- Analytics

- News and Tools

- Market News

CFD Markets News and Forecasts — 02-06-2011

All three major averages were briefly trading in positive territory before the Dow and S&P slipped back below the falt line.

Financials are among the top performing sectors in the S&P 500 today, trading higher by 0.4%.

Goldman Sachs (GS 134.55, -1.62) remains in negative territory, but is well off its worst levels of the day.

Also out this morning was a note from Moody’s saying Bank of America (BAC 11.31, +0.07), Wells Fargo (WFC 27.15, +0.21), and Citigroup (C 40.08, +0.43) were placed on review for a possible downgrade.

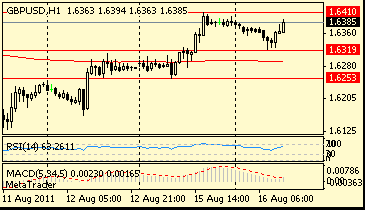

GBP/USD tries to set stable, holding above tech support at $1.6332 (76.4% Fibo of $1.6305/1.6418 move). Rate currently trades around $1.6343. While rate can hold above $1.6332 seen keeping underlying tone buoyant. A break to open a deeper move toward earlier lows at $1.6305.

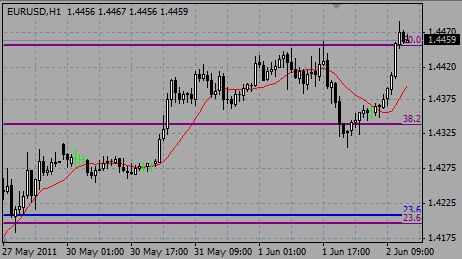

EUR/USD back under $1.4500 after printing session highs on $1.4513. Friday US employment report is in focus now. Rate currently holds around $1.4464 with further stops to $1.4520 and a barrier mentioned at $1.4550.

HFE says they are "hesitate to argue that the underlying trend in claims has now definitely levelled off after the oil/earthquake induced increase of the past two months, but the last three weeks' numbers have all been below 430K so we are quite hopeful." They are hopeful that Q3 will see econ improvement.

The major market averages have been unable to shrug off this morning's disappointing initial and continuing claims data. Earlier weakness has been mostly erased with the Dow and S&P seeing small losses while the Nasdaq holds a slight gain.

Education stocks are among the best performers today, seeing gains on the heels of the Department of Education's favorable gainful employment ruling. The final rules published last night give the for-profit education companies more time to comply with the changes than the initial ruling had proposed. Corinthian Colleges (COCO 5.20, +1.21), Strayer Education (STRA 141.30, +19.43) and Apollo Group (APOL 46.35, +4.16) are among the movers on the news.

Retail stocks have been on many trader's radars as May Same Store Sales were released. Saks (SKS 11.28, +0.22) was a notable outperformer, with sales climbing 20.2% versus the consensus estimate of a 8.2% rise. The reports were generally weaker-than-expected with Gap (GPS 18.27, -0.63), Kohl's (KSS 51.42, -1.50), and JC Penney (JCP 33.05, -0.94) all missing estimates.

Joy Global (JOYG 90.76, +4.87) is buoying today's relative strength in industrial stocks after the company announced strong second quarter results. The company announced earnings of $1.52 per share, topping the Thomson Reuters consensus by $0.17, and reported an 18.6% increase in revenues to $1.06 billion. The company said it expects full year 2011 earnings per share of $5.30-$5.60, up from its previous estimate of $5.10-$5.40. Peer John Deere (DE 84.05, +1.29) is piggybacking gains, trading up 1.5%.

Treasuries continue to hold their losses despite the continued slide in equities. The 10-yr yield has tested the 3.00% level on a couple of occasions, and currently sits at that level.

The euro gained versus the dollar to the highest level in almost a month as German Chancellor Angela Merkel said she’s committed to the shared currency and European Central Bank officials backed the creation of a euro-region finance ministry.

“We don’t have a euro problem in Europe,” Merkel said in a speech in Singapore today on the final day of a three-day Asia trip that also took her to India. “We have more of a debt problem. Financial markets doubt whether some EU states can manage their debt in the long-term.” Germany is committed to the euro, which is stable, she said.

The dollar dropped against the majority of its most-traded peers as weaker economic data, including higher-than-forecast jobless claims, added to speculation the nation’s recovery is slowing. The yen was lower against the euro as Japan’s Prime Minister Naoto Kan survived a no-confidence vote after offering to step down once his work to lead a recovery from March’s earthquake is accomplished.

“A lot of the comments we’ve seen from the euro zone are keeping the currency afloat,” said Kathy Lien, director of currency research with online currency trader GFT Forex in New York. “The jobless claims number is still at lofty levels and because of that the dollar remains under pressure.”

Commodities are trading higher today, while the dollar index continues to trade in the red and is only. The CRB Commodities Index is showing gains of 0.4% currently.

Natural gas futures have been running higher ahead of this morning's inventory data. The energy component opened pit trading around $4.66/MMBtu and rallied up to current session highs of $4.71/MMBtu. Ahead of the data, it was just under that high. Following the data, which showed a build of 83 bcf versus the consensus of a build of ~90bcf, natural gas futures spiked ~2.8% to new session highs of $4.83/MMBtu and are now up 3.8% at $4.80/MMBtu.

Crude oil futures ticked lower at the open of pit trading, but have remained above the $100.00/barrel level all morning. Crude almost hit the $101 area when it rallied this morning in the first 30 minutes of trade, but stopped at $100.96/barrel (current session highs) and is now up 0.1% at $100.39/barrel.

Precious metals were lower earlier this morning and are now extending those losses, mostly notably in silver futures. Silver just quickly fell another ~40 cents/oz to new session lows of $36.46/oz. and is now down 2.9% at $36.59/oz. Gold sold off as well, but the losses are much more modest. Gold lost just over $2/oz. to new session lows of $1535.20/oz. during the time silver sold off in recent trade. Gold is currently 0.5% lower at $1535.90/oz.

Commodities are trading higher today, while the dollar index continues to trade in the red and is only. The CRB Commodities Index is showing gains of 0.4% currently.

Natural gas futures have been running higher ahead of this morning's inventory data. The energy component opened pit trading around $4.66/MMBtu and rallied up to current session highs of $4.71/MMBtu. Ahead of the data, it was just under that high. Following the data, which showed a build of 83 bcf versus the consensus of a build of ~90bcf, natural gas futures spiked ~2.8% to new session highs of $4.83/MMBtu and are now up 3.8% at $4.80/MMBtu.

Crude oil futures ticked lower at the open of pit trading, but have remained above the $100.00/barrel level all morning. Crude almost hit the $101 area when it rallied this morning in the first 30 minutes of trade, but stopped at $100.96/barrel (current session highs) and is now up 0.1% at $100.39/barrel.

Precious metals were lower earlier this morning and are now extending those losses, mostly notably in silver futures. Silver just quickly fell another ~40 cents/oz to new session lows of $36.46/oz. and is now down 2.9% at $36.59/oz. Gold sold off as well, but the losses are much more modest. Gold lost just over $2/oz. to new session lows of $1535.20/oz. during the time silver sold off in recent trade. Gold is currently 0.5% lower at $1535.90/oz.

BMO reminds that initial jobless claims data are volitile but says key is that "the 4-week moving average has been over the 400k mark for six straight weeks" - not a friendly trend.

The major market averages remain mixed with the Nasdaq leading the way with a gain of 0.3%.

Retains a firm tone, with rate seen pushing up against earlier posted highs at stg0.8838. Reported offers have been noted between stg0.8835/45, a break to open a move toward stg0.8865/75 ahead of stg0.8895/00.

U.S. stock futures pointed to a muted open Thursday, following one of the worst sessions of the year, as investors remained on edge ahead of the highly-anticipated May jobs report due Friday.

Economy: Weekly jobless claims fell by 6,000 to 422,000 in the latest week. While investors welcomed the slight dip in unemployment claims, the figure was not as low as economists were hoping for -- and it remained above the key level of 400,000 for the eighth straight week.

Companies: Shares of Corinthian Colleges (COCO) spiked 27%, while shares of Apollo Group (APOL, Fortune 500) rose 12%. Bridgepoint Education's (BPI) stock edged up 10%.

Investors will also keep on eye on major retailers including Target (TGT, Fortune 500), Gap (GPS, Fortune 500), Costco (COST, Fortune 500) and BJ's Wholesale (BJ, Fortune 500), as they release same-store sales data for May.

EUR/USD retreats to current $1.4450 after US data released. Flows remain muted with much of Europe on holiday for Ascension day. Mixed order interest remains below $1.4450 where bids and stops are in focus.

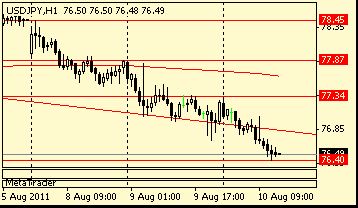

USD/JPY printed lows around Y80.55 before the pair rebounded smartly for trade to the current Y80.78 area. Bids ahead of Y80.50 may be tested. Stops noted lower.

Data released:

08:30 United Kingdom PMI Construction (May) 54.0 53.8 53.3

The euro gained versus the dollar and yen as German Chancellor Angela Merkel said the European Union remains committed to its shared currency and the outlook for German growth is “very positive.”

“We don’t have a euro problem in Europe,” Merkel said today. “We have more of a debt problem. Financial markets doubt whether some EU states can manage their debt in the long-term.” Germany is committed to the euro, which is stable, she said.

The euro has gained 2.4% this year, versus a 5.4% drop by the dollar and a 5.5% decline for the yen.

The yen stayed lower against the euro as Japan’s Prime Minister Naoto Kan survived a no-confidence vote after appealing to ruling party dissidents by offering to step down once his work to lead a recovery from March’s earthquake is accomplished.

The Labor Department will release May unemployment figures tomorrow. Goldman Sachs Group Inc. yesterday revised its estimate for an increase in May nonfarm payrolls to 100,000 from 150,000, while Citigroup Inc. trimmed its projection to 100,000 from 170,000. The median estimate is for a gain of 170,000 following a 244,000 April increase.

EUR/USD continues to recover after decline in Asia to $1.4305. Rate printed session high on $1.4490, after triggering some stops and offers. Options are at $1.4500.

GBP/USD was supported by strong statistic and rose to $1.6420. Later rate retreated to $1.6370.

USD/JPYcontinues to weaken from Asian high on Y81.30. Rate printed lows around Y80.66.

US data starts at 1230GMT with the weekly jobless claims and also the release of non-farm productivity and unit labor costs.

US data continues at 1400GMT with US factory new orders that are expected to fall 0.9% in April.

The weekly EIA Natural Gas and Crude Oil Stocks data releases are due from 1430GMT.

EUR/GBP holds around stg0.8828, a bit lower session high on stg0.8836. Earlier reports noted strong resistance/sell interest to be seen in the area between stg0.8835/45.

The dollar hovered near a one-month low versus a currency basket on Thursday after dismal U.S. economic data stoked fears the country's recovery will be slow, and weak Friday's payrolls may spark more losses.

The euro edged up, clawing back after Moody's on Wednesday slashed its rating on Greece.

The dollar smarted after data on Wednesday showed U.S. companies hired far fewer workers than expected in May and output in the manufacturing sector slowed to its lowest since 2009.

A weak reading of key U.S. nonfarm payrolls on Friday may trigger more dollar losses as it would fuel speculation of the need for more stimulus after a second round of quantitative easing by the Federal Reserve ends this month.

The euro was supported even after Moody's on Wednesday cut Greece's credit rating by three notches to Caa1 on debt restructuring worries.

The euro recovered back as currency investors are optimistic that European officials will reach an agreement on how to help Greece repay its debt.

- Aid to states in need helps crisis from spreading

- Euro a credible currency

GBP/USD holds above session lows on $1.6304 - currently at $1.6396 after a strong data. A break to open a move toward $1.6395/400 ahead of stronger interest between $1.6420/25.

EUR/USD break above the earlier resistance in the $1.4420/25 area, and breaking the 76.4% retrace of the move down from $1.4459 to $1.4307 at $1.4423. Rate currently holds around $1.4447. Resistance now seen into $1.4460 (NY high Weds $1.4459) with stops above.

EUR/JPY Y117.00, Y117.05, Y117.40, Y117.50, Y118.00

GBP/USD $1.6470, $1.6490, $1.6210

AUD/USD $1.0615, $1.0610, $1.0600, $1.0560, $1.0550, $1.0800, $1.0820,

GBP/AUD A$1.5230

Extends recovery, begins to make a show back above $1.6350 and looking set to retest earlier highs at $1.6354. Offers noted from here through to $1.6360 with stops placed above.

The U.S. currency weakened after a private survey showed employment increased by 38,000 last month, the smallest gain since September and a measure of manufacturing output in May declined more than forecast.

U.S. employment increased last month after a revised 177,000 gain in April, according to figures from ADP Employer Services. The median estimate called for a 175,000 advance for May.

The Labor Department will release May unemployment figures June 3. Goldman Sachs Group Inc. revised its estimate today for an increase in May nonfarm payrolls to 100,000 from 150,000, while Citigroup Inc. trimmed its projection to 100,000 from 170,000.

The Institute for Supply Management’s factory index fell to 53.5 in May from 60.4 the prior month. Economists projected the gauge would drop to 57.1.

The Swiss franc strengthened as retail sales rose in April at the fastest rate in two years, boosting speculation the Swiss National Bank may raise borrowing costs. Retail sales climbed 7.5% in the year after a 0.2% drop in March, the most since April 2009.

© 2000-2026. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers