- Analytics

- News and Tools

- Market News

- USD Index extends the gradual upside above 103.00 ahead of data, FOMC

USD Index extends the gradual upside above 103.00 ahead of data, FOMC

- The index advances modestly beyond the 103.00 hurdle.

- US markets return to normal activity following Tuesday’s holiday.

- Factory Orders, FOMC Minutes take centre stage later in the session.

The USD Index (DXY), which tracks the greenback vs. a bundle of its main rivals, trades with small gains and looks to consolidate the trade above the key 103.00 barrier on Wednesday.

USD Index focused on data, FOMC Minutes

The index so far advances for the third session in a row against the backdrop of a generalized consolidative range in the global assets, as US markets slowly resume the activity in the wake of the Independence Day holiday.

In the meantime, investors are expected to shift their attention to the upcoming release of the FOMC Minutes, while the US labour market is seen regaining interest in light of the publication of the ADP report and weekly Initial Claims (Thursday) and June’s Nonfarm Payrolls and Unemployment Rate (Friday).

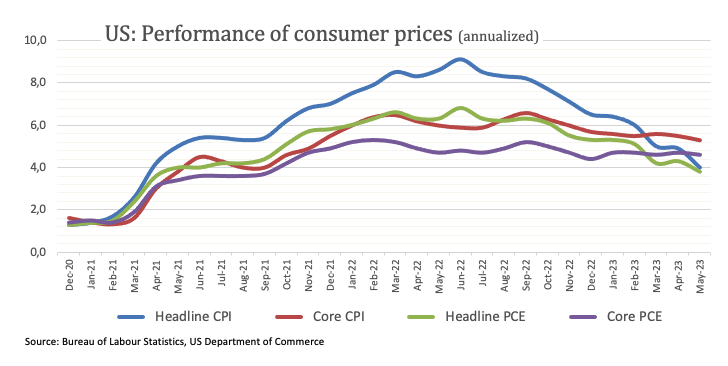

So far, market participants continue to price in a 25 bps rate hike by the Federal Reserve at its July 26 gathering, as the inflation still runs well above the Fed’s target and core prices remain sticky.

Back on the US docket, Factory Orders for the month of May are due later seconded by the IBD/TIPP Economic Optimism index, the FOMC Minutes and the speech by NY Fed John Williams (permanent voter, centrist).

What to look for around USD

The index keeps the trade around the 103.00 zone as key results from the US calendar are expected in the second half of the week.

Meanwhile, the likelihood of another 25 bps hike at the Fed's upcoming meeting in July remains high, supported by the continued strength of key US fundamentals such as employment and prices.

This view was further bolstered by comments from Fed Chief Powell at the June FOMC event, who referred to the July meeting as "live" and indicated that most of the Committee is prepared to resume the tightening campaign as early as next month.

Key events in the US this week: Factory Orders, FOMC Minutes (Wednesday) – ADP Employment Change, Balance of Trade, Initial Jobless Claims, Final Services PMI, ISM Services PMI (Thursday) – Nonfarm Payrolls, Unemployment Rate (Friday).

Eminent issues on the back boiler: Persistent debate over a soft/hard landing of the US economy. Terminal Interest rate near the peak vs. speculation of rate cuts in late 2023/early 2024. Fed’s pivot. Geopolitical effervescence vs. Russia and China. US-China trade conflict.

USD Index relevant levels

Now, the index is up 0.06% at 103.14 and the breakout of 103.54 (weekly high June 30) would open the door to 104.69 (monthly high May 31) and then 104.74 (200-day SMA). On the other hand, the next contention emerges at 101.92 (monthly low June 16) followed by 100.78 (2023 low April 14) and finally 100.00 (round level).

© 2000-2026. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers