- Analytics

- News and Tools

- Market News

- US Dollar Index looks bid near 96.40 ahead of data

US Dollar Index looks bid near 96.40 ahead of data

- DXY leaves behind Wednesday’s pullback and trades near 96.40.

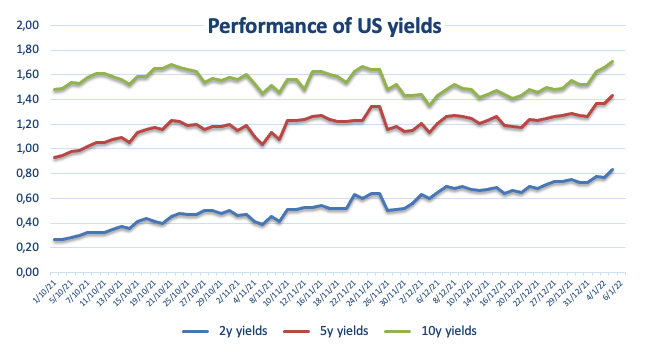

- US yields rose further following the release of FOMC Minutes.

- Initial Claims, ISM Non-Manufacturing, Balance of Trade next on tap.

The greenback, when gauged by the US Dollar Index (DXY), resumes the upside and regains the 96.40 region on Thursday.

US Dollar Index boosted by yields, looks to data

The index reverses the retracement seen in the previous session and regains some buying interest around 96.40 in the second half of the week, as market participants continue to digest the hawkish tilt of the FOMC Minutes published late on Wednesday.

Indeed, the Minutes of the December meeting suggested that March remains a live event, sparking speculation of three or four interest rate hikes amidst a persistent improvement in the US labour market and elevated inflation. Indeed, and according to CME FedWatch Tool, there is almost a 70% probability of an interest rate hike at the 16 March meeting.

Following the release of the Minutes, US yields edged (much) higher across the curve and prompted the buck to trim part of Wednesday’s losses and return to the positive territory so far on Thursday.

Interesting day in the US docket, where the ISM Non-Manufacturing will take centre stage seconded by usual weekly Claims, final Balance of Trade figures and Factory Orders for the month of November.

What to look for around USD

The index trades with certain conviction above the 96.00 hurdle sustained by the strong move higher in US yields, particularly following the hawkish message from the FOMC release (Wednesday). As markets slowly return to normality, the dollar’s constructive outlook is forecast to remain bolstered by the Fed’s intentions to hike the Fed Funds rates later in the year amidst persevering elevated inflation, supportive Fedspeak, higher yields and the solid performance of the US economy.

Key events in the US this week: Initial Claims, ISM Non-Manufacturing, Factory Orders, Trade Balance (Thursday) - Nonfarm Payrolls, Unemployment Rate (Friday).

Eminent issues on the back boiler: Start of the Fed’s tightening cycle. US-China trade conflict under the Biden’s administration. Debt ceiling issue. Potential geopolitical effervescence vs. Russia and China.

US Dollar Index relevant levels

Now, the index is advancing 0.19% at 96.36 and a break above 96.46 (weekly top Jan.4) would open the door to 96.90 (weekly high Dec.15) and finally 96.93 (2021 high Nov.24). On the flip side, the next down barrier emerges at 95.57 (monthly low Dec.31) followed by 95.51 (weekly low Nov.30) and then 94.96 (weekly low Nov.15).

© 2000-2026. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers