- Analytics

- News and Tools

- Market News

- US Dollar Index pushes higher and clinches new 2022 high past 96.80

US Dollar Index pushes higher and clinches new 2022 high past 96.80

- DXY extends the strong upside and records new highs.

- US yields trade on a mixed tone post-FOMC meeting.

- Advanced Q4 GDP, Initial Claims next on tap in the US docket.

The greenback extends the rally and records new highs for the year past the 96.80 level when tracked by the US Dollar Index (DXY) on Thursday.

US Dollar Index now looks to data

The index remains bid and advances for the fourth consecutive session on Thursday, gathering fresh steam following the hawkish message at the FOMC gathering on Wednesday.

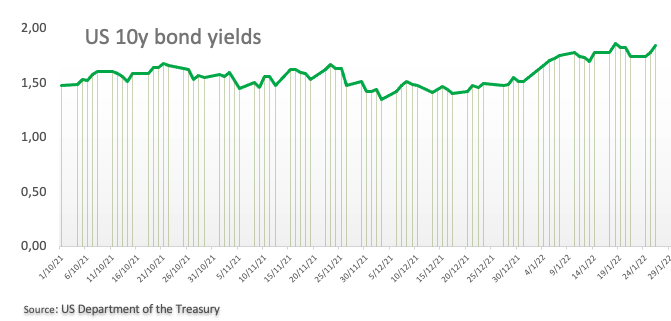

The move higher in the buck comes amidst the mixed performance in the US money markets, where yields in the short end of the curve climb to levels last seen in February 2020 near 1.20% vs. downticks in the belly and the long end.

The dollar reinforces its upside as market participants continue to adjust to the recent announcements by the Fed at its meeting on Wednesday.

While the Federal Reserve kept rates on hold as expected, Chief Powell opened the door to a March hike and did not rule out raising the Fed Funds Target Range at every meeting this year. Investors’ attention, therefore, are expected to remain focused on the quantity of rate hikes this year and the size of them, relegating somewhat speculation surrounding the timing of the balance sheet runoff, which according to Powell will be data dependent.

Later in the US data space, the flash Q4 GDP will take centre stage seconded by usual weekly Claims, Durable Goods Orders and Pending Home Sales.

What to look for around USD

The index extends the sharp advance to new tops and already trades at shouting distance from the 2021 high just below the 97.00 barrier, all after the Fed’s hawkish tilt exacerbated the upside in the dollar on Wednesday. Meanwhile, the constructive outlook for the greenback is expected to remain unchanged for the time being on the back of rising yields, persistent elevated inflation, supportive Fedspeak and the solid pace of the US economic recovery.

Key events in the US this week: Durable Goods Orders, Advanced Q4 GDP, Initial Claims, Pending Home Sales (Thursday) – PCE, Personal Income/Spending, Final Consumer Sentiment (Friday).

Eminent issues on the back boiler: Fed’s rate path this year. US-China trade conflict under the Biden administration. Debt ceiling issue. Escalating geopolitical effervescence vs. Russia and China.

US Dollar Index relevant levels

Now, the index is gaining 0.37% at 96.83 and a break above 96.85 (2022 high Jan.27) would open the door to 96.93 (2021 high Nov.24) and finally 97.00 (round level). On the flip side, the next down barrier emerges at 96.00 (55-day SMA) seconded by 95.41 (low Jan.20) and then 94.62 (2022 low Jan.14).

© 2000-2026. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers