- Analytics

- News and Tools

- Market News

Analytics, News, and Forecasts for CFD Markets: currency news — 20-05-2011.

Krishen Rangasamy of CIBC World Markets says Canadian retail sales, released earlier showing flat sales in March, was well below consensus looking for +0.9%. Ex-auto sales were down 0.1%, also weaker than expected. But February sales were revised higher (both headline and ex-autos).

Stocks recently stretched to fresh afternoon highs, but they have started to pull back a bit. Although the major equity averages remain in the red, the mood among market participants has improved markedly during the course of the past few hours. The improved tone of trade has helped bring stocks back in line with where they had started the week.

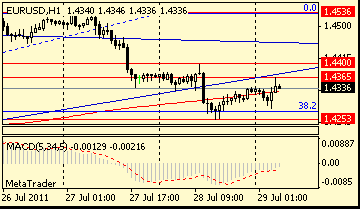

EUR/USD printed hourly high above $1.4220 area as Dow trims losses and oil rebounds further with gains (+$1.16 to $99.60). Stops above $1.4220. Further resistance at the morning high of $1.4260.

Stocks continue to rally. The effort comes as the dollar surrenders some more of its gain, which now stands at a modest 0.3%.

Retailers continue to have a rough session, however. Disappointing guidance from Gap (GPS 19.40, -3.89) and Aeropostale (ARO 18.01, -3.33) has weighed heavily on the two stocks, but Barnes & Noble (BKS 18.32, +4.21) has surged 30% in response to a takeout offer of $17 per share from Liberty Media.

The euro fell versus the dollar for the first time in five days as a policy maker for the European Central Bank said it may not be able to accept Greek sovereign debt as collateral if the bond maturities are extended.

The shared currency dropped as the remarks by Bundesbank President Jens Weidmann, a member of the ECB Governing Council, added to signs of a division between monetary officials and politicians on Greek debt.

Fitch Ratings lowered Greece’s debt rating. The Bundesbank said separately Germany’s economy is losing momentum, damping speculation the central bank will raise interest rates.

“It’s negative for the euro, fundamentally negative for Greece and more broadly negative for European sentiment,” said Nick Bennenbroek, head of currency strategy at Wells Fargo & Co..

The euro also fell after Investor’s Business Daily reported Norway froze a 235 million kroner ($42 million) grant to Greece.

After several sessions of challending the $1500, gold has finally broken higher Friday. Gold holds at $1512.94/oz currently, at the day's high and up from an overnight low of $1487.91. Initial resistance is seen at $1516.40, the May 13 peak.

EUR/USD recovers off lows around $1.4140 to $1.4193 amid shorts pare back positions ahead of weekends. Euro to find resistance now at $1.4220 area of broken support though, in thin Friday conditions, anything can happen.

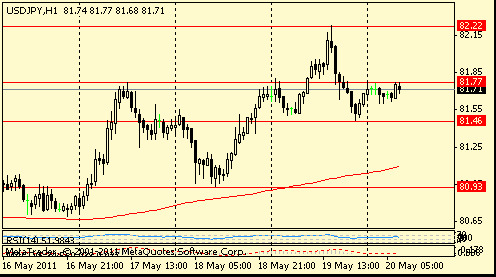

Despite the high volatility in the market USD/JPY has managed to hold close to its midpoint of the session range, trades currently around Y81.64. Dollar bids still expected down to Y81.40 with stops below, Offers in place atop Y82.00.

June light sweet crude (WTI) trades down $1.88 at $96.56/bl after holding in a $95.99 to $99.60 range. The front contract (which shifts to July starting Monday) peaked at a 31-month $114.83 May 2 and troughed at $94.63 May 6. WTI rallied to $104.60 May 11, but since then has held a tight $95.02 to $100.99 range. Stops are expected on a clear cut break of the May lows.

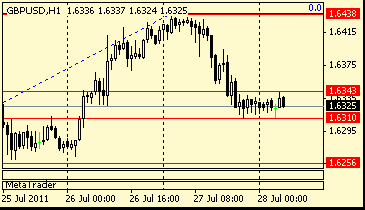

EUR/GBP extends corrective pullback to stg0.8739 as cable extends its recovery off lows at $1.6167 toward $1.6200. Next cross support seen at stg0.8720/15 ahead of stg0.8700 and stg0.8675/70.

Rebound stalled at $1.4175 area and pair slipping again. Downside order books thin but contain some bids at $1.4155/50 and again at $1.4120 area. Below there, stops suggested sub $1.4100.

Greek spreads are widening on local press story that visiting IMF officials, who have been in Athens for the past two weeks, have suspended checks and will return when Greece adopts more measures.

The major market averages have slipped in the opening minutes of trade. The downturn has been broad based; in fact, there isn't a single sector sporting a meaningful gain.

Energy stocks have been hit especially hard. The sector is already down 0.8%. Part of that is attributable to a sharp reversal in crude oil prices, which have dropped to $97.31 per barrel for a 1.6% loss, amid the dollar's climb to a 0.5% gain.

U.S. stocks were poised to open lower Friday, possibly tilting the direction for the full week as well.

Investors have endured a slew of disappointing economic reports in recent days, but have found solace in the Federal Reserve's likely continued support of the market -- even after its $600 billion bond-buying program expires at the end of June.

Companies: After debuting Thursday on the New York Stock Exchange, shares of LinkedIn (LNKD) more than doubled from their IPO price -- making it one of the biggest tech IPOs since Google (GOOG, Fortune 500).

Shares of Barnes & Noble (BKS, Fortune 500) jumped 26% in premarket trading after the bookseller announced a proposal to be bought by Liberty Media for $17 per share in cash, a nearly $1 billion buyout offer.

World markets:

Oil for June delivery gained 36 cents, or 0.2%, to $98.80 a barrel. The contract for June oil settles Friday. The July contract, which is more active, rose 36 cents to $99.29.

Gold futures for June delivery rose $2.50, or 0.2%, to $1,494.90 an ounce.

Silver futures for July delivery shaved 10 cents, or 0.3%, to $34.83 an ounce.

Bonds: The price on the benchmark 10-year U.S. Treasury edged slightly higher, pushing the yield down to 3.15%.

EUR/USD

Offers: $1.4280, $1.4305, $1.4320/25, $1.4350/60, $1.4370/80

Bids: $1.4210/00, $1.4195/90, $1.4155/50

- Mar retail sales ex-autos -0.1% m/m

The euro weakened versus the dollar for the first time in five days as the German Bundesbank said growth in Europe’s largest economy will probably slow, prompting traders to reduce bets the European Central Bank will increase interest rates.

Europe’s common currency snapped four days of gains against the yen. German growth is “likely to ease somewhat in the foreseeable future,” the Frankfurt-based Bundesbank said in its monthly bulletin published today. The krone climbed against the euro as Norges Bank Governor Oeystein Olsen said Norway’s currency may appreciate further as growth accelerates.

“Any kind of sign that growth is slowing in the euro zone, people are overreacting and that’s why we’ve seen this sell- off,” said London-based Kathleen Brooks, research director at Forex.com, a unit of online currency trading company Gain Capital Holdings Inc. “People were looking for any excuse to sell the euro and book a bit of profit.”

- Keeping inflation expectations anchored of upmost importance.

Market talk of a North Asian sovereign name on the bid in the dollar around the Y81.50 level. The pair recently posted a day's low of Y81.48 and currently trades Y81.54/56. Stops await below at Y81.40 and Y81.30.

Eases back under $1.4300, as euro-sterling sales and cable meeting resistance, weighs back on euro-dollar. Demand seen into $1.4295/90, with stops said to have built between $1.4285/80. Break under will target $1.4250.

EUR/GBP stg0.8930

AUD/USD $1.0650, $1.0665, $1.0725

Shanghai Composite -0.04% 2,858.46

European data rounds off at 1000GMT with

France industrial orders, which are released at the same time as the Bundesbank publishes the Monthly Bulletin for May.

Gross domestic product in Japan contracted an annualized 3.7 percent in the three months through March, following a revised 3 percent drop in the previous quarter, the Cabinet Office said today in Tokyo.

The dollar pared losses against currencies of commodity exporters as data showed Philadelphia-area manufacturing grew at the slowest pace in seven months.

The dollar reversed a loss against New Zealand’s currency after the Federal Reserve Bank of Philadelphia’s general economic index unexpectedly fell to 3.9, the weakest reading since October, from 18.5 a month earlier. Readings greater than zero signal expansion. In another report, the National Associated of Realtors said sales of existing U.S. homes slid 0.8 percent in April to a 5.05 million annual pace.

The franc fell against the euro as Swiss Economy Minister Johann Schneider-Ammann said authorities will consider “appropriate” measures if the currency continues to strengthen.

European data starts at 0700GMT, when German PPI. This is later followed at 0800GMT by March current account data. European data rounds off at 1000GMT with

France industrial orders, which are released at the same time as the Bundesbank publishes the Monthly Bulletin for May.

Japanese stocks fell after a report showed the nation’s economy shrank more than estimated in the first quarter and utilities dropped after the Prime Minister said Japan will debate overhauling the energy industry.

Mitsubishi UFJ Financial Group Inc. (8306), Japan’s largest bank by market value, declined 2.1 percent. Tokyo Electric Power Co., the operator of the Fukushima Dai-Ichi nuclear power plant damaged in the record earthquake in March, tumbled 8 percent. Dainippon Screen Manufacturing Co., a chip equipment maker, plunged 5.3 percent after Goldman Sachs Group Inc. cut its rating on chipmaker Intel Corp. (INTC)

European stocks rose for a second day as industrial stocks led gains on the benchmark Stoxx Europe 600 Index after the U.S. Federal Reserve signaled that interest rates will remain low.

Glencore International Plc was unchanged on its first day of trading in London after it sold $10 billion of stock in its initial public offering. BP Plc (BP/) climbed 1.6 percent as BofA Merrill Lynch Global Research advised buying the shares. Pandora A/S, the Danish maker of jewelry, slumped 22 percent after saying it has lifted prices globally for the first time in its history because of the rising cost of silver and gold.

U.S. stocks traded little changed as reports on home sales, leading indicators and manufacturing trailed estimates, tempering optimism in the economy triggered by a bigger-than-forecast drop in jobless claims.

Intel Corp. (INTC), KLA-Tencor Corp. (KLAC) and Applied Materials Inc. (AMAT) slumped at least 1.7 percent as Goldman Sachs Group Inc. cut their ratings, citing increased competition from tablet computers and excess supply. Big Lots Inc. (BIG) tumbled 9.9 percent after the Wall Street Journal reported that the discount retailer won’t sell itself. LinkedIn Corp., the largest professional-networking website, more than doubled in the first day of trading after its initial public offering.

© 2000-2026. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers