD is seen at 1.0810 (May and June highs).

- Slide under 1.0650 to weaken the cross.

The AUD/NZD is rising modestly on Tuesday, as it continues to approach last week highs. The cross rebounded at the 20-day simple moving average an also before the 1.0650 critical support.

The main trend continues to point to the upside and no clear signs of a correction or a consolidation are seen at the moment. A firm break above 1.0750 would continue to keep the aussie on track for its next target at 1.0810. A break above 1.0820 on a daily close basis should point to more gains. If the cross fails to break soon above 1.0750, a correction seems likely.

On the flip side the firs support stands at the 20-day SMA at 1.0675. Below comes the 1.0645/50 zone, a close below should put the aussie under pressure and favor a decline under 1.0600. The next support stands a t 1.0570.

AUD/NZD daily chart

The tug of war between the Federal Reserve (Fed) and the European Central Bank (ECB) will be decisive for EUR/USD this year. Economists continue to expect renewed dollar strength in 202, but also expecting a repricing of the euro towards the end of the year and more sustained euro dominance next year.

The Fed to start on a quarterly hike path

“The Fed is set to hike rates four times this year by 25bp, starting in March, followed by further four hikes in 2023. A decision to allow the balance sheet to contract will be taken during the summer.”

“We expect the ECB to decide in March to stop net bond purchases around the end of August. 25bp rate hikes will follow in December 2022, March 2023 and September 2023.”

“EUR/USD is set to bottom at 1.10 later this year and climb to 1.18 by the end of next year.”

“Long bond yields are expected to climb further, but the curve to flatten from current levels by the end of the forecast horizon.”

- NZD/USD is consolidating under 0.6650 and well within recent intra-day ranges ahead of key US CPI data.

- A firmer-than-expected reading might trigger a further build-up of hawkish Fed bets, analysts have warned.

- In this case, NZD/USD bears would be eyeing tests of support at 0.6590 and 0.6530.

NZD/USD has continued its pattern of stabilisation within recent ranges on Tuesday, trading for the most part just under 0.6650 and well within last Friday’s 0.6670-0.6590ish ranges. Broader macro risk appetite has been fairly directionless since last Friday, making for subdued FX market trade, with the focus firmly on incoming US Consumer Price Inflation (CPI) figures on Thursday. A firmer-than-expected reading might trigger a further build-up of hawkish Fed bets, analysts have warned, which could weigh on crosses like NZD/USD.

Support in the form of last Friday’s post-strong US job report lows just under 0.6600 and last month’s multi-month lows in the 0.6530s are the most obvious levels of support being watched by the bears. In the scenario of a hot US CPI report, these may well be tested, but ahead of then, trading conditions are likely to remain subdued/rangebound. The kiwi is unlikely to get much domestic impetus, though Wednesday's quarterly inflation expectations release is worth watching in the context of an RBNZ that is expected to continue hiking rates aggressively this year.

To the upside, notable levels of resistance in the 0.6680s and then at 0.6700 are worth keeping an eye on. Even if Wednesday’s inflation data does boost hawkish RBNZ bets, it remains far to soon to say that NZD/USD has snapped its negative run over the past few months. While the pair is up more than 1.5% from the late January lows on US dollar profit-taking, it continues to trade about 8% below its Q4 2021 highs.

- During the North American session, silver grinds higher 0.54%.

- A mixed market mood keeps the greenback on the right foot, though it fails to weigh on the precious metals complex.

- XAG/USD daily close above $23.00 keeps silver neutral-bullish biased, as XAG buyers get ready to challenge the 100-DMA.

After Monday’s 2% rally, the white metal consolidated, though clinging to $23.00. At the time of writing, XAG/USD is trading at $23.12. So far in the week, silver is up close to 2%, but the upward move stalled ahead of challenging the 100-day moving average (DMA) at $23.19.

Overall, US dollar strength surrounds the financial markets, as shown by US Treasury yields. The US T-bond 10-year benchmark note is at 1.96%, rises four and a half basis points, a headwind for the non-yielding metal. Meanwhile, US 10-year TIPS yield, a proxy for real yields, climbs four basis points, up to -0.448%, weighing on the prices of precious metals.

In the meantime, the US Dollar Index, a gauge of the greenback’s value against a basket of peers, rises 0.22%, up at 95.61.

The lack of catalyst keeps investors focused on tightening monetary policy and inflation in the US central bank. On Thursday, the Labor Department will reveal the Consumer Price Index (CPI) for January, widely expected to rise to 7.3%, leaving December’s 7% behind. Excluding volatile items, like food and energy, the so-called Core-CPI is foreseen at 5.9%, both readings on an annual basis.

The US economic docket featured the Trade Balance for December, which came at $-80.7 B, better than the $-83 billion estimated. Exports increased $4 B more than the $224.7 B in December, while Imports also grew to $308.9 B, from $304 B.

XAG/USD Price Forecast: Technical outlook

On Monday, XAG/USD broke above the 50-day moving average (DMA), but it faced strong resistance at the $23.00 figure. Nevertheless, the rally broke four resistance levels on its way up, as XAG bulls get ready for a challenge of the 100-DMA at $23.19.

Silver is neutral-bullish biased. A breach of the 100-DMA could send the non-yielding metal upwards. The first resistance would be January 3 high at $23.40, followed by a tenth-month-old downslope trendline, around the $24.00-$24.20 range.

- USD/TRY extends the advance to the 13.70 region.

- News cited a positive meeting between finmin Nebati and investors.

- Turkey 10y reference bond yields hover around 21.50%.

The Turkish lira depreciates further and pushes USD/TRY to fresh multi-session peaks near 13.70 on Tuesday.

USD/TRY maintains its consolidation well in place

USD/TRY challenges the upper end of the range prevailing since mid-January around 13.70 amidst the firmer note in the US dollar and the persistent decline in yields of the Turkey 10y bond.

On the latter, yields navigate the area of monthly lows around 21.50% after climbing as high as the 22.40% zone at the beginning of February.

The lira, in the meantime, seems to have exacerbated the decline after inflation figures rose to 48.69% in the year to January, the highest level in the last 20 years.

On another front, the Turkish Current Account deficit is seen at around $15B in 2021 according to a Reuters poll released on Monday. The result, however, is lower than the government’s $21B estimated.

In the meantime, the meeting between finmin N.Nebati and investors in London appears to have yielded a positive outcome. At the meeting, the unorthodox Turkish economic policy and a planned bond sale took centre stage amidst recent data suggesting that Turkey’s FX reserves rose by $5-6B during last week. Nebati also suggested that the rise in inflation in the country follows reasons that foreigners cannot understand culturally. (wait… what?)

What to look for around TRY

The pair keeps the multi-session consolidative theme well in place, always within the 13.00-14.00 range. While skepticism keeps running high over the effectiveness of the ongoing scheme to promote the de-dollarization of the economy – thus supporting the inflows into the lira - the reluctance of the CBRT to change the (collision?) course and the omnipresent political pressure to favour lower interest rates in the current context of rampant inflation and (very) negative real interest rates are a sure recipe to keep the domestic currency under pressure for the time being.

Key events in Turkey this week: Unemployment Rate (Thursday) - End Year CPI Forecast, Current Account, Industrial Production, Retail Sales (Friday).

Eminent issues on the back boiler: Progress (or lack of it) of the government’s new scheme oriented to support the lira via protected time deposits. Constant government pressure on the CBRT vs. bank’s credibility/independence. Bouts of geopolitical concerns. Much-needed structural reforms. Growth outlook vs. progress of the coronavirus pandemic. Earlier Presidential/Parliamentary elections?

USD/TRY key levels

So far, the pair is advancing 0.44% at 13.6296 and a drop below 13.3226 (55-day SMA) would expose 13.2327 (monthly low Feb.1) and finally 12.7523 (2022 low Jan.3). On the other hand, the next up barrier lines up at 13.9319 (2022 high Jan.10) followed by 18.2582 (all-time high Dec.20) and then 19.0000 (round level).

GBP/USD has managed to bounce off the 1.3500/10 area again to a test of the mid-figure zone that is somewhat limiting upside. A berak above here would clear the path to enjoy further gains, econmists at Scotiabank report.

Support after 1.3490/00 is around 1.3475

“Cable’s rejection of the 1.35 area over the past three days points to a resumption of its gains since late-Jan, but it may have to break more firmly over 1.3550 to negate the downward pressure of the past few days.”

“After the mid-figure zone, ~1.3585 is resistance followed by the 1.36 area and then 1.3615/20.”

“Support after 1.3490/00 is ~1.3475 and the 1.3450 zone.”

EUR/USD has tested the 1.14 level as rate speculation cools. Economists at Scotiabank expect the pair to plummet towards 1.10 once it becomes clearer that the European Central Bank will only marginally hike in 2022.

Break under 1.14 to open up the 1.13 level

“We think the ECB is set to disappoint markets looking for 50bps in hikes this year, and we see EUR gains reversing toward 1.10 once it becomes clearer that the bank will only marginally hike in 2022 (if at all).”

“A clearer EUR decline under 1.14 would open the door to a sharp reversal of its Thursday jump that would set 1.13 in its sights. Intermediate support is ~1.1350 and ~1.1330.”

- WTI dipped on Tuesday amid profit-taking though has recovered from session lows near $89.00 back above the $90.00 level.

- Analysts cited chatter about a potential US/Iran deal on nuclear and French President Macron’s Moscow visit as weighing on prices.

Front-month WTI futures pulled back from close to seven-year highs on Tuesday, at one point dropping as low as the $89.00 per barrel mark, but subsequently recovering back to the north of the $90.00 handle. At current levels, WTI still trades lower by about $1.50 on the session, with traders citing profit-taking ahead of the resumption of indirect US/Iran talks regarding a potential return to the 2015 nuclear pact. Chatter has been building in recent days about what a deal might mean for oil markets.

A return to the old nuclear pact would see US sanctions on Iranian oil exports eased, allowing the country to release a glut of oil stores and increase exports by as much as 1M barrels per day (about 1% of global daily demand). But analysts caution oil traders not to get ahead of themselves in forecasting a breakthrough in talks, which have not yielded anything so far despite eight rounds of negotiations since April 2021.

Another factor weighing on oil markets, market analysts said on Tuesday, is modest dialing down of West/Russia tensions following French President Emmanuel Macron’s visit to Moscow on Monday. The French President said his meeting helped prevent further escalation of tensions, though no broader deal to end the Russia/Ukraine crisis was reached (as expected).

Ahead, oil traders will be keeping one eye on weekly US oil inventory figures, with the private API numbers out later on Tuesday ahead of the official US government figures on Wednesday. Analysts are estimating that inventories rose by 700K barrels in the week ending last Friday, a week when the US was hit by a strong winter storm.

- USD/CHF witnessed two-way price moves on Tuesday before stabilizing in the neutral territory.

- Elevated US bond yields acted as a tailwind for the USD and helped limit any meaningful slide.

- Signs of stability in the equity markets undermined the safe-haven CHF and extended support.

The USD/CHF pair seesawed between tepid gains/minor losses through the early North American session and was last seen trading in the neutral territory, just below mid-0.9200s.

Having climbed to a one-week high, the USD/CHF pair witnessed some intraday selling and touched a daily low, around the 0.9225 area during the latter part of the European session. However, a combination of factors acted as a tailwind and helped limit the downside. Signs of stability in the equity markets undermined the safe-haven Swiss franc and extended some support amid modest US dollar strength.

The greenback drew some support from a fresh leg up in the US Treasury bond yields, bolstered by the prospects for a faster policy tightening by the Fed. In fact, the markets have been pricing in the possibility of a 50 bps rate hike at the March FOMC meeting. This, in turn, pushed the yield on the benchmark 10-year US government bond back closer to the 2% threshold and benefitted the greenback.

That said, the USD/CHF pair, so far, has struggled to gain any meaningful traction as investors seemed reluctant to place aggressive bets ahead of Thursday's release of the US consumer inflation figures. The latest US CPI report could play a key role in determining the Fed's near-term policy outlook, which, in turn, will drive the USD demand and provide a fresh directional impetus to the USD/CHF pair.

In the meantime, the US bond yields will continue to influence the USD price dynamics and provide some impetus to the USD/CHF pair. Apart from this, traders will take cues from the broader market risk sentiment to grab some short-term opportunities amid absent relevant market moving economic releases from the US.

Technical levels to watch

The Federal Reserve (Fed) is hawkish and preparing to deploy monetary tightening tools through higher rates and balance sheet roll-off. This leaves scope for further gains in USD, economists at Citibank report.

More room for USD to gain

“We expect at least 4 Fed hikes in 2022 and 3 in 2023 with QT likely to begin in July 2022.”

“The bottom line is that a Fed which is removing liquidity versus an ECB/BoJ which are still adding liquidity is likely to keep USD elevated medium-term.”

EUR/USD has shied away from testing the 1.1485 area. Economists at Rabobank expect the pair to trade below this level but the shared currency could find support from the European Central Bank (ECB) hawkish tilt.

EUR/USD has the potential to end the year at a more robust level

“In the near-term, we see risk that EUR/USD continues to shy away from breaking about the 1.1485 area with the USD finding support from US inflationary fears.”

“The ECB’s tilt will have awakened EUR bulls and strengthened the view that EUR/USD has the potential to end the year at a more robust level.”

- Canada posted a surprise trade deficit of C$ 0.14B in December versus forecasts for a healthy C$ 2.5B surplus.

- The loonie did not see any reaction to the latest not as good as expected Canadian trade figures.

Canada posted a surprise trade deficit of C$ 0.14B in December against expectations for a trade surplus of C$ 2.5B, data from Statistics Canada showed on Tuesday. That marked a sharp decline from November's C$ 2.47B trade surplus. The surprise deficit was driven by a small decline in monthly exports to C$ 57.61B from C$ 58.15B the month prior, while monthly imports jumped to C$57.75B from C$55.68B the month prior.

Market Reaction

The loonie did not see any reaction to the latest not as good as expected Canadian trade figures.

- The US trade balance rose to $80.7B in December, a little less than expected.

- FX market did not see any reaction to the latest US trade data.

The US Goods and Services trade deficit rose to $80.7B in the month of December, a smaller than expected rise from $79.33B the month prior, according to data from the Bureau of Economic Analysis and the US Census Bureau on Tuesday. The trade deficit had been expected to rise to $83B. Exports rose to $228.10B in December from $224.7B the month prior, while imports rose to $308.9B from $304B the month prior. The US/China trade deficit widened to $36.15B from $32.32B in November.

Market Reaction

FX market did not see any reaction to the latest US trade data.

- EUR/USD adds to Monday’s weakness and retreats to 1.1400.

- The 5-month support line emerges around 1.1400.

EUR/USD accelerates the weekly leg lower and puts the 1.1400 yardstick to the test on Tuesday.

If the pair break below the 5-month line around the 1.1400 zone it could allow for the selling pressure to pick up pace and attempt a move to the temporary contention at the 55-day SMA at 1.1315. The breach of the latter exposes another visit to the 2022 low near 1.1120 (January 28).

While above this 5-month line, further upside in the pair remains likely in the near term at least. In the longer run, the negative outlook remains in place while below the key 200-day SMA at 1.1670.

- A goodish pickup in the USD demand prompted some selling around AUD/USD on Tuesday.

- Hawkish Fed expectations, elevated US bond yields continued acting as a tailwind for the USD.

- Signs of stability in the equity markets could help limit losses for the perceived riskier aussie.

The AUD/USD pair traded with a mild negative bias during the early North American session and was last seen hovering just a few pips above the daily low, around the 0.7115 area.

Having found some support ahead of the 0.7100 mark, the AUD/USD pair attracted some intraday buying on Tuesday, albeit struggled to capitalize on the move beyond the 0.7135-0.7140 region. Elevated US Treasury bond yields underpinned the US dollar, which, in turn, was seen as a key factor that acted as a headwind for the major.

In fact, the 2-year and 5-year US government bonds held steady near the highest level since February 2020 and July 2019, respectively, amid expectations for a faster policy tightening by the Fed. Adding to this, the yield on the benchmark 10-year note shot closer to the 2% threshold and provided an intraday lift to the buck.

It is worth mentioning that investors now seem convinced that the Fed will respond more aggressively to combat high inflation and have been pricing in a 50 bps rate hike in March. Hence, the market focus will remain glued to the release of the US CPI report on Thursday, which might influence the Fed's near-term policy outlook.

In the meantime, signs of stability in the equity markets might hold back traders from placing fresh bullish bets around the safe-haven buck. This, in turn, should lend some support to the perceived riskier aussie and help limit any meaningful slide for the AUD/USD pair amid absent market-moving economic data from the US.

Technical levels to watch

- Spot gold prices are consolidating in the $1820 area, just below earlier weekly highs, as focus turns to US CPI.

- US yields and the US dollar are a little higher this morning, weighing on XAU/USD a tad.

- But the spot metal continues to perform well on the week, as analysts cite ongoing geopolitical uncertainty as supportive.

Spot gold (XAU/USD) prices have come off the boil following Monday’s decent push higher and are for now consolidating in the $1820 area, down about 0.1% on the session, after topping out this week around $1823. US yields have turned higher again on Tuesday and the US dollar is gaining as the euro gives back some of last week’s post-hawkish ECB gains, which isnt helpful to the precious metal, though it still trades about 0.5% up on the week.

Gold’s resilience in recent weeks to higher US yields has baffled some. “"It's hard to say exactly why gold continues to see so much support” analysts at OANDA told Reuters. “The unstable environment in the markets may be feeding some of the safe-haven appeal,” they continued, adding “it's more likely to be inflation anxiety”. Others have cited the ongoing uncertain geopolitical backdrop as Russia continues to amass troops on its border to Ukraine.

Ahead, gold traders will be closely watching the release of US Consumer Price Inflation data for January this Thursday, which is expected to show the headline YoY rate rising to 7.3%, which would be the highest since 1982. Reuters says that a “robust inflation figure could increase pressure on the Fed for faster tightening and raise the opportunity cost of holding non-yielding bullion”.

- EUR/USD continues to ebb lower post-Lagarde’s more measures tone, though has found decent support at the 1.1400 level.

- Focus is on US CPI data on Thursday, which (if hot) could pump Fed tightening expectations, potentially weighing on EUR/USD.

EUR/USD has been trading with a negative bias in wake of Monday’s more measured remarks from ECB President Christine Lagarde that have taken the sting out of the hawkish repricing of ECB tightening expectations that boosted the euro last week. EUR/USD continues to ebb lower from last Friday’s multi-month highs in the 1.1480s and is down a further 0.2% on Tuesday to trade in near-1.1420, though the pair did find decent support at the 1.1400 level.

For reference, Lagarde on Monday said that while the current outlook did warrant policy normalisation with inflation expected to remain stable around 2.0% in the medium-term, there is no need for major policy tightening. Other ECB members have sung a similar tune, with ECB governing council member Pablo Hernandez de Cos on Tuesday saying that any ECB move “has to be gradual”.

Looking ahead, EUR/USD should be wary of US Goods Trade Balance figures out at 1330GMT on Tuesday. However, the massive and seemingly ever-expanding US trade deficit has in recent years played second fiddle to central bank policy divergence (Fed vs rest of G10) as an FX market/USD driver. The main US data focus this week is Consumer Price Inflation data out on Thursday, which analysts say could increase pressure on the Fed to tighten monetary policy at a faster rate.

If that were to be the case, that could boost the dollar versus the euro and risks sending EUR/USD back under 1.1400. Indeed, whilst markets are now pricing more ECB tightening in 2022 (about 50bps) than this time last week, that is still substantially less tightening than is expected from the Fed (well over 100bps). EUR/USD failure to break convincingly above January’s highs in the upper 1.1400s and subsequent double top formation thus may prove a bearish near-term signal.

Economist at UOB Group Barnabas Gan assesses the latest Retail Sales figures in Singapore.

Key Takeaways

“Singapore’s retail sales surged 6.7% y/y (+2.3% m/m sa) in Dec 2021, surprising market estimates for a milder growth of 4.6%. Accounting for the latest data, Singapore’s retail sales rose 11.1% for the whole of 2021.”

“The retail sales index was supported by strong receipts in both durable and consumer discretionary expenditure. Notably, online retail sales in value terms rose to its highest since Dec 2017, while the return of tourism-related demand could have supported overall retail sales as well.”

“The continued expansion Dec’s retail sales point towards a resilient recovery environment for Singapore’s retail sector. For 2022, retail sales performance will depend on the recovery of Singapore’s domestic economy and the gradual reopening of its borders. Barring the exacerbation of COVID-19-related risks in Singapore and around the region, we pencil retail sales to expand by 6.0% in 2022.”

- USD/CAD regained positive traction on Tuesday and was supported by a combination of factors.

- Retreating oil prices undermined the loonie and extended support amid modest USD strength.

- The mixed fundamental backdrop might cap any further gains ahead of the US CPI on Thursday.

The USD/CAD pair maintained its bid tone heading into the North American session and was last seen trading near the daily high, just above the 1.2700 mark.

A combination of factors assisted the USD/CAD pair to catch fresh bids on Tuesday and recover a part of the overnight losses back closer to the 1.2450 support zone. Crude oil prices pulled away from the seven-year high touched last Friday and undermined the commodity-linked loonie. Apart from this, modest US dollar strength acted as a tailwind for the major.

Expectations that the revival of the 2015 international nuclear agreement could return more than 1 million barrels per day of Iranian oil – equating to more than 1% of global supply – in the markets. This, in turn, prompted traders to lighten their bullish bets ahead of the indirect talks between the United States and Iran, due to resume in Vienna on Tuesday.

On the other hand, the greenback drew some support from a fresh leg up in the US Treasury bond yields, bolstered by speculations for a faster policy tightening by the Fed. In fact, the markets have been pricing in the possibility of a full 50 bps rate hike at the March FOMC meeting amid worries about stubbornly high inflationary pressures.

This, in turn, pushed the yield on the benchmark 10-year US government bond well within the striking distance of the 2.0% threshold. Adding to this, the 2-year and 5-year notes – which are highly sensitive to rate hike expectations – held steady near the highest level since February 2020 and July 2019, respectively, and underpinned the greenback.

Hence, the market focus will remain glued to the release of the US consumer inflation figures on Thursday. The US CPI report will determine the Fed's near-term policy outlook and help determine the next leg of a directional move for the USD/CAD pair. In the meantime, traders might prefer to wait on the sidelines and refrain from placing aggressive bets.

Moreover, hopes that global supply would remain tight amid the post-pandemic recovery in fuel demand, along with the conflict between Russia and the West over Ukraine should limit losses for oil prices. This, in turn, should lend some support to the Canadian dollar and further contribute to capping the USD/CAD pair amid absent market-moving economic data.

Technical levels to watch

- DXY meets decent resistance around 95.70 on Tuesday.

- Another drop to the YTD low near 94.60 is not ruled out.

DXY leaves behind Monday’s downtick and resumes the upside, although the 95.70 region has emerged as quite a decent hurdle so far.

The inability of the index to resume the upside on a sustainable note could prompt sellers to return to the market. That scenario should expose the dollar to retest the so far monthly low at 95.13 (February 4). The loss of this level could motivate the 2022 low at 94.62 (January 14) to start emerging on the horizon.

In the near term, the 5-month line near 95.10 is expected to hold the downside for the time being. Looking at the broader picture, the longer-term positive stance in the dollar remains unchanged above the 200-day SMA at 93.52.

Economist at UOB Group Ho Woei Chen, CFA, reviews the latest inflation results in South Korea.

Key Takeaways

“South Korea’s headline and core inflation were both above expectations in Jan. Although the headline inflation is expected to moderate due to a high comparison base, it will likely fall within the BOK’s 2% target only in 4Q22. We expect inflation to average 2.6% in 2022, exceeding the decade-high of 2.5% in 2021.”

“We still foresee another 50bps interest rate hike to 1.75% by end-2022, likely by 25 bps each in 2Q and 3Q.”

“Resilient external demand continued to buoy the outlook for South Korea’s manufacturing and exports, consistent with gains in raw materials and intermediate goods imports as well as further improvement in Markit South Korea manufacturing PMI to 6-month high of 52.8 in Jan from 51.9 in Dec.”

“Thus far, the impact of the extended social curbs has been relatively muted as consumer confidence rebounded in Jan.”

- EUR/JPY resumes the upside following Monday’s pullback.

- Immediate to the upside comes the 2022 high at 132.16.

EUR/JPY came under some selling pressure following new YTD highs past 132.00 the figure at the beginning of the week.

In light of the recent price action, further gains in the cross look likely in the short-term horizon. That said, the surpass of the YTD high at 132.16 (February 7) should open the door to 132.53 (high November 4) seconded by 132.91 (high October 29) and finally the October 2021 peak at 133.48 (October 20).

In the near term, further upside remains on the table while above the 3-month support line, today around 130.80. In the longer run, and while above the 200-day SMA at 1304645, the outlook for the cross is expected to remain constructive.

- A combination of supporting factors pushed USD/JPY to over a one-week high on Tuesday.

- A fresh leg up in the US bond yields boosted the USD and provided a goodish lift to the pair.

- Widening of the US-Japan yield spread, a positive risk tone undermined the safe-haven JPY.

The USD/JPY pair trimmed a part of its intraday gains and was last seen trading around the 115.30 region, still up over 0.15% for the day.

Following the overnight downtick, the USD/JPY pair caught fresh bids and shot to over a one-week high during the early part of the trading on Tuesday. This marked the third day of a positive move in the previous four and was sponsored by a combination of factors – a goodish pickup in the US dollar demand and a fresh leg up in the US Treasury bond yields.

Investors now seem convinced that the Fed will tighten its monetary policy at a faster pace and have been pricing in the possibility of a 50 bps rate hike in March. The market bets were reaffirmed by Friday's mostly upbeat US monthly employment details, which pointed to the underlying strength in the labour market that should support the economic growth.

This was reinforced by the fact that the yield on the 2-year and 5-year US government bonds – which are sensitive to rate hike expectations – shot to the highest level since February 2020 and July 2019, respectively. Adding to this, the benchmark 10-year bond yield jumped closer to the 2.0% threshold, widening the US-Japanese government bond yield spread.

The Bank of Japan is expected to step in to defend its 0% target for the 10-year JGB, which remains within the implicit 50 bps band set as part of an ultra-easy monetary policy. This, along with a positive tone around the equity markets, undermined the safe-haven Japanese yen and should continue to act as a tailwind for the USD/JPY pair, at least for now.

The fundamental backdrop seems tilted firmly in favour of bullish traders and supports prospects for a further near-term appreciating move for the USD/JPY pair. That said, traders seemed reluctant to place aggressive bets ahead of Thursday's release of the US inflation figures. This, in turn, seemed to be the only factor that capped the upside for the major.

There isn't any major market-moving economic data due for release from the US on Tuesday, leaving the USD at the mercy of the USD price dynamics. Apart from this, traders will take cues from the broader market risk sentiment to grab some short-term opportunities around the USD/JPY pair.

Technical levels to watch

Senior Economist at UOB Group Alvin Liew comments on the recently published US Nonfarm Payrolls for the month of January.

Key Takeaways

“There were two major upside surprises in the Jan 2022 US employment report: employment gain of 467,000 and a wage spike of 5.7% y/y, both well above market expectations.”