- Analytics

- News and Tools

- Market News

CFD Markets News and Forecasts — 05-04-2011

Gainers

Symb Last Change Chg %

EXK.N 11.09 +0.91 +8.94

AG.N 25.26 +1.75 +7.44

DVD.N 2.08 +0.11 +5.58

SKH.N 15.70 +0.48 +3.15

BTH.N 35.87 +1.05 +3.02

Losers

Symb Last Change Chg %

DGW.N 3.23 -0.76 -19.05

OC'B 2.38 -0.37 -13.45

RTN' 12.11 -1.64 -11.93

BITA.N 10.02 -1.24 -11.01

CTC.N 3.08 -0.19 -5.81

Recall that staff forecasts were rev down for growth, up for inflation. Members said the econ recovery was on firmer footing, broadly as expected, gaining traction; labor mkt improving gradually; credit conds remained uneven. They expected energy, commods to boost infl but said this should be transitory (also lowers growth). Overall risks seen as 'roughly balanced.' Members said will watch infl expectations (currently stable in a slack environment) for hints the

public expects excessive price moves. MENA, Japan, etc increase uncertainty.

Do little to illuminate QE or rate policy as debate is framed in very mild terms with outliers on both sides. "To mitigate (infl) risks... agreed that FOMC would continue its planning for the eventual exit from the current, exceptionally accommodative stance of monetary policy. In light of uncertainty about the economic outlook, it was seen as prudent to consider possible exit strategies for a range of potential economic outcomes. A few participants indicated that economic conditions might warrant a move toward less-accommodative monetary policy this year; a few others noted that exceptional policy accommodation could be appropriate beyond 2011." Also, "A few members noted that evidence of a stronger recovery, or of higher inflation or rising infl expectations, could make it appropriate to reduce the pace or overall size of the purchase program. Several others indicated that they did not anticipate making adjustments to the program before its intended completion."

Stocks recently stretched to session highs, but overall gains remain rather modest.

Retailers are having an impressive session, however. As such, the SPDR S&P Retail ETF (XRT 52.19, +1.31) is up about 2.5%. Among individual retailers, TJX Co (TJX 50.99, +1.39) is up almost 3% following the firm's decision to raise its dividend by almost 30% to $0.19 per share.

Sterling was the biggest winner versus the dollar among the most-traded currencies as the U.K.’s service industries accelerated at the fastest pace in more than a year last month.

Markit Economics Ltd. and the Chartered Institute of Purchasing and Supply said a gauge of U.K. services based on a survey of companies rose to 57.1, the highest level in 13 months and above the median forecast of 52.6.

“The number was much higher than all expectations across the market, so the net impact has been strong in favor of the pound,” said Roberto Mialich, a senior currency strategist at UniCredit SpA in Milan. “The data hints that the risk of a prolonged stagnation is vanishing. The BOE will be forced to raise rates this year, and this should limit the downside potential for sterling.”

The dollar rose against the yen after Federal Reserve Chairman Ben S. Bernanke said yesterday inflation must be watched “extremely closely,” spurring bets interest rates may be raised sooner than forecast.

Australia’s dollar dropped from almost a record after the Reserve Bank of Australia Governor Glenn Stevens held the overnight cash target rate at 4.75 percent for a fourth straight meeting as floods disrupted coal mining in the nation’s northeast and a rising currency tempered inflation.

Adding lift to euro-dollar, euro-yen stretched to fresh multi-month highs atop Y120.00 where offers had capped earlier. Resistance at Y120.46, the current top of the daily Bollinger band, further resistance at Y120.68 that is a fibo level.

The dollar index continues to show some strength this morning, which is pressuring select commodities.

May crude oil has been in negative territory all session and hit session lows of $107.50/barrel. In current trade, the energy component is down 0.3% at $108.15/barrel.

May natural gas was in the red this morning ahead of pit trading, but when the pits opened, natural gas pushed into positive territory and to new session highs of $4.32. Its currently just above the unchanged line at $2.27/MMBtu.

Precious metals are higher this morning with June gold up 0.4% at $1439.40/ounce and May silver is up 0.4% at $38.66/ounce.

BNY-Mellon says Mar's 57.3 nonmfg ISM marks a 20th consecutive month of growth "and the second month that all index components were in expansionary territory." Members were concerned about "the recent natural disasters in Japan and the associated supply chain ramifications. Additionally, there is concern over rising costs, most notably for fuel and fuel products." Services are "consistent with the 3-4% growth trajectory for 2011" and employment is expanding in both mfg and nonmfg ISM surveys, BNY says.

A flurry of selling in response to the latest ISM Services Index recently took stocks a leg lower, but the major equity averages have been quick to bounce back. Overall trade remains listless, though.

The ISM Services Index for came in at 57.3. Not only is that down from the 59.7 that had been recorded for the prior month, but it is less than the 59.5 that had been broadly expected among economists.

U.S. stocks may open lower Tuesday, as investors mull over the rebalancing of the Nasdaq-100 index to diminish Apple's influence, a rate hike in China and another downgrade of Portugal's debt.

Nasdaq OMX Group announced Tuesday it will rebalance its tech-heavy Nasdaq-100 index, reducing Apple's (AAPL, Fortune 500) weight by almost 40% - to 12.3% from 20.5%. The change takes effect on May 2.

The change will lend more weight to Google (GOOG, Fortune 500), Intel (INTC, Fortune 500), Microsoft (MSFT, Fortune 500) and Oracle (ORCL, Fortune 500).

Apple shares fell nearly 3% in premarket trading. Microsoft, Intel and Oracle each nudged about 1% higher.

The People's Bank of China also surprised investors Tuesday by announcing a quarter percentage point hike in interest rates, as part of its continued efforts to gradually slow down the country's rapidly rising prices.

China's benchmark one-year lending rate now stands at 6.31%.

Economy: At 14:00 GMT the Institute for Supply Management will release its monthly gauge on the service-sector index for March. Economists are looking for the index to slip slightly to 59.5, compared with last month's reading of 59.7.

Later in the day, the Federal Reserve will release minutes from its March 15 policy meeting.

Companies: KB Home (KBH) shares fell nearly 6% after the homebuilder announced a quarterly loss of $114.5 million, or $1.49 a share. That's far deeper than the loss analysts were expecting.

Shares of rival homebuilder Lennar Corp. (LEN) fell 0.5% in early trading after the announcement.

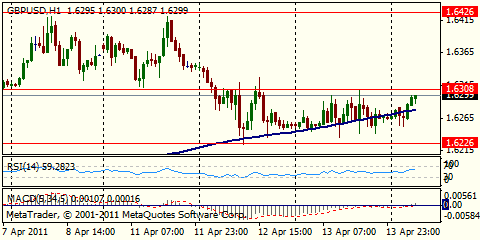

GBP/USD refreshed session highe after rising to $1.6265 where recent reports suggested stops. But rate retreated to $1.6247. Mixed talk of stops staggered up to $1.6300 intermingled with barriers at $1.6280 and $1.6300.

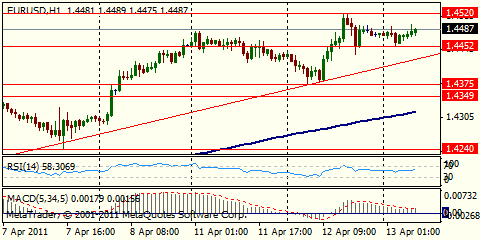

EUR/USD extends recovery and currently holds around $1.4175 after a dip to $1.4160. Earlier bids were mentioned there down to $1.4140 with stops below.

AUD/USD recovered to $1.0320 amid talk of some euro-aussie selling. Talk now also of large stops on a break down $1.0300 despite talk of bids sub $1.0290. Aussie trades $1.0318.

EUR/JPY holds around Y119.57, a bit higher Asian opening at Y119.54. Overnight cross rallied to Y119.92 before settling around Y119.70/80. The pair then came under pressure as Europe opened to a Moody's downgrade of Portugal prompting further sales to a low of Y119.35.

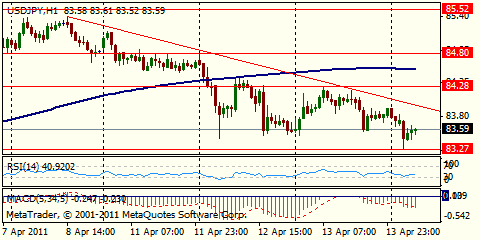

USD/JPY holds around Y84.35. In Asia rate rose to Y84.49 following the comments from Fed Chairman Bernanke before easing back to Y84.20. Talk now of solid bids around Y84.20 with further demand from day traders towards Y83.80. Offers from exporters are seen starting from Y84.50 up to Y84.80.

Early rally paused at $1439.15 before falling back on profit taking to a low of $1430.10. Later prices settled back around $1432.50. The low was a bit lower the support at $1430.50 with further seen towards $1419.50. Resistance remains at the day's high ahead of the all time high of $1447.85.

AUD/USD fell under $0.0300 after the PBOC rate hike. rate triggered bids and stops, printing session lows around $1.0288. Currently rate holds back at $1.0295/00.

The euro hovered below a five-month high against the dollar on Tuesday as investors assessed whether it can make fresh gains given that market players have already positioned themselves for a series of interest rate hikes in the euro zone during 2011.

The European Central Bank is expected to raise rates by a quarter point from a record low of 1% at a meeting on Thursday to rein in inflationary pressures, with two more 25 basis point hikes priced in by year-end .

But the single currency has already risen more than 6% against the dollar and more than 10% versus the yen this year, making investors reluctant to buy more ahead of the meeting this week.

"For the ECB, an April interest rate hike is a done deal and one or two more hikes are priced in. It's hard to see a positive surprise from here," said Masafumi Yamamoto, chief FX strategist at Barclays Bank.

A rise above its November peak of $1.4283 could open the way to $1.4374 (76.4% retracement of the euro's slide from November 2009 to June 2010). Support is seen at $1.4190, with traders citing stops through to below $1.4150.

The Australian dollar dipped, pressured by profit-taking in the wake of its rise to a 29-year high of $1.0422 the previous day. There was talk of both bids and stop-loss offers around $1.0300.

The Reserve Bank of Australia decided to keep interest rates unchanged at 4.75% as widely expected.

"In the medium term, the Aussie remains supported, but there is some room for position reduction. Rather than looking for a run-up in Aussie/U.S. dollar, you would look at Aussie/yen and perhaps Aussie/Swiss franc," said Robert Ryan, senior currency strategist for BNP Paribas.

Later on Tuesday, focus will turn to the Fed minutes for more hints on the Fed's policy outlook.

Underscoring the market's focus on Fed speakers, the dollar edged higher against the yen and the euro earlier on Tuesday, following comments from U.S. Federal Reserve Chairman Ben Bernanke.

Bernanke said a recent pick-up in U.S. inflation was driven primarily by rising commodity prices globally, but added that was unlikely to persist.

GBP/USD retreats after ralling amid strong PMI data. Rate printed high on $1.6249/50 and possibly tweaking a barrier. Talk of further barrier interest $1.6280 and $1.6300, with the March 24 high ahead of them at $1.6268. Cable trades $1.6238.

- European measures will help confidence, econ discipline

- Spain cbank must analyze 13,not 12 bank recap. plans

- On spain's economy, must be patient

- It is key to continue spain savings bank restructuring

- Spain banks must be ready to lend when demand recovers.

- European measures will help confidence, econ discipline

- Spain cbank must analyze 13,not 12 bank recap. plans

- On spain's economy, must be patient

- It is key to continue spain savings bank restructuring

- Spain banks must be ready to lend when demand recovers.

- would like to see inflation move closer to 2%;

- need 300k jobs/mth to help employment situation;

- looking for 4% growth in next 2 years;

- $600b QE is likely right amount.

EUR/JPY Y119.00

The dollar fluctuated against the yen as Federal Reserve Bank of Atlanta President Dennis Lockhart said the U.S. economic recovery faces headwinds, encouraging speculation the central bank will keep borrowing costs low.

The dollar slid versus the euro on April 1 after New York Fed President William C. Dudley said the recovery is “still tenuous,” disagreeing with colleagues who said the central bank should curtail purchases of U.S. debt.

The euro fell on concern an increase in interest rates by the European Central Bank will hurt the economies of the region’s most-indebted nations.

The euro appreciated 3.5% in the first quarter. It was the best three-month performance since the shared currency began trading in 1999.

ECB President Jean-Claude Trichet surprised investors on March 3, when he signaled that policy makers may raise interest rates at their next meeting to curb consumer-price inflation, which reached a two-year high of 2.6% in March.

© 2000-2026. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers