- Analytics

- News and Tools

- Market News

CFD Markets News and Forecasts — 05-08-2024

Federal Reserve Bank of San Francisco President Mary Daly said on Monday that she is more confident US inflation is on course to the Fed's 2% target, per Reuters.

Key quotes

Risks to Fed's mandates are getting in more balance.

Minds are open to cutting rates in coming meetings.

Concern is that we will deteriorate from current place of balance in jobs report; we don't see that right now.

July jobs report reflected a lot of temporary layoffs, hurricane effect.

Will be watching carefully to see if next job market report reflects same dynamic, or reverses.

Underneath july jobs report is some reason for confidence we are slowing but not falling off cliff.

Fed will do what it takes to ensure we achieve both goal.

If react to one data point, we would almost always be wrong.

A 'steady in the boat' approach works well.

Policy needs to be pro-active.

We hear the economy is down shifting.

People are getting inflation relief, but still above 2% target.

Not seeing a move to widespread layoffs yet, that would be an early warning sign.

none of the labour market indicators she looks at are flashing red at present, but she is monitoring carefully.

Fed is prepared to act as we get more information.

It's clear inflation is coming down, labor market is slowing.

I am more confident we are on a sustainable path to 2%.

Communication itself is a policy adjustment.

Market reaction

The US Dollar Index (DXY) is trading 0.06% higher on the day at 102.80, as of writing.

- USD/CAD weakens near 1.3805 in Tuesday’s early Asian session.

- Fears of a looming US recession might trigger the Fed to cut interest rates more aggressively this year.

- Lower crude oil prices might weigh on the Loonie and cap the pair’s downside.

The USD/CAD pair trades on a softer note around 1.3805 during the early Asian session on Tuesday. The US Dollar (USD) bounces off the YTD lows near the 102.00 level and hovers around 102.60 amid fears of a US recession.

A risk sentiment would continue to influence the markets as investors are concerned about the recession in the US economy, which triggered a sell-off among the major stock market indices. Market players are now betting the US Federal Reserve (Fed) to act more aggressively in monetary policy this year.

The Fed is expected to cut its interest rate by 50 basis points (bps) in both September and November and another quarter-point cut in December. According to the CME FedWatch tool, the chance for a 50 bps Fed rate cut at the September meeting is 85%.

On Monday, Chicago Fed President Austan Goolsbee said that the US central bank would respond if economic or financial conditions deteriorate. "We're forward-looking about it, and so if the conditions collectively start coming in like that on the through line, there’s deterioration on any of those parts, we’re going to fix it.” Said Goolsbee.

On the Loonie front, the further decline of crude oil prices might continue to undermine the Canadian Dollar (CAD) and cap the downside for USD/CAD. It's worth noting that higher oil prices generally support the CAD lower as Canada is the leading exporter of Oil to the United States (US).

Canadian Dollar FAQs

The key factors driving the Canadian Dollar (CAD) are the level of interest rates set by the Bank of Canada (BoC), the price of Oil, Canada’s largest export, the health of its economy, inflation and the Trade Balance, which is the difference between the value of Canada’s exports versus its imports. Other factors include market sentiment – whether investors are taking on more risky assets (risk-on) or seeking safe-havens (risk-off) – with risk-on being CAD-positive. As its largest trading partner, the health of the US economy is also a key factor influencing the Canadian Dollar.

The Bank of Canada (BoC) has a significant influence on the Canadian Dollar by setting the level of interest rates that banks can lend to one another. This influences the level of interest rates for everyone. The main goal of the BoC is to maintain inflation at 1-3% by adjusting interest rates up or down. Relatively higher interest rates tend to be positive for the CAD. The Bank of Canada can also use quantitative easing and tightening to influence credit conditions, with the former CAD-negative and the latter CAD-positive.

The price of Oil is a key factor impacting the value of the Canadian Dollar. Petroleum is Canada’s biggest export, so Oil price tends to have an immediate impact on the CAD value. Generally, if Oil price rises CAD also goes up, as aggregate demand for the currency increases. The opposite is the case if the price of Oil falls. Higher Oil prices also tend to result in a greater likelihood of a positive Trade Balance, which is also supportive of the CAD.

While inflation had always traditionally been thought of as a negative factor for a currency since it lowers the value of money, the opposite has actually been the case in modern times with the relaxation of cross-border capital controls. Higher inflation tends to lead central banks to put up interest rates which attracts more capital inflows from global investors seeking a lucrative place to keep their money. This increases demand for the local currency, which in Canada’s case is the Canadian Dollar.

Macroeconomic data releases gauge the health of the economy and can have an impact on the Canadian Dollar. Indicators such as GDP, Manufacturing and Services PMIs, employment, and consumer sentiment surveys can all influence the direction of the CAD. A strong economy is good for the Canadian Dollar. Not only does it attract more foreign investment but it may encourage the Bank of Canada to put up interest rates, leading to a stronger currency. If economic data is weak, however, the CAD is likely to fall.

- GBP/USD took a tumble on Monday after risk-off flows pummeled markets.

- Despite a near-term plunge, bids continue to grind out chart paper near 1.2800.

- Souring US economic data has markets piling into Fed rate cut bets.

GBP/USD kicked off the new trading week with a fresh plunge on Monday, falling into familiar lows just north of 1.2700 before recovering ground to end the day close to where it started just below the 1.2800 handle. Markets reversed course and piled into the Greenback in early trading after more US data came in below expectations, hardening broad-market bets of an accelerated pace of rate cuts from the Federal Reserve (Fed) through the rest of the year.

Forex Today: Fed’s rate cut gathers pace

According to the CME’s FedWatch Tool, rate markets are pricing in nearly 85% odds of a double-cut from the Fed on September 18th for 50 basis points after US data took a turn on Friday and further mixed prints on Monday. The rest of the trading week offers a light affair on the economic data docket, giving markets some breathing room and some time to chew on current positioning.

July’s US Composite Purchasing Managers Index (PMI) printed below expectations on Monday, falling to 54.3 versus the forecast flat hold at 55.0. However, ISM Services PMI for the same period accelerated to 51.4, beating the forecast 51.0 and climbing above the previous 48.8 to settle back in expansion territory above 50.0. However, the ISM Sevices Prices Paid in July accelerated to 57.0 from 56.3, routing the market’s forecast tick down to 55.8 as business-level inflation pressures continue to simmer away.

GBP/USD technical outlook

Monday’s back-and-forth chart action has left Cable battling the 50-day Exponential Moving Average (EMA) at 1.2790, with intraday price action hobbled just south of the 1.2800 price handle. Bids continue to hold on the high end of the 200-day EMA at 1.2672, but bidders are struggling to find a foothold with GBP/USD down 2.58% peak-to-trough from July’s 12-month peak at 1.3044.

GBP/USD daily chart

Pound Sterling FAQs

The Pound Sterling (GBP) is the oldest currency in the world (886 AD) and the official currency of the United Kingdom. It is the fourth most traded unit for foreign exchange (FX) in the world, accounting for 12% of all transactions, averaging $630 billion a day, according to 2022 data. Its key trading pairs are GBP/USD, aka ‘Cable’, which accounts for 11% of FX, GBP/JPY, or the ‘Dragon’ as it is known by traders (3%), and EUR/GBP (2%). The Pound Sterling is issued by the Bank of England (BoE).

The single most important factor influencing the value of the Pound Sterling is monetary policy decided by the Bank of England. The BoE bases its decisions on whether it has achieved its primary goal of “price stability” – a steady inflation rate of around 2%. Its primary tool for achieving this is the adjustment of interest rates. When inflation is too high, the BoE will try to rein it in by raising interest rates, making it more expensive for people and businesses to access credit. This is generally positive for GBP, as higher interest rates make the UK a more attractive place for global investors to park their money. When inflation falls too low it is a sign economic growth is slowing. In this scenario, the BoE will consider lowering interest rates to cheapen credit so businesses will borrow more to invest in growth-generating projects.

Data releases gauge the health of the economy and can impact the value of the Pound Sterling. Indicators such as GDP, Manufacturing and Services PMIs, and employment can all influence the direction of the GBP. A strong economy is good for Sterling. Not only does it attract more foreign investment but it may encourage the BoE to put up interest rates, which will directly strengthen GBP. Otherwise, if economic data is weak, the Pound Sterling is likely to fall.

Another significant data release for the Pound Sterling is the Trade Balance. This indicator measures the difference between what a country earns from its exports and what it spends on imports over a given period. If a country produces highly sought-after exports, its currency will benefit purely from the extra demand created from foreign buyers seeking to purchase these goods. Therefore, a positive net Trade Balance strengthens a currency and vice versa for a negative balance.

Interest rate in Australia is expected to remain unchanged in August.

Reserve Bank of Australia Governor Michele Bullock speech could shed light on the Board's path.

The Australian Dollar under pressure ahead of the verdict.

The Reserve Bank of Australia (RBA) will announce its monetary policy decision on Tuesday, August 6. The central bank is expected to maintain the Official Cash Rate (OCR) unchanged at 4.35% amid stubbornly high inflation. Following the announcement, Governor Michele Bullock will hold a press conference in which she will likely explain the reasons behind the decision and, luckily, offer some hints on what policymakers may do next.

Ahead of the announcement, the Australian Dollar (AUD) is under strong selling pressure amid risk-aversion. Financial markets are all about central banks these days, with mounting hopes the United States (US) Federal Reserve (Fed) will begin loosening monetary policy as soon as September. Even further, market participants are pricing in the US central bank kicking off the new cycle by cutting interest rates by 50 basis points (bps).

Reserve Bank of Australia expected to extend the pause, but what’s next?

But fears are not just because of the Fed. The Bank of Japan (BoJ) is also in the eye of the storm these days as policymakers have finally moved into a more aggressive tightening. The BoJ decided to raise the near-term rate target by 15 bps to 0.15%-0.25% when it met last week, also announcing they would reduce their monthly bond buying by around ¥400 billion each quarter. The decision came after the Japanese Yen (JPY) plummeted to multi-year lows against the US Dollar and was clearly a decision to support the local currency rather than a measure related to inflation.

Back to the RBA, policymakers will likely discuss either holding or hiking, with a rate cut out of the table. When the Board met last June, it noted that the case for a rate rise “could be further strengthened” if supply in the economy was “likely to be more constrained than had been assumed,” and moreover, considering “productivity growth remained very weak.”

Australia reported inflation data last week, and the news were far from good. According to the Australian Bureau of Statistics (ABS), the Consumer Price Index (CPI) rose 1.0% in the second quarter of the year and 3.8% over the twelve months to the June 2024 quarter. The latter came in line with the market expectations but higher than the 3.6% posted in the first quarter of the year.

Meanwhile, the RBA Trimmed Mean CPI, the central bank’s favorite inflation gauge, rose 0.8% QoQ and at an annualized pace of 3.9% in the three months to June, slightly below expected. Finally, the Monthly CPI rose by 3.8% YoY in June, below the previous 4% but still above the RBA’s goal of 2% - 3%.

Australian inflation is not at a point to trigger a rate hike, but given the latest data, the odds for a rate cut are pretty much null.

How will the RBA interest rate decision impact AUD/USD?

Ahead of the announcement, market players are anticipating a “hawkish hold.” Policymakers will likely keep the OCR at 4.35% for a sixth straight meeting on Tuesday and refrain from discussing rate cuts but instead maintain the focus on persistent inflationary pressures and leave the door open for a potential hike.

Governor Michele Bullock and co will probably reiterate that they need to be confident that price growth is moving sustainably back to the central bank’s inflation goal and that, in such a scenario, they are not ruling anything in or out.

If that’s the case, the AUD could find some near-term strength, although it should be short-lived, given the risk-averse environment and the decision matching expectations. A dovish stance, however, will come as a big surprise and could trigger a massive Aussie sell-off.

The AUD/USD pair trades around 0.6450 ahead of the event and after plummeting to 0.6347 at the beginning of the week amid mounting tensions in the Middle East and central banks’ imbalances.

Valeria Bednarik, FXStreet's Chief Analyst, says, “The AUD/USD pair is extremely oversold, yet there are no technical signs of downward exhaustion. However, the accumulative 350 pips slump and the expected hawkish hold from the RBA could help the pair correct higher. The immediate resistance level is the 0.6500 - 0.6520 price zone, with gains beyond the latter unlikely unless a hawkish surprise. In such a scenario, AUD/USD could surge towards 0.6570.”

Bednarik adds: “A break through the 0.6400 mark should lead to a retest of the aforementioned low at 0.6347, moreover if risk aversion continues to dominate financial boards ahead of the announcement. A test of the 0.6300 mark is on the cards, should the latter give up.”

RBA FAQs

The Reserve Bank of Australia (RBA) sets interest rates and manages monetary policy for Australia. Decisions are made by a board of governors at 11 meetings a year and ad hoc emergency meetings as required. The RBA’s primary mandate is to maintain price stability, which means an inflation rate of 2-3%, but also “..to contribute to the stability of the currency, full employment, and the economic prosperity and welfare of the Australian people.” Its main tool for achieving this is by raising or lowering interest rates. Relatively high interest rates will strengthen the Australian Dollar (AUD) and vice versa. Other RBA tools include quantitative easing and tightening.

While inflation had always traditionally been thought of as a negative factor for currencies since it lowers the value of money in general, the opposite has actually been the case in modern times with the relaxation of cross-border capital controls. Moderately higher inflation now tends to lead central banks to put up their interest rates, which in turn has the effect of attracting more capital inflows from global investors seeking a lucrative place to keep their money. This increases demand for the local currency, which in the case of Australia is the Aussie Dollar.

Macroeconomic data gauges the health of an economy and can have an impact on the value of its currency. Investors prefer to invest their capital in economies that are safe and growing rather than precarious and shrinking. Greater capital inflows increase the aggregate demand and value of the domestic currency. Classic indicators, such as GDP, Manufacturing and Services PMIs, employment, and consumer sentiment surveys can influence AUD. A strong economy may encourage the Reserve Bank of Australia to put up interest rates, also supporting AUD.

Quantitative Easing (QE) is a tool used in extreme situations when lowering interest rates is not enough to restore the flow of credit in the economy. QE is the process by which the Reserve Bank of Australia (RBA) prints Australian Dollars (AUD) for the purpose of buying assets – usually government or corporate bonds – from financial institutions, thereby providing them with much-needed liquidity. QE usually results in a weaker AUD.

Quantitative tightening (QT) is the reverse of QE. It is undertaken after QE when an economic recovery is underway and inflation starts rising. Whilst in QE the Reserve Bank of Australia (RBA) purchases government and corporate bonds from financial institutions to provide them with liquidity, in QT the RBA stops buying more assets, and stops reinvesting the principal maturing on the bonds it already holds. It would be positive (or bullish) for the Australian Dollar.

Economic Indicator

RBA Interest Rate Decision

The Reserve Bank of Australia (RBA) announces its interest rate decision at the end of its eight scheduled meetings per year. If the RBA is hawkish about the inflationary outlook of the economy and raises interest rates it is usually bullish for the Australian Dollar (AUD). Likewise, if the RBA has a dovish view on the Australian economy and keeps interest rates unchanged, or cuts them, it is seen as bearish for AUD.

Read more.Next release: Tue Aug 06, 2024 04:30

Frequency: Irregular

Consensus: 4.35%

Previous: 4.35%

Source: Reserve Bank of Australia

- AUD/JPY remains in a downtrend and has declined to lows in a year.

- The pair could be due for a bounce as the RSI is in oversold territory, but the MACD is still rising, indicating continued downside pressure.

- Key support and resistance levels to watch are 95.00 and 93.00, respectively.

Following a decline of almost 2% in Monday's session, the AUD/JPY pair is extending its losses and has fallen to its lowest level since August 2023. The downtrend is technically intact.

The Relative Strength Index (RSI) remains below 30, indicating that the pair is technically oversold and this could lead to a short-term bounce. However, the Moving Average Convergence Divergence (MACD) is rising, indicating that the downtrend could continue.

AUD/JPY daily chart

The AUD/JPY pair is currently trading below its 20,100 and 200-day Simple Moving Averages (SMA) which confirms an overall bearish outlook. A break below the 93.00 level could open the door to a further decline, with the next major support level at 92.00. On the upside, the pair faces resistance at 95.00 - 96.00. A break above might improve somewhat the negative outlook.

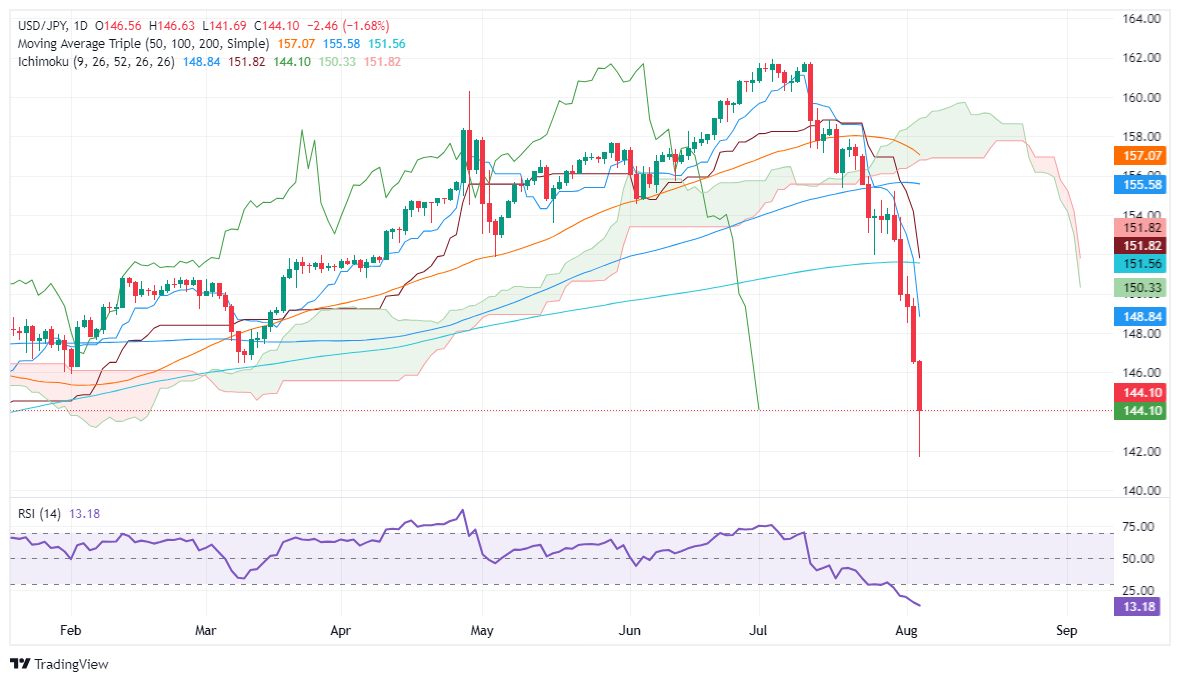

- USD/JPY drops over 4.90% to a low of 141.69 during Asian session before rebounding to 144.16.

- Technical outlook: Downward bias with potential for mean-reversion move as RSI indicates overextension.

- Key resistance levels: 145.00, February 1 bottom at 145.89, and March 11 level at 146.48.

- Key support levels: 144.00, January 9 pivot low at 143.42, and August 5 bottom at 141.69.

The Japanese Yen extended its rally on Monday, registering more than 1.63% gains. This witnessed the USD/JPY drop over 4.90% during the Asian session to a low of 141.69 before trimming some losses and regaining the 144.00 mark. At the time of writing, the USD/JPY trades at 144.16, virtually unchanged as Tuesday’s Asian session begins.

USD/JPY Price Forecast: Technical outlook

The USD/JPY is downward biased yet has found a bottom at around 141.69. Once hit, buyers emerged at the bottom and lifted the exchange rate since the mid-North American session. The latest push saw spot prices above 144.00 as momentum shows the downtrend is overextended, as shown by the Relative Strength Index (RSI).

As the RSI lies beneath 20, the pair is subject to a mean-reversion move.

If USD/JPY climbs past 145.00, the next resistance will be on February 1, bottom at 145.89. Once surpassed, the March 11 146.48 emerges, followed by the 147.00 mark.

Conversely, if USD/JPY extends its losses below 144.00, the next support would be the January 9 pivot low at 143.42, ahead of the August 5 bottom at 141.69.

USD/JPY Price Action – Daily Chart

Japanese Yen PRICE Today

The table below shows the percentage change of Japanese Yen (JPY) against listed major currencies today. Japanese Yen was the strongest against the Swiss Franc.

| USD | EUR | GBP | JPY | CAD | AUD | NZD | CHF | |

|---|---|---|---|---|---|---|---|---|

| USD | -0.00% | -0.01% | -0.06% | -0.02% | 0.02% | 0.10% | 0.03% | |

| EUR | 0.00% | 0.03% | -0.05% | -0.02% | 0.02% | 0.04% | 0.04% | |

| GBP | 0.00% | -0.03% | -0.07% | -0.03% | -0.00% | 0.03% | 0.02% | |

| JPY | 0.06% | 0.05% | 0.07% | 0.02% | 0.08% | 0.08% | 0.27% | |

| CAD | 0.02% | 0.02% | 0.03% | -0.02% | 0.03% | 0.06% | 0.05% | |

| AUD | -0.02% | -0.02% | 0.00% | -0.08% | -0.03% | 0.04% | 0.03% | |

| NZD | -0.10% | -0.04% | -0.03% | -0.08% | -0.06% | -0.04% | 0.04% | |

| CHF | -0.03% | -0.04% | -0.02% | -0.27% | -0.05% | -0.03% | -0.04% |

The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the Japanese Yen from the left column and move along the horizontal line to the US Dollar, the percentage change displayed in the box will represent JPY (base)/USD (quote).

- Silver falls below 100-DMA ($28.67), trading at $27.23 after peaking at same.

- Technicals suggest more silver declines; key supports at $27.00, 200-DMA at $26.02.

- For recovery, silver needs to regain $28.00; resistances at August 2 high of $29.22 and 50-DMA at $29.79.

Silver's price extended its losses below the 100-day moving average (DMA) of $28.67 and is down over 4.50% as risk appetite deteriorated following weaker data from the United States (US). This reignited recession fears, as ISM Manufacturing PMI and Nonfarm Payrolls report disappointed investors, who flock to safe-haven assets, mostly US Treasuries. The XAG/USD trades at $27.23 after hitting a daily high of $28.67.

XAG/USD Price Forecast: Technical outlook

The grey metal tumbled to a three-month high, with buyers battling to reclaim July’s low of $27.31, which would keep them hopeful of higher prices. However, momentum favors sellers, as shown by the Relative Strength Index (RSI), near hitting oversold conditions in normal trading environments.

If XAG/USD drops and achieves a daily close below $27.00, buyers will be pressured to hold forth at the 200-DMA at $26.02. If broken, sellers will drive Silver spot prices to the latest cycle low at $24.33, the March 27 low.

Conversely, if buyers reclaim $28.00, the next resistance would be the August 2 peak at $29.22. Further upside is seen once cleared, with the next supply area at the 50-DMA at $29.79

XAG/USD Price Action – Daily Chart

Silver FAQs

Silver is a precious metal highly traded among investors. It has been historically used as a store of value and a medium of exchange. Although less popular than Gold, traders may turn to Silver to diversify their investment portfolio, for its intrinsic value or as a potential hedge during high-inflation periods. Investors can buy physical Silver, in coins or in bars, or trade it through vehicles such as Exchange Traded Funds, which track its price on international markets.

Silver prices can move due to a wide range of factors. Geopolitical instability or fears of a deep recession can make Silver price escalate due to its safe-haven status, although to a lesser extent than Gold's. As a yieldless asset, Silver tends to rise with lower interest rates. Its moves also depend on how the US Dollar (USD) behaves as the asset is priced in dollars (XAG/USD). A strong Dollar tends to keep the price of Silver at bay, whereas a weaker Dollar is likely to propel prices up. Other factors such as investment demand, mining supply – Silver is much more abundant than Gold – and recycling rates can also affect prices.

Silver is widely used in industry, particularly in sectors such as electronics or solar energy, as it has one of the highest electric conductivity of all metals – more than Copper and Gold. A surge in demand can increase prices, while a decline tends to lower them. Dynamics in the US, Chinese and Indian economies can also contribute to price swings: for the US and particularly China, their big industrial sectors use Silver in various processes; in India, consumers’ demand for the precious metal for jewellery also plays a key role in setting prices.

Silver prices tend to follow Gold's moves. When Gold prices rise, Silver typically follows suit, as their status as safe-haven assets is similar. The Gold/Silver ratio, which shows the number of ounces of Silver needed to equal the value of one ounce of Gold, may help to determine the relative valuation between both metals. Some investors may consider a high ratio as an indicator that Silver is undervalued, or Gold is overvalued. On the contrary, a low ratio might suggest that Gold is undervalued relative to Silver.

- NZD/JPY continues in its relentless sell-off, propelled by bearish technical indicators and dwindling volume.

- The RSI remains in oversold territory, indicating potential exhaustion of the prevailing down move.

- The MACD maintains its bearish alignment, aligning with the general trend.

The NZD/JPY pair remains entrenched in its bearish trajectory, giving no respite to the bears as it approaches critical support levels. This persistent decline has extended across multiple trading sessions, with the NZD/JPY shedding over 10% of its value since its highs in recent weeks. Notably, the pair has breached the 89.00 psychological level and settled well below the 200-day Simple Moving Average (SMA).

On Monday, the NZD/JPY fell by 1.60% to 86.00, reinforcing the sellers' dominance but cleared losses which plunged the index to a low of around 83.00, a critical support level. While the pair has been relentlessly declining, technical indicators like the Relative Strength Index (RSI) continue flashing oversold conditions are approaching. Such conditions may hint at a potential pause in the downtrend. Currently, the RSI resides around 20, signaling a prolonged period of selling, though a potential trend reversal remains a possibility.

NZD/JPY daily chart

Navigating the depths of its descent, the pair is hovering near the 86.00 support level. Should this level fail to hold, further support awaits at 85.50 and 85.00, representing potential areas for a temporary reprieve. Conversely, resistance levels are positioned at 89.00 and 90.00, with the latter coinciding with the 200-day SMA.

- GBP/JPY fell 2% on Monday as market sentiment sours.

- Guppy extended into a fifth straight daily decline.

- Risk-off flows bolster Yen despite upbeat UK data print.

GBP/JPY took a dive on Monday, falling over 2% through the day’s market sessions and testing the 180.00 handle before a meager recovery in the back half of the trading day left bids floundering near 183.80.

The pair is down nearly 13.5% from 16-year highs set above 208.00 in July, and the Guppy’s steep correction was kicked off by a series of “Yenterventions” from the Bank of Japan (BoJ) on behalf of the battered Yen. The thing that finally gave the Yen a leg to stand on was last week’s slim rate hike from the BoJ, which finally helped to ease the wide rate differential that has been weighing down the JPY.

A rate cut from the Bank of England (BoE) last week also helped to crimp the Guppy’s rate differential, forcing a stem-to-stern rebalance in market flows through the GBP/JPY.

The economic calendar remains limited for the remains of the week as both the GBP and the JPY get a breather from large-scale momentum swings, even as broad markets pile into safe havens on a shaky Monday.

GBP/JPY technical outlook

The Guppy is down 13.5% from multi-year peaks above 208.00, with price action smashing through the 200-day Exponential Moving Average (EMA) at 192.57 and hitting the brakes just above the 180.00 handle. Bids are holding steady near 184.00 as Tuesday markets get set to come online.

Daily candlesticks have closed deeply in the red for a fifth straight trading day, and has fallen for all but five of the last 17 consecutive market days. Momentum is finally tilted firmly in the bearish side, but a technical recovery could see bidders stepping back into markets as prices bounce back towards 190.00.

GBP/JPY daily chart

Japanese Yen FAQs

The Japanese Yen (JPY) is one of the world’s most traded currencies. Its value is broadly determined by the performance of the Japanese economy, but more specifically by the Bank of Japan’s policy, the differential between Japanese and US bond yields, or risk sentiment among traders, among other factors.

One of the Bank of Japan’s mandates is currency control, so its moves are key for the Yen. The BoJ has directly intervened in currency markets sometimes, generally to lower the value of the Yen, although it refrains from doing it often due to political concerns of its main trading partners. The current BoJ ultra-loose monetary policy, based on massive stimulus to the economy, has caused the Yen to depreciate against its main currency peers. This process has exacerbated more recently due to an increasing policy divergence between the Bank of Japan and other main central banks, which have opted to increase interest rates sharply to fight decades-high levels of inflation.

The BoJ’s stance of sticking to ultra-loose monetary policy has led to a widening policy divergence with other central banks, particularly with the US Federal Reserve. This supports a widening of the differential between the 10-year US and Japanese bonds, which favors the US Dollar against the Japanese Yen.

The Japanese Yen is often seen as a safe-haven investment. This means that in times of market stress, investors are more likely to put their money in the Japanese currency due to its supposed reliability and stability. Turbulent times are likely to strengthen the Yen’s value against other currencies seen as more risky to invest in.

- Gold dips to $2,364, a six-day low, then recovers above $2,400.

- Market turmoil stems from weak US data, anticipates 50 bps Fed cut in September.

- US Dollar Index falls 0.50% to 102.70; 10-year Treasury yield to 3.783%.

- Rising Middle East tensions buoy Gold; US base in Iraq hit by missiles.

Gold price dropped over 1% during Monday’s North American session but recovered after hitting a new six-day low of $2,364 amid a worldwide market sell-off spurred by last week’s softer-than-expected data in the United States (US). The XAU/USD trades at $2,407, down 1.40%.

The financial markets began to price in a possible recession in the US. Traders expect the Federal Reserve (Fed) will cut interest rates by 50 basis points at the September meeting, following two “bad” reports that showed that manufacturing activity plunged, according to the Institute for Supply Management (ISM), while the economy added fewer people to the workforce.

This spooked investors, who found some relief following the ISM Services PMI release, which revealed the economy continues to expand at a healthier pace. After the data, Gold remained on the backfoot even though the Greenback remained on offer across the board.

The US Dollar Index (DXY), which tracks the performance of six currencies against the US Dollar, sinks 0.50% to 102.70.

US Treasury bond yields tanked further with the 10-year down one basis point to 3.783%. However, it still bounced off multi-week lows of 3.667% hit earlier in the session.

Rising tensions in the Middle East capped bullion losses as Israel awaits a response from Iran and Lebanon following the assassination of the Hamas leader earlier in the week. Sky News Arabia cited Iraqi sources when it revealed that a US base in Iraq was targeted by several missiles.

Daily digest market movers: Gold price stumbles amid recession fears

- A deteriorated market mood would continue to influence traders as fears of a US recession ignited a sell-off among the largest stock market indices.

- The Fed decided to hold rates unchanged last week but indicated that favorable data on inflation and further weakening in the labor market could prompt action.

- Last week, dismal data in the US spooked investors, following the ISM Manufacturing PMI and Nonfarm Payrolls.

- However, Chicago Fed President Austan Goolsbee said on Monday the Fed will not overreact to one month of data, and the board will remain committed to its dual mandate.

- After the data, most banks began to price in more aggressive monetary policy easing by the Fed. Bank of America expects the first cut in September instead of December, while Citi and JP Morgan expect the Fed to lower rates by 50 bps in September and November.

- The CME FedWatch tool shows the odds for a 50 bps Fed rate cut at the September meeting at 85%.

Technical analysis: Gold price tumbles but stays above $2,400

Gold price retreated to the 50-day Simple Moving Average (SMA) at $2,365 during the European session before bouncing off that level and clinched the $2,400 figure. Despite that recovery, momentum still favors sellers.

The Relative Strength Index (RSI) is about to turn bearish after falling steeply during the last three days and is about to cross below the RSI’s neutral line. Once surpassed, this could accelerate Bullion’s losses.

If XAU/USD dives below $2,400, the 50-day SMA could be challenged. Once surpassed, the next support would be the 100-day SMA at $2,340, followed by the May 3 low of $2,277.

Conversely, if buyers reclaim $2,450, the next resistance would be the August 2 peak at $2,477. A breach of the latter will expose the all-time high at $2,483 ahead of $2,500.

Gold FAQs

Gold has played a key role in human’s history as it has been widely used as a store of value and medium of exchange. Currently, apart from its shine and usage for jewelry, the precious metal is widely seen as a safe-haven asset, meaning that it is considered a good investment during turbulent times. Gold is also widely seen as a hedge against inflation and against depreciating currencies as it doesn’t rely on any specific issuer or government.

Central banks are the biggest Gold holders. In their aim to support their currencies in turbulent times, central banks tend to diversify their reserves and buy Gold to improve the perceived strength of the economy and the currency. High Gold reserves can be a source of trust for a country’s solvency. Central banks added 1,136 tonnes of Gold worth around $70 billion to their reserves in 2022, according to data from the World Gold Council. This is the highest yearly purchase since records began. Central banks from emerging economies such as China, India and Turkey are quickly increasing their Gold reserves.

Gold has an inverse correlation with the US Dollar and US Treasuries, which are both major reserve and safe-haven assets. When the Dollar depreciates, Gold tends to rise, enabling investors and central banks to diversify their assets in turbulent times. Gold is also inversely correlated with risk assets. A rally in the stock market tends to weaken Gold price, while sell-offs in riskier markets tend to favor the precious metal.

The price can move due to a wide range of factors. Geopolitical instability or fears of a deep recession can quickly make Gold price escalate due to its safe-haven status. As a yield-less asset, Gold tends to rise with lower interest rates, while higher cost of money usually weighs down on the yellow metal. Still, most moves depend on how the US Dollar (USD) behaves as the asset is priced in dollars (XAU/USD). A strong Dollar tends to keep the price of Gold controlled, whereas a weaker Dollar is likely to push Gold prices up.

- Consolidation persists within the 0.5900-0.6000 range, with neutral technical indicators.

- Bearish momentum remains intact, favoring further declines, but a break above 0.6000 could shift sentiment.

- Volume remains average, with key support and resistance levels inching closer.

On Monday's session, the NZD/USD declined by 0.40% to 0.5930, extending its rangebound trading pattern. On the bright side, bulls managed to clear losses which saw the pair diving below 0.5900 earlier in the session.

The daily chart shows that the Relative Strength Index (RSI) is hovering around 40, indicating a lack of clear direction. The Moving Average Convergence Divergence (MACD) continues to trend lower, suggesting that bearish momentum remains intact. In addition, the pair is currently facing support at 0.5910, a break below which could expose the next support level at 0.5890. On the upside, resistance is found at 0.5980, and a breakout above this level could signal a potential reversal in the trend.

The overall technical outlook for the NZD/USD remains neutral to bearish. While the pair remains rangebound, the bears hold a slight advantage. A break below support or above resistance could trigger a more decisive move. In the meantime, volume is average, with key support and resistance levels inching closer which gives neutrality to the technical outlook.

NZD/USD Daily chart

The Greenback flirted with YTD lows near the 102.00 region amidst an intense sell-off in the global markets following reignited concerns over the likelihood that the US economy might tip into recession. While the RBA is expected to keep rates unchanged on Tuesday, speculation of an inter-meeting rate cut by the Fed remains on the rise.

Here is what you need to know on Tuesday, August 6:

The USD Index (DXY) approached the 102.00 region, or multi-month lows, on the back of declining yields and dominating risk aversion. On August 6 comes the Balance of Trade figures along with the RCM/TIPP Economic Optimism Index.

EUR/USD added to Friday’s uptick and briefly surpassed the psychological 1.1000 barrier, losing some momentum afterwards. Retail Sales in the broader euro area and Germany’s Factory Orders are due on August 6, followed by S&P Global Construction PMI in Germany and the euro bloc.

The intense sell-off in risk-related assets sparked a knee-jerk in GBP/USD, which once again revisited the vicinity of 1.2700. On August 6, the BRC Retail Sales Monitor and the S&P Global Construction PMI will be unveiled.

The increasing risk aversion favoured further JPY-buying on Monday, thus sending USD/JPY briefly below the 142.00 region. Household Spending and Average Cash Earnings are expected on August 6.

AUD/USD managed to reverse the initial pullback to 2024 lows near 0.6350, regaining the 0.6500 hurdle and beyond afterwards. The RBA is expected to keep rates unchanged on August 6.

Recession concerns coupled with sluggish demand from China weighed further on sentiment and dragged prices of WTI briefly below the $72.00 mark on Monday.

Some profit taking mood as well as the broad-based sell-off kept Gold prices on the defensive around the $2,400 mark per ounce troy. Silver prices plummeted to a region last seen in early May around $26.50 per ounce.

- AUD/USD slips amid ongoing bearish sentiment, approaching key support level.

- Economic weakness in Australia intensifies rate-cut expectations for the RBA.

- Technical indicators suggest a potential correction, but bearish momentum remains dominant.

The Australian Dollar (AUD) encountered some selling pressure against the US Dollar (USD) on Monday, declining by 0.50% to 0.6480. During the European session, it fell to its lowest since November 2023 around 0.6350 as risk-off flows dominated the markets, while investors await Tuesday's Reserve Bank of Australia (RBA) decision for further direction.

Despite persistent high inflation, recent data has pointed to weaknesses in the Australian economy. This has prompted markets to shift their expectations from a potential rate hike by the RBA to a rate cut by year-end. The RBA is expected to keep rates steady at 4.35% at its meeting on Tuesday, but investors will be closely monitoring the central bank's policy guidance for any hints of a more dovish stance.

Daily digest market movers: Aussie down as markets digest PMIs ahead of RBA

- Australia's July services and composite PMIs were weaker than expected, with the composite reading falling below 50 for the first time since January.

- The Melbourne Institute Monthly Inflation Gauge showed a decline in inflation to within the RBA's target band.

- The RBA is expected to maintain a neutral policy stance despite inflation remaining above its target range.

- The highlight will be that the RBA will publish new sets of forecasts in its Statement on Monetary Policy, which will guide markets on the next interest rate bets.

AUD/USD technical analysis: Bears continue in command, correction still possible

The AUD/USD pair continues to trade beneath its key Simple Moving Averages (20, 100 and 200-day SMAs), indicating a prevailing bearish sentiment. The Relative Strength Index (RSI) also suggests bearishness, with values hovering between 30-37 in recent sessions. The Moving Average Convergence Divergence (MACD) maintains red bars, further reinforcing the negative momentum.

However, the AUD/USD pair has found some support near the 0.6480 and 0.6350 levels, which could potentially act as a temporary floor. Resistance is anticipated around the 0.6560-0.6570 zone, where selling pressure has previously capped rallies.

Australian Dollar FAQs

One of the most significant factors for the Australian Dollar (AUD) is the level of interest rates set by the Reserve Bank of Australia (RBA). Because Australia is a resource-rich country another key driver is the price of its biggest export, Iron Ore. The health of the Chinese economy, its largest trading partner, is a factor, as well as inflation in Australia, its growth rate and Trade Balance. Market sentiment – whether investors are taking on more risky assets (risk-on) or seeking safe-havens (risk-off) – is also a factor, with risk-on positive for AUD.

The Reserve Bank of Australia (RBA) influences the Australian Dollar (AUD) by setting the level of interest rates that Australian banks can lend to each other. This influences the level of interest rates in the economy as a whole. The main goal of the RBA is to maintain a stable inflation rate of 2-3% by adjusting interest rates up or down. Relatively high interest rates compared to other major central banks support the AUD, and the opposite for relatively low. The RBA can also use quantitative easing and tightening to influence credit conditions, with the former AUD-negative and the latter AUD-positive.

China is Australia’s largest trading partner so the health of the Chinese economy is a major influence on the value of the Australian Dollar (AUD). When the Chinese economy is doing well it purchases more raw materials, goods and services from Australia, lifting demand for the AUD, and pushing up its value. The opposite is the case when the Chinese economy is not growing as fast as expected. Positive or negative surprises in Chinese growth data, therefore, often have a direct impact on the Australian Dollar and its pairs.

Iron Ore is Australia’s largest export, accounting for $118 billion a year according to data from 2021, with China as its primary destination. The price of Iron Ore, therefore, can be a driver of the Australian Dollar. Generally, if the price of Iron Ore rises, AUD also goes up, as aggregate demand for the currency increases. The opposite is the case if the price of Iron Ore falls. Higher Iron Ore prices also tend to result in a greater likelihood of a positive Trade Balance for Australia, which is also positive of the AUD.

The Trade Balance, which is the difference between what a country earns from its exports versus what it pays for its imports, is another factor that can influence the value of the Australian Dollar. If Australia produces highly sought after exports, then its currency will gain in value purely from the surplus demand created from foreign buyers seeking to purchase its exports versus what it spends to purchase imports. Therefore, a positive net Trade Balance strengthens the AUD, with the opposite effect if the Trade Balance is negative.

- Mexican Peso recovers from yearly low, trades at 19.57, still down over 2%.

- Safe-haven demand for Yen and Franc amid turmoil impacts emerging market currencies.

- Wall Street indices' losses heighten financial market stress, affecting USD/MXN volatility.

- Upcoming Mexico data: Auto Exports (Tuesday), Inflation, Banxico decision (Thursday).

The Mexican Peso trims some of its earlier losses held during the Asian session on Monday, with the emerging market currency depreciating almost 6% to a yearly low of 20.22. The USD/MXN is trading back below the 20.00 figure, but still the Peso is down over 1%, exchanging hands at 19.32.

Market sentiment remains sour across the globe, triggering a flight to safe-haven assets like the Japanese Yen and the Swiss Franc in the FX space. Against emerging market currencies, flows outside the latter bolstered the Greenback, which posted substantial gains against the Mexican Peso.

Meanwhile, Wall Street’s post losses between 2% to 3% among its largest indices indicate stress in the financial markets. Hence, USD/MXN traders must be aware of the market mood, which could spark volatility in the exotic pair.

Mexico’s economic docket will be light at the beginning of the week but gains traction on Tuesday and Thursday. Auto Exports for July will be issued on Tuesday, followed by inflation data and the Bank of Mexico (Banxico) monetary policy decision on Thursday.

Across the border, the US docket revealed that contrary to a weaker-than-expected manufacturing activity report, the services segment exceeded estimates, according to Institute for Supply Management (ISM) data.

Other data revealed by S&P Global showed that business activity dipped by a tenth yet remains expanding.

Daily digest market mover: Mexican Peso slumps on market mood, US recession fears

- Sour sentiment will likely continue to drive the financial markets. Fears are broadening after Asia stock indices plummeted sharply as fears that the Federal Reserve is behind the curve could trigger a recession.

- This, along with the Bank of Japan (BoJ) laying the ground for higher interest rates as it battles inflation and a reduction of its balance sheet, drained the liquidity of the financial markets, sparking the global stock market sell-off.

- Mexico’s Auto Exports for July are forecasted to remain at 3.3% YoY and Auto Production at 3.8% YoY.

- July’s inflation is expected to remain unchanged at 0.38% MoM and 4.98% YoY. Core inflation is estimated to hit 4.13% annually.

- The US ISM Services PMI expanded by 51.4 in July, above estimates of 51 and up from June’s 48.8 contraction.

- S&P Global Services’ PMI dipped from 55.3 to 55.0, below forecasts for a 56.0 jump.

- The CME FedWatch Tool shows the odds of a 50-basis-point interest rate cut by the Fed at the September meeting at 86.5%, up from 74% last Friday.

Technical analysis: Mexican Peso depreciates sharply as USD/MXN rises above 19.30

The USD/MXN is trimming some of its gains, following a spike that lifted the pair to a new 22-month high, to levels last seen in October 2022. But it’s still headed for further gains.

The Relative Strength Index (RSI) suggests that buyers are in charge after turning overbought, as seen by the USD/MXN dip from highs toward the current exchange rate. However, once the RSI dives below 70, buyers could re-enter and lift the pair higher.

If USD/MXN achieves a daily close above the August 2 high of 19.22, that will expose the 19.50 psychological figure. A further upside is seen above that level, at 20.00, followed by the current year-to-date (YTD) peak at 19.22.

Conversely, if the pair drops below 19.22, the USD/MXN will be poised to challenge the 19.00 psychological figure. Once cleared, the next support would be the 50-day Simple Moving Average (SMA) at 18.12. In further weakness, the exotic pair could challenge the 17.50 mark.

Mexican Peso FAQs

The Mexican Peso (MXN) is the most traded currency among its Latin American peers. Its value is broadly determined by the performance of the Mexican economy, the country’s central bank’s policy, the amount of foreign investment in the country and even the levels of remittances sent by Mexicans who live abroad, particularly in the United States. Geopolitical trends can also move MXN: for example, the process of nearshoring – or the decision by some firms to relocate manufacturing capacity and supply chains closer to their home countries – is also seen as a catalyst for the Mexican currency as the country is considered a key manufacturing hub in the American continent. Another catalyst for MXN is Oil prices as Mexico is a key exporter of the commodity.

The main objective of Mexico’s central bank, also known as Banxico, is to maintain inflation at low and stable levels (at or close to its target of 3%, the midpoint in a tolerance band of between 2% and 4%). To this end, the bank sets an appropriate level of interest rates. When inflation is too high, Banxico will attempt to tame it by raising interest rates, making it more expensive for households and businesses to borrow money, thus cooling demand and the overall economy. Higher interest rates are generally positive for the Mexican Peso (MXN) as they lead to higher yields, making the country a more attractive place for investors. On the contrary, lower interest rates tend to weaken MXN.

Macroeconomic data releases are key to assess the state of the economy and can have an impact on the Mexican Peso (MXN) valuation. A strong Mexican economy, based on high economic growth, low unemployment and high confidence is good for MXN. Not only does it attract more foreign investment but it may encourage the Bank of Mexico (Banxico) to increase interest rates, particularly if this strength comes together with elevated inflation. However, if economic data is weak, MXN is likely to depreciate.

As an emerging-market currency, the Mexican Peso (MXN) tends to strive during risk-on periods, or when investors perceive that broader market risks are low and thus are eager to engage with investments that carry a higher risk. Conversely, MXN tends to weaken at times of market turbulence or economic uncertainty as investors tend to sell higher-risk assets and flee to the more-stable safe havens.

- The Canadian Dollar (CAD) backslid against the US Dollar on Monday.

- A moderate recovery has the CAD back into the green for the day.

- A Canadian holiday leaves CAD trading flows crimped.

The Canadian Dollar (CAD) tumbled against the Greenback early Monday before a mid-session recovery. The CAD is holding in positive territory against the US Dollar to kick off the new trading week, but market flows remain thin with Canadian markets shuttered for the August Civic Holiday.

CAD traders will be waiting in the wings with meaningful Canadian economic data slated for Friday with July’s updated labor figures. A smattering of mid-tier data from Canada is due throughout the midweek, but impact is set to be limited.

Daily digest market movers: CAD flows take a backseat amid US data fears

- US S&P Global Composite Purchasing Managers Index (PMI) figures in July eased to 54.3, missing the forecast hold at 55.0.

- Further downside misses added to fears of a US recession after last Friday’s miss in US Nonfarm Payrolls (NFP) sparked an extended risk-off decline across global markets.

- Market expectations for a Federal Reserve (Fed) rate cut in September are fully pinned to the ceiling.

- Despite wide misses in recent US data, Monday’s July ISM Services PMI rose to 51.1, beating the forecast 46.5.

- Later in the week, CAD traders will be looking for a recovery in Canada’s Net Change in Employment on Friday. June’s headline figure reported a net contraction of -1.4K.

Canadian Dollar PRICE Today

The table below shows the percentage change of Canadian Dollar (CAD) against listed major currencies today. Canadian Dollar was the strongest against the British Pound.

| USD | EUR | GBP | JPY | CAD | AUD | NZD | CHF | |

|---|---|---|---|---|---|---|---|---|

| USD | -0.33% | 0.41% | -1.50% | -0.18% | 0.32% | 0.41% | -0.56% | |

| EUR | 0.33% | 0.66% | -1.33% | 0.03% | 0.67% | 0.64% | -0.33% | |

| GBP | -0.41% | -0.66% | -1.90% | -0.60% | 0.00% | -0.02% | -0.99% | |

| JPY | 1.50% | 1.33% | 1.90% | 1.39% | 1.81% | 1.97% | 0.99% | |

| CAD | 0.18% | -0.03% | 0.60% | -1.39% | 0.54% | 0.59% | -0.56% | |

| AUD | -0.32% | -0.67% | -0.01% | -1.81% | -0.54% | -0.03% | -0.98% | |

| NZD | -0.41% | -0.64% | 0.02% | -1.97% | -0.59% | 0.03% | -0.97% | |

| CHF | 0.56% | 0.33% | 0.99% | -0.99% | 0.56% | 0.98% | 0.97% |

The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the Canadian Dollar from the left column and move along the horizontal line to the US Dollar, the percentage change displayed in the box will represent CAD (base)/USD (quote).

Canadian Dollar technical outlook: USD/CAD sets new 2024 high as Greenback tests high end

The Canadian Dollar (CAD) eased early Monday before recovering back into the green against the US Dollar. A Canadian market holiday leaves the CAD in a mixed stance to kick off the new trading week, up three-tenths of one percent against the Greenback but down around six-tenths of one percent against the Japanese Yen.

USD/CAD briefly rallied into a fresh high bid for 2024, falling just shy of 1.3950 before turning around and slumping back below 1.3850. The pair chalked in an outside candle on daily charts as price action gets frothy, but bidders are struggling to develop enough momentum to break the pair into an extended bull run.

USD/CAD daily chart

Canadian Dollar FAQs

The key factors driving the Canadian Dollar (CAD) are the level of interest rates set by the Bank of Canada (BoC), the price of Oil, Canada’s largest export, the health of its economy, inflation and the Trade Balance, which is the difference between the value of Canada’s exports versus its imports. Other factors include market sentiment – whether investors are taking on more risky assets (risk-on) or seeking safe-havens (risk-off) – with risk-on being CAD-positive. As its largest trading partner, the health of the US economy is also a key factor influencing the Canadian Dollar.

The Bank of Canada (BoC) has a significant influence on the Canadian Dollar by setting the level of interest rates that banks can lend to one another. This influences the level of interest rates for everyone. The main goal of the BoC is to maintain inflation at 1-3% by adjusting interest rates up or down. Relatively higher interest rates tend to be positive for the CAD. The Bank of Canada can also use quantitative easing and tightening to influence credit conditions, with the former CAD-negative and the latter CAD-positive.

The price of Oil is a key factor impacting the value of the Canadian Dollar. Petroleum is Canada’s biggest export, so Oil price tends to have an immediate impact on the CAD value. Generally, if Oil price rises CAD also goes up, as aggregate demand for the currency increases. The opposite is the case if the price of Oil falls. Higher Oil prices also tend to result in a greater likelihood of a positive Trade Balance, which is also supportive of the CAD.

While inflation had always traditionally been thought of as a negative factor for a currency since it lowers the value of money, the opposite has actually been the case in modern times with the relaxation of cross-border capital controls. Higher inflation tends to lead central banks to put up interest rates which attracts more capital inflows from global investors seeking a lucrative place to keep their money. This increases demand for the local currency, which in Canada’s case is the Canadian Dollar.

Macroeconomic data releases gauge the health of the economy and can have an impact on the Canadian Dollar. Indicators such as GDP, Manufacturing and Services PMIs, employment, and consumer sentiment surveys can all influence the direction of the CAD. A strong economy is good for the Canadian Dollar. Not only does it attract more foreign investment but it may encourage the Bank of Canada to put up interest rates, leading to a stronger currency. If economic data is weak, however, the CAD is likely to fall.

- A disappointing July jobs report sparked hopes of a September rate cut as well as recession fears.

- ISM Services data shows signs of improvement, overall economy remains strong.

- Market prices in 125 bps of Fed easing by year-end.

The US Dollar (USD), measured by the DXY index, came under initial selling pressure at the start of Monday's session but later erased losses after the release of positive ISM Services figures for July. The index initially fell to 102.20 but recovered to trade around 102.70.

Despite the positive data, the market’s fear is that the US economic outlook turned weak and investors worry that the US might be headed toward a recession

Daily digest market movers: USD recovers after ISM Services data, markets worry about a recession in the US

- On the data front, the Services Employment Index climbed from 46.1 to 51.1 while the New Orders Index increased from 47.3 to 52.4.

- The Services PMI moved from contraction to growth, rising from 48.8 to 51.4.

- Soft US jobs data last Friday sparked fears that the Fed is lagging, leading to a global bond rally and equity sell-off on both Friday and Monday.

- The market is fully pricing in a 125 bps easing by year-end, with a 50 bps cut expected in September.

- A total easing of 225 bps over the next 12 months seems unlikely unless a deep US recession occurs. In that sense, it seems that markets are overreacting to one data point, and Fed speakers might cool down the dovish bets as the market has repeatedly misjudged the Fed's easing path throughout this cycle.

DXY technical outlook: Bearish bias persists, indicators now in oversold region

The DXY outlook turned bearish after the disappointing jobs report last week. The index fell below both the 20-day and 200-day Simple Moving Averages (SMAs). The momentum-based Relative Strength Index (RSI) and the Moving Average Convergence Divergence (MACD) also declined, indicating increasing selling pressure. The RSI below 30, however, indicates that a correction might be looming.

Supports: 102.50, 102.20, 102.00

Resistances: 103.00, 103.50, 104.00

US Dollar FAQs

The US Dollar (USD) is the official currency of the United States of America, and the ‘de facto’ currency of a significant number of other countries where it is found in circulation alongside local notes. It is the most heavily traded currency in the world, accounting for over 88% of all global foreign exchange turnover, or an average of $6.6 trillion in transactions per day, according to data from 2022. Following the second world war, the USD took over from the British Pound as the world’s reserve currency. For most of its history, the US Dollar was backed by Gold, until the Bretton Woods Agreement in 1971 when the Gold Standard went away.

The most important single factor impacting on the value of the US Dollar is monetary policy, which is shaped by the Federal Reserve (Fed). The Fed has two mandates: to achieve price stability (control inflation) and foster full employment. Its primary tool to achieve these two goals is by adjusting interest rates. When prices are rising too quickly and inflation is above the Fed’s 2% target, the Fed will raise rates, which helps the USD value. When inflation falls below 2% or the Unemployment Rate is too high, the Fed may lower interest rates, which weighs on the Greenback.

In extreme situations, the Federal Reserve can also print more Dollars and enact quantitative easing (QE). QE is the process by which the Fed substantially increases the flow of credit in a stuck financial system. It is a non-standard policy measure used when credit has dried up because banks will not lend to each other (out of the fear of counterparty default). It is a last resort when simply lowering interest rates is unlikely to achieve the necessary result. It was the Fed’s weapon of choice to combat the credit crunch that occurred during the Great Financial Crisis in 2008. It involves the Fed printing more Dollars and using them to buy US government bonds predominantly from financial institutions. QE usually leads to a weaker US Dollar.

Quantitative tightening (QT) is the reverse process whereby the Federal Reserve stops buying bonds from financial institutions and does not reinvest the principal from the bonds it holds maturing in new purchases. It is usually positive for the US Dollar.

- Dow Jones fell another 1,300 points from Friday’s close.

- Markets are recoiling amidst concerns of an escalation in Middle East conflicts.

- Souring US economic data is increasing concerns of a wider economic slowdown.

The Dow Jones Industrial Average (DJIA) extended into a third straight day of downside momentum as equities plunge in the face of a bad batch of US economic figures signalling the growing possibility of a harder, deeper recession than most investors were prepared for in the coming months. Geopolitical tensions are also on the rise, further batting down risk appetite as the Israel-Palestinian Hamas conflict looks set to widen with the possible involvement with Iran.

Last Friday’s US Nonfarm Payrolls (NFP) would have been a good print in years past, but that was then and this is now. The lowest initial print in the number of net jobs additions since 2019 sent shockwaves through investor markets, dragging down equities and sparking fears of a broad recession over the horizon for the US economy. Monday accelerated losses, sending all US sectors and indexes into the red.

The US S&P Global Services Purchasing Manager Index (PMI) for July eased to 55.0 from the expected hold at 56.0, and July’s Composite PMI also ticked down to 54.3 instead of the forecast flat hold at 55.0. Still, a glimmer of hope on the data front: the ISM Services PMI for July rose to 51.4 on Monday, beating the forecast increase to 51.0 from the previous 48.8.

After the assassination of two of Iran and Hezbollah’s militant leaders last week, markets are bracing for an expected escalation in the Middle East conflict that has been bubbling for months. Iran is expected to retaliate directly against Israel for its hand in assassinations that took place in Beirut and Tehran, and the US is deploying warships to the region in an effort to stave off a further widening of the conflict.

Dow Jones news

The Dow Jones plummeted to a 1,300 point decline from Friday’s close in early Monday trading as the entire stock index prints in the red. All US sectors are down on Monday, with losses being led by Intel Corp. (INTC), which fell -6.3% and is approaching $20.00 per share after the software company announced a minor miss in second-quarter revenue and slightly lowered forward guidance on revenue for the current quarter.

Dow Jones technical outlook

Monday’s bearish plunge dragged the Dow Jones to an eight-week low of 38,382.90. Bids have fallen with touch range of the 200-day Exponential Moving Average (EMA) at 38,108.94, a feat that hasn’t been accomplished since the DJIA soared back over the long-term moving average in November of last year.

Despite near-term declines dragging the Dow Jones into correction territory, down around -7% peak-to-trough from all-time highs set above the 40,000.00 major price handle, price action still has a long way to go before testing full-on bear country at the 20% contraction mark near 33,108.00.

Dow Jones daily chart

Dow Jones FAQs

The Dow Jones Industrial Average, one of the oldest stock market indices in the world, is compiled of the 30 most traded stocks in the US. The index is price-weighted rather than weighted by capitalization. It is calculated by summing the prices of the constituent stocks and dividing them by a factor, currently 0.152. The index was founded by Charles Dow, who also founded the Wall Street Journal. In later years it has been criticized for not being broadly representative enough because it only tracks 30 conglomerates, unlike broader indices such as the S&P 500.

Many different factors drive the Dow Jones Industrial Average (DJIA). The aggregate performance of the component companies revealed in quarterly company earnings reports is the main one. US and global macroeconomic data also contributes as it impacts on investor sentiment. The level of interest rates, set by the Federal Reserve (Fed), also influences the DJIA as it affects the cost of credit, on which many corporations are heavily reliant. Therefore, inflation can be a major driver as well as other metrics which impact the Fed decisions.

Dow Theory is a method for identifying the primary trend of the stock market developed by Charles Dow. A key step is to compare the direction of the Dow Jones Industrial Average (DJIA) and the Dow Jones Transportation Average (DJTA) and only follow trends where both are moving in the same direction. Volume is a confirmatory criteria. The theory uses elements of peak and trough analysis. Dow’s theory posits three trend phases: accumulation, when smart money starts buying or selling; public participation, when the wider public joins in; and distribution, when the smart money exits.

There are a number of ways to trade the DJIA. One is to use ETFs which allow investors to trade the DJIA as a single security, rather than having to buy shares in all 30 constituent companies. A leading example is the SPDR Dow Jones Industrial Average ETF (DIA). DJIA futures contracts enable traders to speculate on the future value of the index and Options provide the right, but not the obligation, to buy or sell the index at a predetermined price in the future. Mutual funds enable investors to buy a share of a diversified portfolio of DJIA stocks thus providing exposure to the overall index.

There was relatively little movement in liquefied natural gas (LNG) prices in July, NAB Group commodity analysts note.

LNG supply is expected to expand

“There was relatively little movement in liquefied natural gas (LNG) prices in July – with the Japan Korea marker trading in a US 55 cent range above US$12/mmbtu over the course of the month, marginally above the levels recorded during the same period in 2023.”

“LNG markets have seen strong demand in recent months (compounding peak demand during the northern summer), as heatwave conditions across much of South and South-east Asia bolstered electricity consumption, while LNG supply saw some unanticipated disruptions.”

“LNG supply is expected to expand in the second half of 2024 and across 2025. Our forecasts for LNG spot prices are unchanged this month – we expect prices to average US$11.0/mmbtu in 2024 before edging down to US$10.5/mmbtu in 2025.”

Having trended higher across June, crude oil prices peaked in early July (at around US$88/barrel for benchmark Brent crude) before trending down across the rest of the month, NAB commodity analysts note.

Supply side fears produce volatility

“In line with subdued global economic conditions, the International Energy Agency noted that oil consumption grew comparatively modestly in Q2 2024 – up by around 710kb/d from Q1 – with Chinese consumption falling year-on-year during this period.”

“Growth in supply outpaced consumption – increasing by 910kb/d – led by higher production in the United States and coming despite ongoing restrictions on supply from OPEC+. Recent volatility in crude prices largely reflects supply side fears, such as concerns of an escalation of conflicts in the Middle East negatively impacting output in the region.”

“Our forecasts are unchanged this month, with Brent crude expected to average US$85/barrel in 2024 and US$84/barrel in 2025.”

Commodity demand expectations embedded within the complex are melting alongside the decline in equity indices and yields, TDS senior commodity strategist Daniel Ghali notes.

Low bar for subsequent CTA selling activity

“This dynamic weighs on the entire complex, but we expect massive CTA selling activity in platinum markets this session, with CTAs likely to shed their entire book long and grow a net short position closer to its effective 'max short' position size.”

“While CTAs are already holding their effective 'max short' position in palladium, silver remains vulnerable to algo selling activity below the $25.80/oz mark. Copper markets are also being weighed down by algo selling activity, as CTAs finally start to shed their books long as we have expected following massive liquidations from macro funds.”

“Our simulations of future prices continue to point to a low bar for subsequent CTA selling activity, with algos likely to continue selling the red metal even in a flat tape over the coming week.”

- EUR/USD jumps to near 1.1000 as the US Dollar plunges on fears of US economic slowdown.

- Upbeat US ISM Services PMI offer support to the US Dollar.

- Stubborn Eurozone inflation has diminished market expectation for ECB subsequent rate cuts.

The EUR/USD pair prints a fresh seven-month high around the psychological resistance of 1.1000 in Monday’s American session. The major currency pair strengthens as the US Dollar (USD) plummets amid growing speculation that the Federal Reserve (Fed) could announce emergency rate cuts as risks have widened to both components of dual mandate.

The US Dollar Index (DXY), which tracks the Greenback’s value against six major currencies, plunges to 102.20. Meanwhile, an asset-specific action has observed in global markets. Global equities continue to face sell-off, while risk-perceived currencies have bounced back strongly due to weakness in the US Dollar.

However, the US Dollar has found an intermediate support after upbeat US ISM Services PMI. The PMI report showed that the service sector activity rose to 51.4 from expectations of 51.0 from the former release of 48.8.

Upside risks to United States (US) economic slowdown have deepened as job demand has slowed and the jobless rate has risen to its highest since November 2021.

On the Eurozone front, stubborn inflationary pressures in July have stemmed doubts over expectations of subsequent rate cuts by the European Central Bank (ECB).

EUR/USD attempts to deliver a breakout of the Channel formation on a daily timeframe. A breakout of an aforementioned chart pattern results in wider ticks on the upside and heavy volume. The 200-day Exponential Moving Average (EMA) near 1.0800 acted as major support for the Euro bulls.

The 14-day Relative Strength Index (RSI) climbs above 60.00. If the RSI sustains above 60.00, a bullish momentum will trigger.

More upside would appear if the major currency pair breaks above intraday high of 1.1009. This would drive the asset towards 10 August 2023 high at 1.1065, followed by the round-level resistance of 1.1100.

In an alternate scenario, a downside move below August 1 low at 1.0777 would drag the asset towards February low near 1.0700. A breakdown below the latter would expose the asset to June 14 low at 1.0667.

EUR/USD daily chart

Euro FAQs

The Euro is the currency for the 20 European Union countries that belong to the Eurozone. It is the second most heavily traded currency in the world behind the US Dollar. In 2022, it accounted for 31% of all foreign exchange transactions, with an average daily turnover of over $2.2 trillion a day. EUR/USD is the most heavily traded currency pair in the world, accounting for an estimated 30% off all transactions, followed by EUR/JPY (4%), EUR/GBP (3%) and EUR/AUD (2%).

The European Central Bank (ECB) in Frankfurt, Germany, is the reserve bank for the Eurozone. The ECB sets interest rates and manages monetary policy. The ECB’s primary mandate is to maintain price stability, which means either controlling inflation or stimulating growth. Its primary tool is the raising or lowering of interest rates. Relatively high interest rates – or the expectation of higher rates – will usually benefit the Euro and vice versa. The ECB Governing Council makes monetary policy decisions at meetings held eight times a year. Decisions are made by heads of the Eurozone national banks and six permanent members, including the President of the ECB, Christine Lagarde.

Eurozone inflation data, measured by the Harmonized Index of Consumer Prices (HICP), is an important econometric for the Euro. If inflation rises more than expected, especially if above the ECB’s 2% target, it obliges the ECB to raise interest rates to bring it back under control. Relatively high interest rates compared to its counterparts will usually benefit the Euro, as it makes the region more attractive as a place for global investors to park their money.

Data releases gauge the health of the economy and can impact on the Euro. Indicators such as GDP, Manufacturing and Services PMIs, employment, and consumer sentiment surveys can all influence the direction of the single currency. A strong economy is good for the Euro. Not only does it attract more foreign investment but it may encourage the ECB to put up interest rates, which will directly strengthen the Euro. Otherwise, if economic data is weak, the Euro is likely to fall. Economic data for the four largest economies in the euro area (Germany, France, Italy and Spain) are especially significant, as they account for 75% of the Eurozone’s economy.

Another significant data release for the Euro is the Trade Balance. This indicator measures the difference between what a country earns from its exports and what it spends on imports over a given period. If a country produces highly sought after exports then its currency will gain in value purely from the extra demand created from foreign buyers seeking to purchase these goods. Therefore, a positive net Trade Balance strengthens a currency and vice versa for a negative balance.

Gold does not hedge against deleveraging or liquidity dynamics. There’s an acute risk of a widespread deleveraging event that could counterintuitively weigh on Gold prices. Markets suspect that recent selling activity has still been limited to the implications of unwinding carry trades, TDS senior commodity strategist Daniel Ghali notes.

Large-scale selling activity to kick off below $2390

“The recent price action following a considerable miss on payrolls data, alongside a meltdown in rates and into a weekend which hosted substantial geopolitical risks tied to the conflict in the Middle East are telling: not only is macro fund positioning bloated, but it is fully tapped out for the time being.”

“Commodity Trading Advisor (CTA) trend followers still hold substantial dry-powder to sell, with large-scale selling activity likely to kick off below $2390/oz in active futures. Shanghai traders still hold near-record length in Gold as a currency-depreciation hedge, but the driver of this build-up in positioning has significantly deteriorated with Asian currencies notably strengthening.”

“De-escalation in the Middle East could exacerbate these flows as safe-haven flows are simultaneously unwound. Overall, this suggests that the implications of a deleveraging event could be significant in Gold markets, which places our attention on a potential bounce in yields as a possible catalyst for large-scale mechanical selling activity from risk parity and vol-control funds, CTAs, macro funds and Shanghai traders.”

- GBP/USD falls to 1.2772, down 0.20%, following significant losses in global markets.

- Technicals show bearish momentum; RSI suggests further declines.

- Key supports: August 2 low at 1.2707, 100-DMA at 1.2683, 200-DMA at 1.2645.

- For bullish reversal, GBP/USD needs to pass 50-DMA at 1.2786 and August 2 high at 1.2840, aiming for 1.2860 and 1.2900.

The Pound Sterling edges lower after trimming some of its earlier losses due to a bloodbath in the financial markets, led by Asian equities, which triggered circuit breakers halting trading as losses deepened. The GBP/USD trades at 1.2772, down by 0.20%.

GBP/USD Price Analysis: Technical outlook

Last Friday, the GBP/USD seemed poised to test higher prices, but due to risk aversion and investors seeking safety, the Cable was under pressure during the Asian and European sessions.

Momentum, as depicted by the Relative Strength Index (RSI), shifted bearishly, and with sellers in charge, further losses loom.

As of writing, the GBP/USD has fallen below 1.2800, and the 50-day moving average (DMA) is at 1.2786, leading for a deeper pullback. If the pair slides below the August 2 low of 1.2707, that could pave the way to test the 100-DMA at 1.2683. A breach of the latter will expose the 200-DMA at 1.2645, which, once broken, would shift and turn the pair bearish.

For a bullish reversal, the GBP/USD must clear the 50-DMA and the August 2 peak at 1.2840. Once hurdle, the next resistance will be the June 12 high at 1.2860, ahead of 1.2900.

GBP/USD Price Action – Daily Chart

British Pound PRICE Today